Standard Financial Statements (“DFP”) -...

119

Standard Financial Statements (“DFP”) CESP - Companhia Energética de São Paulo December 31, 2016

Transcript of Standard Financial Statements (“DFP”) -...

Standard Financial Statements (“DFP”)

CESP - Companhia Energética de São Paulo December 31, 2016

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Contents Company Information

Capital ownership structure ................................................................................................................................1 Cash Dividends and Interest on Equity ...............................................................................................................2 Individual Financial Statements

Statement of Financial Position - Assets.............................................................................................................3 Statement of Financial Position - Liabilities .........................................................................................................5 Statement of operations .....................................................................................................................................7 Statement of comprehensive income (loss) ........................................................................................................8 Cash Flow Statement - Indirect Method ..............................................................................................................9 Statements of Changes in Equity

SCE - 1/1/2016 to 12/31/2016 .......................................................................................................................... 10 SCE - 1/1/2015 to 12/31/2015 .......................................................................................................................... 11 SCE - 1/1/2014 to 12/31/2014 .......................................................................................................................... 12 Statement of Value Added ............................................................................................................................... 13 Management Report ........................................................................................................................................ 15 Notes ............................................................................................................................................................... 33 Other Information that the Company Considers to be Material ........................................................................ 104 Reports and Representations Independent Auditor’s Report - Unqualified .................................................................................................... 106 Opinion by the Supervisory Board or Equivalent Body .................................................................................... 112 Officers’ Representation on the Financial Statements ..................................................................................... 113 Officers’ representation on the Independent Auditor’s Report ......................................................................... 114

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 1 of 114

Company Information / Capital ownership structure Number of shares Last fiscal year (thousand) 12/31/2016

Paid-in Capital Common shares 109,168 Preferred shares 218,335 Total 327,503 Treasury shares Common shares 0 Preferred shares 0 Total 0

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 2 of 114

Company information / Cash Dividends and Interest on Equity

Event Approval Proceeds First payment Type of share Class of share Earnings per share

(Reais / Share)

Annual General Meeting 04/26/2016

Dividend 06/30/2016

Common shares 0,08670

Annual General Meeting 04/26/2016

Dividend 06/30/2016

Preferred shares Class A preferred

shares 1,82454

Annual General Meeting 04/26/2016

Dividend 06/30/2016

Preferred shares Class B preferred

shares 0,08670

Board of Directors’ Meeting. 11/08/2016

Interest on equity 12/30/2016

Common shares 0,39518

Board of Directors’ Meeting. 11/08/2016

Interest on equity 12/30/2016

Preferred shares Class A preferred

shares 1,82454

Board of Directors’ 11/08/2016

Interest on equity 12/30/2016

Preferred shares Class B preferred

shares 0,39518

Meeting

Annual General Meeting 04/26/2017

Dividend 06/30/2017

Common shares 0,48370

Annual and Special 04/26/2017

Dividend 06/30/2017

Preferred shares Class B preferred

shares 0,48370

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 3 of 114

Individual Financial Statements / Statement of Financial Position - Assets

(In thousands of reais) Account code Account description

Last Year Year before last Second year before last 12/31/2016 12/31/2015 12/31/2014

1 Total assets 11,416,449 11,986,763 14,687,886 1.01 Current assets 833,534 994,148 2,948,585 1.01.01 Cash and cash equivalents 1,477 3,558 5,796 1.01.02 Short-term investments 502,552 544,995 2,422,056 1.01.02.01 Short-term investments measured at fair value 502,552 544,995 2,422,056 1.01.02.01.01 Securities held for trading 502,552 544,995 2,422,056 1.01.03 Accounts receivable 165,141 339,567 385,175 1.01.03.01 Trade accounts receivable 165,141 339,567 385,175

1.01.03.01.01 Consumers and resellers / Extraordinary Tariff Adjustment (RTE) and Electric Energy Trade Chamber (CCEE) 165,141 339,567 423,061

1.01.03.01.02 Allowance for doubtful accounts 0 0 (37,886) 1.01.04 Inventories 0 0 34,788 1.01.07 Prepaid expenses 16,086 25,166 6,194 1.01.08 Other current assets 148,278 80,862 94,576 1.01.08.03 Other 148,278 80,862 94,576 1.01.08.03.01 Taxes and contributions to be offset 77,702 4,236 4,473 1.01.08.03.04 Other 70,576 76,626 90,103 1.02 Noncurrent assets 10,582,915 10,992,615 11,739,301 1.02.01 Long-term receivables 3,562,803 3,691,964 3,235,140 1.02.01.03 Accounts receivable 1,885 3,204 4,730 1.02.01.03.01 Trade accounts receivable 1,885 3,204 4,730 1.02.01.04 Inventories 6,977 28,467 0 1.02.01.06 Deferred taxes 799,535 869,431 734,686 1.02.01.06.01 Deferred income and social contribution taxes 799,535 869,431 734,686 1.02.01.07 Prepaid expenses 37,554 52,575 4,807 1.02.01.09 Other noncurrent assets 2,716,852 2,738,287 2,490,917 1.02.01.09.03 Pledges and restricted deposits 767,422 788,857 773,555 1.02.01.09.04 Asset available for reversal 6,337,256 6,337,256 3,529,080 1.02.01.09.05 Provision for contingent asset - Hydro Power Plant (HPP) (4,387,826) (4,387,826) (1,811,718) 1.02.03 Property, plant and equipment 6,979,724 7,260,107 8,494,806

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 4 of 114

Individual Financial Statements / Statement of Financial Position - Assets

(In thousands of reais) Account code Account description

Last year Year before last Second year before last

12/31/2016 12/31/2015 12/31/2014

1.02.03.01 Property, plant and equipment in use 6,979,724 7,260,107 8,494,806 1.02.04 Intangible assets 40,388 40,544 9,355 1.02.04.01 Intangible assets 40,388 40,544 9,355 1.02.04.01.01 Service concession arrangement 40,388 40,544 9,355

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 5 of 114

Individual Financial Statements / Statement of Financial Position - Liabilities

(In thousands of reais) Account

Account description

Last year Year before last Second year before last

code 12/31/2016 12/31/2015 12/31/2014

2 Total liabilities 11,416,449 11,986,763 14,687,886 2.01 Current liabilities 852,390 998,224 2,202,432 2.01.02 Trade accounts payable 10,546 13,925 16,853 2.01.02.01 Trade accounts payable - local 10,546 13,925 16,853 2.01.03 Tax obligations 21,074 56,586 50,030 2.01.03.01 Federal tax liabilities 21,074 56,586 50,030 2.01.03.01.02 Taxes and social contributions 21,074 56,586 50,030 2.01.04 Loans and financing 186,817 206,736 1,149,797 2.01.04.01 Loans and financing 186,817 206,736 1,149,797 2.01.04.01.01 In local currency 5,157 5,158 1,022,827 2.01.04.01.02 In foreign currency 181,660 201,578 126,970 2.01.05 Other liabilities 633,953 720,977 985,752 2.01.05.02 Other 633,953 720,977 985,752 2.01.05.02.01 Dividends and interest on equity payable 156,167 42,463 405,385 2.01.05.02.05 Sector-related charges 229,831 393,642 115,413 2.01.05.02.06 Estimated obligations and Payroll 19,588 31,242 30,194 2.01.05.02.08 Credit assignment investment funds - FIDC 83,151 237,618 290,626 2.01.05.02.09 Other liabilities 145,216 16,012 144,134 2.02 Noncurrent liabilities 3,402,522 3,677,647 3,856,377 2.02.01 Loans and financing 381,577 675,973 605,267 2.02.01.01 Loans and financing 381,577 675,973 605,267 2.02.01.01.01 In local currency 9,904 15,056 20,208 2.02.01.01.02 In foreign currency 371,673 660,917 585,059 2.02.02 Other liabilities 3,020,945 3,001,674 3,251,110 2.02.02.02 Other 3,020,945 3,001,674 3,251,110 2.02.02.02.03 Credit assignment investment funds - FIDC 0 71,704 268,716 2.02.02.02.04 Employee pension entity 0 0 131,891 2.02.02.02.05 Sector-related charges 11,192 20,658 70,969 2.02.02.02.06 Provision for contingencies 2,874,295 2,790,081 2,660,866

