Regulatory Dimensions to Renewable Energy Integration: A U ... · twinning with regulators at CERC...

23

Regulatory Dimensions to Renewable Energy Integration in India: A U.S. Perspective 1st International Conference on Grid Integration of Renewable Energy Delhi, India September 6 th , 2017 Lakshmi Alagappan Director, E3

Transcript of Regulatory Dimensions to Renewable Energy Integration: A U ... · twinning with regulators at CERC...

Regulatory Dimensions to Renewable Energy Integration in India:

A U.S. Perspective

1st International Conference on Grid Integration of Renewable Energy

Delhi, India

September 6th, 2017

Lakshmi Alagappan Director, E3

About Energy and Environmental Economics, Inc. (E3)

Consumer Advocates Environmental

Interests Energy Consumers

State Agencies Regulatory Authorities

State Executive Branches Legislators

Utilities System Operators

Financial Institutions

Project Developers Technology Companies

Asset Owners Financiers/Investors

Founded in 1989, E3 is an industry leading consultancy in North America with a growing international presence

E3 operates at the nexus of energy, environment and economics

Our team employs a unique combination of economic analysis, modeling acumen, and deep institutional insight to solve complex problems and provide critical thought leadership for a diverse client base

2

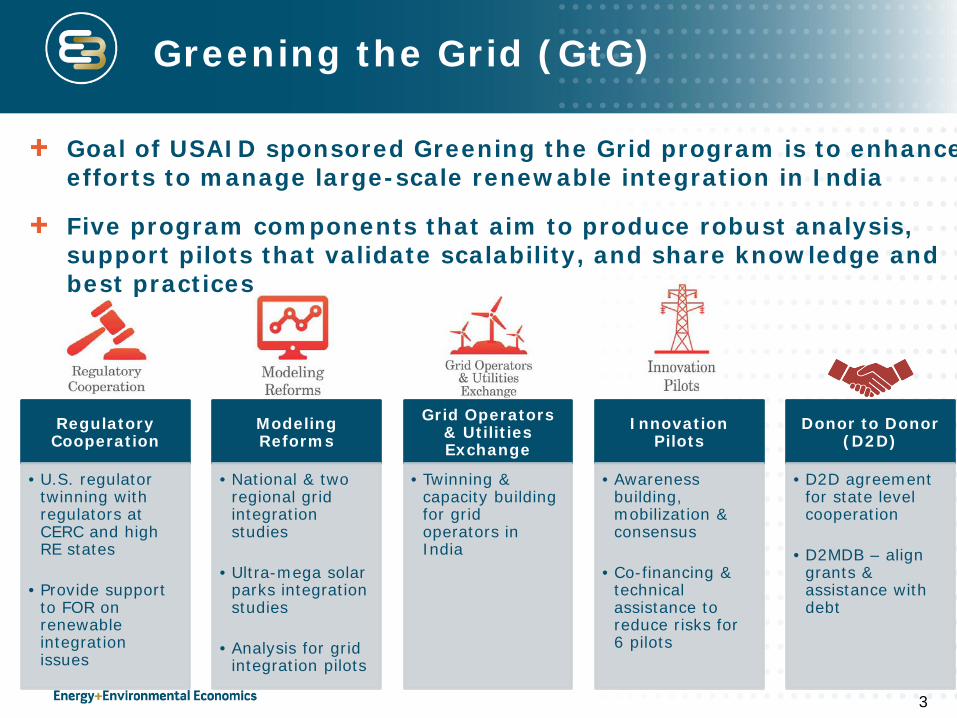

Greening the Grid (GtG)

Goal of USAID sponsored Greening the Grid program is to enhance efforts to manage large-scale renewable integration in India

Five program components that aim to produce robust analysis, support pilots that validate scalability, and share knowledge and best practices

Regulatory Cooperation

• U.S. regulator twinning with regulators at CERC and high RE states

• Provide support to FOR on renewable integration issues

Modeling Reforms

• National & two regional grid integration studies

• Ultra-mega solar parks integration studies

• Analysis for grid integration pilots

Grid Operators & Utilities Exchange

• Twinning & capacity building for grid operators in India

Innovation Pilots

• Awareness building, mobilization & consensus

• Co-financing & technical assistance to reduce risks for 6 pilots

Donor to Donor (D2D)

• D2D agreement for state level cooperation

• D2MDB – align grants & assistance with debt

3

Regulatory Cooperation

• U.S. regulator twinning with regulators at CERC and high RE states

• Provide support to FOR on renewable integration issues

Modeling Reforms

• National & two regional grid integration studies

• Ultra-mega solar parks integration studies

• Analysis for grid integration pilots

Grid Operators & Utilities Exchange

• Twinning & capacity building for grid operators in India

Innovation Pilots

• Awareness building, mobilization & consensus

• Co-financing & technical assistance to reduce risks for 6 pilots

Donor to Donor (D2D)

