Renewable Energy Dividends Effective Renewable Energy Policies For Florida John Burges 2009 Bayonne.

57

Renewable Energy Dividends Effective Renewable Energy Policies For Florida John Burges 2009 Bayonne

-

Upload

angela-barrett -

Category

Documents

-

view

216 -

download

0

Transcript of Renewable Energy Dividends Effective Renewable Energy Policies For Florida John Burges 2009 Bayonne.

Renewable Energy Dividends Effective Renewable Energy Policies

For Florida

John Burges

2009

Bayonne

2

3

RPS REDs Amendment Integrate into RPS legislation 20% by 2020 German / Gainesville model; similar to CA Energy

Comm recommendation A RED for all < 20MW renewable producers Pricing determined cost of power + profit Pricing differentiated by size, technology Cheapest $/MWhr of RE for ratepayers Drive green jobs

4

What’s Required?

Adequate insolation/wind/bio (incoming solar radiation) – Sunshine State very high; 85% of max.

Long-term fixed pricing/same as utilities X

– Payment/Recovery mechanism

– Renewables priority grid access Available/affordable land near demand

– ~10,000 acres per 1000MW Simple siting and permitting process X

– Statewide Leadership for Renewables Entrepreneurs/Developers

– State must allow new entrants

5

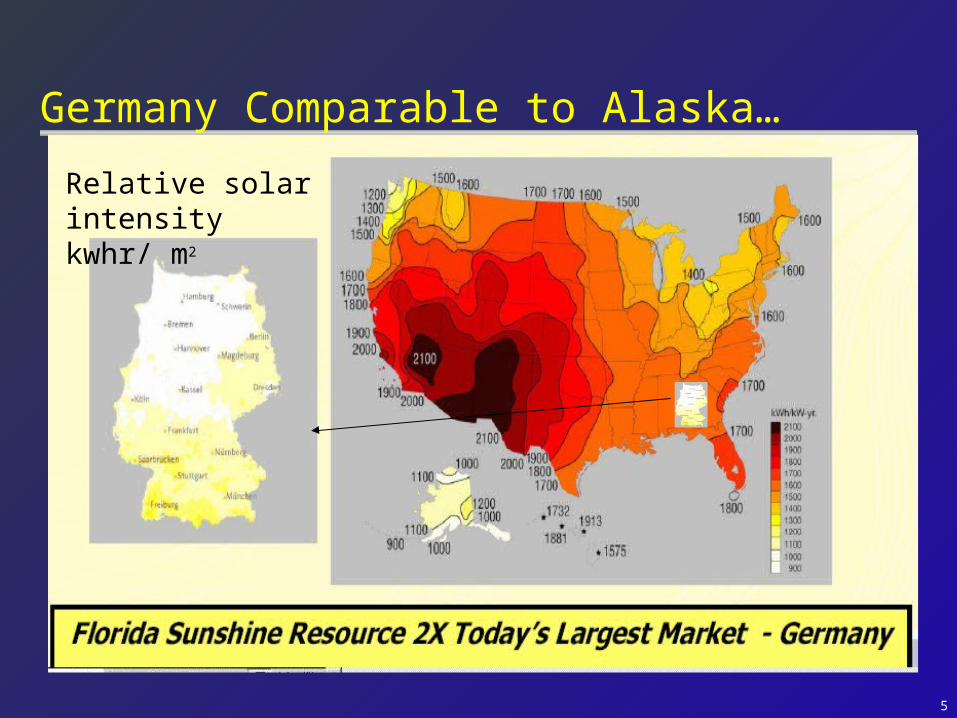

Germany Comparable to Alaska…

Relative solar intensity kwhr/ m2

6

Florida’s Total Installed Capacity On One German Roof

Munich Trade Fair (Germany), 2.1 MWpCompletion November 2002

7

US Utility Trip to Europe - Solar Factory

8

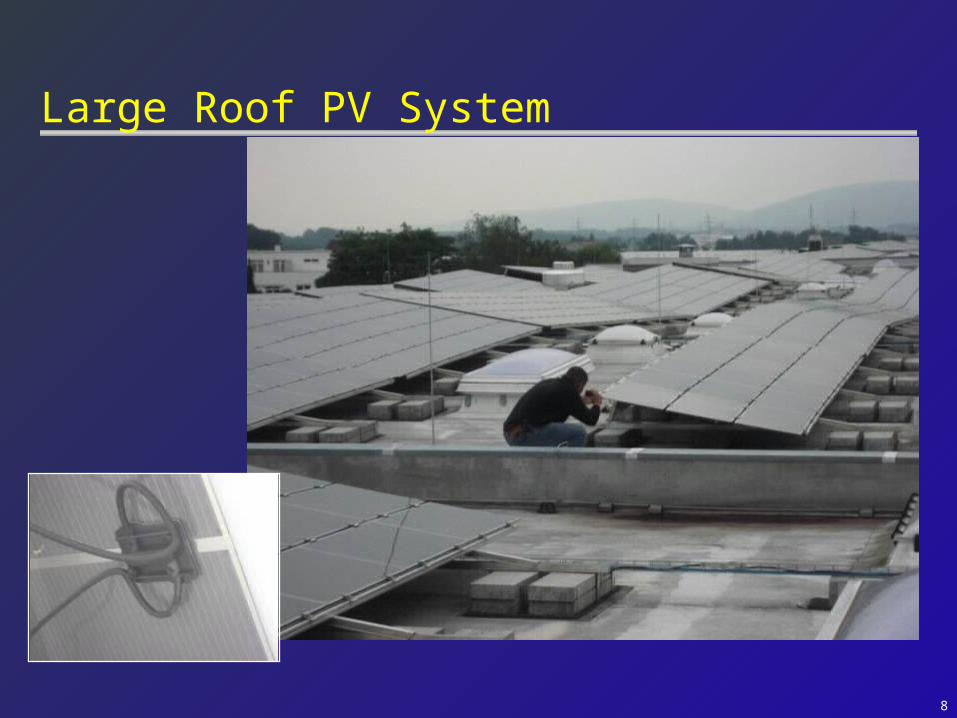

Large Roof PV System

9

Facades and Skylights

10

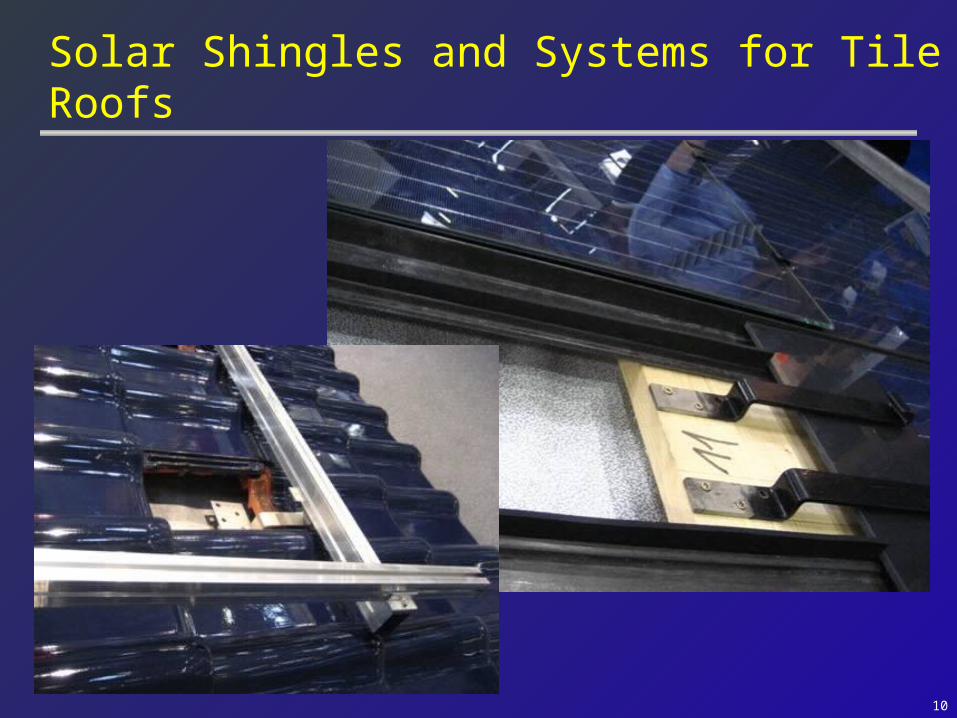

Solar Shingles and Systems for Tile Roofs

11

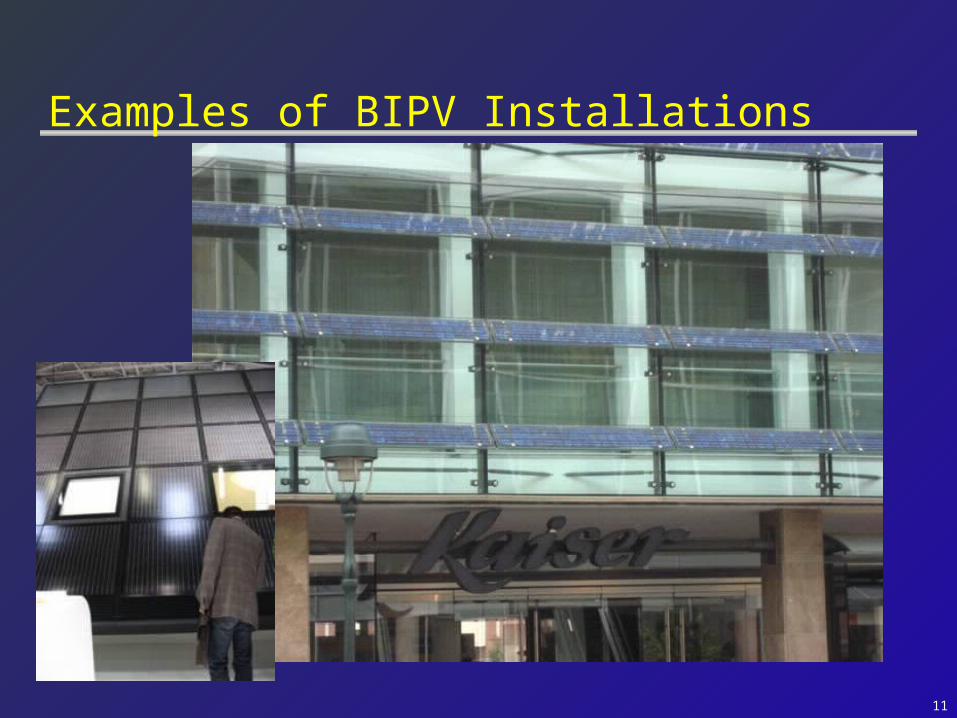

Examples of BIPV Installations

12

Notice The Bicycle Sheds!

13

Concentrator Systems

14

New Forms and Ideas

15

Jobs and Opportunity

16

Solar Job Creation in Germany, 2003 – 2010

0

10,000

20,000

30,000

40,000

50,000

60,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e 2009e 2010e

Source: EuPD Research

Germany enactsFeed-in Tariff Law

Jobs

17

Area

Germany: 357,030 km² US*: 8,154,157 km² *23 times larger, without Alaska

Installed Capacity

Germany*: 22,247 MW US: 16,818 MW

*1.3 times largerMap credit: Ryan Perroy, University of California, Santa Barbara

Landmass vs. Wind energy (MW) in Germany and Continental United States (2007)

Renewables - US Is Left in the Dust…

18

Renewables – Why Bother?

Energy Security - Pickens/Woolsey Reduce dependency Russia/Ukraine, Gazprom, Chavez, Iran Grid security

Wealth Creation - Jobs – Friedman Higher local ownership; beneficial impact on local economy Germany employs 250,000 – forecasting 500,000; “Export

