Educational Establishment in India Financial & Tax Considerations

Upload

agarwal-sanjiv-coCategory

view

358download

3

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

1

SERVICE TAX DOSSIER

on

EDUCATIONAL SERVICES

Introduction

Education is the life line of any nation and blood for economic growth. Our Government realizes

its importance and hence has taken several initiatives to boost the growth of this sector,

including setting up of several universities, deregulating policies and making significant pacts

with foreign nations. While education is a priority in Indian context, given its population base and

mounting service sector and its contribution to GDP, (about 60% now), coaching, which aids or

supplements formal education also plays a catalytic role in advancement of education in our

Country. Coaching, which is generally imparted on commercial basis is deep rooted in Indian

system and cannot be ignored or left unnoticed. Infact coaching and education go hand in hand

to a large extent.

Understanding the Concept of Education and Coaching

All education is not exempted and all coachings are not taxed. However, one needs to

understand the difference between the two terms – education and coaching.

According to Aiyar’s Advanced Law Lexicon, education means the bringing up, the process

of developing and training the powers and capabilities of human beings. It is an act of

providing with knowledge.

Coaching or training is a very narrow activity imparting skill in a particular discipline but

education is a broader term which is a process of development of personality of body, mind

and intellect. The scope of education is broad but training or coaching is in a particular field.

In ICAFI case [2009 -TMI - 32004 - Cestat, Bangalore], tribunal observed that coaching

normally refers to a special teaching or a personalized teaching in certain subjects. Training

is generally used to refer to practical instruction or learning process. Education is the

process of overall development of a person. It included moral, intellectual and physical

development of a child or a person. It is not restricted to a particular subject and it covers

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

2

various subjects and areas. Moreover, as distinguished from coaching, education is not

meant for succeeding in an examination or test but for overall development of the student.

Education is a term of wide import and encompasses within its ambit the specialized

function of training and coaching but this does not make all the three terms synonymous in

nature.

It is also true that Governments need fund to run the welfare state and to meet certain socio-

economic objectives which pave for economic growth. Taxes in various forms direct and

indirect come to the rescue of Government.

Education and coaching, being an important part of our service sector should, therefore also

attract taxation.

Service Tax

Service tax is an indirect tax to which education and coaching services could be exposed.

Service Tax law is a branch of tax where frequent changes have been made ever since it

was enacted in the year 1994 by the Finance Act, 1994 through Budget amendments-

Notifications and CBEC’s Circulars.

W.e.f. 01-07-2012, all services barring those which are in the Negative List (Section 66D of

the Finance Act, 1994) or have been exempted by way of exemption notifications are in

Service Tax net. We discuss the applicability or otherwise of Service Tax on education

related services pre and post 1.07.2012 in this document.

Taxability prior to 01-07-2012

Upto 30-06-2012, only specified services were taxable, i.e., tax was ‘services’ specific. No

special head ‘educational service’ was specified in the service tax law prior to 01-07-2012.

However, Notification No. 33/2011-ST dated 25-04-2011 exempted services of pre-school,

training and coaching or training leading to grant of certificate recognized by law.

What was taxed to Service Tax prior to 01.07.2012 was services of commercial coaching

and training which was defined under section 65 as follows:

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

3

As per section 65(26) of the Finance Act, 1994, ‘commercial training or coaching’

means any training or coaching provided by a commercial training or coaching

centre. (as amended)

As per section 65(27) of the Finance Act, 1994, ‘commercial training or coaching

centre’ means any institute or establishment providing commercial training or

coaching for imparting skill or knowledge or lessons on any subject or field other

than the sports, with or without issuance of a certificate and includes coaching or

tutorial classes.(as amended)

As per section 65(105) (zzzc) of the Finance Act, 1994, services provided to any

person, by a commercial training or coaching centre in relation to commercial

training or coaching;

Explanation.—For the removal of doubts, it is hereby declared that the expression

“commercial training or coaching centre” occurring in this sub-clause and in clauses

(26), (27) and (90a) shall include any centre or institute, by whatever name called,

where training or coaching is imparted for consideration, whether or not such centre

or institute is registered as a trust or a society or similar other organization under

any law for the time being in force and carrying on its activity with or without profit

motive and the expression “commercial training or coaching” shall be construed

accordingly.