• D2D agreement for state level cooperation

• D2MDB – align grants & assistance with debt

4

Greening the Grid (GtG)

Goal of USAID sponsored Greening the Grid program is to enhance efforts to manage large-scale renewable integration in India

Five program components that aim to produce robust analysis, support pilots that validate scalability, and share knowledge and best practices

Focus of today’s

presentation

Project Overview

The National Association of Regulatory Utility Commissioners (NARUC), USAID’s regulatory partner for GtG, engaged E3 and RAP, to identify potential regulatory solutions to help inform more efficient power system operations in India • Focus on market design and imbalance mechanisms • Focus on integration of renewables • Draw from U.S. experience and Indian field research

Four components • Review of regulation and practice in India • Review of U.S. experience • Exchanges of both Indian and U.S. regulators • Mapping of U.S. experience to Indian context

(ongoing) Year 1 work culminated with publication of “Regulatory Dimensions to Renewable Energy Forecasting, Scheduling, and Balancing in India: Regulatory Practices Analysis and Primer” in March 2017 • Link:

http://pdf.usaid.gov/pdf_docs/PA00MNH3.pdf 5

Scale of the Renewable Integration Challenge in India

In 2015, the Government of India set a target of 175 GW of renewable energy nationwide by 2022

As of early 2016, Tamil Nadu and Rajasthan (case study states) ranked first and second, respectively, in installed capacity of renewables in India

Western and Southern regional grids account for more than 90% of existing (February 2016) renewable generation capacity and more than 75% of anticipated solar and wind capacity additions by 2022

This concentration of solar and wind resources implies that, for renewable energy to become a larger part of India’s national power mix, integration is key to enabling power delivery across states and regions

Source: Existing renewable capacity data are from MoP and CEA (2016). Expected solar and wind data are from MNRE, “Tentative State-wise break-up of Renewable Power target to be achieved by the year 2022 So that cumulative achievement is 1,75,000 MW,” http://mnre.gov.in/file-manager/UserFiles/Tentative-State-wise-break-up-of-Renewable-Power-by-2022.pdf. See document for links to other references.

Existing (January 2016) Renewable Generation Capacity and New Solar and Wind Generation Capacity

Anticipated by 2022 for India’s Five Grid Regions

6

Review of Indian Regulations and Practices

Project focused on interstate and intrastate regulatory frameworks for renewable integration

Comprehensive review of current and draft regulations at interstate and intrastate level, supplemented by field research at both the Central level and the state level in Tamil Nadu and Rajasthan

• Central Level: Central Electricity Regulatory Commission (CERC), Ministry of Power (MoP), Power System Operation Company (POSOCO), National Thermal Power Corporation (NTPC), Central Electricity Authority (CEA)

• Rajasthan: Rajasthan Electricity Regulatory Commission (RERC), Rajasthan State Load Dispatch Center (RSLDC), Rajasthan Rajya Vidyut Utpadan Nigam Limited (RUVN, discom coordinator)

• Tamil Nadu: Tamil Nadu Electricity Regulatory Commission (TNERC), Tamil Nadu State Load Dispatch Center (TNSLDC), Tamil Nadu Generation and Distribution Corporation (TANGEDCO, discom)

• Others: Gujarat State Load Dispatch Center (GSLDC), Gujarat State Electricity Commission (GERC) National Institute of Wind Energy (NIWE), Indian Wind Power Association (IWPA), Suzlon (wind developer), Indian Energy Exchange (IEX)

