Study Guide - NCAHAMncaham.com/Publications/CAA Study Guide 2016.docx · Web viewAcupuncture...

39

Certified Access Associate Exam Study Guide 2016

-

Upload

nguyenliem -

Category

Documents

-

view

214 -

download

0

Transcript of Study Guide - NCAHAMncaham.com/Publications/CAA Study Guide 2016.docx · Web viewAcupuncture...

Certified Access Associate Exam

Study Guide

2016

MedicareMedicare Part A - Inpatient hospital careHow often is it covered?Medicare Part A (Hospital Insurance) covers hospital services, including semi-private rooms, meals, general nursing, drugs as part of your inpatient treatment, and other hospital services and supplies. This includes the care you get in acute care hospitals, critical access hospitals, inpatient rehabilitation facilities, long-term care hospitals, inpatient care as part of a qualifying clinical research study, and mental health care.What's not covered

Private-duty nursing Private room (unless medically necessary) Television and phone in your room (if there's a separate charge for these

items) Personal care items, like razors or slipper socks

Who's eligible?All people with Part A are covered when all of these are true:

A doctor makes an official order which says you need 2 or more midnights of medically necessary inpatient hospital care to treat your illness or injury and the hospital formally admits you.

You need the kind of care that can be given only in a hospital. The hospital accepts Medicare. The Utilization Review Committee of the hospital approves your stay while

you're in a hospital.Your costs in Original Medicare

$1,288 deductible for each benefit period. Days 1–60: $0 coinsurance for each benefit period. Days 61–90: $322 coinsurance per day of each benefit period.

1 | P a g e

Days 91 and beyond: $644 coinsurance per each "lifetime reserve day" after day 90 for each benefit period (up to 60 days over your lifetime).

Beyond lifetime reserve days: all costs.Medicare Part B – Outpatient Medical Care

Medicare covers services (like lab tests, surgeries, and doctor visits) and supplies (like wheelchairs and walkers) considered necessary to treat a disease or condition.If you're in a Medicare Advantage Plan or other Medicare plan, you may have different rules, but your plan must give you at least the same coverage as Original Medicare. Some services may only be covered in certain settings or for patients with certain conditions.Part B covers 2 types of services

Medically necessary services: Services or supplies that are needed to diagnose or treat your medical condition and that meet accepted standards of medical practice.

Preventive services: Health care to prevent illness (like the flu) or detect it at an early stage, when treatment is most likely to work best.

You pay nothing for most preventive services if you get the services from a health care provider who accepts assignment.

Part B covers things like: Clinical research Ambulance services Durable medical equipment (DME) Mental health

o Inpatiento Outpatiento Partial hospitalization

Getting a second opinion before surgery Limited outpatient prescription drugs

2 ways to find out if Medicare covers what you need

1. Talk to your doctor or other health care provider about why you need certain services or supplies, and ask if Medicare will cover them. If you need something that's usually covered and your provider thinks that

2 | P a g e

Medicare won't cover it in your situation, you'll have to read and sign a notice saying that you may have to pay for the item, service, or supply.

2. Find out if Medicare covers your item, service, or supply.Medicare coverage is based on 3 main factors

1. Federal and state laws.2. National coverage decisions made by Medicare about whether something

is covered.3. Local coverage decisions made by companies in each state that process

claims for Medicare. These companies decide whether something is medically necessary and should be covered in their area.

What's not covered by Part A & Part B?Medicare doesn't cover everything. If you need certain services that Medicare doesn't cover, you'll have to pay for them yourself unless you have other insurance or you're in a Medicare health plan that covers these services.Even if Medicare covers a service or item, you generally have to pay your deductible, coinsurance, and copayments.

Some of the items and services that Medicare doesn't cover include: Long-term care (also called custodial care) Most dental care Eye examinations related to prescribing glasses Dentures Cosmetic surgery Acupuncture Hearing aids and exams for fitting them Routine foot care

3 | P a g e

An Important Letter from Medicare - IMMHospital Discharge Appeal Notices Hospitals are required to deliver the Important Message from Medicare (IM), CMS-R-193 to all Medicare beneficiaries and Medicare Advantage plan enrollees who are hospital inpatients. The information on the IM informs hospitalized inpatient beneficiaries of their hospital discharge appeal rights. Beneficiaries who choose to appeal a discharge decision must receive the Detailed Notice of Discharge (DND) from the hospital or their Medicare Advantage plan, if applicable. These requirements were published in a final rule, CMS-4105-F: Notification of Hospital Discharge Appeal Rights, which became effective on July 2, 2007.

Advanced Beneficiary Notice – ABN

The ABN is a written notice you must issue to a Fee-For-Service beneficiary before furnishing items or services that are usually covered by Medicare but are not expected to be paid in a specific instance for certain reasons, such as lack of medical necessity. The following CMS notices are approved for this purpose: ™

Advance Beneficiary Notice of Noncoverage (ABN), Form CMS-R-131; ™ Skilled Nursing Facility Advance Beneficiary Notice of Noncoverage

(SNFABN), Form CMS-10055; Hospital-Issued Notice of Noncoverage (HINN).