It can be seen from above definitions that educational services were carved out from the scope

of service / taxable service itself and not liable to Service Tax.

Taxability w.e.f. 01-07-2012

W.e.f. 01.07.2012, the concept of Service Tax has changed. What is taxed now is an activity

which gets covered under the scope of 'service' as defined in section 65B(44) of the Finance

Act, 1994 as amended.

Charge of Service Tax on and after 1.07.2012 is defined under section 66B of the Finance

Act, 1994. Section 66B states that Service Tax shall be charged at the rate of 12% on value

of all taxable services i.e., other than those specified in the negative list or exempted

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

4

services, which are provided or agreed to be provided in the taxable territory by one person

to another and collected in such manner as may be prescribed.

Section 66B specifies the charge of service tax which is essentially that service tax shall be

levied on all services provided or agreed to be provided in a taxable territory, other than

services specified in the negative list. Thus, as per charging section 66B, Service Tax shall

be applicable on all services except negative list services or services which are specifically

exempt from Service Tax.

(A) Services relating to Education Sector covered under Negative List

Section 66D of the Finance Act, 1994 contains Negative List of Services. The clause (l) of

section 66D relates to education related services. The said clause (l) of Section 66D of the

Act provides for the following negative list services in relation to educational sector:

Services by way of—

(i) pre-school education and education up to higher secondary school or equivalent;

(ii) education as a part of a curriculum for obtaining a qualification recognized by any law for

the time being in force;

(iii) education as a part of an approved vocational education course

According to the negative list, there are three categories of education covered under this list

and hence non-taxable:

Pre-school education – includes play schools, pre-nursery and nursery schools,

crèche, day care centre, pre-kindergarten or any such purpose school or centre by

whatever name called.

As per www.newworldencyclopedia.org, ‘Preschool education’ is education that

focuses on educating children from the ages of infancy until six years old. The

system of preschool education varies widely, with different approaches, theories, and

practices within different school jurisdictions. The term preschool education includes

such programs as nursery school, day care, or kindergarten, which are occasionally

used interchangeably, yet are distinct entities. While pedagogies differ, there is the

general agreement that pre-school is responsible for providing education before the

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

5

commencement of statutory education.” In academic parlance, ‘pre-school / early

childhood education’ is defined as a pedagogical approach covering the education of

children from the period from birth to six years of age.

Education upto higher secondary school or equivalent – includes school education

which is up to higher secondary (12th standard) or equivalent level (say,

intermediate). Any education beyond higher secondary is not covered here. The use

of expression ‘equivalent’ provides wider scope to school education implying that all

education up to school leaving are in negative list. Even if it is provided by

international school providing international certificate, it will be out of Service Tax net.

Education as a part of curriculum leading to recognized qualification – unlike school

education where any school education is covered, education qualifies for negative

list only if certain conditions are met, viz,

(i) education must be imparted as part curriculum

(ii) such education should be for obtaining a qualification (say a degree, diploma,

certificate etc.)

(iii) such qualification should be recognized by any law (Indian law only) for the

time being in force.

If any of the aforementioned conditions is not satisfied, the education shall not qualify

to be under the negative list. The use of words "law for the time being in force"

implies that such laws as are applicable in India at a given point of time. In such

cases, education is imparted under a prescribed syllabus or curriculum and the

education must be imparted as a part of such curriculum, i.e. it must be a part of

syllabus for such course or qualification. However, education leading to foreign

qualifications shall be liable to payment of Service Tax. In Indian, context, it may be

noted that recognition is granted by bodies such as University Grants Commission

(UGC), All India Council of Technical Education (AICTE) etc.

Approved vocational education course - Approved vocational education course has

been defined in section 65B(11) of the Finance Act, 1994. These are –

a course run by an industrial training institute or an industrial training centre

