Sporting Nation in the Making - EVENTFAQS Media Nation in the Making Growth & Potential of Sports in...

39

Sporting Nation in the Making Growth & Potential of Sports in India SportzPower-GroupM ESP India Sports Sponsorship Report 2014

Transcript of Sporting Nation in the Making - EVENTFAQS Media Nation in the Making Growth & Potential of Sports in...

SportingNationin the

MakingGrowth & Potential of

Sports in India

SportzPower-GroupM ESP India Sports Sponsorship Report 2014

Sporting Nation in the MakingGrowth & Potential of

Sports in India

SportzPower-GroupM ESP India Sports Sponsorship Report 2014

©Sportz Network Private Limited and GroupM Media India Private Limited

All rights reserved. Copyright of all material in this research report vests with Sportz Network Private Limited and GroupM Media India

Private Limited, and is protected by national and international copyright and trademark laws. The material and contents of this research

report are provided on a non-exclusive, non-commercial, and single-user licence. No part of any of the materials and information made

available in this research report, including, but not restricted to, articles and graphics, can be copied, adapted, abridged, translated or

stored in any retrieval system, computer system, photographic or other system now known or developed in the future, or can be

transmitted in any form by any means whether electronic, mechanical, digital, optical, photographic or otherwise now known or

developed in future, without the prior written permission of the copyright holders – Sportz Network Private Limited and GroupM Media

India Private Limited. Distribution of the material and content for any purposes is prohibited. Any breach will entail legal action and

prosecution to the maximum extent without further notice.

Sportz Network Private Limited

301, Kalash, Sundervan Complex,

Andheri Link Road, Andheri (W),

Mumbai, India – 400 053.

www.sportzpower.com

GroupM Media India Private Limited

8th Floor, Commerz, International Business Park,

Oberoi Garden City, off. Western Express Highway,

Goregaon (East), Mumbai, India – 400 063

facebook.com/GroupM.ESP.India

twitter.com/GroupMESPIndia

Disclaimer: Sportz Network Private Limited and GroupM Media India Private Limited have endeavoured and taken all efforts to provide

the most correct and most reliable information and avoid any kind of mistake in this research report. Sportz Network Private Limited

and GroupM Media India Private Limited do not hold any responsibility for any error that might inadvertently be present in the book.

Sportz Network Private Limited and GroupM Media India Private Limited do not accept any liability whatsoever arising from any form of

inference or conclusion from the information provided in this research report, and Sportz Network Private Limited and GroupM Media

India Private Limited expressly disclaims any liability for direct, indirect, and special losses like loss of profits or loss of business

opportunities or any other kind of losses, and will be free from any liability for damages or losses of any nature arising from or related to

the information in this research report.

Vinit KarnikBusiness Head – GroupM [email protected]

his decade promises to be a

transformational one for Sports in India. TThe triggers are all there. A hungry

spectator base of over a billion people, a dozen

sports television channels beaming sporting

content round the clock, a rapidly growing list of

keen corporates and brands waiting to invest in

emerging cricketing and non-cricketing platforms.

For brands, sports present a highly

impactful and passionate platform, to connect and

engage with trade and consumers. However, there

is very little information and data beyond TV

viewership ratings for brands to evaluate and

leverage the various opportunities available in

sports, which will help them develop brand

marketing strategies and programs.

SportzPower, India's leading provider of

sports business news and knowledge, and GroupM

ESP, the Sports & Entertainment arm of GroupM

Media, have collaborated on an initiative which

seeks to capture and present the trends and

developments in the Indian Sports Industry from

2008 to 2013.

The Report, the first of its kind in India,

documents important events during these eventful

years, including the emergence of league-format

sports in India like the Indian Premier League

(IPL), Hockey India League (HIL), and Indian

Badminton League (IBL).

To increase its utility to Rights Owners,

Advertisers and Agencies, we have divided this

report into four segments – On Ground

Sponsorship, Team Sponsorship, Athlete

Management and On Air.

In recognition of its rising importance as

potentially the biggest sport in India after Cricket,

Football has a dedicated section. With the Under-

17 FIFA World Cup, and the Reliance-Star-IMG

property, the Indian Super League (ISL), in the

pipeline, we believe that the future of Football in

FOREWORD

Thomas AbrahamCo-Founder, SportzPower

India is very bright.

We gratefully acknowledge the valuable

inputs provided by rights owners, agencies and

industry participants who have graciously offered

information and support in preparation of this

report.

We hope that you will find this report

useful and informative. Any feedback or

suggestions to enhance future editions of this

report are most welcome.

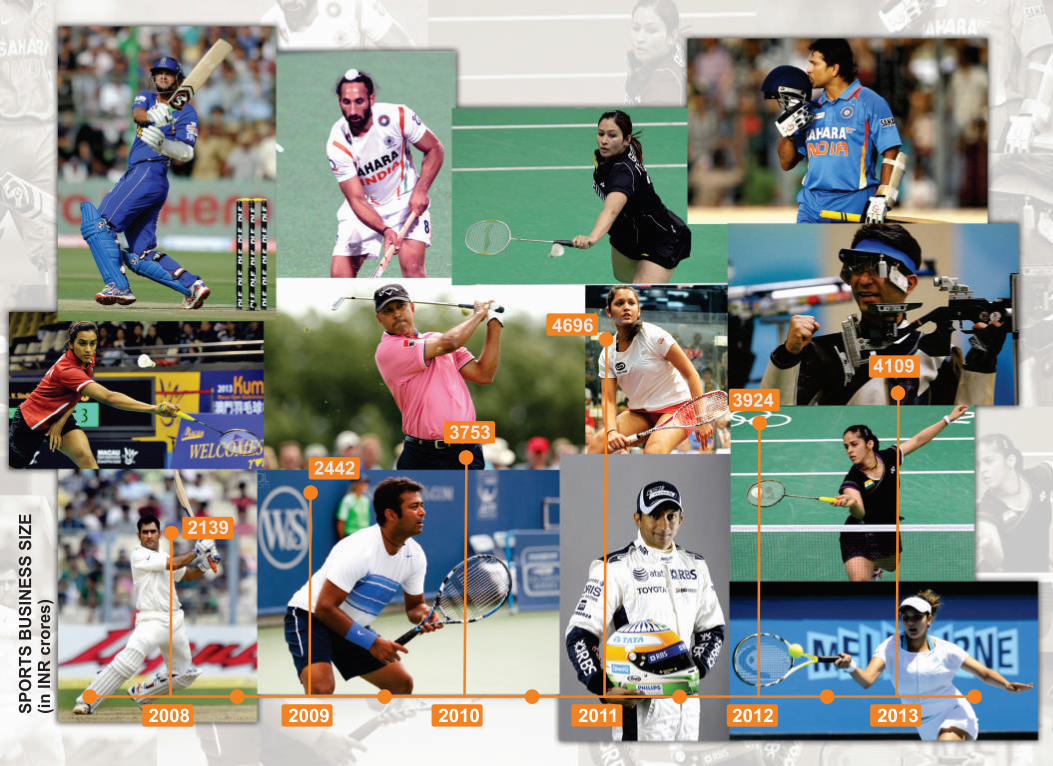

THE TRIGGERS ARE ALL THERE

4696

4109

3924

3753

2442

2139

2008 2009 2010 2011 2012 2013SP

OR

TS

BU

SIN

ES

S S

IZE

(in

IN

R c

rore

s)

The Big Picture

View From The Ground

‘Cricket And Football Will Both Co-exist In Our Marketing Calendar’

Football – A Microcosm Of The Short Non-cricket Tail

‘A Time Of Unrivalled Opportunity For Indian Sports Federations’

‘The Game Changer’

‘Football Is Going To Be Big In India’

Buck Stops At TV

‘Enabling A Paradigm Shift’

Team Sponsorship – All About The Boys In Blue

When It Comes To Talent, Money Chasing Dhoni & Co

‘Other Sports Are Steadily Carving A Niche’

‘Shorter And Newer Formats Key Drivers For Growth’

‘We Are A National Brand And Address Consumers Across Geographies’

