Question 12.3 Accounting by acquirer -...

21

Question 12.3 Accounting by acquirer On 1 July 2016, Angelina Ltd took control of the assets and liabilities of Jolie Ltd. At this date the statement of financial position of Jolie Ltd was as follows: Carrying amount Fair value Machinery $40 000 $67 000 Fixtures & fittings 60 000 68 000 Vehicles 35 000 35 000 Current assets 10 000 12 000 Current liabilities (16 000) (18 000) Total net assets $129 000 Share capital (80 000 shares at $1.00 per share) 80 000 General reserve 20 000 Retained earnings 29 000 Total equity $129 000 Required Prepare the journal entries in the records of Angelina Ltd at 1 July 2016 in each of the following situations, assuming the costs of issuing the shares by Angelina Ltd cost $1600: A. Angelina Ltd issued 80 000 shares having a fair value of $2.40 per share in exchange for the net assets of Jolie Ltd B. Angelina Ltd issued 80 000 shares having a fair value of $2.00 per share in exchange for the net assets of Jolie Ltd. C. Angelina Ltd acquired the shares of Jolie Ltd. The agreement was that Angelina Ltd would pay the shareholders of Jolie Ltd one share in Angelina Ltd for every two shares held in Jolie Ltd plus $1 in cash for each share held in Jolie Ltd. Shares in Angelina Ltd have a fair value of $1.80 per share. A. Acquisition of net assets of Jolie Ltd: FV of an Angelina Ltd shares is $2.40 Net fair value of identifiable assets and liabilities acquired: Machinery $67 000 Fixctures & fittings 68 000 Vehicles 35 000 Current assets 12 000 182 000 Current liabilities (18 000) $164 000 Consideration transferred Shares: 80 000 x $2.40 $192 000 Goodwill = $192 000 - $164 000 $28 000 Journal entries: Angelina Ltd Machinery Dr 67 000 Fixtures & fittings Dr 68 000 Vehicles Dr 35 000 Current assets Dr 12 000 Goodwill Dr 28 000

Transcript of Question 12.3 Accounting by acquirer -...

Question 12.3 Accounting by acquirer On 1 July 2016, Angelina Ltd took control of the assets and liabilities of Jolie Ltd. At this date the statement of financial position of Jolie Ltd was as follows: Carrying amount Fair value Machinery $40 000 $67 000 Fixtures & fittings 60 000 68 000 Vehicles 35 000 35 000 Current assets 10 000 12 000 Current liabilities (16 000) (18 000) Total net assets $129 000 Share capital (80 000 shares at $1.00 per share) 80 000 General reserve 20 000 Retained earnings 29 000 Total equity $129 000 Required Prepare the journal entries in the records of Angelina Ltd at 1 July 2016 in each of the following situations, assuming the costs of issuing the shares by Angelina Ltd cost $1600: A. Angelina Ltd issued 80 000 shares having a fair value of $2.40 per share in exchange

for the net assets of Jolie Ltd B. Angelina Ltd issued 80 000 shares having a fair value of $2.00 per share in exchange

for the net assets of Jolie Ltd. C. Angelina Ltd acquired the shares of Jolie Ltd. The agreement was that Angelina Ltd

would pay the shareholders of Jolie Ltd one share in Angelina Ltd for every two shares held in Jolie Ltd plus $1 in cash for each share held in Jolie Ltd. Shares in Angelina Ltd have a fair value of $1.80 per share.

A. Acquisition of net assets of Jolie Ltd: FV of an Angelina Ltd shares is $2.40 Net fair value of identifiable assets and liabilities acquired: Machinery $67 000 Fixctures & fittings 68 000 Vehicles 35 000 Current assets 12 000 182 000 Current liabilities (18 000) $164 000 Consideration transferred Shares: 80 000 x $2.40 $192 000 Goodwill = $192 000 - $164 000 $28 000 Journal entries: Angelina Ltd Machinery Dr 67 000 Fixtures & fittings Dr 68 000 Vehicles Dr 35 000 Current assets Dr 12 000 Goodwill Dr 28 000

Current liabilities Cr 18 000 Share capital Cr 192 000 (Acquisition of assets and liabilities of Jolie Ltd) Share capital Dr 1 600 Cash Cr 1 600 (Share issue costs) B. Acquisition of net assets of Jolie Ltd: FV of an Angelina Ltd shares is $2.00 Net fair value of net assets acquired $164 000 Consideration transferred Shares: 80 000 x $2.00 $160 000 Gain on bargain purchase = $164 000 - $160 000 $4 000 Journal entries: Jolie Ltd Machinery Dr 67 000 Fixtures & fittings Dr 68 000 Vehicles Dr 35 000 Current assets Dr 12 000 Current liabilities Cr 18 000 Gain on bargain purchase Cr 4 000 Share capital Cr 160 000 (Acquisition of assets & liabilities of Higher Ltd) Share capital Dr 1 600 Cash Cr 1 600 (Share issue costs) C. Acquisition of shares in Jolie Ltd Consideration transferred: Shares: 1/2 x 80 000 x $1.80 $72 000 Cash: $1.00 x 80 000 80 000 $152 000 Journal entries in Angelina Ltd: Shares in Jolie Ltd Dr 152 000 Share capital Cr 72 000 Cash Cr 80 000 (Acquisition of shares in Jolie Ltd) Share capital Dr 1 600 Cash Cr 1 600 (Share issue costs)

