RWC Equity Income - RWC Partners these terms means that for a company that makes ... companies such...

15

Q2 2015 Investor Letter | April 2015 RWC Equity Income For Professional Investors and Advisers Only

-

Upload

nguyencong -

Category

Documents

-

view

223 -

download

2

Transcript of RWC Equity Income - RWC Partners these terms means that for a company that makes ... companies such...

Q2 2015 Investor Letter | April 2015

RWC Equity Income

For Professional Investors and Advisers Only

Portfolio Managers Nick Purves and Ian Lance were previously responsible for income-based

strategies at Schroders, co-managing approximately £5bn within the income

fund range since 2007. Nick and Ian joined RWC in August 2010 to establish

the Equity Income franchise and were joined by John Teahan in September

2010. Since joining RWC the Team has developed low-volatility equity income

funds with a focus on capital preservation. The team has over 60 years’

investment experience between them and currently manage USD 4.4 billion in

equity income mandates.

Contents

1. The Price of Everything and the Value of Nothing

(The Use and Abuse of Price-to-Earnings Ratios) 1-7

Ian Lance looks at the commonly used price -to-earnings ratio, why it

is frequently misused in financial valuation and what adjustments can be

made to make it a more useful tool. He then explores which areas of the

market look over-valued on this basis.

2. Taking Minutes and Wasting Hours 8-9

Ian Lance considers whether company meetings add value to the invest-

ment process and considers how investors can improve their ability to

forecast.

3. The lunatics have taken over the asylum 10-12

Ian Lance looks at ten reasons why financial markets are behaving

strangely.

Q2 2015 Investor Letter | April 2015

RWC Equity Income

Nick Purves, John Teahan and Ian Lance

RWC Q2 2015 Investor Letter | 1

RWC Equity Income

1. Asquith, Mikhail and Au ‘Information Content of Equity Analyst Reports’ Journal of Financial Economics February 2005

2. Modigliani and Miller ‘Dividend policy, growth and the valuation of shares’ 1961

The price-to-earnings (P/E) ratio remains the primary method

used to value stocks with a survey of sell side research

reports suggesting 99% of analysts used some sort of multiple

compared with less than 13% using any variation of a

discounted cash flow model.1 The appeal of P/E multiples is

that they are quick and easy to calculate and, at face value,

make it easy to compare the valuation of a stock to its history

as well as comparing one stock to another. Their ease of

calculation, however, means that they are frequently misused.

Sloppy use of P/E multiples is commonplace. Analysts will

most frequently relate a high P/E with high earnings growth

but not only does their poor ability to forecast invalidate this

but it also takes no account of whether that growth is value

creative or destructive. Most investors would agree with the

point of view that ‘the value of any asset is the present value

of its future cash flows’ and yet most investors will reject any

valuation model that projects and discounts future cash flows

as being ‘too complicated’ or ‘too sensitive’. Whilst it is true

that a discounted cash flow is sensitive to the inputs, at least

those inputs are explicit and can be sense checked and

debated whereas with a P/E multiple they are hidden away.

None of this is to say that P/E’s should not be used but just

that the user should be aware of the explicit assumptions that

he or she is making.

One way of separating out the implied assumptions in a

valuation multiple was originally put forward by Modigliani and

Miller who stated that the value of a company could be split

into two parts as follows.2

Value of firm = steady state value + future value creation

To define these terms further:

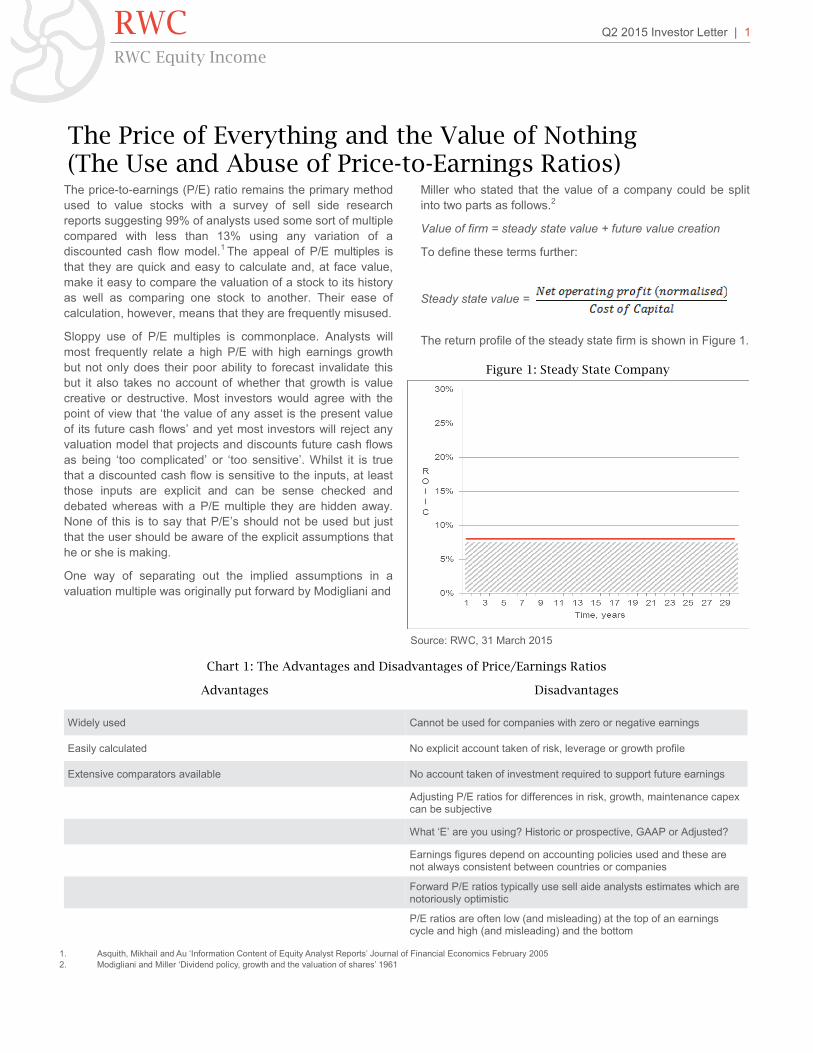

Steady state value =

The return profile of the steady state firm is shown in Figure 1.

