Stakeholder Meeting Terasen Integrated Resource PlanTerasen Integrated ... · Terasen Integrated...

27

Stakeholder Meeting Terasen Integrated Resource Plan Terasen Integrated Resource Plan February 2, 2010

Transcript of Stakeholder Meeting Terasen Integrated Resource PlanTerasen Integrated ... · Terasen Integrated...

Stakeholder MeetingTerasen Integrated Resource PlanTerasen Integrated Resource Plan

February 2, 2010

SummaryAbout the NWGANW Energy FactsNW Energy FactsPolicy OverviewNW Gas Market ForecastObservationsObservations

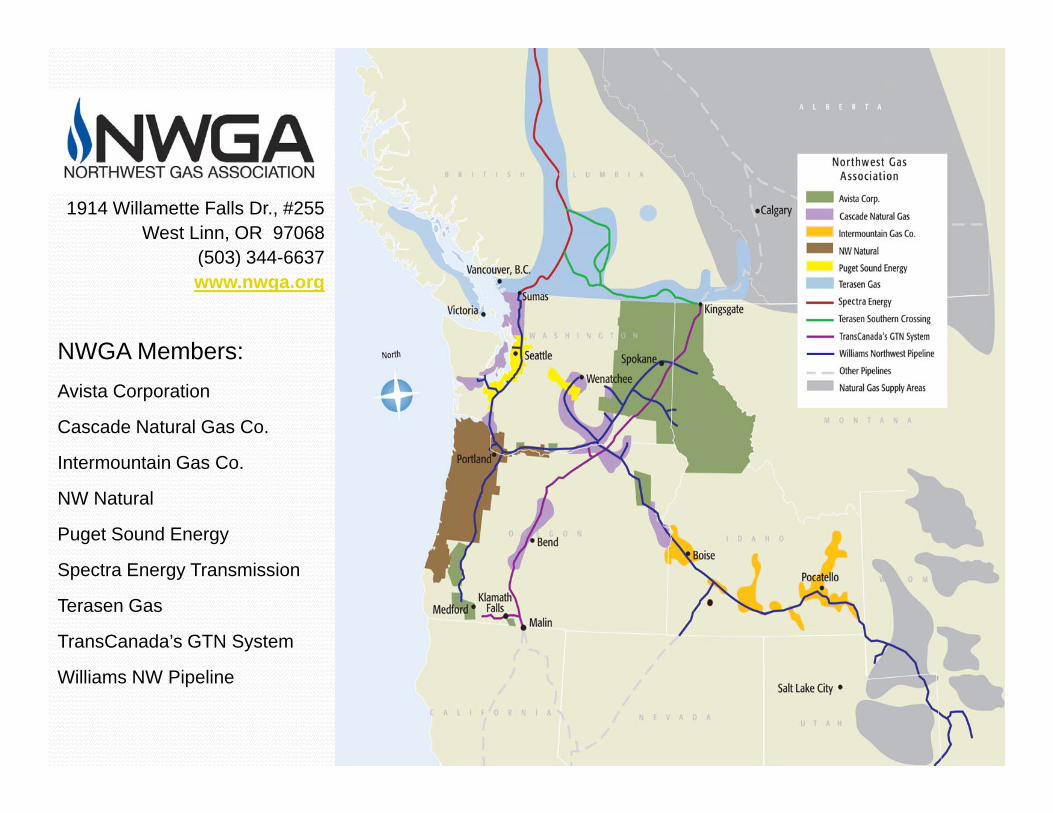

1914 Willamette Falls Dr., #255West Linn, OR 97068

(503) 344 6637(503) 344-6637www.nwga.org

NWGA Members:NWGA Members:Avista Corporation

Cascade Natural Gas Co.

I t t i G CIntermountain Gas Co.

