SGS 2016 Half Year Results Presentation

45

-

Upload

sgs -

Category

Investor Relations

-

view

708 -

download

3

Transcript of SGS 2016 Half Year Results Presentation

2 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

DISCLAIMER

Certain matters discussed in this presentation may constitute forward-looking

statements that are neither historical facts nor guarantees of future performance.

Because these statements involve risks and uncertainties that are beyond control or

estimation of SGS, there are important factors that could cause actual results to

differ materially from those expressed or implied by these forward-looking

statements. These statements speak only as of the date of this document. Except

as required by any applicable law or regulation, SGS expressly disclaims any

obligation to release publicly any updates or revisions to any forward-looking

statements contained herein to reflect any change in SGS Group’s expectations

with regard thereto or any change in events or conditions on which any such

statements are based.

4 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 HIGHLIGHTS

(1) Constant currency basis – (2) Before amortisation of acquisition intangibles, restructuring, transaction and

integration-related costs – (3) Cash flow from operating activities net of capital expenditures

5 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 ACQUISITIONS

(1) Minority equity stake

6 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

SUBSEQUENT EVENTS

(1) Final negotiations. Subject to closing conditions

7 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

88 400 EMPLOYEES(1) AND 1 800 OFFICES & LABORATORIES AROUND

THE GLOBE ENABLING REACH AND LOCAL SUPPORT

(1) End of period

8 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

9 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 FINANCIAL HIGHLIGHTS

(1) Before amortisation of acquisition intangibles, restructuring, transaction and

