Lessons Learnt from Indonesia Vocational Education Strengthening Project by Agung Susanto.pdf

Upload

oecd-governanceCategory

view

234download

0

MINISTRY OF FINANCE

REPUBLIC OF INDONESIA

Strengthening Performance Information for Better Budget Allocation: The Indonesian Experience

Bangkok, 17-18 December 2015

Budgeting System Prior to the 2003 Budget Reform

What’s Next?

Outline

Implementing the Reform

2003 Budget Reform Goals

Moving forward: the Improvement Stage (Introducing ADIK)

2

WB and IMF evaluation in 2000 indicated several weaknesses of previous budgeting system:

• indiscipline in budget implementation (dual budget system)

• no fiscal sustainability the budgeting system was for a single year and used the incremental approach to allocate the budget for the following fiscal year

• inefficiency in budgeting practice no standard cost

• the issue of transparency budget allocations for ministries were not publicly available

• lack of accountability specific program design was not always available; one program was often used by more than one ministry

3

Budgeting System Prior to the 2003 Budget Reform

4

• Government’s focus was turning towards improving the delivery of public services and infrastructure to support development

This includes both the setting and monitoring of high-level objectives, as well as mechanisms of downward accountability, such as performance reports for line ministries along with greater flexibility in managing their programs (reform spirit was ‘let the managers manage’)

• Improving budget transparency level to parliament

Prior to the PFM reforms, parliament can only engage at the program level, while activities were government’s discretion. The PFM reform abolished this ‘rule of engagement’ with the goal of opening up the budget to the ‘output’ level

In practice, parliament engaged at the input level, which contradicted the reform goals

2003 Budget Reform Goals

Pillars in Budget Reforms

5

Pillars Targets

Unified budget budget discipline

Performance Based Budgeting efficiency accountability

Medium Term Expenditure Framework (MTEF) fiscal sustainability transparency

6

Implementing the Reform

7

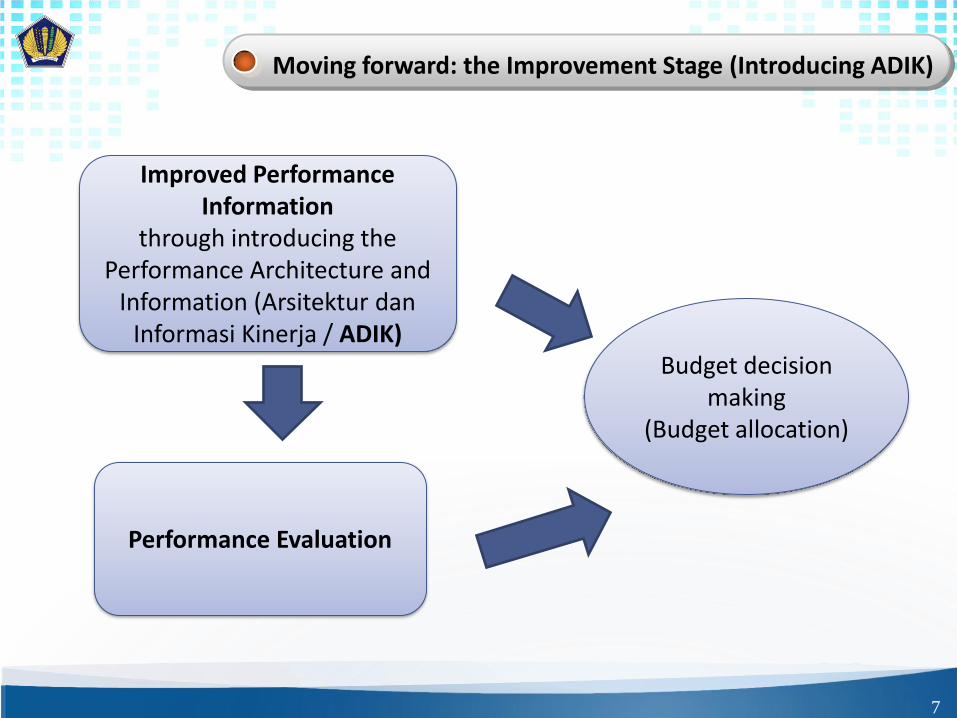

Improved Performance Information

through introducing the Performance Architecture and

Information (Arsitektur dan Informasi Kinerja / ADIK)

