RENEWABLE ENERGY DEVELOPMENT Energy … ENERGY DEVELOPMENT IN ASEAN 2nd Asia Renewable Energy...

36

RENEWABLE ENERGY DEVELOPMENT IN ASEAN 2 nd Asia Renewable Energy Workshop Jakarta, 02 – 04 December 2015 1 Badariah Yosiyana ASEAN Centre for Energy

Transcript of RENEWABLE ENERGY DEVELOPMENT Energy … ENERGY DEVELOPMENT IN ASEAN 2nd Asia Renewable Energy...

RENEWABLE ENERGY DEVELOPMENT IN ASEAN

2nd Asia Renewable

Energy Workshop

Jakarta, 02 – 04 December 2015

1

Badariah YosiyanaASEAN Centre for Energy

OUTLINE

• Introduction

• What is RE Program in ASEAN : - potential, installed power capacity, power generation, the relevant RE policies

• 4th ASEAN Energy Outlook

• RE Financing

• Way forward

2

ASEAN CENTER FOR ENERGY (ACE) IN ASEAN’S STRUCTURE

Intergovernmental

Organisation on

Energy Matters

7 specialized areas

ACE reports to the

ACE Governing

Council

4

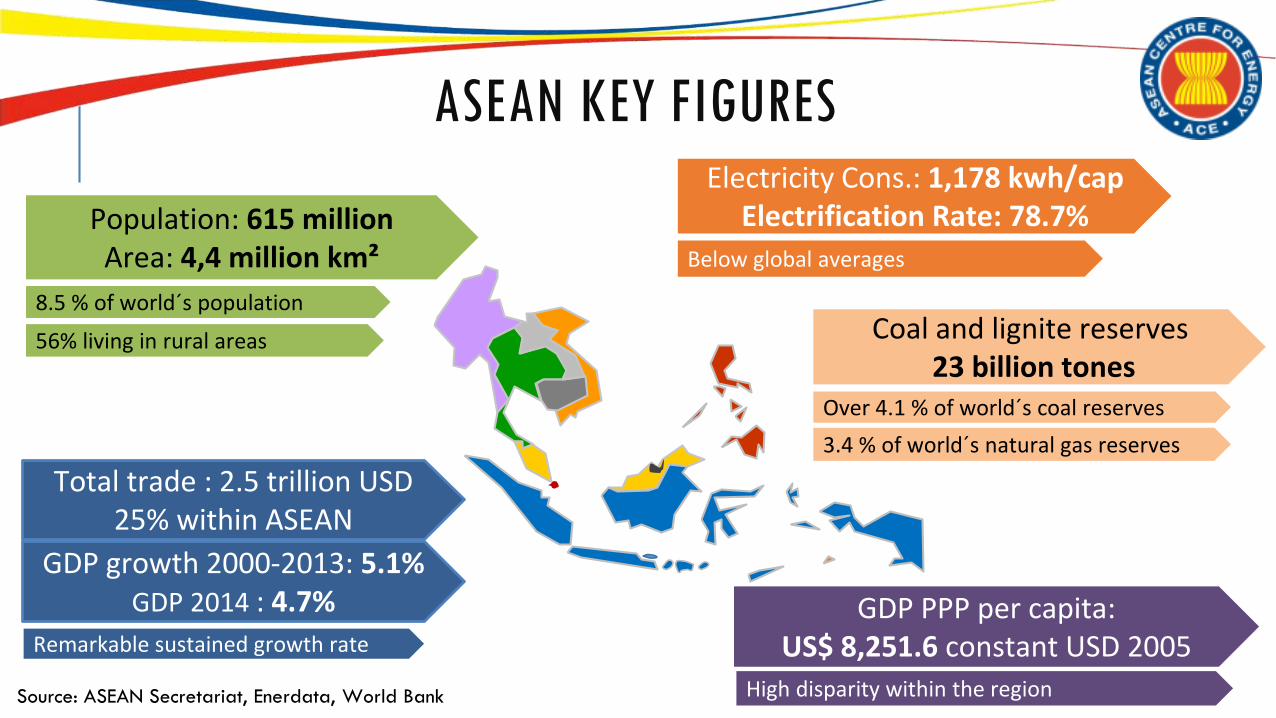

ASEAN KEY FIGURES

GDP growth 2000-2013: 5.1%GDP 2014 : 4.7%

Remarkable sustained growth rate

GDP PPP per capita:US$ 8,251.6 constant USD 2005

High disparity within the region

Electricity Cons.: 1,178 kwh/capElectrification Rate: 78.7%

Below global averages

Coal and lignite reserves23 billion tones

Over 4.1 % of world´s coal reserves

3.4 % of world´s natural gas reserves

Population: 615 millionArea: 4,4 million km²

8.5 % of world´s population

56% living in rural areas

Total trade : 2.5 trillion USD25% within ASEAN

Source: ASEAN Secretariat, Enerdata, World Bank

RENEWABLE ENERGY DEVELOPMENT IN ASEAN

5

REGIONAL COMMITMENTS

ASEAN Plan of Actions for Energy Cooperation (APAEC) 2010 - 2015

15%Share of Renewable Energy in the ASEAN

Installed Power Capacity by 2015

ASEAN Plan of Actions for Energy Cooperation (APAEC) 2016 - 2025

23% Share of Renewable Energy in the ASEAN

Energy Mix by 2025

“Enhancing Energy Connectivity and Market Integration in ASEAN to Achieve Energy Security, Accessibility, Affordability and Sustainability for All”

