Strategic Transfer Pricing, Absorption Costing and ... · Chapter 15. Allocation of Support...

31

1 Chapter 15 Allocation of Support Department Costs, Common Costs, and Revenues

Transcript of Strategic Transfer Pricing, Absorption Costing and ... · Chapter 15. Allocation of Support...

1

Chapter 15

Allocation of Support DepartmentCosts, Common Costs, and Revenues

2

Cost allocation: what it means

Some production centers or departments provide output required by other production centers (Service departments).The costs of these departments are allocated to the internal users according to use and add to their costsso the costs of service departments providing these products and services go indirectly into the cost of saleable outputService department‘s costs are allocated using the actual utilization volume times an allocation rate per unit

3

Allocating Support Departments CostsAn operating department (a production department in manufacturing companies) adds value to a product or serviceA support department (service department) provides the services that assist other operating and support departments in the organization.

4

Secondary Activities

Dire

ctly

attr

ibut

able

fr

om g

ener

al le

dger

Add

ition

al c

ost

not o

ut o

f poc

ket

Product 1

PrimaryActivities

Product n

Attribution to cost pools of the centers; each activity has exactlyone cost driver

Usage × cost driver rate

Reciprocal services

Structure of Service Department Cost Attribution

(Traceablecosts)

Operatingdepartments

Supportdepartments

5

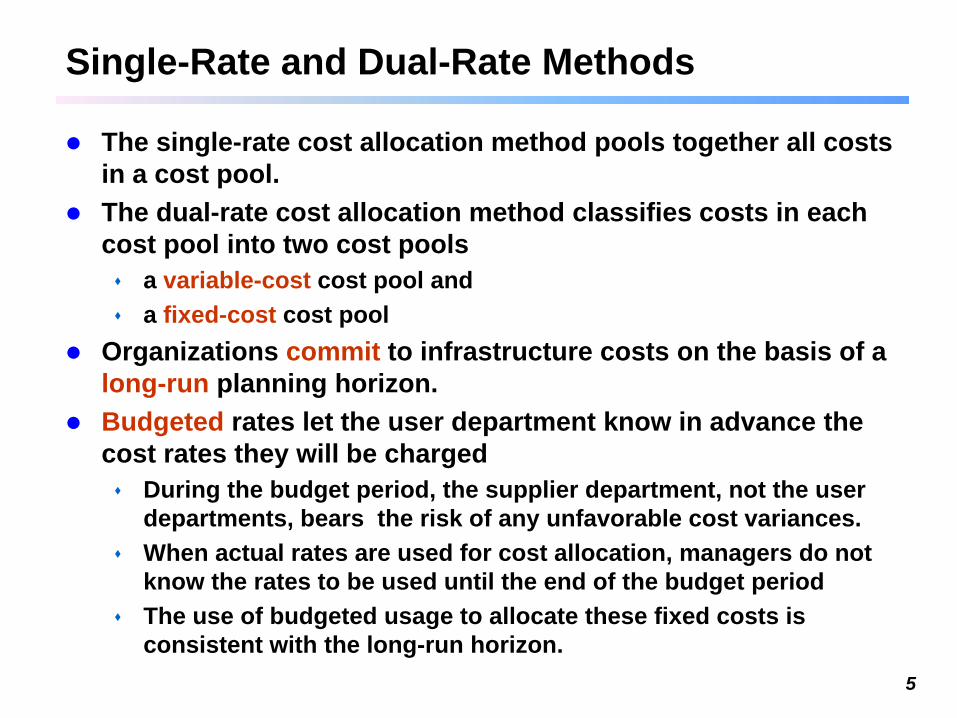

Single-Rate and Dual-Rate Methods

The single-rate cost allocation method pools together all costs in a cost pool.The dual-rate cost allocation method classifies costs in each cost pool into two cost pools

a variable-cost cost pool and a fixed-cost cost pool

Organizations commit to infrastructure costs on the basis of a long-run planning horizon.Budgeted rates let the user department know in advance the cost rates they will be charged

During the budget period, the supplier department, not the user departments, bears the risk of any unfavorable cost variances.When actual rates are used for cost allocation, managers do not know the rates to be used until the end of the budget periodThe use of budgeted usage to allocate these fixed costs is consistent with the long-run horizon.

