SAN MATEO COUNTYcontroller.smcgov.org/sites/controller.smcgov.org/files...San Mateo County Joint...

32

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY (A Component Unit of the County of San Mateo, California) Independent Auditor’s Reports, Management’s Discussion and Analysis, Basic Financial Statements, and Supplementary Information For the Fiscal Year Ended June 30, 2014

Transcript of SAN MATEO COUNTYcontroller.smcgov.org/sites/controller.smcgov.org/files...San Mateo County Joint...

SAN MATEO COUNTY

JOINT POWERS FINANCING AUTHORITY (A Component Unit of the County of San Mateo,

California)

Independent Auditor’s Reports, Management’s Discussion and Analysis,

Basic Financial Statements, and Supplementary Information

For the Fiscal Year Ended June 30, 2014

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

For the Fiscal Year Ended June 30, 2014

Table of Contents

Page Independent Auditor’s Report ................................................................................................................................ 1 Management’s Discussion and Analysis (Required Supplementary Information)............................................. 3 Basic Financial Statements:

Statement of Net Position .................................................................................................................................... 7 Statement of Revenues, Expenses, and Changes in Net Position ........................................................................ 8 Statement of Cash Flows...................................................................................................................................... 9 Notes to the Basic Financial Statements:

(1) Reporting Entity ....................................................................................................................................... 11 (2) Summary of Significant Accounting Policies .......................................................................................... 11 (3) Cash Equivalents and Investments ........................................................................................................... 14 (4) Net Investment in Lease and Installment Agreements ............................................................................. 15 (5) Long-Term Liabilities .............................................................................................................................. 16 (6) Commitments ........................................................................................................................................... 18 (7) Special Item .............................................................................................................................................. 19

Supplementary Information:

Supplementary Schedule of Net Position ........................................................................................................... 20 Supplementary Schedule of Revenues, Expenses, and Changes in Net Position .............................................. 22 Supplementary Schedule of Cash Flows ............................................................................................................ 24

Other Report:

Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ....................................................................................... 27

1

Independent Auditor’s Report

Board of Directors San Mateo County Joint Powers Financing Authority Redwood City, California

Report on the Financial Statements

We have audited the accompanying financial statements of the San Mateo County Joint Powers Financing Authority (Authority), a component unit of the County of San Mateo, California (County), as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the Authority’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Authority, as of June 30, 2014, and the changes in financial position and cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

2

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 3 through 5 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the Authority’s basic financial statements. The supplementary information, as listed in the table of contents, is presented for purposes of additional analysis and is not a required part of the basic financial statements.

The supplementary information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the supplementary information is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated October 30, 2014, on our consideration of the Authority’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Authority’s internal control over financial reporting and compliance.

Walnut Creek, California October 30, 2014

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Management’s Discussion and Analysis Required Supplementary Information (Unaudited)

For the Fiscal Year Ended June 30, 2014

3

This Management’s Discussion and Analysis provides a narrative overview and analysis of the financial activities of the San Mateo County Joint Powers Financing Authority (the Authority) for the fiscal year ended June 30, 2014. We encourage readers to read this section in conjunction with the Authority’s financial statements beginning on page 7.

Financial Highlights In August of 2013, the Authority issued a total of $40 million in Lease Revenue Bonds (the “2013 Bonds”). The

bond proceeds, together with other available moneys, were used to refund the outstanding 1997, 1999, and 2001 Bonds (the Prior Bonds) totaling $39 million, to finance the Skylonda Fire Station Project of $4 million, and to pay bond issuance costs. The economic gain from the refunding was $3.1 million.

In May of 2014, the Authority issued a total of $175 million in Lease Revenue Bonds (the “2014 Bonds”). The bond proceeds, together with other available moneys, were used to finance the construction of a new County jail, to reimburse the County for the jail project expenses, and to pay bond issuance costs.

The assets and deferred outflows of resources of the Authority exceeded its liabilities at the close of the fiscal year

2013-14 by $139 million (net position). Of this amount, $103 million for capital projects, $32 million was restricted for debt service, and $4 million was unrestricted.

The Authority’s total net position increased $107 million, due primarily to a net increase of $176 million in lease

contract revenues from direct financing leases and refunding of the Prior Bonds, and a $65 million project cost reimbursement to the County for the jail construction.

The Authority’s total outstanding long-term debt, including lease revenues bonds and certificates of participation,

has increased $189 million to $535 million from $346 million. The increase was caused by the issuance of the 2013 and 2014 Bonds ($242 million including bond premiums), partially offset by the refunding of the Prior Bonds ($39 million) and the scheduled retirement of outstanding debts ($14 million).

Financial Statements The Authority is a special-purpose government engaged solely in financing capital projects of the County of San Mateo (the County). Pursuant to Governmental Accounting Standards Board Statement No. 34, governments like the Authority that has only business-type activities may present only enterprise fund financial statements: (1) statement of net position; (2) statement of revenues, expenses, and changes in net position; and (3) statement of cash flows, using the economic resources measurement focus and the accrual basis of accounting.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Management’s Discussion and Analysis Required Supplementary Information (Unaudited)

For the Fiscal Year Ended June 30, 2014

4

The Authority’s net position increased to $139 million from the prior fiscal year of $32 million. The Authority’s total net position as of June 30, 2014 and 2013 are as follows:

2014 2013 $ Change % Change

Assets

Current assets 204,778,871$ 55,092,169$ 149,686,702$ 271.70%

Non-current assets 486,200,278 323,967,830 162,232,448 50.08%

Total assets 690,979,149 379,059,999 311,919,150 82.29%

Deferred Outflows of Resources

Unamortized loss on refunding of debt 7,335,619 7,606,509 (270,890) -3.56%

Liabilities

Current liabilities 39,404,893 23,325,950 16,078,943 68.93%

Non-current liabilities 520,165,837 331,533,942 188,631,895 56.90%

Total liabilities 559,570,730 354,859,892 204,710,838 57.69%

Net position

Restricted for capital projects 102,888,275 1,380,038 101,508,237 7355.47%

Restricted for debt service 31,950,802 25,946,952 6,003,850 23.14%

Unrestricted 3,904,961 4,479,626 (574,665) -12.83%

Total net position 138,744,038$ 31,806,616$ 106,937,422$ 336.21%

The Authority’s total assets increased $312 million, primarily from a $150 million increase in cash and a $162 million increase in lease receivable.

In August 2013, the Authority issued the 2013 Bonds to refund the Prior Bonds and to finance the construction of a

new fire station (the Skylonda Fire Station) for the benefit of the County. The proceeds from the 2013 Bonds amounted to $43 million (including $40 million in par value and $3 million in bond premium), and the Authority spent $39 million to retire the Prior Bonds. In May 2014, the Authority issued the 2014 Bonds to finance the jail construction and to reimburse the County for the moneys previously spent on the jail project since 2010. The proceeds from the 2014 Bonds aggregated to $199 million ($175 million in par value and $24 million in bond premium). The Authority immediately reimbursed the County $16 million for the acquisition of real properties in Redwood City to build the jail and $41 million in project costs.

In conjunction with the bond issuance, the Authority (the lessor) entered into two “direct” financing leases with the

County (the lessee). In a direct financing lease, the lessor provides property while the lessee provides regular lease payments in exchange for the use of that property. As a result, the Authority added a total of $215 million in lease receivable (which equals to the face value of the new bonds). The increase in lease receivable was partially offset by $39 million from the early retirement of the Prior Bonds and $14 million from scheduled lease payments from the County.