NW Natural

Puget Sound Energy

Spectra Energy Transmission

Terasen Gas

TransCanada’s GTN System

Williams NW Pipeline

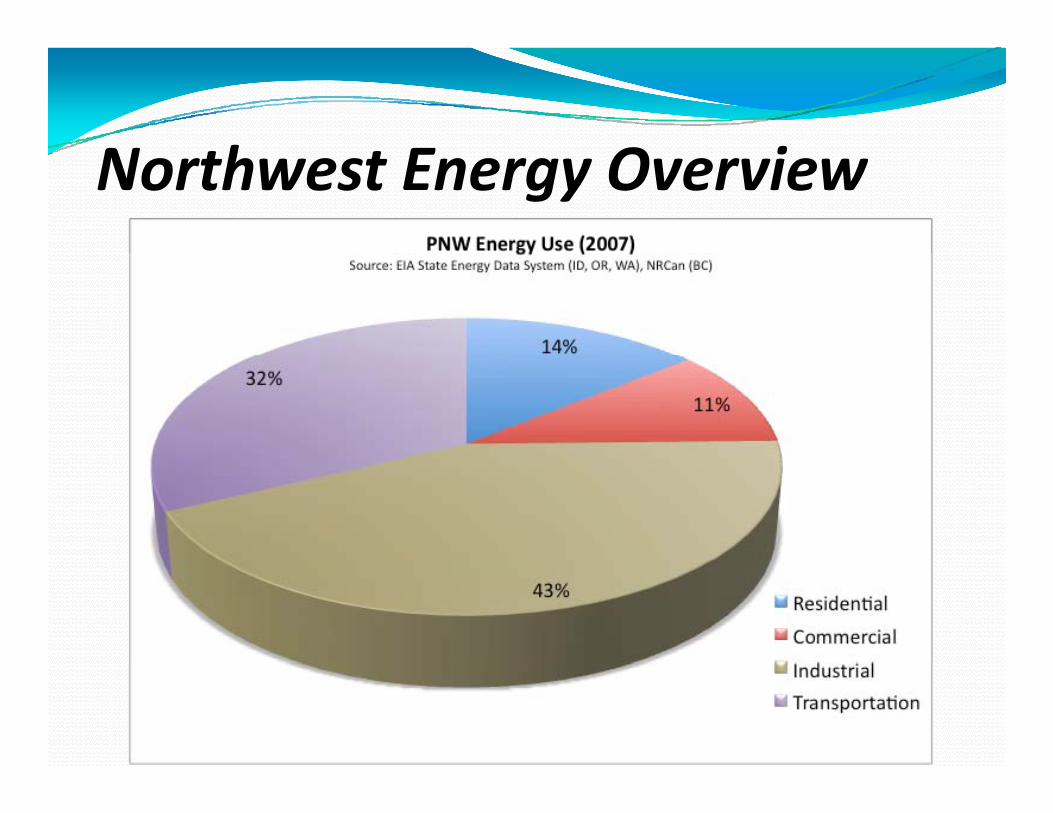

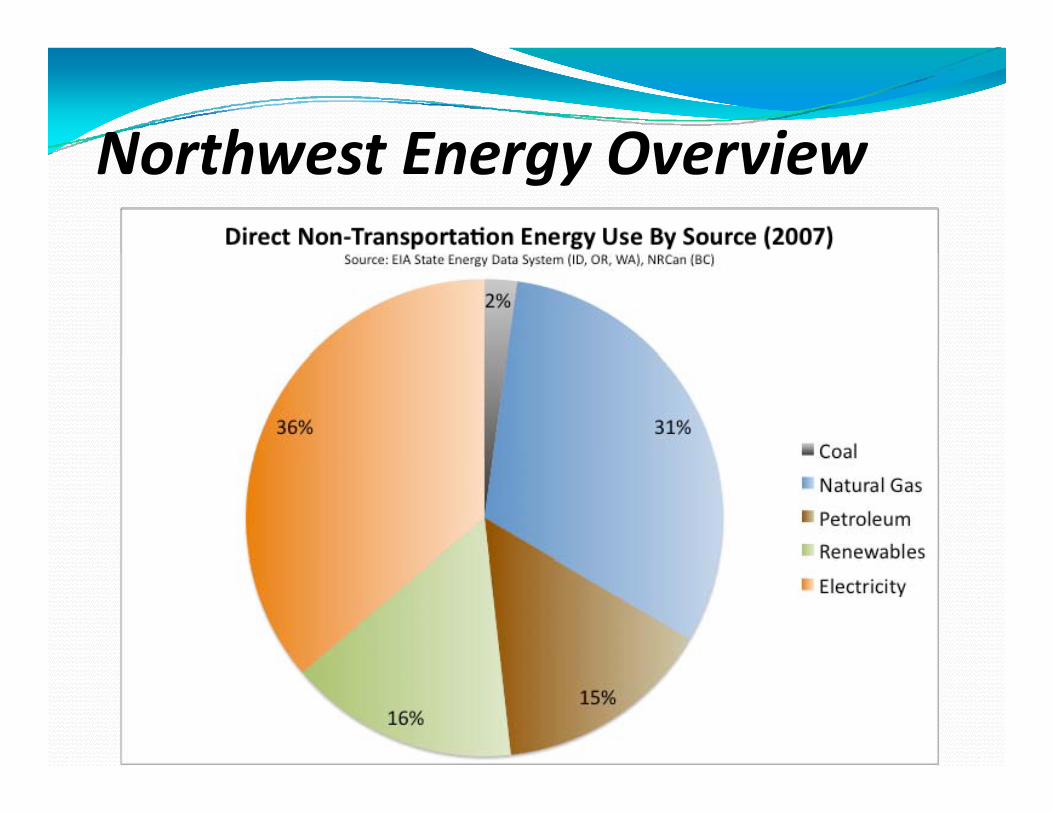

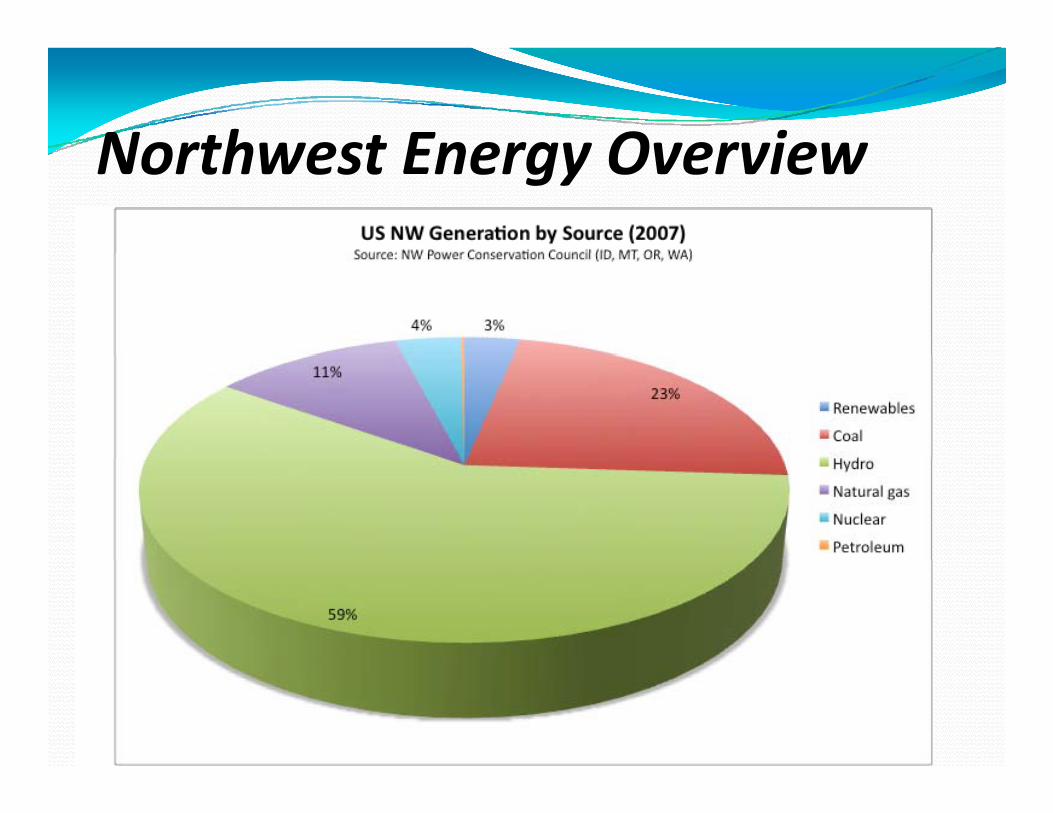

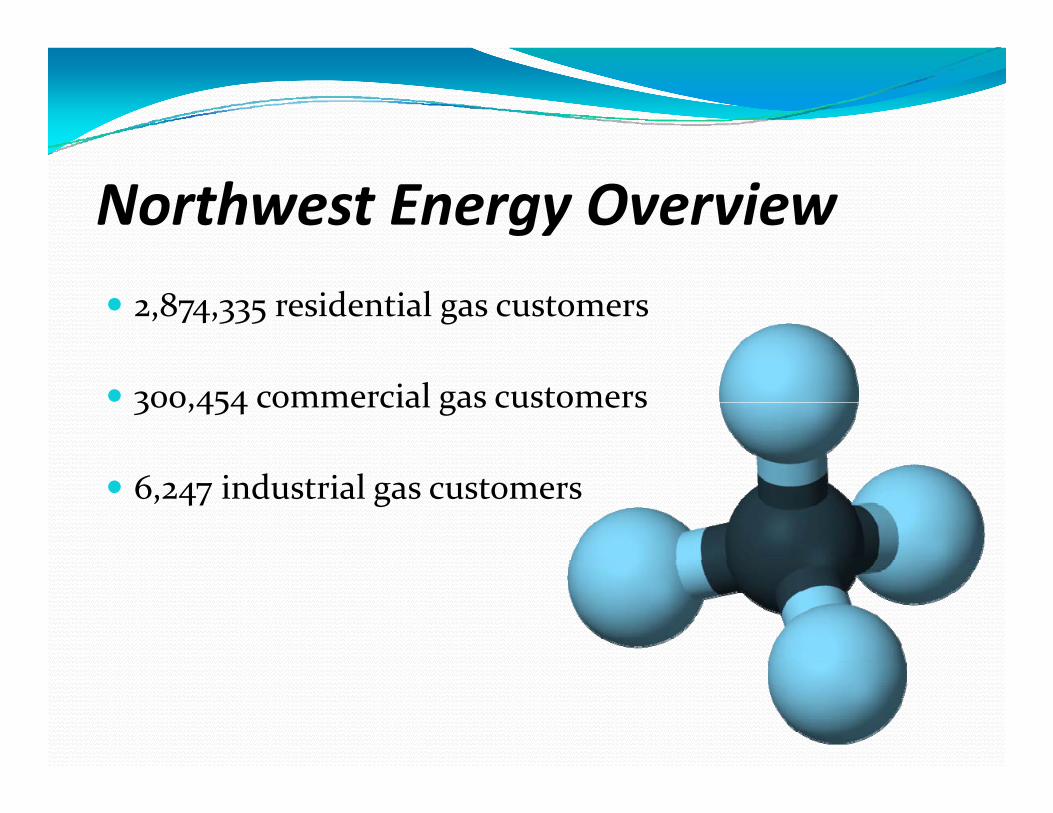

N h E O iNorthwest Energy Overview

Northwest Energy OverviewNorthwest Energy Overview

Northwest Energy OverviewNorthwest Energy Overview

Northwest Energy Overview

2,874,335 residential gas customers

300,454 commercial gas customers

6,247 industrial gas customers

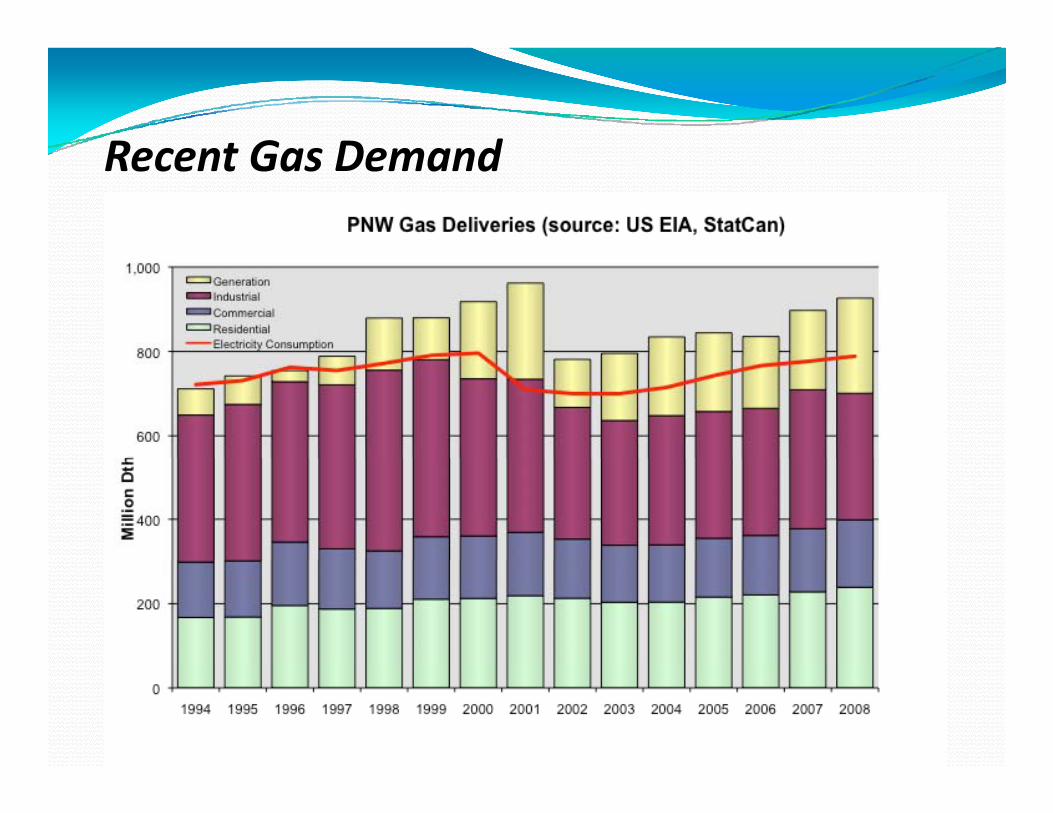

Recent Gas DemandRecent Gas Demand

