Sampo Group 4 MARKET POSITION STRATEGY INVESTMENT ASSETS RETURN TARGET 21.2% • The largest...

50

Sampo Group Debt Investor Presentation Prepared May 13, 2013 Figures March 31, 2013 www.sampo.com/debtpresentation

Transcript of Sampo Group 4 MARKET POSITION STRATEGY INVESTMENT ASSETS RETURN TARGET 21.2% • The largest...

Sampo Group Debt Investor Presentation Prepared May 13, 2013 Figures March 31, 2013

www.sampo.com/debtpresentation

Disclaimer This presentation may contain forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Sampo believes that the expectations reflected in such forward looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors.

Important factors that may cause such a difference for Sampo include, but are not limited to: (i) the macroeconomic development, (ii) change in the competitive climate and (iii) developments in capital markets.

This presentation does not imply that Sampo has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.

14/05/2013

2

Sampo Group Basic Facts

Nordic Financial Group with Strong Brands

14/05/2013

4

MARKET POSITION

STRATEGY

INVESTMENT ASSETS

RETURN TARGET

21.2%

• The largest Pan-Nordic Financial Services group

• Profit oriented • Cost, Risk & Capital

~ EUR 663bn B/S

• Top league ROE • RoE 15% in a normalised economic environment

• Unit-linked products & Wealth Management

• Leading life & pension insurer in Finland with Baltic operations

~ EUR 5.6bn

• RoE 17.5%

• The largest Pan-Nordic P&C insurer

• Underwriting focus • Pan-Nordic synergies

~ EUR 12bn

• RoE 17.5% • CoR 89-92% (2013) • CoR < 95% (long-term)

> 26%

100% 100%

• Long-term Investor • Manager of Capital Structure & Liquidity • Listed Company Sampo Plc

37 841

21 940

21 855

20 699

17 987

17 901

17 728

14 125

5 942

5 563

4 240

4 084

2 682

2 242

1 598

482

0 10000 20000 30000 40000

Nordea Handelsbanken

Swedbank DnB

Sampo SEB

Investor Danske Bank

Gjensidige Industrivärden

Pohjola Tryg

Topdanmark Jyske

Storebrand Alm.Brand

Largest Nordic Financial with Insurance Focus

5

Source: ReutersEcoWin

>26%

>21%

Solidium*,14.16%

Varma Mutual Pension, 8.52%

Ilmarinen Mutual Pension, 0.86%

Björn Wahlroos, 2.1%

Kaleva Mutual Insurance, 0.95%

Other domestic owners, 18.93%

Foreign and nominee registered owners, 54.48%

Ownership structure April 30, 2013

*100 % owned by the Republic of Finland

Market cap May 10, 2013, EURm

14/05/2013

• If generated EUR 204m (198) in pre-tax profits • Excellent combined ratio of 90.9% (91.7%)

– Risk ratio 67.7% (69.0%) – Cost ratio 23.2% (22.7%) – Expense ratio 17.0% (16.4%)

• Resilient business model over the cycle

If P&C ― Well-diversified and Profitable Pan-Nordic Non-life Insurer

• If P&C provides insurance solutions and services in Finland, Sweden, Denmark, Norway, Baltics (and Russia)

for corporates and private persons

• Major Lines of Business - motor - workers´ compensation - liability - accident - property - cargo

Well-established Insurance Subsidiaries

• Mandatum Life is a leading life and pension insurer in Finland • Mandatum has a strong market position in Finland

with ca. 20% of the market • Mandatum contributed with EUR 36m (33) in pre-tax profit to the Group

Mandatum Life ― Leading Finnish Life and Wealth Management Service Provider

• Provides comprehensive Wealth Management & Life insurance solutions in Finland and Baltics for corporates and private persons

• Services provided - pensions & savings - wealth management - reward commitment - risk insurance

14/05/2013

6

Nordea Profitable & The Most Diversified Nordic Bank

895

978

932

1 0

78

885

883

847

781

833

818

832

592

878

730

960

1 0

71

1 0

03

949

566

1 0

29

1 0

37

1 0

99

922

1 0

59

1 0

60

21

36

89

320 35

6

425

358

347

261

245

207 16

6

242

118

112

263

218 21

7

254 24

4

199

-13 -28 -13 -6

171

-300

0

300

600

900

1 200

1 500

1Q07

2Q

07

3Q07

4Q

07

1Q08

2Q

08

3Q08

4Q

08

1Q09

2Q

09

3Q09

4Q

09

1Q10

2Q

10

3Q10

4Q

10

1Q11

2Q

11

3Q11

4Q

11

1Q12

2Q

12

3Q12

4Q

12

Q113

EURm Restructuring provision Write backs Loan losses Operating profit

14/05/2013

7

Group Strategy: Value Creation in Nordic Financials

14/05/2013

8

LONG TERM VALUE CREATION

Value creation through investments in Nordic financials based on knowledge of Nordic markets, Nordic financial institutions & Nordic people. Commitment to the long-term development of affiliated companies.

OPERATIONAL EXCELLENCE IN SUBSIDIARIES

Subsidiary companies have focus on continuous development of services. Economics of scale Pan-Nordic diversification & operational excellence facilitate low volatility.

CONSERVATIVE PARENT WITH PROFIT FOCUS

Conservative capital structure, low leverage and strong liquidity. Parent company steers affiliated companies through Boards by setting (in Nordea by contributing to) strategies, guiding principles and ROE-targets.

GROUP LEVEL PORTFOLIO BENEFITS

Profitable companies, mostly with lowest volatility in the peer group. Profits of affiliated companies have low correlation creating diversification benefits at the group level.