The Authority’s overall liabilities are predominantly made up of lease revenue bonds and certificates of participation. As of June 30, 2014, the Authority’s liabilities increased $205 million resulted mainly from the long-term financing totaling $242 million through bond issuance discussed earlier and early retirement of the Prior Bonds totaling $39 million.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Management’s Discussion and Analysis Required Supplementary Information (Unaudited)

For the Fiscal Year Ended June 30, 2014

5

Changes in the Authority’s net positions between fiscal years 2014 and 2013 are as follows:

2014 2013 $ Change % ChangeRevenues

Lease interest revenue 16,625,241$ 16,966,065$ (340,824)$ -2.01%Lease contract revenue 175,975,000 - 175,975,000 100.00%Interest and investment income 597,772 545,152 52,620 9.65%Other revenues 289,190 97,851 191,339 195.54%

Total revenues 193,487,203 17,609,068 175,878,135 998.79%

ExpensesGeneral and administrative 83,796 159,810 (76,014) -47.57%Reimbursement to the County 37,541,855 900,661 36,641,194 4068.26%Interest expense 16,331,521 16,760,867 (429,346) -2.56%Contribution to the County 1,683,854 288,840 1,395,014 482.97%Bond issuance costs 2,127,190 - 2,127,190 100.00%

Total expenses 57,768,216 18,110,178 39,658,038 218.98%

Income (loss) before speical item 135,718,987 (501,110) 136,220,097 27183.67%

Special item (28,781,565) - (28,781,565) -100%

Change in net position 106,937,422 (501,110) 107,438,532 21440.11%

Net position, beginning of year 31,806,616 32,307,726 (501,110) -1.55%Net position, end of year 138,744,038$ 31,806,616$ 106,937,422$ 336.21%

The Authority’s total revenues increased $176 million. The direct financing leases brought in a total of $215 million in lease contract revenue, which was reduced by a $39 million in lease receivable due to early retirement of the Prior Bonds. The Authority’s total expenses increased $40 million. Such increase included $36 million in reimbursement to the County for the jail construction expenses incurred in fiscal year 2013-14, $2 million in bond issuance costs for the 2013 Bonds and the 2014 Bonds, and $1 million contribution to the County from the residual moneys from the 2001 Bonds to supplement the County’s Radio Interoperable Communications System project. The special item of $29 million represented the overall reimbursement to the County for jail project costs incurred prior to fiscal year 2013-14. Request for Information Questions concerning any information provided in this report or requests for additional financial information can be obtained by writing to the Office of the County Manager, 400 County Center, 1st Floor, Redwood City, CA 94063.

6

This page intentionally left blank

ASSETS

Current assets:Cash equivalents 155,275,769$ Cash equivalents - restricted for debt service 23,675,199 Investments - restricted for debt service 8,344,687 Prepayment 4,083 Net investment in leases - current 10,625,000 Interest receivable:

Net investment in leases 6,757,458 Investments 96,675

Total current assets 204,778,871

Noncurrent assets:Net investment in leases - noncurrent 486,200,278

Total assets 690,979,149

DEFERRED OUTFLOWS OF RESOURCESUnamortized loss on refunding of debt 7,335,619

LIABILITIES

Current liabilities:Accounts payable 7,959,567 Interest payable 7,738,583 Due to the County 1,775,813 Advance from the County 7,033,213 Lease revenue bonds, net of unamortized

discount/premium - current 14,470,546 Certificates of participation, net of

unamortized premium - current 427,171 Total current liabilities 39,404,893

Noncurrent liabilities:Accreted interest on capital appreciation

bonds - noncurrent 4,700,462 Lease revenue bonds, net of unamortized

discount/premium - noncurrent 493,978,090 Certificates of participation, net of

unamortized premium - noncurrent 21,487,285 Total noncurrent liabilities 520,165,837

Total liabilities 559,570,730

NET POSITIONRestricted for capital projects 102,888,275 Restricted for debt service 32,095,223 Unrestricted 3,760,540

Total net position 138,744,038$

The notes to the basic financial statements are an integral part of this statement.

SAN MATEO COUNTY

Statement of Net PositionJune 30, 2014

JOINT POWERS FINANCING AUTHORITY

7

Operating revenuesLease interest revenue from the County 16,625,241$ Lease contract revenue 175,975,000 Other 11,000

Total operating revenues 192,611,241

Operating expensesGeneral and administrative 83,796 Reimbursement of County project costs 37,541,855

Total operating expenses 37,625,651

Operating income 154,985,590

Nonoperating revenues (expenses)Interest and investment income 597,772 Interest expense (16,331,521) Recoveries from investment loss 278,190

Contribution to the County (1,683,854) Bond issuance costs (2,127,190)

Net nonoperating expenses (19,266,603)

Income before special item 135,718,987

Special item - project costs incurred prior to bond issuance (28,781,565)

Change in net position 106,937,422

Net position, beginning of year 31,806,616

Net position, end of year 138,744,038$

The notes to the basic financial statements are an integral part of this statement.

SAN MATEO COUNTY

Statement of Revenues, Expenses, and Changes in Net PositionFor the Fiscal Year Ended June 30, 2014

JOINT POWERS FINANCING AUTHORITY

8

Cash flows from operating activities:Cash received from lessee, principal portion 14,555,000$

Cash received from lessee, interest portion 16,035,937

Cash received from other sources 11,000

Cash paid for general and administrative expenses (107,612)

Cash paid for reimbursement of County project costs (27,953,068)

Net cash provided by operating activities 2,541,257

Cash flows from noncapital financing activities:Due to the County 117,207

Advance from the County 7,033,213

Net cash provided by noncapital financing activities 7,150,420

Cash flows from capital and related financing activities:Cash received from bond proceeds 241,352,488

Cash paid for bond issuance costs (1,042,216)

Cash paid from reserves to the County (2,435,439)

Cash paid for early retirement of debt (39,155,000)

Cash paid for principal on bonds and COPs (14,340,000) Cash paid for interest on bonds and COPs (16,260,144)

Cash paid for project costs incurred prior to bond issuance (28,781,565)

Net cash provided by capital and related financing activities 139,338,124

Cash flows from investing activities:Cash paid for purchase of investments (1,961,793)

Cash received from sale of investments 2,598,973

Cash received from recoveries 278,190

Cash received from earnings on investments and cash equivalents 554,692

Net cash provided by investing activities 1,470,062

Net increase in cash and cash equivalents 150,499,863

Cash and cash equivalents, beginning of year 28,451,105 Cash and cash equivalents, end of year 178,950,968$

Financial statement presentation:Cash equivalents 155,275,769$

Cash equivalents - restricted for debt service 23,675,199 Cash and cash equivalents, end of year 178,950,968$

Reconciliation of operating income to net cash provided by operating activities:Operating income 154,985,590$

Adjustments to reconcile operating income to net cash provided by operating activities:Changes in operating assets and liabilities:

Increase in lease receivable - principal (161,420,000)

Increase in lease receivable - interest (589,304)

Increase in accounts payable 9,564,971

Net cash provided by operating activities 2,541,257$

Supplemental disclosure of noncash activities: Noncash capital and related financing activities:

Amortized premium/discount on lease revenue bonds and COPs 679,395$

Amortized loss on refunding of debt (358,715)

Accreted interest on capital appreciation bonds (387,448)

Transfer of deferred loss on refunding 87,826

Bond issuance costs paid through escrow agent (1,084,974)

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Statement of Cash Flows For the Fiscal Year Ended June 30, 2014

The notes to the basic financial statements are an integral part of this statement.

9

10

This page intentionally left blank

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2014

11

NOTE 1 – REPORTING ENTITY

The San Mateo County Joint Powers Financing Authority (the Authority) was established pursuant to the provisions of the State of California Government Code’s Articles 1 and 4 of Chapter 5 of Division 7 of Title 1 and a Joint Exercise of Powers Agreement, dated May 15, 1993, as amended by the County and the now dissolved Community Development Commission. The Authority assists the County of San Mateo (the County) in the financing of public capital projects. The Authority acts as the issuer for debt financings as well as the lessor of properties leased to the County. The debts issued are limited obligations of the Authority, payable primarily from rent payments made by the County under a “Facility Lease” agreement.

