REPORT ON SOUDERTON AREA SCHOOL DISTRICT …€¦ · · 2017-12-15Expenditures, and Changes in...

112

REPORT ON SOUDERTON AREA SCHOOL DISTRICT SINGLE AUDIT REPORT FISCAL YEAR ENDED JUNE 30, 2009

Transcript of REPORT ON SOUDERTON AREA SCHOOL DISTRICT …€¦ · · 2017-12-15Expenditures, and Changes in...

REPORT ON SOUDERTON AREA SCHOOL DISTRICT

SINGLE AUDIT REPORT FISCAL YEAR ENDED JUNE 30, 2009

SOUDERTON AREA SCHOOL DISTRICT

Single Audit Report

For the Fiscal Year Ended June 30, 2009

TABLE OF CONTENTS

PAGE (S)

-i-

Introductory Section Transmittal Letter ........................................................................................................................... 1

Letter to Management ............................................................................................................... 2 - 8

Report Distribution List ................................................................................................................... 9

Financial Section Independent Auditor's Report................................................................................................ 10 - 11

Management's Discussion and Analysis ............................................................................... 12 - 21

Basic Financial Statements District-wide Financial Statements:

Statement of Net Assets ................................................................................................. 22

Statement of Activities..................................................................................................... 23

Fund Financial Statements:

Balance Sheet - Governmental Funds ........................................................................... 24

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets................................................................................... 25

Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds................................................................................ 26

Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities .........................................................................................27 - 28

Statement of Net Assets - Proprietary Funds................................................................. 29

Statements of Revenues, Expenses, and Changes in Net Assets - Proprietary Funds ......................................................................................... 30

Statements of Cash Flows - Proprietary Funds ......................................................31 - 32

Statement of Net Assets - Fiduciary Funds.................................................................... 33

Statement of Changes in Net Assets - Fiduciary Funds ................................................ 34

SOUDERTON AREA SCHOOL DISTRICT

Single Audit Report

For the Fiscal Year Ended June 30, 2009

TABLE OF CONTENTS (continued)

PAGE (S)

-ii-

Statement of Revenues, Expenditures, and Changes in Fund Balance - Budget and Actual - General Fund ............................................................ 35

Notes to Basic Financial Statements................................................................................. 36 – 74

Required Supplemental Information

Schedule of Funding Progress .................................................................................................. 75

Supplemental Information:

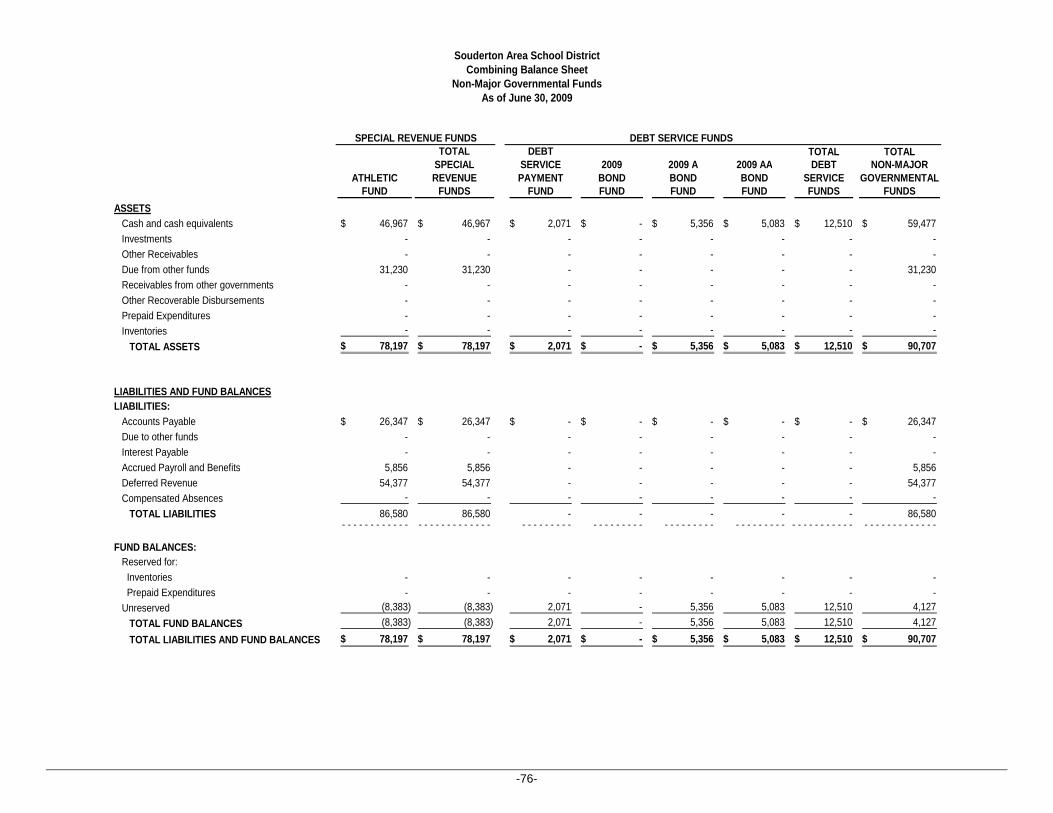

Combining Balance Sheet - Non-Major Governmental Funds ...................................... 76

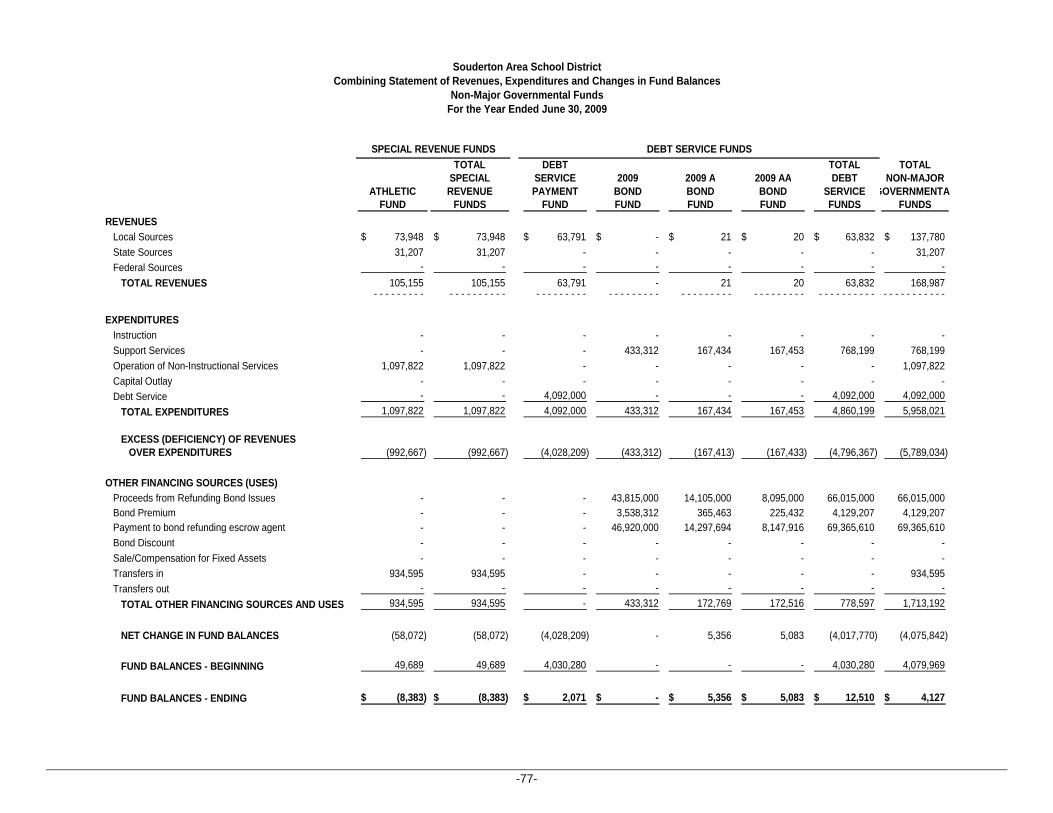

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances - Non-Major Governmental Funds.................................................... 77

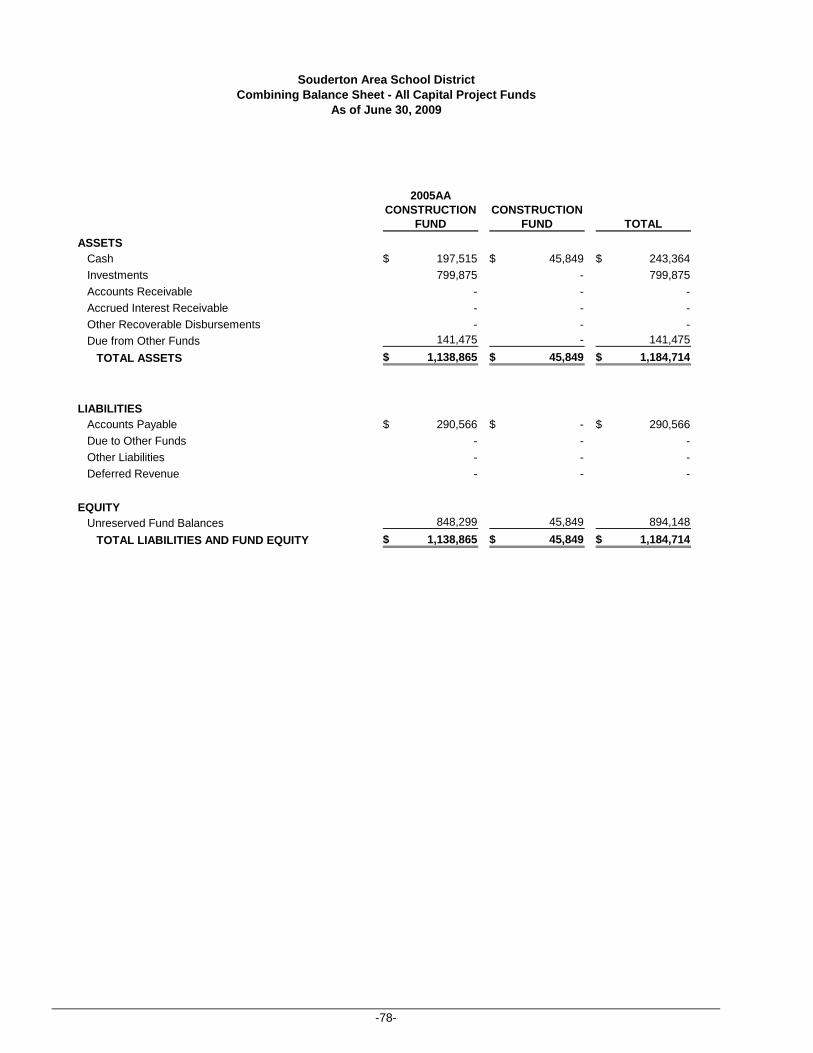

Combining Balance Sheet - All Capital Project Funds................................................... 78

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances - All Capital Project Funds ........................................................................ 79

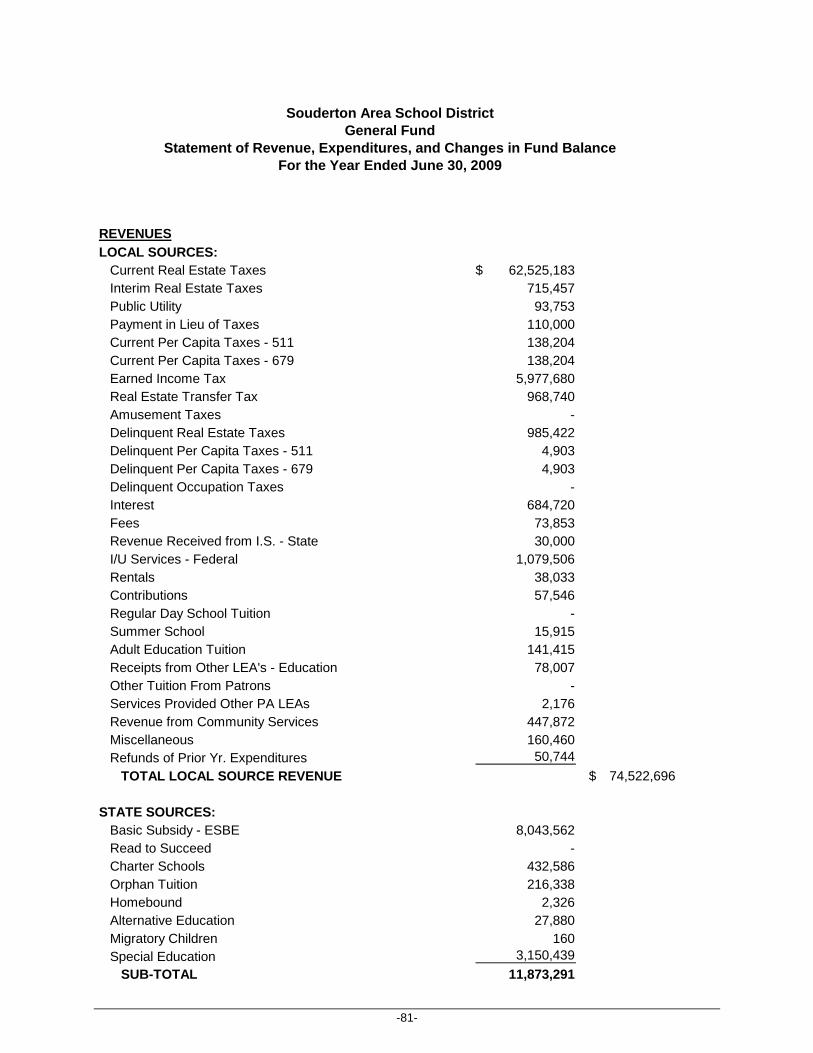

General Fund-Schedule on Tax Collectors’ Receipts.................................................... 80

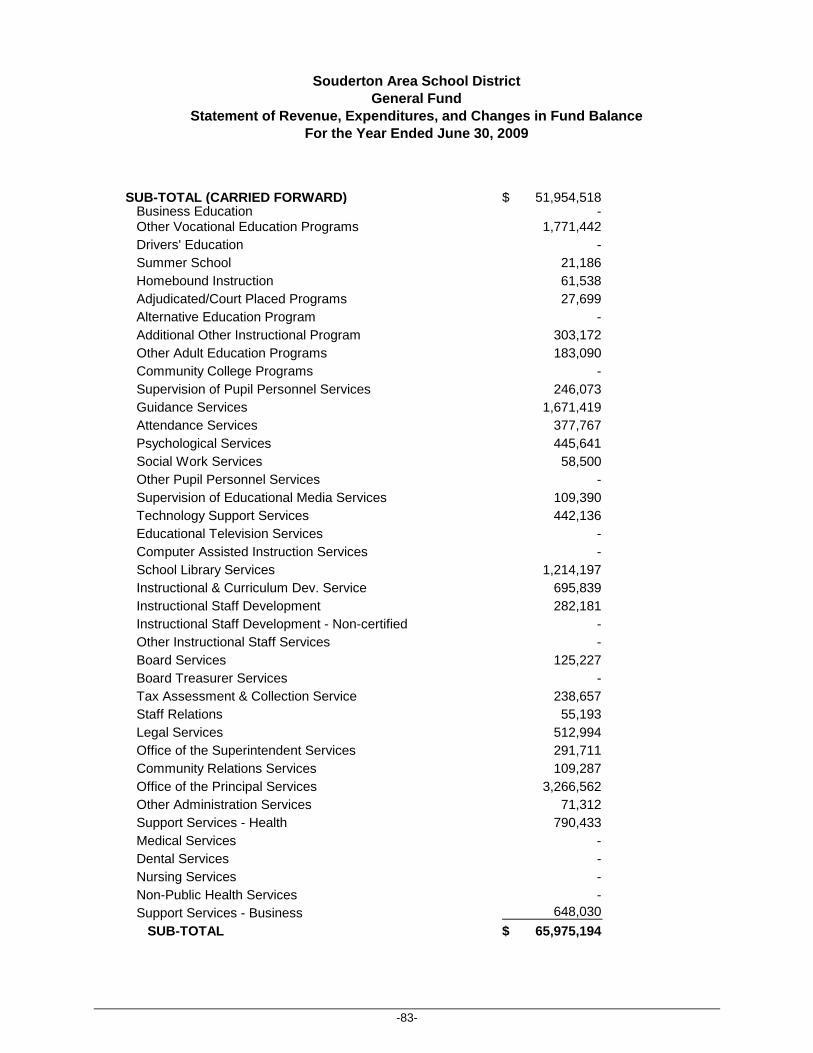

General Fund - Statement of Revenue, Expenditures, and Changes in Fund Balance .................................................................................................81 - 84

