Slide 5.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education...

28

Slide 5.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education 2011 Chapter 5 Accounting information for service businesses

-

Upload

ernest-barnett -

Category

Documents

-

view

212 -

download

0

Transcript of Slide 5.1 Pauline Weetman, Financial and Management Accounting, 5 th edition © Pearson Education...

Slide 5.1

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Chapter 5

Accounting information for service businesses

Slide 5.2

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Assets denotes a decrease in an asset

Liabilities denotes an increase in a liability

Assets – Liabilities = Ownership interest

Accounting equation

Slide 5.3

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

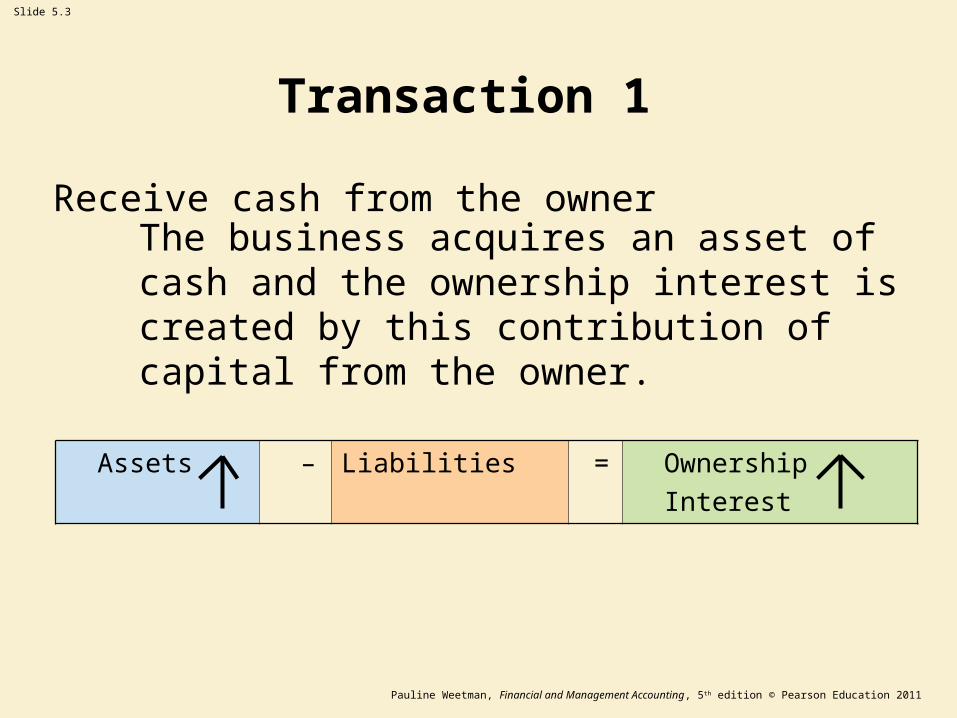

Transaction 1

Receive cash from the owner

The business acquires an asset of cash and the ownership interest is created by this contribution of capital from the owner.

Assets – Liabilities = Ownership

Interest

Slide 5.4

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Transaction 2

Buy a vehicle for cash

The business records an increase in one asset (the vehicle) but a decrease in another asset (cash).

Assets – Liabilities = Ownership interest

Slide 5.5

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Transactions (Continued)

See chapter for further illustrations of the effect of transactions on the accounting equation.