Machine” Germany – 2006 - Net benefit to country $9BN per annum

Environmental Benefits Biomass, wind, solar minimal CO2

19

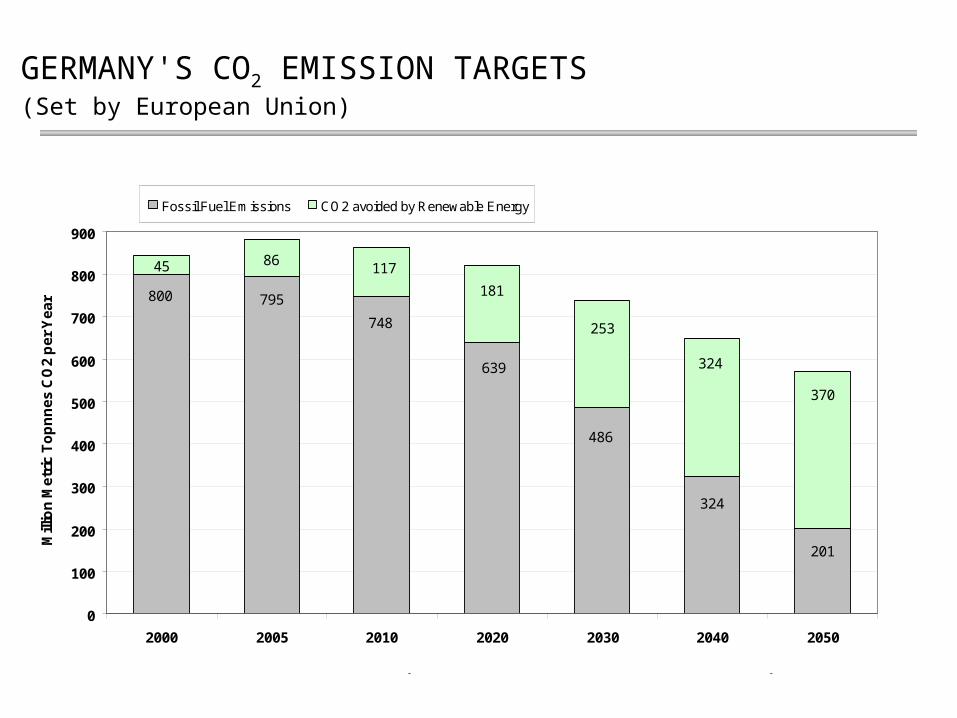

GERMANY'S CO2 EMISSION TARGETS(Set by European Union)

45 86

201

324

486

639

748

795800

370

324

253

181

117

0

100

200

300

400

500

600

700

800

900

2000 2005 2010 2020 2030 2040 2050

Mill

ion

Me

tric

To

pn

ne

s C

O2

pe

r Y

ea

r

Fossil Fuel Emissions CO2 avoided by Renewable Energy

SOURCE: German Federal Ministry for the Environment, Nature Conservation, and Nuclear Safety

2006 Actuals-- 878 million tonnes emitted-- 100 million tonnes avoided

20

Business Perspective – The Opportunity

VC investment in clean energy - $117 BN + 35% 2007 (NEF) Solar is a $ 30 billion industry – $120BN sales by 2011 - 50% CAGR

~$100BN stock market valuation for solar US solar producers largely for export; overseas cannot get enough US / Florida solar initiatives deeply flawed; deterring investment Florida is missing massive solar investment opportunity:

$5BN sales - export industry

Employing 25-50,000 people; Construction/Manufacturing, High tech R&D

Florida has ~ 2MW of solar. Germany installed over 2000MW in 2008 - $12BN Private Investment

21

Strong Global Solar PV Market Growth

QCell Presentation 09-30-07

~$30BN sales

~$100BN Sales

22

PV Financing Requirements: Who Lends?

Source: Good Energies

23

Downward Spiral Global financial meltdown Less tax capacity & capital available by institutional investors

Federal Tax credits become “worthless”

Equity supply dries up; returns increase Fewer renewable energy projects

~3,000 MW less wind farms installed in US in ‘09 vs. ’08 Loss of ~38,000* “green collar” jobs

24

Senior Loan Volume

This chart reflects the estimated primary volume to the US and European loan markets. The US Market includes tranches denominated in non-USD currencies as well as US dollars. The European Market includes tranches denominated in non-Euro or Sterling currencies as well as Euros and Sterling.

Exchange rates from non-USD currencies are based upon date of launch of the individual transactions.