Capital Reserve Fund - Statement of Revenues and Expenditures.............................. 85

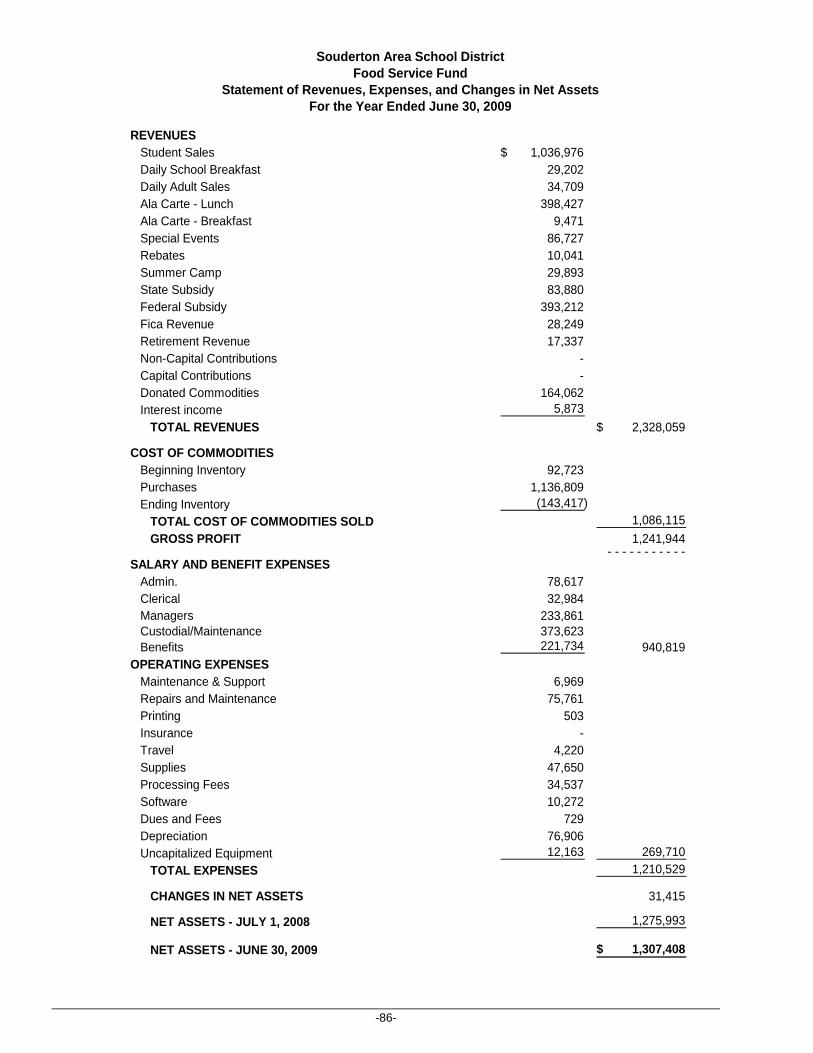

Food Service Fund - Statement of Revenues, Expenses, and Changes in Net Assets............................................................................................... 86

Athletic Fund - Statement of Revenues and Expenditures............................................ 87

Debt Service Payment Fund– Statement of Revenues and Expenditures ................... 88

2009 Bond Fund – Statement of Revenues and Expenditures ..................................... 88

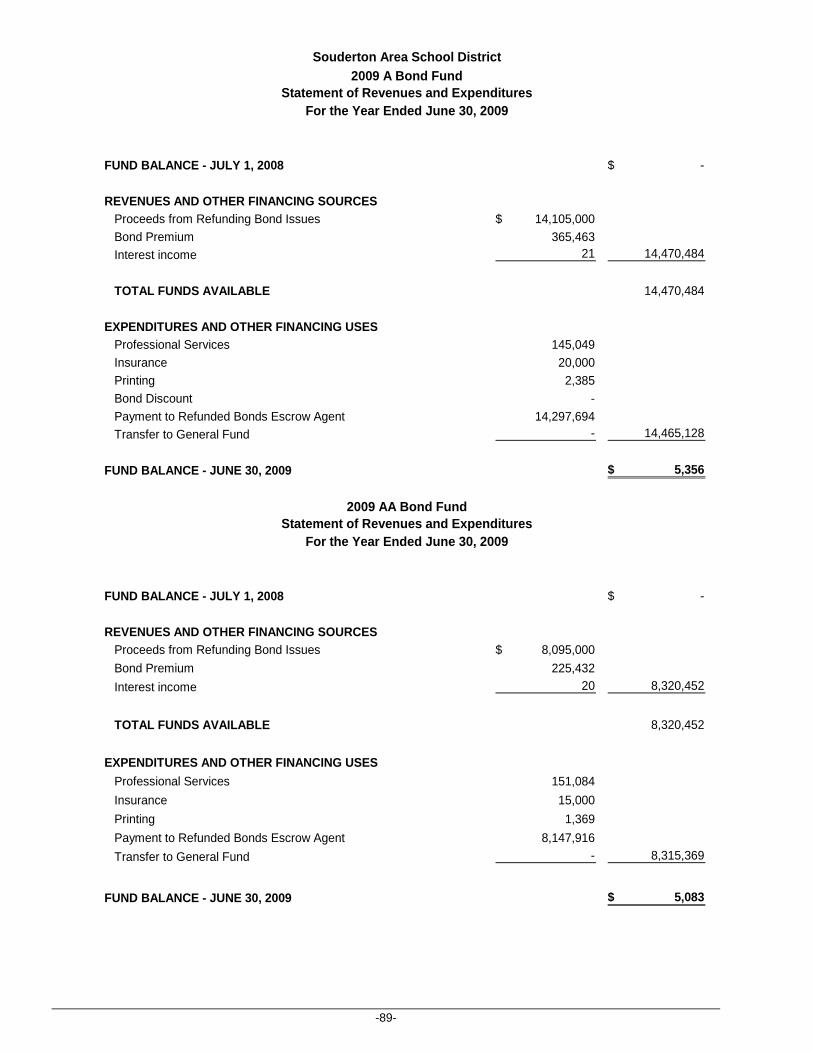

2009A Bond Fund – Statement of Revenues and Expenditures................................... 89

2009AA Bond Fund – Statement of Revenues and Expenditures ................................ 89

2005AA Construction Fund - Statement of Revenues and Expenditures ..................... 90

Construction Fund – Statement of Revenues and Expenditures .................................. 91

SOUDERTON AREA SCHOOL DISTRICT

Single Audit Report

For the Fiscal Year Ended June 30, 2009

TABLE OF CONTENTS (continued)

PAGE (S)

-iii-

General Long-Term Debt:

Schedule on General Obligation Bonds - Series of 2005 .............................................. 92

Schedule on General Obligation Bonds - Series of 2006 .............................................. 92

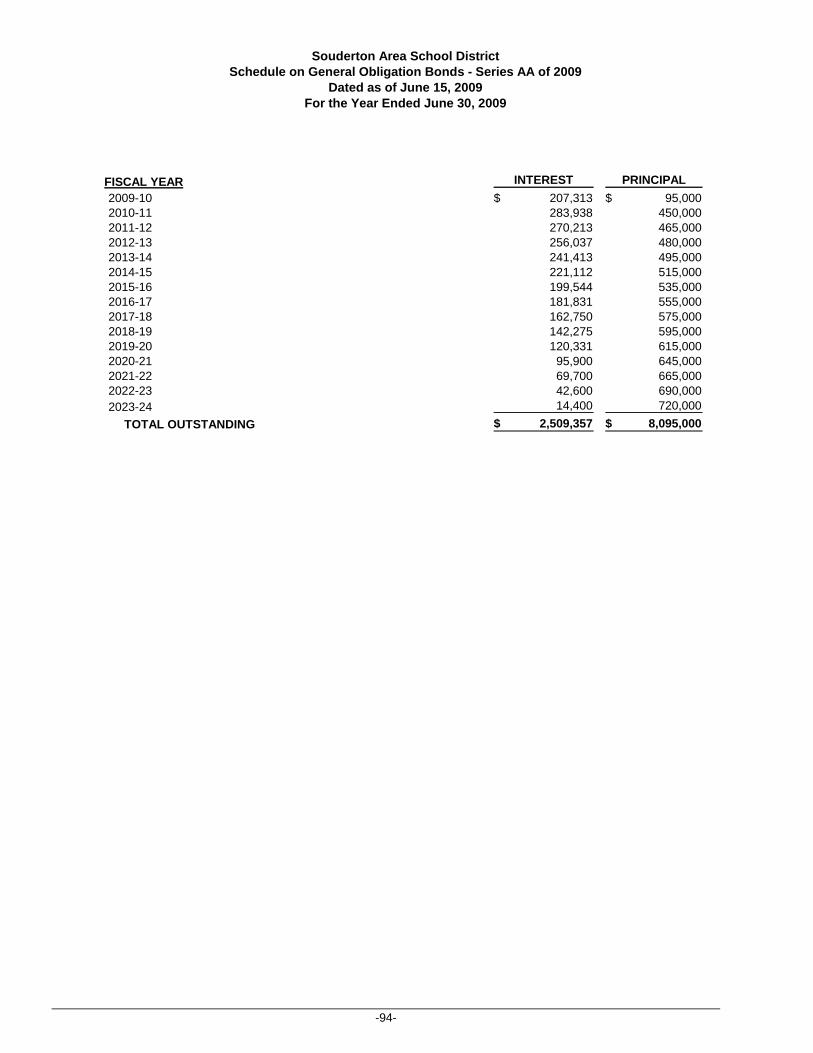

Schedule on General Obligation Bonds - Series of 2009 .............................................. 93

Schedule on General Obligation Bonds – Series A of 2009.......................................... 93

Schedule on General Obligation Bonds – Series AA of 2009 ....................................... 94

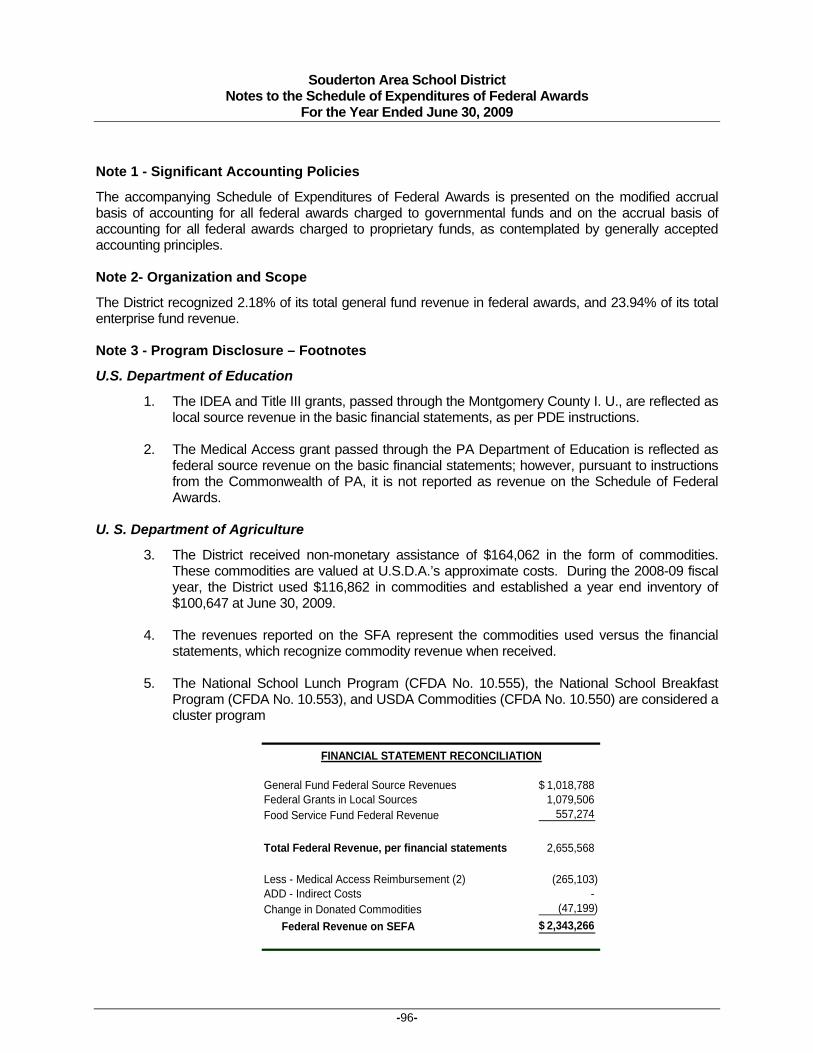

Single Audit Section Schedule of Expenditures of Federal Awards .............................................................................. 95

Notes to the Schedule of Expenditures of Federal Awards .......................................................... 96

Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters based on an Audit of Financial Statements Performed in accordance with Government Auditing Standards................... 97 – 98

Independent Auditor’s Report on Compliance with Requirements Applicable to each Major Program and on Internal Control over Compliance in accordance with OMB Circular A-133 ..................................................... 99 - 100

Schedule of Findings and Questioned Costs .................................................................... 101 - 102

I N T R O D U C T O R Y S E C T I O N

Board of School Directors Dr. Charles Amuso, Superintendent

-3-

In addition, the representation letter provided to us, by management, confirmed there were no uncorrected misstatements. Management has recorded all of our adjusting journal entries, and has agreed to the conversion entries necessary to convert governmental funds and proprietary funds to governmental activities and business-type activities, respectively.

In accordance with auditing standards, generally accepted in the United States of America, we have acquired a sufficient understanding of the District and its environment, including its internal control, to assess the risk of material misstatements of the financial statements whether due to error or fraud, and to design the nature, timing, and extent of further audit procedures that were necessary to express an opinion on the 2008-09 basic financial statements.

Our consideration of the District’s internal control components was not designed for the purpose of making detailed recommendations and would not necessarily disclose all significant deficiencies within the components. Our audit procedures have been appropriately adjusted to compensate for any observed significant deficiencies. The following three paragraphs define the three different types of deficiencies that can occur:

A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis.

A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the entity’s ability to initiate, authorize, record, process, or report financial data reliably, in accordance with generally accepted accounting principles, such that there is more than a remote likelihood that a misstatement of the entity’s financial statements, that is more than inconsequential, will not be prevented or detected by the entity’s internal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the financial statements will not be prevented or detected by the entity’s internal control.

As the primary purpose of our audit is to form an opinion on the basic financial statements, you will appreciate that reliance must be placed on adequate methods of internal control as your principal safeguard against errors and fraud which audit procedures may not disclose. The objective of internal control over financial reporting is to provide reasonable, but not absolute, assurance that assets are safeguarded against loss from unauthorized use and that financial records are reliable for preparing financial statements in accordance with generally accepted accounting principles and for maintaining the accountability for assets. The concept of reasonable assurance recognizes that the cost of internal control should not exceed the related benefits; to operationalize this concept, management is required to formulate estimates and judgments of the cost/benefit ratios of alternative controls.

There are inherent limitations that should be recognized in considering the potential effectiveness of internal control over financial reporting. Errors can result from misunderstanding of instructions, mistakes of judgment, carelessness, fatigue, and other personnel factors. Control procedures whose effectiveness depends upon the segregation of duties can be circumvented by collusion or by management. What's more, any projection of internal control evaluations to future periods is subject to the risk that the procedures may become inadequate because of changes in conditions or due to the deterioration of the degree of compliance with control procedures.

Board of School Directors Dr. Charles Amuso, Superintendent

-4-

As an adjunct to our audit, we remained alert throughout for opportunities to enhance internal controls and operating efficiency. These matters were discussed with management as the audit progressed and have subsequently been reviewed in detail to formulate practical recommendations. We wish to thank your staff for their courtesies and cooperation, which facilitated the efficient performance of audit procedures. The remainder of this letter will explain any internal control deficiencies discovered during the audit, other auditor recommendations, and other information pertinent to the District.

A control deficiency is determined to be considered a material weakness or significant deficiency based upon the magnitude of the problem as it pertains to a particular opinion unit. In other words, what is considered a significant deficiency in one fund may only be a control deficiency in another fund of greater size.

The following section in this governance/management letter is separated by categories based on importance, with any material weaknesses or significant deficiencies listed in the beginning:

CONTROL DEFICIENCIES

General Fund – Tax Collections

During our review of recorded tax revenue, we discovered problems in proving to the various tax duplicates. Although we have had prior year issues associated with the recording of property tax revenues, the business office has attempted to fix these problems each year. The last phase is to correct mispostings and other errors pertaining to the timing of when taxes collected by elected tax collectors are recorded and the District utilizing more accounts than is necessary.

For example, when the elected tax collector deposits taxes collected into the district’s bank accounts, the receipts are not recorded to revenue, until they are transferred to the general fund key account. At that point, they are posted to a revenue clearing account until the tax collector submits the Act 169 monthly report showing what type of tax was collected and deposited during the previous month.