integration-related costs – (2) Constant currency basis

10 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

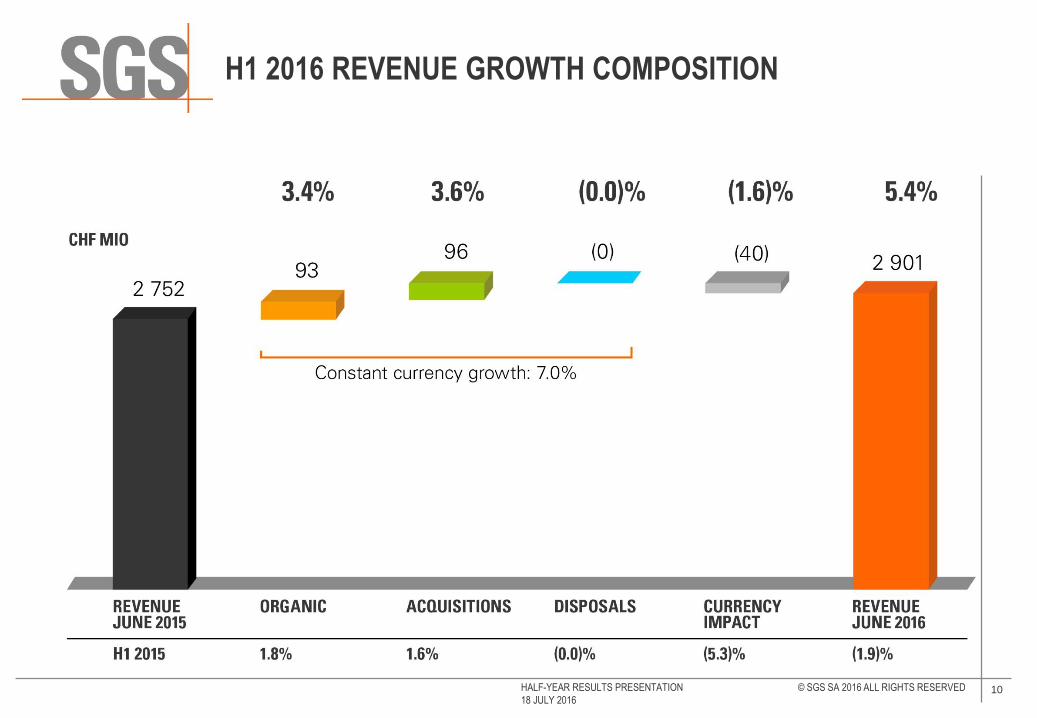

H1 2016 REVENUE GROWTH COMPOSITION

11 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 BUSINESS PORTFOLIO

12 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

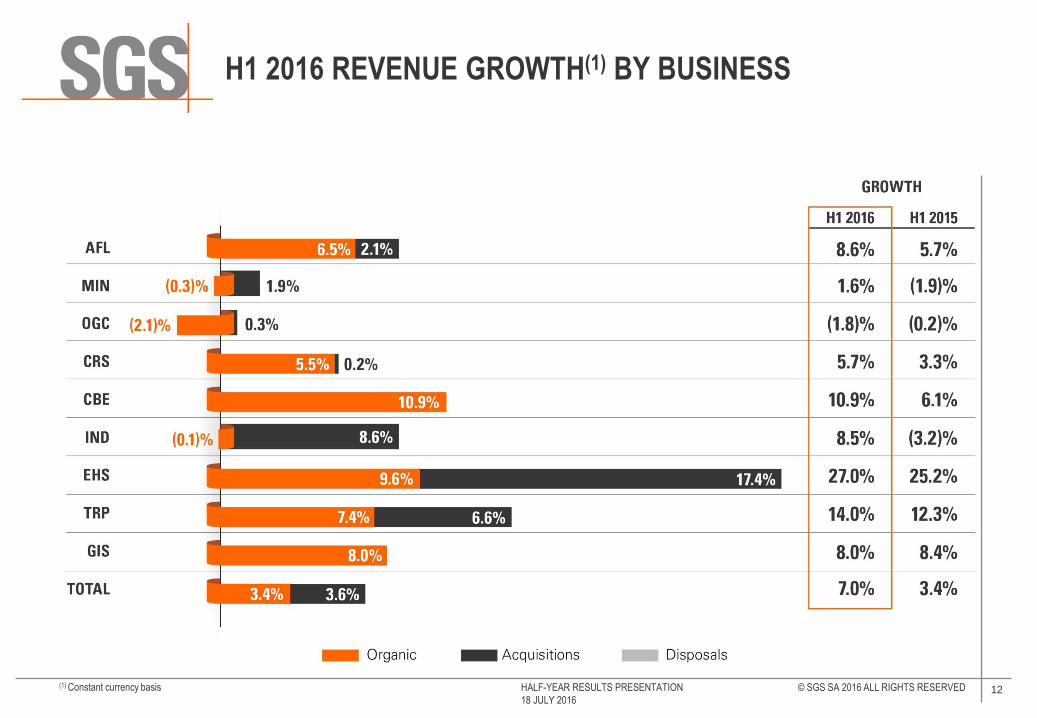

H1 2016 REVENUE GROWTH(1) BY BUSINESS

(1) Constant currency basis

13 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 REVENUE GROWTH(1) BY REGION

(1) Constant currency basis

14 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

EVOLUTION OF HEADCOUNTS

(1) As of 30 June 2016.

