Report - Department of Infrastructure, Regional … · Web viewIBISWorld Industry Report G3911....

113

Impact analysis of potential changes to the current restrictions on the importation of used motor vehicles into Australia Dealer Group Against Used

Transcript of Report - Department of Infrastructure, Regional … · Web viewIBISWorld Industry Report G3911....

Impact analysis ofpotential changes to the current restrictions on the importation of used motor vehicles into Australia

Dealer Group Against UsedCar Imports

9 September 2014

ContentsExecutive Summary....................................................................................................................i

2 Introduction ....................................................................................................................62.1 Background ...................................................................................................................... 62.2 Structure of report............................................................................................................ 7

3 Market analysis ...............................................................................................................93.1 Overview .......................................................................................................................... 93.2 Market segmentation ....................................................................................................... 93.3 Demand.......................................................................................................................... 143.4 Supply ............................................................................................................................ 163.5 Competition in the retail car market ............................................................................... 193.6 Information and regulation ............................................................................................. 203.7 Key trends in the retail car market .................................................................................. 22

4 Policy driver and regulatory analysis..............................................................................314.1 Legal and regulatory framework...................................................................................... 314.2 Past policy rationale for restricting large scale imports .................................................... 344.3 Current policy rationale for removing import restrictions ................................................ 35

5 Pot5.1

ential impacts to the retail car market......................................................................37New Zealand experience ................................................................................................. 37

5.2 Source markets............................................................................................................... 405.3 International comparison................................................................................................ 425.4 Direct effects .................................................................................................................. 455.5 Implications for the Australian market ............................................................................ 47

Conclusions.............................................................................................................................52

Appendix A – Further charts ....................................................................................................54Limitation of our work ............................................................................................................... 57

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its networ k of member firms, each of which is a legally separate and independent entity. Please see w ww . d e l o i t te . c o m / a u / a b o u t for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Liability limited by a scheme approved under Professional Standards Legislation.

© 2014 Deloitte Touche Tohmatsu

Executive Summary

This report has been commissioned by the Dealer Group Against Used Car Imports (DGAUCI) to inform an industry response to suggested changes to existing legislation regulating the large-scale importation of used cars into Australia.

The report analyses potential impacts of removing used car import restrictions on the retail car market. The impetus for this report stems from industry concerns with suggested changes to allow the large-scale importation of used vehicles into Australia presented in a Productivity Commission Review into Australia’s automotive manufacturing industry and the complexities associated with such a change.Currently, the DGAUCI is preparing a response to Motor Vehicle Standards Act (MVSA) review with the aim to inform the review of the complexities of removing used car import restrictions. The NMBDA has engaged Deloitte on behalf of the DGAUCI to prepare a report on the potential impacts of removing used car import restrictions on the Australian retail car market. The analysis in this report was commissioned to help inform the DGAUCI’s response to MVSA review.

This report provides an overview of the Australian retail new car market and an analysis into the potential impacts of regulatory change on the retail car market in Australia.

Market Overview

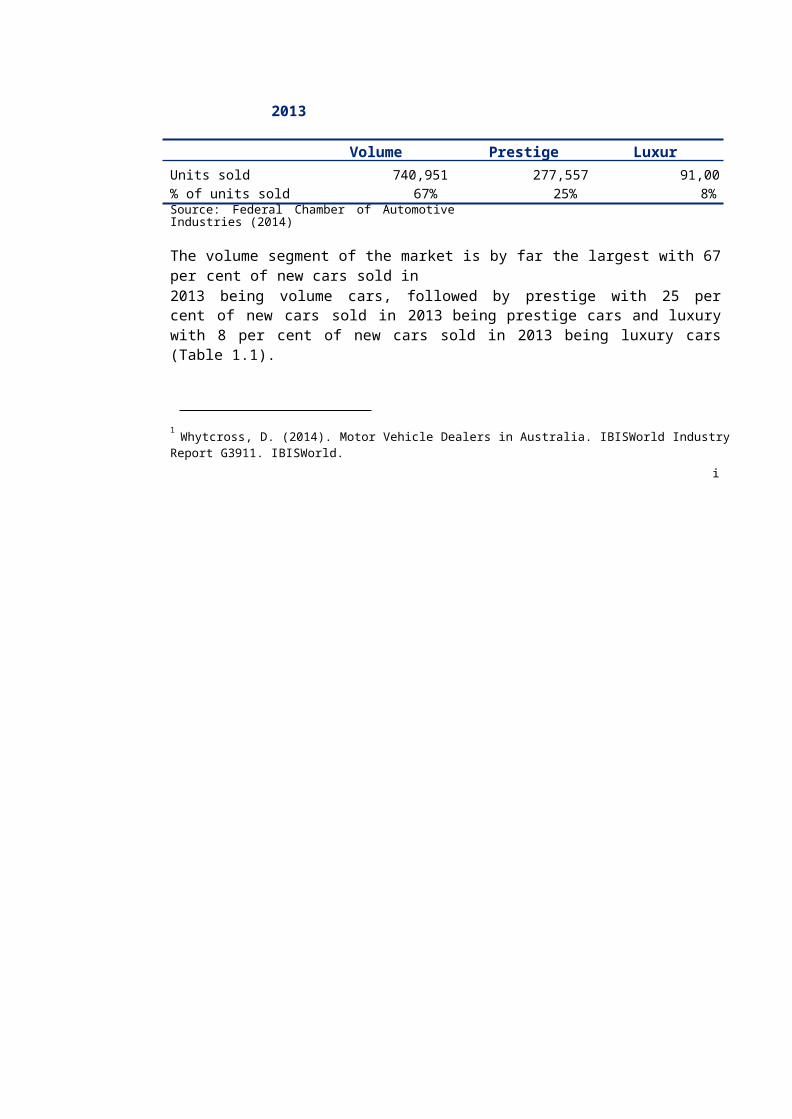

The Australian retail car market is a $74.0 billion industry which employs over 66,000 people, sells in excess of one million new cars each year and adds nearly $6.4 billion to the Australian economy1. The retail car market in Australia is highly competitive with many buyers and many sellers actively participating in the market. There are over 4,700 car dealers in the Australian market dealing in over 60 different marques. Competition primarily takes place in three market segments: the volume segment, the prestige segment and the luxury segment.

Table 1.1: Market segmentation in new car market, 2013

Volume Prestige LuxuryUnits sold 740,951 277,557 91,006% of units sold 67% 25% 8%Source: Federal Chamber of Automotive Industries (2014)

The volume segment of the market is by far the largest with 67 per cent of new cars sold in2013 being volume cars, followed by prestige with 25 per cent of new cars sold in 2013 being prestige cars and luxury with 8 per cent of new cars sold in 2013 being luxury cars (Table 1.1).

1 Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.i

ii

Mot

or V

ehic

le C

PI

When put in an international context, Australia’s high level of competition in the retail car market becomes more apparent. The number of brands and market share of each of these brands of car are good indicators of the level of competition in a market. Table 1.2 presents a comparison of these indicators in Australia, Canada, the UK and the USA – Australia has both a higher number of brands (67) and a lower market size per brand (16,597 unit sales per brand) than each of these other markets, both indicators suggesting that Australia is the most highly competitive.

Table 1.2: Competitiveness of global car markets, 2013

Australia Canada UK USANumber of brands in Australia 67 49 53 51Sales (car units) 1,112,032 1,620,221 2,249,483 13,040,632Market size per brand (car units) 16,597 33,066 42,443 255,699Source: Department of Industry, Innovation, Climate Change, Science, Research and Tertiary Education (2013),March 2013 Automotive update

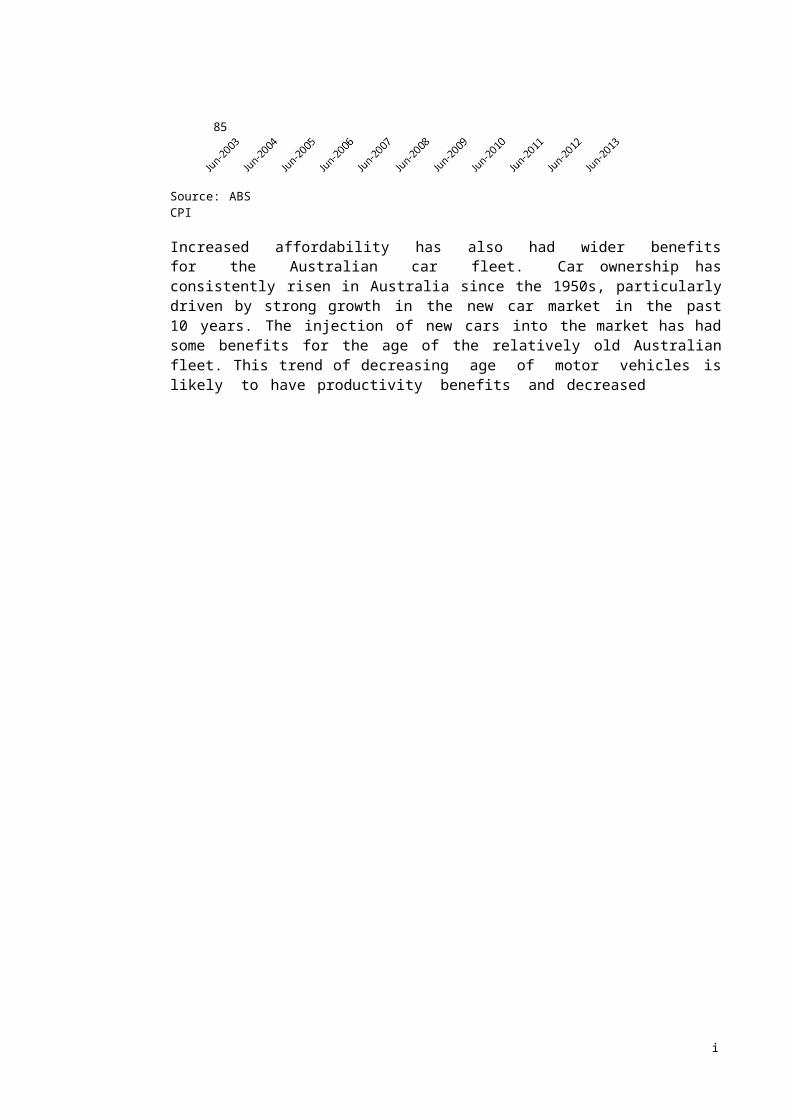

The competitiveness of the Australian retail car market has brought about many positive outcomes for consumers in the past decade. Australia has experienced a significant increase in the affordability of cars over the past decade. There are a range of factors behind this increase including a rising Australian dollar reducing the costs of imported vehicles, increased competition in the local retail car market pushing down prices and a steady increase in the disposable income of the average Australian. Chart 1.1 below shows the decrease in motor vehicle prices as measured by the motor vehicle consumer price index.

Chart 1.1: Decrease in motor vehicle prices, 2003-2013

115

110

105

100

95

90

85

Source: ABS CPI

Increased affordability has also had wider benefits for the Australian car fleet. Car ownership has consistently risen in Australia since the 1950s, particularly driven by strong growth in the new car market in the past 10 years. The injection of new cars into the market has had some benefits for the age of the relatively old Australian fleet. This trend of decreasing age of motor vehicles is likely to have productivity benefits and decreased

iii

Aver

age

age

of c

ars i

n fle

et

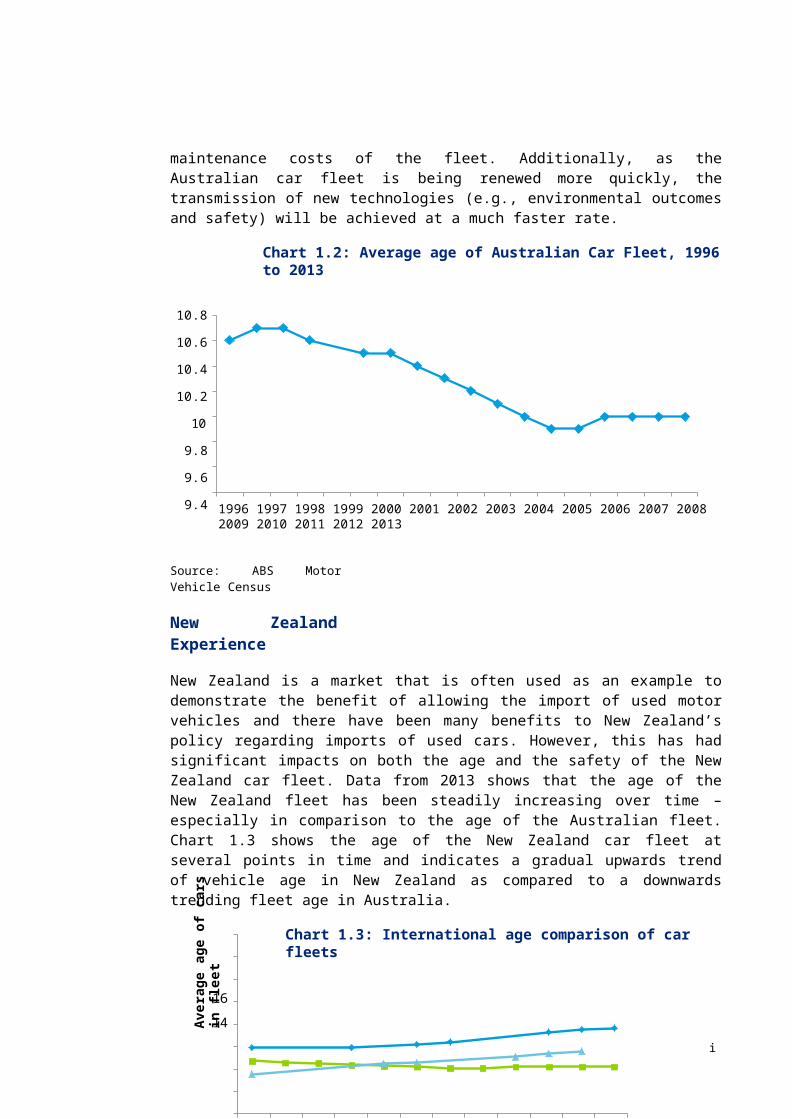

maintenance costs of the fleet. Additionally, as the Australian car fleet is being renewed more quickly, the transmission of new technologies (e.g., environmental outcomes and safety) will be achieved at a much faster rate.

