Recent Actions Announced by RF Government for Fighting Use of Off-shores.

38

Recent Actions Announced by RF Government for Fighting Use of Off-shores

-

Upload

cindy-plank -

Category

Documents

-

view

220 -

download

1

Transcript of Recent Actions Announced by RF Government for Fighting Use of Off-shores.

Recent Actions Announced by RF Government for Fighting Use of Off-shores

Main Reasons for Fighting Off-shores

Tightening of State Control over Foreign Element in Economy

Political will is aimed at tightening the regulations on the use and benefits of offshore SPVs

Foreign investments and re-investment of domestic capital held in offshore vehicles are promoted

Moscow International Financial Center Project is not forgotten, there are measures aimed to improve investment climate

Amendments to Russian law are aimed to make it competitive compared to foreign laws (the major reform of Russian Civil Code is in progress)

Plans for moving up in the “Doing Business” rating

Discouraging of Offshore SPVs Use President’s Annual Speech to the Russian Parliament on December 12, 2012

implementation of which will continue in 2013-2014 years Goals: To cease capital outflows To make tax evasion more difficult To disclose beneficiaries Methods: Re-qualification of transactions and imposing tax implications Requirement to disclose beneficiaries in order to convey transactions Granting public authorities access to data constituting bank secrecy Introduction of Administrative liability for hard currency transactions performed

not through Russian banks in prescribed by law cases Wealth / sumptuary tax is introduced by Federal Law N 214-FZ dated July

23, 2013 coming into force from January 1, 2014 (tax rate on cars over RUB 3 million is increased).

Proposed CFC Legislation

Plans to Enter into Exchange of Information Agreements

Proposed CFC Legislation

The Russian Ministry of Finance is working on the draft tax law which would introduce concepts of CFC (Controlled Foreign Company) for tax purposes

Potentially, such new CFC rules may require Russian companies and individuals to report and account for profits of their CFCs even if no distributions are made

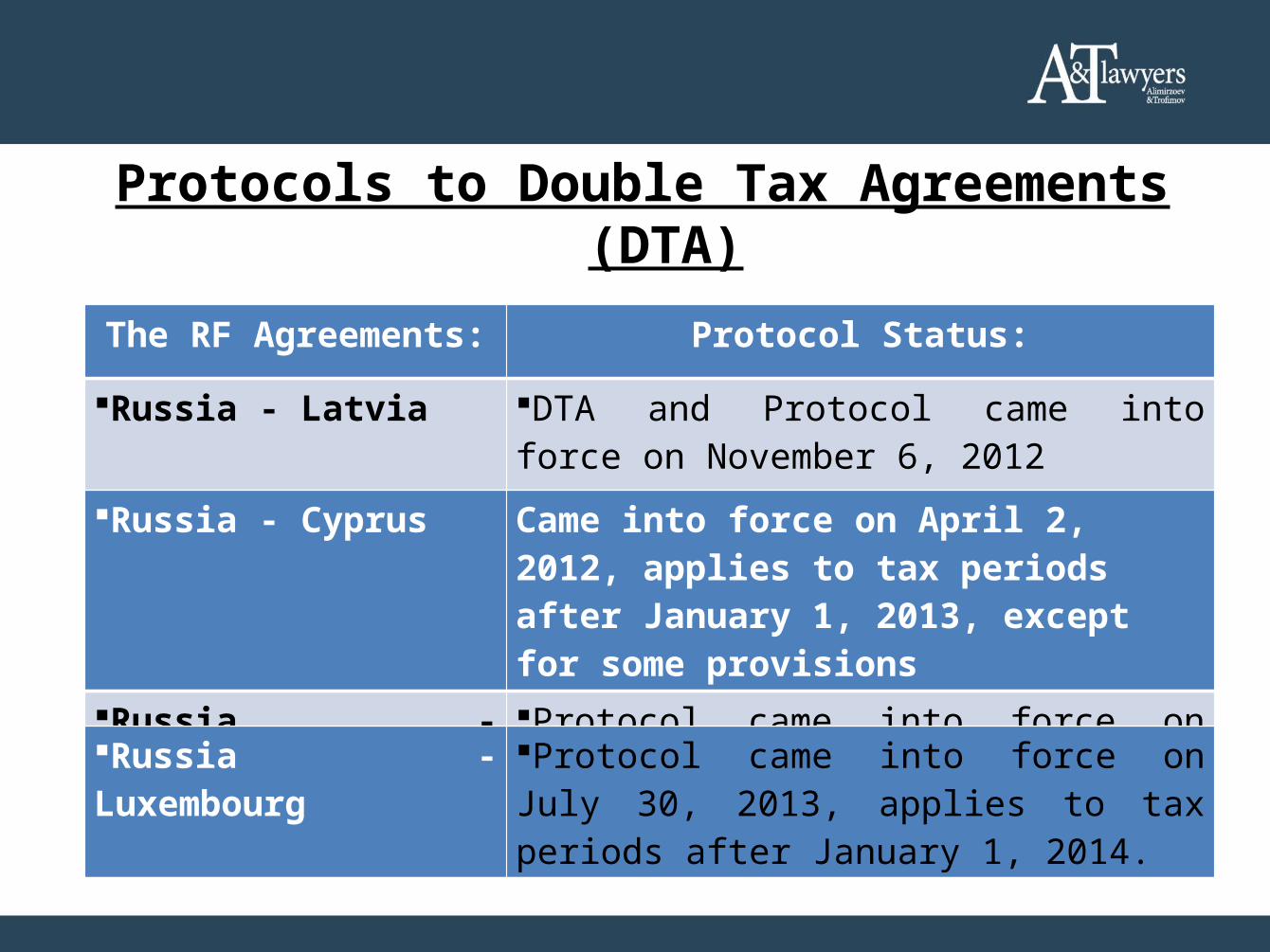

Protocols to Double Tax Agreements (DTA)

