Rong Viet Securities - Investment Strategy Report May 2017

24

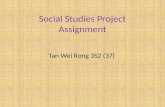

After reaching its peak of 731.33 points, the VNIndex experienced an adjustment period for 2 weeks with a decrease of 3.2%. The difficulty of the index increasing was apparent after large-cap stocks stopped leading the market during late March 2017, following the strong surge in the first quarter of this year. We believe that geopolitical factors were the main catalyst for the aggressive profit taking activities last month. Credit growth dramatically improved in Q1 2017. This movement surprised us because capital demand is usually low during the first quarter. As the results, it is possible that a part of credit flew to the stock market. As a result, liquidity successfully increased over the first 4 months of 2017, achieving an average of VND3,818 billion/session (+38% YoY). When manufacturing production is promoted from Q2 2017, consumers will borrow more from banks, and the capital for the stock exchange could gradually decline. Based on this, we expect that flows from foreign investors will continue to be poured into Vietnam’s stock exchanges. The market may further open up due to the additional room created from Pakistan being promoted to an emerging market this month, allowing Vietnam to take over some of this space. The classic statement “Sell in May” has been a frequently supported idea, which will continue to create a cautious sentiment for investors. Moreover, the annual general meeting season passed, and a large number of companies have announced Q1 business results. Therefore, the overall picture of business prospects for listed companies is quite clear at this moment, as a large amount of information has been announced during AGMs. After this period, there will be less supporting information for companies. Meanwhile, sudden global movements could continue to negatively impact Vietnam’s stock market. Therefore, we believe that May will be a favorable period for the market. However, the business results released in the first quarter may not immediately influence stock prices. Firms with a bright outlook in the remaining quarters of the year will still be able to maintain a fair price or reasonable price increase. We expect the VNIndex to fluctuate between 705 and 730 points with an average trading volume of around VND3,800 billion. In May, the domestic macroeconomic environment may not have much supporting news. Although the probability of a negative downturn is not high, we still do not advise investors to use margin during this period. . Analysis and Investment Advisory Truc Doan – Head of Research [email protected] Ha My Tran [email protected] Lam Nguyen [email protected] Thien Bui [email protected] Hieu Nguyen [email protected] Quang Vo [email protected] Huong Pham [email protected] Please see penultimate page for additional important disclosure Viet Dragon Securities Corp. (“VDSC”) is a foreign broker-dealer unregistered in the USA. VDSC research is prepared by research analysts who are not registered in the USA. VDSC research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities Inc, an SEC registered and FINRA-member broker- dealer. 620 650 680 710 740 0 50 100 150 200 250 300 20/01 10/02 24/02 10/03 24/03 10/04 24/04 Trading Volume (mil. shares) VNINdex (right axis) 07/05/2017 Investment Strategy May 2017 Optimistic Q1 2017 Earnings Season

-

Upload

thomas-farthofer -

Category

Economy & Finance

-

view

106 -

download

2

Transcript of Rong Viet Securities - Investment Strategy Report May 2017

After reaching its peak of 731.33 points, the VNIndex experienced an adjustment period for 2 weeks with a decrease of 3.2%. The difficulty of the index increasing was apparent after large-cap stocks stopped leading the market during late March 2017, following the strong surge in the first quarter of this year. We believe that geopolitical factors were the main catalyst for the aggressive profit taking activities last month.

Credit growth dramatically improved in Q1 2017. This movement surprised us because capital demand is usually low during the first quarter. As the results, it is possible that a part of credit flew to the stock market. As a result, liquidity successfully increased over the first 4 months of 2017, achieving an average of VND3,818 billion/session (+38% YoY). When manufacturing production is promoted from Q2 2017, consumers will borrow more from banks, and the capital for the stock exchange could gradually decline. Based on this, we expect that flows from foreign investors will continue to be poured into Vietnam’s stock exchanges. The market may further open up due to the additional room created from Pakistan being promoted to an emerging market this month, allowing Vietnam to take over some of this space.

The classic statement “Sell in May” has been a frequently supported idea, which will continue to create a cautious sentiment for investors. Moreover, the annual general meeting season passed, and a large number of companies have announced Q1 business results. Therefore, the overall picture of business prospects for listed companies is quite clear at this moment, as a large amount of information has been announced during AGMs. After this period, there will be less supporting information for companies. Meanwhile, sudden global movements could continue to negatively impact Vietnam’s stock market. Therefore, we believe that May will be a favorable period for the market. However, the business results released in the first quarter may not immediately influence stock prices. Firms with a bright outlook in the remaining quarters of the year will still be able to maintain a fair price or reasonable price increase.

We expect the VNIndex to fluctuate between 705 and 730 points with an average trading volume of around VND3,800 billion. In May, the domestic macroeconomic environment may not have much supporting news. Although the probability of a negative downturn is not high, we still do not advise investors to use margin during this period.

.

Analysis and Investment Advisory

Truc Doan – Head of Research

Ha My Tran

Lam Nguyen

Thien Bui

Hieu Nguyen

Quang Vo

Huong Pham

Please see penultimate page for additional important disclosure

Viet Dragon Securities Corp. (“VDSC”) is a foreign broker-dealer unregistered in the USA. VDSC research is prepared by research analysts who are not registered in the USA. VDSC research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities Inc, an SEC registered and FINRA-member broker-dealer.

620

650

680

710

740

0

50

100

150

200

250

300

20/01 10/02 24/02 10/03 24/03 10/04 24/04

Trading Volume (mil. shares) VNINdex (right axis)

07/05/2017

Investment Strategy May 2017

Optimistic Q1 2017 Earnings Season

Rong Viet Securities Corporation – Investment Strategy Report May 2017 2

CONTENTS

WORLD ECONOMY ................................................................................................................................................................................ 3 US: The Economy Lost Some Steam in Q1 .......................................................................................................................................................................... 3 EU: Growth Outlook Remains Intact ..................................................................................................................................................................................... 4 China: Q1 GDP Growth Signaled a Better Outlook .......................................................................................................................................................... 4

WORLD STOCK MARKETS..................................................................................................................................................................... 5 VIETNAM ECONOMY ............................................................................................................................................................................ 6

2017 Trade Outlook: Better Growth but Higher Deficit ................................................................................................................................................. 6 Industries Outlook from a Macro Perspective ................................................................................................................................................................... 7

VIETNAM STOCK MARKET APRIL: ONE CORRECTION PHASE DOSE NOT CHANGE THE BIG PICTURE ........................................... 9 STOCK MARKET OUTLOOKS .............................................................................................................................................................. 12 INVESTMENT STRATEGY .................................................................................................................................................................... 13

Based on these observations of the market, we believe that “surfing” or short-term investments contain higher levels of risk. Instead, investors should focus on companies with solid intermediate and long term plans.

Based on the Q1 2017 earnings of listed companies, an 8% YTD increase of the VNIndex is totally justified. Most companies recorded strong growth in profit not only from core businesses, but also extraordinary profits such as property sales and divestitures. Moreover, a large number of companies in certain sectors recovered from the previous bottom experienced. We recognize that businesses are gradually improving along with positive macroeconomic data, which provides a positive outlook for 2017. Furthermore, a statistical survey of 2017 business plans after annual general meeting season also demonstrated a positive picture for the market, as half of the companies projected revenue to increase by more than 10% YoY. Some of Rong Viet Research’s favorite sectors include construction, building materials, consumer good, hydropower and banking.

In spite of being the trough season, Q1 2017 business results from building materials companies, including stones and ceramic tiles, recorded impressive growth rates. To be more specific, profit after tax of several notable companies such as KSB, DHC, NNC and VIT improved by 83.4%, 58.0%, 7.1% and 83% YoY, respectively thanks to the improvement in output and business efficiency. The higher level of activity in the construction and real estate market in Q2 2017 will be a catalyst for positive growth of earnings for these sectors, as compared to previous quarters.

The probability of Tan Dong Hiep and Nui Nho quarries receiving an extension for 2 – 3 years has significantly improved, with a major consensus (93%) of local citizens. In addition to this, companies are also looking for new mines, acquiring others in the same industry (KSB, C32) and increasing capacity in existing quarries (DHA, KSB, NNC). Regarding VIT, the acquisition and renovation of My Duc brick factory will be a solution for its bottleneck issues, and providing strong future growth prospects for this year and the following year. Investment opportunities for DHA, NNC and VIT in the intermediate term are favorable.

