Samsung Card - Tistory

38

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 07 September 2010 Asia Pacific/South Korea Equity Research Consumer Finance Samsung Card (029780.KS / 029780 KS) ASSUMING COVERAGE Leveraged play on consumption and group restructuring ■ Assuming coverage with OUTPERFORM: We assume coverage of Samsung Card (SSC) with an OUTPERFORM rating and a 12-month (SOTP-based) target price of W71,000. We believe SSCs share price will strengthen in the next six to 12 months, driven by: 1) resilient domestic consumption and 2) the groups impending circular ownership restructuring. ■ SSCs leveraging to resume amid resilient domestic consumption: As SSCs business mix adjustment comes to an end in 2H10, we expect SSC to resume leveraging (i.e., asset growth) from 2H versus negative growth since 2Q09. In terms of macro factors, retail sales remain strong against the backdrop of a recovery from the financial crisis and structural growth factors, i.e., Korean consumers trading-up of consumption, as evidenced by strong retail sales numbers in July-August. ■ SSC as the biggest beneficiary from group ownership restructuring: As part of the belated compliance with the Financial Restructuring Law (FRL), SSC should divest a 20.6% stake in Everland by April 2012. We envisage that SSC will divest its stake through an IPO in 2011. Meanwhile, the market should interpret SSCs divesture of the other affiliate stake before year-end for a tax credit as the start of ownership restructuring, in our view. ■ SOTP target price of W71,000 with new emphasis on holding co. value: We derive our target price by reflecting the holding company value of its Everland stake. Our target price comprises the value of: 1) the credit card operation (W45,000), 2) investment assets (W11,000), and 3) the Everland stake as a de facto holding company (W15,000). Key risks include: 1) a possible funding cost increase driven by a interest rate hike and 2) SG&A cost increase amid competition. Share price performance 20000 40000 60000 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 80 100 120 140 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the KOREA SE COMPOSITE (KOSPI) index which closed at 1787.74 on 07/09/10 On 07/09/10 the spot exchange rate was W1172.12/US$1 Performance Over 1M 3M 12M Absolute (%) 13.9 0.6 Relative (%) -0.2 4.3 -9.5 Financial and valuation metrics Year 12/09A 12/10E 12/11E 12/12E Pre-provision profit (W bn) 658.8 608.4 742.3 859.7 Pre -tax profit (W bn) 690.8 583.1 668.4 769.4 Net attributable profit (W bn) 603.8 582.9 521.3 600.1 EPS (CS adj.) (W) 4,910.59 4,740.66 4,239.89 4,880.77 Change from previous EPS (%) n.a. 31.6 12.8 Consensus EPS (W) n.a. 3,870 4,165 4,761 EPS growth (%) 130.2 -3.5 -10.6 15.1 P/E (x) 10.9 11.2 12.6 10.9 Dividend yield (%) 1.7 2.1 2.1 2.3 CS adj. BVPS (W) 35,997.1 47,262.6 50,930.5 55,079.0 P/B (x) 1.5 1.1 1.0 1.0 ROE 14.8 11.4 8.7 9.3 ROA (%) 4.0 4.0 3.2 3.4 Tier 1 Ratio (%) 35.0 39.1 38.0 37.1 Source: Company data, Thomson Reuters, Credit Suisse estimates. Rating OUTPERFORM* Price (07 Sep 10, W) 53,300.00 Target price (W) (from 60,000) 71,000„ Chg to TP (%) 33.2 Market cap. (W bn) 6,553.71 (US$ 5.59) Enterprise value (W bn) 6,554 Number of shares (mn) 122.96 Free float (%) 32.28 52-week price range 58200 - 45250 *Stock ratings are relative to the relevant country benchmark. „Target price is for 12 months. Research Analysts Sokmo Yun 822 3707 3763 [email protected] Soyeon Hong 822 3707 3740 [email protected] Seok Yun, CFA, CA 822 3707 3730 [email protected]

Transcript of Samsung Card - Tistory

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

07 September 2010Asia Pacific/South Korea

Equity ResearchConsumer Finance

Samsung Card (029780.KS / 029780 KS)

ASSUMING COVERAGE

Leveraged play on consumption and group restructuring ■ Assuming coverage with OUTPERFORM: We assume coverage of

Samsung Card (SSC) with an OUTPERFORM rating and a 12-month (SOTP-based) target price of W71,000. We believe SSC�s share price will strengthen in the next six to 12 months, driven by: 1) resilient domestic consumption and 2) the group�s impending circular ownership restructuring.

■ SSC�s leveraging to resume amid resilient domestic consumption: As SSC�s business mix adjustment comes to an end in 2H10, we expect SSC to resume leveraging (i.e., asset growth) from 2H versus negative growth since 2Q09. In terms of macro factors, retail sales remain strong against the backdrop of a recovery from the financial crisis and structural growth factors, i.e., Korean consumers� trading-up of consumption, as evidenced by strong retail sales numbers in July-August.

■ SSC as the biggest beneficiary from group ownership restructuring: As part of the belated compliance with the Financial Restructuring Law (FRL), SSC should divest a 20.6% stake in Everland by April 2012. We envisage that SSC will divest its stake through an IPO in 2011. Meanwhile, the market should interpret SSC�s divesture of the other affiliate stake before year-end for a tax credit as the start of ownership restructuring, in our view.

■ SOTP target price of W71,000 with new emphasis on holding co. value: We derive our target price by reflecting the holding company value of its Everland stake. Our target price comprises the value of: 1) the credit card operation (W45,000), 2) investment assets (W11,000), and 3) the Everland stake as a de facto holding company (W15,000). Key risks include: 1) a possible funding cost increase driven by a interest rate hike and 2) SG&A cost increase amid competition.

Share price performance

20000

40000

60000

Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-1080100120140

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the KOREA SE COMPOSITE (KOSPI) index which closed at 1787.74 on 07/09/10 On 07/09/10 the spot exchange rate was W1172.12/US$1

Performance Over 1M 3M 12M Absolute (%) � 13.9 0.6 Relative (%) -0.2 4.3 -9.5

Financial and valuation metrics

Year 12/09A 12/10E 12/11E 12/12EPre-provision profit (W bn) 658.8 608.4 742.3 859.7Pre -tax profit (W bn) 690.8 583.1 668.4 769.4Net attributable profit (W bn) 603.8 582.9 521.3 600.1EPS (CS adj.) (W) 4,910.59 4,740.66 4,239.89 4,880.77Change from previous EPS (%) n.a. 31.6 12.8Consensus EPS (W) n.a. 3,870 4,165 4,761EPS growth (%) 130.2 -3.5 -10.6 15.1P/E (x) 10.9 11.2 12.6 10.9Dividend yield (%) 1.7 2.1 2.1 2.3CS adj. BVPS (W) 35,997.1 47,262.6 50,930.5 55,079.0P/B (x) 1.5 1.1 1.0 1.0ROE 14.8 11.4 8.7 9.3ROA (%) 4.0 4.0 3.2 3.4Tier 1 Ratio (%) 35.0 39.1 38.0 37.1

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (07 Sep 10, W) 53,300.00 Target price (W) (from 60,000) 71,000¹ Chg to TP (%) 33.2 Market cap. (W bn) 6,553.71 (US$ 5.59) Enterprise value (W bn) 6,554 Number of shares (mn) 122.96 Free float (%) 32.28 52-week price range 58200 - 45250 *Stock ratings are relative to the relevant country benchmark. ¹Target price is for 12 months.

Research Analysts Sokmo Yun

822 3707 3763 [email protected]

Soyeon Hong 822 3707 3740

Seok Yun, CFA, CA 822 3707 3730

07 September 2010

Samsung Card (029780.KS / 029780 KS) 2

Focus charts and table Figure 1: SSC � a leveraged domestic consumption play Figure 2: SSC�s asset growth to resume from 2H10

6070

8090

100110

120130

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

-25-20-15-10-50510152025(%)

Retail sales index , seasonally adjusted YoY grow th (RHS)

-20

-10

0

10

20

30

1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12

-20

-15

-10

-5

0

5

10

Asset growth Y/Y (LHS) Cardholders growth Y/Y (RHS)

CS estimate(%) (%)

-20

-10

0

10

20

30

1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12

-20

-15

-10

-5

0

5

10

Asset growth Y/Y (LHS) Cardholders growth Y/Y (RHS)

CS estimate(%) (%)

Source: National Statistics Office Source: FSS, and Credit Suisse

Figure 3: SSC � a beneficiary of unwinding of circular Figure 4: Target price of W71,000 based on SOTP

1.8% 3.1%

4.9% 1.9% 3.0%

1.3%

4.7% 4.9%

Samsung Eng. Samsung Fine Chemicals

S1

Hotel Shilla

Samsung F&M

25.1%

Samsung Life

Samsung Elec.

Everland

Family

Samsung Card

20.8%

4.7%

35.3%

26.4%

19.3%

7.5%

25.6%

Samsung Securities

Cheil Ind.

Cheil Worldwide

SSC should reduce below 5% by April 2012

SSC might sell some of these stakes to utilize W1.3 tn of tax credit within 2010

(W bn) Equity and target multiple Value

Shareholders' equity at 2Q10 5,811"Other comprehensive income" at 2Q10 1,550Shareholders' equity excl. "OCI" 4,261Target P/B (x) 1.3Credit card operation value 5,540

Operation value � credit card

Per share 45,000"Other comprehensive income" at 2Q10 1,550(Post-tax) MTM value of investment assets 278Sub-total 1,828Target P/B (x) 0.75Investment asset value 1,371

Investment asset value

Per share 11,00025.6% of Everland's BV at Dec-09 593(Post-tax) Revaluation of SLI stake 33425.6% of Everland's BV (e) at Jun-10 927Target P/B (x) - Applying multiple of SK C&C 3.0Hold co value (excluding BV) 1,854

Hold co value of Everland

Per share 15,000Firm value (W bn) 8,764SOTP value (W) 71,000

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 5: Cost-income ratio remains stable unlike concern Figure 6: Interest rate hike perceived as a potential risk

0

200

400

600

800

1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

(W b

n)

0%

20%

40%

60%

80%

100%

Income (LHS) Cost (LHS) Cost-income ratio (RHS)

CS fo recast

20,000

30,000

40,000

50,000

60,000

70,000

Jul 0

7

Nov

07

Mar

08

Jul 0

8

Nov

08

Mar

09

Jul 0

9

Nov

09

Mar

10

Jul 1

0

(W)

45678910

(%)

Share price (LHS) 3Y Corp. bond (AA0, RHS)

Source: Company data, Credit Suisse estimates Source: Datastream

07 September 2010

Samsung Card (029780.KS / 029780 KS) 3

Leveraged play on consumption and group restructuring We assume coverage of Samsung Card (SSC) with an OUTPERFORM rating and a 12-month target price of W71,000. We believe SSC�s share price will show strength on the back of: 1) a resilient domestic consumption trend, driven by a recovery from a low base and Korean consumers� trading-up of consumption, and 2) Samsung group�s ownership restructuring � the unwinding of circular ownership by listing Everland (Samsung Card is the majority shareholder) within 12-18 months.

