Receivables Chapter 8 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall8-1.

49

Receivables Chapter 8 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-1

-

Upload

marianna-bell -

Category

Documents

-

view

217 -

download

1

Transcript of Receivables Chapter 8 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall8-1.

Receivables

Chapter 8

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-1

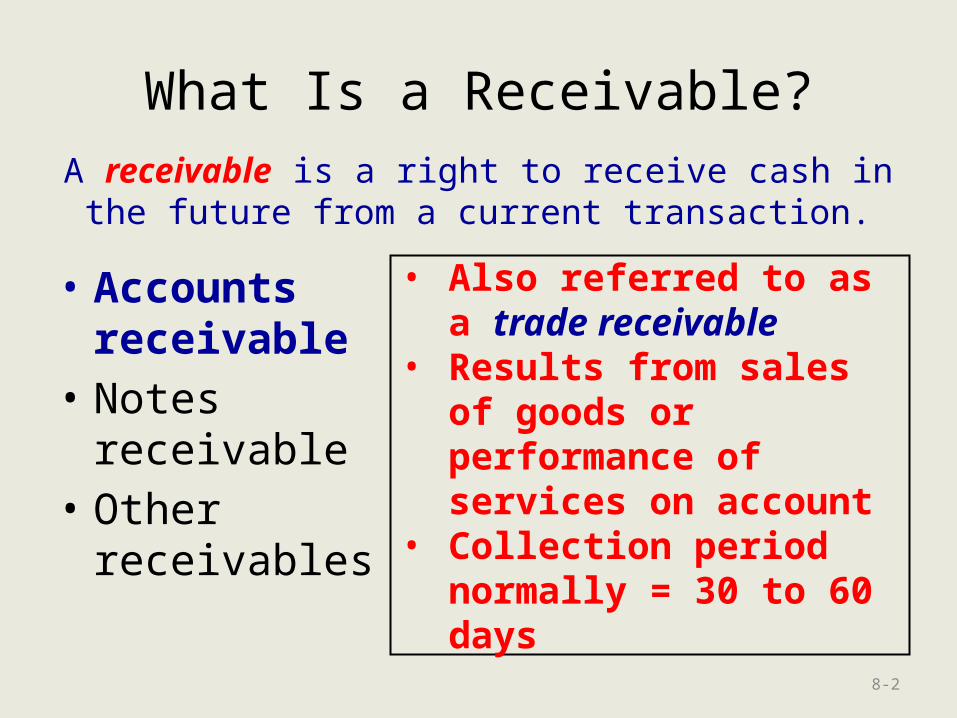

What Is a Receivable?

• Accounts receivable

• Notes receivable

• Other receivables

A receivable is a right to receive cash in the future from a current transaction.

• Also referred to as a trade receivable

• Results from sales of goods or performance of services on account

• Collection period normally = 30 to 60 days

8-2

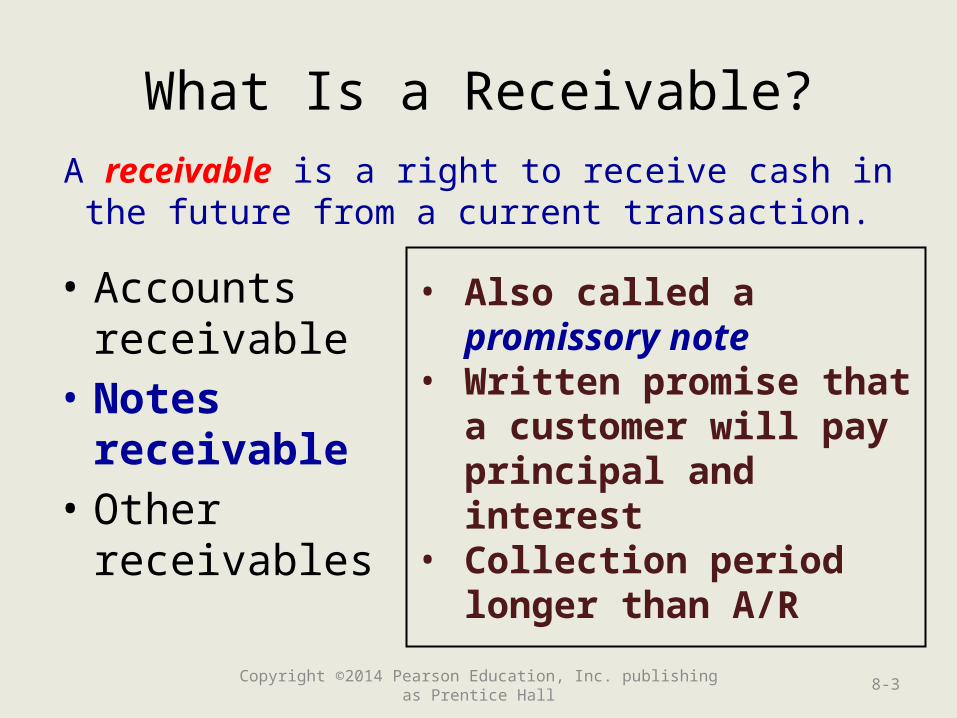

What Is a Receivable?

• Accounts receivable

• Notes receivable

• Other receivables

A receivable is a right to receive cash in the future from a current transaction.

• Also called a promissory note

• Written promise that a customer will pay principal and interest

• Collection period longer than A/R

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-3

Notes Receivable

• More formal than accounts receivable• Usually longer in term

– Debtor promises to pay by maturity date– Maturity date–date the debt must be

completely paid off

• Current assets if due within one year or less

• Long-term assets if due beyond one year• Promissory note

– Written document signed by both parties 4

What Is a Receivable?

• Accounts receivable

• Notes receivable

• Other receivables

A receivable is a right to receive cash in the future from a current transaction.

• Category includes dividends, taxes, and interest receivables

• Can be current or long-term

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-5

Recording Sales on Credit

• Selling “on account” will create an A/R• Suppose that, on August 8, Smart Touch

Learning performs $5,000 in services to Brown on account, and sells $10,000 of inventory on account to Smith.