Our recommendations are two-fold. First, we recommend the business office record the deposit to the tax clearing account at the time the tax collector deposits the funds into the district’s bank account, not when the money is transferred to the key account. This recommendation will clear up timing issues that occur during the year. Second, we recommend that the district’s use of recording discounts and penalties to their own general ledger accounts for each municipality should end. This would eliminate positing errors from occurring during the year between the various account codes that exists for each municipality. Following this recommendation, the business office would only record the net amount received for each tax into one revenue account, per municipality. This recommendation will improve the audit trail making it easier to trace each deposit directly to a corresponding tax revenue account.

General Fund – Purchase Orders

During our review of testing invoices in the general fund, we discovered forty-five invoices with purchase orders attached that did not have any approval on the purchase orders. Proper controls pertaining to expenditures requires each purchase order issued to be properly approved reflecting a supervisor’s signature or initials. We recommend the business office improve their review procedures on issued purchase orders.

Board of School Directors Dr. Charles Amuso, Superintendent

-5-

Activity Clubs

During our review of the student activity clubs, we came across the following clubs that may not be considered a student club by the auditor general’s office. As such, we are recommending that this listing be investigated by management to make sure there are proper by-laws, student officers, and appropriate minutes of meetings:

High School Activity:

• AP Guidance

• All School

• Presidential Classroom

• Physical Education

• Starving Artist

• Student Parking

• Career Day

• Men’s Lacrosse Fundraiser

• Senior CD

• School Pop

• Safe Schools

• Girls Lacrosse Fundraiser

• Women’s Volleyball Fundraiser

• Men’s Cross Country Fundraiser

• Golf Fundraiser

• Arts Night Out

• Girls Track Fundraiser

• Class Gift

Indian Crest Jr. High Activity:

• Athletics - should be in the athletic fund

• 30th anniversary brick pavers sale

• Ferdock Fund

• Target/Genuardi’s

• Lost Textbooks

• Fundraisers

Board of School Directors Dr. Charles Amuso, Superintendent

-6-

• PE

• Shop

• England Trip

• Recycling

• General

• Montgomery County 9/11 Memorial Fund

Indian Valley Jr. High Activity:

• Athletics – should be in Athletic Fund

• Fundraising

• Clubs

• General

• Library

• Hawks

• Knights

• Vikings

• Monarchs

2005 AA Construction Fund

During our review of construction fund invoices, we discovered a number of mispostings that occurred between major object codes 450 and 700 series. As examples, check no. 1381 and 1443 were originally posted to object code 757 and later journalized into code 450 in the amount of $388,563.76. These checks should have been coded to object code 788 for infrastructure technology. Check nos. 1402 and 1459 were also miscoded. We would like to recommend the business office utilize the PA School Accounting Manual more closely to verify the correct posting of all construction fund expenditures.

RECOMMENDATIONS

Journal Entries

We would like to recommend all journal entries made during the year should be numbered in numeric sequence, with proper documentation and explanation attached to each entry, and maintained in a three ring binder, segregated by month. By making this improvement the audit trail will improve by tracing the entries posted in the detailed general ledger directly to the journal entry books.

Board of School Directors Dr. Charles Amuso, Superintendent

-7-

Self-balancing accounts

During this year’s audit, we discovered the district was posting across funds in the pentamation computer system. As such, the computer system developed an automatic self-balancing account that was not cleared at the end of the fiscal year. We do not recommend positing across funds, since this creates a problem in tracing the transactions that should be present in each fund. When one fund pays the expenses of another fund, there should be a corresponding interfund receivable and payable account in both funds. In addition, any support from the general fund to pay athletic fund expenditures should be done by the School Board’s approval of an interfund transfer. OTHER INFORMATION

GASB Statement No. 53 – Derivatives During the 2008 calendar year, the Governmental Accounting Standards Board issued the latest accounting principle standard for all governments to follow. GASB Statement No. 53 is associated with the proper accounting and reporting of derivative instruments. The only derivative instruments to be acquired, in the Commonwealth of Pennsylvania, by governments are derivatives pertaining to debt; i.e. interest rate swaps, forward swaptions, constant maturity basis swaps, and etc. Governments who use this type of financial instrument are now required to record the fair value of the derivative onto the government-wide financial statements reflected as an asset or liability. The recording of the net change in fair value depends on the effectiveness of the hedge. These types of financial instruments can potentially save governments money, but are as risky as adjustable rate mortgages versus fixed rate mortgages. If the District would like further clarification of this accounting standard, we will be happy to discuss it with you. The effective date for this standard is the 2009-10 fiscal year. GASB Statement No. 54 – Fund Balancing Reporting In February 2009, the Governmental Accounting Standards Board issued Statement No. 54 redefining the various components of fund balance that is used in government funds (General Fund, Capital Reserve Fund, Athletic Fund, Capital Project Fund, and Debt Service Funds). This standard goes into effect for the 2010-11 fiscal year. The new categories of fund balance are: Nonspendale Restricted Committed Assigned Unassigned The Nonspendable fund balance classification includes amounts that cannot be spent because they are either (a) not in spendable form or (b) legally or contractual required to be maintained intact. The “not in spendable form” includes items not expected to be converted into cash, for example, inventories and prepaid amounts. The corpus (principal) of a permanent fund is an example of an amount that is legally or contractually required to be maintained intact. The Restricted fund balance classification occurs when constraints placed on the use of resources are either:

a. Externally imposed by creditors (such as debt covenants), grantors, contributors, or laws and regulations of other governments; or

-9-

REPORT DISTRIBUTION LIST

The Souderton Area School District has distributed copies of the Single Audit Act Package to the following:

ONE COPY TO: BUREAU OF THE CENSUS (Electronically Filed) DATA PREPARATION DIVISION ONE COPY TO: COMMONWEALTH OF PENNSYLVANIA (Electronically Filed) BUREAU OF AUDITS ONE COPY TO : MONTGOMERY COUNTY INTERMEDIATE UNIT 1605 WEST MAIN STREET NORRISTOWN, PA 19403-3290

F I N A N C I A L S E C T I O N

Souderton Area School District Souderton, Pennsylvania

MANAGEMENT'S DISCUSSION AND ANALYSIS

Required Supplementary Information (RSI) (UNAUDITED)

For the Year Ended June 30, 2009

-12-

The discussion and analysis of Souderton Area School District's financial performance provides an overall review of the District's financial activities for the fiscal year ended June 30, 2009. The intent of this discussion and analysis is to look at the District's financial performance as a whole; readers should also review the financial statements and notes to enhance their understanding of the District's financial performance.

The Management Discussion and Analysis (MD&A) is an element of the new reporting model adopted by the Governmental Accounting Standards Board (GASB) in their Statement No. 34 Basic Financial Statements - and Management's Discussion and Analysis - for State and Local Governments issued June 1999. Certain comparative information between the current year and the prior year is required to be presented in the MD&A.

FINANCIAL HIGHLIGHTS

The 2008-2009 budgets for Souderton Area School District was the first prepared under the guidelines set forth in Act 1 of 2006. Due to the complexity of Act 1, the annual budget was prepared over a period of nine months. Previously the budget was developed over six months. Construction is completed on the new high school, and it opened in September 2009. The construction project significantly reduced the capital projects fund from $30.5 million the prior year to $894 thousand as the funds were used for its intended purpose to construct the new high school. The capital reserve funds also decreased by one million to $7.1 million as funds were used to support the high school construction project. Enrollment had decreased by 71 students for fiscal year 2008-09 compared to a growth of 19 students for 2007-08. The decline in interest rates will continue to erode investment earnings for the school district. The declining real estate market, financial bank crisis, and the overall weakened economy have resulted in fewer new homes in the district. This situation has led to a stagnant student enrollment population in the immediate future. Special education costs continued to increase, jumping to $12.7 million, and an increase of 8.5% over the previous year. The Board of School Directors were able to balance the revenue and expenditure budgets with no real estate tax increase and utilize $1.4 million of fund balance for 2008-09. Actual revenues exceeded the budget by more than $1.1 million. However, actual expenditures, before transfers, exceeded the budget amount by $805 thousand due to the sharp increase in interest expense on the variable rate bond issue. The original budget appropriated $821 thousand of fund balance to be used. However, the significant increase in interest expense that was incurred in the debt service of the variable rate bond caused the fund balance to decrease by $1.4 million. The fund balance of the general fund decreased from $12.4 million to $10.9 million.

USING THE ANNUAL FINANCIAL REPORT

This annual report consists of a series of financial statements and notes to those statements. These statements are organized so the reader can understand Souderton Area School District as a financial whole, an entire operating entity. The statements then proceed to provide an increasingly detailed look at specific financial activities.

The first two statements are government-wide financial statements - the Statement of Net Assets and the Statement of Activities. These provide both long-term and short-term information about the District's overall financial status.

Souderton Area School District Management’s Discussion and Analysis

-13-

The remaining statements are fund financial statements that focus on individual parts of the District’s operations in more detail than the government-wide statements. The governmental funds statements tell how general District services were financed in the short term as well as what remains for future spending. Proprietary fund statements offer short and long-term financial information about the activities that the District operates like a business. For this District this is our Food Service Fund. Fiduciary fund statements provide information about financial relationships where the District acts solely as a trustee or agent for the benefit of others, to whom the resources in question belong.

The financial statements also include notes that explain some of the information in the financial statements and provide more detailed data.

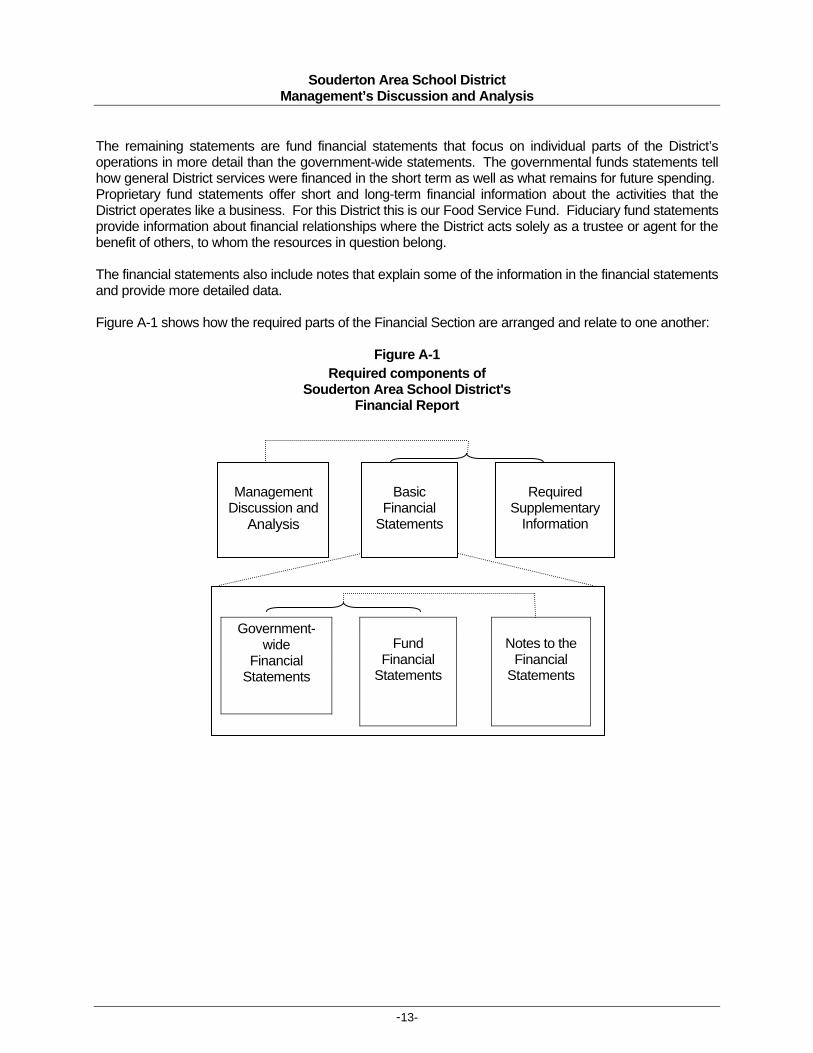

Figure A-1 shows how the required parts of the Financial Section are arranged and relate to one another:

Figure A-1 Required components of

Souderton Area School District's Financial Report

Management

Discussion and Analysis

Basic

Financial Statements

Required

Supplementary Information

Government-wide

Financial Statements

Fund

Financial Statements

Notes to the

Financial Statements

Souderton Area School District Management’s Discussion and Analysis

-14-

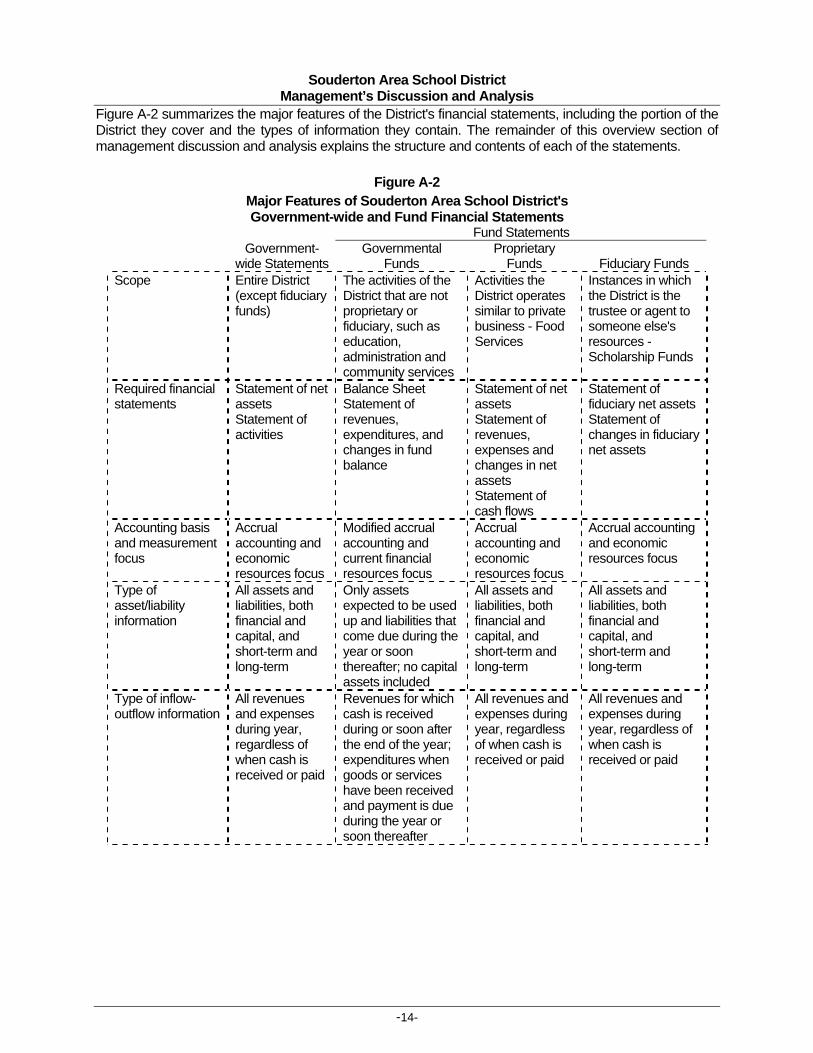

Figure A-2 summarizes the major features of the District's financial statements, including the portion of the District they cover and the types of information they contain. The remainder of this overview section of management discussion and analysis explains the structure and contents of each of the statements.

Figure A-2 Major Features of Souderton Area School District's Government-wide and Fund Financial Statements

Fund Statements Government-

wide Statements Governmental

Funds Proprietary

Funds

Fiduciary Funds Scope Entire District

(except fiduciary funds)

The activities of the District that are not proprietary or fiduciary, such as education, administration and community services

Activities the District operates similar to private business - Food Services

Instances in which the District is the trustee or agent to someone else's resources - Scholarship Funds

Required financial statements

Statement of net assets Statement of activities

Balance Sheet Statement of revenues, expenditures, and changes in fund balance

Statement of net assets Statement of revenues, expenses and changes in net assets Statement of cash flows

Statement of fiduciary net assets Statement of changes in fiduciary net assets

Accounting basis and measurement focus

Accrual accounting and economic resources focus

Modified accrual accounting and current financial resources focus

Accrual accounting and economic resources focus

Accrual accounting and economic resources focus

Type of asset/liability information

All assets and liabilities, both financial and capital, and short-term and long-term

Only assets expected to be used up and liabilities that come due during the year or soon thereafter; no capital assets included

All assets and liabilities, both financial and capital, and short-term and long-term

All assets and liabilities, both financial and capital, and short-term and long-term

Type of inflow-outflow information

All revenues and expenses during year, regardless of when cash is received or paid

Revenues for which cash is received during or soon after the end of the year; expenditures when goods or services have been received and payment is due during the year or soon thereafter

All revenues and expenses during year, regardless of when cash is received or paid

All revenues and expenses during year, regardless of when cash is received or paid

Souderton Area School District Management’s Discussion and Analysis

-15-

OVERVIEW OF FINANCIAL STATEMENTS

Government-wide Statements

The government-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The Statement of Net Assets includes all of the government's assets and liabilities. All of the current year's revenues and expenses are accounted for in the Statement of Activities regardless of when cash is received or paid.