SSC�s leveraging to resume amid resilient domestic consumption We expect SSC to resume asset growth from 2H10. SSC�s asset growth has remained in the negative territory, due largely to management�s decision to reduce leasing and other businesses from 2009. However, as the business reduction will come to an end in 2H10, we believe SSC will likely deliver positive asset growth from 2H10. In terms of macro factors, domestic retail sales have been strong against the backdrop of a recovery from the financial crisis and structural growth factors, with Korean consumers� trading-up of consumption, as evidenced by strong retail sales numbers in July-August.

SSC to benefit most from group restructuring We believe it is high time to look at SSC from an event angle. Since the IPO of Samsung Life in May, the Samsung Group should address the financial restructuring law (FRL) violation case. According to the FRL, chaebol-affiliated financial companies cannot own more than a 5% stake in a non-financial affiliate. SSC is in violation of the FRL with its 25.6% stake in Everland (not listed). As such, SSC should dispose of its 20.6% stake in Everland by April 2012. We envisage SSC will eventually divest its Everland stake by listing Everland in 2011. Meanwhile, the market should interpret SSC�s divesture of the other affiliate stake before year-end for a tax credit as the start of ownership restructuring, in our view. Then, the market is expected to attempt to reflect the value of Everland as a de facto holding company in SSC�s share price. SSC�s tax credit (effective until end-2010) might also be an incentive for SSC to sell its Everland stake within this year. However, due to various constraints, it is difficult for SSC to divest within this year.

Target price of W71,000 with new emphasis on holding co. value We derive our fair value estimates of SSC by reflecting the holding company value of its Everland stake. Our fair value estimate comprises the value of: 1) the credit card operation (W45,000), 2) investment assets (W11,000), and 3) the Everland stake as a de facto holding company (W15,000). Despite all this, for a further rerating of the stock, we believe SSC should address its capital management issues. Since it is already overcapitalised, more proceeds from the sale of Everland stake might be incrementally negative to ROE. It also needs to address corporate governance concerns that SSC might use those proceeds for purchasing irrelevant group assets.

Key risks: funding and SG&A costs Potential risks include: 1) a possible funding cost increase, driven by a market interest rate hike and 2) an SG&A cost increase amid rising competition. However, we believe the actual impact on earnings will be limited unlike the market perception.

Assuming coverage with an OUTPERFORM rating and a target price of W71,000

Resilient domestic consumption provides stable underpinning to SSC�s leveraging efforts

The market is expected to interpret SSC�s divesture of the affiliate stake before end-2010 as the beginning of ownership restructuring

As such, we newly added the holding company value of Everland based on the case of SK C&C, a de facto hold co of SK Group

Aforementioned catalysts outweigh cost concerns, in our view

07 September 2010

Samsung C

ard (029780.K

S / 029780 KS)

4

Valuation comparison Figure 7: Valuation summary Earnings outlook Valuation (x) EPS Book Dividend Loan Equity/ Loan/ Current Target NP Consensus gr gr ROA ROE yield P / P / P / gr NIM assets deposit price % price Upside (W bn) (W bn) NP (%) (%) (%) (%) (%) PPP assets deposit P/E P/B (%) (%) (%) (%) (W) YTD (W) (%)

KB Finanial 08A 1,887.8 -32.8 9.3 0.77 12.1 0.0 3.9 0.06 0.10 8.9 0.94 16.6 3.39 6.9 124 48,800 -18.3 62,000 27.0 Outperform 09A 539.8 -73.3 1.1 0.20 3.2 0.4 6.0 0.07 0.11 33.3 0.93 -2.0 2.69 7.8 114 105560 KS 10E 1,182.3 1,413.6 108.8 3.1 0.44 6.5 1.0 4.3 0.07 0.10 15.9 0.90 1.0 3.09 7.8 107 11E 2,179.7 2,335.1 84.4 10.4 0.76 10.9 2.3 4.0 0.07 0.09 8.6 0.81 2.0 3.12 8.2 102 Shinhan 08A 2,018.6 -16.0 1.1 0.82 15.0 0.0 3.8 0.06 0.13 8.0 1.20 13.6 3.73 5.4 135 43,150 -0.1 62,000 43.7 Outperform 09A 1,305.3 -44.1 1.9 0.50 8.9 0.9 4.9 0.08 0.14 14.4 1.18 -0.8 3.22 6.8 115 055550 KS 10E 2,512.2 2,368.6 87.6 9.3 0.96 14.8 1.6 4.2 0.08 0.13 7.7 1.08 2.1 3.69 7.2 110 11E 3,091.5 2,722.9 7.0 15.1 1.15 14.0 2.5 4.1 0.08 0.13 7.2 0.94 3.1 3.80 8.1 110 Woori 08A 454.5 -77.6 -7.2 0.17 3.5 0.0 3.7 0.04 0.06 23.6 0.88 16.6 2.60 4.2 116 13,300 -4.0 16,000 20.3 Neutral 09A 1,026.0 125.8 12.4 0.35 7.9 0.0 2.7 0.04 0.06 10.4 0.78 -1.3 2.34 4.8 109 053000 KS 10E 1,271.6 1,432.5 23.9 6.8 0.43 9.0 1.5 2.2 0.04 0.06 8.4 0.73 1.8 2.62 4.9 106 11E 2,000.5 1,898.6 57.3 10.1 0.65 13.0 3.0 2.4 0.03 0.05 5.4 0.66 2.1 2.72 5.3 102 Hana 08A 483.4 -62.2 -2.9 0.33 5.3 0.6 3.6 0.04 0.07 13.8 0.74 16.3 2.39 5.7 110 31,500 -4.3 44,000 39.7 Outperform 09A 306.3 -36.6 6.5 0.19 3.4 0.0 5.0 0.04 0.07 21.8 0.69 1.0 1.98 6.4 112 086790 KS 10E 1,118.0 1,012.0 264.9 12.9 0.71 11.0 1.6 2.9 0.04 0.07 6.0 0.6 2.3 2.53 6.9 110 11E 1,208.1 1,146.2 8.1 11.1 0.75 10.6 2.9 2.9 0.04 0.06 5.5 0.55 2.9 2.59 7.6 106 IBK 08A 767.0 -36.6 -4.6 0.59 11.0 0.0 3.2 0.05 0.19 8.9 1.03 17.2 2.70 5.3 263 14,300 2.1 20,000 39.9 Outperform 09A 710.4 -28.4 3.2 0.47 8.3 0.7 3.9 0.06 0.18 12.4 1.00 11.3 2.63 6.1 233 024110 KS 10E 1,317.7 1,327.9 77.6 13.0 0.82 13.5 1.4 2.8 0.06 0.18 7.0 0.88 6.0 2.90 6.6 244 11E 1,538.1 1,529.6 16.7 15.1 0.90 13.8 2.8 2.9 0.05 0.14 6.0 0.77 7.0 2.85 7.1 210 Daegu 08A 261.2 0.1 12.3 1.02 17.6 1.8 3.8 0.07 0.11 7.0 1.14 10.1 3.47 6.0 105 13,800 -19.8 17,000 23.2 Neutral 09A 170.5 -34.7 10.9 0.62 10.2 1.2 3.9 0.07 0.10 10.7 1.03 6.0 3.34 6.4 106 005270 KS 10E 281.2 269.0 64.9 15.5 0.97 14.7 2.9 3.0 0.06 0.10 6.5 0.89 4.0 3.45 7.1 104 11E 321.2 317.0 14.2 13.1 1.07 14.8 3.6 2.9 0.06 0.09 5.7 0.79 3.0 3.56 7.8 99 Busan 08A 275.0 1.6 11.8 1.00 17.8 1.6 3.4 0.07 0.11 6.6 1.11 12.5 3.36 5.9 118 12,450 -10.8 14,500 16.5 Neutral 09A 245.1 -26.8 1.2 0.83 12.7 1.3 4.1 0.08 0.13 9.1 1.10 1.1 3.40 7.0 108 005280 KS 10E 367.0 343.3 43.3 16.7 1.14 16.0 3.2 3.8 0.07 0.12 6.3 0.94 3.0 3.40 7.7 106 11E 380.5 369.4 3.7 12.4 1.13 14.6 4.0 3.7 0.07 0.11 6.1 0.84 3.0 3.49 8.2 98

Samsung Card 08A 258.0 0.0 -51.5 4.7 1.65 7.0 1.1 10.8 0.401) n.a. 25.0 1.74 5.92) 15.93 22.73) n.a. 53,300 -7.3 71,000 33.2 Outperform 09A 603.8 0.0 134.0 17.4 4.04 14.8 1.7 9.9 0.491) n.a. 10.9 1.48 -15.72) 17.18 32.93) n.a. 029780 KS 10E 582.9 483.4 -3.5 31.3 4.02 11.4 2.1 10.8 0.421) n.a. 11.2 1.13 10.22) 18.49 36.83) n.a. 11E 521.3 522.1 -10.6 7.8 3.20 8.7 2.1 8.8 0.391) n.a. 12.6 1.05 10.62) 18.36 36.93) n.a.

1) P/total managed asset, 2) managed receivable growth, 3) Equity/ total managed asset Source: Company data, Bloomberg consensus as of 7 Sep 2010, Credit Suisse estimates

07 September 2010

Samsung Card (029780.KS / 029780 KS) 5

SSC�s leveraging to resume amid domestic consumption SSC is set to resume leveraging from 2H10 We expect SSC to resume asset growth from 2H10. SSC�s asset growth has turned negative since 2Q09, due largely to management�s decision to reduce the (high risk/high return) leasing, instalment financing and consumer loan businesses from 2009. The receivable mix has also changed from cash advance with high credit risk to general credit card sales with low risk. However, as the business reduction comes to an end in 2H10, we expect SSC to deliver high-teen asset growth from 2H10.