Hydropower is also worth considering for intermediate-term investment objectives for the following reasons: (1) The interference between La Nina and El Nino caused high demand for electricity while bringing unseasonal rains in the Mid-Central, Central Highlands and the South. This resulted in high volume from hydropower during the first four months of 2017. Most hydropower plants recorded strong growth in profit, higher than the multi-year average and exceptionally high compared to the same period in 2016. Although there are many comments regarding the possibility of El Nino’s return in the second half of 2017, we think that this event will not be a significant area of concern, especially since the rainy season of the South began earlier; (2) In the first quarter of 2017, electricity consumption growth reached 8.3% YoY. In Q2 2017, the growth rate will be 12%, according to EVN's plan; and (3) The rising input price of thermal power plants (coal and gas) will enhance the advantage for hydropower plants in the CGM. Our favorite hydro plants are CHP, SHP, and VSH. However, the low level of liquidity is the major disadvantage that investors should pay attention to when investing in hydropower stocks. Instead, we think that REE might be a more suitable option with its current hydropower portfolio.

We also think that the construction, banking, textile and port sectors are noteworthy areas for investment. In terms of business results in Q1 2017, construction, banking, and textile companies have delivered stronger growth as compared to last year. We believe that the overall performance of these sectors will be stronger than 2016, as the prospects for the remaining three quarters are also very strong. Given the strong increase in terms of stocks prices in the first four months, we currently give a neutral recommendation for textile stocks and recommend investors to accumulate stocks in the remaining industries.

HIGHLIGHT STOCKS ............................................................................................................................................................................ 18 49 stocks of RongViet Research (analyzing, discussing with companies) and have analysis and specific evaluation in “Company report” or “Analyst pinboard”.

Rong Viet Securities Corporation – Investment Strategy Report May 2017 3

WORLD ECONOMY

• US: The Economy Lost Some Steam in Q1

• EU: Growth Outlook Remains Intact

• China: Q1 GDP Growth Signals a Better Outlook

In the first quarter of 2017, the economic growth of Asian countries outpaced the EU and US. Thanks to the recovery of the manufacturing sector and increased global demand, we expect that the growth momentum will strengthen or at least remain firm in the upcoming quarters of this year. The monetary policies of major central banks appear to be in line with market expectations. Moreover, the uncertainty in global trade policy has also eased. The USD is set to decline because political drivers have failed to boost it and the US wants a weaker USD. We expect that the CNY will depreciate due to structural outflow pressures, while the fall in GBP and EUR will be much more limited, according to HSBC’s forecast.

US: The Economy Lost Some Steam in Q1

In the first quarter of 2017, the economy expanded at the slowest pace in three years. The economy grew at 0.7% this quarter, below expectations of 1.1%. The deceleration in growth was mostly a result of weak consumption, which offset the rise in investment in housing and oil drilling and the rise in exports. Specifically, the dismal performance among US households was largely associated with lower auto sales and home-heating bills, and seasonal effects. As a result, the growth in private consumption decelerated abruptly from 3.5% in the last quarter of last year to 0.3% in Q1 2017. Meanwhile, fixed investments accelerated to a five year high (10.4% in Q1). The pickup in global demand also supported export growth, which experienced a 5.8% increase compared to a 4.5% drop in Q4 2016. Despite the deceleration in the economy being larger than expected, the US. Central Bank expects this downturn to be temporary. The FED now expects economic growth to range between 1.7%-2.3% in 2017.

In the third FOMC meeting held on the 2nd-3rd of May, the FED decided to leave its interest rates unchanged. The decision was broadly in line with market expectations, and the likelihood for an interest rate hike at the next meeting in June is 78.8%, according to the FedWatchTool. At the end of April, President Trump unveiled a tax cut plan for individuals and businesses. At the moment, there are still many unanswered questions about the feasibility of this plan. However, it seems that the Trump administration has now been able to support growth and has been less aggressive in trade protectionism.

Figure 1: US GDP Growth (Unit: %) Figure 2: Rate Hike Probability Historical for the next meeting

Source: Bloomberg Source: CMEGroup

-1.2

4

5

2.3 22.6

2

0.9 0.81.4

3.5

2.1

0.7

Q12

014

Q22

014

Q32

014

Q42

014

Q12

015

Q22

015

Q32

015

Q42

015

Q12

016

Q22

016

Q32

016

Q42

016

Q12

017

0%

20%

40%

60%

80%

05/0

4/20

1605

/20/

2016

06/0

8/20

1606

/24/

2016

07/1

3/20

1607

/29/

2016

08/1

6/20

1609

/01/

2016

09/2

0/20

1610

/06/

2016

10/2

4/20

1611

/09/

2016

11/2

8/20

1612

/14/

2016

01/0

3/20

1701

/20/

2017

02/0

7/20

1702

/24/

2017

03/1

4/20

1703

/30/

2017

04/1

8/20

17

Rong Viet Securities Corporation – Investment Strategy Report May 2017 4

EU: Growth Outlook Remains Intact

The Eurozone recorded a 1.9% YoY growth rate in Q1 2017, which was in line with market expectations. Growth was strong in markets such as Austria, Belgium and Spain, while economic activities lost some momentum in France during political events. The outlook of the region as a whole is stable with a strong labor market and a brighter global demand. The unemployment rate was unchanged at 9.5%, the lowest rate since May 2009 and lower than the average of 10% in 2016. Moreover, there is widespread optimism among firms in the manufacturing sector, highlighted by the multi-year high PMI data in April.

In the latest meeting, the ECB decided to hold interest rates and made no changes in its bond-buying programs. At the moment, there is a strong consensus that the ECB will keep the policy rate unchanged at the current level of 0% to support economic growth.

Figure 3: EU GDP Growth Figure 4: Improving Sentiment

Source: Bloomberg Source: Bloomberg

China: Q1 GDP Growth Signaled a Better Outlook

China’s GDP grew at an above-consensus 6.9% YoY in the first quarter of 2017 thanks to the marked recovery in investment and manufacturing. Industrial production rose 7.6% in March of 2017, accelerating from the 6.6% rise in the first two months of 2017. This was above market expectations and was the fastest growth since 2014. Simultaneously, fixed asset investments expanded 9.2% annually in the first 3 months experiencing the strongest growth in 10 months. Notably, manufacturing investment recovered after six years of decline. Export growth reached 8.2% YoY in Q1, a swift turnaround from the 7.7% decline in 2016. Because the recovery is spreading from manufacturing to private investments and exports, we expect that the economic outlook will improve in 2017.

Figure 5: China GDP Growth and Manufacturing PMI Figure 6: FAI Investment Growth

Source: Bloomberg Source: Bloomberg

2.1

2.2

2.1 2.1

1.8 1.8

1.9 1.9 1.9

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2015 2016 2017

-6

-4

-2

0

2

4

-10

-8

-6

-4

-2

0

04/1

6

05/1

6

06/1

6

07/1

6

08/1

6

09/1

6

10/1

6

11/1

6

12/1

6

01/1

7

02/1

7

03/1

7

Consumer Confidence Business Confidence

6.56.76.97.17.37.57.77.98.1

474849505152535455

01/1

3

04/1

3

07/1

3

10/1

3

01/1

4

04/1

4

07/1

4

10/1

4

01/1

5

04/1

5

07/1

5

10/1

5

01/1

6

04/1

6

07/1

6

10/1

6

01/1

7

GDP PMI

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

01/1

6

03/1

6

04/1

6

05/1

6

06/1

6

07/1

6

08/1

6

09/1

6

10/1

6

11/1

6

12/1

6

01/1

7

03/1

7

04/1

7

Rong Viet Securities Corporation – Investment Strategy Report May 2017 5

WORLD STOCK MARKETS

Figure 7: Performances of Major Global Stock Market Indices in April

Source: Bloomberg, RongViet Research

World stock markets in April were largely influenced by geopolitical tensions over Syria, North Korea and Afghanistan in the first two weeks, and only really flourished after candidate Emmanuel Marcon European Union support school) won the first round of the French presidential election.

The US market was supported by positive expectations regarding President Trump's new tax policy package, along with a slew of positive earnings reports. By the end of the month, the Dow Jones and S&P500 gained 1.34% and 0.91% respectively, while the Nasdaq kept climbing for the sixth consecutive month.

Global investors are looking to France, due to the country’s presidential election. The performance of stock markets in this country suggested that there isn’t likely another “Fraxit” ahead. The market sentiment was calm and tilted to the possibility that the next President would be Emmanuel Macron, who supported France staying in the EU. Except for the FTSE 100 of the UK, which fell 1.62% due to the unclear moves of Brexit, other indices such as CAC 40 and DAX were up from the closing price at the end of March.

The markets in Asia have been similar to other world markets, except China, although it is sending a positive signal from Q1 GDP growth. The Shanghai Composite Index fell by 0.54%. The reason for this is that investors are concerned that the Chinese government is increasingly tightening risk controls in the country's financial system, especially in the recent times when there are many warnings about the heat of the real estate market in this country. Other neighboring countries, such as Japan and South Korea, recorded a recovery in the second half of April (Nikkei 225 and Hang Seng rose 1.52% and 1.09%, respectively). It is worth mentioning that the South Korean Kospi Index rose in spite of severe geopolitical tensions between North Korea and the United States. This may reflect that the risk of war between the two Koreas and America is not high. This is in contrast to the Vietnamese market, where global geopolitical tensions were used to explain the downward movement of the VNIndex in April.