LONG-TERM VALUE FOR SHAREHOLDERS & BONDHOLDERS

If P&C A/A2 Stable

Expense Ratios 2011 (2012)

Largest Nordic P&C Insurer with Synergies

10

Norway 2012 GWP EUR 6.7bn Gjensidige 25% If 25% Tryg 15% Sparebank 1 10%

Denmark 2011 GWP EUR 5.9bn Tryg 21% Topdanmark 18% Codan (RSA) 13% Alm. Brand 10% If 6%

Finland 2012 GWP EUR 4.1bn Pohjola 29% LähiTapiola 27% If 26% Fennia 10%

Sweden 2012 GWP EUR 7.5bn LF 30% If 19% RSA (T-H) 16% Folksam 15% Baltics Q3/2012

GWP ~EUR 1bn RSA 22% If 14% BTA 12% Ergo 14% Gjensidige 8%

Nordic Market shares Total GWP EUR 22bn (-11) Market Shares by Country

* Peer group excl. If 2012, other 2011

If 18 %

Topdanmark 5 %

Tryg 12 %

Gjensidige 9 % RSA

10 %

LF 9 %

Pohjola 5 %

Other 32 %

14/05/2013

17

17

28

28

28

28

28

32

IF Nordic peer group*

Zürich Generali

AXA RSA

Allianz Aviva

Nordic P&C Insurance Market

11

CONSOLIDATED MARKET

LOW EXPENSE RATIOS

The Internet continues to grow in importance as both a distribution and a service channel in the Nordic insurance market. Also, distribution via partnerships with banks and car-dealers etc. are increasingly important channels, in addition to traditional distribution.

GOOD PROFITABILITY

Good profitability since the beginning of 2000. After the last year(s) intense competition and a few years of weather related claims and decreasing profitability for some competitors, profitability has improved again in 2012. Low interest rate environment has made the Industry focus on profitability in the insurance operations.

Renewal rates are around 80-90%.

LOYAL CLIENTS

DISTRIBUTION

The market is characterized by low expense ratios of less than 20% in average compared to the European companies with expense ratios approx 10%-points higher.

The four largest companies account for 77-81% of the markets in Norway, Finland and Sweden. In Denmark the market is less consolidated.

14/05/2013 14/05/2013

By Business Area

Norway; 620

Sweden; 456

Finland ; 501

Denmark; 159

Baltic; 32

By Country

Private; 73

Commercial; 32

Industrial; 11

Baltic; 2

Technical Results, EUR 122m

Norway; 55

Sweden; 38

Finland ; 16

Denmark; 7 Baltic; 2

Gross Written Premiums, EUR 1,775m

By Business Area By Country

Sound Underwriting is Basis for Strong Result

14/05/2013

12

Private; 673

Commercial; 729

Industrial; 334

Baltic; 32

If - Total If Sweden If Norway If Finland If Denmark

Well-diversified Nordic P&C Insurer

14/05/2013

13

Geographical Diversification in CR

Combined Ratio - If P&C and Nordic Peers

Combined Ratio Development

60.0%65.0%70.0%75.0%80.0%85.0%90.0%95.0%

100.0%

2009 MA -09 2010 MA -10 2011 MA -11

IF,CR% Nordic Market Average,CR%

2.5%

5.4%

5.4%

5.8%

5.3%

Standard deviation

74,3 67,0 66,2 65,9 66,9 68,1 68,0 69,1 68,4 65,9 69,0 67,7

26,6 25,6 24,3 24,0 23,7 23,7 24,1 23,7 23,5 23,0 22,7 23,2

100,9 92,6 90,5 89,9 90,6 91,8 92,1 92,8 92,0 88,9 91,7 90,9

0

20

40

60

80

100 %

Risk ratio Cost ratio Target CR

Strong & Stable Annual Profit Development

800 730

534 549 644

707 636

864

-267

1 127

943

308

978

-400

-200

0

200

400

600

800

1 000

1 200

2005 2006 2007 2008 2009 2010 2011 2012

Profit before tax Comprehensive income

14/05/2013

14

EURm Q1/2013 Q1/2012 Profit before taxes 204 198 Compr. Income 279 328

Seasonality in Quarterly Results and C/R

Average Quarterly C/R Q4 Q3 Q2 Q1 2005-2012 ,% 90.4 89.7 89.9 94.5

14/05/2013

EURm Q1/13 Q4/12 Q3/12 Q2/12 Q1/12 Q4/11 Q3/11 Q2/11 Q1/11

Premiums earned 1,115 1,121 1,121 1,054 1,066 1,045 1,029 1,017 1,003

Claims incurred -824 -801 -809 -729 -802 -759 -771 -752 -777

Operating expenses -190 -198 -189 -177 -175 -184 -178 -174 -170

Other technical income and expenses 1 0 -1 1 2 0 1 1 2

Allocated investment return transferred from the non-technical account 20 14 21 25 29 21 26 36 42

Technical result 122 136 143 175 120 124 106 128 100

Investment result 102 84 93 107 113 78 -23 119 178

Allocated investment return transferred to the non-technical account -34 -27 -35 -40 -44 -35 -39 -50 -57

Other income and expenses 14 11 7 12 9 4 0 3 0

Operating result 204 205 208 254 198 171 43 200 221

Risk ratio, % 67.7 65.5 66.2 62.9 69.0 66.2 68.9 67.8 71.0

Combined ratio, % 90.9 89.1 89.0 85.9 91.7 90.2 92.3 91.1 94.4

15

Conservative Investment Portfolio

• Duration 1.1 years • Average Maturity 2.3 years • Fixed Income Running Yield 3.4 %

Mark-to-Market Investment Return Investment Allocation of Total EUR 12.0bn

4,3% 5,8%

4,4% 2,6%

-3,1%

12,4%

7,4%

1,8%

6,1%

1,4%

-4 %

-2 %

1 %

4 %

6 %

9 %

11 %

14 % Money Market

7%

Long-term fixed

income 81%

Equities 11%

Real Estate 1%

14/05/2013

16

If ’s Financial Strength Rating History If P&C Insurance Ltd (Sweden), If P&C Insurance Company Ltd (Finland)

The Sampo Group’s P&C insurance companies became part of If January 2002.

