State space modelsOutline 1ARIMA models in state space form 2RegARMA models in state space form 3The...

72

Rob J Hyndman State space models 3: ARIMA and RegARMA models, and dlm

Transcript of State space modelsOutline 1ARIMA models in state space form 2RegARMA models in state space form 3The...

Rob J Hyndman

State space models

3: ARIMA and RegARMA models, and dlm

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 2

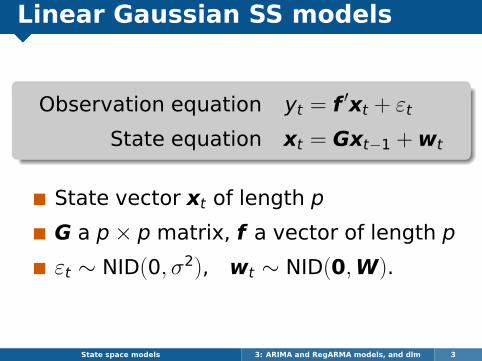

Linear Gaussian SS models

Observation equation yt = f ′xt + εt

State equation xt = Gxt−1 + wt

State vector xt of length p

G a p× p matrix, f a vector of length p

εt ∼ NID(0, σ2), wt ∼ NID(0,W).

State space models 3: ARIMA and RegARMA models, and dlm 3

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 4

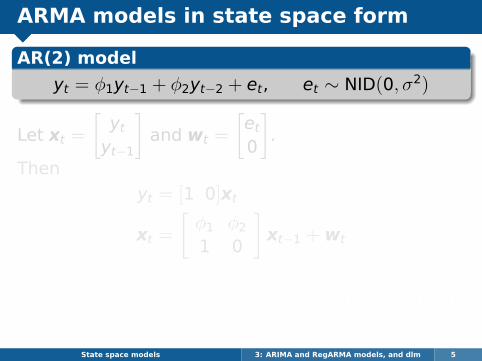

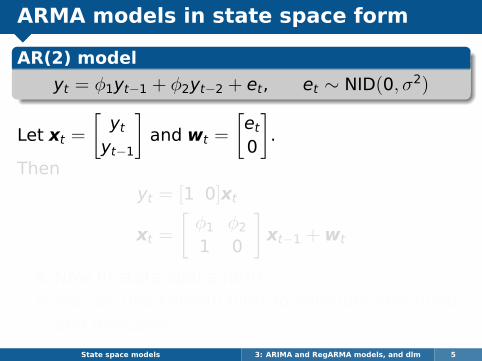

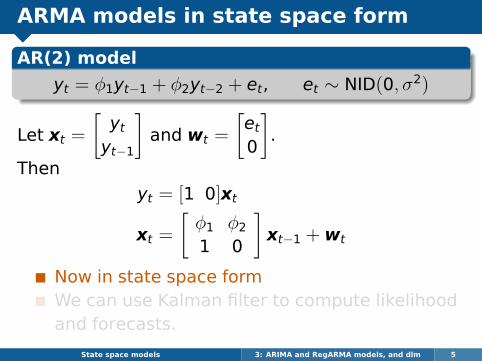

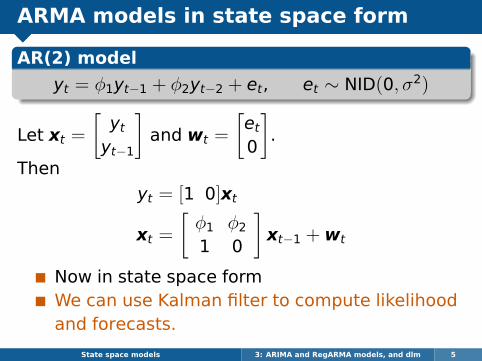

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Let xt =

[ytyt−1

]and wt =

[et0

].

Then

yt = [1 0]xt

xt =

[φ1 φ2

1 0

]xt−1 + wt

Now in state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 5

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Let xt =

[ytyt−1

]and wt =

[et0

].

Then

yt = [1 0]xt

xt =

[φ1 φ2

1 0

]xt−1 + wt

Now in state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 5

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Let xt =

[ytyt−1

]and wt =

[et0

].

Then

yt = [1 0]xt

xt =

[φ1 φ2

1 0

]xt−1 + wt

Now in state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 5

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Let xt =

[ytyt−1

]and wt =

[et0

].

Then

yt = [1 0]xt

xt =

[φ1 φ2

1 0

]xt−1 + wt

Now in state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 5

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Let xt =

[ytyt−1

]and wt =

[et0

].

Then

yt = [1 0]xt

xt =

[φ1 φ2

1 0

]xt−1 + wt

Now in state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 5

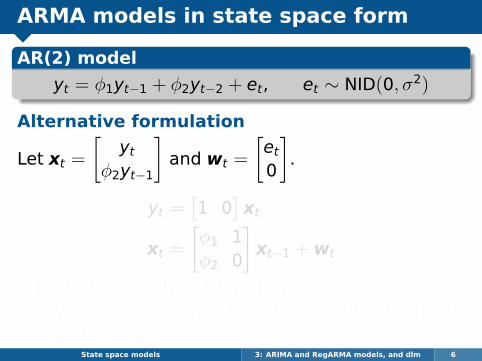

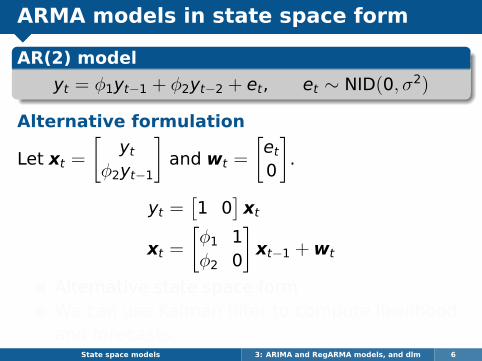

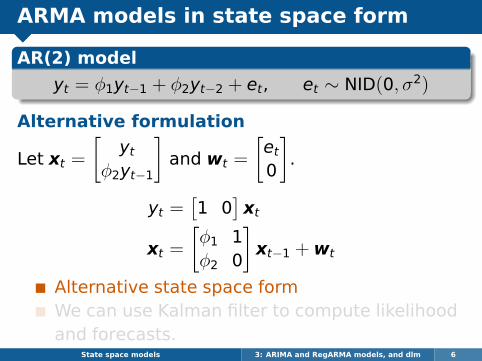

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Alternative formulation

Let xt =

[yt

φ2yt−1

]and wt =

[et0

].