Overall, last April was relatively "quiet" for international stock markets. Although information about the US - North Korea appears quite dense, this reason was not enough for international investors to falter in the past month.

6% 6%

15%

1%

8% 8%

0%3%

12%

7%9%

7% 9% 8%

12%10%

-8%

-15%

-5%

5%

15%

25%

Dow

Jone

s

S&P

500

Nas

daq

FTSE

100

CAC

40

DA

X

Nik

kei 2

25

SSE

(Sha

ngha

i)

Han

g Se

ng (H

ongk

ong)

TSEC

(Tai

wan

)

Kosp

i (Ko

rean

)

JKSE

(Ind

ones

ia)

KLSE

(Mal

aysi

a)

VNIn

dex

(Vie

tnam

)

HN

X-In

dex

(Vie

tnam

)

Gol

d Oil

From 31/03/2017 to 28/04/2017 From 31/12/2016 to 28/04/2017

Rong Viet Securities Corporation – Investment Strategy Report May 2017 6

VIETNAM ECONOMY • 2017 Trade Outlook: Better Growth but Higher Deficit

• Industries Outlook from a Macro Perspective

Economic activities improved in April, most notably industrial production and consumption. The manufacturing sector is the main growth driver, which is largely dependent on the FDI sector. We will provide specific assessments for a variety of manufacturing industries in the note below.

During the first 4 months, banking liquidity remained stable as interbank rates remained below 5%, supporting credit growth in the economy. The SBV actively devalued the dong by adjusting the central exchange rate (0.88%). However, market exchange rates did not change much from the end of 2016, due to the weakness of the USD.

Because of the dismal performance of the mining industry, we revised our GDP growth forecast from 6.58% to 6.4%. Meanwhile, the strong recovery in trade could boost trade growth above our previous forecast. As a result, we raise our export growth forecast for 2017 from 10.4% to 14.1% and import growth from 11.9% to 18%.

2017 Trade Outlook: Better Growth but Higher Deficit

As we mentioned in our 2017 Strategy Report, there will be a recovery in trade despite the uncertainty in global trade policy. In the first 4 months of 2017, export growth was strong, above our expectations. Exports grew 16% YoY, much better than the growth rate of 6.7% in 2016. The improvement was mainly led by processing exports, such as electrical products (+45.5% YoY), machinery (+42.6% YoY), which displays the relatively positive performance of the FDI sector. Samsung’s operations had significant impacts on Vietnam’s exports. The abnormal growth of electrical products was due to Samsung Electronics HCMC CE Complex project, which began operating in June 2016. Meanwhile, negative growth in cellphone exports (-6% YoY) was an abnormal case, resulting from the Samsung Galaxy Note 7 crisis.

Export performance of domestic companies improved during the first 4 months of 2017, with a growth of 13.1% thanks to higher commodity prices. However, one of our most significant concerns is the imbalance in domestic trade. Imports grew 23% YoY, a dramatic gain from 0.3% in 2016. As a result, there was a deficit of ~USD7.9 billion in domestic trade in the first 4 months of 2017, a 53.4% YoY increase.

Performance of Vietnam’s exports to other markets varied substantially. Asian countries were the main drivers for export growth, while exports to the EU and US (key export partners of Vietnam) were not very encouraging in the first 4 months. Most notably, exports to China grew 45.1% YoY, equivalent to USD8.6 billion; exports to the US only grew 3.7% YoY (~USD11.9 billion).

Figure 8: Trade Growth Recovered in The First 4 Months Figure 9: Trade Growth by Key Partners

Source: Customs, RongViet Research Source: Customs, RongViet Research

-20%

-10%

0%

10%

20%

30%

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

Export Import

US: $11.9 bn (+3.7% YoY)

EU: $11.3 bn (+8.8% YoY)

China: $8.6 bn (+45.1% YoY)

ASEAN: $6.7 bn (+26.0% YoY)

Japan: $5.2 bn (+19.3% YoY)

Korea: $4.4 bn (+32.0% YoY)

EXPORTS

China: $17.6 bn (+19.4% YoY)

Korea: $13.7 bn (+45.3% YoY)

ASEAN: $8.9 bn (+20.4% YoY)

Japan: $5.1 bn (+16.9% YoY)

EU: $3.8 bn (+24.3% YoY)

US: $3.0 bn (+23.1% YoY)

IMPORTS

Rong Viet Securities Corporation – Investment Strategy Report May 2017 7

Currently, we see three elements supporting the outlook of trade in 2017:

1. External outlook improving: The first meeting between President Xi and President Trump significantly reduced the risk of a head-on confrontation over trade. We think this is a good signal for not only China but also Vietnam. In addition, TPP countries kick-started discussions towards implementing the pact without the US at the beginning of May 2017. There is now hope that the TPP pact will come alive and support trade growth. Last but not least, the economic outlook of Asian countries became brighter in the first quarter of 2017, pointing to a significant improvement in demand.

2. Steadied FDI flows: Because the FDI sector has taken a great part in Vietnam trade turnovers (~70%), there is no doubt that past investments will contribute to future growth in exports. SEHC, LG Display, and LG Innotek, are some big names that could influence export growth in the short term.

3. There was a pause in the recovery of commodity prices, mainly due to the supply side. However, for commodity-exporting domestic companies, the rebound in prices in 2016 still give them room to grow on a year over year basis.

Based on the above rationales, we raise our export growth forecast for 2017 from 10.4% to 14.1% and import growth from 11.9% to 18%. We estimate that the trade deficit will be $5 billion in 2017, a significant change from a surplus of $1.5 billion in 2016.

Industries Outlook from a Macro Perspective

The breakdown on manufacturing data displays a considerable level of discrepancy in performance for each industry in the first quarter of 2017. Production indicators that performed strongly include the following areas: steel, electrical products and cable industries. There was also very positive demand for products such as milk, fertilizers, electrical products, storage batteries, automobiles and cable industries. It is worth noting that inventory surged in the first quarter of 2017, mainly due to a sharp increase of assembled cars (Thaco Truong Hai) and the declining growth momentum in the steel industry.

From a macro perspective, we expect that the mining sector will be in a more challenging phase. Crude production growth decreased by 14.5% in the first 4 months of 2017. Because the supply gut continues to weigh on oil prices as well as Vietnam’s oil operators, we adjust our 2017 GDP growth forecast from 6.58% to 6.4%.

In Q1 2017, the biggest outperformers came from fiber, fertilizer, electrical products and cable industries. We think companies operating in these industries can continue to perform well. In the absence of a significant rebound in the inflation rate, we expect consumer goods companies to remain positive. In addition, the recovery in textile exports could brighten the 2017 business outlook of textile companies.

Rong Viet Securities Corporation – Investment Strategy Report May 2017 8

Table 1: Manufacturing Activities by Sub-sectors in Q1 2017

Unit: % Production

Growth* Consumption

Growth Inventory

Growth Export

Growth Import

Growth Rating

Crude oil -14.2 Na Na 24.3 27.0 - -

Natural gas, LPG -8.4 Na Na Na 37.4 ~

Fishery 3.0 10.5 13.6 7.6 34.5 ~

Milk 9.3 12.7 1.3 Na -9.6 +

Sugar -2.0 -26.0 4.2 Na Na -

Animal Feeds 12.1 5.1 -21.6 6.0 37.3 ~

Beer 10.3 7.8 45.4 Na Na ~

Fiber 14.2 16.0 -5.2 29.9 23.0 ++

Textile 8.8 8.5 -6.4 10.9 Na +

Shoes & Leather 3.0 6.7 10.5 14.1 Na ~

Paper 7.0 8.0 32.8 Na 19.4 +

Fertilizer 12.5 16.6 -46.0 68.1 21.9 ++

Pharmaceutical 4.5 2.4 3.8 Na 6.4 ~

Plastic 8.5 8.0 23.0 11.9 19.3 +

Cement 7.3 1.8 92.3 6.9 Na ~

Steel 47.5 9.5 54.5 77.7 37.3 +

Telephones -10.4 -27.3 49.5 -6.1 22.6 -

Electrical products 23.3 29.5 14.0 45.5 11.9 ++

Storage battery 4.8 14.0 17.5 Na Na +

Cable 20.8 19.6 5.2 23.7 18.7 ++

Automobile 10.9 17.2 220.8 22.5 -1.5 +

Electricity 9.3 Na Na Na Na ~

Water 6.8 Na Na Na Na ~

Source: GSO, Customs, RongViet Research, *4M2017 vs 4M2016

Seriously negative Negative growth in production, consumption, significant increase in inventory - -

Negative Below-average growth in production, consumption, significant increase in inventory -

Neutral Production, consumption and inventory remain stable compared to the same period ~

Positive Positive growth in production, consumption, inventory remains stable +

Very positive High growth in production, consumption, inventory remains stable + +

Rong Viet Securities Corporation – Investment Strategy Report May 2017 9

VIETNAM STOCK MARKET APRIL: ONE CORRECTION PHASE DOSE NOT CHANGE THE BIG PICTURE

The first significant correction of the market finally occurred in April. The strong profit taking coincided with various geopolitical tensions, which caused the VN-Index to plummet from 731.33 points on April 11th to 707.58 points on April 25th. However, the index gradually recovered from this decline by the end of April; the VN-Index reached 717.73 points, up 8% from the beginning of the year (7% excluding ROS), while the HNX-Index reached 89.54 points, up 11.8%. The strong increase indicates the market's high expectations for business prospects, and this time it seems the market was right. The recently announced Q1 results of 545 companies displayed a positive picture for the market.