The Authority functions as an independent entity and has no employees. The County Board of Supervisors appointed all five members in its governing board to set policies. The County staff and consultants are in charge of its operation. Although legally separate from the County, the Authority is an integral part of the County for its sole purpose is to provide lease financing to the County. As such, the Authority is a component unit of the County, and its basic financial statements are blended within the County’s basic financial statements. Services provided by the County staff are not included in the accompanying basic financial statements since the amount is considered insignificant.

The basic financial statements present only the Authority’s financial activities in conformity with accounting principles generally accepted in the United States of America (GAAP) and are not intended to present fairly the financial position, the change in financial position, and the cash flows of the County.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. Basis of Presentation and Accounting

The Authority is reported as a single enterprise fund. The Authority’s basic financial statements are prepared using the economic resources measurement focus and the accrual basis of accounting in accordance with GAAP. All of its assets, deferred outflows/inflows of resources, and liabilities are included in the statement of net position. The net position (i.e., total assets and deferred outflows of resources net of total liabilities and deferred inflows of resources) is classified into restricted and unrestricted. Restricted portion includes amounts restricted for capital projects and debt service. The preparation of basic financial statements in conformity with GAAP requires management to make certain estimates and assumptions affecting certain reported amounts and disclosures. Accordingly, actual results may differ from those estimates.

Proprietary (enterprise) funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services in connection with the fund’s principal ongoing operations. The principal operating revenue of the Authority is lease interest income from the County. The Authority also recognizes lease contract revenue at the time the lessee covenants to commence base rental payments. Operating expenses of the Authority include project costs and administrative expenses for services solicited from outside entities. Revenues and expenses not meeting these definitions are reported as nonoperating revenues and expenses. B. Statement of Net Position

1. Cash Equivalents and Investments

The Authority considers all liquid investments with maturity of three months or less when purchased to be cash equivalents. This includes deposits and money market mutual funds held in trust as well as investments in the County investment pool. The Authority records investment transactions on the trade date. Investments in nonparticipating interest-earning investment contracts are reported at cost; other investments are reported at fair value. Fair value is defined as the amount, which is generally measured by quoted market prices, the Authority could reasonably expect to receive for an investment in a current sale between a willing buyer and a willing seller. As of June 30, 2014, a portion of the Authority’s investments was held in trust and part was held in the County’s investment pool.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

12

In accordance with the Authority’s bond trust agreements, the types of investment in which the Authority can engage include the following:

a. Government securities.

b. Any obligations which are then legal investments for moneys of the County under the laws of the State of California and comply with the County’s investment policy; provided that such investments shall be rated in the highest short-term or one of three highest long-term rating categories by Moody’s Investors Service and Standard & Poor’s Corporation.

c. Money markets or mutual funds which are rated by Standard & Poor’s Corporation “AAAm-G” or “AAAm” or higher and; if rated by Moody’s Investors Service, are rated “Aaa” or higher.

d. The County of San Mateo Investment Pool.

e. The Local Agency Investment Fund of the State of California.

f. Unsecured certificate of deposit, time deposits, and bankers’ acceptances (having maturities of not more than 30 days) of any bank the short-term of which are rated “A-1” or better by Standard & Poor’s Corporation.

g. Deposits the aggregate amount of which are fully insured by the Federal Deposit Insurance Corporation, in banks which have capital and surplus of at least $5 million.

h. Commercial paper (having original maturities of not more than 270 days) rated “A-1+” by Standard & Poor’s Corporation and “Prime-1” by Moody’s Investors Service.

i. Repurchase agreements.

j. Investment agreements with a domestic or foreign bank or corporation (other than a life or property casualty insurance company) the long-term debt of which, or, in the case of a guaranteed corporation the long-term debt, or, in the case of a monoline financial guaranty insurance company, claims paying ability of the guarantor is rated at least “AA” by Standard & Poor’s Corporation and “Aa” by Moody’s Investors Service.

k. The Investment Agreement.

l. Any other obligations with 30 days prior notice to Standard & Poor’s Corporation and the prior written approval of the Bond Insurer.

m. Unsecured demand deposits of any bank the short-term obligations of which are rated “A-1” or better by Standard & Poor’s Corporation.

2. Net Investment in Leases

Debt service on the outstanding lease revenue bonds and certificates of participation (COPs) are funded with lease payments from the County for the use of equipment and facilities acquired or constructed with proceeds of debt issued by the Authority. Under the lease agreements, the County has covenanted to make rental payments in amounts corresponding to the Authority’s debt service requirements and related costs. Net investment in leases reflects the present value of remaining future lease payments due from the County. Unexpended funds upon completion of all projects will be used to retire outstanding debt and reduce lease payments from the County.

3. Deferred Outflows/Inflows of Resources

In addition to assets, the statement of net position will sometimes report a separate section for deferred outflows of resources. This separate financial statement element represents a consumption of net position that applies to a future period(s) and so will not be recognized as an outflow of resources (expense) until then. As of June 30, 2014, the Authority has deferred outflows of resources related to the unamortized loss on refunding of debt.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

13

In addition to liabilities, the statement of financial position will sometimes report a separate section for deferred inflows of resources. This separate financial statement element represents an acquisition of net position that applies to a future period(s) and so will not be recognized as an inflow of resources (revenue) until that time. The Authority has no amounts reported as deferred inflows of resources as of June 30, 2014. 4. Advance from the County

In May of 2014, the Authority issued the 2014 Lease Revenue Bonds of $175 million to finance the County jail construction project. To meet the required reserve requirement, the County advanced $7.0 million to the Authority to purchase a surety bond.

5. Net Position

Net position, cumulative net earnings from operating and nonoperating activities, is classified into the following categories:

Restricted for capital projects represents funds restricted for the acquisition or construction of equipment and

facilities. Upon the completion of capital projects, residual net position becomes restricted for debt services. Restricted for debt service represents funds held by the trustee for repayment of debt principal and interest.

Unrestricted represent funds with no external restriction as to use or purpose. Restricted resources are

generally depleted first.

C. Statement of Revenues, Expenses, and Changes in Net Position

1. Bond Issuance Costs, Discounts, and Premiums

Bond issuance costs (other than insurance) are expensed once incurred. Bond discounts and bond premiums are deferred and amortized over the life of the bonds. Lease revenue bonds payable and COPs are reported net of the applicable bond discount and premium. 2. Unamortized Loss on Refunding of Debt

The loss on refunding is determined by the difference between the book value of the refunded (old) debt and the amount required to retire the debt. The loss is amortized over the remaining term of the old debt or the term of the new debt issued to finance the refunding, whichever is lesser. The unamortized loss on refunding is reported as deferred outflows of resources in the statement of net position. 3. Contribution to the County

The Authority may utilize interest earnings on reserves to supplement the County’s lease payments and refunding transactions. For the fiscal year 2013-14, the Authority applied $0.3 million of its interest earnings on reserves toward the County’s lease payments. In September 2001, the Authority issued Lease Revenues Bonds (2001 Bonds) to finance the County Crime Lab, Mutual Aid, and the Radio System projects. In January 2003, the three projects were completed. In August 2013, the Authority retired the entire 2001 Bonds through refunding. Residual funds in the 2001 Bonds account can be used for any County approved capital facility projects or reimbursement for costs incurred by the three projects. During fiscal year 2013-14, the Authority contributed a total of $1.4 million from the residual funds to the County Radio Interoperable Communications System project.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

14

NOTE 3 – CASH EQUIVALENTS AND INVESTMENTS

The Authority’s cash equivalents and investments as of June 30, 2014, include the following:

Cash equivalents 155,275,769$ Cash equivalents - restricted for debt service 23,675,199 Investments - restricted for debt service 8,344,687

Total cash equivalents and investments 187,295,655$ Cash Equivalents

The Authority has authorized its trustee to invest cash collections in the money market mutual funds and money market deposit accounts. Such funds can be converted to cash whenever necessary to meet the Authority’s operating needs. As of June 30, 2014, the Authority’s investment in the money market mutual funds and money market deposit accounts aggregated to $15 million and $37 million. The Authority also invests in the County’s investment pool. Its equity in the pool is cash equivalents. The Authority’s investment in the pool amounted to $127 million as of June 30, 2014.