Slide 5.6

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

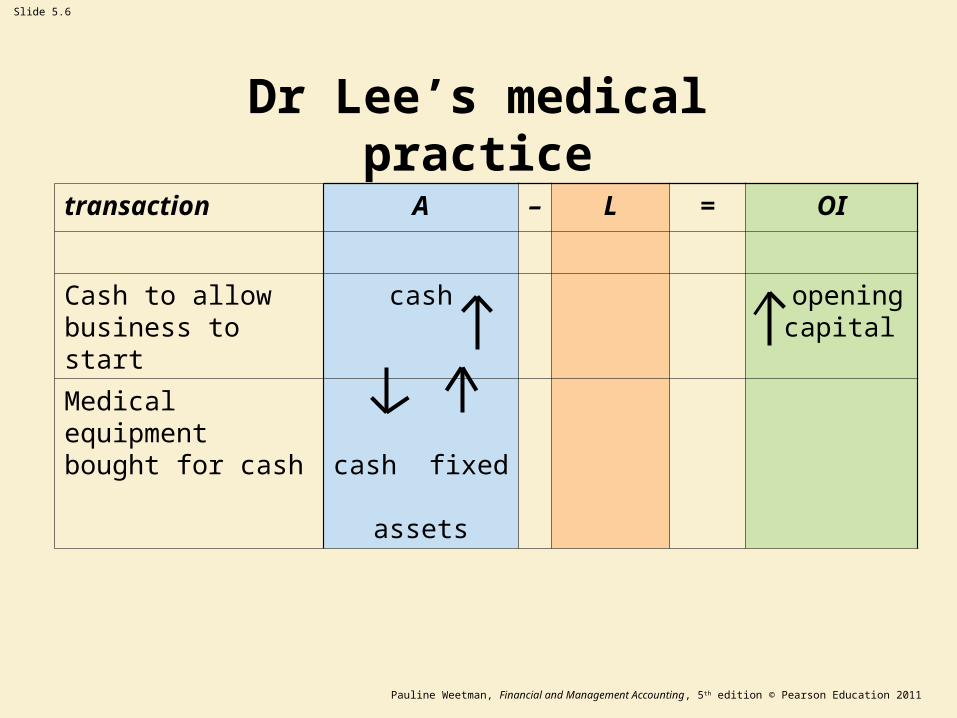

transaction A – L = OI

Cash to allow business to start

cash opening capital

Medical equipment bought for cash

cash fixed assets

Dr Lee’s medical practice

Slide 5.7

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dr Lee’s medical practice (Continued)

Purchase medical supplies on credit

Office furniture bought on credit

expensescashOne month’s rent

OI=L–Atransaction

fixed assets

Inventory(stock) of med.

supplies creditors

creditors

Slide 5.8

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

transaction A – L = OI

Pay employee cash expense

Four patients are examined, each paying £500 cash

cash revenue

The business pays cash for goods acquired on credit

cash Creditors

The business pays an electricity bill in cash

cash expense

Dr Lee’s medical practice (Continued)

Slide 5.9

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

transaction A – L = OI

Pay employee cash expense

Three patients examined, invoice sent requesting payment

trade receivables (debtors)

revenue

Pay employee cash expense

Cash for the examination of three patients

cashdebtors

Dr Lee’s medical practice (Continued)

Slide 5.10

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

transaction A – L = OI

Four patients areexamined; invoice sent requesting payment

trade receivables (debtors)

revenue

Dr Lee draws cashfrom the business for personal use

cash drawings

Pay employee cash expenses

The medical equipment and office furniture is estimated to have fallen in value

fixed assets expenses

Medical supplies costing £350 have been used

inventory (stock) of medical supplies

expenses

Dr Lee’s medical practice (Continued)

Slide 5.11

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

See Chapter 5 for:

• Spreadsheet entries

• Financial statements

Dr Lee’s medical practice (Continued)

Slide 5.12

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Chapter 5

Bookkeeping Supplement

Slide 5.13

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

DEBIT ENTRIES CREDIT ENTRIES

Left-hand side of the equation

Asset Increase Decrease

Right-hand side of the equation

Liability Decrease Increase

Ownership interest Expense Revenue

Capital withdrawn Capital contributed

Debit and credit entries in ledger accounts

Table 5.5 Rules for debit and credit entries in ledger accounts

Slide 5.14

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Transaction Aspects of the transaction

DEBIT ENTRY IN

CREDIT ENTRY IN

Receive cash from the owner

Acquisition of an asset (cash)

CASH

Acceptance of ownership interest

OWNERSHIP INTEREST

Buy a vehicle for cash

Acquisition of an asset (vehicle)

VEHICLE

Reduction in an asset (cash)

CASH

See Supplement to Ch 5 for more illustrations

Analysis of service business transactions

Table 5.6 Analysis of service business transactions (from Table 5.1) to identify two aspects of each

Slide 5.15

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Oct Transactions Amount Debit Credit

£

1 Cash to allow business to start

50,000 Cash Owner

2 Medical equipment bought for cash

30,000 Equipment

Cash

2 One month’s rent 1,900 Rent Cash

2 Office furniture bought on credit

6,500 Furniture Office supplies

Debit and credit transactions of medical practice

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice

Slide 5.16

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Debit and credit transactions of medical practice (Continued)

