State of the Employment Nation

20

Jobs Australia 2011 National Conference KEYNOTE SPEECH: STATE OF THE EMPLOYMENT NATION Matthew Tukaki, CEO The Sustain Group

Transcript of State of the Employment Nation

Jobs Australia 2011 National Conference

KEYNOTE SPEECH: STATE OF THE EMPLOYMENT

NATION

Matthew Tukaki, CEO

The Sustain Group

www.sustaingroup.net

www.sustaingroup.net

- What’s happening in the corporate recruitment

sector?

- What’s happening in the JSA sector?

- Industries rising and industries falling: where

are the jobs at?

- The issue of underemployment

- The challenges of long term unemployment

- The role of innovation in unemployment

- The next 24 months

Themes…

www.sustaingroup.net

www.sustaingroup.net

About Matthew Tukaki

Matthew is currently the CEO of the Sustain Group, a Sydney based corporation with a primary focus on

business transformation, education development and employment. Prior to joining the Sustain Group,

Matthew was the Head of Drake Australia. As one of Australia’s best known corporate brands, Matthew led

the business through the heights of the Global Financial Crisis where he was responsible for maintaining

growth and profitability.

Matthew Tukaki is the current Australian Representative to the United Nations Global Compact and

represents business and industry when it comes to Human Rights, the Environment, Anti-Corruption and

Labour. Matthew was elected as the Local Network Representative at the Inaugural Annual Meeting of the

Global Compact Network Australia on 4 June 2010. Since this time Matthew has at the invitation of the

board of directors of the Global Compact Network Australia attended the meetings of directors and has

actively led planning activities for the Australian Network. He is also a member of the Global Working Group

on Governance. Matthew is also the Public Officer of the UNGCNA and its Company Secretary.

Matthew is a current Director on the Board of Suicide Prevention Australia (one of Australia’s Peak Mental

Health Bodies), Chairman of the Living Earth Initiative, (a project seeking to increase the visibility of

backyard ecology in Australian homes) and former Chairman of both the Chief Information Officers Council

and the Government Policy Advisory Panel.

www.sustaingroup.net

www.sustaingroup.net

About Sustain Group

The Sustain Group is a business that strives to work with other industry, Government and the community to

transform towards a more sustainable future. As an organisation we recognise that climate change, the

environment and corporate social investment can confuse people when it comes to translating a desire to

change to real outcomes and outputs.

At The Sustain Group we provide a range of services and programs from sustainability recruitment and

learning, through to consulting and research. On the technology front, we work to provide products that are

innovative and forward thinking. Our primary goal is to provide our clients with tangible outcomes, not just

advice. Our consulting division works in partnership with some of the worlds most respected institutions on

everything from the calculation of an organisations carbon output, through to research and development.