Investments

The Authority’s investments as of June 30, 2014, include the following:

Fair Weighted AverageValue Maturity (Years)

Repurchase agreementHong Kong and Shanghai Banking Corporation 938,265$ 1.39

Discount noteFederal Home Loan Bank 1,935,972 *

Investment contractFinancial Guaranty Insurance Company Capital Market Services Group 5,470,450 4.59

Total investments 8,344,687$ 3.17

* Weighted average maturity is less than 0.01 year. Interest Rate Risk. Interest rate risk is the risk that changes in interest rates will adversely affect the fair value of an investment. The Authority has not adopted a formal policy that limits investment maturity as a means of managing its exposure to declines in fair values arising from increasing interest rates. As of June 30, 2014, the Authority’s investment portfolio had a weighted average maturity of 3.17 years. Credit Risk. Credit risk is the risk that an issuer or other counterparty to an investment will not fulfill its obligation. The Authority’s bond trust agreements include provisions which restrict the Authority’s investment in (a) money market mutual funds rated “AAm-G” or “AAm” by Standard & Poor’s Corporation, or better; (b) repurchase agreements with any domestic bank the long-term debt of which is rated at least “A” or better by Standard & Poor’s Corporation and Moody’s Investors Service; (c) specific obligations of government sponsored agencies which are not backed by the full faith and credit of the United Stated of America, including Federal Home Loan Bank, and (d) investment agreements. As of June 30, 2014, the money market mutual fund was rated “AAAm” by Standard & Poor’s and “Aaa-mf” by Moody’s Investors Service. The repurchase agreement with the Hong Kong and Shanghai Banking Corporation was rated “AA-” by Standard & Poor’s and “A1” by Moody’s Investors Service. The remaining investments were unrated including the discount note with the Federal Home Loan Bank and the investment contract with Financial Guaranty Insurance Company Capital Market Services Group.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

15

Concentration of Credit Risk. Concentration of credit risk is the risk of loss attributed to the magnitude of the Authority’s investment in a single issuer of securities. The Authority places no limit on the amount invested in any single issuer. The Authority has $1 million, or 11%, of its overall investments in repurchase agreement with the Hong Kong and Shanghai Banking Corporation; $2 million, or 23%, in a discount note with the Federal Home Loan Bank; and $5.5 million, or 66%, in an investment contract with Financial Guaranty Insurance Company Capital Market Services Group.

NOTE 4 – NET INVESTMENT IN LEASE AND INSTALLMENT AGREEMENTS

Under California law, the County cannot make lease payments until the County has constructive use or occupancy of the property being financed. Once construction is completed, the leases act like direct financing leases with lease payments equal to debt service payments. A direct-financing lease is basically the coupling of a sale and financing transaction. In a direct financing lease arrangement, the lessor (the Authority) purchases the property only for the purchase of leasing it. The lessor thus removes the leased asset from its books and replaces it with a receivable from the lessee (the County). The lease revenue bonds are payable by a pledge of revenues from the base rental payments payable by the County and all interest or other interest income from investment, pursuant to individual lease agreements between the Authority and the County. The certificates of participation are payable by a pledge of revenues from the installment payments payable by the County Flood Control District, pursuant to Installment Payment Agreements between the Authority and the County.

In the fiscal year 2013-14, the Authority received $30.6 million of lease payments from the County. The Authority’s net investment in lease and installment agreements at June 30, 2014, is as follows (in thousands):

Fiscal Year Ended June 30, Principal Interest Principal Interest2015 10,200$ 22,196$ 425$ 1,086$ 2016 14,510 21,805 445 1,064 2017 33,000 21,082 470 1,041 2018 33,488 19,649 490 1,016 2019 33,072 18,088 515 991 2020-2024 133,029 68,850 3,010 4,526 2025-2029 109,511 39,310 3,845 3,663 2030-2034 73,030 15,806 4,925 2,555 2035-2039 30,425 2,267 6,285 1,176 2040 - - 1,450 36 Total requirements 470,265 229,053$ 21,860$ 17,154$

Interest accretion 8,941 Less: unaccreted principal (4,241)

Total 474,965$

Lease Revenue Bonds Certificates of Participation

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

16

NOTE 5 – LONG-TERM LIABILITIES

The Authority’s long-term liabilities as of June 30, 2014, are as follows (in thousands): Original Outstanding

Interest Annual Principal Issue at June 30,Type of indebtedness (purpose) Maturities Rates Installments Amount 2014

Lease Revenue Bonds:1993 Issue

Term Current Interest Bonds 7/1/14 - 7/1/16 6.50% $3,505- $3,975 36,170$ 11,210$ Term Current Interest Bonds 7/1/17 - 7/1/21 5% - 6% $4,230 - $5,205 23,520 23,520

1993 Issue 59,690 34,730

1993 Issue - Satellite Clinic

Serial Capital Appreciation Bonds 9/1/17 - 9/1/26 5.9% - 6% $188 - $233 2,085 2,085 Accreted interest on capital appreciation bonds 8,941 4,700

1993 Issue - Satellite Clinic 11,026 6,785

2008 Issue

Series A Current Interest Bonds 7/15/14 - 7/15/25 4% - 5% $3,130 - $5,205 62,480 48,600

Term Interest Bonds 7/15/26 - 7/15/28 5.25% $5,465 - $6,070 17,295 17,295

Term Interest Bonds 7/15/29 - 7/15/33 5% $6,390 - $7,805 35,405 35,405

Term Interest Bonds 7/15/34 - 7/15/36 5% $8,205 - $9,070 25,900 25,900

2008 Issue 141,080 127,200

2009 Issue

Serial Current Interest Bonds 7/15/14 - 7/15/17 4% - 5% $6,080 - $6,145 46,130 25,250 Serial Current Interest Bonds 7/15/18 - 7/15/26 5% - 5.25% $6,475 - $8,990 69,375 69,375

2009 Issue 115,505 94,625

2013 IssuePurpose: To provide funds, together with other available moneys, (i) to redeem outstanding 1997, 1999, and 2001 Bonds, (ii) finance certain capital improvements, and (iii) to pay costs of issuance of the2013 Bonds.

Serial Current Interest Bonds 7/15/14 - 7/15/32 2% - 5.25% $550 - $10,320 40,065 40,065

2014 IssuePurpose: To provide funds, together with other available moneys, to (i) finance the acquisition, constructionand equipping of the Maple Street Correctional Center, (ii) refund all of the outstanding notes previouslyissued by the County in FY 2013-14, the proceeds of which were used to reimburse the County for the purchaseprice of the jail project site, (iii) pay capitalized interest on the 2014 Bonds through May 30, 2016, (iv) providethe Reserve Account Requirement, and (v) pay issuance costs of the 2014 Bonds.

Serial Current Interest Bonds 6/15/17 - 6/15/31 3% - 5% $1,170 - 9,185 157,895 157,895 Term Interest Bonds 6/15/32 - 6/15/35 4% $2,500 - $5,010 15,145 15,145 Term Interest Bonds 6/15/36 -6/15/37 4% $495 - $1,530 2,025 2,025

175,065 175,065

Total lease revenue bonds and accreted interest on capital appreciation bonds 542,431$ 478,470$

(Continued)

Purpose: To defease 1991 Certificates of Participation and finance the costs of a parking garage and jail.

Purpose: To finance a portion of the costs of constructing and equipping the North County Satellite Clinic and an adjacent parking structure.