Date Accounts and Explanation Debit Credit

Prepare both journal entries.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-6

Recording Sales on Credit• Selling “on account” will create an A/R• Suppose that, on August 8, Smart Touch

Learning performs $5,000 in services to Brown on account, and sells $10,000 of inventory on account to Smith. Ignore COGS.

Date Accounts and Explanation Debit Credit

Aug 8 Accounts receivable - Brown 5,000 Service revenue 5,000

Accounts receivable - Smith 10,000 Sales revenue 10,000

8-7

A L + E

Accounts = Service Rev.Receivable

Sales Rev

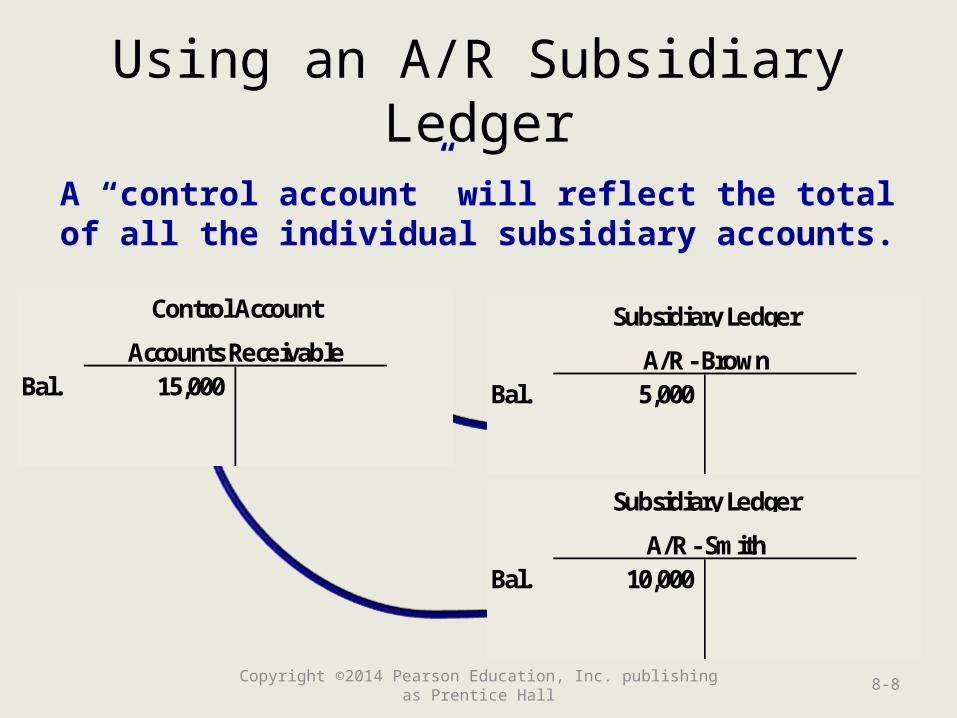

Using an A/R Subsidiary Ledger

A “control account” will reflect the total of all the individual subsidiary accounts.

Bal. 15,000 Accounts Receivable

Control Account

Bal. 5,000 A/R - Brown

Subsidiary Ledger

Bal. 10,000 A/R - Smith

Subsidiary Ledger

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-8

Recording Credit Card and Debit Card Sales

• Recorded the same as Cash sales.• A fee is usually charged by the card

company.– The net cash received is reduced by

the fee.

• 2 Methods are allowed:– Net Method– Gross Method

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-9

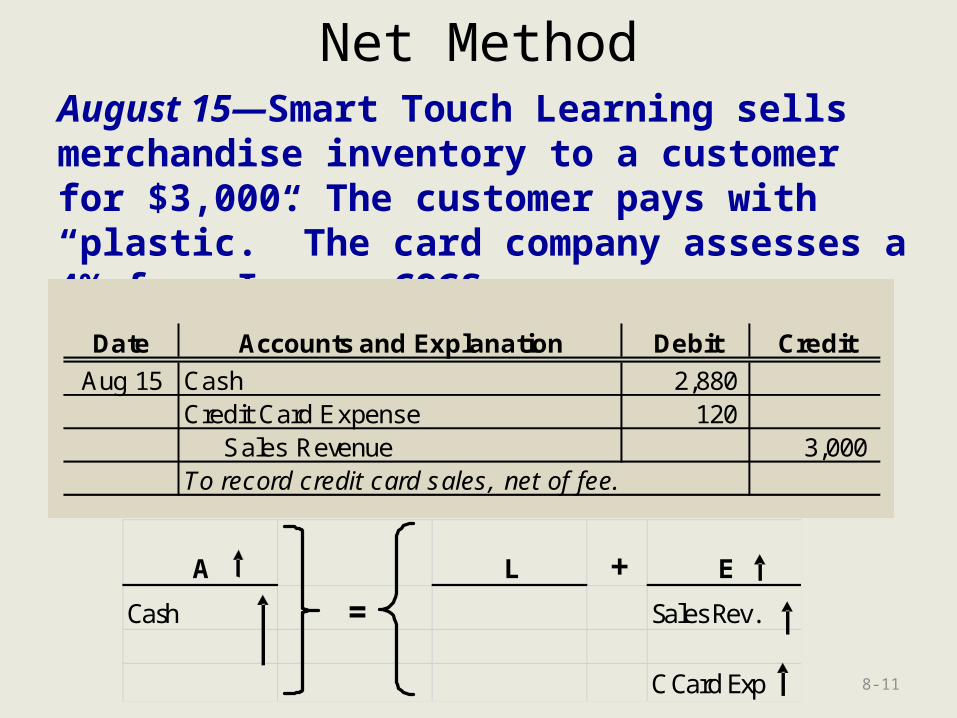

Net Method

• Record the card company fee at the time of the sale.

• Only the net amount of cash is recorded.

Date Accounts and Explanation Debit Credit

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-10

Net MethodAugust 15—Smart Touch Learning sells merchandise inventory to a customer for $3,000. The customer pays with “plastic.” The card company assesses a 4% fee. Ignore COGS.

Date Accounts and Explanation Debit Credit

Aug 15 Cash 2,880 Credit Card Expense 120 Sales Revenue 3,000 To record credit card sales, net of fee.

8-11

A L + E

Cash = Sales Rev.

C Card Exp

Gross Method

• Record the full sale on the sale date.• Record the credit card fee as a separate entry

when the cash is deposited by the third party.

