44CON 2014 - Flushing Away Preconceptions of Risk, Thom Langford

1

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

AspartofourRetailRevolutionseries,thisreportbringstogethersignificantdatapointsthatchartthechangingnatureoftheUSapparelmarketandallowustodigdeeperintosomeestablishednarrativesandpreconceptions.Toptakeawaysinclude:

1) Despitesomereportstothecontrary,Amazonisnotamongthetop10apparelretailersintheUS,byrevenues,ifweconsiderwhatitretailsinitsownright.

2) H&Mhasgrownsubstantially,butitisnowexperiencingdeepdeclinesinitsUScomparablesales,accordingtoanalysts’estimates.

3) Primarkcouldachievejustunder$1billioninUSsalesby2020.

4) Theoff-priceapparelspecialistsegmentgrewrevenuesby39%between2011and2016,andnowaccountsfor22.5%ofallapparelspecialists’sales.

5) Byshoppernumbers,Amazonisthesixth-most-popularretailerforwomenswear,thesecond-most-popularformenswearandthetop-rankingretailerforfootwearintheUS.

Deep Dive: Retail Revolution—

US Apparel Shifts in 20 Charts

Deborah Weinswig

Managing Director,

Fung Global Retail & Technology

US: 917.655.6790

HK: 852.6119.1779

CN: 86.186.1420.3016

2

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

IntroductionTherevolutioninUSretailisperhapsmoreevidentinapparelthaninanyothercategory.E-commerceplayers,international“invaders”andoff-priceretailersarecreatingawhirlwindofdisruptionformiddle-groundincumbents.

Inthisreport,webringtogetherdatafromcompanyfilings,market-researchfirmsandconsumersurveystoillustratein20chartstheshiftsintheUSapparelmarket.Wealsousedatatoexploresomeestablishednarratives,includingthoseaboutAmazon’sscaleinapparelandthegrowthoffast-fashionretailers.

Amongthesubjectswecoverareconsensusexpectationsforgrowthatthebiggestapparelretailersinfiscalyear2018,H&M’ssharpdownturninUStrading,estimatesforstorenumbersandrevenuesatPrimark,anddataonwhereUSconsumersshopforwomenswear,menswearandfootwear.

Thefollowingsectionscover:

• TheTopRetailers• AmazonandE-Commerce• Off-Price• FastFashion• Athleisure• StoreClosures• WhereConsumersShop

Forthepurposesofthisreport,apparelincludesclothing,footwearandaccessories.AlldataarefortheUSonly,unlessotherwisespecified.

Source:Shutterstock

3

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

TheTopRetailers

Figure1.TopRetailers’SalesofApparel,FY16(USDBil.)

AlldataareforfiscalyearendedJanuary2016,exceptforCostco,whichisforfiscalyearendedAugust2016.AlldataareforUSrevenuesonly.(a)Includingjewelry;TJXtotalis$13.1billionexcludingapparelaccessoriesandjewelry.(b)Includingcosmetics(c)Softlines,whichincludeapparelandsmallappliances(d)IncludingjewelryandfragrancesSource:Companyreports/FungGlobalRetail&Technology

WebeginwitharankingofAmerica’s10biggestclothing,footwearandaccessoriesretailers.WalmartovertookMacy’stobecomethetopapparelretailerintheyearendedJanuary2016,weestimate.Twoofthetop10apparelcompaniesareoff-priceretailers:TJXCompanies,whichincludestheT.J.MaxxandMarshallschains,andRossStores.ValueretailisfurtherrepresentedbyWalmart,TargetandCostco,andfourofthetop10aredepartmentstoreretailers:Macy’s,Kohl’s,NordstromandJCPenney.Onlyone,Gap(includingOldNavyandBananaRepublic),isaspecializednondiscountretailer.

Amazon,withanestimated$5.5billioninapparelretailsalesin2016(excludingthird-partysalesonitssite),failstomakethetop10.ButifAmazoncangrowitsfirst-partysalesbyaround20%ayear,itwillberetailinganestimated$9billionofapparelby2019.