The Price of Everything and the Value of Nothing (The Use and Abuse of Price-to-Earnings Ratios)

Advantages Disadvantages

Widely used Cannot be used for companies with zero or negative earnings

Easily calculated No explicit account taken of risk, leverage or growth profile

Extensive comparators available No account taken of investment required to support future earnings

Adjusting P/E ratios for differences in risk, growth, maintenance capex can be subjective

What ‘E’ are you using? Historic or prospective, GAAP or Adjusted?

Earnings figures depend on accounting policies used and these are not always consistent between countries or companies

Forward P/E ratios typically use sell aide analysts estimates which are notoriously optimistic

P/E ratios are often low (and misleading) at the top of an earnings cycle and high (and misleading) and the bottom

Figure 1: Steady State Company

Source: RWC, 31 March 2015

Chart 1: The Advantages and Disadvantages of Price/Earnings Ratios

The steady state value of the firm assumes that current net

operating profit (NOPAT) is sustainable indefinitely and that

incremental investments neither add nor subtract value.

Redefining these terms means that for a company that makes

a long run return on equity in line with its cost of equity, the

price to earnings multiple is calculated as follows:

Steady-state P/E =

So assuming a cost of equity of 8% a P/E for a company

making an 8% return on equity is 12.5x which is (1/0.08). By

just being aware of this value, an analyst can subtract it from

the current market value of a stock and see how much of the

value is associated with future value creation.3

Future value creation essentially comes down to how much

money a company invests, what spread over cost of capital it

makes and how long it can find these value creating

investments.

Future value creation =

For a firm where the return is above the cost of equity, the P/E

ratio is derived as follows:

P/E =

Where:

ROE= the long run return on incremental capital invested

COE= After tax cost of equity (assumed for the purpose of

this exercise to be 8%)

Ge= long run earnings growth rate

Thus for companies where the following growth and ROIC

assumptions are used in perpetuity, the range of price

earnings multiples generated would be as shown in Table 1.

Note that any company where ROIC is 8% and is therefore in

line with COE has a steady state multiple of 12.5x (highlighted

in Table 1). If you could find a company that could invest at

24% to perpetuity and grow at 6% p.a., then it should trade on

38x earnings but to state the obvious, there are not many of

these companies around today.

As a more realistic assumption is that a company will be able

to invest at a rate above its cost of capital for a period of time

before this rate fades back towards its cost of capital, it makes

more sense to combine both valuation methods in a two stage

model. Figure 2 shows the profile of a company which has a

cost of capital of 8% and where the company can invest at a

rate of 24% for 15 years before mean reverting to 8%.

RWC Q2 2015 Investor Letter | 2

RWC Equity Income

3. HOLT estimate that in 1999, 60% of the value of the S&P500 was assumed future value creation vs long run average of 35%.

Return on Invested Capital

Earnings Growth

4% 8% 16% 24%

2% 8.3 12.5 14.6 15.3

4% 0.0 12.5 18.8 20.8

5% n/a 12.5 22.9 26.4

6% n/a 12.5 31.3 37.5

Figure 2

Source: RWC, 31 March 2015

Source: RWC, 31 March 2015

Table 1: How Returns and Growth Rates Impact Price/Earning Ratios

Table 2 shows the same company but varies the ROIC and

growth rates and then shows the implied multiples.

When companies and investors are determining appropriate

price/earnings multiples, the first thing they think about is

growth but Table 2 shows why this is a mistake. Note for a

company that is destroying value, growth is bad as shown by

the low multiples in the left hand column. This is particularly

relevant when we consider companies which overpay for

acquisitions and hence transfer wealth to the selling company.

In many cases, the acquiring company grows and the deal is

earnings accretive and yet value is destroyed because the

additional growth makes a return below the cost of capital. For

a company with ROIC in-line with COE, the second part of the

equation collapses to zero and hence the multiple is just the

steady state multiple. For a company that can add value,

growth is positive and the resulting multiple is higher than

many value investors would be willing to pay for any

company.

With this in mind, we can see how relative valuation multiples

have limited use. Comparing a company’s multiple to history

only makes sense if the key drivers today are the same as

those that existed in the past and the same goes for

comparing two companies; unless you expect them to make

similar returns and growth rates, you should not expect to use

similar multiples. Indeed, it is possible to get to similar

valuation multiples in different ways as shown in Table 3.

Implications for Today’s Valuations As prices have risen faster than underlying earnings for most

companies, valuations have increased and in particular, the

ratings for ‘quality defensive’ companies such as the large

global consumer staples businesses have increased

considerably with most of them trading on price/earnings

ratios in excess of 22x. In Figure 3, we plot the P/E ratio for

these companies against their 7 year EPS growth rate and

interestingly find very little correlation whereas in Figure 4 we

plot P/E against ROIC. Here we find a much better correlation

with the highest ROIC companies also having the highest P/E

ratios. This is mildly encouraging as it validates some of the

theory discussed above and does suggest investors are at

least making some effort to differentiate between the return of

capital of firms.

RWC Q2 2015 Investor Letter | 3

RWC Equity Income

Return on Invested Capital

Earnings Growth

4% 8% 16% 24%

2% 7.1 12.5 15.2 16.1

4% 3.3 12.5 17.1 18.6

5% n/a 12.5 19.2 21.8

6% n/a 12.5 22.4 25.7

Assumes all equity financed, 8% cost of capital, 15 year forecast period. Source: RWC, 31 March 2015.

