STATEOF MICHIGANINVESTMENT BOARD MEETING March …

105

STATE OF MICHIGAN INVESTMENT BOARD MEETING March 7, 2019 State of Michigan Retirement System Quarterly Investment Review Rachael Eubanks, State Treasurer Prepared by Bureau of Investments Michigan Department of Treasury

Transcript of STATEOF MICHIGANINVESTMENT BOARD MEETING March …

STATE OF MICHIGAN INVESTMENT BOARD MEETING

March 7, 2019 State of Michigan Retirement System

Quarterly Investment Review

Rachael Eubanks, State Treasurer Prepared by Bureau of Investments Michigan Department of Treasury

STATE OF MICHIGAN INVESTMENT BOARD MEETING

MARCH 7, 2019

Agenda

9:30 a.m. Call to Order and Opening Remarks

9:40 a.m. Approval of the 12/11/18 SMIB Meeting Minutes

9:45 a.m. Executive Summary & Performance for Periods Ending 12/31/18

10:00 a.m. Current Asset Allocation Review

Markets Review and Outlook

10:15 a.m. Review of Investment Reports

Defined Contribution

Fixed Income

Real, Opportunistic, & Absolute Return

Domestic Equity

Private Equity – Receive and File

International Equity – Receive and File

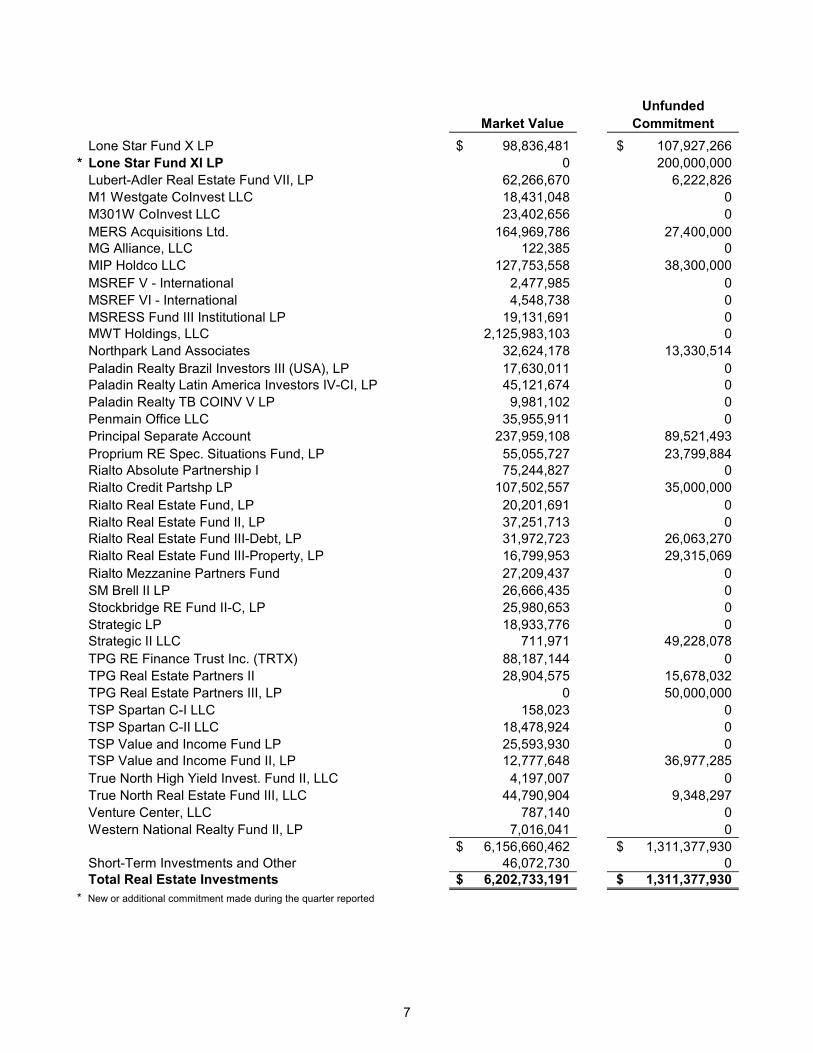

Real Estate & Infrastructure – Receive and File

11:00 a.m. Public Comment

Closing Remarks ~ Adjournment

2019 Meeting Schedule

Thursday, June 6, 2019 Thursday, September 12, 2019 Thursday, December 12, 2019

All meetings start at 9:30 a.m.

www.michigan.gov/treasury

State of Michigan Retirement System

MINUTES State of Michigan Investment Board Meeting

March 7, 2019

Jon M. BraeutigamChief Investment OfficerBureau of Investments

STATE OF MICHIGAN INVESTMENT BOARD December 11, 2018 Meeting Minutes

Members Present: Chair – Treasurer Nick Khouri Budget Director John Walsh (arrived 10:30 am) Ms. Dina Richard Mr. Reginald Sanders

Members by Phone: Mr. James Nicholson

Members of the Public and Bureau of Investments Staff Present: Molly Jason Craig Sabin Jack Behar Karl Borgquist Paul Lerg Richard Holcomb Mary Pollock Anthony Estell Kerrie VandenBosch Dave Klauka Matt Hutson Pavel Stolarczyk Barb Becker Craig Coulter June Morse Ann Stange Mark Porrell Nick Whitman Lan Chen Todd Warstler Jennifer Yeung Jim Elkins Jon Braeutigam Robert Brackenbury Peter Woodford Woody Tyler Travis Haney Greg Parker Giles Feldpausch Ann Storberg Marge McPhee Annette Russell Todd Warstler Patrick Moraniec Janet Sudac Lori Barrett

Treasurer Khouri called the meeting to order at 9:30 am.

Opening Remarks: Brief discussion by Chair Treasurer Khouri explaining that this is his last meeting as he will be retiring at the end of this month. He wished the State of Michigan Retirement System continued success.

Approval of the November 27, 2018 SMIB Special Meeting Minutes – Motion to approve: Reginald Sanders. Seconded: Dina Richard. The vote was unanimous to approve.

AGENDA

Executive Summary Jon Braeutigam, Chief Investment Officer for the Bureau of Investments, discussed the plans returns over the past one, three, five, seven, and ten years. For each time period the plan had higher returns than the peer median. He believes that market returns will be lower going forward, and this view is shared by industry consultants in general.

Asset Allocation Review, Markets Review and Outlook Gregory Parker, Director of Investments - Public Markets for the Bureau of Investments discussed that quality decision making is the foundation to obtain the returns that SMRS has experienced. He also discussed the overwhelming consensus view of lower returns going forward.

1

Review of Investment Reports – Public

Woody Tyler, Senior Investment Manager of Defined Contribution, Trusts & Agencies presented a brief overview of the defined contribution plan noting that a more comprehensive look at defined contribution will ensue at the March meeting.

Daniel Quigley, Senior Investment Manager of the Fixed Income Division discussed that the fixed income portfolio outperformed its benchmark and peer group across all time periods.

Jack Behar, Senior Investment Manager of the Domestic Equity Division explained that they had a very strong year and experienced excellent performance on the growth side of the portfolio.

Patrick Moraniec, Senior Investment Manager of the International Equity Division stated that the portfolio slightly outperformed the benchmark over the last twelve months. This was driven by developed market exposure.

Review of Investment Reports – Private

Peter Woodford, Senior Investment Manager of Private Equity explained that returns have been strong relative to peer median returns, ranking in the top 7% of peers over the past ten years. The outperformance to peers is attributed to fund selectivity and strategy.

Jennifer Yeung, Senior Investment Manager of Real, Opportunistic, & Absolute Return explained that the division experienced a 6% return for the year with outperformance of the benchmark in the third quarter. This outperformance was driven by overweight exposure to credit strategies as well as manager selection.

Todd Warstler, Senior Investment Manager of Real Estate & Infrastructure stated that outperformance relative to the one-year benchmark resulted from the divisions strategy. No big changes in this strategy are anticipated at this time.

Public Comment Treasurer Khouri asked that any attendees wishing to address the Board come forward. No public comment.

Treasurer Khouri adjourned the meeting at 11:02 am. Motion to adjourn by Dina Richard. Seconded: Reginald Sanders. The vote was unanimous to adjourn.

Approved:

_________________________________ Rachael Eubanks, Chairman

2

State of Michigan Retirement System

EXECUTIVE SUMMARY State of Michigan Investment Board Meeting

March 7, 2019

Gregory J. Parker, CFA Director of Investments – Public Markets

Director of Asset Allocation Bureau of Investments

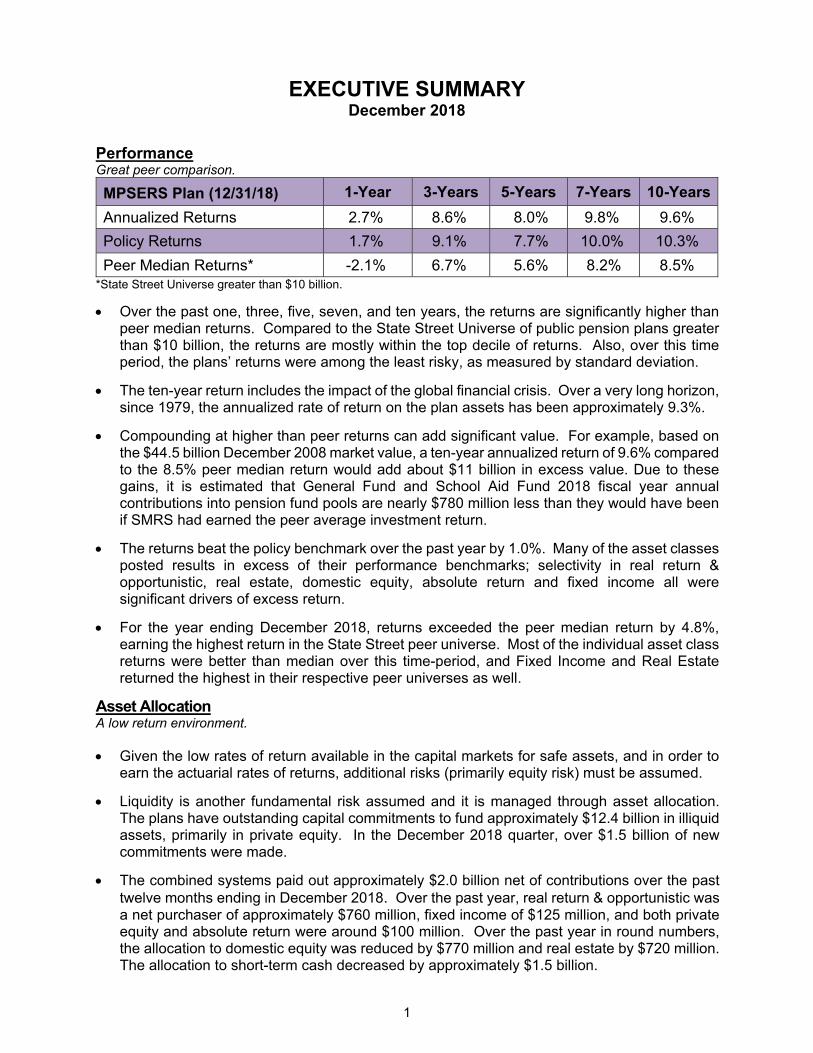

EXECUTIVE SUMMARY December 2018

Performance Great peer comparison.