Figure2.ConsensusEstimatesforTopApparelRetailers’TotalRevenues,FY18(YoY%Change)

AsofFebruary7,2017.Dataarefortotalcompanyrevenues,includinganynonapparelrevenuesandnon-USrevenues.Source:S&PCapitalIQ/FungGlobalRetail&Technology

Above,wechartanalysts’consensusexpectationsfortotalrevenuegrowthamongtheseretailersinfiscalyear2018.Welookaheadto2018becausefiscal2017hasfinishedforallbutoneofthetop10retailers(Costcoistheoutlier;itsfiscal2017yearendsinAugust).

Itwillsurprisefewreadersthattheoff-priceanddiscountchannelsaresettobethestrongestperformersamongthebiggestretailers.TheanticipatedrevenuedeclineforMacy’sisinthecontextofstoreclosures(anissuewecoverlaterinthisreport).

6.9

6.8

5.6

4.6

1.8

1.8

1.6

0.1

(0.2)

(4.0)

TheTJXCompanies

RossStores

Costco

Nordstrom

Walmart

JCPenney

Target

Kohl's

GapInc.

Macy's

Kohl’s

Kohl’s

4

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

AmazonandE-Commerce

Figure3.Amazon:EstimatedUSApparelSales(LeftAxis;USDBil.)andShareofTotalApparelSales(RightAxis;%)

3P=third-partysellers;1P=Amazon’sownretailsales(firstparty).Source:EuromonitorInternational/FungGlobalRetail&Technology

ManyanalystshaveattemptedtoestimateAmazon’ssalesintheapparelcategory,buttheseestimatesaretypicallybasedonlittleharddata.Thepictureiscomplicatedbythird-party(3P)sales,whichnowmakeuphalfofAmazon’stotalsales.

AccordingtoEuromonitorInternationalestimates,clothingandfootwearsalesmadethroughAmazonUStotaled$13billionin2016.Thiswasa$9billionincreasefromfiveyearsearlier.However,$7.56billionofthe2016saleswereAmazonMarketplacesales.Amazonfailstomakeourrankingofthetop10retailersbecauseitfunctionedassimplyaportal,notaretailer,formorethanhalfitssales.

AsestimatedbyEuromonitor,apparelaccountedforabout13%ofAmazon’s2016USgrossmerchandisevolume(GMV),whichseemsasensibleballparkfiguretous.

Figure4.E-CommerceasShareofTotalApparelSales(%)

Source:EuromonitorInternational/KantarWorldpanel/FungGlobalRetail&Technology

Euromonitorestimatesthataround17%ofUSapparelsaleswillbemadeonlinethisyear,whichequatestoaround$62billioninsales.

E-commerce’sshareofapparelcategorysalesintheUSlagsitsshareinpeercountriessuchastheUKandGermany,andthiseffectisexpectedtopersistoverthecomingfiveyears.

• Laterinthisreport,weincludeconsumersurveytrenddatathatshowhowmanyUSconsumersbuyapparelfromAmazon.

1.58 2.38 3.51 4.756.29 7.56

2.202.75

3.343.94

4.705.46

1.21.6

2.1

2.6

3.23.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

2

4

6

8

10

12

14

16

2011 2012 2013 2014 2015 2016

Amazon3P(USDBil.) Amazon1P(USDBil.)TotalShare(%)

15.517.0

22.323.024.5

30.0

17.419.8

30.9

2016 2017E 2021E

US UK Germany

5

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Off-Price

Figure5.Off-PriceDepartmentStoreSalesandOff-PriceApparelSpecialistSales(LeftAxis;USDBil.)andOff-PriceApparelSpecialistSalesas%ofTotalApparelSpecialistSectorSales(RightAxis;%)

Source:EuromonitorInternational/FungGlobalRetail&Technology

Theoff-priceapparelspecialistsegmentgrewrevenuesby39%between2011and2016.Its$44billionofsalesin2016accountedfornearlyone-quarteroftotalapparelspecialistsectorsales.