Purpose: To provide funds, together with other available moneys, to redeem the 2003 Bonds.

Purpose: To provide funds, together with other available moneys, to refund a portion of the outstanding1997 Bonds and the outstanding 1999 Bonds (collectively, the "Prior Bonds"), to pay costs of issuance of the 2009 Bonds, and to pay other costs relating to the refunding of the Prior Bonds.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

17

Interest Annual Principal Issue at June 30,Type of indebtedness (purpose) Maturities Rates Installments Amount 2014

Certificates of Participation:1997 Issue

Term Certificates 8/1/14 - 8/1/17 5.25% $360 - $440 2,000$ 1,640$ Term Certificates 8/1/18 - 8/1/32 5.125% $465 - $935 10,145 10,145

1997 certificates of participation 12,145 11,785

2004 Issue

Serial Certificates 8/1/14 - 8/1/25 3.25% - 4.5% $45 - $70 975 670 Term Certificates 8/1/26 - 8/1/29 4.75% $70 - $85 310 310 Term Certificates 8/1/30 - 8/1/34 4.75% $85 - $1,140 2,500 2,500 Term Certificates 8/1/35 - 8/1/39 5% $1,195 - $1,450 6,595 6,595

2004 certificates of participation 10,380 10,075

Total certificates of participation 22,525$ 21,860$

Purpose: To finance the acquisition, design, construction, improvement, and installation of certain improvements to the flood control system.

Purpose: To finance the design, construction and installation of storm water, and flood control improvements located in the Colma Creek Flood Control Zone.

The table below summarizes changes in the Authority’s long-term liabilities (in thousands).

Amounts Balance Accretion/ Balance Due Within

July 1, 2013 Additions Retirements June 30, 2014 One Year

Lease revenue bonds 311,730$ 215,130$ (53,090)$ 473,770$ 13,705$ Accreted interest on capital

appreciation bonds 4,313 387 - 4,700 - Add: unamortized premium 8,136 27,308 (765) 34,679 766 Less: unamortized discount (88) - 88 - -

Lease revenue bonds, net 324,091 242,825 (53,767) 513,149 14,471

Certificates of participation 22,265 - (405) 21,860 425 Add: unamortized premium 57 - (3) 54 2

Certificates of participation, net 22,322 - (408) 21,914 427

Total long-term liabilities, net 346,413$ 242,825$ (54,175)$ 535,063$ 14,898$ Principal and interest payments on lease revenue bonds and certificates of participation come from lease payments made by the County General Fund and the Flood Control Zone Districts. The Authority’s annual debt service requirements to maturity as of June 30, 2014, are as follows (in thousands):

InterestFiscal Year Ended June 30, Principal Accretion Interest Principal Interest2015 13,705$ -$ 22,196$ 425$ 1,086$ 2016 14,510 - 21,805 445 1,064 2017 33,000 - 21,082 470 1,041 2018 33,488 692 19,649 490 1,016 2019 33,072 728 18,088 515 991 2020-2024 133,029 4,331 68,850 3,010 4,526 2025-2029 109,511 3,190 39,310 3,845 3,663 2030-2034 73,030 - 15,806 4,925 2,555 2035-2039 30,425 - 2,267 6,285 1,176 2040 - - - 1,450 36 Total requirements 473,770 8,941 229,053 21,860$ 17,154$

Less: unaccreted interest - (4,241) - Total 473,770$ 4,700$ 229,053$

Lease Revenue Bonds Certificates of Participation

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

18

Issuance of 2013 Lease Revenue Bonds

In August of 2013, the Authority issued a total of $40 million in Lease Revenue Bonds (the “2013 Bonds”) with an average interest rate of 5% and a bond premium of $3 million. Together with other available moneys, the proceeds of the 2013 Bonds totaling $43 million were used to (i) refund the outstanding 1997, 1999, and 2001 Bonds (collectively, the “Prior Bonds”) with an aggregated total of $39 million, (ii) finance the Skylonda Fire Station Project of $4 million, and (iii) pay costs of issuance of the 2013 Bonds totaling $0.6 million. The refunding resulted in a $0.1 million loss in early retirement of the Prior Bonds (the difference between the funds required to refund the old debt and the net carrying amount of the old debt). The loss is reported as deferred outflow of resources on the Statement of Net Position and amortized over the remaining life of the old debt until July 15, 2032. Despite the loss, the Authority in effect realized an economic gain of $3.1 million (the difference between the present value of the debt service payments on the old debt and the present value of the debt service payments on the new debt) by reducing its aggregate debt service payments of $4.5 million over the next 20 years.

The 2013 Bonds are limited obligations of the Authority payable solely from, and secured solely by, revenues of the Authority, consisting primarily of Base Rental Payments to be received by the Authority from the County under a Master Facility Lease between the Authority and the County, for the right to use and possess certain real property and facilities. Issuance of 2014 Lease Revenue Bonds

In May of 2014, the Authority issued a total of $175 million in Lease Revenue Bonds (the “2014 Bonds”) with an average interest rate of 4.65% and a bond premium of $24 million. Together with other available moneys, the proceeds of the 2014 Bonds totaling $199 million were used to (i) finance the acquisition, construction, equipping of the Maple Street Correctional Center, (ii) refund all of the outstanding County’s 2013-14 Notes previously issued by the County, the proceeds of which were used to reimburse the County for the purchase price of the site, (iii) pay capitalized interest on the 2014 Bonds through May 30, 2016, (iv) provide Reserve Account Requirement, and (v) pay costs of issuance of the 2014 Bonds. The 2014 Bonds are limited obligations of the Authority payable solely from, and secured solely by, revenues of the Authority, consisting primarily of Base Rental Payments to be received by the Authority from the County under a Master Facility Lease between the Authority and the County, for the right to use and possess certain real property and facilities.

NOTE 6 – COMMITMENTS

Youth Services Center In November 2003, the Authority issued lease revenue bonds to construct a new County Youth Services Center. The main facility of the Youth Services Center was completed in September 2006 and the Receiving Home in January 2010. The demolition of the old Hillcrest Facility and re-sculpting of the Berm were completed in November 2011. A risk assessment feasibility study for security improvements along Loop Road was conducted in 2009 and recommended constructing perimeter fencing, gates, controls and associated appurtenances, lighting, communications, and video surveillance. The Loop Road Security project was completed in the spring of 2014 for an overall project cost of $1.3 million. The County also approved one additional project to replace deficient surveillance and security system throughout the facility. As of June 30, 2014, the amount committed is yet to be determined upon receipt of the professional estimator’s report.

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Notes to the Basic Financial Statements (Continued) For the Fiscal Year Ended June 30, 2014

19

Maple Street Correctional Center

In December 2010, the County purchased four parcels of land at 20-80 Chemical Way, Redwood City, to build a new jail (the Maple Street Correctional Center). This new jail is approximately 259,806 square feet, consisting of a 768-bed facility, a surface parking for 189 vehicles, and all necessary on site and off site utility improvements. The jail will consist of a processing/transport area, a non-secure inmate-housing wing, an administrative and support services for laundry and food, and a secure inmate housing. The site will also include Video Visitation for inmates and a 4,660 square feet Central Utility Plant building. In May 2014, the Authority issued lease revenue bonds of $175 million to finance the jail construction. As of June 30, 2014, about $126 million remains in the budget to complete the construction. The estimated date of completion is November 2015. Skylonda Fire Station In August 2013, the Authority issued the 2013 Bonds totaling $40 million. A portion of the proceeds of the 2013 Bonds is used to finance capital improvements to the Skylonda Fire Station located on Skyline Boulevard in the Town of Woodside, California. This project replaces the existing barracks and offices at Station 58 and adds a community room in a new 6,000 square foot facility. The fire station will house two engines (a paramedic engine and a wildland engine) and serves the communities of Skylonda, Kings Mountain, La Honda, Upper Woodside, Alpine Road, Middleton Tract, and Skyline Boulevard. The estimated project cost is $4 million. As of June 30, 2014, $3.9 million has been committed to fund this project.