MPSERS Plan (12/31/18) 1-Year 3-Years 5-Years 7-Years 10-Years

Annualized Returns 2.7% 8.6% 8.0% 9.8% 9.6%

Policy Returns 1.7% 9.1% 7.7% 10.0% 10.3%

Peer Median Returns* -2.1% 6.7% 5.6% 8.2% 8.5% *State Street Universe greater than $10 billion.

Over the past one, three, five, seven, and ten years, the returns are significantly higher than peer median returns. Compared to the State Street Universe of public pension plans greater than $10 billion, the returns are mostly within the top decile of returns. Also, over this time period, the plans’ returns were among the least risky, as measured by standard deviation.

The ten-year return includes the impact of the global financial crisis. Over a very long horizon, since 1979, the annualized rate of return on the plan assets has been approximately 9.3%.

Compounding at higher than peer returns can add significant value. For example, based on the $44.5 billion December 2008 market value, a ten-year annualized return of 9.6% compared to the 8.5% peer median return would add about $11 billion in excess value. Due to these gains, it is estimated that General Fund and School Aid Fund 2018 fiscal year annual contributions into pension fund pools are nearly $780 million less than they would have been if SMRS had earned the peer average investment return.

The returns beat the policy benchmark over the past year by 1.0%. Many of the asset classes posted results in excess of their performance benchmarks; selectivity in real return & opportunistic, real estate, domestic equity, absolute return and fixed income all were significant drivers of excess return.

For the year ending December 2018, returns exceeded the peer median return by 4.8%, earning the highest return in the State Street peer universe. Most of the individual asset class returns were better than median over this time-period, and Fixed Income and Real Estate returned the highest in their respective peer universes as well.

Asset Allocation A low return environment.

Given the low rates of return available in the capital markets for safe assets, and in order to earn the actuarial rates of returns, additional risks (primarily equity risk) must be assumed.

Liquidity is another fundamental risk assumed and it is managed through asset allocation. The plans have outstanding capital commitments to fund approximately $12.4 billion in illiquid assets, primarily in private equity. In the December 2018 quarter, over $1.5 billion of new commitments were made.

The combined systems paid out approximately $2.0 billion net of contributions over the past twelve months ending in December 2018. Over the past year, real return & opportunistic was a net purchaser of approximately $760 million, fixed income of $125 million, and both private equity and absolute return were around $100 million. Over the past year in round numbers, the allocation to domestic equity was reduced by $770 million and real estate by $720 million. The allocation to short-term cash decreased by approximately $1.5 billion.

1

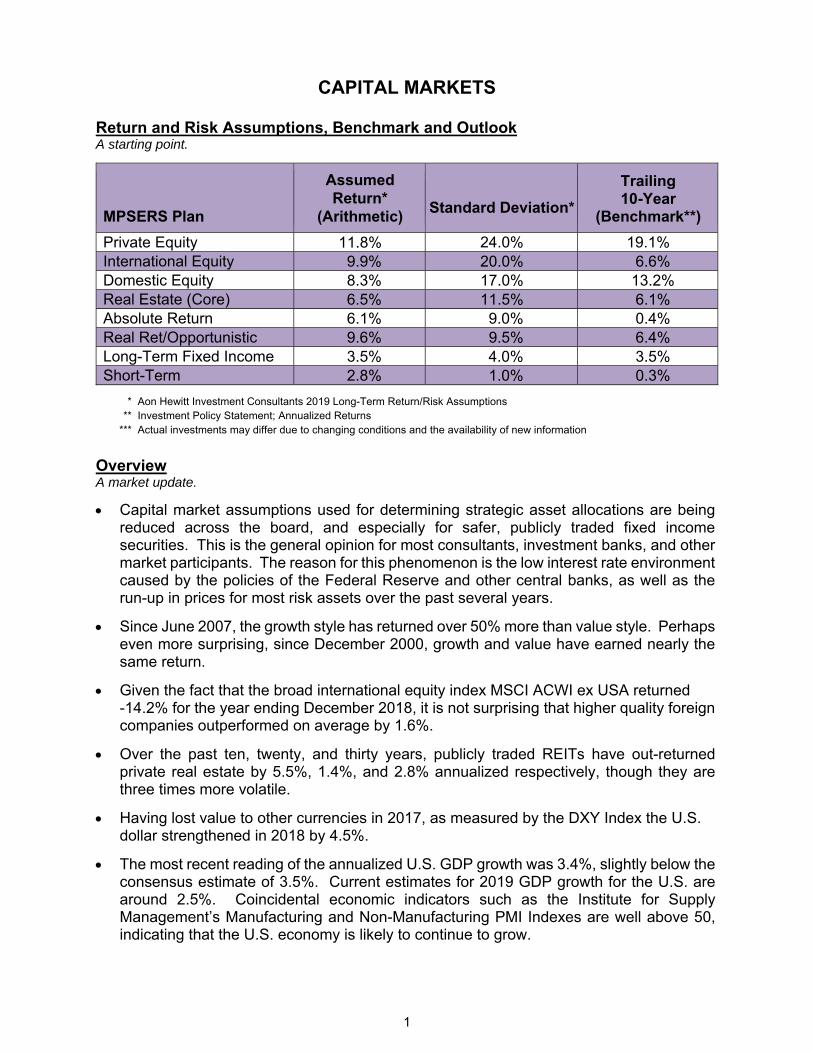

Capital Markets Risk assets in focus.

Capital market assumptions used for determining strategic asset allocations are being reduced across the board, and especially for safer, publicly traded fixed income securities. This is the general opinion for most consultants, investment banks, and other market participants. The reason for this phenomenon is the low interest rate environment caused by the policies of the Federal Reserve and other central banks, as well as the run-up in prices for most risk assets over the past several years since the depths of the Great Recession.

Private real estate was the best performing asset class for 2018, returning approximately 6.7%. Publicly traded REITs fell in value by -4.1% including dividend returns.

Fundamentals supporting domestic equities are still strong. Year-over-year growth in analyst estimated earnings for the next year are close to 12%. Since June 2007, the growth style has returned over 50% more than value style. Perhaps even more surprising, since December 2000 growth and value have earned nearly the same return.

Defined as a pullback of 20% or more on the closing value of the S&P 500, the U.S. equity market has not hit a correction since the Global Financial Crisis.

In 2018, both credit spreads and long-term interest rates increased making it difficult for bond managers to earn extra return. With the yield curve at its flattest levels since the summer of 2007 and credit spreads at fairly normal levels, securitized credit and floating rate assets are attractive alternatives.

The most recent reading of the annualized U.S. GDP growth was 3.4%, slightly below the consensus estimate of 3.5%. Current estimates for 2019 GDP growth for the U.S. is around 2.5%. Coincidental economic indicators such as the Institute for Supply Management’s Manufacturing and Non-Manufacturing PMI Indexes are well above 50, indicating that the U.S. economy is likely to continue to grow.

2

Investment Update

Highlighting the quarter.

($ Millions)

NEW COMMITMENTS

September 30 – December 31, 2018

Asset class Fund Name / (Managed By) Commitment

Private Equity

TSG 8, L.P. (TSG Consumer Partners) $150

Warburg Pincus Global Growth, L.P. (Warburg Pincus Global Growth GP, LP) 150

KKR European Fund V (USD) SCSp (KKR Associates Europe V SCSp) 125

Greenspring Master G, L.P. (Greenspring Associates, Inc.) 100

Flagship Pioneering Special Opportunities Fund II, L.P. (Flagship Opp. Fund II GP, LLC) 100

FS Equity Partners VIII, L.P. (FS Capital Partners VIII, LLC) 75

5AM Opportunities I, L.P. (5AM Partners VI, LLC) 30

Greenspring Micro II, L.P. (Greenspring Associates, Inc.) 25

5AM Ventures VI, L.P. (5AM Partners VI, LLC) 20

Real Estate and Infrastructure Division

Blackstone Real Estate Partners IX, LP (Blackstone Real Estate Advisors) 200

Lone Star Fund XI, LP (Lone Star) 200

Real, Opportunistic, & Absolute Return Division

TSSP Capital Solutions Fund I, L.P. (TSSP Capital Solutions Management I, LLC) 300

Flywheel Energy Co-Invest, LLC (Kayne Anderson) 35

TOTAL $1,510

3

State of Michigan Retirement System

PERFORMANCE State of Michigan Investment Board Meeting

March 7, 2019

Jon M. Braeutigam Chief Investment Officer Bureau of Investments

Bureau of Investments Mission Statement

The Bureau of Investments continually strives to provide quality

investment management services, broad professional expertise, and

independent advice to the State of Michigan Investment Board

as fiduciary of the State of Michigan Retirement System, and

independent of the Board, to the State Treasurer for various Michigan

trust funds and the State’s common cash, for which the State Treasurer

is the fiduciary.