Date Accounts and Explanation Debit Credit

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-12

Gross MethodAugust 15—Smart Touch Learning sells merchandise inventory to a customer for $3,000. The customer pays with “plastic.” The card company assesses a 4% fee. Ignore COGS.

Date Accounts and Explanation Debit Credit

Aug 15 Cash 3,000 Sales Revenue 3,000 To record credit card sales at gross.

8-13

A L + E

Cash = Sales Rev.

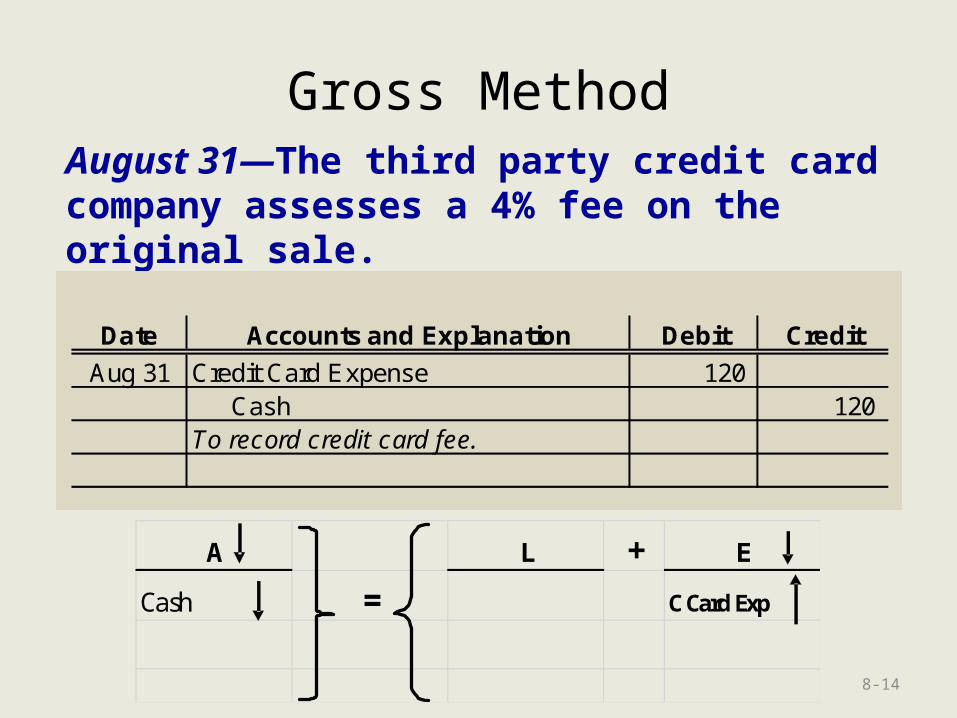

Gross MethodAugust 31—The third party credit card company assesses a 4% fee on the original sale.

Date Accounts and Explanation Debit Credit

Aug 31 Credit Card Expense 120 Cash 120 To record credit card fee.

8-14

A L + E

Cash = C Card Exp

Accounting for Uncollectibles (Bad Debts)

• Selling on credit:– BENEFIT–Increase sales by selling to a wider

range of customers

• Two methods to account for uncollectible accounts:– Allowance method– Direct write-off method

15

How do we record uncollectible accounts using the Direct Method?

• Fact: Not all customers will pay what they owe.

• Accounting Reality: We have to take these “bad” receivables off the books and record a corresponding Bad Debt Expense.

Under the Direct Method, the bad debt expense is

recorded as soon as a receivable is

deemed uncollectible.(Not GAAP)

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-16

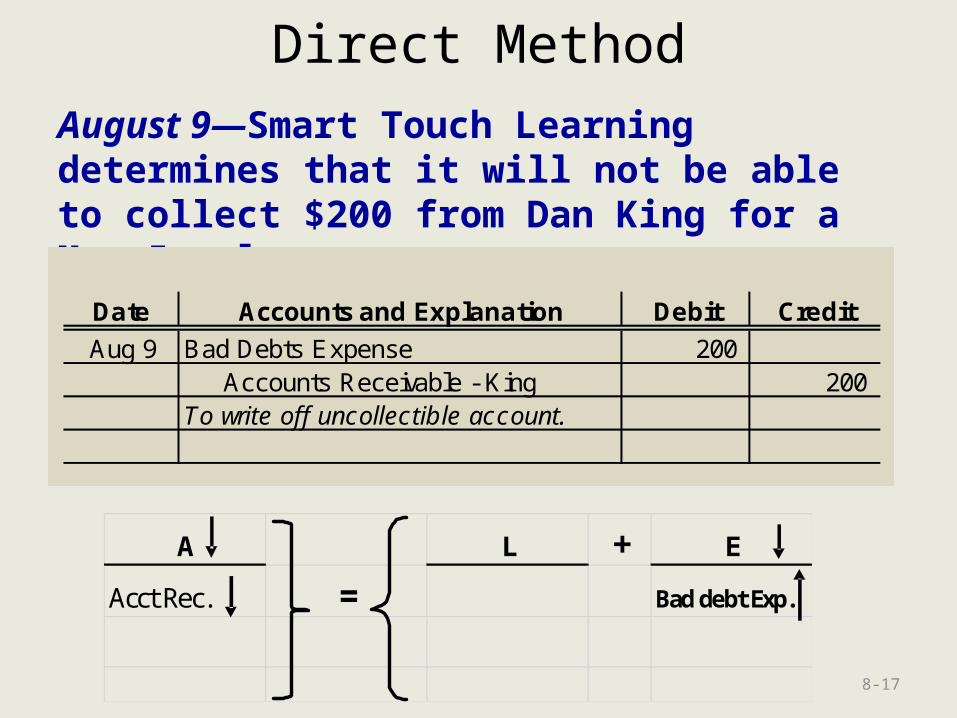

Direct Method

August 9—Smart Touch Learning determines that it will not be able to collect $200 from Dan King for a May 5 sale.

Date Accounts and Explanation Debit Credit

Aug 9 Bad Debts Expense 200 Accounts Receivable - King 200 To write off uncollectible account.

8-17

A L + E

Acct Rec. = Bad debt Exp.