The ABN allows the beneficiary to make an informed decision about whether to get the item or service that may not be covered and accept financial responsibility if Medicare does not pay. If the beneficiary does not get written notice when it is required, he or she may not be held financially liable if Medicare denies payment, and you may be financially liable if Medicare does not pay. The ABN is used for Medicare Part B (outpatient) and Part A (limited to hospice, Home Health Agencies, and Religious Nonmedical Health Care Institutions only) items and services. You must issue the ABN when: ™ You believe Medicare may not pay for an item or service; ™ Medicare usually covers the item or service; and

Medicare is expected to deny payment for the item or service because it is not medically reasonable and necessary for this beneficiary in this case or for one of the reasons listed in the “When You Must Issue an ABN” section below. Services must meet specific medical necessity requirements contained in the statute, regulations, and manuals and specific medical

4 | P a g e

necessity criteria defined by National Coverage Determinations (NCDs) and Local Coverage Determinations (LCDs) (if any exist for the service being reported). For every service billed, you must indicate the specific sign, symptom, or patient complaint that makes the service reasonable and necessary.

Common reasons for Medicare to deny an item or service as not medically reasonable and necessary include care that is: ™

Experimental and investigational or considered “research only”; ™ Not indicated for diagnosis and/or treatment in this case; ™ Not considered safe and effective; or ™ More than the number of services Medicare allows in a specific period

for the corresponding diagnosis.

When You Must Issue an ABN

You must issue an ABN when you expect Medicare may deny payment for an item or service because: ™

It is not considered reasonable and necessary under Medicare Program standards; ™

The care is considered custodial; ™ Outpatient therapy services are in excess of therapy cap amounts and

do not qualify for a therapy cap exception; ™ A beneficiary is not terminally ill (for hospice providers only); A beneficiary is not homebound or there is no need for intermittent

skilled nursing care (for home health services only).

When should you NOT issue an ABN

You may not issue an ABN on a routine basis or when there is no reasonable basis to expect that Medicare may not cover the item or service. You must ensure a reasonable basis exists for noncoverage associated with the issuance of each ABN. Some exceptions to the routine notice prohibition include: ™

Experimental items and services; ™ Items and services with frequency limitations for coverage; ™

5 | P a g e

Medical equipment and supplies denied because the supplier had no supplier number or the supplier made an unsolicited telephone contact;

Services that are always denied for medical necessity.

Other Prohibitions You cannot issue an ABN to: ™

To shift liability and bill the beneficiary for the services denied due to a Medically Unlikely Edit (MUE);

A beneficiary in a medical emergency or under great duress (compelling or coercive circumstances).

o ABN use in the emergency room or during ambulance transports may be appropriate in some cases for a medically stable beneficiary who is not under duress;

Charge a beneficiary for a component of a service when Medicare makes full payment through a bundled payment; ™

Transfer liability to the beneficiary when Medicare would otherwise pay for items and services.

