Sources of Industrial Growth and Structural Change of Industrial Growth and Structural Change ......

196

SWP614 Sources of Industrial Growth and Structural Change The Case of Turkey Merih Celasun WORLD BANK STAFF WORKING PAPERS Numbgei 614-__ Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

phamkhuong -

Category

Documents

-

view

220 -

download

1

Transcript of Sources of Industrial Growth and Structural Change of Industrial Growth and Structural Change ......

SWP614

Sources of Industrial Growthand Structural Change

The Case of Turkey

Merih Celasun

WORLD BANK STAFF WORKING PAPERSNumbgei 614-__

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

w4/s-WORLD BANK STAFF WMRKING PAPERS 0<5 7

Number 614 7

Sources of- Industrial Growthand Structural Change

The Case of Turkey

Merih Celasun

INTERNAnONAL MONETARY FUNDJOINT LIBPARY

MAR 2 {l 1984

INTERNATIONAL BANK FOR1EMONSTRUCTION AND DEVLOPENT

WASHINGTOX, D.C. 20431

The World BankWashington, D.C., U.S.A.

Copyright © 1983The Intemational Bank for Reconstructionand Development / THE WWORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

First printing September 1983All rights reservedManufactured in the United States of America

This is a working document published informally by the World Bank. Topresent the results of research with the least possible delay, the typescript hasnot been prepared in accordance with the procedures appropriate to formalprinted texts, and the World Bank accepts no responsibility for errors. Thepublication is supplied at a token charge to defray part of the cost ofmanufacture and distribution.

The views and interpretations in this document are those of the author(s) andshould not be attributed to the World Bank, to its affiliated organizations, or toany individual acting on their behalf. Any maps used have been preparedsolely for the convenience of the readers; the denominations used and theboundaries shown do not imply, on the part of the World Bank and its affiliates,any judgment on the legal status of any territory or any endorsement oracceptance of such boundaries.

The full range of World Bank publications is described in the Catalog of WorldBank Publications; the continuing research program of the Bank is outlined inWorld Bank Research Program: Abstracts of Current Studies. Both booklets areupdated annually; the most recent edition of each is available without chargefrom the Publications Distribution Unit of the Bank in Washington or from theEuropean Office of the Bank, 66, avenue d'Iena, 75116 Paris, France.

Merih Celasun is a professor at the Middle East Technical University inAnkara and a consultant to the Development Research Department of the WorldBank.

Library of Congress Cataloging in Publication Data

Celasun, Merih.Sources of Industrial growth and structural change.

(World Bank staff working paper ; no. 614)Bibliography: p.1. Turkey--Industries. 2. Turkey--Economic policy.

I. Title. II. Series.HC492.C44 1983 338.09561 83-16981ISBN 0-8213-0283-2

Abstract

This study provides an empirical analysis of the sources of Turkey'sgrowth and structural change since the 1950's, and considers the prospects forits transition from and inward-looking development strategy to trade-orientedgrowth in the 1980s. The paper discusses the major planning issues forimproved adjustment to current domestic and international economic problems,with special attention to the role of Turkey's public and private sectors inthe industrialization process. As part of a project on industrialization inselected semi-industrial countries, the study also compares Turkey'sexperience with those of other countries.

Acknowledgements

The author wishes to thank Hollis B. Chenery, Larry Westphal, BelaBalassa and Sherman Robinson for their encouragement and constant interest.The development of the present work in successive stages owes much to thegenerous data provided by Yusuf Hamurdan, Erdogan Ozotun and Cetin Akbay andcomments on the methodology given by Yuji Kubo, Moises Syrquin and KemalDervis are gratefully acknowledged. The author is indebted to KathleenJordan, Tevfik Yaprak nd Selcuk Caner for very competent computerprogramming. Ayse Tan and Kim Tran deserve special thanks for typingsuccessive drafts. The author is also grateful to Anne Vorce, who edited thefinal text for publication, and improved the presentation.

iii

Summary

This paper analyzes the sources of Turkey's growth and structural

change since the 1950s, with an emphasis on the limits of an inward-looking

development strategy for Turkey's industrialization and its adjustment to

current economic conditions. The analysis suggests that Turkey needs to alter

its trade orientation and the paper describes the major issues that must be

faced for a successful transition to a trade-oriented development strategy in

the 1980s.

For economic, historic, institutional and policy reasons, Turkey's

postwar growth strategy has generally been inward-looking. In comparison to

other semi-industrial countries of a similar size, Turkey has had a very low

share of trade in GDP until recently. As this study emphasizes, internal

factors and domestic demand have been the main sources of Turkish growth and

structural change. The limited role of trade in Turkey's industrialization

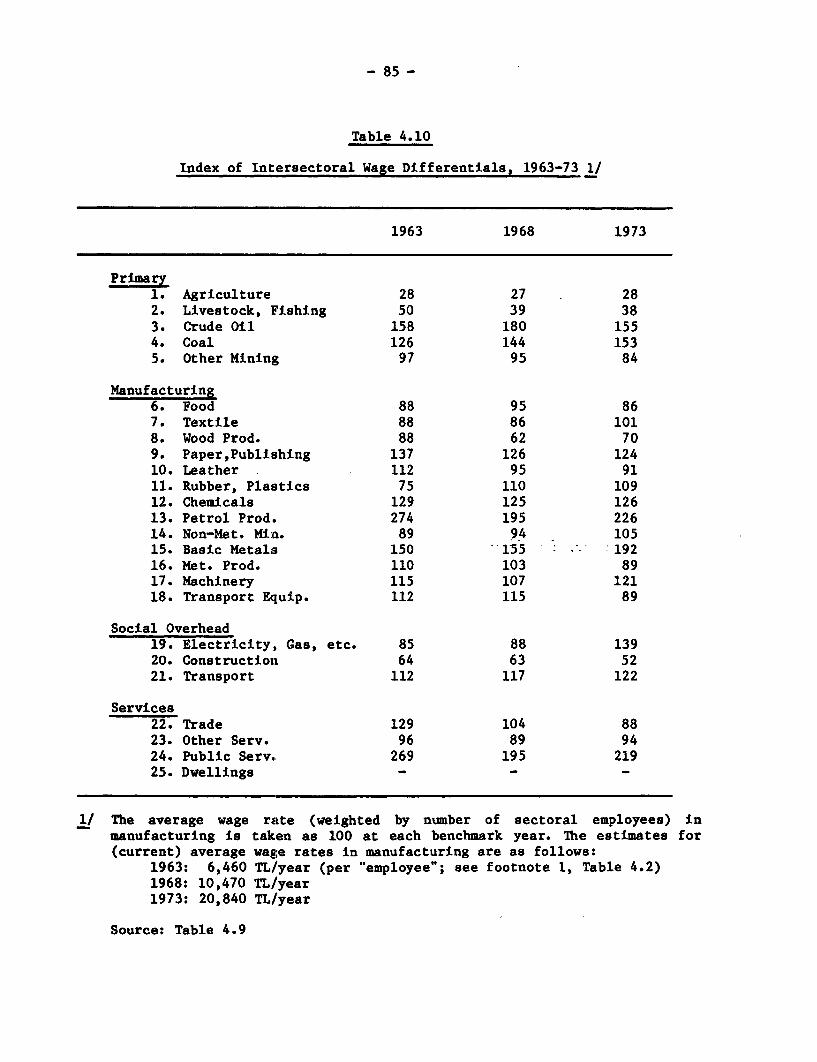

has been due primarily to the relatively large size of its domestic markets,

its natural resotlrce diversity, political conditions, and the structure of

incentives. Unlike other semi-industrial countries that had successfully

switched from an import substitution to an export-oriented strategy, Turkey

thus prolonged the inward-oriented phase of its manufacturing growth. As a

result, a highly protected industrial structure that relied heavily on the

import of intermediate goods became a costly feature of Turkish

industrialization. However, with the external economic shocks of the 1970s,

it became clear that Turkey's narrow trade focus could not be sustained.

These new developments in the world economic scene added to already serious

iv

adjustment problems resulting from increased import intensity and stagnant

export growth.

This paper also analyzes the sources of changes in factor uses and

relative prices and the implications of these results for policy planners.

Despite the growth of the manufacturing sector, Turkey's structural transition

has not been accompanied by sufficient increases in employment, and employment

problems will continue to be a major item on the policy agenda. Increased

trade-oriented growth, with a gradual decline in the levels of protection for

domestic market-oriented industries, will generate important shifts in

sectoral prices, real wages and profits.

Finally, for planners, the study indicates several problems that

could be remedied through policy measures. The lack of integrative mechanisms

and common rules of market behavior in Turkey's dualistic mixed economy system

has led to pervasive distortions in the structure of savings, costs and

prices. In addition, the reliance on non-price measures and selective

policies rather than general policy instruments to achieve economy-wide

objectives has created difficulties for the consistency and efficiency of

savings generation and resource allocation, and has led to recurrent balance

of payments problems. The concluding part of the paper reviews the major

directions of policy changes required for a more viable growth process in the

l980s.

v

TABLE OF CONTENTS

Page

INTRODUCTION ..................... 1

1. HISTORICAL BACKGROUND: 1923-80............... 4

A. Economic Development Before 19509... 0......-......... 4B. Economic Development in 195O-73..oo......... ........ 7C. Economic Development After 1973 ............... *.....o11

2. PATTERNS OF DEVELOPMENT, 1953-78: An Overview.....o....14

3. SOURCES OF INDUSTRIALIZATION, 1953-73 .................... 21

A. Scope of the Analysis. ........ 21B. Basic Data ........ 24C. Policy Characteristics and Trade

Orientation of the Subperiods .............. o...o.28D. Sources of Growth and Structural Change:

An Economy-Wide Analysis ............. . ... .31

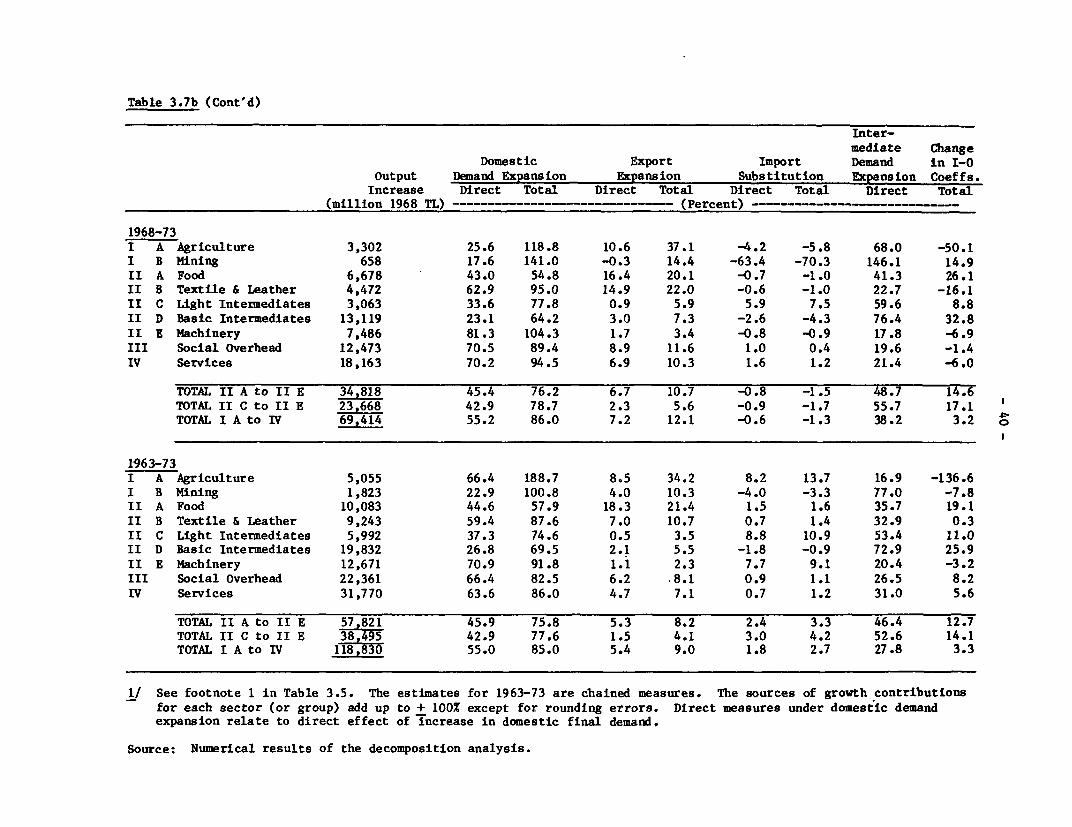

E. Sources of Growth and Structural Changein Gross Output: An Analysis byMajor Sectors ............. 38

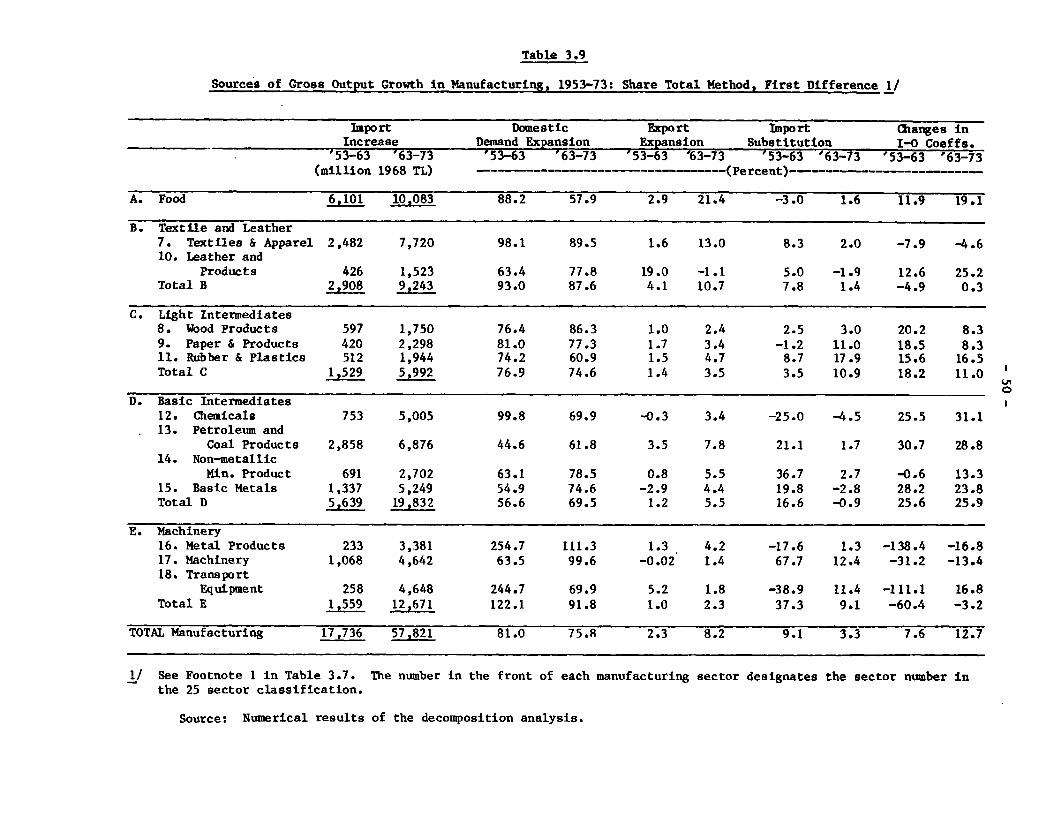

F. Sources of Growth Patterns inManufacturing Industries..oo..o..oo.. o ............ 48

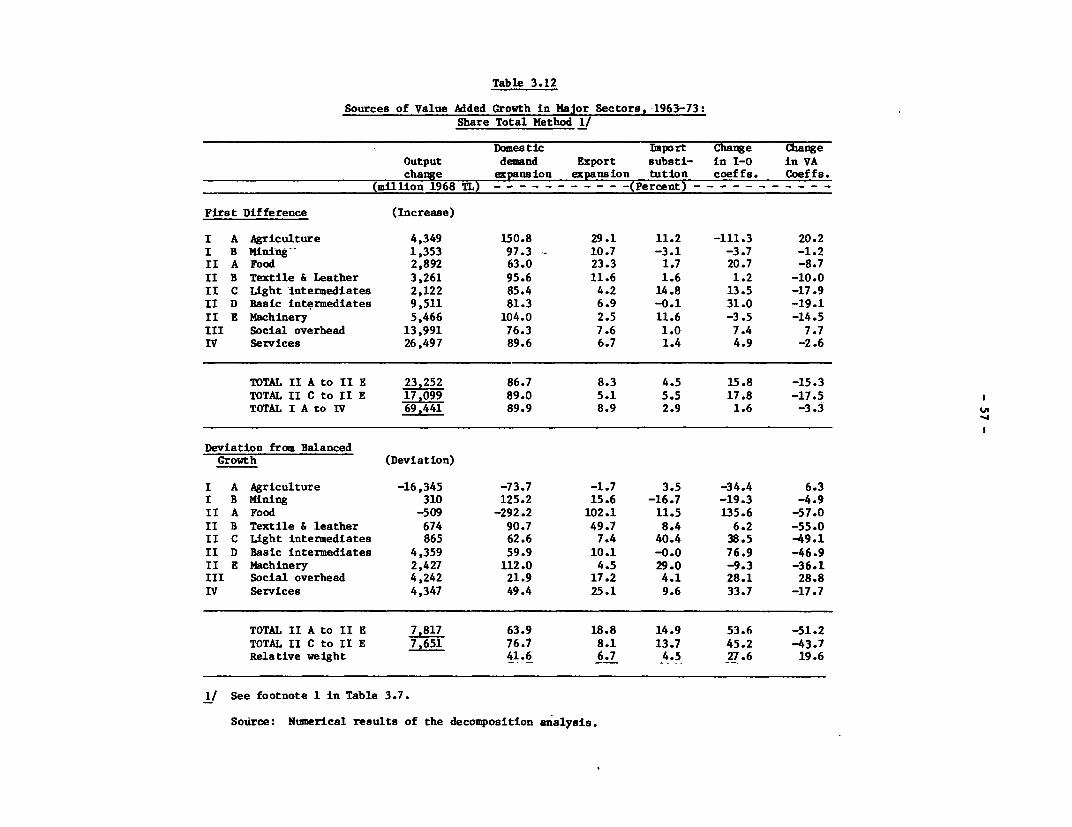

G. Sources of Import Growth by Commodity.....#* ....... 52H. Decomposition of Value Added ....................... oo56I. Sources of Turkish Industrialization in

the Light of Experience Elsewhere:An Overview.oooo.~.oo.o* .. o.o.- 58

4. SOURCES OF CHANGES IN FACTOR USESAND RELATIVE PRICES .............. ...... ..... . .... . ... o 64

A. Historical Patterns of Employment andProductivity Growth.*....,...*** .. . . ... .. .o.64

B. Sources of Changes in Employment..o..o.....oo.e..o 70C. Sources of Changes in Investment

Requirementsoooo -oo.. .. s...0.. 76D. Sources of Changes in Relative

Sectoral Prices..ooo .. e .. 80E. Domestic Price Distortions, Labor Reallocation

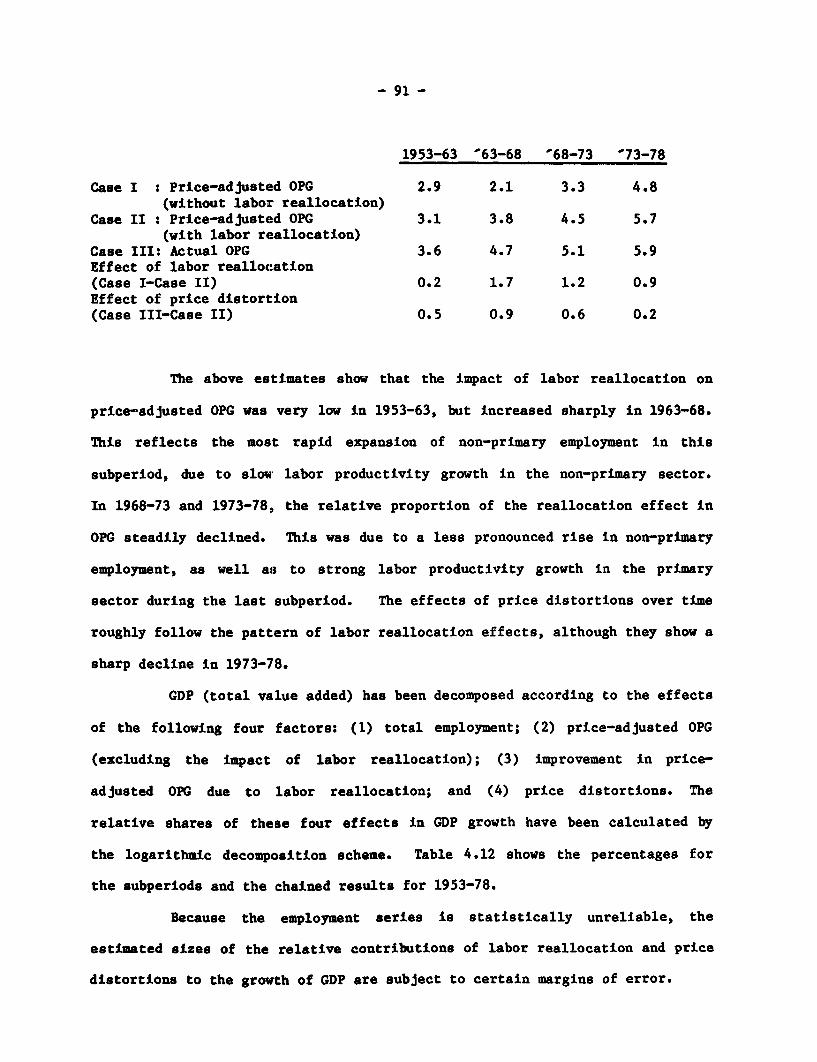

and Value Added Growth Rates 87

vi

Page

5. STRUCTURAL CHANGE IN THE MANUFACTURING SECTOR ............... 96

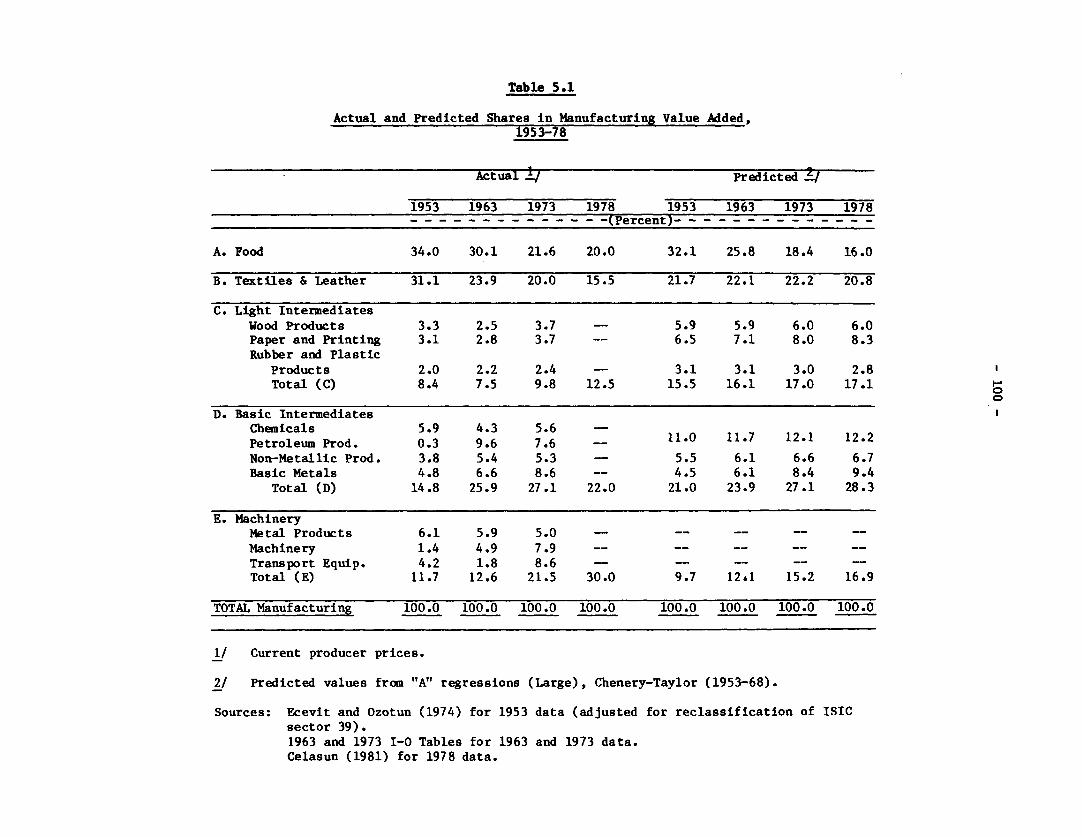

A. Actual and Predicted Patterns inManufacturing Output....................................... 96

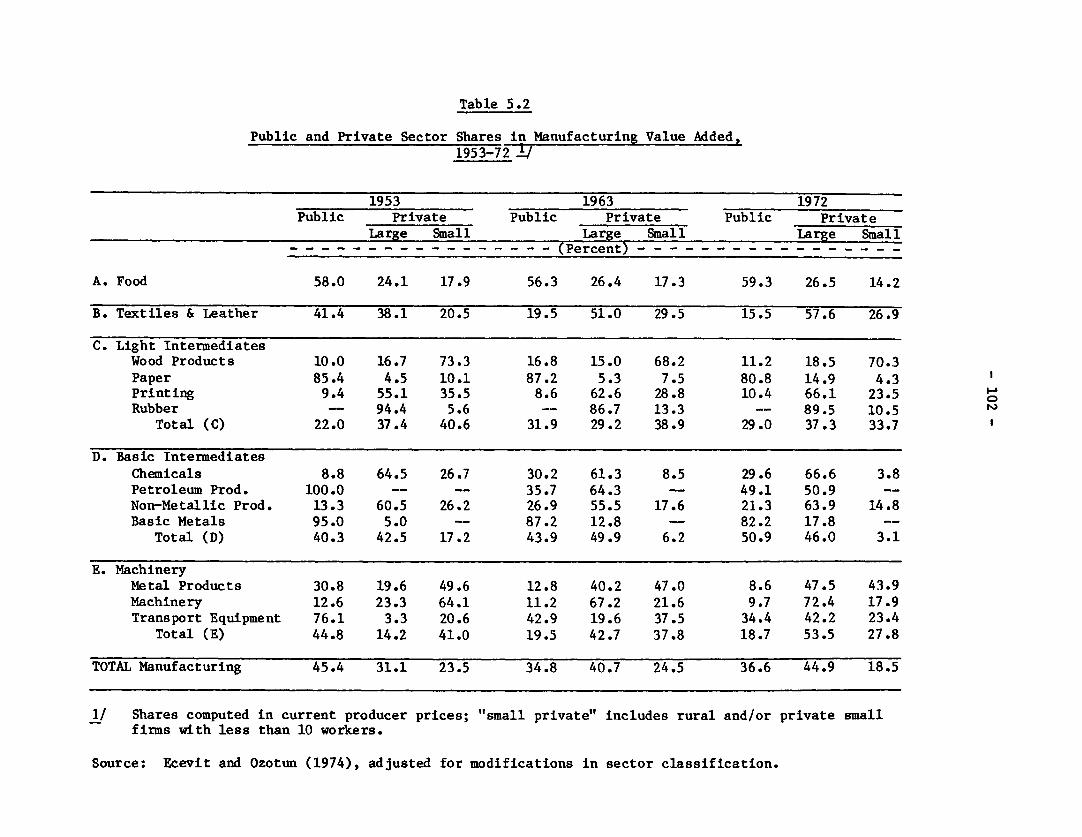

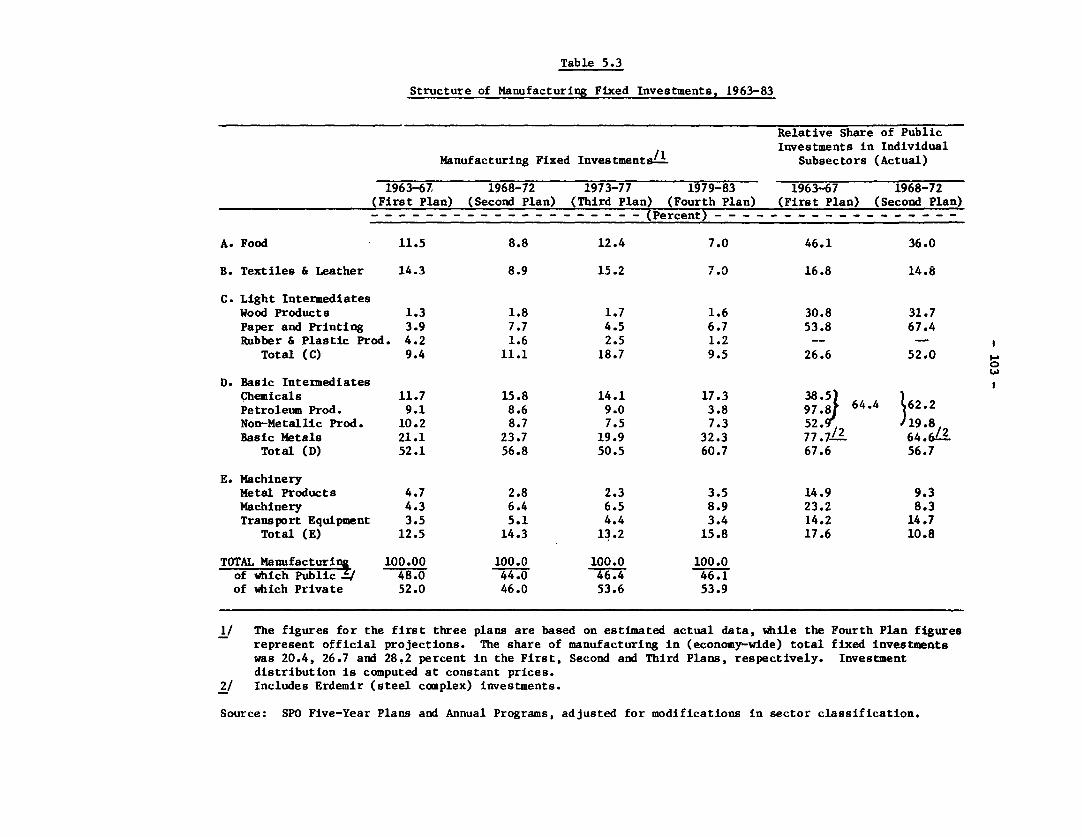

B. Patterns of Public and PrivateShares in Turkish Manufacturingo.......... ... ........ .101

6. TOWARD TRADE-ORIENTED GROWTH AND STRUCTURAL CHANGEIN THE 188...........................,1

A. Trade Effects on Turkish Industrialization.............,llB. Prospects for Transition....... . . ...... .. .. ..... .. . ... .,,117C. Future Research. .. . .. e e. .. . . .. . .. *.. . ,,125