NOPAT growth

ROIC Multiple

High growth, low spread

12.0% 8.8% 15.0x

Moderate growth, moderate spread

6.0% 11.0% 15.0x

Low growth, high spread

3.0% 23.0% 15.0x

Table 3: Three Different Route to 15x Price/Earnings Multiple

Figure 4: Price/Earnings Multiples of Global Consumer Staples Companies Versus ROIIC

Source: RWC, 31 March 2015. Source: RWC, 31 March 2015

Source: RWC, 31 March 2015

Table 2: Implied Price/Earnings Models Using Two Stage Model

Figure 3: Price/Earnings Ratios of Global Consumer Staples Versus Earnings Growth

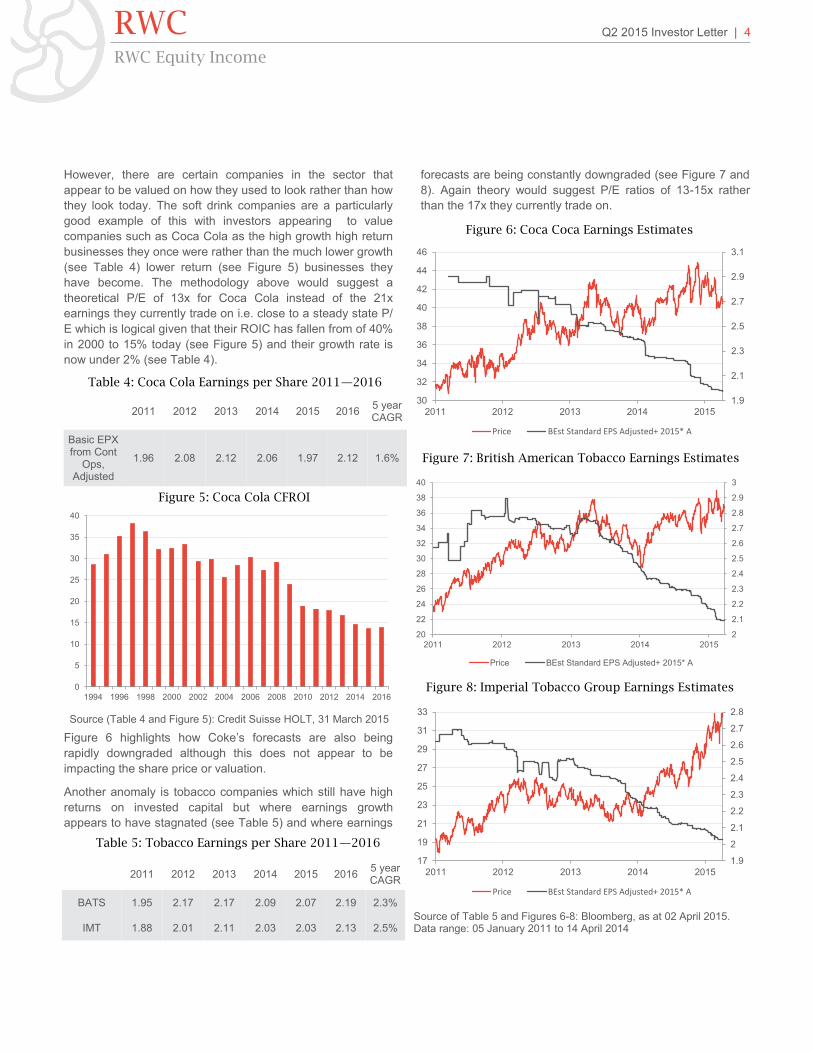

However, there are certain companies in the sector that

appear to be valued on how they used to look rather than how

they look today. The soft drink companies are a particularly

good example of this with investors appearing to value

companies such as Coca Cola as the high growth high return

businesses they once were rather than the much lower growth

(see Table 4) lower return (see Figure 5) businesses they

have become. The methodology above would suggest a

theoretical P/E of 13x for Coca Cola instead of the 21x

earnings they currently trade on i.e. close to a steady state P/

E which is logical given that their ROIC has fallen from of 40%

in 2000 to 15% today (see Figure 5) and their growth rate is

now under 2% (see Table 4).

Figure 6 highlights how Coke’s forecasts are also being

rapidly downgraded although this does not appear to be

impacting the share price or valuation.

Another anomaly is tobacco companies which still have high

returns on invested capital but where earnings growth

appears to have stagnated (see Table 5) and where earnings

forecasts are being constantly downgraded (see Figure 7 and

8). Again theory would suggest P/E ratios of 13-15x rather

than the 17x they currently trade on.

RWC Q2 2015 Investor Letter | 4

RWC Equity Income

2011 2012 2013 2014 2015 5 year CAGR

2016

Basic EPX from Cont

Ops, Adjusted

1.96 2.08 2.12 2.06 1.97 1.6% 2.12

Table 4: Coca Cola Earnings per Share 2011—2016

Figure 5: Coca Cola CFROI

Figure 6: Coca Coca Earnings Estimates

Figure 7: British American Tobacco Earnings Estimates

Figure 8: Imperial Tobacco Group Earnings Estimates

2011 2012 2013 2014 2015 5 year CAGR

2016

BATS 1.95 2.17 2.17 2.09 2.07 2.3% 2.19

IMT 1.88 2.01 2.11 2.03 2.03 2.13 2.5%

Table 5: Tobacco Earnings per Share 2011—2016

Source (Table 4 and Figure 5): Credit Suisse HOLT, 31 March 2015

Source of Table 5 and Figures 6-8: Bloomberg, as at 02 April 2015. Data range: 05 January 2011 to 14 April 2014

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3

20

22

24

26

28

30

32

34

36

38

40

2011 2012 2013 2014 2015

Price BEst Standard EPS Adjusted+ 2015* A

1.9

2.1

2.3

2.5

2.7

2.9

3.1

30

32

34

36

38

40

42

44

46

2011 2012 2013 2014 2015

Price BEst Standard EPS Adjusted+ 2015* A

1.9

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

17

19

21

23

25

27

29

31

33

2011 2012 2013 2014 2015

Price BEst Standard EPS Adjusted+ 2015* A

0

5

10

15

20

25

30

35

40

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

RWC Q2 2015 Investor Letter | 5

RWC Equity Income

4. Robert.J. Shiller “Price-Earnings Ratios as Forecasters of Returns: 21 July 1996

5. Berkshire Hathaway 2014 Letter to Shareholders

6. http://uk.businessinsider.com/warren-buffett-gordon-gekko-comparison-2015-3?r=US#ixzz3W9v7oWiF, 27 March 2015

Conclusion The price/earnings ratio is a convention that emerged mostly

as a result of ‘tradition and convenience rather than logic’

according to Robert Shiller.4 We have highlighted, however,

that as long as the user is explicit in the assumptions he is

making, they do have some practical use. In addition we can

make the following comments:

1. Multiples are not valuation; they are a shorthand for

the process of valuation and this applies to all

multiples, not just price-earnings;

2. If you want to consider the effect of leverage, use an

enterprise multiple, if you want to adjust for cyclicality,

use normalised forecasts;

3. In assessing capital allocation, consider incremental

return on capital first and growth second. Growth at

below cost of capital has zero or negative value;

4. Don’t use the recent past to understand the future

unless it is likely to be very similar;

5. In common with many companies, the ROIIC and

earnings growth of global consumers staples has been

declining and yet their Price/earnings ratios have been

expanding leaving them trading on valuations that are

not justified by their underlying fundamentals. This is,

of course, symptomatic of a market being driven by

central banking largesse rather than fundamentals.