Recovery of Previously Written Off A/R

September 10—King pays the $200 previously written off as uncollectible.

Date Accounts and Explanation Debit Credit

Sep 10 Accounts Receivable - King 200 Bad Debts Expense 200 To reinstate previously written off A/R.

Sep 10 Cash 200 Accounts Receivable - King 200 To record cash collection.

8-18

• Reverse the earlier write-off• Record the receipt of the payment

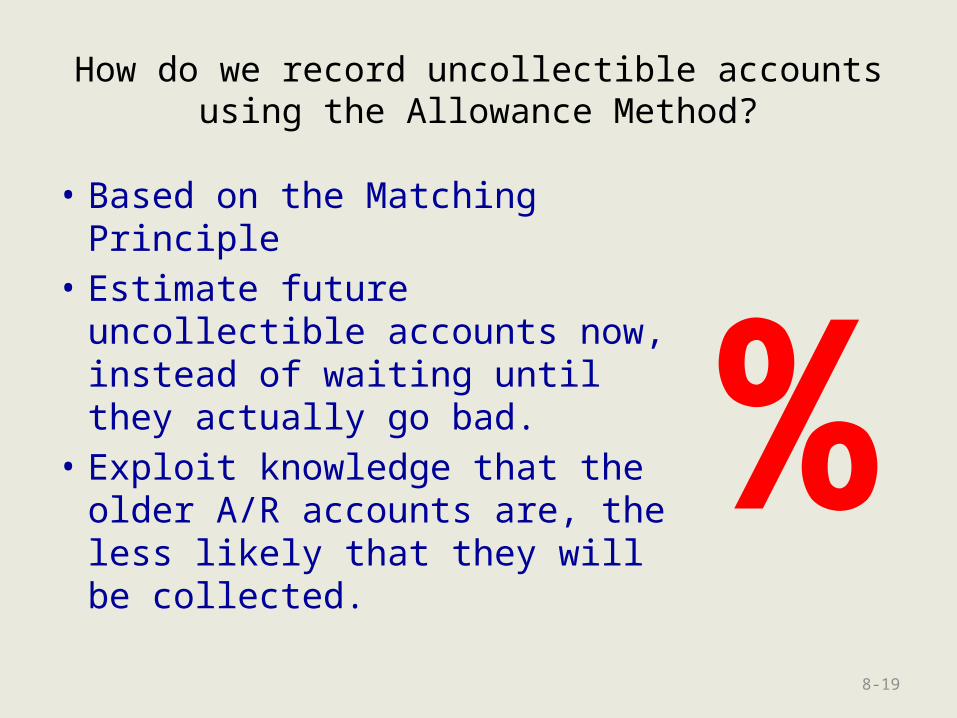

How do we record uncollectible accounts using the Allowance Method?

• Based on the Matching Principle

• Estimate future uncollectible accounts now, instead of waiting until they actually go bad.

• Exploit knowledge that the older A/R accounts are, the less likely that they will be collected.

%8-19

How do we record uncollectible accounts using the Allowance Method?

• At the end of each period, record the Bad Debts Expense and put the credit in Allowance for Bad Debts.– The Allowance for Bad Debts

account is a Contra-Asset

• As actual accounts become uncollectible, charge them against the Allowance account.

%8-20

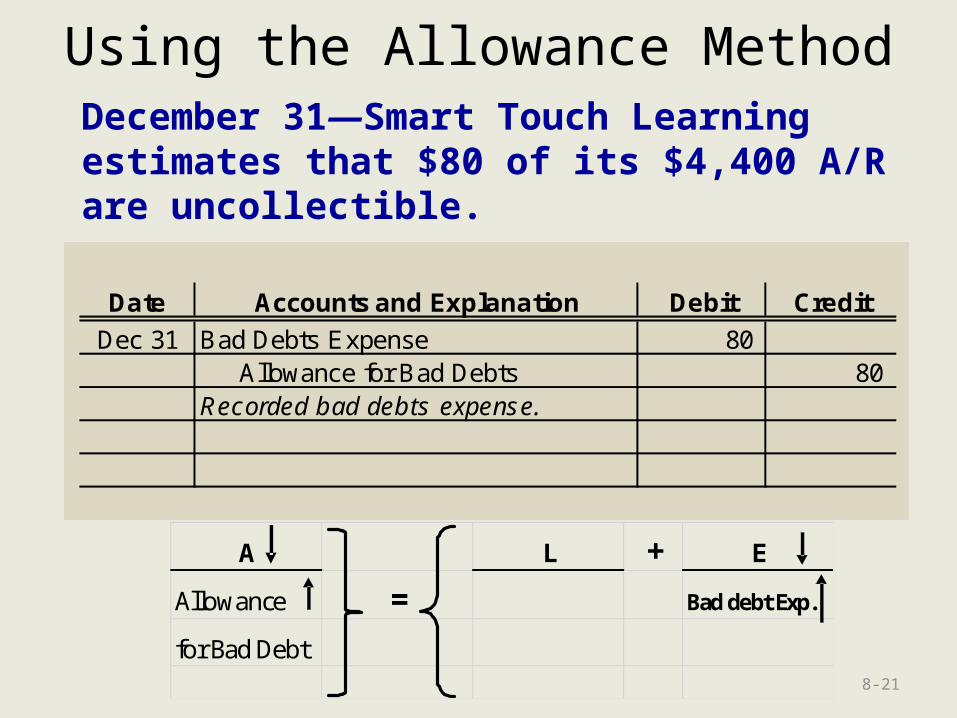

Using the Allowance MethodDecember 31—Smart Touch Learning estimates that $80 of its $4,400 A/R are uncollectible.

Date Accounts and Explanation Debit Credit

Dec 31 Bad Debts Expense 80 Allowance for Bad Debts 80 Recorded bad debts expense.

8-21

A L + E

Allowance = Bad debt Exp.

for Bad Debt

Using the Allowance MethodThe Contra-Asset account will be shown as

reduction of Accounts Receivable.

8-22

Writing Off an Uncollectible Account

• When an account become uncollectible, it is written off.

• The bad account is charged against the Allowance Account.