Chart 1.2: Average age of Australian Car Fleet, 1996 to 2013

10.8

10.6

10.4

10.2

10

9.8

9.6

9.41996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: ABS Motor Vehicle Census

New Zealand Experience

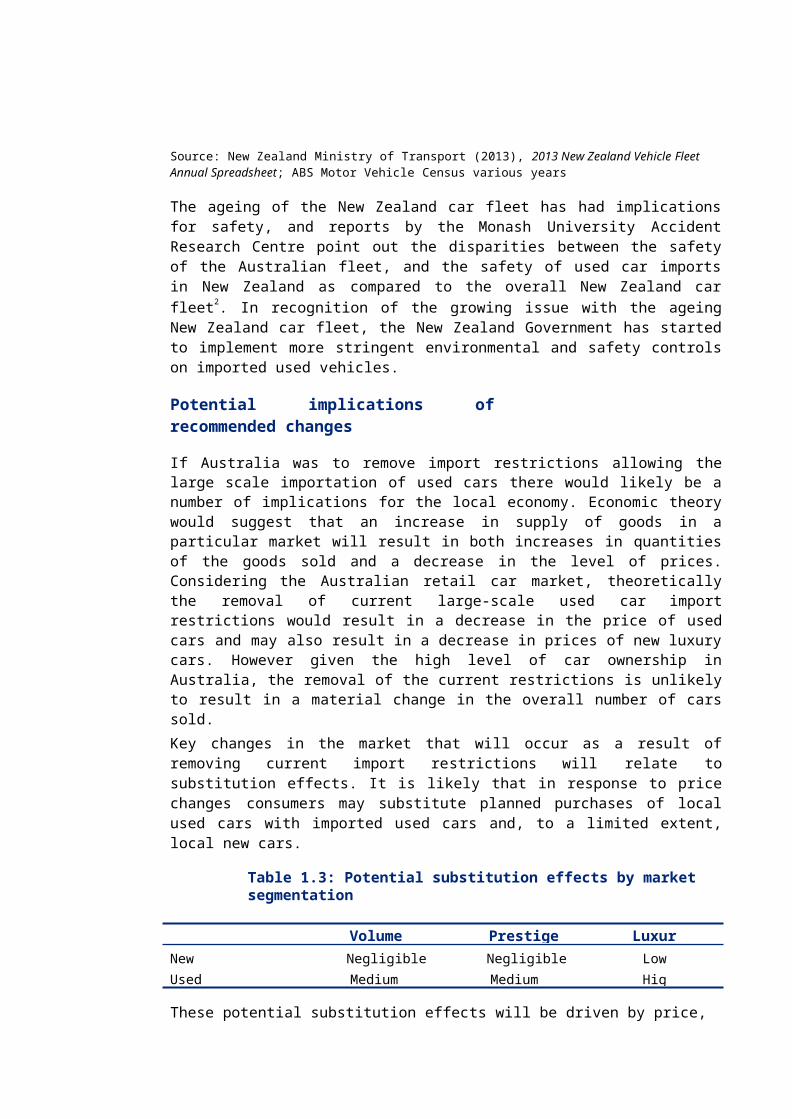

New Zealand is a market that is often used as an example to demonstrate the benefit of allowing the import of used motor vehicles and there have been many benefits to New Zealand’s policy regarding imports of used cars. However, this has had significant impacts on both the age and the safety of the New Zealand car fleet. Data from 2013 shows that the age of the New Zealand fleet has been steadily increasing over time – especially in comparison to the age of the Australian fleet. Chart 1.3 shows the age of the New Zealand car fleet at several points in time and indicates a gradual upwards trend of vehicle age in New Zealand as compared to a downwards trending fleet age in Australia.

Chart 1.3: International age comparison of car fleets

16

14

12

10

8

6

4

2

02002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

New Zealand Australia USA

Source: New Zealand Ministry of Transport (2013), 2013 New Zealand Vehicle Fleet Annual Spreadsheet; ABS Motor Vehicle Census various years

The ageing of the New Zealand car fleet has had implications for safety, and reports by the Monash University Accident Research Centre point out the disparities between the safety of the Australian fleet, and the safety of used car imports in New Zealand as compared to the overall New Zealand car fleet2. In recognition of the growing issue with the ageing New Zealand car fleet, the New Zealand Government has started to implement more stringent environmental and safety controls on imported used vehicles.

Potential implications of recommended changes

If Australia was to remove import restrictions allowing the large scale importation of used cars there would likely be a number of implications for the local economy. Economic theory would suggest that an increase in supply of goods in a particular market will result in both increases in quantities of the goods sold and a decrease in the level of prices. Considering the Australian retail car market, theoretically the removal of current large-scale used car import restrictions would result in a decrease in the price of used cars and may also result in a decrease in prices of new luxury cars. However given the high level of car ownership in Australia, the removal of the current restrictions is unlikely to result in a material change in the overall number of cars sold.Key changes in the market that will occur as a result of removing current import restrictions will relate to substitution effects. It is likely that in response to price changes consumers may substitute planned purchases of local used cars with imported used cars and, to a limited extent, local new cars.

Table 1.3: Potential substitution effects by market segmentation

Volume Prestige LuxuryNewUsed

NegligibleMedium

NegligibleMedium

LowHigh

These potential substitution effects will be driven by price, which will depend largely on: The implementation design of the suggested changes to current import restrictions The volume of available vehicles from source markets The new car price differential between Australia and other markets.

The substitution effects will likely have wide reaching implications for the retail car market. It is expected that: In the short run, the suggested changes will have disruptive effects for car dealerships;

however, in the long run, dealerships will likely adjust to the new status quo

2 Newstead, S., Watson, L. and Cameron, M. (2013). Vehicle safety ratings estimated from police reported crash data: 2013 update: Australian and New Zealand crashes during 1987-2011; Newstead, S., Watson, L. and Cameron, M. (2012). Trends in crashworthiness of the New Zealand vehicle fleet by year of manufacture: 1964 to 2010: supplement to Report 313: Vehicle safety ratings estimated from police reported crash data: 2012

update.

Industry Consumers

New car salesNear-new luxury car prices overseas are lower than comparable Australian cars. It is possible that there will be some substitution between new and used luxury cars in Australia; however, this is a small part of the market.Value of existing new stock will decrease as resale value of used cars decreases.Used car salesDealer network will require time to adapt to new sources of supply and adjust pricesPrice of existing used car stock will decrease, devaluing existing stockRecall managementDealers and manufacturers face brand risk if a robust recall management system is not in place for imported used cars.

BenefitsPrice of used cars will likely decrease and there may be an increase in the number of models and variants available.CostsLikely to be higher operating costs associated with imported used cars. Australian dealers have noted that this will be due to higher parts and servicing costs and higher insurance.The value of existing cars held by consumers will fall.Information asymmetriesInformation asymmetry may lead to consumers not making the best choice they can.Cognitive biasesConsumers, when facing complex decisions, make mental shortcuts and may base their decision on factors that they easily relate to. These could include factors such as make of car, or how expensive the same model is in Australia. If the specification is different this may not be the best choice for the consumer.

Consumers will gain some benefit from reduced prices of used cars, however, the extent of these decreases is unclear. Additionally, consumers may face information asymmetries and cognitive bias issues.

Government will need to consider consumer protection issues, policy issues and the fiscal costs of such a policy.

These implications are described in further detail in Table 1.4 below.

Table 1.4 Potential implications of removing large scale import restrictions of used cars

Government

Consumer protection issuesThe recall system needs to be able to cope with an increased number of used imports. Additionally, Government may need to assess the adequacy of the current policy framework to deal with issues such as potential odometer fraud.Policy issuesFleet safety improvement – allowing large scale importation of used cars could increase the age of the fleet and slow the spread of safety technologies.Environmental protection – likely to be an increase in scrapped cars and possibility of imported cars not meeting emissions standardsImplementation, compliance and enforcement of new regulation may be difficult and costly for government.Fiscal costsThere may also be implications for luxury car tax and stamp duty revenues depending on the extent to which the policy change results in a decrease in car prices and the volume of new luxury cars sold.

2 IntroductionThis chapter provides background for the report and sets out the structure for the remainder of the report.

2.1 BackgroundThis report has been commissioned by the Dealer Group Against Used Car Imports (DGAUCI) to inform an industry response to suggested changes to existing legislation regulating the large-scale importation of used cars into Australia. The report analyses potential impacts of removing used car import restrictions on the retail car market. The impetus for this report stems from industry concerns with suggested changes to allow the large-scale importation of used vehicles into Australia presented in a Productivity Commission Review into Australia’s automotive manufacturing industry and the complexities associated with such a change.

Productivity commission review

In October 2013, the Minister for Industry tasked the Productivity Commission (PC) to conduct a review into government support for Australia’s automotive manufacturing industry. The broader focus of the review was on the sustainability of Australia’s automotive manufacturing industry, however, the PC also considered Australia’s current policy regarding the importation of used motor vehicles. The review has now been completed and the PC has publicly released both a preliminary findings report and a positions paper.

In the position paper released in January 2014, the PC came to a draft finding regardingAustralia’s used car import policy:

Draft Finding 3.2

The policy rationale for prohibiting the large-scale importation of second-hand vehicles into Australia is weak. However, appropriate regulatory measures are required to ensure that consumer protection, community safety, and environmental performance standards are maintained before the restrictions are removed. These concerns are best dealt with directly, through regulatory standards applicable to all vehicles sold in Australia.

The $12 000 specific duty on imported second-hand vehicles appears to be largely redundant, providing a prima facie case for its removal.

Following the completion of our report, the PC has since released their final review report. The core finding recommending the removal of large scale used car import restrictions was reiterated in the final inquiry report in Recommendation 5.4, though the PC’s stance on this appeared to have weakened. It is important to note that though the analysis of our report was carried out in reference to the position paper, our conclusions are not changed regarding the potential impacts of removing used car import restrictions in Australia.

7

2014 review of the Motor Vehicle Standards Act 1989

In January 2014, the Assistant Minister for Infrastructure and Regional Development approved the commencement of a comprehensive review of the Motor Vehicle Standards Act 1989 (MVSA) with a specific focus to: Reduce the regulatory burden on business Improve the safety provisions of the legislation Improve the environmental provisions of the legislation Improve the anti-theft provisions of the legislation.The review is tasked with identifying options for addressing the above concerns, which will be formally assessed in a Regulatory Impact Statement (RIS). Our understanding is that if the Government were looking to remove restrictions on large-scale importation of used vehicles, that this would be considered as part of the review of the MVSA.

Dealer Group Against Used Car ImportsThe Dealer Group Against Used Car Imports (DGAUCI) is an association of retail car dealer associations in Australia who oppose the import of used cars into Australia. The group is formed by six national car dealership groups: National Mercedes-Benz Dealers Association BMW National Dealer Council Nissan National Dealer Council Mazda Dealer Association of NSW Hyundai National Dealer Council.

Currently, the DGAUCI is preparing a response to MVSA review with the aim to inform the review of the complexities of removing used car import restrictions. The NMBDA has engaged Deloitte on behalf of the DGAUCI to prepare a report on the potential impacts of removing used car import restrictions on the Australian retail car market. The analysis in this report was commissioned to help inform the DGAUCI’s response to MVSA review.

2.2 Structure of reportThis report provides an overview of the Australian retail new car market and an analysis of the potential impacts of regulatory change on the retail car market in Australia. The report is structured as follows: Chapter 3 summarises the Australian retail car market and includes detailed

descriptions of market segmentation, key market participants, the dealership business model, and key market trends.

Chapter 4 describes the regulatory and legislative framework governing the retail car market, and analyses the policy rationale behind historical regulation of used imports and the current policy rationale for the suggested removal of used car import restrictions.

8

• Chapter 5 is a detailed analysis of the potential implications of removing used car import restrictions on the retail car market.

9

3 Market analysisThis chapter provides an analysis of the retail car market and discusses past, current and future trends.

3.1 OverviewThe Australian retail car market is a $74.0 billion industry which employs over 66,000 people, sells in excess of one million new cars each year and adds nearly $6.4 billion to the Australian economy3. The retail car market can be defined as the market in which the buying and selling of new and used motor vehicles between retail dealerships and consumers, companies and government entities takes place. Products sold in the market are slightly differentiated with different market segments focused on selling volume (low end), prestige (middle range) and luxury (high end) cars. With many buyers and sellers in the market, recent years have seen high levels of competition in the retail car market resulting in lower prices, higher vehicle specifications and diversification of the dealership business model. These features of the retail car market are described in further detail in the following sections. Although the retail car market also facilitates the trade for commercial vehicles, this report focuses on passenger vehicles.