Addendum—the ‘alternative’ view from

private equity

No sooner had I finished writing this note, then Heinz

launched a takeover bid for Kraft, which was a share that, in

common with other consumer staples names, already looked

very over-valued at nearly 20x 2015 EPS for a company with

virtually no growth. Heinz clearly disagree as they and their

private equity backers 3G have come in with an offer roughly

30% above the market price. We thought it might be

interesting to look at the numbers involved in these two deals

(the 2013 takeover of Heinz and the subsequent takeover of

Kraft) to see how private equity gets them to work employing

the standard buyout techniques.

Deal 1:

Berkshire Hathaway and 3G bought Heinz for $23bn in March

2013 which looked like a pretty full price at 14x EV/EBITDA

multiple which was a 40% premium above the decade

average sector multiple. However, in our new normal ZIRP

world, any multiple can be made to work by employing the

following three steps; leverage, restructure, rerate and flip.

1. Leverage

Buffett and 3G loaded Heinz with $12bn of new debt taking

net debt to EBITDA up to 6.3x. In addition to this, Buffett

issued $8bn preferred stock with a 9% dividend which meant

the debt load was significant enough for Fitch to immediately

downgrade Heinz from investment grade to junk bond status.

Including the preference shares as debt the net debt to

EBITDA ratio was 10x.

2. Restructure

3G have raised margins by a whopping 800bps in two years

by firing a fifth of the workers, cutting advertising spend from

the standard 8% of sales to 4%. This has taken EBITDA

margins to 28% which is way higher than the global sector

average of 20% despite the fact that Heinz is smaller than

many of the global players such as Nestle and Unilever. In

addition, it assumes that hollowing out the company in this

way can be achieved without damaging the fabric of the

business or its growth potential. In the short term, however, it

is great news for shareholders (Buffett and 3G) although not

so great for other stakeholders such as employees, suppliers

and the wider economy. One does have to wonder when

Buffett claims ‘Americas best days are ahead’,5 how he

thinks loading companies with debt, firing their employees and

avoiding tax helps the wider economy. As Deutsche Bank

recently pointed out in a note to clients ‘how would this

"merger" have been reported if you swapped the popular,

cuddly Warren Buffet with Gordon Gekko?’6

3. Rerate

Rerate and then flip back on to the stock market at a higher

price (often back to the same investors you bought it from in

the first place) or use that expensive currency to buy

something else (see page 6).

Deal 2: Heinz (3G + Buffett) bid for Kraft

Before we jump into the detail first a little bit of context. Kraft,

is a low-growth business that sells Jell-O, Lunchables,

Maxwell House and Kool-aid (which is ironic as this has been

the drink of choice for many investors in the past decade)

amongst other brands; 2014 sales of $18.2bn were only just

above $17.8bn recorded in 2010 and operating income of

$3bn was the same as recorded in 2010. However, for Wall

Street, Kraft is the gift that keeps on giving – some investment

bankers must have been able to put their kids through college

on the generous fees that Kraft keeps dolling out. The

business was formerly owned by the tobacco company Philip

Morris but was IPO’d in 2001. In 2010 the next investment

banking payday came for advising on the $18.5bn takeover of

Cadbury and then yet more fees for spinning it out of parent

company Mondelez in 2012. But the financial engineering did

not stop there. At that point it gifted a $7.2bn goodbye

dividend to its parent followed by three years of dividends and

share re-purchases which combined amounted to $10bn. Now

given that Kraft’s free cash flow from operations only

amounted to $3bn over the period, the rest had to be

borrowed albeit at an ultra-low interest rate of 3%.

Enter Heinz who according to the terms of the deal, are

offering Kraft shareholders a 49% stake in the new combined

entity plus a special cash dividend of $16.50 per share (which

3G and Buffett are generously funding via a $10 billion

injection in to the new company). The remaining 51% share

would go to the existing Heinz shareholders – (Berkshire

Hathaway and 3G Capital) that jointly own Heinz. So despite

the fact that Kraft has nearly twice the revenues of Heinz and

a greater profit, the private equity guys are using their fancy

rating to get half the business. The company estimate cost

savings of $1.5bn although the ever optimistic street analysts

have plugged $2.2bn in to their models already. As Heinz gets

half of Kraft we know that Heinz is now implicitly being valued

at $45bn or 16 times 2014 EBITDA.

This is, of course, the new normal at work. $4 trillion of

quantitative easing has not brought about a sustainable

recovery and hence companies increasingly have to rely on

financial engineering to generate growth. Fed policies have,

however, made this financing cheaper than ever and the

guarantees that rates will stay low forever encourage

investors to lever up. Earnings growth is also boosted by firing

employees so the net effect of the Feds policies is that Wall

Street ends up better off whilst Main Street is worse off. I still

don’t fully understand why Main Street has been so tolerant

about this treatment.

RWC Q2 2015 Investor Letter | 6

RWC Equity Income

“Meetings are indispensable when you don't want to do

anything.”

― John Kenneth Galbraith

“If you had to identify, in one word, the reason why the human

race has not achieved, and never will achieve, its full

potential, that word would be 'meetings’.”

― Dave Barry8

One of the questions that we have been asked the most since

we joined RWC is ‘Don’t you miss all those company

meetings – how do you cope without them?’

And the honest answer is ‘no we don’t miss them’. In fact, we

now look back and realise how much time fund managers

waste in company meetings which begs the obvious question,

‘Why do fund managers spend so much time in meetings?’

One reason is that it helps to pass the time because as the

late economist and Nobel Prize Winner Paul Samuelson

implied, investing should be unutterably boring.

“Investing should be more like watching paint dry or watching

grass grow. If you want excitement, take $800 and go to Las

Vegas.”