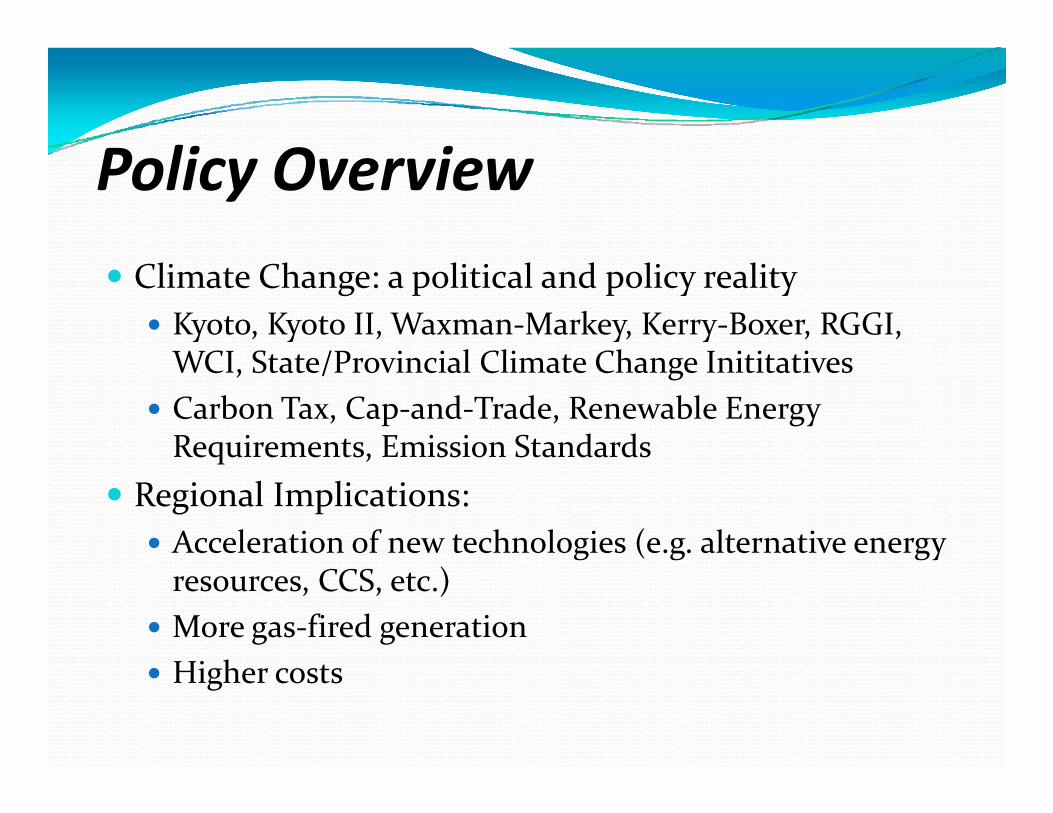

P li O iPolicy Overview

Climate Change: a political and policy reality Kyoto, Kyoto II, Waxman-Markey, Kerry-Boxer, RGGI,

WCI St t /P i i l Cli t Ch I itit tiWCI, State/Provincial Climate Change Inititatives Carbon Tax, Cap-and-Trade, Renewable Energy

Requirements, Emission Standardsq , Regional Implications:

Acceleration of new technologies (e.g. alternative energy resources, CCS, etc.)

More gas-fired generationHi h Higher costs

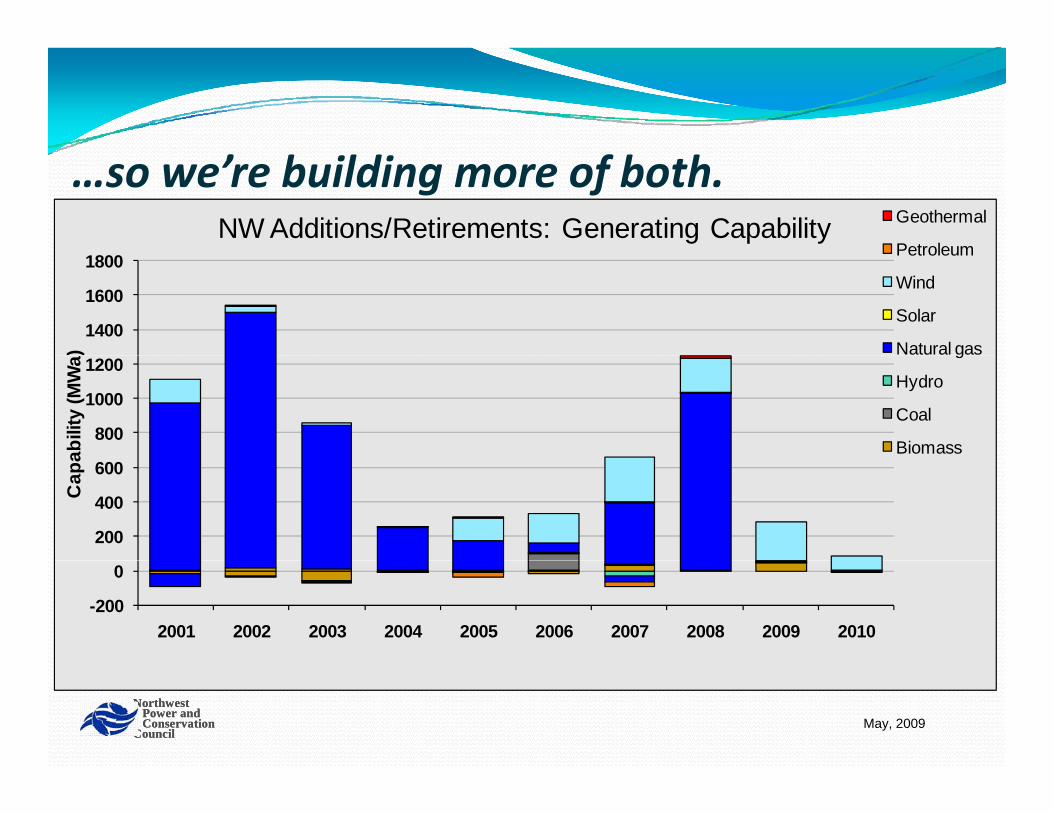

…so we’re building more of both.NW Additions/Retirements: Generating Capability Geothermal

Petroleum

1400

1600

1800

)

