Statutory Residence presentation - STEP

23

Statutory Residence Test Laura Poots

Transcript of Statutory Residence presentation - STEP

Statutory Residence Test Laura Poots

Timetable

• Originally intended for April 2012, delayed to April 2013 • June 2012 – Summary of Consultation and Draft Legislation (with new questions for consultation!) • September 2012 – Further consultation closed

• Autumn 2012 – Further draft legislation expected

• April 2013 – New Legislation intended to take effect

Overview

• Conclusive Non-Residence

• Conclusive Residence

• For all the rest: UK Ties and Day Counting

Day Counting – Para 12

All three tests require day-counting: • Present in the UK at midnight • Except where:

• In transit through UK; OR • Exceptional circumstances beyond individual’s control prevent

departure (eg sudden illness or natural disaster)

• Only 60 days can be ignored by reason of exceptional circumstances

Home - Para 14

Tests consider the concept of a “home”: • Any place, including a vehicle or vessel

• Can be a home without holding any interest in it

• Having an interest in a place does not make it automatically a home

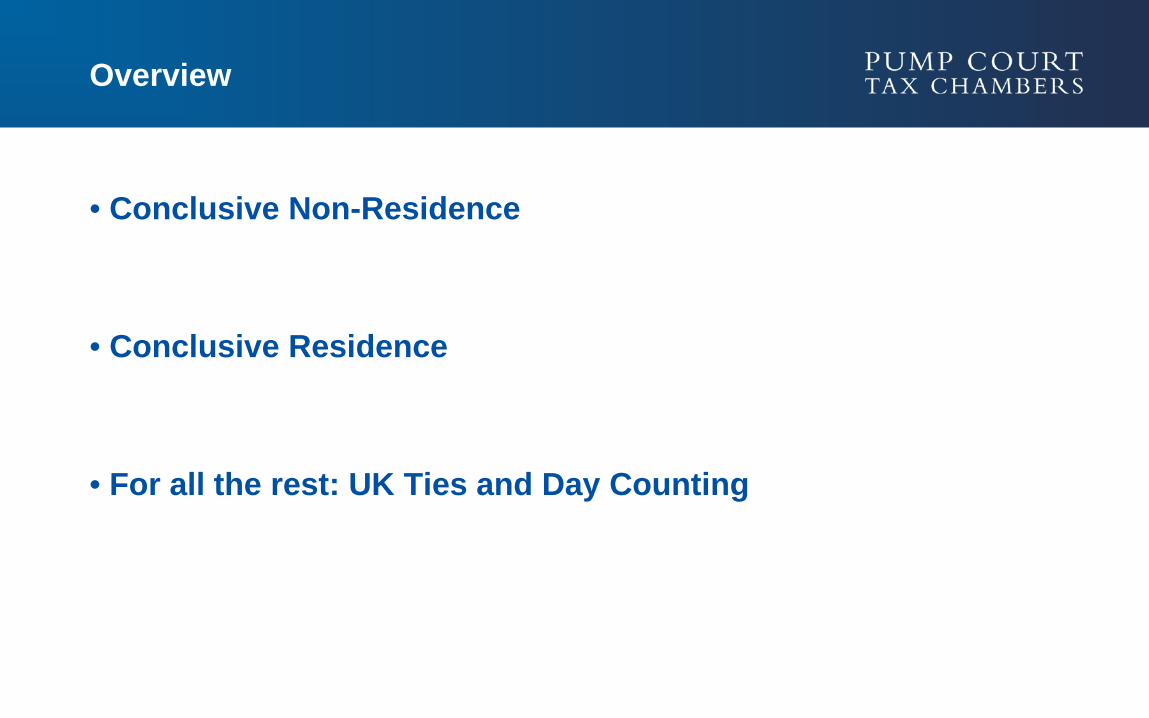

Working – Paras 16 and 17

• Work is done where it is actually done! • Work done in the course of travelling by air, sea or tunnel under

the sea is done overseas.

• Full-time work is an average of 35 hours per week or more.

• Travelling (but not commuting) counts as working time.