3.2 Market segmentationThe retail market for cars in Australia can be broadly segmented into passenger vehicles and commercial vehicles. This report has a particular focus on passenger vehicles and as such, when looking at passenger vehicles, we apply a more granular lens of segmentation.

3.2.1 Passenger vehicles

The retail car market offers a broad range of passenger vehicles that vary significantly in price and in target market. As such, it is useful to break the market for passenger vehicles down into segments to allow a more detailed analysis. This segmentation groups each make of car into categories based on the marketing strategy of the manufacturer. The specific criteria used to segment brands are based on the manufacturer’s in-market positioning in regards to volume and unit gross margin. Under the Deloitte system of segmentation, each brand is classified as volume, prestige or luxury, where: Volume brands sell a high volume of cars at a low gross margin per unit. Prestige brands sell a medium volume of cars at a mid-range gross margin per unit Luxury brands sell a low volume of cars at a high gross margin per unit.

Deloitte’s Motor Industry Services Group maintains a market segmentation database with information on each of the relevant brands. As brands can adjust their in-market strategy and move between market segments, this segmentation is only approximate and based on

3 Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. I BISWorld.

10

currently available data. Table 3.1 shows a sample breakdown of our most recently available data.

Table 3.1: Market segmentation of brands, sample

Volume Prestige LuxuryFord Alfa Romeo AudiHolden Chrysler BMWHyundai Citroen JaguarKia Dodge Land RoverMitsubishi Fiat Mercedes-BenzNissan Honda VolvoSource: Deloitte Motor Industry Services data (2014)

3.2.2 Volume

Volume brands, in addition to the segmentation criteria, generally can be described as brands which are priced at a lower price range and occupy the majority of the market. Some notable volume brands operating in Australia include Toyota, Ford and Holden. In2013, in total there were 721,616 new volume brand vehicles sold, an increase of 4,888from 2012. Most of the gross profit of volume dealerships comes from new cars (28.8 per cent) and service (27.1 per cent). For a more detailed discussion of the dealership business model see subsection 3.4.1.

Table 3.2: Departmental contribution to gross profit, Volume (2012-13)

Department Contribution to gross profit (%)

New 28.8

Used 13.5

Parts 12.3

Service 27.1

Finance and insurance 18.3

Source: Deloitte Motor Industry Services data (2014)

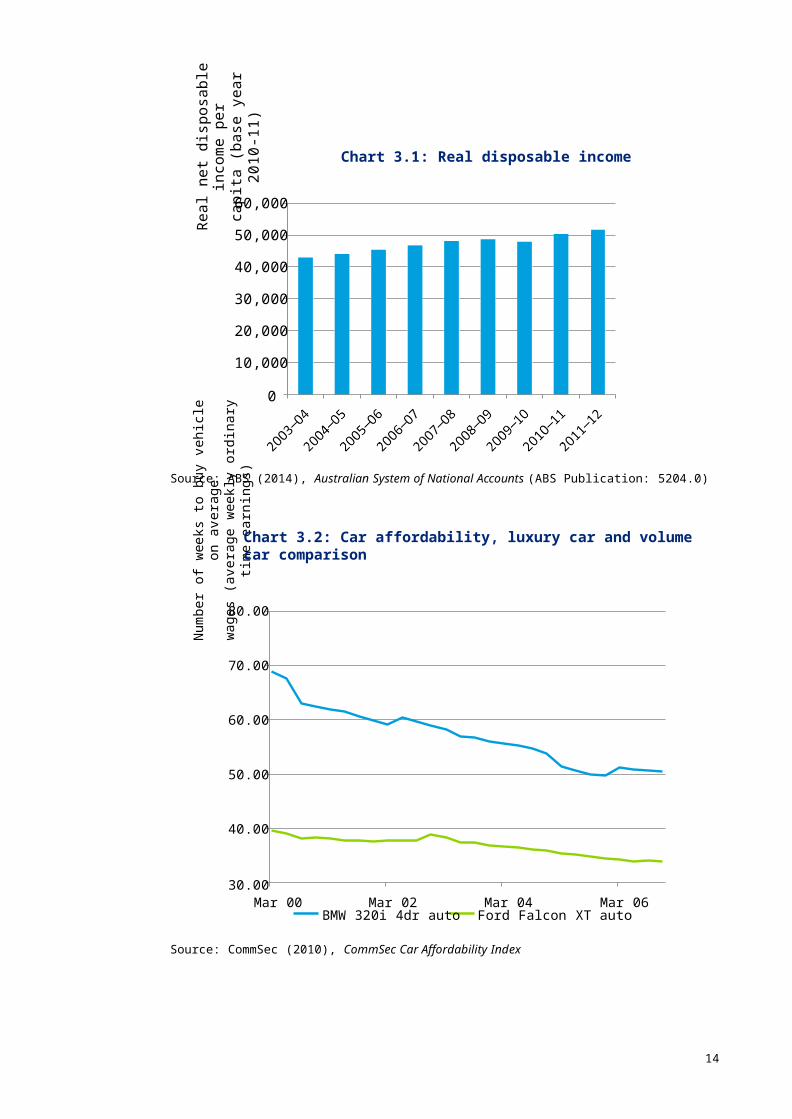

Over the past 10 years, there has been a decline in demand for Volume cars; this is likely a result of an increase in income per capita (see Chart 3.1) and a decrease in prices of prestige and luxury cars relative to volume cars (see Chart 3.2) leading to consumers being able to afford more expensive cars.

Num

ber o

f wee

ks to

buy

veh

icle

on

aver

age

wag

es (a

vera

ge w

eekl

y or

dina

ry ti

me

earn

ings

)Re

al n

et d

ispo

sabl

e in

com

e pe

rca

pita

(bas

e ye

ar 2

010-

11)

11

Chart 3.1: Real disposable income

60,000

50,000

40,000

30,000

20,000

10,000

0

Source: ABS (2014), Australian System of National Accounts (ABS Publication: 5204.0)

Chart 3.2: Car affordability, luxury car and volume car comparison

80.00

70.00

60.00

50.00

40.00

30.00Mar 00 Mar 02 Mar 04 Mar 06

BMW 320i 4dr auto Ford Falcon XT auto

Source: CommSec (2010), CommSec Car Affordability Index

12

3.2.3 Prestige

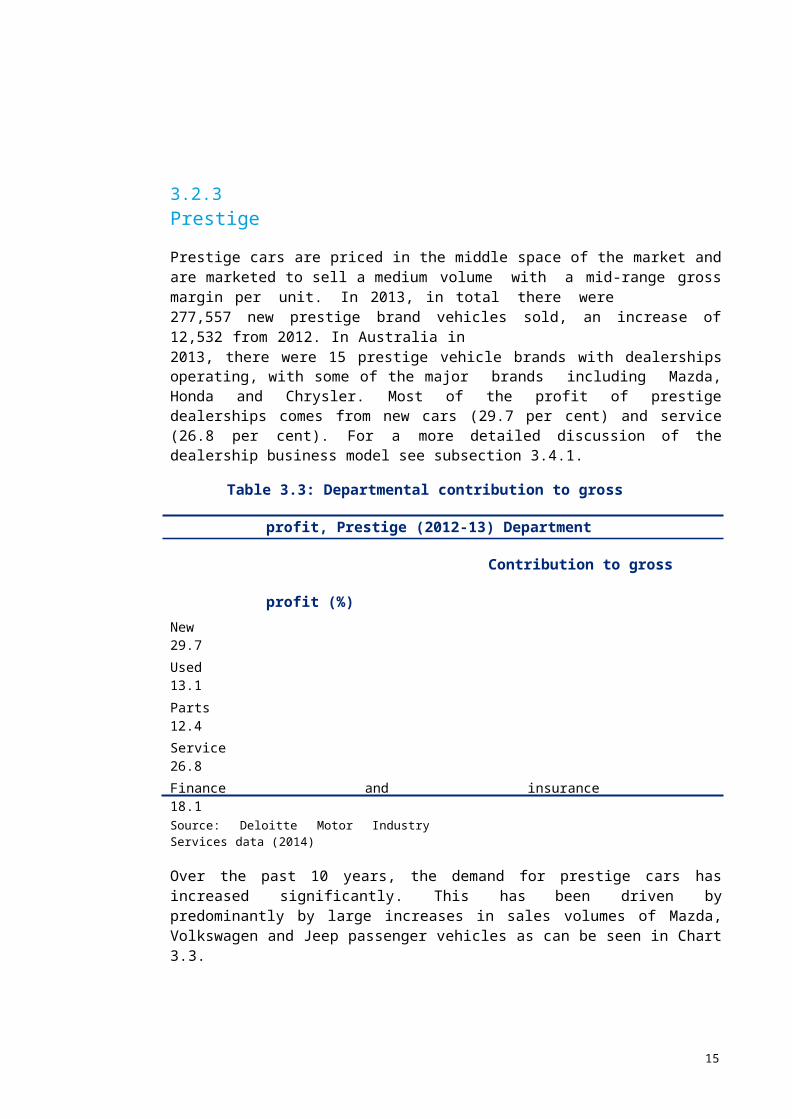

Prestige cars are priced in the middle space of the market and are marketed to sell a medium volume with a mid-range gross margin per unit. In 2013, in total there were277,557 new prestige brand vehicles sold, an increase of 12,532 from 2012. In Australia in2013, there were 15 prestige vehicle brands with dealerships operating, with some of the major brands including Mazda, Honda and Chrysler. Most of the profit of prestige dealerships comes from new cars (29.7 per cent) and service (26.8 per cent). For a more detailed discussion of the dealership business model see subsection 3.4.1.

Table 3.3: Departmental contribution to gross profit, Prestige (2012-13)

Department Contribution to gross profit (%)New 29.7Used 13.1Parts 12.4Service 26.8Finance and insurance 18.1Source: Deloitte Motor Industry Services data (2014)

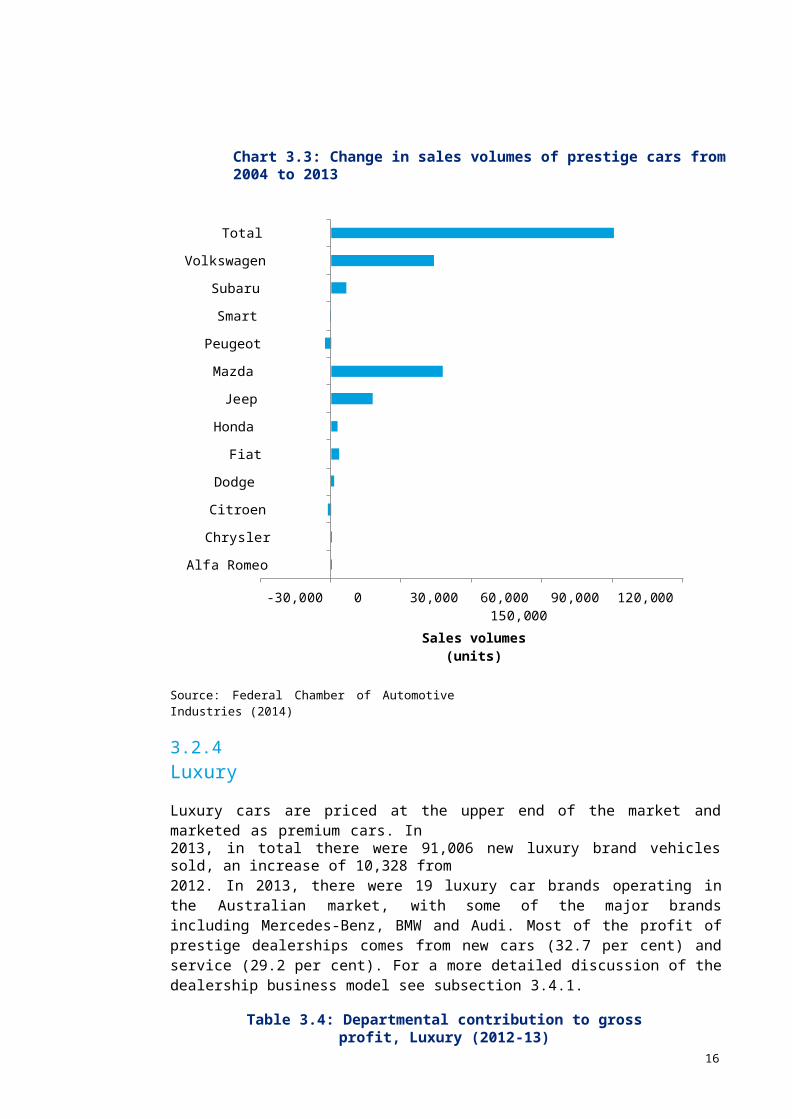

Over the past 10 years, the demand for prestige cars has increased significantly. This has been driven by predominantly by large increases in sales volumes of Mazda, Volkswagen and Jeep passenger vehicles as can be seen in Chart 3.3.

13

Chart 3.3: Change in sales volumes of prestige cars from 2004 to 2013

Total

Volkswagen

Subaru

Smart

Peugeot

Mazda

Jeep

Honda

Fiat

Dodge

Citroen

Chrysler

Alfa Romeo

-30,000 0 30,000 60,000 90,000 120,000 150,000Sales volumes (units)

Source: Federal Chamber of Automotive Industries (2014)

3.2.4 Luxury

Luxury cars are priced at the upper end of the market and marketed as premium cars. In2013, in total there were 91,006 new luxury brand vehicles sold, an increase of 10,328 from2012. In 2013, there were 19 luxury car brands operating in the Australian market, with some of the major brands including Mercedes-Benz, BMW and Audi. Most of the profit of prestige dealerships comes from new cars (32.7 per cent) and service (29.2 per cent). For a more detailed discussion of the dealership business model see subsection 3.4.1.