AMS COMMITMENTS IN RE

7

10% RE share in power generation by 2035

More than 2 GW of hydropower in 2020

23% NRE share of total energy consumption in 2025

30% RE share of total energy consumptions by 2025

34% RE share in installed capacity, 13% RE share in power generation in 2050

15 GW installed capacity in 2030

350 MW installed capacity of solar by 2020

25% AE share in total energy consumption by 2021

15% - 20% RE share in installed capacity by 2030

6% RE share in power generation in 2030

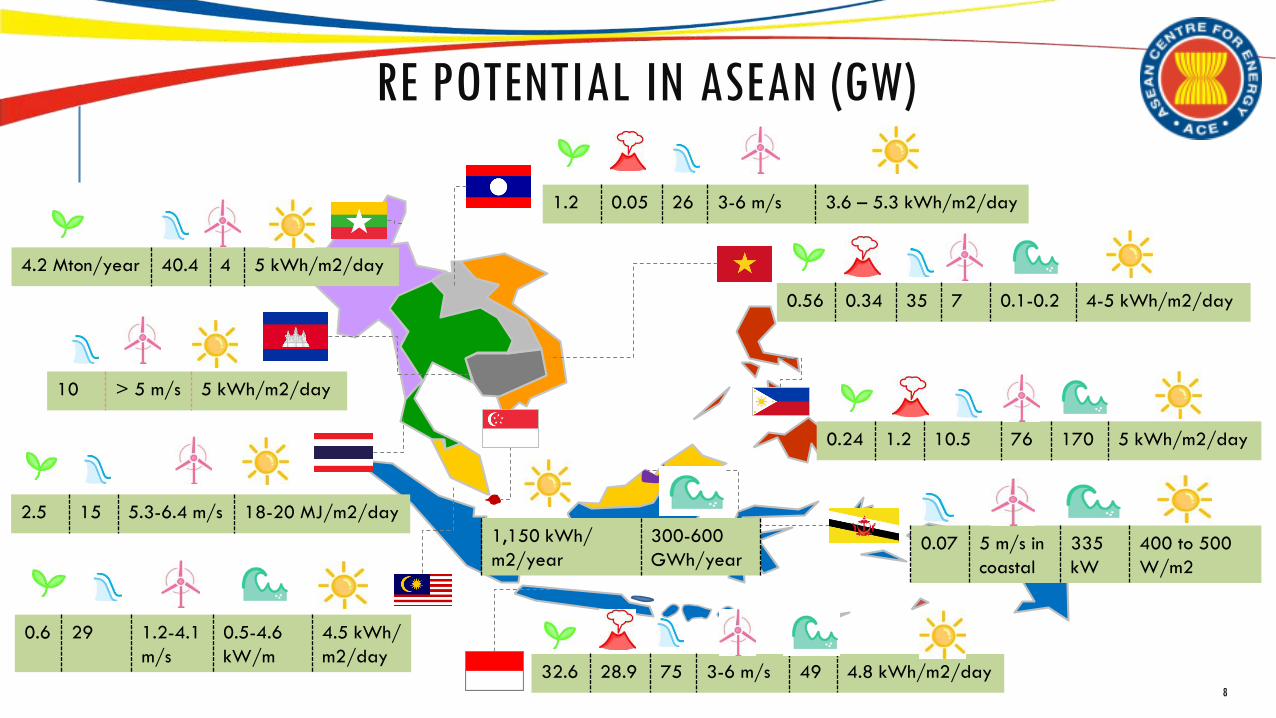

RE POTENTIAL IN ASEAN (GW)

32.6 28.9 75 3-6 m/s 49 4.8 kWh/m2/day

0.24 1.2 10.5 76 170 5 kWh/m2/day

0.56 0.34 35 7 0.1-0.2 4-5 kWh/m2/day

1.2 0.05 26 3-6 m/s 3.6 – 5.3 kWh/m2/day

0.6 29 1.2-4.1

m/s

0.5-4.6

kW/m

4.5 kWh/

m2/day

2.5 15 5.3-6.4 m/s 18-20 MJ/m2/day

10 > 5 m/s 5 kWh/m2/day

4.2 Mton/year 40.4 4 5 kWh/m2/day

0.07 5 m/s in

coastal

335

kW

400 to 500

W/m2

1,150 kWh/

m2/year

300-600

GWh/year

8

ASEAN INSTALLED CAPACITY AND GENERATION (2013)

Installed Power Capacity for Renewable Energy :