www.sustaingroup.net

www.sustaingroup.net

Wh

at’s h

ap

pe

nin

g in

the

co

rpo

rate

recru

itm

ent secto

r

Margins are falling

Competition is at its height

Undercutting of margins and contract fees

Too many players in the marketplace for the

population – the jobs market is overcrowded

Have higher turnover and lower average retention

rates

Recruiters moving from business to business

Recruitment companies beginning to diversify

their business models

Increasing competition

from JSA and not-for

profit organisations…

www.sustaingroup.net

www.sustaingroup.net

Wh

at’s h

ap

pe

nin

g in

the

JS

A s

ecto

r

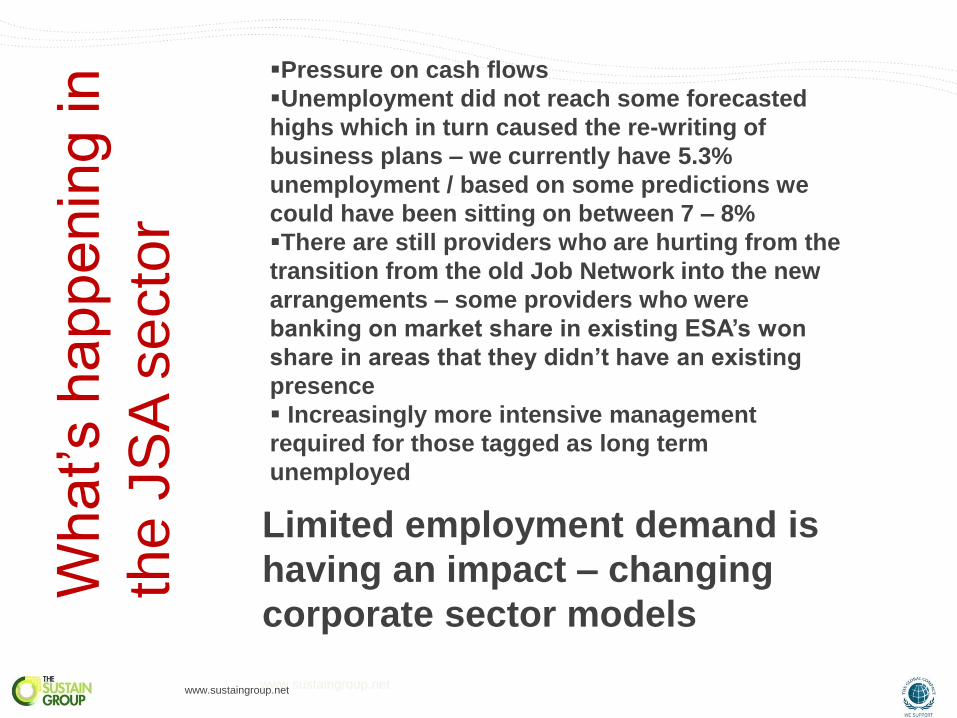

Pressure on cash flows

Unemployment did not reach some forecasted

highs which in turn caused the re-writing of

business plans – we currently have 5.3%

unemployment / based on some predictions we

could have been sitting on between 7 – 8%

There are still providers who are hurting from the

transition from the old Job Network into the new

arrangements – some providers who were

banking on market share in existing ESA’s won

share in areas that they didn’t have an existing

presence

Increasingly more intensive management

required for those tagged as long term

unemployed

Limited employment demand is

having an impact – changing

corporate sector models

www.sustaingroup.net

www.sustaingroup.net

Sa

me

ch

alle

ng

es a

cro

ss

the

fo

r p

rofit

an

d n

ot

for

pro

fit se

cto

rs

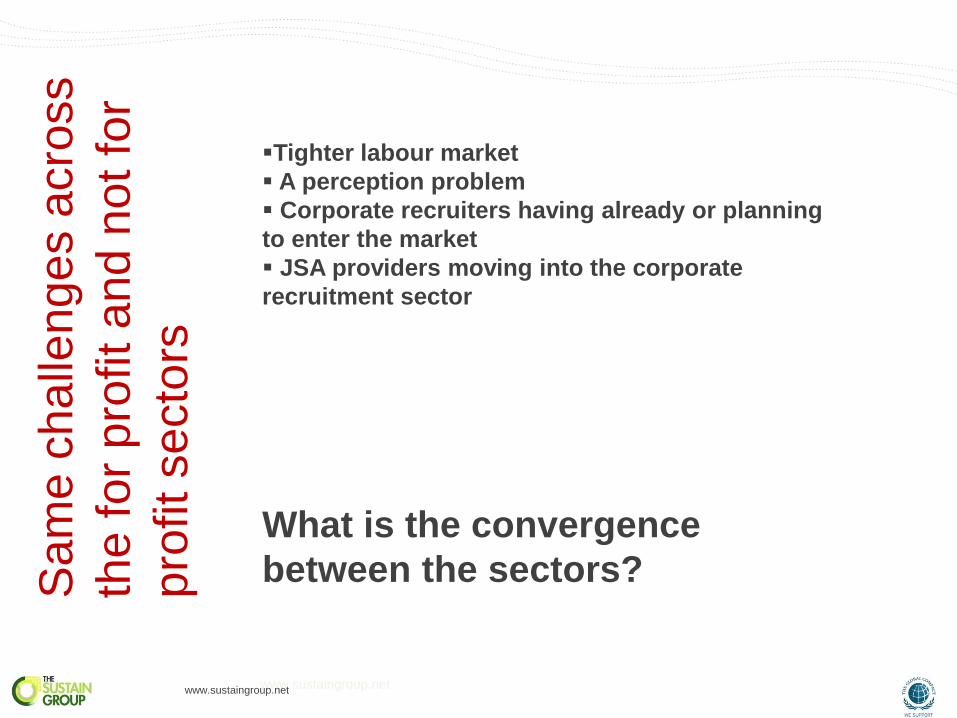

Tighter labour market

A perception problem

Corporate recruiters having already or planning

to enter the market

JSA providers moving into the corporate

recruitment sector

What is the convergence

between the sectors?