Table 3.4: Departmental contribution to gross profit, Luxury (2012-13)

Department Contribution to gross profit (%)New 32.7Used 10.1Parts 14.3Service 29.2F&I 13.7Source: Deloitte Motor Industry Services data (2014)

Sale

s vol

umes

(uni

ts)

14

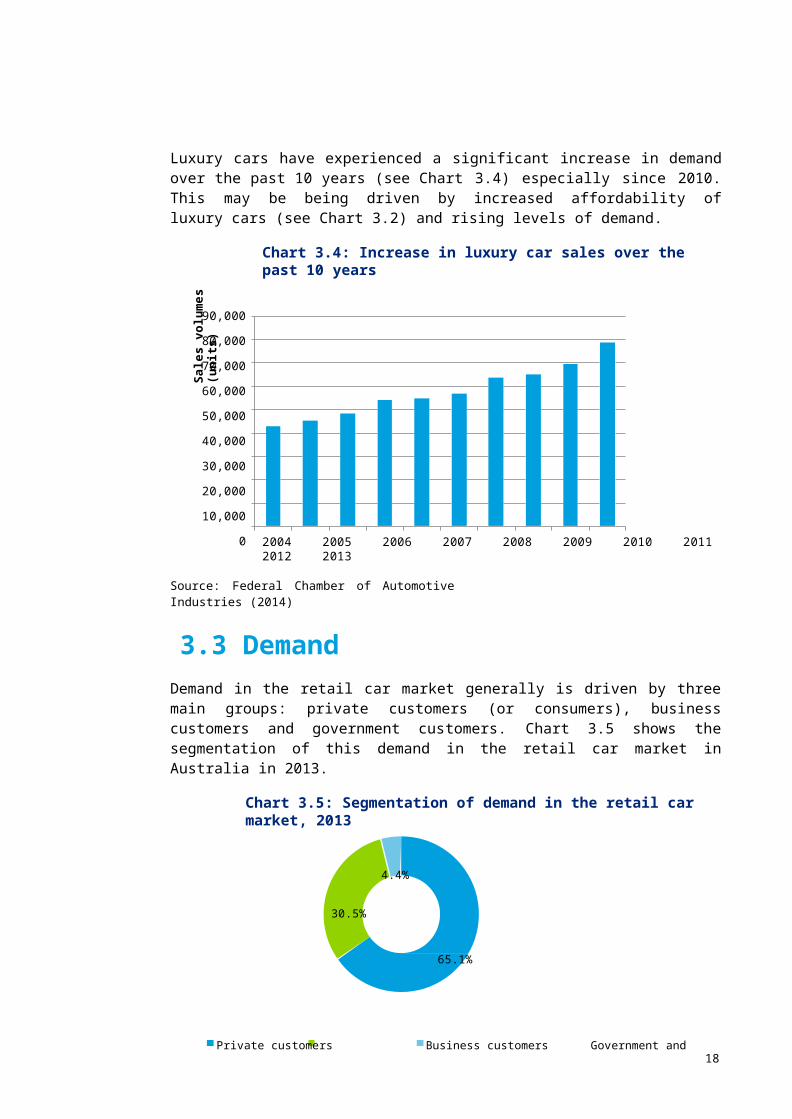

Luxury cars have experienced a significant increase in demand over the past 10 years (see Chart 3.4) especially since 2010. This may be being driven by increased affordability of luxury cars (see Chart 3.2) and rising levels of demand.

Chart 3.4: Increase in luxury car sales over the past 10 years

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

02004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: Federal Chamber of Automotive Industries (2014)

3.3 DemandDemand in the retail car market generally is driven by three main groups: private customers (or consumers), business customers and government customers. Chart 3.5 shows the segmentation of this demand in the retail car market in Australia in 2013.

Chart 3.5: Segmentation of demand in the retail car market, 2013

4.4%

30.5%

65.1%

Private customers Business customers Government and other customers

Source: Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.

6 Ibid.

15

3.3.2 Buyers

Private customers

Private customer spending accounts for more than 65 per cent of revenue in the retail car market4. Generally speaking, the core reason private customers purchase cars is to satisfy a transport need, however, the decision to buy a specific car is driven by a number of factors including disposable income, price, personal preference, brand loyalty and social norms. Once a private customer has made the decision to purchase a vehicle, they will often set a mental budget and aim to get the ‘best’ possible car for this price. This practice is likely a contributing factor in the rise of prestige and luxury cars in the past 10 years – as Australian consumers’ disposable incomes have increased and car prices decreased, instead of purchasing the same cars at a lower price, consumers have sought a higher quality car.

Within the group of private customers, there are several subgroups who behave distinctly differently from each other. Those aged 25 years and younger5, are typically buyers of‘volume’ vehicles as they have a high need for transport and a limited capacity to pay. Families and couples tend to purchase multiple vehicles as they generally have higher disposable income and a need for flexible transport.

The decision to buy a car is essentially an economic one, in which a consumer evaluates their need for the benefit of private transport and weighs this up against the cost of purchasing and maintaining a vehicle. Once the decision to buy a car is made, a subsequent choice is made between a new or used vehicle. This choice is generally guided by financial constraints as although most consumers would prefer to purchase a new vehicle, if they cannot afford to do so, they will purchase a used vehicle.

Businesses

Spending by businesses on cars contributes more than 30 per cent of the revenue6 to the retail car market. Businesses generally buy cars for specific purposes. The types of vehicles vary widely and can include passenger vehicles and commercial vehicles. Business demand for passenger vehicles is generally limited to the volume and prestige vehicles as luxury cars are not economical for businesses. Important drivers of business demand for cars include: Government taxes and incentives Business confidence Economic growth.Government incentives to businesses proved to be a strong driver of business demand for cars in the aftermath of the GFC as businesses could claim up to 50 per cent of the cost back in tax deductions.

4 Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.5 Ibid.

7 Ibid.

16

Government

Spending from government in the retail car market is relatively small (4.4 per cent of total revenue)7, however, government still has a significant role as a buyer in the market as it has the ability to make large purchases of a single model of car. These large purchases are often guided by government strategic direction and policy and in Australia have historically been directed by policy issues such as support for the Australian car manufacturing industry and/or environmental considerations.

3.3.3 Price elasticity of demand

The price elasticity of demand plays an important role in the retail car market. Price elasticity, or the sensitivity of demand to price changes, describes how consumers behave when there is a price change in a good. High price elasticity means that consumers are highly reactive to price changes and that a small change in the price (whether upwards or downwards) will result in a proportionally larger change in how much of that good is demanded by consumers. Low price elasticity means that consumers are not very reactive to changes in price and a change in the price of a good will result in a proportionally smaller change in consumer demand for the good. The price elasticity of demand generally depends on several factors including: Availability of substitutes – goods that are easily substituted by other goods generally

have a higher price elasticity of demand Proportion of income – consumers are generally less responsive to price changes in

goods that only require a low proportion of income, and more responsive to price changes in goods that require a high proportion of income.

Necessity – the more reliant a consumer is on a certain good, the less responsive the consumer will be to changes in price of that good.

Brand loyalty – customers who are loyal to a particular brand will be less likely to respond to price incentives, so the higher the brand loyalty is for a particular good the lower the price elasticity of demand is for that good.

Demand in the retail car market is generally elastic as there are a wide range of almost identical substitutes and the cost of a car represents a large proportion of an average income.

3.4 Supply3.4.1 The business model

The retail car market in Australia is dominated by the dealership business model. Under this model, independent car dealers purchase franchise rights from motor vehicle manufacturers or local importer companies that allow the dealers to: Use the manufacturers’ branding Sell the manufacturers’ cars Employ authorised service staff.

17

As part of the franchise agreement, dealers have to pay a franchise fee of up to $2 million8

(for larger dealerships) and have a range of obligations including: Meet sales targets Satisfy performance measures Maintain high working capital.

Retail car dealers operate on very thin margins: the average Australian dealer achieved a net profit of 1.9 per cent over the 20139 calendar year.

In section 3.2, it was noted that for volume, prestige and luxury car dealers, new car sales and service were the most profitable departments. However, after accounting for overhead expenses, this pattern changes. Chart 3.6 shows a breakdown of an average dealer’s 2013 profit after overhead costs have been allocated to each department on the basis of gross contribution. From this we can see that dealers can maximise profit by focusing on “Other Income” and “Finance and Insurance”. Other Income largely relates to factory incentives that are not directly attributed to a vehicle model. These can be associated with the overall dealership performance as well maintaining brand standards. Note, Chart 3.6 shows that after allocating overhead expenses, new vehicle and used vehicles sales actually make a loss and a negative contribution to net profit.

Chart 3.6 Contribution of departments to total net profit

100%

80%

60%

40%

20%

0%

-20%

-40%

-60%

-80%

New Vehicles

Used Vehicles

Parts

Service

F&I

Other Income

* Overhead expenses allocated using departmental contribution to total gross profit

Source: Deloitte Motor Industry Services data (2013)

The dealership business is fundamentally based on the sale of new vehicles but, as Chart3.6 depicts, this area of the business typically generates little to no profit for the business. However, by generating sales volumes, dealers create opportunities to build customer relationships which result in a future stream of revenue. Such revenue includes adding and installing aftermarket accessories10 on the new vehicle sale, dealership finance and

8 Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.9 Based on the 800 dealers across Australia that report to Deloitte ProfitFocus system, the average dealer achieved a net profit of 1.9 per cent.10 Aftermarket refers to additional services such as extended warranty and accessories refer to additional features such as tinted windows.

insurance (F&I), and servicing the customer’s vehicle throughout the life of the car. This stream of revenue is completed when the car is traded in for another new vehicle.

The profit structure described above is driven by a whole-of-industry dynamic. The ultimate goal of a manufacturer is to wholesale a vehicle to every member of their target market. As these target markets become less targeted and more volume driven (in the pursuit of greater profits) dealers are expected to take these additional vehicles and find customers for them. As a result of these greater volumes the industry has been experiencing a supply push market for the last couple of years.

As a way of aligning dealers with the manufacturers’ overall business strategy the manufacturers create incentives programmes. These targets are generally set at three levels. The first promotes volume and depending on the strategy of a franchise they may choose to reward based on vehicles sold or registered, share of PMA, sales only with in the PMA or wholesale take up. The second layer of incentives generally addresses customer satisfaction and relates to both front end and aftersales customers (i.e. new car buyers and service customers). Finally, the third layer of incentives is in place to ensure brand standards, corporate identity and overall business management is on par with franchise requirements.

There are a large number of ways that these incentives are implemented and measured. In particular the first layer of incentives, which encourages the sale of vehicles, is applied by each brand for each dealership several ways. In the recent years with the supply push market, a trend has emerged in the retail car market which is commonly known as “the gamification of the industry”. With the aim of first driving new car volumes and then, later, addressing stock concerns, the franchises have changed the way dealerships earn profits at the retail level by introducing complex bonus and incentives programmes. The profit outcomes of these programmes for dealers are often unpredictable. Manufacturers are now awarding monthly, quarterly and annual bonuses for achievement of targets.

Multi-franchise dealers (over 90 per cent of the dealers in Australia) need to invest significant amounts of time and effort to maintain a current understanding of all the programs in place across all their brands as programmes change on a monthly basis. In addition to understanding the available incentive programs, dealers need to calculate the most profitable path for their dealership to take through overlapping, and sometimes conflicting, incentives. However, there are benefits to be had for those who can successfully work through the programs on offer and choose the ones most likely to pay off for their dealership. Dealers who do successfully play the variable margin game fare much better than those who either do not or cannot.

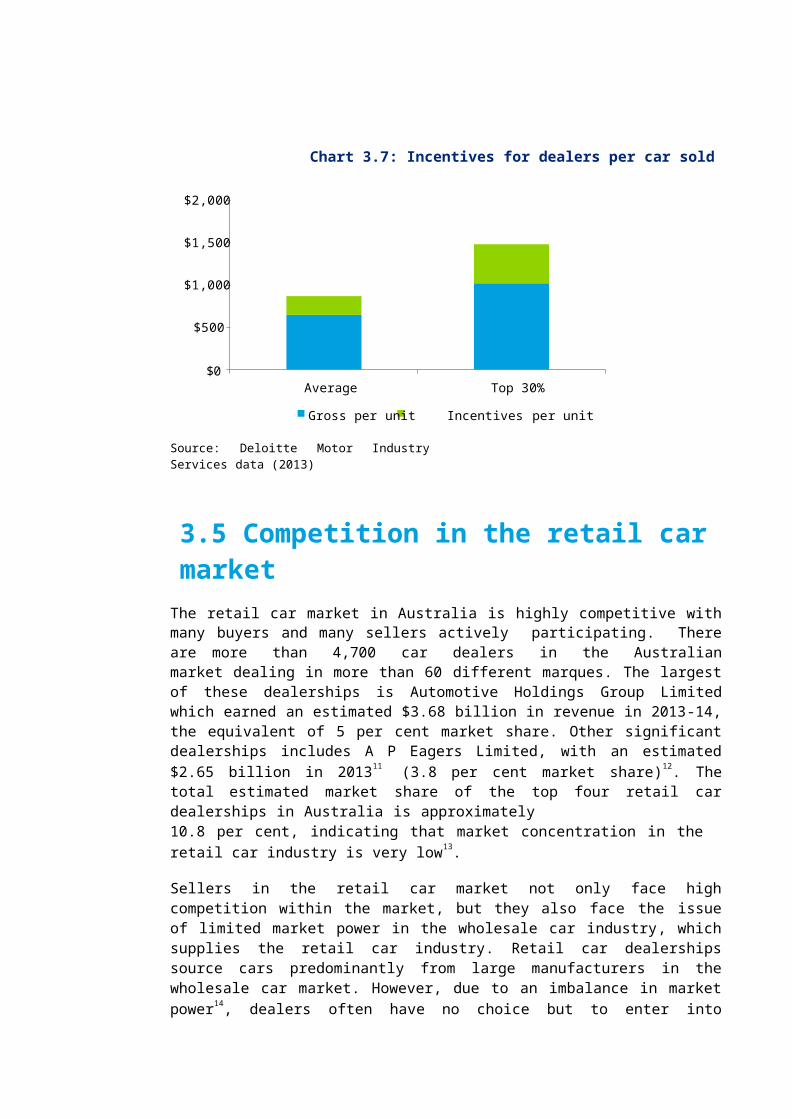

The average dealer in Australia during 2013 received around $220 worth of incentives for each new vehicle they sold. However, the top 30 per cent of dealers – those who played the incentive game well – received more than double that at $460 per unit.