AA-/Aa3

A+/A1

A/A2

A-/A3

BBB+/Baa1

BBB/Baa2

Poss

ible

dow

ngra

de Ja

n 03

Moody´s S&P

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Stab

le F

eb 0

2

Neg

ativ

e Au

g 02

Stab

le A

pr 0

3

Poss

ible

upg

rade

Feb

04

Stab

le M

ay 0

4

Posi

tive M

ay 0

6

Stab

le N

ov 0

8

A- F

eb 0

2

Neg

ativ

e Ju

l 03

Stab

le A

ug 0

3

Wat

ch n

eg F

eb 0

4 St

able

Apr

04

Stab

le S

ep 0

4

Stab

le O

ct 0

5

14/05/2013

17

Mandatum Life

Finnish Life Insurer with Asset Management Focus

19

Client Segment

Underlying Market

Critical Success Factors Sales & Client Services

Corporates Employee Benefit Expertise in Incentive-, Pension- and Life Risk Solutions, Expertise in Asset Management, Management of Client Relationship

Mandatum Life

HNWI Wealth Management

Professional Wealth Management, Management of Client Relationship

Mandatum Life

Retail Clients Bankassurance Distribution Power Danske Bank

14/05/2013

Premiums Written*, total EUR 264m Insurance Savings, total EUR 7,876m

*) Direct insurance

92

28 96

6 29

12

1

Unit-linked life Unit-linked pension Unit-linked capital redemption Unit-linked Baltic Other life Other pension Other capital redemption Other Baltic

1 375

1 321

1 213

137

248

3 560

5 18

Mandatum Life Business Volumes

U-L EUR 4,045m

With-Profit EUR 3,831m

U-L EUR 222m

With-Profit EUR 42m

Focus area

4 652 4 626 4 738 4 695 4 621 4 487 4 431 4 410 4 249 4 071 4 044

607 884 1 262 1 752 2 071 1 637 2 359 3 124 3 054 3 833 4 050

0

2 000

4 000

6 000

8 000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Q1/2013 Guaranteed interest rates Unit-linked

14/05/2013

20

Technical Reserves, EUR 8,094m

EURm

17,9 19,5 20,4 19,8 19,3

24,8 22,0

24,9 24,5

18,2

25,5

20,8

25,2 22,4 21,5

27,9 28,2 26,8 26,2

18,9

0

5

10

15

20

25

30 %

All products

Unit-linked

Strong Market Position

14/05/2013

21

Market Share in Finland

30.4%

Group Pension

18.9%

Unit-Linked

33.7%

Corporates

15.3 %

Private Customers

Market Shares of Premiums Written

Finnish with-profit Life Insurance Market

14/05/2013

22

PRINCIPLE OF FAIRNESS

There is no exact rule on profit sharing (e.g. 90%/10%). In the current markets, the principle is reflected in policyholders´ reasonable expectations for total accrual, which is average annual yield of Finnish government bonds over time.

SMOOTHENED BONUSES AND DIVIDENDS OVER TIME

When company decides on yearly bonuses and dividends it takes into account (i) policy holders´ reasonable expectations, (ii) realized investment returns and current solvency and (iii) uncertainty about the future market environment => Bonuses and dividends can be smoothened over time.

BETTER POSITION FOR RISK TAKING BENEFITS STAKEHOLDERS

Finnish Profit sharing mechanism facilitates and incentives for active investment strategies and risk taking. Profit sharing mechanism have benefited both policyholders and shareholders over the years.

Profit Development

295 342

140 121 142 137 136

286

80

-378

495

332

-115

286

-500

-250

0

250

500

2006 2007 2008 2009 2010 2011 2012

EURm

Profit before taxes Comprehensive income

14/05/2013

23

Q1/2013 Q1/2012 Profit before taxes 36 33 Compr. Income 66 172

Profit by Components

14/05/2013

24

EURm 1-3/2013 1-3/2012 Net investment income 188.8 271.3

- Transferred to expense result -4.8 -4.4 - Return on unit-linked policies -109.2 -185.0 - Return on with-profit policies* -46.1 -48.3

INVESTMENT RESULT 28.7 33.7 EXPENSE RESULT** 0.2 -0.2 RISK RESULT 6.7 4.5 OTHERS*** 0 -4.9 PROFIT BEFORE TAXES 35.6 33.0 Change in the market value of investments 50.1 192.6 PROFIT AT MARKET VALUES 85.7 225.6

* Includes guaranteed interest, bonuses and change in the reserves of the above items ** Result of unit-linked business EURm 1.6 *** Includes operating expenses for Innova Pension and Personnel Fund Services

Total expense ratio, % 119.1 112.7(2012) Incl. kick backs, % 98.0 93.4 (2012)