Figure 8: SSC to resume its asset growth from 2H10 Figure 9: Gradual leveraging resumes from 2H10

-20-15

-10

-5

05

10

1520

25

1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12

-20

-15

-10

-5

0

5

10

Asset growth Y/Y (LHS) Cardholders growth Y/Y (RHS)

CS estimate(%) (%)

-20-15

-10

-5

05

10

1520

25

1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12

-20

-15

-10

-5

0

5

10

Asset growth Y/Y (LHS) Cardholders growth Y/Y (RHS)

CS estimate(%) (%)

0

5

10

15

20

25

30

1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

(x)

0%

5%

10%

15%20%

25%30%

35%

40%

45%

Card receivable / shareholders' fund (LHS) Tier 1 CAR (RHS)

CS estimate

0

5

10

15

20

25

30

1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

(x)

0%

5%

10%

15%20%

25%30%

35%

40%

45%

Card receivable / shareholders' fund (LHS) Tier 1 CAR (RHS)

CS estimate

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 10: Samsung Card � active cardholders rise faster from 3Q10

Figure 11: Samsung Card has relatively high-rated credit card holders

3,000

4,000

5,000

6,000

7,000

8,000

9,000

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

(e)

('000)

Av ailable cardholders Activ e cardholders

0%

10%

20%

30%

40%A

B

C

D

E

F

G

H

ShinhanSamsung

Hy undaiLotte

Source: Company data, Credit Suisse estimates Source: CREFIA

Against this backdrop, Samsung Card has stepped up its promotion efforts since the beginning of this year. Samsung Card is aggressively acquiring new customers by taking advantage of its affiliate Samsung Electronics� distribution network. According to management, this cross-selling initiative in collaboration with Samsung Electronics is likely

SSC�s leveraging (i.e. asset growth) is set to begin from 2H10

Negative knock-on effect should be limited from asset/volume growth

07 September 2010

Samsung Card (029780.KS / 029780 KS) 6

to materialise from July 2010 or 3Q10. Although Samsung Card stepped up promotion efforts from the start of this year, we believe the negative knock-on effect should be limited, as: 1) strong asset or volume growth is likely to be driven more by the low base of last year, 2) cost-to-income ratio remains at a disciplined level, as evidenced by 1H10 results, 3) Samsung Card strategically focuses on high-quality customers, and 4) asset growth is likely to be funded by sizeable excess capital rather than costly wholesale funding. Although our growth estimate is not enough to dissolve the overcapitalised status, we believe it should enhance capital efficiency to a certain degree.

Resilient domestic consumption provides positive underpinning to SSC�s leveraging efforts Korean consumers� trading-up of consumption positive for credit card issuers

In terms of macro factors, domestic retail sales have been strong since 2009 against the backdrop of a recovery from the financial crisis. However, there were some structural growth factors behind the retail sales growth besides the low base effect. Korean consumers� trading-up of consumption and wage growth have supported sales at department stores as well as discount stores. As we move into 2H10, some investors may have concerns about the higher base, which could drag down the sales growth momentum; however, July-August sales numbers actually trended stronger than expected � 6-10% at department stores and 3-6% at discount stores in August. Backed by benign retail sales growth, credit card spending should also increase, in our view.

Figure 12: Retail sales index trend Figure 13: Retailers� same-store-sales growth trend

60

70

80

90

100

110

120

130

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

-25-20-15-10-50510152025(%)

Retail sales index , seasonally adjusted YoY grow th (RHS)

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

(%)

Discount store - 3mo. mov. avg. Department store - 3mo. mov. avg.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

(%)

Discount store - 3mo. mov. avg. Department store - 3mo. mov. avg.

Source: NSO Source: Ministry of Knowledge Economy

Credit card business continues its steady growth with benign asset/credit quality

Despite the bleak economic outlook, further downside to the credit card business appears limited, in our view. The main rationales for this are: 1) asset/credit quality as well as capitalisation are in much better shape; 2) the cash to credit migration continues; 3) credit card spending is mostly focused on non-discretionary items; and 4) the stable trend of NIM amid the financial market turmoil at 15-20% for the past three years. The overall asset quality of credit card companies shows a clear improvement for the past year. Delinquency ratio fell to 1.84% as of June 2010. Capital adequacy ratio stood at 30.2% as of June 2010, up about 2 p.p. over the past one year. In general, the slowdown in high-risk/high-return businesses, such as cash advances, improved asset quality as well as capitalisation, but lowered profitability, in our view.

July-August domestic consumption is actually trending stronger than expected

Growth with stable margins, benign asset/credit quality, and improving capitalisation

07 September 2010

Samsung Card (029780.KS / 029780 KS) 7

Figure 14: Credit card firms� asset quality and CAR (%) Figure 15: Credit card companies� earnings trends (W bn)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1Q08 2Q 3Q 4Q 1Q09 2Q 3Q 4Q 1Q10 2Q0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

CAR (LHS) Delinquency ratio (RHS)

0

200

400

600

800

1000

1200

4Q 1Q07 2Q 3Q 4Q 1Q08 2Q 3Q 4Q 1Q09 2Q 3Q 4Q 1Q10 2Q

NP

Source: FSS. Source: FSS.

Figure 16: Shinhan Card vs Samsung Card NP (W bn) Figure 17: Trend of net interest margin

-200

-

200

400

600

800

1,000

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10

Shinhan Card Samsung Card

Shinhan Card (ex . Writeback)

0%

5%

10%

15%

20%

25%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 18: NPL ratio Figure 19: Equity-to-card receivable ratio

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

0%

10%

20%

30%

40%

50%

60%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

07 September 2010

Samsung Card (029780.KS / 029780 KS) 8

Industry trend shows �Goldilocks� environment for credit card issuers Increased risk aversion with more focus on the credit sales

Credit card sales (merchant/instalment sales) have continuously increased while cash advances have been tightly controlled by credit card companies after the credit card burst in 2003. Total credit card usage for 2009 amounted to W472 tn, up 1.7% YoY. Credit sales increased to W373 tn, up 4.6% YoY, on the back of increased new car sales amid tax incentives, but cash advances dropped to W99 tn, down 7.9% YoY, mainly due to tightened risk management.

Cash-to-credit migration decelerating a little

The credit card payment portion has also steadily increased since 2004, currently at 65% of the total. We anticipate further growth, as we see continued aggressive marketing by credit card companies and the regulatory changes � the scope of credit card sales is likely to expand as seen in tax payments and car purchases.

Figure 20: Annual credit card sales trend Figure 21: Private consumption vs credit card payment portion

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

1997 1999 2001 2003 2005 2007 2009

(W tn

)

Merchants Installments Cash advances

14.112.214.7

24.1

48.2

64.957.4

52.955.655.958.963.564.6

0

100

200

300

400

500

600

700

1997 1999 2001 2003 2005 2007 2009

(W tn

)

0

10

20

30

40

50

60

70

(%)

Private consmuption (LHS)Credit card payment portion (merchant+installments, RHS)

Source: Credit Finance Association (CREFIA) Source: BOK, CREFIA

�Negative� settlement system � The reform of the Specialized Credit Financial Business Act took place in June 2010 which included the change to the �negative� credit card settlement system from the �positive� settlement system. Under the �negative� settlement system, consumers are instructed on what they cannot pay by credit card, not what they can pay. In other words, consumers can use credit cards for purchases of all goods and services unless listed in the Act � a few exceptions include investment in securities, derivatives and other financial products, bank savings deposits, and purchases in casinos and horse racing. For example, college tuition, public utility bills and other various goods and services would be able to be paid by credit card. Along with the revision of national tax laws (effected last February) which implemented an expanded range of taxes payable by credit card, the reform of this Act should boost structural growth in the credit card market, in our view.

However, despite the revision of the law, a few problems remain unsolved. Some colleges and public institutions are still not willing to take credit cards blaming high credit card fees on the credit card companies. Recently, big life insurance companies in Korea announced they would not take credit cards for customers� paying monthly premiums. The companies are complaining about the high credit-card fees and different treatment applied compared

Credit card companies focus more on credit sales than cash advance

Cash to credit migration continues slower than before

07 September 2010

Samsung Card (029780.KS / 029780 KS) 9

to other derivatives/investments/savings products. Though the relevant law is revised, it will take some time to come into effect in reality.

Credit sales still recovering along with private consumption:

Credit card sales growth has been picking up along with the remarkable private consumption recovery since 2H09. The recent strong growth trend is due to the low base from last year (7% in July 2009) and the continued consumption recovery after the global financial crisis. However, sales growth has slowed more recently, posting 15% in June from 19% in March, and 21% in February largely owing to concerns over the weak global macro environment; however, as seen in Figure 22, sales growth has started to pick up from July posting 17% growth from 15% in June.

Figure 22: Private consumption vs credit card sales growth

Figure 23: Monthly credit card sales trend

-5.0

0.0

5.0

10.0

15.0

20.0

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

(% Y

oY)

Nominal private consumption Credit card sales

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

(W b

n)

-15

-10

-5

0

5

10

15

20

25

30

(%)

Credit card settlement % YoY (RHS)

Source: BOK Source: CREFIA

As well as fiscal tightening in the Euro zone and concerns on the weak global macro recovery, other factors such as domestically another potential interest rate hike in 2H, a declining property market and a slowdown in employment growth might negatively affect private consumption growth, in our view. As seen in Figure 23, credit card sales growth has been slowing for a few months. July�s number picked up to 17.1% from 15.3% in June mainly due to a low base from last year; however, if we take into account the relatively high base in 2H of last year, it is hard to expect strong credit card sales growth in 2H this year. Despite credit card companies� efforts to boost demand by lowering merchant fee rates, and lifting the cash advance-related handling fee, the effect has been somewhat lukewarm.

More consumption on non-discretionary items � limited downside

Domestically, credit card sales at retailers (27.2%) and restaurants (11.4%) and for fuel purchases (10.8%) account for half of total credit card sales. The notable trend of credit sales with retailers is that credit sales at online shopping malls are almost equivalent to those of discount stores. And this segment is the major growth driver in the retailers whereas credit sales at department stores have dwindled. As a substantial portion of credit card sales is for the purchase of non-discretionary items as well as more frugal outlets, credit card sales are not expected to be too volatile even in a potential economic slowdown.