The RF Agreements: Protocol Status:

Russia - Latvia DTA and Protocol came into force on November 6, 2012

Russia - Cyprus Came into force on April 2, 2012, applies to tax periods after January 1, 2013, except for some provisions

Russia - Switzerland Protocol came into force on November 9, 2012

Russia - Luxembourg Protocol came into force on July 30, 2013, applies to tax periods after January 1, 2014.

Tax implications of Protocols to Double Tax Agreements

Sale of real estate in RF via transfer of corporate control in SPV

Rules on thin capitalization (Ruling of the Presidium of the Supreme Arbitration Court of the RF dated November 15, 2011 N 8654/11 in the OJSC “Ugolnaya companiya “Severniy Kuzbass” case)

Withholding of tax at source

Place of effective management

Information Exchange Provisions in Protocols to Double Tax Agreements

There are still no elaborated Russian rules, regulations and established practices on applying of Protocols for provisions on information exchange

First practical experiences after introduction of Protocol between the RF and Cyprus

Protocol between the RF and Switzerland: first practice of use.

Active Work of Department of Transfer Pricing and International Cooperation of RF Federal Tax Service

Exchange of Information Agreements with Offshore Jurisdictions

Agreements with Offshore Jurisdictions

With Dutch Antilles

(DTA with the Netherlands came into

force in 1989 )

With Malaysian Labuan

(DTA with Malaysia came into force in

1988)

Russia has two DTA with

“black” list offshore zones:

Judicial Doctrines on Ultimate Beneficial Owners

Disclosure

Removal of Corporate Veil

The earliest known attempt by Russian Courts to apply this concept is the dispute on injunction imposed over flat owned by Shalva Chigirinskiy’s spouse (Ruling of Federal Arbitration Court of Moscow region dated October 29, 2010 N KG-А40/14698-09-B-N)

Case on recognition of Parex Bank, Citadele Bank to be actually carrying out banking business in the RF via “conduit companies” (Ruling of the Presidium of the Supreme Arbitration Court of the RF № 16404/11 dated April 24, 2012)

Similar position was mentioned in dicta by the Court in OJSC “Ugolnaya companiya “Severniy Kuzbass” case – thin capitalization via “associated companies” (Ruling of the Presidium of the Supreme Arbitration Court of the RF dated November 15, 2011 N 8654/11)

Conclusion: As Russian Courts equip themselves with instruments to pierce the corporate veil, the Clients’ demand for better structuring will grow.

Offshore SPV claiming “bona fide purchaser” protection may be required to reveal it’s beneficiary

• Case facts: purchase of immovable property in favour of a company, beneficiaries of which are not known, is deemed to be suspicious (Ruling of the Supreme Arbitration Court of the RF dated January 9, 2013 N ВАС-14828/12)

• The Supreme Arbitration Court position: the burden of good faith proof lies with offshore; necessity of beneficiaries’ revealing (Ruling of the Supreme Arbitration Court of the RF dated January 9, 2013 N ВАС-14828/12)

• Supreme Arbitration Court mentioned in dicta, that offshore SPVs and anonymity they grant are often used in bad faith for asset stripping

• Side Remarks: After bombings in Domodedovo airport the state was unable to reveal true airport owners, stated plans for introducing of beneficiaries’ register

PEPs and Public Officers:Prohibitions and Restrictions

Federal Law No. 79-FZ of May 7, 2013

Came info force on May 19, 2013

Purposes:• Ensuring of RF national security• Regulating of lobbying activities• Promotion and expansion of investments in the national

economy• Improvement of anti-corruption effectiveness

Federal Law No. 79-FZ of May 7, 2013

Prohibits to open and have accounts (deposits), to keep cash and assets in foreign banks, to have and/or use securities of foreign issuers;

Defines persons in respect of which the prohibition is set (“target persons”);

Establishes procedure for verification of compliance of target persons with this prohibition;

Establishes penalties for its violation.