Digital Media – Score Big With Early Adoption

On The Front Foot

CONTENTS

. . . . . . . . . 06

. . . . . . . . . 08

. . . . . . . . . 10

. . . . . . . . . 12

. . . . . . . . . 14

. . . . . . . . . 15

. . . . . . . . . 16

. . . . . . . . . 18

. . . . . . . . . 22

. . . . . . . . . 24

. . . . . . . . . 26

. . . . . . . . . 28

. . . . . . . . . 30

. . . . . . . . . 31

. . . . . . . . . 32

. . . . . . . . . 34

06

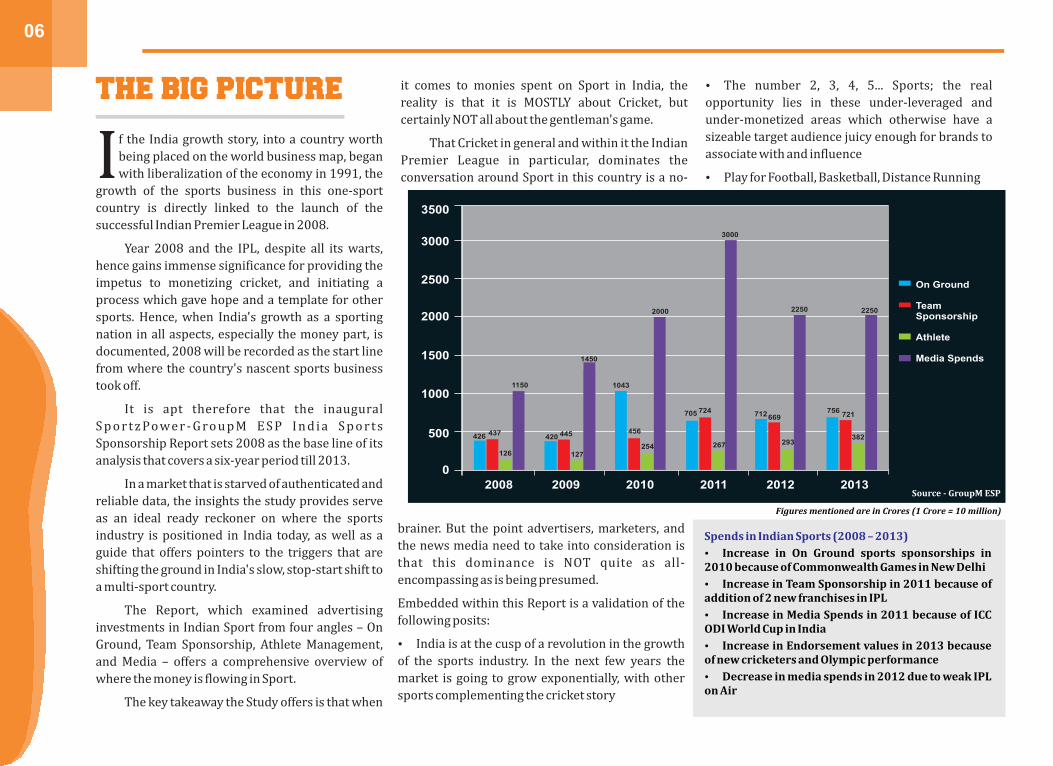

f the India growth story, into a country worth

being placed on the world business map, began Iwith liberalization of the economy in 1991, the

growth of the sports business in this one-sport

country is directly linked to the launch of the

successful Indian Premier League in 2008.

Year 2008 and the IPL, despite all its warts,

hence gains immense significance for providing the

impetus to monetizing cricket, and initiating a

process which gave hope and a template for other

sports. Hence, when India's growth as a sporting

nation in all aspects, especially the money part, is

documented, 2008 will be recorded as the start line

from where the country's nascent sports business

took off.

It is apt therefore that the inaugural

S p o r t z Po we r - G ro u p M E S P I n d i a S p o r t s

Sponsorship Report sets 2008 as the base line of its

analysis that covers a six-year period till 2013.

In a market that is starved of authenticated and

reliable data, the insights the study provides serve

as an ideal ready reckoner on where the sports

industry is positioned in India today, as well as a

guide that offers pointers to the triggers that are

shifting the ground in India's slow, stop-start shift to

a multi-sport country.

The Report, which examined advertising

investments in Indian Sport from four angles – On

Ground, Team Sponsorship, Athlete Management,

and Media – offers a comprehensive overview of

where the money is flowing in Sport.

The key takeaway the Study offers is that when

it comes to monies spent on Sport in India, the

reality is that it is MOSTLY about Cricket, but

certainly NOT all about the gentleman's game.

That Cricket in general and within it the Indian

Premier League in particular, dominates the

conversation around Sport in this country is a no-

THE BIG PICTURE

brainer. But the point advertisers, marketers, and

the news media need to take into consideration is

that this dominance is NOT quite as all-

encompassing as is being presumed.

Embedded within this Report is a validation of the

following posits:

Ÿ India is at the cusp of a revolution in the growth

of the sports industry. In the next few years the

market is going to grow exponentially, with other

sports complementing the cricket story

Figures mentioned are in Crores (1 Crore = 10 million)

Spends in Indian Sports (2008 – 2013)

Ÿ Increase in On Ground sports sponsorships in 2010 because of Commonwealth Games in New Delhi

Ÿ Increase in Team Sponsorship in 2011 because of addition of 2 new franchises in IPL

Ÿ Increase in Media Spends in 2011 because of ICC ODI World Cup in India

Ÿ Increase in Endorsement values in 2013 because of new cricketers and Olympic performance

Ÿ Decrease in media spends in 2012 due to weak IPL on Air

Ÿ The number 2, 3, 4, 5... Sports; the real

opportunity lies in these under-leveraged and

under-monetized areas which otherwise have a

sizeable target audience juicy enough for brands to

associate with and influence

Ÿ Play for Football, Basketball, Distance Running

0

500

1000

1500

2000

2500

3000

3500

2008 2009 2010 2011 2012 2013

1150

437426

126

420 445

127

1450

1043

456

254

2000

705 724

267

3000

2250

712 669

293

2250

756 721

382

On Ground

Team Sponsorship

Athlete

Media Spends

Source - GroupM ESP

07

Ÿ Close on their heels are Golf, Motorsports,

Tennis, Hockey, Badminton, Contact Sports

It should serve as a wake-up call for all

stakeholders in the Sports sector that in the six-year

time frame that the Study covers, the highest share

of On Ground revenue Cricket has commanded in

percentage terms was in 2009 – all of 79%. And the

lowest? It was just 52% in 2010, which was also the

year when New Delhi hosted the Commonwealth

Games.

On Ground sponsorship has a direct linkage to

stadium attendance. And therefore reflects active

fan engagement. What this shows is that in the IPL

era, it takes an event the size of the Commonwealth

Games to significantly shift the needle.

But that is not to say that the ground is not

shifting as far as other sports are concerned. In

2012, the share of non-cricket On Ground

sponsorship stood at 34.5%, dipping to 32.8% in

2013, ironically a year that saw the launch of two

new IPL-style tournaments – the Hockey India

League as well as the Indian Badminton League.

It is true that Sport still has a long and winding

road to traverse from being a peripheral element of

mass consciousness and entertainment to being a

big part of it in the manner that, say, movies are. It

certainly was, and to a significant extent still is, also

true that with the honorable exception of cricket,

sport just does not matter that much.

But it is also true that between 2008, when IPL

first burst onto India's consciousness and shook

everything up, and 2013, advertising investments in

Indian Sport – On Ground, Team Sponsorship,

Athlete Management, and Media – rose roughly two-

fold.

Ÿ Total spend rose 92 per cent to Rs 41.1 billion in

2013 from Rs 21.39 billion in 2008

Ÿ Media spends touched a high of Rs 30 billion in

2011, the year when India hosted (and won) ICC's

ODI World Cup

08

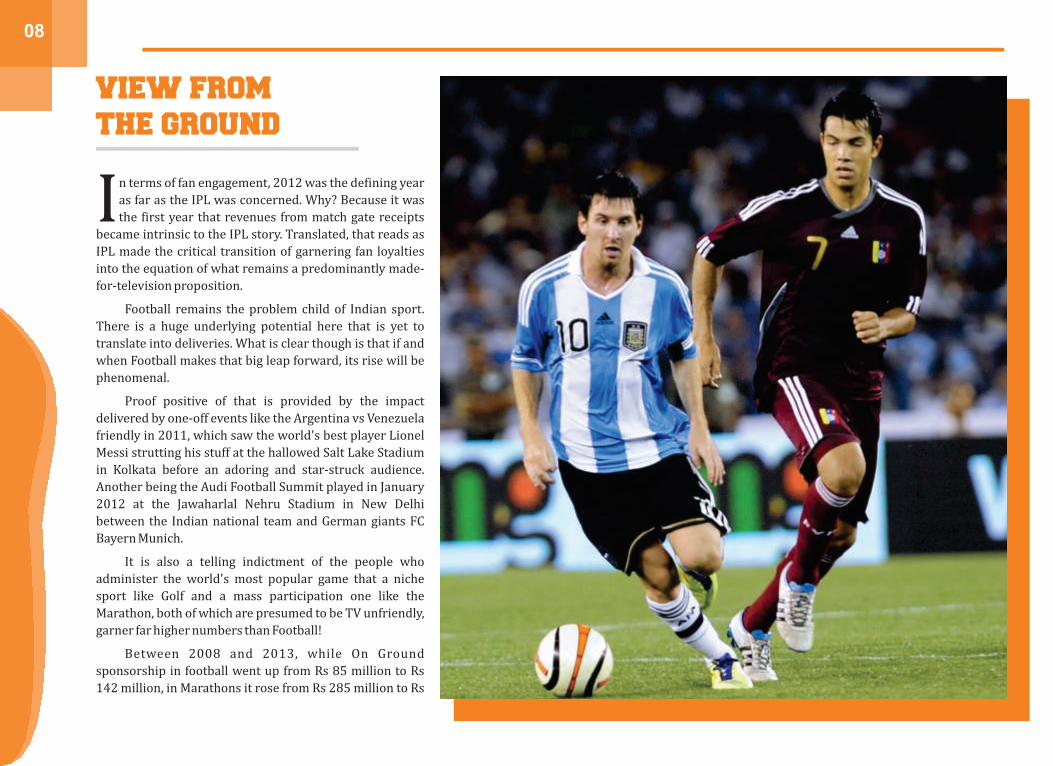

n terms of fan engagement, 2012 was the defining year

as far as the IPL was concerned. Why? Because it was Ithe first year that revenues from match gate receipts

became intrinsic to the IPL story. Translated, that reads as

IPL made the critical transition of garnering fan loyalties

into the equation of what remains a predominantly made-

for-television proposition.