Whilst some fund managers try to liven up their day by

constantly trading in and out of shares on their clients’ behalf,

another way to while away the hours is to attend lots of

company meetings. Company meetings are also a good

marketing ploy; large asset managers with 100+ global

analysts can boast of x thousand company meetings they

have every year thus suggesting they have some sort of

informational advantage over their smaller competitors

although they seem to confuse more information with better

information. At this point, it’s worth recalling the 1973 study by

Paul Slovic in which bookmakers were asked to forecast the

results of horse races and were given relevant pieces of

information in increments of 5, 10, 20, 40 i.e. each time they

ranked the horses, they were given more information and

asked to re-rank them. The study showed that the addition of

information beyond five pieces did not increase the accuracy

of their forecasts although it did increase their confidence.

This logic can be applied to company meetings – the addition

of lots of pieces of spurious information does not increase a

fund managers ability to pick stocks but it probably increases

his confidence as he feels that he ‘knows his company well’.

For others, company meetings go hand in hand with

namedropping company CEOs and creates the impression

that this gives them an advantage. Anecdotally, one well

known fund manager used to stand at the front of packed

meeting rooms of clients/prospects, waving his mobile phone

around whilst claiming that he had the mobile number of the

CEO of every company that he invested in. Apparently this

was meant to impress his audience.

Now there are times when a meeting is important, usually

during some sort of crisis that the company is facing or when

an impending acquisition is being discussed, but in general

their usefulness is massively over stated by the industry. Here

are six reasons why we believe they are given way too much

importance by the fund managers in general.

1. Assuming fund managers attend company meetings

looking for an informational advantage over their rivals, there

is one quite obvious hurdle to that strategy; companies cannot

tell you anything that is not already publicly disclosed

otherwise it is known as inside information and if you act on it

and get caught you can end up in jail.

2. Corporate management suffer from cognitive dissonance

as much as the rest of us and are likely to be either

consciously or sub consciously over optimistic about their

company’s fortunes and over-confident about their ability to

predict the future. The IR of a telecoms company once

assured us the dividend was totally safe a few months before

the company passed it completely and had a rescue rights

issue. I don’t think he was being deliberately misleading (at

least I hope not) but I just think he had seriously

underestimated how difficult their markets had become.

3. Sometimes managers will go out of their way to put a

positive spin on their company. One of the latest innovations

in the world of financial spin is the ‘Capital Markets Day’ which

is now known on our desk as a ‘Bull Up your Share Price

Day’. At these events, sell side analysts who are desperate

for bullish news in order to pump share prices higher are fed a

stream of positive news from company management and then

obligingly go away and write bullish investment reports. These

are usually published the following day and will invariably

drive the company’s share price higher (although this process

is now so tried and tested that the share price now starts to

move in advance of the Capital Markets Day).

4. Fund managers suffer from confirmatory bias; they will go

in to a meeting with a company they own and are positive

about and ask questions that confirm their positive outlook

rather than ask questions to test their belief. I once tried to

chair a meeting with the CEO of a large telecoms company on

one side of the table and twelve fund managers on the other,

each of whom owned the stock, was positive about it and had

one burning question to get across. To say that the meeting

was rambling, disjointed and ultimately fruitless is an

understatement.

5. Companies tell you what you want to hear and these days

are very good at it. The CEO of one large technology

RWC Q2 2015 Investor Letter | 7

RWC Equity Income

7. Taken from the title of a play by Damian Trasler

8. Dave Barry is a Pulitzer Prize-winning American author and columnist

Taking Minutes and Wasting Hours7

company knew investors were concerned about him making a

large acquisition and sought to assure them by saying that he

would ‘not make an acquisition that would make them lose

sleep at night’ before promptly making a $12bn deal at an

80% premium to the market price which wiped this amount

and more off the value of his own shareholders company.

6. The final and most important reason is that company

meetings tend to result in a wood from the trees problem

which we originally discussed in 2012 and re-visit below.

Consider the following statement, taken from Rick

Bookstaber’s “Why are We “Irrational”: The Path from

Neoclassical to Behavioural Economics 2.0.

“Linda is 31, single, outspoken and very bright. She majored

in philosophy. As a student she was deeply concerned with

issues surrounding equality and discrimination.

Is it more likely that Linda is a) a bank clerk or b) a bank clerk

and active in the feminist movement?”9

Most people choose answer b) because they focus on the

information provided about Linda’s past and use it to paint a

picture of her. This is, however, irrational as group b) is a sub

set of group a) i.e. there are more bank tellers in the US than

bank tellers who are active in the feminist movement.

Probability therefore favours answer a). In the same way, fund

managers use company meetings to drill down into the

minutest detail (the tax rate on the new Taiwanese subsidiary,

the CEO’s choice of bow tie) which is invariably less relevant

than bigger issues.

Is it possible for investors to shut out the entertaining but

misleading noise and hence improve the accuracy of the

forecasts that they make? According to American

psychologists Daniel Kahneman and Amos Tversky, there is

one way in which all forecasters could improve and that is to

distinguish between the two types of information available to

them: singular (or case) data and distributional (or base)

data10. Singular data consists of evidence about a particular

case under consideration so if you were analysing the spirits

company Diageo, this might involve making forecasts about

Chinese demographics and income distribution, propensity to

spend on branded spirits etc. Distributional data, on the other

hand, consists of knowledge about the distribution of

outcomes in similar situations. In this sense, a forecaster may

look at the financial performance of all large companies, for

example, to see what lessons he might draw from their

history. For instance, the knowledge that sales growth rates

are highly mean reverting (see Figure 9) is likely to be very

useful to the forecaster despite the fact that it is not company

specific information.

Research suggests that forecasters typically rely too heavily

on singular data, even when it is scant and unreliable, and

place too little emphasis on distributional data. This is exactly

what is going on when fund managers sit in endless company

meetings. Kahneman and Tversky have noted that humans

are poor at assessing probabilities because they rely on a

number of heuristic principles which reduce the complex task

of assessing probabilities and assessing values to simpler

judgemental values. One of the most common is called the

representative bias in which people try to assess probability

by asking to what extent is situation A is similar to situation B.

In our example above, investors may consciously or

subconsciously deem Diageo to be similar to Coca Cola

which was a very successful investment for Warren Buffett

and hence let this influence their prediction of whether

Diageo will be a successful investment. This explains

investor’s propensity to buy in to the excitement of ‘story

stocks’ despite the fact that base data would suggest that

continually buying expensive stocks produces poor returns.