Key Persons Covered by Restrictions

State officials of the RF;

State officials of the RF sub-federal units (regions);

Officials in state legal entities, appointed and dismissed by RF President or Government;

Members of the Board of directors of the RF Central Bank

Officials of federal state service appointed and dismissed by RF President, Government or Chief State prosecutor

Others

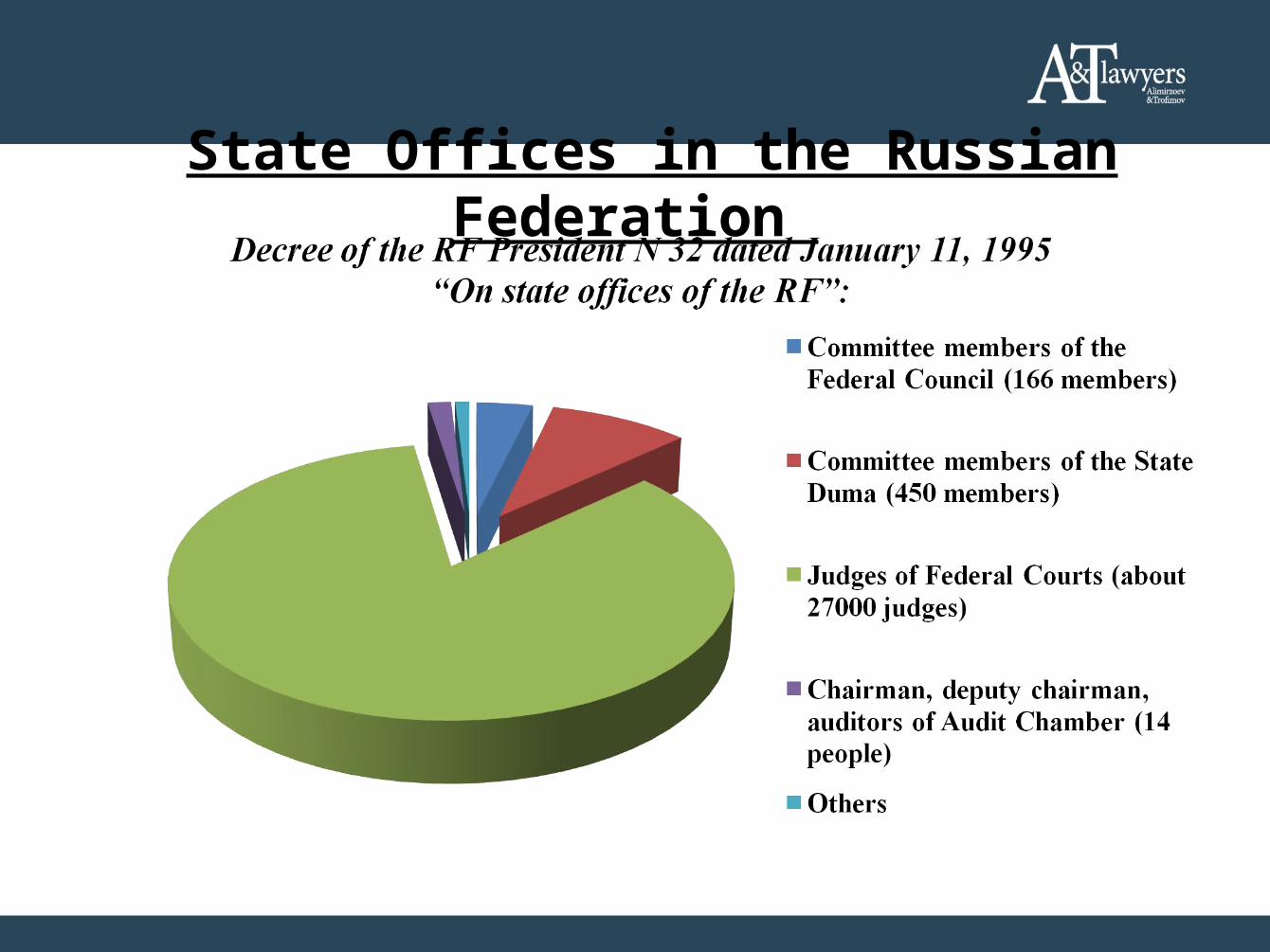

State Offices in the Russian Federation

State Offices in the RF Sub-federal Units

Decree of the RF President N 1381 dated December 4, 2009 “On standard state offices in the RF sub-federal units”

The 1st deputy and deputy director of the supreme executive body of

the RF sub-federal unit;Member of the supreme executive body of the RF sub-federal unit;Chairman of the legislative body

in the RF sub-federal unit and its deputies;Deputy of the legislative body in

the RF sub-federal unit;Chairmen of the Constitutional Court in the RF sub-federal unit, its deputy; Constitutional Court

judges;Chairman of Election Committee

in the RF sub-federal unit, its deputy, secretary, members with a

deciding vote;Chairman, deputy chairman ,

auditor of audit body in the RF sub-federal unit;Ombudsman in the RF sub-federal

unit;

Magistrates (7461 judges)