6

Allocating Support Departments Costs

Direct method:Allocates support department costs to operatingdepartments only.

Step-down (sequential allocation) method:Allocates support department costs to other supportdepartments and to operating departmentscharge rates are calculated for support departments according to a rank order. Those departments rank highest that get the least from other departmentsat each step support is charged only from the departments whose charge rate has already been calculated

Reciprocal allocation method:Allocates costs by services provided among all support departmentssimultaneous equations approach

7

Example

The Canton Division of Smith Corporation has twooperating departments

Assembly and Finishingand two support departments

Maintenance• allocated using square feet.• Total square feet = 255,000

Human Resources• allocated using number of employees• Total number of employees = 95

Maintenance Human Resources Assembly Finishing

Budgeted costsbefore allocations: $300,000 $2,160,000 $1,700,000 $900,000Square feet: 5,000 30,000 110,000 110,000# of employees: 8 15 48 27

8

Direct Method

Support Departments Operating Departments

$1,700,000Assembly

$900,000Finishing

110/220

24/72

0% 0%

Maintenance$300,000

HumanResources$2,160,000

Assembly FinishingOriginal costs: $1,700,000 $ 900,000Maintenance Allocated: 150,000 150,000Human Resources Allocated: 1,440,000 720,000Total $3,290,000 $1,770,000

9

Step-Down Method

Which support department should be allocated first?Maintenance provides 12% of its services to Human Resources.Human Resources provides 10% of its services to Maintenance.

Maintenance to Human Resources:12% × $300,000 = $36,000

Maintenance to Assembly: 44% × $300,000 = $132,000Maintenance to Finishing: 44% × $300,000 = $132,000

Human Resources costs to be allocated become$2,160,000 + $36,000 = $2,196,000

Human Resources to Assembly: 48 ÷ 72 × $2,196,000 = $1,464,000

Human Resources to Finishing: 24 ÷ 72 × $2,196,000 = $732,000

10

Overhead Allocation Sheet (Step down method)

Costs from general ledger

+additional

non-out-of-pocket cost

S1S2 S3

S1 S2 S3 Sj

Primary activitiesSecondary activities

j does not use > j One line for eachkind of input used.Entries in each line sum up to the respective amountin the cost recording column

x1 x2 x3 x3

π2 π3 π3

Sum of column j:total cost of center j

Total cost drivervolume, center j

Cost driver rate

j = 1 j = 2 j = 3

π1 x12 π1 x13

π1 =S1 /x1

π2 x23... π3 x3j ...

Sum of row i = Si

Start

xij = aijxijusage of

i by j

Traceable costs

Cost driver rates

11

Reciprocal

M HR A FMaintenance – 12% 44% 44%Human Resources 10% – 60% 30%

Total Cost(j) = traceable cost (j) + Σ αij × Total cost(i)all i

where αij denotes j‘s share of total i‘s service

M = 300,000 + 0.10 HRHR = 2,160,000 + 0.12 M

M – 0.10 HR = 300,000– 0.12 M + HR = 2,160,000

10 M – HR = 3,000,000– 0.12 M + HR = 2,160,000

9.88 M = 5,160,000M = 5,160.000 / 9.88 = 522,267HR = 2,160,000 + 0.12× 522,267

= 2,222,672

12

Reciprocal

M HR A FBeforeallocation: $300,000 $2,160,000 $1,700,000 $ 900,000Allocation: (522,267) 62,672 229,797 229,797Allocation: 222,267 ($2,222,672) 1,333,603 666,802Total $3,263,400 $1,796,599

Total cost Assembly Department: $3,263,400Total cost Finishing Department: $1,796,599