Mandatum Life, Group Life expense ratio

Absolute Return Investment Portfolio

14/05/2013

25

• Duration 1.7 years • Average Maturity 2.0 years • Fixed Income Running Yield 4.4%

Mark-to-Market Investment Returns Investment Allocation of Total EUR 5.6bn

8,3%

12,0% 9,7%

5,0%

-7,8%

16,8%

11,1%

-1,4%

9,4%

2,3%

-10 %

-5 %

0 %

5 %

10 %

15 %

20 %

Money Market 14%

Long-term fixed income

44%

Equities 28%

Private Equity 4%

Real Estate 3%

Other 6%

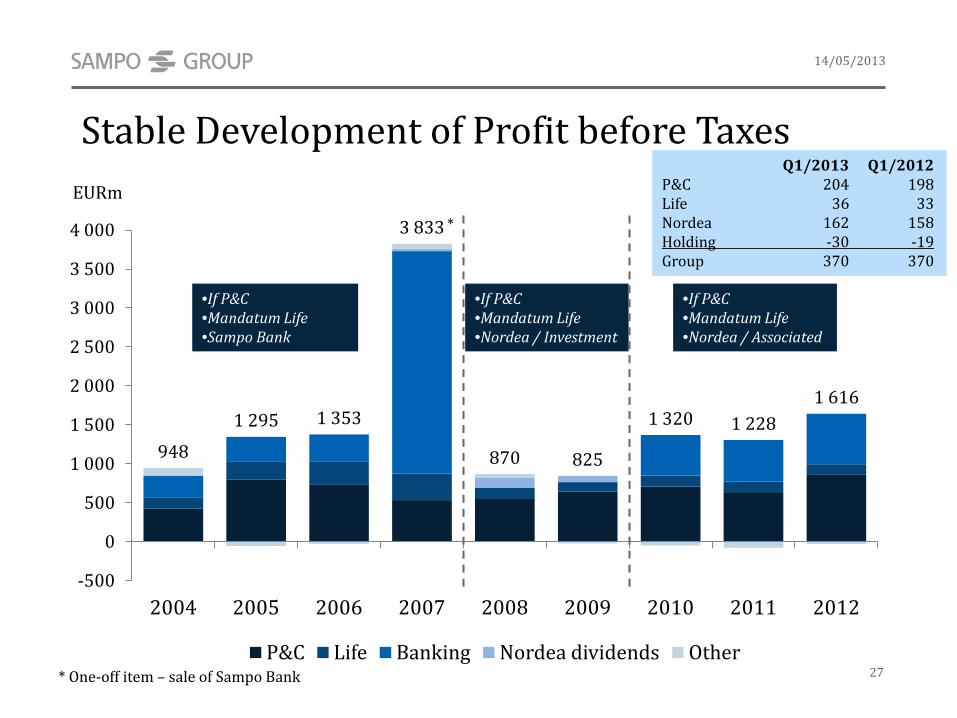

Sampo Group Results, Capitalisation and Investments

948

1 295 1 353

3 833

870 825

1 320 1 228 1 616

-500

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2004 2005 2006 2007 2008 2009 2010 2011 2012

P&C Life Banking Nordea dividends Other

14/05/2013

27

Stable Development of Profit before Taxes

* One-off item – sale of Sampo Bank

EURm *

•If P&C •Mandatum Life •Sampo Bank

•If P&C •Mandatum Life •Nordea / Investment

•If P&C •Mandatum Life •Nordea / Associated

Q1/2013 Q1/2012 P&C 204 198 Life 36 33 Nordea 162 158 Holding -30 -19 Group 370 370

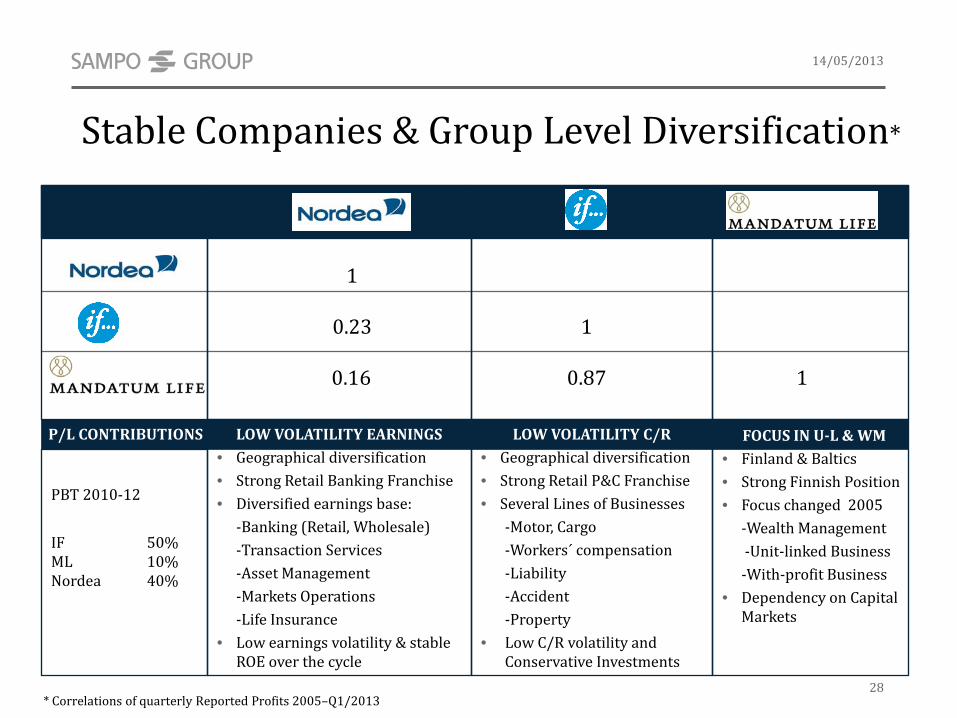

Stable Companies & Group Level Diversification*

14/05/2013

28

LOW VOLATILITY EARNINGS • Geographical diversification • Strong Retail Banking Franchise • Diversified earnings base: -Banking (Retail, Wholesale) -Transaction Services -Asset Management -Markets Operations -Life Insurance • Low earnings volatility & stable