affiliated to the National Council for Vocational Training, offering courses in

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

6

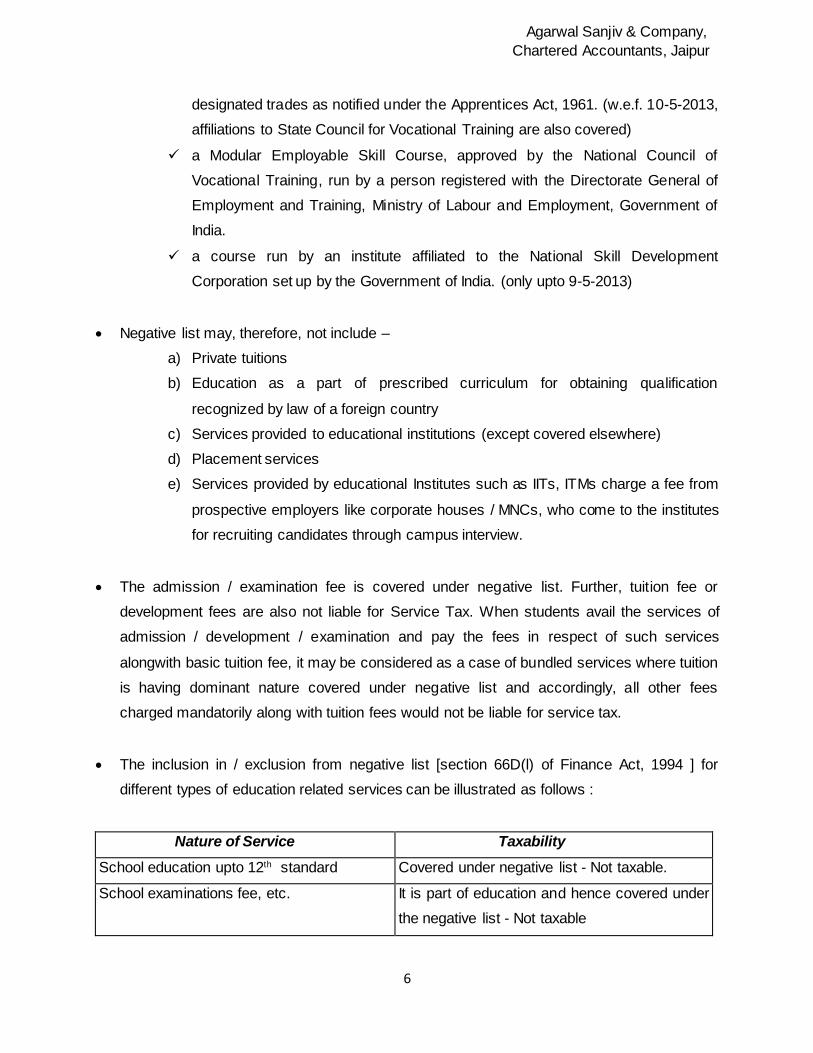

designated trades as notified under the Apprentices Act, 1961. (w.e.f. 10-5-2013,

affiliations to State Council for Vocational Training are also covered)

a Modular Employable Skill Course, approved by the National Council of

Vocational Training, run by a person registered with the Directorate General of

Employment and Training, Ministry of Labour and Employment, Government of

India.

a course run by an institute affiliated to the National Skill Development

Corporation set up by the Government of India. (only upto 9-5-2013)

Negative list may, therefore, not include –

a) Private tuitions

b) Education as a part of prescribed curriculum for obtaining qualification

recognized by law of a foreign country

c) Services provided to educational institutions (except covered elsewhere)

d) Placement services

e) Services provided by educational Institutes such as IITs, ITMs charge a fee from

prospective employers like corporate houses / MNCs, who come to the institutes

for recruiting candidates through campus interview.

The admission / examination fee is covered under negative list. Further, tuition fee or

development fees are also not liable for Service Tax. When students avail the services of

admission / development / examination and pay the fees in respect of such services

alongwith basic tuition fee, it may be considered as a case of bundled services where tuition

is having dominant nature covered under negative list and accordingly, all other fees

charged mandatorily along with tuition fees would not be liable for service tax.

The inclusion in / exclusion from negative list [section 66D(l) of Finance Act, 1994 ] for

different types of education related services can be illustrated as follows :

Nature of Service Taxability

School education upto 12th standard Covered under negative list - Not taxable.

School examinations fee, etc. It is part of education and hence covered under

the negative list - Not taxable

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

7

Conveyance facilities to students If part of education and cannot be separately

covered under negative list - Not taxable

Approved vocational educational course Covered under negative list - Not taxable

Boarding school (package offered inclusive

of food, rent, etc.)