13

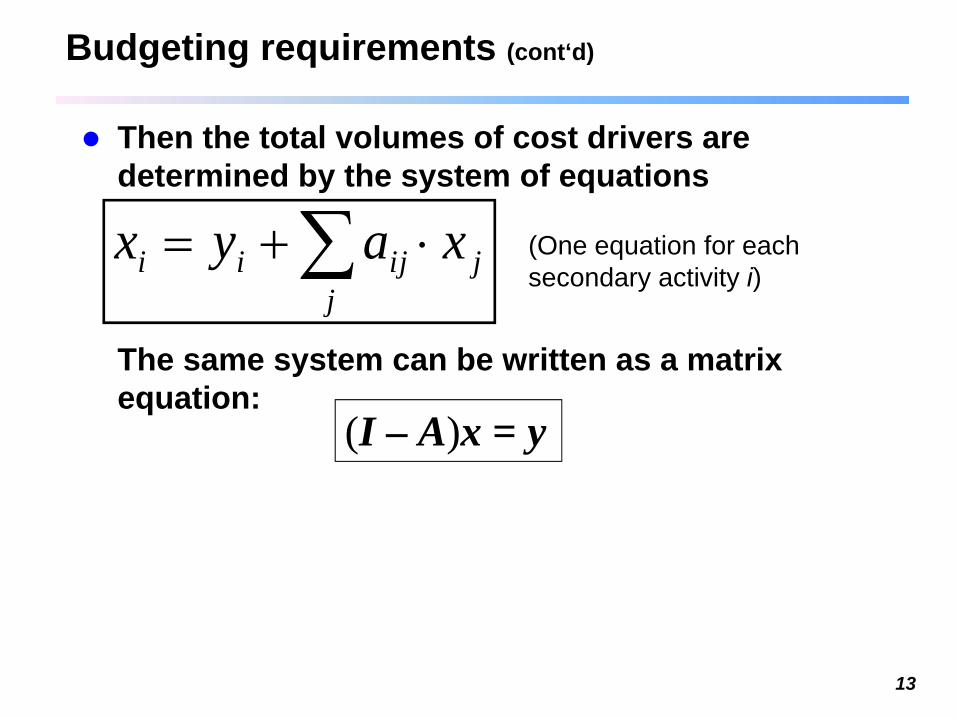

Budgeting requirements (cont‘d)

Then the total volumes of cost drivers are determined by the system of equations

The same system can be written as a matrix equation:

∑ ⋅+=j

jijii xayx (One equation for each secondary activity i)

(I – A)x = y

14

Cost driver rates πi

Activity account balance

Traceable costsKP

j

Cost of secondary activities

Service delivered

πj ·xj

Activity j

∑ ⋅i iji xπ

jji

ijij

Pj

jjji

jijiPj

jjji

ijiPj

axK

xxaK

xxK

ππ

ππ

ππ

=⋅+

⋅=⋅⋅+

⋅=⋅+

∑

∑

∑

≠

≠

≠

=: kPj

Pj

jiijij ka =⋅− ∑

≠

ππ

(I – AT)π = k

15

Example: „Fall River Company“*)

Service centers: Power Department, Water Department; Production centers: Divisions 1 und 2.Data:

*) Kaplan/Atkinson, Advanced Management Accounting, 3rd ed. p.74-76 and 80-81. Numbers modified.

⇒

Units of service provided to:

Power Water Div.1 Div.2 Total

Power 20 70 80 70 240Units of serviceprovided from: Water 30 10 70 50 160

traceable costs $ 4.9 $ 1.25

Activity account balances:

240 π1 = 20 π1 + 30 π2 + 4.9 220 π1 – 30 π2 = 4.9160 π2 = 70 π1 + 10 π2 + 1.25 – 70 π1 + 150 π2 = 1.25

16

Calculationdirect solution matrix calculus

220 π1 – 30 π2 = 4.9 | ×5– 70 π1 + 150 π2 = 1.25

1100 π1 – 150 π2 = 24.5– 70 π1 + 150 π2 = 1.25

1030 π1 = 25.75

π1 = 0.025

π2 = = 0.021.75+1.25150

+

⎟⎟⎠

⎞⎜⎜⎝

⎛=

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

=−

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

=−

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

−

−

=−

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

=

⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜

⎝

⎛

=

−

−

02.0025.0

16025.1

2409.4

309352

10356

10316

103120

)(

309352

10356

10316

103120

)(

160150

16070

24030

240220

)(

16010

24030

16070

24020

1

1

2

22

1

21

2

12

1

11

PT

T

T

kAI

AI

AI

A

xx

xx

xx

xx

Power and water cost:Div. 1: $3.4 mill., Div. 2: $2.75 mill.