45,584.9 MW

Sources : ACE Database, as of 2013.*Others : Biogas and waste

Renewable Energy24.8%

Non-renewable

Energy75.2%

184,068 MW

Renewable Energy20.6%

Non-renewable

Energy79.4%

820,834GWh

Power Generation for Renewable Energy

169,073 GWh

9

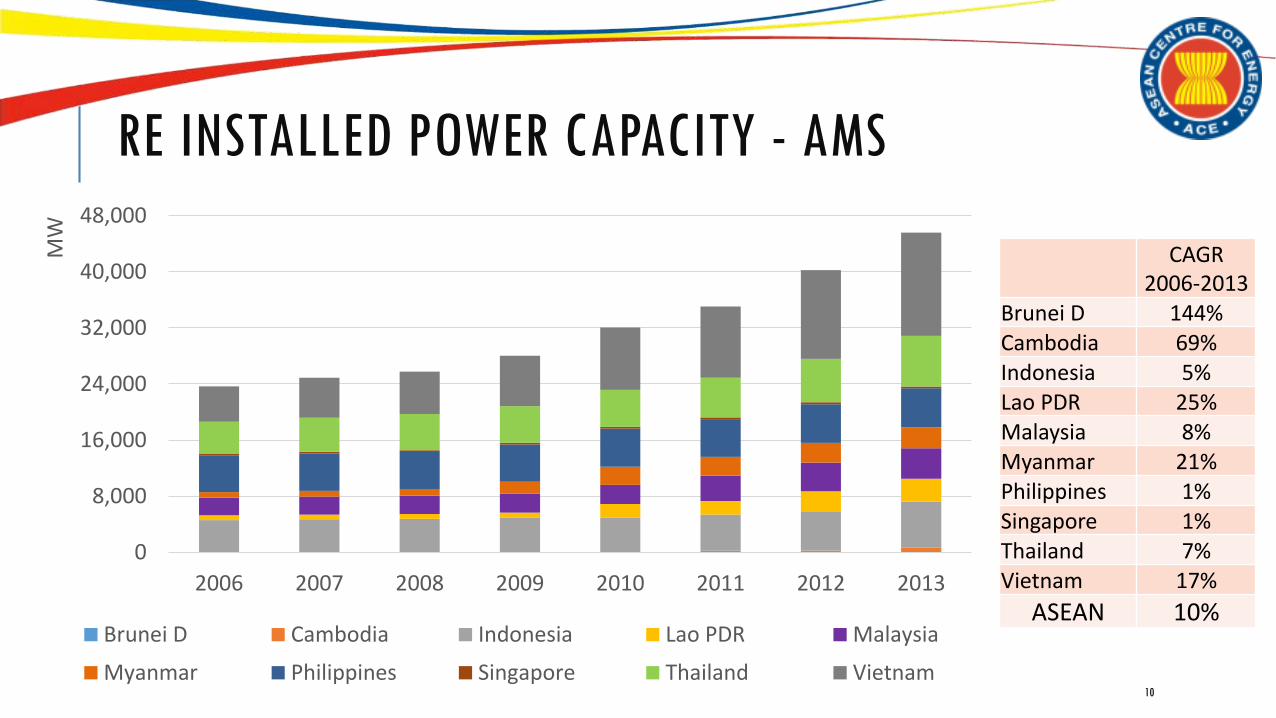

RE INSTALLED POWER CAPACITY - AMS

10

0

8,000

16,000

24,000

32,000

40,000

48,000

2006 2007 2008 2009 2010 2011 2012 2013

MW

Brunei D Cambodia Indonesia Lao PDR Malaysia

Myanmar Philippines Singapore Thailand Vietnam

CAGR 2006-2013

Brunei D 144%Cambodia 69%Indonesia 5%Lao PDR 25%Malaysia 8%Myanmar 21%Philippines 1%Singapore 1%Thailand 7%Vietnam 17%

ASEAN 10%

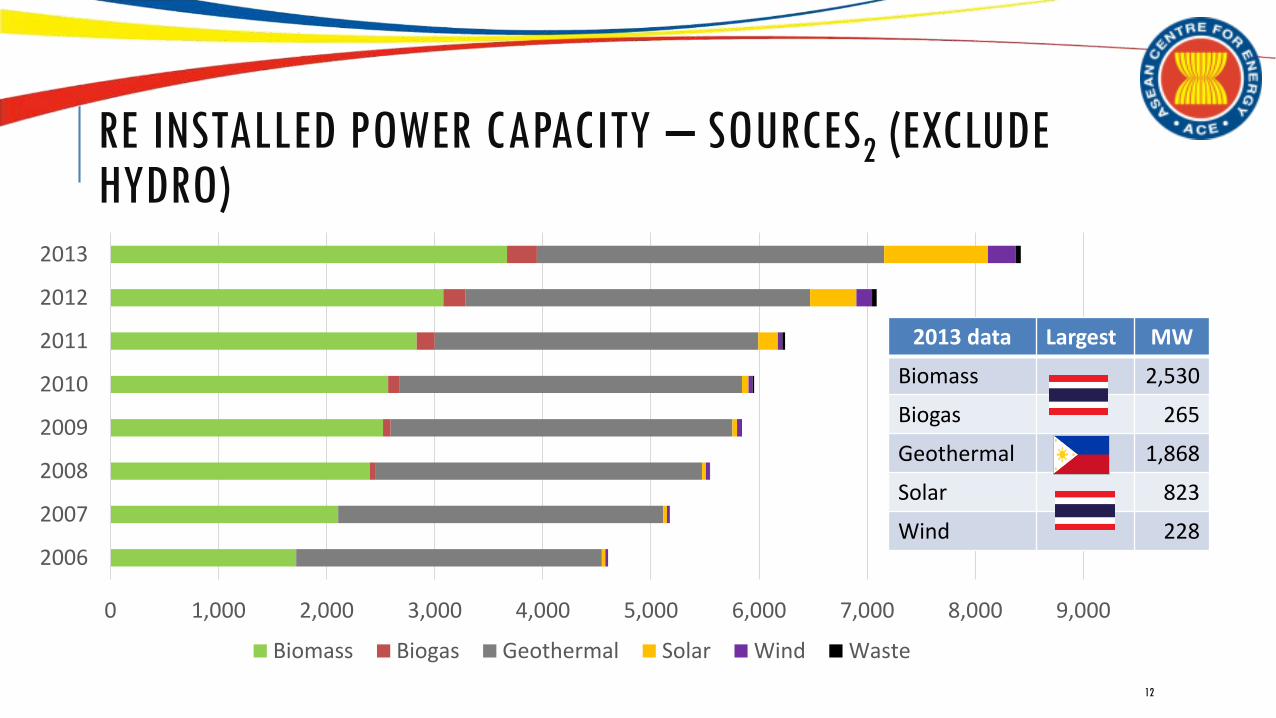

RE INSTALLED POWER CAPACITY – SOURCES1

11

0

10,000

20,000

30,000

40,000

50,000

2006 2007 2008 2009 2010 2011 2012 2013

MW

Biomass Biogas Geothermal Solar Wind Hydro Waste

RE SourcesCAGR

2006-2013Biomass 11 %Biogas 102 %

Geothermal 2 %Solar 62 %Wind 39 %Hydro 10 %ASEAN 10 %

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

2006

2007

2008

2009

2010

2011

2012

2013

Biomass Biogas Geothermal Solar Wind Waste

2013 data Largest MW

Biomass 2,530

Biogas 265

Geothermal 1,868

Solar 823

Wind 228

RE INSTALLED POWER CAPACITY – SOURCES2 (EXCLUDE HYDRO)