ROE over the cycle

LOW VOLATILITY C/R • Geographical diversification • Strong Retail P&C Franchise • Several Lines of Businesses -Motor, Cargo -Workers´ compensation -Liability -Accident -Property • Low C/R volatility and

Conservative Investments

FOCUS IN U-L & WM • Finland & Baltics • Strong Finnish Position • Focus changed 2005 -Wealth Management -Unit-linked Business -With-profit Business • Dependency on Capital

Markets

1 0.23 1 0.16 0.87 1

* Correlations of quarterly Reported Profits 2005–Q1/2013

PBT 2010-12

IF 50% ML 10% Nordea 40%

P/L CONTRIBUTIONS

1 645

1 126

3 450

-832

5 389

8 511

876 -37

398

-1 000

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

P&C Life Nordea Diversific. Group EC Group ASC Regulatory minimum

Strong Group Capitalization

14/05/2013

29

• Economic Capital need (EC) is measured at 99.5% conf. level

• By nature SII framework is similar to EC techniques used by Sampo

• EC models are developed to be in line with regulatory requirements for Internal models

• Current Ratio of Adjusted Solvency Capital and EC is 164% (8,872/5,389)

EURm

Nordea 3,698

Internal Treatment ≈ S II

• Minimum requirement (4,841) is sum of IF, ML (SI) and Nordea (BII) with transition rules

• Additive figure does not include diversification effects and Nordea´s requirement is calculated at 99.90% conf.level

• Current Ratio 176% (8,511/4,841)

Regulatory Treatment = S I

Sampo plc 41

*) Liability side adjustments which equal discount effect less risk margin **) Finnish equalisation provisions

*

**

Life 226

8,872

4,841

Sampo Group Capital Base above Capital Needs

14/05/2013

30

1 89

5

1 97

6 2 65

7 3 27

9

3 78

3

4 02

4

4 13

1

4 18

9

4 28

1

4 28

1

4 22

2

4 39

4

4 37

4

4 62

9

4 61

9

4 67

8

4 56

0 5 38

9

2 17

5

2 29

4 3 05

4 3 73

8

4 24

5

4 60

0

4 72

2

4 79

9

4 95

4

4 94

7

4 85

8

5 07

6

5 01

5

5 26

2

5 23

4

5 31

7

5 17

9 6 22

1

4 02

3

4 10

9

6 40

1

7 66

6

7 07

6

7 56

5

7 16

8

7 27

9

8 52

1

8 43

2

8 12

0

6 83

0

7 26

2 7 87

5

7 58

1

8 07

5

8 19

7 8 87

2

0 1 000 2 000 3 000 4 000 5 000 6 000 7 000 8 000 9 000

10 000

EC,Diversified EC,Undiversified ASC

Increase of Nordea holding

EURm

Investment Allocations by Risk Profile

14/05/2013

31

Total Group (MEUR) 17,523 18,237 18,164 18,623

06/12 09/12 12/12 03/13

Money Market 10% 9% 82% 11% 9% 81% 7% 10% 89% 7% 14% 94%Bonds 78% 52% 8% 77% 51% 12% 81% 48% 8% 81% 44% 4%Equity 10% 26% 4% 10% 27% 4% 11% 29% 2% 11% 28% 2%Private Equity 0% 5% 4% 0% 5% 2% 0% 5% 1% 0% 4% 1%Other 1% 9% 1% 1% 8% 1% 1% 9% 1% 1% 9% 1%

11,638

5,421

464

12,245

5,519

473

11,717

5,519

928

11,986

5,577

1,060

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

If P&C

Man

datu

m

Life Sam

po

Plc If P&

C

Man

datu

m

Life Sam

po

Plc If P&

C

Man

datu

m

Life Sam

po

Plc If P&

C

Man

datu

m

Life Sam

po

Plc

Investment & Counterpart Exposures*

14/05/2013

32 * In Exposure tables the calculation rules may differ in some areas from Allocation tables

31.3.2013 AAA AA+ - AA-

A+ - A-

BBB+ - BBB-

BB+ - C

D NonRated

Fixed Income Total

Equities Other Derivatives (Counterparty Risk)