yt =[1 0

]xt

xt =

[φ1 1φ2 0

]xt−1 + wt

Alternative state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 6

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Alternative formulation

Let xt =

[yt

φ2yt−1

]and wt =

[et0

].

yt =[1 0

]xt

xt =

[φ1 1φ2 0

]xt−1 + wt

Alternative state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 6

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Alternative formulation

Let xt =

[yt

φ2yt−1

]and wt =

[et0

].

yt =[1 0

]xt

xt =

[φ1 1φ2 0

]xt−1 + wt

Alternative state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 6

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Alternative formulation

Let xt =

[yt

φ2yt−1

]and wt =

[et0

].

yt =[1 0

]xt

xt =

[φ1 1φ2 0

]xt−1 + wt

Alternative state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 6

ARMA models in state space form

AR(2) model

yt = φ1yt−1 + φ2yt−2 + et, et ∼ NID(0, σ2)

Alternative formulation

Let xt =

[yt

φ2yt−1

]and wt =

[et0

].

yt =[1 0

]xt

xt =

[φ1 1φ2 0

]xt−1 + wt

Alternative state space formWe can use Kalman filter to compute likelihoodand forecasts.

State space models 3: ARIMA and RegARMA models, and dlm 6

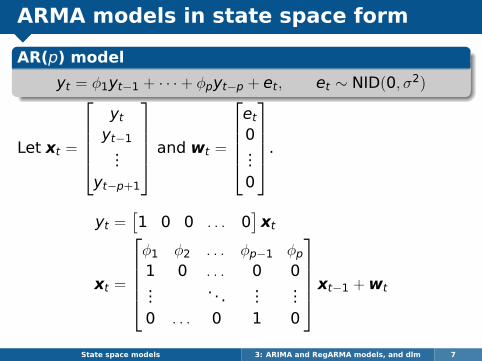

ARMA models in state space form

AR(p) model

yt = φ1yt−1 + · · ·+ φpyt−p + et, et ∼ NID(0, σ2)

Let xt =

ytyt−1

...yt−p+1

and wt =

et0...0

.

yt =[1 0 0 . . . 0

]xt

xt =

φ1 φ2 . . . φp−1 φp1 0 . . . 0 0...

. . ....

...0 . . . 0 1 0

xt−1 + wt

State space models 3: ARIMA and RegARMA models, and dlm 7

ARMA models in state space form

AR(p) model

yt = φ1yt−1 + · · ·+ φpyt−p + et, et ∼ NID(0, σ2)

Let xt =

ytyt−1

...yt−p+1

and wt =

et0...0

.

yt =[1 0 0 . . . 0

]xt

xt =

φ1 φ2 . . . φp−1 φp1 0 . . . 0 0...

. . ....

...0 . . . 0 1 0

xt−1 + wt

State space models 3: ARIMA and RegARMA models, and dlm 7

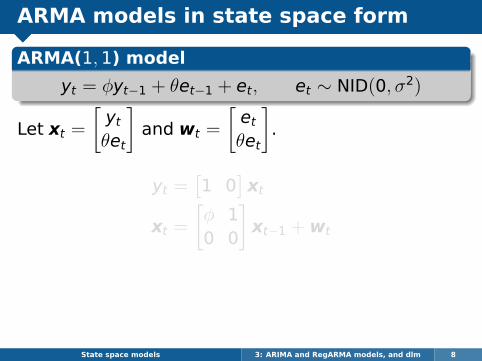

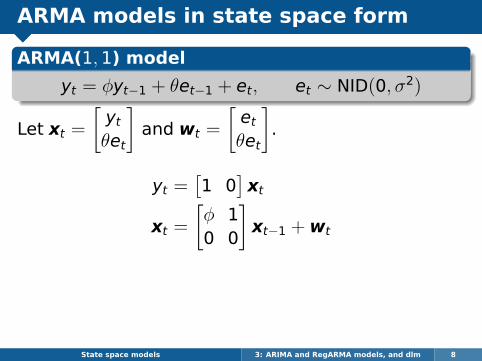

ARMA models in state space form

ARMA(1,1) model

yt = φyt−1 + θet−1 + et, et ∼ NID(0, σ2)

Let xt =

[ytθet

]and wt =

[etθet

].

yt =[1 0

]xt

xt =

[φ 10 0

]xt−1 + wt

State space models 3: ARIMA and RegARMA models, and dlm 8

ARMA models in state space form

ARMA(1,1) model

yt = φyt−1 + θet−1 + et, et ∼ NID(0, σ2)

Let xt =

[ytθet

]and wt =

[etθet

].

yt =[1 0

]xt

xt =

[φ 10 0

]xt−1 + wt

State space models 3: ARIMA and RegARMA models, and dlm 8

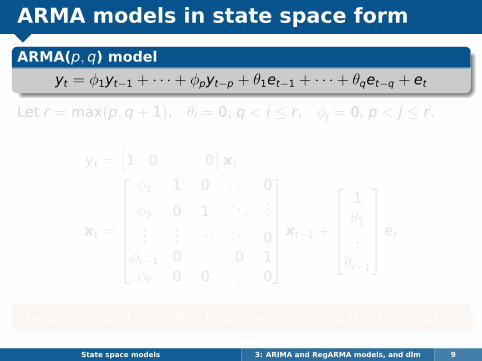

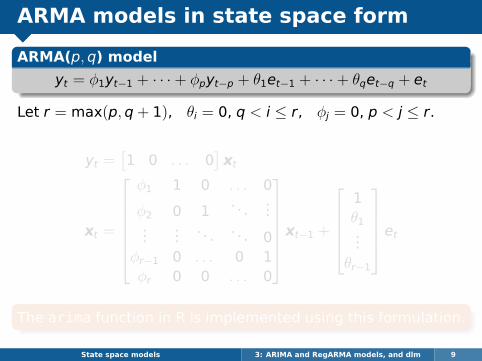

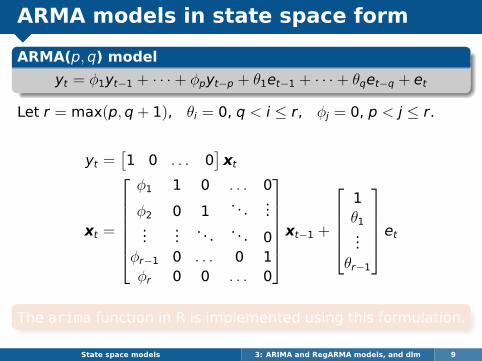

ARMA models in state space form

ARMA(p,q) model

yt = φ1yt−1 + · · ·+ φpyt−p + θ1et−1 + · · ·+ θqet−q + et

Let r = max(p,q+ 1), θi = 0, q < i ≤ r, φj = 0, p < j ≤ r.

yt =[1 0 . . . 0

]xt

xt =

φ1 1 0 . . . 0

φ2 0 1. . .