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 6 of 114

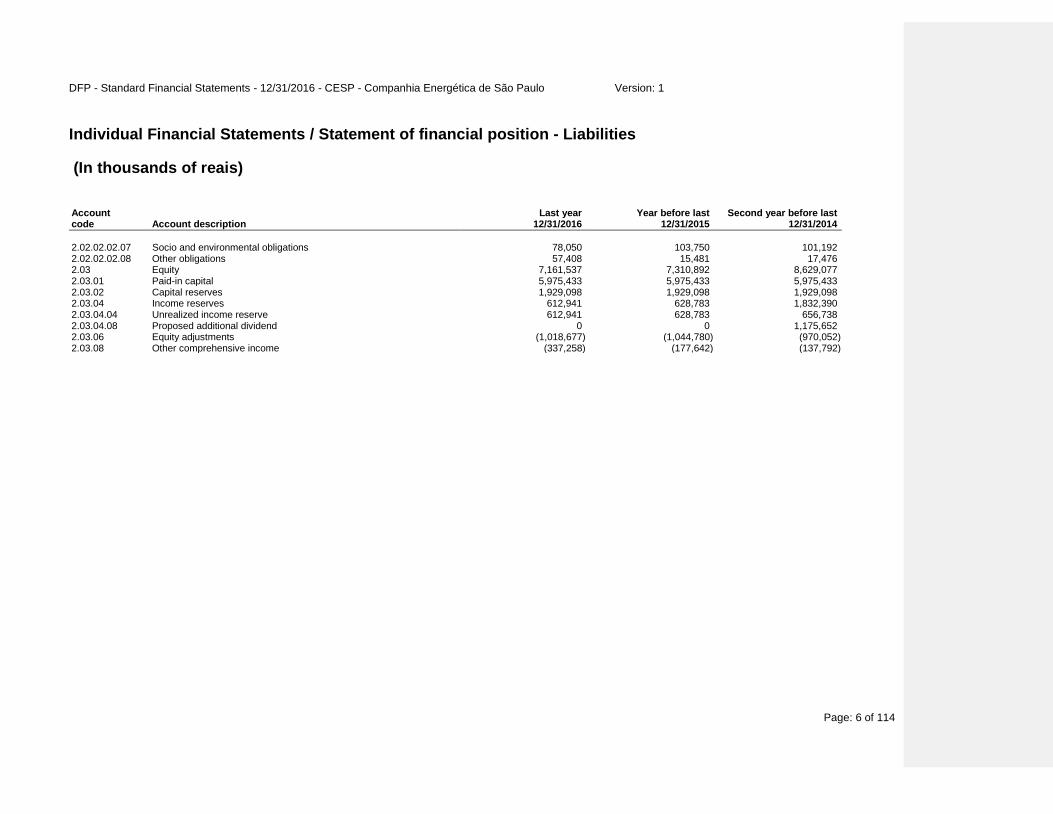

Individual Financial Statements / Statement of financial position - Liabilities

(In thousands of reais) Account

Account description Last year Year before last Second year before last

code 12/31/2016 12/31/2015 12/31/2014

2.02.02.02.07 Socio and environmental obligations 78,050 103,750 101,192 2.02.02.02.08 Other obligations 57,408 15,481 17,476 2.03 Equity 7,161,537 7,310,892 8,629,077 2.03.01 Paid-in capital 5,975,433 5,975,433 5,975,433 2.03.02 Capital reserves 1,929,098 1,929,098 1,929,098 2.03.04 Income reserves 612,941 628,783 1,832,390 2.03.04.04 Unrealized income reserve 612,941 628,783 656,738 2.03.04.08 Proposed additional dividend 0 0 1,175,652 2.03.06 Equity adjustments (1,018,677) (1,044,780) (970,052) 2.03.08 Other comprehensive income (337,258) (177,642) (137,792)

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 7 of 114

Individual Financial Statements / Statement of Operations

(In thousands of reais) Account

Account description

Last year Year before last Second year before last

code 1/1/2016 to 12/31/2016 1/1/2015 to 12/31/2015 1/1/2014 to 12/31/2014

3.01 Revenue from sales and/or services 1,668,590 2,950,982 4,856,023 3.02 Cost of sales and/or services (785,040) (1,420,607) (1,270,282) 3.03 Gross profit 883,550 1,530,375 3,585,741 3.04 Operating expenses/income (601,322) (1,080,874) (2,570,927) 3.04.02 General and administrative expenses (196,175) (214,657) (226,826) 3.04.04 Other operating income (90,566) (633,912) (2,139,257) 3.04.05 Other operating expenses (314,581) (232,305) (204,844) 3.05 Income before financial income and taxes 282,228 449,501 1,014,814 3.06 Financial income (expenses) 135,203 (358,693) (132,284) 3.06.01 Financial income 101,147 165,008 259,014 3.06.02 Financial expenses 34,056 (523,701) (391,298) 3.07 Income (loss) before income taxes 417,431 90,808 882,530 3.08 Income and social contribution taxes (112,336) (152,165) (322,391) 3.08.01 Current (42,440) (286,910) (759,503) 3.08.02 Deferred (69,896) 134,745 437,112 3.09 Net income (loss) from continuing operations 305,095 (61,357) 560,139 3.11 Income/loss for the period 305,095 (61,357) 560,139 3.99 Earnings per share (Reais/share)

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 8 of 114

Individual Financial Statements / Statement of Comprehensive Income (Loss)

(In thousands of reais) Account

Account description Last year Year before last Second year before last

code 1/1/2016 to 12/31/2016 1/1/2015 to 12/31/2015 1/1/2014 to 12/31/2014 4.01 Net income for the period 305,095 (61,357) 560,139 4.02 Other comprehensive income (loss) (159,616) (39,850) (204,371) 4.02.01 Adjustment - CPC 33/IAS 19 (159,616) (39,850) (204,371) 4.03 Comprehensive income (loss) for the period 145,479 (101,207) 355,768

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 9 of 114

Individual Financial Statements / Cash Flow Statement - Indirect Method (In thousands of reais) Account

Account description

Last year Year before last Second year before last

code 1/1/2016 to 12/31/2016 1/1/2015 to 12/31/2015 1/1/2014 to 12/31/2014

6.01 Net cash from operating activities 585,229 1,230,286 3,117,870 6.01.01 Cash from operating activities 1,058,651 1,744,556 4,219,255 6.01.01.01 Income before income and social contribution taxes 417,431 90,808 882,530 6.01.01.02 Depreciation 303,545 460,380 642,499 6.01.01.03 Interest and monetary and exchange gains (losses) (45,683) 449,115 360,128 6.01.01.04 Divestiture / disposal of PPE 1,075 617 353 6.01.01.05 Provision for contingent asset - HPP Três Irmãos 0 580,798 0 6.01.01.06 Employee pension entity - CPC 33/ IAS19 7,786 8,938 3,409 6.01.01.07 Allowance for doubtful accounts 13,379 5,321 (21,030) 6.01.01.08 Provision for contingencies 325,905 248,885 362,678 6.01.01.09 Provision for adjustment to realizable value of storerooms 16,487 0 0 6.01.01.11 Provision for environmental commitments (25,700) 2,558 (8,608) 6.01.01.12 Provision for impairment 0 0 1,997,296 6.01.01.13 Rescheduling of hydrological risk 0 (102,864) 0 6.01.01.14 Bonus for rescheduling of hydrological risk 24,155 0 0 6.01.01.15 Provision for Ad Exitum fees 20,271 0 0 6.01.02 Changes in assets and liabilities (473,422) (514,270) (1,101,385) 6.01.02.01 Interest paid on loans and financing (48,409) (106,224) (136,783) 6.01.02.02 Receivables 171,387 61,514 107,134 6.01.02.03 Taxes and contributions to be offset (73,466) 237 35,018 6.01.02.04 Storeroom 5,714 6,321 176 6.01.02.05 Prepaid expenses (54) 9,990 201 6.01.02.06 Pledges and Restricted Deposits 21,740 (14,770) (163,754) 6.01.02.07 Other receivables (2,971) (6,224) (9,380) 6.01.02.08 Trade accounts payable (3,379) (2,928) (5,054) 6.01.02.09 Taxes and social contributions (6,786) 28,014 (10,507) 6.01.02.10 Payments to private pension entity (167,402) (180,679) (138,804) 6.01.02.11 Sector-related charges (184,718) 102,763 18,975 6.01.02.12 Payments of contingencies (83,215) (89,385) (53,884) 6.01.02.14 Payment sof socio and environmental obligations 0 0 (12,683) 6.01.02.15 Estimated obligations and payroll (11,654) 1,048 (2,100) 6.01.02.16 Other obligations (19,043) (15,579) 20,676 6.01.02.17 Income and social contribution taxes paid (71,166) (308,368) (750,616) 6.02 Net cash from investing activities (13,365) (74,504) (32,483) 6.02.01 In PPE (9,761) (69,221) (32,483) 6.02.02 Additions to intangible assets (3,604) (5,283) 0 6.03 Net cash from financing activities (616,388) (3,035,081) (1,497,184) 6.03.01 Payments of loans and financing (435,258) (1,455,181) (456,330) 6.03.02 Dividends and interest on equity (181,130) (1,579,900) (1,040,854) 6.05 Increase (decrease) in cash and cash equivalents (44,524) (1,879,299) 1,588,203 6.05.01 Opening balance of cash and cash equivalents 548,553 2,427,852 839,649 6.05.02 Closing balance of cash and cash equivalents 504,029 548,553 2,427,852

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 10 of 114

Individual Financial Statements / Statement of Changes in Equity / SCE - 1/1/2016 to 12/31/2016

(In thousands of reais)

Account code Account description

Paid-in capital

Capital Reserves, options granted and

treasury shares Income reserves Retained earnings

accumulated losses) Other comprehensive

income (loss) Equity

5.01 Opening balances 5,975,433 1,929,098 628,783 0 (1,222,422) 7,310,892 5.03 Adjusted Opening Balances 5,975,433 1,929,098 628,783 0 (1,222,422) 7,310,892 5.04 Capital transactions with shareholders 0 0 (31,097) (263,737) 0 (294,834) 5.04.06 Dividends 0 0 0 (154,834) 0 (154,834) 5.04.07 Interest on equity 0 0 0 (140,000) 0 (140,000) 5.04.08 Realization of unearned income reserve 0 0 (31,097) 31,097 0 0 5.05 Total comprehensive income (loss) 0 0 0 305,095 (159,616) 145,479 5.05.01 Net income for the period 0 0 0 305,095 0 305,095 5.05.03 Reclassifications to P&L 0 0 0 0 (159,616) (159,616) 5.05.03.02 Adjustment CPC 33 (R1) at December 31, 2016 0 0 0 0 (159,616) (159,616) 5.06 Internal changes in equity 0 0 15,255 (41,358) 26,103 0 5.06.01 Set-up of reserves 0 0 15,255 (15,255) 0 0 5.06.04 Equity adjustment realized 0 0 0 (26,103) 26,103 0