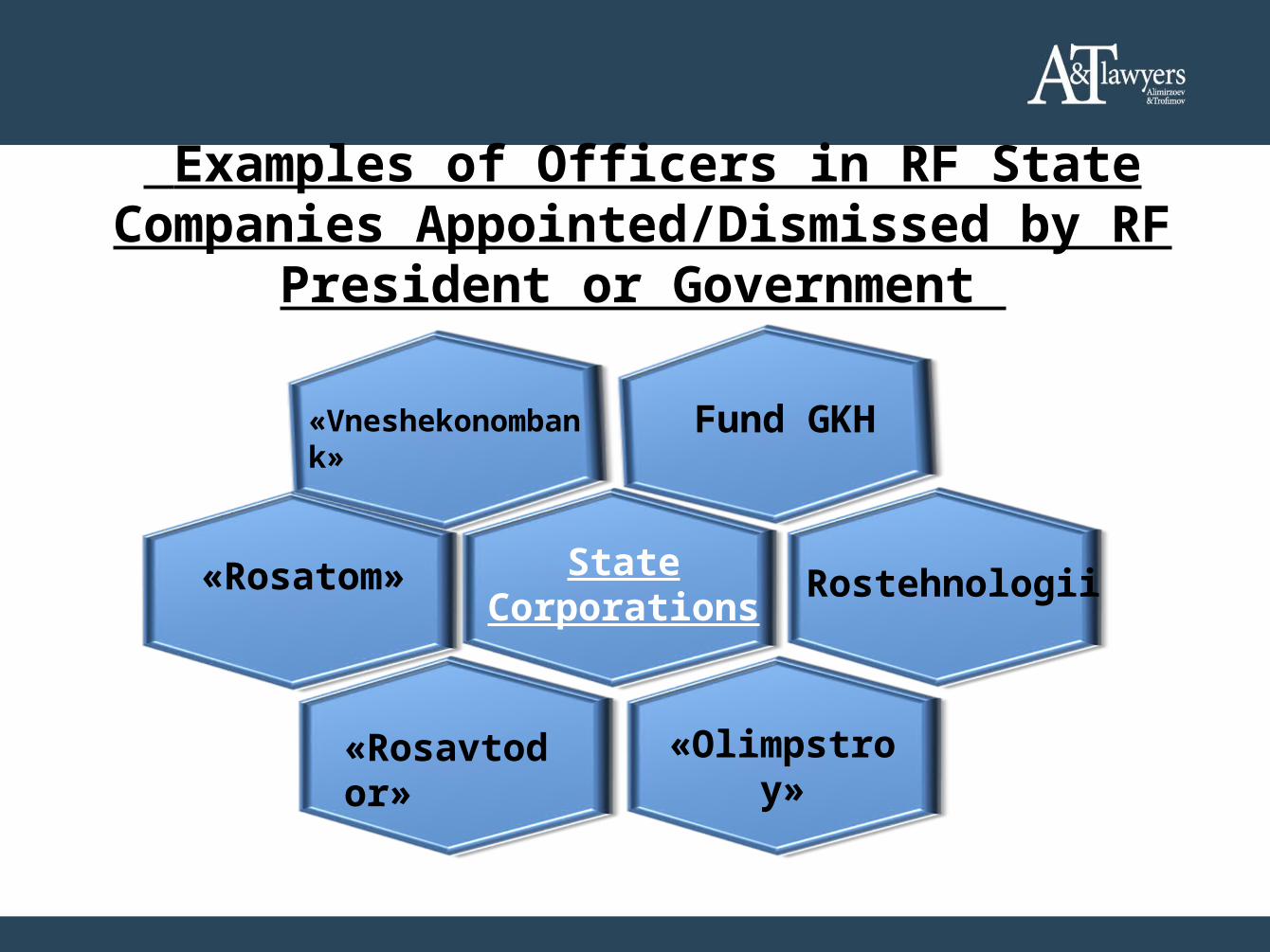

Examples of Officers in RF State Companies Appointed/Dismissed by RF President or Government

«Vneshekonombank»

«Rosatom» State Corporations

Fund GKH

«Rosavtodor» «Olimpstroy»