......

.... . . . . . 0

φr−1 0 . . . 0 1φr 0 0 . . . 0

xt−1 +

1θ1...

θr−1

et

The arima function in R is implemented using this formulation.

State space models 3: ARIMA and RegARMA models, and dlm 9

ARMA models in state space form

ARMA(p,q) model

yt = φ1yt−1 + · · ·+ φpyt−p + θ1et−1 + · · ·+ θqet−q + et

Let r = max(p,q+ 1), θi = 0, q < i ≤ r, φj = 0, p < j ≤ r.

yt =[1 0 . . . 0

]xt

xt =

φ1 1 0 . . . 0

φ2 0 1. . .

......

.... . . . . . 0

φr−1 0 . . . 0 1φr 0 0 . . . 0

xt−1 +

1θ1...

θr−1

et

The arima function in R is implemented using this formulation.

State space models 3: ARIMA and RegARMA models, and dlm 9

ARMA models in state space form

ARMA(p,q) model

yt = φ1yt−1 + · · ·+ φpyt−p + θ1et−1 + · · ·+ θqet−q + et

Let r = max(p,q+ 1), θi = 0, q < i ≤ r, φj = 0, p < j ≤ r.

yt =[1 0 . . . 0

]xt

xt =

φ1 1 0 . . . 0

φ2 0 1. . .

......

.... . . . . . 0

φr−1 0 . . . 0 1φr 0 0 . . . 0

xt−1 +

1θ1...

θr−1

et

The arima function in R is implemented using this formulation.

State space models 3: ARIMA and RegARMA models, and dlm 9

ARMA models in state space form

ARMA(p,q) model

yt = φ1yt−1 + · · ·+ φpyt−p + θ1et−1 + · · ·+ θqet−q + et

Let r = max(p,q+ 1), θi = 0, q < i ≤ r, φj = 0, p < j ≤ r.

yt =[1 0 . . . 0

]xt

xt =

φ1 1 0 . . . 0

φ2 0 1. . .

......

.... . . . . . 0

φr−1 0 . . . 0 1φr 0 0 . . . 0

xt−1 +

1θ1...

θr−1

et

The arima function in R is implemented using this formulation.

State space models 3: ARIMA and RegARMA models, and dlm 9

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 10

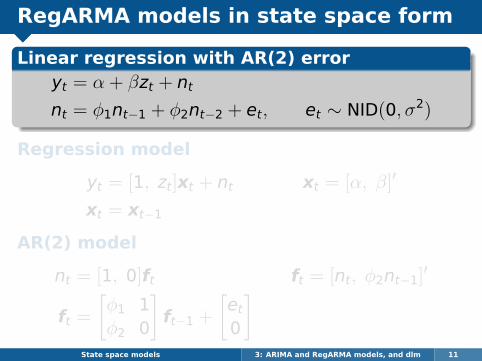

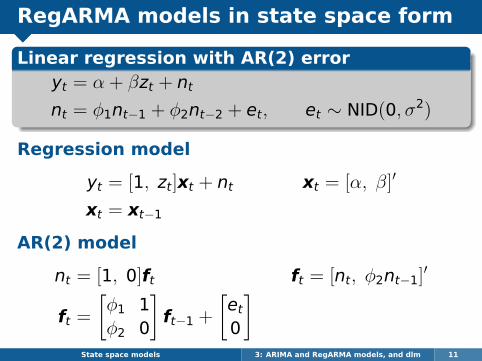

RegARMA models in state space form

Linear regression with AR(2) erroryt = α + βzt + ntnt = φ1nt−1 + φ2nt−2 + et, et ∼ NID(0, σ2)

Regression model

yt = [1, zt]xt + nt xt = [α, β]′

xt = xt−1

AR(2) model

nt = [1, 0]ft ft = [nt, φ2nt−1]′

ft =

[φ1 1φ2 0

]ft−1 +

[et0

]State space models 3: ARIMA and RegARMA models, and dlm 11

RegARMA models in state space form

Linear regression with AR(2) erroryt = α + βzt + ntnt = φ1nt−1 + φ2nt−2 + et, et ∼ NID(0, σ2)

Regression model

yt = [1, zt]xt + nt xt = [α, β]′

xt = xt−1

AR(2) model

nt = [1, 0]ft ft = [nt, φ2nt−1]′

ft =

[φ1 1φ2 0

]ft−1 +

[et0

]State space models 3: ARIMA and RegARMA models, and dlm 11

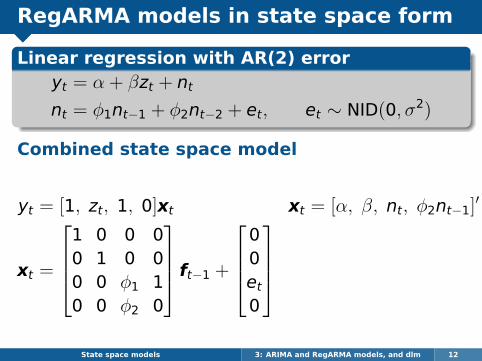

RegARMA models in state space form

Linear regression with AR(2) erroryt = α + βzt + ntnt = φ1nt−1 + φ2nt−2 + et, et ∼ NID(0, σ2)