16 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

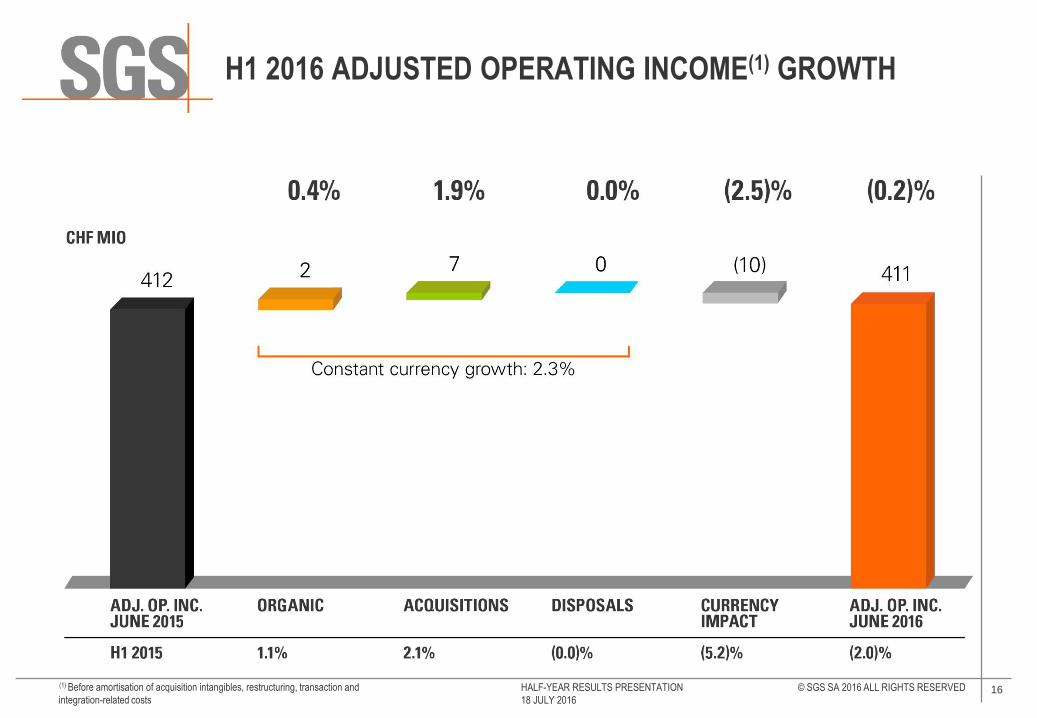

H1 2016 ADJUSTED OPERATING INCOME(1) GROWTH

(1) Before amortisation of acquisition intangibles, restructuring, transaction and

integration-related costs

17 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 ADJUSTED OPERATING INCOME(1) PORTFOLIO

(1) Before amortisation of acquisition intangibles, restructuring, transaction and

integration-related costs

18 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 ADJUSTED OPERATING MARGIN(1) BY

BUSINESS

(1) Before transaction and integration related costs, amortisation of acquisition intangibles and restructuring – (2) Constant currency basis – (3) Restated figures due to the change in business structure

20 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

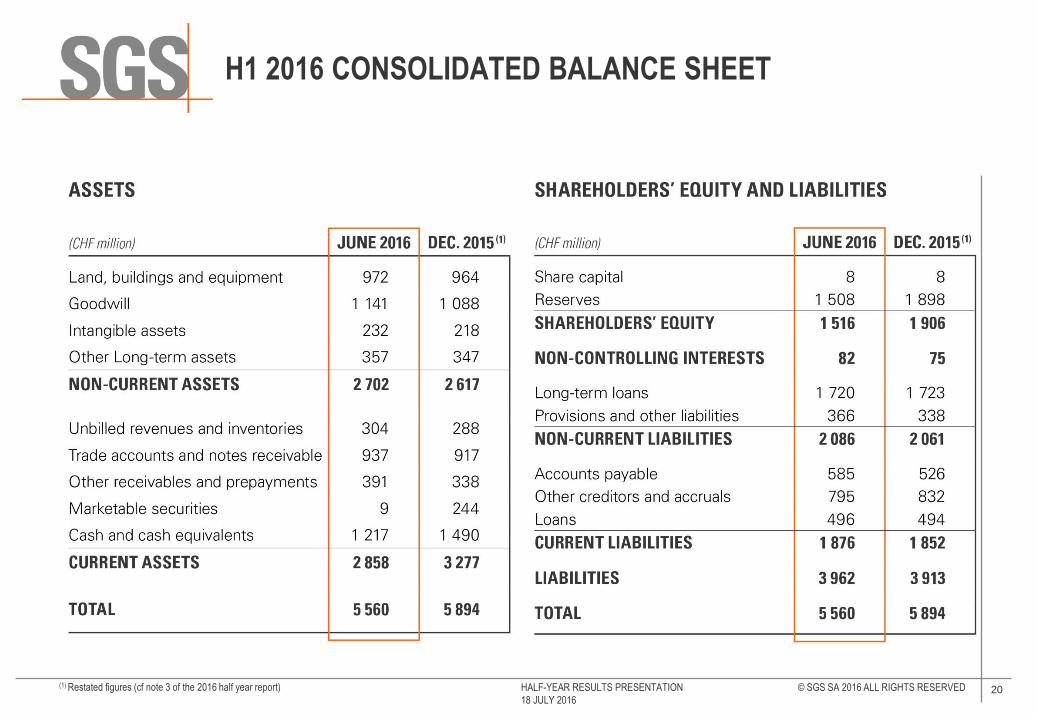

H1 2016 CONSOLIDATED BALANCE SHEET

(1) Restated figures (cf note 3 of the 2016 half year report)