Chart 3.7: Incentives for dealers per car sold

$2,000

$1,500

$1,000

$500

$0Average Top 30%

Gross per unit Incentives per unit

Source: Deloitte Motor Industry Services data (2013)

3.5 Competition in the retail car marketThe retail car market in Australia is highly competitive with many buyers and many sellers actively participating. There are more than 4,700 car dealers in the Australian market dealing in more than 60 different marques. The largest of these dealerships is Automotive Holdings Group Limited which earned an estimated $3.68 billion in revenue in 2013-14, the equivalent of 5 per cent market share. Other significant dealerships includes A P Eagers Limited, with an estimated $2.65 billion in 201311 (3.8 per cent market share)12. The total estimated market share of the top four retail car dealerships in Australia is approximately10.8 per cent, indicating that market concentration in the retail car industry is very low13.

Sellers in the retail car market not only face high competition within the market, but they also face the issue of limited market power in the wholesale car industry, which supplies the retail car industry. Retail car dealerships source cars predominantly from large manufacturers in the wholesale car market. However, due to an imbalance in market power14, dealers often have no choice but to enter into franchise agreements which tend to favour the manufacturer.

11 Year end for A P Eagers Limited is in December.12 Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.13 According to the Australian Competition and Consumer Merger Guidelines 2008, an industry is considered to be concentrated if the Herfindal-Hirschman Index (HHI) value of the industry is greater than 2000. Using the above market shares to calculate HHI for the retail car market gives a maximum score of approximately 100, well below the level that would be considered concentrated.14 The combined market share of the top 4 manufacturers is approximately 39 per cent, nearly four times larger

than the combined market share of the top 4 dealers, which is approximately 10.8 per cent. Whytcross, D. (2014). Motor Vehicle Wholesaling in Australia. IBISWorld Industry Report F3501. IBISWorld.

Competition in an international context

When put in an international context, Australia’s high level of competition in the retail car market becomes more apparent. The number of brands and market share of each of these brands of car are good indicators of the level of competition in a market. Table 3.5 presents a comparison of these indicators in Australia, Canada, the UK and the USA – Australia has both a higher number of brands (67) and a lower market size per brand (16,597 unit sales per brand) than each of these other markets, both indicators suggesting that Australia is highly competitive.

Table 3.5: Competitiveness of global car markets, 2013

Australia Canada UK USANumber of brands in Australia 67 49 53 51Sales (car units) 1,112,032 1,620,221 2,249,483 13,040,632Market size per brand (car units) 16,597 33,066 42,443 255,699Source: Department of Industry, Innovation, Climate Change, Science, Research and Tertiary Education (2013),March 2013 Automotive update

3.6 Information and regulationThe Australian retail car market is a well-developed market with many consumer protections that have been integrated through industry self-regulation and government regulation. High levels of competition in the retail car market have made self-regulation possible as car dealers and manufacturers (who supply the dealers) place a high value on the ‘brand’ of their business and will go to lengths to maintain this.

3.6.1 Information asymmetries

In the retail car industry where such a complex product is being sold, there is a natural risk of information asymmetry. Information asymmetry is defined as the imbalance of information between a buyer and a seller of a particular good, which leads to an economic advantage for either the buyer or seller. An example of this would be if a car dealer was selling a car to a customer and the dealer falsely informed the customer that the particular car was very popular and had high resale value – if the customer had no access to genuine information regarding the popularity and resale information of the car, they may believe the dealer and be willing to pay a higher price than they would if they knew the truth. Cars are generally complex products and often consumers are unable to understand or compare competing claims.

In the Australian retail car market there are numerous consumer protections in place to alleviate problems of information asymmetry. This is especially important for the used car market. As new cars tend to have extensive documentation on specifications produced by car manufacturers, it is possible for customers to research the car that they are interested in buying rebalancing the information asymmetry. Third part sources such as newspapers, magazines and speciality car sales websites publish information and often compare competing vehicles. The quality of a used car, however, is affected by many factors that only the previous owner knows of – as such there is much regulation in place that protects

consumers from issues of information asymmetries when purchasing used cars. An

important component of this is the nation-wide register, the Personal Property SecuritiesRegister, which includes the following for motor vehicles: Written off status Registration status Stolen status.The market has also provided for additional regulation with numerous websites such as w w w . c ara d v i c e . c o m . a u , w w w . c arsa l e s . c o m . au and w w w . red boo k . c o m . au emerging that provide information relating to used car prices, specifications, common issues with cars and tips when purchasing used cars.

3.6.2 Cognitive biases

Cognitive biases often described in the field of behavioural economics, such as salience and heuristics, are of great relevance in the retail car market. Simply speaking, salience describes the tendency of consumers to make decisions based only on what is most relevant to them, and heuristics are decision making shortcuts that consumers employ when facing complex decisions (i.e. using a rule of thumb measure). These phenomena are described further in Box 2.1. These cognitive biases are important because many consumers taking part in the retail car market have limited understanding of motor vehicles. As consumers are often unaware of the technical attributes of cars, they rely on heuristics to make decisions and filter out information that is not salient to them.

Box 2.1 Salience and Heuristics

Salience

The concept of salience explains the cognitive bias that occurs where people filter out complex information and only consider information that is relevant to them. Examples of this effect can include the bias where the size of government expenditure on benefits of particular government reform are much more understandable to consumers or taxpayers if they are expressed in amount per capita rather than as the overall amount. Other examples may include the tendency for consumers to filter out trailing digits of numbers. This has been found in the United States where consumers purchasing used cars tend to overemphasise the increase in mileage where the first few digits change and overlook increases in mileage where the trailing digits change. This was shown where the valuation of a used car was not greatly different between a car with a mileage of 49,000 mi and49,500 mi but the valuation would suddenly drop if the mileage of a car increased from49,500 mi to 50,000 mi.

Heuristics

Consumers display another type of cognitive bias where, in order to make sense of complicated information, consumers may rely on rules-of-thumb or maintain consumer brands/products with which they are most familiar. Using rules-of-thumb and familiarity as a basis for choice can closely approximate the optimal choice process assumed in the consumer theory of economics. Some examples of heuristics include: deciding that a particular brand of cars is more reliable than other brand because it is more popular, deciding that a luxury car has higher specifications than a non-luxury car, or deciding that a person is more believable and/or trustworthy because they have the title of Doctor.

It is important to note that using heuristics to make decisions is not necessarily wrong, however, in some cases consumers may not be choosing or deciding what they think they are.

Source: Busse and Lacetera et al. (2013), Estimating the effect of Salience in Wholesale and Retail Car Markets; Office of Best Practice Regulation (2012)

3.7 Key trends in the retail car marketTo gain a better understanding of the retail car market, it is important to look at key trends and changes that have been occurring over time. This is important as it can give insight into how the retail car market has reacted to changes in the past and, hence where it may be headed in the future.

Key overview statistics

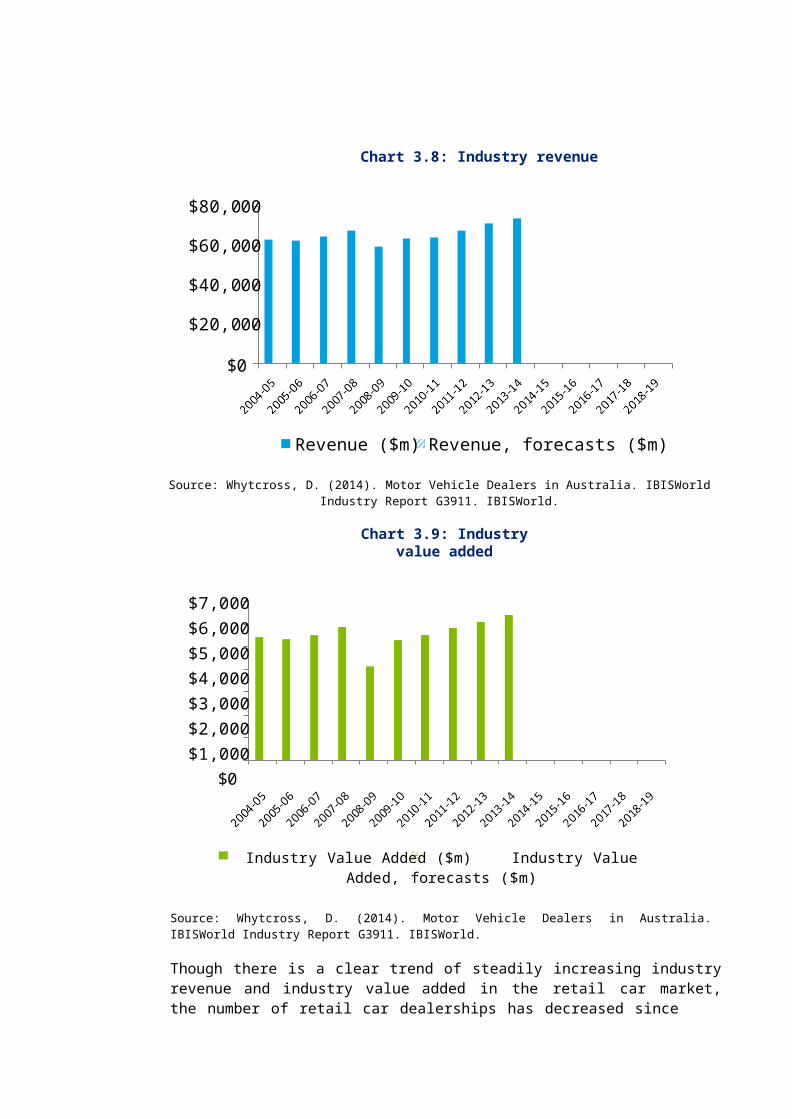

The retail car market has experienced overall growth over the past 10 years as evidenced by steadily increasing industry revenue and industry value added (see Chart 3.8 and Chart3.9). During the global financial crisis in 2008-09 industry revenue and industry value added experienced a dip, most likely as a result of consumers delaying large expenses. Forecasts for the next five years are predicting stable growth with minor increases in both industry

revenue ($0.3m increase) and industry value added ($0.1m increase).

Chart 3.8: Industry revenue

$80,000

$60,000

$40,000

$20,000

$0

Revenue ($m) Revenue, forecasts ($m)

Source: Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.

Chart 3.9: Industry value added

$7,000$6,000$5,000$4,000$3,000$2,000$1,000

$0

Industry Value Added ($m) Industry Value Added, forecasts ($m)

Source: Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.