Combined state space model

yt = [1, zt, 1, 0]xt xt = [α, β, nt, φ2nt−1]′

xt =

1 0 0 00 1 0 00 0 φ1 10 0 φ2 0

ft−1 +

00et0

State space models 3: ARIMA and RegARMA models, and dlm 12

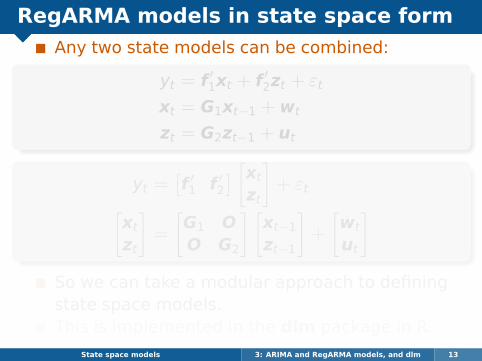

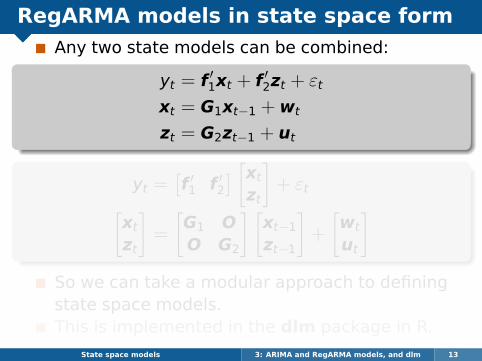

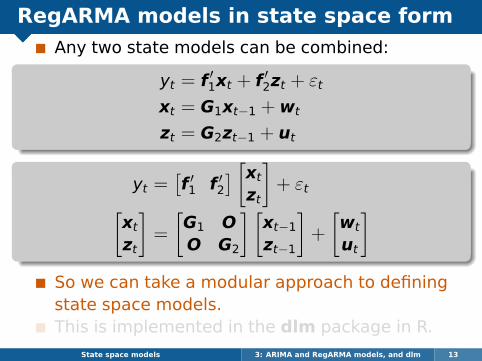

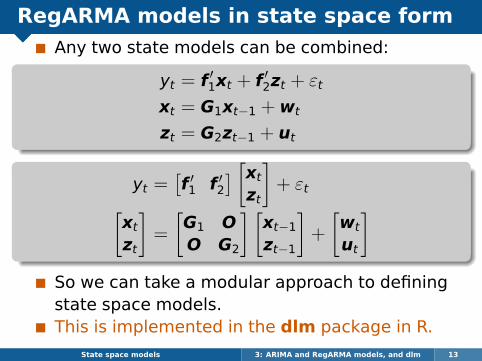

RegARMA models in state space form

Any two state models can be combined:

yt = f ′1xt + f ′2zt + εtxt = G1xt−1 + wt

zt = G2zt−1 + ut

yt =[f ′1 f ′2

] [xt

zt

]+ εt[

xt

zt

]=

[G1 OO G2

] [xt−1

zt−1

]+

[wt

ut

]So we can take a modular approach to definingstate space models.This is implemented in the dlm package in R.

State space models 3: ARIMA and RegARMA models, and dlm 13

RegARMA models in state space form

Any two state models can be combined:

yt = f ′1xt + f ′2zt + εtxt = G1xt−1 + wt

zt = G2zt−1 + ut

yt =[f ′1 f ′2

] [xt

zt

]+ εt[

xt

zt

]=

[G1 OO G2

] [xt−1

zt−1

]+

[wt

ut

]So we can take a modular approach to definingstate space models.This is implemented in the dlm package in R.

State space models 3: ARIMA and RegARMA models, and dlm 13

RegARMA models in state space form

Any two state models can be combined:

yt = f ′1xt + f ′2zt + εtxt = G1xt−1 + wt

zt = G2zt−1 + ut

yt =[f ′1 f ′2

] [xt

zt

]+ εt[

xt

zt

]=

[G1 OO G2

] [xt−1

zt−1

]+

[wt

ut

]So we can take a modular approach to definingstate space models.This is implemented in the dlm package in R.

State space models 3: ARIMA and RegARMA models, and dlm 13

RegARMA models in state space form

Any two state models can be combined:

yt = f ′1xt + f ′2zt + εtxt = G1xt−1 + wt

zt = G2zt−1 + ut

yt =[f ′1 f ′2

] [xt

zt

]+ εt[

xt

zt

]=

[G1 OO G2

] [xt−1

zt−1

]+

[wt

ut

]So we can take a modular approach to definingstate space models.This is implemented in the dlm package in R.

State space models 3: ARIMA and RegARMA models, and dlm 13

RegARMA models in state space form

Any two state models can be combined:

yt = f ′1xt + f ′2zt + εtxt = G1xt−1 + wt

zt = G2zt−1 + ut

yt =[f ′1 f ′2

] [xt

zt

]+ εt[

xt

zt

]=

[G1 OO G2

] [xt−1

zt−1

]+

[wt

ut

]So we can take a modular approach to definingstate space models.This is implemented in the dlm package in R.

State space models 3: ARIMA and RegARMA models, and dlm 13

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 14

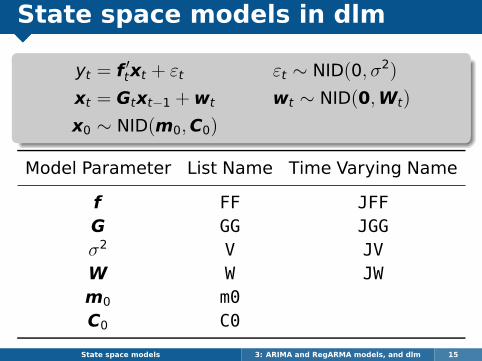

State space models in dlm

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

Model Parameter List Name Time Varying Name

f FF JFFG GG JGGσ2 V JVW W JWm0 m0C0 C0

State space models 3: ARIMA and RegARMA models, and dlm 15

State space models in dlm

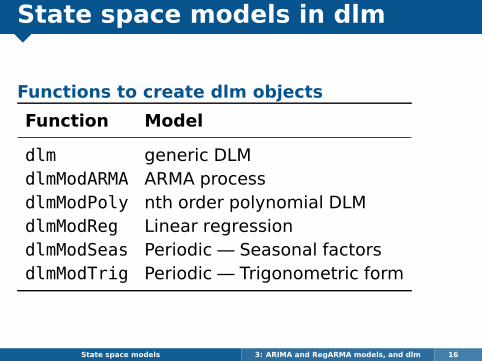

Functions to create dlm objects

Function Model

dlm generic DLMdlmModARMA ARMA processdlmModPoly nth order polynomial DLMdlmModReg Linear regressiondlmModSeas Periodic — Seasonal factorsdlmModTrig Periodic — Trigonometric form