22 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 CONDENSED CASH FLOW

(1) Before cash flows related to pension funds special contribution – (2) Cash flow from operating activities net of

capital expenditures

23 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

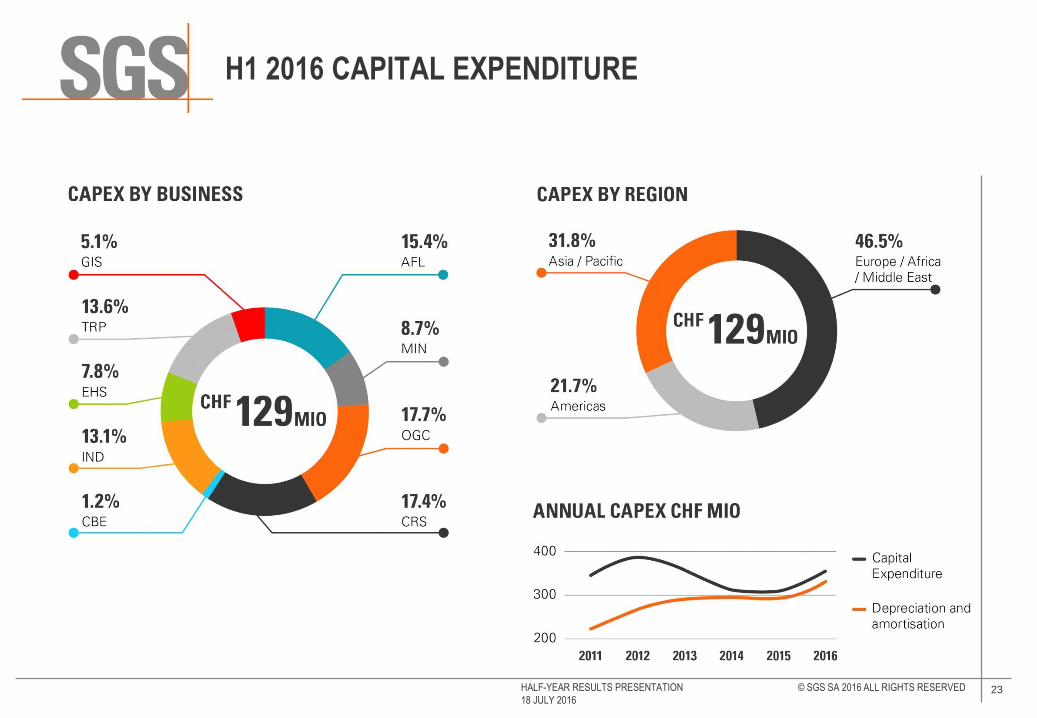

H1 2016 CAPITAL EXPENDITURE

25 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

H1 2016 FOREIGN CURRENCY REVENUES

26 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

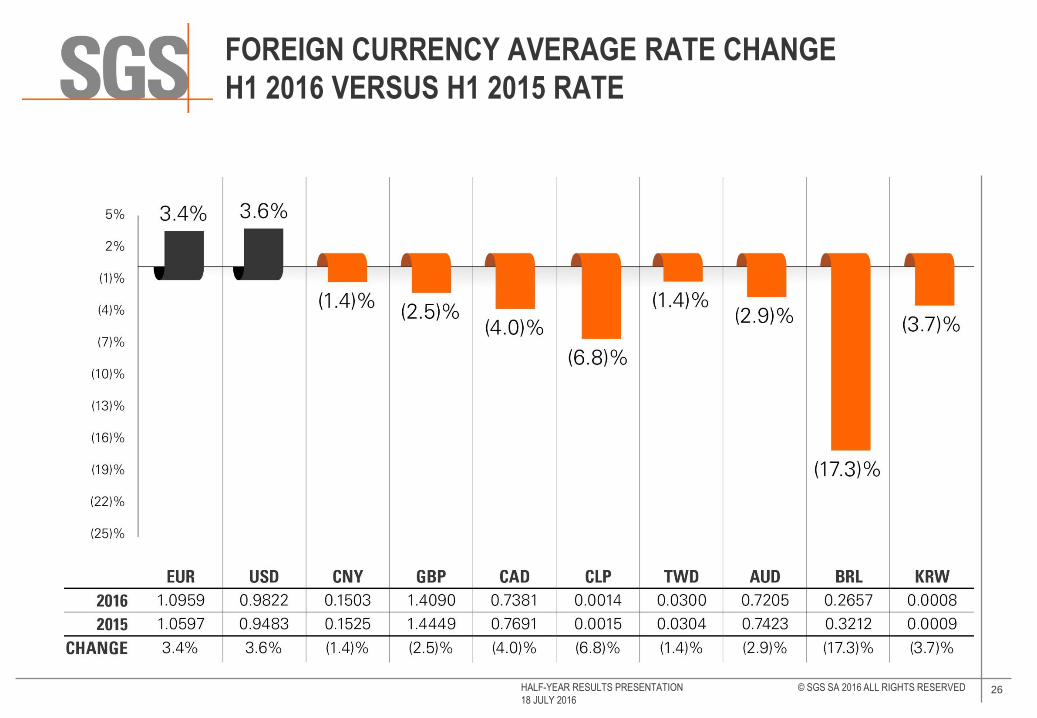

FOREIGN CURRENCY AVERAGE RATE CHANGE

H1 2016 VERSUS H1 2015 RATE

27 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

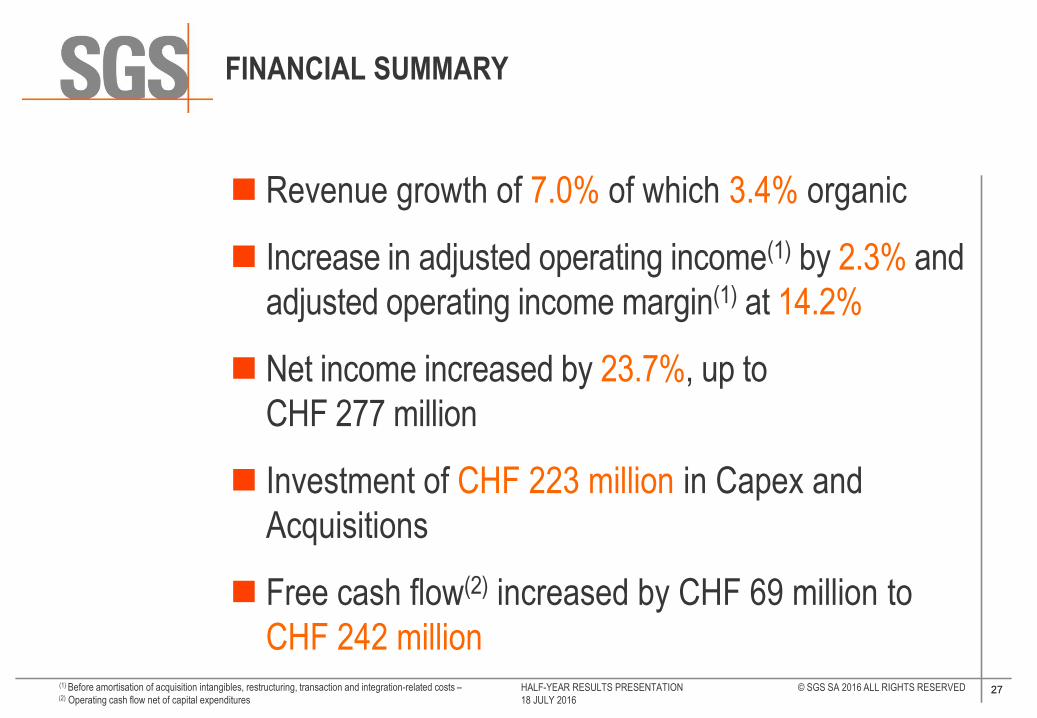

FINANCIAL SUMMARY

27

Revenue growth of 7.0% of which 3.4% organic

Increase in adjusted operating income(1) by 2.3% and

adjusted operating income margin(1) at 14.2%

Net income increased by 23.7%, up to

CHF 277 million

Investment of CHF 223 million in Capex and

Acquisitions

Free cash flow(2) increased by CHF 69 million to

CHF 242 million (1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs – (2) Operating cash flow net of capital expenditures

29 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

AGRICULTURE, FOOD & LIFE (AFL)

PERFORMANCE

Strong growth from Food and Life activities

Solid growth from Trade-related services

Seed & Crop impacted by slowdown in

agricultural input market

Food growth continues to be fuelled by