Figure 10: VN-Index movement in April Figure 11: HNX-Index movement in April

Source: RongViet Research Source: RongViet Research

Large and mid-cap stocks had excellent Q1 results overall. The total NPAT of 26/30 companies in the VN-30 basket delivered growth of 27%, with only six companies experiencing negative growth (BMP, DPM, KDC, MSN, NT2 and PVD). For the VN-MID basket, the figure was even more impressive. Enterprises such as PPC, DCM, HBC, PNJ, DXG, NKG, VSH, SHP, SAM, PHR, KSB, STK, PDR, and ELC delivered earnings growth from 70% to over 200% over the same period. This robust growth has justified the rally of the VN-MID since the beginning of this year.

Figure 12: Revenue and NPAT Growth of the Main Index in Q1 2017

Source: FiinPro, RongViet Research *excluding CII and STG

680

700

720

740

0

50

100

150

200

250

300

20/01 10/02 24/02 10/03 24/03 10/04 24/04

Trading Volume (mil. shares) VNINdex (right axis)

79

83

87

91

95

0

30

60

90

20/01 10/02 24/02 10/03 24/03 10/04 24/04

Trading Volume (mil. shares) HNXIndex (right axis)

8.3%

17.7%

9.3% 8.0%11.8%

20.7%

8.4% 7.9%

14.1%10.5%

26.9%

38.1%

8.0%

27.7%24.0%

VN-30 VN-MID VN-SML HOSE HNX

Performance YTD Revenue NPAT

Rong Viet Securities Corporation – Investment Strategy Report May 2017 10

The financial services sector led in profitability growth. The strong activity of the stock market in Q1 has led to a sharp increase in the average daily trading value and margin lending, which in turn boosted the earnings of brokerage firms. However, these positive business results were not fully reflected in the stock price. The stock price of top brokerage firms like VND, SSI, and HCM have only increased by less than 20% YTD.

However, there are still dark spots for earnings results in Q1. The operations of two oil & gas companies, PVS and especially PVD, have still not improved. PVD reported a loss for the first time since the beginning of the low oil price era in 2014. The automobile & parts sector also experienced some troubles, as HTL, HSC, TMT, DRC, SRC, CSM, and VKC all had negative growth. Meanwhile, the insurance, chemicals, and travel & leisure sectors only achieved single digit growth in earnings.

Figure 13: Revenue and NPAT Growth of Sectors in Q1 2017

Source: FiinPro, RongViet Research *excluding CII and STG, which have abnormal financial income (CII: VND1,300 billion, STG: VND571 billion)

The highlight of Q1 results is the improvement of the margins of companies. Although the improvement can be partly attributed to abnormal financial income of some companies, it is still a combination of good control in COGS, selling and administration expenses.

Figure 14: Gross and Net Margin of Sectors in Q1 2017

Source: FiinPro, RongViet Research *excluding CII and STG

-20%

-10%

0%

10%

20%

30%

-100%

0%

100%

200%

Retail

Insurance

Real Estate

Technology

Oil &

Gas

Financial Services

Utilities

Travel & Leisure

Industrial Goods &

Services

Personal & H

ouseholdG

oods

Chemicals

Banks

Autom

obiles & Parts

Basic Resources

Food & Beverage

Media

Construction &M

aterials

Health Care

Revenue NPAT Performance (YTD)

17.2%18.1%

8.2%9.2%

0%

10%

20%

30%

40%

50%

Retail

Insurance

Real Estate

Technology

Oil &

Gas

Financial Services

Utilities

Travel & Leisure

Industrial Goods &

Services

Personal & H

ouseholdG

oods

Chemicals

Banks

Autom

obiles & Parts

Basic Resources

Food & Beverage

Media

Construction & M

aterials

Health Care

Total

Gross margin Q1 2016 Gross margin Q1 2017 Net margin Q1 2016 Net margin Q1 2017

Rong Viet Securities Corporation – Investment Strategy Report May 2017 11

April is a peak time in Vietnam’s stock market, with a large number of AGM sessions taking place. Our overall impression after attending the AGMs of our coverage list is fairly optimistic. Statistics for the 2017 business plans of 349 listed companies has also confirmed our view, as half of these have targeted at least 10% growth in revenue. Considering what these companies have achieved so far in Q1, the optimism seems to be reasonable.

Figure 15: 2017 Revenue Plan vs 2016 Actual Revenue

Source: FiinPro, RongViet Research

Companies have started off on the right foot, and expect to maintain this momentum through Q2. Consequently, we retain our positive view regarding the market in Q2, but still leave room for some possible corrections down the road. We would also like to remind investors about the dividend payment schedule in May, as the dividend season has still continued.

Figure 16: Foreign Investors trading in the first 4 months

Source: FiinPro, RongViet Research

22%

10%

16%28%

12%

5%3% 3%

(+)30%

(+)20%-30%

(+)10%-20%

(+)0-10%

(-)0-10%

(-)10%-20%

(-)20%-30%

(-)30%

0

1000

2000

3000

4000

5000

6000

7000

-400

-300

-200

-100

0

100

200

300

400

500

600

03/01 21/03

Net bought/sold Accumulated Value

Rong Viet Securities Corporation – Investment Strategy Report May 2017 12

STOCK MARKET OUTLOOKS

After reaching its peak of 731.33 points, the VNIndex experienced an adjustment period for 2 weeks with a decrease of 3.2%. The difficulty of the index increasing was apparent after large-cap stocks stopped leading the market during late March 2017, following the strong surge in the first quarter of this year. We believe that geopolitical factors were the main catalyst for the aggressive profit taking activities last month.

Credit growth dramatically improved in Q1 2017. This movement surprised us because capital demand is usually low during the first quarter. As the results, it is possible that a part of credit flew to the stock market. As a result, liquidity successfully increased over the first 4 months of 2017, achieving an average of VND3,818 billion/session (+38% YoY). When manufacturing production is promoted from Q2 2017, consumers will borrow more from banks, and the capital for the stock exchange could gradually decline. Based on this, we expect that flows from foreign investors will continue to be poured into Vietnam’s stock exchanges. The market may further open up due to the additional room created from Pakistan being promoted to an emerging market this month, allowing Vietnam to take over some of this space.

The classic statement “Sell in May” has been a frequently supported idea, which will continue to create a cautious sentiment for investors. Moreover, the annual general meeting season passed, and a large number of companies have announced Q1 business results. Therefore, the overall picture of business prospects for listed companies is quite clear at this moment, as a large amount of information has been announced during AGMs. After this period, there will be less supporting information for companies. Meanwhile, sudden global movements could continue to negatively impact Vietnam’s stock market. Therefore, we believe that May will be a favorable period for the market. However, the business results released in the first quarter may not immediately influence stock prices. Firms with a bright outlook in the remaining quarters of the year will still be able to maintain a fair price or reasonable price increase.

We expect the VNIndex to fluctuate between 705 and 730 points with an average trading volume of around VND3,800 billion. In May, the domestic macroeconomic environment may not have much supporting news. Although the probability of a negative downturn is not high, we still do not advise investors to use margin during this period.