• Training generally counts as working time.

Conclusive Non-Residence – Para 6

Referred to as “automatic overseas tests”: 1. Resident in UK for 1 out of 3 previous years AND fewer than 16

days here.

2. Not resident for any of previous 3 years AND fewer than 46 days here.

3. In the relevant year, working abroad full time, fewer than 91 days AND fewer than 21 days of working for more than 3 hours in the UK.

Conclusive Residence

4 automatic residence tests: 1. 183 days in the UK

2. Only home in the UK for at least 91 days in or straddling the

relevant year.

3. Working full-time in the UK for 276 days in or straddling the relevant year AND more than 75% of the days of work (3 hours or more) are days of work in the UK (3 hours or more).

4. Special rule for year of death

All the Rest: Ties – Para 19

1. Family Tie

2. Accommodation Tie

3. Work Tie

4. 90 day Tie

5. Country Tie

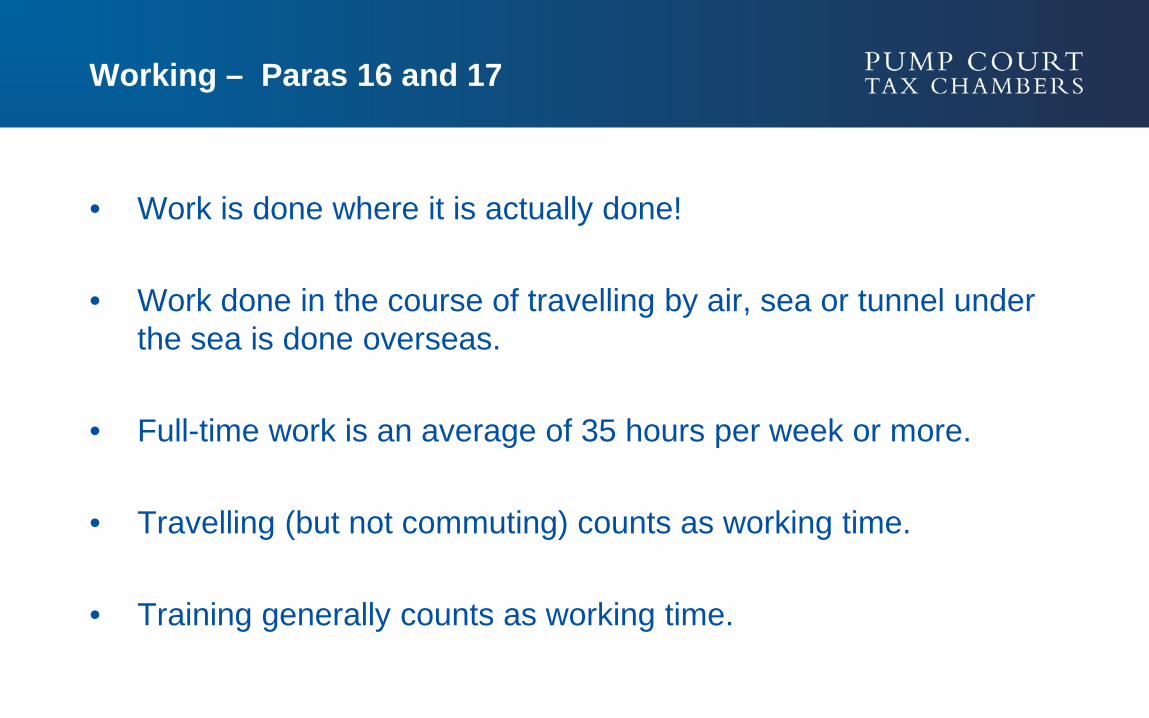

Sufficient Number of Ties

Depends – Arriver or Leaver? • Leaver: Resident in one of three previous years

• Arriver: Not resident in any of three previous years

The Country Tie does not apply to Arrivers

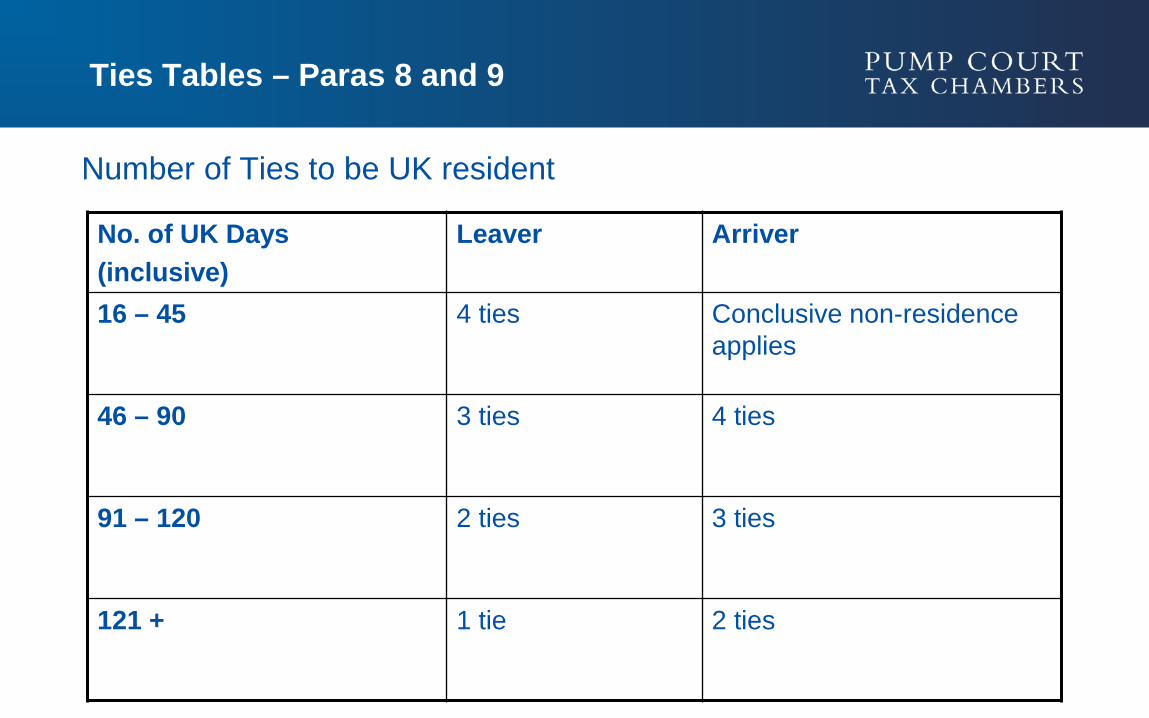

Ties Tables – Paras 8 and 9

Number of Ties to be UK resident

No. of UK Days (inclusive)