consumer safety concerns and investments in

testing capabilities

Stable Trade growth expected and agricultural

input market continues to be challenging

Life Lab growth in high single digits

Focus on solution enhancements and improve

efficiency

OVERVIEW

OUTLOOK

30 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis

MINERALS (MIN)

PERFORMANCE OVERVIEW

OUTLOOK

Onsite laboratories continue to grow

Geochem laboratories sample volumes

increase by 16% vs. prior year

Energy performs well, particularly in Russia

and South Africa

Trade Services remain flat

Metallurgy activities impacted by reduced

exploration spend

H2 expected to be flat

Interest in onsite gold laboratories strong

Optimise mine and plant services and

integration of Bateman Engineering services

Lean efficiency programmes to continue

31 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

OIL, GAS & CHEMICALS (OGC)

PERFORMANCE OVERVIEW

OUTLOOK

Flat growth in Trade related activity

Single-digit growth in Non-Inspection related

testing

Low single-digit growth in Plant and Terminal

Operations

Solid results in Fuel Integrity Programmes

activities and Oil Condition Monitoring

Project shutdowns and delays impact

Upstream services

Soft growth in Upstream services for the

Production segment from new contracts

Trade Related and Plant and Terminal

Operations to deliver low single-digit growth

Non-Inspection related testing is expected to