17

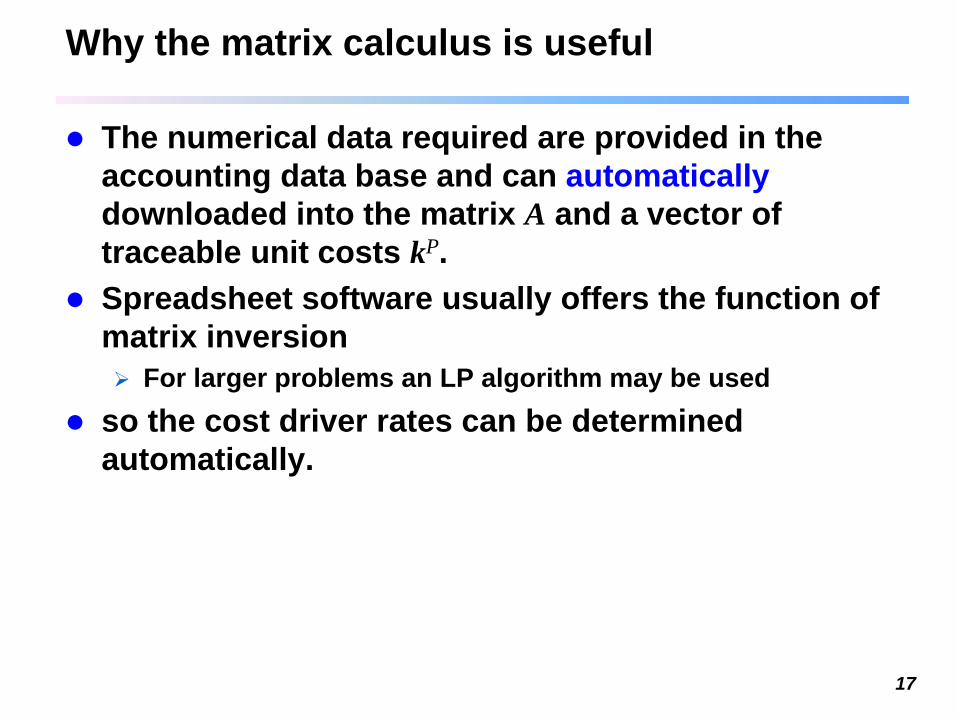

Why the matrix calculus is useful

The numerical data required are provided in the accounting data base and can automaticallydownloaded into the matrix A and a vector of traceable unit costs kP.Spreadsheet software usually offers the function of matrix inversion

For larger problems an LP algorithm may be usedso the cost driver rates can be determined automatically.

18

Interpretation of R:=(I − A)-1

Consider the equation for required total output of service i as a function of external requirements y:

xi (y) = Σj rij yj

Differentiate this function w.r.t. yj . You get:

= rij

This means: rij represents the additional total output of service i required per additional unit of external output requirement of service j.Therefore the matrix R is sometimes called the total requirements matrix)