BetweentheyearsendedJanuary2012andJanuary2016,segmentleaderTJXCompaniesgrewsalesatitsUST.J.MaxxandMarshallschainsby30%,to$19.9billion.

Figure6.SelectedMajorOff-PriceRetailers:StoreNumbers

FiscalyearsendedJanuarySource:Companyreports

Themajoroff-priceretailersgrewtheirstorenumbersby23%,to4,463,betweentheyearsendedJanuary2012andJanuary2016.Thiscompareswith2.2%growthinstorenumbersacrossthetotalclothingandfootwearspecialistsector,bringingthattotalto118,561incalendar2015,accordingtoEuromonitor.

NewentrantssuchasMacy’sBackstageandFind@Lord&Taylorarenotincludedduetolackoftrenddata.

31.634.7

36.738.8

41.3 44.1

2.32.7

3.03.5

3.84.0

18.7

19.920.5

21.021.7

22.5

17

18

19

20

21

22

23

24

25

0

5

10

15

20

25

30

35

40

45

50

2011 2012 2013 2014 2015 2016

Off-PriceDepartmentStoreSales(USDBil.)Off-PriceApparelSpecialistSales(USDBil.)Off-PriceasShareofApparelSpecialistSector(%)

1,867 2,163

1,125

1,446477

567105

197

60

90

FY12 FY16

SaksOFF5TH NordstromRackBurlingtonCoatFactory RossStoresT.J.Maxx/Marshalls

3,634

4,463

6

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure7.ConsumerSurvey:ShoppersWhoUseOff-PriceFormatsasPartofApparelShoppingRoutines,byWhereTheyShop,March2015(%)

Source:KantarRetail

AroundhalfofUSconsumersbuyfromoff-priceretailers;theproportionisslightlyhigheramongthesubgroupthatalsoshopsatKohl’sandMacy’s.Off-pricespecialistretailers,suchasT.J.Maxx,continuetobeshoppedmoreheavilythanoff-priceordiscountdivisionsofdepartmentstores,suchasNordstromRackandSaksOFF5TH.

FastFashion

Figure8.USRevenuesofH&M,InditexandASOS(LeftAxis;USDMil.)andH&M’sUSMarketShareofClothing,FootwearandAccessories(RightAxis,%)

DataforH&MandASOSareforthenearestfiscalyearstocalendaryears.H&Mincludessalestax.Source:S&PCapitalIQ/EuromonitorInternational/companyreports/FungGlobalRetail&Technology

Inrecentyears,Europeanfast-fashionspecialistshavebeenperceivedasasignificantthreattoincumbentapparelretailers.H&Mhasledthechargeofinternationalfast-fashioninvaders.Its$3.2billioninrevenuein2016gaveitanapparelmarketshareofjustunder1%.

Amongapparelspecialists,H&MranksbetweenprivatelyownedForever21,whichgenerated$4.4billioninsalesin2015,accordingtopressreports,andAmericanEagleOutfitters,whichturnedover$3.1billionintheyearendedJanuary2016(latest).

Inditex(Zara)remainsmuchsmallerand,intermsofrevenue,isinthesameballparkasBritishonline-onlyretailerASOS.

49

37

51

36

52

40

4742

Off-PriceRetailers Off-Price/DiscountDivisionsofDepartmentStores

AllShoppers Kohl'sShoppersMacy'sShoppers NordstromShoppersMacy’sShoppers

Kohl’sShoppers

1,494

3,164288

390

65

267

0.5

0.9

0.00.10.20.30.40.50.60.70.80.91.0

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2011 2016

H&M Inditex(Est.) ASOS H&MMarketShare

7

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure9.H&MUSTotalSalesGrowthandEstimatedComparableSalesGrowth,andTotalUSClothingRetailers’Sales(%)

Clothingretailers’salesfor4Q16areforNovemberandDecember(latest).Source:Companyreports/GoldmanSachs/USCensusBureau/FungGlobalRetail&Technology

Despiteitssubstantialmedium-termgrowth,H&M’sUSperformancehasrecentlynosedived,withtotalsalesgrowthsupportedbycontinuedstoreopenings.Anumberofbrokersestimatethatcomparablesaleswerenegativein2016,andweredeeplynegativeinthethreemostrecentquarters.Forcomparison,thechartaboveshowsH&M’stotalUSsalesgrowthversustotalsalesgrowthintheclothingspecialistsector,asrecordedbytheUSCensusBureau.