www.sustaingroup.net

www.sustaingroup.net

lets take a look at where the jobs are at:

Irrespective of what people say, there are those sectors that are

rising and those that are falling

There are no skill shortages in the IT sector in Australia and it

is a falsehood to suggest there are – if there were then we would

no longer have the same size of taxi fleets in Sydney and

Melbourne

There is also a false premise that job creation is happening in

our capital cities – there is more job creation opportunities in

the regions than there are in some of our capitals

Next slide: lets take a look at just what industries are creating

and will create jobs, and some of the locations where there are

immense numbers of opportunities….

www.sustaingroup.net

www.sustaingroup.net

Disa

bilit

y ser

vices

Environment

Primary production

Ho

sp

itali

ty

Banking & finance

Renewables

Nurses

Carbon Auditing

Training

Aged c

are

serv

ice

Mining & resources

Trades & vocations

Rail

Compliance

Infr

astr

uct

ure

OH&S

Health services

Climate change

Development

Logistics

CSG

Sm

all b

usin

es

s (2

01

2)

Utilities

Hortic

ultu

re

Construction

Social Media

Security

Ne

w m

ed

ia

Energy Agriculture and horticulture

Public policy

Northern

Territory

North Queensland

The Bowen Basin G

lad

sto

ne

W.A

Darwin

Galilee

Where the jobs are in Australia

www.sustaingroup.net

www.sustaingroup.net

Lets take a close look at an industry on the

rise and what we mean by the jobs supply

channel, both directly and indirectly….

Example: BHP and the recently announced Olympic Dam

project: what will it mean in terms of jobs?

Example: Agriculture and horticulture

www.sustaingroup.net

www.sustaingroup.net

Min

ing

Mining and commodities

Labour Hire

Consulting

Project Managers

Training

Professional Services

OH&S Retail

Research Building

Sustainability Airlines

Finance Hospitality

Management

Project Management

Trades

Engineers

Admin

Catering

1. Direct Job

Creation

2. Indirect Job

creation

3. Indirect

Channel Job

Creation

+10,000 Direct Jobs

@ Olympic Dam

1. Direct job: created by the

employer

2. Indirect Job: created in the

supply chain of the employer

3. Indirect Channel Job

Creation: services providers

to both the indirect and direct

channels

Example: 2,000 people FIFO

once per month return = 24,000

seats is nearly 112 flights in and

out – 2 pilots, ground crew and

cabin crew – admin and booking

staff

Example: Project

managers will be

needed on the ground

to directly manage the

infrastructure build,

trades to build it and

maintain it, admin to

pay the wags, caterers

on the ground to feed

them and

management to

administer –

compliance and risk

managers to ensure

environmental risk Example: Increase in the number of

environmental and policy makers required to

ensure compliance

www.sustaingroup.net

www.sustaingroup.net

Lets take a close look at an industry on the

slide and consider what needs to be done to

grow and develop, innovate and create….

