SOLVENCY II – UNDERWRITING CREDIT RISK MODELS1-6/ 2010, 295-319, Universidad Pontificia Javeriana...

34

SOLVENCY II – UNDERWRITING CREDIT RISK MODELS By Juan Casanovas Arbo Dpto: Economía, Estadística y Economía Española Universitat de Barcelona

Transcript of SOLVENCY II – UNDERWRITING CREDIT RISK MODELS1-6/ 2010, 295-319, Universidad Pontificia Javeriana...

SOLVENCY II – UNDERWRITING CREDIT RISK MODELS

By Juan Casanovas Arbo Dpto: Economía, Estadística y Economía Española Universitat de Barcelona

Contents and introduction

Solvency II Background Documents

Directive of Solvency II (25/11/2009), Directive 2009/138/CE. Draf Implementing measures Level 2 (2010), Working Document EIOPC/SEG/IM13/2010. ROSP (1998) BOE 282/1998 25/11/1998

QIS5 – Thecnical Specifications Sumamary (201)

EIOPA 2011 QIS5 Report. EIOPA Report on the fifth Quantitative Impact Study (QIS5) for Solvency II. EIOPA-TFQIS5-11/001 de 14 de Marzo de 2011, https://eiopa.europa.eu

UNESPA QIS5 Informe. UNESPA: Resultados QIS5 Mercado Español. Madrid 23/3/2011, www.dgsfp-meh.es/sector/sol2_Qis5/qis5230311.asp, julio/2012

DGSyFP Presentación Resultados QIS5 23/03/2011. Disponible en : www.dgsfp-meh.es/sector/sol2_Qis5/qis5230311.asp, julio/2012

Bibliography

Bermúdez y Morata, L. (2010) Métodos Estocásticos para el Cálculo de la Provisión Técnica de Prestaciones Pendientes en Solvencia II. Grupo de Investigación RFA-IREA, Universidad de Barcelona. http://www.ub.edu/dpees/risk, julio/2012. Carrillo, S. (2005). Basilea II: Una Mirada Crítica, Mediterraneo Económico” nº 8, ISBN 84-95531-28-3DL AL-400-2005. Editado por: Instituto de Estudios Económicos de Cajamar. Casanovas, J. (2012). La medición de la Solvencia del Riesgo de Suscripción en el ramo de Crédito. Master de Investigación en Empresas, Finanzas y Seguros. Universidad de Barcelona. Diers, D. (2011). Management Strategies in Multi-year Enterprise Risk Management. Risk Management, Provinzial NordWest Holding and University of Ulm, Provinzial Alice 1, Muenster 48131, Germany. The Geneva Papers 2011, 36, (107-125). www.genevaassociation.org. ©The International Association for the Study of Insurance Economics 1018-5895/11. England, P. y Verrall, R. (1999). Analytic and Bootstrap estimates of prediction errors in claims reserving. Insurance: Mathematics and Economics 25(1999) 281-293. England, P. y Verrall, R. (2002). Stochastic Claims Reserving in General Insurances. Presentación al Instituto de Actuarios 28 Enero 2002, B.A.J. 8,III, 443-544(2002). Galicia, M. (2003). Nuevos enfoques del Riesgo de Crédito. Instituto de Riesgo Financiero. México 2003. Gesmann, M. (2009). Claims Reserving in R The Chain-ladder package. Conference paper: One-Day Workshop 24 July, Stample Inn London. Rodríguez, E. ( 2007). Un modelo de reservas bancarias con correcciones macroeconómicas y financieras. Edición electrónica Diciembre 2007, ISBN 1850-3977 .Saavedra, M.L. y Saavedra, M.J. (2010). Modelos para medir el riesgo de crédito de la banca. Cuadernos de Administración vol. 23 num. 40 1-6/ 2010, 295-319, Universidad Pontificia Javeriana – Colombia. Sandström, A. (2006). Solvency, Models, Assessment and Regulation. Chapman & Hall/CRC ( Taylor and Francis Group ) 2006, ISBN 1-58488-554-8. The Solvency II Handbook (2009), Developing ERM Frameworks in Insurance and Reinsurance Companies. List of 33 authors. Edited by Marcelo Cruz. Risk Books, a división of Incisive Finantial Publishing Ltd.