∂ xi (y) ∂ yj

19

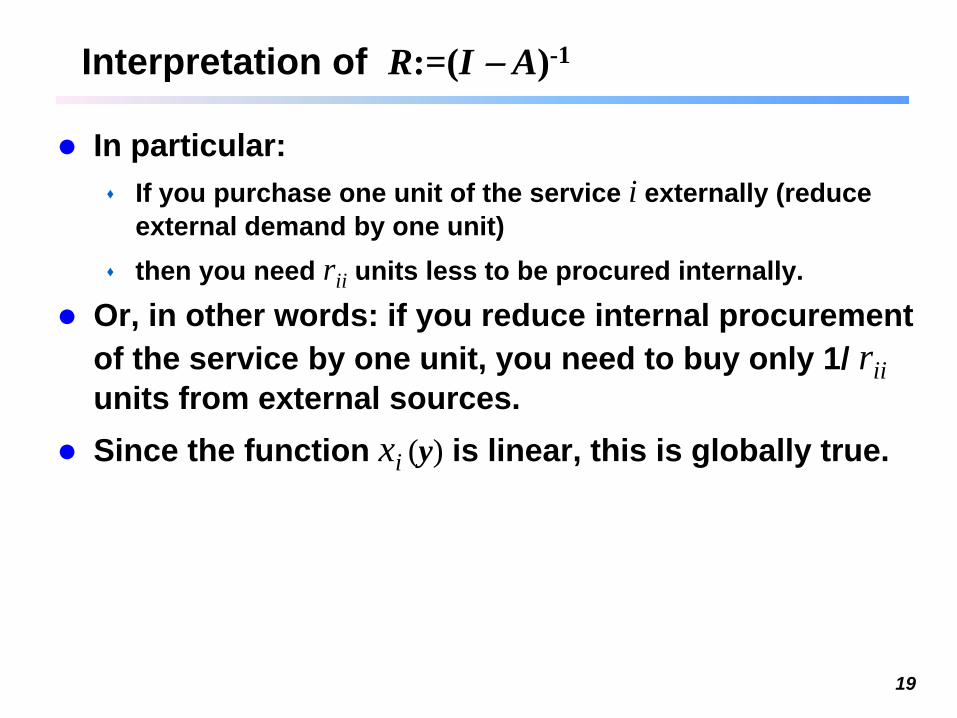

Interpretation of R:=(I − A)-1

In particular:If you purchase one unit of the service i externally (reduce external demand by one unit)then you need rii units less to be procured internally.

Or, in other words: if you reduce internal procurement of the service by one unit, you need to buy only 1/ riiunits from external sources. Since the function xi (y) is linear, this is globally true.

20

Interpretation of R:=(I − A)-1

This means:If you close down service center i then you

can save the total reciprocal cost πi xi for this center butneed xi/rii units of the service externally

You will break even if the external procurement price pi satisfies:

pi xi / rii= pi xii.e. you may pay at most an external price of

pi = πi rii

21

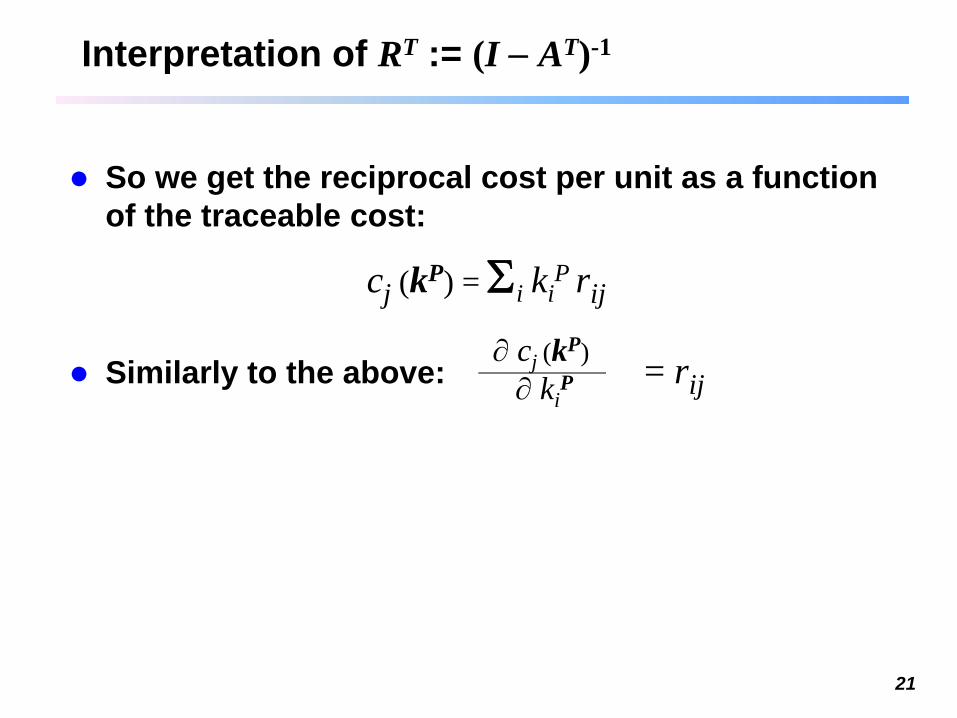

Interpretation of RT := (I − AT)-1

So we get the reciprocal cost per unit as a function of the traceable cost:

cj (kP) = Σi kiP rij

Similarly to the above: = rij∂ cj (kP)

∂ kiP

22

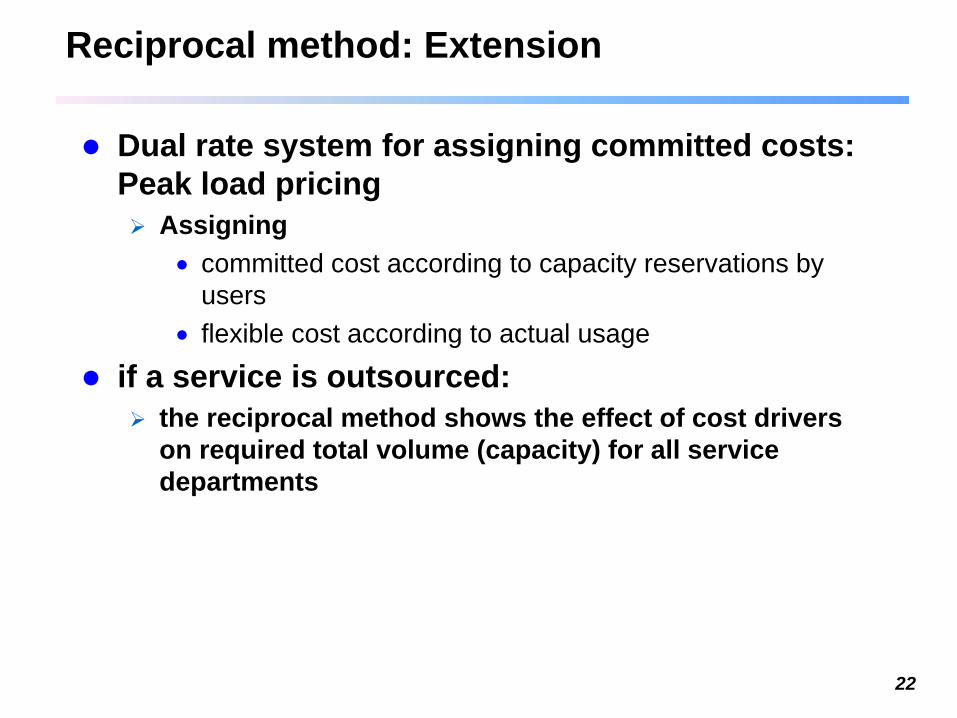

Reciprocal method: Extension

Dual rate system for assigning committed costs: Peak load pricing

Assigning • committed cost according to capacity reservations by

users• flexible cost according to actual usage

if a service is outsourced: the reciprocal method shows the effect of cost drivers on required total volume (capacity) for all service departments

23

Allocating Common Costs

Two methods for allocating common cost1. Stand-alone cost allocation method

actual cost is allocated in the ratio of stand-alone costs2. Incremental cost allocation method

a sequence of cost objects is definedeach object bears the incremental cost according to the sequence

3. Shapley Valuethe average of incremental costs over all possible sequences is charged to the objectthe Shapley Value can be justified based on a set of plausible axioms