Petroleum

Wind

Solar

Natural gas

800

1000

1200

abili

ty (M

Wa g

Hydro

Coal

Biomass

200

400

600

Cap

a

-200

0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

NorthwestPower andConservation

Council

NorthwestPower andConservation

CouncilMay, 2009

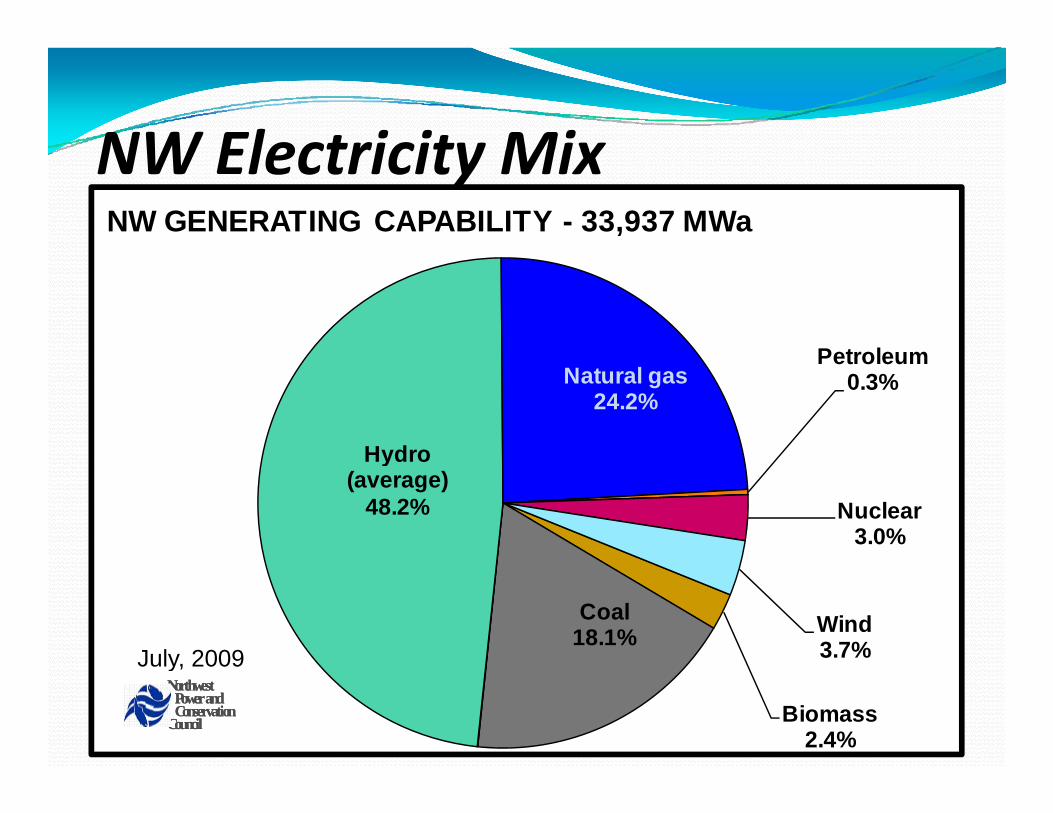

NW Electricity MixNW Electricity MixNW GENERATING CAPABILITY - 33,937 MWa

Petroleum

Hydro

Natural gas24.2%

Petroleum0.3%

Hydro (average)

48.2% Nuclear3.0%

Coal18.1% Wind

3.7%July 2009

Biomass2.4%

NorthwestPower andConservation

Council

NorthwestPower andConservation

Council

July, 2009

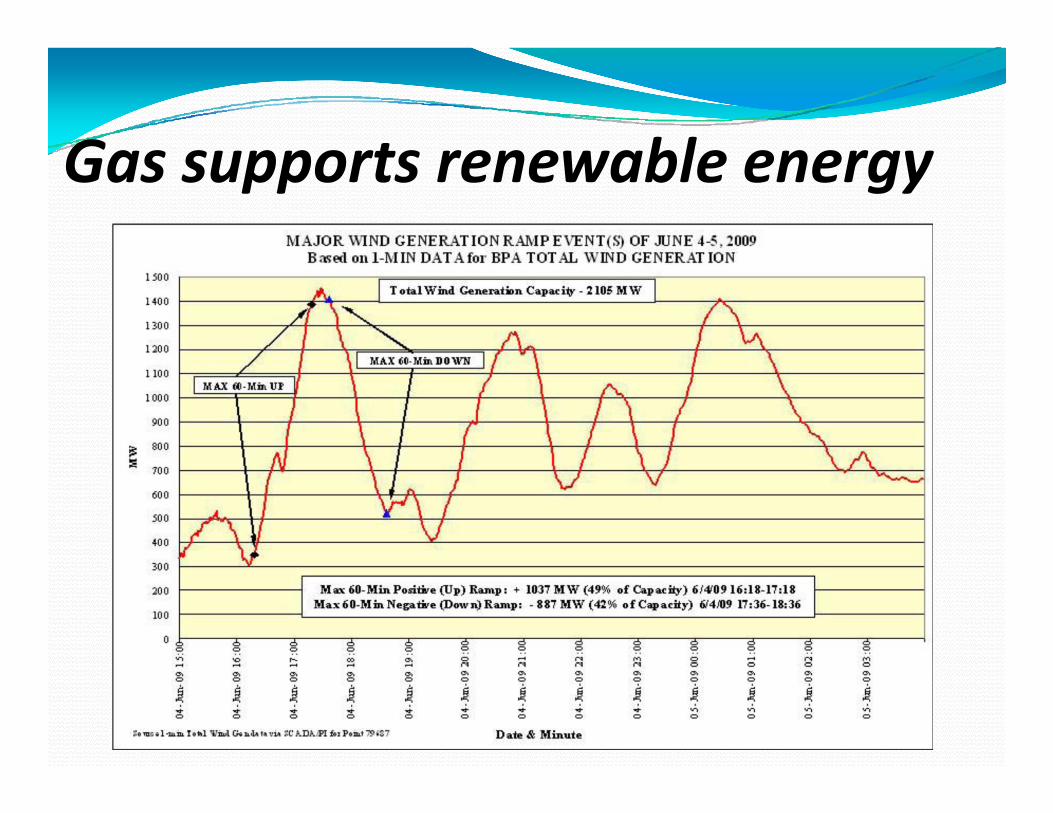

Gas s pports rene able energGas supports renewable energy

More NG Customers Fewer GHG EmissionsMore NG Customers Fewer GHG Emissions

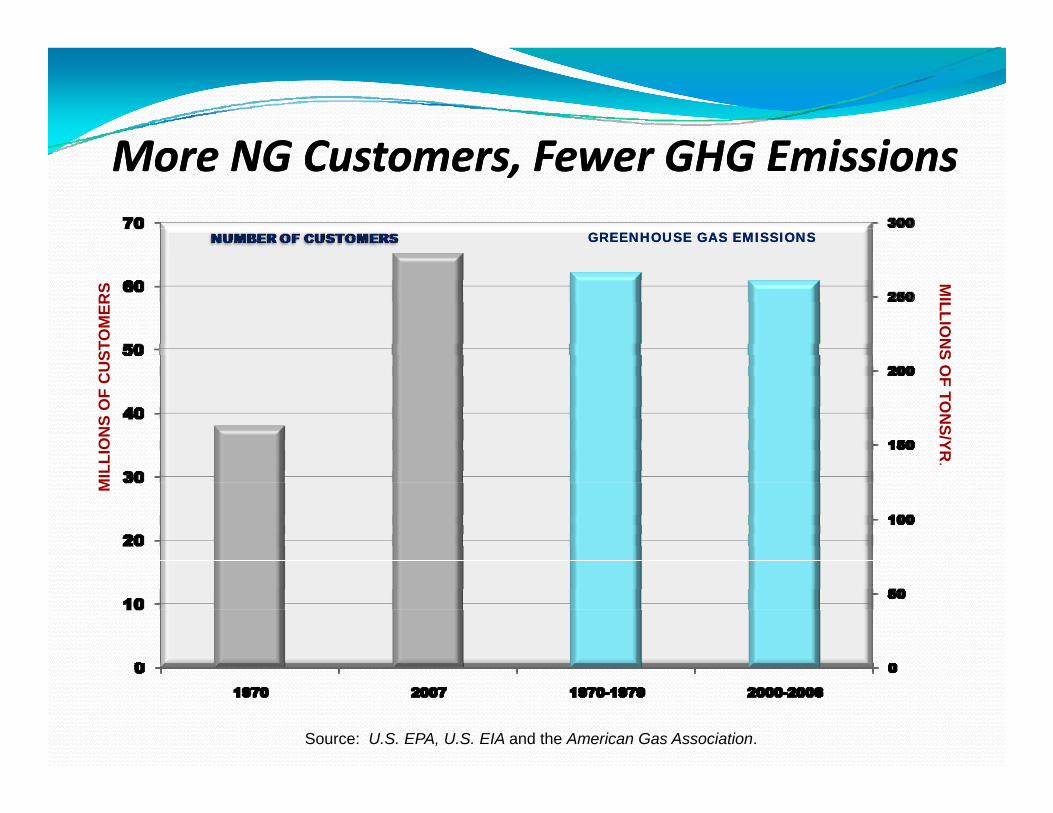

GREENHOUSE GAS EMISSIONSGREENHOUSE GAS EMISSIONS

More NG Customers, Fewer GHG EmissionsMore NG Customers, Fewer GHG EmissionsM

ILLION

SST

OM

ERS

S OF TO

NS/YR

LIO

NS

OF

CU

SR

.M

ILL

Source: U.S. EPA, U.S. EIA and the American Gas Association.