In order to improve the accuracy of forecasts, extremeness of

predictions must be moderated by considerations of

predictability e.g. if analysts were honest they would concede

that their ability to forecast is very low. The lower the

predictability, the closer the prediction should move to the

class average. Imagine a bell curve of historic oil prices with

$150 on one tail and $10 on the other with the median around

$70. Do you think your chances of getting the forecast correct

are improved by placing your prediction close to $70 rather

than at $150 or $10? Of course this will not stop analysts

either simply extrapolating this year’s price or building large

models of the decline rates of oil fields. In my desk draw I

have both the March 1999 article from The Economist

predicting that oil would fall to $5 per barrel when it was

already at $10 and a 2008 note from Goldman Sachs

RWC Q2 2015 Investor Letter | 8

RWC Equity Income

9. http://rick.bookstaber.com/2011/02/why-are-we-irrational-path-from.html. 01 February 2011

10. In Kahnemans 2011 book ‘Thinking Fast and Slow’ these became referred to as ‘inside’ and ‘outside’ views

Figure 9: Sample, US Industrial/Service Firms, minimum market cap $250m, 1990-2013

Source: Prepared for Chance by Bryant Matthews, February 2015

predicting oil would go to $200 when it was already $140. As

Figure 10 shows, neither of those predictions turned out that

well.

Former US Treasury Secretary, Robert Rubin once said

“Some people are more certain of everything than I am of

anything." For some reason, financial services remains an

industry where historic lack of success in forecasting does not

prevent ‘experts’ being very confident in future predictions no

matter how difficult they may be. By accepting that the future

is a lot less predictable than we might think, focusing on base

rate data, averages and mean reversion, rather than the allure

of stories gained in company meetings, it may be that we can

all increase our chances of success. One thing is certain,

however, spending lots of time in company meetings might

help pass the time, but it does not improve our ability to

forecast or to pick stocks. In our opinion, this time is better

spent reading a report and accounts or an industry circular

than taking minutes and wasting hours in meetings.

RWC Q2 2015 Investor Letter | 9

RWC Equity Income

Figure 10 : WTI Crude Oil

Source: Bloomberg, as at 24 March 2015. Data range: 31 January 1984 to 31 March 2015

0

20

40

60

80

100

120

140

160

180

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

$ p

er

barr

el

What is going on in financial markets strikes us as more

bizarre than anything we have ever experienced in our life

time and yet it has been going on for so long it has now

become accepted as the norm and as such never really

attracts any comment. Of course, all this craziness can be

traced back to the same source; bubble loving central banks

who believe the way to cure too little aggregate demand is to

send prices of all financial assets to the moon. Below we

highlight ten things that suggest the lunatics really have taken

over the asylum.

1. $3.6 trillion of government debt or in other words nearly a

fifth of all global government debt is now trading with a

negative yield and yet a few weeks ago EPFR data showed

inflows to all fixed income funds of $16.04 billion – the highest

on record going back to at least 2008. This is despite

repeated warnings from regulators about the lack of liquidity in

bond markets and the fact that the actions of the ECB are

making liquidity even worse.

2. €2.0 trillion of Euro area government bonds over one year

maturity have negative yields and yet Mario Draghi thinks if he

can just get interest rates down a bit further he can turn the

European economy around. The reality is that the ECB is

playing the role of ‘the greater fool’ providing an exit to those

hedge funds and prop desks who have bought bonds with a

negative yield to maturity i.e. anyone buying bonds with a

guaranteed loss to maturity can only be doing so in the belief

some ‘greater fool’ will buy them at a higher price (a greater

loss to maturity). At the first sign that the ECB is going to

taper its purchases, this money will stampede for the exit at

the same time with some ‘interesting’ results.

3. Japan are now printing money to buy equities (that is worth

repeating-printing money to buy equities – FA Hayek must

be spinning in his grave). According to The Wall Street

Journal ‘The Bank of Japan’s aggressive purchasing of stock

funds has helped Japanese shares climb to multiyear highs in

recent months. But some within the central bank are growing

uncomfortable about the fast-paced rally and the bank’s

own role in fuelling it.’

Since Gov. Haruhiko Kuroda took office in March 2013

and introduced monetary easing of what he called a

“different dimension,” the central bank has sharply

increased its buying of baskets of stocks known as

exchange-traded funds. By directly underpinning the

market, officials have tried to encourage private investors to

follow suit and put more money in stocks in the hope of

stimulating the economy and increasing inflation.

During the past two years, the central bank entered the

stock market roughly once every three days, picking up a

total of ¥2.8 trillion ($23 billion) of ETFs that track Japan’s

major stock indexes, according to Bank of Japan records.

That distinguishes it from the U.S. Federal Reserve and

European Central Bank, both of which have bought bonds to

pump up the economy but haven’t directly bought stocks.’

4. The fact that the S&P500 is close to its all-time high would

tell you the US economy is firing on all cylinders and yet the

Federal Reserve seems frightened to remove emergency

monetary policy seven years in to the recovery. Janet Yellen

removed ‘patient’ from the Federal Reserve’s statement but

promptly rushed to assure financial markets that this didn’t

mean she was ‘impatient’ to raise rates. As has been the case

with every announcement from Chairman Yellen since she

took over, the market was immediately sent in to raptures.

5. In 2007, global debt of $142 trillion was enough to nearly

blow the financial system to smithereens but seven years later

global debt stands at $199 trillion and nobody seems to

believe this is an issue.

6. In 2009, General Motors emerged from government backed

Chapter 11 with a final cost of the GM bailout to the U.S.

taxpayers of $12 billion. A group of hedge funds have recently

taken a stake in the company and have come up with the

brilliant idea of GM gearing itself up again. The company has

instantly capitulated and announced it is authorizing an

immediate $5 billion stock buyback, and plans to return all

cash above a $20 billion floor to shareholders. Another victory

for ‘activist shareholders’! Some companies that have been

leveraging up their balance sheets for a while, have now hit

the point where anymore debt will result in them being

downgraded to junk status. Viacom announced on 6th April

RWC Q2 2015 Investor Letter | 10

RWC Equity Income

10. Golding, Lynval/Hall, Terry/Staples, Neville Egunton Universal Music Publishing Group

The lunatics have taken over the asylum10

2015 it would have to cease its share buyback in order to stay

within its ‘target leverage ratio’.