REFERENCES 122

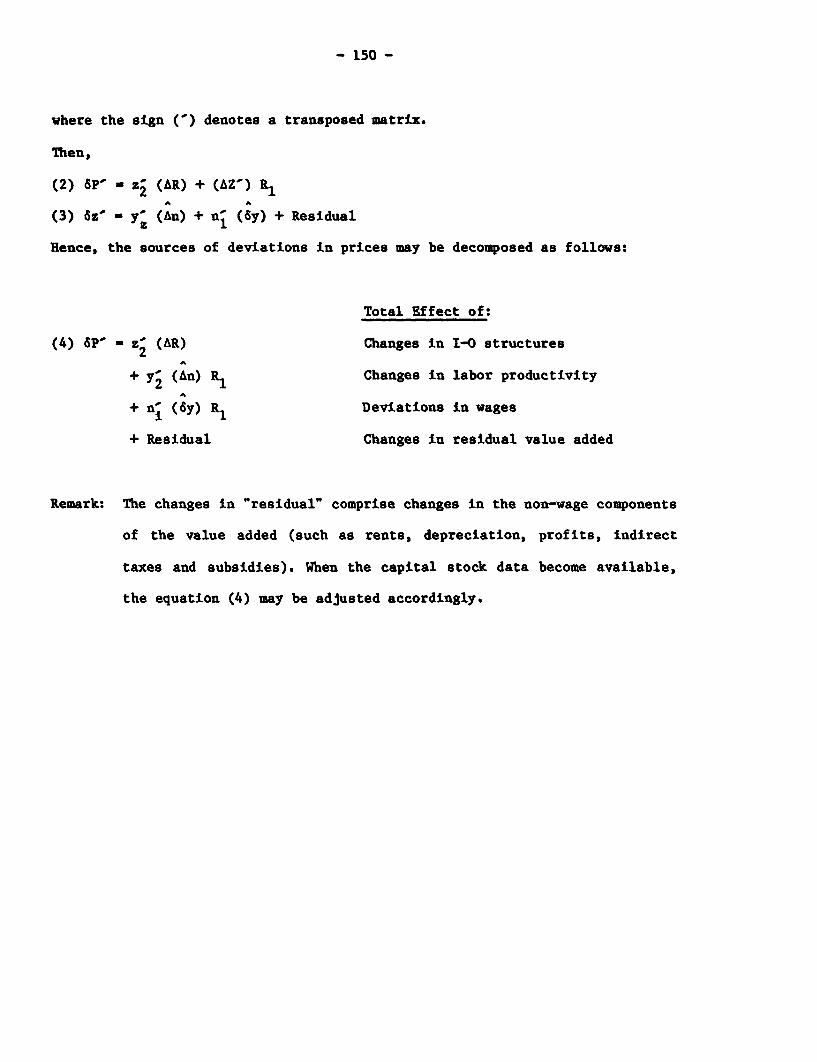

APPENDIX 1. MODELS FOR SOIURCES OF GROWTH DECOMPOSITION ....... ..... 132

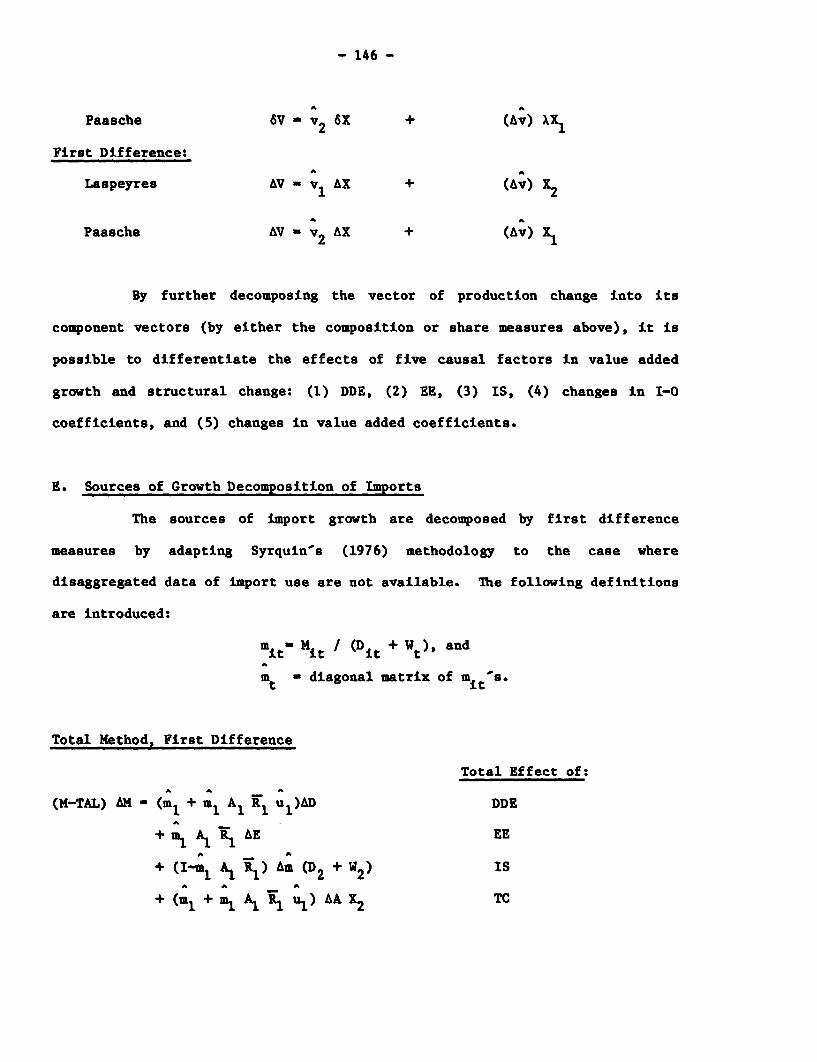

A. Methodology in Brief. . . . . .. .. o .o oo.o . o.,,132Be Notationo ooooooooooesossooooooo..138C. Sources of Growth Decomposition of

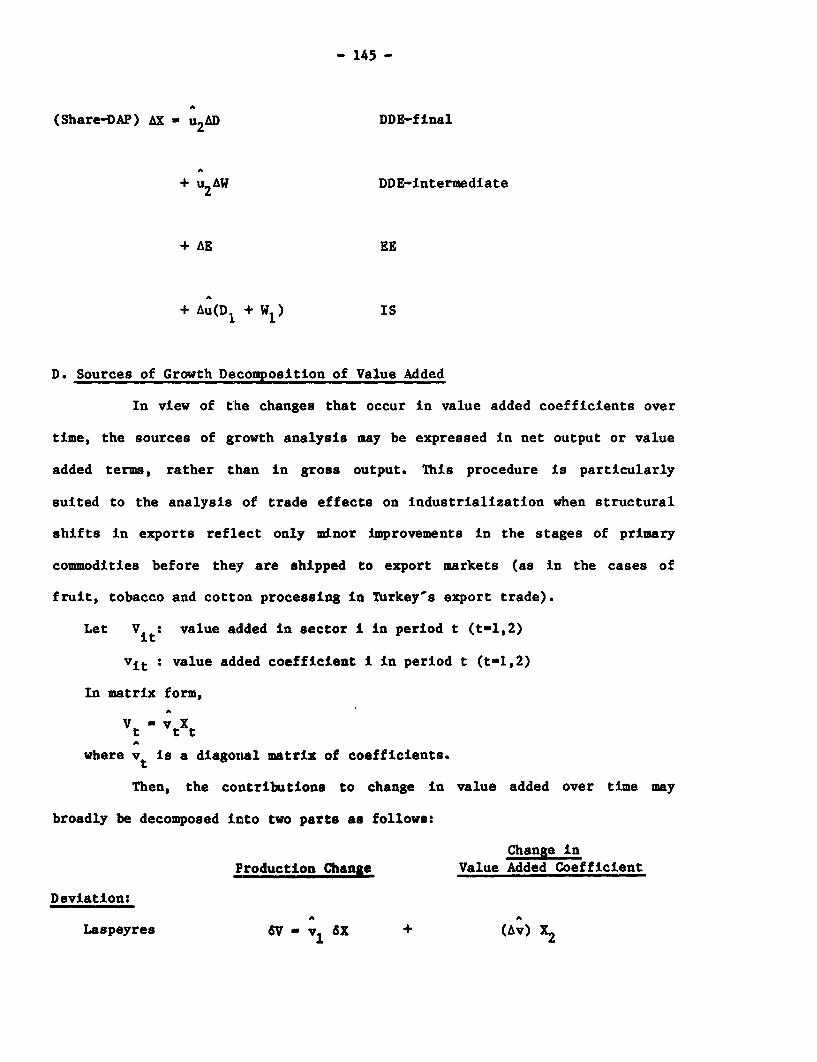

Production (Gross Output)ooooo..o...ooo......o..... .139D. Sources of Growth Decomposition of

Value Added oosoooooooo..o.o.o .o..145E. Sources of Growth Decomposition

of Importso.ooo.o..ooooo..ooo..oo..oo.oo..o.oo... a,146

F. Sources of Growth Decompositionof Primary Factors. ... . oo.o. oo o..o oo .. o...,147

G. Sources of Changes in Relative SectorPriceso osooooooooooooooesooo...149

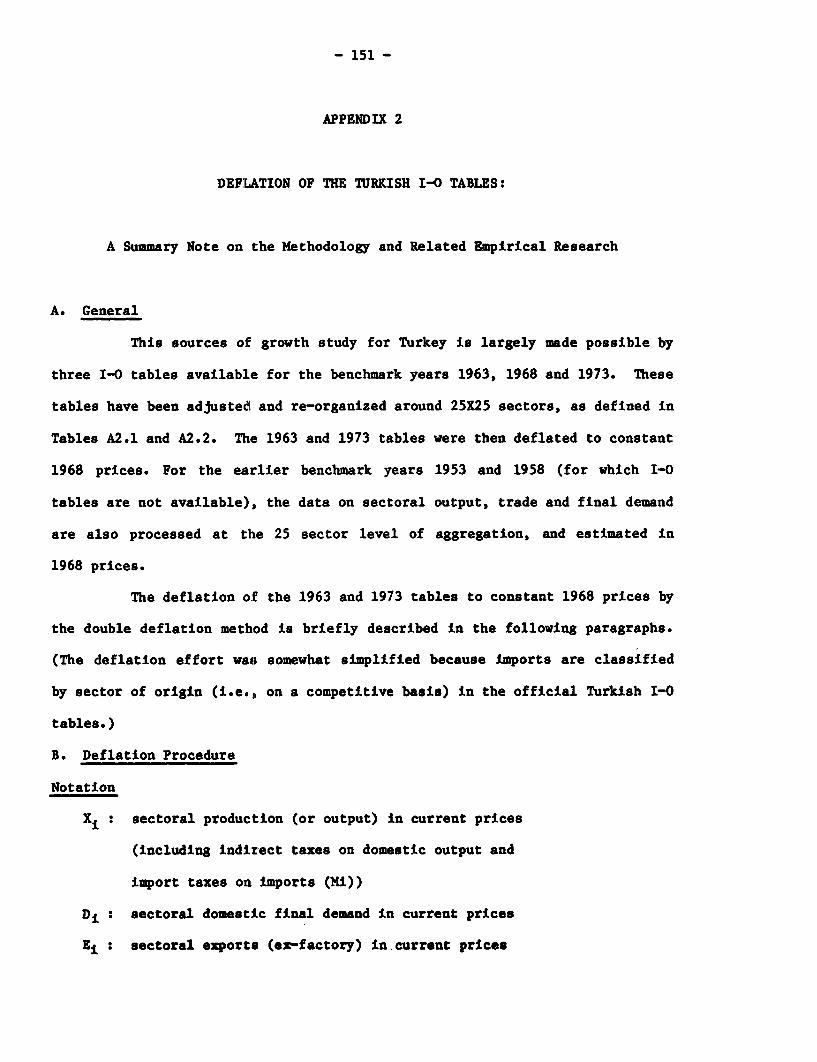

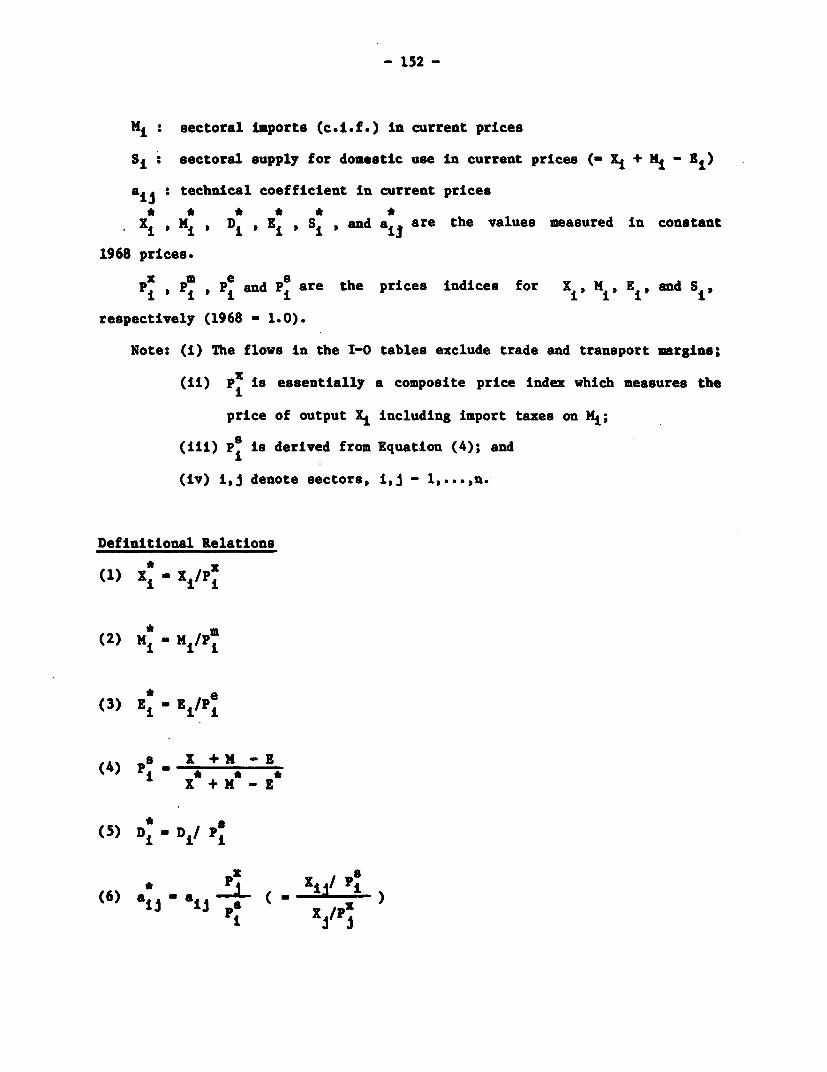

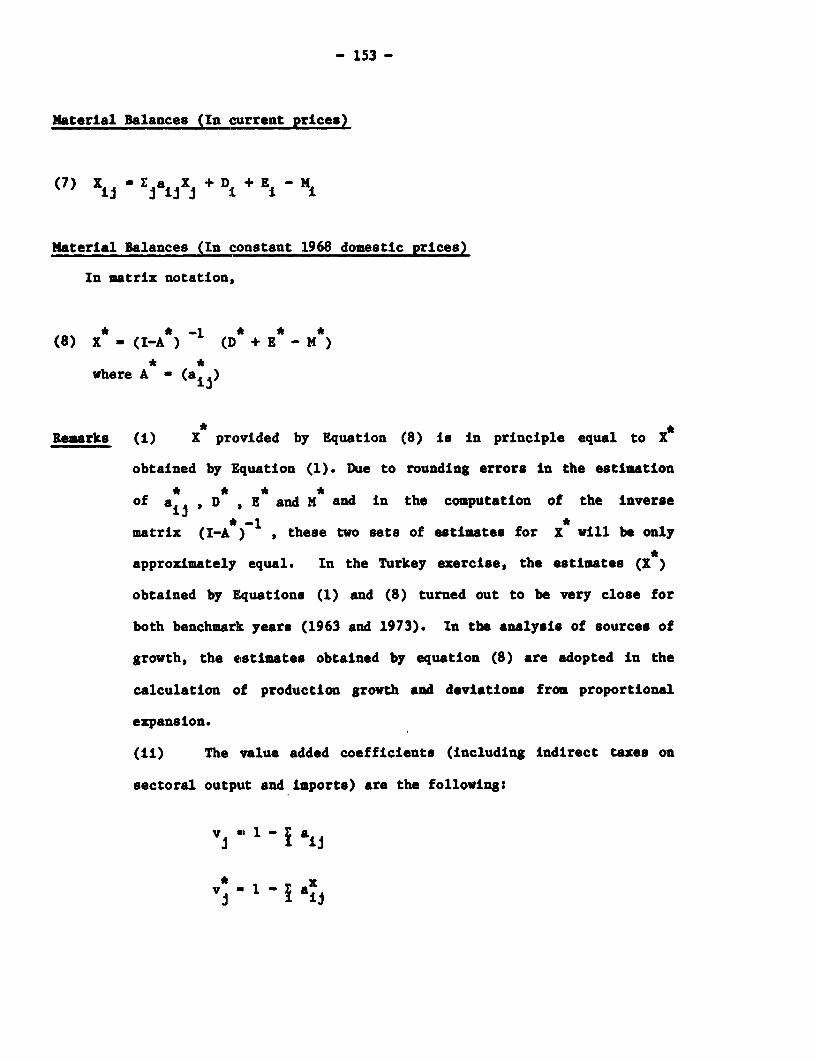

APPENDIX 2. DEFLATION OF THE TURKISH I-0 TABLES ..... ,.oo.........151

Ao Generalosoo oooosooooooosoooooo...151B. Deflation Procedure. . . . . .. ooo.o. oo oe. oo.o o151C. Construction of Trade Price Indiceso...ooo. 1.o... o.ol54

D. Construction of Price Indices forProduction and Supply..o... .. . . . o o. oo o..ooo.157

vii

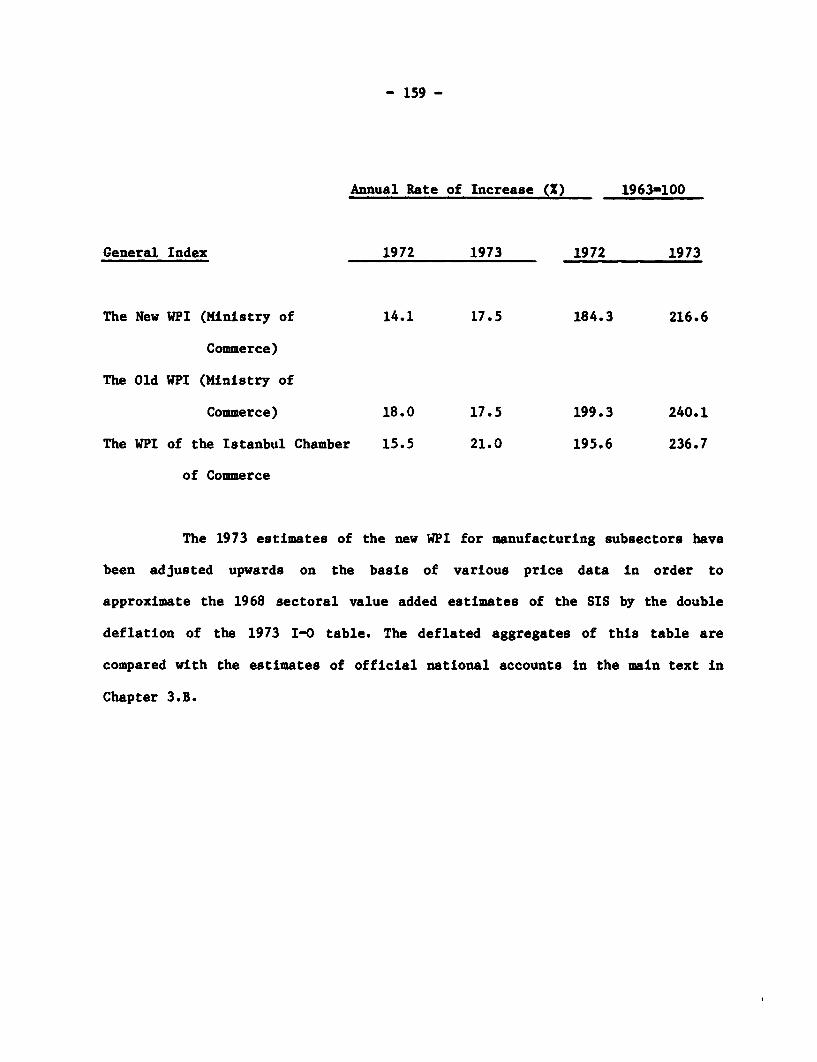

LIST OF TABLESPage

Chapter 1

1.1 Major Economic Indicators, 1923-73... .................. .... 99.9..5

Chapter 2

2.1 Resource Accumulation and Allocational Processes, 1953-78 ...... 16

2.2 Demographic and Income Distributional Processes, 1953-78 ....... 17

Chapter 3

3.1 Value Added Estimates in the Deflated Input-Output (I-O) andNational Accounts (NY) Data Systems, 1963 and 1973 ............. 26

3.2 Variation in Aggregate Trade Ratios Over Time, 1953-78.........30

3.3 Growth in Sector Output, 1953-73...............................32

3.4 Trade by Major Sectors, 1953-73................................33

3.5 Sources of Growth and Structural Change in Gross Output,1953-73: A Summary of Aggregate Results (Alternate Measures)...35

3.6 Sources of Growth in Value Added, 1963-73: A Summary ofAggregate Results (Total Measures) ............................ 39

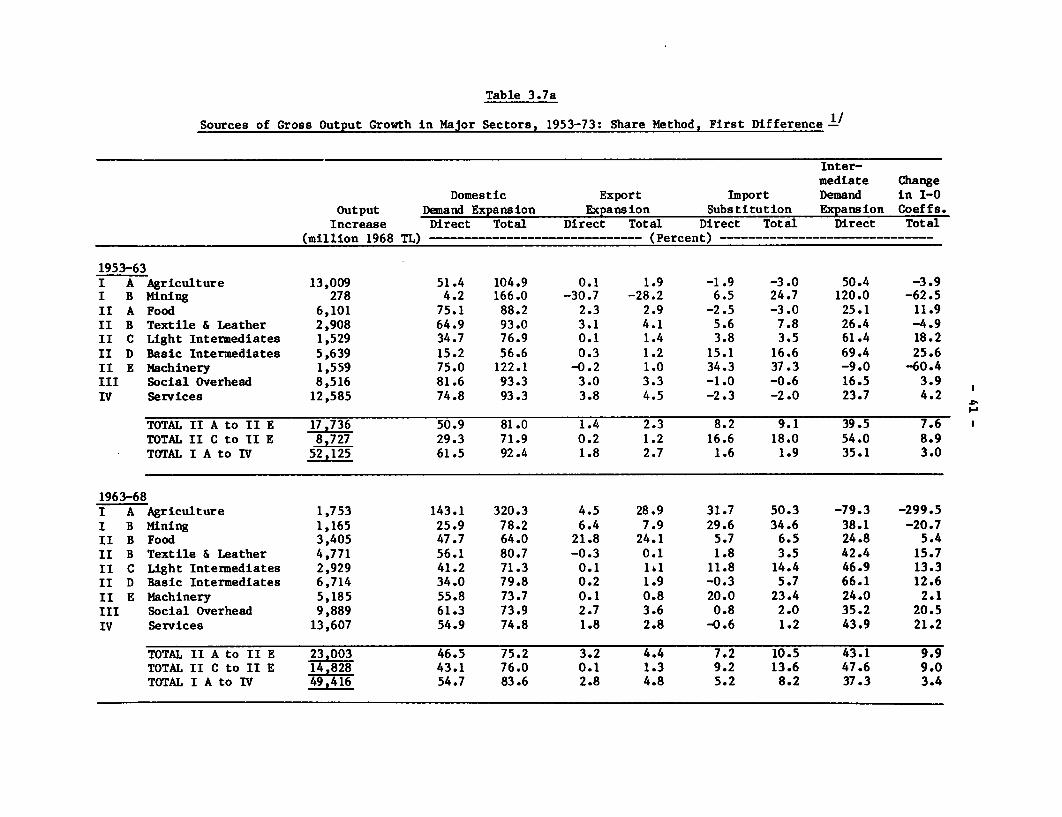

3.7 Sources of Gross Output Growth in Major Sectors, 1953-73:Share Method, First Difference * o ** * o ..............................o..............40