Figure10.ProportionofUSConsumersWhoHadShoppedforWomenswearatH&Mvs.SelectedPeersinthePast90Days,asofApril2016(%)

Base:7,008adultsaged18+Source:ProsperInsights&Analytics

H&M’srelativelysmalloverallmarketsharebeliesitsstrengthinitscoreconsumersegment:itranksmuchmorehighlyamongyoungershoppersthanamongtheoverallpopulationofshoppers.Accordingtodatafromourresearchpartner,ProsperInsights&Analytics,some6%ofAmericanssurveyedsaidtheyhadshoppedforwomenswearatH&Minthepast90daysin2016.Thatfigure,however,was12.6%among18–34-year-olds(and13.5%among18–24-year-olds,arangenotchartedabove).

• Laterinthisreport,weincludemoresurveydataonwhereconsumersshopforwomenswear,menswearandfootwear.

28

2117

811

4 3 3

17.0

9.4

4.9

(2.9)

0.1

(7.2) (8.3)(10.1)

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

H&MTotal H&MComps(Est.)ClothingRetailers'SalesClothingRetailers’Sales

8

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure11.PrimarkUS:EstimatedSales(LeftAxis,USDMil.)andStoreNumbers(RightAxis)

Source:Companyreports/FungGlobalRetail&Technology

Primarklookstobethenextbigchallengertoincumbents.ItopeneditsfirstUSstore,inBoston,inSeptember2015,andhadopenedfivestoresbyitslatestyear-end,September2016.

BasedonPrimark’sexpansioninsignificantcontinentalEuropeanmarkets,weestimateitwillopenapproximatelysevenUSstoresperyear.Basedonaveragesalesperstoreinnon-UKmarkets,thatwouldtakeitsUSsalestojustunder$1billionbythefiscalyearendingSeptember2020.

Thecompanydoesnotbreakoutrevenuesbygeographicmarket.

Athleisure

Figure12.SelectedApparelSegments:Sales(YoY%Change)

Source:EuromonitorInternational/FungGlobalRetail&Technology

Athleisureremainsanimportantdriveroftotalapparelsalesgrowth.Euromonitorrecordedverystrongperformancesacrosssportsclothingandfootwearin2016,anditforecaststhatthisgrowthwillstrengthenthisyear.

DatafromEuromonitorandTheNPDGroupsuggestthatthestrongestgrowthhasbeenseeninsports-inspiredproductsratherthaninperformanceproducts(seealsoFigure13).

5.0

11.0

18.0

25.0

32.0

92

251

465

706

957

0

200

400

600

800

1000

1200

0

5

10

15

20

25

30

35

FY16 FY17E FY18E FY19E FY20E

StoreNum

bersSales(USD

Mil.)

StoreNumbers EsrmatedSales(USDMil.)

2.9

4.4

4.7

6.3

6.7

8.1

8.9

4.1

5.8

5.9

7.1

7.3

8.2

9.3

TotalApparel&Footwear

PerformanceClothing

OutdoorClothing

Sports-InspiredClothing

PerformanceFootwear

OutdoorFootwear

Sports-InspiredFootwear

2017E 2016

9

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Figure13.SelectedSegmentsofAthleticFootwearMarket:Sales,2016(YoY%Change)

*SegmentwithinClassicTrainersSource:TheNPDGroup

In2016,TheNPDGroupfoundthatgrowthintheathleticfootwearmarketwasdrivenbythe“classics”segment(thefashionsegment)ratherthanbythe“performance”segment.Theclassicssegmentincludesretroandsports-inspiredlines.Performancerunningshoesrecordedzerogrowthandperformancebasketballfootwearsalesdeclinedbyanunspecifiedamountin2016.