Football remains the problem child of Indian sport.

There is a huge underlying potential here that is yet to

translate into deliveries. What is clear though is that if and

when Football makes that big leap forward, its rise will be

phenomenal.

Proof positive of that is provided by the impact

delivered by one-off events like the Argentina vs Venezuela

friendly in 2011, which saw the world's best player Lionel

Messi strutting his stuff at the hallowed Salt Lake Stadium

in Kolkata before an adoring and star-struck audience.

Another being the Audi Football Summit played in January

2012 at the Jawaharlal Nehru Stadium in New Delhi

between the Indian national team and German giants FC

Bayern Munich.

It is also a telling indictment of the people who

administer the world's most popular game that a niche

sport like Golf and a mass participation one like the

Marathon, both of which are presumed to be TV unfriendly,

garner far higher numbers than Football!

Between 2008 and 2013, while On Ground

sponsorship in football went up from Rs 85 million to Rs

142 million, in Marathons it rose from Rs 285 million to Rs

VIEW FROM

THE GROUND

09

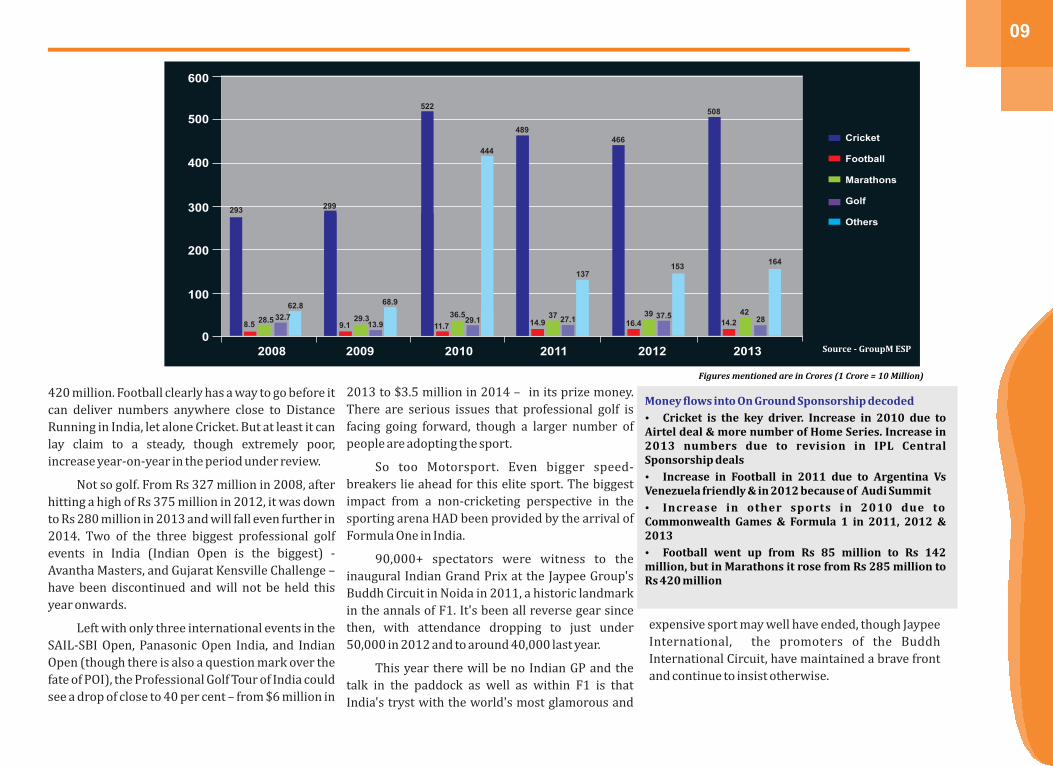

420 million. Football clearly has a way to go before it

can deliver numbers anywhere close to Distance

Running in India, let alone Cricket. But at least it can

lay claim to a steady, though extremely poor,

increase year-on-year in the period under review.

Not so golf. From Rs 327 million in 2008, after

hitting a high of Rs 375 million in 2012, it was down

to Rs 280 million in 2013 and will fall even further in

2014. Two of the three biggest professional golf

events in India (Indian Open is the biggest) -

Avantha Masters, and Gujarat Kensville Challenge –

have been discontinued and will not be held this

year onwards.

Left with only three international events in the

SAIL-SBI Open, Panasonic Open India, and Indian

Open (though there is also a question mark over the

fate of POI), the Professional Golf Tour of India could

see a drop of close to 40 per cent – from $6 million in

Figures mentioned are in Crores (1 Crore = 10 Million)

Money flows into On Ground Sponsorship decoded

Ÿ Cricket is the key driver. Increase in 2010 due to Airtel deal & more number of Home Series. Increase in 2013 numbers due to revision in IPL Central Sponsorship deals

Ÿ Increase in Football in 2011 due to Argentina Vs Venezuela friendly & in 2012 because of Audi Summit

Ÿ Increase in other sports in 2010 due to Commonwealth Games & Formula 1 in 2011, 2012 & 2013

Ÿ Football went up from Rs 85 million to Rs 142 million, but in Marathons it rose from Rs 285 million to Rs 420 million

2013 to $3.5 million in 2014 – in its prize money.

There are serious issues that professional golf is

facing going forward, though a larger number of

people are adopting the sport.

So too Motorsport. Even bigger speed-

breakers lie ahead for this elite sport. The biggest

impact from a non-cricketing perspective in the

sporting arena HAD been provided by the arrival of

Formula One in India.

90,000+ spectators were witness to the

inaugural Indian Grand Prix at the Jaypee Group's

Buddh Circuit in Noida in 2011, a historic landmark

in the annals of F1. It's been all reverse gear since

then, with attendance dropping to just under

50,000 in 2012 and to around 40,000 last year.

This year there will be no Indian GP and the

talk in the paddock as well as within F1 is that

India's tryst with the world's most glamorous and

expensive sport may well have ended, though Jaypee

International, the promoters of the Buddh

International Circuit, have maintained a brave front

and continue to insist otherwise.

Cricket

Football

Marathons

Golf

Others

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013

293

62.8

32.7 28.58.5

299

9.129.3

13.9

68.9

522

11.7

36.5 29.1

444

489

137

37 27.114.9

466

153

39 37.5 16.4

508

14.2

42

28

164

Source - GroupM ESP

10

Homi BattiwallaEVP, Pepsico India

hat are the main factors that come

into play for your company while Wchoosing a sport, event or team for

sponsorship?

For a youth brand like ours, it's imperative to

always have a thinking cap on. We continuously

evaluate interesting properties to leverage brand

Pepsi's proposition. Our efforts are not only

towards being relevant to what the Gen X is

expecting from Pepsi, but also identify emerging

trends ahead of time and incorporate these

insights into our campaigns. Being a true youth

soul mate, Pepsi has always taken the lead in

celebrating newer and emerging youth passions –

cricket, movies, music and football too. The brand

has successfully created memorable campaigns

and experiences for the youth today.

It is said that sponsoring a sport might lead to

alienation of fans from other sports. Is that an

important criterion to be considered? How

does a company like yours, which deals with

different target audiences, manage this factor?

I don't agree with you here. Cricket is a sport

which Pepsi has been associated with for close to

two decades; and when we launched our first ever

football campaign in the country in 2011, it didn't

mean that we were alienating ourselves from

cricket. For us at brand Pepsi, cricket is one of the

strongest youth platforms only after Bollywood,

and football is emerging in India like never before.

We are proud to be associated with both sporting

platforms and going forward, cricket and football

will both co-exist in our marketing calendar.

It is said that in sponsorship it is not what you

have bought, but what you do with it.

Activation around a property can be much

more expensive and stretch limited time and

resources available with the organization.

What kind of budgets would go into such

activities? Please give examples of some

cutting-edge activation that has been

undertaken by your company in the sports

space.

For us at Pepsi, we don't associate with a youth

platform for a short time. We believe in long-

standing strong associations that spread over

years. Take cricket and Bollywood for example. We

have been associated with these youth passions

for years now and have always launched path-

breaking campaigns to bring this alive. From

CRICKET AND FOOTBALL WILL BOTH

CO-EXIST IN OUR MARKETING CALENDAR

11

biggest supporters of the game of cricket. With the

successful bidding, we have reaffirmed our

passion and commitment to this sport.

To add further, we also believe that no large scale

association with cricket is possible in India

without a sizeable IPL presence. IPL – the biggest

cricket event in the subcontinent – has now

become the new face of Indian cricket which

combines the best of cricket with entertainment,

regional club passion, and international glamour.