benefit from strong project pipeline

32 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

CONSUMER & RETAIL (CRS)

PERFORMANCE OVERVIEW

OUTLOOK

Strong results from Eastern Europe and

Middle East

Softlines and Hardlines experienced robust

growth recovery

Cosmetics, Personal Care and Household

(CPCH) remained strong in H1

Electrical & Electronics (E&E) performed well

despite challenges in Wireless Testing

Growth to continue in Softlines and Hardlines

Better E&E performance from Safety, EMC

and RSTS activities

Investment in capacities in new sourcing

countries

Focus on acquisitions to strengthen position in

key segments (CPCH, E&E)

33 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

CERTIFICATION & BUSINESS ENHANCEMENT (CBE)

PERFORMANCE OVERVIEW

OUTLOOK

Overall strong results with solid organic growth

Strong growth in medical device activities with

introduction of unannounced audits

Single-digit growth in Management System

Certification driven by new 2015 standards

Strong growth in Training activities from ISO

9001:2015 and Technical Training in China

Double-digit growth in Performance

assessment with several contract wins

Growth expected to remain healthy in the high

single digits driven by all major activities

Global Service Centre in Asia to open to

consolidate 4 countries by end of 2016

bringing further efficiency

34 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

INDUSTRIAL SERVICES (IND)