State space models 3: ARIMA and RegARMA models, and dlm 16

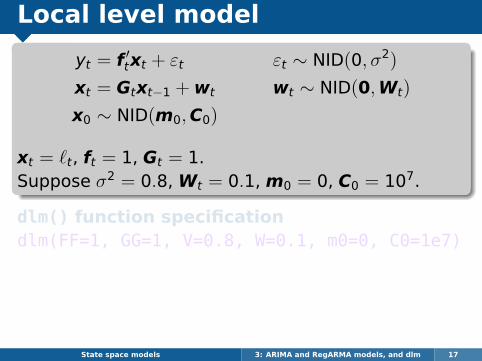

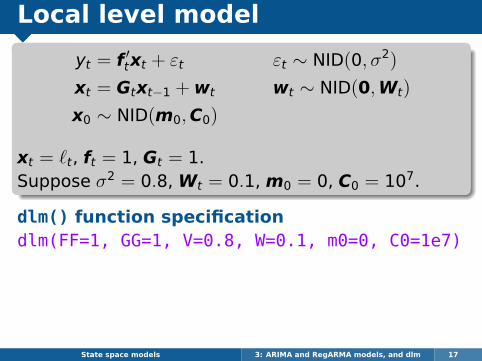

Local level model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt = `t, ft = 1, Gt = 1.Suppose σ2 = 0.8, Wt = 0.1, m0 = 0, C0 = 107.

dlm() function specificationdlm(FF=1, GG=1, V=0.8, W=0.1, m0=0, C0=1e7)

State space models 3: ARIMA and RegARMA models, and dlm 17

Local level model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt = `t, ft = 1, Gt = 1.Suppose σ2 = 0.8, Wt = 0.1, m0 = 0, C0 = 107.

dlm() function specificationdlm(FF=1, GG=1, V=0.8, W=0.1, m0=0, C0=1e7)

State space models 3: ARIMA and RegARMA models, and dlm 17

Local level model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt = `t, ft = 1, Gt = 1.Suppose σ2 = 0.8, Wt = 0.1, m0 = 0, C0 = 107.

dlm() function specificationdlm(FF=1, GG=1, V=0.8, W=0.1, m0=0, C0=1e7)

dlmModPoly() function specification

dlmModPoly(order=1, dV=0.8, dW=0.1)

State space models 3: ARIMA and RegARMA models, and dlm 18

Local level model

> mod <- dlmModPoly(order=1, dV=.8, dW=.1)

> names(mod)

[1] "m0" "C0" "FF" "V" "GG" "W" "JFF" "JV" "JGG" "JW"

> FF(mod)

[,1]

[1,] 1

> GG(mod)

[,1]

[1,] 1

> class(mod)

[1] "dlm"

State space models 3: ARIMA and RegARMA models, and dlm 19

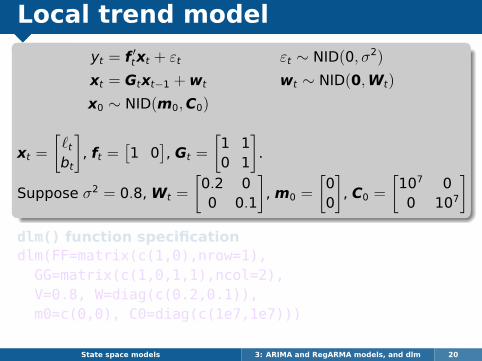

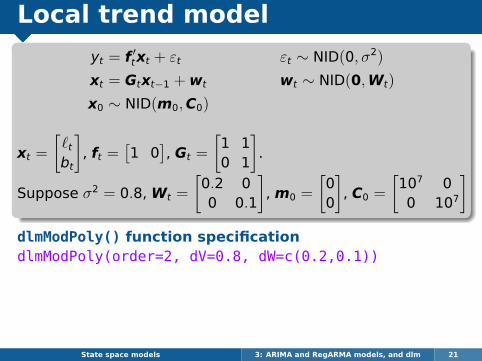

Local trend model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

[`tbt

], ft =

[1 0

], Gt =

[1 10 1

].

Suppose σ2 = 0.8, Wt =

[0.2 00 0.1

], m0 =

[00

], C0 =

[107 00 107

]dlm() function specificationdlm(FF=matrix(c(1,0),nrow=1),GG=matrix(c(1,0,1,1),ncol=2),V=0.8, W=diag(c(0.2,0.1)),m0=c(0,0), C0=diag(c(1e7,1e7)))

State space models 3: ARIMA and RegARMA models, and dlm 20

Local trend model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

[`tbt

], ft =

[1 0

], Gt =

[1 10 1

].

Suppose σ2 = 0.8, Wt =

[0.2 00 0.1

], m0 =

[00

], C0 =

[107 00 107

]dlm() function specificationdlm(FF=matrix(c(1,0),nrow=1),GG=matrix(c(1,0,1,1),ncol=2),V=0.8, W=diag(c(0.2,0.1)),m0=c(0,0), C0=diag(c(1e7,1e7)))

State space models 3: ARIMA and RegARMA models, and dlm 20

Local trend model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

[`tbt

], ft =

[1 0

], Gt =

[1 10 1

].

Suppose σ2 = 0.8, Wt =

[0.2 00 0.1

], m0 =

[00

], C0 =

[107 00 107

]dlmModPoly() function specificationdlmModPoly(order=2, dV=0.8, dW=c(0.2,0.1))

State space models 3: ARIMA and RegARMA models, and dlm 21

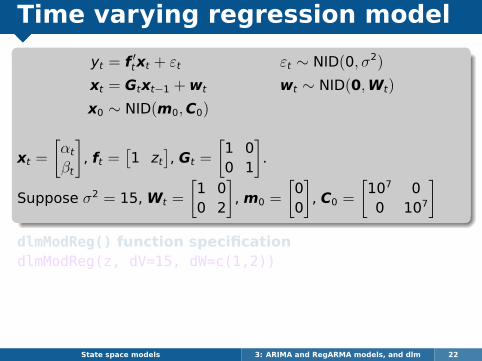

Time varying regression model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

[αt

βt

], ft =

[1 zt

], Gt =

[1 00 1

].