Now, with this association we hope to catapult

brand Pepsi to an even higher orbit as the most

universal, popular, trend-setting youth brand. The

title association of Pepsi IPL and other benefits

will allow brand Pepsi and other PepsiCo brands

to gain more than conventional sponsorship

benefits and generate immense universality across

the country.

Pepsi has been associated with the sport for close

to two decades now and is known for its

memorable and path-breaking campaigns. Apart

campaigns such as Yehi Hai Right Choice Baby,

Nothing Official About it, Yeh Dil Mange More,

Change the Game all have a strong recall in the

mind of the consumers.

What methodologies are utilized to measure

the exposure for the brand and success of the

sponsorship to justify the ROI?

To measure the success of any campaign, tangible

as well as intangible tools are available to

marketers. We continuously evaluate our

campaigns through a combination of each of these

tools. We have in place regular tracking tools

which are run by renowned research agencies like

Nielsen/IMRB that help us quantify the impact of

sponsorship on Brand Salience, Equity and share

movements by triangulating media inputs.

Separately we also use statistical modeling to

triangulate Spends vs Impact to assess ROI.

Pepsi taking the IPL title rights has been a

huge brand lift for the IPL. But it also surprised

market watchers in that there was a thought

doing the rounds that it would be a brand

needing to build a national brand recall as well

as presence that was likely to bid for the rights.

Pepsi as well as the second-highest bidder

Airtel already has/had that. So what were the

key reasons in making an investment

commitment that was twice the existing deal

value?

We are delighted that we have succeeded in

rebranding the tournament as Pepsi-IPL, thus

cementing a five-year partnership between two

brands which enjoy an iconic status not only in

India but globally. With our continuing

sponsorship of the ICC World Cup, we are now the

from Bollywood, cricket is the single largest youth

passion in the country and we are confident that

Pepsi IPL will give us a multiplier higher than our

investment. Our belief is reinstated due to three

reasons:

Ÿ History of Cricket & IPL association –

Historically, we have gained tremendously through

cricket / IPL association, both in terms of cost per

rating point (CPRP) and the benefits for the

brands we have been able to derive from the

broadcaster. Pepsi and cricket are synonymous

with each other and the same echoes through

consumer feedback on our campaigns over the

years

Ÿ Long-term strategic investment – We see this

investment as a long-term strategic fit spread over

a five-year horizon, which will get better every

year as we go about activating this property in

partnership with brand IPL. We realize the power

of being a 'title sponsor' and are confident to

derive 5-6 times value for the investment we have

made

Ÿ Right timing – The timing of the tournament is

ideal given that packaged beverages is an impulse

category and nearly 50% of consumption happens

in these months

As the IPL title rights holder till 2017, how

much of a bearing will the move have on

Pepsi's battle with Coke for leadership in the

Indian market?

Our contract with IPL has very strong anti-ambush

marketing clauses. As title sponsor, we will also

strengthen our associations across all aspects of

IPL, including franchise partnerships.

12

FOOTBALL -A MICROCOSM OFTHE SHORTNON-CRICKET TAIL

hat is Real Madrid worth? According to a

report put out in April 2013 by Forbes Wmagazine, which placed the Spanish

giants at the top of the heap in 2012 among football

teams across the globe, it is $3.3 billion! And what

was the sum total of On Ground sponsorship monies

that Indian football attracted in the 2012 calendar

year? All of Rs 164.5 million ($3.05 million at

exchange rates prevailing then)!

Please note, though, that this was still almost

twice what the Beautiful Game garnered four years

earlier in 2008, where ground sponsorships stood

at a miserable Rs 89.5 million.

This in a country that has the history – Durand

Cup dates back to 1888, Rovers Cup to 1891, and IFA

Shield to 1893 – that has the population, and that

has enough young people playing as well as

watching the game.

So where is the problem? There is no critical

mass of young people watching Indian football,

either at club level or the national team, is the

straight answer.

Nothing new here and not something that has

not already been much lamented upon. The million-

dollar question is really whether that can change?

Yes, but...

The YES part first.

FIFA president Sepp Blatter has described

India as football's "sleeping giant", alluding to the

potential for growth that a country of 1.2 billion

holds. It is this potential that the game's global

governing body was looking at when it exhorted

India to go the extra mile to ensure that it got

hosting rights for the 2017 Under-17 World Cup.

And it is this potential that ensured FIFA itself

went the extra mile while granting India the right to

host the U-17 World Cup. And with it, one of the

major 'buts' will perforce be fast-tracked towards

resolution, which is infrastructure development.

With India given the mandate to host the U-17

World Cup, also come guarantees from the host

centres of stadiums that are world class. And

because this tournament is not the World Cup, fears

that there will be a lot of white elephants a la South

Africa will not arise. Upgrading existing facilities is

what is being envisioned. Capacity that is being

talked about is for 15,000 seating and under, which

is actually what club football in India requires,

considering the stage it is in at the moment.

FIFA awarding India the rights to host the 2017

edition of the event means not just major

infrastructural advances for the game in India, but

also a massive push for youth and grassroots

development of football, the bedrock upon which

the sport can really build a story going forward.

And the BUT part…

All stadiums in the country are either owned

by state or local municipal corporations, leaving

football officials at the mercy of bureaucracies and

political dispensations with a vested interest in

maintaining status quo, and by extension little

interest in improving facilities.

Coming back to the sponsorship front, the

money coming into the game may have gone up but

it is a poor advertisement for the game that the

national team today has no shirt sponsor after

consumer electronics giant Panasonic declined to

renew after the contract expired in December 2012,

though the upside is that that the I-League now has

a title sponsor in telecom company Airtel after a

fairly long gap.

It is ironic that institutional side ONGC, the

league's title rights-holder for many years, is out of

the I-League after the All India Football Federation

(AIFF) decreed that the team needs a separate

holding company if it was to continue in the top

flight of Indian football.

On the flip side, a big positive in 2013 of course

was the induction of the JSW Steel-owned

Bengaluru FC into the I-League. The impact of the

entry of the corporate entity into India's top tier of

club football has been immediate, what with the

new team sitting at the top of the I-League table on

points going into the winter break in what is but its

inaugural season. Whether it will ultimately be

crowned I-League champions remains to be seen,

that it will be in contention for top honors is a

certainty.

As already pointed out, there is money coming

into the game, and multiple grassroots initiatives

cropping up across the country, as various players

13

big and small look to leverage the potential that

football offers.

The biggest deal of course being the agreement

the AIFF signed in late 2010 with IMG Reliance

(IMG-R), an equal joint venture between the world's

biggest sports management company and India's

richest corporate.

The agreement, valued at Rs 7 billion ($140

million) over 15 years, gave IMG-R all commercial

rights to the professional game in India.

With plans for the Indian Super League (ISL), a

franchise-based league, moving forward in a

calibrated manner, and with the recent

announcement that the country's biggest broadcast

network Star India had taken an equity position in

the tournament, expectations around the ISL, which

is scheduled to see its inaugural edition in late 2014,

have gone up several notches.

More so because the interim also witnessed

the failure of Premier League Soccer (PLS), a

franchise-based football league set up in West

Bengal along the lines of cricket's Indian Premier

League and America's MLS, to take off as planned in

early 2012.

The still-born PLS offers a good case study of

not just the potential this market offers but also its

pitfalls. A league featuring semi-retired stars like

Argentina striker Hernan Crespo and Italy's World

Cup-winning captain Fabio Cannavaro could not

only garner global attention, but also attract serious

money as well. The fact that six franchises that were

to feature in the first edition of the league attracted

buyers who collectively committed Rs700m+ for a

tournament confined to just one Indian state speaks

for itself.

The PLS' failure is just as illustrative of the

challenges potential investors in football are

confronting. And the reasons were almost wholly

political in nature and all about patronage. PLS was

conceived when the Left Front government that had

been ruling the West Bengal state in an

uninterrupted 35-year reign was on its last legs. Put

simply, it was a change of government, and by

extension, loss of patronage, that put paid to the

plans the India Football Association (IFA), the

controlling body for the sport in West Bengal, and its

commercial partners Celebrity Management Group,

had laid out.

Fast forwarding to the present, if there is a lot

riding on the ISL, the expectations around the

I-League have also gone up several notches – in the

wake of IMG-R's commitment to refurbish and

spruce up India's top-tier club football tournament.

The U-17 World Cup is some way down the

road. In the near term, it is the ISL that is expected to

give football much to talk about in the second half of

2014.

14

Peter HuttonChief Executive OfficerMP&Silva

or the first time in 20 years, I'm in a job that

isn't primarily about Sport in India. In many Fways it's a relief.

Outside cricket, the sports bodies were slow

to change from the Gandhi-era model. Reliant on

Central Government funding, run by honorary

secretaries, the federations didn't have the skill

sets to market their sports to participants,

broadcasters or sponsors.

The benefits of running a sports body were

always considerable: Olympic tickets, foreign trips,

social importance. As a result, change at the top

has been slow.

It led to a pay TV environment that was

unique in that a high proportion of Indian TV

rights fees were paid for international rather than

Indian sport, and the sport was presented in a

language which was alien to the common man.