Rostehnologii

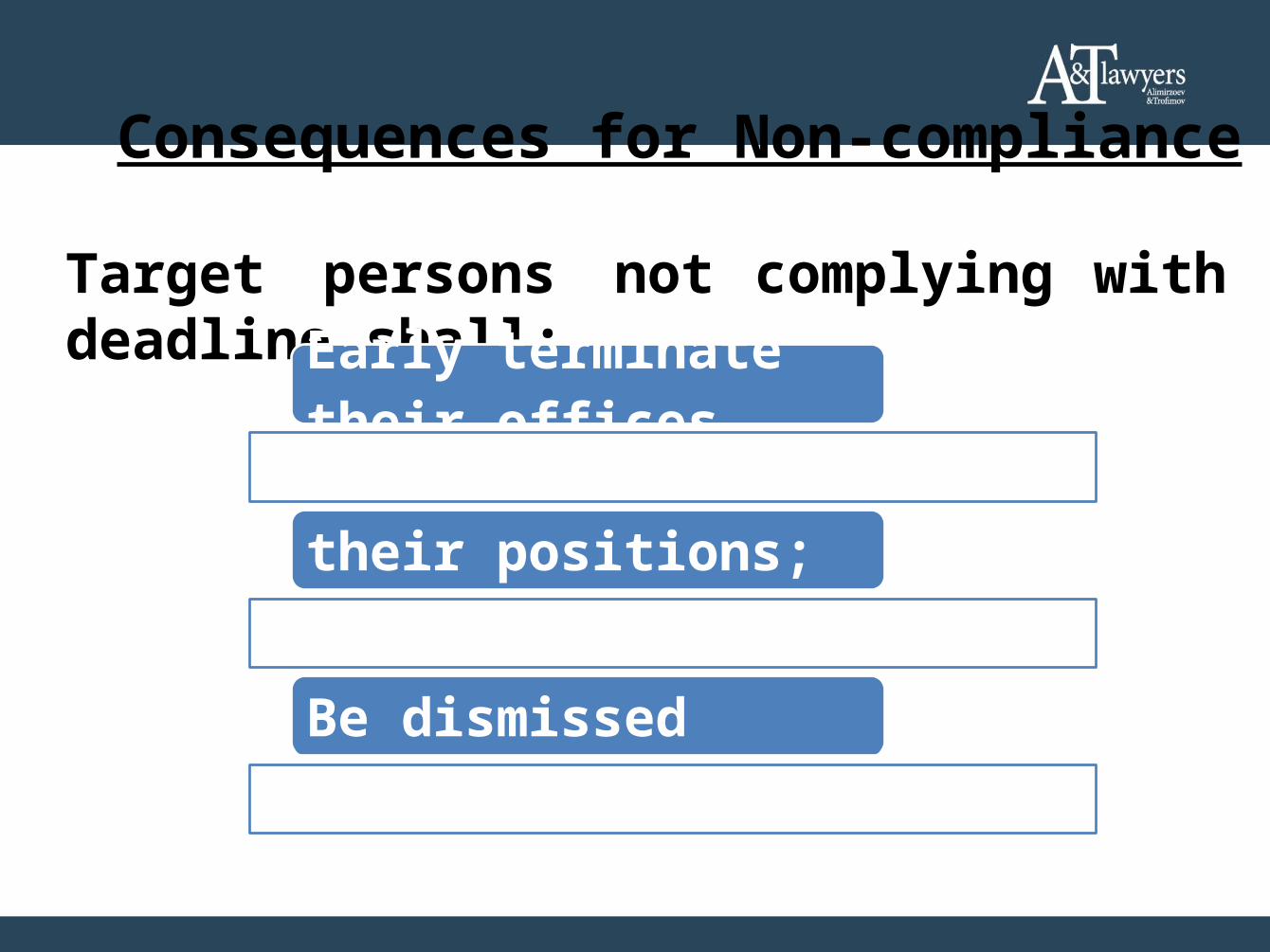

Consequences for Non-compliance

Target persons not complying with deadline shall:

Early terminate their offices

Be released from their positions; or

Be dismissed

Tax Returns on Property Abroad

Key restricted persons shall file reports listing:Real estate located abroad owned by them, their spouses and minor children;

Sources of funds on which such real estate was acquired;Their obligations abroad, as well as their spouses’ and minor children’s (mortgages, etc.).

Their accounts (deposits), cash and assets in foreign banks abroad as well as their spouses’ and minor children’s – only for citizens applying for state offices in the RF