Leaver Arriver

16 – 45 4 ties Conclusive non-residence applies

46 – 90 3 ties 4 ties

91 – 120 2 ties 3 ties

121 + 1 tie 2 ties

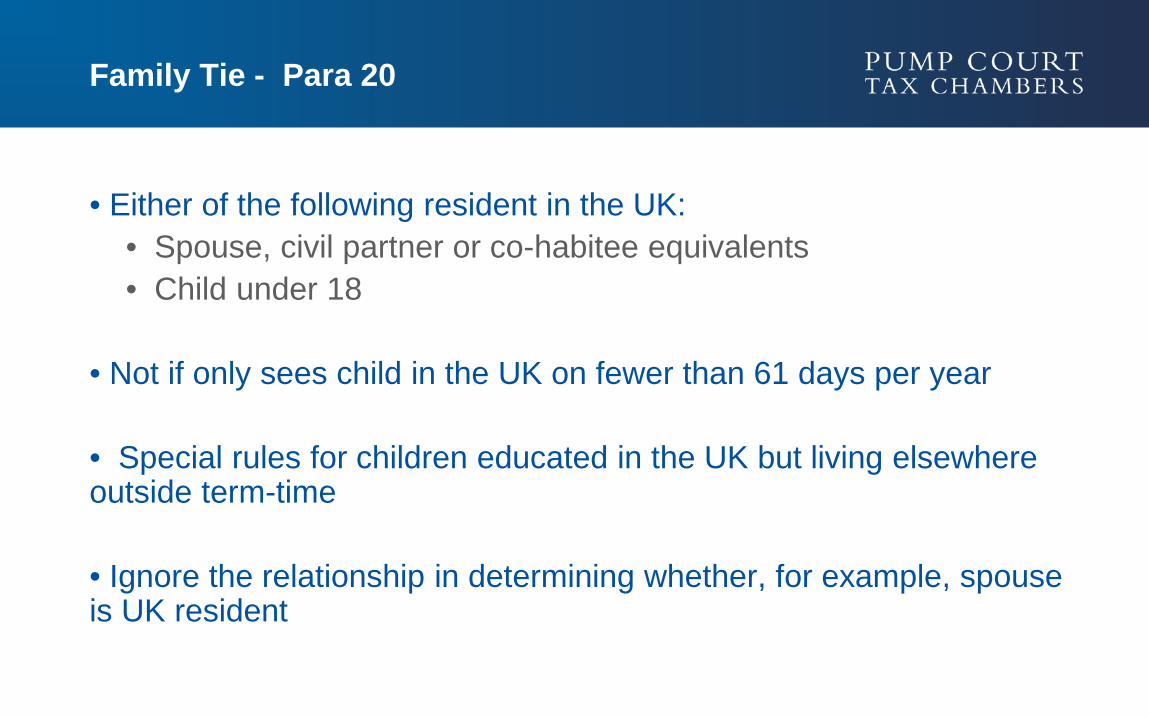

Family Tie - Para 20

• Either of the following resident in the UK: • Spouse, civil partner or co-habitee equivalents • Child under 18

• Not if only sees child in the UK on fewer than 61 days per year

• Special rules for children educated in the UK but living elsewhere outside term-time

• Ignore the relationship in determining whether, for example, spouse is UK resident