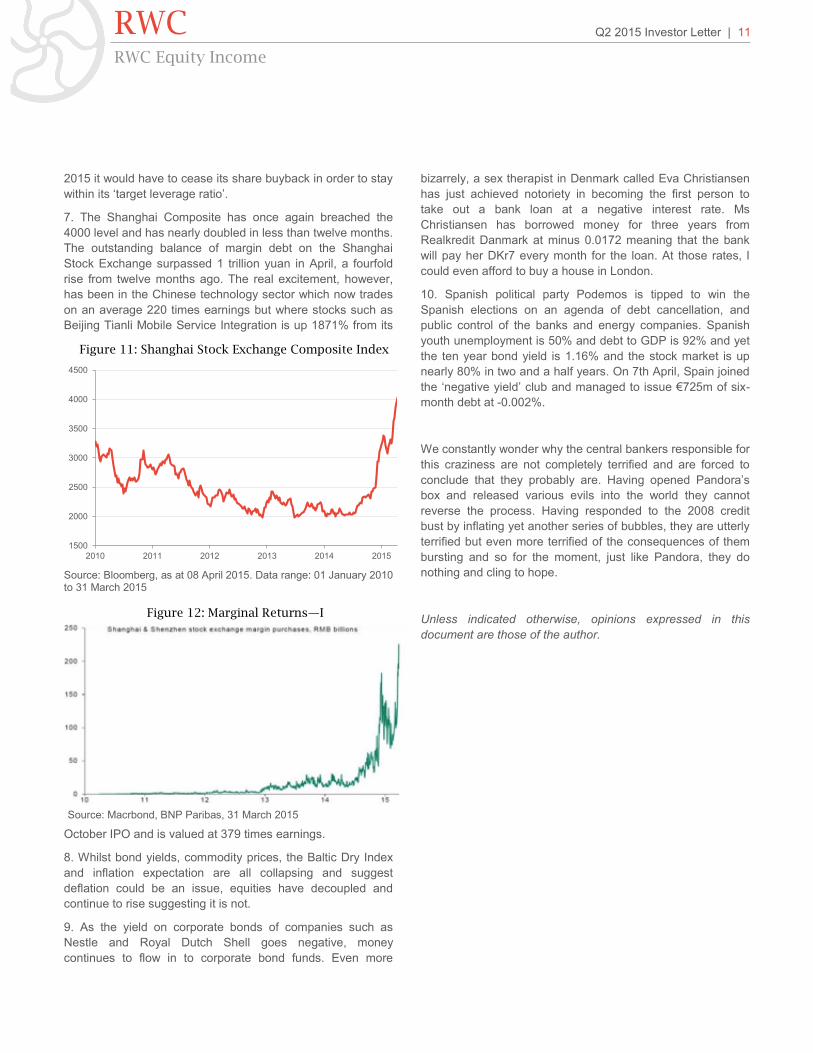

7. The Shanghai Composite has once again breached the

4000 level and has nearly doubled in less than twelve months.

The outstanding balance of margin debt on the Shanghai

Stock Exchange surpassed 1 trillion yuan in April, a fourfold

rise from twelve months ago. The real excitement, however,

has been in the Chinese technology sector which now trades

on an average 220 times earnings but where stocks such as

Beijing Tianli Mobile Service Integration is up 1871% from its

October IPO and is valued at 379 times earnings.

8. Whilst bond yields, commodity prices, the Baltic Dry Index

and inflation expectation are all collapsing and suggest

deflation could be an issue, equities have decoupled and

continue to rise suggesting it is not.

9. As the yield on corporate bonds of companies such as

Nestle and Royal Dutch Shell goes negative, money

continues to flow in to corporate bond funds. Even more

bizarrely, a sex therapist in Denmark called Eva Christiansen

has just achieved notoriety in becoming the first person to

take out a bank loan at a negative interest rate. Ms

Christiansen has borrowed money for three years from

Realkredit Danmark at minus 0.0172 meaning that the bank

will pay her DKr7 every month for the loan. At those rates, I

could even afford to buy a house in London.

10. Spanish political party Podemos is tipped to win the

Spanish elections on an agenda of debt cancellation, and

public control of the banks and energy companies. Spanish

youth unemployment is 50% and debt to GDP is 92% and yet

the ten year bond yield is 1.16% and the stock market is up

nearly 80% in two and a half years. On 7th April, Spain joined

the ‘negative yield’ club and managed to issue €725m of six-

month debt at -0.002%.

We constantly wonder why the central bankers responsible for

this craziness are not completely terrified and are forced to

conclude that they probably are. Having opened Pandora’s

box and released various evils into the world they cannot

reverse the process. Having responded to the 2008 credit

bust by inflating yet another series of bubbles, they are utterly

terrified but even more terrified of the consequences of them

bursting and so for the moment, just like Pandora, they do

nothing and cling to hope.

Unless indicated otherwise, opinions expressed in this

document are those of the author.

RWC Q2 2015 Investor Letter | 11

RWC Equity Income

Figure 11: Shanghai Stock Exchange Composite Index

Figure 12: Marginal Returns—I

Source: Macrbond, BNP Paribas, 31 March 2015

Source: Bloomberg, as at 08 April 2015. Data range: 01 January 2010 to 31 March 2015

1500

2000

2500

3000

3500

4000

4500

2010 2011 2012 2013 2014 2015

About RWC

RWC is an independent investment firm founded in 2000,

providing high-alpha asset management to institutions,

professional investors and intermediaries.

The firm provides an intense focus on investment performance

and extracting maximum ‘alpha’ (manager skill). Each of our

select range of strategies is based around the proven skills of

talented investment professionals.

The firm only launches strategies where it can secure top-

performing managers to run them. The firm provides an

environment in which talented managers, supported by

dedicated analysts, can focus on delivering performance using

their preferred process and philosophy.

This focus on performance sits within a culture of strong risk

management. At all times, the firm’s results are based on

delivering returns within known and acceptable levels of risk. In

each strategy, protecting clients’ assets is as important as

capturing return.

RWC is independently managed and controlled. The majority of

the firm’s equity is owned by the firm’s portfolio managers,

directors and other employees. Schroders owns a minority stake

in the business. Most RWC staff have chosen to invest directly in

equity and/or funds managed by the business.

