Student Loan Exit Session. Please complete and sign the Personal Data Sheet All forms will be...

25

Student Loan Exit Session

-

date post

20-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of Student Loan Exit Session. Please complete and sign the Personal Data Sheet All forms will be...

Student Loan Exit Session

Please complete and sign the Personal Data Sheet

All forms will be collected at the end of this session. If you do not have all the information necessary you can email the information to: [email protected]

Agenda

Loan Repayment Handbook Credit Stafford Loans Perkins Loan Cancellation Consolidation NU Private Loans Default

Your Credit

All of your federal loans are reported to at least one credit bureau.

Factors reported– Timeliness of your payment– Non payment – Outstanding balance

Credit Score

Loan Repayment Summary

Current Principal Balance

Accrued Interest

Repayment Interest

Date Interest

Capitalizes

Current Interest

Rate

Number of P & I

Payments

Estimated Monthly Payment

Monthy Payment

Starts

Federal Subsidized Stafford Loan8,500.00 2,170.00 4.70% 120 89.00 Oct-06

Federal Unsubsidized Stafford Loan10,000.00 855 2,553.00 11/1/2006 4.70% 120 105.00 Oct-06

Federal Perkins Loan12,000.00 3,600.00 5.00% 120 130.00 Mar-07

SUPSL21,824.00 1,360.58 6,598.00 8/30/2006 5.50% 120 237.00 Sept/Oct 06

GPAL28,901.00 1,002.31 9,602.00 8/30/2006 6.00% 120 321.00 Sept/Oct 06

Federal Stafford Loans

Interest rates are variable and are subject to change every July 1st

6 month grace period Subsidized Stafford loan will accrue

interest after the 6 month grace period Unsubsidized Stafford loan has accrued

interest since initial disbursement Accrued interest will capitalize at the end

of the 6 month grace period 10 Year term

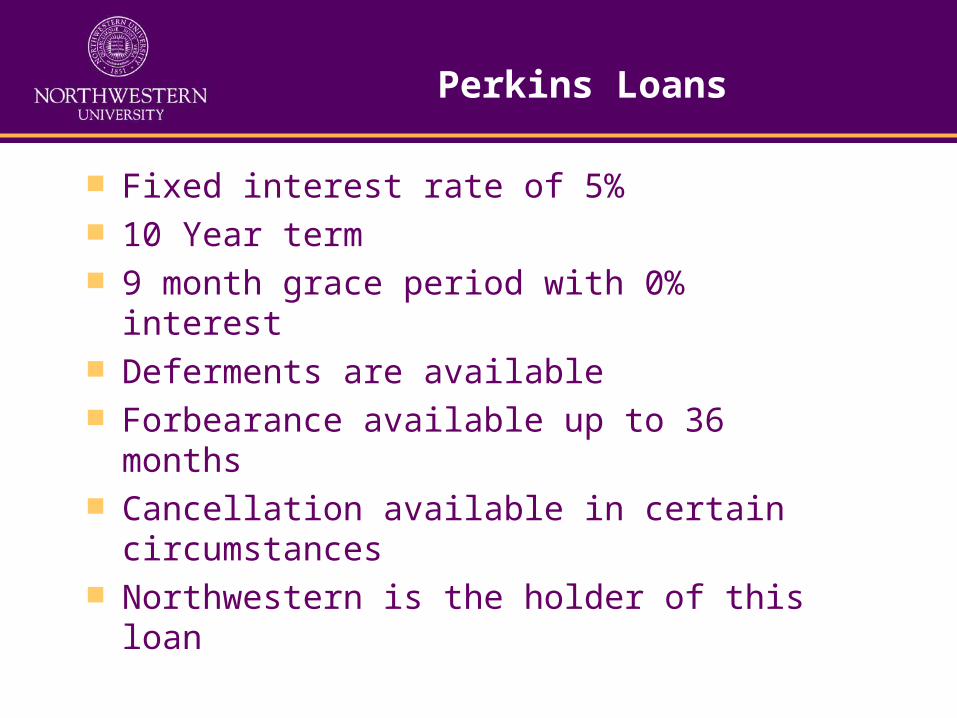

Perkins Loans

Fixed interest rate of 5% 10 Year term 9 month grace period with 0% interest Deferments are available Forbearance available up to 36 months Cancellation available in certain