The two government-wide statements report the District’s net assets and how they have changed. Net assets, the difference between the District's assets and liabilities, are one way to measure the District's financial health or position.

Over time, increases or decreases in the District's net assets are an indication of whether its financial health is improving or deteriorating, respectively.

To assess the overall health of the District, you need to consider additional factors, such as the increasing property tax base, outlook for future growth, strength of financial policies and planning, and student performance and achievement.

The government-wide financial statements of the District are divided into two categories:

• Governmental activities - All of the District's basic services are included here, such as instruction, administration and community services. Property taxes and state and federal subsidies and grants finance most of these activities.

• Business type activities -The District operates a food service operation and charges fees to staff, students and visitors to help it cover the costs of the food service operation.

Fund Financial Statements

The District's fund financial statements provide detailed information about the most significant funds - not the District as a whole. Some funds are required by state law and by bond requirements.

Governmental funds - Most of the District's activities are reported in governmental funds, which focus on the determination of financial position and change in financial position, not on income determination. They are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the District's operations and the services it provides. Governmental fund information helps the reader determine whether there are more or fewer financial resources that can be spent in the near future to finance the District's programs. The relationship (or differences) between governmental activities (reported in the Statement of Net Assets and the Statement of Activities) and governmental funds is reconciled in the financial statements.

Proprietary funds - These funds are used to account for the District activities that are similar to business operations in the private sector; or where the reporting is on determining net income, financial position, changes in financial position, and a significant portion of funding through user charges. When the District charges customers for services it provides - whether to outside customers or to other units in the District - these services are generally reported in proprietary funds. The Food Service Fund is the District's proprietary fund and is the same as the business-type activities we report in the government-wide statements, but provide more detail and additional information, such as cash flows.

Souderton Area School District Management’s Discussion and Analysis

-16-

Fiduciary funds - The District is the trustee, or fiduciary, for some scholarship funds. All of the District's fiduciary activities are reported in separate Statements of Fiduciary Net Assets. We exclude these activities from the District's other financial statement because the District cannot use these assets to finance its operations.

FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE

The District's total net assets were $74,859,145 at June 30, 2009. This is a decrease in net assets of $2,808,872 from the net assets for the previous fiscal year.

Table A-1 Fiscal Year ended June 30

Net Assets (In Millions)

Govern- Business- Total Govern- Business- Totalmental Type Primary mental Type Primary

Activities Activities Government Activities Activities GovernmentCurrent assets 25.3$ 0.6$ 25.9$ 43.6$ 0.5$ 44.1$ Non-Current assets 178.9 0.8 179.7 169.5 0.9 170.4

Total Assets 204.2$ 1.4$ 205.6$ 213.1$ 1.4$ 214.5$

Current and other liabilities 10.9 0.1 11.0 12.2 0.1 12.3 Long-term liabilities 119.7 - 11.0 124.5 - 124.5

Total Liabilities 130.6 0.1 22.0 136.7 0.1 136.8

Net AssetsInvested in capital assets, net of related debt 56.8 0.8 57.6 51.2 0.9 52.1 Retirement of Long-Term Debt - - - - - - Other Restrictions 0.3 - 0.3 0.5 0.5 Capital Projects - - - - - - Unrestricted 16.4 0.5 16.9 24.7 0.4 25.1

Total Net Assets 73.5$ 1.3$ 74.8 76.4$ 1.3$ 77.7

2009 2008

Most of the District's net assets are invested in capital assets (buildings, land, and equipment). At June 30, 2009, the District had a balance of $57,587,629 for this class of assets. This is a 10% increase from the $52 million at June 30, 2008. Unrestricted net assets reflect a positive balance which consists of the effect of funds on hand to be invested in capital in future years and the District’s decision not to currently fund long-term benefits for accumulated and unused vacation, sick, other post employment benefits, and early retirement incentive payments.

The results of this year's operations as a whole are reported in the Statement of Activities. All expenses are reported in the first column. Specific charges, grants, revenues and subsidies that directly relate to specific expense categories are represented to determine the final amount of the District's activities that are supported by other general revenues. The two largest general revenues are the local real estate taxes assessed on residents and property owners and grants and entitlements not restricted to specific

Souderton Area School District Management’s Discussion and Analysis

-17-

programs. The Basic Education Subsidy provided by the State of Pennsylvania is the largest example of such a grant. Table A-2 takes the information from that Statement and rearranges it slightly, so that you can see our total revenues for the year.

Table A-2 Fiscal Year ended June 30

Changes in Net Assets (In Thousands)

Govern- Business- Total Govern- Business- Totalmental Type Primary mental Type Primary

Activities Activities Government Activities Activities GovernmentREVENUESProgram revenuesCharges for services 826$ 1,635$ 2,461$ 1,051$ 1,579$ 2,630$ Operating grants and contributions 11,748 687 12,435 12,548 638 13,186 Capital grants and contributions 1,096 - 1,096 1,056 - 1,056 General revenuesProperty taxes 64,208 - 64,208 66,084 - 66,084 Other taxes 7,443 - 7,443 6,793 - 6,793 Grants, subsidies and contributions,

unrestricted 10,126 - 10,126 7,638 - 7,638 Other 1,302 6 1,308 2,489 710 3,199

TOTAL REVENUES 96,749$ 2,328$ 99,077$ 97,659$ 2,927$ 100,586$ - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

EXPENSESInstruction 54,709$ -$ 54,709$ 53,453$ -$ 53,453$ Instructional student support 6,471 - 6,471 6,563 - 6,563 Administrative and financial support 7,435 - 7,435 6,917 - 6,917 Operation and maintenance of plant 8,095 - 8,095 9,267 - 9,267 Pupil transportation 7,404 - 7,404 6,852 - 6,852 Student activities 1,180 - 1,180 1,259 - 1,259 Community services 478 - 478 453 - 453 Interest on long-term debt 12,024 - 12,024 4,718 - 4,718 Unallocated depreciation expense 1,793 - 1,793 1,730 - 1,730 Food Services - 2,297 2,297 - 2,378 2,378

TOTAL EXPENSES 99,589 2,297 101,886 91,212 2,378 93,590

Increase (decrease) in net assets (2,840)$ 31$ (2,809)$ 6,447$ 549$ 6,996$

2009 2008

Total governmental activities expenses of $99,589,977 include $1,793,436 of unallocated depreciation expense. Wages and benefits comprise about two thirds of the total Governmental Activity expenses. Total Business-Type Activities (food services) expenses of $2,296,644 include the costs necessary to operate the cafeterias in all the schools. The District’s practice is to operate food service activities on a break-even basis. Menu prices are reviewed each year and changed to attain this goal. Any excess revenue at year-end is accumulated to offset future large purchases of food service/kitchen equipment. In future years, the Board of Directors may elect to transfer excess funds to the general fund in partial for indirect expenses, such as utilities and cleaning costs. The tables below present the expenses of both the Governmental Activities and the Business-type Activities of the District.

Souderton Area School District Management’s Discussion and Analysis

-18-

Table A-3 shows the District's eight largest functions - instructional programs, instructional student support, administrative, operation and maintenance of plant, pupil transportation, student activities, community services, food service as well as each program's net cost (total cost less revenues generated by the activities). This table also shows the net costs offset by the other unrestricted grants, subsidies and contributions to show the remaining financial needs supported by local taxes and other miscellaneous revenues. Unrestricted grants and subsidies of $10,126,063 were available to reduce the cost of services of governmental activities to a net cost of $75,793,584. Significant unrestricted grants and subsidies include the Basic Education Subsidy which equaled $8,043,562 for 2008-09.

Table A-3 Fiscal Year ended June 30

Governmental Activities (In Thousands)

Total Cost Net Cost Total Cost Net CostFunctions/Programs of Services of Services of Services of ServicesInstruction 54,709$ 46,104$ 53,453$ 44,086$ Instructional student support 6,471 5,843 6,563 5,965 Administrative 7,435 7,206 6,917 6,650 Operation and maintenance 8,095 7,927 9,267 9,062 Pupil transportation 7,404 5,083 6,852 4,304 Student activities 1,180 1,006 1,259 1,111 Community services 478 29 453 (12) Interest on long-term debt 12,024 10,928 4,718 3,662 Unallocated depreciation expense 1,793 1,793 1,730 1,730

Total governmental activities 99,589$ 85,919 91,212$ 76,558 Less:

Unrestricted grants, subsidies 10,126 7,638 Total needs from local

taxes and other revenues 75,793$ 68,920$

2009 2008

Table A-4 reflects the activities of the Food Service program, the only Business-type activity of the District.

Table A 4 Fiscal Year ended June 30 Business-type Activities

Total Cost Net Cost Total Cost Net CostFunctions/Programs of Services of Services of Services of ServicesFood Services 2,296,644$ 25,542$ 2,378,176$ (161,392)$ Less:

Investment earnings & other misc. 5,873 710,388 Total business-type activities 31,415$ 548,996$

2009 2008

The Statement of Revenues, Expense, and Changes in Fund Net Assets for this proprietary fund will further detail the actual results of the operations.

Souderton Area School District Management’s Discussion and Analysis

-19-

THE DISTRICT FUNDS

At June 30, 2009, the District governmental funds reported a combined fund balance of $19,035,553, a decrease of $17,035,815 from the previous year. This was primarily due to the construction of the new high school and the related Capital Project’s fund balance decrease of $9,483,654. The Capital Reserve’s fund balance also declined $2,025,916, as a result of the high school project. The Capital Reserve Fund is also used for unexpected and proposed capital projects each year. In order to fund these projects without the need for additional borrowing issues, the District has established this fund and makes transfers from available fund balance of the General Fund to this fund.

The District General Fund also dropped $1,450,403 to $10,992,058, as a result of the increased interest expense related to the spike in the interest rate on the variable rate bond issue Series of 2007. This situation has been corrected by refinancing this bond with a fixed rate General Obligation Series of 2009. This decrease in the fund balance of other Non-Major Governmental Funds is also related to this refinancing. This fund balance declined by $4,075,842, primarily due to the refinancing of the variable rate bond series of 2007 and the termination of the interest rate swap attached to the bond.

General Fund Budget

During the fiscal year, the Board of School Directors (The Board) authorizes revisions to the original budget to accommodate differences from the original budget to the actual expenditures of the District. All adjustments are again confirmed at the time the annual audit is accepted, which is after the end of the fiscal year, which is not prohibited by state law. A statement showing the District's original and final budget amounts compared with amounts actually paid and received is provided in the Annual Financial Report.

Our local revenues exceeded budgetary figures due to higher than anticipated earned income tax and delinquent real estate. Earned income tax exceeded the budget by $443 thousand and delinquent real estate tax came in at $485 thousand over the budget amount. Interest income on investments came to under the budget by $315 thousand generating $684 thousand in revenues. This is a result of the drop in interest rates due to the weakened economy. State revenue was slightly more than originally budgeted, as was federal revenue.

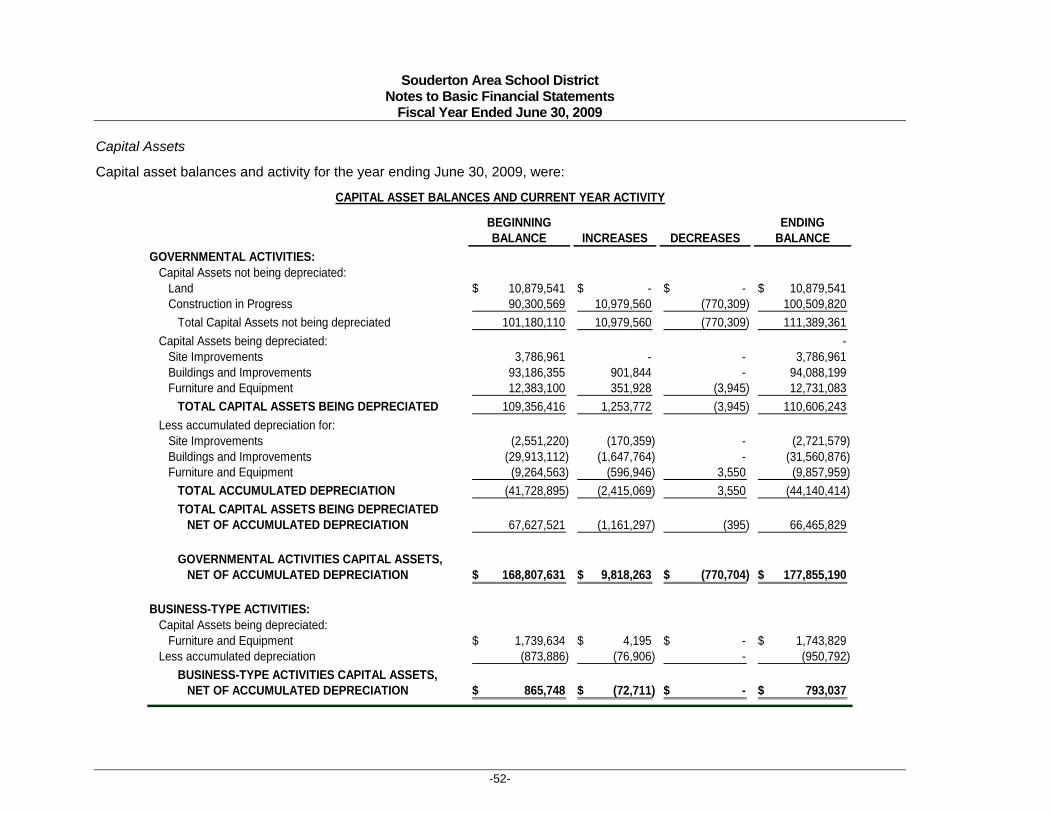

CAPITAL ASSET AND DEBT ADMINISTRATION

CAPITAL ASSETS

At June 30, 2009, the District had $178,648,227 invested in a broad range of capital assets, including land, buildings and furniture and equipment. This amount represents a net increase (including additions, deletions and depreciation) of $8,974,848 from last year. The majority of the increase is the direct result of the construction of the new high school.

Table A-5 Governmental Activities

Fiscal Year Ended June 30 Capital assets - net of depreciation

2009 2008Land 10,879,541$ 10,879,541$ Site Improvements 1,065,382 1,235,741 Buildings 62,527,323 63,273,243 Furniture & Equipment 3,666,161 3,984,285 Construction in Progress 100,509,820 90,300,569

Souderton Area School District Management’s Discussion and Analysis

-20-

The District did not have any significant additions in capital assets other than construction in progress and site improvements.