Potential PNW Energy and GHG SavingsPotential PNW Energy and GHG Savings

Natural Gas A Competitive Transportation FuelNatural Gas A Competitive Transportation FuelCompeting Fuel Prices

$30.00Settled prices to January 12, 2010

$22.00

$24.00

$26.00

$28.00 NYMEX PROMPT MONTH LIGHT CRUDE

NYMEX PROMPT MONTH NAT GAS

HEATING OIL#2 - EIA

FUEL OIL 1% - EIA

$16.00

$18.00

$20.00

$ 00

US/

MM

Btu

$8 00

$10.00

$12.00

$14.00$U

$2.00

$4.00

$6.00

$8.00

Jan-03

Apr-03

Jul-0

3Oct-

03Ja

n-04Apr-0

4Ju

l-04

Oct-04

Jan-05

Apr-05

Jul-0

5Oct-

05Ja

n-06Apr-0

6Ju

l-06

Oct-06

Jan-07

Apr-07

Jul-0

7Oct-

07Ja

n-08Apr-0

8Ju

l-08

Oct-08

Jan-09

Apr-09

Jul-0

9Oct-

09Ja

n-10Apr-1

0Ju

l-10

Oct-10

Jan-11

Apr-11

Jul-1

1Oct-

11Ja

n-12Apr-1

2Ju

l-12

Oct-12

Jan-13

Apr-13

Jul-1

3Oct-

13Ja

n-14

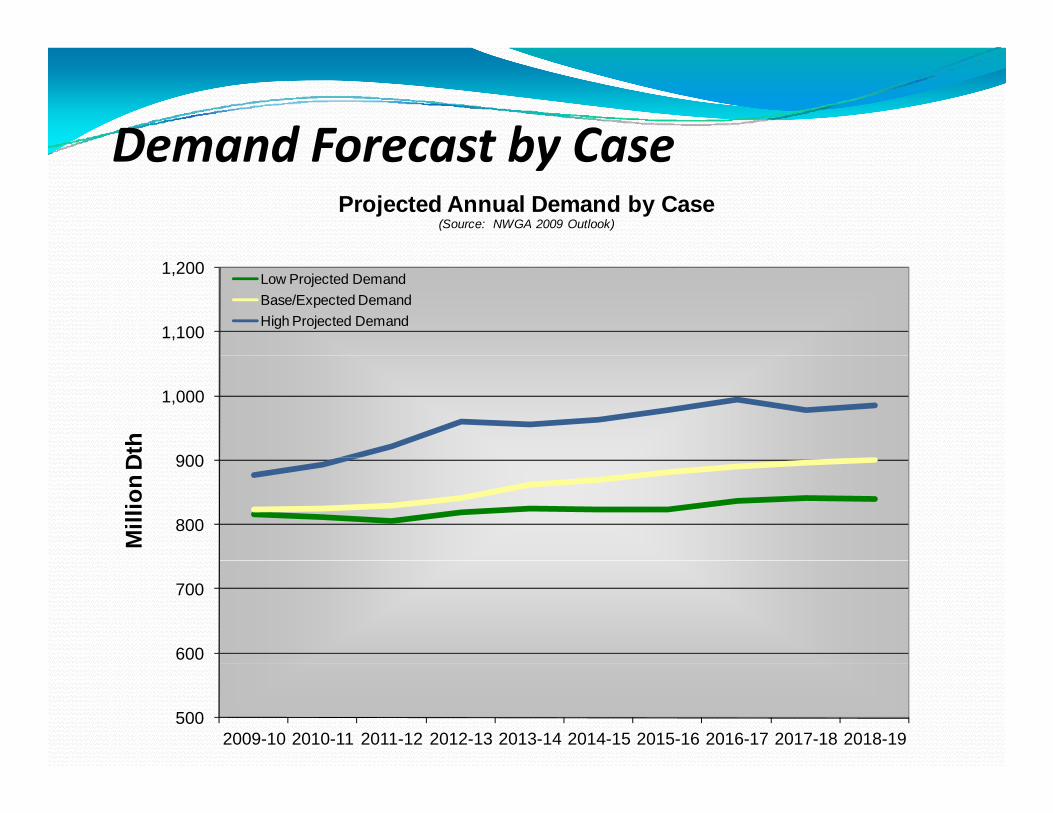

Demand Forecast by CaseDemand Forecast by CaseProjected Annual Demand by Case

(Source: NWGA 2009 Outlook)

1,100

1,200Low Projected DemandBase/Expected DemandHigh Projected Demand

900

1,000

Dth

800

900

Mill

ion

D

600

700

5002009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

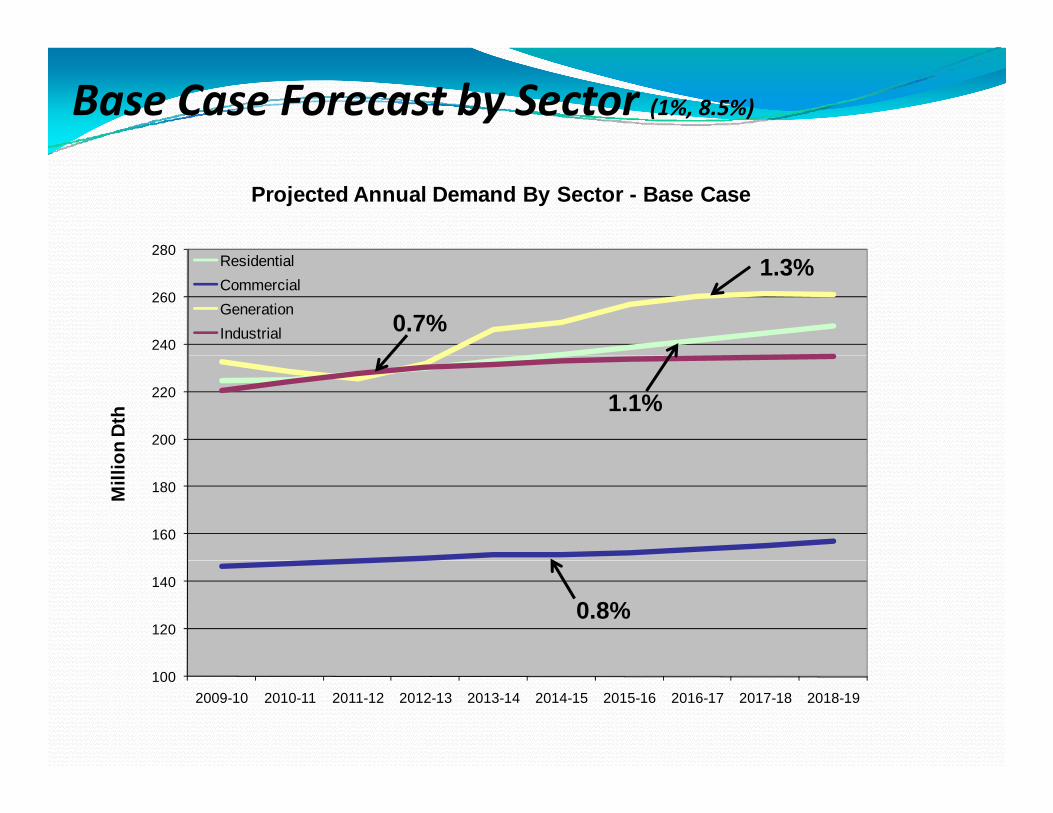

Base Case Forecast by Sector (1%, 8.5%)