NOTE 7 – SPECIAL ITEM In 2010, the County purchased four real properties in Redwood City to construct a new County jail (the Maple Street Correctional Center). The center will provide a permanent relief to the overpopulated jail facilities and various programs to better transition offenders back into society. In May of 2014, the Authority issued the 2014 Bonds for a total of $175 million to finance the jail construction, to reimburse the County for expenses incurred for the jail project, and to pay bond issuance costs. As a result, the Authority reimbursed $28.8 million to the County for project expenses incurred prior to the fiscal year 2013-14.

The Authority usually issues bonds to provide funds for capital projects and improvements before construction begins. For the jail project the Authority issued bonds to raise capital four years later after the groundbreaking, and part of the bond proceeds was specifically used to reimburse related project expenses previously incurred by the County. Given that the nature of this funding arrangement is infrequent, the Authority reported the reimbursement of $28.8 million to the County as a special item on its financial statements.

1997 1999 20011993 Satellite Health Capital 1997 Capital Capital

Refunding Clinic Center Projects Colma Creek Projects ProjectsASSETS

Current assets:Cash equivalents 4,341,704$ -$ 320,078$ -$ 17,925$ -$ 2,152,945$ Cash equivalents - restricted for debt service 845,266 677,988 - - - - - Investments - restricted for debt service 5,470,450 938,265 - - - - - Prepayment - - - - - - - Net investment in leases - current - - - - 380,000 - - Interest receivable:

Net investment in leases - - - - 252,513 - - Investments - 18,344 8 - - - 4,068

Total current assets 10,657,420 1,634,597 320,086 - 650,438 - 2,157,013

Noncurrent assets:Net investment in leases - noncurrent 31,225,000 6,785,278 - - 11,405,000 - -

Total assets 41,882,420 8,419,875 320,086 - 12,055,438 - 2,157,013

DEFERRED OUTLFOWS OF RESOURCESUnamortized loss on refunding of debt - - - - - - -

LIABILITIES

Current liabilities:Accounts payable - 2,500 3,750 - 2,500 - - Interest payable 981,125 - - - 252,513 - - Due to the County - - - - - - 117,207 Advance from the County - - - - - - - Lease revenue bonds, net of unamortized

discount/premium - current 3,505,000 - - - - - - Certificates of participation, net of

unamortized premium - current - - - - 380,000 - - Total current liabilities 4,486,125 2,500 3,750 - 635,013 - 117,207

Noncurrent liabilities:Accreted interest on capital appreciation

bonds - noncurrent - 4,700,462 - - - - - Lease revenue bonds, net of unamortized

discount/premium - noncurrent 31,225,000 2,084,816 - - - - - Certificates of participation, net of

unamortized premium - noncurrent - - - - 11,405,000 - - Total noncurrent liabilities 31,225,000 6,785,278 - - 11,405,000 - -

Total liabilities 35,711,125 6,787,778 3,750 - 12,040,013 - 117,207

NET POSITIONRestricted for capital projects - - - - - - - Restricted for debt service 6,315,716 1,632,097 - - 15,425 - - Unrestricted (deficit) (144,421) - 316,336 - - - 2,039,806

Total net position 6,171,295$ 1,632,097$ 316,336$ -$ 15,425$ -$ 2,039,806$

(continued)

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Supplementary Schedule of Net PositionJune 30, 2014

20

2013 20142004 2008 2009 Refunding and Capital

Colma Creek Refunding Refunding Capital Project Projects TotalASSETS

Current assets:6,411$ 1,993,694$ 20,151$ 3,954,233$ 142,468,628$ 155,275,769$ Cash equivalents

- 9,360,433 - 5,758,278 7,033,234 23,675,199 Cash equivalents - restricted for debt service- - - 1,935,972 - 8,344,687 Investments - restricted for debt service- - - 333 3,750 4,083 Prepayment

45,000 3,130,000 6,080,000 990,000 - 10,625,000 Net investment in leases - currentInterest receivable:

204,529 2,862,094 2,144,954 898,774 394,594 6,757,458 Net investment in leases3 3,074 1 45,356 25,821 96,675 Investments

255,943 17,349,295 8,245,106 13,582,946 149,926,027 204,778,871 Total current assets

Noncurrent assets:10,030,000 124,070,000 88,545,000 39,075,000 175,065,000 486,200,278 Net investment in leases - noncurrent

10,285,943 141,419,295 96,790,106 52,657,946 324,991,027 690,979,149 Total assets

DEFERRED OUTLFOWS OF RESOURCES- 6,445,406 806,635 83,578 - 7,335,619 Unamortized loss on refunding of debt

LIABILITIES

Current liabilities:- 12,500 - 44,775 7,893,542 7,959,567 Accounts payable

204,529 2,862,094 2,144,954 898,774 394,594 7,738,583 Interest payable- - - - 1,658,606 1,775,813 Due to the County- - - - 7,033,213 7,033,213 Advance from the County

Lease revenue bonds, net of unamortized - 3,191,162 6,595,857 1,134,470 44,057 14,470,546 discount/premium - current

Certificates of participation, net of47,171 - - - - 427,171 unamortized premium - current

251,700 6,065,756 8,740,811 2,078,019 17,024,012 39,404,893 Total current liabilities

Noncurrent liabilities:Accreted interest on capital appreciation

- - - - - 4,700,462 bonds - noncurrentLease revenue bonds, net of unamortized

- 125,356,944 94,240,922 41,773,955 199,296,453 493,978,090 discount/premium - noncurrent Certificates of participation, net of

10,082,285 - - - - 21,487,285 unamortized premium - noncurrent10,082,285 125,356,944 94,240,922 41,773,955 199,296,453 520,165,837 Total noncurrent liabilities

10,333,985 131,422,700 102,981,733 43,851,974 216,320,465 559,570,730 Total liabilities

NET POSITION- 99,715 - 1,151,232 101,637,328 102,888,275 Restricted for capital projects- 9,360,433 - 7,738,318 7,033,234 32,095,223 Restricted for debt service

(48,042) 6,981,853 (5,384,992) - - 3,760,540 Unrestricted (deficit)

(48,042)$ 16,442,001$ (5,384,992)$ 8,889,550$ 108,670,562$ 138,744,038$ Total net position

Supplementary Schedule of Net PositionJune 30, 2014

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

21

1997 1999 20011993 Satellite Health Capital 1997 Capital Capital

Refunding Clinic Center Projects Colma Creek Projects Projects

Operating revenuesLease interest revenue from the County 1,962,250$ 387,448$ -$ 23,169$ 607,606$ 26,698$ 33,259$ Lease contract revenue - - - - - - - Other - - - - - - -

Total operating revenues 1,962,250 387,448 - 23,169 607,606 26,698 33,259

Operating expensesGeneral and administrative 4,500 8,387 14,525 - 5,000 2,800 7,000 Reimbursement of County project costs - - - - - - -

Total operating expenses 4,500 8,387 14,525 - 5,000 2,800 7,000

Operating income (loss) 1,957,750 379,061 (14,525) 23,169 602,606 23,898 26,259

Nonoperating revenues (expenses)Interest and investment income 371,307 55,496 349 - - 230 28,347 Interest expense (1,962,250) (387,448) - (54,651) (607,606) (65,855) (77,901) Extinguished receivable due to refunding - - - (10,850,000) - (12,815,000) (15,490,000) Recoveries from investment loss - - - - - - - Contribution to the County (288,840) - - - - - (1,395,014) Bond issuance costs - - - - - - -

Net nonoperating revenues (expenses) (1,879,783) (331,952) 349 (10,904,651) (607,606) (12,880,625) (16,934,568)

Income (loss) before special item and transfers 77,967 47,109 (14,176) (10,881,482) (5,000) (12,856,727) (16,908,309)