Remarkably, the people making the decisions

on Indian TV sport were based outside the

country – ESPN Star Sports in Singapore (the

earlier Star Sports in Hong Kong), Ten Sports in

Dubai, Nimbus in Singapore.

Now that tide has turned. In the last year, Star

has followed Nimbus in exiting Singapore, Ten has

moved from Dubai. All the decision makers are

suddenly in India, and investing in Hindi language

content is at the heart of the business for Star

Sports.

It means a time of unrivalled opportunity for

the Indian sports federations. Star's investment in

University cricket is a good example of finding

value where broadcasters had previously seen

none. The Indian content business should thrive.

The channel business by contrast is a tougher

proposition. Regulatory frustrations are still

limiting the pay TV income for the territory and no

one is making money. The most transparent of the

businesses in financial terms is Ten Sports, who

announce their figures as part of the Zee Group.

The clear pattern in the Ten figures is they

get better when they have no India cricket tours in

a financial year. The pattern of major events

leading to sizeable losses for the broadcaster is

well established, and yet competition is keeping

acquisition prices high.

Why does everyone bother? Because Sports

is the unique driver of the pay TV business

worldwide, and is not susceptible to the time shift

phenomenon where more and more people

around the world are watching entertainment

content on delay through catch-up services or

broadband.

Of course, I couldn't possibly ignore India

going forward. It's still the most interesting TV

market going forward and full of potential. With

the ICC rights coming up later this year we may

see further headline deals being announced and I

look forward to being further confounded by a

fascinating area.

A TIME OF UNRIVALLED OPPORTUNITY

FOR INDIAN SPORTS FEDERATIONS

15

Kushal DasGeneral Secretary All India Football Federation

THE GAME CHANGER

he U-17 FIFA World Cup 2017 will be a

game changer for engaging the youth and Tcommunities in football, and reignite the

passion and interest of our youth towards Indian

football.

Ÿ The most important aspect is to create a

program to identify the best talent and develop a

competitive U-17 Indian team. In a country like

India, talent identification is not an easy task,

especially with the lack of technical inputs in many

states. Our endeavour would be to speak to our

partners, mainly companies like Coca-Cola, which

support youth competitions (Coca-Cola Cup), to

work with the All India Football Federation (AIFF)

for targeted talent identification through the

competition which engages schools, districts, and

finally the national championship. The message

will be clear direction to identify talent for the U-

17 World Cup in 2017 (boys born in January 2000

and after). It may be called "Road to 2017". This

will have a clear connect with the youth across the

country and generate significant interest and

following for this campaign.

Ÿ The State Associations will be motivated to

identify the best available talent for the national

championship and festivals organised by AIFF.

Ÿ We would like to engage the I-League clubs. As

part of the licensing criteria, it is a requirement for

them to have U-14 teams. The AIFF plans to select

at least 60 boys to be placed in two Academies

specifically for the U-17 World Cup. These

academies will engage the best coaches and we

plan to organise a league/tournament with

participation of the I-League clubs and the AIFF

Academies so we can continuously identify new

talent.

Ÿ The Academies will have the best exposure in

age group tournaments across the world.

Hopefully some potential stars may be identified,

who may get offers to join top-level European club

academies, which may also help in creating youth

icons before the tournament.

Ÿ This of course is not just a one-off target but an

ongoing one. The Indian U-17 team will be eligible

to try and qualify for the AFC U-16 championship

in 2016 before playing the World Cup in 2017. It

will also be our endeavour to qualify for the U-17

World Cup in 2019 and so on. So in other words,

this gives a clear goal towards youth development

and creating youth icons with whom the millions

of young fans in the country can identify and

connect and thereby raise the level of Indian

football. These young footballers with the right

technical skills and training will eventually be the

platform for the U-20, U-22, and senior national

teams.

These are some of my thoughts on how

important a tournament like the U-17 World Cup

is to connect with young Indians and change the

landscape of Indian football. I believe this is the

tipping point for Indian football.

Needless to say, we will do our best to ensure

a world class event so that we can aspire for

perhaps the U-20 World Cup in the near future!

16

Viral OzaMarketing DirectorNokia India

FOOTBALL IS GOING TO BE BIG IN INDIA

hat are the main factors that come

into play for your company while Wchoosing a sport, event or team for

sponsorship?

One, that the sport has to be appreciated by the

viewers, and second that the sport should treat us

as partners and jointly promote the event, and of

course should also allow consumer engagement.

It is said that in sponsorship it is not what you

have bought, but what you do with it.

Activation around a property can be much

more expensive and stretch limited time and

resources available with the organization.

What kind of budgets would go into such

activities? Please give examples of some

cutting-edge activation that has been

undertaken by your company in the sports

space.

Classic example is our association with the IPL

team, Kolkata Knight Riders (KKR). We have,

normally, over the last 5 years, put in 1:2 monies

behind activating the whole sponsorship – sales-

linked contests, sending consumers to watch

matches, giving them an opportunity of a life time

to meet SRK and KKR players. Our communication

related to IPL has always being about taking a step

forward, be it asking consumers for tips on

relieving tension of the players etc.

How much of the company's sponsorship

budget is earmarked for sports-focused

properties?

About 10-12% of the Nokia's sponsorship budget

is earmarked for sports-related properties.

In choosing what to sponsor, marketing

executives often aim to match the event to the

image of their brand. Due to the dearth of high-

17

profile national-level sporting events in India,

it might be necessary to spread the budget

across sports and geographies. Please explain

the methodology followed by your team.

We believe in one sport, one nation. Taking the

KKR example, though it's a Kolkata-based

franchisee, our IPL-related offers have always

been across the nation, be it flying the consumer

from Kerala all the way to Kolkata.

What methodologies are utilised to measure

the exposure for the brand and success of the

sponsorship to justify the RoI on the

sponsorship and activation around it?

We have very strict metrics on Brand KPIs, Digital

engagement, Sales, and we follow Repucom to

measure the exposure value – Nokia believes in a

minimum 3X ROI in any sponsorship that we do

Nokia's association with KKR is seen as a

"package deal" and extension of Shah Rukh

Khan's endorsement deal with Nokia. Beyond

that, please offer some case study pointers on

some unique activations Nokia has done with

KKR.

Not really. Though it was initiated because of SRK,

the sponsorship was a punt that has worked very

well.

Please elaborate on the value derived from

associating with just one team rather than

being a central sponsor for the IPL.

All I can say is that we have 7X returns for the last

5 editions of the IPL.

Nokia was title sponsor for the Champions

Trophy for only a year. Please expand on why

Nokia chose to delink from Champions League

as well as an assessment of the long term

future of the Champions League as a property

from a brand like Nokia's point of view.

The only reason we parted ways with the property

is because they moved the event to South Africa.

Otherwise the property delivered 11X ROI.

The association with Shillong Lajong FC is

interesting. How does Nokia plan to evolve the

association? Are there any plans on the

youth/talent development side?

This was a very hardworking decision. Football is

big in NE and our cricket sponsorships did not

reflect a rub off, hence this association. Football is

going to be big in India and we have seen the club

culture grow at a very rapid pace; this is the

principle reason behind signing up with FC

Barcelona as India Partners.

18

THE BUCK STOPS AT TV

ndian sports TV broadcasting was, is, and will

continue to be dominated by Cricket for the Iforeseeable future, contributing to 80 to 85% of

the total television sports media revenues.

The year 2011 was a phenomenal year for

sports broadcasters, with media revenue up by 50%

compared to the previous year on the back of India

hosting (and winning) the ICC ODI World Cup as

well as the IPL registering a peak year. The Indian

Grand Prix 2011 was also very popular in India, with

the inaugural edition delivering the high ratings for

the Formula One race.

However, other sports are also gaining

prominence, especially Football, though interest

remains predominantly for international

leagues/tournaments. That is expected as the I-

League improves as a television-friendly product

and also with the launch of the Indian Super League

(ISL) later this year.

Other sports such as Badminton and Hockey

have started making their presence felt because of

improved performances by Indian players in the

international arena, coupled with increased

investments flowing into the two sports due to the

launch of the Indian Badminton League (IBL) and

the Hockey India League (HIL) respectively.

What is common to Cricket, Football, Hockey

and Badminton? The way the country's lead

broadcaster STAR is looking to become the network

that controls all the significant television real estate

that is out there in these sports, but also takes equity

positions in tournaments such as ISL, in which it is a

35% stakeholder.

And it is not as if the rival networks are just

sitting by. Multi Screen Media (MSM) aka Sony

Entertainment Television, which holds the rights to

Indian sport's biggest annual jamboree – the Indian

Premier League – is also putting its all behind

another sport that SportzPower bets will become

big in India going forward – Basketball.

Some months ahead of the announcement last

October that the National Basketball Association

(NBA) had entered into a multi-year partnership

with the Reliance Foundation to launch a

comprehensive school-based youth Basketball

program in India, MSM's sports channel Sony SIX

had entered into a multi-year television

partnership.

That was followed up in October with the

announcement of an expansion of their existing

deal, which will see more NBA games and

programming broadcast in India than ever before.

Just as this report was being finalized, came

the news hot off the press that Sony SIX had won the

exclusive broadcast rights to the 2014 and 2018

FIFA World Cups for $90 million. The deal also

includes rights to broadcast the Under-17 World

Cup 2017 to be hosted by India.