Credit sales growth picking up to 15-17%

Retail consumption so far focused on the non-discretionary, but the recent pattern of Korean consumers� trading up should be a upside risk in the near term

07 September 2010

Samsung Card (029780.KS / 029780 KS) 10

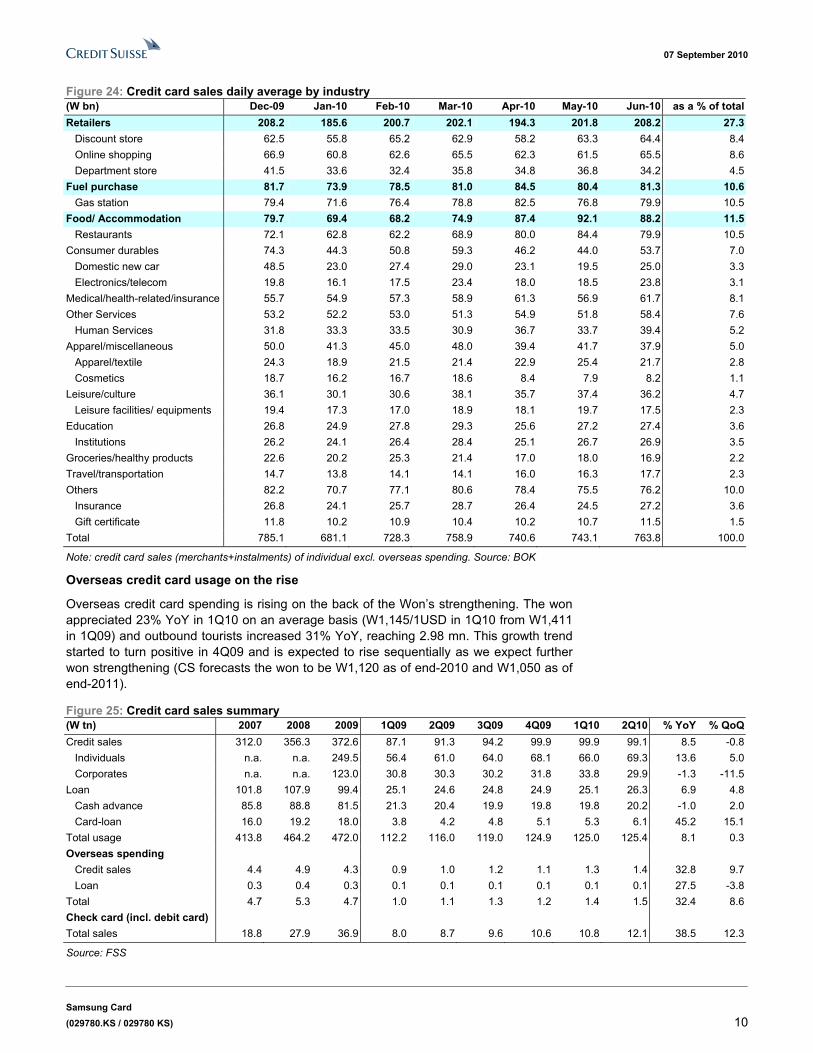

Figure 24: Credit card sales daily average by industry (W bn) Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 as a % of totalRetailers 208.2 185.6 200.7 202.1 194.3 201.8 208.2 27.3 Discount store 62.5 55.8 65.2 62.9 58.2 63.3 64.4 8.4 Online shopping 66.9 60.8 62.6 65.5 62.3 61.5 65.5 8.6 Department store 41.5 33.6 32.4 35.8 34.8 36.8 34.2 4.5Fuel purchase 81.7 73.9 78.5 81.0 84.5 80.4 81.3 10.6 Gas station 79.4 71.6 76.4 78.8 82.5 76.8 79.9 10.5Food/ Accommodation 79.7 69.4 68.2 74.9 87.4 92.1 88.2 11.5 Restaurants 72.1 62.8 62.2 68.9 80.0 84.4 79.9 10.5Consumer durables 74.3 44.3 50.8 59.3 46.2 44.0 53.7 7.0 Domestic new car 48.5 23.0 27.4 29.0 23.1 19.5 25.0 3.3 Electronics/telecom 19.8 16.1 17.5 23.4 18.0 18.5 23.8 3.1Medical/health-related/insurance 55.7 54.9 57.3 58.9 61.3 56.9 61.7 8.1Other Services 53.2 52.2 53.0 51.3 54.9 51.8 58.4 7.6 Human Services 31.8 33.3 33.5 30.9 36.7 33.7 39.4 5.2Apparel/miscellaneous 50.0 41.3 45.0 48.0 39.4 41.7 37.9 5.0 Apparel/textile 24.3 18.9 21.5 21.4 22.9 25.4 21.7 2.8 Cosmetics 18.7 16.2 16.7 18.6 8.4 7.9 8.2 1.1Leisure/culture 36.1 30.1 30.6 38.1 35.7 37.4 36.2 4.7 Leisure facilities/ equipments 19.4 17.3 17.0 18.9 18.1 19.7 17.5 2.3Education 26.8 24.9 27.8 29.3 25.6 27.2 27.4 3.6 Institutions 26.2 24.1 26.4 28.4 25.1 26.7 26.9 3.5Groceries/healthy products 22.6 20.2 25.3 21.4 17.0 18.0 16.9 2.2Travel/transportation 14.7 13.8 14.1 14.1 16.0 16.3 17.7 2.3Others 82.2 70.7 77.1 80.6 78.4 75.5 76.2 10.0 Insurance 26.8 24.1 25.7 28.7 26.4 24.5 27.2 3.6 Gift certificate 11.8 10.2 10.9 10.4 10.2 10.7 11.5 1.5Total 785.1 681.1 728.3 758.9 740.6 743.1 763.8 100.0

Note: credit card sales (merchants+instalments) of individual excl. overseas spending. Source: BOK

Overseas credit card usage on the rise

Overseas credit card spending is rising on the back of the Won�s strengthening. The won appreciated 23% YoY in 1Q10 on an average basis (W1,145/1USD in 1Q10 from W1,411 in 1Q09) and outbound tourists increased 31% YoY, reaching 2.98 mn. This growth trend started to turn positive in 4Q09 and is expected to rise sequentially as we expect further won strengthening (CS forecasts the won to be W1,120 as of end-2010 and W1,050 as of end-2011).

Figure 25: Credit card sales summary (W tn) 2007 2008 2009 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 % YoY % QoQCredit sales 312.0 356.3 372.6 87.1 91.3 94.2 99.9 99.9 99.1 8.5 -0.8 Individuals n.a. n.a. 249.5 56.4 61.0 64.0 68.1 66.0 69.3 13.6 5.0 Corporates n.a. n.a. 123.0 30.8 30.3 30.2 31.8 33.8 29.9 -1.3 -11.5Loan 101.8 107.9 99.4 25.1 24.6 24.8 24.9 25.1 26.3 6.9 4.8 Cash advance 85.8 88.8 81.5 21.3 20.4 19.9 19.8 19.8 20.2 -1.0 2.0 Card-loan 16.0 19.2 18.0 3.8 4.2 4.8 5.1 5.3 6.1 45.2 15.1Total usage 413.8 464.2 472.0 112.2 116.0 119.0 124.9 125.0 125.4 8.1 0.3Overseas spending Credit sales 4.4 4.9 4.3 0.9 1.0 1.2 1.1 1.3 1.4 32.8 9.7 Loan 0.3 0.4 0.3 0.1 0.1 0.1 0.1 0.1 0.1 27.5 -3.8Total 4.7 5.3 4.7 1.0 1.1 1.3 1.2 1.4 1.5 32.4 8.6Check card (incl. debit card) Total sales 18.8 27.9 36.9 8.0 8.7 9.6 10.6 10.8 12.1 38.5 12.3

Source: FSS

07 September 2010

Samsung Card (029780.KS / 029780 KS) 11

Figure 26: Overseas credit card spending (incl. Check card and debit card sales) 2005 2006 2007 2008 2009 1Q09 2Q09 3Q09 4Q09 1Q10Spending (US$ mn) 3,647 4,808 6,373 6,796 5,379 1,100 1,283 1,487 1,509 1681 % YoY 30.7 31.8 32.6 6.6 -20.9 -40.0 -31.5 -19.5 21.2 52.8# of persons (thou) 5,919 7,054 8,866 9,371 8,438 1,852 2,040 2,237 2,309 2,810 % YoY 18.0 19.2 25.7 5.7 -10.0 -22.7 -18.6 -9.8 16.1 51.7Spending per person (US$) 616 682 719 725 637 594 629 665 654 598 % YoY 10.8 10.6 5.5 0.9 -12.1 -22.3 -15.8 -10.7 4.4 0.7

Source: BOK

Debit card gains popularity, but not meaningful yet

Debit card transactions have steadily increased since the launch due to tax deduction benefits and aggressive marketing by credit card companies. However, in terms of sales amount, they are still not comparable to credit cards.

Figure 27: Credit card vs check card (transaction) Figure 28: Credit card vs check card (sales)

050,000

100,000150,000200,000250,000300,000350,000400,000450,000500,000

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10

(thou

)

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

(thou

)

Credit card sales (ex cl. cash adv ance) Check card sales (RHS)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10

(W b

n)

05001,0001,5002,0002,5003,0003,5004,0004,500

(W b

n)

Credit card sales (ex cl. cash adv ance) Check card sales (RHS)

Source: BOK Source: BOK

07 September 2010

Samsung Card (029780.KS / 029780 KS) 12

SSC to benefit from group restructuring We believe that it is high time to look at Samsung Card from an event angle � unlocking the value amid the unwinding of its circular ownership structure. Since Samsung Life�s IPO in May, Samsung Group should address the FRL violation case. According to the FRL, chaebol-affiliated financial companies cannot own more than a 5% stake in a non-financial affiliate. Samsung Card violates the FRL with its 25.6% stake in Everland. As such, Samsung Card should dispose of its 20.6% stake in Everland by April 2012. Separately, Samsung Card�s tax credit (effective until end-2010) might also be an incentive for Samsung Card to sell its Everland stake within this year. However, due to time constraints, it appears difficult for Samsung Card to do so within this year.

Figure 29: Samsung Card from an event angle � unlocking the value amid the unwinding of its circular ownership structure

1.8%

3.1%

4.9%

1.9%

3.0%

1.3%

4.7%

4.9%

Samsung Eng.

Samsung Fine Chemicals

Cheil Ind.

S1

Hotel Shilla

Samsung Securities

Samsung F&M

Cheil Worldwide

25.1%

Samsung Life

Samsung Elec.

Everland

Family

Samsung Card

20.8%

4.7%35.3%

26.4%

19.3%

7.5%

25.6%

Samsung Card should reduce below 5% by April 2012

Samsung Card might sell some of these stakes to utilize W1.3 tn of tax credit within 2010

Source: Company data, Credit Suisse estimates

Given that Everland is a de facto holding company for the whole of Samsung Group affiliates and Samsung Group previously had legal trouble with the transaction of unlisted affiliate shares, we envisage that Samsung Card will divest its Everland stake by listing it sometime in 2011. We expect this discussion is likely to kick off from early next year. Then, we expect the market will attempt to reflect the value of Everland as a de facto holding company in the share price of Samsung Card.