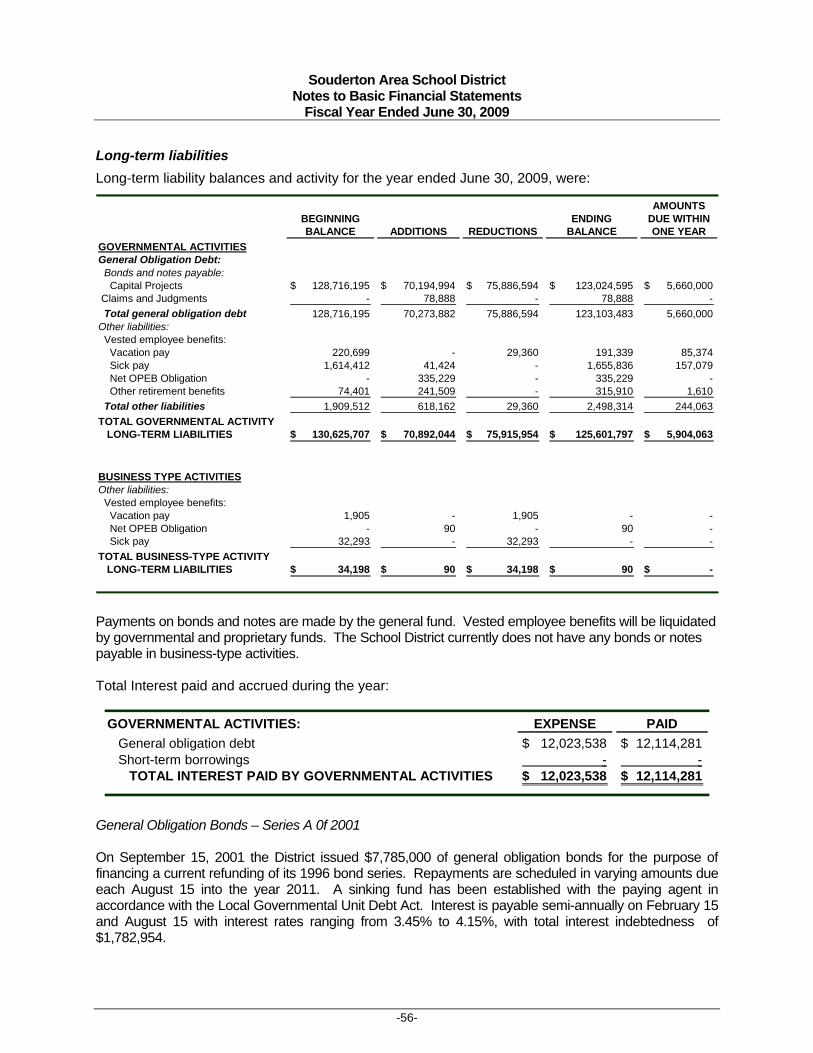

DEBT ADMINISTRATION

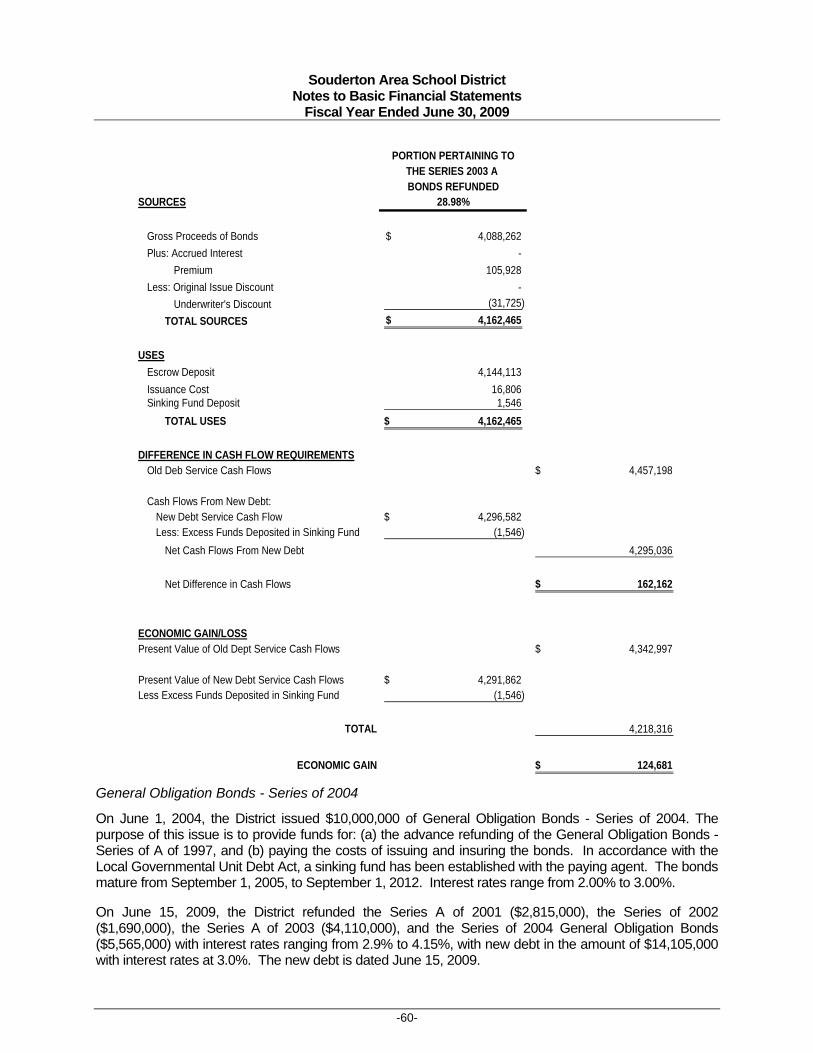

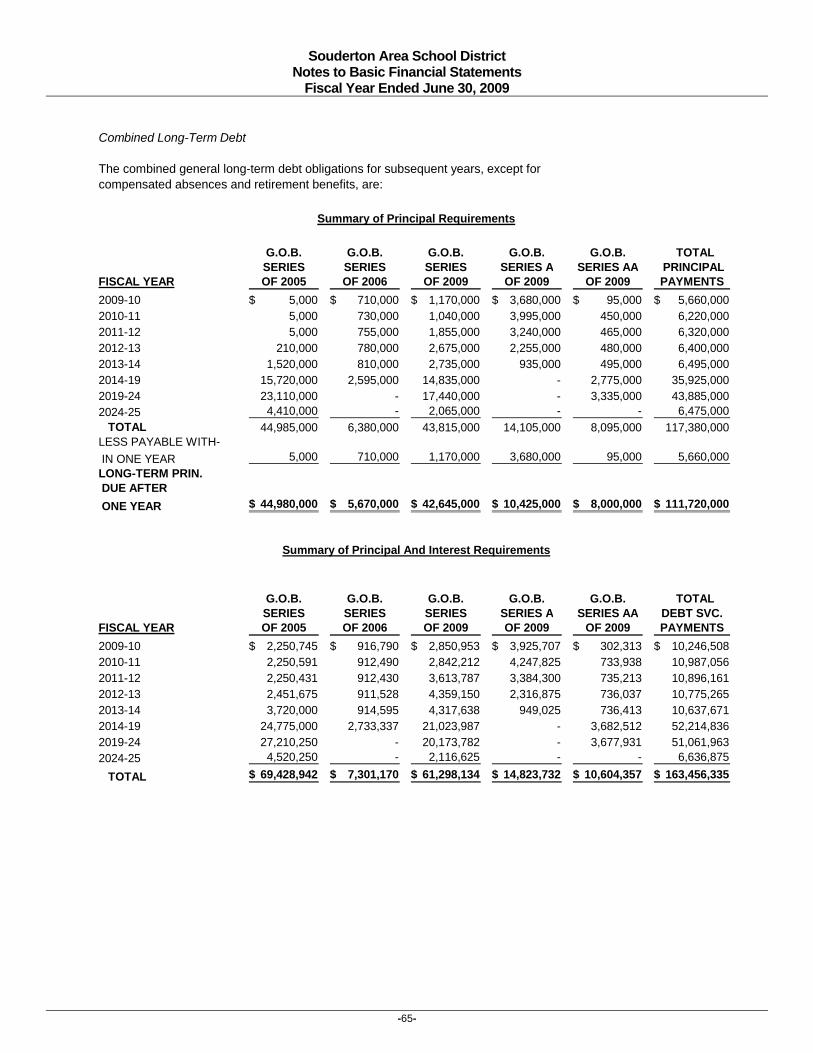

As of July 1, 2008, the District had total outstanding debt of $126,325,000. The District took advantage of lower interest rates last year and refinanced six bond issues to save on interest expense on outstanding debt. The Series of 2007 was refunded and replaced by the Series of 2009. Four bond issues; Series A of 2001, Series of 2002, Series A of 2003, and Series of 2004 were refunded and replaced by Series A 2009. Additionally, Series of 2003 was refunded and replaced by Series AA of 2009. The total savings to the district amounted to $677,265. During the year, the District issued no additional debt and retired and repaid $8,945,000 of principal resulting in ending outstanding debt as of June 30, 2009, of $117,380,000.

Table A-6 Outstanding Debt

2009 2008General Obligation Notes/Bonds: - Bonds, Series of 2009 AA 8,095,000$ -$ - Bond, Series of 2009 A 14,105,000 - - Bonds, Series of 2009 43,815,000 - - Bonds, Series of 2007 46,920,000 - Bonds, Series of 2006 6,380,000 7,060,000 - Bonds, Series of 2005 44,985,000 44,990,000 - Bonds, Series of 2004 - 6,860,000 - Bond, Series A of 2003 - 4,865,000 - Bonds, Series of 2003 - 8,515,000 - Bonds, Series of 2002 - 3,430,000 - Bonds, Series A of 2001 - 3,685,000

TOTAL 117,380,000$ 126,325,000$

Other obligations include accrued vacation pay and sick leave for specific employees of the District. More detailed information about our long-term liabilities is included in the notes to the financial statements.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS AND RATES

In May, 2009, Standard and Poor’s issued an underlying rating of “AA”. This rating means the district has an extremely strong capacity to meet its financial commitments. It is expected the “the district will maintain a stable financial position given a track record of conservative budgeting practices.

The financial future of the District will be impacted by employment agreements and/or contracts for the employee groups listed below. Included is the expiration date of each existing agreement.

a) Employee Group b) Members c) Agreement

Expiration Date

Act 93 Administration June 30, 2010 Souderton Area Education Assn. Professional Staff June 30, 2012 Secretaries Secretaries/Bookkeepers June 30, 2010 Teamsters Custodial/Maintenance/Grounds June 30, 2010 Building Facility Managers Building Facility Managers June 30, 2010 Support Staff Aides June 30, 2010 Cabinet Administrators Cabinet Administration June 30, 2010 Cabinet Secretaries Cabinet Secretaries June 30, 2010

Souderton Area School District Management’s Discussion and Analysis

-21-

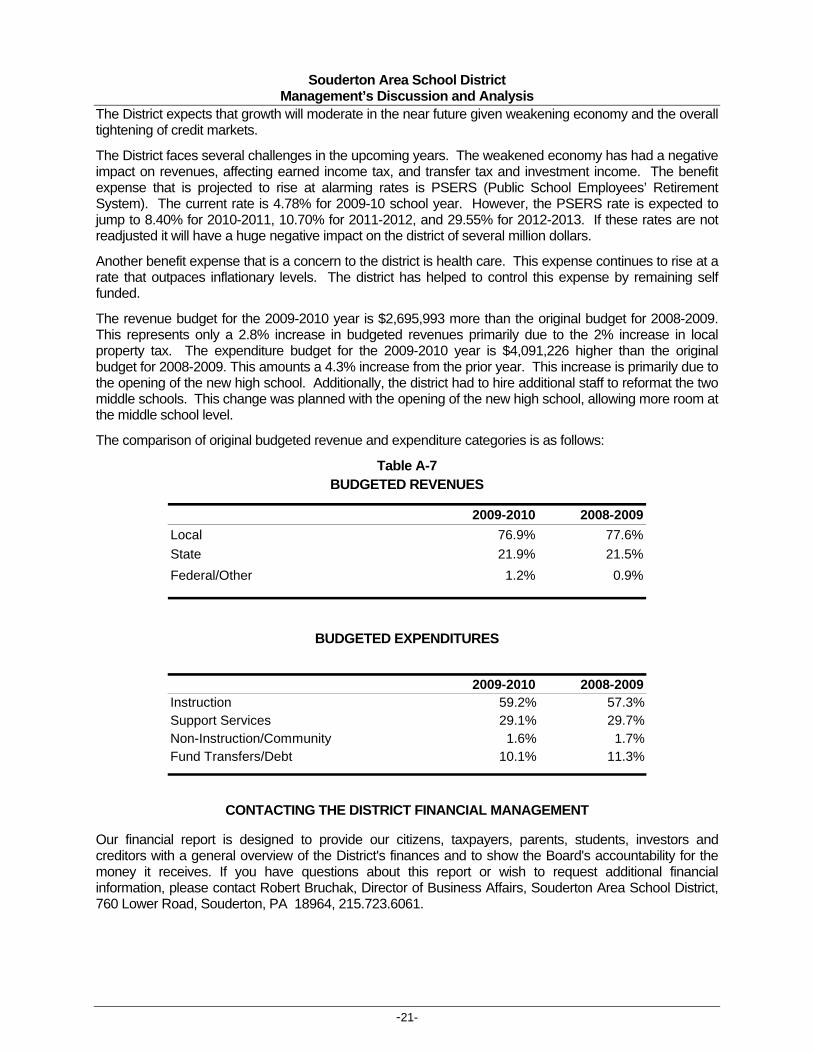

The District expects that growth will moderate in the near future given weakening economy and the overall tightening of credit markets.

The District faces several challenges in the upcoming years. The weakened economy has had a negative impact on revenues, affecting earned income tax, and transfer tax and investment income. The benefit expense that is projected to rise at alarming rates is PSERS (Public School Employees’ Retirement System). The current rate is 4.78% for 2009-10 school year. However, the PSERS rate is expected to jump to 8.40% for 2010-2011, 10.70% for 2011-2012, and 29.55% for 2012-2013. If these rates are not readjusted it will have a huge negative impact on the district of several million dollars.

Another benefit expense that is a concern to the district is health care. This expense continues to rise at a rate that outpaces inflationary levels. The district has helped to control this expense by remaining self funded.

The revenue budget for the 2009-2010 year is $2,695,993 more than the original budget for 2008-2009. This represents only a 2.8% increase in budgeted revenues primarily due to the 2% increase in local property tax. The expenditure budget for the 2009-2010 year is $4,091,226 higher than the original budget for 2008-2009. This amounts a 4.3% increase from the prior year. This increase is primarily due to the opening of the new high school. Additionally, the district had to hire additional staff to reformat the two middle schools. This change was planned with the opening of the new high school, allowing more room at the middle school level.

The comparison of original budgeted revenue and expenditure categories is as follows:

Table A-7 BUDGETED REVENUES

2009-2010 2008-2009Local 76.9% 77.6%State 21.9% 21.5%Federal/Other 1.2% 0.9%

BUDGETED EXPENDITURES

2009-2010 2008-2009Instruction 59.2% 57.3%Support Services 29.1% 29.7%Non-Instruction/Community 1.6% 1.7%Fund Transfers/Debt 10.1% 11.3%

CONTACTING THE DISTRICT FINANCIAL MANAGEMENT

Our financial report is designed to provide our citizens, taxpayers, parents, students, investors and creditors with a general overview of the District's finances and to show the Board's accountability for the money it receives. If you have questions about this report or wish to request additional financial information, please contact Robert Bruchak, Director of Business Affairs, Souderton Area School District, 760 Lower Road, Souderton, PA 18964, 215.723.6061.

B A S I C F I N A N C I A L S T A T E M E N T S

-22-

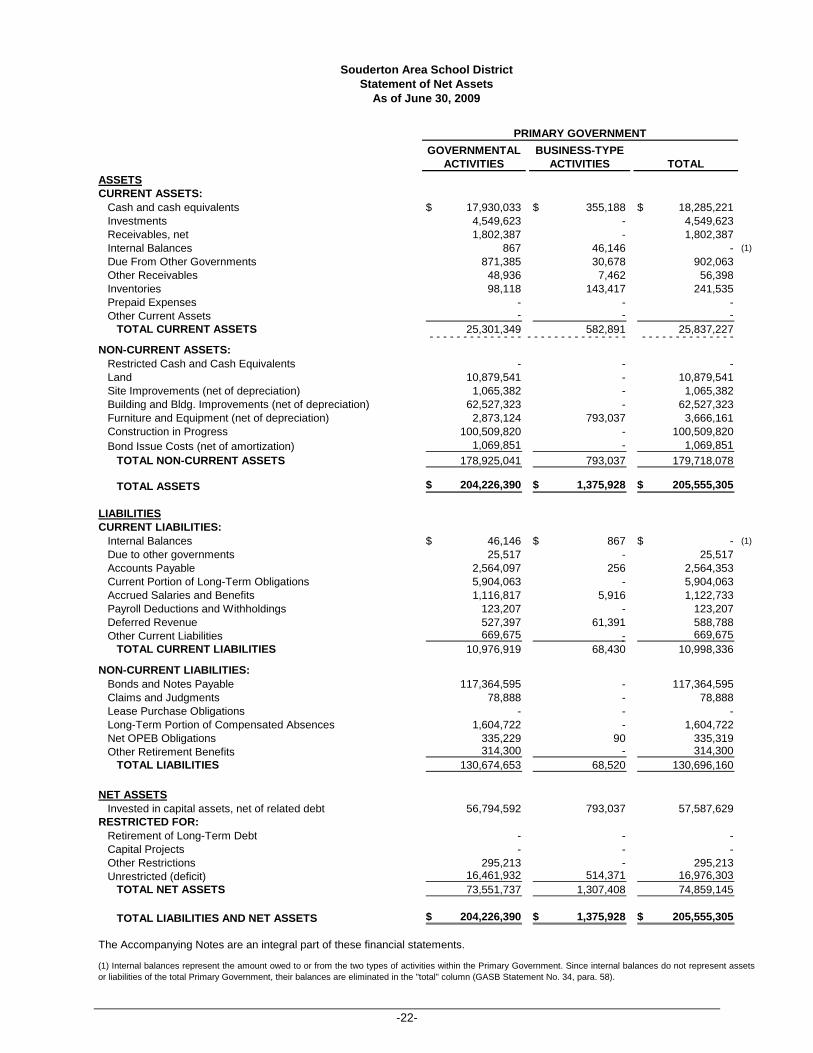

GOVERNMENTAL BUSINESS-TYPEACTIVITIES ACTIVITIES TOTAL

ASSETSCURRENT ASSETS:

Cash and cash equivalents 17,930,033$ 355,188$ 18,285,221$ Investments 4,549,623 - 4,549,623 Receivables, net 1,802,387 - 1,802,387 Internal Balances 867 46,146 - (1)Due From Other Governments 871,385 30,678 902,063 Other Receivables 48,936 7,462 56,398 Inventories 98,118 143,417 241,535 Prepaid Expenses - - - Other Current Assets - - -

TOTAL CURRENT ASSETS 25,301,349 582,891 25,837,227 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -NON-CURRENT ASSETS:

Restricted Cash and Cash Equivalents - - - Land 10,879,541 - 10,879,541 Site Improvements (net of depreciation) 1,065,382 - 1,065,382 Building and Bldg. Improvements (net of depreciation) 62,527,323 - 62,527,323 Furniture and Equipment (net of depreciation) 2,873,124 793,037 3,666,161 Construction in Progress 100,509,820 - 100,509,820 Bond Issue Costs (net of amortization) 1,069,851 - 1,069,851

TOTAL NON-CURRENT ASSETS 178,925,041 793,037 179,718,078

TOTAL ASSETS 204,226,390$ 1,375,928$ 205,555,305$

LIABILITIESCURRENT LIABILITIES:

Internal Balances 46,146$ 867$ -$ (1)Due to other governments 25,517 - 25,517 Accounts Payable 2,564,097 256 2,564,353 Current Portion of Long-Term Obligations 5,904,063 - 5,904,063 Accrued Salaries and Benefits 1,116,817 5,916 1,122,733 Payroll Deductions and Withholdings 123,207 - 123,207 Deferred Revenue 527,397 61,391 588,788 Other Current Liabilities 669,675 - 669,675

TOTAL CURRENT LIABILITIES 10,976,919 68,430 10,998,336

NON-CURRENT LIABILITIES:Bonds and Notes Payable 117,364,595 - 117,364,595 Claims and Judgments 78,888 - 78,888 Lease Purchase Obligations - - - Long-Term Portion of Compensated Absences 1,604,722 - 1,604,722 Net OPEB Obligations 335,229 90 335,319 Other Retirement Benefits 314,300 - 314,300

TOTAL LIABILITIES 130,674,653 68,520 130,696,160

NET ASSETSInvested in capital assets, net of related debt 56,794,592 793,037 57,587,629

RESTRICTED FOR: Retirement of Long-Term Debt - - - Capital Projects - - - Other Restrictions 295,213 - 295,213 Unrestricted (deficit) 16,461,932 514,371 16,976,303

TOTAL NET ASSETS 73,551,737 1,307,408 74,859,145

TOTAL LIABILITIES AND NET ASSETS 204,226,390$ 1,375,928$ 205,555,305$

The Accompanying Notes are an integral part of these financial statements.

(1) Internal balances represent the amount owed to or from the two types of activities within the Primary Government. Since internal balances do not represent assetsor liabilities of the total Primary Government, their balances are eliminated in the "total" column (GASB Statement No. 34, para. 58).

PRIMARY GOVERNMENT

Souderton Area School DistrictStatement of Net Assets

As of June 30, 2009

-23-

OPERATING CAPITAL

CHARGES FOR GRANTS AND GRANTS AND GOVERNMENTAL BUSINESS-TYPEFUNCTIONS/PROGRAMS EXPENSES SERVICES CONTRIBUTIONS CONTRIBUTIONS ACTIVITIES ACTIVITIES TOTALGOVERNMENTAL ACTIVITIES:

Instruction 54,709,379$ 235,337$ 8,368,588$ -$ (46,105,454)$ -$ (46,105,454)$ Instructional Student Support 6,470,429 - 627,948 - (5,842,481) - (5,842,481) Admin. & Fin'l Support Services 7,435,243 - 228,800 - (7,206,443) - (7,206,443) Oper. & Maint. of Plant Svcs. 8,095,328 - 168,766 - (7,926,562) - (7,926,562) Pupil Transportation 7,404,286 2,176 2,319,011 - (5,083,099) - (5,083,099) Student activities 1,180,311 140,576 33,907 - (1,005,828) - (1,005,828) Community Services 478,027 447,872 1,350 - (28,805) - (28,805) Interest on Long-Term Debt 12,023,538 - - 1,095,999 (10,927,539) - (10,927,539) Unallocated Depreciation Expense 1,793,436 - - - (1,793,436) - (1,793,436)

TOTAL GOVERNMENTAL ACTIVITIES 99,589,977 825,961 11,748,370 1,095,999 (85,919,647) - (85,919,647)

BUSINESS-TYPE ACTIVITIES: Food Services 2,296,644 1,635,446 686,740 - - 25,542 25,542 Other Enterprise Funds - - - - - - -

TOTAL PRIMARY GOVERNMENT 101,886,621$ 2,461,407$ 12,435,110$ 1,095,999$ (85,919,647)$ 25,542$ (85,894,105)$ - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

GENERAL REVENUES:Property taxes. Levied for general purposes, net 64,207,870$ -$ 64,207,870$ Taxes levied for specific purposes 7,443,341 - 7,443,341 Grants, subsidies, & contributions not restricted 10,126,063 - 10,126,063 Investment Earnings 988,525 5,873 994,398 Miscellaneous Income 313,880 - 313,880 Special item - Gain (Loss) on sale of capital assets (319) - (319) Extraordinary Items - - Transfers - - -

TOTAL GENERAL REVENUES, SPECIAL ITEMS,EXTRAORDINARY ITEMS, AND TRANSFERS 83,079,360 5,873 83,085,233

CHANGE IN NET ASSETS (2,840,287) 31,415 (2,808,872)

NET ASSETS - BEGINNING 76,392,024 1,275,993 77,668,017

NET ASSETS - ENDING 73,551,737$ 1,307,408$ 74,859,145$

The Accompanying Notes are an integral part of these financial statements.

PROGRAM REVENUES NET (EXPENSE) REVENUEAND CHANGES IN NET ASSETS

Souderton Area School DistrictStatement of Activities

For the Year Ended June 30, 2009

-24-

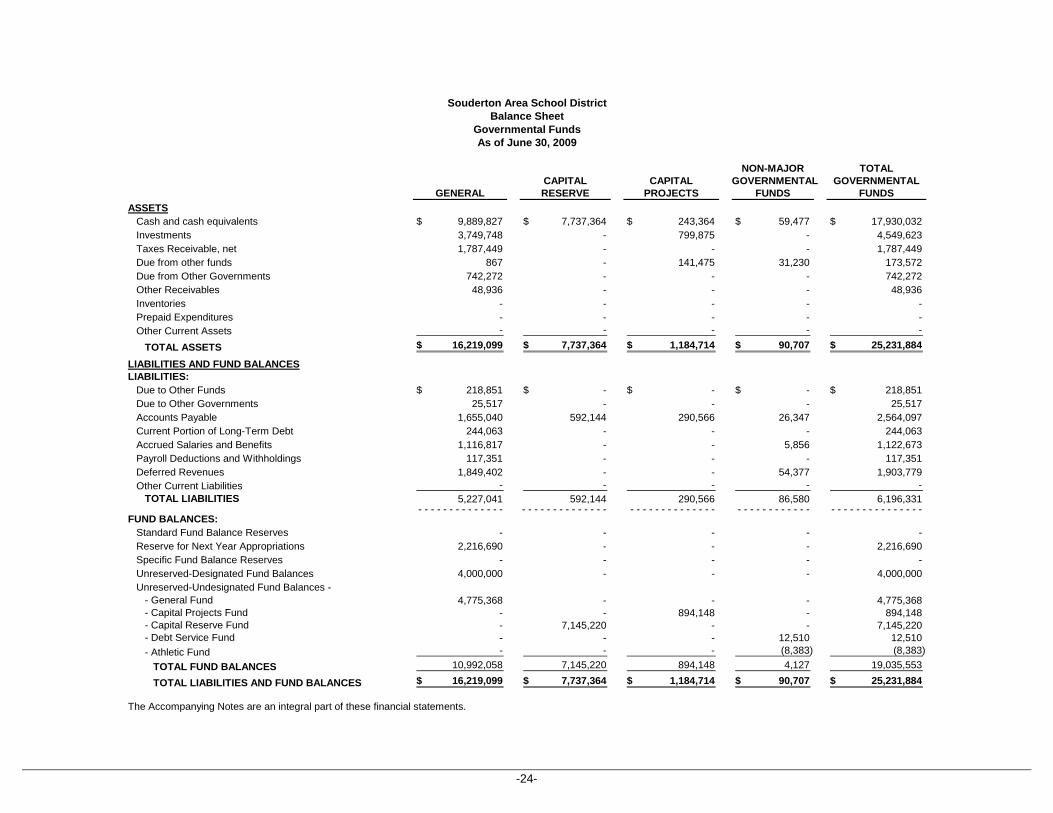

NON-MAJOR TOTALCAPITAL CAPITAL GOVERNMENTAL GOVERNMENTAL

GENERAL RESERVE PROJECTS FUNDS FUNDSASSETS

Cash and cash equivalents 9,889,827$ 7,737,364$ 243,364$ 59,477$ 17,930,032$ Investments 3,749,748 - 799,875 - 4,549,623 Taxes Receivable, net 1,787,449 - - - 1,787,449 Due from other funds 867 - 141,475 31,230 173,572 Due from Other Governments 742,272 - - - 742,272 Other Receivables 48,936 - - - 48,936 Inventories - - - - - Prepaid Expenditures - - - - - Other Current Assets - - - - -

TOTAL ASSETS 16,219,099$ 7,737,364$ 1,184,714$ 90,707$ 25,231,884$

LIABILITIES AND FUND BALANCESLIABILITIES:

Due to Other Funds 218,851$ -$ -$ -$ 218,851$ Due to Other Governments 25,517 - - - 25,517 Accounts Payable 1,655,040 592,144 290,566 26,347 2,564,097 Current Portion of Long-Term Debt 244,063 - - - 244,063 Accrued Salaries and Benefits 1,116,817 - - 5,856 1,122,673 Payroll Deductions and Withholdings 117,351 - - - 117,351 Deferred Revenues 1,849,402 - - 54,377 1,903,779 Other Current Liabilities - - - - -

TOTAL LIABILITIES 5,227,041 592,144 290,566 86,580 6,196,331 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

FUND BALANCES:Standard Fund Balance Reserves - - - - - Reserve for Next Year Appropriations 2,216,690 - - - 2,216,690 Specific Fund Balance Reserves - - - - - Unreserved-Designated Fund Balances 4,000,000 - - - 4,000,000 Unreserved-Undesignated Fund Balances -

- General Fund 4,775,368 - - - 4,775,368 - Capital Projects Fund - - 894,148 - 894,148 - Capital Reserve Fund - 7,145,220 - - 7,145,220 - Debt Service Fund - - - 12,510 12,510 - Athletic Fund - - - (8,383) (8,383)

TOTAL FUND BALANCES 10,992,058 7,145,220 894,148 4,127 19,035,553

TOTAL LIABILITIES AND FUND BALANCES 16,219,099$ 7,737,364$ 1,184,714$ 90,707$ 25,231,884$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictBalance Sheet

Governmental FundsAs of June 30, 2009

-25-

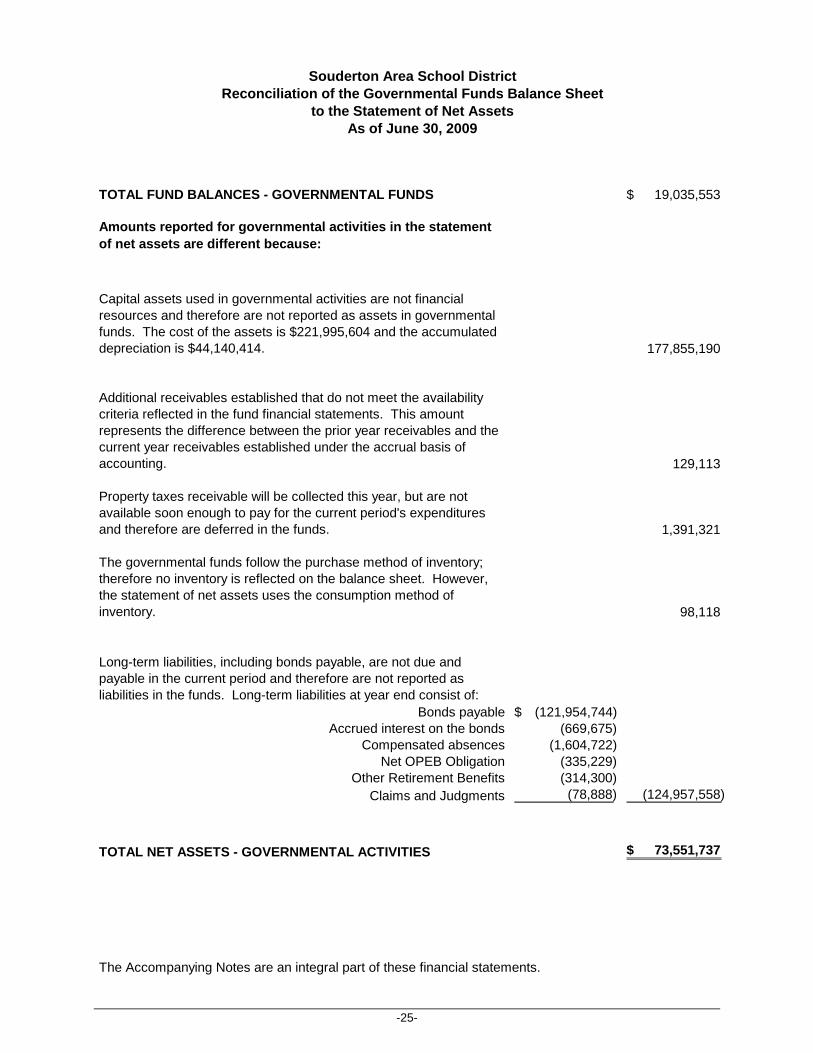

TOTAL FUND BALANCES - GOVERNMENTAL FUNDS 19,035,553$

Amounts reported for governmental activities in the statement of net assets are different because:

Capital assets used in governmental activities are not financial resources and therefore are not reported as assets in governmental funds. The cost of the assets is $221,995,604 and the accumulated depreciation is $44,140,414. 177,855,190

Additional receivables established that do not meet the availability criteria reflected in the fund financial statements. This amount represents the difference between the prior year receivables and the current year receivables established under the accrual basis of accounting. 129,113

Property taxes receivable will be collected this year, but are not available soon enough to pay for the current period's expenditures and therefore are deferred in the funds. 1,391,321

The governmental funds follow the purchase method of inventory; therefore no inventory is reflected on the balance sheet. However, the statement of net assets uses the consumption method of inventory. 98,118

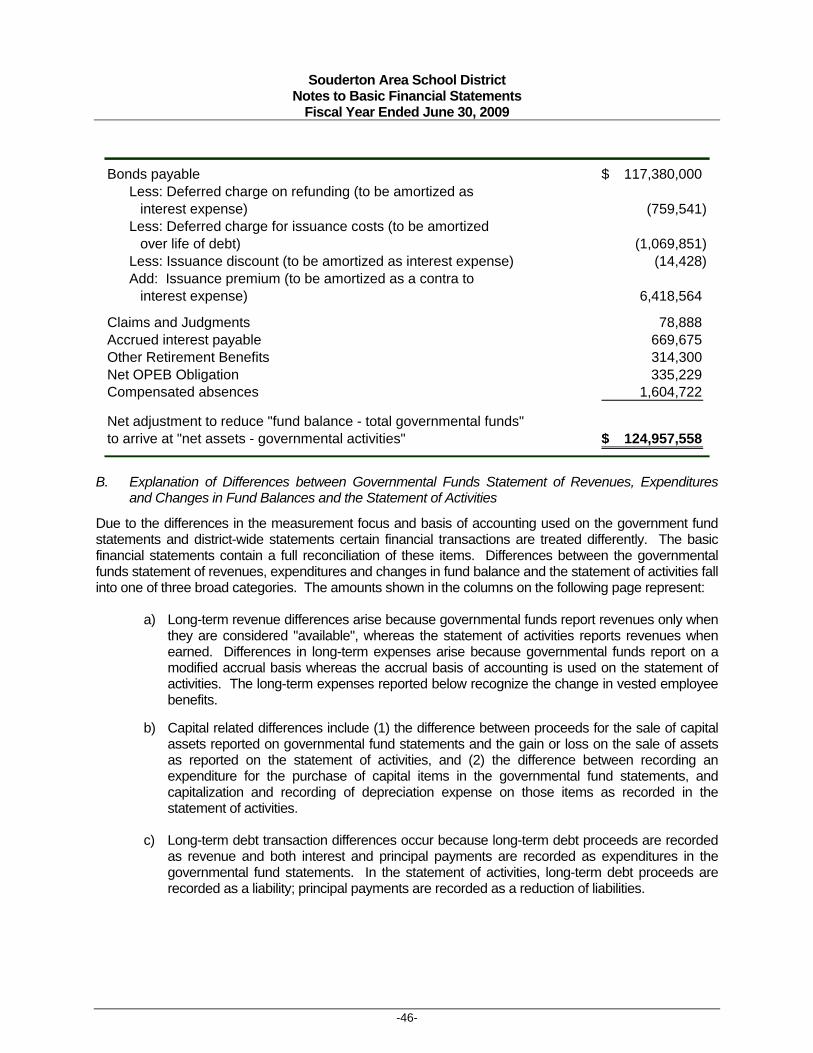

Long-term liabilities, including bonds payable, are not due and payable in the current period and therefore are not reported as liabilities in the funds. Long-term liabilities at year end consist of:

Bonds payable (121,954,744)$ Accrued interest on the bonds (669,675)

Compensated absences (1,604,722) Net OPEB Obligation (335,229)

Other Retirement Benefits (314,300) Claims and Judgments (78,888) (124,957,558)

TOTAL NET ASSETS - GOVERNMENTAL ACTIVITIES 73,551,737$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictReconciliation of the Governmental Funds Balance Sheet

to the Statement of Net AssetsAs of June 30, 2009

-26-

NON-MAJOR TOTALCAPITAL CAPITAL GOVERNMENTAL GOVERNMENTAL

GENERAL RESERVE PROJECTS FUNDS FUNDSREVENUES

Local Sources 74,522,696$ 142,308$ 97,536$ 137,780$ 74,900,320$ State Sources 20,681,819 - - 31,207 20,713,026 Federal Sources 1,018,788 - - - 1,018,788

TOTAL REVENUES 96,223,303 142,308 97,536 168,987 96,632,134 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

EXPENDITURESInstruction 54,322,645 - 118,080 - 54,440,725 Support Services 28,027,791 617 21,974 768,199 28,818,581 Operation of Non-Instructional Services 578,438 - 9,656 1,097,822 1,685,916 Capital Outlay - 2,215,638 9,431,480 - 11,647,118 Debt Service 13,762,281 - - 4,092,000 17,854,281

TOTAL EXPENDITURES 96,691,155 2,216,255 9,581,190 5,958,021 114,446,621

EXCESS (DEFICIENCY) OF REVENUES OVER EXPENDITURES (467,852) (2,073,947) (9,483,654) (5,789,034) (17,814,487)

OTHER FINANCING SOURCES (USES)Proceeds from Bond Issues - - - - - Refunding Bond Proceeds - - - 66,015,000 66,015,000 Bond Premiums - - - 4,129,207 4,129,207 Proceeds from Extended Term Financing - - - - - Interfund Transfers In - 48,031 - 934,595 982,626 Sale/Compensation for Fixed Assets 75 - - - 75 Payment to bond refunding escrow agent - - - (69,365,610) (69,365,610) Bond Discounts - - - - - Refunds of Prior Year Receipts - - - - - Operating Transfers Out (982,626) - - - (982,626)

TOTAL OTHER FINANCING SOURCES (USES) (982,551) 48,031 - 1,713,192 778,672

SPECIAL/EXTRAORDINARY ITEMSSpecial Items - - - - - Extraordinary Items - - - - -

NET CHANGE IN FUND BALANCES (1,450,403) (2,025,916) (9,483,654) (4,075,842) (17,035,815)

FUND BALANCES - BEGINNING 12,442,461 9,171,136 10,377,802 4,079,969 36,071,368

FUND BALANCES - ENDING 10,992,058$ 7,145,220$ 894,148$ 4,127$ 19,035,553$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Revenues, Expenditures, and Changes in Fund Balances

Governmental FundsFor the Year Ended June 30, 2009

-27-

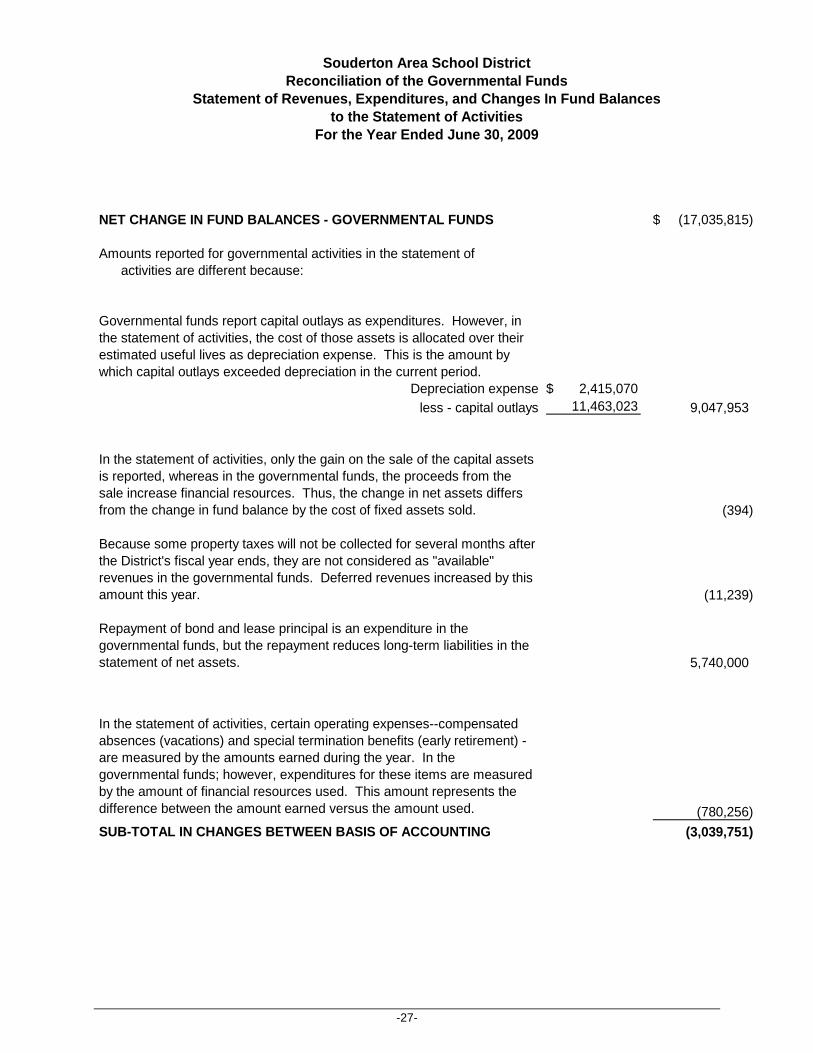

NET CHANGE IN FUND BALANCES - GOVERNMENTAL FUNDS (17,035,815)$

Amounts reported for governmental activities in the statement ofactivities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the current period.

Depreciation expense $ 2,415,070 less - capital outlays 11,463,023 9,047,953

In the statement of activities, only the gain on the sale of the capital assets is reported, whereas in the governmental funds, the proceeds from the sale increase financial resources. Thus, the change in net assets differs from the change in fund balance by the cost of fixed assets sold. (394)

Because some property taxes will not be collected for several months after the District's fiscal year ends, they are not considered as "available" revenues in the governmental funds. Deferred revenues increased by this amount this year. (11,239)

Repayment of bond and lease principal is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in the statement of net assets. 5,740,000

In the statement of activities, certain operating expenses--compensated absences (vacations) and special termination benefits (early retirement) - are measured by the amounts earned during the year. In the governmental funds; however, expenditures for these items are measured by the amount of financial resources used. This amount represents the difference between the amount earned versus the amount used. (780,256) SUB-TOTAL IN CHANGES BETWEEN BASIS OF ACCOUNTING (3,039,751)

For the Year Ended June 30, 2009

Souderton Area School DistrictReconciliation of the Governmental Funds

Statement of Revenues, Expenditures, and Changes In Fund Balancesto the Statement of Activities

-28-

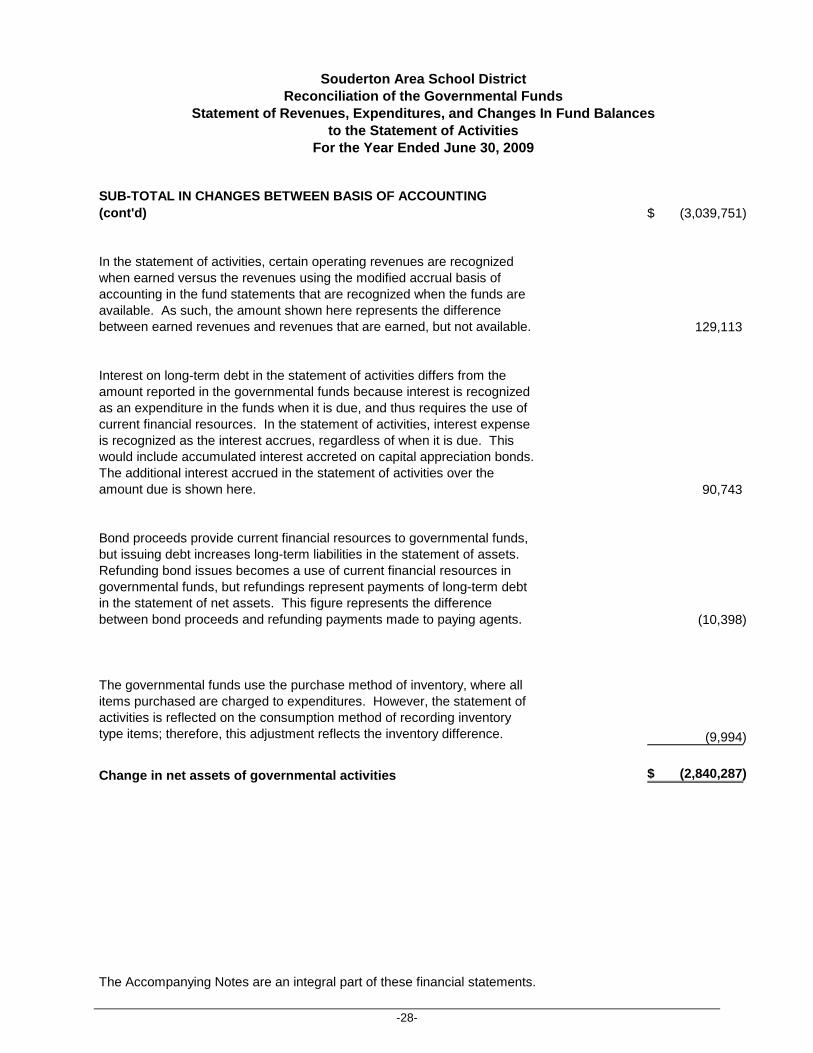

SUB-TOTAL IN CHANGES BETWEEN BASIS OF ACCOUNTING (cont'd) (3,039,751)$

In the statement of activities, certain operating revenues are recognized when earned versus the revenues using the modified accrual basis of accounting in the fund statements that are recognized when the funds are available. As such, the amount shown here represents the difference between earned revenues and revenues that are earned, but not available. 129,113

Interest on long-term debt in the statement of activities differs from the amount reported in the governmental funds because interest is recognized as an expenditure in the funds when it is due, and thus requires the use of current financial resources. In the statement of activities, interest expense is recognized as the interest accrues, regardless of when it is due. This would include accumulated interest accreted on capital appreciation bonds. The additional interest accrued in the statement of activities over the amount due is shown here. 90,743

Bond proceeds provide current financial resources to governmental funds, but issuing debt increases long-term liabilities in the statement of assets. Refunding bond issues becomes a use of current financial resources in governmental funds, but refundings represent payments of long-term debt in the statement of net assets. This figure represents the difference between bond proceeds and refunding payments made to paying agents. (10,398)

The governmental funds use the purchase method of inventory, where all items purchased are charged to expenditures. However, the statement of activities is reflected on the consumption method of recording inventory type items; therefore, this adjustment reflects the inventory difference. (9,994)

Change in net assets of governmental activities (2,840,287)$

The Accompanying Notes are an integral part of these financial statements.

to the Statement of ActivitiesFor the Year Ended June 30, 2009

Souderton Area School DistrictReconciliation of the Governmental Funds

Statement of Revenues, Expenditures, and Changes In Fund Balances

-29-

FOOD NON-MAJORSERVICE FUNDS TOTAL

ASSETSCURRENT ASSETS:

Cash and cash equivalents 355,188$ -$ 355,188$ Investments - - - Due from other funds 46,146 - 46,146 Due From Other Governments 30,678 - 30,678 Other Receivables 7,462 - 7,462 Inventories 143,417 - 143,417 Prepaid expenses - - - Other Current Assets - - -

TOTAL CURRENT ASSETS 582,891 - 582,891 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

NON-CURRENT ASSETS:Building & Bldg. Improvements (net) - - - Machinery & Equipment (net) 793,037 - 793,037 Other Long-Term Receivables - - -

TOTAL NON-CURRENT ASSETS 793,037 - 793,037

TOTAL ASSETS 1,375,928$ -$ 1,375,928$

LIABILITIESCURRENT LIABILITIES:

Due to Other Funds 867$ -$ 867$ Due to Other Governments - - - Accounts Payable 256 - 256 Compensated Absences - - - Accrued Salaries and Benefits 5,916 - 5,916 Payroll Deductions and Withholdings - - - Deferred Revenue 61,391 - 61,391

TOTAL CURRENT LIABILITIES 68,430 - 68,430 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

NON-CURRENT LIABILITIES:Long-Term Portion of Compensated Absences - - - Net OPEB Obligation 90 - 90

TOTAL NON-CURRENT LIABILITIES 90 - 90 TOTAL LIABILITIES 68,520 - 68,520

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

NET ASSETSInvested in capital assets, with no related debt 793,037 - 793,037 Restricted for Legal Purposes - - - Unrestricted 514,371 - 514,371

TOTAL NET ASSETS 1,307,408 - 1,307,408 TOTAL LIABILITIES AND NET ASSETS 1,375,928$ -$ 1,375,928$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Net Assets

Proprietary FundsAs of June 30, 2009

-30-

FOOD NON-MAJOR SERVICE FUNDS TOTAL

OPERATING REVENUES:Food Service Revenue 1,595,512$ -$ 1,595,512$ Charges for Services - - - Other Operating Revenues 39,934 - 39,934

TOTAL OPERATING REVENUES 1,635,446 - 1,635,446 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

OPERATING EXPENSES: Salaries 719,085 - 719,085 Employee Benefits 221,734 - 221,734 Purchased Professional and Technical Services 6,969 - 6,969 Purchased Property Service 75,761 - 75,761 Other Purchased Services 4,723 - 4,723 Supplies 1,168,302 - 1,168,302 Depreciation 76,906 - 76,906 Dues and Fees 729 - 729 Claims and Judgments - - - Other Operating Expenses 22,435 - 22,435

TOTAL OPERATING EXPENSES 2,296,644 - 2,296,644 OPERATING INCOME (LOSS) (661,198) - (661,198)

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

NON-OPERATING REVENUES (EXPENSES)Earnings on investments 5,873 - 5,873 Contributions and Donations - - - Gain/Loss on Sale of Fixed Assets - - - State Sources 129,466 - 129,466 Federal Sources 557,274 - 557,274

TOTAL NON-OPERATING REVENUES (EXPENSES) 692,613 - 692,613

INCOME (LOSS) BEFORE CONTRIBUTIONS 31,415 - 31,415

Capital Contributions - - - Transfers in (out) - - -

CHANGES IN NET ASSETS 31,415 - 31,415

NET ASSETS - BEGINNING 1,275,993 - 1,275,993

NET ASSETS - ENDING 1,307,408$ -$ 1,307,408$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Revenues, Expenses, and Changes in Net Assets