Question 12.6 Accounting by the acquirer, provisional accounting, disclosures by the acquirer Matt Ltd was a pharmaceutical company operating in Brisbane while Damon Ltd operated a number of research laboratories on the Gold Coast, being particularly concerned with producing products that were related to the effects of mosquito bites. Matt Ltd believed that the acquisition of Damon Ltd would be of significant benefit to it as Damon Ltd had an excellent research facility that would add value to the products manufactured by Matt Ltd. It was prepared to pay a premium for the assets of Damon Ltd because of the high quality of the research staff of Damon Ltd and their ability to provide synergies between the two companies.

On 1 June 2016, Matt Ltd acquired all the assets and liabilities of Damon Ltd. In exchange for these, Matt Ltd issued 50 000 shares. Based on recent market transactions, it was determined that these shares had a fair value at acquisition date of $3.04. At this date, Matt Ltd could only determine a provisional fair value for the machinery. Matt Ltd also recognised an intangible asset relating to research and development undertaken by Damon Ltd, but it was not recognised by that entity as it did not meet the recognition criteria under AASB 138 Intangible Assets. This asset was considered to have a fair value of $4000.

Subsequent to the end of the reporting period of 30 June 2016, the final fair value was determined on 2 September 2016 to be $104 800. Depreciation on machinery was charged at 20% p.a. The assets and liabilities of Damon Ltd at 1 June 2016 were as follows: Carrying amount Fair value Machinery $98 000 $100 000 Fixtures 15 000 16 000 Accounts receivable 20 000 20 000 Cash 24 000 24 000 Accounts payable (6 400) (6 400) Loans (13 600) (13 600) Required A. Prepare the journal entries at 1 June 2016 in the accounting records of Matt Ltd to

record the acquisition of Damon Ltd as well as any disclosures regarding the acquisition in the notes to the accounts at 30 June 2016.

B. Prepare any journal entries at 2 September 2016 in relation to the provisional measurement of the machine.

A: At 1 June 2016: Net fair value of identifiable assets and liabilities of Damon Ltd = $100 000 + $16 000 + $20 000 + $24 000 +$4 000 - $6 400 - $13 600 = $144 000 Consideration transferred = 50 000 shares x $3.04 = $152 000 Goodwill = $152 000 - $144 000 = $8 000

The journal entries at acquisition date, 1 June 2016 are: Machinery Dr 100 000 Fixtures Dr 16 000 In-process research and development Dr 4 000 Accounts receivable Dr 20 000 Cash Cr 24 000 Goodwill Dr 8 000 Accounts payable Cr 6 400 Loans Cr 13 600 Share capital Cr 152 000 (Acquisition of assets and liabilities of Damon Ltd) Check disclosures against the following paragraphs from AASB 3 Appendix B: Paragraph B64 (a) the names and descriptions of the combining businesses [Matt Ltd is a

pharmaceutical company; Damon Ltd is a company involved in research] B64 (b) the acquisition date: 1 June 2016 B64 (d) primary reasons for the business combination [ R&D] B64 (e) a qualitative description of the factors making up goodwill [excellent work force

and synergies] B64 (f) the consideration transferred: $152 000 Fair value of each major class of consideration, including for equity instruments issued:

- the number [50 000] - the method of determining fair value [recent market transactions]

B64 (i) amounts recognised for each major class of assets acquired and liabilities assumed [see journal entry]

B. See paragraphs 45-50 of AASB 3 in relation to initial accounting determined provisionally. At 1 June 2016, the provisional amounts must be used as per journal entries in (A.) on the previous page. Note the disclosure required by paragraph B67 of AASB 3. In 2016, as per paragraph 45, the carrying amount of the machinery must be calculated as if its fair value at the acquisition date had been recognised from that date, with an adjustment to goodwill. If the machinery had a 5-year life from acquisition date, Damon Ltd would have charged depreciation for 1 month in 2016. Extra depreciation of $80 is required, being 1/5 x 1/12 x $4 800. The adjusting entry at 2 September 2016 is: Machinery Dr 4 800 Goodwill Cr 4 800 (Adjustment for provisional accounting) Retained earnings (1/7/16) Dr 80 Accumulated depreciation Cr 80 (Adjustment to depreciation due to provisional accounting) If depreciation has been calculated monthly for 2016, further adjustments would be required.