Special item - project costs incurred prior to bond issuance - - - - - - -

Transfers in - - - 10,883,982 - 12,854,157 15,534,145 Transfers out - - (2,638,819) (14) - (1,908,672) (4,098,398)

Change in net position 77,967 47,109 (2,652,995) 2,486 (5,000) (1,911,242) (5,472,562)

Net position, beginning of year 6,093,328 1,584,988 2,969,331 (2,486) 20,425 1,911,242 7,512,368

Net position, end of year 6,171,295$ 1,632,097$ 316,336$ -$ 15,425$ -$ 2,039,806$

(continued)

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Supplementary Schedule of Revenues, Expenses, and Changes in Net PositionFor the Fiscal Year Ended June 30, 2014

22

2013 20142004 2008 2009 Refunding and Capital

Colma Creek Refunding Refunding Capital Project Projects Elimination Total

Operating revenues491,001$ 6,249,553$ 4,690,244$ 1,759,419$ 394,594$ -$ 16,625,241$ Lease interest revenue from the County

- - - 40,065,000 175,065,000 (39,155,000) 175,975,000 Lease contract revenue11,000 - - - - - 11,000 Other

502,001 6,249,553 4,690,244 41,824,419 175,459,594 (39,155,000) 192,611,241 Total operating revenues

Operating expenses4,667 25,000 2,500 8,667 750 - 83,796 General and administrative

- 1,219,345 - 163,216 36,159,294 - 37,541,855 Reimbursement of County project costs4,667 1,244,345 2,500 171,883 36,160,044 - 37,625,651 Total operating expenses

497,334 5,005,208 4,687,744 41,652,536 139,299,550 (39,155,000) 154,985,590 Operating income (loss)

Nonoperating revenues (expenses)16 28,983 149 92,502 20,393 - 597,772 Interest and investment income

(488,832) (6,480,809) (4,236,436) (1,619,196) (350,537) - (16,331,521) Interest expense- - - - - 39,155,000 - Extinguished receivable due to refunding

25 278,165 - - - - 278,190 Recoveries from investment loss- - - - - - (1,683,854) Contribution to the County- - - (609,911) (1,517,279) - (2,127,190) Bond issuance costs

(488,791) (6,173,661) (4,236,287) (2,136,605) (1,847,423) 39,155,000 (19,266,603) Net nonoperating revenues (expenses)

Income (loss) before special item 8,543 (1,168,453) 451,457 39,515,931 137,452,127 - 135,718,987 and transfers

Special item - project costs incurred prior to - - - - (28,781,565) - (28,781,565) bond issuance- - - 8,645,903 - (47,918,187) - Transfers in- - - (39,272,284) - 47,918,187 - Transfers out

8,543 (1,168,453) 451,457 8,889,550 108,670,562 - 106,937,422 Change in net position

(56,585) 17,610,454 (5,836,449) - - - 31,806,616 Net position, beginning of year

(48,042)$ 16,442,001$ (5,384,992)$ 8,889,550$ 108,670,562$ -$ 138,744,038$ Net position, end of year

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Supplementary Schedule of Revenues, Expenses, and Changes in PositionFor the Fiscal Year Ended June 30, 2014

23

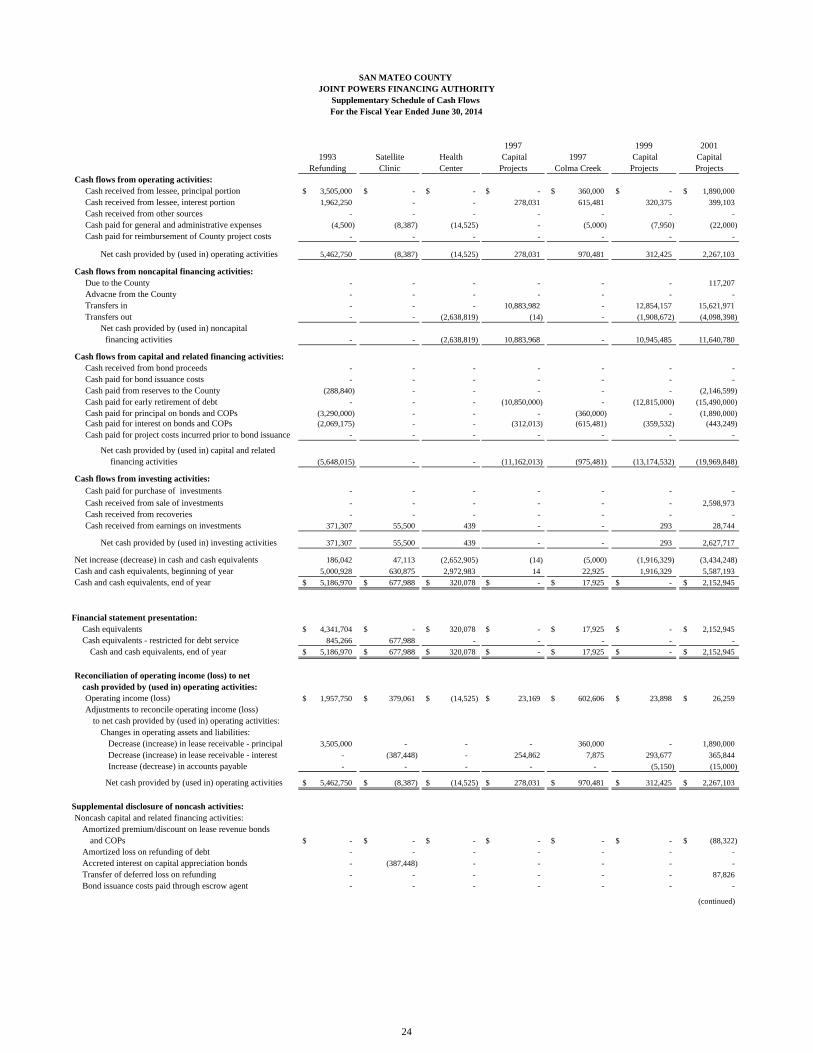

1997 1999 20011993 Satellite Health Capital 1997 Capital Capital

Refunding Clinic Center Projects Colma Creek Projects ProjectsCash flows from operating activities:

Cash received from lessee, principal portion 3,505,000$ -$ -$ -$ 360,000$ -$ 1,890,000$

Cash received from lessee, interest portion 1,962,250 - - 278,031 615,481 320,375 399,103

Cash received from other sources - - - - - - -

Cash paid for general and administrative expenses (4,500) (8,387) (14,525) - (5,000) (7,950) (22,000)

Cash paid for reimbursement of County project costs - - - - - - -

Net cash provided by (used in) operating activities 5,462,750 (8,387) (14,525) 278,031 970,481 312,425 2,267,103

Cash flows from noncapital financing activities:Due to the County - - - - - - 117,207

Advacne from the County - - - - - - -

Transfers in - - - 10,883,982 - 12,854,157 15,621,971

Transfers out - - (2,638,819) (14) - (1,908,672) (4,098,398)

Net cash provided by (used in) noncapital financing activities - - (2,638,819) 10,883,968 - 10,945,485 11,640,780

Cash flows from capital and related financing activities:Cash received from bond proceeds - - - - - - -

Cash paid for bond issuance costs - - - - - - -

Cash paid from reserves to the County (288,840) - - - - - (2,146,599)

Cash paid for early retirement of debt - - - (10,850,000) - (12,815,000) (15,490,000)

Cash paid for principal on bonds and COPs (3,290,000) - - - (360,000) - (1,890,000) Cash paid for interest on bonds and COPs (2,069,175) - - (312,013) (615,481) (359,532) (443,249)

Cash paid for project costs incurred prior to bond issuance - - - - - - -

Net cash provided by (used in) capital and related financing activities (5,648,015) - - (11,162,013) (975,481) (13,174,532) (19,969,848)

