RealTime Dynamix™: Renal Anemia US · The majority of nephrologists report being comfortable with...

3

RealTime Dynamix™: Renal Anemia US The majority of nephrologists report being comfortable with the risk benefit profile of ESAs in both dialysis and CKD. Although about one-quarter of the surveyed nephrologists feel that there is a high unmet need for new therapeutic agents to treat renal anemia in CKD-ND, this need is significantly lower than other areas, particularly diabetic nephropathy and ADPKD. A similar pattern is observed in the dialysis setting. Percent of respondents Percent of respondents 11% of the respondents report some use of Triferic, from 14% in Q4 and 13% in Q3, 11% in Q2 and 10% in Q1 for a mean HD share of 1.5%. Among the very few patients on Triferic, 58% also receive IV iron. Mean Prevalence and Treatment Rates While the use of ESAs and IV iron increases as disease severity worsens, the converse is reported for oral iron. The use of specific ESA brands is highly dependent on dialysis chain affiliation. Unmet Need in Nephrology Attitudes About Renal Anemia Percent of patients ESA HD Share by Chain Affiliation Percent of respondents

Transcript of RealTime Dynamix™: Renal Anemia US · The majority of nephrologists report being comfortable with...

RealTime Dynamix™: Renal Anemia US

The majority of nephrologists report being comfortable with the risk benefit profile of ESAs in both dialysis and CKD.

Although about one-quarter of the surveyed nephrologists feel that there is a high unmet need for new therapeutic agents to

treat renal anemia in CKD-ND, this need is significantly lower than other areas, particularly diabetic nephropathy and ADPKD. A

similar pattern is observed in the dialysis setting.

Perc

ent of re

spondents

P

erc

ent of re

spondents

11% of the respondents report some use of Triferic, from 14% in Q4 and

13% in Q3, 11% in Q2 and 10% in Q1 for a mean HD share of 1.5%.

Among the very few patients on Triferic, 58% also receive IV iron.

Mean Prevalence and Treatment Rates

While the use of ESAs and IV iron increases as disease severity worsens, the converse is reported for oral iron. The use of

specific ESA brands is highly dependent on dialysis chain affiliation.

Unmet Need in Nephrology

Attitudes About Renal Anemia

Perc

ent of patie

nts

ESA HD Share by Chain Affiliation

Percent of respondents

To order or to get more information, please contact

[email protected] or call (484) 879-4284

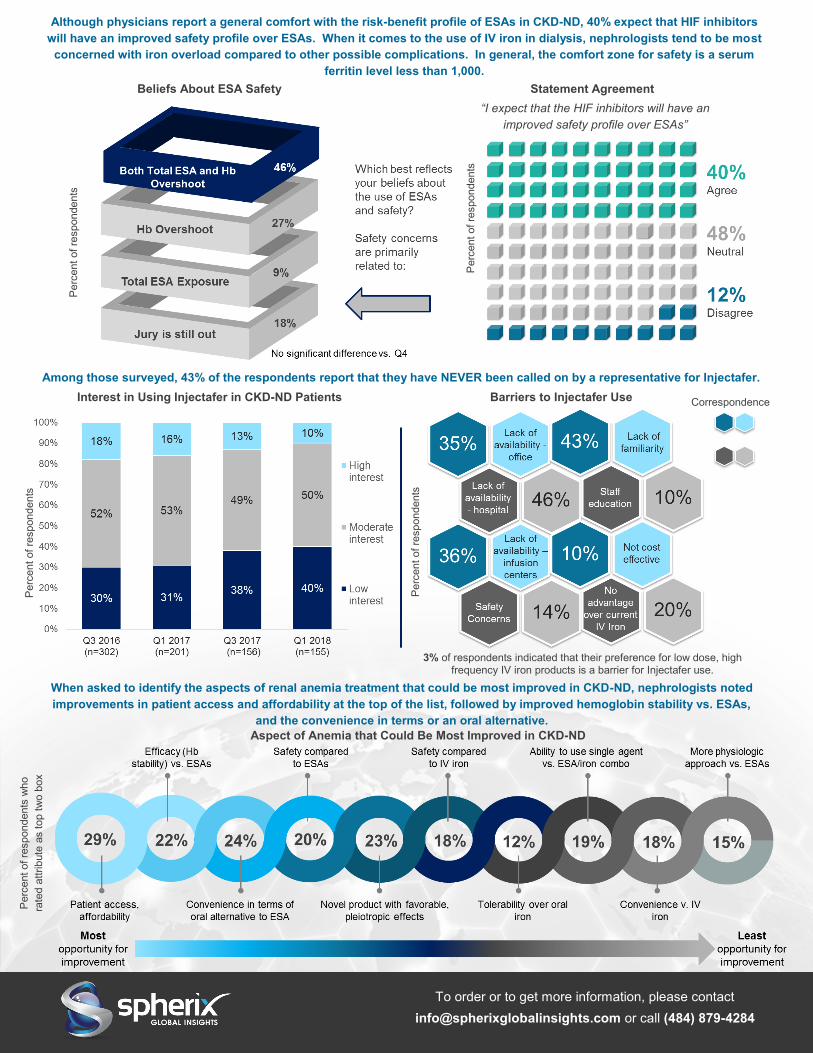

Although physicians report a general comfort with the risk-benefit profile of ESAs in CKD-ND, 40% expect that HIF inhibitors

will have an improved safety profile over ESAs. When it comes to the use of IV iron in dialysis, nephrologists tend to be most

concerned with iron overload compared to other possible complications. In general, the comfort zone for safety is a serum

ferritin level less than 1,000.