AccordingtoTheNPDGroup,totalmarketgrowthwasimpactedinthefourthquarterduetothebankruptciesofSportsAuthorityandSportsChalet.

Figure14.Sportsvs.Non-SportsApparel:ShareofTotalMarket,2016(%)

Source:EuromonitorInternational/FungGlobalRetail&Technology

Sportsapparelaccountsfor30%ofthetotalUSclothingandfootwearmarket.Thissharehasrisenbyapproximatelyonepercentagepointperyearoverthepastfiveyears.

26

36

27

11

03

ClassicTrainers

Classics:InspiredbyRunning*

Classics:InspiredbyBasketball*

CasualAthlerc

PerformanceRunning

TotalMarketTotalMarket

PerformanceClothing,11.4

Sports-InspiredClothing,7.4

PerformanceFootwear,5.7

Sports-InspiredFootwear,2.9

OutdoorClothing,1.7

OutdoorFootwear,1.0

Non-SportsClothingandFootwear,69.9%

10

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

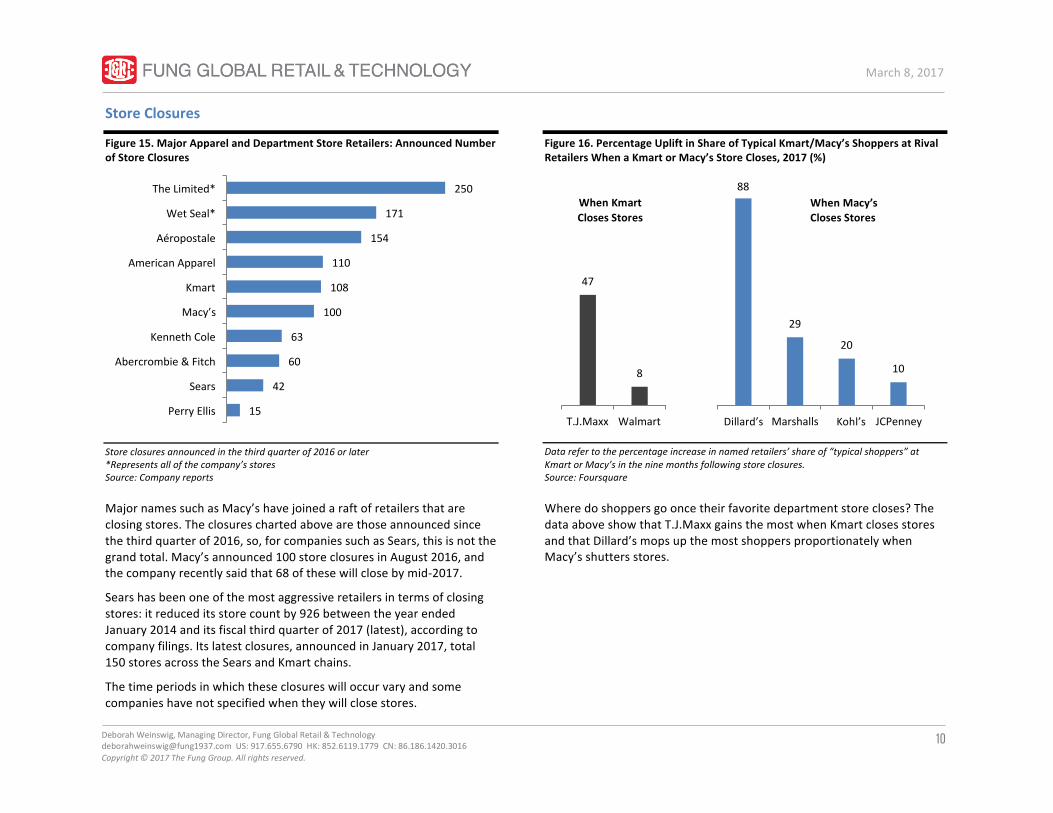

StoreClosures

Figure15.MajorApparelandDepartmentStoreRetailers:AnnouncedNumberofStoreClosures

Storeclosuresannouncedinthethirdquarterof2016orlater*Representsallofthecompany’sstoresSource:Companyreports

MajornamessuchasMacy’shavejoinedaraftofretailersthatareclosingstores.Theclosureschartedabovearethoseannouncedsincethethirdquarterof2016,so,forcompaniessuchasSears,thisisnotthegrandtotal.Macy’sannounced100storeclosuresinAugust2016,andthecompanyrecentlysaidthat68ofthesewillclosebymid-2017.