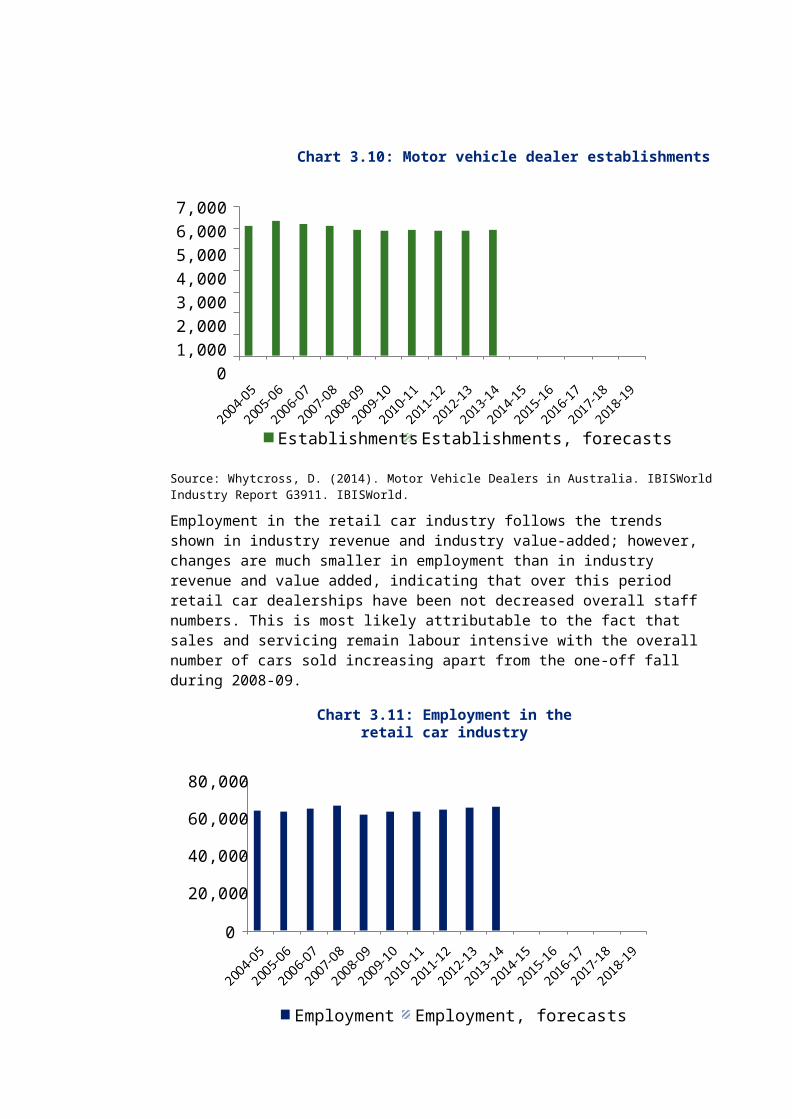

Though there is a clear trend of steadily increasing industry revenue and industry value added in the retail car market, the number of retail car dealerships has decreased since2004-05. After peaking in 2005-06, the number of car dealerships has decreased from 6,342 to 5,915. The beginning of the decrease in the number of retail car dealerships preceded the global financial crisis but was likely exacerbated by it. As industry revenue and value added have increased above pre-GFC levels, it is likely that, as retail car dealerships have found new sources of revenue and profit, the equilibrium number of car dealerships has changed.

Chart 3.10: Motor vehicle dealer establishments

7,0006,0005,0004,0003,0002,0001,000

0

Establishments Establishments, forecasts

Source: Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.

Employment in the retail car industry follows the trends shown in industry revenue and industry value-added; however, changes are much smaller in employment than in industry revenue and value added, indicating that over this period retail car dealerships have been not decreased overall staff numbers. This is most likely attributable to the fact that sales and servicing remain labour intensive with the overall number of cars sold increasing apart from the one-off fall during 2008-09.

Chart 3.11: Employment in the retail car industry

80,000

60,000

40,000

20,000

0

Employment Employment, forecasts

Source: Whytcross, D. (2014). Motor Vehicle Dealers in Australia. IBISWorld Industry Report G3911. IBISWorld.

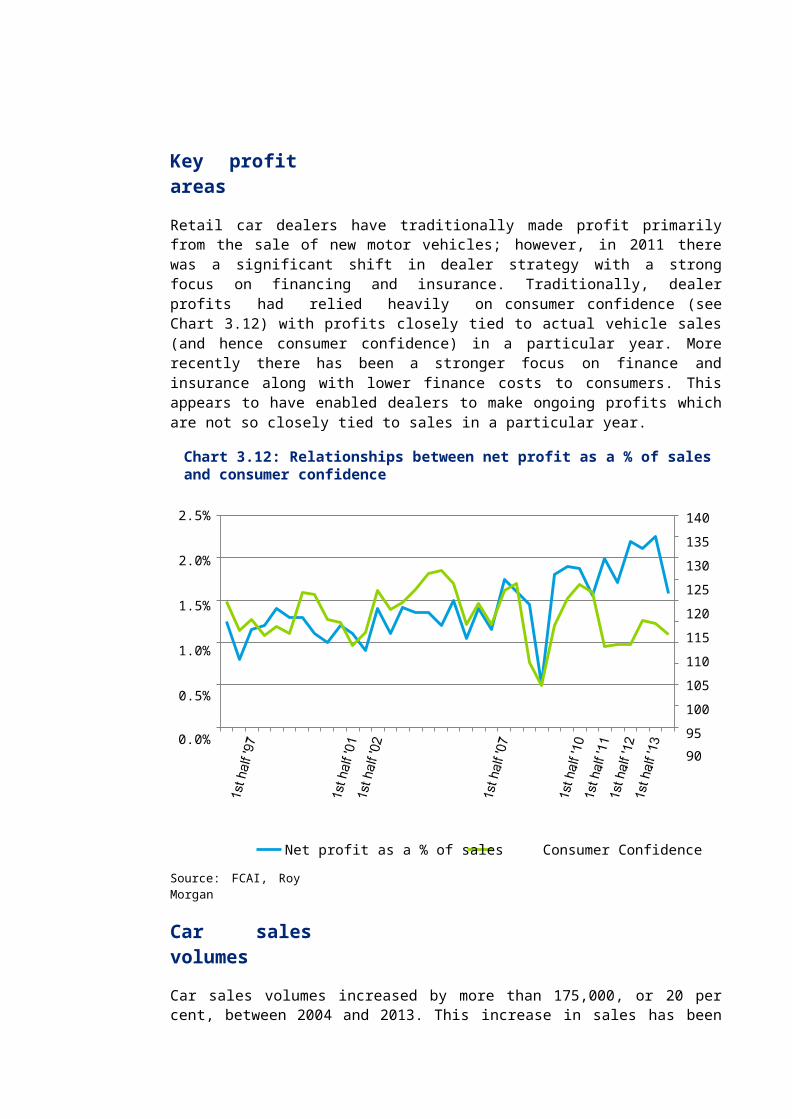

Key profit areas

Retail car dealers have traditionally made profit primarily from the sale of new motor vehicles; however, in 2011 there was a significant shift in dealer strategy with a strong focus on financing and insurance. Traditionally, dealer profits had relied heavily on consumer confidence (see Chart 3.12) with profits closely tied to actual vehicle sales (and hence consumer confidence) in a particular year. More recently there has been a stronger focus on finance and insurance along with lower finance costs to consumers. This appears to have enabled dealers to make ongoing profits which are not so closely tied to sales in a particular year.

Chart 3.12: Relationships between net profit as a % of sales and consumer confidence

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

1401351301251201151101051009590

Net profit as a % of sales Consumer Confidence

Source: FCAI, Roy Morgan

Car sales volumes

Car sales volumes increased by more than 175,000, or 20 per cent, between 2004 and 2013. This increase in sales has been predominantly driven by increases in sales of prestige cars (68 per cent of the increase) and luxury cars (23 per cent of the increase). The increase in car sales volumes is likely an indication of the increasing affordability of cars, especially luxury and prestige cars – this is discussed further in the following section. For more detailed breakdowns of sales unit volumes see Appendix A.

Mot

or V

ehic

le C

PI

Source: FCAI

Affordability

Chart 3.13: Unit sales volumes by market segment

Australia has experienced a significant increase in the relative affordability of cars over the past decade. There are a range of factors behind this increase including the appreciation of the Australian dollar reducing the costs of imported vehicles, increased competition in the local retail car market pushing down prices and a steady increase in the disposable income of the average Australian. Chart 3.14 shows the decrease in motor vehicle prices as measured by the consumer price index. The consumer price index (CPI) is the primary measure of inflation (or overall increase in nominal prices over time) and is made up of many smaller indices which measure specific types of goods and services. The motor vehicle CPI sub-index acts as a good measure of the general increase in prices of commonly purchased vehicles.

Chart 3.14: Decrease in motor vehicle prices, 2003-2013

115

110

105

100

95

90

85

Source: ABS CPI

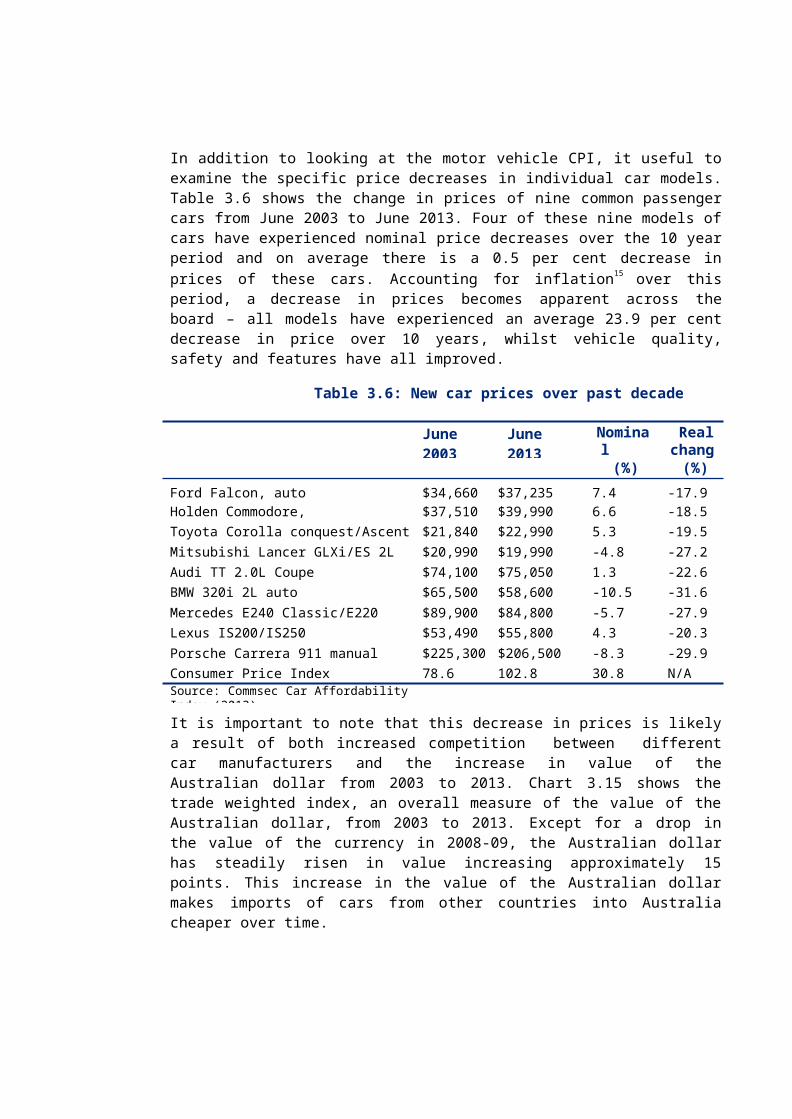

In addition to looking at the motor vehicle CPI, it useful to examine the specific price decreases in individual car models. Table 3.6 shows the change in prices of nine common passenger cars from June 2003 to June 2013. Four of these nine models of cars have experienced nominal price decreases over the 10 year period and on average there is a 0.5 per cent decrease in prices of these cars. Accounting for inflation15 over this period, a decrease in prices becomes apparent across the board – all models have experienced an average 23.9 per cent decrease in price over 10 years, whilst vehicle quality, safety and features have all improved.

Table 3.6: New car prices over past decade

June 2003 June 2013 Nominal change

Real change

(%) (%)Ford Falcon, auto $34,660 $37,235 7.4 -17.9Holden Commodore, Acclaim/Omega auto $37,510 $39,990 6.6 -18.5Toyota Corolla conquest/Ascent 1.8 $21,840 $22,990 5.3 -19.5Mitsubishi Lancer GLXi/ES 2L manual $20,990 $19,990 -4.8 -27.2Audi TT 2.0L Coupe $74,100 $75,050 1.3 -22.6BMW 320i 2L auto $65,500 $58,600 -10.5 -31.6Mercedes E240 Classic/E220 Elegance $89,900 $84,800 -5.7 -27.9Lexus IS200/IS250 $53,490 $55,800 4.3 -20.3Porsche Carrera 911 manual $225,300 $206,500 -8.3 -29.9Consumer Price Index 78.6 102.8 30.8 N/ASource: Commsec Car Affordability Index (2013)

It is important to note that this decrease in prices is likely a result of both increased competition between different car manufacturers and the increase in value of the Australian dollar from 2003 to 2013. Chart 3.15 shows the trade weighted index, an overall measure of the value of the Australian dollar, from 2003 to 2013. Except for a drop in the value of the currency in 2008-09, the Australian dollar has steadily risen in value increasing approximately 15 points. This increase in the value of the Australian dollar makes imports of cars from other countries into Australia cheaper over time.

15 Inflation here is measured by CPI. The CPI differs from the motor vehicle CPI, which is a subindex

and component of the more general CPI.

Trad

e W

eigh

ted

Inde

xRe

al n

et d

ispo

sabl

e in

com

e pe

r cap

ita

Chart 3.15: Change in the Trade Weighted Index, 2003-2013

90.080.070.060.050.040.030.020.010.0

0.0

Source: Reserve Bank of Australia (2014)

In addition to the decrease in prices of cars in Australia, over the past decade disposable incomes have risen significantly. Chart 3.16 shows that an average Australian’s disposable income16 has increased $8,741 in real terms over the period 2003-04 to 2011-12. This increase equates to a 20 per cent increase in disposable income – allowing Australians’ discretionary spending to significantly increase.