251.9192.9

138.5 144.8 165.7

274.4 297.9

480.6536.2

154.5

36.2

54.8

65.7 38.253.7

81.4

147.0

163.2

226.2

81.2

235.7

288.2

247.7

204.2183.0

219.3

355.8

444.8

$0B

$100B

$200B

$300B

$400B

$500B

$600B

$700B

$800B

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

US Market European Market

643.8

762.4

Source: S&P

25

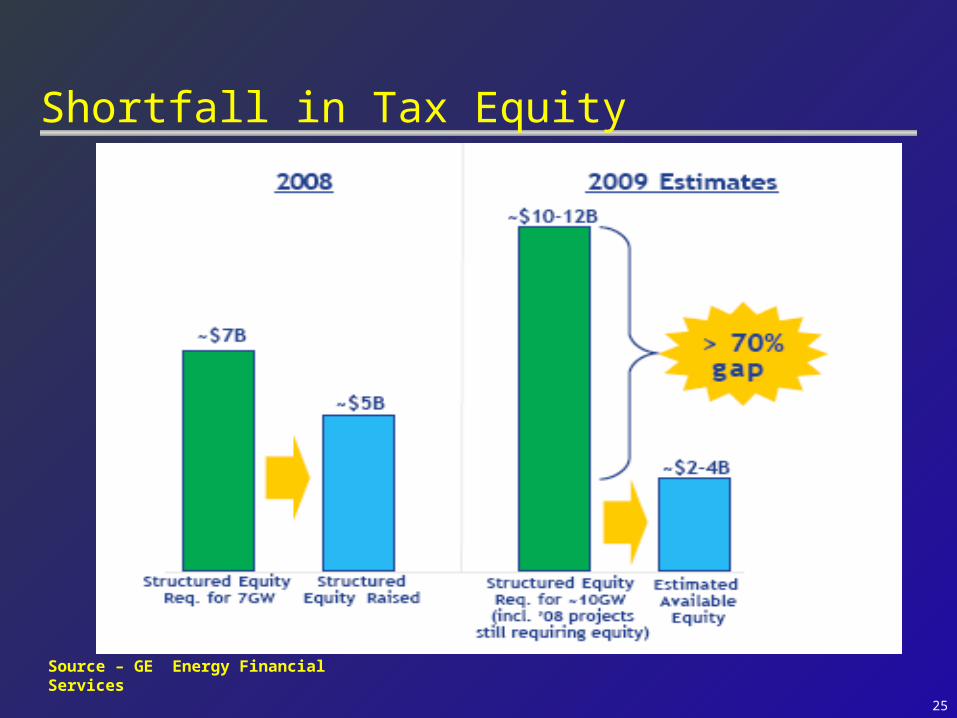

Shortfall in Tax Equity

Source – GE Energy Financial Services

26

Solutions

Modify Federal ITC

Refundable RE Performance Based Incentives

Feed In Tariffs

Quotas – tradable RECs

27

Regulatory Regimes – High Risk ROCs (UK)

RPS / RECs / SRECs (US)

Price risk for electricity

Price risk for the ROCs / RECs (usually)

Lending restricted to duration of RPS obligation and stability of regime

Price & volume risk reduces maturities; reduces leverage and increases price

28

Regulatory Regimes – Low Risk

Feed-in Tariffs

No price risk

No volume risk

Limited or no regulatory risk once project is built

Counterparty risk is utility/sovereign

Attracts more capital on better terms

29

Post Banking Crisis…creates new uncertainty

(end 2007)

Feed-in

RECs / RPS

PTC

Leverage (debt, %)

>90%

70-80%

60-80%

50-70%

75% ???

Maturity (after completion)

15-18y

13-15y

3-15y

Mini-perms

12y ???

Margins

60-100pb

170-200bp

90-120pb

200-250bp

100-125pb

???

Capital will flow to least risk regulatory mechanism

Dexia Bank

30

What are Feed in Tariffs ?