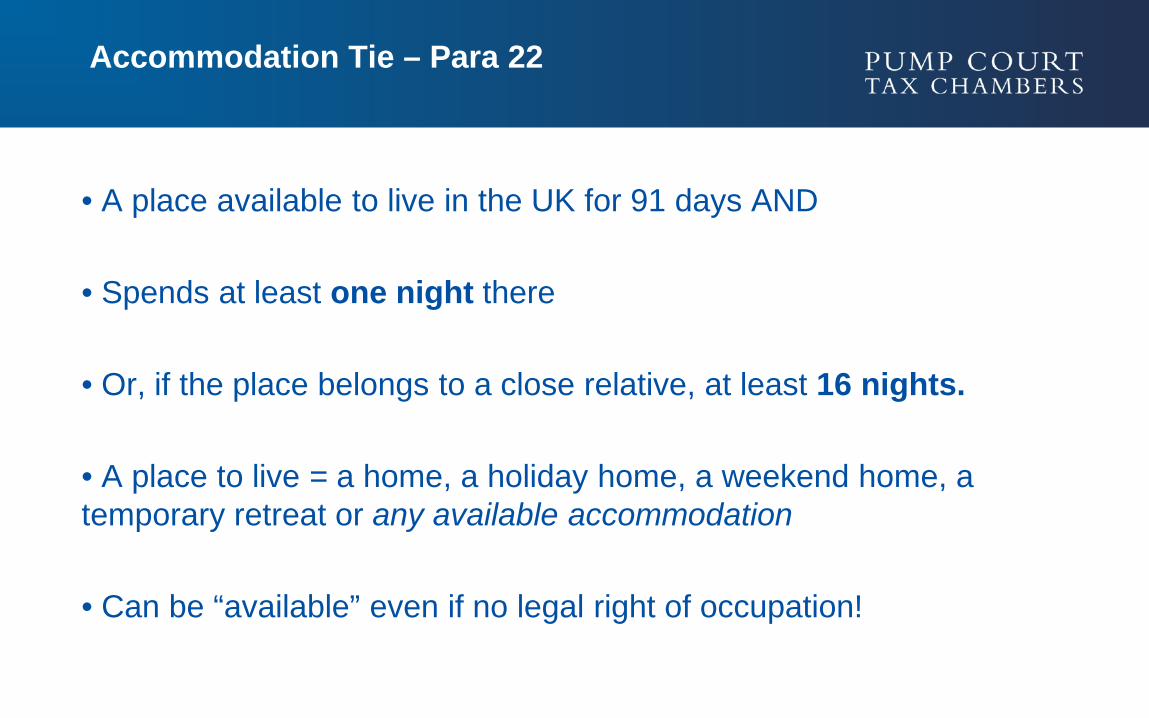

Accommodation Tie – Para 22

• A place available to live in the UK for 91 days AND • Spends at least one night there

• Or, if the place belongs to a close relative, at least 16 nights.

• A place to live = a home, a holiday home, a weekend home, a temporary retreat or any available accommodation

• Can be “available” even if no legal right of occupation!

Work Tie – Para 23

•Works in the UK for at least 40 days

•Working day means more than 3 hours.

90 Day Tie - Para 24

More than 90 days in the UK in: • Relevant Year; and/or

• Previous Year

Country Tie - Para 25

The country in which the taxpayer spends the greatest number of days is the UK. Or equal greatest number of days with another country (or other countries!).

Does not apply to Arrivers

Special Rules: Year of Death

Automatically resident if: • Automatically resident in UK for previous three years;

• Year of death would not be a split year; AND • At time of death, normal home was in the UK.

For the purposes of the Ties Test: reduction in number of days for each test.

Special Rules: International Transport Workers

Employment duties or trade performed on vehicle, aircraft or ship making international journeys. • Automatic residence: Full time work in UK test not applicable. • Automatic non-residence: Full time work overseas test not applicable.

• For Work Tie: Working day in the UK on any day with an international journey starting in the UK.