SMRS Goals Maintain sufficient liquidity to pay benefits.

Meet or exceed the actuarial assumption over the long term.

Perform in the top half of the public plan universe over the long term.

Diversify assets to reduce risk.

Exceed individual asset class benchmarks over the long term.

1

MP

SE

RS

PE

NS

ION

Tim

e-W

eig

hte

d R

ates

of

Ret

urn

Per

iod

s E

nd

ing

Dec

emb

er 3

1, 2

018

% o

f T

enS

even

Fiv

eT

hre

eO

ne

Cu

rren

tP

ort

folio

12/3

1/18

Rat

eR

ank

Rat

eR

ank

Rat

eR

ank

Rat

eR

ank

Rat

eR

ank

Rat

eR

ank

TO

TA

L P

LA

N10

0.0

9.6

99.

85

8.0

48.

613

2.7

5-4

.215

M

ed

ian

- G

rea

ter

than

$10

Bill

ion

28.

58.

25.

66.

7-2

.1-5

.9

MP

SE

RS

To

tal P

lan

Pol

icy

10.3

10.0

7.7

9.1

1.7

-3.9

DO

ME

ST

IC E

QU

ITIE

S22

.613

.330

12.9

188.

322

9.5

18-3

.817

-15.

086

M

edia

n 2

13.0

12.4

7.6

8.3

-5.9

-13.

5

S

&P

150

0 In

dex

13.2

12.6

8.3

9.2

-5.0

-14.

0

INT

ER

NA

TIO

NA

L E

QU

ITIE

S15

.97.

553

6.1

572.

032

4.8

23-1

4.3

54-1

1.7

29

Med

ian

27.

66.

31.

34.

1-1

4.2

-12.

1

Int

erna

tiona

l Ble

nded

Ben

chm

ark

35.

85.

00.

74.

5-1

4.2

-11.

5

PR

IVA

TE

EQ

UIT

IES

18.0

13.5

714

.910

14.6

1414

.811

18.2

73.

912

M

edia

n 2

8.9

10.3

9.3

9.5

7.7

1.0

Alte

rnat

ive

Ble

nded

Ben

chm

ark

419

.120

.117

.220

.721

.48.

5

BO

ND

S12

.85.

229

3.5

203.

914

4.1

191.

24

0.8

41

Med

ian

24.

42.

62.

72.

5-0

.30.

7

B

arcl

ays

Agg

rega

te3.

52.

12.

52.

10.

01.

6

RE

AL

ES

TA

TE

& I

NF

RA

ST

RU

CT

UR

E10

.15.

651

11.5

2712

.021

10.4

2912

.24

2.3

23

Med

ian

25.

710

.210

.58.

78.

91.

6

NC

RE

IF -

Pro

pert

y B

lend

ed I

ndex

56.

18.

37.

95.

85.

41.

1

NC

RE

IF O

pen

Fun

d In

dex

Net

6.0

10.0

9.4

7.3

7.4

1.5

RE

AL

RE

TU

RN

AN

D O

PP

OR

TU

NIS

TIC

11.5

11.5

13.6

12.4

19.5

6.6

50%

(C

PI

+50

0 bp

s) +

50%

(6.

8% a

ctua

rial

rat

e)7.

37.

27.

57.

31.

2

AB

SO

LU

TE

RE

TU

RN

6.2

6.1

5.7

4.0

4.4

4.3

0.2

HF

RI

FO

F C

ons

1 m

onth

lagg

ed2.

93.

02.

11.

80.

6-2

.0

CA

SH

EQ

UIV

AL

EN

TS

2.8

0.8

0.8

1.0

1.4

2.2

0.6

1 M

onth

T-B

ill0.

30.

40.

60.

91.

80.

6

1 A

nnua

lized

Ret

urns

and

Per

cent

ile R

ank.

2 C

ompa

rison

uni

vers

e is

the

Sta

te S

tree

t Uni

vers

e co

mpr

ised

of P

ublic

Fun

ds g

reat

er th

an $

10 b

illio

n on

the

tota

l pla

n le

vel a

nd g

reat

er th

an $

1 bi

llion

for

asse

t cla

sses

.3

Inte

rnat

iona

l ble

nded

ben

chm

ark

is S

&P

Dev

elop

ed B

MI-

EP

AC

50/

50 p

rior

to 1

/1/1

0. S

&P

Dev

elop

ed B

MI-

EP

AC

75

US

D /

25 L

ocal

, 1/1

/10

to 9

/30/

10.

MS

CI A

CW

I ex

US

A G

ross

10/

1/10

to p

rese

nt.

4 S

P 5

00 +

300

bps

thru

12/

31/0

6. E

ndin

g m

arke

t val

ue (

EM

V)

wei

ghte

d bl

end

of 1

0 yr

yie

ld +

300

bps

and

SP

500

+ 3

00 b

ps 1

2/31

/06

to 9

/30/

09.

EM

V w

eigh

ted

blen

d of

10

yr y

ield

+ 3

00 b

ps a

nd S

P 5

00 +

300

bps

3-m

onth

lagg

ed 9

/30/

09 to

pre

sent

.5

NC

RE

IF -

Pro

pert

y B

lend

ed In

dex

is N

PI m

inus

75

bps

prio

r to

Oct

ober

200

5, N

PI m

inus

130

bps

cur

rent

.

So

urc

e:

Sta

te S

tre

et

An

aly

tics;

th

e N

CR

EIF

- N

PI (

Pro

pe

rty

Ind

ex)

so

urc

e is

NC

RE

IF; t

he

S&

P B

MI-

EP

AC

Ind

ex

sou

rce

is S

&P

.

Yea

rs 1

Yea

rs 1

Yea

rQ

uar

ter

Yea

rs 1

Yea

rs 1

2

Tota

l Fun

d Pe

rfor

man

ce 0.0%

0.9%

1.8%

2.7%

3.6%

4.5%

Tota

l Fun

d

Tota

l Fun

d Be

nchm

ark

Tota

l Val

ue A

dded

2.7%

1.7%

1.0%

Tota

l Val

ue A

dded

:1.0

%

0.0%

1.0%

2.0%

3.0%

-1.0

%-2

.0 %

Oth

er

Man

ager

Val

ue A

dded

Asse

t Allo

catio

n

0.0%

1.5%

-0.5

%

Tota

l Ass

et A

lloca

tion:

-0.5

%

Aver

age

Activ

e W

eigh

t

0.0%

3.0%

6.0%

-3.0

%-6

.0 %

Tota

l Rea

l Ret

urn

and

Opp

ortu

nist

ic

Tota

l Rea

l Est

ate

and

Infra

stru

ctur

e

Tota

l Priv

ate

Equi

ty

Tota

l Sho

rt Te

rm

Tota

l Abs

olut

e R

etur

n

Tota

l Fix

ed In

com

e

Tota

l Int

erna

tiona

l Equ

ity

Tota

l Dom

estic

Equ

ity

Weight (%)