Date Accounts and Explanation Debit Credit

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-23

Writing Off an Uncollectible AccountJanuary 10, 2016—Smart Touch Learning determines that it will not collect $25 from customer Shawn Callahan.

Date Accounts and Explanation Debit Credit

Jan 10 Allowance for Bad Debts 25 Accounts Receivable - Callahan 25

8-24

A L + E

Allowance =for Bad DebtAcct Rec.

Before AfterAR 4,400 4375

Less Allowance (80) (55)4,320 4,320

Recovery of Previously Written Off A/R

March 4—Smart Touch Learning receives $25 from Callahan to cover the written off account.

Date Accounts and Explanation Debit Credit

Mar 4 Accounts Receivable - Callahan 25 Allowance for Bad Debts 25 To reinstate previously written off A/R.

Mar 4 Cash 25 Accounts Receivable - Callahan 25 To record collection of cash.

8-25

• Reverse the earlier write-off• Record the receipt of the payment

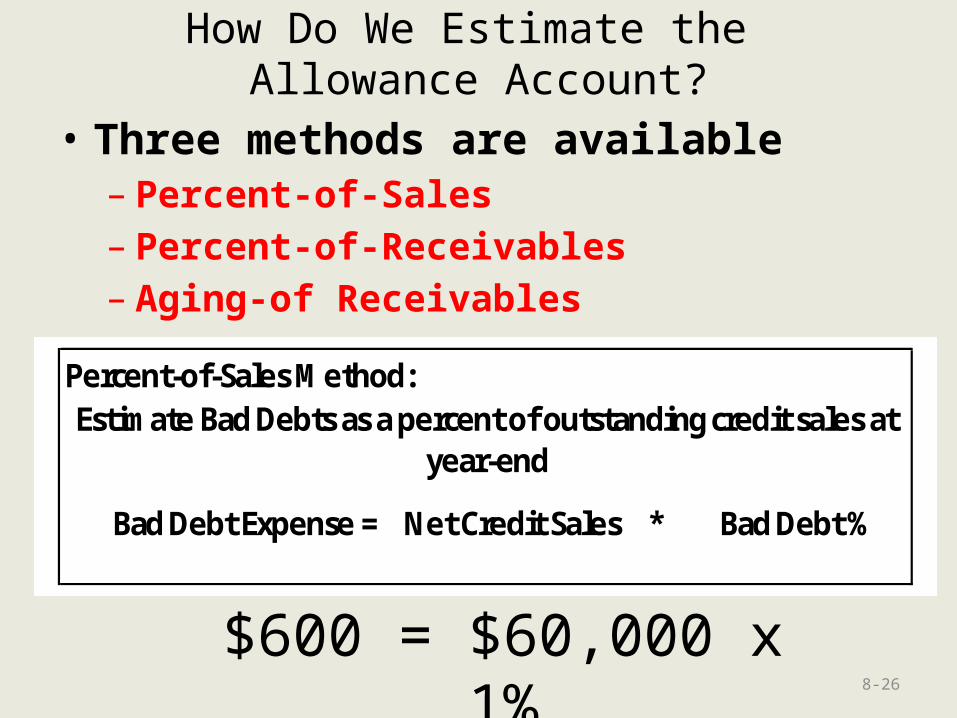

How Do We Estimate the Allowance Account?

• Three methods are available– Percent-of-Sales– Percent-of-Receivables– Aging-of Receivables

Percent-of-Sales Method:

Bad Debt Expense = Net Credit Sales * Bad Debt %

Estimate Bad Debts as a percent of outstanding credit sales at year-end

8-26

$600 = $60,000 x 1%

How Do We Estimate the Allowance Account?

Percent-of-Receivables Method:Step 1:

Target Balance = Ending A/R * Bad Debt %

Step 2:

Target Balance -

Existing credit balance of Allowance for Bad Debts

Determine the target balance for Allowance for Bad Debts

Determine Bad Debts Expense by evaluating the Allowance account

Bad Debts Expense =

8-27

How Do We Estimate the Allowance Account?

Aging-of-Receivables MethodStep 1:

Target Balance = Σ (Each Age Group * Bad Debt %)

Step 2:

Bad Debts Exp. =

Target Balance -Existing credit balance of Allowance for Bad Debts

Determine the target balance for Allowance for Bad Debts based on account age

Determine Bad Debts Expense by evaluating the Allowance account

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-28

Using the Aging-of-Receivables Method

8-29

Smart Touch Learning’s unadjusted credit balance in

the allowance account is $55(80 – 25).

Per the previous computation, the desired balance is $185.

Smart Touch Learning’s unadjusted credit balance in

the allowance account is $55(80 – 25).

Per the previous computation, the desired balance is $185.

80 25 130

185

Allowance for Bad Debts

Using the Aging-of-Receivables Method

Date Accounts and Explanation Debit Credit

Dec 31 Bad Debts Expense 130 Allowance for Bad Debts 130 To record bad debts expense.