Proprietary FundsFor the Year Ended June 30, 2009

-31-

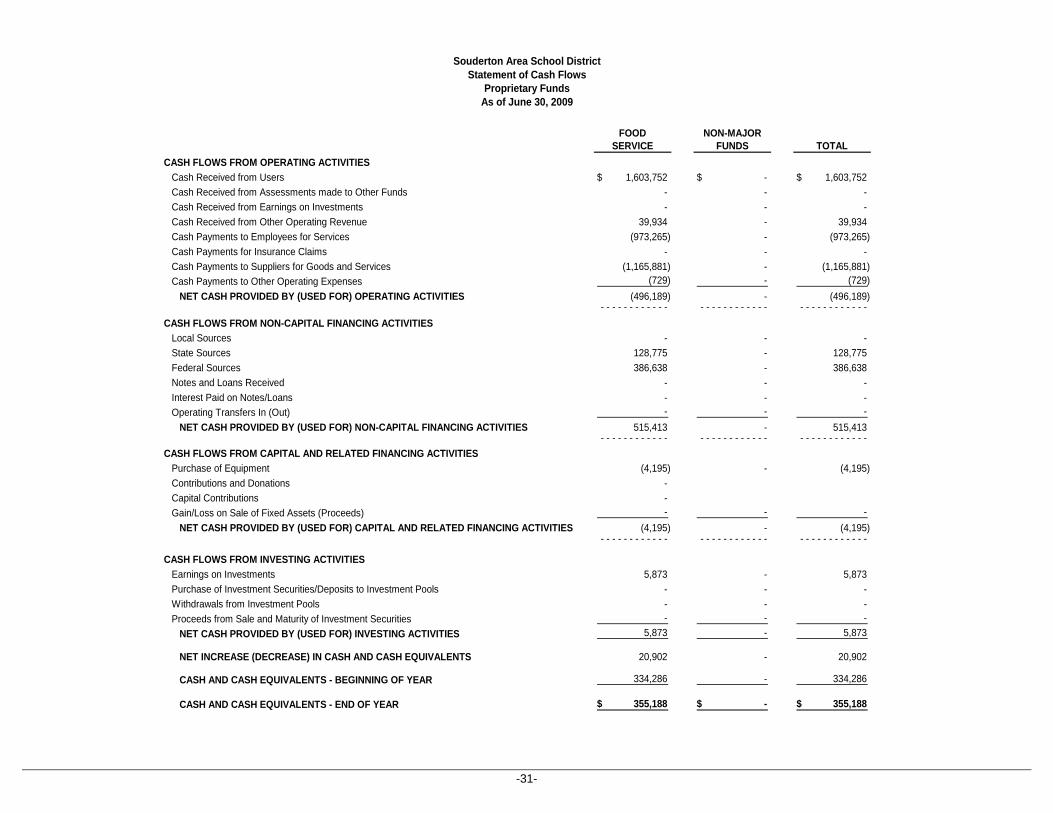

FOOD NON-MAJORSERVICE FUNDS TOTAL

CASH FLOWS FROM OPERATING ACTIVITIESCash Received from Users 1,603,752$ -$ 1,603,752$ Cash Received from Assessments made to Other Funds - - - Cash Received from Earnings on Investments - - - Cash Received from Other Operating Revenue 39,934 - 39,934 Cash Payments to Employees for Services (973,265) - (973,265) Cash Payments for Insurance Claims - - - Cash Payments to Suppliers for Goods and Services (1,165,881) - (1,165,881) Cash Payments to Other Operating Expenses (729) - (729)

NET CASH PROVIDED BY (USED FOR) OPERATING ACTIVITIES (496,189) - (496,189) - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CASH FLOWS FROM NON-CAPITAL FINANCING ACTIVITIESLocal Sources - - - State Sources 128,775 - 128,775 Federal Sources 386,638 - 386,638 Notes and Loans Received - - - Interest Paid on Notes/Loans - - - Operating Transfers In (Out) - - -

NET CASH PROVIDED BY (USED FOR) NON-CAPITAL FINANCING ACTIVITIES 515,413 - 515,413 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIESPurchase of Equipment (4,195) - (4,195) Contributions and Donations - Capital Contributions - Gain/Loss on Sale of Fixed Assets (Proceeds) - - -

NET CASH PROVIDED BY (USED FOR) CAPITAL AND RELATED FINANCING ACTIVITIES (4,195) - (4,195) - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CASH FLOWS FROM INVESTING ACTIVITIESEarnings on Investments 5,873 - 5,873 Purchase of Investment Securities/Deposits to Investment Pools - - - Withdrawals from Investment Pools - - - Proceeds from Sale and Maturity of Investment Securities - - -

NET CASH PROVIDED BY (USED FOR) INVESTING ACTIVITIES 5,873 - 5,873

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 20,902 - 20,902

CASH AND CASH EQUIVALENTS - BEGINNING OF YEAR 334,286 - 334,286

CASH AND CASH EQUIVALENTS - END OF YEAR 355,188$ -$ 355,188$

Souderton Area School DistrictStatement of Cash Flows

Proprietary FundsAs of June 30, 2009

-32-

RECONCILIATION OF OPERATING INCOME TO NET CASH PROVIDED BY (USED FOR) OPERATING ACTIVITIES

FOOD NON-MAJORSERVICE FUNDS TOTAL

OPERATING INCOME (LOSS) (661,198)$ -$ (661,198) - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

ADJUSTMENTS TO RECONCILE OPERATING INCOME (LOSS) TO NET CASHPROVIDED BY (USED FOR) OPERATING ACTIVITIES

Depreciation and Net Amortization 76,906 - 76,906 Provision for Uncollectible Accounts - - - Donated Commodities Used 116,862 - 116,862

CHANGE IN ASSETS AND LIABILITIES:(Increase) Decrease in Accounts Receivable (354) - (354) (Increase) Decrease in Advances from Other Funds 8,594 - 8,594 (Increase) Decrease in Inventories (3,495) - (3,495) (Increase) Decrease in Prepaid Expenses - - - (Increase) Decrease in Other Current Assets - - - Increase (Decrease) in Accounts Payable (1,676) - (1,676) Increase (Decrease) in Accrued Salaries and Benefits (32,535) - (32,535) Increase (Decrease) in Advances to Other Funds 867 - 867 Increase (Decrease) in Net OPEB Obligation 90 - 90 Increase (Decrease) in Other Current Liabilities (250) - (250)

TOTAL ADJUSTMENTS 165,009 - 165,009

NET CASH PROVIDED BY (USED FOR) OPERATING ACTIVITIES (496,189)$ -$ (496,189)$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Cash Flows

Proprietary FundsAs of June 30, 2009

-33-

PENSION AND

PRIVATE OTHER EMPLOYEEPURPOSE BENEFIT AGENCY

TRUST TRUST FUNDSASSETS

Cash and cash equivalents -$ -$ 151,130$ Investments - - 135,000 Due from Other Funds - - - Other Receivables - - - Prepaid Expenses - - - Other Current Assets - - -

TOTAL ASSETS -$ -$ 286,130$

LIABILITIESAccounts Payable -$ -$ -$ Due to Other Funds - - - Due to Student Clubs - - 286,130 Other Current Liabilities - - -

TOTAL LIABILITIES - - 286,130

NET ASSETSRestricted - - - Unrestricted - - -

TOTAL NET ASSETS -$ -$ -$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Net Assets

Fiduciary FundsAs of June 30, 2009

-34-

PENSION ANDOTHER EMPLOYEE

PRIVATE-PURPOSE BENEFITTRUST FUND TRUST FUNDS

ADDITIONSContributions -$ -$ Transfers from other funds - - INVESTMENT EARNINGS: Interest and Dividends - - Net increase (decrease) in fair value of investments - - Less investment expense - -

TOTAL ADDITIONS - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

DEDUCTIONSTransfers to other funds - - Administrative charges - - Scholarships - -

TOTAL DEDUCTIONS - -

CHANGE IN NET ASSETS - -

NET ASSETS - BEGINNING OF YEAR - -

NET ASSETS - END OF YEAR -$ -$

The Accompanying Notes are an integral part of these financial statements.

Souderton Area School DistrictStatement of Changes in Net Assets

Fiduciary FundsFor the Year Ended June 30, 2009

-35-

VARIANCE WITH FINAL BUDGET BUDGET TO ACTUAL

ACTUAL POSITIVE GAAP AMOUNTSORIGINAL FINAL (BUDGETARY BASIS) (NEGATIVE) DIFFERENCE GAAP BASIS

REVENUES Local Sources 73,809,047$ 73,809,047$ 74,522,696$ 713,649$ -$ 74,522,696$ State Sources 20,400,337 20,400,337 20,681,819 281,482 - 20,681,819 Federal Sources 855,029 855,029 1,018,788 163,759 - 1,018,788

TOTAL REVENUES 95,064,413 95,064,413 96,223,303 1,158,890 - 96,223,303 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

EXPENDITURES Regular Instruction 40,127,777 39,216,652 39,214,226 2,426 - 39,214,226 Special Programs 12,389,400 12,748,884 12,740,292 8,592 - 12,740,292 Vocational Programs 1,771,442 1,771,442 1,771,442 - - 1,771,442 Other Instructional Programs 444,071 418,071 413,595 4,476 - 413,595 Adult Education Programs 201,563 187,563 183,090 4,473 - 183,090 Community/Junior College Ed. Programs - - - - - - Pupil Personnel Services 2,894,057 2,809,057 2,799,400 9,657 - 2,799,400 Instructional Staff Services 3,121,735 2,756,041 2,743,743 12,298 - 2,743,743 Administrative Services 4,677,645 4,687,748 4,670,943 16,805 - 4,670,943 Pupil Health 811,990 793,990 790,433 3,557 - 790,433 Business Services 690,841 649,841 648,030 1,811 - 648,030 Operation & Maintenance of Plant Services 8,015,162 7,366,162 7,363,883 2,279 - 7,363,883 Student Transportation Services 6,735,918 7,403,918 7,401,220 2,698 - 7,401,220 Central Support Services 1,431,200 1,555,900 1,536,286 19,614 - 1,536,286 Other Support Services 76,327 76,327 73,853 2,474 - 73,853 Student Activities 1,151,541 113,541 100,667 12,874 - 100,667 Community Services 479,175 479,175 477,771 1,404 - 477,771 Facilities, Acquisition and Construction - - - - - - Debt Service 10,866,028 12,851,560 13,762,281 (910,721) - 13,762,281

TOTAL EXPENDITURES 95,885,872 95,885,872 96,691,155 (805,283) - 96,691,155 Excess (deficiency) of revenues over expenditures (821,459) (821,459) (467,852) 353,607 - (467,852)

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -OTHER FINANCING SOURCES (USES)

Proceeds From Extended Term Financing - - - - - - Interfund Transfers In - - - - - - Sale/Compensation for Fixed Assets - - 75 75 - 75 Fund Transfers Out - - (982,626) (982,626) - (982,626) Budgetary Reserve - - - - - -

TOTAL OTHER FINANCING SOURCES (USES) - - (982,551) (982,551) - (982,551) Special Items - - - - - - Extraordinary Items - - - - - -

NET CHANGE IN FUND BALANCES (821,459) (821,459) (1,450,403) (628,944) - (1,450,403)

FUND BALANCE - JULY 1, 2008 11,161,698 11,161,698 12,442,461 1,280,763 - 12,442,461

FUND BALANCE - JUNE 30, 2009 10,340,239$ 10,340,239$ 10,992,058$ 651,819$ -$ 10,992,058$

The Accompanying Notes are an integral part of these financial statements.

BUDGET AMOUNTS

Souderton Area School DistrictStatement of Revenues, Expenditures, and Changes in Fund Balance - Budget and Actual -

General FundFor the Year Ended June 30, 2009

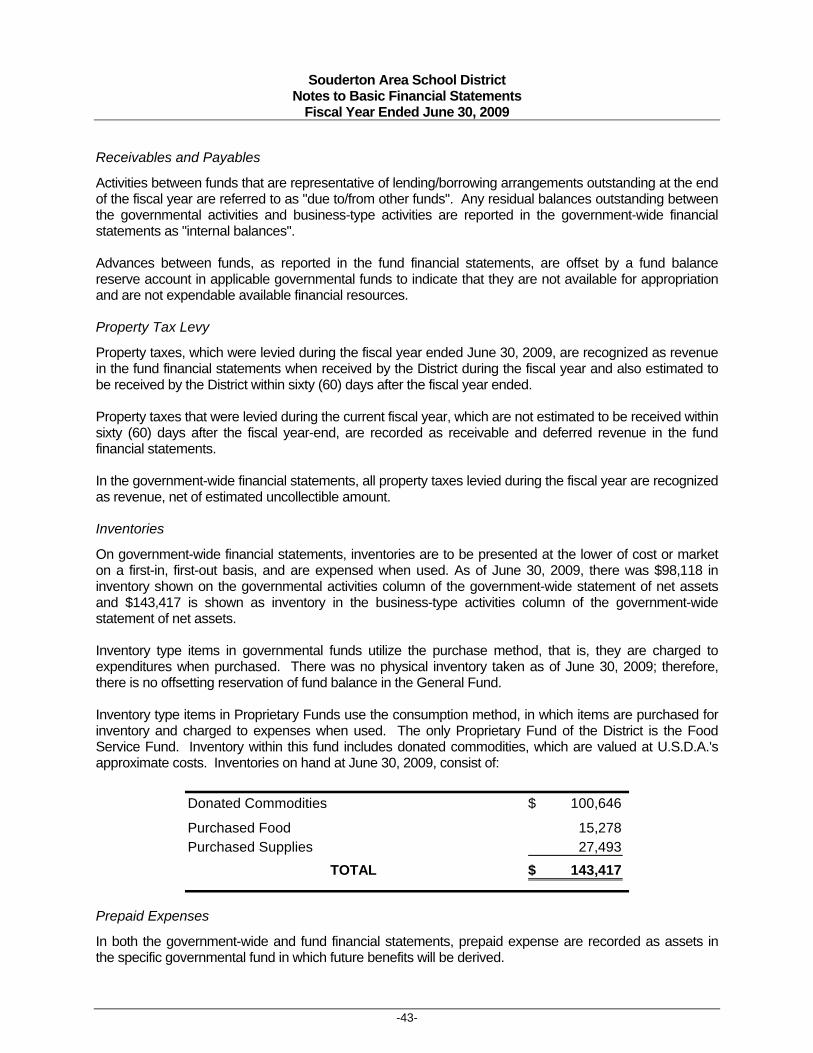

Souderton Area School District Notes to Basic Financial Statements

Fiscal Year Ended June 30, 2009

-36-

Note 1 - Description of the School District and Reporting Entity

School District

The Souderton Area School district (SASD) includes an area of 49 square miles in Upper Montgomery County. It is the largest school district in square miles, in the County. The district is situated midway between the cities of Allentown and Philadelphia. Due to its locale the district has the best of both worlds: proximity to the city, while in a semi-rural setting. Six municipalities are within the boundaries of the SASD: the two boroughs of Souderton and Telford and the four townships of Franconia, Lower Salford, Upper Salford and Salford.

Souderton Area is a growing community with farmlands becoming home sites at a steady pace. To meet the needs of this growing community, the school district closely monitors student population. Vernfield Elementary, the district’s seventh elementary school, opened in September 2003. The opening of Vernfield answered SASD’s elementary space concerns. However, at the secondary level crowded conditions have resulted in modular classroom additions at the high school, Indian Crest Junior High, and Indian Valley Middle School. Subsequent to year end, a new high school opened in September 2009.

The Souderton Area School District is a unit established, organized and empowered by the Commonwealth of Pennsylvania for the express purpose of carrying out, on the local level, the Commonwealth's obligation to public education, as established by the constitution of the Commonwealth and by the School Law Code of the same (Article II; Act 150, July 8, 1968).

As specified under the School Law Code of the Commonwealth of Pennsylvania, this and all other school districts of the state "shall be and hereby are vested as, bodies corporate, with all necessary powers to carry out the provisions of this act." (Article II, Section 211).

Board of School Directors

The public school system of the Commonwealth shall be administered by a board of school directors, to be elected or appointed, as hereinafter provided. At each election of school directors, each qualified voter shall be entitled to cast one vote for each school director to be elected.

The Souderton Area School District is governed by a board of nine School Directors who are residents of the School District and who are elected every two years, on a staggered basis, for a four-year term.

The Board of School Directors has the power and duty to establish, equip, furnish, and maintain a sufficient number of elementary, secondary, and other schools necessary to educate every person, residing in such district, between the ages of six and twenty-one years, who may attend.

In order to establish, enlarge, equip, furnish, operate, and maintain any schools herein provided, or to pay any school indebtedness which the school district is required to pay, or to pay any indebtedness that may at any time hereafter be created by the school district, the board of school directors are vested with all the necessary authority and power annually to levy and collect the necessary taxes required and granted by the legislature, in addition to the annual State appropriation, and are vested with all necessary power and authority to comply with and carry out any or all of the provisions of the Public School Code of 1949.

Souderton Area School District Notes to Basic Financial Statements

Fiscal Year Ended June 30, 2009

-37-

Administration

The Superintendent of Schools shall be the executive officer of the Board of School Directors and, in that capacity shall administer the School District in conformity with Board policies and the School Laws of Pennsylvania. The Superintendent shall be directly responsible to, and therefore appointed by, the Board of School Directors. The Superintendent shall be responsible for the overall administration, supervision, and operation of the School District.