7 Purchase medical supplies on credit

1,200 Inventory (stock)

P. Jones

8 Pay employee 300 Wages Cash

10 Four patients are examined, each paying £500 cash

2,000 Cash Patients’ fees

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

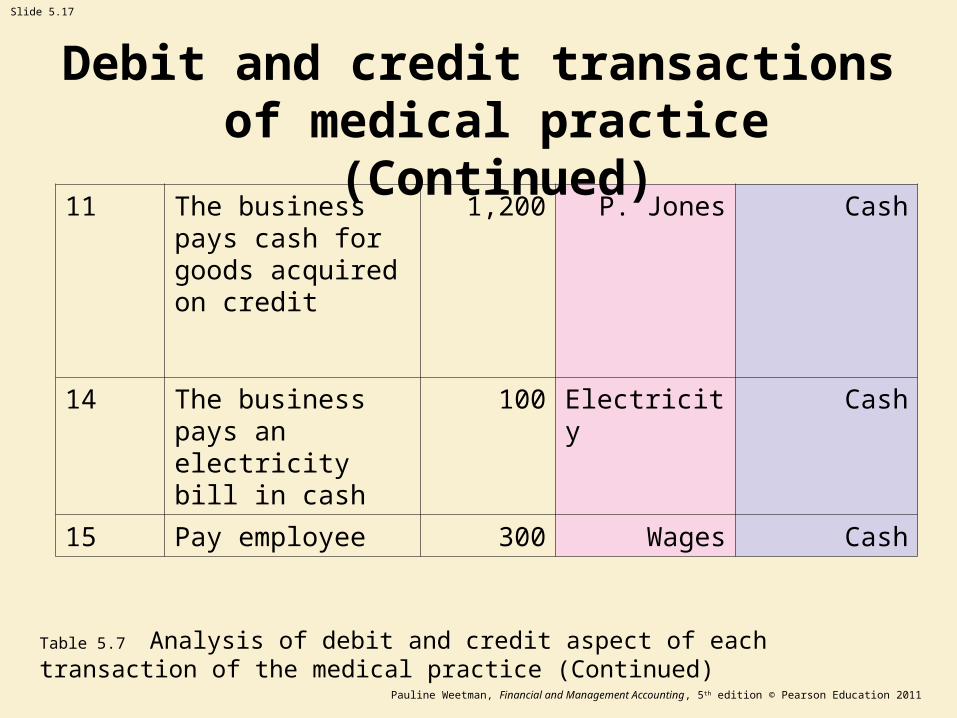

Slide 5.17

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

11 The business pays cash for goods acquired on credit

1,200 P. Jones Cash

14 The business pays an electricity bill in cash

100 Electricity Cash

15 Pay employee 300 Wages Cash

Debit and credit transactions of medical practice (Continued)

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

Slide 5.18

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

17 Three patients examined, invoice sent requesting payment

1,500 Mrs West Fees

22 Pay employee 300 Wages Cash

Debit and credit transactions of medical practice (Continued)

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

Slide 5.19

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

23 The employer (Mrs West) pays in cash for the examination of three patients

1,500 Cash Mrs West

24 Four patients are examined, invoice sent requesting payment

2,000 Mr East Fees

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

Debit and credit transactions of medical practice (Continued)

Slide 5.20

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

28 Dr Lee draws cash from the business for personal use

1,000 Owner Cash

29 Pay employee 300 Wages Cash

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

Debit and credit transactions of medical practice (Continued)