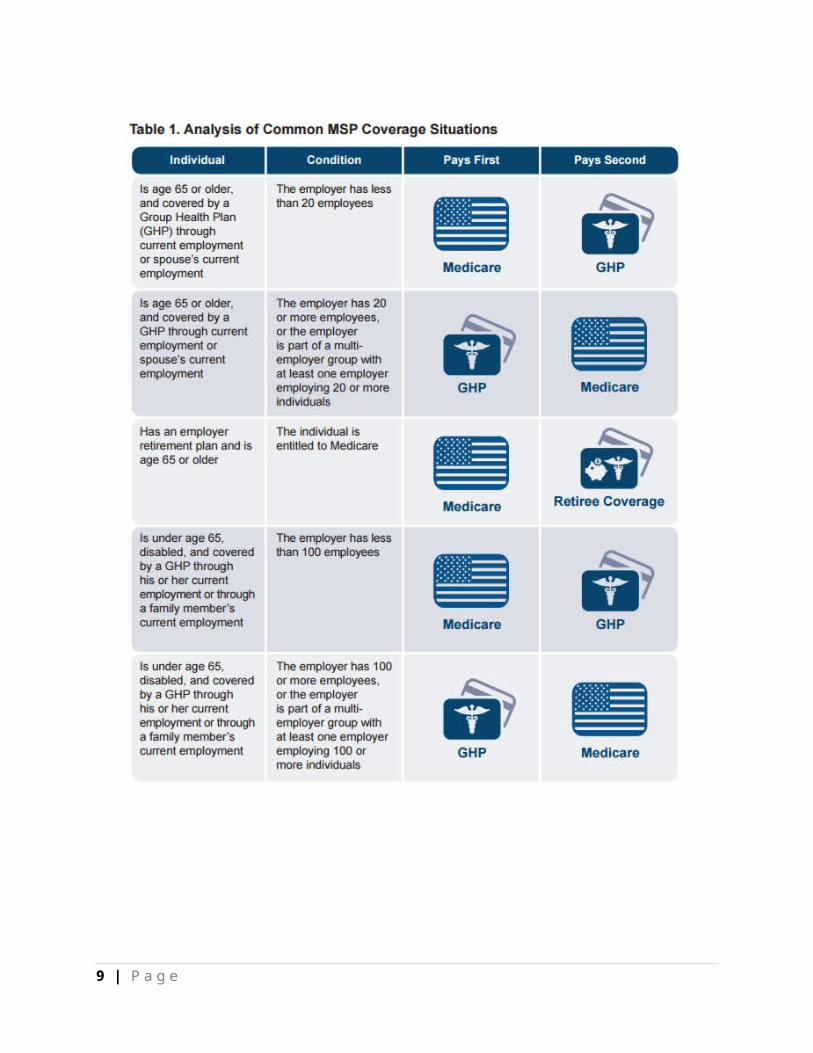

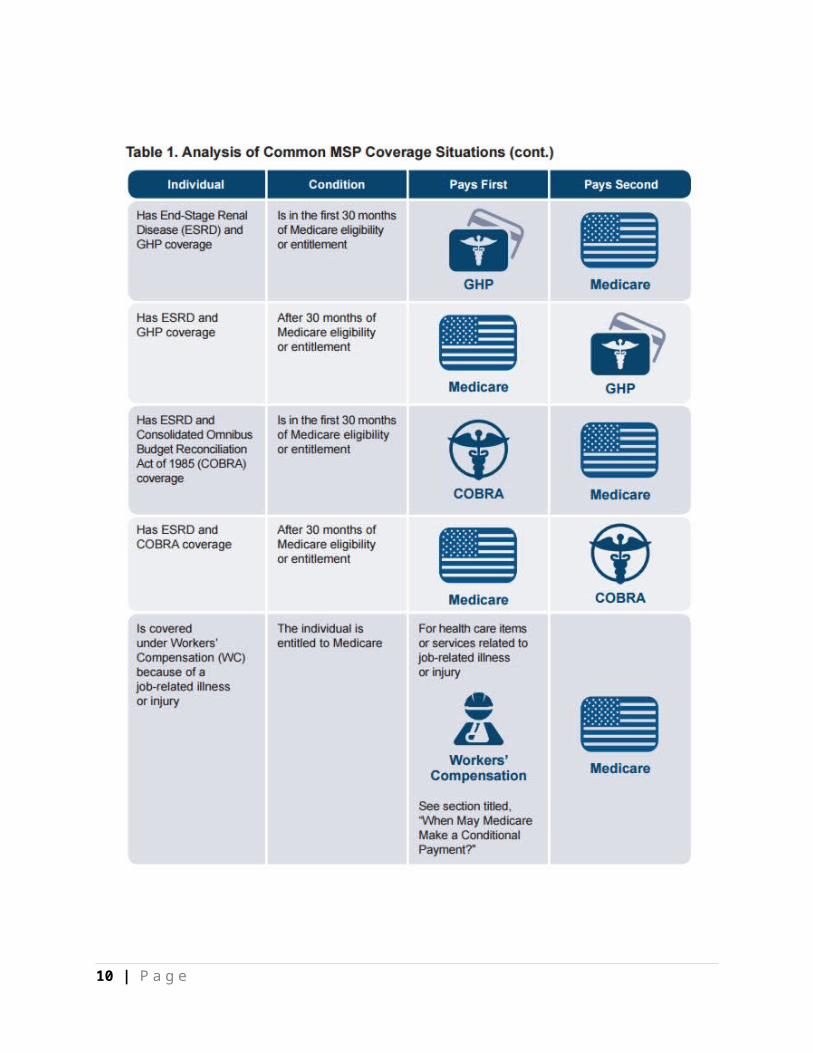

MSP – Medicare Secondary PayerThe MSP provisions protect the Medicare Trust Fund by ensuring Medicare does not pay for items and services when other health insurance coverage is primarily responsible for paying. The MSP provisions apply to situations where Medicare is not the primary or first payer of claims.

Are There Any Exceptions to the MSP Provisions?

There are no exceptions to the MSP provisions. Federal law takes precedence over State laws and private contracts. Even if an entity believes it is the secondary payer to Medicare due to State law or the contents of its insurance policy, the MSP provisions apply when billing for services.

What Happens if the Primary Payer Denies a Claim?

n the following situations, Medicare may make payment, assuming the service is a Medicare-covered and payable service and the provider files a proper claim: •

6 | P a g e

A no-fault or liability insurer does not pay during the “paid promptly” period or denies the medical bill;

A WC program denies payment (for example, where WC excludes a particular medical condition);

The beneficiary has exhausted a WC Medicare Set-Aside Arrangement (WCMSA);

A GHP denies payment for services because: o The beneficiary has exhausted plan benefit services;o The beneficiary has no coverage under the GHP; o The beneficiary needs services not covered by the GHP.

When submitting a claim to Medicare in these situations, you should include information showing why the other payer denied the claim, made an exhausted benefits determination, or both.