This latest acquisition by Sony SIX comes on

the back of broadcasting the UEFA and CONMEBOL

matches from the 2014 FIFA World Cup qualifying

rounds, in addition to acquiring the rights for

qualifiers for UEFA Euro 2016 and UEFA Euro 2016.

This acquisition massively strengthens the

channel's equity vis-a-vis quality Football telecast

in India.

Then there is Neo Sport, which has

repositioned itself as a niche player after the loss of

BCCI rights to STAR. It is putting a lot of investment

behind Golf, not just on air but through sister

concern Nimbus Sport. Nimbus signed a three-year

contract with the Indian Golf Union (IGU) in 2011

that sees the sportscaster market and deliver the

Indian Masters as well as the Indian Open.

But as already noted, the big news in Indian

sports TV broadcasting remains Cricket. A slugfest

is expected when the ICC media rights come up for

bidding. And further down the road an even bigger

one when the BCCI issues tenders for the next cycle

of rights to its crown jewel – the IPL.

The battle royale that is developing in the UK

market over key football rights between dominant

player SKY and telecom giant BT could well be

replicated in the Indian market over the next five

years, but with prized cricket properties being the

bone of contention.

BT's push into sports broadcasting has gained

massive heft with the confirmation by UEFA that BT

Sport has won the 2015–18 Champions League and

Europa League media rights for the UK territory. BT

Sport will pay £897 million ($1.4 billion, 1.1 billion

euros) for the rights to 350 games, becoming the

first UK broadcaster to win exclusive rights to all

matches in both European tournaments.

SportzPower sees a similar scenario unfolding

around two big-ticket cricket properties that open

for bidding over the next five years – the ICC cricket

19

20

21

Figures mentioned are in Crores (1 Crore = 10 Million)

Highlights of Media Spends on TV

Ÿ Increase in 2011 due to ICC World Cup & good IPL

Ÿ 2013 is flat on 2012. This is owing to less number of cricket matches India played and also that the series under question had more Test matches

Ÿ Media industry had grown nearly parallel with the inflation rates

rights and the Indian Premier League telecast

rights. Between the two, it is the IPL that will be the

bigger draw, seeing as how MSM has garnered such

massive profits from being the rights holder of the

biggest property the sport has on offer.

We reckon the bidding for IPL in the next cycle

(2018-2027) could well go as high as $2 billion+,

which means Rs 120 billion (at current exchange

rates) could potentially be the investment

commitment that whoever finally wins the rights

will have to make.

And who would likely be in the running here?

That Sony and STAR will be there is a given.

SportzPower will be more interested in the

moves that Mukesh Ambani-controlled Reliance Jio

Infocom, which has just got its unified telecom

licence, will be making for this particular high value

cricket property.

Before its latest coup, BT's move into acquiring

a piece of English Premier football rights in the UK

earlier in 2013, breaking the traditional lock that

STAR's sister network SKY had on it, was the big

news as far as UK football rights bidding was

concerned.

would be football. For the three-year current cycle of

EPL rights, STAR has committed $150 million. It can

only go up post 2015.

Mukesh Ambani's ambitions around sport are

gradually being unfolded and in terms of scale and

ambition they are huge. Stands to reason therefore

that Reliance Jio Infocom could well prove the Joker in

the pack when the next round of big ticket cricket

rights bidding comes into play.

SportzPower expects Reliance Jio Infocom to

have a similar disruptive impact on the IPL rights

bidding.

As for the ICC rights piece, considering that it

went for $1.1 billion last time round, it is reasonable

to assume that the next cycle (2016 onwards) will

go for a higher price.

Then there are of course the cricket rights for

England, Australia, and going to the next tier which

0

500

1000

1500

2000

2500

3000

3500

2008 2009 2010 2011 2012 2013

3000

22502250

2000

1450

1150

Media Spends

Source - GroupM ESP

22

23

Nitin KukrejaPresident (Sports)Star India

ENABLING A PARADIGM SHIFT

t Star India, we are excited to be at the

forefront of a sweeping change to the Asports viewership landscape.

When we decided to make a foray in the sports

genre, the first thing we questioned was the belief

that India is a 'one sport, one language country'.

Our first attempt has been to make sports

viewership more inclusive. In the last 15 years in

India, entertainment and movie channels have

gone local with a vengeance; however, sports has

remained aloof from localization. Telecast of

cricket was limited to English, a language spoken

by less than 10% of India. Introducing

commentary in Hindi in Cricket, followed by other

sports, has made the action accessible for a much

wider audience. We have taken this a step further

by launching India's first 24x7 Hindi sports

channel – Star Sports 3. We see potential to go

even more local – both in terms of language and

content.

Cricket too, as we know it, is restricted to the

senior men's team international cricket. We have

widened the scope of cricket to under-19 cricket,

women's cricket, and university cricket – with

much encouraging results. Our appetite here, and

as we discovered, the viewer's appetite too, is only

constrained by supply!

Pockets of passion exist across the country

for a variety of local sports, but these have never

been tapped or harnessed in the way they should

have been. Apart from cricket, sport as we know it

was restricted only to international soccer leagues,

motor sports and the like – no homegrown, local

sports leagues of the kind that exist in most other

markets, most notably the USA. We matched intent

with investment – thus the Hockey India League,

Indian Badminton League, and Kolkata Football

League made their debut on our channels in the

last one year. Not only did this get significant

support from viewers in all parts of the country, it

has resulted in providing visibility of a whole new

generation of players and talent across sports.

Unlike previous years, a young talented

sportsperson who is passionate about hockey,

football or badminton sees a viable avenue to

pursue their sport of choice, possibly make a

career out of it.

Viewers today consume content on multiple

screens beyond TV – the internet, the smartphone

and the tablet. Why then would Star be limited to

TV? This thought gave birth to starsports.com – a

platform that provides a rich and personalized

experience to sports fans, unlike anything on TV.

Viewers can pause, rewind and relive the

moments that they want to see, not what the TV

broadcaster has chosen for them to see.

We believe that these initiatives have set the

ball rolling and will create serious momentum in

transforming the way sports is played and

consumed in the country. However, it is a fact that

much more remains to be done before India can

claim pride of place in the international sports

arena.

Beyond broadcasters, the mind-set of the

entire ecosystem – the sports federations, the

government and the news media and advertisers

needs to change so that a variety of sports get the

money, resources, infrastructure and coverage that

they deserve. The government has a huge role to

play – by allocating adequate monies, developing

stadiums and infrastructure, and putting in

enabling policies in place. The sports federations

must enable and nurture talent, and work together

with other stakeholders to promote and market

the game.

In a young country like India, sports have a

crucial role to play in youth development and can

even be a huge generator of employment. It will

take a spirit of partnership with federations and

people with vision to take sports to the next level

in this country.

24

TEAM SPONSORSHIP- ALL ABOUT THEBOYS IN BLUE

It also revealed that, given the right platform,

there are enough brands willing to explore the

unknown. In 2008, when tire major Bridgestone

considered IPL as a medium for brand

communication, it was put off by the price tags for

premium rights. For example, real estate company

DLF, at that time, was paying Rs 400 million per year

for the title sponsorship of IPL. So, Bridgestone

made a modest entry into cricket as a co-sponsor of

IPL franchise Mumbai Indians.

Four years later, in 2012, the decision to

become the title sponsor for World Series Hockey

(WSH), came easy. For one, the investment was low:

Bridgestone was paying Rs 20 million per year in a

three-year deal. And it gave the tire company an

opportunity to target North India, a market where

hockey is popular and where Bridgestone was

f there is one area that validates the proposition

that Sport in India is all about Cricket, then the Iendorsement arena is certainly it. It is not

happy reading on the Team Sponsorship front if you

are a non-Cricket proponent. In the six years under

review, Cricket accounted for a low of 91 per cent in

2012 and a high of 97 per cent in 2009 of overall

Team Sponsorship monies.

Having said that, the trends shown in 2012

look to be a pointer to better things to come for non-

Cricket team sports with Football and Hockey both

coming into the reckoning. For Football in

particular, it is safe to say that these numbers are but

a fraction of what is possible if there is a better

mining of the potential the game holds in India.

What we've also noticed is that a major part of

Football team sponsorship number has come from

Indian Brands associating with European Football

Clubs – Airtel & Manchester United, Nokia with FC

Barcelona, Tata Tea with Arsenal and Inter Milan,

among others.

A clear positive in 2012 of course was the

launch of the 'rebel' World Series Hockey (WSH) co-

promoted by the de-recognized Indian Hockey

Federation (IHF) and Nimbus Sport. What WSH

showed up in stark relief was that though Cricket

has long past taken over the mantle of our National

sport, the sticks sport has still got game.

Figures mentioned are in Crores (1 Crore = 10 Million)

Revenue Allocations Around Team Sponsorship

Ÿ Increase in Cricket in 2011 due to addition of 2 IPL teams. Dip in 2012 because franchise Kochi Tuskers eliminated from IPL

Ÿ Increase in Football due to Brands like Airtel, Nokia, Tata Tea, etc. signing deals with European Football Clubs

Ÿ Increase in other sports in 2011 due to Formula 1.