Cash flows from investing activities:Cash paid for purchase of investments - - - - - - -

Cash received from sale of investments - - - - - - 2,598,973

Cash received from recoveries - - - - - - -

Cash received from earnings on investments 371,307 55,500 439 - - 293 28,744

Net cash provided by (used in) investing activities 371,307 55,500 439 - - 293 2,627,717

Net increase (decrease) in cash and cash equivalents 186,042 47,113 (2,652,905) (14) (5,000) (1,916,329) (3,434,248)

Cash and cash equivalents, beginning of year 5,000,928 630,875 2,972,983 14 22,925 1,916,329 5,587,193

Cash and cash equivalents, end of year 5,186,970$ 677,988$ 320,078$ -$ 17,925$ -$ 2,152,945$

Financial statement presentation:Cash equivalents 4,341,704$ -$ 320,078$ -$ 17,925$ -$ 2,152,945$

Cash equivalents - restricted for debt service 845,266 677,988 - - - - -

Cash and cash equivalents, end of year 5,186,970$ 677,988$ 320,078$ -$ 17,925$ -$ 2,152,945$

Reconciliation of operating income (loss) to netcash provided by (used in) operating activities:Operating income (loss) 1,957,750$ 379,061$ (14,525)$ 23,169$ 602,606$ 23,898$ 26,259$

Adjustments to reconcile operating income (loss)to net cash provided by (used in) operating activities:

Changes in operating assets and liabilities:Decrease (increase) in lease receivable - principal 3,505,000 - - - 360,000 - 1,890,000

Decrease (increase) in lease receivable - interest - (387,448) - 254,862 7,875 293,677 365,844

Increase (decrease) in accounts payable - - - - - (5,150) (15,000)

Net cash provided by (used in) operating activities 5,462,750$ (8,387)$ (14,525)$ 278,031$ 970,481$ 312,425$ 2,267,103$

Supplemental disclosure of noncash activities:Noncash capital and related financing activities:

Amortized premium/discount on lease revenue bonds and COPs -$ -$ -$ -$ -$ -$ (88,322)$

Amortized loss on refunding of debt - - - - - - -

Accreted interest on capital appreciation bonds - (387,448) - - - - -

Transfer of deferred loss on refunding - - - - - - 87,826

Bond issuance costs paid through escrow agent - - - - - - -

(continued)

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Supplementary Schedule of Cash Flows For the Fiscal Year Ended June 30, 2014

24

20142004 2008 2009 2013 Capital

Colma Creek Refunding Refunding Refunding Projects Elimination TotalCash flows from operating activities:

45,000$ 2,990,000$ 5,765,000$ -$ -$ -$ 14,555,000$ Cash received from lessee, principal portion491,658 6,304,369 4,804,025 860,645 - - 16,035,937 Cash received from lessee, interest portion11,000 - - - - - 11,000 Cash received from other sources(9,250) (25,000) (2,500) (4,000) (4,500) - (107,612) Cash paid for general and administrative expenses

- (1,222,481) - (123,441) (26,607,146) - (27,953,068) Cash paid for reimbursement of County project costs

538,408 8,046,888 10,566,525 733,204 (26,611,646) - 2,541,257 Net cash provided by (used in) operating activities

Cash flows from noncapital financing activities:- - - - - - 117,207 Due to the County- - - - 7,033,213 - 7,033,213 Advance from the County- - - 8,645,903 - (48,006,013) - Transfers in- - - (39,360,110) - 48,006,013 - Transfers out

Net cash provided by (used in) noncapital- - - (30,714,207) 7,033,213 - 7,150,420 financing activities

Cash flows from capital and related financing activities:- - - 42,835,883 198,516,605 - 241,352,488 Cash received from bond proceeds- - - (392,899) (649,317) - (1,042,216) Cash paid for bond issuance costs- - - - - - (2,435,439) Cash paid from reserves to the County- - - - - - (39,155,000) Cash paid for early retirement of debt

(45,000) (2,990,000) (5,765,000) - - - (14,340,000) Cash paid for principal on bonds and COPs(491,657) (6,304,368) (4,804,025) (860,644) - - (16,260,144) Cash paid for interest on bonds and COPs

- - - - (28,781,565) (28,781,565) Cash paid for project costs incurred prior to bond issuance

Net cash provided by (used in) capital and related (536,657) (9,294,368) (10,569,025) 41,582,340 169,085,723 - 139,338,124 financing activities

Cash flows from investing activities:- - - (1,935,972) (25,821) - (1,961,793) Cash paid for purchase of investments- - - - - - 2,598,973 Cash received from sale of investments

25 278,165 - - - - 278,190 Cash received from recoveries15 30,706 149 47,146 20,393 - 554,692 Cash received from earnings on investments

40 308,871 149 (1,888,826) (5,428) - 1,470,062 Net cash provided by (used in) investing activities

1,791 (938,609) (2,351) 9,712,511 149,501,862 - 150,499,863 Net increase (decrease) in cash and cash equivalents4,620 12,292,736 22,502 - - - 28,451,105 Cash and cash equivalents, beginning of year6,411$ 11,354,127$ 20,151$ 9,712,511$ 149,501,862$ -$ 178,950,968$ Cash and cash equivalents, end of year

Financial statement presentation:6,411$ 1,993,694$ 20,151$ 3,954,233$ 142,468,628$ - 155,275,769$

- 9,360,433 - 5,758,278 7,033,234 - 23,675,199

6,411$ 11,354,127$ 20,151$ 9,712,511$ 149,501,862$ -$ 178,950,968$ Cash and cash equivalents, end of year

Reconciliation of operating income (loss) to netcash provided by (used in) operating activities:

497,334$ 5,005,208$ 4,687,744$ 41,652,536$ 139,299,550$ (39,155,000)$ 154,985,590$ Operating income (loss)Adjustments to reconcile operating income (loss)

to net cash provided by (used in) operating activities:Changes in operating assets and liabilities:

45,000 2,990,000 5,765,000 (40,065,000) (175,065,000) 39,155,000 (161,420,000) Decrease (increase) in lease receivable - principal657 54,816 113,781 (898,774) (394,594) - (589,304) Decrease (increase) in lease receivable - interest

(4,583) (3,136) - 44,442 9,548,398 - 9,564,971 Increase (decrease) in accounts payable

538,408$ 8,046,888$ 10,566,525$ 733,204$ (26,611,646)$ -$ 2,541,257$ Net cash provided by (used in) operating activities

Supplemental disclosure of noncash activities:Noncash capital and related financing activities:

Amortized premium/discount on lease revenue bonds 2,171$ 61,162$ 515,857$ 144,470$ 44,057$ -$ 679,395$ and COPs

- (292,419) (62,049) (4,247) - - (358,715) Amortized loss on refunding of debt- - - - - - (387,448) Accreted interest on capital appreciation bonds- - - - - - 87,826 Transfer of deferred loss on refunding- - - (217,012) (867,962) - (1,084,974) Bond issuance costs paid through escrow agent

Cash equivalentsCash equivalents - restricted for debt service

SAN MATEO COUNTY JOINT POWERS FINANCING AUTHORITY

Supplementary Schedule of Cash Flows For the Fiscal Year Ended June 30, 2014

25

26

This page intentionally left blank

27

Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based On an Audit of Financial Statements

Performed In Accordance with Government Auditing Standards

Board of Directors San Mateo County Joint Powers Financing Authority Redwood City, California We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the San Mateo County Joint Powers Financing Authority (Authority), a component unit of the County of San Mateo, California (County), as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the Authority’s basic financial statements, and have issued our report thereon dated October 30, 2014. Internal Control over Financial Reporting

In planning and performing our audit of the financial statements, we considered the Authority’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Authority’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Authority’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Authority’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an

28

opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Authority’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Authority’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose. Walnut Creek, California October 30, 2014