(Depreciation) 5.07 Closing balances 5,975,433 1,929,098 612,941 0 (1,355,935) 7,161,537

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 11 of 114

Individual Financial Statements / Statement of Changes in Equity / SCE - 1/1/2015 to 12/31/2015

(In thousands of reais)

Account code Account description

Paid-in capital

Capital Reserves, options granted and

treasury shares Income reserves Retained earnings

accumulated losses) Other comprehensive

income (loss) Equity

5.01 Opening balances 5,975,433 1,929,098 1,832,390 0 (1,107,844) 8,629,077 5.03 Adjusted Opening Balances 5,975,433 1,929,098 1,832,390 0 (1,107,844) 8,629,077 5.04 Capital transactions with shareholders 0 0 (1,203,607) (13,371) 0 (1,216,978) 5.04.06 Dividends 0 0 0 (41,326) 0 (41,326) 5.04.08 Realization of unearned income reserve 0 0 (27,955) 27,955 0 0

5.04.09 Proposed additional dividends - AGM held on 4/23/2015 0 0 (1,175,652) 0 0 (1,175,652)

5.05 Total comprehensive income (loss) 0 0 0 (61,357) (39,850) (101,207) 5.05.01 Net income for the period 0 0 0 (61,357) 0 (61,357) 5.05.03 Reclassifications to P&L 0 0 0 0 (39,850) (39,850) 5.05.03.02 Adjustment CPC 33 (R1) at December 31, 2015 0 0 0 0 (39,850) (39,850) 5.06 Internal changes in equity 0 0 0 74,728 (74,728) 0 5.06.04 Equity adjustment realized 0 0 0 74,728 (74,728) 0

(Depreciation) 5.07 Closing balances 5,975,433 1,929,098 628,783 0 (1,222,422) 7,310,892

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 12 of 114

Individual Financial Statements / Statement of Changes in Equity / SCE - 1/1/2014 to 12/31/2014

(In thousands of reais)

Account code Account description

Paid-in capital

Capital Reserves, options granted and

treasury shares Income reserves Retained earnings

accumulated losses) Other comprehensive

income (loss) Equity

5.01 Opening balances 5,975,433 1,929,098 368,223 0 1,044,632 9,317,386 5.03 Adjusted Opening Balances 5,975,433 1,929,098 368,223 0 1,044,632 9,317,386 5.04 Capital transactions with shareholders 0 0 1,017,633 (2,061,710) 0 (1,044,077) 5.04.06 Dividends 0 0 0 (404,543) 0 (404,543) 5.04.07 Interest on equity 0 0 0 (193,000) 0 (193,000) 5.04.08 Income reserve 0 0 28,007 (28,007) 0 0 5.04.09 Realization of unearned income reserve 0 0 (33,405) 33,405 0 0 5.04.10 Statutory reserve 0 0 293,913 (293,913) 0 0 5.04.11 Proposed additional dividends (Note 22.6 (6)) 0 0 1,175,652 (1,175,652) 0 0 5.04.12 Additional dividends paid - AGM held on 4/26/2014 0 0 (446,534) 0 0 (446,534) 5.05 Total comprehensive income (loss) 0 0 0 560,139 (204,371) 355,768 5.05.01 Net income for the period 0 0 0 560,139 0 560,139 5.05.03 Reclassifications to P&L 0 0 0 0 (204,371) (204,371) 5.05.03.02 Adjustment CPC 33 (R1) at December 31, 2014 0 0 0 0 (204,371) (204,371) 5.06 Internal changes in equity 0 0 0 1,501,571 (1,501,571) 0 5.06.04 Equity adjustment realized (depreciation) 0 0 0 183,356 (183,356) 0 5.06.05 Equity adjustment realized (impairment) 0 0 0 1,318,215 (1,318,215) 0 5.07 Closing balances 5,975,433 1,929,098 1,385,856 0 (661,310) 8,629,077

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 13 of 114

Individual Financial Statements / Statement of Value Added

(In thousands of reais) Account

Account description Last year Year before last Second year before last

code 1/1/2016 to 12/31/2016 1/1/2015 to 12/31/2015 1/1/2014 to 12/31/2014

7.01 Revenues 2,039,402 3,520,809 5,484,591 7.01.01 Sale of goods, products and services 2,052,781 3,526,130 5,463,562 7.01.04 (Reversal of) Allowance for Doubtful Accounts (13,379) (5,321) 21,029 7.02 Inputs acquired from third parties (517,034) (1,027,252) (504,544) 7.02.02 Materials, electric energy, third-party services and other (82,499) (111,934) (104,313) 7.02.04 Other (434,535) (915,318) (400,231) 7.02.04.01 Sector-related charges (2,350) (2,918) (385,983) 7.02.04.02 Electric energy purchased (421,020) (892,200) 0 7.02.04.03 Other operating costs (11,165) (20,200) (14,248) 7.03 Gross value added 1,522,368 2,493,557 4,980,047 7.04 Retentions (303,545) (460,380) (642,499) 7.04.01 Depreciation, amortization and depletion (303,5450 (460,380) (642,499) 7.05 Net value added produced 1,218,823 2,033,177 4,337,548 7.06 Value added received in transfer (229,579) (876,645) (1,744,300) 7.06.02 Financial income 101,147 165,008 259,014 7.06.03 Other (330,726) (1,041,653) (2,003,314) 7.06.03.01 Foreign exchange gains (losses), net 133,328 (310,483) (82,645) 7.06.03.02 Employee pension entity - CPC 33/IAS 19 (7,786) (8,938) 4,935 7.06.03.03 Deferred income and social contribution tax assets (69,896) 134,745 437,112 7.06.03.04 Operating provisions (280,531) (224,376) (224,773) 7.06.03.05 Provision for reduction in realizable value of storerooms (16,487) 0 0 7.06.03.06 Other expenses / (income), net (89,354) (632,601) (2,137,943) 7.07 Total value added to be distributed 989,244 1,156,532 2,593,248 7.08 Distribution of value added 989,244 1,156,532 2,593,248 7.08.01 Personnel 145,864 159,795 166,308 7.08.01.01 Direct compensation 142,997 156,949 157,964 7.08.01.04 Other 2,867 2,846 8,344 7.08.02 Taxes, charges and contributions 236,942 568,358 1,178,744 7.08.02.01 Federal 236,758 568,064 1,178,506

DFP - Standard Financial Statements - 12/31/2016 - CESP - Companhia Energética de São Paulo Version: 1

Page: 14 of 114

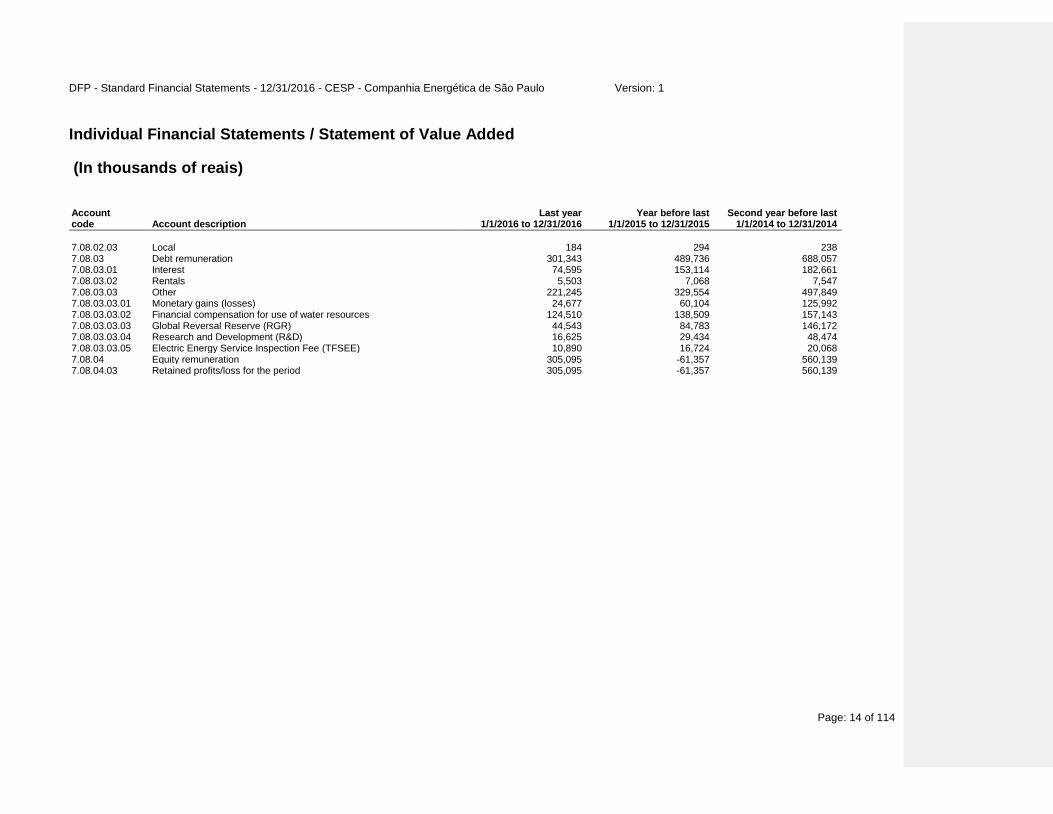

Individual Financial Statements / Statement of Value Added

(In thousands of reais) Account

Account description Last year Year before last Second year before last

code 1/1/2016 to 12/31/2016 1/1/2015 to 12/31/2015 1/1/2014 to 12/31/2014

7.08.02.03 Local 184 294 238 7.08.03 Debt remuneration 301,343 489,736 688,057 7.08.03.01 Interest 74,595 153,114 182,661 7.08.03.02 Rentals 5,503 7,068 7,547 7.08.03.03 Other 221,245 329,554 497,849 7.08.03.03.01 Monetary gains (losses) 24,677 60,104 125,992 7.08.03.03.02 Financial compensation for use of water resources 124,510 138,509 157,143 7.08.03.03.03 Global Reversal Reserve (RGR) 44,543 84,783 146,172 7.08.03.03.04 Research and Development (R&D) 16,625 29,434 48,474 7.08.03.03.05 Electric Energy Service Inspection Fee (TFSEE) 10,890 16,724 20,068 7.08.04 Equity remuneration 305,095 -61,357 560,139 7.08.04.03 Retained profits/loss for the period 305,095 -61,357 560,139