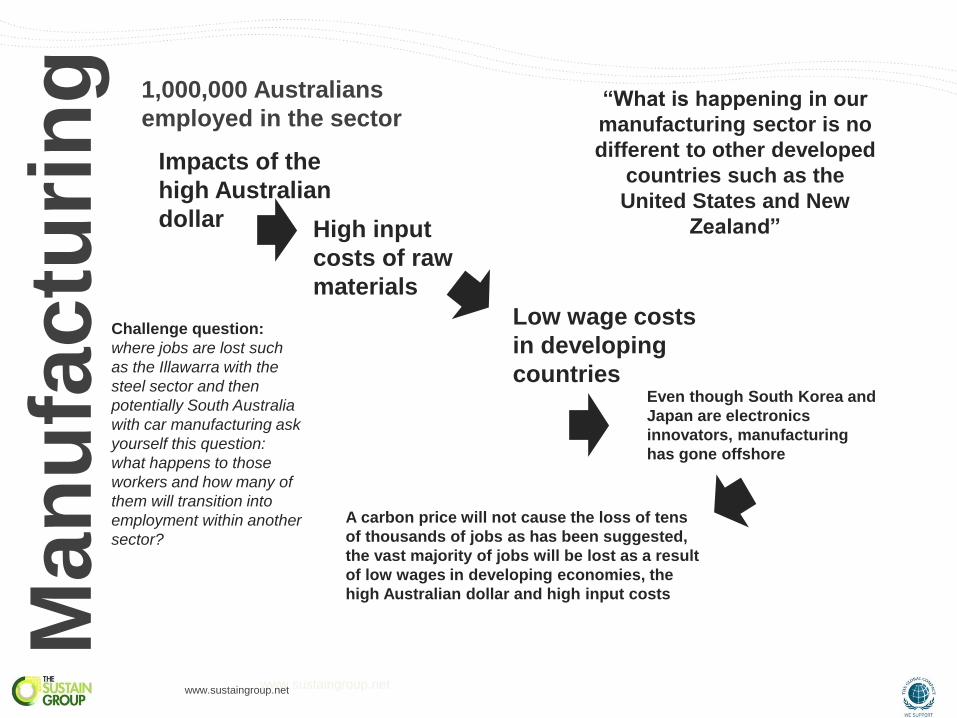

Example: Manufacturing

1. A traditional backbone of the Australian economy that employs more than a million

Australians

2. Under pressure from outside forces such as a high Australian dollar an input cost

Example: Retail

1. Under pressure from new sales channels such as online retail and trade

2. Like manufacturing under pressure from outside forces such as a high Australian dollar

an input cost

www.sustaingroup.net

www.sustaingroup.net

Man

ufa

ctu

rin

g

Impacts of the

high Australian

dollar

Low wage costs

in developing

countries

High input

costs of raw

materials

1,000,000 Australians

employed in the sector “What is happening in our

manufacturing sector is no

different to other developed

countries such as the

United States and New

Zealand”

Even though South Korea and

Japan are electronics

innovators, manufacturing

has gone offshore

Challenge question:

where jobs are lost such

as the Illawarra with the

steel sector and then

potentially South Australia

with car manufacturing ask

yourself this question:

what happens to those

workers and how many of

them will transition into

employment within another

sector?

A carbon price will not cause the loss of tens

of thousands of jobs as has been suggested,

the vast majority of jobs will be lost as a result

of low wages in developing economies, the

high Australian dollar and high input costs

www.sustaingroup.net

www.sustaingroup.net

Business models in the retail sector need to

evolve and so look towards where the jobs

are being created: online retail and trade…

Brick and mortar is expensive, less jobs

because of high input costs

Who are

we?

The way people are buying

is changing

We live our lives

increasingly online and it is

making more sense to buy

online

Cheaper to buy online

because of the exchange

rate and the removal of the

middle man

The devices we use are

leading us online

Re

tail a

nd

sh

op

fr

on

ts

Traditional ways of

selling from brick and

mortar operations are

changing …

More and more often

we are moving online

Online buying is creating jobs in

warehousing and distribution /

traditional jobs are changing /

Australia Post has experienced a

significant increase in parcel deliveries

while experiencing a decline in

traditional letter sending revenue lines

www.sustaingroup.net

www.sustaingroup.net

What does this mean for the JSA and

employment sector?

Just as industries are evolving and developing, declining or

contracting, the business models of organisations who provide

them with labour supply, training or employment services also

needs to change. The reality is, when you are in the employment

supply chain you are as equally challenged by supply and

demand as any business or industry sector….

…people also have to be aware of where the

jobs are being created and will be created

tomorrow…for example: lets take a look at

where more future jobs are being created…

www.sustaingroup.net

www.sustaingroup.net

The Aged Care sector

Population shifts from our

major capital cities and into

coastal regions such as the

Gold Coast and the Central

Coast of New South Wales

Aging population means

an increase in demand for

workers in the sectors that

support aging communities

Additional ancillary

health workers / nurses /

aged care facility workers /

administrators / social

workers / community care

workers / rest home

managers / funeral services

QLD: The Gold Coast NSW: The Central Coast

www.sustaingroup.net

www.sustaingroup.net

The challenges of underemployment / the

silent problem of the Australian employment

market

While the unemployment rate will remain steady and decline further

in the lead up to the last quarter of 2012 – the reality is tens of

thousands of Australian’s remain underemployed.