Chart 3.16: Rise in disposable incomes, 2003-04 to 2011-12

60,000

50,000

40,000

30,000

20,000

10,000

02003–04 2004–05 2005–06 2006–07 2007–08 2008–09 2009–10 2010–11 2011–12

Source: ABS (2014), Australian System of National Accounts (ABS Publication: 5204.0)

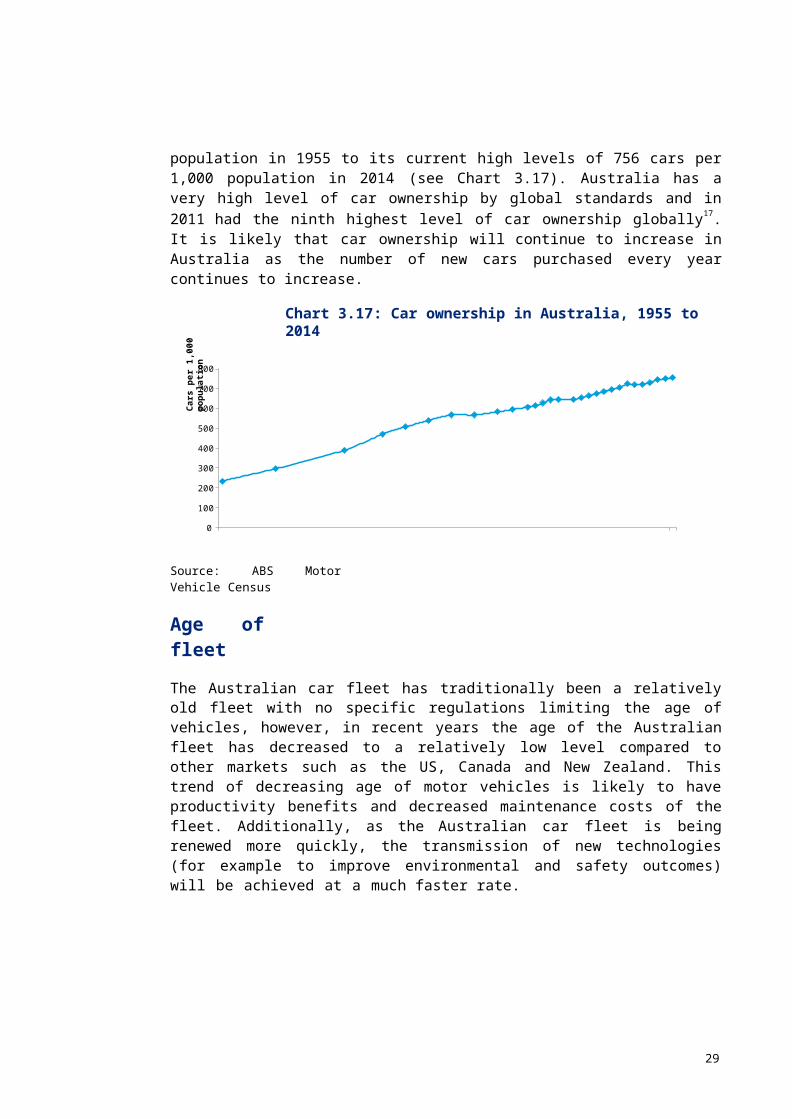

Ownership

Australia has traditionally had a very high level of car ownership. There are a range of reasons for this including geography and climate, low population density, the focus on suburban development in town planning and a strong cultural affinity with cars. Ownership of cars in Australia largely increased in the post-World War II era from 234 cars per 1,000

16 Measured by real net disposable income per capita.

29

Cars

per

1,0

00 p

opul

atio

n

population in 1955 to its current high levels of 756 cars per 1,000 population in 2014 (see Chart 3.17). Australia has a very high level of car ownership by global standards and in 2011 had the ninth highest level of car ownership globally17. It is likely that car ownership will continue to increase in Australia as the number of new cars purchased every year continues to increase.

Chart 3.17: Car ownership in Australia, 1955 to 2014

800

700

600

500

400

300

200

100

0

Source: ABS Motor Vehicle Census

Age of fleet

The Australian car fleet has traditionally been a relatively old fleet with no specific regulations limiting the age of vehicles, however, in recent years the age of the Australian fleet has decreased to a relatively low level compared to other markets such as the US, Canada and New Zealand. This trend of decreasing age of motor vehicles is likely to have productivity benefits and decreased maintenance costs of the fleet. Additionally, as the Australian car fleet is being renewed more quickly, the transmission of new technologies (for example to improve environmental and safety outcomes) will be achieved at a much faster rate.

17 World Bank World Development Indicators

30

Chart 3.18: Average age of Australian Car Fleet, 1996 to 2013

10.8

10.6

10.4

10.2

10

9.8

9.6

9.41996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: ABS Motor Vehicle Census

4 Policy driver and regulatoryanalysis

This chapter provides context for regulation in the retail car market and analyses the key policy rationale driving potential changes to import restrictions of used cars.

4.1 Legal and regulatory frameworkStandards in the Australian retail car market are primarily regulated by the following pieces of legislation and regulation: Motor Vehicle Standards Act 1989 (MVSA) Motor Vehicle Standards Regulations 1989 (MVSR) Australian Design Rules (ADRs) Registered Automotive Workshop Scheme (RAWS) Competition and Consumer Act 2010.

Other important pieces of legislation for the retail car market are related to the regulation of car dealership businesses and consumer protection. These include: Motor Dealers Act 1974 (NSW) Motor Vehicle Dealers Act 1973 (WA) Motor Car Traders Act 1986 (VIC) Property Agents and Motor Dealers Regulation 2001 (QLD) Motor Vehicle Regulations 1996 (SA) Second-Hand Vehicle Dealers Act 1995 (SA) Motor Vehicle (Accident Towing Roster Scheme) Regulations 2001 (SA) Consumer Affairs and Fair Trading Act (NT) Australian Consumer Law (Cwth).

Motor Vehicle Standards Act 1989 and Motor Vehicle StandardsRegulations 1989

The MVSA is the broad legislative framework which governs standards of motor vehicles sold in Australia. The objects of this legislation include achieving uniform vehicle standards for new vehicles in Australia and regulating the ‘first supply to the market of used imported vehicles’. One of the key drivers in the initial development of the MVSA was evidence that demonstrated imported used cars offered lower levels of safety than cars that had been built to comply with the ADRs. The MVSA also has the benefit of removing the need for multiple vehicle inspection, certification schemes and approval regimes across different jurisdictions in Australia.

One of the major concerns that the Government had at the time of the drafting of the MVSA was that large scale importation of used motor vehicles would have negative safety implications for the Australian car fleet. To this end the Government noted that the MVSA would ‘enable the Federal Government to establish and apply nationally uniform standards for motor vehicle safety and environmental equality as expected by the community.18

The mechanism through which the importation of used vehicles is restricted is set out in sections 13, 16, 17, 18, 19 and 20 of the MVSA19. Though the MVSA restricts the large scale importation of used vehicles, there is allowance made for the importation of specialty and/or personal vehicles. Importation of specialty vehicles is carried out through a Registered Automotive Workshop (RAW).

The MVSR20 is guided by the intent of the MVSA and is the instrument through which the Government sets up detailed provision for both import restrictions of used cars and concessions for particular vehicles. Some specific regulations included in the MVSR include: Provision for a register of specialist and enthusiast vehicles Provision for a review panel to govern the specialist and enthusiast vehicle register Rules around the import of used vehicles for personal vehicles Rules around the import of used vehicles for specialty vehicles Rules around the import of used vehicles of a certain age Application criteria to become a RAW21.

Australian Design Rules

The ADRs are rules which set out national standards for vehicle safety, anti-theft and emissions. The ADRs set performance based standards for vehicles including occupant safety, structures, lighting, noise, emissions and braking. After having gone through several review processes and jurisdictional changes, the ADRs are currently in the third edition. The first edition of the ADRs was developed as a discussion paper and was not legally binding in any Australian jurisdiction. However, the second edition of the ADRs was selectively applied as a legally binding standard in certain States and Territories in 1969.

The third edition of the ADRs was developed between 1983 and 1986 and became effective from 1988 as a national standard for vehicle design. The third edition of the ADRs was developed for the purposes of the MVSA and in 1989 gained national application when the MVSA was implemented. Since the implementation of the MVSA, the ADRs are continually updated and revised and are also subject to a full review every ten years to ensure that they are relevant, cost effective and do not become a barrier to importation of safer vehicles and vehicle components.22

18 Second reading speech of the MVSA, as quoted in Consultation Paper on the Motor Vehicle Standards Act1989, 201319 Motor Vehicle Standards Act 198920 Motor Vehicle Standards Regulations 198921 Ibid.22 Infrastructure.gov.au, (2014). Australian Design Rules. [online] Available at:

htt p:/ /www. i nf rast ructure. gov. au/ roads/ mot or/desi gn/ [Accessed 7 Aug. 2014].

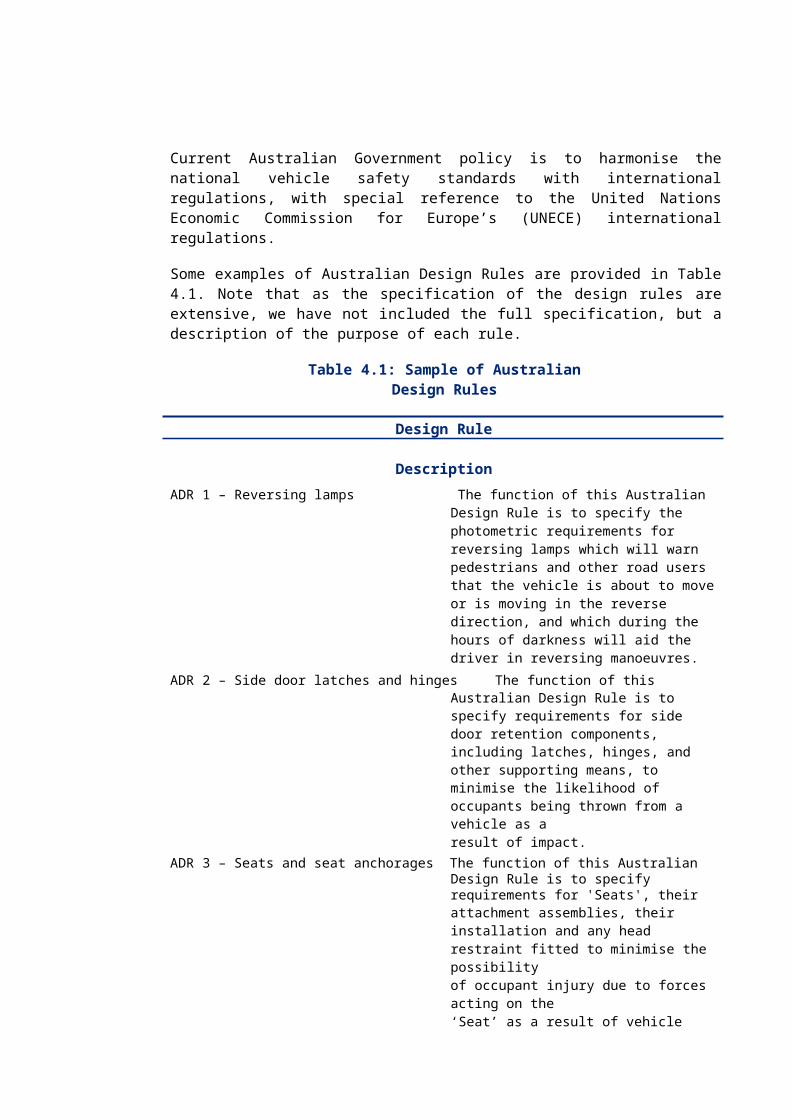

Current Australian Government policy is to harmonise the national vehicle safety standards with international regulations, with special reference to the United Nations Economic Commission for Europe’s (UNECE) international regulations.

Some examples of Australian Design Rules are provided in Table 4.1. Note that as the specification of the design rules are extensive, we have not included the full specification, but a description of the purpose of each rule.

Table 4.1: Sample of Australian Design Rules

Design Rule DescriptionADR 1 – Reversing lamps The function of this Australian Design Rule is to

specify the photometric requirements for reversing lamps which will warn pedestrians and other road users that the vehicle is about to move or is moving in the reverse direction, and which during the hours of darkness will aid the driver in reversing manoeuvres.

ADR 2 – Side door latches and hinges The function of this Australian Design Rule is to specify requirements for side door retention components, including latches, hinges, and other supporting means, to minimise the likelihood of occupants being thrown from a vehicle as aresult of impact.

ADR 3 – Seats and seat anchorages The function of this Australian Design Rule is to specify requirements for 'Seats', theirattachment assemblies, their installation and any head restraint fitted to minimise the possibilityof occupant injury due to forces acting on the‘Seat’ as a result of vehicle impact.

ADR 4 – Seatbelts The function of this Australian Design Rule is to specify requirements for seatbelts to restrain vehicle occupants under impact conditions, facilitate fastening and correct adjustment, assist the driver to remain in his ‘Seat’ in an emergency situation and thus maintain control of thevehicle, and protect against ejection in anaccident situation.

Source: Infrastructure.gov.au, (2014). Third Edition Australian Design Rules. [online] Available at: h tt p : / / ww w . i n f ra s t r uc t u r e . go v . a u / r o a d s / m o t o r / de s i g n / a d r _ on l i n e . a s px [Accessed 8 Aug. 2014]. Low Volume Scheme

The Low Volume Scheme was established with the MVSA in 1989 with the intent of providing an avenue for motor enthusiasts to gain access to specialist and enthusiast vehicles (SEVs). Initially, the low volume scheme was effective in providing concessions for the importation of SEVs, however, in the 1999 review of the MVSA it was found that the Low Volume Scheme had become an avenue for people to import used vehicles into Australia that could not be classified as a SEV and generally had low safety standards. In response to this, an amendment was passed for the MVSA in 2001 that established the RAW Scheme.