7 | P a g e

8 | P a g e

9 | P a g e

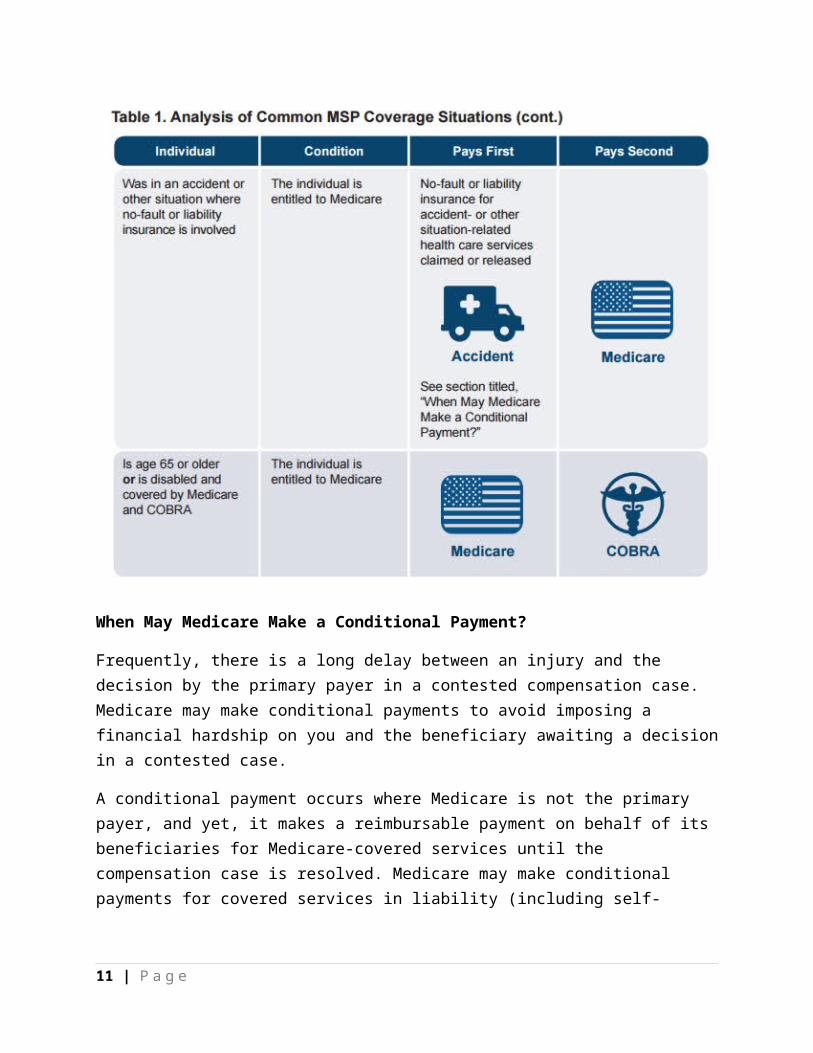

When May Medicare Make a Conditional Payment?

Frequently, there is a long delay between an injury and the decision by the primary payer in a contested compensation case. Medicare may make conditional payments to avoid imposing a financial hardship on you and the beneficiary awaiting a decision in a contested case.

A conditional payment occurs where Medicare is not the primary payer, and yet, it makes a reimbursable payment on behalf of its beneficiaries for Medicare-covered services until the compensation case is resolved. Medicare may make conditional payments for covered services in liability (including self-insurance), no-fault, and WC situations under the following circumstance:

Liability (including self-insurance), no-fault, or WC insurer is responsible for payment;

The claim is not expected to be paid promptly.

10 | P a g e

INSURANCE TERMINOLOGYHSA

Health Savings Accounts (HSAs) were created in 2003 so that individuals covered by high-deductible health plans could receive tax-preferred treatment of money saved for medical expenses.EOB

Explanation of Benefits (EOB). An EOB does look like a bill. It contains the date of service, the code used to bill a particular service to an insurance company, the fee charged by the healthcare provider, the allowed amount under the third-party payers’s contractual fee schedule, the patient’s responsibility under the terms of their coverage, the payment made by the payer, and the contractual write-off. The final entry of each line item is usually the titled something along the lines of, “what you owe,” or, “your responsibility.” This is why some patients confuse an EOB with a medical bill. Like most medical billing transactions, EOBs consist of medical code, not only the Healthcare Common Procedure Coding System (HCPCS Level I and Level II) codes, but also explanation codes that have been established by the Healthcare Portability and Accountability Act of 1996 (HIPAA). These explanation codes are easily understood by professional medical billers who are schooled in the language of healthcare reimbursement, but they are a mystery to laypeople who only encounter them in EOBs. While each EOB normally includes a definition of the adjustment and adjudication codes, they are often in fine print and their definitions are not always apparent to a person unfamiliar with reading them.

Coordination of Benefits

Coordination of benefits (COB) allows plans that provide health and/or prescription coverage for a person with more than one insurance to determine their respective payment responsibilities (i.e., determine which insurance plan has the primary payment responsibility and the extent to which the other plans will contribute when an individual is covered by more than one plan).

11 | P a g e

Primary Insurance

Primary insurance coverage protects against medical expenses up to the policy's limit, regardless of whatever other insurance you hold. The primary insurance coverage always kicks in first before any secondary insurance coverage begins. Such secondary policies come into play only once the primary insurance coverage has been completely exhausted.Secondary Insurance

Supplemental or secondary health insurance is merely another policy that serves to “wrap around” your primary healthcare policy. When you’re sick, your primary insurer picks up the brunt of your medical expenses and is usually billed by your care provider. Your doctor then bills you for any additional charges, such as copays or coverage limits, your primary insurer won’t spring for. If you have secondary insurance, you may then submit these charges to that insurer for reimbursement. While your secondary insurance may not cover all of your out-of-pocket costs, it can help defray large expenses in many cases.Tertiary Insurance

The word "tertiary" literally means "third," so a tertiary insurance policy provides coverage beyond an insured party's primary and secondary policies. The tertiary insurance company works with the other two insurers on "coordination of benefits," an agreement on which company will pay which part of a claim. A tertiary insurance policy kicks in only when the primary and secondary policies are inadequate.