Performance Evaluation

Moving forward: the Improvement Stage (Introducing ADIK)

Budget decision making

(Budget allocation)

8

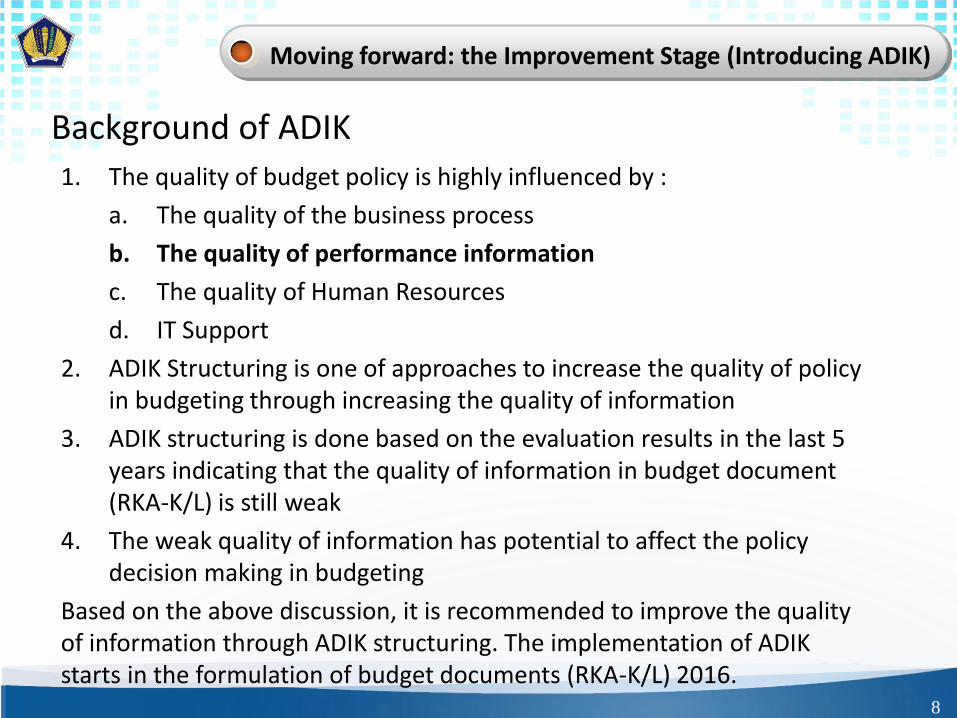

Background of ADIK

1. The quality of budget policy is highly influenced by :

a. The quality of the business process

b. The quality of performance information

c. The quality of Human Resources

d. IT Support

2. ADIK Structuring is one of approaches to increase the quality of policy in budgeting through increasing the quality of information

3. ADIK structuring is done based on the evaluation results in the last 5 years indicating that the quality of information in budget document (RKA-K/L) is still weak

4. The weak quality of information has potential to affect the policy decision making in budgeting

Based on the above discussion, it is recommended to improve the quality of information through ADIK structuring. The implementation of ADIK starts in the formulation of budget documents (RKA-K/L) 2016.

Moving forward: the Improvement Stage (Introducing ADIK)

Why Changing the Architecture? (1)

9

1. The existing architecture of RKA-K/L has been applied since 2005.

2. Through that existing architecture, the transition from dual budgeting to unified budgeting run well.

3. The existing architecture has introduced the concept of performance information (outcome and output) used in the implementation of performance-based budgeting.

4. In 2009, restructuring of programs and activities was carried out. It was done because the evaluation on budget documents from previous years indicated that many programs and activities were not suitable and not focused on the target of organization.