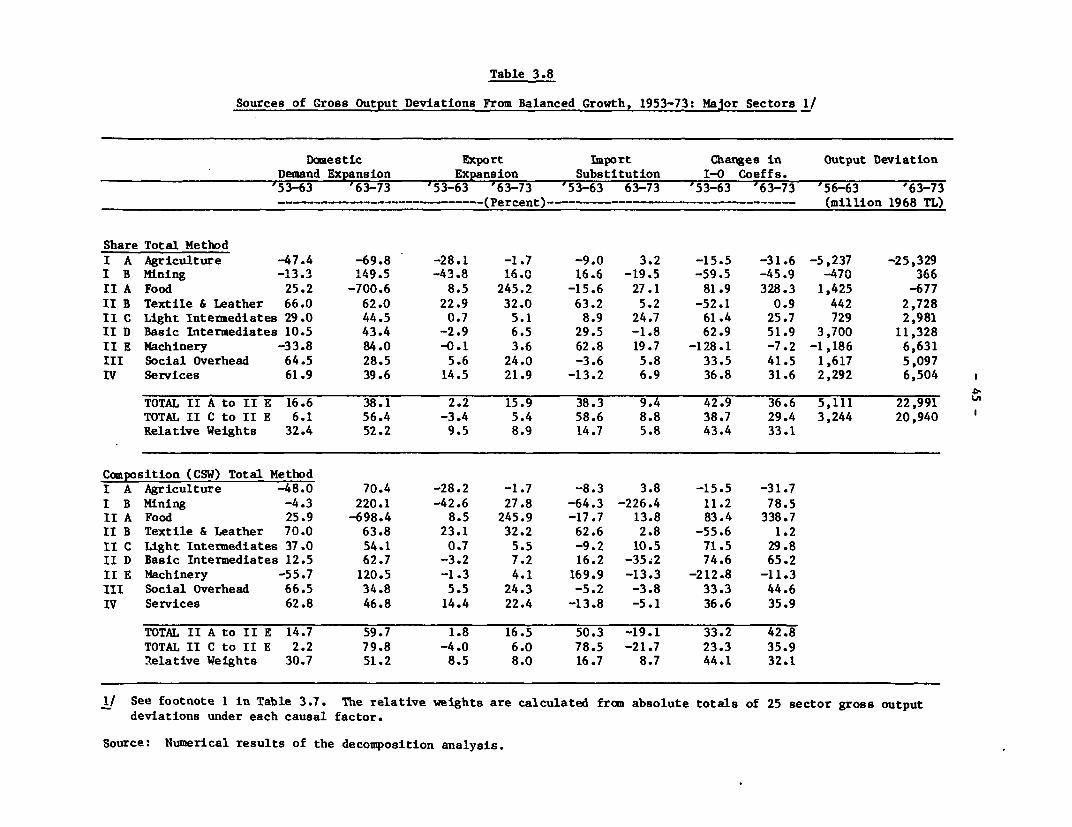

3.8 Sources of Gross Output Deviations from BalancedGrowth, 1953-73: Major Sectors............ ....................... 45

3.9 Sources of Gross Output Growth in Manufacturing, 1953-73:Share Total Method, First Difference...........................50

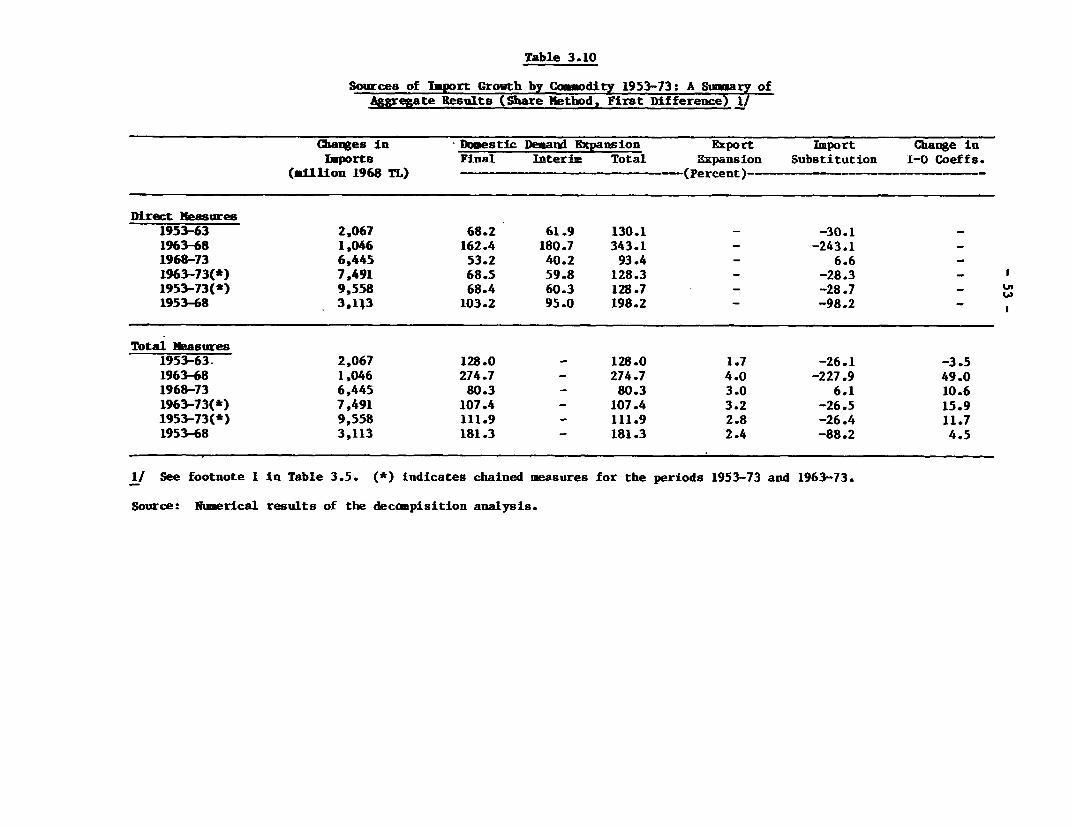

3.10 Sources of Import Growth by Commodity, 1953-73: A Summaryof Aggregate Results (Share Method, First Difference) ...... 53

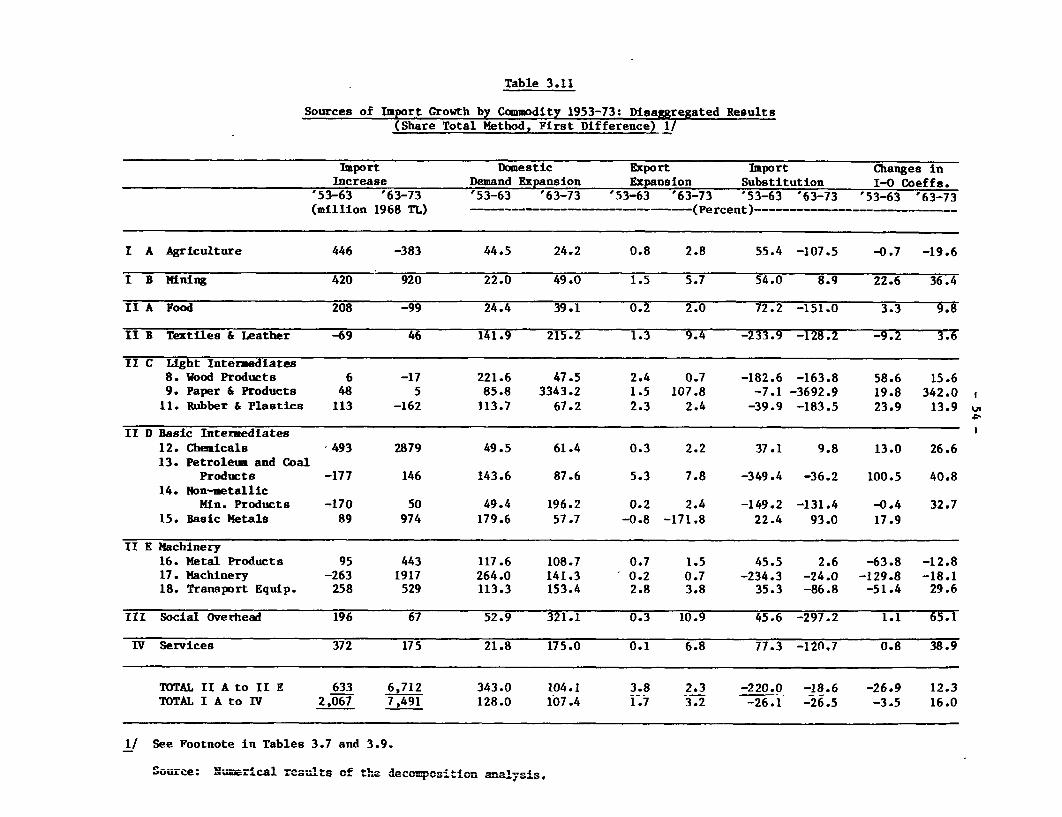

3.11 Sources of Import Growth by Commodity, 1953-73: Disag-gregated Results (Share Total Method, First Difference)........ 54

3.12 Sources of Value Added Growth in Major Sectors, 1963-73:Share Total Method..........................

3.13 A Summary of Measures for Sources of Growth in Manufacturing,1953-73: Share Total Method, First Difference................. 60

3.14 Sources of Manufacturing Gross Output Deviation fromBalanced Growth: An Inter-Country Comparison (Based onShare Total Method, Deviation). e .9.61

viii

Page

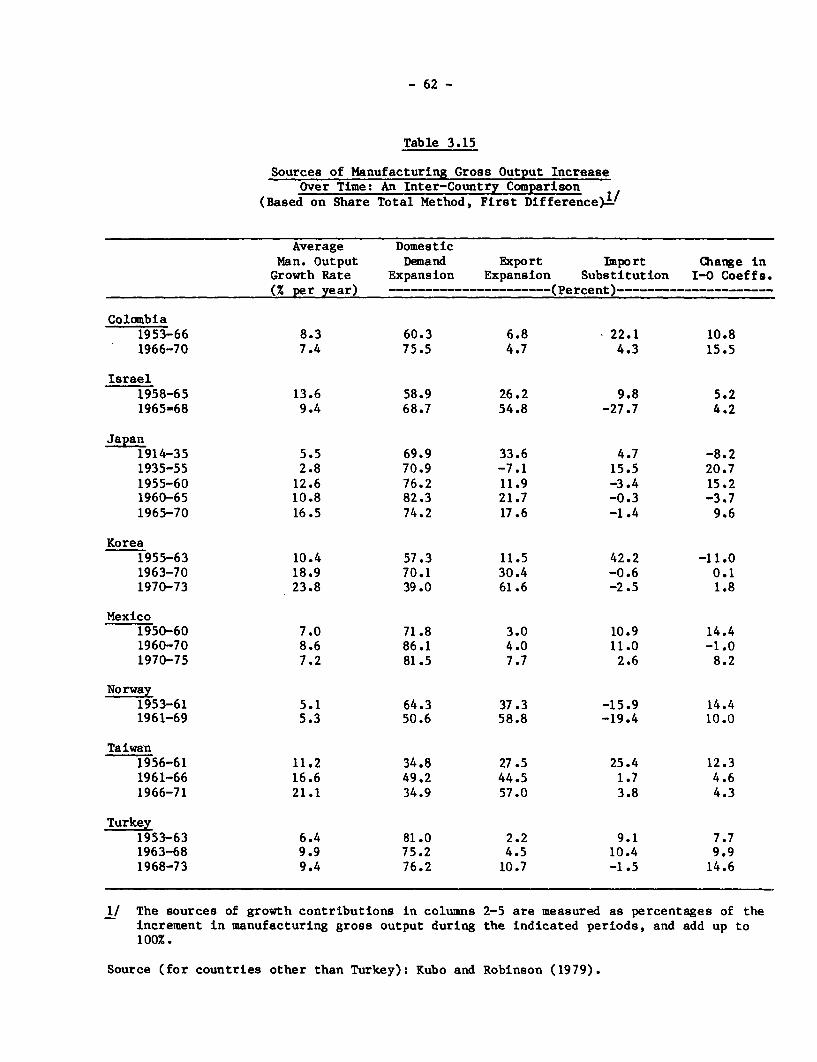

3.15 Sources of Manufacturing Gross Output Increase Over Time:An Inter-Country Comparison (Based on Share TotalMethod, First Difference). .... ... . .. . . ... . . . . . . . . . . .* . ** * ** * 62

Chapter 4

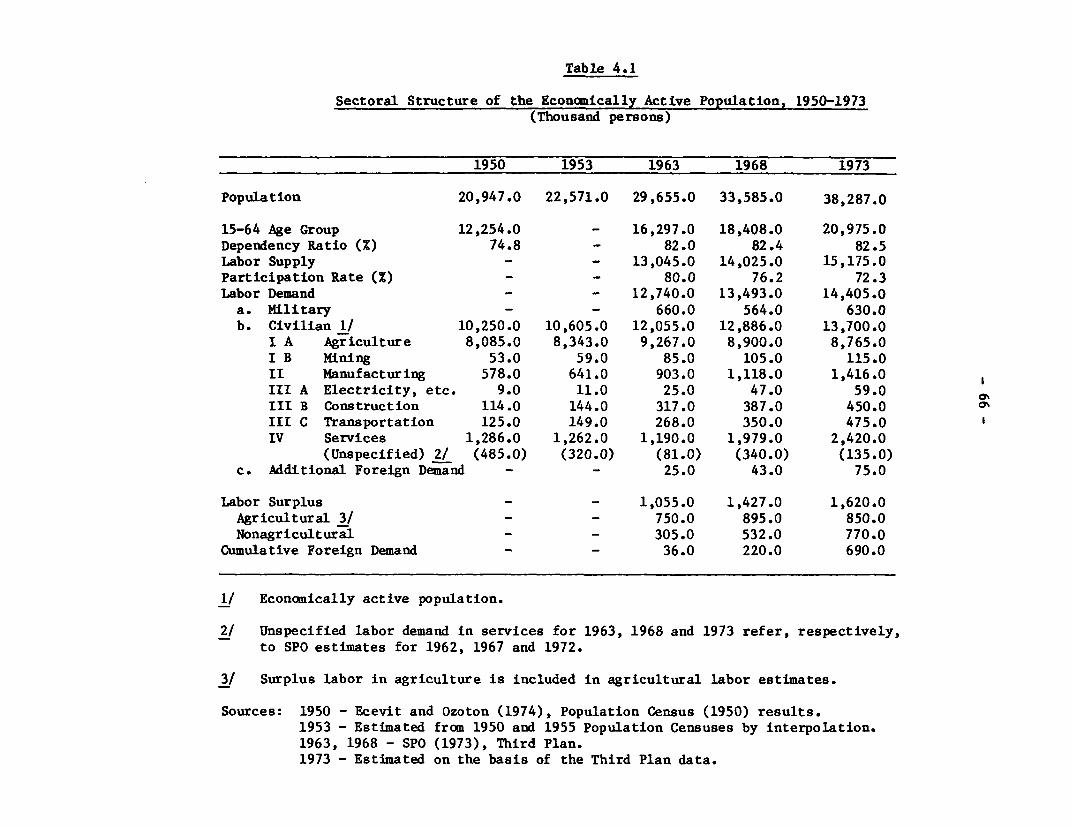

4.1 Sectoral Structure of the Economically Active Population,1950-71o ... o...so... o e....so... o......................... 6

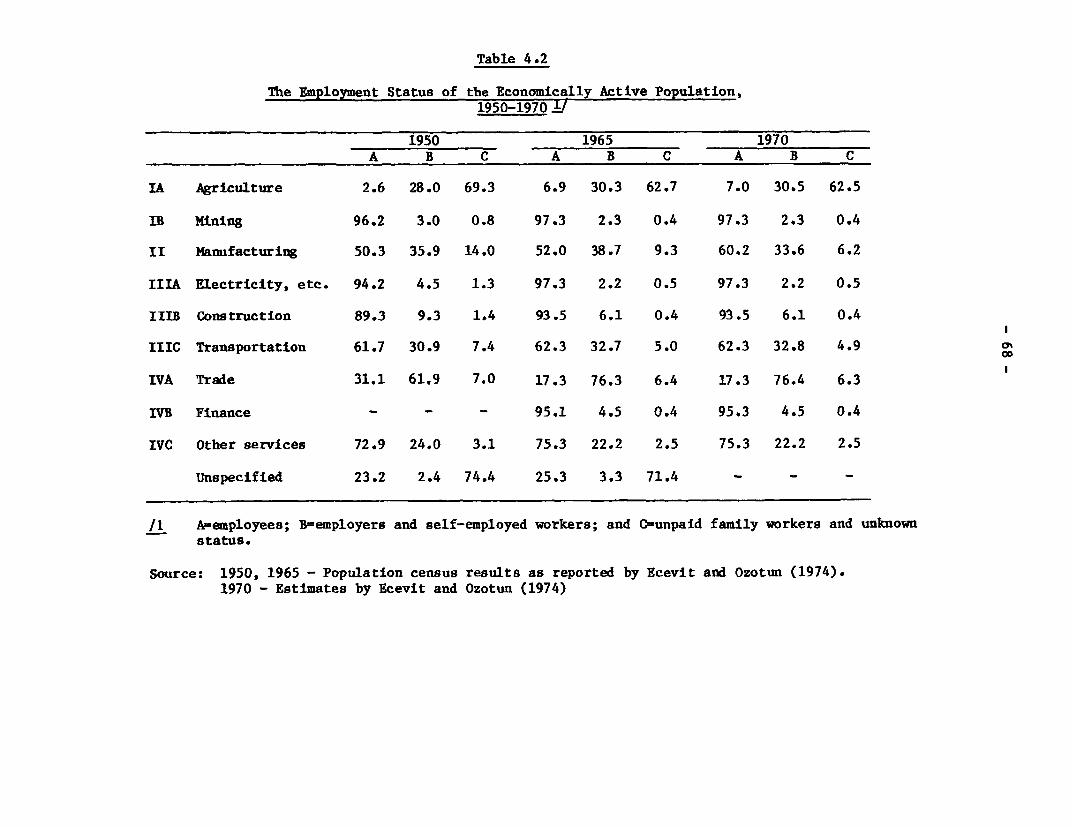

4.2 The Employment Status of the Economically Active Population,1950-70o ... o..*.... o....so... *e.o... oooo........................68

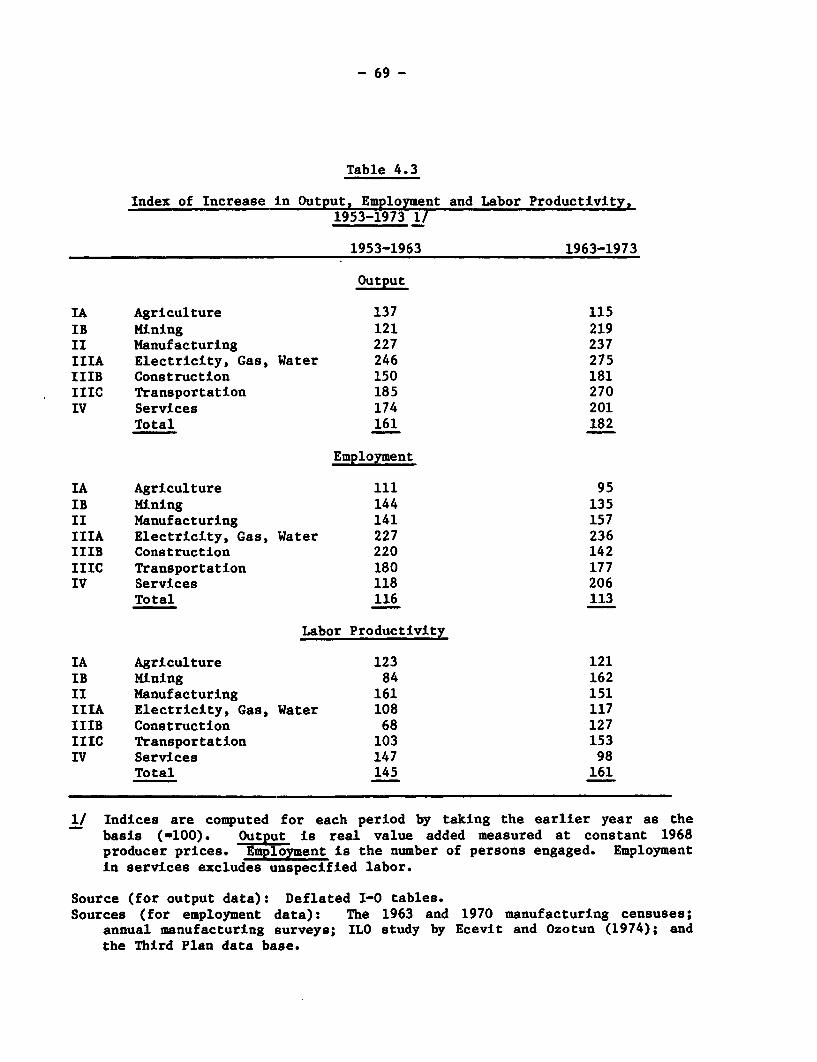

4.3 Index of Increase in Output, Employment and LaborProductivity, 1953-73 .... .................. ...... .69

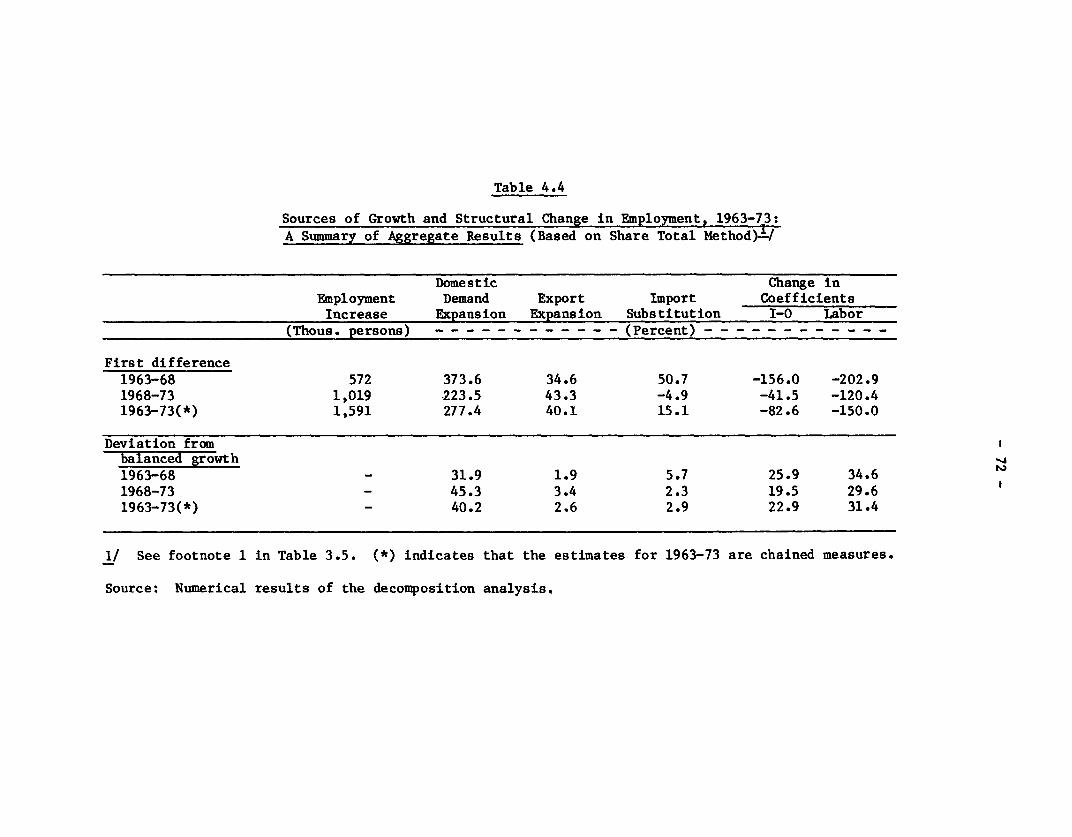

4.4 Sources of Growth and Structural Change in Employment,1963-73: A Summary of Aggregate Results (Based on ShareTotal Method) ............