12

-

2,000

4,000

6,000

8,000

10,000

2007 2008 2009 2010 2011 2012 2013

MW

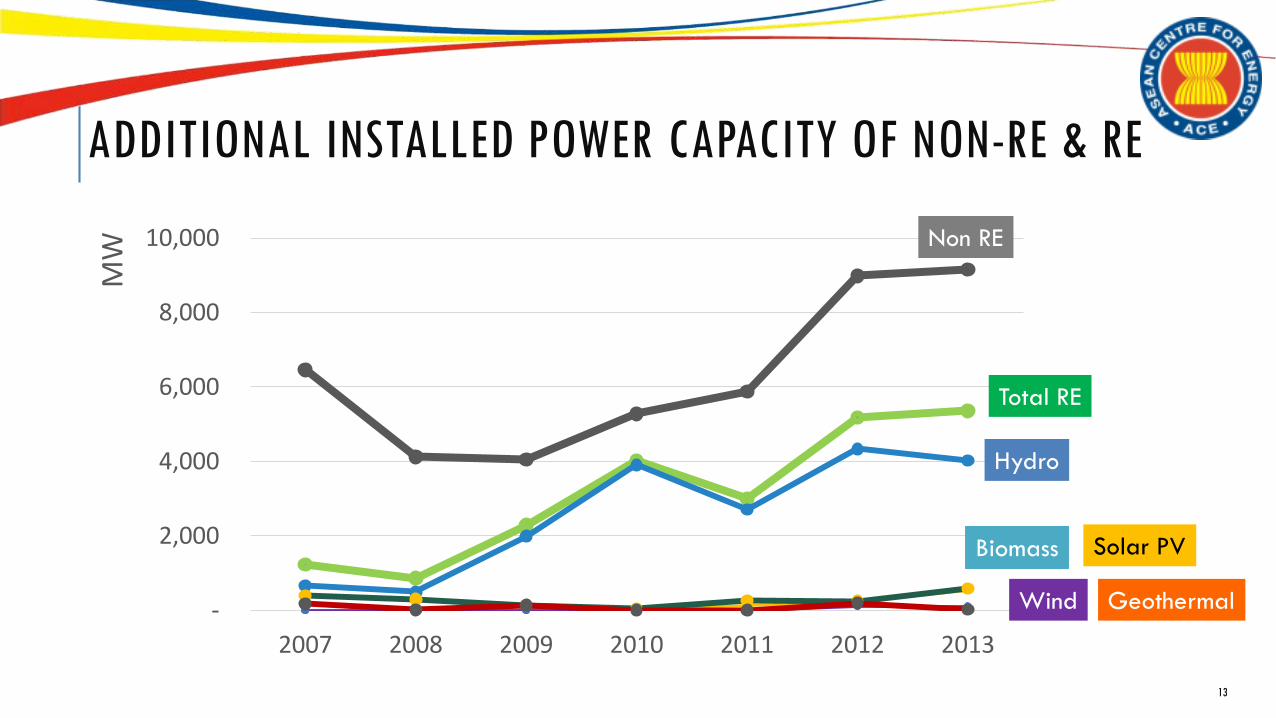

ADDITIONAL INSTALLED POWER CAPACITY OF NON-RE & RE

Non RE

Total RE

Hydro

Biomass Solar PV

Wind Geothermal

13

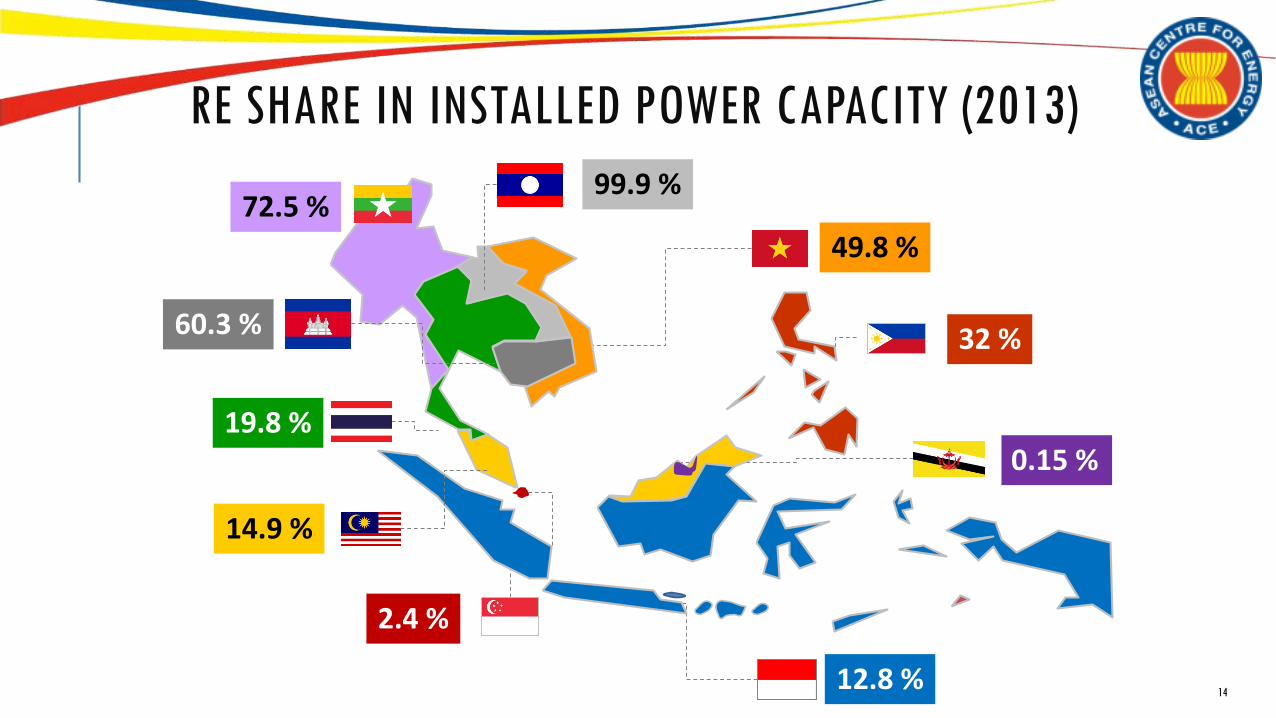

RE SHARE IN INSTALLED POWER CAPACITY (2013)