280

Projected Annual Demand By Sector - Base Case

240

260

280ResidentialCommercialGenerationIndustrial

1.3%

0.7%

200

220

on D

th 1.1%

160

180Mill

io

120

140

0.8%

1002009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

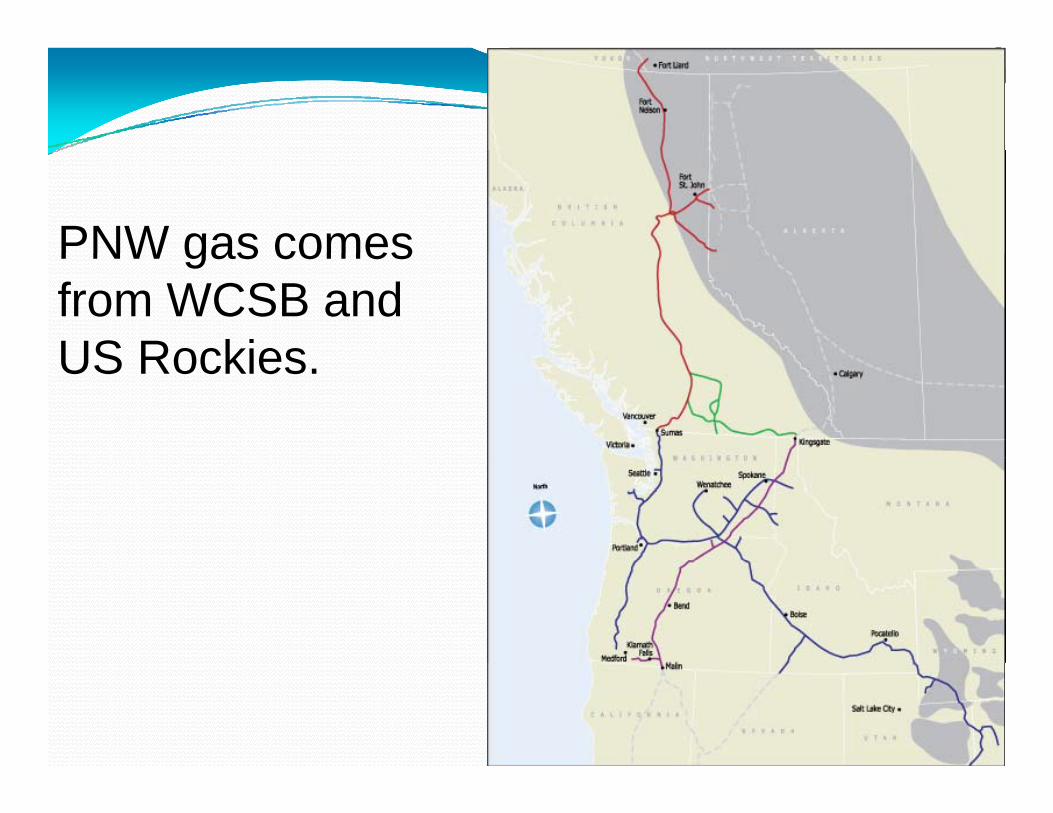

PNW gas comesPNW gas comes from WCSB and US RockiesUS Rockies.