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 15 of 114

Declaration Pursuant to the provisions of items V and VI, article 25 of CVM Ruling No. 480 of December 7, 2009, the Executive Board members of CESP - Companhia Energética de São Paulo, a publicly-held company with head office at Avenida Nossa Senhora do Sabará, 5312, Bairro de Pedreira, in the city and state of São Paulo, enrolled with Brazilian IRS Registry of Legal Entities (“CNPJ”) No. 60.933.603/0001-78, declare that: (i) reviewed, discussed and agreed with the Company’s Financial Statements for the fiscal year ended December 31, 2016; and (ii) reviewed, discussed and agreed with the opinions expressed in the Ernst & Young Auditores Independentes’ report regarding the Company’s Financial Statements for the fiscal year ended December 31, 2016.

Annual Management Report - 2016

I. Message from shareholders Dear Shareholders, The Management of CESP - Companhia Energética de São Paulo, in compliance with legal and statutory provisions, hereby submits to your appreciation the Management Report and the corresponding Financial Statements, together with the Independent Auditor’s report and the Supervisory Board’s opinion for the fiscal year ended December 31, 2016. In 2016, CESP celebrated 50 years of existence, period in which it built its benchmark of excellence in the electric power industry, adopting quality practices and commitment to social and corporate responsibility. Its plants are in an excellent state of conservation and operation, presenting high levels of availability for power production, which exceed ANEEL standards and the average of the industry. In 2016, in compliance with the standards of Brazil’s National Electric Energy Operator System (ONS), the production of CESP’s plants was once again impacted by the water shortage period, requiring ONS to commission a significant volume of thermal energy, to the detriment of hydroelectric production. The Generation Scaling Factor (GSF), which measures the ratio between the effective production of hydroelectric plants and their guaranteed power output, recorded 86.9% in 2016 (84.3% in 2015), resulting in expenses from purchase of energy to the Company. Brazil’s National Electric Energy Agency (ANEEL), through Order No. 190/2016, approved the rescheduling required by CESP regarding the Hydrological Risk of the energy contracted in the regulated market of Porto Primavera Plant, by means of insurance payment. With the expiration of the concession of HPPs Ilha Solteira and Jupiá on July 7, 2015, CESP continued to operate them until June 30, 2016 under the quota system. From July 1, 2016, approximately 220 employees allocated in these plants were terminated and admitted by the new concession operator. Through an agreement entered into in the Labor Court, CESP paid compensation to employees, and received from the new concession operator 50% of expenses incurred with the Unemployment Compensation Fund (“FGTS”) and 100% of expenses incurred with the employees’ notice period, as a refund. Considering its new operational reality resulting from the concession expiration of two of its main plants, CESP began a structural readjustment and cost reduction process, which can already be observed from the second half of 2016. At the end of the year, São Paulo state regulatory agencies authorized a Voluntary Dismissal Program (“PDV”), which should be completed by the end of the first quarter of 2017.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 16 of 114

On August 23, 2016, the Steering Committee of the State Privatization Program decided to recommend to the Governor of São Paulo state to resume the work and studies required for the privatization of CESP, pursuant to article 5 of Law 9361 of July 5, 1996. In November, the State Finance Department published a bid notice for contracting advisory services, consisting of the economic and financial evaluation, modeling proposition and sale of movable assets owned by the State, corresponding to shares representing CESP’s capital. The bid winner was Banco Fator S.A. that started the services in December, which are in progress. CESP is characterized as a company with strong cash generation, low operating costs, low working capital requirements, and low indebtedness. Total loans and financing (current and noncurrent liabilities) decrease from R$1,192.0 million in 2015 to R$651.5 million at December 31, 2016 (a 45.3% decrease). In current year, the Company recorded income of R$305.1 million and, considering the realization of reserves and equity adjustments, it is offering to its shareholders dividends in the amount of R$294.8 million, including interest on equity, as described in Note 25.6 - Proposal for Allocation of Profit, in accordance with the Proposal that the Board of Directors is taking to the resolution of the shareholders at the Annual General Meeting to be held on April 26.

II. CESP and its market CESP has 3 HPPs: Engenheiro Sérgio Motta - Porto Primavera (1,540 MW), Paraibuna (87.02 MW) and Jaguari (27.6 MW), totaling 1,654.62 MW of installed capacity. HPPs Ilha Solteira (3,444 MW) and Jupiá (1,551.2 MW), whose concessions expired on July 7, 2015, remained under CESP’s operation and maintenance, under the quota system, until the total takeover of the new concession operator, which took place on January 7, 2016. Production of electric energy The electric energy production of CESP’s plants is scheduled and executed in accordance with the Grid Procedures and coordinated by ONS, ensuring the preservation of its assets and compliance with its social and environmental obligations. The pursuit of efficiency in production is based on the association of the basic resources of availability, water resources and production allocation opportunities in the Brazilian National Interconnected System (SIN). In 2016, CESP produced 2,243 average MW, which corresponded to approximately 2.0% of the electric energy generated by the hydroelectric supply in the SIN, including considering the operation of HPPs Ilha Solteira and Jupiá under the quota system until June 30, 2016.

In average MW 2010 2011 2012 2013 2014* 2015** 2016***

Production 4.674 4.687 4.822 4.103 3.327 2.747 2.243

* Considering the production of HPP Três Irmãos until September/2014 (expiration of the temporary

operation).

** Considering the production of HPPs Ilha Solteira and Jupiá until December 31, 2015.

*** Considering the production of HPPs Ilha Solteira and Jupiá until June 30, 2016.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 17 of 114

Sale of power Guaranteed power output CESP’s gross guaranteed power output in 2016 was approximately of 1,081 average MW (excluding HPPs Ilha Solteira and Jupiá, operated under the quota system), sold (i) in the Regulated Market (ACR), with 36 distribution companies; and (ii) in the Free Market (ACL), with 4 free customers and 3 sellers.

The differences between the energy produced, the guaranteed power output and the contracted energy were accounted for and settled at the Electric Energy Trade Chamber (CCEE). On December 22, 2016, Ordinance No. 258 of the Ministry of Mines and Energy (MME) reduced the guaranteed power output of HPP Porto Primavera from 1,017 to 992.6 average MW, given the determination of the Federal Audit Court, due to the limitation of the reservoir in the portion of 257 meters by the operation license. This measure had immediate effect, as from its publication, and the Company filed an administrative appeal with the MME, seeking to revert the effects of this Ordinance. With this reduction, the guaranteed power output in force of CESP totals 1,056.6 average MW. In 2016, CESP sold 1,030 average MW in contracts, a 50% reduction compared with 2015, due to the need to be compatible with the new guaranteed power output coverage of the Company. Generation Scaling Factor (GSF) Due to the worsening of hydrological situation that affected most of the generation agents, ANEEL held a public hearing in 2015, which resulted in a proposal to reschedule hydrological risk in the regulated and free markets. In January 2016, CESP adhered to the rescheduling agreement for this risk, set forth by Law No. 13203 of 12/08/2015, regulated by ANEEL Normative Resolution No. 684 of 12/11/2015, transferring to the consumer the effects arising from hydrological risk in the amount of 350 average MW of its guaranteed power output, contracted in the regulated market for 2016, upon payment of a risk bonus. The rescheduling agreement comprises all energy contracted in the regulated market during the concession period. Similarly, in 2016, the unfavorable hydrological conditions caused the commissioning of the HPPs of the Energy Reallocation Mechanism (MRE), which generated below their guaranteed power output during a large period of the year, resulting in the application of the Generation Scaling Factor (GSF). Accordingly, the generators of MRE bear the deficit between generation and guaranteed power output, which is valued at the Difference Settlement Price (PLD). In this context, CESP was impacted by 138 average MW, which valued at the PLD, represented an additional cost of R$123.6 million. By contrast, on account of the adhesion to the hydrological risk rescheduling in the regulated market, CESP was reimbursed in the amount of R$52 million. Regulated Market (ACR) In 2016, CESP allocated to the electric energy distribution companies the average amount of 335 MW, which represented 33% of the total sold in contracts that year. In relation to 2015, there was a 39.2% reduction in the quantities sold in the Regulated Market (ACR), due to the termination of the contracts related to the 2

nd Existing Electric Energy Auction, effective from

2008 to 2015 and of the contracts effective between the beginning of 2014 and the end of the 1st half of

2015, arising from the 12th Existing Electric Energy Auction.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 18 of 114

CESP earned R$576.5 million in Energy Sale Agreements in the Regulated and Free Markets (CCEARs) with distribution companies. This revenue represented a 28.4% reduction compared with 2015 and is justified by the reductions already mentioned in the amounts sold. Free Market (ACL) In this market segment, the energy portion referring to medium and long-term energy sales contracts corresponded to average 695 MW in 2016, representing 67% of the total amount sold that year. Compared with 2015, there was a 54% reduction in the quantities sold in this market due to the expiration of contracts over the year and the lower availability of energy, due to the expiration of concessions. In the free market, revenues amounted to R$1,035.8 million in long- and medium-term bilateral contracts, whereby 7 customers were served, of which 4 were free consumers and 3 were sellers. The reduction was 48.9% compared with revenue for 2015. Revenues from energy settled in the CCEE The Company’s revenue in the CCEE totaled R$48.3 million, including the Spot Market and the Energy Reallocation Mechanism (MRE). Due to the hydrological and energy balance conditions, the Spot Market resulted in R$35.1 million referring to prior years. Conversely, MRE recorded R$13.2 million. The operation and maintenance of HPPs Ilha Solteira and Jupiá by CESP, under the quota system up to June 30, 2016, provided the Company with revenue of R$385.3 million, accounted for by the CCEE. Revenue CESP’s revenues from sales of energy amounted to R$2,045.9 million, a 41.8% reduction on R$3,517.4 million earned in 2015. Of this total, R$385.3 million refer to revenues earned from the portions of assisted operations in HPPs Ilha Solteira and Jupiá; and R$1,660.6 million derived from bilateral contracts in regulated and free markets.