14

0.15 %

32 %

49.8 %

99.9 %72.5 %

60.3 %

19.8 %

14.9 %

2.4 %

12.8 %

CURRENT STATUS ON RE POLICIESCountry RE Target Feed in Tariff

RE Financing/

Incentives

Brunei 10% RE share in Power Generation by 2035 No No

Cambodia More than 2 GW of hydropower by 2020 No Yes

Indonesia 23% NRE share in total energy consumption in 2025 Yes Yes

Lao PDR 30% RE share of total energy consumptions by 2025 No Yes

Malaysia 34% RE share in installed capacity, 13% RE share in power generation in 2050

Yes Yes

Myanmar 15% - 20% RE share in installed capacity by 2030 No No

Philippines 15 GW installed capacity in 2030 Yes Yes

Singapore 350 MW installed capacity of solar by 2020 Net-settlement No

Thailand 25% AE share in total energy consumption by 2021 Yes Yes

Vietnam 6% RE share in power generation in 2030 Yes Yes15

FEED-IN-TARIFF FOR RE IN ASEAN

0

5

10

15

20

25

30

Cent

/kW

h

8.5

3 P

HP

6.6

3 P

HP

9.6

8 P

HP

5.9

0 P

HP

0.7 RM

0.24 RM

0.92 RM

0.27 RM

0.32 RM

4.5 THB

3.5 THB

0.3 THB

0.5 THB1.5 THB

0.8 THB

3.5 THB

3.5 THB

MSW

7.8 US

cent5.8 US

cent7.28

US cent

10.05

US cent

MSW

1,050 IDR

1,500 IDR

750 IDR

2.032 IDR

25 US cent

30 US cent

16

FiT for Solar

PV is being

reviewed

FiT for wind is

being

reviewed

4TH ASEAN ENERGY OUTLOOK (AEO4)

17

THE 4TH ASEAN ENERGY OUTLOOK (4AEO)

Controlled approachFraunhofer developed a regional model to countercheck and discuss findings

Cooperative ApproachNational ASEAN officials developed country projections and included knowledge on national policies and projections

Harmonized approachThe ASEAN Centre for Energy (ACE) and Fraunhofer guided country representatives in the development of national models

www.aseanenergy.org

4AEO SCENARIOS

Both scenarios based on AMS socio-economic and policy framework assumptions

Advancing Policies Scenario (APS)

Successful implementation of stronger policies as defined by the AMS’ official targets for renewable

energy and energy efficiency.

Business as Usual Scenario (BAU)

Continuation of past developments while taking into consideration

future changes in activities driving energy consumption

KEY FINDINGS: TPES

-

150

300

450

600

750

900

1,050

1,200

1,350

1,500

1,650

1,800

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Mto

e

Historical BAU APS

1,468 Mtoe

1,685 Mtoe

BAU ( CAGR)– 4.7 %

APS ( CAGR)– 4.0 %

BAU APSCoal 7.0% 5.3%Oil 2.7% 2.7%Natural gas 5.5% 3.3%Renewables 5.3% 7.4%

Year BAU APS2013 10.2% 10.2%2020 10.6% 15.4%2035 11.2% 20.0%

GAGR 2013 - 2035

RE % mix of TPES

TPES (2013~2035) increases by:

BAU - 272%

APS - 237%) Coal is expected to have the highest increase,

overshadowing oil with 33% share

Higher efficiency standards in the transformation sector, demand side management, and deployment of RE are the key factors in APS

KEY FINDINGS: POWER GENERATION - BAU VS APS

21

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2013 2020 2025 2030 2035 2013 2020 2025 2030 2035

TWh

Coal Oil Natural gas Nuclear Hydro Geothermal Other Renewables

BAU APS

In 2035:

BAU of electricity generation reaches 2,883 TWh; while in APS reaches 2,473 TWh.

Both in BAU and APS, coal share is expected to significantly grow to 55% and 45% respectively.

Renewable Energy is predicted to reach 399 TWh in BAU; and 548 TWh in APS

RE Potential still mainly untapped. Gas/oil/coal reserves intensively deployed

KEY FINDINGS: INSTALLED POWER CAP. - BAU VS APS

22

-

100

200

300

400

500

600

700

2013 2015 2020 2025 2030 2035 2013 2015 2020 2025 2030 2035

GW

Coal Oil Natural Gas Nuclear Hydro Geothermal Other Renewables

In 2035:

Installed power cap. will reach around 607 GW in; while in APS reaches 588 GW.