7

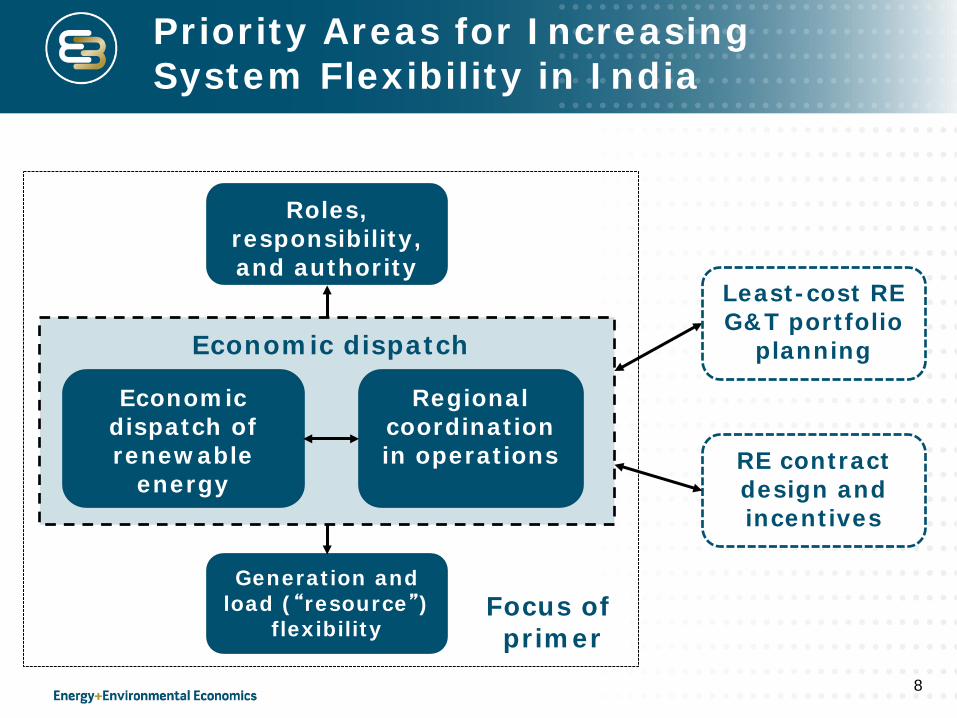

Roles, responsibility, and authority

Economic dispatch of renewable

energy

Regional coordination in operations

Economic dispatch

Generation and load (“resource”)

flexibility

Least-cost RE G&T portfolio

planning

RE contract design and incentives

Focus of primer

Priority Areas for Increasing System Flexibility in India

8

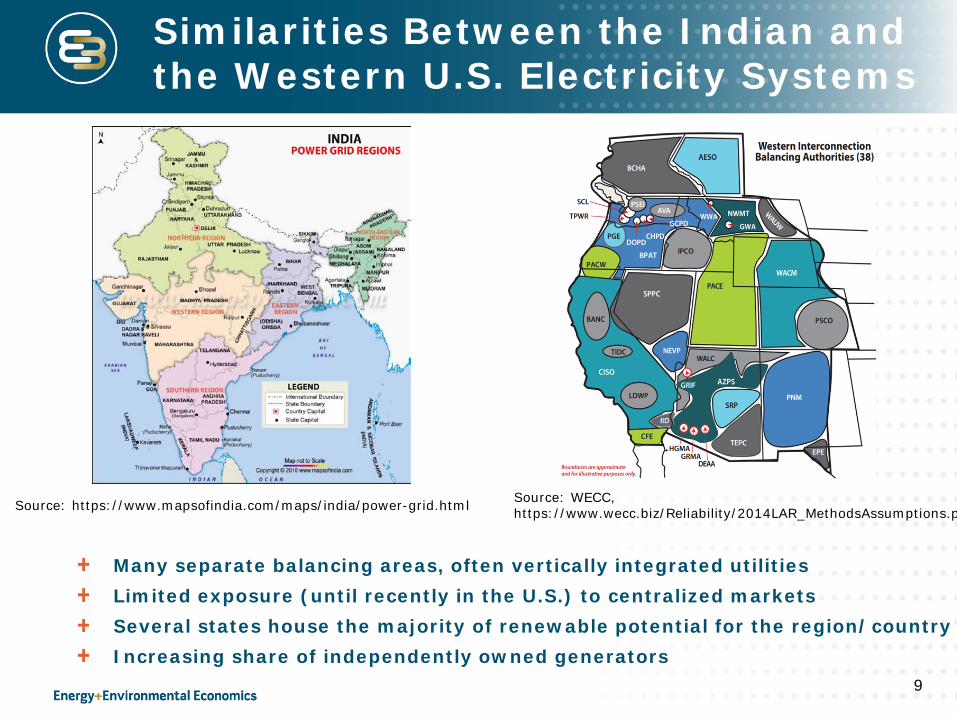

Similarities Between the Indian and the Western U.S. Electricity Systems

Many separate balancing areas, often vertically integrated utilities Limited exposure (until recently in the U.S.) to centralized markets Several states house the majority of renewable potential for the region/country Increasing share of independently owned generators

9

Source: https://www.mapsofindia.com/maps/india/power-grid.html Source: WECC, https://www.wecc.biz/Reliability/2014LAR_MethodsAssumptions.p

Renewable Energy Integration in the Western U.S.

RE development anticipated to have major impacts on system operations throughout the Western U.S.