8-30

A L + E

Allowance = Bad Debt

for Bad Debt Exp

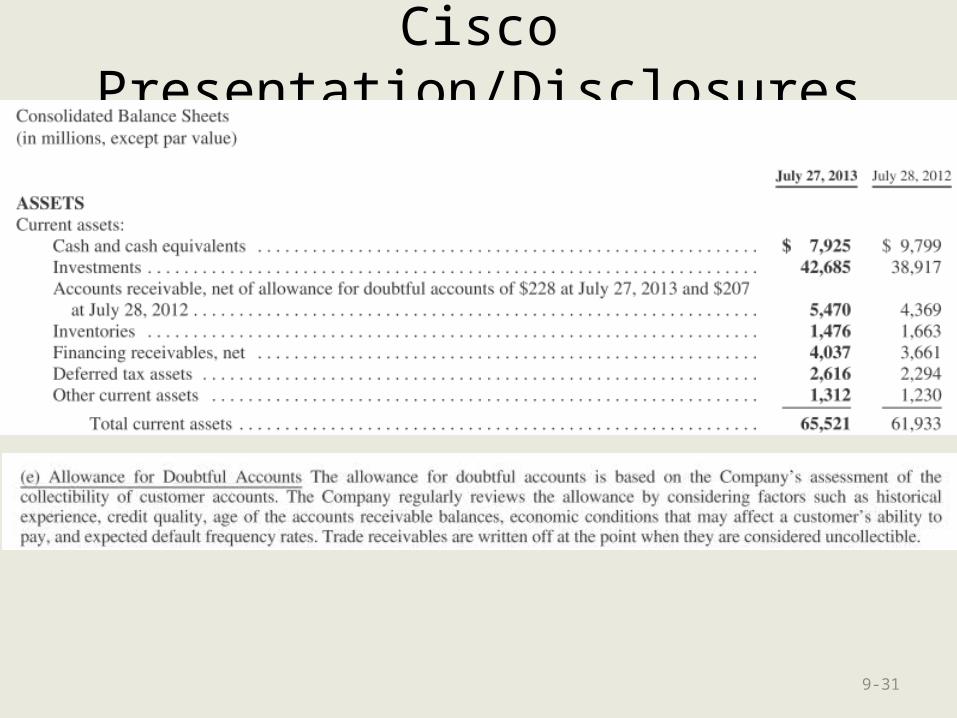

Cisco Presentation/Disclosures

9-31

Eastman Presentation/Disclosures

9-32

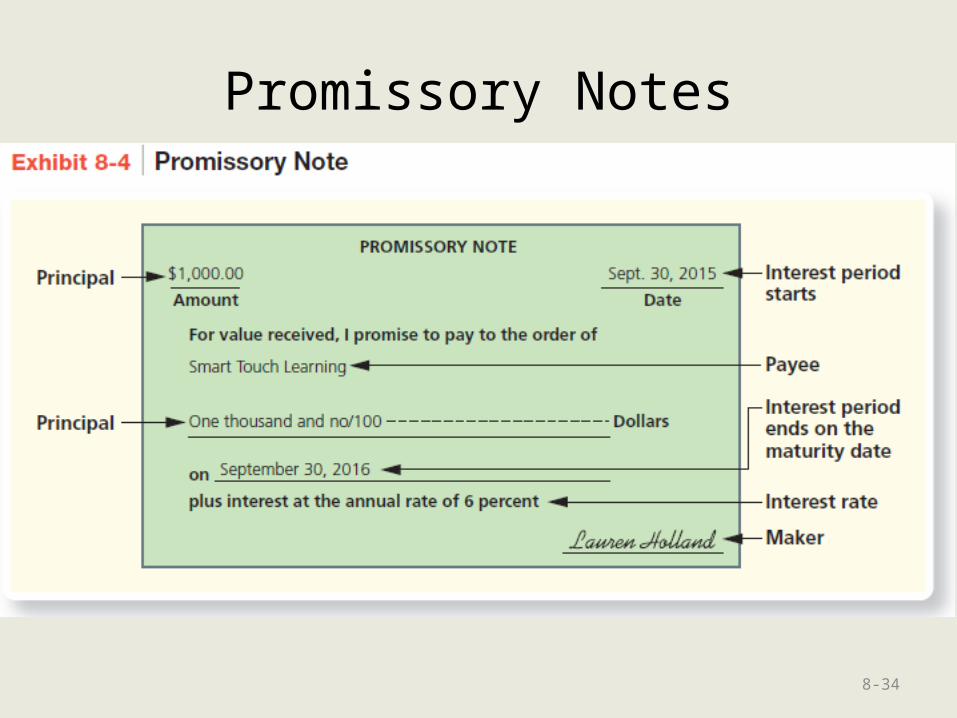

Accounting for Notes Receivable

• Record the note on the date the loan is made.

• Periodically accrue interest revenue and record interest receipts.

• Record collection of note principal.

Notes are evidenced by a signed

document called a Promissory Note.

Must include certain components.

8-33

Promissory Notes

8-34

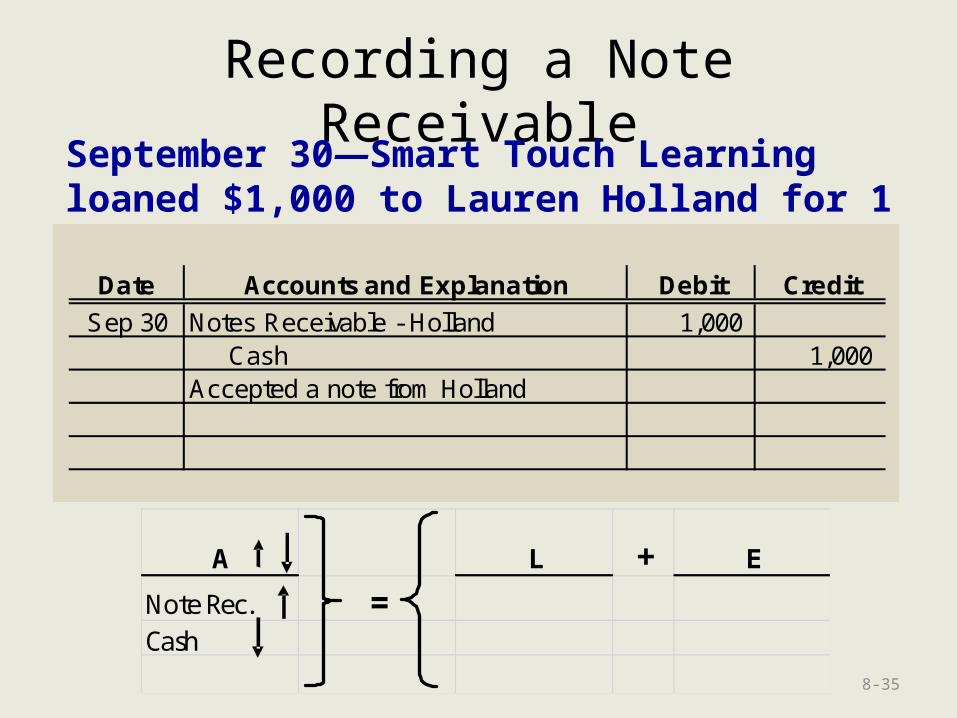

Recording a Note ReceivableSeptember 30—Smart Touch Learning loaned $1,000 to Lauren Holland for 1 year @ 6%.