10

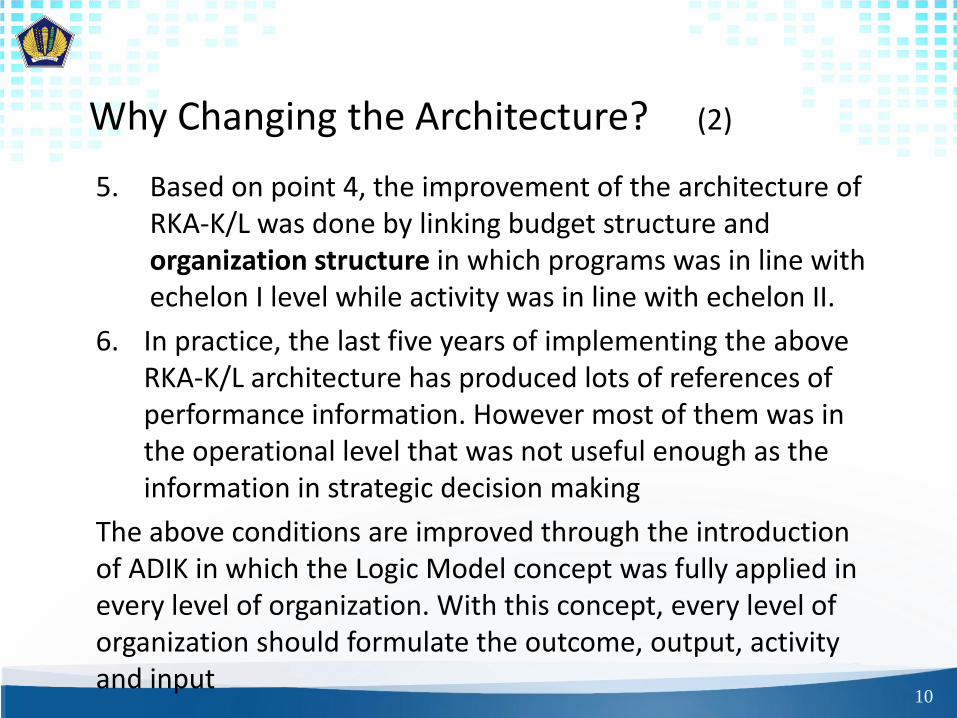

5. Based on point 4, the improvement of the architecture of RKA-K/L was done by linking budget structure and organization structure in which programs was in line with echelon I level while activity was in line with echelon II.

6. In practice, the last five years of implementing the above RKA-K/L architecture has produced lots of references of performance information. However most of them was in the operational level that was not useful enough as the information in strategic decision making