PERFORMANCE OVERVIEW

OUTLOOK

Canada delivered solid results following

restructuring

In Eastern Asia, lab activity slowdown from

reduced investments

Strong organic growth in Middle East and

South America

Diversification strategy in South America led to

increased revenue

Fully integrated 2015 acquisitions expected to

perform well

Market condition expected to remain difficult

during H2

Sample volumes to increase in laboratories in

all regions

Digital technology to support new services in

construction supervision market

35 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

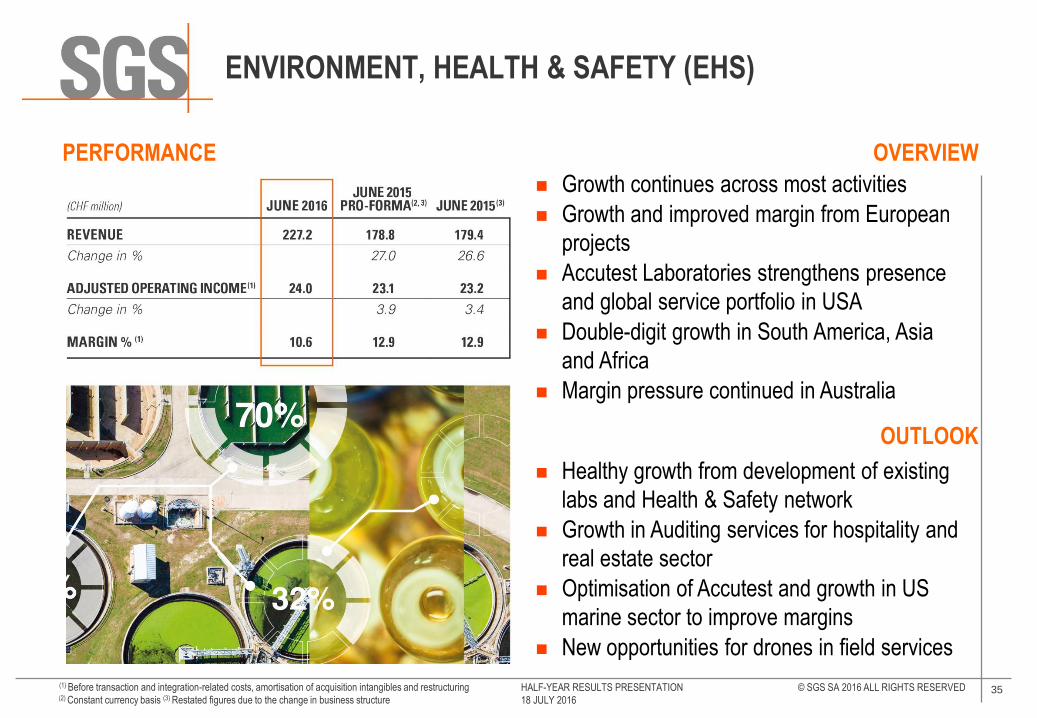

ENVIRONMENT, HEALTH & SAFETY (EHS)

PERFORMANCE OVERVIEW

OUTLOOK

Growth continues across most activities

Growth and improved margin from European

projects

Accutest Laboratories strengthens presence

and global service portfolio in USA

Double-digit growth in South America, Asia

and Africa

Margin pressure continued in Australia

Healthy growth from development of existing

labs and Health & Safety network

Growth in Auditing services for hospitality and

real estate sector

Optimisation of Accutest and growth in US

marine sector to improve margins

New opportunities for drones in field services

36 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis (3) Restated figures due to the change in business structure

TRANSPORTATION (TRP)

PERFORMANCE OVERVIEW

OUTLOOK

Solid performance globally in Regulated

services

Strong performance in commercial inspection

activities

Retail network solutions fully operational and

performing well

Recent acquisitions performing in line

Tightening of exhaust emissions regulations

will drive growth in emission testing

Technology shift to Connectivity and

Digitalisation will support solid supply chain

solutions growth

Positive outlook for regulated services in Africa

and South America

Focus on acquisitions in the Aerospace sector

37 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

(1) Before transaction and integration-related costs, amortisation of acquisition intangibles and restructuring (2) Constant currency basis