III. CESP electric system CESP ensures compliance with its commercial commitments, reconciling them to the Availability (ANEEL Resolution No. 614/2014) and Systemic (generation needs to meet systemic demand) regulatory requirements, within the principles of economicity. The efficiency of the SIN’s HPPs is determined by the ONS by means of the Availability Index (AI) calculated through the Equivalent Forced Outage Rate (EFOR) and the Equivalent Planned Outage Factor (EPOF) defined by ANEEL. Under its management, to ensure availability and reliability of supply, the Company has exceeded the reference values established by ANEEL, weighted average of 0.897 for AI and 0.0249 for EFOR. In 2016, AI and EFOR of 0.939 (0.941 in 2015) and 0.0048 (0.0050 in 2015), respectively, were determined.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 19 of 114

The dam safety activities at CESP precede the guidelines of Law No. 12334 of September 20, 2010, which established the National Dams Safety Policy. The current Dam Safety Plan is implemented through a rigorous program of regular and special inspections at the HPPs and monitoring of dam behavior through a wide range of auscultation instruments associated with a preventive and corrective maintenance program. As required by ANEEL Normative Resolution No. 696/15, CESP dams are classified as “B - low accident risk and high potential damage”. The innovations of Law No. 12334 and regulation, such as the Periodic Dam Safety Reviews (“RPSB”) and Emergency Action Plans (EAP) in case of burst, have been developed within the established criteria and deadlines. For operation in flood situations, the HPPs use the Operation System for Emergency Situations (SOSEm), a set of operation and maintenance standards and procedures involving technical, organizational and administrative aspects, aiming to ensure the safety of reservoirs hydraulic operation. This comprises 6 manuals maintained and updated annually.

IV. Corporate sustainability To ensure that the current demands for Sustainability are one of the guiding factors of its management in all phases of its ventures, CESP express the evidence of its public commitment, fully aligned with the main concepts of Corporate Sustainability, among which the following are highlighted: CDP - Driving Sustainable Economies Since 2007, CESP responds the survey of the Driving Sustainable Economies, former Carbon Disclosure Project (CDP), which has collaborated to the reflection on climate changes in the Company. The Climate Changes and Carbon Sequestration Program, the tradition in the annual disclosure of the greenhouse gas (GHG) inventory, the management of opportunities and research and development projects are the highlights of climate changes. CESP is a low carbon intensity company, producing electric energy exclusively from HPPs, in water basins considered of low influence in view of climate changes and with potential opportunities in a future low carbon economy. Ecoteams Ecoteams are multidisciplinary teams formed by employees from different CESP areas, the purpose of which is to contribute to the improvement of certain environmental processes existing in the Company. These groups actions are focused on the following themes: occupational health and safety (in partnership with Internal Committees for Accident Prevention - CIPAs); energy and water conscious consumption; solid waste management; realization of campaigns for recycling and donation of footwear, vegetable oil, radiology films, among other materials. Environmental Management System (“SGA”) This is a set of procedures with emphasis on sustainability and focus on the adoption of practices to reduce at most the environmental impact arising from the Company activities. The SGA of HPP Eng. Sergio Motta is being readjusted and that related to HPPs Paraibuna and Jaguari are under implementation phase.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 20 of 114

Spring program This is a State Government program that aims to reforest springs, streams and rivers that form the basins that supply the reservoirs used to serve urban centers. CESP participates in this program, recovering the surroundings of HPP Jaguari reservoir, in the municipalities of Jacarei, Santa Isabel and Igaratá, in Vale do Paraíba. The recovered area in 2016 totaled 46 hectares, with 77,000 seedlings planted. Corporate Sustainability Index (“ISE”) ISE is a tool for comparative analysis of performance of companies listed in BM&FBOVESPA regarding corporate sustainability, based on economic efficiency, environmental balance, social justice and corporate governance. Every year the participating companies are revalued based on a methodology developed by Fundação Getúlio Vargas (FGV), São Paulo. ISE started in 2005 and CESP was present in ten editions, including in 2016 and will not be part of the current portfolio for 2017. Annual report on social and environmental and economic and financial responsibility The Annual report on Social and Environmental and Economic and Financial Responsibility of CESP aims at gathering and presenting economic, financial, industry, social, environmental and corporate governance data of the Company. This report follows the guidelines from “ANEEL Manual for Preparing the Annual Report on Social and Environmental Responsibilities of Electric Energy Companies”, together with the Global Reporting Initiative (GRI) methodology, including the Electric Utility Sector Supplement (GRI-EU). The internationally recognized GRI methodology establishes a reporting standard aligned with the best practices of governance, environmental, economic and social performance for sustainability reports. Social and environmental manual The procedures related to social and environmental issues adopted by CESP during the rainy season, mainly due to the increase in outflows, were gathered in this manual that integrates the manuals of SOSEm - Operation System for Emergency Situation, aiming the safety of dams, reservoirs, employees and of the communities around the HPPs. Supplier Manual Available on CESP website, it establishes values, principles and guidelines that drive the relationship with suppliers and set CESP Supply Policy. The Supplier Manual was updated in 2015 to include guidelines provided in the Anti-corruption Law.

V. Social Responsibility Diversity CESP kept Selo Paulista da Diversidade (São Paulo State Diversity Seal) - Full Category, granted by São Paulo State government. This seal reflects the policy of non-exclusion concerning racial, social, sexual, ideological and religious differences, among others.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 21 of 114

In 2016 various actions related to this certification were carried out, involving the following activities: speech “Diversities: Living Together, Talking and Building” (VII Semana Interna da Diversidade - SIDI); awareness of employees on the following dates of the Diversity calendar: Women’s Day, International Day for the Elimination of Racial Discrimination; Indian Day; International Day Against Homophobia; National Black Awareness Day and ecumenical celebration at the end of the year. Social actions Website Accessible to Visually Impaired Persons CESP counts on resources that facilitates access to its corporate website, including the Investor Relations module, to visually impaired persons who have screen reader software in their computers and want to know the Company or use any page as a working tool. Instituto Criança Cidadã (ICC) CESP continued its participation as founding and sponsor company of Instituto Criança Cidadã (ICC), contributing to the operation of the 16 educational units of the institution. The voluntary work by employees who assist the institution with technical and administrative orientation is added to the financial support. As in prior years, ICC, an educational entity that has the history of its projects initiated by CESP in 1987, presented in 2016 important actions and achievements that allowed the renewal of recognition of the entity as Federal, State and Municipal Public Utility. In 2016, more than 7,500 services were provided to children, young people and adults, all residents of poor communities in the eastern, southern, northern and western regions of the capital and of the municipality of Guarulhos within the four projects of the institution: Transmitindo Cidadania, Gerando Talentos, Manancial de Produção-Escola de Moda e Beleza and Nossa Comunidade. ICC ensures balanced nutrition, supervised by a nutritionist; comprehensive support for child development by a multidisciplinary health team; primary education, art, education and work orientation, offered by educators, coordinators and educational directors; and activities focused sports and leisure, community development and income generation. Social Inclusion of Apprentices Social inclusion of apprentices, which is promoted by the CESP’s Professional Learning Program, aims to prepare not only good professionals, but mainly better citizens for Brazil. This program includes actions focused on apprentices and their families, conducting, among other activities, speeches and dynamics with apprentices. In 2016, young people participated in events related to organizational environment, such as interpersonal relationship, and also participated in the Internal Week of Accident Prevention (“SIPAT”), where they were able to learn more about prevention of technological dependence, sedentary lifestyle, nutrition and quality of life. Visits to the production units In 2016, CESP’s production units were visited by 41,529 people. Students, engineers, technicians and tourists have on these visits the opportunity to obtain information on the operation of a HPP and also take notice of the various programs developed by the Company in the search for knowledge and conservation of native fauna and flora. In the case of HPP Porto Primavera, visitors also have contact with aspects of the region’s culture in the Museum of Regional Memory.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 22 of 114

Until June 30, CESP still was responsible for HPPs Ilha Solteira and Jupiá and the results of visits to these units are computed in the general result. Porto Primavera received 6,059 visitors in its facilities while Paraibuna received 1,469 visitors.