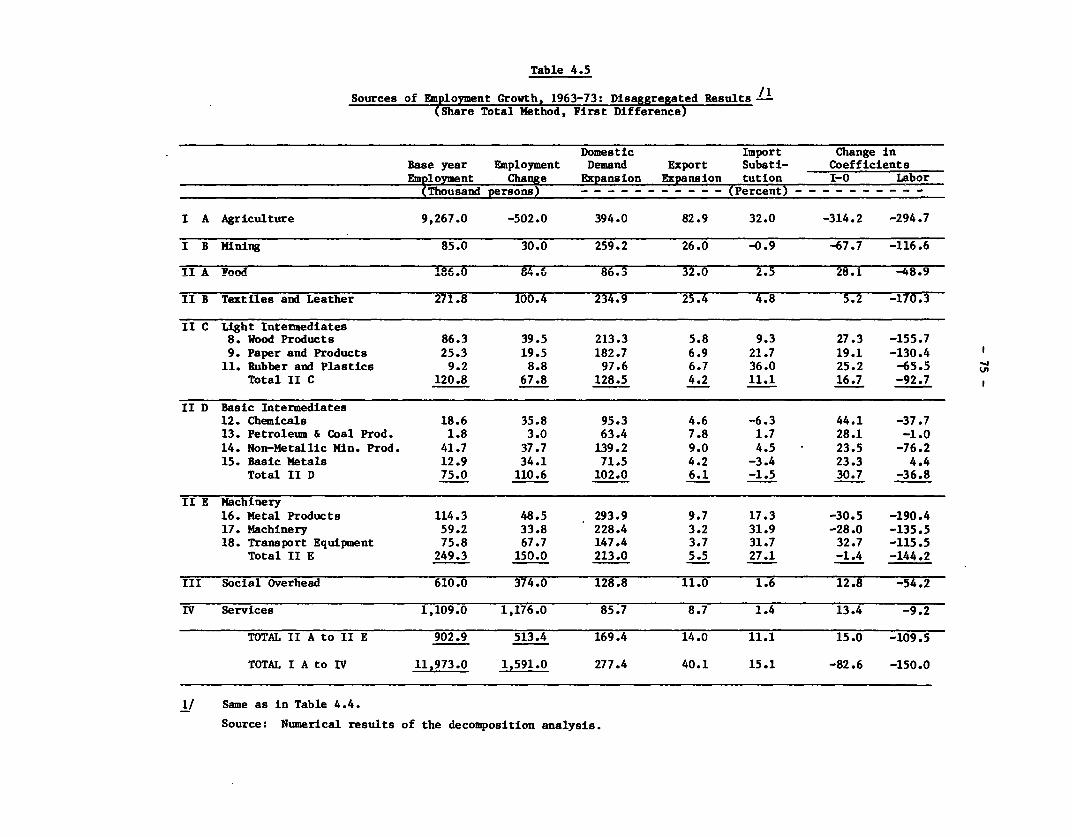

4.5 Sources of Employment Growth, 1963-73: Disaggregated Results(Share Total Method, First Difference)........................75

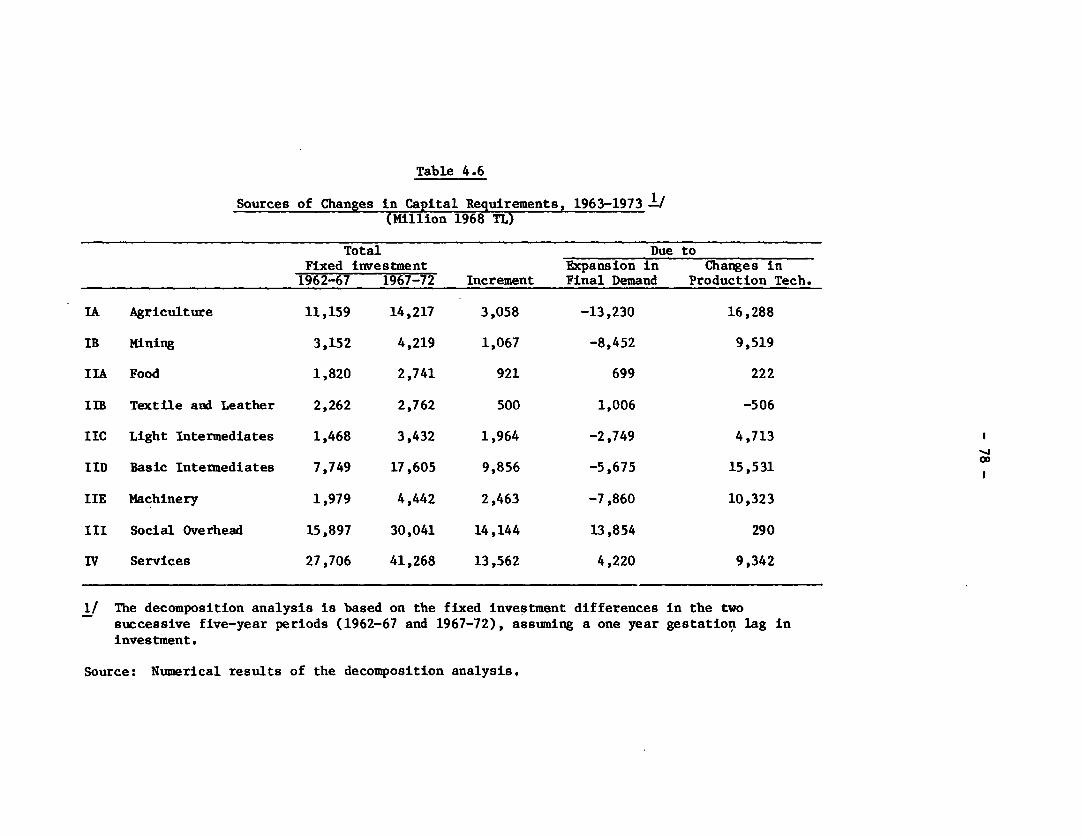

4.6 Sources of Changes in Capital Requirements, 1963-73............78

4.7 Incremental Capital-Output and Capital-Labor Ratios,

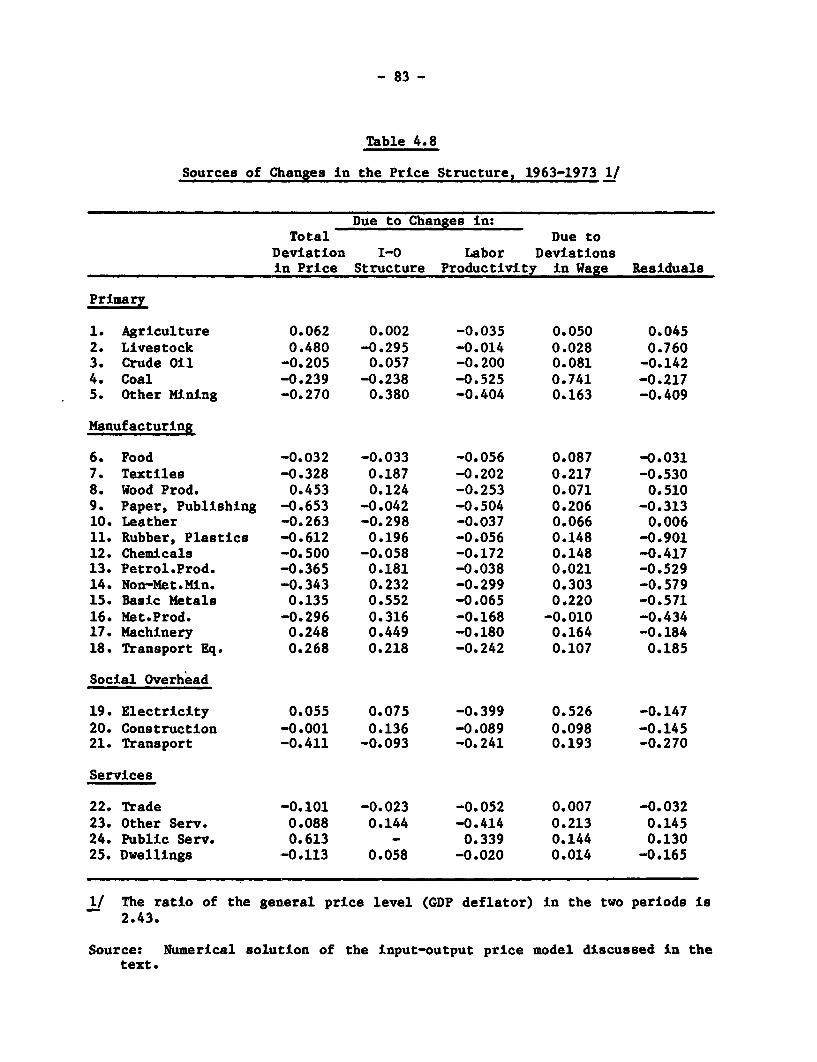

4.8 Sources of Changes in the Price Structure, 1963-73.. .ooos.o.83

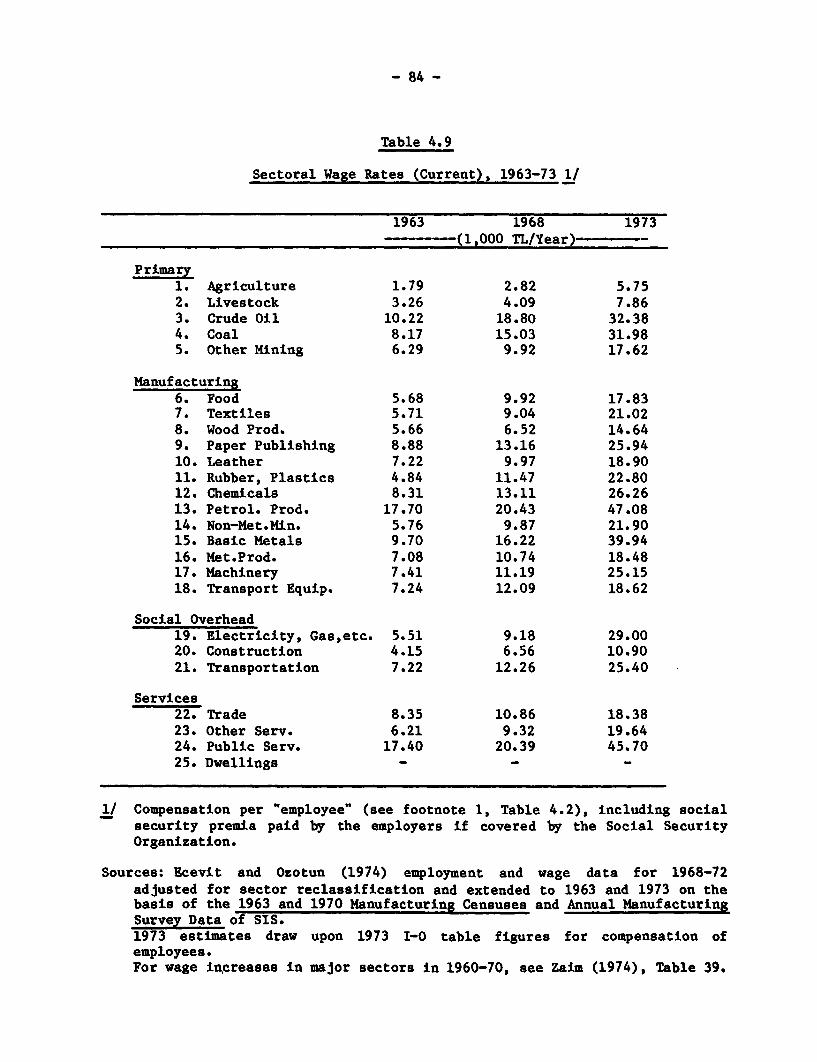

4.9 Sectoral Wage Rates (Current), 1963-73...84

4.10 Index of Intersectoral Wage Differentials, 1963-73. ..... o. .85

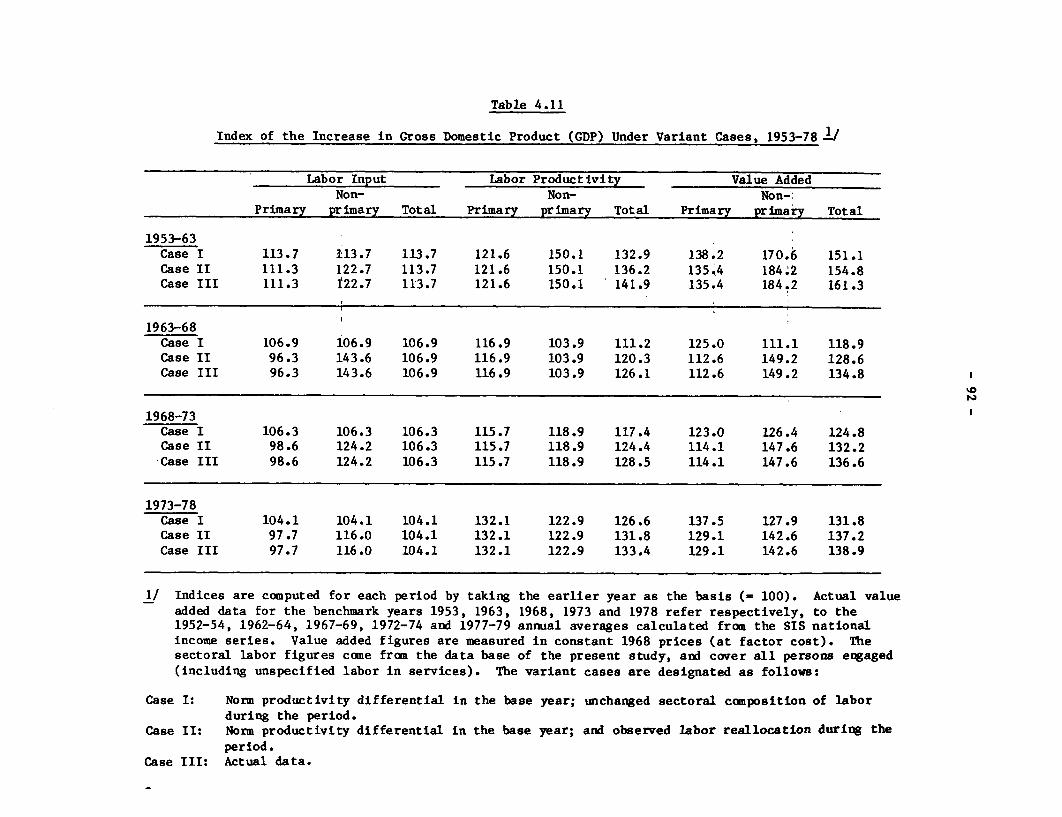

4.11 Index of the Increase in Gross Domestic Product (GDP)Under Variant Cases, 1953-78 . 92

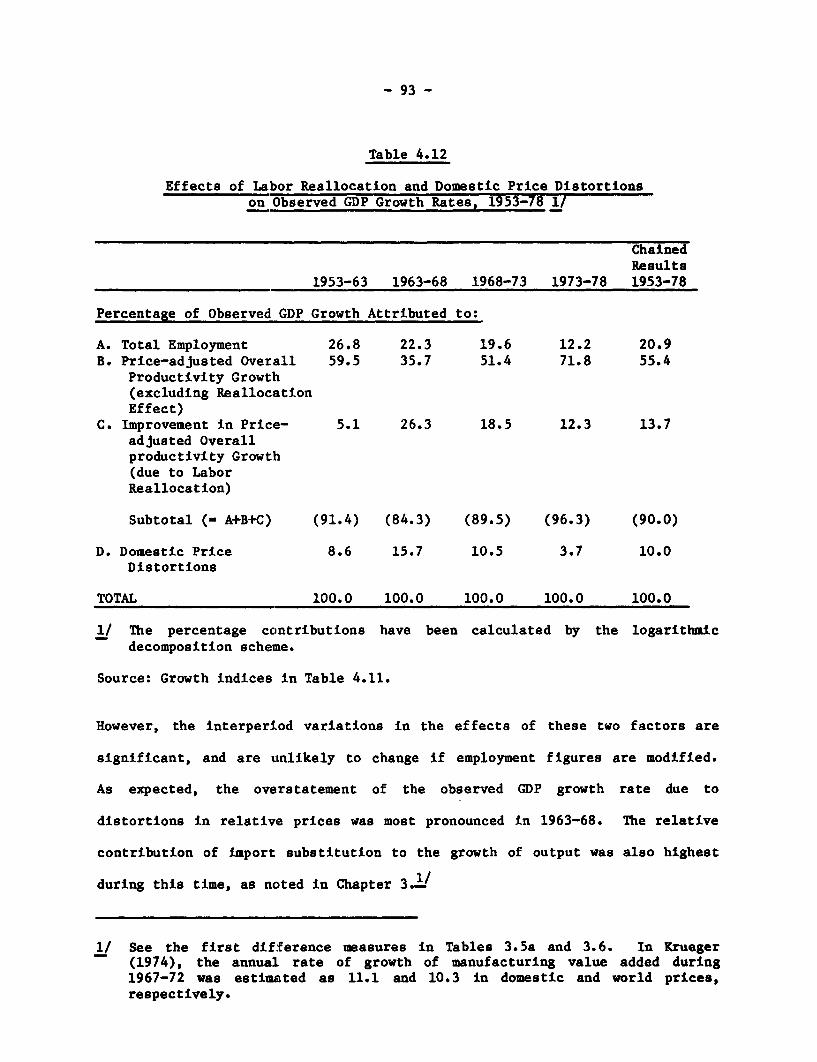

4.12 Effects of Labor Reallocation and Domestic PriceDistortions on Observed GDP Growth Rates, 1953-78 ...... ooo...93

Chapter 5

5.1 Actual and Predicted Shares in Manufacturing ValueAdded, 1953-78 .......

5.2 Public and Private Sector Shares in ManufacturingValue Added, 1953-72.........e................... . ..... 102

5.3 Structure of Manufacturing Fixed Investments, 1963-83 .... ... 103

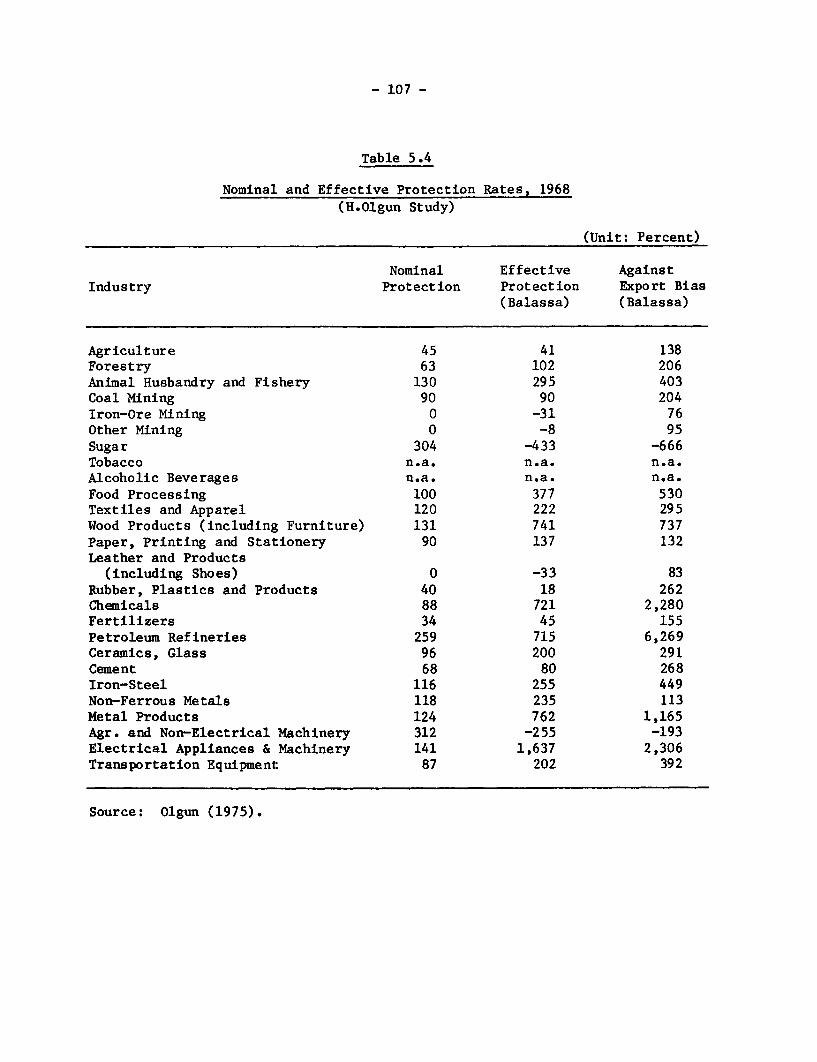

5.4 Nominal and Effective Protection Rates, 1968(R. Olgun Study) ........................ 107

ix

Page

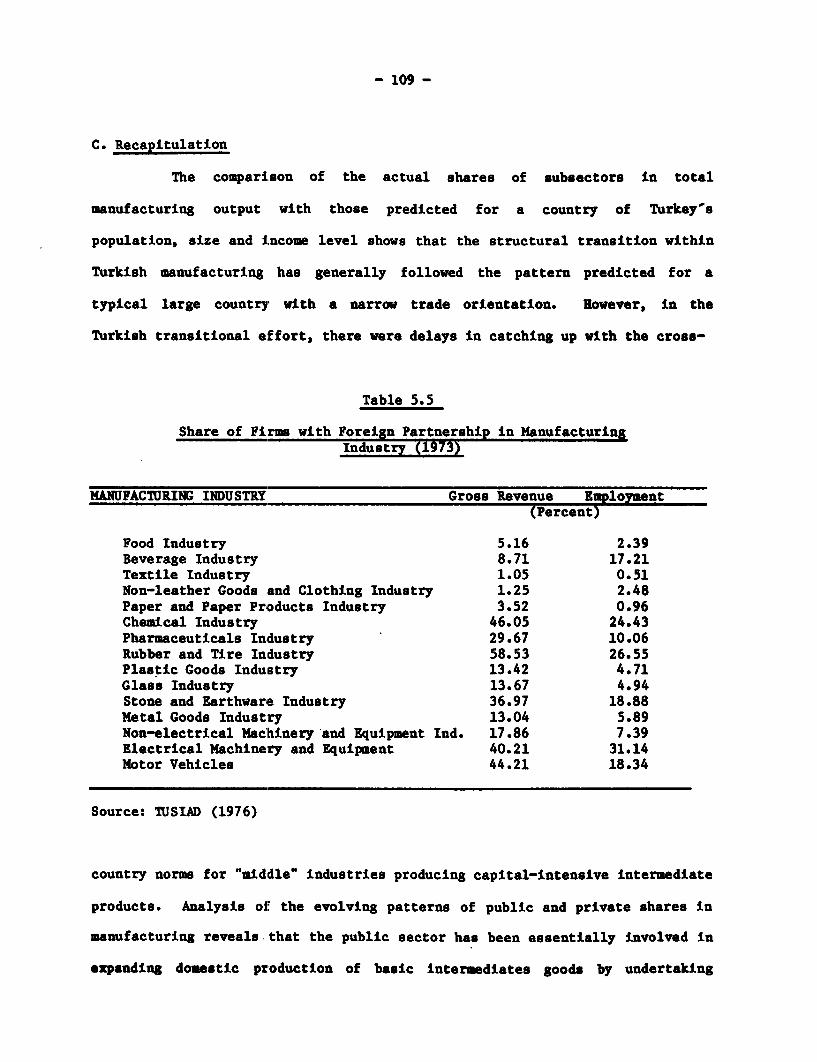

5.5 Share of Firms with Foreign Partnership in ManufacturingIndustry (1973)...............................................109

APPENDIX 2

2.1 Sector Classification (25 Sector Level)........................160

2.2 Major Sectors (9 Sector Level) ................................161

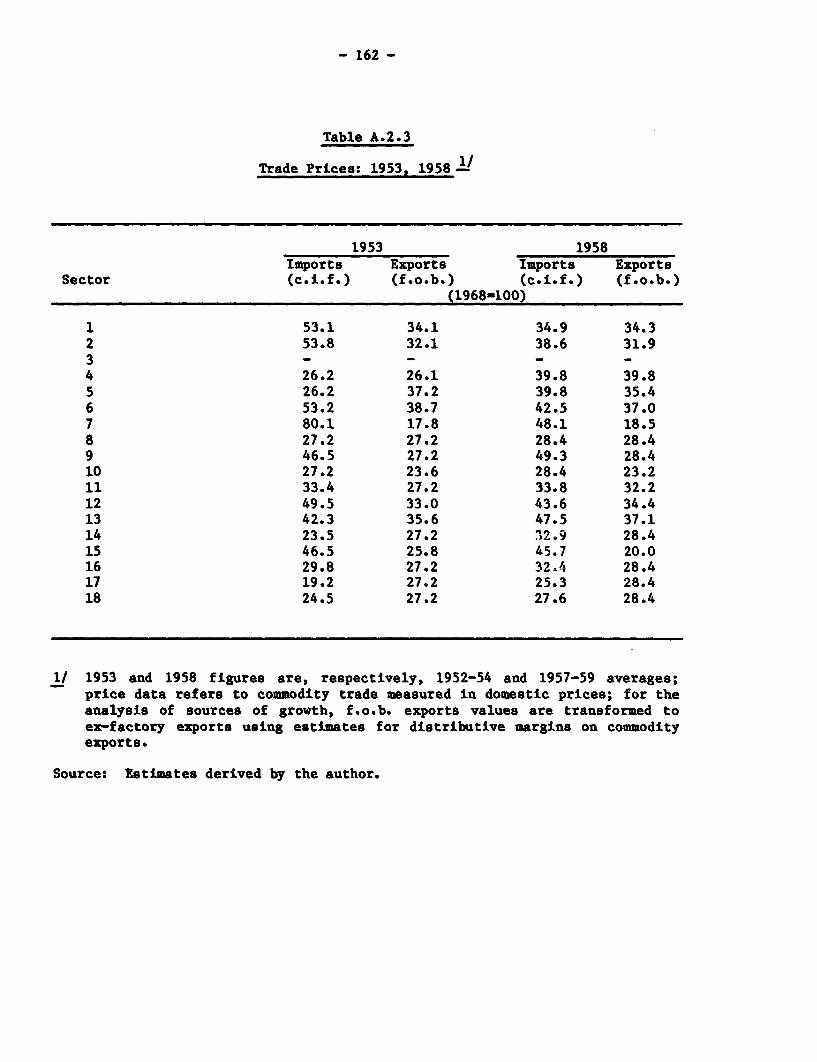

2.3 Trade Prices: 1953, 1958....* ...................... ..... 162

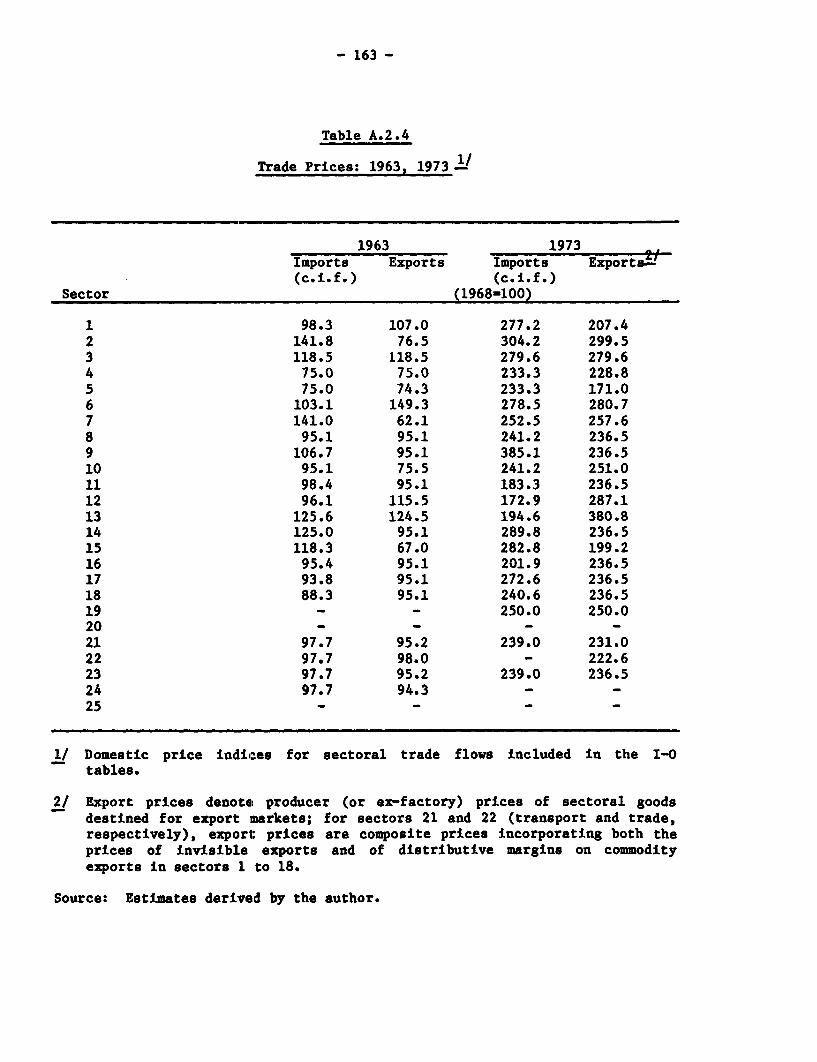

2.4 Trade Prices: 1963, 1973 ....... *so . .oo. 163

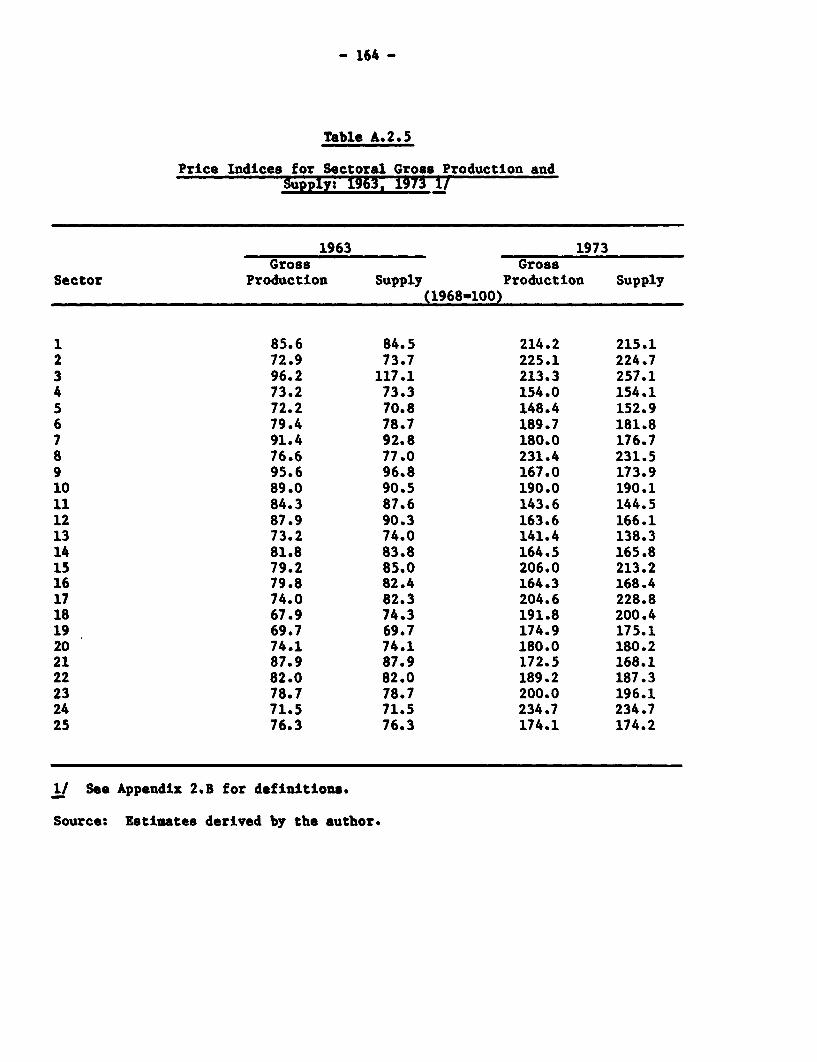

2.5 Price Indices For Sectoral Gross Production and Supply:1963, 1973oo. ... .o.o..oo... o ... oo................................... 164