Suppose σ2 = 15, Wt =

[1 00 2

], m0 =

[00

], C0 =

[107 00 107

]dlmModReg() function specificationdlmModReg(z, dV=15, dW=c(1,2))

State space models 3: ARIMA and RegARMA models, and dlm 22

Time varying regression model

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

[αt

βt

], ft =

[1 zt

], Gt =

[1 00 1

].

Suppose σ2 = 15, Wt =

[1 00 2

], m0 =

[00

], C0 =

[107 00 107

]dlmModReg() function specificationdlmModReg(z, dV=15, dW=c(1,2))

State space models 3: ARIMA and RegARMA models, and dlm 22

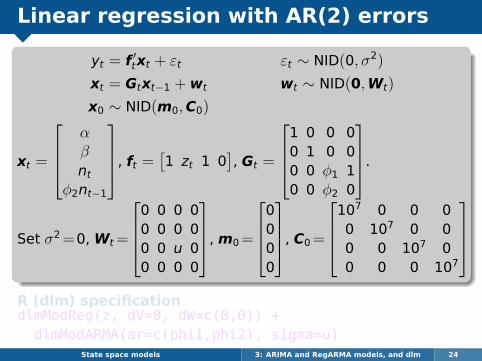

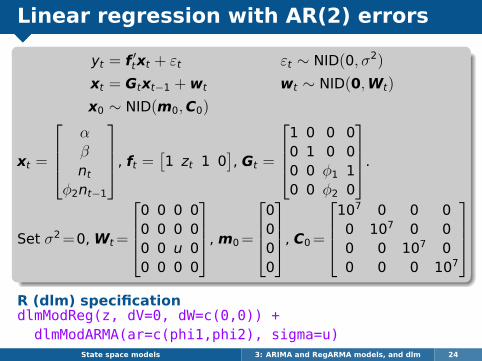

Linear regression with AR(2) errors

yt = α + βzt + ntnt = φ1nt−1 + φ2nt−2 + et, et ∼ NID(0,u)

State space models 3: ARIMA and RegARMA models, and dlm 23

Linear regression with AR(2) errors

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

αβnt

φ2nt−1

, ft =[1 zt 1 0

], Gt =

1 0 0 00 1 0 00 0 φ1 10 0 φ2 0

.

Set σ2=0, Wt=

0 0 0 00 0 0 00 0 u 00 0 0 0

, m0=

0000

, C0=

107 0 0 00 107 0 00 0 107 00 0 0 107

R (dlm) specificationdlmModReg(z, dV=0, dW=c(0,0)) +

dlmModARMA(ar=c(phi1,phi2), sigma=u)State space models 3: ARIMA and RegARMA models, and dlm 24

Linear regression with AR(2) errors

yt = f ′txt + εt εt ∼ NID(0, σ2)

xt = Gtxt−1 + wt wt ∼ NID(0,Wt)

x0 ∼ NID(m0,C0)

xt =

αβnt

φ2nt−1

, ft =[1 zt 1 0

], Gt =

1 0 0 00 1 0 00 0 φ1 10 0 φ2 0

.

Set σ2=0, Wt=

0 0 0 00 0 0 00 0 u 00 0 0 0

, m0=

0000

, C0=

107 0 0 00 107 0 00 0 107 00 0 0 107

R (dlm) specificationdlmModReg(z, dV=0, dW=c(0,0)) +

dlmModARMA(ar=c(phi1,phi2), sigma=u)State space models 3: ARIMA and RegARMA models, and dlm 24

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 25

Local level model estimation

Requirements

A “build” function that takes possibleparameter values and returns the model.

Initial values for the parameters.

Example

loclvl <- function(p) {dlmModPoly(1, dV=exp(p[1]), dW=exp(p[2]))

}

fit <- dlmMLE(oil, parm=c(0,0), build=loclvl)mod <- loclvl(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 26

Local level model estimation

Requirements

A “build” function that takes possibleparameter values and returns the model.

Initial values for the parameters.

Example

loclvl <- function(p) {dlmModPoly(1, dV=exp(p[1]), dW=exp(p[2]))

}

fit <- dlmMLE(oil, parm=c(0,0), build=loclvl)mod <- loclvl(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 26

Local level model estimation

Requirements

A “build” function that takes possibleparameter values and returns the model.

Initial values for the parameters.

Example

loclvl <- function(p) {dlmModPoly(1, dV=exp(p[1]), dW=exp(p[2]))

}

fit <- dlmMLE(oil, parm=c(0,0), build=loclvl)mod <- loclvl(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 26

Local level model estimation

Requirements

A “build” function that takes possibleparameter values and returns the model.

Initial values for the parameters.

Example

loclvl <- function(p) {dlmModPoly(1, dV=exp(p[1]), dW=exp(p[2]))

}

fit <- dlmMLE(oil, parm=c(0,0), build=loclvl)mod <- loclvl(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 26

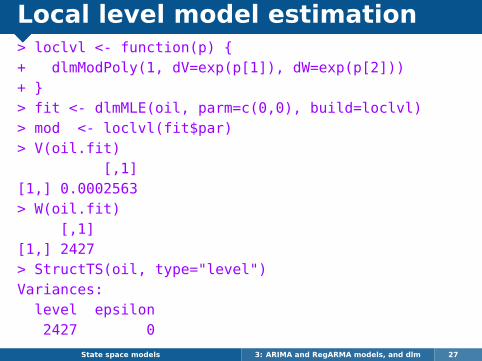

Local level model estimation> loclvl <- function(p) {+ dlmModPoly(1, dV=exp(p[1]), dW=exp(p[2]))+ }> fit <- dlmMLE(oil, parm=c(0,0), build=loclvl)> mod <- loclvl(fit$par)> V(oil.fit)

[,1][1,] 0.0002563> W(oil.fit)