10

Previous Efforts at Market Reforms in the Western U.S. Have Been Unsuccessful

Numerous Previous Attempts at Market Reform in the West

• IndeGO, RTO West, Grid West, Desert Star, Northwest SCED, CCED

What is different this time?

• Changing grid dynamics and needs (High RPS, GHG policies)

• New leadership (e.g., Mid-American/Berkshire)

• Markets now have a track record of reasonable success

• SPP market seen as providing benefits in a region where utilities remain vertically integrated

• Low-cost, low-risk options to participate

11

Non-RTO, mostly vertically

integrated utilities

Source: FERC, http://sustainableferc.org/iso-rto-operating-regions/

U.S. Case Studies: CAISO, PacifiCorp, PSCo

PacifiCorp Vertically integrated, multi-state utility covering parts of California, Idaho, Oregon, Utah, Washington, Wyoming; now part of CAISO’s Western EIM; owned by Berkshire Hathaway Energy

California ISO (CAISO) Predominantly state-based ISO; “hybrid” market, with resource adequacy overseen by the CPUC, a day-ahead and real-time market overseen by CAISO, and limited retail choice (IOUs serve most load)

Public Service Company (PSCo) Vertically integrated utility in Colorado; owned by Xcel Energy

12

Important Developments in Case Study Areas

Moving toward much higher penetrations of RE • CAISO – 50% by 2030, potentially 100% by 2045 • PacifiCorp (Oregon) – 50% by 2040 • PSCo – 30% by 2020

Transitioning to new regional markets • CAISO and PacifiCorp create Western EIM • PSCo creates joint dispatch service with

neighboring utilities • Outside of CAISO, vertically integrated utilities

operate monopolies under FERC access rules

13

Key Priority Areas & Research Questions

Enabling economic dispatch • Why is it important for supporting RE?

• How do policies, contract terms, open access regulations, and market design shape the economic dispatch of RE?

Enabling greater regional coordination • How do operations differ between a vertically integrated utility without

access to centralized markets and regional coordination models?

• What is the value proposition of regional coordination? What were the key benefits of regional coordination in the Western U.S.?

Increasing resource flexibility • What is driving the need for increased flexibility in power systems?

• What can we learn from coal plant cycling experience in the U.S.?

• How will demand-side programs need to evolve in their design in response to electric systems with higher penetrations of renewables?

Clarifying roles, responsibilities, and authority • Where does the division of jurisdiction exist between central and state

regulators?

• Who is responsible for forecasting, scheduling, and balancing under different market structures?

• Why did the roles, responsibilities, and authority for various entities develop the way they did in the U.S.?

14

Market Transitions Energy imbalance market (EIM) and joint dispatch service (JDS) are prominent examples of market transition in the U.S.

Market transition is a learning process • Market designs in the

U.S. are bottom-up and always evolve

• Utilities often have to learn how to use the market

Also provides learning opportunities for an external audience

The Energy Imbalance Market (EIM) is a bid-based real-time market that will cover at least 12 utilities and the CAISO by 2019. Created by PacifiCorp and CAISO in 2014, the EIM is an intrahour balancing market; it does not directly affect utilities’ day-ahead or hour-ahead scheduling

Joint Dispatch Service (JDS) is a cost-based imbalance market covering three utilities in Colorado that was approved in 2016 and is set to become operational. JDS is also an intrahour balancing market and does not affect day- or hour-ahead scheduling