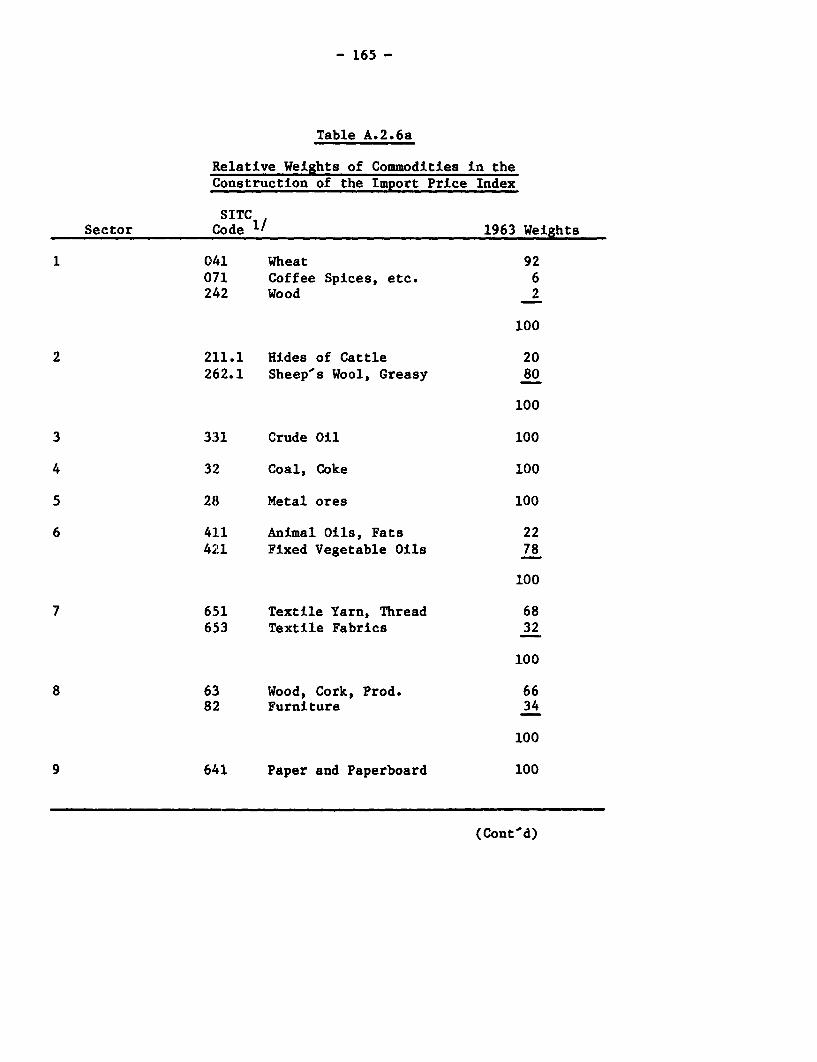

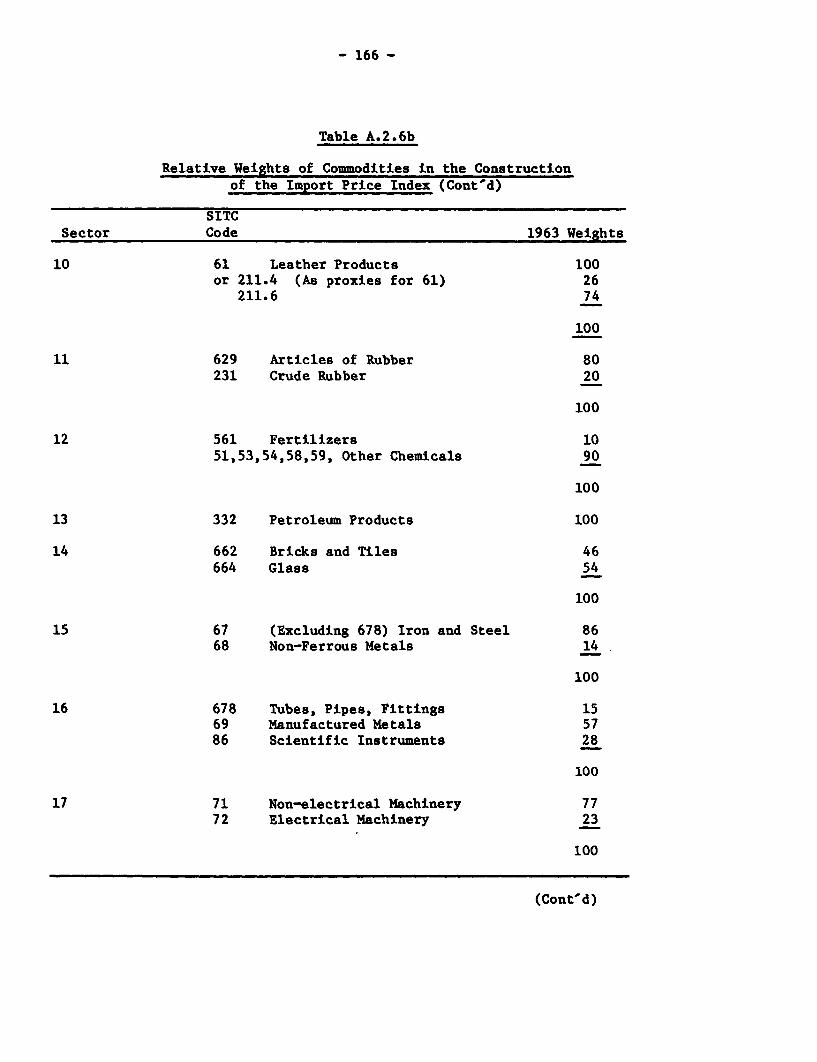

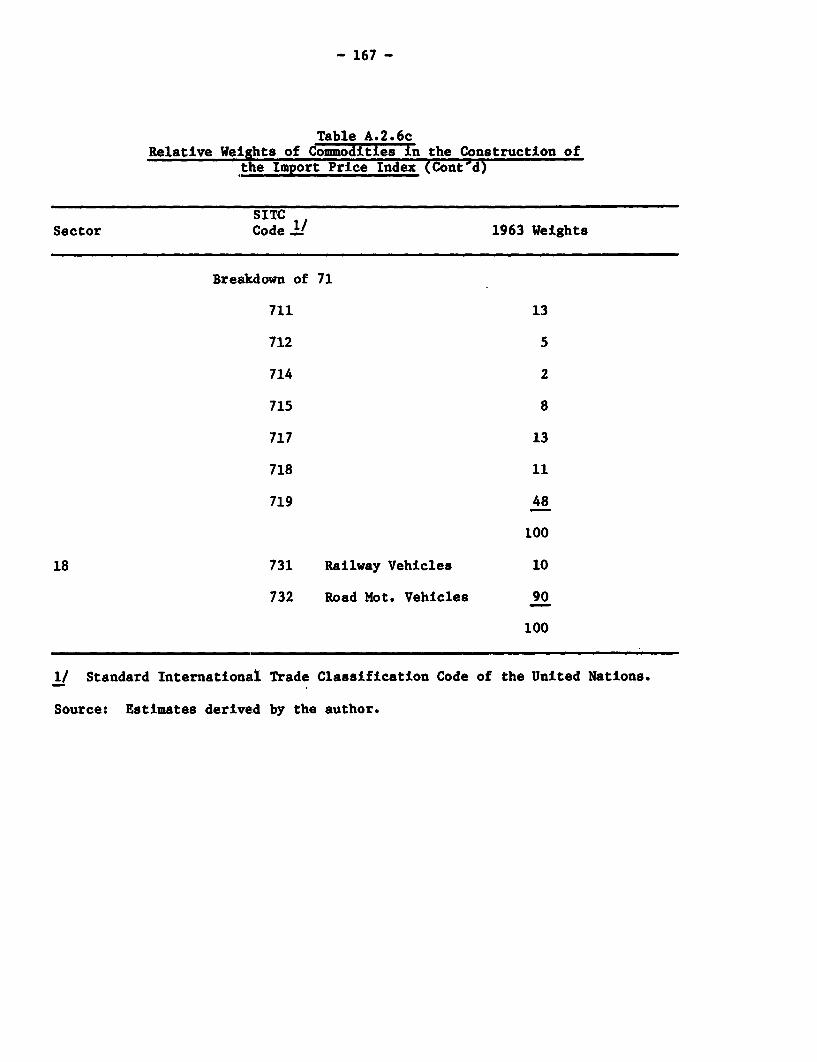

2.6 Relative Weights of Commodities in the Constructionof the Import Price Index ... ................................. 165

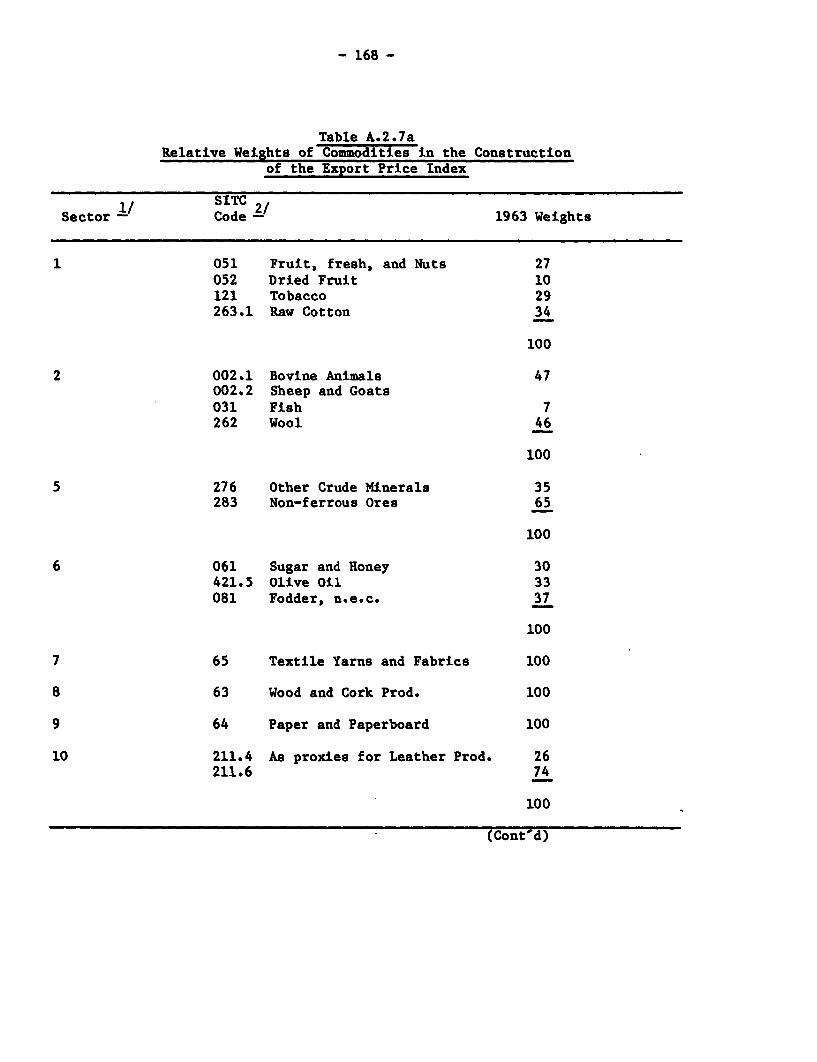

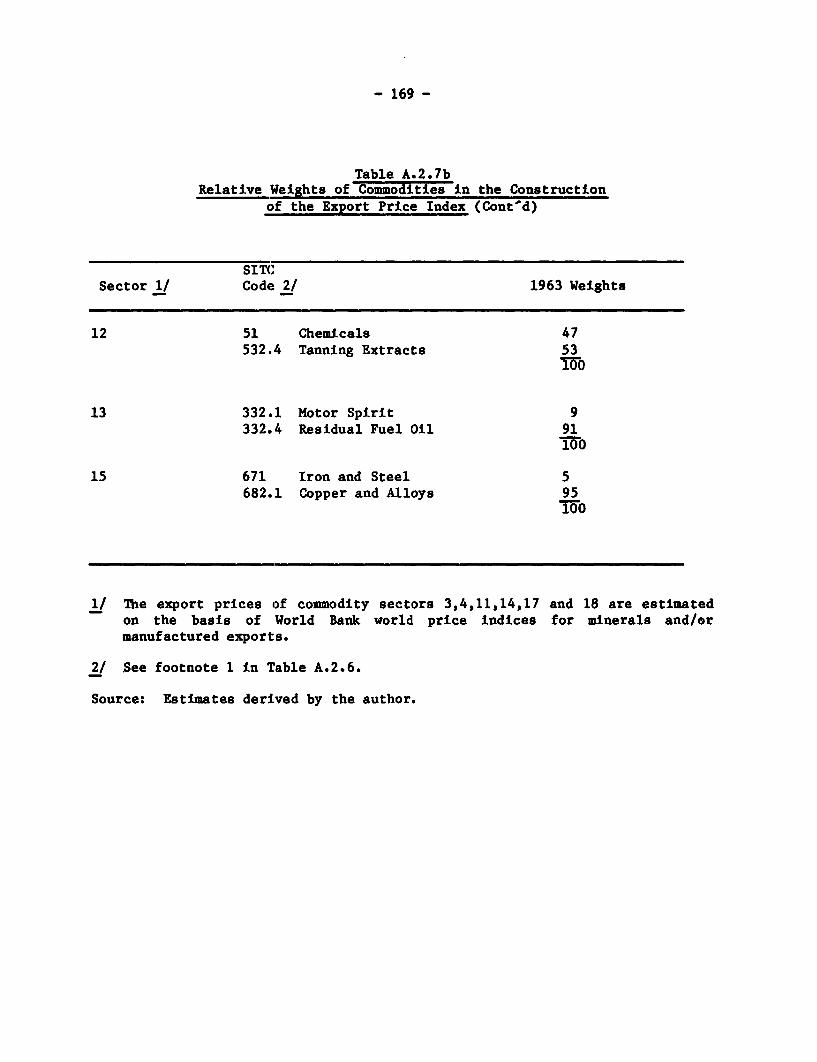

2.7 Relative Weights of Commodities in the Construction ofthe Export Price Index. .o....................................... .168

SOURCES OF INDUSTRIAL GROWTHAND STRUCTURAL CHANGE:

The Case of Turkey

Merih Celasun

INTRODUCTION

Turkey's delayed adjustment to the external economic shocks of the

mid-1970s has resulted in costly growth losses, hyperinflation and political

instability. At the heart of the adjustment difficulties were certain

structural trends that minimized the role of trade in the development

process. Institutional features and policy also played important roles. This

study examines the various factors that have shaped Turkey's economy since

1950, with an emphasis on the implications of an inward-looking trade

strategy. A major objective of the historical analysis is to delineate the

scope of the major planning issues involved in the transition toward trade-

oriented growth in the 1980s.

This paper is part of a comparative study of industrialization in

selected semi-industrial countries 1/ The broad objectives of these

coordinated research efforts are to determine the common features of

industrialization, and to explain country differences in terms of specific

policies and resource endowments. Technical economic analysis is an important

part of the project. Varied input-output methods, which are used to analyze

the changing combinations of factors in growth under different conditions,

have been applied to each country.

The analysis of Turkey primarily concerns the estimation of the

1/ Chenery (1979, Chapter 3) presents an overview of the typical patterns andsources of industrialization at various stages of the development process.Kubo and Robinson (1979) give the initial results of the comparativeanalysis of the sources of industrial growth in eight countries (includingTurkey). The seven others are Japan, Norway, Korea, Taiwan, Mexico,Colombia and Israel.

- 2 -

sources of growth and structural change in production and imports in 1953-73

(Chapter 3). The sources of change in value added, factor use and relative

product prices from 1963-73 have also been studied because more detailed

information is available for that period (Chapter 4). The overall structural

assessment has been extended to 1978 based on the average country patterns

estimated by Chenery and Syrquin (1975) and Chenery and Taylor (1968).

Accordingly, Chapter 5 examines the transformation of the manufacturing sector

in more detail and discusses the roles of the public and private sectors in

the growth of individual manufacturing industries.

Development policy has played a significant role in Turkish growth

and structural change. During 1953-73, the style and framework of development

policy changed. The first decade was an era of uncoordinated development,

which was characterized by frequent shifts in the government's ad hoc economic

policies. In contrast, from 1963-73 formal economy-wide planning techniques

and institutions were adopted and a stronger emphasis on non-inflationary

growth and industrialization was apparent. The trade and balance of payments

regime had essentially a semi-closed character during 1953-70, but became more

open in the early 1970s. The relatively larger role of export expansion as a

source of growth from 1968-73 reflected both the effects of switching to a

semi-open trade regime and the impact of the world commodity boom in 1971-

73. The final section (Chapter 6) provides a brief review of the basic

institutional and policy factors that have been instrumental in Turkey's

inward-looking industrialization strategy. It also discusses Turkey's recent

(1980-81) policy changes and the prospects for a trade-oriented transition in

the 1980s. Suggestions for future planning and research are offered as well.

Extensive empirical work on the construction of price indices for

production, imports and exports that have shown considerable intersectoral and

intrasectoral variation has been an integral part of the project. The data

base largely consists of sectoral output and trade data for 1953 and 1958 and

official input output tables for 1963, 1968 and 1973. The sector information

has been adjusted for consistency and reclassified at the 25 sector level 1/

A useful by-product of this study is a set of deflated input-output tables,

which closely conform to the official national accounts published by Turkey's

State Institute of Statistics (SIS). The analytical methods of the sources of

growth analysis are reviewed in Appendix 1. The deflation procedures used,

sectoral price indices constructed and sector classification adopted in data

processing are presented in Appendix 2.

1/ For brevity in presentation, the computer printouts (for decompositionmeasures) at the 25 sector level of aggregation are summarized in the textin tables prepared at the 9 sector level of aggregation.

- 4 -

1. HISTORICAL BACKGROUND: 1923-1980

Although the sources of growth analysis covers 1953-73, further

historical background on Turkey's economic growth is needed to indicate trends

over a longer perspective. Chapter 1 presents a survey of the major phases of

development marked by important institutional and/or policy changes since the

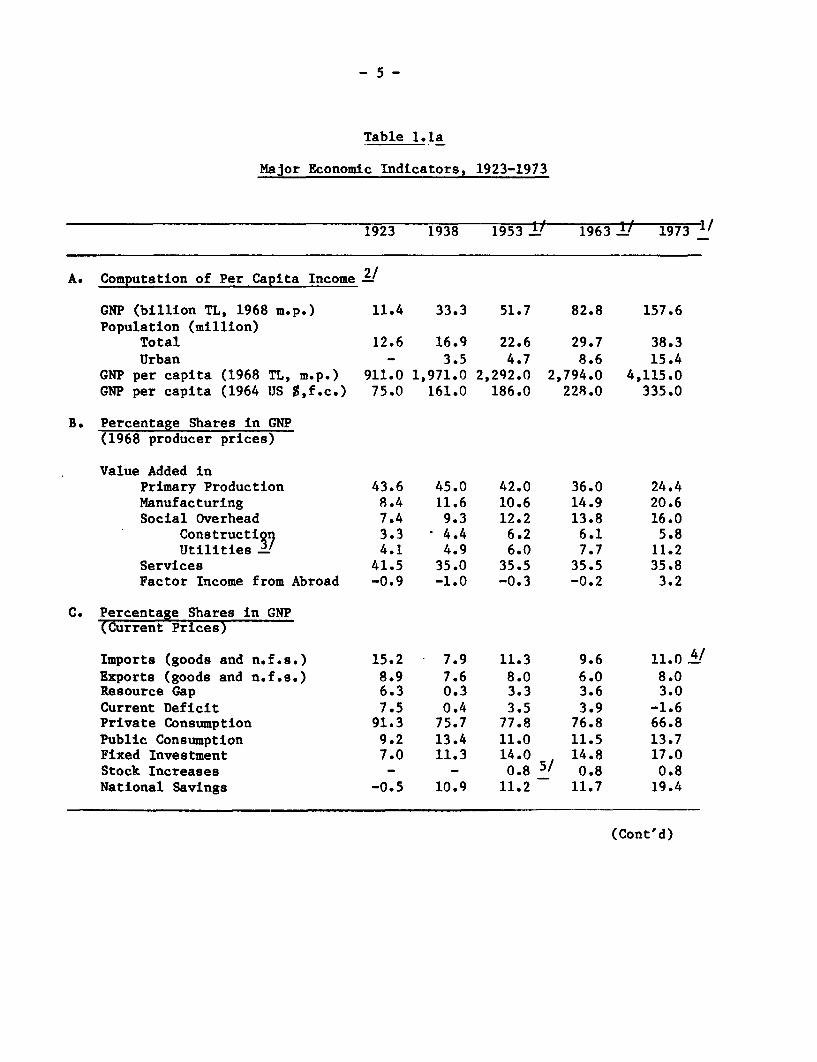

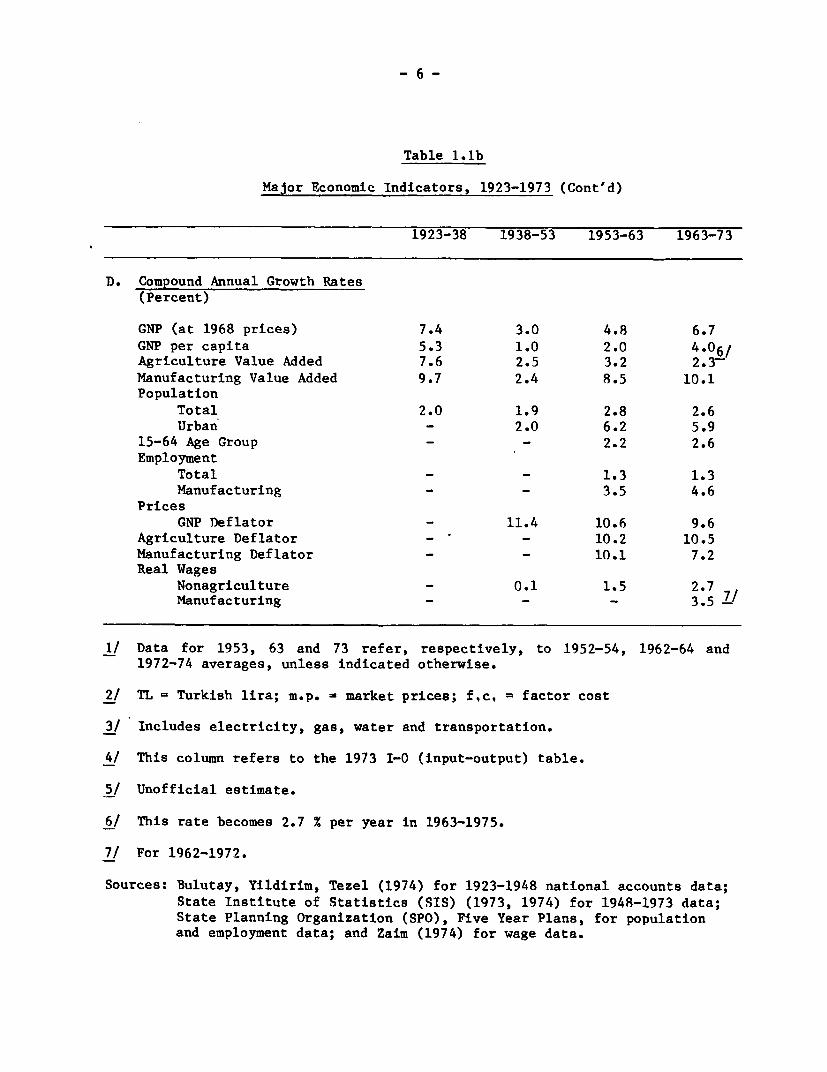

early days of the Republic. The major economic indicators assembled in Tables

l.la and 1.lb describe the historical evolution of the economy according to

its principal structural features from 1923-73. 1/

A. Economic Development Before 1950

The Turkish Republic was established in 1923 upon the end of the War

of Independence that erupted after the Ottoman Empire was dissolved. As shown

in Table 1.lb, economic growth was very rapid between 1923 and 1938 before it

was interrupted by World War II. (The annual increase of per capita GNP was

5.3 percent.) The first fifteen years of the new republican period was

characterized by profound social reforms. However, these reforms were

accompanied by only moderate changes in economic organization and productive

structure.

1/ Some of the structural characteristics are recalculated in Chapter 2 forconsistent comparisons with the cross-country norms, which are expressedin terms of percentage shares in GDP at factor cost.