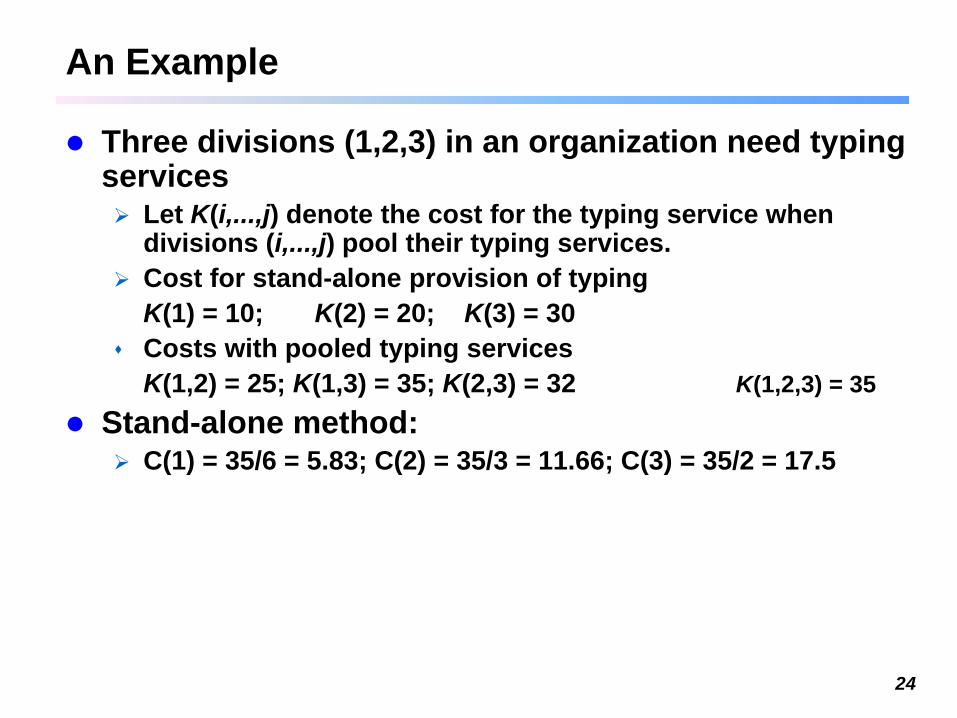

An Example

Three divisions (1,2,3) in an organization need typing services

Let K(i,...,j) denote the cost for the typing service when divisions (i,...,j) pool their typing services.Cost for stand-alone provision of typing K(1) = 10; K(2) = 20; K(3) = 30Costs with pooled typing services K(1,2) = 25; K(1,3) = 35; K(2,3) = 32 K(1,2,3) = 35

Stand-alone method:C(1) = 35/6 = 5.83; C(2) = 35/3 = 11.66; C(3) = 35/2 = 17.5

24

Incremental Method and Shapley ValueApplication to the exampleCost Function

Cost increments occuring when divisions join the pool in a certain order for each possible sequence

= Table of allocationsby incremental method:

Shapley-Value:Stand-alone method: 5.83; 11.66; 17.5

Sequence Div. 1 Div. 2 Div. 31,2,3 10 15 10 1,3,2 10 0 25 2,1,3 5 20 10 2,3,1 3 20 12 3,1,2 5 0 30 3,2,1 3 2 30 Σ/6 6 9½ 19 ½

K(1) = 10; K(2) = 20; K(3) = 30K(1,2) = 25; K(1,3) = 35; K(2,3) = 32

K(1,2,3) = 35

26

Revenues and Bundled Products

A bundled product is a package of two or moreproducts (or services) sold for a single price. Bundled product sales are also referred to as “suite sales.” The individual components of the bundle also may be sold as separate items at their own“stand-alone” prices.Examples