31

Renewable Energy Dividendsor Feed in tariffs Simple, transparent – available to all

Priority access to the grid for all renewable producers

Long term standard offer contracts; fixed price guaranteed

– 20 years

Cost + reasonable profit (tba by PSC)

– Price Differentiation by size, technology

Price degression

– Germany 9-10% fall

– Spain 30%

32

Renewables - Issues ► Solution Utilities finance fossil fuel under 20 yr rate base

Guaranteed – cost pass through Renewables require same treatment; private sector will finance Solution:

Covers all renewables; solar likely to be most productive

RE priority access to grid, 20 yr contracts, differentiated pricing,

We need every school, church, farmer, household and real estate developer to become entrepreneurs & sell back power & so drive us to a more secure clean electricity future

FACT – happening now throughout Europe; growing in US

33

Renewable Energy Dividends Policies Deliver More Capacity--

--More Quickly --More Equitably

By Enabling Participation --Everyone

18 EU Countries use Electricity Feed Laws 46 Countries world wide 2008 additions: UK, Switzerland, Ukraine, India US – Hawaii, OR, CA, IL, MI, MN, RI, LADWP, City of

Gainsville

Paul Gipe, wind-works.org

34

35

Feed In Policies &Solar Photovoltaics in Germany

Renewable Tariffs Launched

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

0

1

2

3

4

MW Total (Thousands)

Renewable Tariffs Launched

1,000-Rooftops (2,500 x 3kW)

100,000 Rooftops

36

Solar Photovoltaic Development

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

0

1

2

3

4

Total Installed MW (Thousands)

USA

Japan

Germany

37

Paul Gipe, wind-works.org

World PV Capacity 2007~8,000 MW

Germany53%

Japan28%

USA11%

Rest of World7%

3,963

2,120

806

550

38

Paul Gipe, wind-works.org

World Wind Generating Capacity

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

0

20

40

60

80

100

Megawatts (Thousands)

Europe

North America

Asia

39

German Homeowners

500 MW on Home Rooftops/yr 2,000 MW+ Total 2 TWh/yr ~ €1 Billion/yr Revenue Anyone with a Roof Can Do Solar in

Germany!

Paul Gipe, wind-works.org

40

German Farms--Solar PV Crop ~700 MW on Barn Rooftops in 2007 ~1,500 MW Total in 2007 (€9 Billion) ~1.5 TWh/yr (€700 Million)

Paul Gipe, wind-works.org

41

sGermany’s Feed in PoliciesThe Results (2007)

Renewables 15% of Supply; 27% target 2020, 45% 2030 Renewables 6% of Primary Energy 70,000 Employed in Wind Industry 50,000 Employed in PV Industry 8,000 Employed in Biogas Industry 250,000 Employed in Renewables €22 (~$30) Billion Turnover Net Benefit $9BN annually

Paul Gipe, wind-works.org

42

NREL Research Findings Countries with REDs:

Have highest RE deployment

Have highest job creation; highest economist benefits tied to industry, manufacturing & services

Have counter-intuitively delivered lower-cost RE generation than countries employing “competitive” policies like the RPS & RO in the UK

National Renewable Energy Laboratory

43

REDs/FITS vs. Alternative Policies Wind power deployment in the EU:

0

10

20

30

40

50

60

70

80

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Elec

tric

ity

Gen

erati

on (T

Wh)

Counties with wind FIT Counties with alternative support

Source: EUROSTAT, 2008; NREL, 2008

National Renewable Energy Laboratory Innovation for Our Energy Future

44

NREL Findings - RE Policy & Cost

Average per kWh Payment for Onshore Wind (2008)

0

5

10

15

20

25

Germany Spain UK* Italy*

Countries

Pu

rch

ase

Pri

ce

(US

D c

ents

/kW

h)

* Electricity price + Tradable Green Certificate (i.e. REC)

Source: BMU 2008; ISI, 2008; Fouquet, D. et al., 2008

FITs

RPS + RECs

45

NREL - REDs vs. RPS on Cost Expected Profit/kWh for

Onshore Wind 2006

0

1

2

3

4

5

6

7

8

Ge

rma

ny

Sp

ain

UK

Ita

ly

Ex

pe

cte

d P

rofi

t (E

uro

ce

nts

/kW

h)