Searshasbeenoneofthemostaggressiveretailersintermsofclosingstores:itreduceditsstorecountby926betweentheyearendedJanuary2014anditsfiscalthirdquarterof2017(latest),accordingtocompanyfilings.Itslatestclosures,announcedinJanuary2017,total150storesacrosstheSearsandKmartchains.

Thetimeperiodsinwhichtheseclosureswilloccurvaryandsomecompanieshavenotspecifiedwhentheywillclosestores.

Figure16.PercentageUpliftinShareofTypicalKmart/Macy’sShoppersatRivalRetailersWhenaKmartorMacy’sStoreCloses,2017(%)

Datarefertothepercentageincreaseinnamedretailers’shareof“typicalshoppers”atKmartorMacy’sintheninemonthsfollowingstoreclosures.Source:Foursquare

Wheredoshoppersgooncetheirfavoritedepartmentstorecloses?ThedataaboveshowthatT.J.MaxxgainsthemostwhenKmartclosesstoresandthatDillard’smopsupthemostshoppersproportionatelywhenMacy’sshuttersstores.

250

171

154

110

108

100

63

60

42

15

TheLimited*

WetSeal*

Aéropostale

AmericanApparel

Kmart

Macy's

KennethCole

Abercrombie&Fitch

Sears

PerryEllis

Macy’s

47

8

88

29

20

10

T.J.Maxx Walmart Dillard's Marshalls Kohl's JCPenney

WhenKmart ClosesStores

WhenMacy's ClosesStores WhenMacy’s

Dillard’s Kohl’s

11

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

WhereConsumersShopInthissection,weshowcasesurveydatafromourresearchpartner,ProsperInsights&Analytics,onwhereconsumersshopforapparel.

Womenswear

Figure17.ConsumerSurvey:RetailersWhereFemaleRespondentsShoppedforWomenswearinthePast90Days(%)

Base:2,541–3,651femalesaged18+ineachsurveyperiod;surveyswereconductedinAprilofeachyear.Source:ProsperInsights&Analytics/FungGlobalRetail&Technology

Womenswearaccountsforaroundhalfoftheclothingmarket,makingitmuchthemostvaluablesegmentforretailers.Departmentstorescontinuetotakeleadingpositionsforwomenswear,byfemaleshoppernumbers.Amazoniscomfortablyinsidethetop10bynumberofshoppers.

Figure18.ConsumerSurvey:RetailersWhereRespondentsShoppedforWomenswearinthePast90Days,AllShoppersvs.AmazonShoppers(%)

“Amazonshoppers”definedasrespondentsthatrankAmazonasthestoretheyshopatthemostoftenforanycategorywithinthesurvey.Base:4,912–7,008adultsaged18+ineachsurveyperiod;surveyswereconductedinAprilofeachyear.Source:ProsperInsights&Analytics/FungGlobalRetail&Technology

WhenwedrilldowntowhereAmazonshoppers(maleorfemale)buywomenswear,Amazonitselfranksmuchmorehighly,witharoundone-thirdbuyingwomenswearfromtheretailer.“Amazonshoppers”aredefinedasrespondentswhostatedtheyshopatAmazonthemostoftenforanycategoryaboutwhichProspersurveysconsumers(fromgroceriestotoystoelectronicstoapparel).