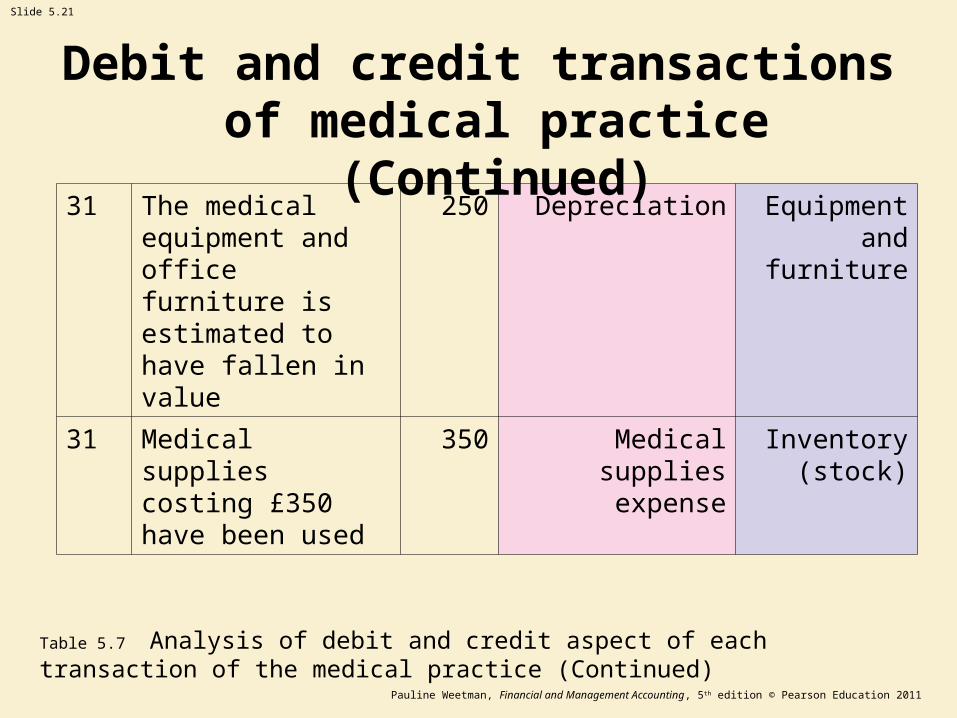

Slide 5.21

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

31 The medical equipment and office furniture is estimated to have fallen in value

250 Depreciation Equipment and furniture

31 Medical supplies costing £350 have been used

350 Medical supplies expense

Inventory (stock)

Table 5.7 Analysis of debit and credit aspect of each transaction of the medical practice (Continued)

Debit and credit transactions of medical practice (Continued)