Date Accounts and Explanation Debit Credit

Sep 30 Notes Receivable - Holland 1,000 Cash 1,000 Accepted a note from Holland

8-35

A L + E

Note Rec. =Cash

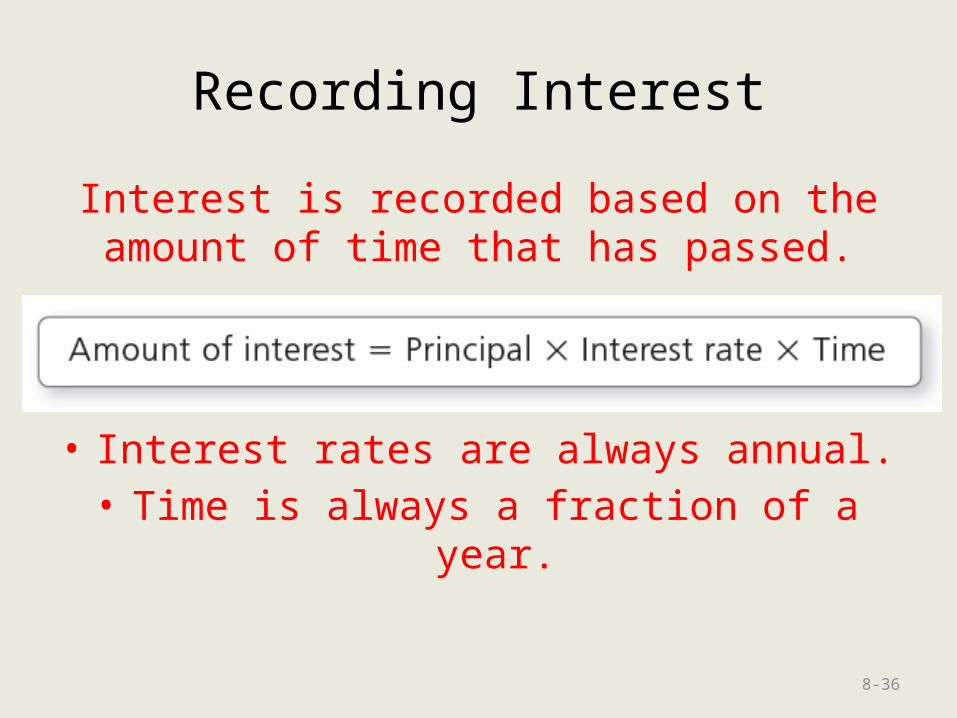

Recording Interest

Interest is recorded based on the amount of time that has passed.

• Interest rates are always annual.• Time is always a fraction of a year.

8-36

Computing Interest(examples)

• By the year

• By the month

• By the day

37

360 days used in this example to simplify

calculations

Recording a Note ReceivableDecember 31—The $1,000 loan to Lauren Holland is not yet due, but interest must be accrued at the rate of 6%.

Date Accounts and Explanation Debit Credit

Dec 31 Interest Receivable 15 Interest Revenue 15 Accrued interest revenue.

8-38

A L + E

Int. Rec. = Int. Rev

Recording Dishonored Notes Receivable

• When the maker of the note does not pay, it is dishonored.

• Often the dishonored note AND the unpaid interest are transferred to an A/R.

• Later, the A/R can be written off.

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

If a unit has many notes receivable,

such as a financing division, it can also set up a Loan Loss Reserve similar to Allowance for Bad

Debts.

8-39

Use the acid-test ratio, accounts receivable

turnover ratio, and days’ sales in receivables to

evaluate business performance(Liquidity)