Table 1.la

Major Economic Indicators, 1923-1973

1923 1938 1953 1963±/ 1973

A. Computation of Per Capita Income 2/

GNP (billion TL, 1968 m.p.) 11.4 33.3 51.7 82.8 157.6Population (million)

Total 12.6 16.9 22.6 29.7 38.3Urban - 3.5 4.7 8.6 15.4

GNP per capita (1968 TL, m.p.) 911.0 1,971.0 2,292.0 2,794.0 4,115.0GNP per capita (1964 US $,f.c.) 75.0 161.0 186.0 228.0 335.0

B. Percentage Shares in GNP(1968 producer prices)

Value Added inPrimary Production 43.6 45.0 42.0 36.0 24.4Manufacturing 8.4 11.6 10.6 14.9 20.6Social Overhead 7.4 9.3 12.2 13.8 16.0

Constructi2l) 3.3 4.4 6.2 6.1 5.8Utilities __ 4.1 4.9 6.0 7.7 11.2

Services 41.5 35.0 35.5 35.5 35.8Factor Income from Abroad -0.9 -1.0 -0.3 -0.2 3.2

C. Percentage Shares in GNP(Current Prices)

Imports (goods and n.f.s.) 15.2 7.9 11.3 9.6 11.0 4/Exports (goods and n.f.s.) 8.9 7.6 8.0 6.0 8.0Resource Gap 6.3 0.3 3.3 3.6 3.0Current Deficit 7.5 0.4 3.5 3.9 -1.6Private Consumption 91.3 75.7 77.8 76.8 66.8Public Consumption 9.2 13.4 11.0 11.5 13.7Fixed Investment 7.0 11.3 14.0 14.8 17.0Stock Increases - - 0.8 5/ 0.8 0.8National Savings -0.5 10.9 11.2 11.7 19.4

(Cont'd)

-6-

Table 1.lb

Major Economic Indicators, 1923-1973 (Cont'd)

1923-38 1938-53 1953-63 1963-73

D. Compound Annual Growth Rates(Percent)

GNP (at 1968 prices) 7.4 3.0 4.8 6.7

GNP per capita 5.3 1.0 2.0 4.06/Agriculture Value Added 7.6 2.5 3.2 2.3-Manufacturing Value Added 9.7 2.4 8.5 10.1Population

Total 2.0 1.9 2.8 2.6Urban - 2.0 6.2 5.9

15-64 Age Group - - 2.2 2.6Employment

Total - 1.3 1.3Manufacturing - - 3.5 4.6

PricesGNP Deflator - 11.4 10.6 9.6

Agriculture Deflator - - 10.2 10.5Manufacturing Deflator - - 10.1 7.2Real Wages

Nonagriculture - 0.1 1.5 2.7Manufacturing - - - 3.5 -

1/ Data for 1953, 63 and 73 refer, respectively, to 1952-54, 1962-64 and1972-74 averages, unless indicated otherwise.

2/ TL = Turkish lira; m.p. - market prices; f,c, - factor cost

3/ Includes electricity, gas, water and transportation.

4/ This column refers to the 1973 I-0 (input-output) table.

5/ Unofficial estimate.

6/ This rate becomes 2.7 % per year in 1963-1975.

7/ For 1962-1972.

Sources: Bulutay, Yildirim, Tezel (1974) for 1923-1948 national accounts data;State Institute of Statistics (SIS) (1973, 1974) for 1948-1973 data;State Planning Organization (SPO), Five Year Plans, for populationand employment data; and Zaim (1974) for wage data.

A major shift in economic policy took place in the early 1930s

partly in response to the Depression. A renewed emphasis was placed on the

creation and expansion of government-owned enterprises in industrial

sectors. Because of the vigorous initiatives of public enterprises in

commodity-producing sectors, the share of the non-service sectors in GDP

increased from 60 percent in the mid-1920s to 67 percent in 1938. 1/ However,

growth and price stability were interrupted by World War II. As a result,

average annual GNP growth fell to -2.9 and 1.2 percent in 1938-43 and 1938-48,

respectively. Following a major exchange rate adjustment in 1946, government

policies gradually shifted back toward a free enterprise orientation.2/ A

more decisive shift in that direction occurred after the political changes

resulting from the 1950 election.3 / Because of shifting political attitudes

and priorities, a draft five-year plan was not formally adopted in 1947-52.4/

B. Economic Development in 1950-1973

Aided by a steep rise in agricultural output (due to favorable

weather conditions and extension of farmland) and primary exports, the economy

expanded rapidly at an average annual rate of 7.9 percent from 1948-53.

However, after the crop failure of 1954, Turkey entered a phase of severe

balance of payments problems and stagnant growth. As a result of continual

difficulties in increasing agricultural output, controlling domestic inflation

1/ For a full discussion of national accounts data for this period seeBulutay et al (1974). Non-service sectors include "A" and "M+" sectorsaccording to Kuznets' classifications (1969).

2/ The exchange rate was adjusted in August 1946 from 1.28 TL to 2.80 TL perUS dollar.

3/ The Democratic Party, winner of the 1950 election over the RepublicanParty, which governed the country in 1923-50, remained in power until themilitary intervention of May, 1960.

4/ See Tekeli and Ilkin (1974) for a discussion of the 1947 Vaner Plan.

- 8 -

and revitalizing the trade sector, annual growth averaged around 4.0 percent

during 1953-58. This led to the introduction of a devaluation and stabili-

zation policy package in August 1958.1/

From 1958-63, major factors accompanying Turkey's average growth of

5.0 percent annually were a military intervention (1960); the gradual

transition to price stability; the design of a more systematic incentive

structure; and the institutionalization of formal development planning. The

economic difficulties faced in the late 1950s were further aggravated by rapid

population growth (2.8 percent a year) and an upsurge in rural-urban migration

at nearly 6.5 percent a year (see Table l.lb). 2/

There were important differences in the instruments and style of

development policy between the two consecutive ten-year periods from 1953-

73. The 1963-73 period was characterized by the implementation of two five-

year plans, whereas the earlier period was a time of ad hoc shifts in the

government's policies, as well as frequent fluctuations in output and trade

conditions. Turkey's development planning in the 1960s, which emphasized

economy-wide as well as balanced growth, was part of the country's response to

the imbalances experienced and limited resource mobilization achieved in the

1950s.

Turkey's economic performance improved in the second ten-year

period. Despite sluggish growth in agricultural production, annual GNP growth

for 1963-73 averaged around 6.7 percent, as compared with 4.8 percent in

1/ The exchange rate was adjusted de facto from 2.8 to 9.0 TL per US dollarfor numerous transactions.

2/ For a review of the policy experience of 1953-63, see Okyar (1979).

- 9 -

1953-63S The average share of fixed investment in GNP (at market prices)

increased from about 14.0 percent in 1953-62 to 16.1 percent in 1963-72.

During the First and Second Plans (1963-67 and 1968-72), emphasis was placed

on improving domestic savings performance. This led to marginal savings

ratios of 32 and 26 percent, respectively. In turn, the observed ratios of

current account deficit to GNP (at market prices) were quite low, and they

averaged around 1.8 and 0.6 percent, respectively, under the two consecutive

five-year plans. Public savings were about 45-50 percent of total domestic

savings. The proportionally larger share of public fixed investment in the

total (around 52-53 percent) reflected the significant role assigned to the

public sector in major development programs.2/

However, the adoption of formal planning did not significantly

change the restrictive trade policies which discriminated against exports, and

relied heavily on import rationing measures.!/ To the contrary, annual import

programs featuring quantitative restrictions became an important policy device

under the successive five-year plans. The structure of protection resulting

from the trade regime allowed high-cost and import-dependent private

manufacturing plants to be established and maintained.

Turkeyos decision to join the European Economic Community (EEC) was

an important policy development in 1963-73. In September 1963, Turkey and the

EEC signed the Association Agreement, which stipulated that two stages

(preparatory and transitional) would occur before full membership. The

1/ The observed value added growth rates in 1953-73 are somewhat overstatedby domestic price distortions, as shown in Chapter 4.

2/ See Celasun (1980 a).

3/ A path-breaking research effort by Krueger (1974) provides a comprehensiveanalysis of the trade and payments policies of Turkey during the 1950-71period with a clear focus on trade-growth relationships.

- 10 -

preparatory stage was completed by the end of the 1960s, and the Additional

Protocol was signed in November 1970. The latter protocol, which became

effective in January 1973, specified the ground rules for the transitional

stage of establishing a customs union with the EEC before the full membership

stage.

At the beginning of the transitional stage, the EEC removed tariff

barriers for Turkish manufactured exports, except for certain products, such

as cotton yarns and numerous processed food items in which Turkey has a

considerable comparative advantage. For agricultural exports, the EEC

provided selective trade facilities, which were eroded shortly thereafter by

the EEC's subsequent agreements with other countries.l/ In turn, Turkey

agreed to remove gradually tariff and non-tariff barriers for EEC manufactured

imports according to two timetables (over 12 and 22 year periods, as

differentiated by products), and eventually to realign her tariff structure

with the EEC's external tariff structure. Until foreign exchange restrictions

appeared in 1978, tariff reductions were carried out as scheduled in the

Additional Protocol. Free movement for Turkish workers, one of the next

hurdles, is likely to be limited due to growing unemployment in the EEC.

The cyclical position of the economy in the early 1970s affects the

analysis because 1973 marks the end of the period studied. GNP growth in

1971-73 received a substantial boost from a huge increase in workers'

1/ FPI (1978) presents the proceedings of a symposium on Turkey-EECrelations, including discussion on the effects of the new EEC policiestowards other countries. See Hic (1972) for an informative review of theTurkey-EEC relations in the earlier stages.

- 11 -

remittances following the devaluation of August 1970.1/ The remittances, in

turn, reflected the rapid expansion of the Western European economies in 1970-

73. Net factor income from abroad reached an all-time high, 4.6 percent of

GNP, in 1973. This sharp rise in the export of factor services was also

accompanied by a significant increase in agriculture-based exports, largely as

the result of expanding world demand and favorable shifts in relative

prices. The improved foreign exchange position of the country also led to the

rapid growth of imports of basic intermediate goods, investment goods and

parts for consumer durables.

C. Economic Development After 1973

Despite the oil crisis and related external shocks, Turkey attempted

to preserve its growth momentum under the Third Plan (1973-77) through rapid

reserve decumulation and massive external borrowing. Instead of relying upon

internal adjustment to promote balance of payments improvement, the various

coalition governments pursued expansionary policies, while allowing a decline

in marginal savings ratios, and negative import substitution in the energy and

manufacturing sectors.!/ The average rate of GNP growth was about 6.5 percent

a year (despite a 4 percent growth in 1977), and the investment/GNP ratio

increased from 18 percent in 1973 to 23.5 percent in 1977. The marginal

1/ In August 1970, the exchange rate was adjusted from 9 TL to 15 TL per U.S.dollar for a wide range of transactions, excluding certain agriculturalexports.

2/ In Balassa (1979 and 1981), Turkey's adjustment policies (after 1973) arereviewed in the light of the experience of other industrializing eco-nomics. Celasun (1980 a) provides an appraisal of the real and monetaryaspects, while Dervis and Robinson (1978) analyze the erosion of the realforeign exchange rate in the 1973-77 period. In World Bank (1980), thesalient features of the 1978 and 1979 Stabilization Programs are dis-cussed.

- 12 -

savings ratio for the five-year period averaged around 12 percent, while the

current account deficit as a proportion of GNP rose sharply and reached

unsustainable proportions in 1976 and 1977 (around 5.7 and 8.0 percent,

respectively). The heavy borrowing soon led to a high external debt ($14

billion by the end of 1978, including $7.5 billion in short-term debt).

In addition to the adverse impact of the sharp rise in imported oil

prices, the implementation of the Third Plan involved major difficulties in

coping with the increasing import intensity of intermediate inputs in the

production structure. By the early 1970s, the Turkish economy had developed

to the intermediate stage of import substitution, which had the following

characteristics: (1) the exhaustion of easy import substitution possibilities

in the early industries; (2) the pronounced shifts in the structure of

intermediate inputs towards more technology-intensive and capital-intensive

materials; and (3) the need for increased selectivity in the choice of trade-

improving investment programs. 1/ Despite the large increase in levels of

fixed investment, net import substitution was negative and hurt the balance of

payments in 1973-77. Turkey's export market shares also decreased noticeably

in this period 2/

Because it could not sustain heavy external borrowing as the main

adjustment mechanism, the Turkish economy finally faced a severe crisis in

1978-80. The juncture of structural, cyclical and political difficulties of

unprecedented proportions worsened matters. The measures contained in two

stabilization programs in 1978 and 1979 proved to be inadequate in reducing

1/ For a more detailed analysis, see Chapters 3 and 5.

2/ See Balassa (1981, Tables LA and 1B).

- 13 -

distortions of resource allocation and curbing domestic inflation.1/ Annual

growth declined from 4.0 percent in 1977 to 0.4 percent in 1979, while

inflation rose from 49 percent in 1978 to 81 percent in 1979.2/

The government introduced a bold and comprehensive policy package in

January 1980 to correct the rapidly worsening economic situation, and to

redirect growth toward exports with a greater reliance on market forces. The

package included substantial increases in the prices of public enterprises;

elimination of price controls for a wide range of industrial products; a major

currency devaluation; improved incentives for exports; better conditions for

foreign private capital; and a flexible policy for further exchange rate

adjustments. The monetary side of the package was strengthened in July 1980

when most of the interest rates in the banking system were freed. Turkey's

military government, which assumed power in September 1980, supported the new

policy framework, and moved to consolidate its components under more stable

institutional arrangements. Following the massive cost-push and deflationary

impacts of these measures during 1980, the Turkish economy showed an

improvement in 1981, with particularly encouraging results in export

expansion, public finance and control over monetary expansion.

1/ See World Bank (1980, Chapter 1), and Chapter 6.

2/ As measured by the Wholesale Price Index.

- 14 -

2. PATTERNS OF DEVELOPMENT, 1953-78:

An Overview

This study of Turkish development is based on previous work

concerning patterns of development. The stages of structural transformation

generally experienced by a developing country have been investigated by

Chenery and Taylor (1968) and Chenery and Syrquin (1975). These

investigations attempt to determine average or normal patterns of development

for all countries, as opposed to factors in development for a specific

country. They provide a quantitative basis to examine how Turkish development

conforms to or diverges from the norms predicted for a country of its size (as

measured by population), income level and, in some comparisons, net resource

inflow.

Chenery and Syrquin suggested that there are ten development

processes in structural transformation. Six stages are related to resource

accumulation and allocation, and four to demographic and income distributional

aspects. For this study, their actual and predicted values have been

determined for the benchmark years 1953, 1963, 1973 and 1978. The results are

summarized in Tables 2.1 and 2.2 A/ Cyclical influences have not been

eliminated in 1978, during which severe shortages of intermediate goods

imports and disruptions in industrial production occurred. In the

determination of the predicted values from the basic regressions of Chenery-

1/ The author is thankful to Selcuk Caner and Tevfik Yaprak for their ablehelp in the computation of the cross-country norms in Chapters 2 and 5.An earlier version of the results of this analysis is discussed briefly inCelasun (1978).

- 15 -

Syrquin, the following data have been used for the explanatory variables "per

capita income" and 'population":"/

1953 1963 1973 1978

Per capita GNP (factor cost) 186 228 335 403(1964 U.S.$)

Population (millions) 22.6 29.7 38.3 43.2

Source: SIS national income series and population data.

According to the cross-country regressions, Turkey's overall

development transition should have been half-completed by 1973, when per

capita income was above $300. This is based on the findings that some

development processes occur in earlier stages of overall transition, while

others are delayed until later stages, with the stages measured by per capita

income ranging from $100 (least developed) to $1000 (most developed), in 1964

prices. 2/ For example, on the average, the transition is half-completed at

about $300 for all ten processes, whereas the midpoint for investment,

savings, school enrollment ratio, food consumption, primary production, total

exports and imports and urbanization is around $200, and at much higher levels

for others.

1/ In order to reduce the upward bias caused by overvalued exchange rates,per capita income levels for the benchmark years are estimated bydeflating national income series to constant 1964 prices, and using thenominal 1964 exchange rate of 9.00 TL per US dollar for conversions. Thelatter rate was a relatively realistic value at the time. The populationfigures used in the calculations exclude workers employed abroad.

2/ See Chenery and Syrquin (1975, Figures 1 to 6).

- 16 -

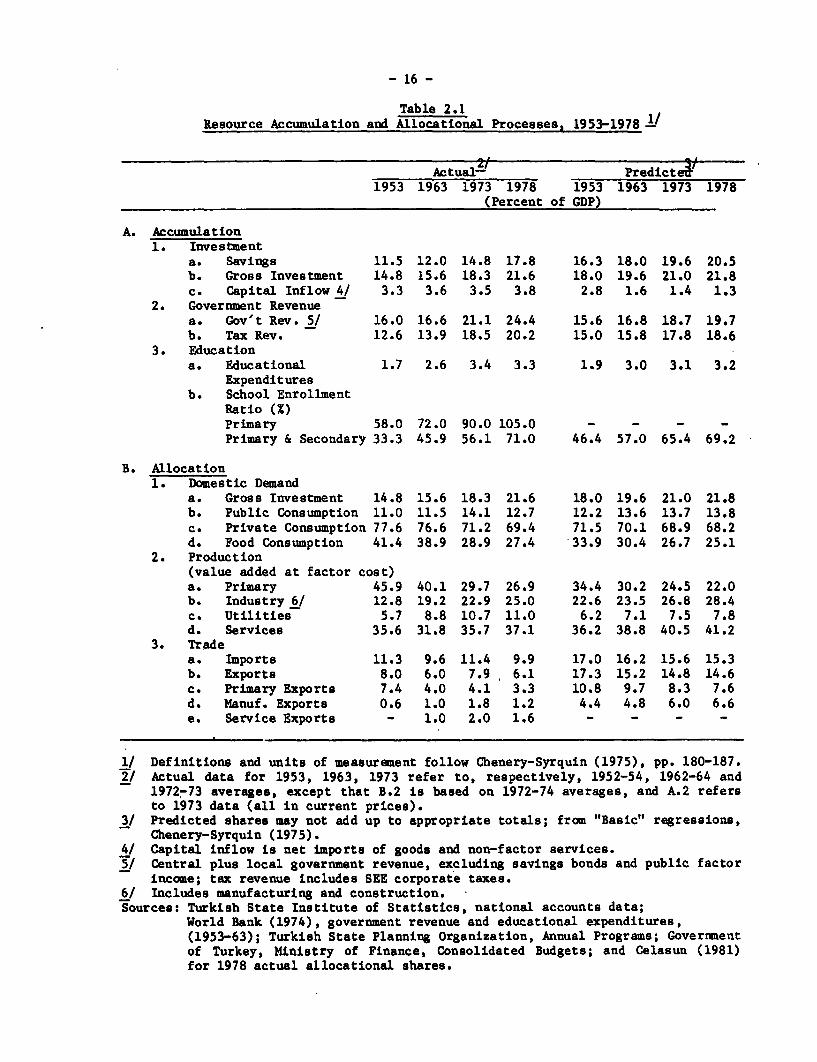

Table 2.1Resource Accumulation and Allocational Processes, 1953-1978 1,

Actual- Predicte;1953 1963 1973 1978 1953 1963 1973 1978

(Percent of GDP)

A. Accumulation1. Investment

a. Savings 11.5 12.0 14.8 17.8 16.3 18.0 19.6 20.5b. Gross Investment 14.8 15.6 18.3 21.6 18.0 19.6 21.0 21.8c. Capital Inflow 4/ 3.3 3.6 3.5 3.8 2.8 1.6 1.4 1.3

2. Government Revenuea. Gov't Rev. 5/ 16.0 16.6 21.1 24.4 15.6 16.8 18.7 19.7b. Tax Rev. 12.6 13.9 18.5 20.2 15.0 15.8 17.8 18.6

3. Educationa. Educational 1.7 2.6 3.4 3.3 1.9 3.0 3.1 3.2

Expendituresb. School Enrollment

Ratio (%)Primary 58.0 72.0 90.0 105.0 - - - -Primary & Secondary 33.3 45.9 56.1 71.0 46.4 57.0 65.4 69.2

B. Allocation1. Domestic Demand

a. Gross Investment 14.8 15.6 18.3 21.6 18.0 19.6 21.0 21.8b. Public Consumption 11.0 11.5 14.1 12.7 12.2 13.6 13.7 13.8c. Private Consumption 77.6 76.6 71.2 69.4 71.5 70.1 68.9 68.2d. Food Consumption 41.4 38.9 28.9 27.4 33.9 30.4 26.7 25.1

2. Production(value added at factor cost)a. Primary 45.9 40.1 29.7 26.9 34.4 30.2 24.5 22.0b. Industry 6/ 12.8 19.2 22.9 25.0 22.6 23.5 26.8 28.4c. Utilities 5.7 8.8 10.7 11.0 6.2 7.1 7.5 7.8d. Services 35.6 31.8 35.7 37.1 36.2 38.8 40.5 41.2

3. Tradea. Imports 11.3 9.6 11.4 9.9 17.0 16.2 15.6 15.3b. Exports 8.0 6.0 7.9 6.1 17.3 15.2 14.8 14.6c. Primary Exports 7.4 4.0 4.1 3.3 10.8 9.7 8.3 7.6d. Manuf. Exports 0.6 1.0 1.8 1.2 4.4 4.8 6.0 6.6e. Service Exports - 1.0 2.0 1.6 - - - -

1/ Definitions and units of measurement follow Chenery-Syrquin (1975), pp. 180-187.2/ Actual data for 1953, 1963, 1973 refer to, respectively, 1952-54, 1962-64 and

1972-73 averages, except that B.2 is based on 1972-74 averages, and A.2 refersto 1973 data (all in current prices).

3/ Predicted shares may not add up to appropriate totals; from "Basic" regressions,Chenery-Syrquin (1975).

4/ Capital inflow is net imports of goods and non-factor services.5/ Central plus local government revenue, excluding savings bonds and public factor

income; tax revenue includes SEE corporate taxes.6/ Includes manufacturing and construction.Sources: Turkish State Institute of Statistics, national accounts data;

World Bank (1974), government revenue and educational expenditures,(1953-63); Turkish State Planning Organization, Annual Programs; Governmentof Turkey, Ministry of Finance, Consolidated Budgets; and Celasun (1981)for 1978 actual allocational shares.

- 17 -

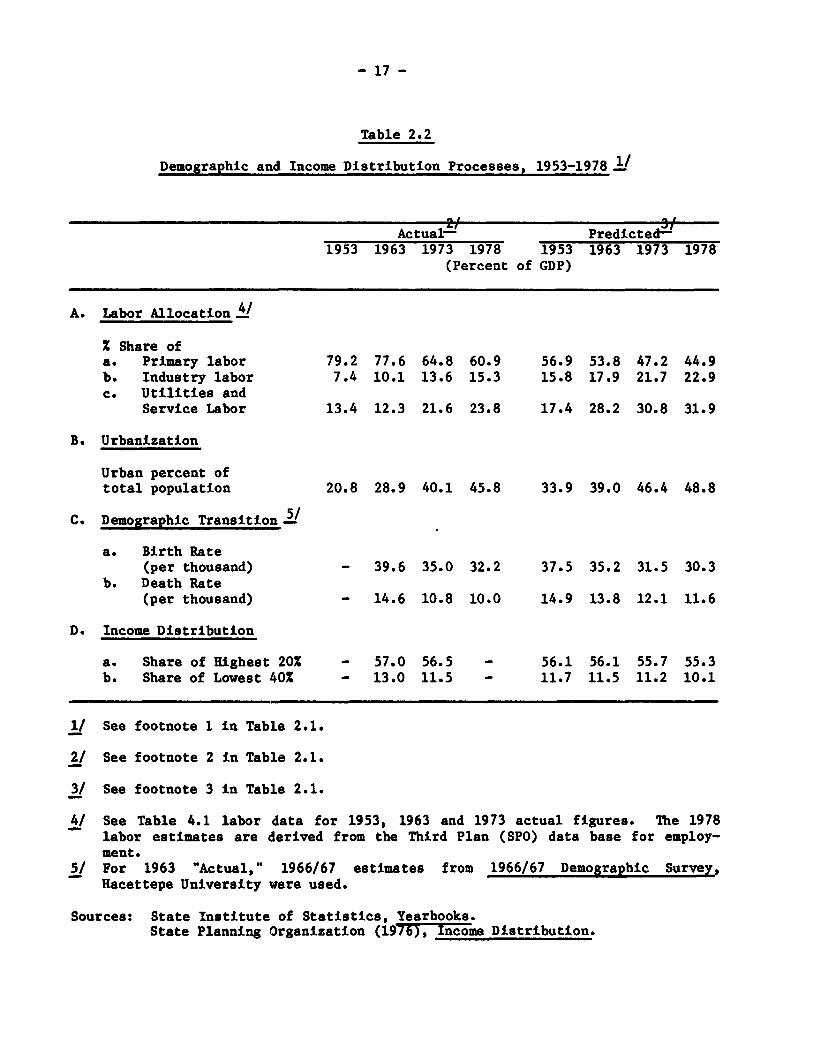

Table 2.2

Demographic and Income Distribution Processes, 1953-1978 1/

Actual- Predicted&1953 1963 1973 1978 1953 1963 1973 1978

(Percent of GDP)

A. Labor Allocation 4/

X Share ofa. Primary labor 79.2 77.6 64.8 60.9 56.9 53.8 47.2 44.9b. Industry labor 7.4 10.1 13.6 15.3 15.8 17.9 21.7 22.9c. Utilities and

Service Labor 13.4 12.3 21.6 23.8 17.4 28.2 30.8 31.9

B. Urbanization

Urban percent oftotal population 20.8 28.9 40.1 45.8 33.9 39.0 46.4 48.8

C. Demographic Transition5/

a. Birth Rate(per thousand) - 39.6 35.0 32.2 37.5 35.2 31.5 30.3

b. Death Rate(per thousand) - 14.6 10.8 10.0 14.9 13.8 12.1 11.6

D. Income Distribution

a. Share of Highest 20X - 57.0 56.5 - 56.1 56.1 55.7 55.3b. Share of Lowest 40% - 13.0 11.5 - 11.7 11.5 11.2 10.1

1/ See footnote 1 in Table 2.1.

2/ See footnote 2 in Table 2.1.

3/ See footnote 3 in Table 2.1.

4/ See Table 4.1 labor data for 1953, 1963 and 1973 actual figures. The 1978labor estimates are derived from the Third Plan (SPO) data base for employ-ment.

5/ For 1963 "Actual," 1966/67 estimates from 1966/67 Demographic Survey,Hacettepe University were used.

Sources: State Institute of Statistics, Yearbooks.State Planning Organization (1976), Income Distribution.

- 18 -

Based on the evaluation of structural transition in terms of the ten

development processes, Turkey had the following characteristics:

(1) In the 1950s and early 1960s, Turkey performed substantially below

the predicted levels for a country of its size and income in the accumulation

of capital and skills, the restructure of domestic demand and production, and,

particularly, the development of a "normal" export base. The actual

government revenues (excluding public factor income) were comparable to the

predicted values, but their composition and patterns of usage must be studied

separately.

(2) Unlike the preceding ten years, from 1963-73 there was considerable

structural transformation in capital accumulation and primary schooling as

well as in reduction of the share of primary production. In this period, the

change in the share of industrial labor was unexpectedly low in view of the

rapid pace of population growth and urbanization, and the continuing large

labor surplus in rural areas. (See Table 5.1) Despite favorable economic

conditions in the early 1970s, the shares of total and industrial exports

continued to remain drastically below cross-country norms.

(3) Income distribution, described in terms of the shares of the highest

20 percent and lowest 40 percent, is comparable with the typical country

standards. However, the 1963 and 1973 figures indicate a decline for the

poorest groups that benefited mainly upper-middle income classes from 1963-73,

as discussed by the Turkish State Planning Organization (SPO), (1976).

(4) The share of educational expenditure in GDP was comparatively low in

1953-63, but showed an increase after 1963. This was also reflected by the

improvement in school enrollment ratios during those years. From 1963-78, the

increase in primary and secondary school enrollment (taken as a whole) mainly

indicated the expansion of primary schooling. As a result, the need for

- 19 -

development of secondary school capacities, particularly in the field of

vocational training, is not apparent from these figures.