-0.4

%

0.9%

-2.0

%

1.1%

-0.2

%

1.7%

1.8%

-2.9

%

Asse

t Allo

catio

n Va

lue

Adde

d

0.0%

0.3%

0.6%

-0.3

%-0

.6 %

0.0%

0.0%

-0.3

%

-0.1

%0.0%

0.0%

-0.3

%

0.1%

Tota

l Man

ager

Val

ue A

dded

:1.5

%

Man

ager

Val

ue A

dded

0.0%

0.8%

1.6%

-0.8

%-1

.6 %

1.0%

0.7%

-0.5

%

0.0%

-0.1

%

0.1%

-0.1

%

0.3%

Tota

l Fun

d A

ttrib

utio

n1

Year

End

ing

Dec

embe

r 31,

201

8

Tota

l Mic

higa

n vs

. Tot

al F

und

Ben

chm

ark

3

1 Y

ear

2 Y

ear

3 Y

ear

4 Y

ear

5 Y

ear

6 Y

ear

7 Y

ear

8 Y

ear

9 Y

ear

10 Y

ear

MP

SE

RS

2.7

9.2

8.6

7.2

8.0

9.3

9.8

9.0

9.4

9.6

Pu

bli

c P

lan

- M

ed

ian

(>

$1

0 b

illi

on

)*-2

.16

.36

.75

.25

.67

.28

.27

.27

.88

.5

Ra

nk

55

13

94

45

55

9

bp

Dif

fere

nc

e -

Me

dia

n4

78

29

41

90

19

82

34

21

01

58

17

51

56

11

3

12/1

812

/17

12/1

612

/15

12/1

412

/13

12/1

212

/11

12/1

012

/09

MP

SE

RS

2.7

16

.27

.42

.81

1.3

16

.41

2.6

3.3

12

.71

2.1

Pu

bli

c P

lan

- M

ed

ian

(>

$1

0 b

illi

on

)*-2

.11

5.3

7.9

0.4

7.1

15

.71

3.2

1.7

12

.71

7.4

Ra

nk

53

96

84

53

76

51

25

38

0

bp

Dif

fere

nc

e -

Me

dia

n4

78

86

-45

23

84

21

73

-53

16

5-4

-53

0

1 Y

ear

2 Y

ear

3 Y

ear

4 Y

ear

5 Y

ear

6 Y

ear

7 Y

ear

8 Y

ear

9 Y

ear

10 Y

ear

MS

ER

S2

.79

.38

.77

.28

.09

.39

.88

.99

.39

.6

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

6.3

6.7

5.1

5.3

7.2

8.0

7.1

7.8

8.5

Ra

nk

43

86

34

44

42

0

bp

Dif

fere

nc

e -

Me

dia

n5

62

29

91

95

20

22

63

21

61

76

18

71

51

11

0

12/1

812

/17

12/1

612

/15

12/1

412

/13

12/1

212

/11

12/1

012

/09

MS

ER

S2

.71

6.2

7.5

2.8

11

.31

6.3

12

.63

.21

2.5

11

.9

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

15

.07

.90

.36

.91

5.9

13

.01

.31

2.9

18

.4

Ra

nk

43

56

32

34

46

61

56

18

5

bp

Dif

fere

nc

e -

Me

dia

n5

62

11

7-3

92

49

44

04

0-4

51

89

-36

-64

8

*Sta

te S

tree

t Pub

lic F

unds

Uni

vers

e

Cu

mu

lati

ve a

nd

Co

nse

cuti

ve

MP

SE

RS

To

tal

Fu

nd

Ret

urn

s

Cu

mu

lati

ve

Fo

r Y

ea

rs E

nd

ing

12

/31

/18

Co

ns

ec

uti

ve

Fo

r Y

ea

rs E

nd

ing

MS

ER

SC

um

ula

tiv

e F

or

Ye

ars

En

din

g 1

2/3

1/2

01

8

Co

ns

ec

uti

ve

Fo

r Y

ea

rs E

nd

ing

4

1 Y

ear

2 Y

ear

3 Y

ear

4 Y

ear

5 Y

ear

6 Y

ear

7 Y

ear

8 Y

ear

9 Y

ear

10 Y

ear

MS

PR

S2

.79

.38

.67

.28

.09

.39

.78

.99

.39

.5

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

6.3

6.7

5.1

5.3

7.2

8.0

7.1

7.8

8.5

Ra

nk

43

86

44

44

42

0

bp

Dif

fere

nc

e -

Me

dia

n5

61

29

91

94

20

12

62

21

31

72

18

61

51

10

6

12/1

812

/17

12/1

612

/15

12/1

412

/13

12/1

212

/11

12/1

012

/09

MS

PR

S2

.71

6.2

7.5

2.8

11

.31

6.2

12

.53

.31

2.6

11

.5

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

15

.07

.90

.36

.91

5.9

13

.01

.31

2.9

18

.4

Ra

nk

43

56

43

34

46

91

36

08

8

bp

Dif

fere

nc

e -

Me

dia

n5

61

11

7-4

22

48

43

63

2-5

22

04

-29

-68

6

1 Y

ear

2 Y

ear

3 Y

ear

4 Y

ear

5 Y

ear

6 Y

ear

7 Y

ear

8 Y

ear

9 Y

ear

10 Y

ear

MJ

RS

2.7

9.3

8.7

7.2

7.9

9.2

9.6

8.8

9.2

9.2

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

6.3

6.7

5.1

5.3

7.2

8.0

7.1

7.8

8.5

Ra

nk

43

86

44

55

62

5

bp

Dif

fere

nc

e -

Me

dia

n5

58

30

11

96

20

22

58

20

11

62

17

31

36

76

12/1

812

/17

12/1

612

/15

12/1

412

/13

12/1

212

/11

12/1

012

/09

MJ

RS

2.7

16

.37

.42

.81

1.0

15

.61

2.5

3.1

12

.29

.9

Pu

bli

c P

lan

- M

ed

ian

(>

$1

bil

lio

n)*

-2.9

15

.07

.90

.36

.91

5.9

13

.01

.31

2.9

18

.4

Ra

nk

43

36

53

35

37

01

56

99

0

bp

Dif

fere

nc

e -

Me

dia

n5

58

12

6-4

32

48

41

3-2

5-5

61

78

-66

-84

7

Cu

mu

lati

ve a

nd

Co

nse

cuti

veT

ota

l F

un

d R

etu

rns

MS

PR

SC

um

ula

tiv

e F

or

Ye

ars

En

din

g 1

2/3

1/1

8

Co

ns

ec

uti

ve

Fo

r Y

ea

rs E

nd

ing

MJR

SC

um

ula

tiv

e F

or

Ye

ars

En

din

g 1

2/3

1/1

8

Co

ns

ec

uti

ve

Fo

r Y

ea

rs E

nd

ing

*Sta

te S

tree

t Pub

lic F

unds

Uni

vers

e

5

State of Michigan Retirement System

ASSET ALLOCATION REVIEW State of Michigan Investment Board Meeting

March 7, 2019

Jon M. Braeutigam Chief Investment Officer Bureau of Investments

ST

AT

E O

F M

ICH

IGA

N R

ET

IRE

ME

NT

SY

ST

EM

PR

OF

ILE

- D

EC

EM

BE

R 2

018

Ass

et A

lloca

tion

By

Mar

ket V

alue

(In M

illio

ns)

12/3

1/20

1812

/31/

2017

D

om

es

tic

Eq

uit

y$

15

,693

22.6

%$1

7,05

124

.4%

P

riva

te E

qu

ity

12,5

4018

.0%

10,6

2915

.2%

Pen

sio

n P

lan

OP

EB

**C

om

bin

ed

In

tern

atio

nal

Eq

uit

y11

,084

16.0

%12

,990

18.6

%M

kt.

Val

ue

Mkt

. V

alu

eM

kt.

Val

ue

%

Fix

ed I

nco

me

8,89

412

.8%

8,67

512

.4%

8,01

711

.5%

6,10

38.

7%

MP

SE

RS

$47,

472

$6,0

22$5

3,49

476

.9%

7,04

510

.1%

6,96

410

.0%

M

SE

RS

- (

clo

se

d)

11,6

752,

475

14,1

5020

.4%

A

bso

lute

Ret

urn

4,28

06.

2%4,

002

5.7%

M

SP

RS

1,41

218

51,

597

2.3%

S

ho

rt T

erm

***

1,94

32.

8%3,

520

5.0%

M

JRS

- (c

los

ed

)25

41

255

0.4%

T

OT

AL

$69,

496

100.

0%$6

9,93

410

0.0%

T

OT

AL

$60,

813

$8,6

83$6

9,49

610

0.0%

MS

ER

S in

clud

es th

e M

ilita

ry P

ensi

on F

und

Sh

ort

Ter

m S

trat

egy*

**$1

.9

S

ho

rt T

erm

in

Oth

er I

nv.

Str

ateg

ies

0.6

TO

TA

L S

HO

RT

TE

RM

$2.5

3.6%

of

To

tal

Fu

nd

s

*Th

e co

mbi

ned

net p

ayou

t for

the

plan

s fo

r FY

201

7 w

as $

2.2

billio

n w

ith $

24.2

billi

on p

aid

out s

ince

FY

200

8 th

ru F

Y 2

017

(SO

MC

AFR

). T

his

repr

esen

ts th

e am

ount

pai

d to

ben

efic

iarie

s in

exc

ess

of e

mpl

oyer

and

em

ploy

ee c

ontri

butio

ns.

**O

PE

B -

Oth

er P

ost E

mpl

oym

ent B

enef

its

18th

Lar

gest

DB

Pub

lic P

ensi

on F

und

in th

e U

.S.

Pens

ions

& In

vest

men

ts S

urve

y - F

ebru

ary

4, 2

019

issu

e

Inve

stm

ent

Str

ateg

ies

Mar

ket V

alue

By

Plan

~ 1

2/31

/18

(in M

illio

ns)

R

eal

Est

ate

& I

nfr

a. Shor

t Ter

m E

quiv

alen

ts (i

n B

illio

ns)

R

ea

l R

etu

rn &

Op

po

rt.

Pri

vate

Eq

uit

y18

.0%

Inte

rnat

ion

al E

qu

ity

16.0

%

Rea

l R

etu

rn &

O

pp

ort

un

isti

c 11

.5% Fix

ed In

com

e 12

.8%

Ab

solu

te

Ret

urn

6.2%

Sh

ort

Ter

m2.

8%

Do

mes

tic

Eq

uit

y22

.6%

Rea

l E

stat

e &

In

fras

tru

ctu

re10

.1%

Ass

et A

lloca

tion

12/3

1/18

$44.5

$47.1

$49.7

$48.1

$51.0

$56.6

$60.7

$60.1

$62.2

$6

9.9$6

9.5

$0

$10

$20

$30

$40

$50

$60

$70

$80

Mar

ket V

alue

*(B

illio

ns o

f Dol

lars

)

1

A n

egat

ive

num

ber

in a

n as

set c

ateg

ory

indi

cate

s a

use

of c

ash,

a p

ositi

ve n

umbe

r in

dica

tes

a so

urce

of

cash

.D

olla

rs in

mill

ions

-$10

9-$

103

$769

$0

-$62

$723

-$76

4

-$2,

032

So

urc

es a

nd

Use

s o

f C

ash

Ja

nu

ary

20

18

~ D

ec

em

be

r 2

01

8

Ab

solu

teR

etu

rn

Fix

ed

Inco

me

Pri

vat

eE

qu

ity

Do

mes

tic

Eq

uit

y

Inte

rnat

ion

alE

qu

ity

Rea

l E

stat

e &

Infr

astr

uct

ure

Rea

l R

etu

rn &

Op

po

rtu

nis

tic

Net

Ben

efit

Pay

men

ts

1/01

/18

Bal

ance

of

Sh

ort

-Ter

m C

ash

:

$ 3

,521

12/3

1/18

Bal

ance

of

Sh

ort

-Ter

m C

ash

:

1,94

3

Net

Sh

ort

-Ter

m C

ash

Dec

reas

e:

$

1,57

8

2

SM

RS

Ass

et C

lass

12/3

1/18

Targ

et*

12/3

1/18

Targ

et*

12/3

1/18

Targ

et*

12/3

1/18

Targ

et*

Ran

ges

Do

mes

tic

Eq

uit

y22

.6%

28.0

%22

.6%

28.0

%22

.6%

28.0

%22

.6%

28.0

%20

% -

35%

Pri

vat

e E

qu

ity

18.0

%18

.0%

18.0

%18

.0%

18.0

%18

.0%

18.0

%18

.0%

10%

- 2

0%

Inte

rnat

ion

al E

qu

ity

15.9

%16

.0%

15.9

%16

.0%

15.9

%16

.0%

15.9

%16

.0%

15%

- 2

5%

Lo

ng

Ter

m F

ixed

In

com

e12

.8%

10.5

%12

.8%

10.5

%12

.8%

10.5

%12

.8%

10.5

%10

% -

20%

Ab

solu

te R

etu

rn6.