Market Transitions

15

Comparison: BAU Practice vs. JDS and EIM

Item BAU Practice Under JDS or

EIM Sub-hourly Transactions

Very few bilateral transactions

Automated through JDS or EIM

Dispatch and balancing

Manual dispatch for each of 38 individual BAs

Security-constrained economic dispatch over footprint

Transmission utilization

May leave within hour capacity unused

Utilizes unused within hour transmission capacity

Flexibility reserves

Each BA holds reserves to meet expected within hour changes

Fluctuations netted across BAs requiring fewer reserves

Hour ahead scheduling & trading

No change

Reserves: Regulation (<5min) & Contingency

No change

Transmission & Gen Capacity Planning

No change

16

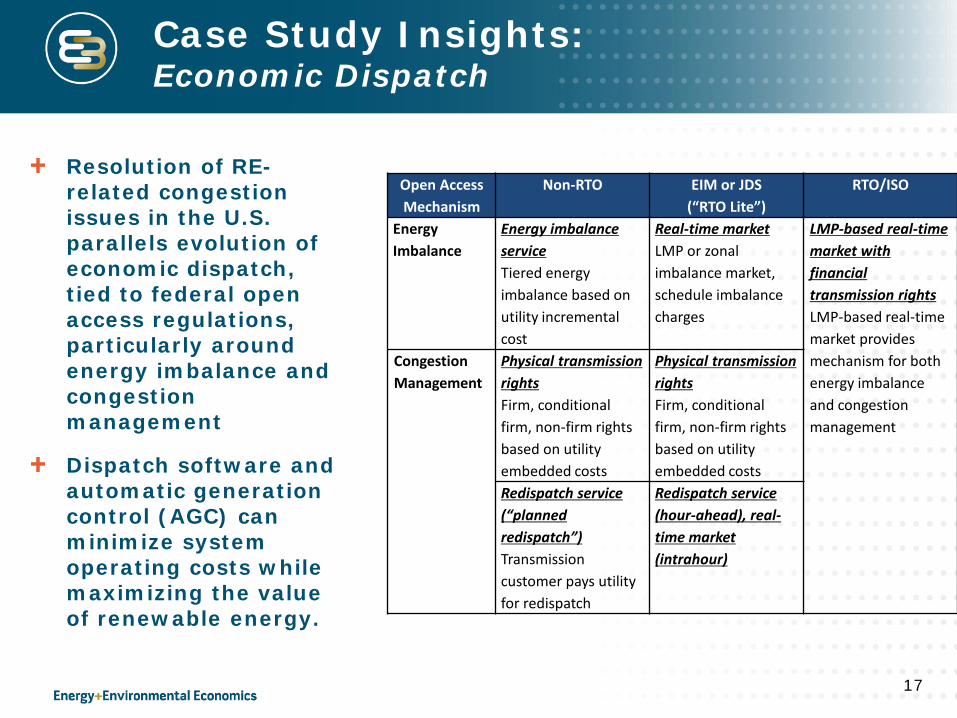

Case Study Insights: Economic Dispatch

Resolution of RE-related congestion issues in the U.S. parallels evolution of economic dispatch, tied to federal open access regulations, particularly around energy imbalance and congestion management

Dispatch software and automatic generation control (AGC) can minimize system operating costs while maximizing the value of renewable energy.

17

Open Access Mechanism

Non-RTO EIM or JDS (“RTO Lite”)

RTO/ISO

Energy Imbalance

Energy imbalance service Tiered energy imbalance based on utility incremental cost

Real-time market LMP or zonal imbalance market, schedule imbalance charges

LMP-based real-time market with financial transmission rights LMP-based real-time market provides mechanism for both energy imbalance and congestion management

Congestion Management

Physical transmission rights Firm, conditional firm, non-firm rights based on utility embedded costs

Physical transmission rights Firm, conditional firm, non-firm rights based on utility embedded costs

Redispatch service (“planned redispatch”) Transmission customer pays utility for redispatch

Redispatch service (hour-ahead), real-time market (intrahour)

Case Study Insights: Regional Coordination

Multiple approaches to centralized regional balancing are possible

Broad stakeholder engagement and clear value propositions are important for creating consensus

Regional balancing can be a low-cost, low-risk step toward deeper regional coordination efforts

Ex-post verification of expected benefits helps create trust in market

18

Most EIM participants conducted a benefits assessment prior to joining the EIM to better understand the value it provides to its system.

Case Study Insights: Increasing Resource Flexibility

EIM and JDS create price signals for resources to evaluate operational changes to harness flexibility

• PacifiCorp found that showing the financial implications of certain operational patterns to coal plant operators, operators were more likely to think creatively on how to improve processes to increase plant flexibility and profitability

19

Figure shows operation of coal units under “inflexible” (left hand side) and “flexible” (right hand side) assumptions in the WECC Flexibility Study. More flexible operation of coal units reduces wind and solar curtailment.

Market transitions lead to a need to clarify roles, responsibilities, and authority for various responsibilities

As the level of regional coordination increases, the more utilities cede their authority in forecasting, scheduling, and balancing to the market operator

Governance principles define matters which market operators do and do not have jurisdiction over

Nature and timing of transition depends on extent new market can leverage existing governance structures, software and institutional knowledge of markets

20

Case Study Insights: Roles, Responsibilities, and Authority

Next Steps

Regulatory primer was the first step in trying to map relevant U.S. experience to the rapidly evolving Indian electricity sector

Next steps may include:

• Regulatory and market guidelines document which provides short-term and medium-term milestones on renewable integration issues, challenges, and facilitative market structures

• Continued partnerships and exchanges with CERC and SERCs on renewable integration issues

21

Regulatory Exchange – Aug. 2016

22

Thank You!

Lakshmi Alagappan, Director ([email protected])

Energy and Environmental Economics, Inc. (E3) 101 Montgomery Street, Suite 1600 San Francisco, CA 94104 Tel 415-391-5100 http://www.ethree.com