Among those surveyed, 43% of the respondents report that they have NEVER been called on by a representative for Injectafer.

Aspect of Anemia that Could Be Most Improved in CKD-ND

Beliefs About ESA Safety

Perc

ent of re

spondents

Statement Agreement

Perc

ent of re

spondents

Interest in Using Injectafer in CKD-ND Patients

Perc

ent of re

spondents

P

erc

ent of re

spondents

who

rate

d a

ttrib

ute

as top t

wo b

ox

Perc

ent of re

spondents

Barriers to Injectafer Use

3% of respondents indicated that their preference for low dose, high frequency IV iron products is a barrier for Injectafer use.

“I expect that the HIF inhibitors will have an

improved safety profile over ESAs”

When asked to identify the aspects of renal anemia treatment that could be most improved in CKD-ND, nephrologists noted

improvements in patient access and affordability at the top of the list, followed by improved hemoglobin stability vs. ESAs,

and the convenience in terms or an oral alternative.

Correspondence

OVERVIEW The management of renal anemia in dialysis patients as well as in those with later stage chronic kidney disease is becoming increasingly complex. In the dialysis setting, clinical management is further complicated by a reimbursement model that treats commonly used therapies like erythropoiesis stimulating agents (ESAs) and iron therapies as cost centers. Novel products in development such as the oral HIF-Ph inhibitors offer a new mechanism approach and may change the treatment paradigm in both the dialysis and CKD-ND settings. This quarterly report series focuses on tracking key performance metrics for ESAs and iron products (oral iron, IV iron and dialysate iron) in both the dialysis and CKD-ND settings. Emphasis is placed on the growing familiarity with pipeline agents as well as the evolving role of Keryx’s Auryxia as a treatment for iron-deficiency anemia in non-dialysis patients. The rapid field-to insight turnaround, highly relevant content an unparalleled market understanding make RealTime Dynamix™ an essential tool for companies with commercial products in the space, those that will soon be launching and those looking for business development opportunities in nephrology.

SAMPLE & METHODOLOGY Each quarter, ~200 US nephrologists complete an online survey. The respondents are recruited from the Spherix Network, proprietary panel of over 900 US nephrologists. Recruiting is managed to capture a regionally and demographically representative sample.

KEY QUESTIONS ANSWERED • What shifts are occurring in renal anemia in the dialysis setting and

do these changes vary by chain (i.e. DaVita, FMC)?

• How do treatment rates and approaches for ESAs and IV iron differ between dialysis and CKD-ND patients?

• Do nephrologists have a preference for long-acting or short-acting ESAs and what does this mean for biosimilar ESAs coming to market? Will it impact HIF-PH inhibitor adoption?

• What is the market uptake for Rockwell Medical’s Triferic?

• Are nephrologists using Auryxia for the dual action of phosphate lowering and improvement in anemia parameters? How has the IDA launch of Auryxia expanded use and perceptions of the product?

• How does in-office infusion for IV iron or stocking of ESAs influence treatment rates and brand preference?

• How does the unmet need for new anemia drugs compare to the unmet need in other areas of nephrology?

• How are nephrologists becoming familiar with the HIF-Ph inhibitors, where will these agents likely play and how will they be differentiated from ESAs and, more importantly, from each other?

Renal Anemia (US)

Products Profiled

Commercial Products

AMAG (Feraheme), Amgen (Aranesp, Epogen), American Regent/Luittpold/Vifor (Injectafer), FMC, generics (Venofer ), FMC/Roche (Mircera), Janssen (Procrit), Keryx (Auryxia), Rockwell Medical (Triferic), Sanofi-Genzyme, generics (Ferrlecit)

Pipeline Agents

Akebia/Mitsubishi/Otsuka (Vadadustat), AstraZeneca/Astellas/Fibrogen (Roxadustat), Bayer (Molidustat), GSK (Daprodustat), Hospira/VFMCRP (Retacrit)

Key Dates

• Q1 March

• Q2 June

• Q3 September

• Q4 December

Deliverables

• PowerPoint report

• Frequency table & summary statistics

• On-site presentation

• Proprietary questions (for purchasers

of the annual series)

Related Reports 2018

• RealTime Dynamix:™ Bone and

Mineral US

• RealWorld Dynamix™: Chronic

Kidney Disease US, Nephrology Perspective

• RealWorld Dynamix™: Chronic

Kidney Disease US, PCP Perspective

• Market Dynamix: Renal Anemia

• RealWorld Dynamix™: Dialysis US

To order or to get more information, please contact

[email protected] or call (484) 879-4284