Despite all this, for a further rerating of the stock, we believe that Samsung Card should address its capital management issues. Since it is already overcapitalised, more proceeds from the sale of Everland stake might be incrementally negative to its ROE. It also needs to address corporate governance concerns that Samsung Card might use those proceeds for the purchase of irrelevant group assets.

We envisage the IPO of Everland in 2011 as part of Samsung group�s ownership restructuring 1) The recent IPO of Samsung Life has allowed the creditor banks (of Samsung Motors

(unlisted)) to cash out their long-held 35.4 mn shares in Samsung Life (given by Chairman Lee to pay off Samsung Motors� debts back in 1999). Our computation shows that the IPO price of W110,000 looks sufficient for the creditor banks to cover their original loan principal and foregone interest (due to a delay in the IPO) at an

High potential for Samsung Group to seek some sort of holding company structure over the coming years

SSC should reduce its 25.6% Everland stake below 5% by April 2012

The IPO of Everland is an effective solution, in our view

SSC should address its overcapitalisation, especially in terms of sales proceeds

07 September 2010

Samsung Card (029780.KS / 029780 KS) 13

interest rate of 6.0%. With this, the group is soon likely to resolve its long-pending dispute with the creditor banks of Samsung Motors;

2) The group has strong incentives for reforming its current circular ownership structure and moving towards some sort of holding company structure over the medium term, given the combination of Samsung Card�s regulatory need to reduce its 25.6% stake in Everland, a de facto holding company for the group, to below 5% by April 2012 and the majority shareholders� ongoing desire for better control and smooth inheritance; and

3) Several recent regulatory developments (i.e. easing restrictions on the Financial Holding Company Act, the enactment of the Insurance Holding Company Act, etc.) have collectively reduced the cost of transformation towards a holding company structure for those conglomerates which rely heavily on their financial affiliates for overall control.

To this end, we not only see high potential for the group to pursue some sort of holding company transition over the medium term, but also expect increased signs of progress over the next six to 12 months. Even if this is the case, we find that the group�s whole transition is likely to be a fairly complicated, multi-year process given the combination of a large number of sizeable affiliates involved and a complex web of cross-shareholdings between them. As such, it looks premature to exactly tell what form this potential transformation will take. But with the group likely to take increased transitional steps over the next six to 12 months, we expect the market to increasingly revisit the group�s potential holding company transition story. In our view, key questions for the shareholders of Samsung Card on this front are two-fold:

1) How much out of W1.3 tn of tax credit (which expires in December 2010) Samsung Card will take advantage of by selling its equity stake in affiliate companies.

2) How Samsung Card will deal with its equity stake in the financial affiliates, such as Samsung Fire & Marine and Samsung Securities. Will Samsung Card sell them to Samsung Life as part of the steps for the holding company transition.

3) How Samsung Card will lower its equity stake in Everland to below 5%. Also how Samsung Card will deal with the sales proceeds of its Everland stake in the mid- and long-term, especially considering its low ROE and overcapitalisation. Whether Samsung Card can use them to boost its capital efficiency through share buyback.

SSC poised to benefit from a possible Everland IPO According to our checks with management, we presume that Samsung Card cannot sell its stake in Everland within this year. This means that Samsung Card is likely to sell another affiliate stake, such as Samsung Fire & Marine Insurance (000810 KS) and Samsung Securities (016360 KS). And given the group ownership structure, we presume that Samsung Card will likely sell its financial affiliate stake to Samsung Life. And we believe that this will likely boost the value of Everland as a true holding company of the whole group. In particular, if SSC divest some of its investment equities within 2010 in order to utilise tax credit, market will likely interpret the equity sales as another progress of resolving Samsung Group�s circular ownership structure.

Figure 30 shows our projected roadmap for the group�s potential journey towards its holding company structure. Among a few plausible scenarios, we view our roadmap as one of the most logical and cost-efficient options for the group given the combination of its current shareholding structure and the type of business that each affiliate is engaged. We believe that this whole transition will essentially comprise the following two phases:

1) Phase I: the beak-up of the group�s long-held circular ownership structure between Samsung Electronics (005930 KS), Samsung Card, and Everland; and

The market is expected to interpret SSC�s divesture of the affiliate stake before end-2010 for a tax credit as the beginning of ownership restructuring

07 September 2010

Samsung Card (029780.KS / 029780 KS) 14

2) Phase II: the re-alignment of the group�s current ownership structure by several major business lines, triggering the separation of the whole group between the manufacturing and financial business segments and the creation of several sub-holding companies (i.e. financial, electronic, and etc.).

That said, we see a high chance of phase I taking place over the next 12-18 months given Samsung Card�s regulatory need to bring down its current 25.6% stake in Everland to below 5% by April, 2012. And we believe that phase I may well involve:

1) the IPO of Everland: this would establish an �undisputable� market price for Everland, leading Samsung Card to unload its Everland stakes at prevailing market prices; and

2) Samsung Card�s buy-back of the bulk of stakes held by Samsung Electronics using its excess capital: Since share buybacks from selective shareholders are not allowed, Samsung Card cannot directly buy back its stake from Samsung Electronics alone. However, the buyback in an indirect way would lead not only Samsung Electronics to eliminate its entire stakes in Samsung Card, but also for Samsung Life to become Samsung Card�s single-largest shareholder with a 40% stake.

Meanwhile, we find no strong need for the group to rush into phase II (which involves a series of potential share swaps between different affiliates and the creation of sub-holding companies to form some sort of holding company structure, including the transformation of Samsung Life as the group�s financial holding company). This, plus a heavy transition cost burden (to meet the shareholding requirement at the subsidiary level, i.e. 20% for listed subsidiaries and 30% for unlisted subsidiaries, and capital gains tax from potential share swaps), suggests that phase II may well prove to be a gradual and long-term process.

Nonetheless, the phase I itself is likely to be a meaningful share price catalyst for Samsung Card over the next six to 12 months, in our view. Timing-wise, Samsung Card is likely to dispose of some of its affiliate stake to utilise its tax credit before end-2010 and then the group is likely to initiate the IPO process of Everland from early 2011. In the meantime, we reckon that the market is likely to attempt to reflect the value of Everland as a holding company of the group in the share price of Samsung Card.

The group is likely to unravel its circular ownership web over the next 12-18 months

But further transition is likely to be a more gradual and long-term process

07 September 2010

Samsung C

ard (029780.K

S / 029780 KS)

15

Figure 31: Samsung group�s holding company transition road map

Source: Credit Suisse estimates

07 September 2010

Samsung Card (029780.KS / 029780 KS) 16

Target price of W71,000 with new emphasis on holding co. value Given that: 1) one of Samsung Card�s core assets is its 25.6% equity stake in Everland (a de facto holding company of Samsung Group); 2) Samsung Card should dispose its 20.6% stake in Everland by April 2012; and 3) the IPO of Everland, presumably sometime in 2011, is the most feasible way to dispose of the Everland stake, we believe that it is time to reflect the value of Everland stake as a de facto holding company into the Samsung Card valuation. As such, we derived our fair value estimate based on a sum-of-the-parts valuation � 1) the value of the credit card operation, 2) the value of investment assets and 3) the value of the Everland stake as a de facto holding company of Samsung Group.

Figure 32: Samsung Card � its sum-of-the-parts valuation (W bn) Equity & target multiple Value

Shareholders' equity at 4Q10E 5,811 �Other comprehensive income� at 2Q10 1,550 Shareholders' equity ex. �other comprehensive income� 4,261 Target P/B (x) 1.3 Credit card operation value 5,540

I. Operation value

Per share 45,000 �Other comprehensive income� at 2Q10 1,550 (Post-tax) MTM value of investment assets (refer to Figure 34) 278 Sub-total 1,828 Target P/B (x) 0.75 Investment asset value 1,371

II. Investment value

Per share 11,000 25.6% of Everland's BV at Dec-09 593 Revaluation gain of Everland's stake in Samsung Life (refer to Figure 36) 334 25.6% of Everland's BV (e) at Jun-10 927 Target P/B (x) - Applying multiple of SK C&C 3.0 Hold co value 2,780 Hold co value (excluding BV) 1,854

III. Hold co value of Everland

Per share 15,000 Firm value (W bn) 8,764 # of shares (mn) 123.0 SOTP value (W) 71,000 Source: Company data, Credit Suisse estimates.

■ I. Value of credit card operation: We stripped out the investment asset (booked as W1,550 bn of �other comprehensive income� as of the end of 2Q10) from the shareholders� equity. Based on our normalised ROE estimate (12%), we get our fair P/B multiple of 1.3x for the credit card operation. As such, we derived W5,540 bn or W45,000 per share for the fair value of Samsung Card�s credit card operation.

Fair value of W71,000 based on the sum of three parts: 1) the value of the credit card operation, 2) the value of investment assets, and 3) the value of a de facto holding company

07 September 2010

Samsung Card (029780.KS / 029780 KS) 17

Figure 33: SSC � ROE estimates ex. investment assets or �other comprehensive income� (%) 2007A 2008A 2009A 2010E 2011E 2012EMerchant fee rate 2.0 1.9 2.0 2.2 2.2 2.2Lending yield (based on mgd receivables) 19.3 20.0 21.3 21.7 21.7 22.0Funding cost 5.7 6.0 6.3 6.0 6.2 6.4Net interest spread 13.7 14.0 15.0 15.7 15.5 15.6Net interest margins 15.4 15.9 17.2 18.5 18.4 18.5SG&A costs / average managed receivables 11.8 11.6 11.9 13.6 13.0 12.8PPP margins 4.2 4.9 5.9 5.6 6.1 6.4LLP / average managed receivables 0.0 2.9 0.9 0.7 1.0 1.0ROA (based on mgd total assets) 3.7 1.6 4.0 4.0 3.2 3.4Leverage ratio (x) 5. 4.3 3.7 2.8 2.7 2.7ROE 19.4 7.0 14.8 11.4 8.7 9.3ROE excl. �Other comprehensive income� 24.9 8.4 17.1 14.5 11.8 12.4Card receivable / shareholders' fund (x) 3.3 3.3 2.4 2.0 2.1 2.1 Card receivable / shareholders' fund (ex. OCI) (x) 4.1 3.8 2.8 2.7 2.8 2.8 Tier 1 CAR 27.8 26.6 35.0 39.1 38.0 37.1Tier 1 CAR (ex. OCI) 22.1 23.0 30.0 28.4 28.1 27.8

Source: Company data, Credit Suisse estimates

■ II. Value of investment assets: We derived the value of investment assets by adding the MTM gain of investment assets to �Other comprehensive income� at end-1H10. The MTM gain of the available-for-sale stocks is only W9 bn as of June 2010. Since Samsung Card revalued its Everland stake in 2Q10 (mainly reflecting the [post-IPO] market value of Samsung Life held by Everland), we used the book value as of 2Q10 for the current (or fair market) value. We separately discuss about the possible valuation premium above the book value as a holding company of the group in the �III. Hold co value of Everland�. Thus, most of the MTM gain of investment assets are from: 1) 25.64% of Samsung Everland�s additional value of Samsung Life stake (W171 bn) and 2) 25.64% of Samsung Everland�s incremental land value (W165 bn). In addition, Samsung Everland is likely to see 3) the MTM gain of its 3.71% stake in recently listed �I Market Korea�. So, we reflected 25.64% of the MTM gain, or W10.3 bn, based on the closing price at the end of 2Q10. And then, we applied a 0.75x multiple, or 25% discount, as a typical holding company of the affiliate stocks in Korea.