RWC Asset Management LLP is a wholly-owned subsidiary of

RWC Partners Limited and provides the majority of investment

management services for the group. Both businesses are UK

based and are regulated by the Financial Conduct Authority.

About the team

Nick Purves

Nick joined RWC in August 2010. He was previously senior

portfolio manager at Schroders for over 16 years managing both

Institutional Specialist Value Funds and the Schroder Income

Fund and Income Maximiser Fund together with Ian Lance.

During his time at Schroders, Nick was Citywire AAA, Nick and

Ian’s Income fund was Morningstar 5 star rated, AA rated by

OBSR and won the Moneywise award in 2009 in the UK Equity

Income and Equity Income and Growth sectors. Nick is a

qualified Chartered Accountant.

Ian Lance

Ian joined RWC in August 2010. He was previously senior

portfolio manager at Schroders managing both Institutional

Specialist Value Funds and the Schroder Income Fund and

Income Maximiser Fund together with Nick Purves. During his

time at Schroders, Ian was Citywire AAA rated, Nick and Ian’s

Income fund was Morningstar 5 star rated, AA rated by OBSR

and won the Moneywise award in 2009 in the UK Equity Income

and Equity Income and Growth sectors. Previously Ian was the

Head of European Equities and Director of Research at Citigroup

Asset Management and Head of Global Research at Gartmore.

John Teahan

John joined RWC and the Equity Income Team in September

2010. He previously worked at Schroders, where he co-managed

the Schroder Income Maximiser with Nick Purves and Ian Lance.

John also co-managed the Schroder Global Dividend Maximiser,

Schroder European Dividend Maximiser and Schroder UK

Income Defensive funds, all three of which employed a covered

call strategy. John also specialised in trading and managing

derivative securities for a range of structured funds. Previously he

worked as a performance and risk analyst for Bank of Ireland

Asset Management UK. John is a CFA Charterholder.

Larry Furness

Larry joined RWC in August 2010 as a graduate recruit and

currently works in the Equity Income Team. He graduated from

the University of Nottingham in 2009 with an honours degree in

Economics and during his tenure successfully completed two

intern positions; the first at Permal Investment Management

where he was involved in manager research for the firm as an

Investment Analyst, and the Government Economic Service as

an Assistant Economist. Larry is a CFA Level II candidate.

Q2 2015 Investor Letter | 12

RWC Equity Income

RWC

This document contains information relating to RWC Partners Limited, RWC Focus Asset Management Limited and RWC Asset Management LLP (collectively, “RWC”), each of which is authorised and

regulated in the United Kingdom by the Financial Conducr Authority (“FCA”), and services provided by them and may also contain information relating to certain products managed or advised by RWC

(“RWC Funds”).

RWC may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. RWC

seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is issued by RWC Partners Limited, 60 Petty France, London SW1H 9EU, only for, and is directed only at, persons that qualify as Professional Clients or Eligible Counterparties under

rules of the FCA. The services provided by RWC are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a Retail Client.

This document is provided for informational purposes only. The information contained in it is subject to updating, completion, modification and amendment. RWC does not accept any liability (whether

direct or indirect) arising from the reliance on or other use of the information contained in it. The information set out in this document is to the reasonable belief of RWC, reliable and accurate at the date

hereof, but is subject to change without notice. In producing this document, RWC may have relied on information obtained from third parties and no representation or guarantee is made hereby with

respect to the accuracy or completeness of such information.

This document contains information that is not purely historical in nature. Such forward looking information is based upon certain assumptions about future events or conditions and is intended only to

illustrate hypothetical results under those assumptions (not all of which are set out or specified in this document). Actual events or conditions are unlikely to be consistent with, and may differ materially

from, those assumed. In addition, not all relevant events or conditions may have been considered in developing such assumptions. Accordingly, actual results will vary and the variations may be materi-

al.

This document is for discussion purposes only and is not an offer, or solicitation of an offer, to buy or sell any security or financial instrument or to participate in any trading strategy. The information

contained in this document is RWC’s summary, interpretation and analysis of available information, research, assumptions, estimates, views, predictions and opinions.

As mentioned above, this document does not constitute an invitation, inducement, offer or solicitation to anyone in any jurisdiction of or to acquire interests in any RWC Fund. Nevertheless, investment

in any RWC Fund should be considered high risk. Past performance is not a reliable indicator of future performance and may not be repeated. The value of investments in RWC Funds and the income

from them may fall as well as rise and may be subject to sudden and substantial falls. Changes in rates of exchange may cause the value of such investments to fluctuate. An investor may not be able to

get back the amount invested and the loss on realisation may be very high and could result in a substantial or complete loss of the investment. No representations or warranties of any kind are intended

or should be inferred with respect to the economic return from, or the tax consequences of, an investment in RWC Funds. Current tax levels and reliefs may change. Depending on individual circum-

stances, this may affect investment returns. There is no guarantee that the securities referred to in this document will be held by RWC Funds in the future. Nothing in this document constitutes advice on

the merits of buying or selling a particular investment. This document does not constitute investment, legal or tax advice.

The distribution and offering of RWC Funds in the United Kingdom and other jurisdictions may be restricted by law. It is the responsibility of every person reading this document to satisfy himself as to

the full observance of the laws of any relevant country, including obtaining any government or other consent which may be required or observing any other formality which needs to be observed in that

country. Nothing in this document constitutes an offer or solicitation by anyone in any jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such an offer or

solicitation. Interests in RWC Funds are available only in jurisdictions where their promotion and sale are permitted.

A United Kingdom investor may not have the right (otherwise provided under the FCA Handbook of Rules and Guidance) to cancel any agreement constituted by acceptance by or on behalf of an RWC

Fund of an application for interests in an RWC Fund. In addition, most if not all of the protections provided by the United Kingdom regulatory structure will not apply to investments in an RWC Fund.

Investors in an RWC Fund will not receive compensation under the Financial Services Compensation Scheme in the United Kingdom in the event that the fund is unable or likely to be unable to satisfy

claims against it.

RWC Partners Limited is registered in England and Wales (No. 03517613) with its registered address as above.

Contact Us

Please contact us if you have any questions

or want to discuss any of our strategies.

RWC 60 Petty France

London

SW1H 9EU

Tel: +44 20 7227 6000

Fax: +44 20 7227 6003

Email: [email protected]

Web: www.rwcpartners.com

RWC Equity Income

RWC