Total Change from 31.12.2012

Basic Industry - - 4 127 336 - 195 662 250 - - 911 - 38

Capital Goods - 3 91 56 20 - 117 287 513 - - 800 + 25

Consumer Products - - 32 312 31 - 172 547 397 - - 944 - 30

Energy - 6 80 19 101 - 438 645 43 - - 687 + 4

Financial Institutions 28 1,915 2,725 476 492 - 16 5,652 54 21 21 5,747 + 47

Governments 45 - - - - - - 45 - - - 45 - 3

Government Guaranteed 228 - - - - - - 228 - - 3 231 + 2

Health Care - - - - 43 - 43 86 37 - - 123 + 123

Insurance - - 27 21 - - 21 69 34 - - 103 - 1

Media - - - - 12 - 42 54 10 - - 64 - 3

Public Sector, Other 555 32 - - - - - 587 - - - 587 + 136

Real Estate - 10 - - - - 205 216 - 262 - 478 + 100

Services - - - 18 36 - 23 78 42 12 - 131 - 16

Technology and Electronics - - - - 34 - 16 50 54 - - 104 + 29

Telecommunications - - 192 116 46 - 22 376 86 - - 462 - 12

Transportation - 28 6 - - - 294 328 12 - - 340 - 4

Utilities - - 329 151 - - 62 541 81 - - 622 - 9

Others - - - - - - 16 16 12 0 - 28 - 15

Asset-backed Securities - - - - - - - - - - - - -

Covered Bonds 3,871 187 11 10 - - - 4,080 - - - 4,080 + 141

Funds - - - - - - 282 282 1,265 591 - 2,137 - 6

Total 4,728 2,182 3,498 1,307 1,150 - 1,963 14,828 2,888 885 23 18,625 + 470

Change from 31.12.2012 + 329 + 157 + 16 - 128 + 36 - + 30 + 440 + 45 - 14 - 0 + 470 EURm

Note: Category Other includes private equity and non-listed real estate. Category Derivatives includes only OTC derivatives and corresponding collaterals.

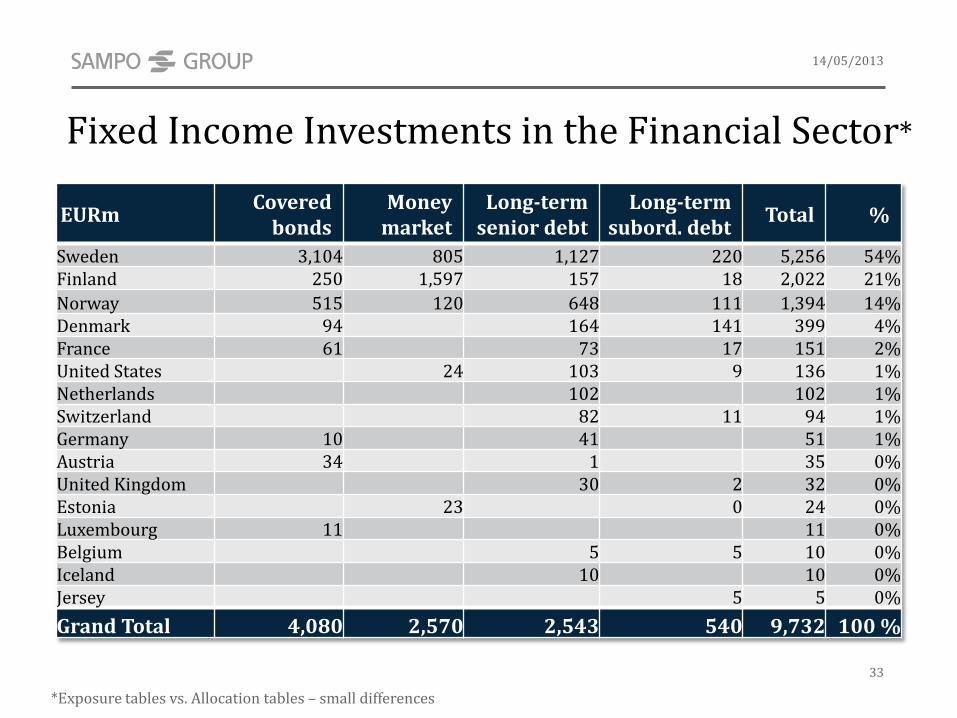

Fixed Income Investments in the Financial Sector*

14/05/2013

33

*Exposure tables vs. Allocation tables – small differences

EURm Covered

bonds Money

market Long-term

senior debt Long-term

subord. debt Total %

Sweden 3,104 805 1,127 220 5,256 54% Finland 250 1,597 157 18 2,022 21% Norway 515 120 648 111 1,394 14% Denmark 94 164 141 399 4% France 61 73 17 151 2% United States 24 103 9 136 1% Netherlands 102 102 1% Switzerland 82 11 94 1% Germany 10 41 51 1% Austria 34 1 35 0% United Kingdom 30 2 32 0% Estonia 23 0 24 0% Luxembourg 11 11 0% Belgium 5 5 10 0% Iceland 10 10 0% Jersey 5 5 0% Grand Total 4,080 2,570 2,543 540 9,732 100 %

Fixed Income Investments in the Public Sector - no Periphery*

14/05/2013

34 * Exposure tables vs. Allocation tables – small differences

EURm Governments Government

guaranteed Public sector,

other Total

Sweden 16 56 335 407 Norway 27 141 168 Finland 12 55 83 150 Germany 79 79 Denmark 12 27 40 Netherlands 17 17 Total 45 228 587 860

Sampo plc Baa2 Stable

Straightforward Cash Flows & Strong Balance Sheet

14/05/2013

36

Dividends • If P&C • Mandatum Life • Nordea

• Internal Administration Costs • Discretionary Dividends for Shareholders • Interest Expenses for Bondholders

Income • Interest on Liquidity • Income on other

investments

Sampo Plc

Assets EURm 9,268 Liabilities EURm 9,268

Liquidity 984 CPs Issued 385

Investment assets 28 LT Senior Debt 1,723

-Real Estate 4 -Private Placements 148

-Private Equity 7 -Bonds Issued 1,575

-Other investm. 18 -Pension Ins. Loans 0

Subordinated Loans 231 Subordinated Debt 0

Equity Holdings 7,928 Capital 7,061

-Subsidiaries 2,370 - Undistributable 98

-Associated 5,557 - Distributable 6,962

Other Assets 97 Other Liabilities

100

Flow of Funds Balance Sheet

Key Credit Metrics well in Single A -range

Sampo plc Q1/2013 Gross Debt EUR 2,108 m Gross Debt to Equity 29.9% Financial Leverage 23.0%