Source: OPTRES, 2007; NREL 2009

NREL Research finding that REDs/FITs offer better value for money

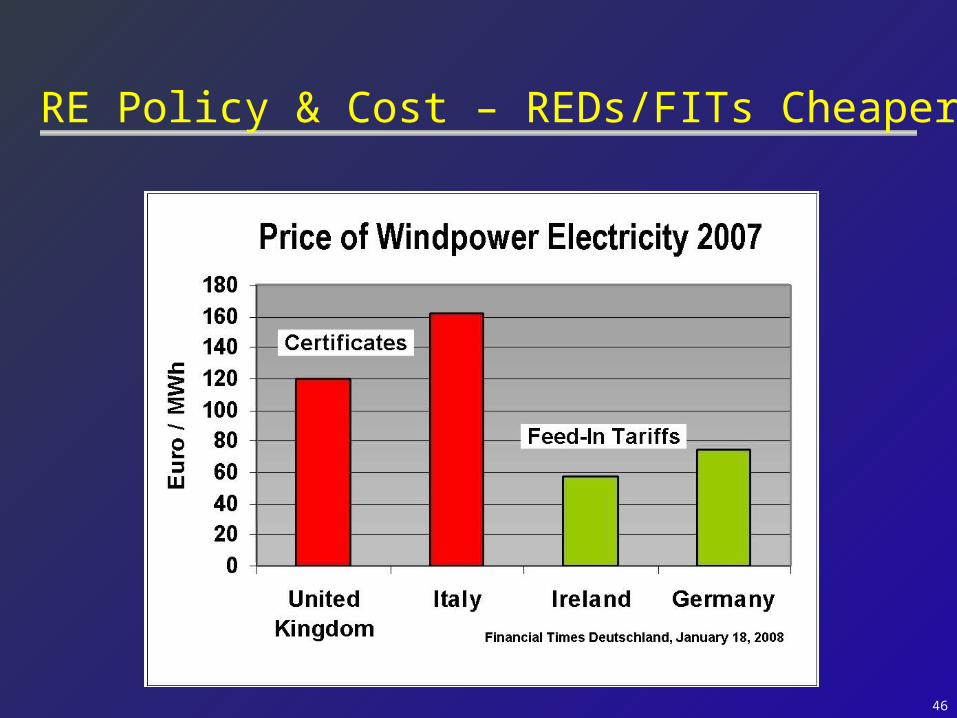

46

RE Policy & Cost – REDs/FITs Cheaper

47

Florida’s Energy Issues Over-reliant on fossil fuels; imported Gas > 50%

power• $50+ oil - (IEA - $200 by 2030 ) FL’s long term

electricity costs?• Utility rate increases of 10-15%

Renewables - Speed

• Currently < 3% of power generation mix

48

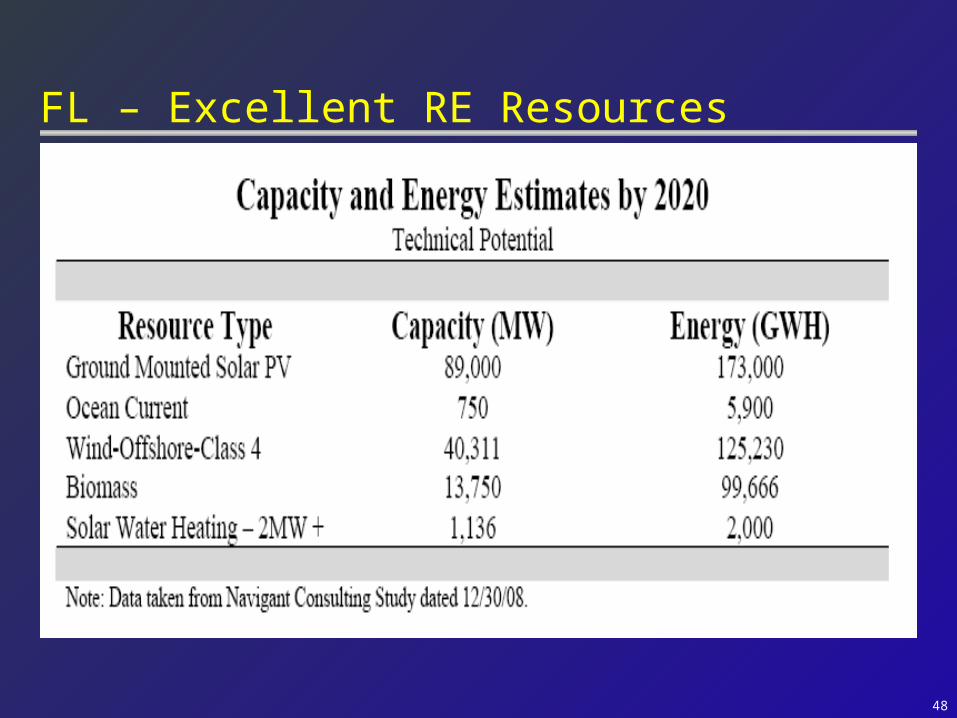

FL – Excellent RE Resources

49

Florida PSC RPS Rule/Senate Bill

20% RE & Nuclear by 2020 Rate cap of 2% IOU sales ~ $370MM Recommended tradable REC market

Spot; longer term contracts (unclear how) Nuclear 25% of targets; RE 75% Carve out for wind and solar Utility decides which projects get done, by whom ROE penalties for non-compliance 3rd party administrator appointed by IOUs

50

A Trading System

51

SRECs – Not A “Trading” System

TRADABLE SRECS GIVE NO INVESTMENT SECURITY

52

GRU’s Solar Feed in Tariff ScheduleEffective March 1, 2009

Building or Pavement Mounted (any size) or Ground Mounted

< 25 kW

2009 2030 $0.32 $0.262010 2031 $0.32 $0.262011 2032 $0.30 $0.252012 2033 $0.28 $0.232013 2034 $0.27 $0.222014 2035 $0.26 $0.212015 2036 $0.25 $0.202016 2037 $0.23 $0.19

Contract Entered into Under This Policy

During Calendar Year

Fixed Rate per kWh Applied Uniformly From the Date of

Installation Through December 31,

Fixed Rate $/kWh Over Life of Contract

Free Standing (Non-Building or Non-Pavement

Mounted)

53

GRU Achieves First Year Target for Solar Program equaling $35MM of private investment

4MW completed applications; doubles FL capacity