[,1][1,] 2427> StructTS(oil, type="level")Variances:level epsilon2427 0

State space models 3: ARIMA and RegARMA models, and dlm 27

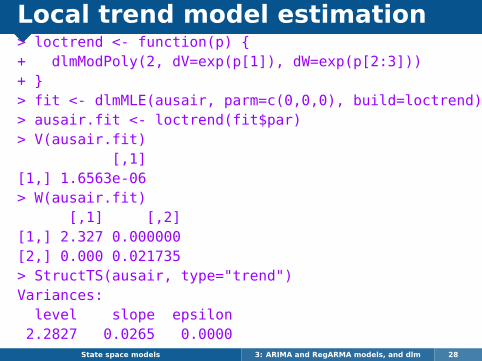

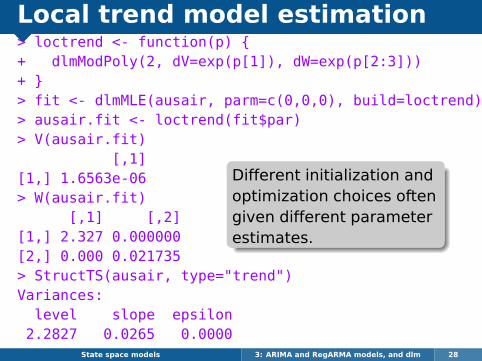

Local trend model estimation> loctrend <- function(p) {+ dlmModPoly(2, dV=exp(p[1]), dW=exp(p[2:3]))+ }> fit <- dlmMLE(ausair, parm=c(0,0,0), build=loctrend)> ausair.fit <- loctrend(fit$par)> V(ausair.fit)

[,1][1,] 1.6563e-06> W(ausair.fit)

[,1] [,2][1,] 2.327 0.000000[2,] 0.000 0.021735> StructTS(ausair, type="trend")Variances:level slope epsilon2.2827 0.0265 0.0000

State space models 3: ARIMA and RegARMA models, and dlm 28

Local trend model estimation> loctrend <- function(p) {+ dlmModPoly(2, dV=exp(p[1]), dW=exp(p[2:3]))+ }> fit <- dlmMLE(ausair, parm=c(0,0,0), build=loctrend)> ausair.fit <- loctrend(fit$par)> V(ausair.fit)

[,1][1,] 1.6563e-06> W(ausair.fit)

[,1] [,2][1,] 2.327 0.000000[2,] 0.000 0.021735> StructTS(ausair, type="trend")Variances:level slope epsilon2.2827 0.0265 0.0000

Different initialization andoptimization choices oftengiven different parameterestimates.

State space models 3: ARIMA and RegARMA models, and dlm 28

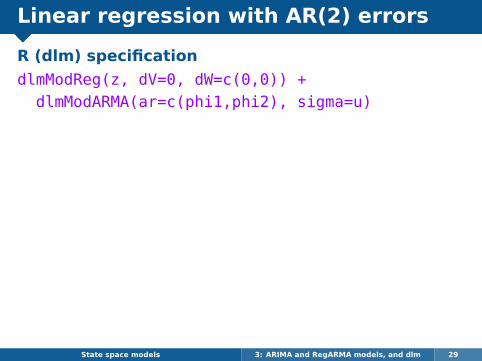

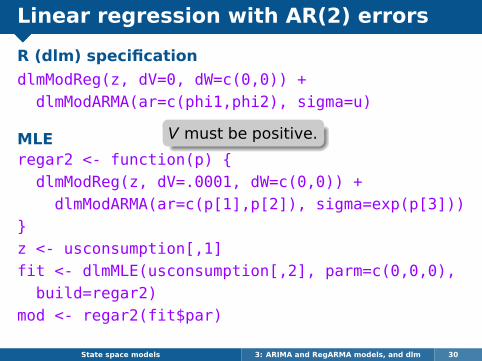

Linear regression with AR(2) errors

R (dlm) specification

dlmModReg(z, dV=0, dW=c(0,0)) +dlmModARMA(ar=c(phi1,phi2), sigma=u)

State space models 3: ARIMA and RegARMA models, and dlm 29

Linear regression with AR(2) errors

R (dlm) specification

dlmModReg(z, dV=0, dW=c(0,0)) +dlmModARMA(ar=c(phi1,phi2), sigma=u)

MLEregar2 <- function(p) {

dlmModReg(z, dV=.0001, dW=c(0,0)) +dlmModARMA(ar=c(p[1],p[2]), sigma=exp(p[3]))

}z <- usconsumption[,1]fit <- dlmMLE(usconsumption[,2], parm=c(0,0,0),

build=regar2)mod <- regar2(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 30

Linear regression with AR(2) errors

R (dlm) specification

dlmModReg(z, dV=0, dW=c(0,0)) +dlmModARMA(ar=c(phi1,phi2), sigma=u)

MLEregar2 <- function(p) {

dlmModReg(z, dV=.0001, dW=c(0,0)) +dlmModARMA(ar=c(p[1],p[2]), sigma=exp(p[3]))

}z <- usconsumption[,1]fit <- dlmMLE(usconsumption[,2], parm=c(0,0,0),

build=regar2)mod <- regar2(fit$par)

V must be positive.

State space models 3: ARIMA and RegARMA models, and dlm 30

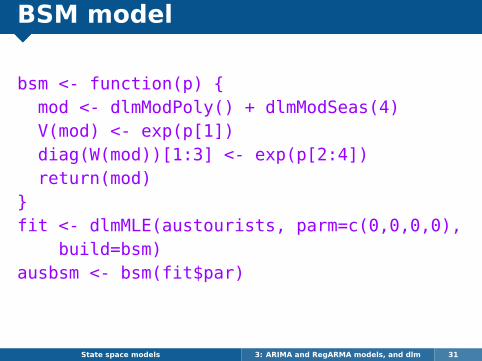

BSM model

bsm <- function(p) {mod <- dlmModPoly() + dlmModSeas(4)V(mod) <- exp(p[1])diag(W(mod))[1:3] <- exp(p[2:4])return(mod)

}fit <- dlmMLE(austourists, parm=c(0,0,0,0),

build=bsm)ausbsm <- bsm(fit$par)

State space models 3: ARIMA and RegARMA models, and dlm 31

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 32

More dlm functions

dlmFilter: Kalman filter. Returns

filtered values of state vectors.

dlmSmooth: Kalman smoother. Returns

smoothed values of state vectors.

dlmForecast: Means and variances of

future observations and states.