Renewable Energy is predicted to reach 149 GW in BAU; and 156 GW in APS

BAU APS

CLOSER LOOK ON RE INSTALLED POWER CAPACITY

The share of biomass, wind and solar increases strongly in APS Hydro share to shrink and geothermal share stable

0

30

60

90

120

150

180

2013 2025BAU

2025APS

2035BAU

2035APS

GW

0%

20%

40%

60%

80%

100%

2013 2025BAU

2025APS

2035BAU

2035APS

Share of RE Technologies

Biomass

Hydro

Wind

Solar

Geothermal

RENEWABLE ENERGY FINANCING

24

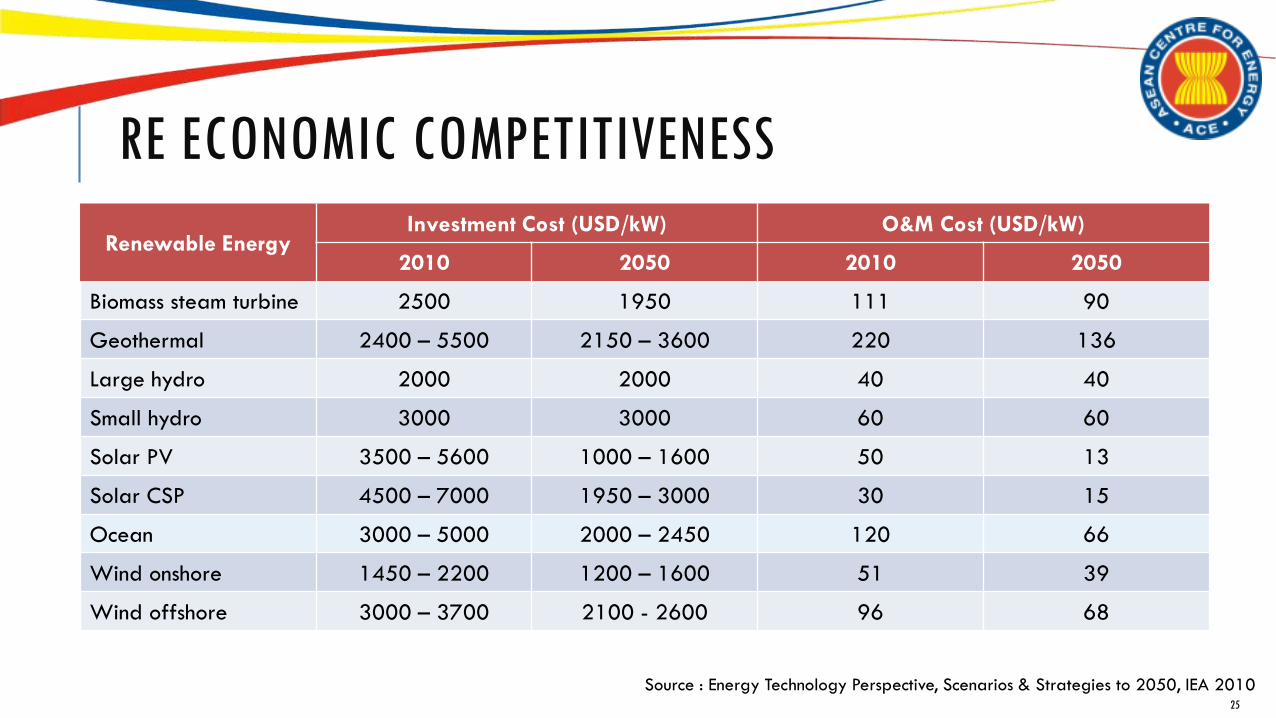

RE ECONOMIC COMPETITIVENESS

Renewable EnergyInvestment Cost (USD/kW) O&M Cost (USD/kW)

2010 2050 2010 2050

Biomass steam turbine 2500 1950 111 90

Geothermal 2400 – 5500 2150 – 3600 220 136

Large hydro 2000 2000 40 40

Small hydro 3000 3000 60 60

Solar PV 3500 – 5600 1000 – 1600 50 13

Solar CSP 4500 – 7000 1950 – 3000 30 15

Ocean 3000 – 5000 2000 – 2450 120 66

Wind onshore 1450 – 2200 1200 – 1600 51 39

Wind offshore 3000 – 3700 2100 - 2600 96 68

Source : Energy Technology Perspective, Scenarios & Strategies to 2050, IEA 201025

LCOE FOR RENEWABLE ENERGY

0

10

20

30

40

50

60

70

US C

ent

/kW

h

1

2

3

4

5

26

Source : 1. IRENA. Renewable Power Generation Costs. 20122. SI Ocean, Ocean Energy: Cost of Energy and Cost Reduction Opportunities, 20133. Doshi, et.al, The Economics of Solar PV in Singapore. 2013

4. GIZ-GDE/MOIT 2014. Summary of Studies on Supporting Mechanism for Grid-connected Bioenergy Power in Viet Nam. 2014

5. NREL and DOE 2013. Simple LCOE Calculator Documentation

LANDSCAPE FOR RE PROJECTS

Renewable Energy Project

Project Developer

Govern-mental

Institution

Local Community

Power Utilities

Financial Institutions

Security of energy supply

No negative impacts

Poverty alleviation

Job creationStable power networks

Economical viability, profitable

and sustainable

CHALLENGES IN RE DEPLOYMENT

b. Non Technical Issues• Complex and time-consuming procedures

• Difficult to get external financing

• Feasibility study is not bankable

• Lack of reference RE projects

• Reliable supply of the fuel (e.g. biomass or biogas power plant)

a. Technical Issues• Unavailable of data for preliminary assessment

• Have knowledge, but still lack of know-how in the project development

• Skill and reliability of technical consultant who develop the project

• Locating the grid connection point,

• Scale or size of the project does matter, etc

• Bad previous experiences with failed RE project / bad track record

• Necessary document cannot be provided in the early phase

• Power utility has a final decision (go-no go for RE project)