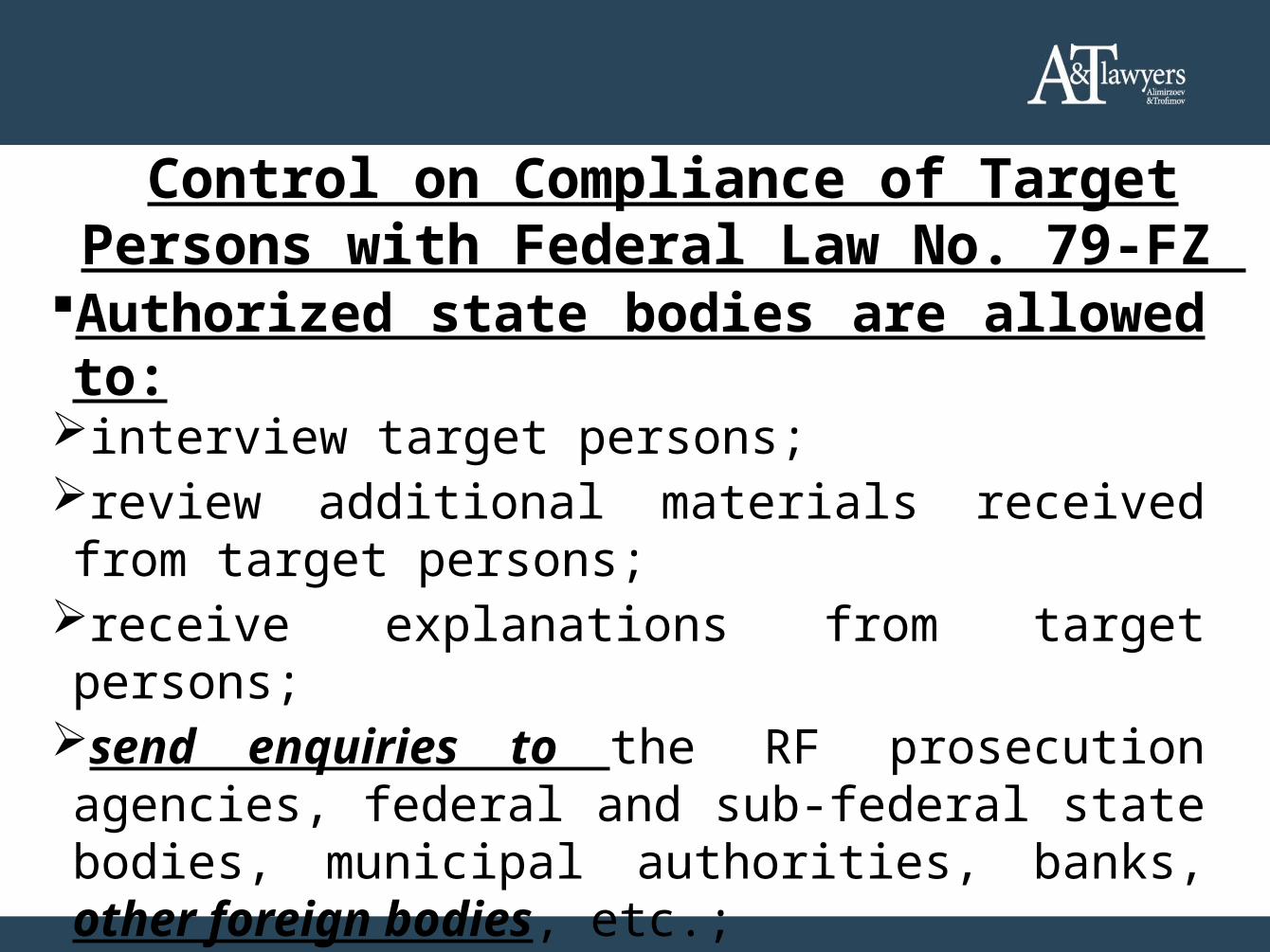

Control on Compliance of Target Persons with Federal Law No. 79-FZ

Authorized state bodies are allowed to:interview target persons;review additional materials received from target persons;receive explanations from target persons;send enquiries to the RF prosecution agencies, federal and sub-federal state bodies, municipal authorities, banks, other foreign bodies, etc.;

inquire individuals and receive information upon their consent

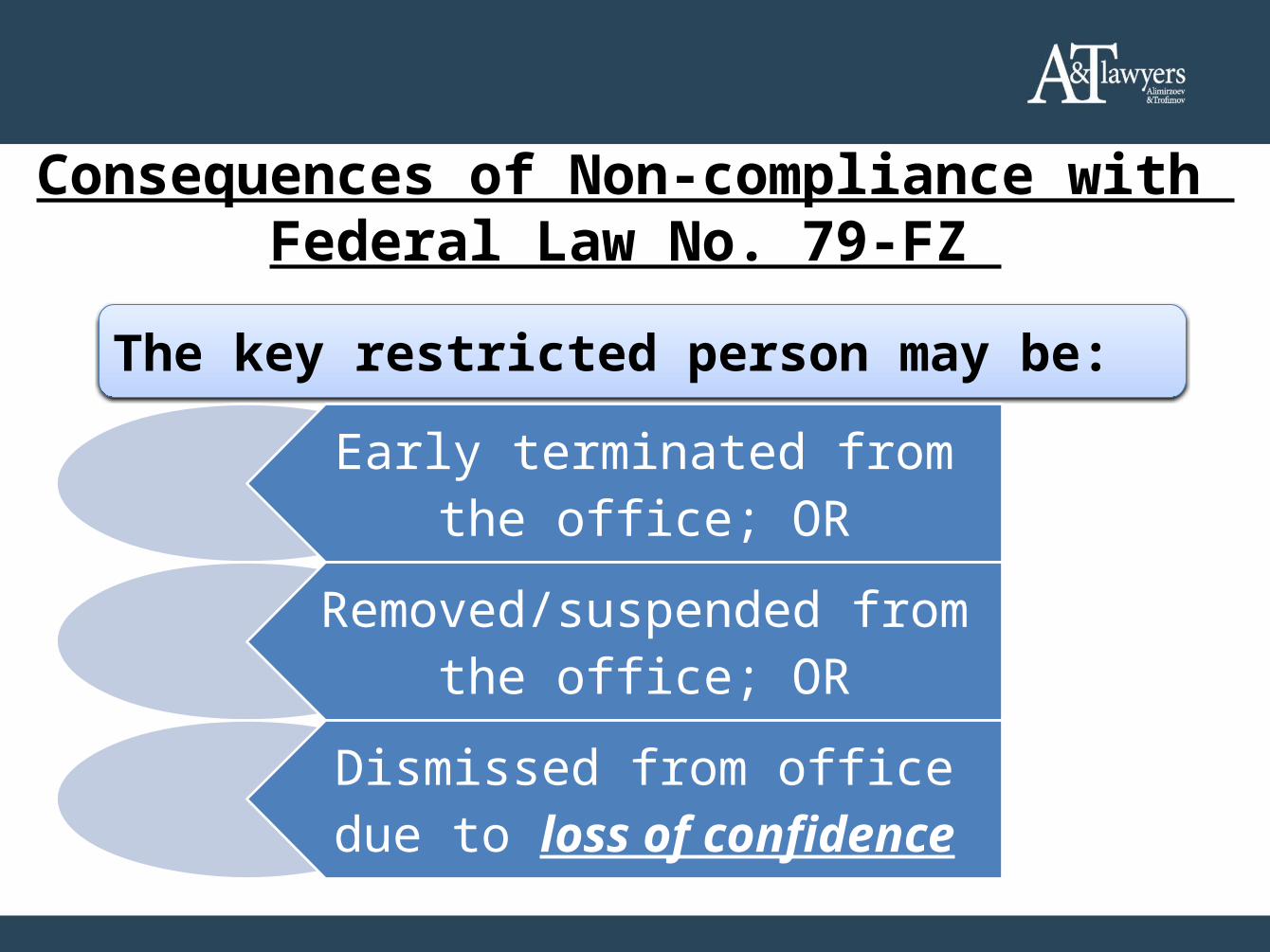

Consequences of Non-compliance with Federal Law No. 79-FZ

The key restricted person may be:

Early terminated from the office; OR

Removed/suspended from the office; OR

Dismissed from office due to loss of confidence

Consequences of Non-compliance with Federal Law No. 79-FZ

Under the RF legislation loss of confidence includes: – Non-compliance with Federal Law No. 79-FZ; – Failure to prevent or to resolve a conflict of interest;– Failure of a target person to file a tax return on income,

expenses, property and property obligations, as well as on his spouse and minor children, or submission of willfully false or incomplete information;

– Participation in business entities and receiving any income; – Conducting business activity;– Participation in foreign non-commercial non-governmental

entities.