(5) Changes between 1973 and 1978 reflected the continuation of

structural trends in 1963-73, and led to the further restructuring of domestic

demand and production. However, because the actual trade ratios for 1978 were

still markedly below the cross-country norms, the urgency of shifting toward a

trade orientation is clear. The growth-limiting effects of the lower share of

imports in GDP were accentuated by the smaller share of non-petroleum products

in total imports in 1978 as compared to the share in 1973.

(6) The relatively high share of tax revenue in GDP in 1973 and,

particularly, 1978 largely reflects the distorting effects of inflation on

income tax, which was based on tax schedules that had not been changed since

1963. The progressive tax rates applied to the rapidly increasing gross

salaries of public employees resulted in misleading tax increments of

considerable proportions from 1973-80, until revised income tax legislation

was adopted in 1981.

(7) Finally, the capital inflow figures shown in Table 2.1 measure the

net imports of goods and non-factor services, and do not reflect the sizable

contribution of workers' remittances to the trade adjustment process in 1963-

78. In terms of current account deficits, external resource inflows were

quite moderate by inter-country standards, and normally less than 2 percent of

GDP in 1963-73.

The deviations of the Turkish economic structure from the average

country patterns are particularly significant in the following four main

areas, which are examined in more detailed below:

1. The actual export/GDP ratios have been far below the cross-country

norms throughout 1953-78. This indicates the inward orientation of the

- 20 -

development strategy.

2. The actual import/GDP ratios have been higher than those for exports,

but still markedly below the predicted values. This suggests the relatively

narrow scope for import substitution at the economy-wide level.

3. Although the Turkish industrialization process was considerably

delayed until 1963, the subsequent catching-up effort has been significant in

terms of the rising share of industry in total value added.

4. The share of industry in total employment has remained below cross-

country standards. This indicates the need for more labor-absorbing patterns

of industrial growth in the future.

- 21 -

3. SOURCES OF INDUSTRIALIZATION, 1953-73

A. Scope of the Analysis

As comparison of Turkey's development with the cross-country norms

discussed in Chapter 2 indicated, a considerable amount of restructuring in

domestic production occurred during 1953-73 despite the continued lag with

"normal" trade patterns. Chapter 3 examines the sources of different

expansion of sectors, which led to a rapid increase of the share of industry

in total production.

The changes in sectoral production (or gross output) have been

explained in terms of the following four factors:

1. Domestic final demand expansion

2. Export expansion

3. Import substitution

4. Technological change or changes in input-output coefficients.

The analysis has been conducted in empirically-based input-output

(I-0) frameworks incorporating these factors. The relative importance (or, in

mathematical terms, weights) of these sources of growth have been determined

for different sectoral aggregations at various times in order to compare

sectors and/or time periods as policy orientation shifts. The computational

process of distinguishing and estimating the relative weights of these factors

is known as decomposition analysis.

The estimates for the sources of gross output growth also provide a

basis to explain changes in sectoral value added and factor use in terms of

the same causal factors plus changes in value added and factor coefficients,

respectively. With minor modifications, the analytical framework is also used

to estimate the sources of import growth to shed additional light on the

- 22 -

process of import substitution experienced in the economy. In this section,

the estimates for the sources of gross output and import growth are derived

for the various subperiods of 1953-73. The sources of changes in value added

are examined for 1963-68 and 1968-73 only, because complete I-0 tables are

unavailable for the earlier periods, for which the interindustry data have

been compiled on a partial basis. The sources of change in factor use are

analyzed in Chapter 4.

The type of sources of growth analysis used here is different from

the production function approach, which relates output expansion to changes in

factor inputs and productivities-11 In this study, the process of sectoral

growth is primarily considered from the demand side based on the consistent

accounting identities of input-output relations. There are two methods that

can be used to analyze growth from this perspective. The first approach is

known as the constant composition method (referred to hereinafter as the

"composition method"). Following the tradition of the celebrated analysis of

Chenery, Shishido and Watanabe (CSW, 1962) for Japan, it attempts to explain

the nonproportional expansion of sectoral output in terms of the non-

proportional growth of causal factors observed in individual sectors.

Nonproportional growth is measured by deviations from the balanced (or norm)

growth path, in which all elements expand proportionally at the growth rate of

aggregate demand or aggregate value added.

The second approach is designated the constant share method

(referred to hereinafter as the "share method"). It differs from the

composition method in the treatment of import substitution as a cause of

expansion. The share method, which was elaborated by Syrquin (1976), defines

1/ In Chapter 4, the roles of labor reallocation and productivity changes inthe aggregate growth process are briefly considered.

- 23 -

the constant (initial year) share of imports in domestic demand as the norm in

individual sectors, and defines import substitution in terms of changes in the

import (or, symmetrically, domestic supply) shares rather than changes in the

commodity composition of imports. In contrast, the composition method

measures import substitution in terms of deviations of sectoral import

expansion from the expected growth path, or from the constant (initial year)

composition of sectoral imports. The share method also allows two sets of

decomposition measures which explain different phenomena under

consideration. Changes in the relevant factors are defined in terms of first

differences (or increments) and/or deviations from propositional growth.

While the deviation measures clarify the causes of structural change (seen in

compositional shifts), the first difference measures are used in examining

growth processes and policy effects in individual sectors.

For both methods, changes in intermediate input requirements have

been studied to differentiate the direct and indirect demand effects on

growth. The decomposition analysis has been divided into two variations,

known as the direct and total methods.1J The total measures combine the

direct and indirect (known as backward-linkage) effects of changes in domestic

final demand, exports and import substitution, and identify changes in I-0

coefficients (which represent technological change) as a separate source of

growth.l/ In turn, the direct measures include all intermediate uses of the

products of a particular sector under the domestic demand contribution to the

growth process.

1/ These terms also apply to variations of any approach in the sources ofgrowth literature.

2/ In the abeence of separate import matrices for all benchmark years, thepresent analysis quantifies the effects of changes in total (rather thandomestic) I-0 coefficients as a source of growth.

- 24 -

The choice of initial or terminal year coefficients (and

correspondingly terminal or initial year volume weights) in the decomposition

equations is important. This issue has been treated as an index number

problem by separately estimating the Laspeyres and Paasche indices on the

basis of structural coefficients being taken as the relevant weights. 1/ The

arithmetic means of these two indices are used here (unless otherwise

indicated) to reduce possible bias in the estimation process. For time

intervals consisting of at least two subperiods, the averages of the Laspeyres

and Paasche measures for successive subperiods are simply summed to obtain the

"chained" measures for sources of growth. Appendix 1 provides a method-

ological review of the sources of growth models of the types employed in the

present study, and gives the algebraic formulations of the decomposition

equations under the variant methods.

B. Basic Data

The data base consists of interindustry data analyzed for five

benchmark years spaced at five-year intervals from 1953-73. The three I-0

tables compiled by the official agencies for the years 1963, 1968 and 1973

have been adjusted for differences in sector coverage, reorganized in 25x25

sector matrices, and deflated to constant 1968 domestic prices.2/ Before the

1/ In the cases where the initial year I-0 matrix is not available (e.g., fortime periods starting with 1953 in the Turkish case), a modified form ofLaspeyres index is used, as noted in Appendix 1.

2/ The SPO made an earlier attempt to prepare a 15 sector table for 1959,which is not comparable with the later tables because of the differencesin sector classification and price conventions. See Korum (1963) for adetailed review of the 1959 table. Another unpublished table by the SP0for 1967 has not been used in the present study. The 1963 table wascompiled by the SP0, while the 1968 and 1973 tables were published by theState Institute of Statistics. See Appendix 2 for a detailed account ofthe deflation work needed to prepare a consistent set of data for thisstudy.

- 25 -

data was deflated, the 1963 I-0 table required substantial adjustments in the

imputed values of some of the component parts of agricultural and livestock

outputs (such as straw, pasture and animal services), and in the

classification of utilities, public services, crude oil and oil refining

sectors. The treatment of cotton ginning also had to be modified in the 1973

I-0 table to ensure compatability with the export commodity classification of

the earlier tables.

The data for the benchmark years 1953 and 1958 represent 1952-54 and

1957-59 averages to minimize the distorting effects of cyclical factors in the

analysis. In the absence of complete I-0 matrices for these two benchmark

years, the gross output, domestic final and intermediate demand, and trade

data were estimated at the 25 sector level of aggregation to establish the

minimum levels for estimating the sources of output and import growth for

periods starting with 1953 or 1958.21 In the latter stages of the research,

the year 1958 was dropped from the analysis. It appeared to be an

inappropriate benchmark year because of unusually severe import shortages and

economic disruptions.

The figures totalled from the deflated I-0 data of this study are

comparable to the estimates of the official national income (NY) accounts

published by the State Institute of Statistics (SIS) in current as well as in

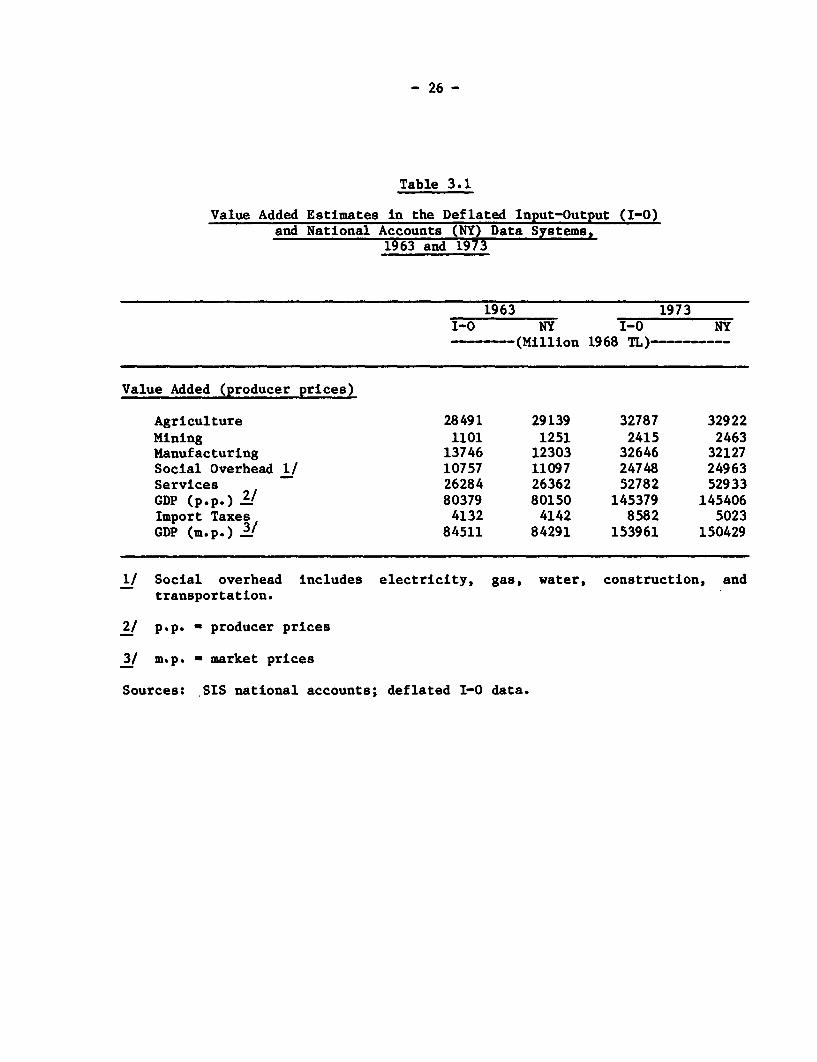

constant 1968 prices. As shown in Table 3.1, the constant price value added

1/ For the years 1953 (1952-54 average) and 1958 (1957-59 average), thecommodity trade data from the United Nations Yearbook of InternationalTrade Statistics was processed according to the trade classifications ofthe 1963 and 1968 I-0 tables, and then deflated to constant prices bydeflators given in Annex II. The net output figures of Ecevit and Ozotun(1974) and various SIS sources were converted into gross output estimateson the basis of available production data. For estimation of the elementsof domestic demand, the data analysis drew upon partial official dataavailable on fixed investment and various estimates based on incomeelasticities for private consumption.

- 26 -

Table 3.1

Value Added Estimates in the Deflated Input-Output (I-O)and National Accounts (NY) Data Systems,

1963 and 1973

1963 1973I-0 NY I-0 NY----- (Million 1968 TL)-----

Value Added (producer prices)

Agriculture 28491 29139 32787 32922Mining 1101 1251 2415 2463Manufacturing 13746 12303 32646 32127Social Overhead 1/ 10757 11097 24748 24963Services 26284 26362 52782 52933GDP (p.p.) 2/ 80379 80150 145379 145406Import Taxes 4132 4142 8582 5023GDP (m.p.) 3/ 84511 84291 153961 150429

1/ Social overhead includes electricity, gas, water, construction, andtransportation.

2/ p.p. - producer prices

3/ m.p. - market prices

Sources: SIS national accounts; deflated I-0 data.

- 27 -

estimates for the major sectors in the I-0 and NY data systems are nearly

the same for the 1963 and 1973 benchmark years.l/

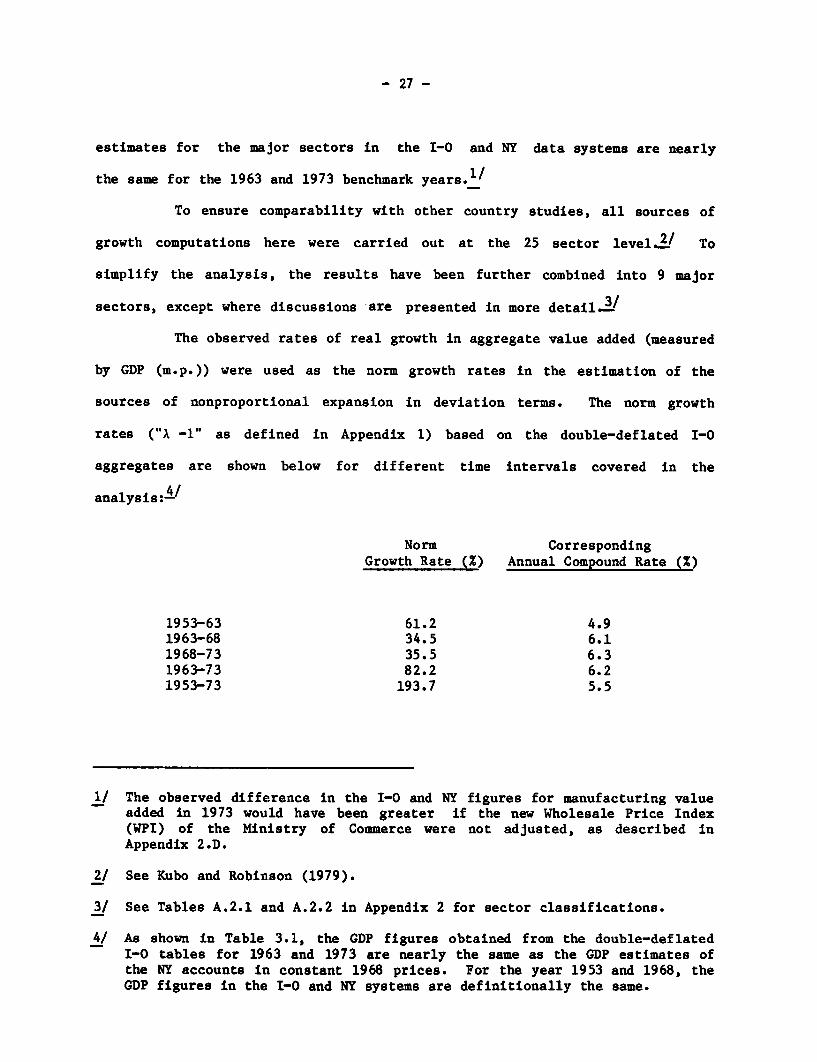

To ensure comparability with other country studies, all sources of

growth computations here were carried out at the 25 sector level 2 To

simplify the analysis, the results have been further combined into 9 major

sectors, except where discussions are presented in more detail.3/

The observed rates of real growth in aggregate value added (measured

by GDP (m.p.)) were used as the norm growth rates in the estimation of the

sources of nonproportional expansion in deviation terms. The norm growth

rates ("A -1" as defined in Appendix 1) based on the double-deflated I-0

aggregates are shown below for different time intervals covered in the

analysis:gl

Norm CorrespondingGrowth Rate (%) Annual Compound Rate (%)

1953-63 61.2 4.91963-68 34.5 6.11968-73 35.5 6.31963-73 82.2 6.21953-73 193.7 5.5

1/ The observed difference in the I-0 and NY figures for manufacturing valueadded in 1973 would have been greater if the new Wholesale Price Index(WPI) of the Ministry of Commerce were not adjusted, as described inAppendix 2.D.

2/ See Kubo and Robinson (1979).

3/ See Tables A.2.1 and A.2.2 in Appendix 2 for sector classifications.

4/ As shown in Table 3.1, the GDP figures obtained from the double-deflatedI-0 tables for 1963 and 1973 are nearly the same as the GDP estimates ofthe NY accounts in constant 1968 prices. For the year 1953 and 1968, theGDP figures in the I-0 and NY systems are definitionally the same.

- 28 -

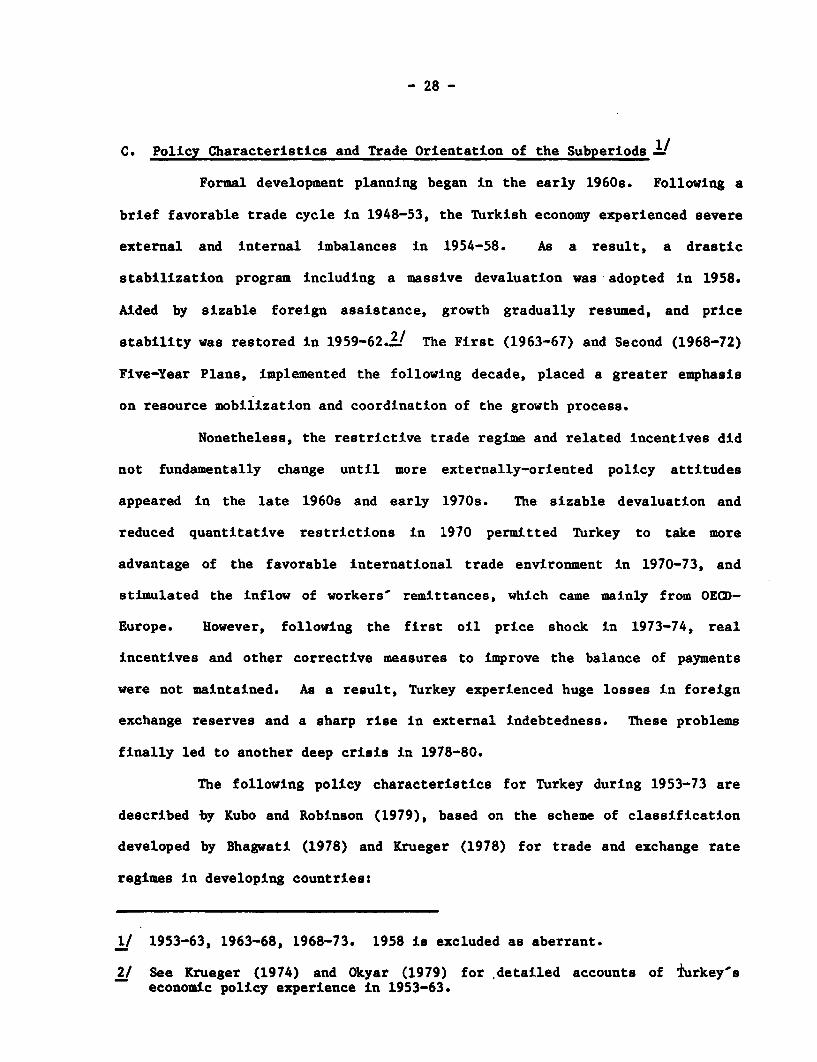

C. Policy Characteristics and Trade Orientation of the Subperiods /

Formal development planning began in the early 1960s. Following a

brief favorable trade cycle in 1948-53, the Turkish economy experienced severe

external and internal imbalances in 1954-58. As a result, a drastic

stabilization program including a massive devaluation was adopted in 1958.

Aided by sizable foreign assistance, growth gradually resumed, and price

stability was restored in 1959-62..L/ The First (1963-67) and Second (1968-72)

Five-Year Plans, implemented the following decade, placed a greater emphasis

on resource mobilization and coordination of the growth process.

Nonetheless, the restrictive trade regime and related incentives did

not fundamentally change until more externally-oriented policy attitudes

appeared in the late 1960s and early 1970s. The sizable devaluation and

reduced quantitative restrictions in 1970 permitted Turkey to take more

advantage of the favorable international trade environment in 1970-73, and

stimulated the inflow of workers remittances, which came mainly from OECD-

Europe. However, following the first oil price shock in 1973-74, real

incentives and other corrective measures to improve the balance of payments

were not maintained. As a result, Turkey experienced huge losses in foreign

exchange reserves and a sharp rise in external indebtedness. These problems

finally led to another deep crisis in 1978-80.

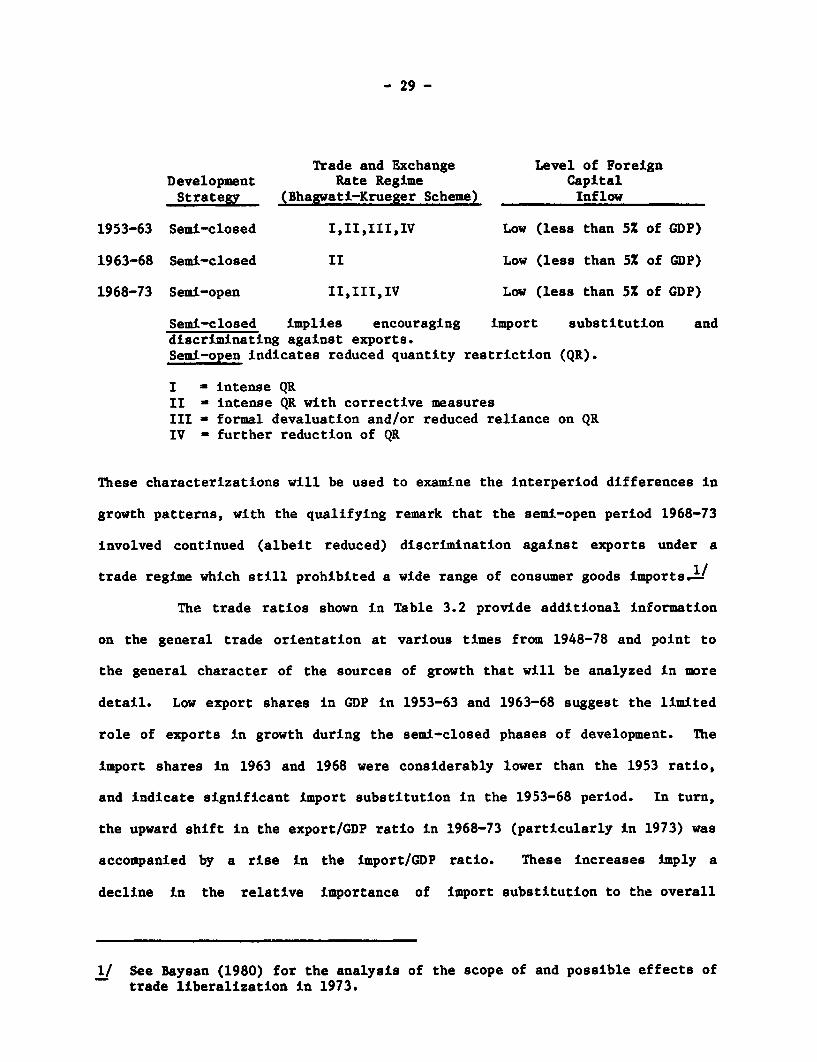

The following policy characteristics for Turkey during 1953-73 are

described by Kubo and Robinson (1979), based on the scheme of classification

developed by Bhagwati (1978) and Krueger (1978) for trade and exchange rate

regimes in developing countries:

1/ 1953-63, 1963-68, 1968-73. 1958 is excluded as aberrant.

2/ See Krueger (1974) and Okyar (1979) for detailed accounts of Turkey'seconomic policy experience in 1953-63.

- 29 -

Trade and Exchange Level of ForeignDevelopment Rate Regime CapitalStrategy (Bhagwati-Krueger Scheme) Inflow

1953-63 Semi-closed I,II,III,IV Low (less than 51 of GDP)

1963-68 Semi-closed II Low (less than 51 of GDP)

1968-73 Semi-open II,III,IV Low (less than 51 of GDP)

Semi-closed implies encouraging import substitution anddiscriminating against exports.Semi-open indicates reduced quantity restriction (QR).

I - intense QRII - intense QR with corrective measuresIII - formal devaluation and/or reduced reliance on QRIV - further reduction of QR

These characterizations will be used to examine the interperiod differences in

growth patterns, with the qualifying remark that the semi-open period 1968-73

involved continued (albeit reduced) discrimination against exports under a

trade regime which still prohibited a wide range of consumer goods imports.L/

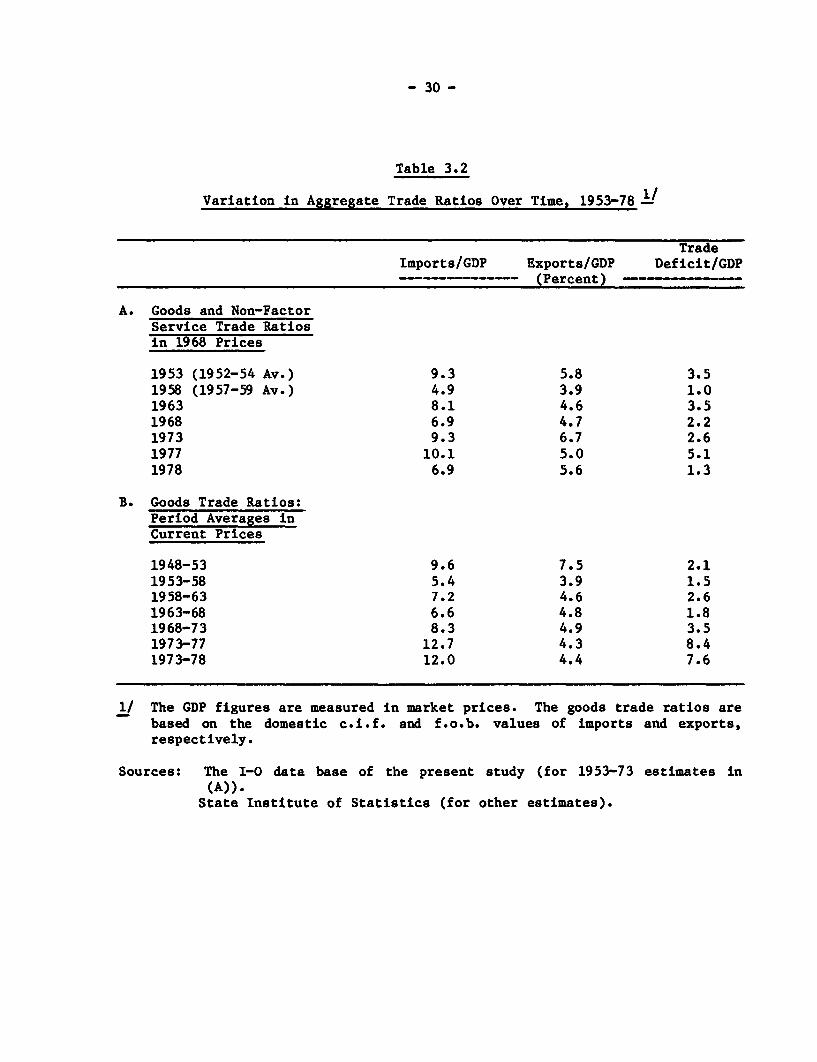

The trade ratios shown in Table 3.2 provide additional information

on the general trade orientation at various times from 1948-78 and point to

the general character of the sources of growth that will be analyzed in more

detail. Low export shares in GDP in 1953-63 and 1963-68 suggest the limited

role of exports in growth during the semi-closed phases of development. The

import shares in 1963 and 1968 were considerably lower than the 1953 ratio,

and indicate significant import substitution in the 1953-68 period. In turn,

the upward shift in the export/GDP ratio in 1968-73 (particularly in 1973) was

accompanied by a rise in the import/GDP ratio. These increases imply a

decline in the relative importance of import substitution to the overall

1/ See Baysan (1980) for the analysis of the scope of and possible effects oftrade liberalization in 1973.