Covered under negative list - Not taxable;

Essential character being education, non-

taxable as per rule of bundled services

College education (affiliated to an Indian

university)

Recognized by law, covered in negative list -

Not taxable

Test for admission in a college / institution If recognized by law, covered in negative list -

Not taxable

Campus recruitment fee Taxable

Courses recognized by foreign law Not covered under negative list - Taxable

Coaching centre's services Taxable

Placement services Taxable

Grants-in-aid As per Rule 6(2)(vii) of the Service Tax

(Determination of Value) Rules, 2006, subsidies

and grant disbursed by the Government, not

directly affecting the value of service, will be

excluded from the value of service - Not taxable

(B) Exemptions to Services relating to Education Sector

Only specified services provided by educational institutions are included in the negative list.

Services provided to educational institutions are not covered under negative list. However,

certain services provided to and by educational institutions are separately exempted vide

Notification No. 25/2012-ST, dated 20-6-2012.

(1) Exemption under Entry No. 9 of Notification No. 25/2012-ST dated 20.06.2012 (as

amended)

(i) During the period 1.7.2012 to 31.03.2013 :

The following services provided to or by an educational institution in respect of education

were exempted from service tax, by way of,-

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

8

(a) Auxiliary educational services; or

(b) Renting of immovable property

‘Auxiliary educational services’ were defined in the mega exemption notification dated

20.06.2012. In terms of the said definition, the following activities were covered under

auxiliary educational services:

any services relating to imparting any skill, knowledge or education, or

development of course content, or

any other knowledge – enhancement activity, whether for the students or the

faculty, or

any other services which educational institutions ordinarily carry out themselves

but may obtain as outsourced services from any other person, including

following services relating to:

— admission to such institution

— conduct of examination

— catering for the students under any mid-day meals scheme sponsored by

Government

— transportation of students, faculty or staff of such institution.

If any of the aforementioned auxiliary services do not pertain to education per

se, it may not be termed as auxiliary education service. To have a nexus with

education is a necessary pre-condition. It must relate to the specified activities

viz,

skill, knowledge or education (but not coaching)

development of course content (e.g. syllabus)

any knowledge enhancing activity (say a seminar, conference or quiz

event)

activities outsourced in ordinary course of education (admission,

examination etc.)

During this period exemption was available for the services provided to or by educational

institutions in respect of education which was itself exempted from service tax.

Therefore, service tax was chargeable on such auxiliary educational services which

were in respect of services education chargeable to Service Tax.