Figure 34: Samsung Card-MTM gain of investment assets (W bn) Book value (4Q09) Current value Gain

1. MTM gain of available-for-sale stocks (Refer to below Figure 35) 2,582.4 2,591.4 9.02. 25.64% of Samsung Everland's additional value of Samsung Life stake 1) 171.33. 25.64% of Samsung Everland's 3.71% stake in I Market Korea 10.34. 25.64% of Samsung Everland�s incremental land value 2) 165.4Total gain before tax 356.1Total gain after tax 277.8Gain per share (W) 2,2591) Gap between 19.34% of Samsung Life's current shareholders' equity and Samsung Everland's current book value accrual of its 19.34% Samsung Life stake. 2) Assuming a 100% price appreciation relative to the current book value based on the 1998 appraisal value Source: Company data, Credit Suisse estimates

07 September 2010

Samsung Card (029780.KS / 029780 KS) 18

Figure 35: Samsung Card � details of available-for-sale equity investment in the group affiliates (W bn) % stake # of shares (�000) Purchase value Book value (end-2Q10) Current valueSamsung Securities 4.70 3,141.3 57.3 171.6 189.1Samsung Fire & Marine 4.85 2,297.7 90.4 449.3 482.5Hotel Shilla 1.34 525.9 4.6 13.0 11.4Cheil Worldwide 3.04 139.9 22.8 45.0 48.8Cheil Industry 4.90 2,450.0 18.3 231.3 203.8S-one 1.91 725.8 16.2 37.8 34.3Samsung Engineering 1.76 704.0 9.0 80.6 76.4Samsung Fine Chemicals 3.12 805.0 15.7 51.7 43.0Samsung Renault Motors 19.90 87.6 145.7 145.7Others 38.3 15.9 15.9Sub-total 360.4 1,241.9 1,250.9Samsung Everland 25.64 64.1 1,340.5 1,340.5Available-for-sale securities 424.5 2,582.4 2,591.4Gains before tax 9.0

Source: Company data, Credit Suisse estimates

■ III. Value of Everland stake as a de facto holding company of Samsung Group:

Before we derive the value of Everland as a de facto holding company of the group, we adjusted Everland�s BV. Basically, we calculated the book value estimate of Everland as of June 2010 by adding the revaluation gain (W334 bn) of Everland�s stake in Samsung Life to Everland�s BV as of December 2010. As a result, we derived W927 bn for 25.6% of Everland�s BV estimate as of June 2010.

Figure 36: Details of revaluation gain of Everland�s stake in Samsung Life Items Reference Amount (W bn) Samsung Life share price as of June-10 (W) (a) 103,500 Samsung Life shares held by Everland (mn) (b) 38.7 SLI market value as of Jun-10 (c) =(a)x(b) 4,004 SLI book value as of Dec-09 (d) 2,321 Revaluation gain of SLI shares (e) = (c) - (d) 1,683 (Post-tax) Revaluation gain (f) = (1-22.5%) x (e) 1,304 Samsung Card: 25.6% of (post-tax) revaluation gain 25.6% x (f) 334

Source: Company data, Credit Suisse estimates

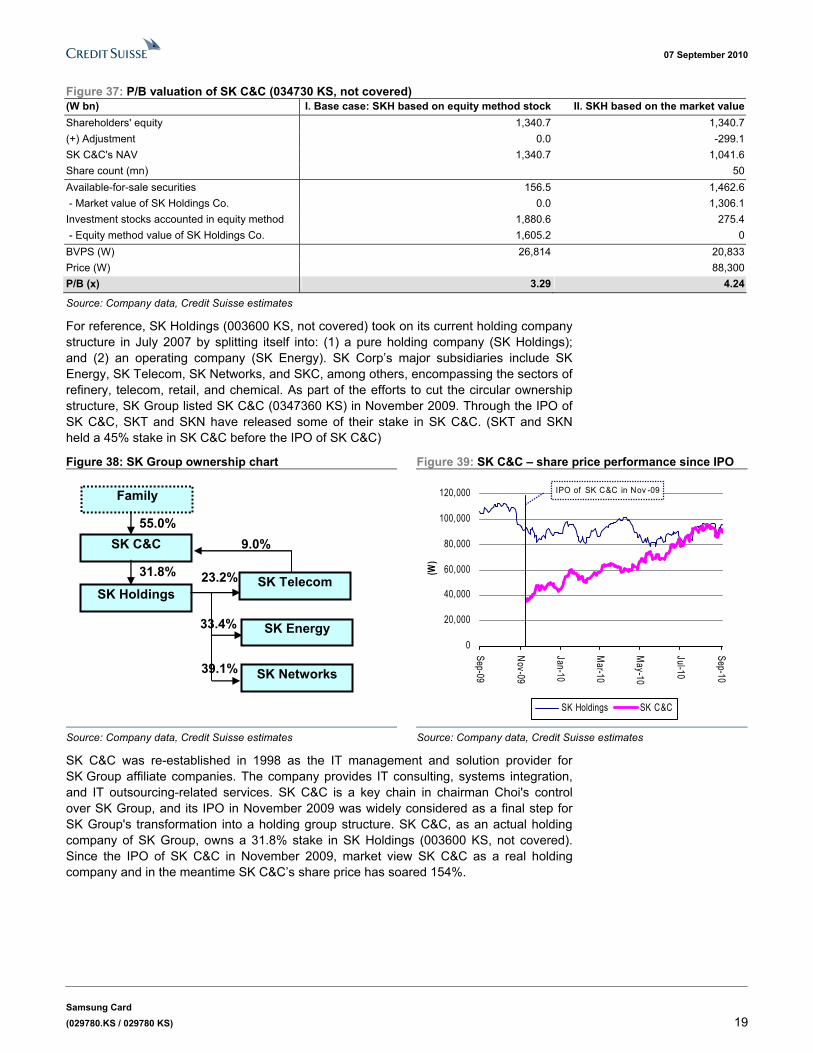

Given Samsung Card should dispose of its 20.6% stake in Everland by April 2012 and that the IPO of Everland is the most feasible option, we expect that Everland is likely to go public sometime in 2011. If this is the case, we expect that the (post-IPO) share price of Everland is likely to show a similar pattern to that of SK C&C (034730 KS, not covered). As such, we applied the P/B multiple of SK C&C�s share price to our BV estimate of Everland.

One of SK C&C�s main investment assets is its 31.8% equity stake in SK Holdings vis-a-vis Everland�s 25.6% equity stake in Samsung Life. Although SK Holdings is a listed company, SK C&C currently booked its stake under the equity method. Thus, we calculated the P/B multiple in two ways � 1) a base case assuming SKH shares, based on the equity method and 2) applying the market value of SKH shares, based on the assumption of SKH as �available for sale� securities. Since we cannot presume whether Everland is likely to book the Samsung Life stake as �available-for-sale� stock or equity-method stock, we review both. However, since SK Holdings� share price has languished since the IPO of SK C&C, the P/B multiple based on the market value might be overstated. Thus, for conservatism�s sake, we used the lower multiple between scenario I and scenario II, or around 3.0x. By applying this multiple, we derived the holding company value of the Everland stake.

Samsung Group�s holding company transition is likely to follow the case of SK Group. SK C&C�s IPO in November 2009 is an especially good comparison for Everland

07 September 2010

Samsung Card (029780.KS / 029780 KS) 19

Figure 37: P/B valuation of SK C&C (034730 KS, not covered) (W bn) I. Base case: SKH based on equity method stock II. SKH based on the market valueShareholders' equity 1,340.7 1,340.7(+) Adjustment 0.0 -299.1SK C&C's NAV 1,340.7 1,041.6Share count (mn) 50Available-for-sale securities 156.5 1,462.6 - Market value of SK Holdings Co. 0.0 1,306.1Investment stocks accounted in equity method 1,880.6 275.4 - Equity method value of SK Holdings Co. 1,605.2 0BVPS (W) 26,814 20,833Price (W) 88,300P/B (x) 3.29 4.24

Source: Company data, Credit Suisse estimates

For reference, SK Holdings (003600 KS, not covered) took on its current holding company structure in July 2007 by splitting itself into: (1) a pure holding company (SK Holdings); and (2) an operating company (SK Energy). SK Corp�s major subsidiaries include SK Energy, SK Telecom, SK Networks, and SKC, among others, encompassing the sectors of refinery, telecom, retail, and chemical. As part of the efforts to cut the circular ownership structure, SK Group listed SK C&C (0347360 KS) in November 2009. Through the IPO of SK C&C, SKT and SKN have released some of their stake in SK C&C. (SKT and SKN held a 45% stake in SK C&C before the IPO of SK C&C)

Figure 38: SK Group ownership chart Figure 39: SK C&C � share price performance since IPO

Family

SK C&C

SK HoldingsSK Telecom

SK Energy

SK Networks

55.0%

31.8% 23.2%

33.4%

39.1%

9.0%

0

20,000

40,000

60,000

80,000

100,000

120,000

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

Sep-10

(W)

SK Holdings SK C&C

IPO of SK C&C in Nov -09

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

SK C&C was re-established in 1998 as the IT management and solution provider for SK Group affiliate companies. The company provides IT consulting, systems integration, and IT outsourcing-related services. SK C&C is a key chain in chairman Choi's control over SK Group, and its IPO in November 2009 was widely considered as a final step for SK Group's transformation into a holding group structure. SK C&C, as an actual holding company of SK Group, owns a 31.8% stake in SK Holdings (003600 KS, not covered). Since the IPO of SK C&C in November 2009, market view SK C&C as a real holding company and in the meantime SK C&C�s share price has soared 154%.