19

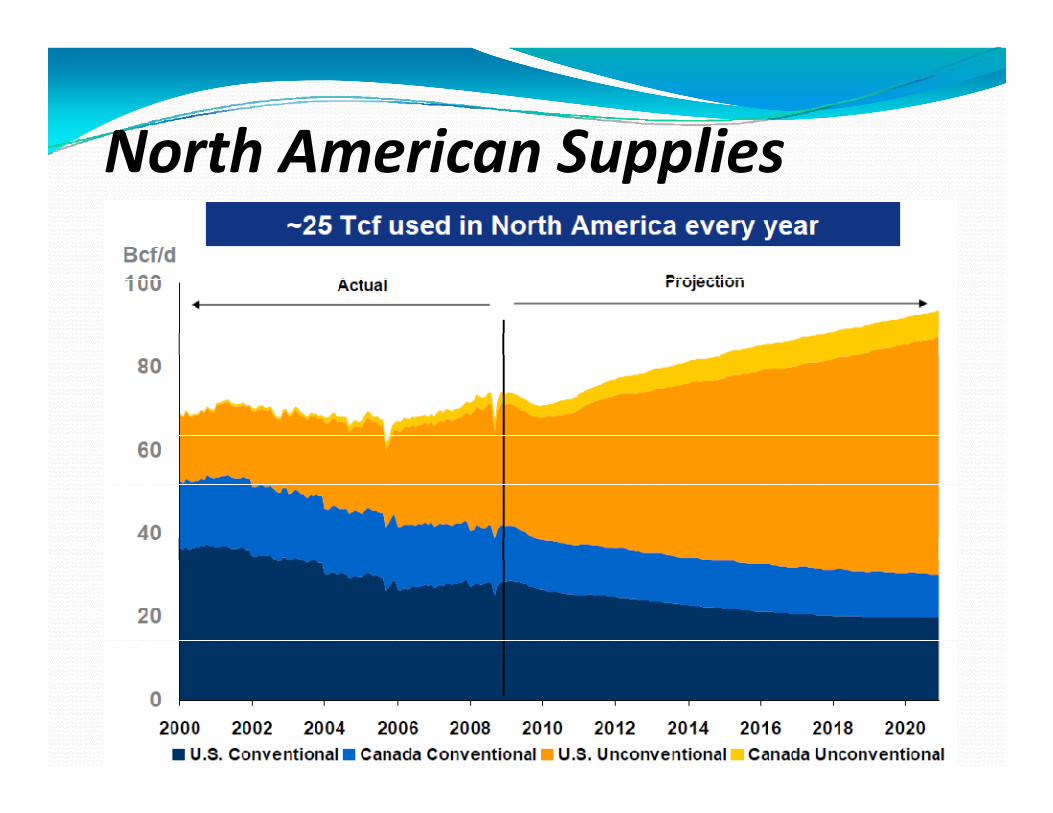

North American SuppliesNorth American Supplies

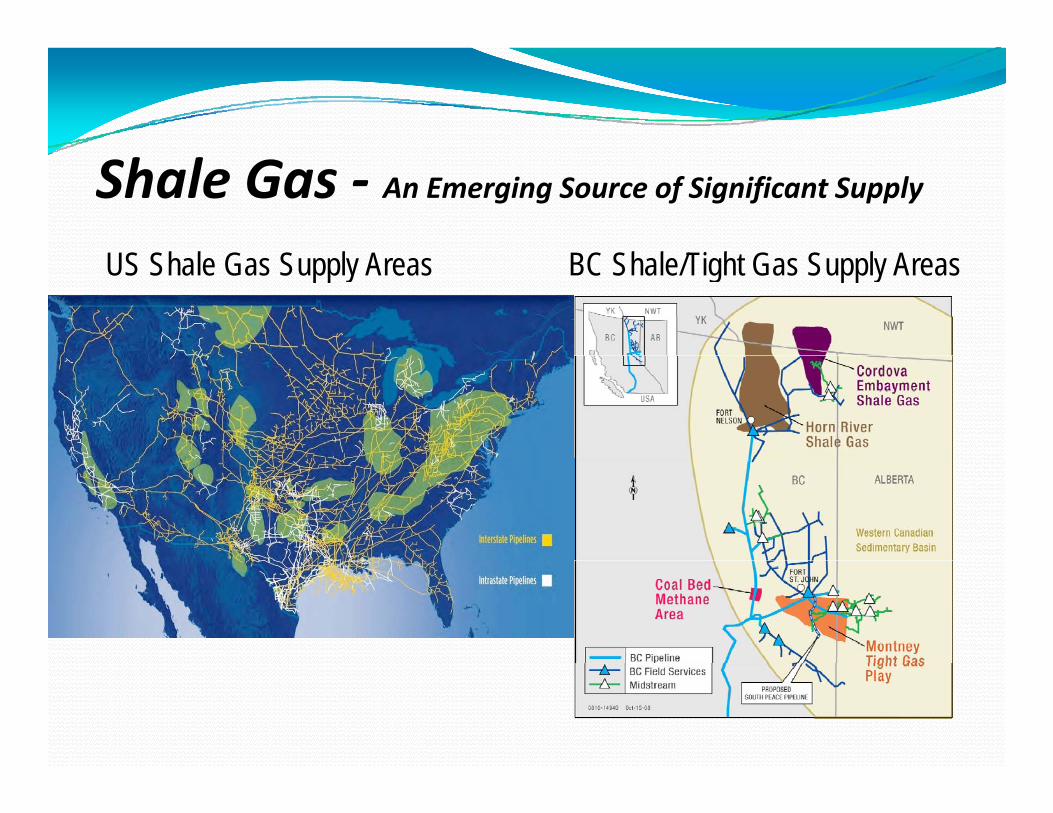

US Sh l G S l A BC Sh l /Ti h G S l A

Shale Gas - An Emerging Source of Significant Supply

US Shale Gas Supply Areas BC Shale/Tight Gas Supply Areas

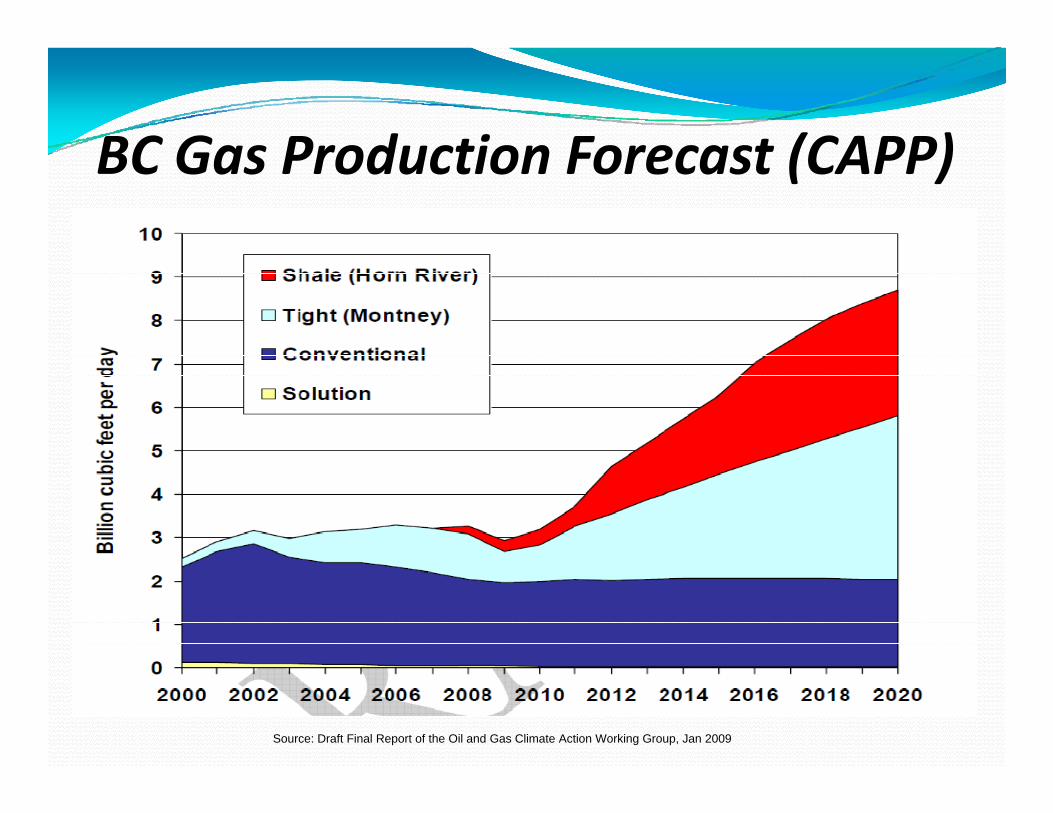

BC Gas Production Forecast (CAPP)BC Gas Production Forecast (CAPP)

Source: Draft Final Report of the Oil and Gas Climate Action Working Group, Jan 2009

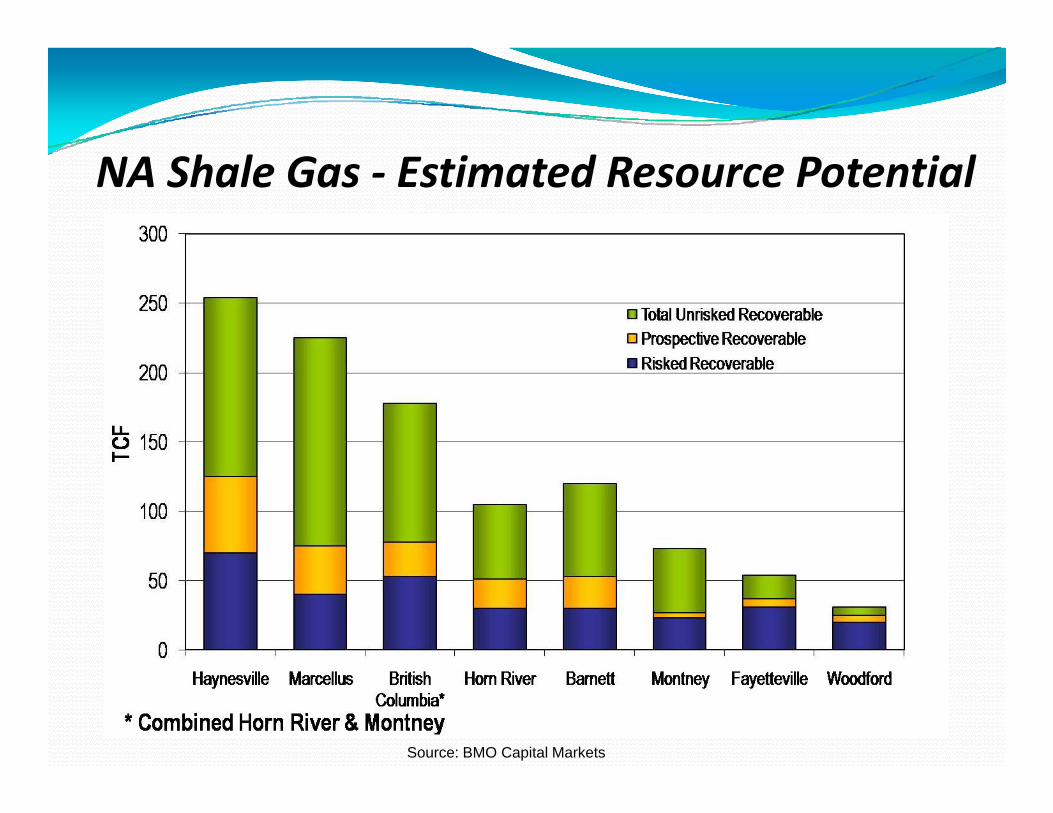

NA Shale Gas - Estimated Resource Potential

Source: BMO Capital Markets

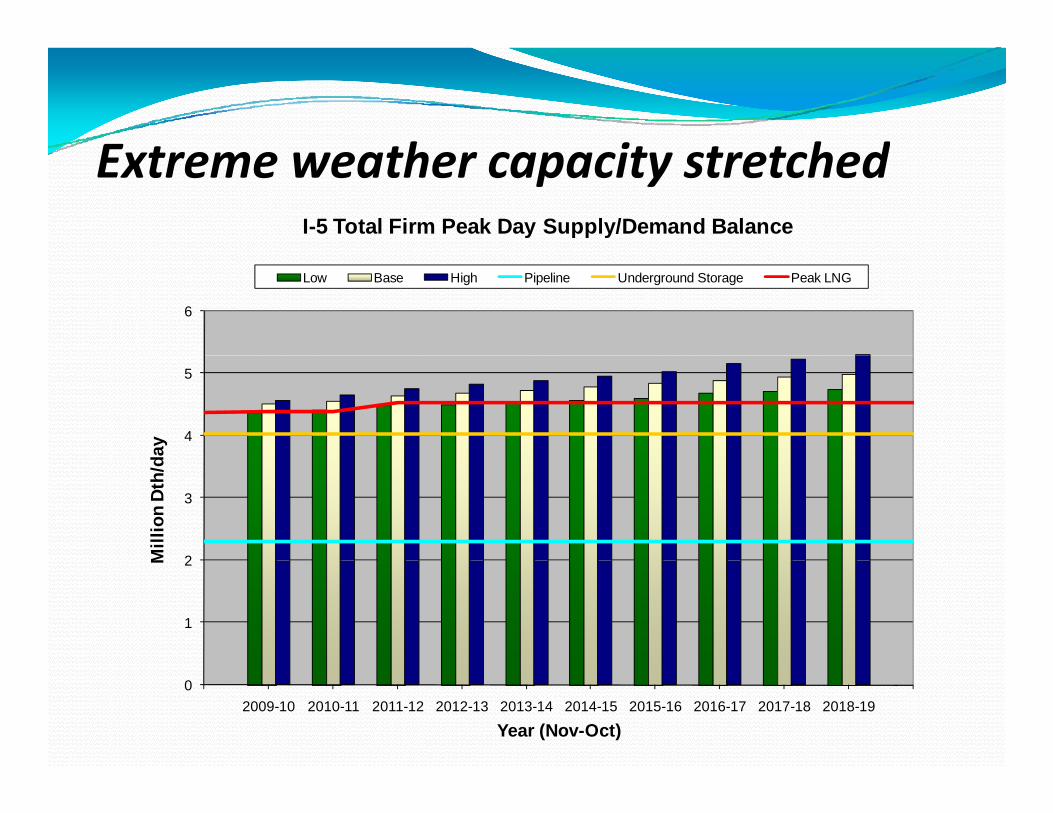

E t th it t t h dExtreme weather capacity stretchedI-5 Total Firm Peak Day Supply/Demand Balance

6

Low Base High Pipeline Underground Storage Peak LNG

4

5

day

2

3

Mill

ion

Dth

/d

1

2M

02009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Year (Nov-Oct)