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

9

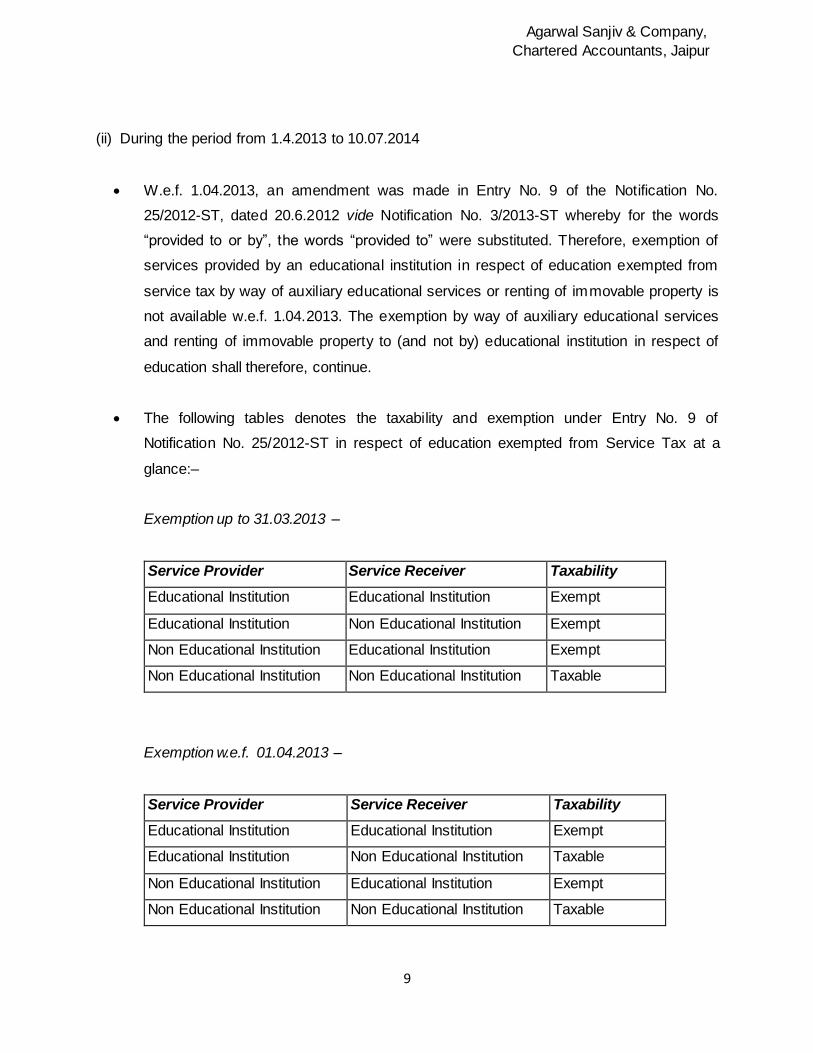

(ii) During the period from 1.4.2013 to 10.07.2014

W.e.f. 1.04.2013, an amendment was made in Entry No. 9 of the Notification No.

25/2012-ST, dated 20.6.2012 vide Notification No. 3/2013-ST whereby for the words

“provided to or by”, the words “provided to” were substituted. Therefore, exemption of

services provided by an educational institution in respect of education exempted from

service tax by way of auxiliary educational services or renting of immovable property is

not available w.e.f. 1.04.2013. The exemption by way of auxiliary educational services

and renting of immovable property to (and not by) educational institution in respect of

education shall therefore, continue.

The following tables denotes the taxability and exemption under Entry No. 9 of

Notification No. 25/2012-ST in respect of education exempted from Service Tax at a

glance:–

Exemption up to 31.03.2013 –

Service Provider Service Receiver Taxability

Educational Institution Educational Institution Exempt

Educational Institution Non Educational Institution Exempt

Non Educational Institution Educational Institution Exempt

Non Educational Institution Non Educational Institution Taxable

Exemption w.e.f. 01.04.2013 –

Service Provider Service Receiver Taxability

Educational Institution Educational Institution Exempt

Educational Institution Non Educational Institution Taxable

Non Educational Institution Educational Institution Exempt

Non Educational Institution Non Educational Institution Taxable

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

10

CBEC Clarifications on Exemption

CBEC in its Letter No. 334/3/2013-TRU dated 28/02/2013, has clarified that -

“Exemption by way of auxiliary educational services and renting of

immovable property by (and not to) specified educational institutes under

S.No. 9 will not be available w.e.f. 1.4.2013.”

Circular No. 172/7/2013 –ST dated 19.09.2013 has clarified that -

“By virtue of the entry in the negative list and by virtue of the portion of

the exemption notification, it will be clear that all services relating to

education are exempt from service tax. There are many services

provided to an educational institution. These have been described as

“auxiliary educational services” and they have been defined in the exemption

notification. Such services provided to an educational institution are exempt

from service tax. For example, if a school hires a bus from a transport

operator in order to ferry students to and from school, the transport services

provided by the transport operator to the school are exempt by virtue of the

exemption notification.

It is also clarified that in addition to the services mentioned in the definition

of “auxiliary educational services”, other examples would be hostels,

housekeeping, security services, canteen, etc.”

(iii) Applicable w.e.f. 11.07.2014

Entry No. 9 has been substituted vide Notification No. 06/2014–ST dated 11.07.2014

w.e.f. 11.07.2014 and now exemption entry read as follows –

“Services provided,-

(a) by an educational institution to its students, faculty and staff;

(b) to an educational institution, by way of,-

(i) transportation of students, faculty and staff;

(ii) catering, including any mid-day meals scheme sponsored by the Government;

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

11

(iii) security or cleaning or house-keeping services performed in such educational

institution;

(iv) services relating to admission to, or conduct of examination by, such

institution.”

The entire scheme of exemption in relation to educational has thus been modified.