VI. Social statement of financial position

1 - Calculation basis Amount for 2016 (in thousands of reais) Amount for 2015 (in thousands of

reais)

Net revenue (NR)

2,950,982

1,668,590

Gross operating income (GOI) 883,550 1,530,575

Gross payroll (GP) 181,474 208,621

2 - Internal Social Indicators Amount

(thousand) % on GP % on NR Amount

(thousand) % on GP % on NR

Meal 7,947 4.38% 0.48% 9,431 4.52% 0.32%

Compulsory social charges 31,910 17.58% 1.91% 43,281 20.75% 1.47%

Private pension 6,554 3.61% 0.39% 8,351 4.00% 0.28%

Health 12,717 7.01% 0.76% 10,531 5.05% 0.36%

Education 495 0.27% 0.03% 664 0.32% 0.02%

Professional training and development 639 0.35% 0.04% 695 0.33% 0.02%

Day care or day-care allowance 54 0.03% 0.00% 32 0.02% 0.00%

Other 0 0.00% 0.00% 226 0.11% 0.01%

Total - Internal Social Indicators 60,316 33.24% 3.61% 73,211 35.09% 2.48%

3 - External Social Indicators Amount

(thousand) % on OR % on NR Amount

(thousand) % on GOI % on NR

Education 1,913 0.22% 0.11% 2,959 0.19% 0.10%

Culture 2,910 0.33% 0.17% 6,400 0.42% 0.22%

Sports 418 0.05% 0.03% 1,074 0.07% 0.04%

Other 125,739 14.23% 7.54% 142,092 9.28% 4.82%

Total contributions for the company 130,980 14.82% 7.85% 152,525 9.97% 5.17%

Taxes (less social charges) 205,032 23.21% 12.29% 525,078 34.31% 17.79%

Total - Internal and External Social Indicators 336,012 38.03% 20.14% 677,603 44.27% 22.96%

4 - Environmental Indicators Amount

(thousand) % on OR % on NR Amount

(thousand) % on GOI % on NR

Investments related to production/operation of Company 15,057 1.70% 0.90% 29,554 1.93% 1.00%

Investments in external programs and/or projects 3,278 0.37% 0.20% 6,462 0.42% 0.22%

Total investments in the environment 18,335 2.08% 1.10% 36,016 2.35% 1.22%

5 - Personnel Indicators 2016 2015

Number of employees at the end of the period 568 802

Number of admissions over the period 9 23

Number of interns 0 13

Number of employees with more than 45 years 461 640

Number of women working in the company 103 131

% of management positions occupied by women 5.77% 6.67%

Number of blacks working in the Company 127 179

% of management positions occupied by blacks 1.92% 1.75%

Number of people with disabilities or special needs 9 11

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 23 of 114

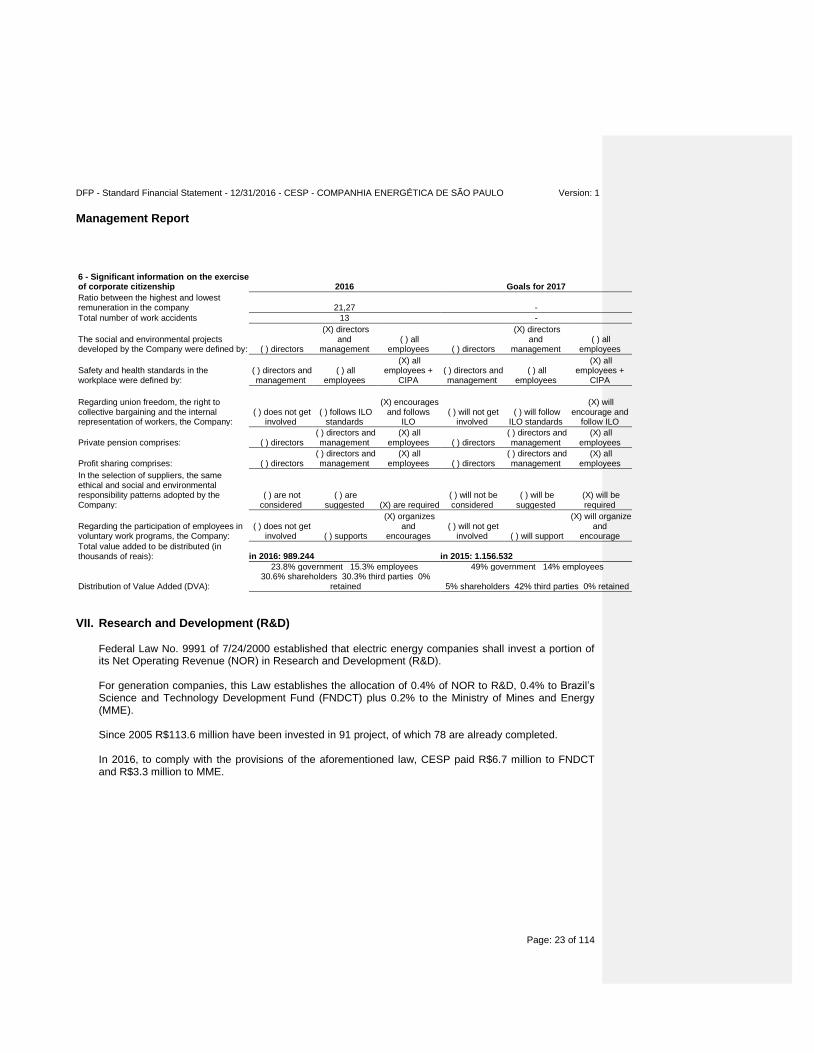

6 - Significant information on the exercise of corporate citizenship 2016 Goals for 2017

Ratio between the highest and lowest remuneration in the company 21,27 -

Total number of work accidents 13 -

The social and environmental projects developed by the Company were defined by: ( ) directors

(X) directors and

management ( ) all

employees ( ) directors

(X) directors and

management ( ) all

employees

Safety and health standards in the workplace were defined by:

( ) directors and management

( ) all employees

(X) all employees +

CIPA ( ) directors and

management ( ) all

employees

(X) all employees +

CIPA

Regarding union freedom, the right to collective bargaining and the internal representation of workers, the Company:

( ) does not get involved

( ) follows ILO standards

(X) encourages and follows

ILO ( ) will not get

involved ( ) will follow

ILO standards

(X) will encourage and

follow ILO

Private pension comprises: ( ) directors ( ) directors and

management (X) all

employees ( ) directors ( ) directors and

management (X) all

employees

Profit sharing comprises: ( ) directors ( ) directors and

management (X) all

employees ( ) directors ( ) directors and

management (X) all

employees

In the selection of suppliers, the same ethical and social and environmental responsibility patterns adopted by the Company:

( ) are not considered

( ) are suggested (X) are required

( ) will not be considered

( ) will be suggested

(X) will be required

Regarding the participation of employees in voluntary work programs, the Company:

( ) does not get involved ( ) supports

(X) organizes and

encourages ( ) will not get

involved ( ) will support

(X) will organize and

encourage

Total value added to be distributed (in thousands of reais): in 2016: 989.244 in 2015: 1.156.532

Distribution of Value Added (DVA):

23.8% government 15.3% employees 49% government 14% employees 30.6% shareholders 30.3% third parties 0%

retained 5% shareholders 42% third parties 0% retained

VII. Research and Development (R&D) Federal Law No. 9991 of 7/24/2000 established that electric energy companies shall invest a portion of its Net Operating Revenue (NOR) in Research and Development (R&D). For generation companies, this Law establishes the allocation of 0.4% of NOR to R&D, 0.4% to Brazil’s Science and Technology Development Fund (FNDCT) plus 0.2% to the Ministry of Mines and Energy (MME). Since 2005 R$113.6 million have been invested in 91 project, of which 78 are already completed. In 2016, to comply with the provisions of the aforementioned law, CESP paid R$6.7 million to FNDCT and R$3.3 million to MME.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 24 of 114

VIII. Corporate governance Since 2006, CESP is part to BM&FBOVESPA’s Corporate Governance Level 1, a set of rules that governs the relations among the controlling shareholder, the Board of Directors, the Executive Board, the other shareholders and, particularly, the financial market, which is provided with information with quality, agility and transparency. In addition to the procedures required by Corporate Governance Level 1, CESP, adopted the following practices, which were included in its Articles of Incorporation: - Adhesion to the Market Arbitration Chamber of BM&FBOVESPA to eliminate any questions of

corporate nature;

- Tag Along - Right to class B preferred shareholders (CESP 6) to receive an amount per share corresponding to 100% (one hundred percent) of the amount paid to the controlling shareholder, in the event of divesture of the Company's control;

- Board of Directors made up by 20% of independent directors. Investor Relations CESP has an Investor Relations (IR) area that coordinates the distribution of information to the financial market in general, investors, market analysts, financial institutions, regulatory and supervision agencies, through quarterly results conference calls, annual public meetings, corporate website, RI module (http://ri.cesp.com.br), e-mail [email protected] and mailing list. Throughout 2016, approximately 40 events were held with market analysts and investors. CESP is monitored by 12 market analysts, who periodically issue reports with recommendations on the Company’s actions. The list of analysts is available on our investor relations website: ri.cesp.com.br. Board of Directors According to the Company’s Articles of Incorporation, the Board of Directors may be composed of up to 15 members, with at least 20% of independent directors elected for a term of two (2) years. At the Annual General Meeting held in 2015, 13 members were elected, 3 of them were independent directors and one was elected by the preferred shareholders. A member elected by the Company’s employees is also part of the Board of Directors. Member Luiz Gonzaga Vieira de Camargo resigned on 5/31/2016 and Member Renato A. Z. Villela dos Santos resigned on 8/31/2016, 11 members remaining, whose term will expire at the Annual General Meeting to be held in April, 2017. The Board of Directors’ Meetings in their ordinary form, pursuant to our Articles of Incorporation, are held once a month, and on a special form, whenever necessary to the interests of the Company. In 2016, 12 ordinary meetings were held in person against 1 special meeting also in person. The average level of members’ attendance was 87.7%. Executive Board The Executive Board, in accordance with the Articles of Incorporation, is composed of a Chief Executive Officer, a Chief Financial and Investor Relations Officer, a Chief Generation Officer, who also responds as deputy Chief Engineering and Construction Officer, and a Chief Administrative Officer. The Executive Board shall meet, ordinarily, at least twice a month and, on a special basis, by call of the CEO or of other officers. In 2016, 37 Board of Directors’ meetings were held.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 25 of 114