Indemnity Insurance

Indemnity plans allow you to direct your own health care and visit almost any doctor or hospital you like. The insurance company then pays a set portion of your total charges. Indemnity plans are also referred to as "fee-for-service" plans. Under an Indemnity plan, you may see whatever doctors or specialists you like, with no referrals required. Though you may choose to get the majority of your basic care from a single doctor, your insurance company will not require you to choose a primary care physician. An

12 | P a g e

Indemnity plan may also require that you pay up front for services and then submit a claim to the insurance company for reimbursement.

You'll likely be required to pay an annual deductible before the insurance company begins to pay on your claims. Once your deductible has been met, the insurance company will typically pay your claims at a set percentage of the "usual, customary and reasonable (UCR) rate" for the service. The UCR rate is the amount that healthcare providers in your area typically charge for any given service.

Authorizations

An authorization is an approval of medical services by an insurance company, usually prior to services being rendered. For services that require an authorization, if no authorization is obtained, there is no guarantee that the insurance company will pay for the procedure.

Medical Necessity

Medical necessity refers to a decision by your health plan that your treatment, test, or procedure is necessary for your health or to treat a diagnosed medical problem. Most health plans will not pay for healthcare services that they deem to be not medically necessary. The most common example is a cosmetic procedure, such as the injection of medications (such as Botox) to decrease facial wrinkles or tummy-tuck surgery. Many health insurance companies also will not cover procedures that they determine to be experimental, or not proven to work.

MEDICAID

EligibilityWho is eligible for Medicaid coverage? People need to meet certain eligibility criteria to qualify for Medicaid in North Carolina:

Citizenship or a qualified alien Residency Type of person (eligible category) Income

In North Carolina, Medicaid only covers certain types of people, including: Pregnant woman

13 | P a g e

Child under age 21 Parents of dependent children Disabled (meet SSA disability definition) Elderly (65 or older) Women who have been diagnosed with breast or cervical cancer

through a Breast and Cervical Cancer screening program

There are other, more limited programs, for specific populations Family planning Certain people automatically receive Medicaid because they are getting other federal benefits. This includes:

Older adults or people with disabilities who are receiving Supplemental Security

Income (SSI) paymentsNote: SSI is not the same as Social Security disability or retirement paymentsBoth Social Security and SSI are administered through the Social Security Administration, but SSI is for low-income people. Social Security income or Disability payments are based on past contributions into the Social Security system

NPI and Carolina ACCESSIf a Carolina ACCESS beneficiary is referred to another provider, the NPI of the referring Carolina ACCESS provider must be included on all claims. If the beneficiary is enrolled with an individual provider, obtain the individual provider’s NPI. If the individual is enrolled with the healthcare practice, use the practice’s NPI.

Pre-Registration and Verification of BenefitsPre-Registration consists of:

Obtaining demographic and insurance information prior to a patients hospital visit.

Demographic and Insurance Information can be obtained from the patient or referring doctor’s office.

Verification of Insurance eligibility and pre-certification must be obtained.

14 | P a g e

Determining if there is any financial responsibility, if so payment arrangements can be made prior to visit.

Online services for the patient to complete themselves. Financial Counseling. Scheduling. Performing up front ABN checking and or medical

necessity review. Setting standards to assure completing the registration

within three days after scheduling.

Verification of Benefits: Verification of Benefits is to verify if the patient has

coverage for specific services Verification of Benefits also checks to see how much

the insurance will pay for the specific services. Verification of Benefits is as important as verifying a

patients insurance coverage. Insurance companies may not pay for certain services although the patient does have insurance coverage.

Each patient has their own specific insurance policy; coverage will vary depending on the patients plan. This is why verifying a patients benefits is very important.

Service Excellence and Customer Service

Achieving excellent levels of service includes the daily practice of living our service standards.Through Service Excellence We:♦ Provide exceptional levels of customer service to all customers

15 | P a g e

♦ Communicate our commitment to respect, kindness and compassion♦ Show people that excellent service is as important as quality care

Standards of Service Excellence

Service standards translate our mission, vision and values into specific behaviors.Through these standards, we are accountable for building a strong and respectful relationship with all our customers.Achieving our vision of service excellence means you know and apply the standards every day. This shows our commitment to quality healthcare.COURTESY

Treat people with the respect we want our loved ones to receive• Always be empathetic to each person you come in contact

with. No one comes to the hospital for fun, there is a reason and it is serious.

• Make eye contact with and acknowledge each person you pass in

hallways and public areas.• Immediately acknowledge customers in your work area.• Allow customers to exit and enter doorways and elevators first,

and hold doors open for them.

DIRECTIONS

Ensure people get where they need to go• Be familiar with the physical layout of the campus and the

location of Departments and services.

16 | P a g e

• Approach anyone who looks lost or hesitant and ask, “May I help you?”

• Always try to escort customers to their destination and use the walk time to make them feel welcome.

CUSTOMER WAITING

Minimize waits as much as possible• Respond to call lights, doorbells, intercom systems, and

telephone requests immediately.• Provide customers with estimates of expected wait times and

regular status updates.• If delays occur, take responsibility and apologize.• Keep waiting areas clean and comfortable with access to

reading materials.