Banks Hotels Tours

CheckingSafety deposit boxesInvestment advisory

LodgingFood and beverage

servicesRecreation

TransportationLodgingGuides

27

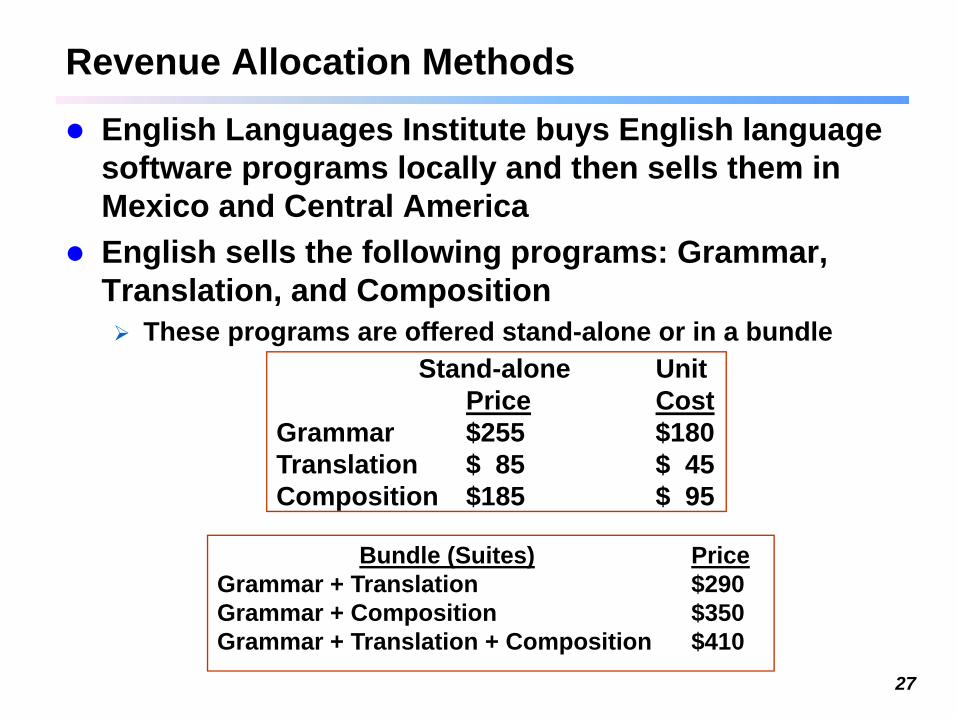

Revenue Allocation Methods

English Languages Institute buys English language software programs locally and then sells them in Mexico and Central America English sells the following programs: Grammar, Translation, and Composition

These programs are offered stand-alone or in a bundleStand-alone Unit

Price CostGrammar $255 $180Translation $ 85 $ 45Composition $185 $ 95

Bundle (Suites) PriceGrammar + Translation $290Grammar + Composition $350Grammar + Translation + Composition $410

28

Revenue Allocation Methods

The two main revenue allocation methods1. The stand-alone method with alternative weights

a) Selling pricesb) Unit costsc) Physical unitsd) Stand-alone product revenues

2. The incremental method with alternative sequences3. The Shapley Value

29

Stand-Alone Revenue Allocation Method

Consider the Grammar and Translation suite, which sells for $290 per copy.1a) Grammar: $290× 255/(255 + 85) = $217.50

Translation: $290× 85/(255 + 85) = $72.501b) Grammar: $290× 180/(180 + 45) = $232

Translation: $290× 45/(180 + 45) = $581c) Grammar: $290/2 = $145

Translation: $290/2 = $1451d) Assume that the stand-alone revenues in 2003

Grammar $734,400; Translation $81,600, Composition $133,200.

Grammar: $734,400 ÷ $816,000 = 0.90, $290 × 0.90 = $261Translation: $81,600 ÷ $816,000 = 0.10, $290 × 0.10 = $29

30

Incremental Revenue Allocation Method

The first-ranked product is termed the primary product in the bundle

If the suite selling price exceeds the stand-alone price of the primary product, the primary product is allocated 100% of its stand-alone revenue.

The second-ranked product is termed the first incremental product The third-ranked product is the second incremental product, and so on. Assume that Grammar is designated as the primary product:

Grammar and Translation suite selling price = $290 per copyAllocated to Grammar: $255Remaining to be allocated: ($290 – $255) = $35 > Translation

Shapley Value, compared to other methods

G T CGrammar, Translation, Composition: 255 45 110Grammar, Composition Translation: 255 60 95Translation, Grammar, Composition: 205 85 120Translation, Composition, Grammar: 140 85 185Composition, Grammar, Translation: 165 60 185Composition, Translation, Grammar: 140 85 185

Shapley Value: 193.33 70 146.67Stand alone: 199.14 66.38 144.48

31