Table 2: Key sectors performance

No Name % 1M Price Change

% 3M Price Change

% 12M Price Change

Market Cap (VND Billion)

ROA (%)

ROE (%) Basic P/E P/B

1 Retail -1.3% 4.3% 90.7% 29,475 8.0% 25.1% 13.7 5.2 2 Insurance -2.7% -2.0% 9.1% 60,182 2.3% 8.7% 21.9 2.4 3 Real Estate 0.4% 9.2% 13.7% 229,278 1.6% 4.6% 20.7 3.1 4 Technology -1.3% 3.2% 18.0% 27,625 6.4% 14.0% 11.6 2.0 5 Oil & Gas -10.4% -12.5% -11.2% 15,224 1.5% 2.7% 15.2 0.6 6 Financial Services -4.2% 9.7% 7.8% 27,725 2.6% 4.9% 10.9 1.2 7 Utilities 2.1% -3.7% 14.5% 145,621 10.4% 17.2% 12.7 2.3 8 Travel & Leisure -1.8% 11.9% 2.7% 8,016 3.1% 5.0% 11.9 2.4 9 Industrial Goods & Services 0.5% 4.8% 15.1% 70,388 6.1% 11.9% 10.9 1.7

10 Personal & Household Goods 4.9% 8.3% 20.0% 27,353 8.7% 19.1% 13.0 3.2 11 Chemicals 1.7% 5.3% 5.6% 40,951 7.0% 11.8% 9.9 1.3 12 Banks -3.2% -2.7% 9.2% 341,903 0.7% 11.0% 14.4 1.6 13 Automobiles & Parts 2.0% 7.1% -4.5% 17,588 7.9% 14.8% 13.5 1.7 14 Basic Resources -0.8% 7.8% 30.2% 68,845 8.4% 20.8% 6.1 1.4 15 Food & Beverage 1.5% 2.8% 37.3% 330,368 7.6% 17.1% 18.8 5.9 16 Media 4.6% 7.6% 18.4% 2,351 5.4% 9.4% 16.5 1.8 17 Construction & Materials -2.2% 13.1% 101.9% 181,988 4.8% 13.3% 16.7 4.5 18 Health Care 1.4% 19.1% 56.3% 28,307 4.6% 9.1% 16.4 3.5

Source: RongViet Research, FiinPro

Rong Viet Securities Corporation – Investment Strategy Report May 2017 13

INVESTMENT STRATEGY

Based on these observations of the market, we believe that “surfing” or short-term investments contain higher levels of risk. Instead, investors should focus on companies with solid intermediate and long term plans.

Based on the Q1 2017 earnings of listed companies, an 8% YTD increase of the VNIndex is totally justified. Most companies recorded strong growth in profit not only from core businesses, but also extraordinary profits such as property sales and divestitures. Moreover, a large number of companies in certain sectors recovered from the previous bottom experienced. We recognize that businesses are gradually improving along with positive macroeconomic data, which provides a positive outlook for 2017. Furthermore, a statistical survey of 2017 business plans after annual general meeting season also demonstrated a positive picture for the market, as half of the companies projected revenue to increase by more than 10% YoY. Some of Rong Viet Research’s favorite sectors include construction, building materials, consumer good, hydropower and banking.

In spite of being the trough season, Q1 2017 business results from building materials companies, including stones and ceramic tiles, recorded impressive growth rates. To be more specific, profit after tax of several notable companies such as KSB, DHC, NNC and VIT improved by 83.4%, 58.0%, 7.1% and 83% YoY, respectively thanks to the improvement in output and business efficiency. The higher level of activity in the construction and real estate market in Q2 2017 will be a catalyst for positive growth of earnings for these sectors, as compared to previous quarters.

The probability of Tan Dong Hiep and Nui Nho quarries receiving an extension for 2 – 3 years has significantly improved, with a major consensus (93%) of local citizens. In addition to this, companies are also looking for new mines, acquiring others in the same industry (KSB, C32) and increasing capacity in existing quarries (DHA, KSB, NNC). Regarding VIT, the acquisition and renovation of My Duc brick factory will be a solution for its bottleneck issues, and providing strong future growth prospects for this year and the following year. At the current price level, investment opportunities for DHA, NNC and VIT in the intermediate term are favorable.

Stock picks Target price Horizon Investment Thesis

DHA N/a Intermediate • We expect that consumption at its main quarry, Thanh Phu, will improve after the bridge collapse incident, which has been overcome, as well as the breakers has been transferred to the new treated areas.

• Positive growth in output for Tan Cang and Nui Gio quarries, thanks to the improvement in demand from areas of these quarries and Western region.

• The divestiture from financial investments will support cash flows for future quarry acquisitions and investment in new building materials.

• Dividend yield is stable, at nearly 7%.

NNC 90,100 Intermediate • High possibility for the expansion of Nui Nho after receiving approval from local citizens. Moreover, there is a huge demand from infrastructure construction activities in HCM City and Binh Duong.

• Boosting consumption in Tan Lap quarry leads to the improvement in revenue and profit margin.

• Ability to successfully acquire new quarries in order to maintain its core business.

• Business performance exceeds the industry average.

VIT 36,000 Long-term • Revenue growth from its new My Duc factory.

• Increase in gross margin thanks to technology improvements, decline in shrinkage rate and focusing more on products with higher added-value.

• Local granite tile consumption prospects (VIT’s products) will grow by more than 20%/year according to the Ministry of Construction.

Rong Viet Securities Corporation – Investment Strategy Report May 2017 14

Hydropower is also worth considering for intermediate-term investment objectives for the following reasons:

(1) The interference between La Nina and El Nino caused high demand for electricity while bringing unseasonal rains in the Mid-Central, Central Highlands and the South. This resulted in high volume from hydropower during the first four months of 2017. Most hydropower plants recorded strong growth in profit, higher than the multi-year average and exceptionally high compared to the same period in 2016. Although there are many comments regarding the possibility of El Nino’s return in the second half of 2017, we think that this event will not be a significant area of concern, especially since the rainy season of the South began earlier.

(2) In the first quarter of 2017, electricity consumption growth reached 8.3% YoY. In Q2 2017, the growth rate will be 12%, according to EVN's plan.

(3) The rising input price of thermal power plants (coal and gas) will enhance the advantage for hydropower plants in the CGM.

However, the low level of liquidity is the major disadvantage that investors should pay attention to when investing in hydropower stocks. Instead, we think that REE might be a more suitable option with its current hydropower portfolio including 8 companies (1 Subsidiary, 5 Affiliated companies and 2 Long-term financial investments).

PPC, a thermal power plant company, is also another stock worth noting, as it has begun recovering from its bottom, and is a strong pick for investors with an intermediate term horizon.

Stock Picks Target Price Time Horizon Investment Rationales

CHP 25,000 Intermediate-term

• Revenue and PAT in Q1 2017 increased by 158% and 14.8% respectively.

• Favorable hydrological conditions and the growing demand for electricity will support the company during the remaining quarters of 2017.

• We expect that its PAT will reach VND356 billion during 2017, corresponding to an EPS of VND2,695.

• The Cash dividend for 2016 and 2017 was approved by the AGM at VND1,600 dong/share and VND1,500 – 1,700/share.

SHP 22,800 Intermediate-term

• Revenue increased by 112% YoY and PAT in Q1 2017 was VND -12 billion (Q12016: VND -54 billion)

• Favorable hydrological conditions and growing demand for electricity will support the company during the remaining quarters of 2017.

• We expect that the company’s PAT will be VND356 billion in 2017, corresponding to an EPS of VND2,695.

VSH N/a Long-term • Revenue and PAT of Q1 2017 increased by 83% and 97% respectively.

• Favorable hydrological conditions and growing demand for electricity will support the company during the remaining quarters of 2017.

• The participation of REE will bring about positive changes in VSH's corporate governance.

REE 35,500 Long-term • Revenue and PAT of Q1 2017 increase 97% and 217% respectively.

• Positive outlook of the company’s power sector thanks to (1) Positive outlook of hydropower and (2) PPC's debt repayment before maturity will help consolidated profit from this company, and it will no longer has much fluctuations due to exchange rate fluctuations.

• The remaining business sectors followed our expectations.

• We expect that its PAT for 2017 will be VND1,175 billion, corresponding to an EPS of VND3,791.

PPC 19,400 Intermediate-term

• Revenue and PAT of Q1 2017 reached VN1,476 billion and VND142 billion (Q12016: VND -158 billion) due to (1) The sharp increase in average selling prices of PL1, (2) the VND32billion profit from divestment in a subsidiary (3) the decrease in foreign exchange losses.

• Exchange rate risks decreases since PPC plans to prepay its debt before maturity. In which, the company will pay JPY16 billion in the first half of 2017 with funds from (1) cash and short-term bank deposits and (2) short-term commercial bank loans (if necessary). We forecast that the company’s net interest income will be around VND200 billion (-25% YoY).

Rong Viet Securities Corporation – Investment Strategy Report May 2017 15

• We expect that its PAT for 2017 will be VND719 billion (+31% YoY), corresponding to EPS of VND2,096.

We also think that the construction, banking, textile and port sectors are noteworthy areas for investment. In terms of business results in Q1 2017, construction, banking, and textile companies have delivered stronger growth as compared to last year. We believe that the overall performance of these sectors will be stronger than 2016, as the prospects for the remaining three quarters are also very strong. Given the strong increase in terms of stocks prices in the first four months, we currently give a neutral recommendation for textile stocks and recommend investors to accumulate stocks in the remaining industries.

Newly listed stocks have been attracting the attention of investors over the last few years. Rong Viet Research would like to introduce several stocks which have been recently listed or under the procedure to be listed in the future.

CTCP Siam Brother (SBG – HSX)

• CTCP Siam Brother (SBG) was approved to be listed and will begin trading on the HSX (20.54 million shares) at VND 40,000/share this month (16/5/2017).

• Siam Brother is a longtime brand (over 50 years) in rope production and distribution in Thailand. The company started to penetrate Vietnam’s market in 199, and currently accounts for 40% of the market. Siam Brother is leading the market with 2.5 times the scale of company in 2nd position.