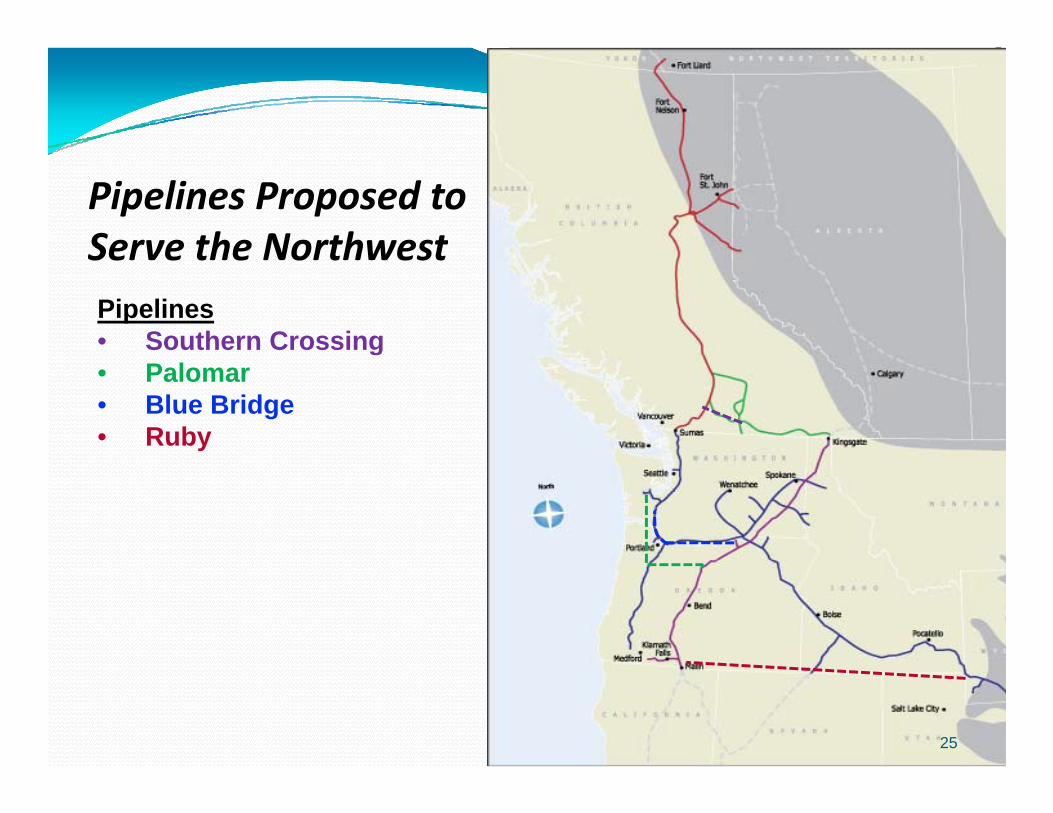

Pipelines Proposed to Serve the NorthwestServe the NorthwestPipelines• Southern Crossing• Palomar• Blue Bridge• Ruby

25

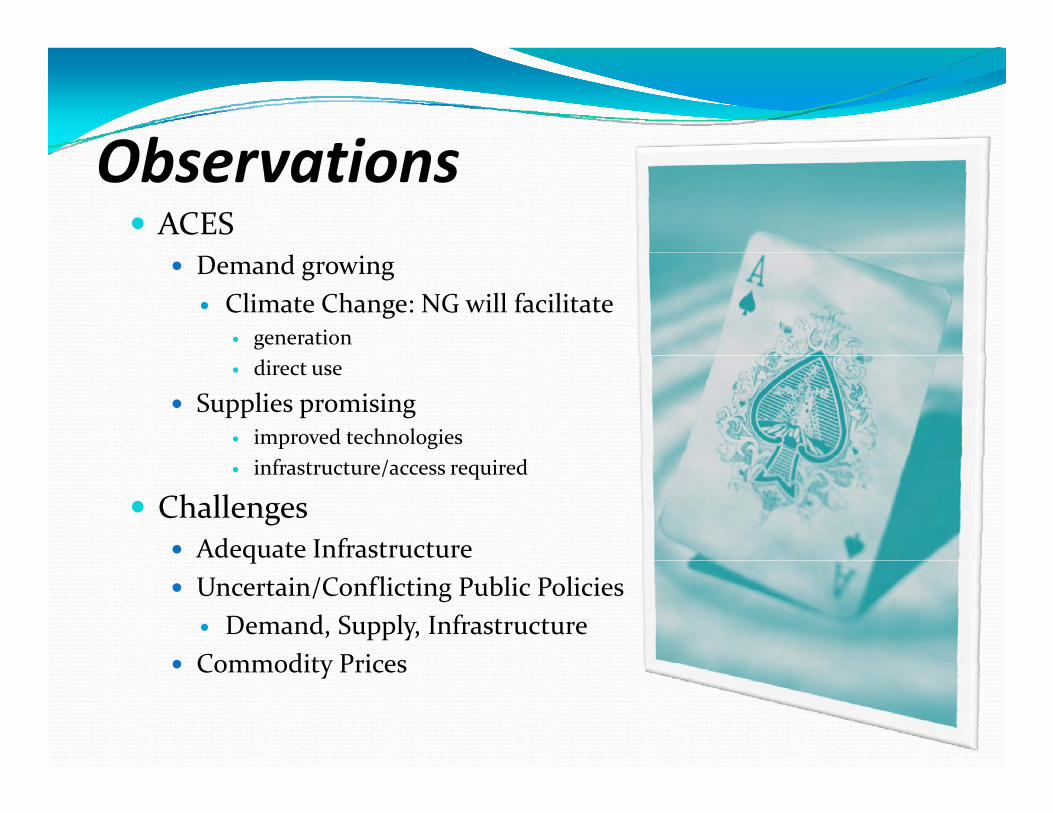

Obser ationsObservations ACES

Demand growing Climate Change: NG will facilitate

generation direct use

Supplies promising improved technologies infrastructure/access required

Challenges Adequate Infrastructureq Uncertain/Conflicting Public Policies

Demand, Supply, Infrastructure Commodity Prices Commodity Prices

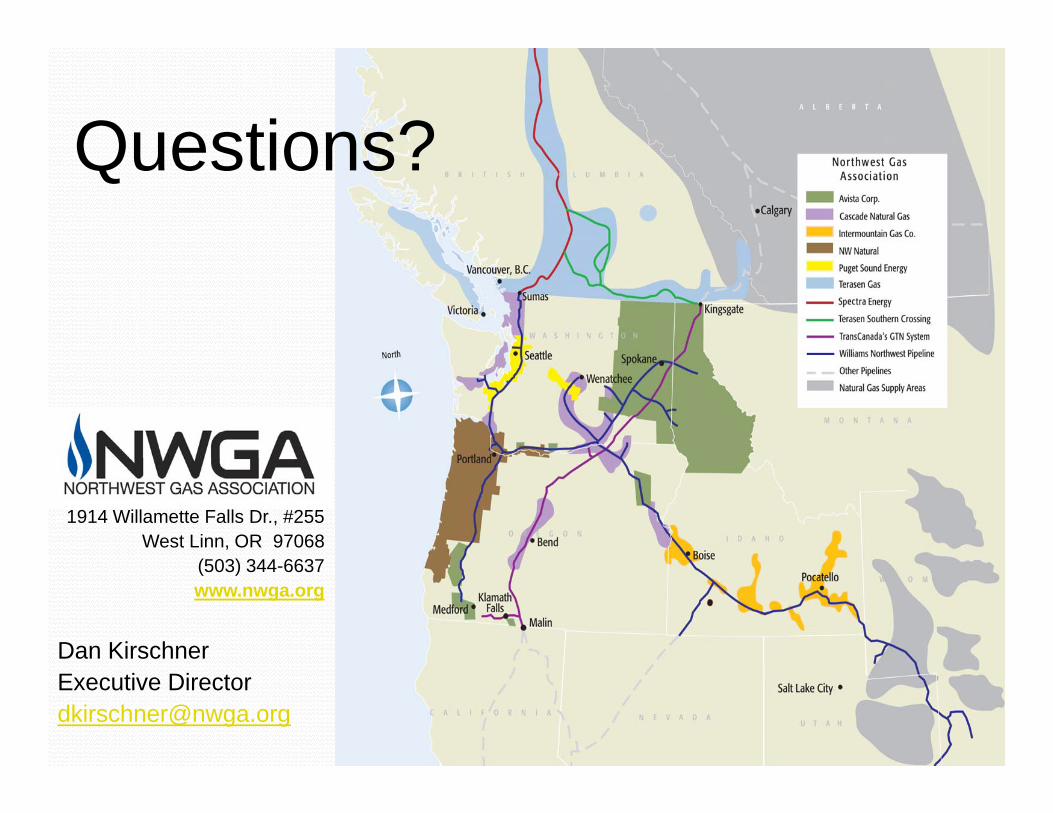

Questions?Questions?

1914 Willamette Falls Dr., #255West Linn, OR 97068

(503) 344 6637(503) 344-6637www.nwga.org

Dan KirschnerExecutive [email protected]