Sampo Group 2011 2012 Shareholders' Equity 8 ,920 10,113 Hybrid Bonds 202 200 Senior Debt 2,329 2,162 Financial leverage 22.1% 18.9% Allianz Group / FL* 28.5% 26.0% * Company´s own information

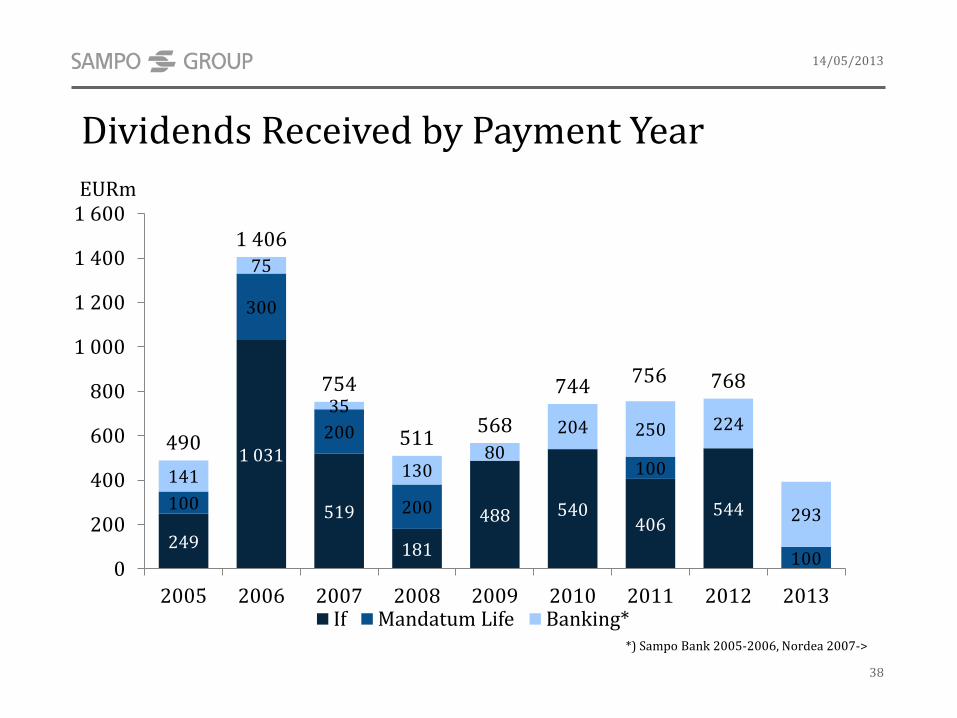

Dividends & Reported Profits

14/05/2013

37 * Parent Company is not equal to Holding Segment; Dividend Income includes also dividends from Private Equity investments

514

-15

65

564 569

-16 -31

522

747

-8 -37

702 762

-10 -70

683

773

-17 -20

737

-100

0

100

200

300

400

500

600

700

800

Dividend income Operating expenses Net financial expenses

Profit before taxes

2008 2009 2010 2011 2012

* EURm

EURm 1-3/2013 1-3/2012 Dividends 293 224 Operating expenses -5.4 -4.0 Net financial expenses -24.8 -16.0 Profit before taxes 262.8 205.0

Dividends Received by Payment Year

*) Sampo Bank 2005-2006, Nordea 2007->

EURm

**

249

1 031

519

181

488 540 406

544 100

300

200

200

100

100

141

75

35

130 80

204 250 224

293

490

1 406

754

511 568

744 756 768

0

200

400

600

800

1 000

1 200

1 400

1 600

2005 2006 2007 2008 2009 2010 2011 2012 2013 If Mandatum Life Banking*

14/05/2013

38

Sampo Plc Debt Instruments

14/05/2013

39

Comments on Debt

• Most of the debt tied to short-term indices - mitigation of group level interest rate risk - use of swaps

• Diversification is actively sought over

- maturities - investor base

• Private Placements

- targeted for a Finnish retail investors - related to Mandatum Life´s services

Maturity Structure

0

200

400

600

800

1 000

2013 2014 2015 2016 2017

CP´s Senior under EMTN Senior Retail Private

EURm

Instrument & Principal Coupon Swap Effective Rate Maturity Senior Bond 4,000 SEKm (EMTN) Stibor3M + 1,5000% ---- 2,7360% 16.09.2013

Senior Bond under EMTN 300 EURm (EMTN) 3,2500 % ---- 3,0377% 03.10.2014

Senior Bond under EMTN 300 EURm (EMTN) 4,2500 % Euribor3M + 1,4727% 1,6937% 22.02.2016

Senior Bond 500 EURm (EMTN) 4,2500% Euribor3M + 2,7910% 3,0040% 27.02.2017

CP’s issued 385 EURm Euribor + Margin 0,7900% 3M

Public debt 1,959 EURm 2,3095%

Private placements 148 EURm 2,5655%

Total 2,108 EURm 2,3275%

Sampo plc Key Credit Considerations

40

Diversification through Insurance & Banking in the Nordic Region

Management has a proven Track Record in long-term Value Creation

Conservative Financial Profile, strong Capitalization and Liquidity

14/05/2013

Stable Dividend Flow from Affiliated Companies with strong Brands

Bondholder Value Created

Appendix

Nordea BV on Consolidated Balance Sheet

14/05/2013

Figures Per Share EUR Acquisition price 6.46 Book value 7.57 Market Value* 9.34 No. of shares 860,440,497