Environment

Solvency II

Solvency II Manager

Other Managers

Internal teams

Advisors

Regulators/College of Regulators

Environment

The managers have a lack of knowledge of Internal Models

The advisors want to sell their own Solvency II product/model/software/time

The internal teams and the regulators are also more comfortable with as much capital as possible

The other managers have too many problems to help you

Standard Formula vs Internal Model

Scenario:

Standard Formula vs Internal Model

Scenario:

What do we need to use, SF or IM ?

Is it possible to apply more than one type of Internal Model ?

What about the SCR for each IM ?

At what cost ?

Scenario:

To answer this question we need to know

How many Models it is possible to use ?

The consecuences and Advantages of using each one.

How many Models is it possible to use ?

1.- Standard Formula

2.- IM imported from the Bank Sector

3.- IM according to the Insurance Technical P&L

4.- IM related to the BE of the Technical Provisions

How many Models is it possible to use

First approach:

The methodologies and the data are extremely different

It is possible to use these different methodologies ?

Is possible to use these different methodologies ?

The Solvency II Directive and the QIS5 Technical Specifications :

Premium and Reserve Credit and Suretyship Standard Formula => Non life insurance standard formula

But, the most important Credit Insurance players are using the “Bank credit methodology defined in Basel II”

The consequences of using each one

When we apply these different models to one specific portfolio, the resulting Underwriting SCR resulting from

each different model, shows a wide range

The consequences of using each one

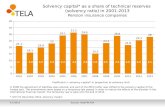

What wide range means ( only Underwriting Credit Risk)

Source: Percentatges come from Own source

QIS5 Spanish line of business results

Premium and Reserve SCR / Premium

source: DGSyFP Presentacion Resultados QIS 23/03/2011, and UNESPA Informe Resultados QIS5 Mercado Español

Catastrophic SCR / Premium

Source: DGSyFP Presentacion Resultados QIS% 23/03/2011, and UNESPA Informe Resultados QIS5 Mercado Español

QIS5 Spanish line of business results

The target

The target

To improve the knowledge of the different models in evaluating the Solvency II Underwriting Credit Risk Capital Required, and to analyse the reasons for the wide range of

results

And taking into consideration for each selected model The treatment of Catastrophic Risk The 12 month time horizon defined in Solvency II

The Risks

Underwriting Risk includes

Premium and Reserve Risk

Lapse Risk

Catastrophic Risk

The Standard Formula

(1) Carrillo 2005 – Basilea II – Una mirada Crítica

The Standard Formula

:it is the BASELINE REFERENCE for all Internal Models. In any case companies need to evaluate the standard formula

LIMITATIONS:

Use the VaR methodology over Premiums and Reserves. => That means assuming the Normal Distribution.

In the Credit Insurance business, we know, the variables are “Financial” and show leptocurtosis + Asymmetric distribution.

Also they lose subaditivity and diversification effects.

Complex to work with, and easy to make mistakes (1) Carrillo 2005 – Basilea II – Una mirada Crítica

The Standard Formula

Lapse Risk:

Catastrophic Risk: The SF-> 2 scenarios: 3 Big Claims + Recession Risk. Double Accounting ? Is it possible to separate the catastrophic information ?