circumstances Northwestern is the holder of this loan

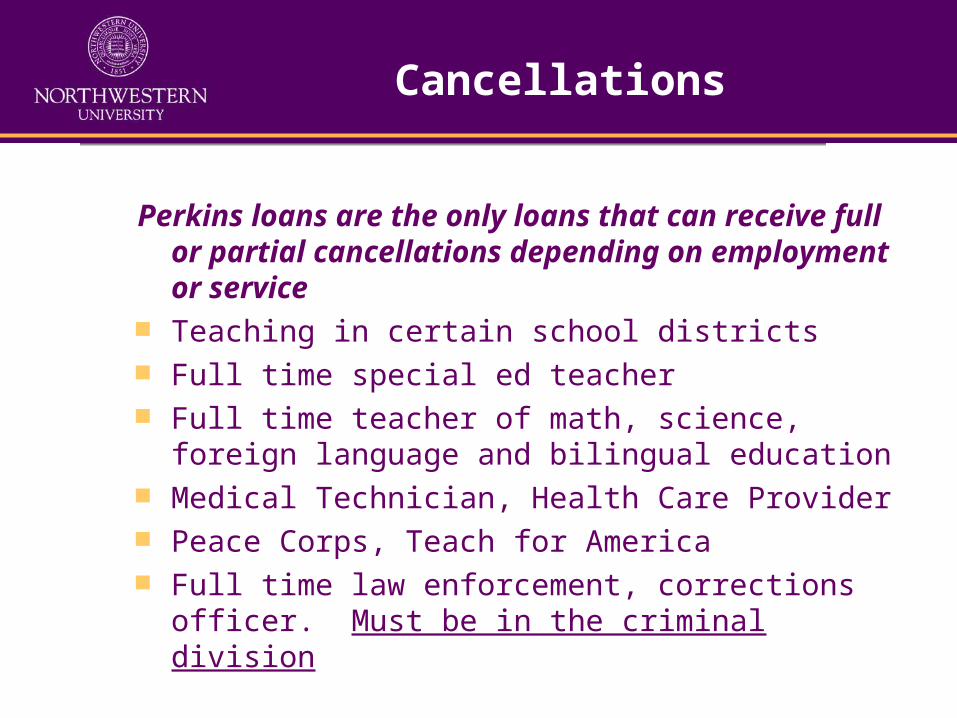

Cancellations

Perkins loans are the only loans that can receive full or partial cancellations depending on employment or service

Teaching in certain school districts Full time special ed teacher Full time teacher of math, science, foreign

language and bilingual education Medical Technician, Health Care Provider Peace Corps, Teach for America Full time law enforcement, corrections officer.

Must be in the criminal division

Repayment Schedules

Standard Repayment– Ten year maximum– Fixed Schedule of monthly payments– Minimum $50 monthly payment

Graduated Repayment– Monthly schedule starts with small payments that

increase gradually over time– You will pay a higher total interest

Extended Repayment Income-Sensitive Repayment

Approximate Monthly Payment(using maximum interest of 8.25% over 10

years)

Amount Borrowed Monthly Payment&Interes

t

Total Principle and Interest

$5,000 $61 $7,359

$15,000 $184 $22,077

$25,000 $307 $36,796

$40,000 $491 $58,873

$65,000 $797 $95,669

$90,000 $1,104 $132,465

Payment Estimate and Other Calculators

www.mapping-your-future.org/features/loancalc.htm

www.salliemae.com

To Obtain Additional Information

of Your Loans

Access information about Federal Loans, outstanding balances, disbursements, loan status, and holder by checking with the National Student Loan Data System (NSLDS)

www.nslds.ed.gov

Consolidation

Consolidation allows you to: Combine all your eligible federal

education loans into a new loan with a single payment

Lengthen the payback period up to 30 years and reduce your monthly payment

Stafford and Perkins loans are eligible for consolidation.