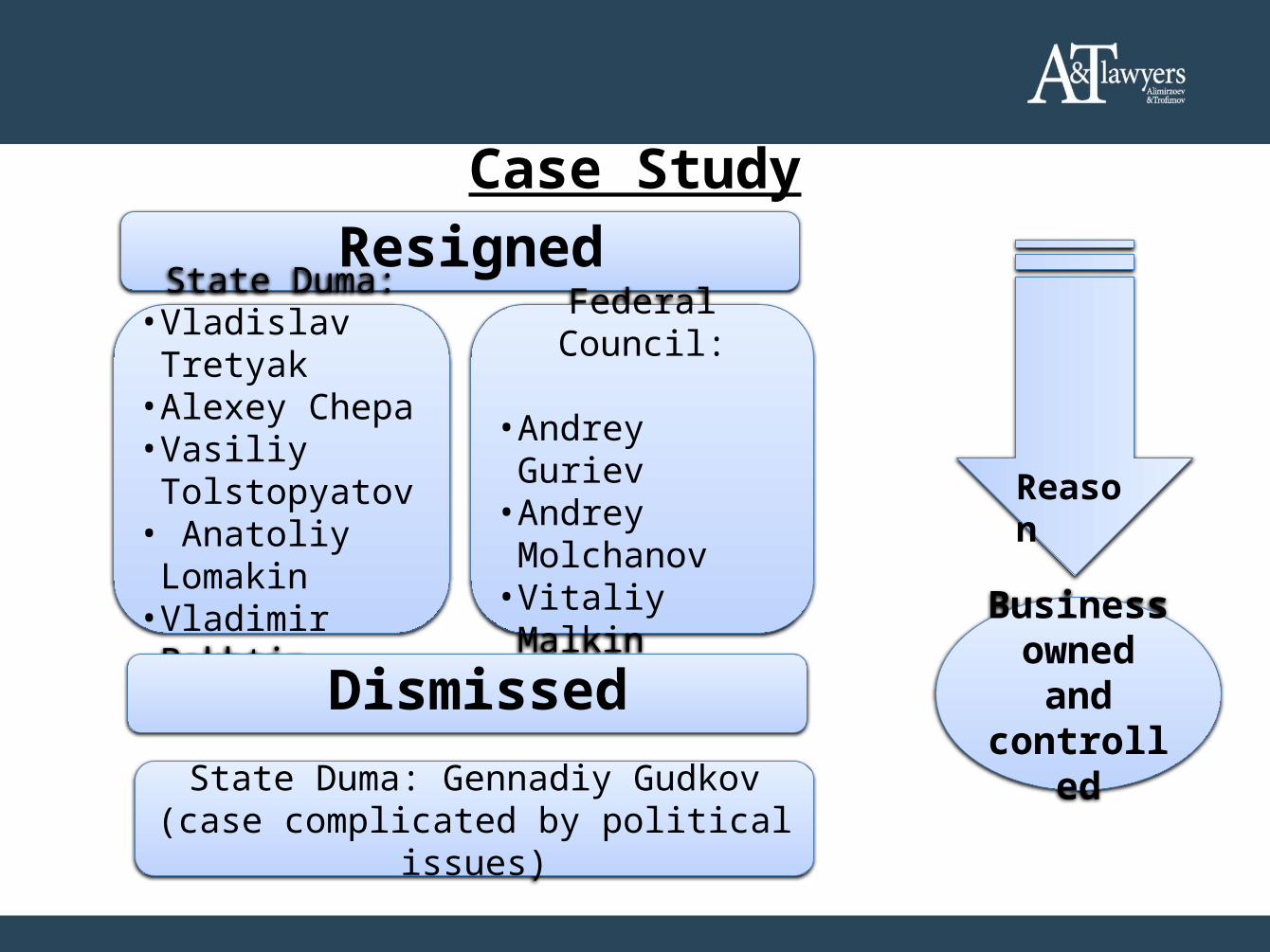

Case Study

Businessowned and controlled

Reason

ResignedState Duma:

• Vladislav Tretyak• Alexey Chepa• Vasiliy

Tolstopyatov• Anatoliy

Lomakin• Vladimir Pekhtin

Federal Council:

• Andrey Guriev• Andrey

Molchanov• Vitaliy Malkin

Dismissed

State Duma: Gennadiy Gudkov(case complicated by political issues)

Case StudyMikhail Prokhorov (Onexim Group)

Reportedly considered two ways for disposing of foreign assets and business by the beginning of Moscow mayor elections campaign

Scheme No. 1re-registration of

Cyprus company into Russian one with Prokhorov being the sole shareholder

the Russian company is managed by Prokhorov’s trustees under PoA.