15.4%

18.4%

20.7%

21.1%

22.6%

24.4%

27.9%

19.4%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

T.J.Maxx

Amazon

Macy's

Target

JCPenney

Walmart

Kohl's

NotShopped

2016 2015 2014

Kohl’s

Macy’s

31.0%

21.5%

18.5%

17.5%

17.4%

16.6%

15.0%

11.4%

30.0%

19.5%

15.6%

14.1%

16.5%

32.9%

16.0%

11.3%

NotShopped

Kohl's

Walmart

JCPenney

Macy's

Amazon

Target

T.J.Maxx

All AmazonShoppers

Kohl’s

Macy’s

12

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

Menswear

Figure19.ConsumerSurvey:RetailersWhereMaleRespondentsShoppedforMenswearinthePast90Days(%)

Base:2,763–3,373malesaged18+ineachsurveyperiod;surveyswereconductedinJuneofeachyear.Source:ProsperInsights&Analytics/FungGlobalRetail&Technology

Menswearaccountsforaroundone-thirdofthetotalclothingmarket.Here,WalmartleapfrogsKohl’stotakefirstpositionandAmazonseizessecondplace,havingregisteredaleapinshoppernumbersbetween2015and2016.ThedifferencesinrankingandthepresenceofOldNavyformenswearsuggestagreaterfocusonlowpricesamongmaleshoppersthanamongfemaleshoppers.

Footwear

Figure20.ConsumerSurvey:RetailersWhereRespondentsShoppedforFootwearinthePast90Days(%)

Base:6,178–6,809adultsaged18+ineachsurveyperiod;surveyswereconductedinJulyofeachyear.Source:ProsperInsights&Analytics/FungGlobalRetail&Technology

Amazonratesmorehighlyforfootwearthanforclothing.InProsper’s2016survey,respondentsindicatedthatAmazonwasthemost-shoppedretailerforshoes.

• ReaderscanfindfurtheranalysisofProsperdatainourrecentreportUSConsumerAnalysis:ApparelandFootwear.

8.7%

14.5%

15.5%

16.2%

17.3%

23.4%

23.9%

24.5%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

OldNavy

Target

Macy's

JCPenney

Kohl's

Amazon

Walmart

NotShopped

2016 2015 2014

Kohl’s

Macy’s

7.9%

8.8%

8.9%

9.0%

11.9%

12.7%

16.2%

35.3%

0.0% 10.0% 20.0% 30.0% 40.0%

Macy's

JCPenney

Payless

Target

Kohl's

Walmart

Amazon

NotShopped

2016 2015 2014

Kohl’s

Macy’s

13

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

KeyTakeawaysWhileoff-priceande-commerceremainthemajorgrowthchannelsinUSapparelretailing,thestoryforfastfashionislessclear,givenH&M’sstallinggrowthandInditex’sstillmarginalshareofthemarket.Meanwhile,departmentstoresremainamongthemostpopulardestinationsforapparelshoppers.

Price-ledretailersretainverystrongpositionsinthemarket,andweestimatethatWalmartovertookMacy’sintermsofannualapparelsalesintheyearendedJanuary2016.Byshareofshoppers,valueretailersrankmorehighlyinthemenswearcategorythaninwomenswear.Primarkisanewchallengerintheultralow-pricesegmentandcouldbeturningovernearly$1billioninannualUSsalesby2020.

Amazonisaverypopulardestinationforfootwearandmenswear,butisslightlylesspopularforwomenswear.Thisislikelydueinparttothefactthatshoppinginthemenswearcategoryismorefunctionalandprice-ledinnaturethanitisinwomenswear.Amazonisnotyetamongthetop10retailersofapparelintheUS,ifweconsideronlyestimatesforsalesthatitmakesitself,andnotthird-partysalesthatitfacilitates.However,thosefirst-partysalesappeartobegrowingrapidly,andwillalmostcertainlypropelAmazonintothetop10inthenot-too-distantfuture.

14

March8,2017

DeborahWeinswig,ManagingDirector,FungGlobalRetail&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2017TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFungGlobalRetail&TechnologyNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

HongKong:8thFloor,LiFungTower888CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NewYork:1359Broadway,9thFloorNewYork,NY10018Tel:6468397017FungGlobalRetailTech.com