Providing Information/Communication

Remember patients and their families are in an unfamiliar and often intimidating environment

Always introduce yourself by stating your full name, role and department.

Ask questions to better understand and restate your understanding of what’s been said.

When sharing information, communicate in terms and language that the customer can understand.

If you don’t have the information the customer needs, follow-up with someone who does.

• Appreciate the emotional state of our customers.• Learn about your facilities and services so that you can provide better information to others.• Learn your facility’s procedure for requesting interpreting services.17 | P a g e

Environment & Cleanliness

Everything Speaks – a dirty bathroom can equal a dirty OR to a patient• Never walk past trash on the floor – stop and pick it up.• Report immediately to Plant Facilities any broken furniture, nonfunctioning equipment, repair needs, or poor lighting.• Clean up spills and/or report them to Environmental Services.• Keep work area clean, neat, and orderly.

Privacy, Respect & Dignity

Purposefully protect our patient's privacy and dignity at all times Knock and wait for an answer before entering a patient’s

room, an exam room, or a workspace. Close curtains and doors when examining or treating

patients, or interviewing or counseling patients and families.

Provide patients and families with privacy to deal with emotions, spiritual needs, and decisions regarding care.

Be culturally sensitive to the needs of a diverse population.

Professionalism

You represent the hospital to your patients; they base their perceptions on YOU• Keep your promises

18 | P a g e

• Speak positively of our facilities, fellow employees, physicians, and support services.• Acknowledge each member of the patient care team as a valuable and “manage up” by assuring patients Dr X ranks highly in his field, your nurse Y is one of the best and she will take great care of you etc

Telephone Courtesy

Meet the needs of our callers quickly and accurately• Answer phones within 3 rings.• Use your most pleasant voice.• Offer a greeting (good morning/afternoon), identify yourself, your department, and offer assistance.• Ask for permission and wait for an answer before placing a caller on hold.• Provide updates every 30-45 seconds for callers on hold.• Tell the customer where they are being transferred and the extension.• Confirm that you have written messages accurately.Peer Relationships

It takes a village to make a healthcare facility great• Respect and appreciate cultural differences among fellow staff members.• Remain open-minded and listen to each other’s points of view.• If disagreements occur between staff members, take them to a private area. 19 | P a g e

• Address issues with each other in a direct, prompt, and timely manner.• Recognize and acknowledge the individual expertise of all team members.

SERVICE RECOVERY

Problems are an opportunity to develop relationships. People are more forgiving of an error properly corrected. In fact, people are more unforgiving of an error when no attempt to fix it is made than that the error was even committed. When things don't go perfectly, we work quickly to make things rightBe sincere about resolving customer service problems.Complaints are really wonderful opportunities to develop customer loyalty. Just remember that it doesn’t count if you don’t really mean it.Always understand the value of your service to your customers.Understanding what is really important to the customer will always vary and it is dangerous to make assumptions. Talk to the customer to gain clarity on what will make him feel he has received value.Find the humor in daily occurrences and share them with othersEvery time we laugh and include others, our stress level is lowered. It distracts your attention, changes attitude and outlook on life, causes relaxation and reduction of tension.

20 | P a g e

Patient Experience/Customer Service

When we talk about Patient Access, we’re referring to all the things patients have to deal with before they can engage with their clinicians. These include scheduling, working with the care options that are presented to them, and navigating the pre-visit process. Each stage of this three-part journey is shaped by a series of factors that set the tone for the patient’s trip through the system. The patient experience always starts with Patient Access!SOFTEN your patient experience!

S-smile O-open posture F-facial expression T-touch E-eye contact N-nod

Smile Smiles are contagious: It’s not just a saying: smiling really is contagious. In a study conducted in Sweden, people had difficulty frowning when they looked at other subjects who were smiling, and their muscles twitched into smiles all on their own.Open PostureOpen posture is a posture in which the vulnerable parts of the body are exposed. The head is raised and arms are uncrossed. Open posture is often perceived as communicating a friendly and positive attitude. Facial ExpressionThe face communicates our most basic emotions. Our facial expressions are designed to communicate our most basic yet necessary emotions for survival.

21 | P a g e

TouchTouch is the first sense to develop in humans, and may be the last to fade. There are approximately 5 million touch receptors in our skin- 3000 in a fingertip. A touch of any kind can reduce the heart rate and lower blood pressure.Eye ContactOften what is not spoken out loud is expressed in the eyes. Eye contact is meaningful and important sign of confidence and social communication. NodA nod of the head is used to indicate agreement, acceptance, or acknowledgment.

You are This Hospital…

You are what the people see when they arrive.Yours are the eyes they look into when they are frightened and lonely.Yours are the voices people hear when they ride the elevators and when they try to sleep and when they try to forget their problems. Your comments are the ones they hear on their way to appointments that could affect their destinies and what they hear after they leave those appointments.Yours are the comments people hear when you think they can’t.Yours is the intelligence and caring that people hope they’ll find here. If you’re noisy, so is your hospital. If you’re rude, so is your hospital. And, if you’re wonderful – so is Your Hospital.No visitor, no patient, no other employee can ever know the real you, the you that you know is there – unless you let them see it. All they can know is what they see and hear and experience. 22 | P a g e

And, so everyone at Your Hospital has a stake in your attitude and in the collective attitudes of everyone who works at Your Hospital. We are all judged and measured by your performance…..and that is the care you give, the attention you pay and the courtesies and empathy you extend. Taken from “you are this medical center”Wendy Leebov & Gail Scott

POS Study Guide

What is Point of Service (POS)? This is money that is collected at the time of service.Why collect at Point of Service?