Scheme No. 2making agreement with

Prokhorov’s trustees on buying of foreign assets with a deferred payment for a year.

in case after 1 year Prokhorov does not become Mayor, the money is not paid and all assets return to Prokhorov.

Decided not to

run for Mayor

NOTE:

• between residents and non-residents

• in foreign currency

Sale of assets in foreign

countries

• as foreign exchange transaction in accordance with the RF currency legislation

will be recognized

In February 13, 2013 there was introduced an administrative responsibility in the form of a fine from 75% to 100% of the transaction amount.

All settlements/ transactions in

currency shall be carried out via an

account of an individual in the RF

authorized bank.

Protocols to the Agreement on Avoidance of Double Taxation:

Russia-Cyprus (came into force)Russia – Latvia (came into force)Russia – Switzerland (came into

force)Russia - Luxembourg (came info

force)

Mechanisms for receiving information

by tax authorities:

Automatic exchange of information between tax services in

OECD countries and Russia

Other Countries’ ExperienceItaly No prohibition for public officers to have foreign bank accounts and foreign

financial instruments. Obligation to file tax returns. Breach entails criminal liability for tax fraud and money laundering with aggravating circumstances.

Colombia / Kuwait

No restrictions similar to Russian ones.

China Notice of the General Office of the CPC Central Committee and the General Office of the State Council on Issuing the Provisions on Reporting Personal and Related Matters of Leading Cadres (May, 2010)Obligations of relevant officers to report their assets, as well as spouses and minors. No restrictions on opening accounts and keeping assets in foreign banks situated abroad.

Egypt Egyptian Illicit Gain Law No. 62 of 1975 and its executive regulation No. 1112 of 1975.Obligations of state officials to prepare regular financial disclosures on all assets owned by them, their spouses or minors, in Egypt or abroad. Breach entails imprisonment and/or fine.

Anti-money Laundering Legislation

Federal Law No. 134-FZ as of June 26, 2013 on Fighting of Illegal Financial Operations

Beneficial Owner (UBO) is defined: “beneficial owner - an individual who directly or indirectly (through third parties) owns (has prevailing ownership of 25% in charter capital) the entity-client or who has a possibility to determine actions (decisions) of the client”;

Banks and Financial institutions are now required to establish and update information on UBO: practical experience on Russian level

The Law increased powers of the RF tax authorities authorized to receive banking data on individuals;

Other important changes to company, tax and bankruptcy laws

Recent/pending changes to Russian legislation on fighting use of off-shores

New Withholding Tax Rules on Distributions to Foreign Investors introduced to RF Tax Code (published on 3rd November, 2013)

• Apply further to regulate recently allowed “cascade” payments of dividend (bond) income arising from organized securities markets;

• Apply to dividend (bond) income to be credited to custody accounts, foreign nominee holder, foreign authorized holder or depositary programs accounts;

• Foreign nominee holders, etc. are required to supply Russian Tax Agents (Depositaries, Brokers, Issuers, etc.) with information on tax jurisdiction of ultimate owners of securities and any claimed DDT benefits;

Recent/pending changes to Russian legislation on fighting use of off-shores

New Withholding Tax Rules on Distributions to Foreign Investors(continued)

• If required supporting documentation (in full detail and correct format) is not supplied, Tax Agent is required to withhold tax on dividend (bond) income at the rate of 30%;

• Information Disclosure is voluntary;• Tax Liability of Tax Agents can be limited in cases when foreign

counterparties provided wrong or incomplete information;• Direct application of DDT benefits is limited to situations when no

specials conditions are imposed under DDT (Examples of special conditions: investment over EUR 100,000 or equity stake over 10%);

Recent/proposed changes to Russian legislation on fighting use of off-shores

Proposed Changes to Russian Criminal Procedure Code (brought to the State Duma on 11th October, 2013)

• Initiative of the Presidential Administration to reinstate previously applied rules (existed before 2011) on powers to open tax criminal cases;

• Investigating officers shall be allowed to open criminal cases on alleged tax crimes without preceding tax audit confirming event of tax offence/crime;

• Apparently the intent is to tighten control over capital flow by “efficient” criminal procedure controls.

Recent/proposed changes to Russian legislation on fighting use of off-shores

Proposed changes To Russian Tax Code (Investigating Committee of Russia is working on draft bill)The Bill proposes definitions of “sham” and “fictitious” transactions for tax purposes:

• “sham” transactions shall mean transactions which are aimed to disguise real transactions with the aim of obtaining unlawful tax benefits and tax minimization;

• “fictitious” transactions are defined as transactions which were not really executed.If this bill is passed and the tax bodies begin to use these definitions to prevent tax minimization, business will have to review its usual financing schemes.

Anticorruption and Anti-Laundering Aspects

There is a demand in society for fighting corruption and state authorities make attempts to respond to it

Russia joined OECD Anti-Bribery Convention in international business transactions.

OECD recommendations are partly fulfilled (including prohibition to reduce the tax profit on the amounts of bribes paid).

Most independent research works, however, show that in reality corruption level is still a serious problem

Thank You For Attention!