Ÿ Increase in 2012 because Sahara renewed Hockey India deal in better value & emergence of World Series Hockey

Ÿ Increase in 2013 due to Hockey India League and Indian Badminton League

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2013

800

424

10 3

425

17 3

425

28 3

685

31 8

610

35 24

612

44

65

Cricket

Football

Others

Source - GroupM ESP

25

weak. South India had always been Bridgestone's

strong market and the association with Mumbai

Indians was good enough to deliver there.

From Bridgestone's perspective, even if the

company's return on investment (RoI) from WSH

was Rs 100 million worth of media mileage

annually, they would have been happy. That they

were not able to fully test that theory as it turned out

seeing that WSH died a premature death due to it

being a non-sanctioned league is another story in

itself.

WSH remained a short-lived event as the

establishment ensured it would go down in history

as the hockey equivalent of the Zee Group-

promoted Indian Cricket League (ICL), which was

followed and bettered many times over by the IPL.

What IPL did to ICL, the Hockey India League

(HIL) has effectively done to WSH. The successful

launch of HIL and the IBL has set the stage for

franchise-based leagues, with more already

running and in the offing – wrestling, kabbadi,

boxing, tennis, athletics. All this action augurs well

and promises to attract more money into team

sponsorships and rewards for players in non-

cricket offerings.

26

WHEN IT COMESTO TALENT, MONEYCHASING DHONI & CO

nd if Cricket overwhelmingly dominates

Team Sponsorships, the same is the case on Athe Athlete Management side. The Big Boys

of Indian sport's brand endorsement bandwagon

are cricketers. And it doesn't make any difference

whether they are active on the field or retired. They

are the ones who are grabbing all the attention, and

the moolah that goes with it.

In the six years under review, the gap between

the cricket stars and the best of the rest has only

been increasing on the endorsement value index.

That is not going to change in relative terms

but in absolute terms, as the money and

investments coming in to sports increases, so too

will the trickle-down to other sports.

A case in point being India's badminton ace

Saina Nehwal, who in 2012 signed a three-year deal

worth Rs 400 million with sports management firm

Rhiti Sports, soon after her bronze-medal feat in the

London Olympic Games.

That said, Rhiti and Saina have recently parted

ways, an indicator that non-cricketers have a long

wait ahead before they can hope to have a sniff at the

kind of monies the top cricketers command.

27

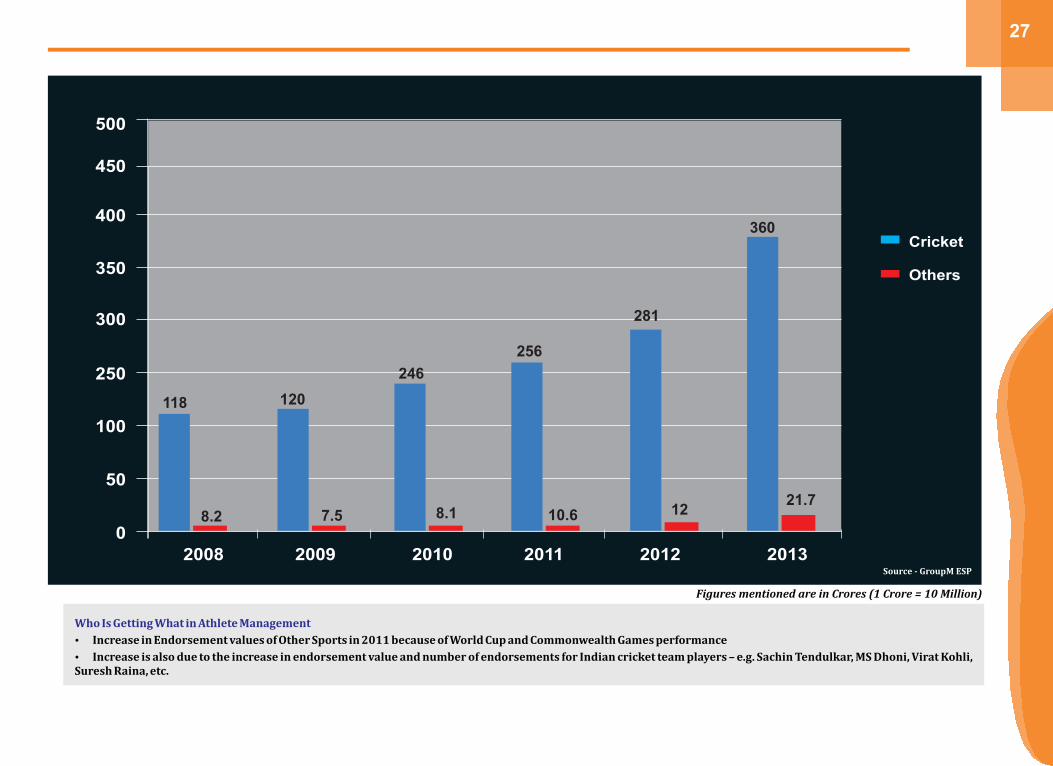

Figures mentioned are in Crores (1 Crore = 10 Million)

Who Is Getting What in Athlete Management

Ÿ Increase in Endorsement values of Other Sports in 2011 because of World Cup and Commonwealth Games performance

Ÿ Increase is also due to the increase in endorsement value and number of endorsements for Indian cricket team players – e.g. Sachin Tendulkar, MS Dhoni, Virat Kohli, Suresh Raina, etc.

2008 2009 2010 2011 2012 2013

0

50

100

250

300

350

400

450

500

Cricket

Others

118

8.2

120

7.5

246

8.1

256

10.6

281

12

360

21.7

Source - GroupM ESP

28

Bunty SajdehChief Executive OfficerCornerstone Sport & Entertainment

OTHER SPORTS ARE STEADILY

CARVING A NICHE

hat were the trends in investments

in brand endorsement from 2008 to W2013?

2008 was an interesting year in terms of brand

endorsements. Due to the global meltdown,

markets worldwide had taken a beating and

economies were reeling from the subprime crisis.

Incidentally, 2008 was also the year the IPL was

launched in India which gave brands a lucrative

new platform of brand advertising. It was

interesting to note that the general market

environment at the time did not drastically effect

the investments brands made in the IPL that year.

In terms of brand endorsements over the years,

what is most noticeable is that brands are putting

in a lot more research before embarking on an

association with a Celebrity, be it from sports or

entertainment.

The science behind an association has become

paramount today. With the aid of social media, one

can easily identify each celebrity's fan base in

terms of demographics, which in turn is

used to determine whether the brand and

the celebrity are speaking to the same

audience. In terms of commercials involved,

it is largely dependent on the popularity of

the said celebrity. Successful performances

of celebrities in their respective fields are

directly proportional to their perceived

market value.

This period has seen the retirements of

the Indian greats – Ganguly, Dravid,

Kumble and Laxman – as well as the

greatest, in Sachin. We would assume

that Sachin and Dravid will retain their

brand salience, but not so the others.

Please share your point of view.

Ganguly, Kumble, and Laxman were seldom

perceived as individuals who would carry

brands. It was more of a personal choice on

their part to focus on their Cricket rather

than commercial commitments. While each

of them had their own persona and

individuality, Ganguly, often being the most

flamboyant of the lot, still did not see as

many endorsements as cricketers today. This

is partly due to the fact that the sports

management industry was still in a very

nascent stage during that time, coupled with

Sachin dominating the endorsement space.

Over the years, sports management agencies

29

such as ours have refined the way brands perceive

athletes. While Sachin was and will be the poster

child of Indian cricket for the perceivable future,

Dravid was very comfortable in the space he had

carved out for himself. Dravid's image was and

still is the boy next door, controversy free,

intelligent, and well-spoken. These are traits

which will always attract brands no matter what

the age. Sachin on the other hand is difficult to

compare with the rest of the players. The respect

and reverence he enjoys around the world is

seldom seen in sport. He will continue to carry

that aura around with him.

Then there is the fading of the next tier big

names – Sehwag, Yuvraj, Gambhir, Harbhajan,

Zaheer. Also we've seen new players taking the

baton – Virat Kohli, Shikhar Dhawan, Suresh

Raina, Rohit Sharma. What is their future

looking like?

Age catches up with us all and athletes are subject

to this saying more than any. Once stalwarts of the

India cricket team, the likes of Sehwag, Yuvraj,

Gambhir, Harbhajan, Zaheer have all been

dominating in the their respective disciplines at

their peak. Both generations of cricketers have an

important role to play during this passage of

change. It is up to the senior members who are in

the twilight of their career to guide and nurture

the younger players and make sure the legacy,

which was passed down to them as youngsters, is

in safe hands. The incoming crop of younger

Cricketers should respect prevailing customs

which have been passed down, while at the same

time bringing their own individuality to the game.

Each set of players represent the current trends

and styles of their respective generation. The likes

of Virat, Rohit, Dhawan, and Raina are prime

examples of the evolution of Indian Cricket. They

are clued in to things like their image off the field

and their social media interaction etc. These

parameters directly affect how brands perceive

them and will hence determine the kind of

endorsements they attract. Agencies such as

Cornerstone also play a vital role in identifying

each individual's strengths and weaknesses and

will in turn help mould their personalities and

image to suit the best of both worlds.