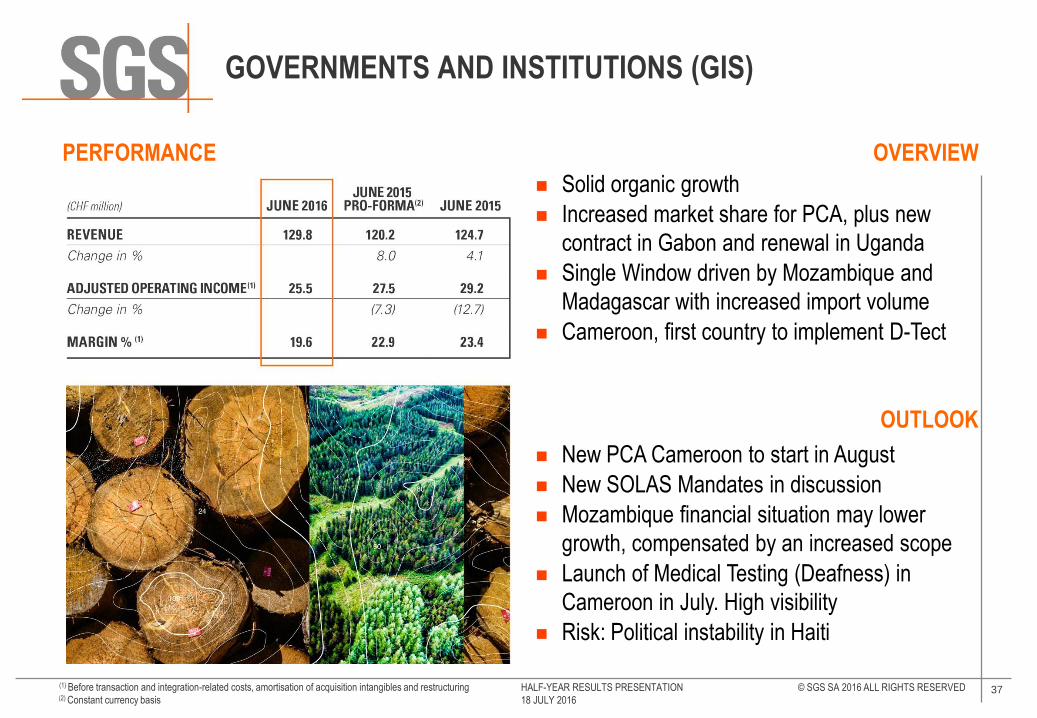

GOVERNMENTS AND INSTITUTIONS (GIS)

PERFORMANCE OVERVIEW

OUTLOOK

Solid organic growth

Increased market share for PCA, plus new

contract in Gabon and renewal in Uganda

Single Window driven by Mozambique and

Madagascar with increased import volume

Cameroon, first country to implement D-Tect

New PCA Cameroon to start in August

New SOLAS Mandates in discussion

Mozambique financial situation may lower

growth, compensated by an increased scope

Launch of Medical Testing (Deafness) in

Cameroon in July. High visibility

Risk: Political instability in Haiti

39 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

2016 GUIDANCE(1)

(1) At stable market conditions

40 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

SGS OUTLOOK 2016 – 2020

Mid single-digit organic growth on average with improvement over the period supported by the new focused structure and new strategic initiatives

Accelerating M&A activities with acquired revenue over the period in the range of CHF 1 billion

Adjusted operating income margin(1) of at least 18% by end of the period supported by the new focused structure, efficiency improvement initiatives and improved pricing

Strong cash conversion

Solid returns on invested capital

Solid dividend distributions, in line with improvement in net earnings

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related

costs

45 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

ACRONYMS AND OTHER ABBREVIATIONS

46 HALF-YEAR RESULTS PRESENTATION © SGS SA 2016 ALL RIGHTS RESERVED

18 JULY 2016

INVESTOR RELATIONS INFORMATION

WWW.SGS.COM

© S

GS

Gro

up M

anag

emen

t SA

– 2

016

– A

ll rig

hts

rese

rved

– S

GS

is a

reg

iste

red

trad

emar

k of

SG

S G

roup

Man

agem

ent S

A.