- 30 -

Table 3.2

Variation in Aggregate Trade Ratios Over Time, 1953-78 l/

TradeImports/GDP Exports/GDP Deficit/GDP

(Percent)

A. Goods and Non-FactorService Trade Ratiosin 1968 Prices

1953 (1952-54 Av.) 9.3 5.8 3.51958 (1957-59 Av.) 4.9 3.9 1.01963 8.1 4.6 3.51968 6.9 4.7 2.21973 9.3 6.7 2.61977 10.1 5.0 5.11978 6.9 5.6 1.3

B. Goods Trade Ratios:Period Averages inCurrent Prices

1948-53 9.6 7.5 2.11953-58 5.4 3.9 1.51958-63 7.2 4.6 2.61963-68 6.6 4.8 1.81968-73 8.3 4.9 3.51973-77 12.7 4.3 8.41973-78 12.0 4.4 7.6

1/ The GDP figures are measured in market prices. The goods trade ratios arebased on the domestic c.i.f. and f.o.b. values of imports and exports,respectively.

Sources: The I-0 data base of the present study (for 1953-73 estimates in(A)).

State Institute of Statistics (for other estimates).

- 31 -

growth process. However, as the figures in Table 3.2 broadly suggest, the

trend in declining import substitution continued in 1973-77, but it was not

accompanied by export-oriented restructuring in domestic production.!I

Consequently, the sharp fall in the imports/GDP ratio in 1978 signalled the

emergence of a massive external imbalance in the economy.

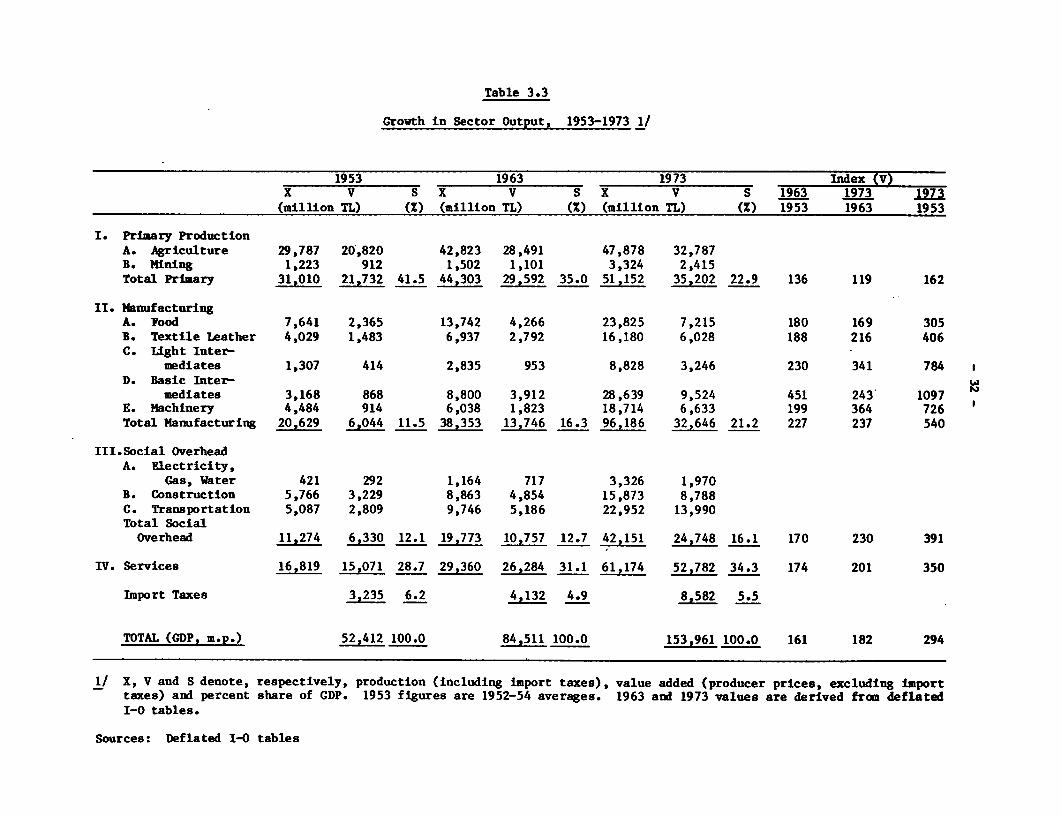

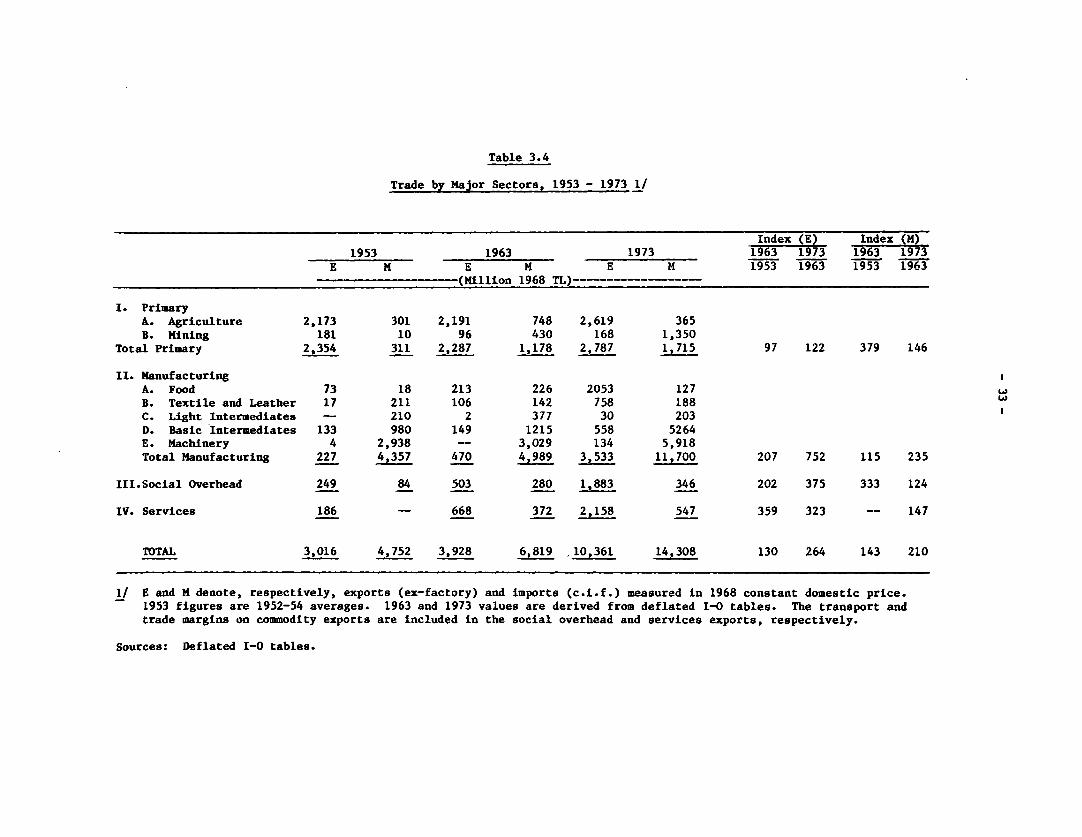

Tables 3.3 and 3.4 present a set of complementary data. Output and

trade growth are broken down by major sectors in the two successive ten-year

periods of 1953-63 and 1963-73. As these tables show, economic growth was

more rapid in 1963-73. In addition, it was accompanied by a considerable

change in the sectoral mix of output. The share of the primary sectors in GDP

(m.p.) declined from 41.5 percent in 1963 to 22.7 percent in 1973, while the

share of manufacturing increased from 11.5 percent to 21.2 percent. Although

the high rates of protection in Turkey undoubtedly cause industrial shares to

be overestimated, shifts toward manufacturing and other non-agricultural

sectors clearly indicate a transitional process toward industrialization.._/

The sources of growth analysis represents an empirical attempt to measure the

relative importance of several factors which affected and shaped such a

process.

D. Sources of Growth and Structural Change: An Economy-Wide Analysis

Internal factors were prominent sources of industrialization in

Turkey's recent economic history. The decomposition measures for the sources

of growth and structural change in gross output (production) and value added

are first aggregated and examined at the national economy level. The

aggregate first difference measures are calculated from the algebraic sums of

1/ See Balassa (1979) and Celasun (1980 a) for appraisals of macroeconomicdevelopments in 1973-78.

2/ See Olgun (1975) for an analysis of the structure of protection in Turkishmanufacturing based on the 1968 data. The main results are summarized inTable 5.4.

Table 3.3

Growth in Sector Output, 1953-1973 1/

1953 1963 1973 Index (V)x V S X V S X V S 1963 1973 17

(million TL) (%) (million TL) (Z) (million TL) (%) 1953 1963 1953

I. Primary ProductionA. Agriculture 29,787 20,820 42,823 28,491 47,878 32,787B. Mining 1,223 912 1,502 1,101 3,324 2,415Total Primary 31,010 21,732 41.5 44,303 29,592 35.0 51,152 35,202 22.9 136 119 162

II. ManufacturingA. Food 7,641 2,365 13,742 4,266 23,825 7,215 180 169 305B. Textile Leather 4,029 1,483 6,937 2,792 16,180 6,028 188 216 406C. Light Inter-

mediates 1,307 414 2,835 953 8,828 3,246 230 341 784D. Basic Inter-

mediates 3,168 868 8,800 3,912 28,639 9,524 451 243 1097E. Machinery 4,484 914 6,038 1,823 18,714 6,633 199 364 726Total Manufacturing 20,629 6,044 11.5 38,353 13,746 16.3 96,186 32,646 21.2 227 237 540

III.Social OverheadA. Electricity,

Gas, Water 421 292 1,164 717 3,326 1,970B. Construction 5,766 3,229 8,863 4,854 15,873 8,788C. Transportation 5,087 2,809 9,746 5,186 22,952 13,990Total SocialOverhead 11,274 6,330 12.1 19,773 10,757 12.7 42,151 24,748 16.1 170 230 391

IV. Services 16,819 15,071 28.7 29,360 26,284 31.1 61,174 52,782 34.3 174 201 350

Import Taxes 3,235 6.2 4,132 4.9 8,582 5.5

TOTAL (GDP, m.p.) 52,412 100.0 84,511 100.0 153,961 100.0 161 182 294

1/ X, V and S denote, respectively, production (including import taxes), value added (producer prices, excluding importtaxes) and percent share of GDP. 1953 figures are 1952-54 averages. 1963 and 1973 values are derived from deflatedI-0 tables.

Sources: Deflated I-0 tables

Table 3.4

Trade by Major Sectors, 1953 - 1973 1/

Index (E) Index (M)1953 1963 1973 1963 1973 1963 1973E M E M E M 1953 1963 1953 1963------------ (Million 1968 TL) ------------------

I. PrimaryA. Agriculture 2,173 301 2,191 748 2,619 365B. Mining 181 10 96 430 168 1,350Total Primary 2,354 311 2,287 1,178 2,787 1,715 97 122 379 146

II. ManufacturingA. Food 73 18 213 226 2053 127B. Textile and Leather 17 211 106 142 758 188C. Light Intermediates - 210 2 377 30 203D. Basic Intermediates 133 980 149 1215 558 5264E. Machinery 4 2,938 - 3,029 134 5,918Total Manufacturing 227 4,357 470 4,989 3,533 11,700 207 752 115 235

III.Social Overhead 249 84 503 280 1,883 346 202 375 333 124IV. Services 186 - 668 372 2,158 547 359 323 -- 147

TOTAL 3,016 4,752 3,928 6,819 10,361 14,308 130 264 143 210

1/ E and M denote, respectively, exports (ex-factory) and imports (c.i.f.) measured in 1968 constant domestic price.1953 figures are 1952-54 averages. 1963 and 1973 values are derived from deflated I-0 tables. The transport andtrade margins on commodity exports are included in the social overhead and services exports, respectively.

Sources: Deflated I-O tables.

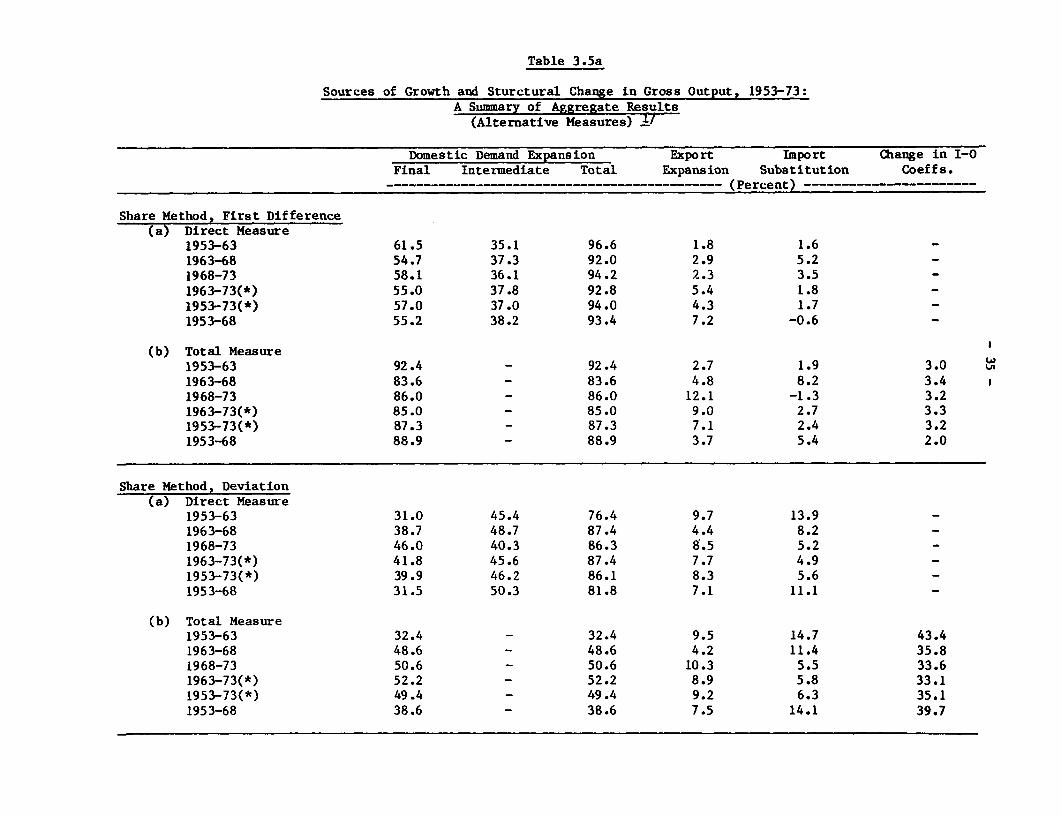

- 34 -

sectoral changes, whereas the economy-wide deviation measures are based on the

absolute totals of sectoral deviations, disregarding their algebraic signs.

The measures derived from the decomposition of gross output are shown in

percentage terms in Table 3.5 (a and b) for all the methods used in the

analysis.

Table 3.5 shows that the relative importance of the relevant factors

significantly varies according to which decomposition measure is used. This

indicates which factors contributed more to growth (as represented by the

first difference measures) or to structural change (as represented by the

deviation measures). Under the first difference measure, the increase in

domestic final demand accounted for 87.3 percent of the increase in total

gross output in 1953-73. Yet, according to the deviation measure,

nonproportional growth of this factor explained 49.4 percent of the structural

change in production. Technological change is also a significant factor in

nonproportional expansion (structural change), in addition to its minor role

in total growth.

Table 3.5 also indicates the significance of trade in growth and

structural change. From 1953-73 the combined trade effects (of export

expansion and import substitution) accounted for 9.5 percent of growth (first

difference total measure), and 15.5 percent of the structural change in the

overall economy (deviation total measure). Import substitution was more

important in structural change than aggregate growth (6.3 versus 2.4 percent).

Yet the differences in the growth and structural effects of export expansion

are less pronounced in nearly all subperiods. This reflects relative

stability in the commodity composition of exports during the period.

Furthermore, a comparison of the total measures with the direct

measures indicates the predominant role of domestic final demand expansion in

Table 3.5a

Sources of Growth and Sturctural Change in Gross Output, 1953-73:A Summary of Aggregate Results

(Alternative Measures) Yf

Domestic Demand Expansion Export Import Change in I-0Final Intermediate Total Expansion Substitution Coeffs.

…----------…----------------------------- (Percent) -----------------…

Share Method, First Difference(a) Direct Measure

1953-63 61.5 35.1 96.6 1.8 1.6 -1963-68 54.7 37.3 92.0 2.9 5.2 -1968-73 58.1 36.1 94.2 2.3 3.5 -1963-73(*) 55.0 37.8 92.8 5.4 1.8 -1953-73(*) 57.0 37.0 94.0 4.3 1.7 _1953-68 55.2 38.2 93.4 7.2 -0.6 -

(b) Total Measure1953-63 92.4 - 92.4 2.7 1.9 3.01963-68 83.6 - 83.6 4.8 8.2 3.41968-73 86.0 - 86.0 12.1 -1.3 3.21963-73(*) 85.0 - 85.0 9.0 2.7 3.31953-73(*) 87.3 - 87.3 7.1 2.4 3.21953-68 88.9 - 88.9 3.7 5.4 2.0

Share Method, Deviation(a) Direct Measure

1953-63 31.0 45.4 76.4 9.7 13.9 -1963-68 38.7 48.7 87.4 4.4 8.2 -1968-73 46.0 40.3 86.3 8.5 5.2 -1963-73(*) 41.8 45.6 87.4 7.7 4.9 -1953-73(*) 39.9 46.2 86.1 8.3 5.6 _1953-68 31.5 50.3 81.8 7.1 11.1 -

(b) Total Measure1953-63 32.4 - 32.4 9.5 14.7 43.41963-68 48.6 - 48.6 4.2 11.4 35.81968-73 50.6 - 50.6 10.3 5.5 33.61963-73(*) 52.2 - 52.2 8.9 5.8 33.11953-73(*) 49.4 - 49.4 9.2 6.3 35.11953-68 38.6 - 38.6 7.5 14.1 39.7

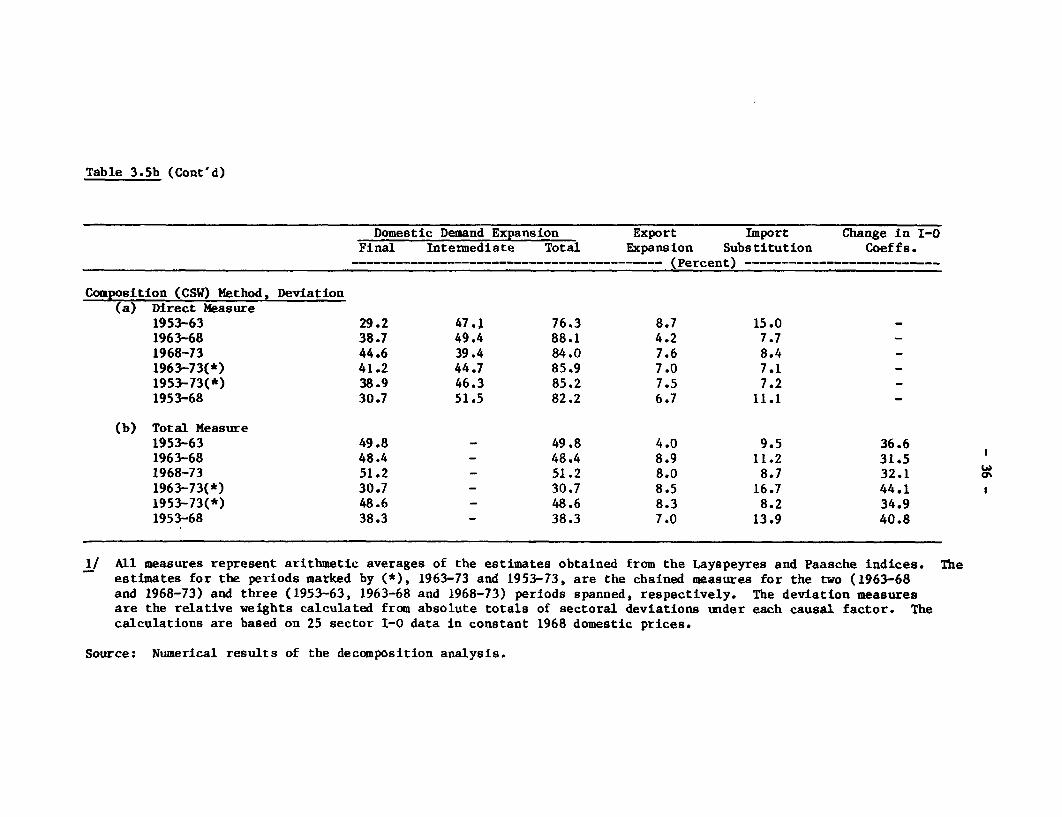

Table 3.5b (Cont'd)

Domestic Demand Expansion Export Import Change in I-0Final Intermediate Total Expansion Substitution Coeffs.

------------------------------------------ (Percent) --------------------------

Composition (CSW) Method, Deviation(a) Direct Measure

1953-63 29.2 47.1 76.3 8.7 15.0 -1963-68 38.7 49.4 88.1 4.2 7.7 -1968-73 44.6 39.4 84.0 7.6 8.4 -1963-73(*) 41.2 44.7 85.9 7.0 7.1 _1953-73(*) 38.9 46.3 85.2 7.5 7.2 _1953-68 30.7 51.5 82.2 6.7 11.1 -

(b) Total Measure1953-63 49.8 - 49.8 4.0 9.5 36.61963-68 48.4 - 48.4 8.9 11.2 31.51968-73 51.2 - 51.2 8.0 8.7 32.11963-73(*) 30.7 - 30.7 8.5 16.7 44.11953-73(*) 48.6 - 48.6 8.3 8.2 34.91953-68 38.3 - 38.3 7.0 13.9 40.8

1/ All measures represent arithmetic averages of the estimates obtained from the Layspeyres and Paasche indices. Theestimates for the periods marked by (*), 1963-73 and 1953-73, are the chained measures for the two (1963-68and 1968-73) and three (1953-63, 1963-68 and 1968-73) periods spanned, respectively. The deviation measuresare the relative weights calculated from absolute totals of sectoral deviations under each causal factor. Thecalculations are based on 25 sector 1-0 data in constant 1968 domestic prices.

Source: Numerical results of the decomposition analysis.

- 37 -

generating intermediate demand increases. This result, known as the backward

linkage effect, explains about 37 percent of the increase in total output from

1953-73. Under deviation analysis, nonproportional growth of intermediate

demand is largely attributed to the effects of technological change rather

than to the nonproportional growth of domestic final demand. Additionally,

the backward linkage effects of trade factors on the general economy appear to

be small, except in 1963-68 and 1968-73 when import substitution and export

expansion, respectively, became more important.

A general view of the economy also demonstrates the varying

proportions of trade effects over time. The relative contributions of import

substitution were higher than those of export expansion during 1953-63 and

1963-68, while a sharp reversal occurred in their relative roles in 1968-73.

These results are broadly in line with the shifts in trade policies previously

noted. According to the measures calculated separately for 1953-68, import

substitution had a significant impact on structural change in production under

the semi-closed development policies of the 1950s and 1960s, but it lost most

of its influence in the early 1970s.

The differences in the treatment of import substitution under these

various approaches is indicated by a comparison of the deviation measures

obtained under the composition and share methods. Under the composition

method, which treats import substitution in relation to total GDP rather than

to sector demand, the relative contribution of import substitution appears to

be affected by variations in the nonproportional growth rates of imports.

This point will be discussed below in regard to the major sectors.

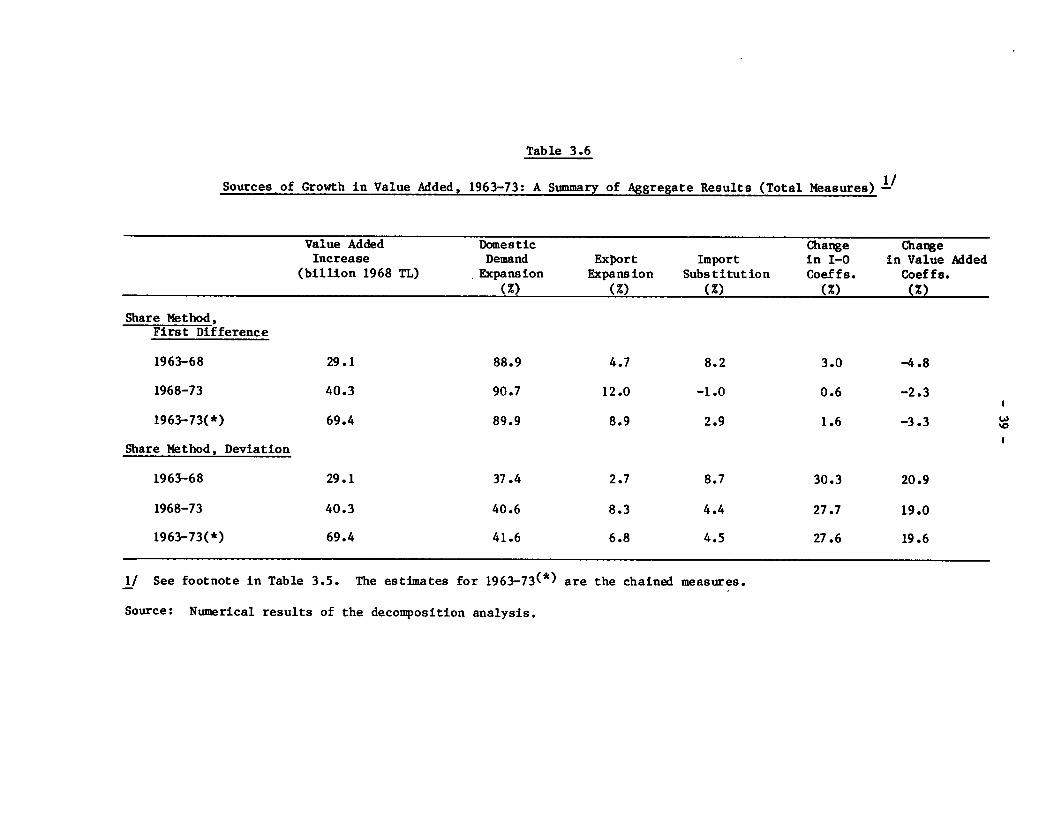

The measures for the decomposition of value added are also combined

at the national economy level, as shown in Table 3.6. These measures support