2%6.

0%6.

2%6.

0%6.

2%6.

0%6.

2%6.

0%3%

- 9

%

Sh

ort

Ter

m F

ixed

In

com

e2.

8%2.

0%2.

8%2.

0%2.

8%2.

0%2.

8%2.

0%1%

- 6

%

TO

TA

L10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%

*Co

mp

lies

wit

h b

aske

t cl

ause

an

d i

nte

rnat

ion

al r

estr

icti

on

s.

As

of

12/3

1/18

MJ

RS

5% -

15%

Ass

et A

llo

cati

on

Tar

get

s

11.5

%9.

5%11

.5%

9.5%

11.5

%9.

5%11

.5%

9.5%

MS

PR

S

Rea

l Ret

urn

&

Op

po

rtu

nis

tic

MP

SE

RS

MS

ER

S

Rea

l Est

ate

&

Infr

astr

uct

ure

10.1

%10

.0%

10.1

%10

.0%

10.1

%5%

- 1

5%10

.0%

10.1

%10

.0%

3

State of Michigan Retirement System

MARKETS REVIEW AND OUTLOOK State of Michigan Investment Board Meeting

March 7, 2019

Gregory J. Parker, CFA Director of Investments – Public Markets

Director of Asset Allocation Bureau of Investments

CAPITAL MARKETS

Return and Risk Assumptions, Benchmark and Outlook A starting point.

MPSERS Plan

Assumed Return*

(Arithmetic) Standard Deviation*

Trailing 10-Year

(Benchmark**)

Private Equity 11.8% 24.0% 19.1% International Equity 9.9% 20.0% 6.6% Domestic Equity 8.3% 17.0% 13.2% Real Estate (Core) 6.5% 11.5% 6.1% Absolute Return 6.1% 9.0% 0.4% Real Ret/Opportunistic 9.6% 9.5% 6.4% Long-Term Fixed Income 3.5% 4.0% 3.5% Short-Term 2.8% 1.0% 0.3%

* Aon Hewitt Investment Consultants 2019 Long-Term Return/Risk Assumptions** Investment Policy Statement; Annualized Returns

*** Actual investments may differ due to changing conditions and the availability of new information

Overview A market update.

Capital market assumptions used for determining strategic asset allocations are beingreduced across the board, and especially for safer, publicly traded fixed incomesecurities. This is the general opinion for most consultants, investment banks, and othermarket participants. The reason for this phenomenon is the low interest rate environmentcaused by the policies of the Federal Reserve and other central banks, as well as therun-up in prices for most risk assets over the past several years.

Since June 2007, the growth style has returned over 50% more than value style. Perhapseven more surprising, since December 2000, growth and value have earned nearly thesame return.

Given the fact that the broad international equity index MSCI ACWI ex USA returned-14.2% for the year ending December 2018, it is not surprising that higher quality foreigncompanies outperformed on average by 1.6%.

Over the past ten, twenty, and thirty years, publicly traded REITs have out-returnedprivate real estate by 5.5%, 1.4%, and 2.8% annualized respectively, though they arethree times more volatile.

Having lost value to other currencies in 2017, as measured by the DXY Index the U.S.dollar strengthened in 2018 by 4.5%.

The most recent reading of the annualized U.S. GDP growth was 3.4%, slightly below theconsensus estimate of 3.5%. Current estimates for 2019 GDP growth for the U.S. arearound 2.5%. Coincidental economic indicators such as the Institute for SupplyManagement’s Manufacturing and Non-Manufacturing PMI Indexes are well above 50,indicating that the U.S. economy is likely to continue to grow.

1

International Equity A compelling case.

International equities continue to underperform domestic equities. Over the year ending December 2018, the international market index, MSCI ACWI ex USA, underperformed the S&P 1500 index by -9.2%. Over the past three, five, seven, and ten years, international underperformed domestic by -4.7%, -7.6%, -7.7, and -6.6% annualized, respectively.

Based on a forward estimated price-to-earnings valuation multiple, developed international markets trade at approximately a 20% discount to U.S. counterparts while emerging markets are at a 25% discount.

Year-over-year earnings growth for international markets is estimated to be roughly 9.8% for the year. Earnings in international markets can grow around 30% just to get back to all-time highs, suggesting that there could be a runway for earnings to grow at a high rate for some time. Trading at a valuation multiple discount, international equity represents a leveraged play on continued global growth.

Within international equities, emerging markets underperformed developed markets last year by -0.5%. Over the past three and five years, emerging beat developed by 6.1% and 1.3% annualized, respectively. The plan is overweight emerging markets, with a weight of 30.8% compared to the benchmark weight of 25.7%.

Given the fact that the broad international equity index MSCI ACWI ex USA returned -14.2% for the year ending December 2018, it is not surprising that higher quality foreign companies outperformed on average by 1.6%.

The plan is underweight international equity against a global benchmark (approximately 41% versus 45% of total public equity) though at a higher allocation than the peer median allocation; 16.0% versus peer median of 14.6%.

Domestic Equity High earnings growth.

The broad U.S. stock market return for the one year ending December 2018 was -4.4%. Small caps have underperformed larger caps over the past decade. Over the past one, three, five, seven, and ten years, small caps have underperformed large caps by -6.6%, -1.9%, -4.1%, -2.3% and -1.2% annualized, respectively.

Meanwhile, growth extended its dominance over value stocks in the U.S., having outperformed by 8.5%, 3.3%, 4.2%, 2.8% and 3.5% annualized over the past one, three, five, seven and ten years, respectively. Since June 2007, the growth style has returned over 50% more than value style. Perhaps even more surprising, since December 2000, growth and value have earned nearly the same return.

Analysts are estimating year-over-year growth in earnings for the next year to be nearly 12%, which is about half the rate of the trailing twelve months, but almost twice as fast as the cumulative average growth rate of the past 40 years.

Many valuation metrics are near historical averages. However, the absolute returns over the next cycle may not be as strong as the historical average of 11 – 12% year-over-year total returns. One reason for this is the fact that market EPS is above trend as is returns on equity. However, the largest securities in the market today are less cyclical (economically sensitive) as past market leaders.

2

Interest Rates The Fed on pause?

At the end of December 2018, the U.S. 10-year Treasury was yielding only 17 basis points more than the 2-year Treasury. That is the narrowest spread between the two rates since June 2007 and the dawning of the global financial crisis.

Flat yield curves are often viewed as worrisome. One material difference between the environment of today’s flat yield curve and the one in 2007 is the fact that the current Fed Fund’s rate is accommodative by historical standards, yielding a real yield of close to 0.5% while in the summer of 2007 the real yield was close to 2.5%.

At its December 2018 meeting, the Federal Reserve Board voted to raise its key interest rate by an additional 25 basis points, the ninth of this tightening cycle. At the beginning of 2019, the market has priced in very low odds of a tenth tightening, and in fact is now saying that there is a slight chance of a Fed cut in late 2019.

Spreads on investment-grade fixed income are just slightly above its average level of 1.1%. Spreads on riskier high-yield assets are slightly tighter at around 30 basis points below average. The plan has reduced its credit exposure and has instead allocated towards securitized assets which now represent 36.0% of the fixed income portfolio. Over the past year ending December 2018, the Structured Fixed Income portfolio returned 3.2% while the benchmark Aggregate index was essentially flat.

Real Estate REIT market adjustment.

Over the one year ending December 2018, the REIT market, as measured by the NAREIT index, fell -4.1% including its dividend yield.

Dividend yields on REITs are around 3.9% which is 1.25% higher than the yield of the ten-year U.S. Treasury and at its historical average spread.

Although investing in similar assets, the returns of publicly traded REITs (measured by NAREIT) and private real estate (measured by the NCREIF-ODCE Index), have historically been lowly (and at times are anti) correlated to one another. Over the past ten, twenty, and thirty years, publicly traded REITs have out-returned private real estate by 5.5%, 1.4%, and 2.8% annualized, respectively, though they are three times more volatile.

Commodities Falling prices.

Over the past ten years, commodities prices broadly have been falling, as measured by the Thomson Reuters CRB Commodity Index, down more than 60% from the peak in 2008 and, since their lows in 2016, prices are up less than 10%.

The price for crude oil has decreased over the past year ending December 2018, down 25% year-over-year to approximately $45.40 per barrel.

Having lost value to other currencies in 2017, as measured by the DXY Index the U.S. dollar strengthened in 2018 by 4.5%.

3

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Bes

tIn

t'l

Gov

'tC

orp.

Gov

'tIn

t'l

Int'

lR

eal

Int'

lIn

t'l

Gov

'tIn

t'l

U.S

.R

eal

Int'

lU

.S.

U.S

.R

eal

U.S

.In

t'l

Rea

lB

est

Equ

ity

Bon

dsB

onds

Bon

dsE

quit

yE

quit

yE

stat

eE

quit

yE

quit

yB

onds

Equ

ity

Equ

ity

Est

ate

Equ

ity

Equ

ity

Equ

ity

Est

ate

Equ

ity

Equ

ity

Est

ate

26.9

7%13

.23%

10.4

0%11

.50%

40.8

2%20

.90%

20.0

6%26

.65%

16.6

5%12

.38%

41.4

4%16

.38%

14.2

6%16

.83%

32.8

0%13

.08%

13.3

2%11

.93%

27.1

9%6.

71%

U.S

.R

eal

Rea

lC

orp.

U.S

.R

eal

Int'

lR

eal

Rea

lC

ash

U.S

.R

eal

Gov

'tU

.S.

Int'

lR

eal

U.S

.R

eal

U.S

.In

fla-

Equ

ity

Est

ate

Est

ate

Bon

dsE

quit

yE

stat

eE

quit

yE

stat

eE

stat

eE

quit

yE

stat

eB

onds

Equ

ity

Equ

ity

Est

ate

Equ

ity

Est

ate

Equ

ity

tion

20.2

7%12

.24%

7.28

%10

.52%

29.5

8%14

.48%

16.6

2%16

.59%

15.8

4%2.