• SBG’s business results grew continuously, even during Vietnam’s economic downturn. During 2012 – 2016, revenue and profit after tax of SBG achieved CARG of 12.0% and 22.6% respectively. The company’s profit margin has gradually improved and is currently at a high level. The company’s gross margin and net margin for 2016 were 42.5% and 22.4% respectively.

• Existing factories reached the maximum designed capacity. The company’s new factory is projected to have capacity of 3,000 tons/year, equivalent to 30% of current capacity and will begin operating in July of 2017.

• With ample room for growth from the agriculture market, and its increased focus on exports, RongViet Research expects the demand prospects to be positive. In 2017, SBG targets to achieve VND601.28 billion in revenue and VND 149.77 billion in PAT, equivalent to EPS of VND6,000. Furthermore, SBG has an attractive cash dividend (nearly 10%).

Loc Troi Group

• Loc Troi, formerly known as An Giang Plant Protection Joint Stock Company, was established in 1993 and was equitized in September 2004 with chartered capital of VND150 billion. Currently, the company has a chartered capital of VND672 billion and is targeting a vertical agricultural value chain, with its three main segments including pesticides, rice and seeds. The

Rong Viet Securities Corporation – Investment Strategy Report May 2017 16

company’s pesticide segment has been maintaining a strong growth rate and a gross margin of 31% - 33%, well above the sector average of 24.6%. The company’s seed segment is still fairly stable with a gross margin of 35%, despite strong competition from the NSC. The only segment that is struggling is its rice segment, due to the unfinished production value chain and unfavorable weather conditions.

• In 2017, Loc Troi plans to achieve revenue growth of 6.5%, equivalent to VND8,857 billion, which will primarily be driven by its plant and medicine segment, while it expects for its rice segment to experience negative growth. We expect that the company’s pesticides and seeds segments will achieve positive growth. The company plans for its PBT and PAT to reach VND597 billion (+28.7% YoY) and VND460 billion (+31.8% YoY). According to this plan, EPS in FY2017 will be VND5,822 (+32% YoY). We think that this plan is quite ambitious due to (1) unfavorable weather conditions, its incomplete value chain, and new business lines that have not been implemented. Unfavorable weather conditions are a key negative factor for this company, as seen by rice exports falling by 8% YoY during the first four months of this year.

• There are 3 highlights of the company’s FY2017 business plan. (1) Loc Troi will sign a joint venture with China to export rice to this market in May 2017. (2) The company will develop a value chain in fruit trees with HAG after its initiation in 3 western provinces, including Tien Giang, Ben Tre and Vinh Long. (3) Finally, Loc Troi will also begin growing coffee, as it has been doing with rice products since 2010. The company’s fruit tree and coffee projects will take Loc Troi a very long time to implement, and it will take time before they begin to significantly impact its business.

• 67 million shares of Loc Troi might be listed on UPCOM by the end of this May. Changes in shareholder structure, namely a new major shareholder of Viet Nam Marina Ltd, has just received a 25.5% transfer from Standard Charter Private Equity, which may be a sign for this listing.

• Currently, there aren’t many shares in the agribusiness and Loc Troi is a notable one as it is targeting a vertical value chain in this sector. Although Loc Troi plant protection products are comparatively favorable to its competitors, its rice and seed products are still in the process of improvement. Although there are many companies working in the same fields (food and seedlings) with Loc Troi, their firm size is relatively small, and has a low product value, and undefined brand and output. Loc Troi has the ability to take advantage of its chain to promote its competitive advantages.

• The company’s forward P/E at present is 9.9 times, based on its growth plans and current OTC price. We hold the view that Loc Troi’s shares are undervalued. However, investors should note that the investment period should be long term, and it will take a long time for the company to put its agribusiness chain into operation

• In addition, there are some risks to investing in Loc Troi shares such as: (1) objective factors in the industry such as weather and diseases (2) risk of instability in agricultural policy, and (3) many product value chains that are deployed at the same time but are not yet effective.

In addition, the correction of the market in the month will also be the opportunity to accumulate stocks for long-term investment objectives. RongViet Research’s favorite stocks are those with leading role in their industry or those in sectors that expect to see positive changes in the recovery of the economy or the supportive of policies.

Figure 17: RongViet Research’s stock pick

Rong Viet Securities Corporation – Investment Strategy Report May 2017 17

Source: RongViet Research; Price @ May 5th, 2017

Rong Viet Securities Corporation – Investment Strategy Report May 2017 18

Ticker Exchange Target price

(VND)

Price @ May 5th

(VND)

Upside (%)

Rating Time horizon

2016 2017F 2018F PER

Trailing (x)

PER 2017F

(x)

PBR Cur. (x)

Div Yield

(x)

+/- Price

1y (%)

3M avg. daily vol.

(‘1000 shares)

3M avg. daily turnover

(USD thousand)

Market cap

(USD mn)

Foreign remaining

room (%)

+/- Rev. (%)

+/- NPAT

(%)

+/- Rev. (%)

+/- NPAT

(%)

+/- Rev. (%)

+/- NPAT

(%)

ACV UPCOM 67,000 49,100 36.5 Buy Long-term 21.1 198.2 16.2 -20.1 17.1 26.3 31.0 22.3 4.3 1.0 0.0 287 644 4,699 45.6

FPT HSX 63,500 47,100 34.8 Buy Long-term 4.1 3.1 23.6 32.9 15.0 32.4 10.5 8.2 2.2 4.2 18.5 988 2,014 955 -

ITD HSX 33,900 25,400 33.5 Buy Intermediate-term 57.5 137.8 19.9 19.0 N/a N/a 7.3 6.0 1.6 2.4 47.3 136 162 21 31.9

TNG HNX 17,000 12,800 32.8 Buy Intermediate-term -1.9 13.9 17.0 16.5 10.5 11.1 5.3 5.3 0.8 0.0 -28.9 128 76 19 26.5

PHP HNX 20,800 15,700 32.5 Buy Intermediate-term 2.2 3.9 -0.6 6.5 8.0 9.6 11.6 11.9 1.5 5.1 -21.6 6 5 226 48.6

VSC HSX 73,700 56,500 30.4 Buy Long-term 16.6 -10.0 18.2 23.8 6.0 9.6 10.3 9.2 1.8 6.2 11.9 121 313 113 -

DRC HSX 35,900 28,150 27.5 Accumulate Long-term 1.3 -4.8 17.4 -1.3 14.4 7.9 8.9 9.3 2.0 8.0 -15.1 373 513 147 18.3

PC1 HSX 48,000 38,100 26.0 Accumulate Long-term -3.0 24.1 13.4 3.7 48.1 93.6 10.4 12.7 1.4 0.0 0.0 193 328 126 24.0

VIT HNX 36,000 28,800 25.0 Accumulate Long-term 41.6 53.5 17.8 18.4 33.4 25.7 7.1 6.7 1.9 5.2 25.8 35 46 19 46.2

HPG HSX 36,000 29,200 23.3 Accumulate Long-term 21.2 89.4 30.7 13.2 19.4 4.4 4.9 5.3 1.2 0.0 48.5 4,229 7,049 1,622 12.3

PTB HSX 153,600 125,200 22.7 Accumulate Long-term 20.2 52.8 25.6 25.5 16.1 9.8 10.0 9.1 3.6 0.0 29.5 68 396 119 37.8

PVT HSX 15,400 12,700 21.3 Accumulate Long-term 16.9 12.9 6.2 1.3 10.6 10.0 8.0 9.0 1.0 7.9 28.9 745 424 157 23.8

REE HSX 35,500 29,300 21.2 Accumulate Long-term 38.4 28.2 23.1 19.0 6.4 13.7 6.8 7.7 1.3 1.7 50.5 1,222 1,468 399 -

VFG HSX 90,700 74,900 21.1 Accumulate Long-term 13.4 5.2 9.6 16.2 6.1 7.6 9.8 9.0 1.7 1.3 21.0 10 32 60 27.7

CTD HSX 237,700 200,500 18.6 Accumulate Long-term 52.0 113.5 30.4 22.2 9.9 9.8 9.3 9.5 2.4 2.7 60.5 193 1,679 678 5.1

CTG HSX 21,000 17,750 18.3 Accumulate Long-term 16.3 20.0 8.2 17.3 7.4 14.5 9.6 8.2 1.1 3.9 10.8 1,600 1,289 2,904 -

BFC HSX 41,000 35,000 17.1 Accumulate Long-term -1.6 21.0 17.8 18.4 15.8 10.1 6.7 6.8 2.1 8.6 52.7 252 389 88 32.1

MBB HSX 19,400 16,700 16.2 Accumulate Long-term 12.4 16.7 16.5 16.7 7.4 18.4 9.4 9.2 1.1 1.8 21.1 1,211 812 1,257 -