07 September 2010

Samsung Card (029780.KS / 029780 KS) 20

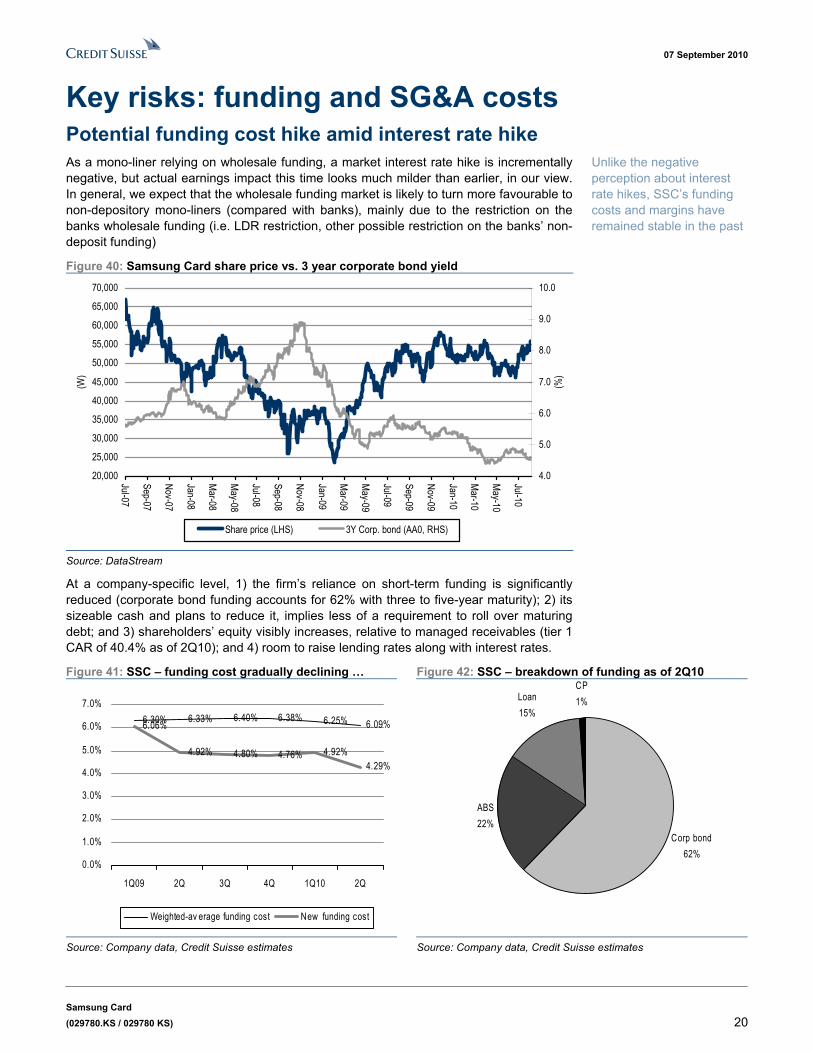

Key risks: funding and SG&A costs Potential funding cost hike amid interest rate hike As a mono-liner relying on wholesale funding, a market interest rate hike is incrementally negative, but actual earnings impact this time looks much milder than earlier, in our view. In general, we expect that the wholesale funding market is likely to turn more favourable to non-depository mono-liners (compared with banks), mainly due to the restriction on the banks wholesale funding (i.e. LDR restriction, other possible restriction on the banks� non-deposit funding)

Figure 40: Samsung Card share price vs. 3 year corporate bond yield

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

(W)

4.0

5.0

6.0

7.0

8.0

9.0

10.0

(%)

Share price (LHS) 3Y Corp. bond (AA0, RHS)

Source: DataStream

At a company-specific level, 1) the firm�s reliance on short-term funding is significantly reduced (corporate bond funding accounts for 62% with three to five-year maturity); 2) its sizeable cash and plans to reduce it, implies less of a requirement to roll over maturing debt; and 3) shareholders� equity visibly increases, relative to managed receivables (tier 1 CAR of 40.4% as of 2Q10); and 4) room to raise lending rates along with interest rates.

Figure 41: SSC � funding cost gradually declining � Figure 42: SSC � breakdown of funding as of 2Q10

6.30% 6.33% 6.40% 6.38% 6.25% 6.09%6.06%

4.92% 4.80% 4.76% 4.92%4.29%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1Q09 2Q 3Q 4Q 1Q10 2Q

Weighted-av erage funding cost New funding cost

Corp bond62%

ABS22%

Loan15%

CP1%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Unlike the negative perception about interest rate hikes, SSC�s funding costs and margins have remained stable in the past

07 September 2010

Samsung Card (029780.KS / 029780 KS) 21

Figure 43: Funding cost trend Figure 44: Net interest margin trend

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

0%

5%

10%

15%

20%

25%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

In terms of middle-line margin, NIM remains largely unchanged, hovering around the 18-19% level. However, as new funding costs drop to 4.29% in 2Q10 from 4.92% in 1Q10, management expects the average funding cost to be around 6% (versus 6.09% in 2Q10) from 3Q onwards. Separately, the company�s delinquency ratio remained stable at 2.77% in 2Q10 versus 2.72% a quarter ago, and 4.2% a year ago. And credit costs (LLP/receivables) dropped to 1.6% in 2Q10 from 2.0% a quarter ago and 1.8% a year ago.

Figure 45: PPOP margin Figure 46: ROA

0%

2%

4%

6%

8%

10%

12%

14%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1Q07 3Q 1Q08 3Q 1Q09 3Q 1Q10 3QE

Shinhan Card Samsung Card

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Potential SG&A cost hike amid rising competition There have been several signs of rising competition, such as: 1) Hana Financial Group�s credit card joint venture with SK Telecom; 2) mono-line credit card companies� increased mileage bonuses; 3) KB Bank�s plan to spin off its credit card operation sometime in 2011; and 4) KT (Korea Telecom)�s purchase of BC Card stake. Against this backdrop, Samsung Card has stepped up its promotion efforts since the beginning of this year. Samsung Card is aggressively acquiring new customers by taking advantage of its affiliate Samsung Electronics� distribution network. Although Samsung Card stepped up promotion efforts from the start of the year, the cost to income ratio YTD remains stable.

Unlike market concern about potential cost increases amid rising competition, SSC has so far maintained its disciplined cost efficiency

07 September 2010

Samsung Card (029780.KS / 029780 KS) 22

Figure 47: Samsung Card � quarterly trend of cost-income ratio

0

100

200

300

400

500

600

700

800

1Q04 4Q04 3Q05 2Q06 1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12

(W b

n)

0%10%20%30%40%50%60%70%80%90%100%

Income (LHS) Cost (LHS) Cost-income ratio (RHS)

CS forecast

Source: Company data, Credit Suisse estimates

In general, although the system�s credit sales growth is robust (15-18% YoY), our view is that the sector is rather overcrowded especially for the new entrant. Although Hana Financial Group�s new experiment on the mobile credit card so far has not received much traction in the market, overall competition might turn more heated in the mobile credit card market. The new chairman of KB Financial Group recently said it will spin off its credit card operation as a subsidiary (it is part of the bank�s operation). KB Financial Group�s management believe that KB credit cards lost market share to competitors, mainly due to the conflict of risk management and marketing promotions between the bank and credit card. Separately, he revealed his interest in a strategic alliance with KT (Korea Telecom), although he did not specifically mention the mobile credit card business, etc. So, in this case, we should wait to see how other mono-line credit card companies, such as Hyundai Card (not listed), are likely to react.

Despite all this, the recent trend basically reaffirms that concerns over an SG&A cost increase for market share gains is overdone. Credit card receivables are increasing at a healthy pace (4.1% QoQ and 12.2% YoY), while delinquency is under control. In terms of market share (based on new credit purchases), Samsung Card slightly regained its market share to 14.2% in 1H10 from 13.6% in 2009. Management revealed that it plans to maintain its market share at least above the 14% level.

07 September 2010

Samsung Card (029780.KS / 029780 KS) 23

Figure 48: Samsung Card � one-year forward P/B (W) Figure 49: Samsung Card � one-year forward P/PPP (W)

0

20,000

40,000

60,000

80,000

100,000

120,000Ju

n-07

Oct-0

7

Feb-

08

Jun-

08

Oct-0

8

Feb-

09

Jun-

09

Oct-0

9

Feb-

10

Jun-

10

0.65x

0.95x

1.25x

1.80x

2.10x

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Jun-

07

Oct-0

7

Feb-

08

Jun-

08

Oct-0

8

Feb-

09

Jun-

09

Oct-0

9

Feb-

10

Jun-

10

4.5x

8.0x

9.5x

12.0x

14.0x

Source: Datastream, company data, Credit Suisse estimates Source: Datastream, Company data, Credit Suisse estimates

07 September 2010

Samsung C

ard (029780.K

S / 029780 KS)