Payor agreements require customer to pay their out-of-pocket expenses (co-pays, deductibles, co-insurance, etc.) at the Point-of-Service

Healthcare providers are obligated to collect these amounts (in accordance with their contracts), thus increasing payor compliance.

POS Collections takes minimal effort, but can yield high benefits.

POS Collections increases cash flow.

Things to know:

23 | P a g e

Once the patient leaves the institution, the value of that uncollected payment decreases, because of:

Loss of urgency/importance at time of service Cost of statements Cost of credit letters Cost of billing/follow-up staff Collection agency commissions Lost investments (time value)

How to collect $$$

Be positive and professional in all contacts Choose words wisely and be upbeat yet direct (Do not ask

“IF” they would like to pay, but “How” they would like to pay)

Convey a sense of urgency Ask for money with Confidence Use Motivators = Pride, Fear, Sense of Fairness, Saving

Additional Time & Expense Communicate convenience for the patient Listen and look for clues Make sure you have options to offer to the patient. Patients

can live with a NO if it is softened by alternatives Determine the ability of self-pay patients to make payments Speak in terms of solutions

Final tips:

Maintain a positive attitude Be simple and brief

24 | P a g e

Build understanding with the patient (Know their name) Ask questions that give you “YES” answers Keep control of the conversation Involve the patient in finding solutions Offer alternatives (other sources of payment) Overcome objections by actively listening for the real

problem and finding the solution (Why aren’t they paying their bill?)

Make action your message

WAYFINDINGIn small medical facilities, way finding may refer to a signage system that directs patients, family, and visitors to their destinations. As medical facilities expand, the physical environment may be very complicated. Directions that seem self-evident to employees and people who are familiar with the facility may be confusing to others.

Way finding also encompasses such issues as: directions and alternate means of transportation to the

facility location of parking and patient drop-off points in relation to

the location of the service area campus maps visual cues (such as color-coding and repetitive designs)

Way finding can be categorized as a: User experience: the experience of orienting and choosing a

path, self-navigating through the surroundings, going from point-to-point along a predetermined route

25 | P a g e

- Process: the process of generating a design solution providing aids to assist the navigational process.

Tools often include maps/user guides, audible communication/written directions, tactile elements, consistent simplistic terminology and environment graphics

Plan: the plan includes recognizing the human factor and bringing communication to the lowest common denominator including provisions for users unfamiliar with their environment who are under stress and may have special needs such as being visually impaired

System: recognizing that the plan takes careful orchestration, preplanning and commitment

Effective way finding through a medical facility can help alleviate anxiety among patients and reduce strain on staff who are less likely to be needed to provide directions. Way finding tools should be compliant with ADA (Americans with Disabilities Act), JCAHO and other governing agencies and regulations. One trend in way finding is interactive digital signage—the use of electronic kiosks and flat-panel screens that display instantly updated information. In a hospital setting, where patients and visitors are searching for department locations that may change frequently,

ORDER ENTRYAlthough Computerized Physician Order Entry (CPOE) is more and more common in health care, Patient Access still may need to process handwritten physician orders. Entering orders for clinical services into the healthcare information system frequently involves some interpretation. When a physician's terminology does not match the expected standard, some follow up communication may be required.

Charge Capture

26 | P a g e

What is Charge Capture? The definition is simple: it’s the capture of information for use in a medical claim document, a critical element of the overall revenue cycle. Charge capture is the process of electronically or manually applying appropriate predetermined fees associated with service delivery. This can include order entry, charge entry, verification and charge correction. The process must assure charges are accurately applied to the correct account so that the process flows effectively to billing.

BILLING

Billing is the process of collecting and presenting to the payor all agreed upon data elements that are necessary to secure payment for services rendered. This Includes initial billing, follow-up, cash posting, and management of accounts receivable. Patient access needs to be aware of the various types of insurance plans to ensure accurate information is obtained and entered in the system for billing.

A persistent problem for hospitals is the high percentage of claims that payors reject resulting from inaccurate data entered during registration. For many hospitals, these inaccuracies remain the number one cause for claims being rejected or denied.

Additionally, incorrect Critical Data Elements (CDEs) result in returned mail and make it difficult to perform routine collection activities with the patient.Some of the Critical Data Elements that are commonly entered in error include:- Patient name on claim not matching patient name on file with payor- Incorrect or missing Member ID- Claim submitted to wrong payor (e.g. traditional Medicaid versus Medicaid HMO)- Incorrect address- Missing or incorrect phone number(s)- Missing pre-cert/authorization/referral information needed in order to submit claim27 | P a g e

Confirming this information has been collected and is correct at time of registration eliminates many downstream issues associated with billing payors and collecting from the patient resulting in improvements to patient satisfaction.