Do not consolidate your Perkins loanif you qualify for full or partial cancellation

When can borrowers consolidate?

Anytime during the post-school, six month grace period

Anytime during repayment During a period of deferment or

forbearance In-school status

Advantages and Disadvantages of Loan Consolidation

Advantages– Possible lower interest

rate– May choose to lower

the monthly payment by extending the term (up to 30 years depending on size of loan

– Single Payment to one lender

Disadvantages– In many cases a loss

of borrower benefits or incentives earned on the Stafford Loans

– Loss of some deferment benefits

– In some cases a loss of the grace period

– In some cases if the term is extended you will pay more interest

What should I consider before I make the decisions to Consolidate my

Perkins Loan? Perkins loans have a 9 month grace

period. If you consolidate your other loans before their 6 month grace period expires, you can add the Perkins within 180 days of the consolidation

Loss of interest subsidy during periods of deferment (Subsidized Stafford loans do not lose interest subsidy on that portion of the loan during periods of deferment)

Consider the impact of the Perkins on the interest rate for the Consolidation Loan since it is a weighted average

Possible loss of eligibility for cancellations/loan forgiveness

What to look for when choosing a Consolidation Lender

Make sure it’s a FEDERAL consolidation program If all of the borrowers loans are currently held by

one lender, they must consolidate through that lender unless they do not offer a consolidation program

What are the repayment incentives, if any? What payment options do I have?Online?Phone? What kind of customer service will I get? Are late fees charged for delinquent payments? If

so, how much?

NU Loan

Formerly known as the Parent/Student loan Interest rates are variable and change every

Sept. 1st Interest accrues from date of first disbursement.

Unpaid interest will be capitalized at the end of the 3 month grace period.

10 Year repayment term NU Loans are eligible for forbearance only

NU Loans Cannot be consolidated

What can I do if I am not able to make payments?

There are times when you might have trouble making your loan payments. To help you through difficult financial times, deferments and forbearances are available.

DefermentsStafford and Perkins

Deferment: allows you to postpone payments for several reasons including:

Returning to school– deferments are unlimited

Unemployment and Economic Hardship– deferments available up to 36 months

Subsidized Stafford loans do not accrue interest during periods of deferment.

Unsubsidized Stafford loans accrue interest and interest is capitalized at the end of the deferment period if it is not paid.

Keep full term of loan

ForbearanceAll Student Loans

6 month intervals for a period up to 3 years.

Receiving forbearance results in higher payments once forbearance ends.

Interest will continue to accrue and will be capitalized if eligible at the end of the forbearance period if it is not paid.

Term is lost

Default Consequences

Your academic records will be placed on hold.

You may have to pay additional collection costs after your loan is assigned to a private collection agency for collection.

You may be subject to Administrative Wage Garnishment.

You may be sued with court costs and legal fees added to your balance.

Your income tax refund may be withheld.

Your credit rating and ability to borrow will be seriously damaged.

You may lose future eligibility for financial aid and student loans.

Your professional license could be denied or revoked.

You may be denied certain jobs.

My Responsibilities

KEEP IN TOUCH WITH YOUR LENDERS/ SERVICER Notify lender of change in demographic

information or if unable to make payments for ANY reason

Make payments even if you have not completed the program

Make payments even if you are unable to obtain employment upon completion

Make payments even if dissatisfied with the quality of the school’s programs and services

Make payments even is a billing statement is not received

Student Loan Office

For students with Perkins and NU Loans

We have outsourced our billing to Campus Partners in March

On their website, http://mycampusloan.com

you can check your account status and pay online

Good luck in all your future endeavors!