05%

27.2

4%13

.11%

9.02

%16

.17%

15.2

9%11

.81%

1.01

%7.

97%

21.1

3%1.

91%

Hed

geC

orp.

Gov

'tR

eal

Hed

geU

.S.

U.S

.U

.S.

Gov

'tIn

fla-

Cor

p.In

t'l

Cor

p.R

eal

Rea

lC

orp.

Gov

'tC

orp.

Rea

lC

ash

Fund

sB

onds

Bon

dsE

stat

eFu

nds

Equ

ity

Equ

ity

Equ

ity

Bon

dsti

onB

onds

Equ

ity

Bon

dsE

stat

eE

stat

eB

onds

Bon

dsB

onds

Est

ate

18.9

3%9.

40%

7.24

%6.

74%

9.01

%11

.78%

5.65

%15

.34%

8.67

%0.

10%

16.0

5%11

.15%

8.35

%10

.54%

10.9

9%7.

53%

0.86

%5.

63%

6.96

%1.

88%

Rea

lC

ash

Cas

hH

edge

Rea

lH

edge

Hed

geH

edge

Hed

geC

orp.

Hed

geC

orp.

Infl

a-C

orp.

Hed

geG

ov't

Infl

a-In

t'l

Cor

p.G

ov't

Est

ate

Fund

sE

stat

eFu

nds

Fund

sFu

nds

Fund

sB

onds

Fund

sB

onds

tion

Bon

dsFu

nds

Bon

dsti

onE

quit

yB

onds

Bon

ds

11.3

6%6.

16%

4.43

%3.

57%

8.99

%5.

83%

5.13

%9.

21%

7.68

%-3

.07%

9.65

%8.

46%

2.96

%9.

37%

7.70

%4.

92%

0.66

%4.

50%

6.42

%0.

88%

Cas

hH

edge

Hed

geIn

fla-

Cor

p.C

orp.

Infl

a-C

ash

U.S

.R

eal

Infl

a-G

ov't

U.S

.H

edge

Infl

a-H

edge

Hed

geIn

fla-

Hed

geH

edge

Fund

sFu

nds

tion

Bon

dsB

onds

tion

Equ

ity

Est

ate

tion

Bon

dsE

quit

yFu

nds

tion

Fund

sFu

nds

tion

Fund

sFu

nds

4.83

%5.

77%

3.11

%2.

39%

7.69

%5.

25%

3.42

%4.

81%

5.47

%-6

.46%

2.72

%5.

52%

1.75

%4.

22%

1.49

%3.

14%

0.37

%2.

09%

3.88

%-1

.05%

Infl

a-In

fla-

Infl

a-C

ash

Gov

'tG

ov't

Cas

hC

orp.

Cor

p.H

edge

Cas

hH

edge

Cas

hG

ov't

Cas

hIn

fla-

Cas

hH

edge

Gov

'tC

orp.

tion

tion

tion

Bon

dsB

onds

Bon

dsB

onds

Fund

sFu

nds

Bon

dsti

onFu

nds

Bon

dsB

onds

2.68

%3.

39%

1.55

%1.

79%

2.36

%3.

48%

3.06

%4.

27%

5.10

%-1

9.86

%0.

19%

5.07

%0.

10%

2.02

%0.

07%

0.68

%0.

01%

1.89

%2.

30%

-2.5

1%C

orp.

U.S

.U

.S.

Int'

lIn

fla-

Infl

a-G

ov't

Gov

'tC

ash

U.S

.G

ov't

Infl

a-H

edge

Infl

a-C

orp.

Cas

hC

orp.

Gov

'tIn

fla-

U.S

.B

onds

Equ

ity

Equ

ity

Equ

ity

tion

tion

Bon

dsB

onds

Equ

ity

Bon

dsti

onFu

nds

tion

Bon

dsB

onds

Bon

dsti

onE

quit

y

-1.9

4%-6

.98%

-10.

64%

-14.

95%

1.88

%3.

25%

2.65

%3.

46%

5.03

%-3

6.72

%-2

.19%

1.50

%-3

.55%

1.70

%-2

.01%

0.04

%-0

.77%

1.05

%2.

12%

-4.9

6%G

ov't

Int'

lIn

t'l

U.S

.C

ash

Cas

hC

orp.

Infl

a-In

fla-

Int'

lR

eal

Cas

hIn

t'l

Cas

hG

ov't

Int'

lIn

t'l

Cas

hC

ash

Int'

lB

onds

Equ

ity

Equ

ity

Equ

ity

Bon

dsti

onti

onE

quit

yE

stat

eE

quit

yB

onds

Equ

ity

Equ

ity

Equ

ity

Wo

rst

-2.2

5%-1

5.31

%-1

9.74

%-2

1.30

%1.

16%

1.33

%1.

95%

2.55

%4.

06%

-45.

52%

-16.

86%

0.13

%-1

3.71

%0.

11%

-2.6

0%-3

.87%

-5.6

7%0.

27%

0.84

%-1

4.20

%W

ors

t

An

nu

aliz

ed R

etu

rns

1999

- 2

018

Cas

hIn

fl.

Hed

geG

ov't

.C

orp.

Int'

l.U

S E

q.R

.E.

Ret

urn

1.90

%2.

17%

3.73

%4.

12%

5.24

%4.

64%

5.99

%8.

97%

Ret

urn

Ris

k1.

01%

1.34

%5.

14%

4.46

%5.

18%

18.8

5%16

.06%

4.55

%R

isk

- H

edge

Fun

ds a

re r

epre

sent

ed b

y th

e H

FR

I FO

F C

onse

rvat

ive

Inde

x-

U.S

. Equ

ity is

rep

rese

nted

by

the

S&

P 1

500

- In

flatio

n is

rep

rese

nted

by

the

U.S

. Con

sum

er P

rice

Inde

x-

Rea

l Est

ate

is r

epre

sent

ed b

y th

e N

PI

- In

tern

atio

nal E

quity

is r

epre

sent

ed b

y th

e M

SC

I - A

C W

orld

EX

-US

A In

dex

- C

orpo

rate

Bon

ds a

re r

epre

sent

ed b

y th

e B

arcl

ays

Cap

ital -

Cre

dit I

ndex

- C

ash

is r

epre

sent

ed b

y 30

-day

T-B

ills

- G

over

nmen

t Bon

ds a

re r

epre

sent

ed b

y th

e B

arcl

ays

Cap

ital U

.S. G

over

nmen

t

An

nu

al

To

tal

Ret

urn

s o

f K

ey A

sset

Cla

sses

199

9 -

2018

4

State of Michigan Retirement System

DEFINED CONTRIBUTION REVIEW

State of Michigan Investment Board Meeting March 7, 2019

Woodrow S. TylerSenior Investment Manager

Defined Contribution, Trusts & Agencies Division

EXECUTIVE SUMMARY

Overview

The State of Michigan’s Defined Contribution (DC) plan has over 177,590 participants across four constituent bases as shown below. The State’s DC program initially started as a supplemental retirement plan, but for many of the plans it is now participants’ primary retirement vehicle.

DC plans are participant led investments. The role of the Bureau of Investments is to offer a sufficient range of investment options to allow the Participants to diversify their individual retirement accounts and construct portfolios that reasonably span the risk/return spectrum. To this end, the Plans may be comprised of at least one investment option from the categories below.

SOM Plans

(12-31-18)

Number of

Participants

Combined 401k & 457

State Employees 74,611 $6,979

School Employees 101,326 585

Judges 686 253

State Police 968 23

Total 177,591 $7,841 ($ in millions)

Investments Options

Tier I: Target Date Funds and Passively Managed Index Funds Target Date Funds (TDFs) are the default option for plan participants. Each TDF seeks

to achieve its objective by investing in a set of underlying index funds representing various asset classes. Over time, the allocation to asset classes and funds change according to a predetermined "glide path" and will become more conservative as it approaches the target retirement date.

Passively Managed Index Funds are comprised of low-cost index funds which seek to replicate the performance of a variety of cash, bond and stock indices with very little tracking error and at a low fee.

Tier II: Actively Managed Funds These are funds actively managed by investment managers in an attempt to

outperform various cash, bond and stock indices over long periods of time.

Tier III: Self Directed Brokerage Account – Non-Core Options TD Ameritrade provides access to a broad range of investment choices including

individual stocks, bonds, CDs, over 100 commission-free ETFs, and more than 13,000 mutual funds—including more than 2,100 no-load, no-transaction-fee (NTF) mutual funds.

1

Investment Selection The selection of each investment option for the Plans is to be based on the prudence

standards set by the Governing Documents and applicable law, with flexibility built-in to allow a search to take full advantage of strategic opportunities. The search will focus on finding opportunities which are tailored to the Plans’ specific needs. The BOI, in consultation with the Office of Retirement Services (ORS), will establish search criteria that aligns with the purpose and objective an investment option is seeking to attain. Due diligence will be completed with the goal of selecting a plan that, in the totality of circumstances, offers fair and reasonable investment options for the Plan participants.

With respect to Tier III investments, the universe of available options is extensive. Since the selection of investments is directed solely by the Participants which elect the Tier III option, the State does not provide any criteria for selecting or monitoring these non-core investment options.

Investment Monitoring The ORS and the BOI may examine each investment option as circumstances require,

to ensure that a particular investment option’s investment style and other relevant investment criteria, such as performance, fee and expense levels or the occurrence of a significant change are acceptable, given the purpose of each investment option.

Market Environment and Outlook Structural changes in the U.S. retirement system are supporting growth in the DC

industry: o Rapid decline of employer funded pensions o Potential erosion of Social Security benefits o Workforce aging o New regulations, specifically, the Pension Protection Act of 2006;

Automatically enroll employees into the DC plan Establish safe harbor investments known as QDIA

In an effort to simplify the investment process for participants, industry trend has been to

reduce the number of investment options offered in a DC plan. Based on the recent CEM benchmark report, the average number of investments offered by similarly sized plans is 13 options. The State of Michigan currently offers 20 investment options. The desired outcome of streamlining would be to benefit from economies of scale and ease the burden of asset allocation at the participant level.