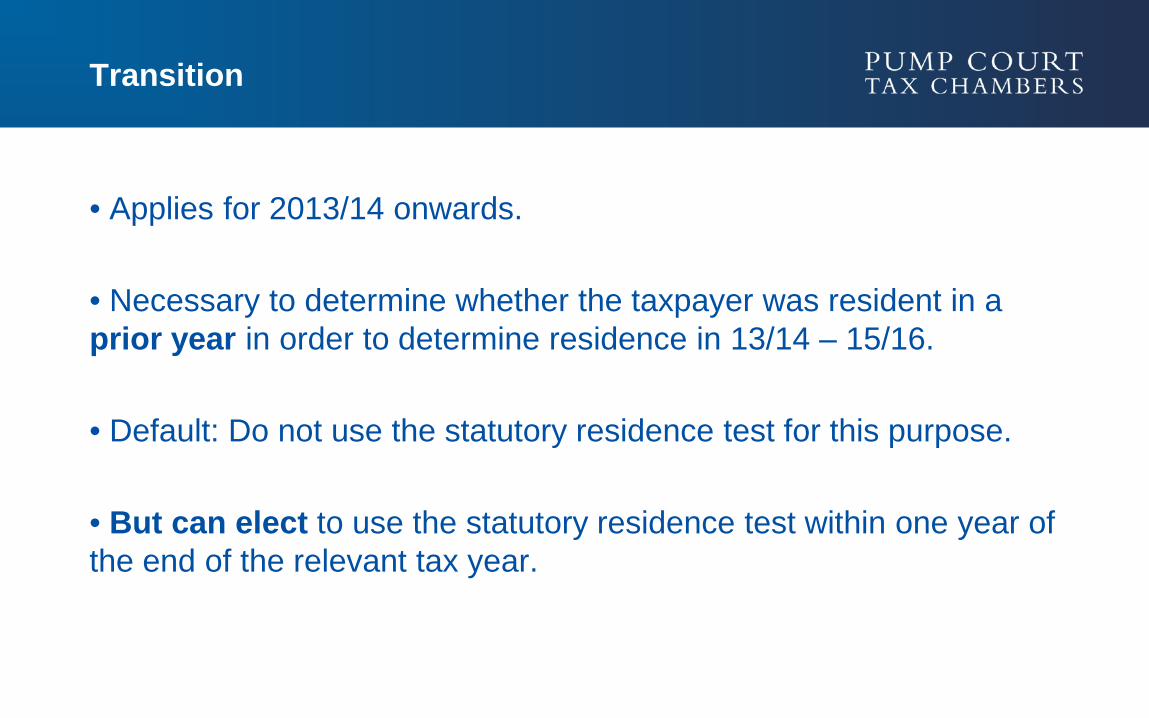

Transition

• Applies for 2013/14 onwards. • Necessary to determine whether the taxpayer was resident in a prior year in order to determine residence in 13/14 – 15/16.

• Default: Do not use the statutory residence test for this purpose.

• But can elect to use the statutory residence test within one year of the end of the relevant tax year.

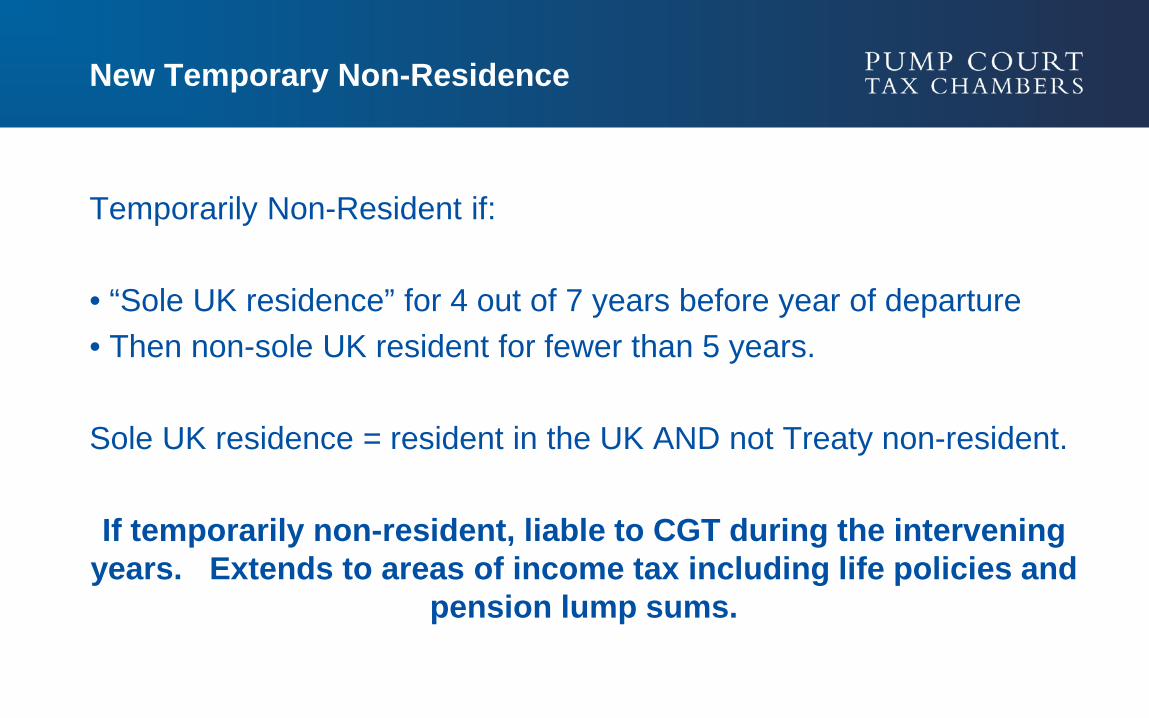

New Temporary Non-Residence

Temporarily Non-Resident if: • “Sole UK residence” for 4 out of 7 years before year of departure • Then non-sole UK resident for fewer than 5 years.

Sole UK residence = resident in the UK AND not Treaty non-resident. If temporarily non-resident, liable to CGT during the intervening

years. Extends to areas of income tax including life policies and pension lump sums.