How are other sports athletes contributing to

the industry and how is their future looking

like?

Other sports in India have slowly and steadily

carved out a niche for themselves. In recent years,

Abhinav Bindra has put shooting on the map by

winning India's first Olympic Gold Medal. Sania

Mirza reformed women's tennis in India by

becoming the first Indian woman to win a Grand

Slam title in doubles. Our performance in the

recently concluded London Olympic Games was

testament to other sports gaining popularity in the

country. Saina Nehwal has made badminton

popular again by giving the otherwise Chinese

dominated sport a new face. Dipika Pallikal has

been consistently beating top-ranked players in

squash to become the first woman from India to

break into the Top 10 in the world. Sunil Chhetri

has recently become the highest goal scorer for

India overtaking Baichung Bhutia. What this does

is give brands an entirely new dimension to work

with when it comes to associating with athletes.

30

Prasanth KumarManaging PartnerGroupM India, Central Trading Group

SHORTER AND NEWER FORMATS

KEY DRIVERS FOR GROWTH

hat were the trends in investments

in sports from 2008 to 2013? WSports investments have been trending the same

as overall market TV ADEX (investments highly

dependent on nature of the tournaments and the

kind of teams participating). With the advent of

HIL, IBL, Indian F1, and the upcoming ISL, it

augurs well for Sports advertising in India. Shorter

and newer formats would be the key drivers for

growth for all sports (cricket, football, hockey etc).

Promotion of these properties in a big way by both

sponsors and broadcasters likely to set the trend

for non-cricket advertising spends in India.

This period has also been marked by the

switch from analog to digital which would have

had a disruptive impact. What influence has it

had in the period under review?

Higher traction among digital audiences – 25%

higher viewership as compared to analogue

audiences for Sports channels.

Between 2008 and 2013, the ratings in Cricket

have been going down but that can also be

explained by the fact that the television

viewing universe has been incrementally

expanding. How are the numbers playing out

here, both in terms of rating and ad rates?

Cricket ratings are more or less stable between

2010 and 2013 – no significant drop in ratings

across ODI, Test and T20. Investments still skewed

with 90-95% of Sports spends on Cricket and this

is likely to continue in future too. Tournaments

involving class A teams like Australia, England,

South Africa prosper better from advertising POV.

With Star promoting EPL with Hindi

commentary, FIFA World Cup next year, IMG

launching Indian Super League – will Football

be the alternate sport in India?

Hindi commentary is a positive; however, quality

of content and commentators could impact

viewership. Football likely to emerge as an

alternate sport in India, but would do so on the

long term. Some of the FIFA matches in 2010 have

rated as high as IPL matches and the tournament

average was at 1.41. Higher ratings were observed

in 2006 FIFA too. FIFA factor is a huge draw for the

viewership. FIFA in 2014 to be a huge draw for

advertisers in India too.

31

Basant DhawanGeneral Manager – MediaVodafone India

WE ARE A NATIONAL BRAND AND ADDRESS

CONSUMERS ACROSS GEOGRAPHIES

hat are the main factors that

come into play for your Wcompany while choosing a

sport, event or team for sponsorship?

It is a combination of reach and consumer's

connect with the sport that contributes to

this decision.

In choosing what to sponsor, marketing

executives often aim to match the event to

the image of their brand. Due to the

dearth of high-profile national-level

sporting events in India, it might be

necessary to spread the budget across

sports and geographies. Please explain

the methodology followed by your team.

We are a national brand and address

consumers across geographies. The scale of

activation may vary in certain geographies

but the consumer experience and

engagement is kept standard.

What methodologies are utilized to

measure the exposure for the brand and

success of the sponsorship to justify the

ROI on the sponsorship and activation

around it?

The measures for determining the ROI vary

from sport to sport. It broadly includes

media value generated, impact on brand

metrics and brand engagement generated.

The F1 association in India is more of an

extension of a global partnership. Having

said that, are there any unique

insights/brand uplifts that F1 has

delivered for Vodafone in this market?

F1 has enabled us to reach out to our

enterprise and SME consumer base to drive

brand adoption and loyalty amongst these

segments.

32

33

DIGITAL MEDIA -SCORE BIG WITHEARLY ADOPTION

ndia today stands at the threshold of a major

digital revolution in the making. Digital India is Igrowing rapidly, boasting the world's third

largest online population that is also the second

fastest growing.

Indian consumers are fast adapting to multi-

platform digital consumption which is expected to

grow further as broadband becomes accessible

(faster and cheaper), combined with cheaper smart

phones and connected devices. India, with a large

and growing digital literate population, has its

unique challenges, but presents immense potential

across several developing and underdeveloped

sectors (sports, travel, online entertainment,

healthcare, communication, government services,

education etc.) with windfall opportunities for

growth.

Sport on digital media has still some ways to go

however. As per Comscore's last report, while reach

of sports within the web population is slightly

better than some of the BRICs nations, time spent is

lowest and almost half of the Global average.

Sport consumption is largely driven by cricket

with leading sites being ESPN's Cricinfo, Yahoo

Cricket, Cricbuzz. The consumption is largely

limited to score updates, news consumption, blogs

etc.

While Live Streaming of most series is

available, the consumer adoption is limited and

streaming quality is a large reason for this with

bandwidth still being a challenge.

Advertiser adoption on digital sports is also

largely limited to sponsorships. While properties

like IPL have tried selling spot buys, they have met

with limited success so far.

All this does not mean the potential does not

exist. Consumer interest is clearly growing but have

been impeded by poor infrastructure. The fact that

better bandwidth speeds have helped grow

consumption clearly points out that once

technologies like 4G, etc. become embedded, this

will explode.

The strategic use of digital media will be

particularly critical for the non-cricket sports in

India, not just in terms of reaching out to the existing

community, but growing the fan base. There are

practical considerations that need to be taken into

account as well. In television, there is the cost

impediment, in print there is the space impediment.

Digital is the future and sports administrators that

embrace this reality will be the ones that score.

Reach of Sports Category Average Time Spent on Sports Category(Minutes)

Worldwide

China

India

Russia

Brazil

38%

20%

26%

24%

53%

55.1

31.0

29.6

51.3

50.1

Source - GroupM ESP

34

ON THE FRONT FOOT

ven as 2013 has wound up, Indian Sports'

biggest blockbuster – the IPL – goes into E2014 with many questions to answer.

Primarily those that have been raised by the spot-

fixing scandal that rocked the cosy cross-

relationships that have thrived in India's most high

profile by-invitation-only Super Club.

As for the IPL's owner, the Board of Control for

Cricket in India (BCCI), the world's richest and by

extension most powerful cricketing body, has been

made to realize the hard way that it cannot take for

granted an endless money flow from its

stakeholders. With the Sahara Group pulling the

plug on both the IPL as well as its lead sponsorship

of the Indian cricket team, the BCCI has had to come

to terms with the market correction around the

sponsorship monies advertisers are willing to put

behind its big-ticket properties as well as the prices

it can demand for the sale of a new franchise (if it

chooses to open bidding next year).

Does this imply that Indian Sport's most high

value property is going down? Most certainly not.

It's more like a course correction and price

correction. And whatever may be the short-term

pull-backs, in the long run, accountability, better

corporate governance, more transparency, are all

good for not just the IPL, but the BCCI too.

As for other sports, the big

news of 2014 will be the inaugural

edition of the IMG-Reliance-Star co-

owned Indian Super League, the

franchise-based tournament that is

set to bring all the bells and whistles

associated with the IPL to football.

There is also the commitment that

IMG Reliance, the commercial rights

holders for football in the country,

has to improve the country's top-tier

soccer tournament. The I-League

clubs will be hoping that IMG-R

walks the talk on that front, though

the prevailing sentiment is one of

wariness as to what the future holds.

Additionally, both the Hockey

Indian League and the Indian

B a d m i n t o n L e a g u e w i l l b e

conducting their second editions in

2014, the deliveries around which

will be critical to how the respective

sports improve monetization.

All in all, 2014 has more

upsides than down. While there will

be no Indian Grand Prix next year,

there will be more leagues, sports

like basketball are making rapid

strides, and the whole wellness and

fitness movement is gaining

ever-increasing traction, which in

turn means more interest in sport as

a participation activity and not just

as spectator engagement.

35

More Power to Sports,we say!

www.facebook.com/groupm.india www.twitter.com/GroupMIndia

About GroupM

GroupM is the leading global media investment management operation, part of the WPP Group. It serves as the parent

company to WPP media agencies including Mindshare, Maxus, MEC, MediaCom, and Motivator in India. GroupM India

also have several niche specialist units across content, digital and experiential marketing, as well as consulting. Our

primary purpose is to maximize the performance of WPP's media communications agencies on behalf of our clients,

our stakeholders and our people by operating as a parent and collaborator in performance-enhancing activities such

as trading, content creation, sports, digital, finance, proprietary tool development and other business-critical

capabilities. The agencies that comprise GroupM are all global operations in their own right with leading market