Medical TerminologyIt is vital that patient access employees understand and accurately spell medical terms. Physician orders must be reviewed and the diagnosis and procedure information accurately captured to provide the appropriate service. Facilities distribute a list of approved abbreviations to both clinical and non-clinical staff in order to provide clarity to any abbreviations used in the patient’s medical record.

In addition to medical terminology, patient access employees should understand the classification systems used to translate narrative diagnosis and procedure information into universal numeric and alphanumeric codes that are used to process insurance claims and report specific clinical information to government and performance improvement organizations.

International Classification of Diseases, Tenth edition (aka ICD-10) was implemented on October 1, 2015. ICD-10-CM contains an increased number of codes (from Approximately 13,600 to 120,000) and categories that allow for a more specific and accurate representation of current and future medical diagnoses and procedures.

RED FLAG RULE

The Red Flags Rule tells you how to develop, implement, and administer an identity theft prevention program. A program must include four basic elements that create a framework to deal with the threat of identity theft.21. A program must include reasonable policies and procedures to

identify the red flags of identity theft that may occur in your day-to-day operations. Red Flags are suspicious patterns or

28 | P a g e

practices, or specific activities that indicate the possibility of identity theft.3 For example, if a customer has to provide some form of identification to open an account with your company, an ID that doesn’t look genuine is a “red flag” for your business.

2. A program must be designed to detect the red flags you’ve identified. If you have identified fake IDs as a red flag, for example, you must have procedures to detect possible fake, forged, or altered identification.

3. A program must spell out appropriate actions you’ll take take when you detect red flags.

4. A program must detail how you’ll keep it current to reflect new threats.

Just getting something down on paper won’t reduce the risk of identity theft. That’s why the Red Flags Rule has requirements on how to incorporate your program into the daily operations of your business. Fortunately, the Rule also gives you the flexibility to design a program appropriate for your company — its size and potential risks of identity theft. While some businesses and organizations may need a comprehensive program to address a high risk of identity theft, a streamlined program may be appropriate for businesses facing a low risk.Securing the data you collect and maintain about customers is important in reducing identity theft. The Red Flags Rule seeks to prevent identity theft, too, by ensuring that your business or organization is on the lookout for the signs that a crook is using someone else’s information, typically to get products or services from you without paying for them. That’s why it’s important to use a one-two punch in the battle against identity theft: implement data security practices that make it harder for crooks to get access to the personal information they use to open or access accounts, and pay attention to the red flags that suggest that fraud may be afoot.The most common red flags for healthcare access professionals are found in Personal Identifying Information.

29 | P a g e

Personal identifying information can indicate identity theft: inconsistencies with what you know — for example, an address

that doesn’t match the credit report or the use of a Social Security number that’s listed on the Social Security Administration Death Master File

inconsistencies in the information a customer has submitted to you

an address, phone number, or other personal information already used on an account you know to be fraudulent

a bogus address, an address for a mail drop or prison, a phone number that’s invalid, or one that’s associated with a pager or answering service

a Social Security number used by someone else opening an account

an address or telephone number used by several people opening accounts

a person who omits required information on an application and doesn’t respond to notices that the application is incomplete

a person who can’t provide authenticating information beyond what’s generally available from a wallet or credit report — for example, someone who can’t answer a challenge questionThe Joint CommissionThe Joint Commission is an independent, not-for-profit organization which accredits and certifies nearly 21,000 health care organizations and programs in the United States. Joint Commission accreditation and certification is recognized nationwide as a symbol of quality that reflects an organization’s commitment to meeting certain performance standards. TJC Mission: To continuously improve health care for the public, in collaboration with other stakeholders, by evaluating health care organizations and inspiring them to excel in providing safe and effective care of the highest quality and value. National Patient Safety Goal #1 - Identify patients correctly

30 | P a g e

Use at least two ways to identify patients. For example, use the patient’s name and date of birth. This is done to make sure that each patient gets the correct medicine and treatment. Make sure that the correct patient gets the correct blood when they get a blood transfusion.

REFERENCES

2008 National Patient Safety Goals, Hospitals, Goal 1. (n.d.). Retrieved from The JointCommission: www.thejointcommission.com

ICD-10 Frequently Asked Questions. (n.d.). Retrieved 2008, from ahima.org:http://www.ahima.org/icd10/faq.asp

Identity Theft Victim Complaint Data. (2007). Retrieved 2008, from ftc.gov:http://www.ftc.gov/sentinel/reports/idt-annualoverall-figures/idt-cy2006.pdf

Medicaid Program - General Information. (2006, April 25). Retrieved 2008, fromcms.hhs.gov: http://www.cms.hhs.gov/MedicaidGenInfo/

Medicare and Other Health Benefits: Your Guide to Who Pays First. (2008, May).Retrieved 2008, from http://www.medicare.gov/Publications/Pubs/pdf/02179.pdf

Medicare Beneficiary Notices Initiative. (2008, March 20). Retrieved 2008, fromhttp://www.cms.hhs.gov/BNI/02_ABNGABNL.asp

Patient Tracking / Patient Flow. (n.d.). Retrieved 2008, from awarepoint.com:http://www.awarepoint.com/patient-tracking-patientflow.shtml?gclid=CP7T24HQmpQCFQOjFQodjiSPtA

31 | P a g e