• Environmental issues, etc

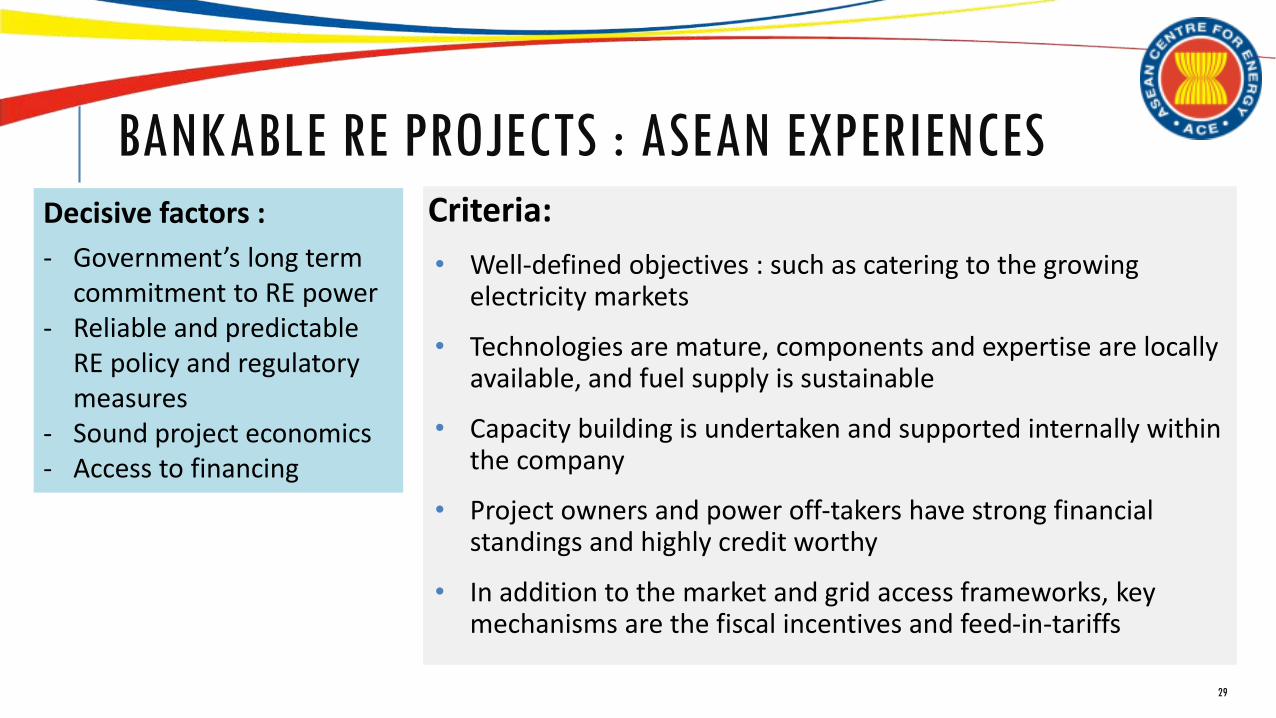

BANKABLE RE PROJECTS : ASEAN EXPERIENCES Criteria:

• Well-defined objectives : such as catering to the growing electricity markets

• Technologies are mature, components and expertise are locally available, and fuel supply is sustainable

• Capacity building is undertaken and supported internally within the company

• Project owners and power off-takers have strong financial standings and highly credit worthy

• In addition to the market and grid access frameworks, key mechanisms are the fiscal incentives and feed-in-tariffs

Decisive factors :

- Government’s long term commitment to RE power

- Reliable and predictable RE policy and regulatory measures

- Sound project economics- Access to financing

29

RENEWABLE ENERGY FINANCING IN ASEAN

ACE, under Renewable Energy Support Programme for ASEAN (RESP) has been conducting Renewable Energy Lending Guidelines for Bankers in ASEAN : Thailand, Philippines, Indonesia and Malaysia

The focus of the workshop:• Technology and Design: Key technologies and technology-related

risks, certification and guarantees-related risks, civil design risks, and electrical design risks;

• Plant Performance: Robust resource prediction, energy yield modelling considerations, uncertainty and probability scenarios, and plant operation risks;

• Contracts and Costs: PPA risks, construction contracting risks, operation contracting risks, construction and operation cost, etc.

30

RE PERMIT PROCEDURES

Key items discussed: Administrative procedures including requirements for project developers and/or investors, Legal and regulatory provisions and necessary permit, country specific challenges for project

development, information on how to obtain financial closure

Biomass and Biogas

Power Project

Development in Indonesia

Large Solar Photovoltaic

Project Development in

the Philippines

Small Solar Photovoltaic

Project Development in the

Philippines

31

Next Year:

Malaysia : Solar PV

&

Vietnam : Biomass

http://re-guidelines.info/

WAY FORWARD

32

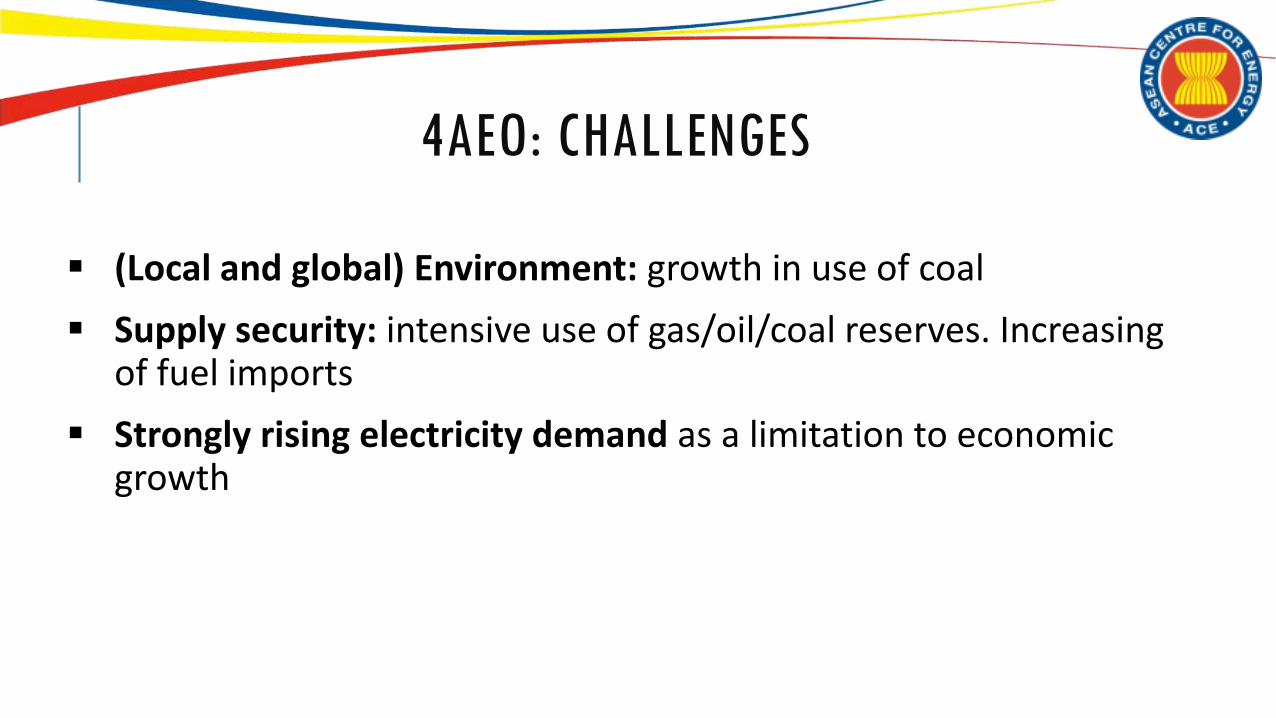

4AEO: CHALLENGES

(Local and global) Environment: growth in use of coal

Supply security: intensive use of gas/oil/coal reserves. Increasing of fuel imports

Strongly rising electricity demand as a limitation to economic growth

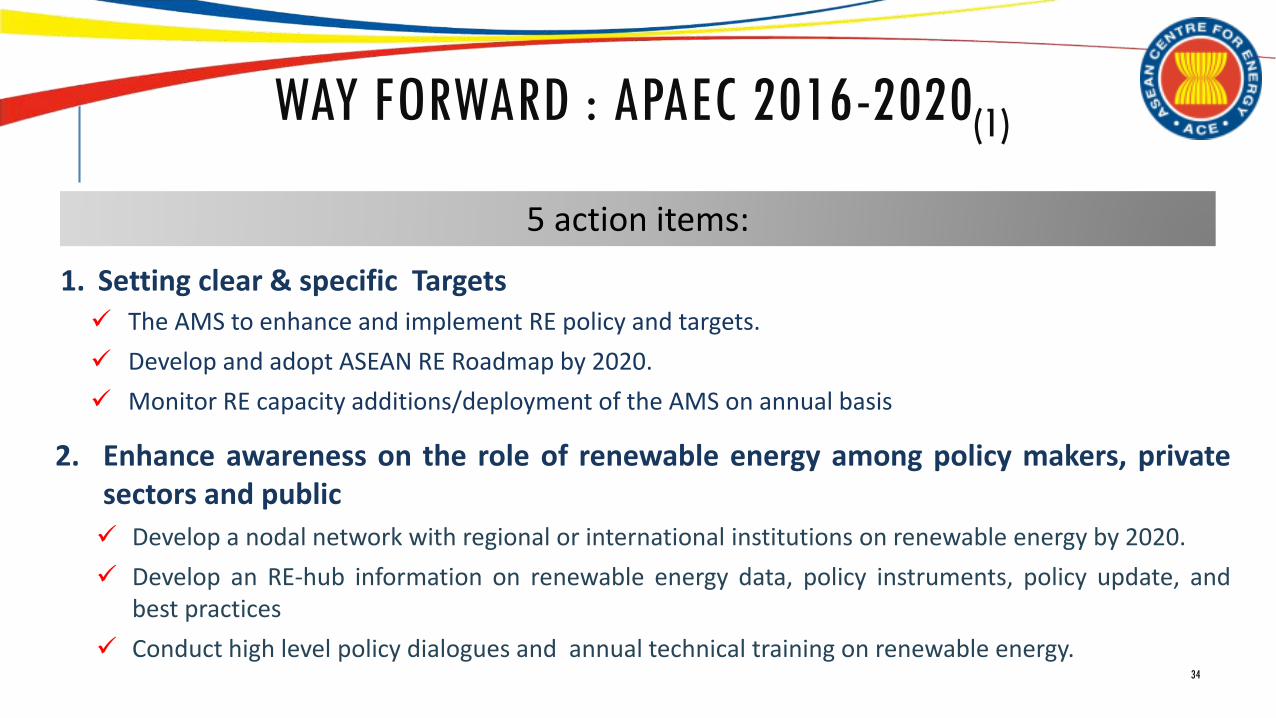

WAY FORWARD : APAEC 2016-2020(1)

34

5 action items:

1. Setting clear & specific Targets The AMS to enhance and implement RE policy and targets.

Develop and adopt ASEAN RE Roadmap by 2020.

Monitor RE capacity additions/deployment of the AMS on annual basis

2. Enhance awareness on the role of renewable energy among policy makers, privatesectors and public

Develop a nodal network with regional or international institutions on renewable energy by 2020.

Develop an RE-hub information on renewable energy data, policy instruments, policy update, andbest practices

Conduct high level policy dialogues and annual technical training on renewable energy.

3. Enhance R&D network on RE technology development and utilisation within the region.

Establish a nodal network with at least minimum two (2) research institutions or universities to promote cooperation,

technology development, sharing of research facilities and exchange and mobility of researchers on renewable by

2020.

4. Increase the promotion of renewable energy financing scheme

Establish a nodal network with at least two (2) national / regional / international financial institutions for

renewable energy financing.

Develop a guideline of RE Support Mechanism for Bankable Projects.

Conduct regular training on renewable energy financing.

5. Increase the commercial development and utilization of biofuels with a reference standard to facilitate deployment.

Develop a nodal network with automotive and related industries on technological know-how and R&D activities

for biofuel.

Conduct market studies to fully determine the commercial potential of bioenergy.35

WAY FORWARD : APAEC 2016-2020(2)