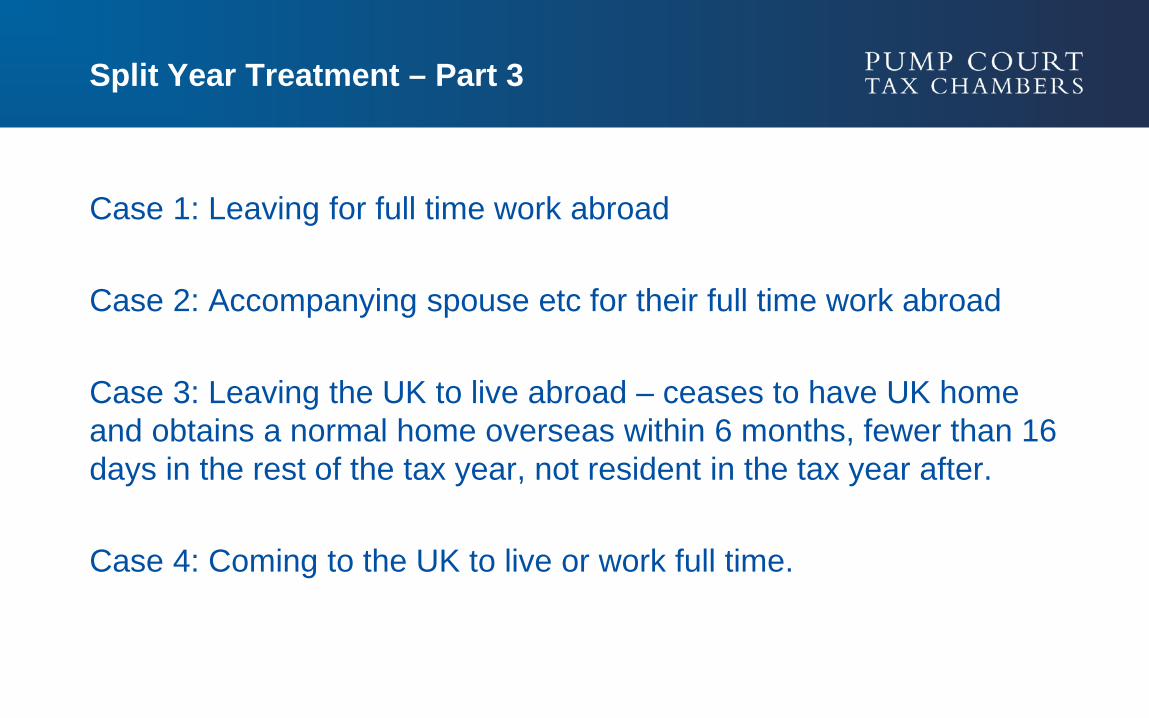

Split Year Treatment – Part 3

Case 1: Leaving for full time work abroad Case 2: Accompanying spouse etc for their full time work abroad Case 3: Leaving the UK to live abroad – ceases to have UK home and obtains a normal home overseas within 6 months, fewer than 16 days in the rest of the tax year, not resident in the tax year after. Case 4: Coming to the UK to live or work full time.

Open Questions

• Automatic non-residence: Full time work abroad. Increase the number of working days permitted in the UK from 20 to 25?

• Working day – increase number of hours from 3 to 5?

• Any other amendments to full time working abroad?

• Automatic residence: Full time work in the UK. Increase the period from 9 months to 12?

• Is there a risk of manipulation of the midnight rule?

Summary

• Detailed contemporaneous records will be key – including working hours and days and days in other countries. • Useful to have a test but still many areas for potential argument

• Cohabiting as spouses? • Exceptional circumstances? • Homes/accommodation? • Normal home?

• Currently not applicable for NICs

![NEWS RELEASE 28 a RESIDENCE RESIDENCE] 10 20 as 18 11 15 … · news release 28 a residence residence] 10 20 as 18 11 15 a (±) 70 201 residence residence] residence (itþ#) : : jr](https://static.fdocuments.us/doc/165x107/5f4178718a31a4664d3bc562/news-release-28-a-residence-residence-10-20-as-18-11-15-news-release-28-a-residence.jpg)