Supervisory Board The Supervisory Board is made up of five members and their respective deputies, elected annually at the Annual General Meeting, with one of the Directors representing the preferred shareholders and another one representing the noncontrolling common shareholders. The term of Supervisory Board Members is unified for one year and they may be reelected under the terms of the law. The Supervisory Board’s meetings are held at least once a month. In 2016, 12 meetings were held in person and the members’ attendance level was 100%. Among other responsibilities, the Supervisory Board has to analyze, on a quarterly basis, the trial balances and other financial statements prepared for the fiscal year, and also express an opinion on the annual management report, stating in such opinion any further information deemed necessary for the resolution at the Annual General Meeting. The Supervisory Board also reports to shareholders in matters related to investment plans or budget, capitalization changes, payment of dividends and corporate reorganizations. This Board is responsible for overseeing management activities and keeping shareholders informed of its findings. Internal audit CESP counts on an Internal Audit Department in connection with the CEO, whose mission is to provide assessments on control system adequacy and efficiency, accuracy of operations, legitimacy of actions carried out and performance quality in relation to defined policies, plans and objectives. It is also responsible for coordinating Corporate Risk Management activities, attending to external audit agencies such as the State Audit Court (‘TCE”), Control and Evaluation Center (“CCA”) of the State Finance Department, among others, in addition to assist the activities of the Supervisory Board. Code of Ethics and Business Conduct CESP’s Code of Ethics and Business Conduct is intended for disseminating the Company’s principles and values to all of its employees, in addition to guiding relations with its stakeholders. Pursuant to good corporate governance practices, in 2015 CESP reviewed such code and, among other updates, the provisions of Federal Law No. 12846 of 8/1/2013 (Anti-Corruption Law) and of State Decree No. 60106 of 1/29/2014 were integrated, which provides for the administrative and civil responsibility of legal entities for the practice of acts against the public, national and international administration. In 2016, CESP promoted a Web-Based Training Session concerning of its Code of Ethics and Business Conduct with the purpose of recycling knowledge and strengthening the awareness of its professionals regarding the principles and values that govern the Company’s relations. The Code is available at intranet (Netcesp) and on CESP's website: (http://www.cesp.com.br). Upon accessing it, a link is already available so that the registration of representation is made, as the case may be. There is also the e-mail [email protected], so that stakeholders can make representations. Environmental policy CESP’s Environmental Policy was approved at the 1643

rd Board of Directors’ Meeting held on May 4,

2015, aimed at disseminating a culture of social and environmental responsibility to employees, service providers, suppliers, surrounding communities and other stakeholders.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 26 of 114

Concerned about the effects that climate changes may have on the society, as well as about the economic, social and environmental dynamics of its hydroelectric power generation activities, CESP has incorporated in its Environmental Policy its commitment to promote sustainable development and exercise of social responsibility, as well as the environmental management of its activities. Supply policy Approved at the 631

st Board of Directors’ Meeting held on January 17, 2012, the Supply Policy was

established to meet, in a planned, integrated, effective and transparent manner, guided by defined guidelines, purchases of materials and services for the Company.

Information security policy The purpose of this Policy is to guarantee information privacy and to protect it previously against unauthorized use. It provides guidance for the use of technological resources only for the purposes approved by CESP, and also aims to ensure data security through backup with “deduplication” and information contingency in in-house environments (at the head office and at Porto Primavera), enabling immediate recovery of data in case of claim, so that the Company’s business does not suffer solution of continuity. Corporate social policy CESP’s Corporate Social Policy presents the principles and guidelines that grounds the Company’s practices in relations with stakeholders shareholders, creditors, customers, employees, partners, community, government and society. This Policy addresses human and labor right practices as well as practices of relationships with suppliers and the community, such as not hiring child labor or analogous to slavery; non-discriminatory hiring; incentive to diversity among employees; promotion of health and safety of employees and third parties; support to educational actions for young people in local communities; narrowing of internal and external communication channels. In 2015, to adjust such policy to the current concepts, the repudiation and prohibition of any practice regarding the sexual exploitation of men, women, children and teenagers were pointed out. The Corporate Social policy is available at intranet and on the Company’s website. Policy of relations with internal entities On March 30, 2007, the Policy of Relations with Internal Entities was implemented, through which CESP recognizes and respects the right of its employees to join and act in Internal Entities, with own legal entity, legally established, and proposes to receive and evaluate proposals and suggestions from employees’ associations, in order to improve the Company’s activities and the relationship with its employees. Health and safety policy Established on September 25, 2006, the Health and Safety Policy reaffirms CESP’s commitment to seek excellence in electric power generation, considering respect for life, protection against occupational health and safety of its employees and service providers, key components of corporate performance and key management responsibility at all levels. CESP still grounds health and safety management on compliance with prevailing legislation and on the search for continuous improvement of production processes. The Company maintains in its organizational structure a formally defined body with the technical competence to diagnose and propose measures for Occupational Health and Safety and issues.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 27 of 114

Union relations policy Approved on March 30, 2007, CESP grounds its relations with Unions on the effective recognition that these entities are the lawful representatives of employees in filing of claims and conducting negotiations so as to resolve labor relations issues.

Disclosure policy The Company’s Disclosure Policy, approved by the Board of Directors on July 15, 2002 aims to establish the rules to be observed by the Chief Investor and other Related Persons Relations Officer regarding the disclosure of Significant Information and the maintenance of confidentiality on relevant acts or facts that have not yet been disclosed to the public. Policy of securities trading issued by the Company itself In 2011, the Board of Directors approved the Policy on Securities Trading Issued by the Company itself, which establishes the rules by which the related parties, as defined in the Policy, should be guided for securities trading issued by the Company itself. Dividend policy In 2011, the Board of Directors also approved the Dividend Policy, which defines the periods and criteria adopted for the payment of dividends and interest on equity. This Policy is based on the rules of the Articles of Incorporation and emphasizes the role of the Board of Directors in the conduction of this Policy. Policy of conversion of class “A” registered preferred shares In 2013, the Board of Directors approved the Policy of Conversion of Class “A” Registered Preferred Shares, which defines the periods and criteria adopted for the conversion of class “A” preferred shares. This Policy is based on article 5 of the Articles of Incorporation and aims to establish the rules that should be observed for the conversion of class “A” registered preferred shares into registered common shares and/or class “B” registered preferred shares. Risk management policy CESP’s Risk Management Policy was submitted to the approval by the Board of Directors on June 7, 2011 and was unanimously approved. The Company has implemented a corporate risk management framework, based on the principles of COSO II - Enterprise Risk Management Integrated Framework (ERM), international pattern on risk management. CESP’s Risk Management Policy establishes the process, methods and criteria for identifying, evaluating, monitoring and reporting of risks and respective control or mitigation actions to be observed by agents responsible for the risk management activity within the scope of the Company. The Risk Committee, the Risk Management Coordination and the Decentralized Risk Management are included in the risk management control organization framework. The Company’s Strategic Risk Matrix was reviewed with the support of the Boards and of the Decentralized Risk Management, and submitted to the Risk Committee’s evaluation and subsequently to the Board of Directors’ appreciation at the 692

nd Annual Meeting on May 10, 2016.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 28 of 114

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 29 of 114

Risk Committee This is composed of the Chairman and Officers, Executive Coordination Management of the CEO and of the Internal Audit Department. It is incumbent upon the Risk Committee to define the guidelines and strategies for risk management and evaluation of controls, for the follow-up of the action plans presented by the Company’s managing officers, as well as to drive the activities carried out by the Risk Management Coordination. Risk Management Coordination This is responsible for monitoring the actions of the Decentralized Risk Management in the identification, evaluation and monitoring of risks and regular reporting to the Risk Committee. It should also guide the Company’s managing officers regarding the self-assessment control methodology, to ensure the efficiency of controls that mitigate the risks mapped, as well as support the CEO, the Risk Committee and other stakeholders in matters related to risk and control management. Decentralized Risk Management Representatives appointed by the Boards to assist the Managing Officers of the Company's various areas in the identification, evaluation, control and monitoring of risks inherent to the objectives in their areas of responsibilities. It is also incumbent upon the Decentralized Risk Management to position periodically the Risk Management Coordination and its Board of subordination on the risks and controls inherent in the responsibility of their performance. Internal control system CESP complies with the best practices of the Internal Control System, such as: Environment and Control Activities, Risk Assessment, Information, Communication and Monitoring. The Internal Control System is defined as the set of policies, standards and procedures and activities established in the Company to reduce the possibility of financial losses, scratched institutional image, to improve the quality of accounting, financial and managerial information as well as to safeguard compliance with prevailing legislation and regulation to ensure that the objectives are achieved. The Company’s Internal Control System was submitted to the Board of Directors’ appreciation on September 13, 2016, mentioning all external auditors to whom the Company is subject, namely: State Audit Court (“TCE”), Management General Comptroller (“CGA”), Electric Energy Sale Chamber (CCEE), Brazil's National Electric Energy Agency (ANEEL); Brazil's National Electric Energy Operator System (ONS), Environmental Agencies - IBAMA/SEMA/IMASUL; Brazilian Securities and Exchange Commission (“CVM”); and Control and Evaluation Center (“CCA”) in connection with the State Finance Department. The Company’s Internal Control System comprises Corporate Policies, Standards and Procedures, Delegation of Authority Manual “(MDA”), Code of Ethics and Business Conduct, Computerized Systems, Internal Audit body, in addition to Risk Management and other control practices and processes.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 30 of 114