State space models 3: ARIMA and RegARMA models, and dlm 33

More dlm functions

dlmFilter: Kalman filter. Returns

filtered values of state vectors.

dlmSmooth: Kalman smoother. Returns

smoothed values of state vectors.

dlmForecast: Means and variances of

future observations and states.

State space models 3: ARIMA and RegARMA models, and dlm 33

More dlm functions

dlmFilter: Kalman filter. Returns

filtered values of state vectors.

dlmSmooth: Kalman smoother. Returns

smoothed values of state vectors.

dlmForecast: Means and variances of

future observations and states.

State space models 3: ARIMA and RegARMA models, and dlm 33

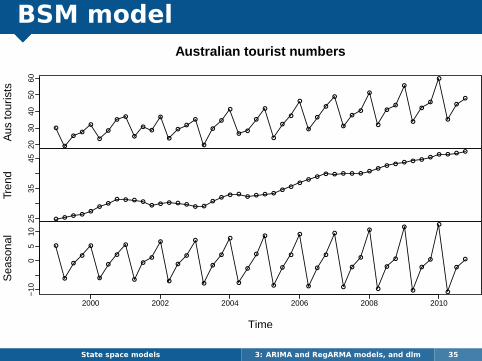

BSM model

Decomposition by Kalman smoothing

ausSmooth <- dlmSmooth(austourists, mod = ausbsm)

x <- cbind(austourists, dropFirst(ausSmooth$s[,c(1,3)]))

colnames(x) <- c("Aus tourists", "Trend", "Seasonal")

plot(x, type = ’o’, main = "Australian tourist numbers")

State space models 3: ARIMA and RegARMA models, and dlm 34

BSM model

●

●

●●

●

●

●

●●

●

●●

●

●

●●

●

●

●

●

●

●●

●

●

●

●

●

●

●

●

●

●

●

●●

●

●

●●

●

●

●

●

●

●

●

●

2030

4050

60

Aus

tour

ists

● ● ● ●●

●●

● ● ● ●● ● ● ● ● ● ●

●●

● ●● ● ● ●

●●

●●

●● ● ● ● ● ●

●● ● ● ● ●

●● ● ● ●

2535

45

Tren

d

●

●

●

●

●

●

●

●

●

●

●●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

−10

05

10

2000 2002 2004 2006 2008 2010

Sea

sona

l

Time

Australian tourist numbers

State space models 3: ARIMA and RegARMA models, and dlm 35

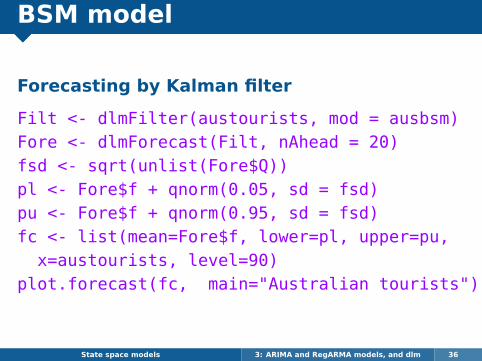

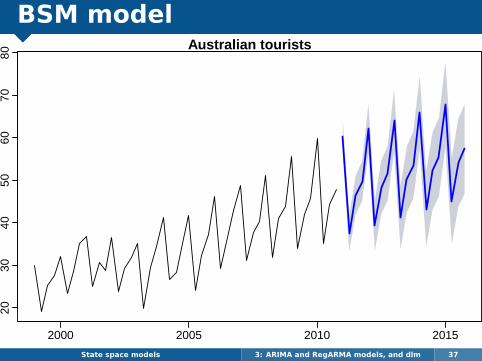

BSM model

Forecasting by Kalman filter

Filt <- dlmFilter(austourists, mod = ausbsm)Fore <- dlmForecast(Filt, nAhead = 20)fsd <- sqrt(unlist(Fore$Q))pl <- Fore$f + qnorm(0.05, sd = fsd)pu <- Fore$f + qnorm(0.95, sd = fsd)fc <- list(mean=Fore$f, lower=pl, upper=pu,

x=austourists, level=90)plot.forecast(fc, main="Australian tourists")

State space models 3: ARIMA and RegARMA models, and dlm 36

BSM modelAustralian tourists

2000 2005 2010 2015

2030

4050

6070

80

State space models 3: ARIMA and RegARMA models, and dlm 37

Outline

1 ARIMA models in state space form

2 RegARMA models in state space form

3 The dlm package for R

4 MLE using the dlm package

5 Filtering, smoothing and forecasting usingthe dlm package

6 Final remarks

State space models 3: ARIMA and RegARMA models, and dlm 38

Final remarks

State space models come in lots of flavours. Wehave only touched the surface.

We haven’t even mentioned the Bayesianflavours.

State space models are a flexible way ofhandling lots of time series models and providea framework for handling missing values,likelihood estimation, smoothing, forecasting,etc.

State space models 3: ARIMA and RegARMA models, and dlm 39

Final remarks

State space models come in lots of flavours. Wehave only touched the surface.

We haven’t even mentioned the Bayesianflavours.

State space models are a flexible way ofhandling lots of time series models and providea framework for handling missing values,likelihood estimation, smoothing, forecasting,etc.

State space models 3: ARIMA and RegARMA models, and dlm 39

Final remarks

State space models come in lots of flavours. Wehave only touched the surface.

We haven’t even mentioned the Bayesianflavours.

State space models are a flexible way ofhandling lots of time series models and providea framework for handling missing values,likelihood estimation, smoothing, forecasting,etc.

State space models 3: ARIMA and RegARMA models, and dlm 39

Recommended References

1 RJ Hyndman, AB Koehler, J Keith Ord, andRD Snyder (2008). Forecasting withexponential smoothing: the state spaceapproach. Springer

2 AC Harvey (1989). Forecasting, structuraltime series models and the Kalman filter.Cambridge University Press

3 J Durbin and SJ Koopman (2001). Time seriesanalysis by state space methods. OxfordUniversity Press

4 G Petris, S Petrone, and P Campagnoli (2009).Dynamic Linear Models with R. Springer

State space models 3: ARIMA and RegARMA models, and dlm 40

Contact details

www.robjhyndman.com

State space models 3: ARIMA and RegARMA models, and dlm 41