Hence, w.e.f. 11.07.2014, exemption is available as follows –

As per Entry 9(a), all services provided by an educational institution (as defined) to

its students, faculty and staff would be exempt; and

As per Entry 9(b), exemption is granted to services provided ‘to’ an educational

institution, by way of,-

a) transportation of students, faculty and staff;

b) catering, including any mid-day meals scheme sponsored by the

Government;

c) security or cleaning or house-keeping services performed in such

educational institution;

d) services relating to admission to, or conduct of examination by, such

institution.

The effect of changes in exemption are -

concept of ‘auxiliary educational services’ under para 2(f) of the Notification

25/2012-ST dated 20.06.2012 stands deleted.

scope of exemption remains the same as earlier in the case of services provided

by eligible educational institutions.

in the case of services received by the eligible educational institutions, exemption

will be available only in respect of the services specified as above.

services provided by way of renting of immovable property to educational

institutions stands withdrawn w.e.f. 11.07.2014.

‘Educational institution’ has been defined in para 2(oa) of the notification. Accordingly,

‘educational institution’ means an institution providing services specified in clause (l) of

section 66D of the Finance Act, 1994.

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

12

In view of the aforesaid, following twin tests ought to be satisfied now for availing the

said exemption–

Institution who is engaged in providing education to students must be educational

institute as defined in para 2(oa) of the Notification No. 25/2012-ST, dated

20.06.2012. (i.e. pre-school, high secondary school)

Such educational institute must provide services which are specified in Entry No.

9 of this Notification. The concept of auxiliary education services has been

omitted. Now the entry itself is clear as to on which facility or service, educational

institutes will get exemption. This entry is self- explanatory.

Accordingly, the following services received by eligible educational institutions

shall be exempted from service tax -

(a) transportation of students, faculty and staff of the eligible educational

institution;

(b) catering service, including any mid-day meals scheme sponsored by the

Government;

(c) security or cleaning or house-keeping services in such educational

institutions;

(d) services relating to admission to such institutions or conduct of

examinations.

Now, all the services provided by an educational institution to its students, faculty and

staff shall be exempt from Service Tax. However, exemptions to services provided to

educational institutions have been limited only to the scope specified in Entry No. 9.

Such services would include services like transport facility to students, faculty and staff,

catering including mid-day meals scheme, security services, cleaning or housekeeping

services and services relating to admission or conduct of examination.

Ancillary services relating to admission process, examination work such as processing of

applications, preparation of exams, conduct of exams, evaluation, result etc. shall be

exempt from levy of Service Tax.

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

13

(2) Exemption under Entry No. 12 of Notification No. 25/2012-ST dated 20.06.2012 (as

amended)

Services in relation to construction, erection, maintenance etc. of building / structure

This exemption is available to –

Services provided to the Government, a local authority or a governmental authority by

way of construction, erection, commissioning, installation, completion, fitting out,

repair, maintenance, renovation, or alteration of -

(a) a civil structure or any other original works meant predominantly for use other

than for commerce, industry, or any other business or profession;

(b) a historical monument, archaeological site or remains of national importance,

archaeological excavation, or antiquity specified under the Ancient Monuments

and Archaeological Sites and Remains Act, 1958;

(c) a structure meant predominantly for use as (i) an educational, (ii) a clinical, or (iii)

an art or cultural establishment;

(d) canal, dam or other irrigation works;

(e) pipeline, conduit or plant for (i) water supply (ii) water treatment, or (iii) sewerage

treatment or disposal; or

(f) a residential complex predominantly meant for self-use or the use of their

employees or other persons specified in the Explanation 1 to clause 44 of section

65B of the said Act;

Under this exemption, two conditions are important, viz, —

(a) Services should be provided to –

(i) Government,

(ii) Local authority, or

(iii) Governmental Authority

(b) Services shall be in relation to those specified in the entry i.e., construction, erection,

commissioning etc.

These could be services provided to the Government or local authority or governmental

authority for –

a civil structure or any other original works meant predominantly for use other than

commerce, industry or any other business or profession;

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

14

a historical monument, archaeological site or remains of national importance,

archaeological excavation, or antiquity specified under Ancient Monuments and

Archaeological Sites and Remains Act, 1958;

a structure meant predominantly for use as (i) an educational, (ii) a clinical, or(iii) an

art or cultural establishment;

canal, dam or other irrigation works;

pipeline, conduit or plant for (i) drinking water supply (ii) water

treatment(iii)sewerage treatment or disposal; or

a residential complex predominantly meant for self-use or the use of their

employees or other persons specified in the Explanation 1 to clause 44 of section

65B of the Finance Act;

Thus, if services of construction of a structure (e.g. school building etc.) predominantly used

in education to Government, local authority and Governmental authority are exempted from

service tax.