8-40

Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall 8-41

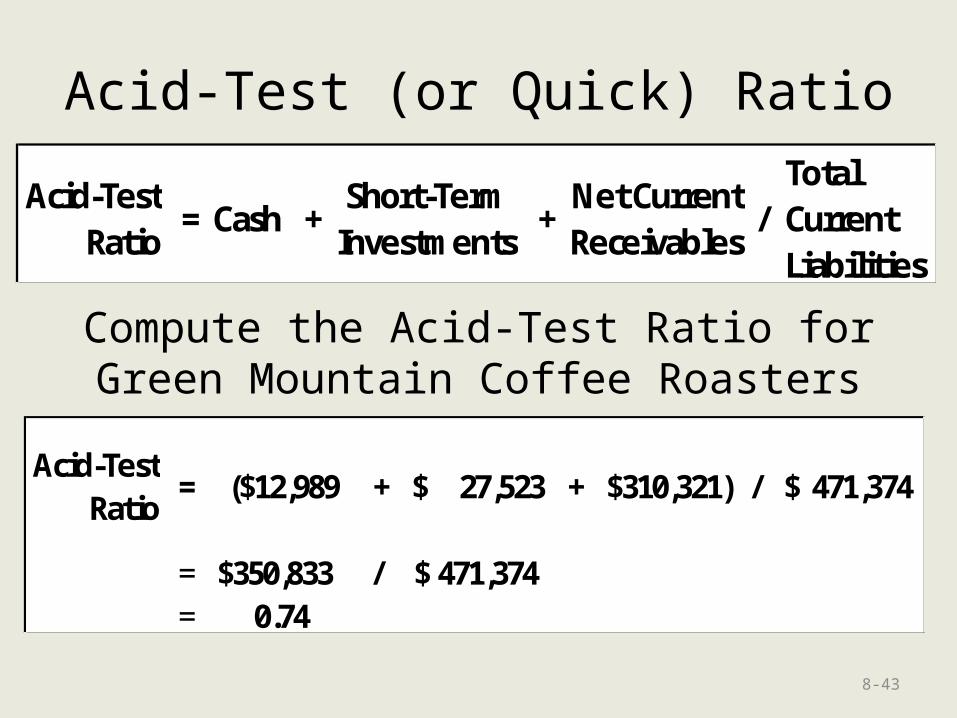

Acid-Test (or Quick) Ratio

Compute the Acid-Test Ratio for Green Mountain Coffee Roasters

©2014 Pearson Education, Inc. publishing as Prentice Hall

Acid-Test Ratio

= Cash +Short-Term

Investments +

Net Current Receivables

/Total Current Liabilities

8-42

Acid-Test (or Quick) Ratio

Compute the Acid-Test Ratio for Green Mountain Coffee Roasters

Acid-Test Ratio

= Cash +Short-Term

Investments +

Net Current Receivables

/Total Current Liabilities

Acid-Test Ratio

= ($12,989 + $ 27,523 + $310,321) / $ 471,374

= $350,833 / 471,374$ = 0.74

8-43

Walmart Acid-Test

9-44

(7,281 + 6,697) / 69,345 = .2015

9-45

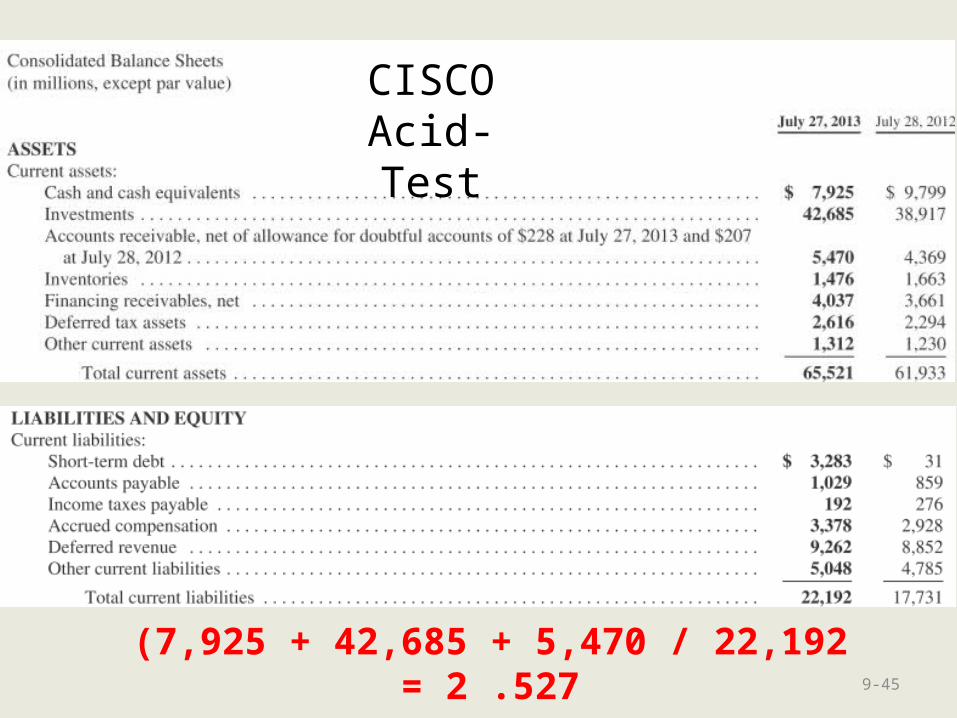

(7,925 + 42,685 + 5,470 / 22,192 = 2 .527

CISCO Acid-Test

Eastman Chemical Acid-Test

9-46

(237 + 880) / 1,470 = .76

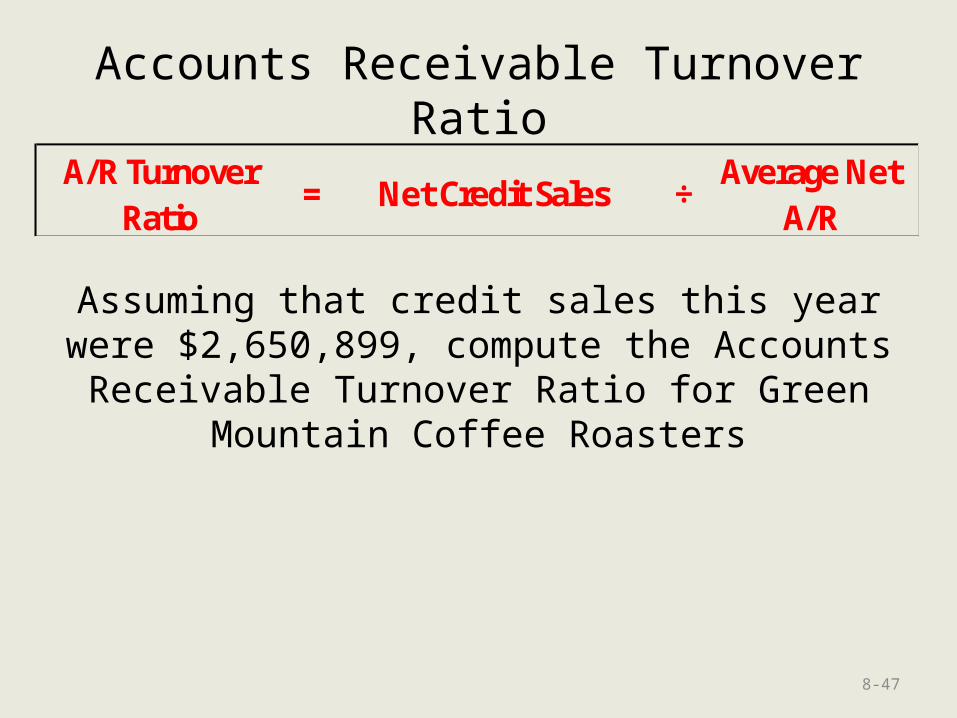

Accounts Receivable Turnover Ratio

Assuming that credit sales this year were $2,650,899, compute the Accounts Receivable

Turnover Ratio for Green Mountain Coffee Roasters

A/R Turnover Ratio

= Net Credit Sales ÷Average Net

A/R

8-47

Accounts Receivable Turnover Ratio

Assuming that credit sales this year were $2,650,899, compute the Accounts Receivable

Turnover Ratio for Green Mountain Coffee Roasters.

A/R Turnover Ratio

= $ 2,650,899 ÷ [($310,321 + $172,200) ÷ 2]

= 2,650,899$ ÷ $241,261 = 10.99

8-48

A/R Turnover Ratio

= Net Credit Sales ÷Average Net

A/R

Eastman Chemical A/R Turnover = $9,350 / 863 = 10.83

Days’ Sales in Receivables

Compute the Days’ Sales in Receivables for Green Mountain Coffee Roasters

Days' Sales In Receivables

= 365 days ÷A/R Turnover

Ratio

Days' Sales In Receivables

= 365 days ÷A/R Turnover

Ratio = 365 ÷ 10.99 = 33

8-49