Our workforce is heavily casualised and part time in nature

More workers remain on less than they earned prior to the GFC

Cost of living pressures

Workers who don’t qualify for any support

Pressure on employment providers by people who are not funded to

seek or utilise the service

Lets take a look at an example: the Nerang Community Centre

in Brisbane and its coordinator Vicky Va’a

www.sustaingroup.net

www.sustaingroup.net

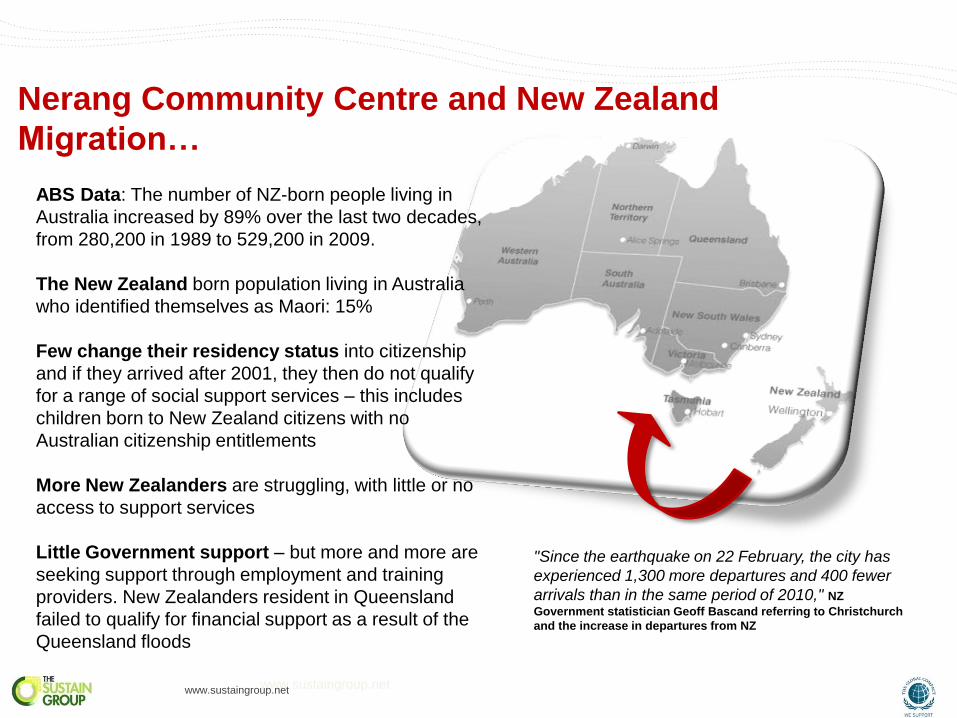

Nerang Community Centre and New Zealand

Migration…

ABS Data: The number of NZ-born people living in

Australia increased by 89% over the last two decades,

from 280,200 in 1989 to 529,200 in 2009.

The New Zealand born population living in Australia

who identified themselves as Maori: 15%

Few change their residency status into citizenship

and if they arrived after 2001, they then do not qualify

for a range of social support services – this includes

children born to New Zealand citizens with no

Australian citizenship entitlements

More New Zealanders are struggling, with little or no

access to support services

Little Government support – but more and more are

seeking support through employment and training

providers. New Zealanders resident in Queensland

failed to qualify for financial support as a result of the

Queensland floods

"Since the earthquake on 22 February, the city has

experienced 1,300 more departures and 400 fewer

arrivals than in the same period of 2010," NZ

Government statistician Geoff Bascand referring to Christchurch

and the increase in departures from NZ

www.sustaingroup.net

www.sustaingroup.net

Carb

on Pr

icing

Bra

nd

ing

Cash flow

Increased compliance

Hig

h w

ag

e d

em

an

d

Global Economy

US Job Numbers

Greece US Unemployment

Th

e P

rice o

f Ir

on O

re

The Chinese Economy G

illard

’s p

ollin

g

Staff well being

Sa

les p

erf

orm

an

ce

Skills demand

To grow or not to grow

Interest rates

Inflation

Ta

x

Cost controls

Bu

yer

beh

avio

ur

The Board

Governance

Japans

recovery

Demographics

Executive loss

Climate change

Corruption

Competitors

Partners

Suppliers

The Banks

Early election

Co

alit

ion

po

licie

s

Reve

nu

e d

ive

rsity

Payroll tax

Pro

du

ctiv

ity

Leadership

YouTube

Social Media

Trade Barriers

Tw

itte

r

Invoicing

IT Systems

Budget

Blow outs

Security Public

Rela

tions

Mark

et s

hare

Death

Court

Rulings

Customer Attrition and Gain

Political Environment

www.sustaingroup.net

www.sustaingroup.net

Matthew Tukaki

www.sustaingroup.net

www.unglobalcompact.org.au

Thank you