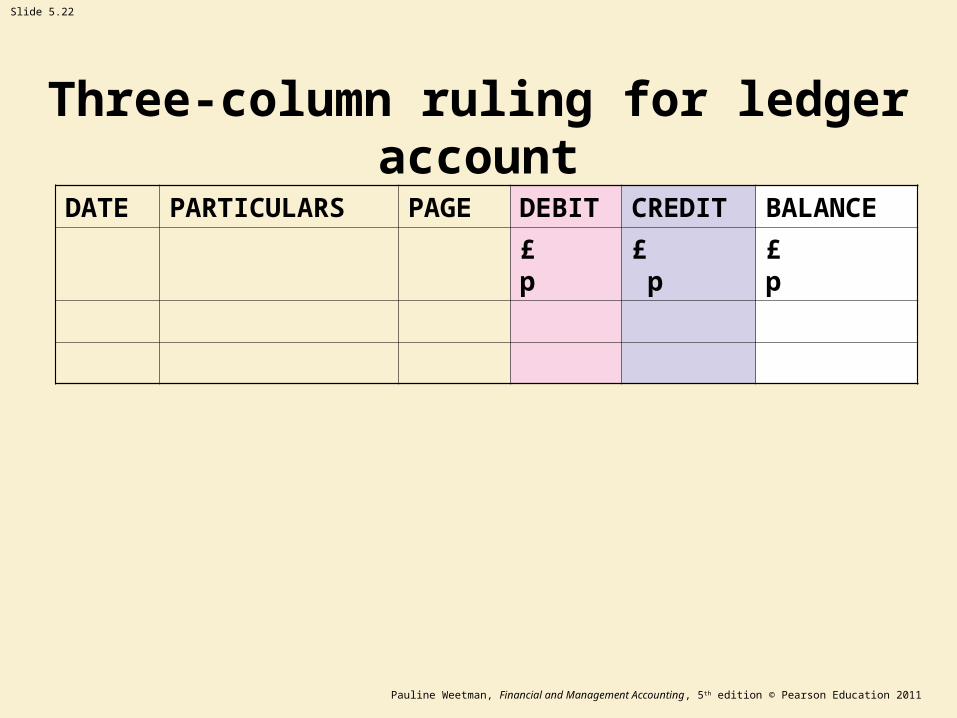

Slide 5.22

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

DATE PARTICULARS PAGE DEBIT CREDIT BALANCE

£ p £ p £ p

Three-column ruling for ledger account

Slide 5.23

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

DEBIT ENTRIES CREDIT ENTRIES

DATE PARTIC-ULARS

PAGE £ p DATE PARTIC-ULARS

PAGE £ p

Balance

T-Account form of ledger account

Slide 5.24

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

L1 Cash L8 Inventory (stock) of medical supplies

L2 Ownership interest L9 P. Jones

L3 Medical equipment and office furniture

L10 Electricity

L4 Office Supplies Company L11 Mrs West

L5 Rent L12 Mr East

L6 Wages L13 Depreciation

L7 Patients’ fees L14 Expense of medical supplies

Ledger account titles

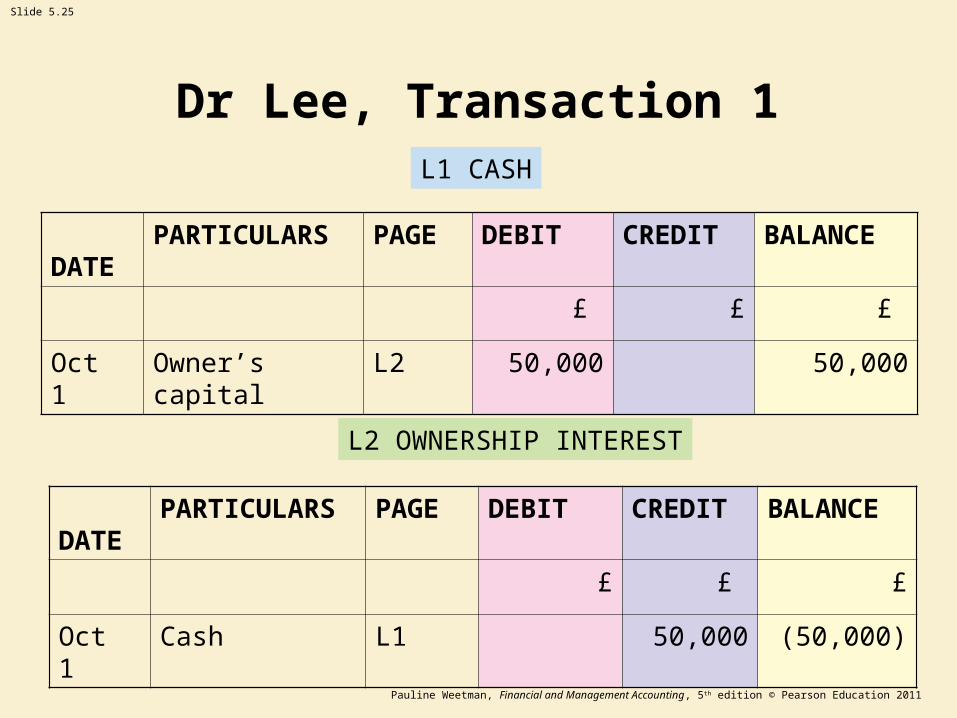

Slide 5.25

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

L1 CASH

DATEPARTICULARS PAGE DEBIT CREDIT BALANCE

£ £ £

Oct 1 Owner’s capital L2 50,000 50,000

L2 OWNERSHIP INTEREST

DATEPARTICULARS PAGE DEBIT CREDIT BALANCE

£ £ £

Oct 1 Cash L1 50,000 (50,000)

Dr Lee, Transaction 1

Slide 5.26

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Checking the accuracy of double entry records

• A summary of all the balances at the end of the accounting period is called a Trial Balance (‘trial’ means ‘tests the accuracy’ of the balances).

• If the total of the debit balances equals the total of the credit balances then we know that the total of the debit entries in the ledger accounts must equal the total of the credit entries in the ledger accounts.

Slide 5.27

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Error detection

Errors which will be detected by unequal totals in the trial balance

• Entering only one aspect of a transaction (e.g. a debit entry but no credit entry).

• Writing different amounts in each entry (e.g. debit £290 but credit £209).

• Writing both entries in the same column (e.g. two debits, no credit).

• Incorrect calculation of ledger account balance.

Slide 5.28

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Error detection (Continued)

Errors which will not be detected because they leave the trial balance totals equal

• Omitting both aspects of a transaction.

• Errors in both debit and credit entry of the same magnitude.

• Entering the correct amount in the wrong ledger account (e.g. debit for wages entered as debit for heat and light).