VCB HSX 41,700 36,100 15.5 Accumulate Long-term 17.3 28.6 7.7 14.1 12.9 32.0 18.1 16.3 2.6 2.2 5.6 1,201 1,972 5,706 9.4

PHR HSX 30,600 26,500 15.5 Accumulate Intermediate-term -4.0 3.9 61.0 48.6 20.0 11.0 6.7 8.2 0.9 3.8 40.3 711 918 91 44.9

SHP HSX 22,800 19,800 15.2 Accumulate Intermediate-term -13.7 -40.4 19.7 78.7 -0.3 1.0 13.2 10.6 1.6 8.1 17.6 23 20 82 45.2

PGS HNX 20,900 18,200 14.8 Accumulate Intermediate-term -16.5 206.7 23.2 -65.5 9.7 9.3 9.3 7.8 0.9 6.9 14.8 418 326 40 32.8

CDN HNX 27,200 23,800 14.3 Accumulate Intermediate-term -3.5 2.1 16.0 8.9 26.9 4.3 11.4 12.2 1.8 4.2 0.0 4 4 69 48.6

BMP HSX 208,400 182,400 14.3 Neutral Long-term 18.5 20.9 11.2 7.9 13.1 10.0 15.8 13.6 3.5 4.2 30.3 75 641 364 0.3

HIGHLIGHT STOCKS

Rong Viet Securities Corporation – Investment Strategy Report May 2017 19

Ticker Exchange Target price

(VND)

Price @ May 5th

(VND)

Upside (%)

Rating Time horizon

2016 2017F 2018F PER

Trailing (x)

PER 2017F

(x)

PBR Cur. (x)

Div Yield

(x)

+/- Price

1y (%)

3M avg. daily vol.

(‘1000 shares)

3M avg. daily turnover

(USD thousand)

Market cap

(USD mn)

Foreign remaining

room (%)

+/- Rev. (%)

+/- NPAT

(%)

+/- Rev. (%)

+/- NPAT

(%)

+/- Rev. (%)

+/- NPAT

(%)

NNC HSX 90,100 79,500 13.3 Accumulate Intermediate-term 14.9 49.8 23.5 25.7 8.1 3.4 7.1 7.6 2.9 4.1 55.6 30 100 57 28.3

VNR HNX 27,300 24,200 12.8 Neutral Long-term 0.0 -1.2 18.2 9.7 4.3 6.8 12.7 12.1 1.2 6.2 34.6 81 89 139 19.2

NT2 HSX 31,900 28,900 10.4 Neutral Long-term 18.6 -4.9 -13.2 -10.6 4.5 0.3 8.0 9.0 1.6 8.8 6.2 336 456 366 26.7

PPC HSX 19,400 17,900 8.4 Neutral Long-term -22.0 -2.2 17.7 33.0 1.8 -3.3 6.8 8.5 1.0 10.9 13.9 74 56 250 32.3

DPM HSX 25,000 23,250 7.5 Neutral Long-term -18.8 -23.3 16.4 4.9 20.5 -3.8 9.6 8.9 1.1 8.6 -12.2 1,020 1,090 400 29.5

CHP HSX 25,000 23,350 7.1 Neutral Intermediate-term -10.9 -21.5 22.2 38.1 -10.2 -10.8 7.6 8.7 1.6 6.9 0.0 130 126 129 45.6

PGI HSX 24,900 23,600 5.5 Neutral Long-term 0.0 5.2 10.3 55.5 13.2 -13.5 14.7 10.6 1.9 1.7 47.2 246 251 74 47.9

CTI HSX 31,500 29,900 5.4 Neutral Long-term 23.8 58.4 22.3 12.4 12.8 22.3 10.4 16.4 1.9 4.8 36.3 388 472 56 20.4

ACB HNX 24,500 23,500 4.3 Neutral Long-term 21.6 28.9 11.4 21.9 27.9 46.2 15.5 15.8 1.6 0.0 45.2 3,594 3,641 1,018 -

HSG HSX 51,700 49,650 4.1 Neutral Intermediate-term 16.5 145.3 31.7 -0.5 17.6 22.2 5.6 6.0 2.1 1.0 54.6 1,425 3,062 436 19.0

DNP HNX 29,600 28,500 3.9 Neutral Long-term 60.9 91.6 34.7 50.6 17.6 10.8 10.4 6.6 2.0 0.0 22.6 56 63 38 45.5

NKG HSX 46,110 44,400 3.9 Neutral Intermediate-term 55.4 310.7 62.0 29.0 14.6 10.4 4.1 4.8 1.7 0.0 150.8 383 673 129 19.3

VNM HSX 151,800 146,600 3.5 Neutral Long-term 16.8 20.3 19.9 12.1 13.4 10.9 21.0 22.6 8.6 0.3 30.4 1,292 7,808 9,348 45.2

PNJ HSX 97,300 94,800 2.6 Neutral Long-term 11.1 195.8 21.7 43.3 13.1 21.4 16.2 15.6 5.3 1.1 68.4 210 778 409 -

SVC HSX 54,500 53,700 1.5 Neutral Long-term 38.0 18.4 11.2 20.4 -5.0 4.5 10.9 10.1 1.5 3.0 56.8 117 258 59 7.5

TCM HSX 25,300 26,000 -2.7 Neutral Long-term 10.0 -25.6 6.2 55.6 1.9 7.4 9.1 8.5 1.3 1.9 -0.9 673 630 56 -

VGC HNX 14,600 15,200 -3.9 Neutral Long-term 4.1 56.4 7.9 17.3 13.6 9.1 7.7 8.2 1.1 4.6 0.0 301 202 205 39.9

PAC HSX 36,800 38,500 -4.4 Neutral Long-term 8.2 34.1 19.4 0.5 12.4 10.5 14.9 15.9 3.2 4.7 48.7 214 337 79 20.7

HT1 HSX 21,200 22,200 -4.5 Neutral Long-term 8.3 9.5 6.6 13.7 5.2 6.7 10.7 10.8 1.6 0.0 -4.2 398 380 372 39.9

VJC HSX 121,000 131,000 -7.6 Neutral Long-term 38.6 113.3 41.7 24.9 22.0 25.2 15.6 13.6 8.2 1.1 0.0 550 3,110 1,839 3.9

GMD HSX 33,000 36,050 -8.5 Reduce Intermediate-term 4.3 -3.1 11.2 23.7 22.3 26.8 15.8 22.1 1.2 5.5 35.4 1,074 1,587 284 19.1

IMP HSX 54,900 60,100 -8.7 Neutral Long-term 4.8 8.9 24.6 33.5 18.4 17.8 16.9 19.5 1.7 3.3 41.4 56 152 103 -

DHG HSX 125,400 140,000 -10.4 Reduce Long-term 4.9 20.6 12.4 10.0 9.7 9.2 16.7 17.9 4.0 1.1 72.0 111 636 536 -

SAB HSX 158,400 199,300 -20.5 Sell Long-term 12.6 31.3 11.2 4.2 12.9 4.2 27.5 29.2 10.2 1.0 0.0 73 675 5,615 39.2

MWG HSX 134,500 172,000 -21.8 Sell Intermediate-term 76.7 47.2 63.2 41.4 35.9 16.5 14.9 14.2 6.0 0.9 123.4 184 1,371 1,162 -

Rong Viet Securities Corporation – Investment Strategy Report May 2017 20

APPENDIX: LIST OF COMPANIES PAYING DIVIDEND IN MAY

Ticker Ex-dividend date Payment date Exchange Close Price Cash Dividend Dividend Yield Stock Dividend

VE4 5/18/2017 6/20/2017 HNX 14,600 2,000 14%

PPY 5/4/2017 6/1/2017 HNX 13,000 1,600 12%

PBP 5/15/2017 5/20/2017 HNX 14,200 1,500 11%

HMC 5/15/2017 5/31/2017 HSX 10,700 1,100 10%

VC1 5/23/2017 6/30/2017 HNX 19,500 2,000 10%

EBS 5/4/2017 5/25/2017 HNX 8,800 900 10%

PSC 5/4/2017 6/2/2017 HNX 13,500 1,350 10%

NBC 5/12/2017 6/29/2017 HNX 6,600 550 8%

LHG 5/9/2017 5/31/2017 HSX 21,650 1,500 7%

NCT 5/12/2017 6/9/2017 HSX 87,900 6,000 7%

PJC 5/3/2017 5/18/2017 HNX 17,200 1,100 6%

BHT 5/8/2017 5/18/2017 HNX 2,700 150 6%

PSE 5/12/2017 6/5/2017 HNX 12,600 700 6%

TVD 5/18/2017 6/9/2017 HNX 5,900 300 5%

SRF 5/4/2017 5/22/2017 HSX 27,200 1,200 4%

GDT 5/10/2017 5/24/2017 HSX 62,000 2,500 4%

FTS 5/8/2017 6/9/2017 HSX 13,700 500 4% 10%

HCM 5/15/2017 6/7/2017 HSX 32,900 1,200 4% 50%

TMC 5/10/2017 5/25/2017 HNX 13,800 500 4%

CLC 5/4/2017 5/26/2017 HSX 59,300 2,000 3%

INN 5/9/2017 5/26/2017 HNX 64,000 2,000 3%

TDW 5/11/2017 5/29/2017 HSX 25,000 700 3%

SGC 5/11/2017 5/23/2017 HNX 47,300 1,200 3%

DHG 5/4/2017 5/17/2017 HSX 140,000 3,500 3%

DXG 5/15/2017 6/29/2017 HSX 22,450 500 2% 13%

VNC 5/12/2017 6/15/2017 HNX 36,500 800 2%

VFG 5/3/2017 5/19/2017 HSX 74,900 1,500 2%

VNM 5/4/2017 5/22/2017 HSX 146,600 2,000 1%

SMA 5/9/2017 6/12/2017 HSX 8,000 100 1%

VJC 5/9/2017 5/30/2017 HSX 129,800 1,000 1%

TV2 5/24/2017 6/26/2017 HNX 215,000 1,000 0% 15%

Source: FiinPro, RongViet Research *Close price and dividend yield as of 5/5/2017