42 * As of 7/05/2013

Nordea in Sampo Group’s B/S EURm

Acquisition price 5,557.3

Retained earnings 1,156.0

Accumulated other changes in Nordea’s equity -25.9

Share of Nordea’s net profit 169.2

Amortisation -8.8

Deferred tax 1.9

Dividends -292.5

Share of Nordea’s other comprehensive income 8.9

Share of Nordea’s other changes in equity -57.2

Share of Nordea’s goodwill change 3.2

Total 6,512.1

Principles of Capital Management • Risk Capital Available > Risk Capital needed

– Risk Capital Available = SI Capital + Other items absorbing economic losses – Risk Capital Need = Measured Economic Capital + ”Non-measurable” risks – Buffer between measures under constant considerations – Pro-Active management of Risks/Capitalisation

• Economic Capital at 99.5% as a basis for Risk Capital Need

– Economic capital is an estimate of Risk Capital needed to keep the Group solvent – EC is calculated at 99.5% confidence level and 1 year risk horizon – ”Non-measurable” risks include liquidity, market , illiquidity and business environment risks

• Adjusted Solvency Capital is a measure of Risk Capital Available – Solvency I capital items included as such – The difference between Undiscounted technical provisions in balance sheet and their

discounted value (so called Liability Side adjustment) – Capital instruments excluded from regulatory capital in Solvency I

14/05/2013

43

Economic Capital Reporting Principles • Definitions

– Economic capital (EC) is used as an internal measure of capital required for measurable risks the Group is exposed to.

– EC is defined as the amount of capital to protect the solvency over a one year time horizon with a probability of 99.5 per cent.

• EC at company level – EC is calculated in If P&C and Mandatum Life using a set of calculation methods, which have been

developed for the specific needs of each company. – In If P&C and Mandatum Life EC accounts for market, credit, insurance and

operational risks, as well as the diversification effect between these risks. – EC figure calculated and reported by Nordea is used in Sampo Group reporting.

Because Nordea’s reported figures are expressed at 99.97% confidence level they are converted by Sampo into 99.5% confidence level.

• EC at Group Level – Correlations between companies’ risks are assessed and diversification effect is calculated. – Group wide EC is a sum of Companies’ EC and the diversification effects.

14/05/2013

44

Principles of Investment Management • Company specific needs form the basis for all investments

– Liabilities intensively analysed and modelled – Regulatory requirements

• Strategy

– Absolute Return targets taking into account the liabilities and general business targets – Direct Investments into Nordic countries mainly, Outside Nordics Funds mainly – No diversification for the sake of diversification

• Centrally Managed

– Sampo plc Chief Investment Officer responsible for all investments, all portfolio managers have a direct reporting line to him

– Common infrastructure for investment administration and reporting – Investment strategies coordinated and streamlined, no overlapping activities to

prevent Group Wide concentrations

14/05/2013

45

Source: FSA

14/05/2013

46

IF Regulatory Solvency Capital & Ratio*

54%

70%

88%

74% 71% 66%

77% 79%

72%

75%

79%

0%

20%

40%

60%

80%

100%

0

1 000

2 000

3 000

4 000 % EURm

Solvency capital (lhs) Solvency ratio (rhs)

14/05/2013

47 * Solvency ratio, (IFRS) % = + solvency capital + premiums earned from 12 months

x 100%

Mandatum Life Regulatory Solvency Ratio*

14/05/2013

48

* Solvency ratio, % of technical provision, (IFRS) = + solvency capital + liabilities for insurance and investment contracts - reinsurers’ share of insurance liabilities - 75% x technical provisions relating to unit-linked insurance

x 100%

17,7%

21,3% 20,1%

16,5%

7,9%

18,5%

25,8%

20.9%

27,7% 27,3%

0 %

5 %

10 %

15 %

20 %

25 %

30 %

Average C/R & Standard Deviation 2007-E2014

49

0

1

2

3

4

5

6

7

90 91 92 93 94 95 96 97 98 99 100

Gjensidige

Topdanmark

Swiss Re

Tryg

Sampo

Munich Re

Generali AXA

Aviva Zig

SCOR Hannover Re

Stan

dar

d d

evia

tion

, %

Combined ratio, %

Sub-group 1

Sub-group 2 Sub-group 3

Sub-group 4

AVERAGE

Allianz

Source: Macquarie, European Insurance, 22.01. 2013

14/05/2013

Latest History of Sampo Group

Sampo’s P&C insurance operations are merged with If. Following the transaction, Sampo owns 38 per cent of If’.

Sampo Insurance Company and Leonia merge into the Sampo-Leonia financial services group.

Mandatum Bank joins the Group, and the Group’s name is shortened to Sampo.

Sampo Group divests Sampo Bank Group to Danske Bank A/S. Sampo´s business areas are P&C insurance and life insurance.

Sampo´s Nordea holding exceeds 20% and Nordea becomes an associated company.

2007 2004 2002 2001 2000 2010 2011

Sampo Group´s (If P&C´s) Topdanmark holding exceeds 23% and Topdanmark becomes If´s associated company.

2012

Sampo Group (If P&C) acquires Tryg´s Finnish business. If P&C signs a partnership agreement with Nordea.

Finland If becomes fully owned by Sampo. Sampo has three core businesses: P&C insurance, banking and long-term savings.

14/05/2013

50