Another trend in the industry is the focus on retirement income. As fewer individuals have access to pension plans and DC plans have become the primary retirement vehicle for many Americans, more plan sponsors are exploring the ability to generate sustainable income in retirement.

2

Target Date Funds The Pension Protection Act of 2006 established safe harbor investments known as Qualified Default Investment Alternative (QDIA). To qualify as a QDIA, the investment must offer; “a mix of investments which take into account the individual’s age or retirement date.” Target Date Funds (TDFs) are an example of this. Over time, the allocation to asset classes and funds change according to a predetermined "glide path" and will become more conservative as it approaches the target retirement date. The allocations in the glide path are not due to tactical decisions to overweight or underweight a particular asset class based on its market outlook. Because index funds are used, each Fund attempts to closely match the characteristics and returns of its custom benchmark as opposed to any attempts to outperform this benchmark.

Ret. Income

TDF 2015

TDF 2020TDF 2025

TDF 2030

TDF 2035TDF 2040

TDF 2045

TDF 2050

TDF 2055

TDF 2060

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0 0.2 0.4 0.6 0.8 1 1.2 1.4

Return %

Beta

Return vs Beta 2015 ‐ 2018

3

Index Funds Tier I is comprised of low-cost funds which seek to replicate the performance of a variety of bond and stock market indices.

Actively Managed FundsTier II is comprised of actively managed funds which attempt to outperform various bond and stock indices.

Non-Core Options Tier III is a Self Directed Brokerage Account.

Short Term Investments

SSgA Bond Fund

S&P 500 Index

S&P Midcap

Global Equities Fund

Emerging Markets Fund

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0 0.2 0.4 0.6 0.8 1 1.2 1.4

Return %

Beta

Return vs Beta 2015 ‐ 2018

Stable Value

PIMCO Total ReturnPrudential High Yield

Oakmark

Dodge & CoxT. Rowe Price Mid Cap

Value

Artisan Mid‐Cap Growth

Virtus Small Cap Value

VoyaSmall Cap Growth

American Funds EuroPacific Growth

Jennison Large Cap Growth

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0 0.2 0.4 0.6 0.8 1 1.2 1.4

Return %

Beta

Return vs Beta 2015 ‐ 2018

4

Plan Awards and Recognitions 2014-2018 2018 2018 Signature Award

ORS tied for third place in the Retirement Readiness category of the 2018 Signature Awards, presentedby the Plan Sponsor Council of America (PSCA) during its 71st annual National Conference inScottsdale, Arizona. The Signature Award recognizes excellence in retirement plan communications toboth plan sponsors and plan participants. ORS and Voya Financial received the award for the Women'sGuide to Retirement. The guide was developed after focus group and survey results showed thatwomen had significant concerns about retirement. The 16-page guide breaks planning for retirementdown into achievable steps and provides web and phone resources.

Two NAGDCA Leadership AwardsORS received two 2017 Leadership Recognition Awards through the National Association ofGovernment Defined Contribution Administrators (NAGDCA). These awards recognize DC plans fortheir outstanding achievements. The Road to Retirement campaign won the award for outstandingachievement in Technology and Social Media. The Small Steps campaign won the award foroutstanding achievement in Plan Design.

2016 State of Michigan and Voya Financial® win Plan Sponsor Council of America (PSCA) Signature

AwardFor the second consecutive year, ORS received a Signature Award from PSCA. The NearingRetirement Guide from The State of Michigan and Voya® took second place in PSCA's PlanPublications for Participants category. The guide is handed out during ORS's Pre-RetirementOrientations and at Voya's Get Ready to Retire seminars.

2015 ORS and Voya share Eddy Award

ORS won second place as the plan sponsor in the Special Projects category for public plans at theEddy Awards. The Eddy Award is the annual recognition by Pensions & Investments (P&I) of bestpractices by defined contribution plans in providing investment education to participants. VoyaFinancial™, which designed the award-winning campaign, shares the award with ORS. The winningentry was the “Mix It Up” campaign, designed to give state employee 401(k) participants a simple wayto improve their investment mix.

ORS recognized with two industry awardsNAGDCA, the National Association of Government Defined Contribution Administrators, Inc., selectedORS to receive two 2014 Leadership Awards. The first award was in the EffectiveCommunication/Participant Education category, while the second award was in the Plan Designcategory. Plan design covers how the DC plan functions – what features are offered to plan participants,investment portfolio options, loan or withdrawal provisions, and other aspects covering how the DCplan work.

2014 NAGDCA Award

ORS has been chosen as a recipient of the 2013 Leadership Recognition Award through the NationalAssociation of Government Defined Contribution Administrators' (NAGDCA). This award recognizesdefined contribution plans for outstanding achievements in Participant Education and EffectiveCommunication. Only the top five projects in each category receive a Leadership Award, and this is thethird year in a row ORS has been recognized.

Best in Show AwardThe State of Michigan 401(k) & 457 Plans have won a Best in Show award from the Insurance andFinancial Communicators Association. Chosen from 650 submissions, the award recognizes thecreativity, design, and writing in the State of Michigan Match Campaign.

Plan Sponsor AwardORS was awarded as a finalist for the 2014 PLAN SPONSOR Plan Sponsor of the Year award in thePublic DC category for our 457 Plan. The finalists were featured in the March 2014 issue ofPLANSPONSOR Magazine.

5

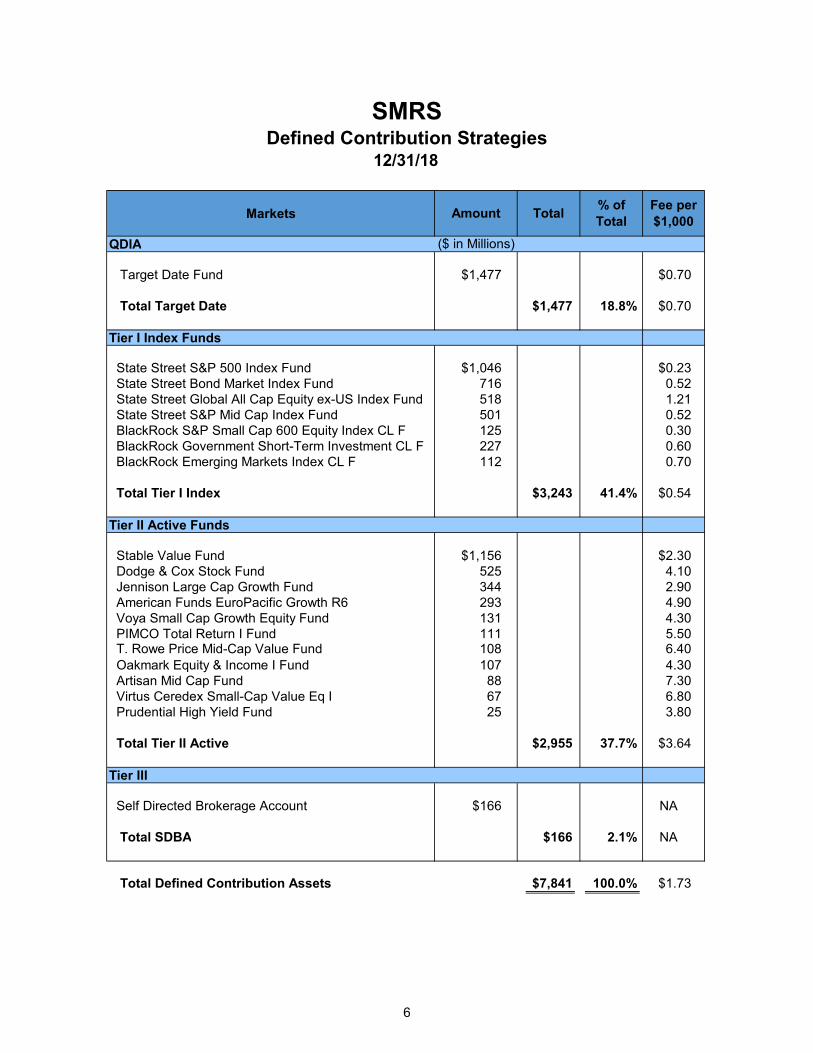

SMRSDefined Contribution Strategies

Markets

QDIA

Target Date Fund $1,477 $0.70

Total Target Date $1,477 18.8% $0.70

Tier I Index Funds

State Street S&P 500 Index Fund $1,046 $0.23 State Street Bond Market Index Fund 716 0.52 State Street Global All Cap Equity ex-US Index Fund 518 1.21 State Street S&P Mid Cap Index Fund 501 0.52 BlackRock S&P Small Cap 600 Equity Index CL F 125 0.30 BlackRock Government Short-Term Investment CL F 227 0.60 BlackRock Emerging Markets Index CL F 112 0.70

Total Tier I Index $3,243 41.4% $0.54

Tier II Active Funds

Stable Value Fund $1,156 $2.30 Dodge & Cox Stock Fund 525 4.10 Jennison Large Cap Growth Fund 344 2.90 American Funds EuroPacific Growth R6 293 4.90 Voya Small Cap Growth Equity Fund 131 4.30 PIMCO Total Return I Fund 111 5.50 T. Rowe Price Mid-Cap Value Fund 108 6.40 Oakmark Equity & Income I Fund 107 4.30 Artisan Mid Cap Fund 88 7.30 Virtus Ceredex Small-Cap Value Eq I 67 6.80 Prudential High Yield Fund 25 3.80

Total Tier II Active $2,955 37.7% $3.64

Tier III

Self Directed Brokerage Account $166 NA

Total SDBA $166 2.1% NA

Total Defined Contribution Assets $7,841 100.0% $1.73

12/31/18

Amount Total

($ in Millions)