Law No. 13303/2016 Based on Law No. 13303 of June 30, 2016, the set of items already complied with by CESP, in accordance with such Law, was presented to CESP’s Board of Directors on October 18, 2016, such as the Information Disclosure Policy, Dividend Payment Policy, Annual Sustainability Reports (GRI model) and Social and Environmental and Financial and Economic Responsibility Report (ANEEL model), the Code of Ethics and Business Conduct, the risk management model (under review), as well as the existence of a permanent Supervisory Board. Other items requiring actions should be implemented throughout 2017. In compliance with article 23, paragraph 1, item II of Law No. 13303/2016, on November 8, 2016 the Board of Directors approved the Company’s Long-Term Strategy. State Decree No. 62349/2016 On December 26, 2016, State Decree No. 62349/2016 was enacted, regulating the application of Federal Law No. 13303/2016. The Company presented to the Board of Directors, at the Annual Meeting held on January 24, 2017, a schedule of activities to fulfill the obligations arising from such State Decree. Ombudsman CESP, together with the Ombudsman System of São Paulo State Government, makes available on its website a channel of relationship with the purpose of receiving, clarifying and responding any and all expressions of citizen’s interest regarding the Company. It acts as final level in its defense, including causing internal transformation actions aimed at improving the quality of the services provided by the Company. In 2016, the CESP’s Ombudsman recorded 62 expressions. Among the main topics, the instructions and clarifications of doubts related to human resources, equity and environment were highlighted, as well as complaints regarding electric energy distribution companies, an activity that is not part of CESP’s business since 1998. Complaints of citizen warning the Company were also recorded, through the Ombudsman office, in relation to invasions or interventions in border areas of reservoirs. Citizen Information Service In accordance with the provisions of São Paulo State Government (State Decree No. 58052 of May 16, 2012, which regulated Federal Law No. 12527 of November 18, 2011), CESP joined the Citizen Information Service (“SIC”), through which the Company gives access to information requested by citizens and entities, reinforcing the good practices of governance and transparency. Access to the system is done through the website www.sic.sp.gov.br. In 2016, the Company recorded 33 applications received and served through SIC System, which presents various forms of citizen access to information, including on-site, with service in an exclusive room for this service.

IX. Capital markets The Company was not required to resort to capital markets in 2016. Total Payables reduced by 9%, from R$4,675.9 million in 2015 to R$4,254.9 million in 2016.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 31 of 114

The Company’s cash and cash equivalents at the end of 2016 reached R$504 million, reduction by 8.1% compared with 2015. In June 2016, Standard & Poor’s reaffirmed ratings “BB” on the global scale and “brAA-“ on the Company’s Brazilian National Scale. The Stand-Alone Credit Profiles (SACP) remains unchanged in “bbb-“. The negative perspective reflects that of sovereign ratings of Brazil and of São Paulo State. CESP shares in BM&FBOVESPA Class “B” Preferred Shares (CESP6), which represent 64.4% of the Company’s total capital and which are the most traded, appreciated 0.67% in 2016, with a price quotation at the end of the year of R$13.49. The CESP6 traded volume in 2016 reached a daily average of R$20.9 million and 5,503 transactions. Common Shares (CESP3), which represents 33.3% of capital, closed the year with an appreciation of 22.5%, quoted at R$12.50. Class “A” Preferred Shares (CESP5), which represent 2.3% of capital, increased by 48.40% and were traded in the last trading session of the year at R$19.30. Electric Power Index (“IEE”) closed 2016 with an appreciation of 45.6% while IBOVESPA recorded appreciation of 38.9%. In 2016, the Company paid to its shareholders R$41.3 million of dividends referring to 2015 and R$140 million as interest on equity.

X. Economic and financial performance In 2016, CESP reported net income of R$305.1 million, reversing the loss of R$61.4 million recorded in prior year. Among other reasons, this result arises from the reduction of expenses, mainly (i) energy purchased and sector-related charges (which includes the use of the transmission system); (ii) reduction of expenses with personnel, material, third-party services and other; (iii) reduction in provisions recorded under “Other revenues (expenses), net” (against “Provision for contingent assets” in the amount of R$580.8 million of HPPs Ilha Solteira and Jupiá in 2015); and (iv) the appreciation of the Brazilian real against the US dollar this year (against a significant devaluation of the Brazilian real in prior year). On July 7, 2015, the concession of HPPs Ilha Solteira and Jupiá expired. As from that date, the Company has been facing an evident decrease in revenue, since it can no longer rely on the electric energy from those plants traded under the Price Regime. Currently, the Company is temporarily recording two types of revenue: (i) revenues from other plants, based on the prices and quantities of electric energy sold in free markets, both regulated and in the Electric Energy Trade Chamber (CCEE); and (ii) the transitional income as an operator under the Quota System at the plants Ilha Solteira and Jupiá from July 8, 2015 to June 30, 2016, a period known as “assisted operation”. Accordingly, operating revenues for 2016 reached R$2,052.8 million, a reduction of 41.8% compared with 2015, mainly due to the reduction of guaranteed power output arising from the expiration of the concession, on July 7, 2015, of HPPs Ilha Solteira and Jupiá, as well as the termination in the second half of 2016 of the “assisted operation” period of these plants, under the quota system (Notes 26.2 and 26.3). The decrease in operating revenue totaled R$384.2 million, a 33.2% decrease compared with 2015, resulting in Net Operating Revenue of R$1,688.6 million, a 43.5% decrease compared with 2015.

The Cost of Electric Energy Service totaled R$785 million, a 44.7% decrease, separated by items Cost of Electric Energy and Cost of Operation (Note 27). The Cost of Electric Energy decreased by 52% mainly due to Sector-Related Charges (which include

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 32 of 114

transmission system charge) and purchase of electric energy. The Cost of Operation decreased by 34.7%, mainly as a result of the decrease in expenses with personnel, material, third-party services and other, as well as depreciation expenses. CESP recorded Gross Operating Income of R$883.6 million in 2016, representing a 42.3% decrease compared with prior year. General and Administrative Expenses decreased by 9.1% and Other Operating Expenses increased by 35.9%, mainly due to higher provisions for labor and environmental contingencies, as a matching entry to the reduction in the provision for civil proceedings. Other Revenues (Expenses), Net decreased by 85.7% and ended 2016 in R$90.6 million, compared with R$633.9 million in 2015, mainly due to the provision for contingent assets in the amount of R$580.8 million related to HPPs Ilha Solteira and Jupiá recorded that year, (Note 27.2), so that Operating Income before Financial Income totaled R$282.2 million, 37.2% lower than in prior year. Adjusted EBITDA for operating provisions totaled R$911.7 million, representing a 47.6% decrease compared with prior year. The Financial Income reached a positive result of R$135.2 million (negative result of R$358.7 million in 2015, see Note 28). Financial Revenues decreased by 38.7% and reached R$101.1 million, mainly due to the decrease in short-term investment yield due to the reduction in cash and cash equivalents and investments. Debt Charges and Other Financial Expenses recorded a 51.3% decrease, totaling R$74.6 million, reflecting the reduction of indebtedness in local currency, as well as Monetary Variations, Net, which closed the year at R$24.7 million (a 58.9% decrease). Foreign Exchange Gains (Losses), net reached R$133.3 million due to an appreciation of 16.5% of the Brazilian real against the US Dollar compared with expenses of R$310.5 million in prior year. The Company recorded Income before Taxes of R$417.4 million. After appropriation of Income and Social Contribution Tax Expenses on taxable income and reversal of deferred taxes, the Company closed 2016 with Net Income of R$305.1 million. Note 25.6 comprises the Management’s proposal, based on net income, less of legal reserve of R$15.3 million and of equity adjustment on the depreciation in the amount of R$26.1 million, increased by the realization of Unrealized Income Reserve in the amount of R$31.1 million. The distribution of profits in the amount of R$294.8 million, corresponding to 100% of the adjusted income for the year, is being proposed, of which R$140 million will be deducted, which were already paid as Interest on Equity.

DFP - Standard Financial Statement - 12/31/2016 - CESP - COMPANHIA ENERGÉTICA DE SÃO PAULO Version: 1

Management Report

Page: 33 of 114

I. Economic and Financial Indicators

References 2016 2015 Var.

Average Price - R$ per MWh 178.15 164.93 8.0% Operating Margin (%) 53.0% 36.7% 44.3% US Dollar Fluctuation (%) -16.5% 47.0% - 63.5 pp

Liquidity/indebtedness/Per-Share Equity Value (VPA) 2016 2015 Var.

Indebtedness of Assets 0.37 0.39 -4.4% Participation of third-party capital 0.59 0.64 -7.2% Current Liquidity 0.98 1.02 -4.1% Share Price - R$ 21.87 22.32 -2.0%

EBIT/ EBITDA Statement (CVM Ruling No. 527 dated October 14, 2012) 2016 2015 Var.

Net income for the period 305,095 (61,357) nm

Income and social contribution taxes 112,336 152,165 -26.2% Financial income (expenses) (135,203) 358,693 nm

= EBIT 282,228 449,501 -37.2% Depreciation 303,545 460,380 -34.1%

= EBITDA 585,773 909,881 -35.6%

Provision for contingent assets - 580,798 nm Provision for contingencies 325,905 248,885 30.9%

= ADJUSTED EBITDA 911,678 1,739,564 -47.6%