“We are extremely excited about the popularity of the program - our efforts to stimulate the market have been successful,” said Bob Hunzinger, GRU GM

Guarantees purchase of all electricity produced by the PV system at a fixed rate for 20 years at $0.32 kwhr for customers for first 2 yrs

The rate of $0.32 per kilowatt hour will remain in effect for 2010, falls 5% per annum thereafter

FIT Results – Feb 5th – March 1st

54Summit Blue Consulting 54

NJ BPU Analysis By Summit Blue – Projected Tradable SREC ~ 50% More Expensive For Ratepayers

Ratepayer ImpactsWgt. Avg. by Project Type

$0.0000 $0.0005 $0.0010 $0.0015 $0.0020 $0.0025 $0.0030

Base Case (w/o $300 SCAP)

SREC Only

Underwriter Model 15y

Commodity Market Model

Auction Model

15 Yr Tariff Model

Hybrid-Tariff Model

$/kWh

Source: Summit Blue

55

NJ – REC Market - What Actually Happened

2.1% solar by 2021; 1500MW or ~ 117-140MW per annum 2008 target – 90MW; 63MW actual – off track for RPS ACP 71c kwhr REC value - declines 3% Spot: 65-67c/kwhr + 15c net metered energy = 2.5x GRU FIT Some 3 yr contract -5-7 yr rare; 50-55c > 2x GRU FIT BPU recognizes that lack of long term contract a problem –

securitization being discussed

Source: Vanguard Energy Partners

Without must take long term fixed price contracts – ratepayers pay 2x GRU

56

What Can You Do? Contact local Representatives Contact House Leadership

Speaker – Larry Cretul - 850 488-1450 Contact Senate Leadership

Jim King – Chair of Utility - 850 487-5030

Thad Altman – Chair of Finance & Tax

57

Contact Details

www.FAREnergy.org

Executive Director – Mike Antheil

Tel # 561 703 4345