% of Total

Fee per $1,000

6

SMRSDefined Contribution by Investment Strategy

12/31/18

Market Value in Millions

12/31/18 12/31/17Passive Strategies $3,243 41.4% $4,548 55.2%Active Strategies 2,955 37.7% 2,123 25.8%Target Date Retirement Fund 1,477 18.8% 1,382 16.8%Self Managed Account 166 2.1% 184 2.2%

Total Investments $7,841 100.0% $8,237 100.0%

*Loan Fund $192M as of 12/31/18

Passive Strategies

41.4%

Active Strategies37.7%

Target Date Retirement Fund

18.8%

Self Managed Account

2.1%

7

Fund Name Market Value 1-Year 3-Years 5-Years 10-Years

State Street Target Retirement Income Fund $36,495,096 -2.8% 3.7% 2.7% 5.6%State Street Income Custom Index -2.8% 3.7% 2.7% 5.8%Morningstar Target-Date Retirement -3.2% 3.4% 2.5% 5.7%Variance State Street Income Custom Index 0.0% 0.0% 0.0% -0.2%Variance Morningstar Target-Date Retirement 0.4% 0.2% 0.1% -0.1%

State Street Target Retirement 2015 Fund 51,679,117 -3.1% 4.4% 3.3% 7.5%State Street 2015 Custom Index -3.2% 4.3% 3.3% 7.6%Morningstar Target-Date 2015 -3.9% 4.3% 3.2% 6.9%Variance State Street 2015 Custom Index 0.0% 0.0% 0.0% -0.1%Variance Morningstar Target-Date 2015 0.8% 0.1% 0.2% 0.6%

State Street Target Retirement 2020 Fund 122,746,583 -4.5% 5.2% 3.9% 8.5%State Street 2020 Custom Index -4.5% 5.1% 3.9% 8.5%Morningstar Target-Date 2020 -4.6% 4.4% 3.2% 7.3%Variance State Street 2020 Custom Index 0.0% 0.1% 0.0% 0.0%Variance Morningstar Target-Date 2020 0.1% 0.8% 0.6% 1.1%

State Street Target Retirement 2025 Fund 151,640,528 -5.9% 5.8% 4.3% 9.1%State Street 2025 Custom Index -5.9% 5.8% 4.3% 9.2%Morningstar Target-Date 2025 -5.4% 5.0% 3.7% 8.3%Variance State Street 2025 Custom Index 0.0% 0.0% 0.0% -0.1%Variance Morningstar Target-Date 2025 -0.5% 0.8% 0.7% 0.8%

State Street Target Retirement 2030 Fund 165,505,713 -6.7% 6.1% 4.5% 9.6%State Street 2030 Custom Index -6.7% 6.0% 4.5% 9.7%Morningstar Target-Date 2030 -6.3% 5.4% 3.8% 8.6%Variance State Street 2030 Custom Index 0.0% 0.0% 0.0% -0.1%Variance Morningstar Target-Date 2030 -0.4% 0.7% 0.6% 1.1%

State Street Target Retirement 2035 Fund 176,168,615 -7.3% 6.3% 4.6% 9.9%State Street 2035 Custom Index -7.3% 6.3% 4.6% 10.0%Morningstar Target-Date 2035 -7.1% 5.8% 4.1% 9.2%Variance State Street 2035 Custom Index 0.0% 0.1% 0.0% -0.1%Variance Morningstar Target-Date 2035 -0.3% 0.5% 0.5% 0.7%

State Street Target Retirement 2040 Fund 169,494,516 -7.9% 6.6% 4.7% 10.0%State Street 2040 Custom Index -7.9% 6.5% 4.7% 10.1%Morningstar Target-Date 2040 -7.8% 5.9% 4.2% 9.3%Variance State Street 2040 Custom Index 0.0% 0.1% 0.0% -0.1%Variance Morningstar Target-Date 2040 -0.1% 0.7% 0.5% 0.8%

State Street Target Retirement 2045 Fund 169,012,014 -8.4% 6.7% 4.7% 10.1%State Street 2045 Custom Index -8.5% 6.6% 4.7% 10.1%Morningstar Target-Date 2045 -8.1% 6.1% 4.3% 9.6%Variance State Street 2045 Custom Index 0.0% 0.1% 0.0% -0.1%Variance Morningstar Target-Date 2045 -0.3% 0.6% 0.4% 0.4%

State Street Target Retirement 2050 Fund 207,969,361 -8.6% 6.7% 4.7% 10.1%State Street 2050 Custom Index -8.6% 6.6% 4.7% 10.1%Morningstar Target-Date 2050 -8.4% 6.1% 4.3% 9.5%Variance State Street 2050 Custom Index 0.0% 0.1% 0.0% -0.1%Variance Morningstar Target-Date 2050 -0.1% 0.6% 0.4% 0.5%

State Street Target Retirement 2055 Fund 189,330,185 -8.6% 6.7% 4.7% N/AState Street 2055 Custom Index -8.6% 6.6% 4.7% N/AMorningstar Target-Date 2055 -8.4% 6.2% 4.4% N/AVariance State Street 2055 Custom Index 0.0% 0.1% 0.0% N/AVariance Morningstar Target-Date 2055 -0.1% 0.5% 0.3% N/A

Defined Contribution Performance by Fund12/31/18

8

Fund Name Market Value 1-Year 3-Years 5-Years 10-Years

State Street Target Retirement 2060 Fund $37,126,336 -8.5% 6.7% N/A N/AState Street 2060 Custom Index -8.6% 6.6% N/A N/AMorningstar Target-Date 2060+ -8.5% 6.2% N/A N/AVariance State Street 2060 Custom Index 0.0% 0.1% N/A N/AVariance Morningstar Target-Date 2060+ 0.0% 0.5% N/A N/A

TIER I

State Street S&P 500 Index Fund 1,045,641,904 -4.4% 9.2% 8.5% 13.1%S&P 500 Index -4.4% 9.3% 8.5% 13.1%Morningstar Large Blend -6.2% 7.5% 6.3% 11.4%Variance S&P 500 Index 0.0% 0.0% 0.0% 0.0%Variance Morningstar Large Blend 1.8% 1.7% 2.2% 1.6%

State Street Bond Market Index Fund 715,603,370 0.0% 2.0% 2.5% 3.4%Bloomberg Barclays U.S. Aggregate Index 0.0% 2.1% 2.5% 3.5%Morningstar Intermediate-Term Bond -0.5% 2.1% 2.2% 4.3%Variance Bloomberg Barclays U.S. Aggregate Index 0.0% -0.1% 0.0% -0.1%Variance Morningstar Intermediate-Term Bond 0.5% -0.1% 0.2% -0.9%

State Street Global All Cap Equity ex-U.S. Index Fund 517,884,681 -14.6% 4.8% 1.0% N/AMSCI ACWI ex USA IMI (Net) -14.8% 4.4% 0.9% N/AMorningstar Foreign Large Blend -14.6% 2.5% 0.1% N/AVariance MSCI ACWI ex USA IMI (Net) 0.2% 0.4% 0.2% N/AVariance Morningstar Foreign Large Blend 0.0% 2.3% 0.9% N/A

State Street S&P Mid Cap Index Fund 501,266,011 -11.1% 7.6% 6.0% 13.6%S&P 400 Index -11.1% 7.7% 6.0% 13.7%Morningstar Mid-Cap Blend -11.3% 5.3% 3.8% 11.7%Variance S&P 400 Index 0.0% 0.0% -0.1% -0.1%Variance Morningstar Mid-Cap Blend 0.2% 2.3% 2.2% 1.9%

BlackRock Government Short-Term Investment CL F 226,745,077 1.8% 1.0% 0.6% N/ABofA Merill Lynch US 3-Month Treasury Bill Index 1.9% 1.0% 0.6% N/AVariance BofA Merill Lynch US 3-Month Treasury Bill Index 0.0% 0.0% 0.0% N/A

BlackRock S&P Small Cap 600 Equity Index CL F 124,519,131 -8.5% N/A N/A N/ARussell 2000 Index -11.0% N/A N/A N/AMorningstar Small Blend -12.7% N/A N/A N/AVariance Russell 2000 Index 2.5% N/A N/A N/AVariance Morningstar Small Blend 4.2% N/A N/A N/A

BlackRock Emerging Markets Index CL F 111,538,819 -14.6% 9.4% 1.6% N/AMSCI Emerging Market (Net) -14.6% 9.3% 1.7% N/AMorningstar Diversified Emerging Mkts -16.1% 6.9% 0.4% N/AVariance MSCI Emerging Market (Net) 0.0% 0.2% -0.1% N/AVariance Morningstar Diversified Emerging Mkts 1.5% 2.5% 1.1% N/A

TIER II

Stable Value Fund 1,155,620,948 2.1% 2.1% 2.1% 2.2%Barclays Int Gov/Credit A or Higher Index 1.2% 1.4% 1.7% 2.4%Hueler Universe 2.2% 2.0% 1.9% 2.2%Variance Barclays Int. Gov Credit A or Better Index 0.9% 0.7% 0.5% -0.2%Variance Hueler Universe -0.2% 0.1% 0.3% 0.0%

Dodge & Cox Stock Fund 525,248,803 -7.6% 9.9% 7.0% 13.1%Russell 1000 Value Index -8.3% 7.0% 6.0% 11.2%Morningstar Large Value -8.6% 6.7% 5.1% 10.5%Variance Russell 1000 Value Index 0.7% 2.9% 1.0% 1.9%Variance Morningstar Large Value 1.0% 3.1% 1.8% 2.7%

9

Fund Name Market Value 1-Year 3-Years 5-Years 10-Years

Jennison Large Cap Growth Fund $344,316,131 0.2% 11.5% N/A N/ARussell 1000 Growth Index -1.5% 11.2% N/A N/AMorningstar Large Growth -2.2% 8.9% N/A N/AVariance Russell 1000 Growth Index 1.7% 0.3% N/A N/AVariance Morningstar Large Growth 2.4% 2.6% N/A N/A