24

Figure 50: Samsung Card � financial statement summary (W bn) 2008 2009 2010E 2011E 2012E 2008 2009 2010E 2011E 2012EProfit & loss Key ratio (%) Interest revenue 1,766 1,592 1,405 1,598 1,841 Merchant fee rate 1.88 1.98 2.18 2.21 2.21 Merchant fees 705 770 957 1,035 1,108 Lending yield (based on mgd receiv.) 20.0 21.3 21.7 21.7 22.0Total interest revenue 2,471 2,362 2,361 2,633 2,949 Funding cost 6.0 6.3 6.0 6.2 6.4Interest expenses 499 453 351 409 462 Net interest spread 14.0 15.0 15.7 15.5 15.6Net interest income 1,972 1,909 2,010 2,224 2,487 Net interest margins (%) 15.9 17.2 18.5 18.4 18.5Non-interest income 79 70 82 88 94 SG&A costs / avg mgd receivables 11.6 11.9 13.6 13.0 12.8Gross revenues 2,051 1,979 2,092 2,312 2,582 PPP margins 4.9 5.9 5.6 6.1 6.4SG&A costs 1,442 1,320 1,484 1,570 1,722 LLP / avg mgd receivables 2.9 0.9 0.7 1.0 1.0Pre-provision profit 609 659 608 742 860 ROA (based on mgd total assets) 1.6 4.0 4.0 3.2 3.4Loan-loss provision 354 104 81 118 135 ROE 7.0 14.8 11.4 8.7 9.3Non-operating gains 74 136 56 45 45 Equity-to-mgd receivables ratio (%) 30.2 42.0 50.1 48.8 47.5Net profit before tax 329 691 583 668 769 Credit card usage Tax 71 87 0 147 169 Card sales 37,434 38,931 43,865 46,936 50,221Net profit after tax 258 604 583 521 600 Cash advance 8,981 8,726 8,590 8,481 8,374# of common shares (mn) 123 123 123 123 123 Total usage 46,415 47,657 52,455 55,417 58,595Managed receivables Cash advance as a % of total usage 19.3 18.3 16.4 15.3 14.3Normal receivables 11,245 9,973 11,146 12,366 13,723 Asset quality (%) Over 1M delinquent loans 556 224 188 296 417 NPL ratio 3.7 1.7 1.4 1.4 1.2Re-aged loans not/below 1M delinquent 689 333 272 179 117 Precautionary loan ratio 5.9 3.8 3.2 2.9 2.6Managed receivables 12,490 10,530 11,606 12,841 14,257 New NPLs of avg. receivables 1.5 0.4 1.3 1.7 1.6Average managed IEA 12,230 11,344 10,741 11,941 13,233 Write-offs / average receivables 2.4 3.1 1.6 1.6 1.6Per share data LLP as % of avg credits 2.9 0.9 0.7 1.0 1.0EPS (W) 2,134 4,911 4,741 4,240 4,881 New over 1M / average receivables -0.5 0.7 0.7 1.7 2.0BVPS (W) 30,653 35,997 47,263 50,931 55,079 'True' delinquent loan ratio 10.0 5.3 4.0 3.7 3.7DPS (W) 600 900 1,100 1,100 1,200 Reserves / True > 1M 52.7 61.2 74.9 78.4 74.1Source: Company data, Credit Suisse estimates

07 September 2010

Samsung Card (029780.KS / 029780 KS) 25

As of close of business 6 September 2010, Credit Suisse Securities (Europe) Limited, Seoul Branch performs the role of liquidity provider on the warrants of which underlying asset is Samsung Electronics/ Samsung Securities/ Samsung F&M/ Samsung Eng./ Samsung SDI/ SEMCO/ Samsung Techwin/ Samsung C&T/ Samsung Heavy/ SK Corp/ SK Telecom/ SK Energy/ KB Financial/ Shinhan FG/ Woori FH/ Hana FG/ Hynix Semi and holds 35,307,480/ 16,642,100/ 13,454,310/ 3,399,280/ 16,286,520/ 17,782,390/ 13,066,710/ 23,473,460/ 13,449,370/ 3,396,040/ 46,966,840/ 20,323,500/ 16,393,280/ 16,602,270/ 15,037,870/ 6,703,700/ 18,490,210 of warrants concerned. These may be covered warrants that constitute part of a hedged position.

Credit Suisse is acting as financial advisor to the Share Management Council on the potential sale of their collective stake in Hynix Semiconductor. The Share Management Council is composed of the following companies: Korea Exchange Bank; Woori Bank; Korea Development Bank; Shinhan Bank; Resolution & Finance Corp; National Agricultural Cooperative Federation; SH Asset Management; Daewoo Securities; and, Woori Investment and Securities.

07 September 2010

Samsung Card (029780.KS / 029780 KS) 26

Companies Mentioned (Price as of 07 Sep 10) Busan Bank (005280.KS, W12,450, NEUTRAL [V], TP W14,500) Cheil Industries Inc (001300.KS, W103,000, NEUTRAL, TP W91,000) Cheil Worldwide (030000.KS, W13,200, OUTPERFORM, TP W15,000) Daegu Bank (005270.KS, W13,800, NEUTRAL, TP W17,000) Hana Financial Group (086790.KS, W31,500, OUTPERFORM [V], TP W44,000) Hotel Shilla Co Ltd (008770.KS, W29,200, NOT RATED) Hynix Semiconductor (000660.KS, W21,500, RESTRICTED [V]) Industrial Bank of Korea (024110.KS, W14,300, OUTPERFORM [V], TP W20,000) KB Financial Group (105560.KS, W48,800, OUTPERFORM [V], TP W62,000) S1 Corporation (012750.KS, W59,200, NEUTRAL, TP W60,000) Samsung C&T Corporation (000830.KS, W55,900, NEUTRAL [V], TP W62,000) Samsung Card (029780.KS, W53,300, OUTPERFORM, TP W71,000) Samsung Electro-Mechanics (009150.KS, W120,500, NEUTRAL, TP W141,500) Samsung Electronics (005930.KS, W788,000, OUTPERFORM, TP W940,000) Samsung Engineering Co Ltd (028050.KS, W129,500, OUTPERFORM [V], TP W150,000) Samsung Fine Chemicals Co. Ltd (004000.KS, W66,100, NOT RATED) Samsung Fire & Marine (000810.KS, W195,000, OUTPERFORM, TP W245,000) Samsung Heavy Industries (010140.KS, W26,650, NEUTRAL [V], TP W22,000) Samsung Life Insurance (032830.KS, W113,500, NEUTRAL [V], TP W118,000) Samsung SDI (006400.KS, W174,500, UNDERPERFORM, TP W130,000) Samsung Securities (016360.KS, W59,800, UNDERPERFORM, TP W47,000) Samsung Techwin Co. Ltd (012450.KS, W114,500, NOT RATED) Shinhan Financial Group (055550.KS, W43,150, OUTPERFORM, TP W62,000) SK C&C (034730.KS, W88,100, NOT RATED) SK Energy (096770.KS, W127,000, OUTPERFORM [V], TP W181,000) SK Holdings (003600.KS, W94,800, NOT RATED) SK Networks (001740.KS, W10,100, NOT RATED) SK Telecom (017670.KS, W163,500, NEUTRAL, TP W183,000) Woori Finance Holdings (053000.KS, W13,300, NEUTRAL [V], TP W16,000)

Disclosure Appendix Important Global Disclosures Sokmo Yun, Soyeon Hong & Seok Yun, CFA, CA each certify, with respect to the companies or securities that he or she analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. See the Companies Mentioned section for full company names. 3-Year Price, Target Price and Rating Change History Chart for 005280.KS 005280.KS Closing

Price Target

Price

Initiation/ Date (W) (W) Rating Assumption 11-Apr-08 13450 17000 O X 29-Sep-08 10700 14900 20-Oct-08 8200 10000 12-Dec-08 6250 7000 27-Apr-09 6900 N 18-Jun-09 9280 10000 O 24-Jul-09 10900 12200 22-Oct-09 13900 17000 15-Jun-10 11300 13000 N X 30-Jul-10 12750 14500

17000

14900

10000

7000

10000

12200

17000

13000

14500

11-Apr-08 15-Jun-10

N

O

N

O

4985

6985

8985

10985

12985

14985

16985

8-Sep-07

8-Nov-07

8-Jan-

08

8-Mar-0

8

8-May-08

8-Jul-08

8-Sep-08

8-Nov-0

8

8-Jan-0

9

8-Mar-09

8-May-

09

8-Jul-09

8-Sep-09

8-Nov-09

8-Jan-10

8-Mar-10

8-May-

10

8-Jul-1

0

Closing Price Target Price Initiation/Assumption Rating

W

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

07 September 2010

Samsung Card (029780.KS / 029780 KS) 27

3-Year Price, Target Price and Rating Change History Chart for 001300.KS 001300.KS Closing

Price Target

Price

Initiation/ Date (W) (W) Rating Assumption 14-Feb-08 39000 47000 22-Jul-08 50400 49500 9-Feb-09 36500 36500 29-Jul-09 48300 45000 3-Feb-10 56800 51500 6-May-10 85000 72000 30-Jul-10 90800 91000

47000 49500

36500

4500051500

72000

91000

32550

42550

52550

62550

72550

82550

92550

102550

8-Sep-07

8-Nov-07

8-Jan-

08

8-Mar-0

8

8-May-08

8-Jul-08

8-Sep-08

8-Nov-0

8

8-Jan-0

9

8-Mar-09

8-May-

09

8-Jul-09

8-Sep-09

8-Nov-09

8-Jan-10

8-Mar-10

8-May-

10

8-Jul-1

0

Closing Price Target Price Initiation/Assumption Rating

W

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

3-Year Price, Target Price and Rating Change History Chart for 030000.KS 030000.KS Closing

Price Target

Price

Initiation/ Date (W) (W) Rating Assumption 17-Jan-08 10280 11200 25-Apr-08 10660 11320 15-Jul-08 8880 9400 24-Oct-08 7100 8400 7-Jul-09 9600 12000 O 23-Oct-09 12720 13200 N 26-Feb-10 12120 13520 31-May-10 12600 15000 O

11200 11320

94008400

12000

13200 13520

15000

ON

O

5360

6360

7360

8360

9360

10360

11360

12360

13360

14360

8-Sep-07

8-Nov-07

8-Jan-

08

8-Mar-0

8

8-May-08

8-Jul-08

8-Sep-08

8-Nov-0

8

8-Jan-0

9

8-Mar-09

8-May-

09

8-Jul-09

8-Sep-09

8-Nov-09

8-Jan-10

8-Mar-10

8-May-

10

8-Jul-1

0

Closing Price Target Price Initiation/Assumption Rating

W

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

3-Year Price, Target Price and Rating Change History Chart for 005270.KS 005270.KS Closing

Price Target

Price

Initiation/ Date (W) (W) Rating Assumption 11-Apr-08 13950 18000 O X 29-Sep-08 10750 15700 20-Oct-08 7800 10500 12-Dec-08 6980 8000 28-Apr-09 8540 N 18-Jun-09 11600 12800 O 29-Jul-09 13700 14900 29-Oct-09 15950 20100 15-Jun-10 14300 15600 N X 2-Aug-10 15150 17000

18000

15700

10500

8000

12800

14900

20100

1560017000

11-Apr-08 15-Jun-10

N

O

N

O

5500

7500

9500

11500

13500

15500

17500

19500

8-Sep-07

8-Nov-07

8-Jan-

08

8-Mar-0

8

8-May-08

8-Jul-08

8-Sep-08

8-Nov-0

8

8-Jan-0

9

8-Mar-09

8-May-

09

8-Jul-09

8-Sep-09

8-Nov-09

8-Jan-10

8-Mar-10

8-May-

10

8-Jul-1

0