Registered Automotive Workshop Scheme

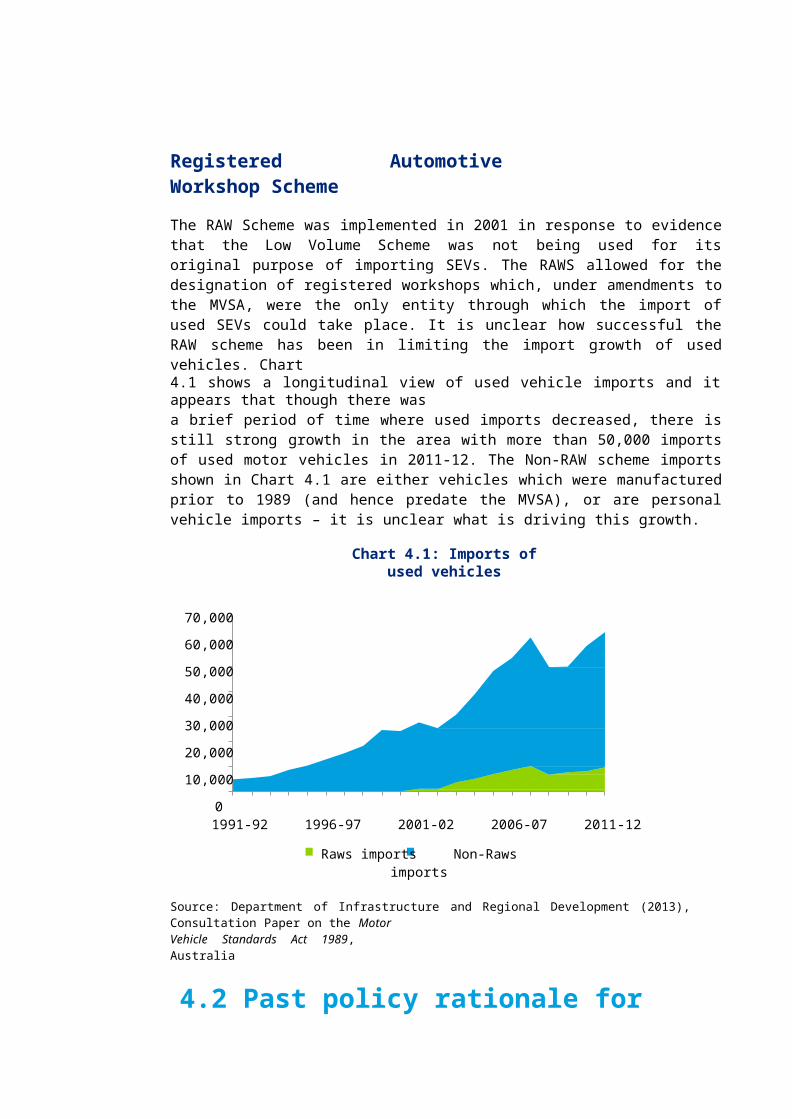

The RAW Scheme was implemented in 2001 in response to evidence that the Low Volume Scheme was not being used for its original purpose of importing SEVs. The RAWS allowed for the designation of registered workshops which, under amendments to the MVSA, were the only entity through which the import of used SEVs could take place. It is unclear how successful the RAW scheme has been in limiting the import growth of used vehicles. Chart4.1 shows a longitudinal view of used vehicle imports and it appears that though there wasa brief period of time where used imports decreased, there is still strong growth in the area with more than 50,000 imports of used motor vehicles in 2011-12. The Non-RAW scheme imports shown in Chart 4.1 are either vehicles which were manufactured prior to 1989 (and hence predate the MVSA), or are personal vehicle imports – it is unclear what is driving this growth.

Chart 4.1: Imports of used vehicles

70,000

60,000

50,000

40,000

30,000

20,000

10,000

01991-92 1996-97 2001-02 2006-07 2011-12

Raws imports Non-Raws imports

Source: Department of Infrastructure and Regional Development (2013), Consultation Paper on the MotorVehicle Standards Act 1989, Australia

4.2 Past policy rationale for restricting large scale imports

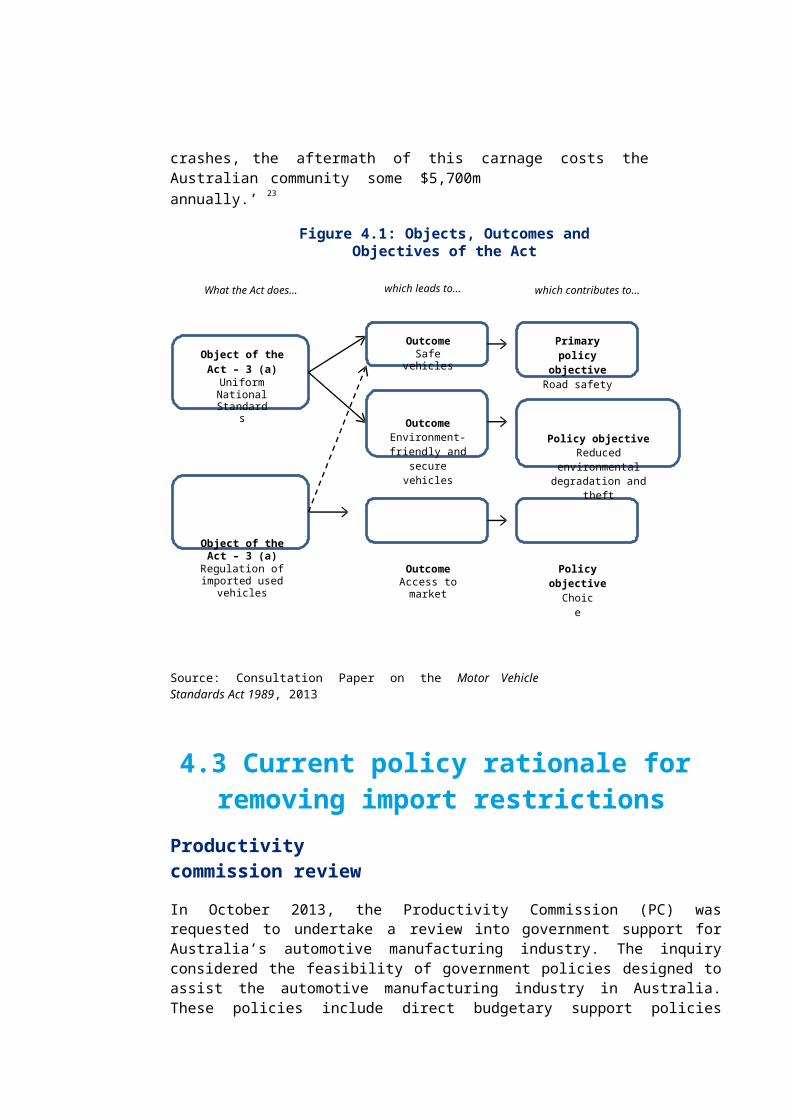

The policy rationale behind the initial restriction of large scale imports of used cars into Australia has primarily been based on safety concerns. At the time of drafting the MVSA, the Government was concerned with used car imports not complying with ADRs and as a result not meeting the standards that Australians had come to expect of motor vehicle safety. Maintaining safe driving conditions is a primary concern of government and the main focus of the MVSA (see Figure 4.1). Unsafe vehicles have both personal injury and broader economic implications. During the development of the MVSA, it was also noted by Government that ‘each year in Australia some 2,800 people are killed on our roads and30,000 seriously injured. In addition to the trauma and suffering which results from these

crashes, the aftermath of this carnage costs the Australian community some $5,700mannually.’ 23

Figure 4.1: Objects, Outcomes and Objectives of the Act

What the Act does… which leads to… which contributes to…

Object of the Act – 3 (a)

Uniform NationalStandards

OutcomeSafe vehicles

Outcome Environment-

friendly and secure vehicles

Primary policy objective Road

safety

Policy objective Reduced environmental

degradation and theft

Object of the Act – 3 (a)

Regulation of imported used vehicles

OutcomeAccess to market

Policy objectiveChoice

Source: Consultation Paper on the Motor Vehicle Standards Act 1989, 2013

4.3 Current policy rationale for removing import restrictions

Productivity commission review

In October 2013, the Productivity Commission (PC) was requested to undertake a review into government support for Australia’s automotive manufacturing industry. The inquiry considered the feasibility of government policies designed to assist the automotive manufacturing industry in Australia. These policies include direct budgetary support policies wherein the government subsidises certain activities of the automotive manufacturing industry, and indirect policies where government employs regulation to benefit the automotive manufacturing industry.

One such regulatory policy is the restriction of importation of second-hand vehicles through the MVSA. This regulatory policy has the primary aim of ensuring high safety standards in imported second-hand cars, and achieves this through both limiting the number of second- hand cars that can be imported by an entity each year, and by applying a specific customs duty of $12,000.

23 Second reading speech of the MVSA, as quoted in Consultation Paper on the Motor Vehicle Standards Act

1989, 2013

The PC came to the view in the position paper that restrictions on the importation of second-hand vehicles, particularly the barriers to large-scale importation of such vehicles, reduces competition in the car market and removal of such restrictions would benefit the community as a whole. In support of this view, the PC released a draft finding in relation to the restriction of importation of second-hand vehicles:

Draft Finding 2.2

The policy rationale for prohibiting the large-scale importation of second-hand vehicles into Australia is weak. However, appropriate regulatory measures are required to ensure that consumer protection, community safety, and environmental performance standards are maintained before the restrictions are removed. These concerns are best dealt with directly, through regulatory standards applicable to all vehicles sold in Australia.

The $12 000 specific duty on imported second-hand vehicles appears to be largely redundant, providing a prima facie case for its removal.

Following the completion of our report, the PC has since released their final review report. The core finding recommending the removal of large scale used car import restrictions was reiterated in the final inquiry report in Recommendation 5.4, though the PC’s stance on this appeared to have weakened. It is important to note that though the analysis of our report was carried out in reference to the position paper, our conclusions are not changed regarding the potential impacts of removing used car import restrictions in Australia.

Policy rationale for removing import restrictions

The policy rationale behind the PC’s recommendation is one of free market competition improving consumer outcomes. The PC points to New Zealand’s experience and argues that as a result of removing large scale import restrictions of used vehicles, there weresignificant benefits for New Zealand consumers in terms of price and choice. Economictheory suggests that removing market distortions (e.g. import restrictions) will increase the supply of a good in a particular market and result in increased competition, lower prices and higher choice of goods. It must be noted that the outcomes of such microeconomic reform may not be straightforward if there are issues such as market failures or non-rational behaviour of consumers (including bounded rationality – i.e., that the rationality of consumer decisions is limited by available information and their understanding of that information available).

5 Potential impacts to the retail carmarket

This chapter provides context for regulation in the retail car market and analyses the key policy rationale driving potential changes to import restrictions of used cars.

5.1 New Zealand experienceA useful starting place for the analysis of potential implications for the suggested policy changes is a brief analysis of New Zealand’s experience with the same policy move in 1986. New Zealand is a useful comparison to Australia as the government, culture and income per capita of both countries are similar24.

New Zealand’s decision to remove import tariffs and open up the domestic market to the large scale import of used vehicles was primarily driven by the desire to improve affordability of motor vehicles in New Zealand. In the 1970s and 1980s car ownership in New Zealand was anecdotally very low, and prices of motor vehicles were high. In addition to this, the New Zealand car fleet was aged, of a low specification, and facing sustainability problems. The New Zealand government responded to these issues by removing import tariffs on used car imports, effectively allowing the large scale importation of used cars.

Following the removal of import tariffs, the number of registered motor vehicles in New Zealand increased dramatically. Chart 5.1 shows the number of registered cars in New Zealand and the number of registered imported used cars in New Zealand. Up until 1986 the number of used imports was very low, a likely outcome of the import restrictions that New Zealand had in place prior to 1986; however, after 1986 the number of used imports dramatically increased and became the predominant type of registered cars in the market. Anecdotally, this paradigm change in the New Zealand car market came about because prior to 1986 the car fleet was ageing and of poor quality, so when relatively new cars with high specification could be imported there was a high substitution of both new and used cars.

24There are some differences in terms of car affordability and the history of car manufacturing, however, of all

countries which import used cars, New Zealand is the most comparable.

25 Additional factors also influence the age of the car fleet including new car affordability and other government policies.

38

Uni

ts o

f car

s

Chart 5.1: Car registrations

250,000

200,000

150,000

100,000

50,000

01960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Total number of registered cars Ex-overseas cars

Source: New Zealand Transport Agency (2014), MVR Statistics Book 2013

Currently there is a high level of approximately 700 cars per thousand populations – one of the highest rates of car ownership in the world; this is likely a direct result of allowing used imports.

There have been many benefits from New Zealand’s policy regarding imports of used cars; however, this may have been at the cost of both the age and the safety of the New Zealand car fleet25. Data from 2013 shows that the age of the New Zealand fleet has been steadily increasing over time – especially in comparison to the age of the Australian fleet. Chart 5.2 shows the age of the car fleet at several points in time and indicates a clear upwards trend of vehicle age in New Zealand as compared to a downwards trending fleet age in Australia.

39

Aver

age

age

of c

ars i

n fle

et

Chart 5.2: International age comparison of car fleets

16

14

12

10

8

6

4

2

02002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

New Zealand Australia USA

Source: New Zealand Ministry of Transport (2013), 2013 New Zealand Vehicle Fleet Annual Spreadsheet; ABS Motor Vehicle Census various years