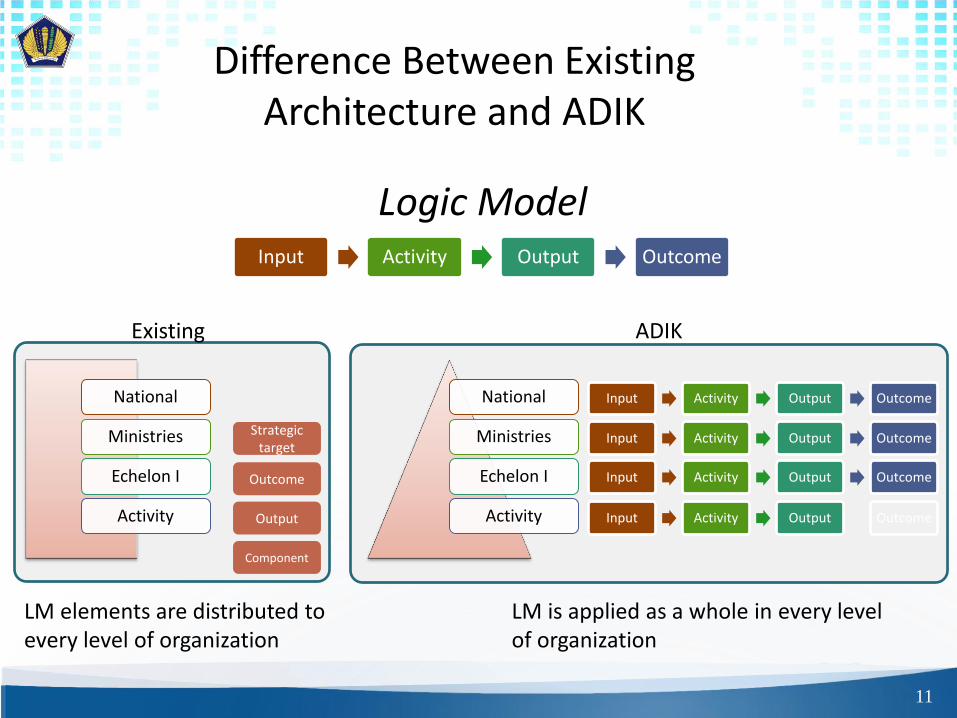

The above conditions are improved through the introduction of ADIK in which the Logic Model concept was fully applied in every level of organization. With this concept, every level of organization should formulate the outcome, output, activity and input

Why Changing the Architecture? (2)

Difference Between Existing Architecture and ADIK

Logic Model

11

Input Activity Output Outcome

National

Ministries

Echelon I

Activity

Input Activity Output Outcome

Input Activity Output Outcome

Input Activity Output Outcome

Input Activity Output Outcome

National

Ministries

Echelon I

Activity

Outcome

Output

Component

Strategic target

Existing ADIK

LM elements are distributed to every level of organization

LM is applied as a whole in every level of organization

Stages in ADIK Implementation (1)

12

1. The format of budget document (RKA-K/L) is adjusted a. Currently, there are Form I, Form II, dan Form III of the

new RKA-K/L that are in line with ADIK concept, but the format is not yet enacted in the formal form of RKA-K/L.

b. The adjustment of RKA-K/L format should be carried out in order to accommodated all information that has been set based on ADIK concept.

c. Without adjustment of RKA-K/L format, the following information cannot be clearly identified : • Output at the ministries level and Echelon I • Outcome and Output indicators is every level • Activity at Ministry and Echelon I level • Input in every level

13

2. IT Support (application) a. Currently, the ADIK application has been available and

integrated with existing RKA-K/L application. b. This application has been used by all ministries in structuring

data for ADIK. c. The data in Form III of ADIK has been used as the RKA-K/L

reference. While the data in Form I and II have not yet used.

3. Efforts that have been done by DG Budget in running ADIK structuring : a. Providing the manual guidance b. Capacity building for internal DG Budget c. Providing socialization and technical guidance to ministries

through workshops

Stages in ADIK Implementation (2)

Problems and Challenges

14

1. Difficulty in changing the mindset a. Line ministries are till trapped in existing structure

b. Still attempt to show off their task and function

2. Few Ministries are in the process of reorganization and function structuring.

3. Improved application is required >> The integration of performance information is still limited on form III of RKA-K/L, cannot be fully applied (on form I and II of ADIK).

4. There are generic outputs in the application of ministries work plan>> Thus the logic model framework cannot be fully applied.

5. Some outcome and output formulation are still not clear and similar >> Understanding strategic target as Output (the word “target” tends to lead ministries to formulating performance information of output like outcome,

15

In future, the technical steps is undertaken to integrate ADIK framework into budgeting process (and RKA-K/L)

1. Improvement on RKA-K/L Form:

Form I & Form II which were taken from Ministries work plan are derived from ADIK application

Form III is taken from ADIK application

2. Using Form I of ADIK in the Trilateral meeting

3. Revision on budget document (DIPA) is done through aplikasi ADIK Application (Form III), such as changing the nomenclature, adding/deducting output or satker,

Further improvement on current ADIK framework to continuously increase the quality of performance information

What’s Next?

Thank you

www.anggaran.depkeu.go.id

16