(C) Provisions of Reverse Charge Mechanism

As per Notification No. 30/2012-ST dated 20.06.2012 (as amended) and conditions

stipulated therein, the liability to deposit Service Tax to the credit of Central Government

shall be on service receiver. Reverse charge mechanism can be full or partial as follows:

Full Reverse Charge Mechanism: The liability to pay 100% Service Tax is on the service

receiver. In respect of certain services as specified, 100% Service Tax is to be paid by

service receiver and there is no obligation on the part of the service provider to pay

Service Tax. (For example, legal services, GTA services etc.)

Partial or Joint Reverse Charge Mechanism: The liability of payment of Service Tax shall

be both, on the service provider and the service recipient.

In terms of serial number 7(b), 8 and 9 of the table specified in Notification No.

30/2012 - ST dated 20.6.12, the partial/joint reverse charge mechanism is

applicable to services provided or agreed to be provided by way of

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

15

a) renting of a motor vehicle designed to carry passengers on non-abated value to

any person who is not engaged in a similar business, or

b) supply of manpower for any purpose, or

c) service portion in execution of a works contract;

by any individual, Hindu Undivided Family or partnership firm, whether registered or

not, including association of persons, located in the taxable territory to a business

entity registered as a body corporate located in the taxable territory. Thus, the

nature of the service and the status of both the service provider and service receiver

are important to determine the applicability of partial reverse charge provisions.

‘Body corporate' has been defined in clause (11) of section 2 of the Companies Act,

2013 which applies in Service Tax. Accordingly, 'body corporate' or 'corporation'

includes a company incorporated outside India, but does not include –

i) a co-operative society registered under any law relating to co-operative

societies; and

ii) any other body corporate (not being a company as defined in this Act), which

the Central Government may, by notification, specify in this behalf.

As most of the education institutions are run under Trust and registered under

12AA/80G of the Income Tax Act, 1961. Since Trust is not a body corporate,

therefore, the provisions of partial reverse charge mechanism on works contract,

supply of manpower, and renting of a motor vehicle shall not be applicable in such

cases and whole of Service Tax shall be payable by service provider irrespective of

its status. However, the provisions of full RCM will be applicable in normal course.

Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

16

Relevant Provisions / Notifications etc.

Upto 30.06.2012

1. Section 65(26) of the Finance Act, 1994 – Meaning of Commercial Training or Coaching

2. Section 65(27) of the Finance Act, 1994 – Meaning of Commercial Training or Coaching

Centre

3. Section 65(105) (zzzc) of the Finance Act, 1994 – Taxable Services relating to

Commercial Training & Coaching

w.e.f. 01.07.2012

1. Section 65B(11) of Finance Act, 1994 - Definition of Approved Vocational Education

Course

2. Clause (l) of Section 66D of Finance Act, 1994 i.e. Negative List – Pre –school, higher

secondary, vocational education etc.

3. Notification 25/2012 – ST dated 20.06.2012 - Entry No. 9 & 12 – Services provided to or

by educational institutions and construction services respectively

4. Para 2 (f) of Notification 25/2012 – ST dated 20.06.2012 – Definition of Auxiliary

Education Services (deleted w.e.f 11.07.2014)

5. Para 2 (oa) of Notification 25/2012 – ST dated 20.06.2012 - Education Institution [para 2

(oa)]

6. Notification No. 30/2012-ST dated 20.06.2012 – Reverse charge provisions

7. CBEC Letter No. 334/3/2013-TRU dated 28/02/2013 – CBEC clarification on exemption

8. Circular No. 172/7/2013 –ST dated 19.09.2013- CBEC clarification on exempt services –

Auxiliary Education Services

For clarification, please contact:

AGARWAL SANJIV & COMPANY CHARTERED ACCOUNTANTS

503, GURUKRIPA TOWER, MAHAVEER MARG,

C-SCHEME, JAIPUR-302001

Phone : 0141-2368071, Fax : 0141-2369250 E- mail :[email protected]