(1) Carrillo 2005 – Basilea II – Una mirada Crítica

The adapted Bank Credit Model

The adapted Bank Credit Model

The Bank Credit Model needs to be calibrated in order to adapt it to the insurance activity The Insurance Short term risk vs the Bank large term risk A significant portion of risk is ceded to the reinsurers Different reasons for losses and different levels of loss amounts It is possible to re-underwrite or cancel the risk at “any” moment The client takes part of their own risk Additional conditions: e.g. Prudent credit management requirement

The adapted Credit Bank Model

The Model: We generate and important number of interactions with a Monte-Carlo methodology, mixing Internal Information of buyers and credit exposures plus the enviroment factors through the scenario calculation which give the maximum expected loss at 99.5% ADVANTATGES and LIMITATIONS Well adapted to day by day operation Complex and Expensive Models Complex to coordinate with the BE of Technical Provisions With high SCR Volatility Models without empirical testing in their adaptation to the Insurance product Difficult to change the 12 month time horizon The Catastrophic Risk is implicit in the data for the General Model and it is not easy to segregate and evaluate separately

IM based on the Technical P&L

IM based on the Technical P&L

The Model: We generate from the distribution functions from each element of the technical P&L with it´s correlations and important number of interactions with a Monte-Carlo methodology which give the maximum expected loss at 99.5% ADVANTATGES and LIMITATIONS: Models relatively easy to assimilate Easy to assume a different time horizon The Model implies the BE sub-model in order to evaluate the technical Provisions The Model is defined by internal parameters, normally means lower SCR Volatility Catastrophic Risk is implicit in the data for the General Model and it is not easy to segregate and evaluate separately

IM according to the BE of the Technical Provisions ?

IM according to the BE of the Technical Provisions The Model: We are evaluating the BE of the Technical Provisions at 50% of default probability and we include it in our Balance Sheet in IFR´s. It is easy to select the value (Claims Provisions SCR)at 99.5% This Model only answers the Cleims Provisions with any extreme scenario, including the catastrohic escenario. We know the methodology and the results wery well. It is easy to adapt and include a simple procedure to add the Premium SCR and the Lapse Risk. ADVANTATGES and LIMITATIONS Models in work and easy to adapt. Contrasted Models Defined by Internal Parameters. Lower SCR Volatility Specific Time Horizon: Only referred to a claims occurred before date Catastrophic Risk: Not easy to evaluate separetely with normal claims in the triangles

The time horizon

Solvency II establish a 12 months Time Horizon: Consequently by the treatment of the catastrophic events, the Reinsurance contracts, or the Business strategies (the ORSA report) the Capital Models and the Enterprise Risk Management need to be coherent and all together point at longer time horizon ( 3 or 5 years depending on the author) (1).

The present crisis is closing our access to the Financial Markets. A 12 months time horizon means if we have problems we need to close the business because even in the best case we don´t have/found enough capital to cover the SCR

(1) Diers D. (2011), Management Strategies in Milti-year Enterprise isk Management

Catastrophic Risk

Basically two options - Included in the Model ( all internal models) As well as accepting “ the past explain the future “ If not, how can we include the effects of unknow events ? - Evaluating separatly ( standard formula) In our practice, it was absolutely impossible to segregate the catastrophic events from our data.

Conclusions after analysis

The Standard Formula is not a Baseline Reference

There are enough evidence to give as the idea “we can reduce the SCR wide range ”

The Time Horizon need to be adapted according to the companies policies and the capital market and to be coherent with ORSA

The treatment of the Catastrophic risk need to be defined with realistic scenarios – take care with Double accounting and -- please not to use as a capital add-on –

Next steps

Next steps toward Underwriting Credit Insurance Risk 1.- Evaluate All Models one by one 2.- Suggest the changes to introduce in each model in order to reduce the wide range of SCR 3- To propose a new time horizon according to the Internal Models, the companies policies and the ORSA 4.- To propose a complementary definition of Catastrophic Risk acording the Internal models

SOLVENCY II – UNDERWRITING CREDIT RISK MODELS

By Juan Casanovas Arbo Dpto: Economía, Estadística y Economía Española Universitat de Barcelona

Thankyou for coming and for

your time