Rong Viet Securities Corporation – Investment Strategy Report May 2017 21

MACRO WATCH

Headline Inflation Steadied In April Slight Recovery In Retail Sales

Source: GSO, RongViet Research Source: GSO, RongViet Research

Manufacturing Remained Strong Exports Growth Surprised On The Upside

Source: GSO, RongViet Research Source: GSO, RongViet Research

Resilient FDI Flows Government Bonds Become More Attractive

Source: FII, RongViet Research Source: VBMA, RongViet Research

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

Headline inflation Core inflation

240000

260000

280000

300000

320000

340000

0%

4%

8%

12%

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

Retail Sales (VND B) Growth (Ex-inflation)

-10.0-8.0-6.0-4.0-2.0

.02.04.06.08.0

10.0

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

48

49

50

51

52

53

54

55

PMI IP (3m moving average)

-10%-5%0%5%

10%15%20%25%30%35%

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

Export Import

0

1000

2000

3000

4000

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

04/2

017

Implemented capital Registered capital

0%

20%

40%

60%

80%

100%

120%

0

10000

20000

30000

40000

50000

60000

01/2

016

02/2

016

03/2

016

04/2

016

05/2

016

06/2

016

07/2

016

08/2

016

09/2

016

10/2

016

11/2

016

12/2

016

01/2

017

02/2

017

03/2

017

Winning volumeOffering volumeWinning/Offering Ratio

Rong Viet Securities Corporation – Investment Strategy Report May 2017 22

INDUSTRY INDEX

Level 1 industry movement Level 2 industry movement

Source: RongViet Research Source: RongViet Research

Industry PE comparison Industry PB comparison

Source: RongViet Research Source: RongViet Research

-1% -2%

-10%

-1%

1% 2%

-3%

0%

-1%

2%

Tech

nolo

gy

Indu

stria

ls

Oil

& G

as

Cons

umer

Ser

vice

s

Hea

lth C

are

Cons

umer

Goo

ds

Bank

s

Basi

c M

ater

ials

Fina

ncia

ls

Util

ities

-1%-3%

0%-1%

-10%-4%

2%-2%

1%5%

2%-3%

2%-1%

1%5%

-2%1%

RetailInsurance

Real EstateTechnology

Oil & GasFinancial Services

UtilitiesTravel & Leisure

Industrial Goods & ServicesPersonal & Household Goods

ChemicalsBanks

Automobiles & PartsBasic Resources

Food & BeverageMedia

Construction & MaterialsHealth Care

11.6

15.1 15.213.5

16.418.1

14.4

7.5

20.1

12.7

16.9

11.5

Tech

nolo

gy

Indu

stria

ls

Oil

& G

as

Cons

umer

Serv

ices

Hea

lth C

are

Cons

umer

Goo

ds

Bank

s

Basi

c M

ater

ials

Fina

ncia

ls

Util

ities

HSX

HN

X

2.0

3.7

0.6

4.5

3.5

5.5

1.61.3

2.8

2.3

3.8

1.6

Tech

nolo

gy

Indu

stria

ls

Oil

& G

as

Cons

umer

Ser

vice

s

Hea

lth C

are

Cons

umer

Goo

ds

Bank

s

Basi

c M

ater

ials

Fina

ncia

ls

Util

ities

HSX

HN

X

Rong Viet Securities Corporation – Investment Strategy Report May 2017 23

DISCLAIMERS

This report is prepared in order to provide information and analysis to clients of Rong Viet Securities only. It is and should not be construed as an offer to sell or a solicitation of an offer to purchase any securities. No consideration has been given to the investment objectives, financial situation or particular needs of any specific. The readers should be aware that Rong Viet Securities may have a conflict of interest that can compromise the objectivity this research. This research is to be viewed by investors only as a source of reference when making investments. Investors are to take full responsibility of their own decisions. VDSC shall not be liable for any loss, damages, cost or expense incurring or arising from the use or reliance, either full or partial, of the information in this publication.

The opinions expressed in this research report reflect only the analyst's personal views of the subject securities or matters; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or opinions expressed in the report.

The information herein is compiled by or arrived at Rong Viet Securities from sources believed to be reliable. We, however, do not guarantee its accuracy or completeness. Opinions, estimations and projections expressed in this report are deemed valid up to the date of publication of this report and can be subject to change without notice.

This research report is copyrighted by Rong Viet Securities. All rights reserved. Therefore, copy, reproduction, republish or redistribution by any person or party for any purpose is strictly prohibited without the written permission of VDSC.

IMPORTANT DISCLOSURES FOR U.S. PERSONS

This research report was prepared by Viet Dragon Securities Corp. (“VDSC”), a company authorized to engage in securities activities in Vietnam. VDSC is not a registered broker-dealer in the United States and, therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This research report is provided for distribution to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Any U.S. recipient of this research report wishing to effect any transaction to buy or sell securities or related financial instruments based on the information provided in this research report should do so only through Rosenblatt Securities Inc., 40 Wall Street 59th Floor, New York, NY 10005, a registered broker dealer in the United States. Under no circumstances should any recipient of this research report effect any transaction to buy or sell securities or related financial instruments through VDSC. Rosenblatt Securities Inc. accepts responsibility for the contents of this research report, subject to the terms set out below, to the extent that it is delivered to a U.S. person other than a major U.S. institutional investor.

The analyst whose name appears in this research report is not registered or qualified as a research analyst with the Financial Industry Regulatory Authority (“FINRA”) and may not be an associated person of Rosenblatt Securities Inc. and, therefore, may not be subject to applicable restrictions under FINRA Rules on communications with a subject company, public appearances and trading securities held by a research analyst account.

Ownership and Material Conflicts of Interest

Rosenblatt Securities Inc. or its affiliates does not ‘beneficially own,’ as determined in accordance with Section 13(d) of the Exchange Act, 1% or more of any of the equity securities mentioned in the report. Rosenblatt Securities Inc, its affiliates and/or their respective officers, directors or employees may have interests, or long or short positions, and may at any time make purchases or sales as a principal or agent of the securities referred to herein. Rosenblatt Securities Inc. is not aware of any material conflict of interest as of the date of this publication.

Compensation and Investment Banking Activities

Rosenblatt Securities Inc. or any affiliate has not managed or co-managed a public offering of securities for the subject company in the past 12 months, nor received compensation for investment banking services from the subject company in the past 12 months, neither does it or any affiliate expect to receive, or intends to seek compensation for investment banking services from the subject company in the next 3 months.

Additional Disclosures

This research report is for distribution only under such circumstances as may be permitted by applicable law. This research report has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient, even if sent only to a single recipient. This research report is not guaranteed to be a complete statement or summary of any securities, markets, reports or developments referred to in this research report. Neither VDSC nor any of its directors, officers, employees or agents shall have any liability, however arising, for any error, inaccuracy or incompleteness of fact or opinion in this research report or lack of care in this research report’s preparation or publication, or any losses or damages which may arise from the use of this research report.

Rong Viet Securities Corporation – Investment Strategy Report May 2017 24

VDSC may rely on information barriers, such as “Chinese Walls” to control the flow of information within the areas, units, divisions, groups, or affiliates of VDSC.

Investing in any non-U.S. securities or related financial instruments (including ADRs) discussed in this research report may present certain risks. The securities of non-U.S. issuers may not be registered with, or be subject to the regulations of, the U.S. Securities and Exchange Commission. Information on such non-U.S. securities or related financial instruments may be limited. Foreign companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in effect within the United States.

The value of any investment or income from any securities or related financial instruments discussed in this research report denominated in a currency other than U.S. dollars is subject to exchange rate fluctuations that may have a positive or adverse effect on the value of or income from such securities or related financial instruments.