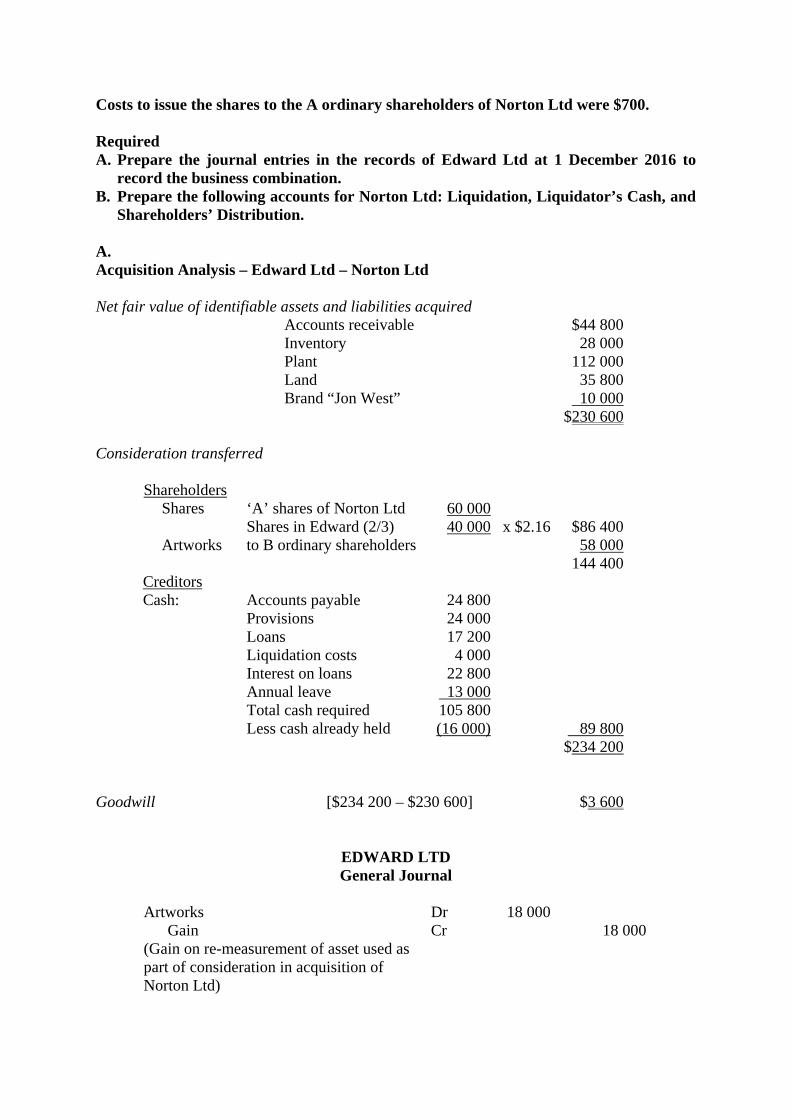

Question 12.10 Accounting by the acquirer, liquidation of the acquiree Edward Ltd is a manufacturer of frozen foods in Geelong. His products include many forms of vegetables and meats but one item lacking in its product range is frozen fish. The board of Edward Ltd decided to investigate a takeover of a Tasmanian company, Norton Ltd, whose prime product was the packaging of frozen Huon salmon. The reason this company was of particular interest was that Edward Ltd already owned a number of factories in Hobart some of which were under-utilized. If Norton were acquired, then Edward Ltd would liquidate the company and transfer all the processing work to its other Hobart factories.

The financial statements of Norton Ltd at 1 December 2016 showed the following information:

Plant $133 600 Accumulated depreciation – plant (32 000) Land 20 800 Cash 16 000 Accounts receivable 44 800 Inventory 23 200 Total assets 206 400 Accounts payable 24 800 Provisions 24 000 Loans 17 200 Total liabilities 66 000 Share capital – 60 000 A ordinary shares 48 000 – 40 000 B ordinary shares 32 000 Retained earnings 60 400 Total equity 140 400

All the assets and liabilities of Norton Ltd were recorded at amounts equal to fair

value except for: Fair value Plant 112 000 Land 35 800 Inventory 28 000

Norton Ltd also had a brand ‘Jon West’ that was not recorded by the company because it had been internally generated. It was valued at $10 000. Norton Ltd had not recorded both the interest accrued on the loans amounting to $22 800 and annual leave entitlements of $13 000.

Edward Ltd decided to acquire all the assets of Norton Ltd except for the cash. In exchange for these assets, Edward Ltd agreed to provide: Two shares in Edward Ltd for every three A ordinary shares held in Norton Ltd. The

fair value of each Edward Ltd share was agreed to be $2.16. Artworks to the owners of the B ordinary shares held in Norton Ltd. (These artworks

were held in the records of Edward Ltd at $40 000 and valued at $58 000.) Sufficient additional cash to enable Norton Ltd to pay off its liabilities including the

expected liquidation costs of $4000. The business combination occurred on 1 December 2016. Legal and accounting costs

incurred by Edward Ltd in undertaking this business combination amounted to $1300.

Costs to issue the shares to the A ordinary shareholders of Norton Ltd were $700. Required A. Prepare the journal entries in the records of Edward Ltd at 1 December 2016 to

record the business combination. B. Prepare the following accounts for Norton Ltd: Liquidation, Liquidator’s Cash, and

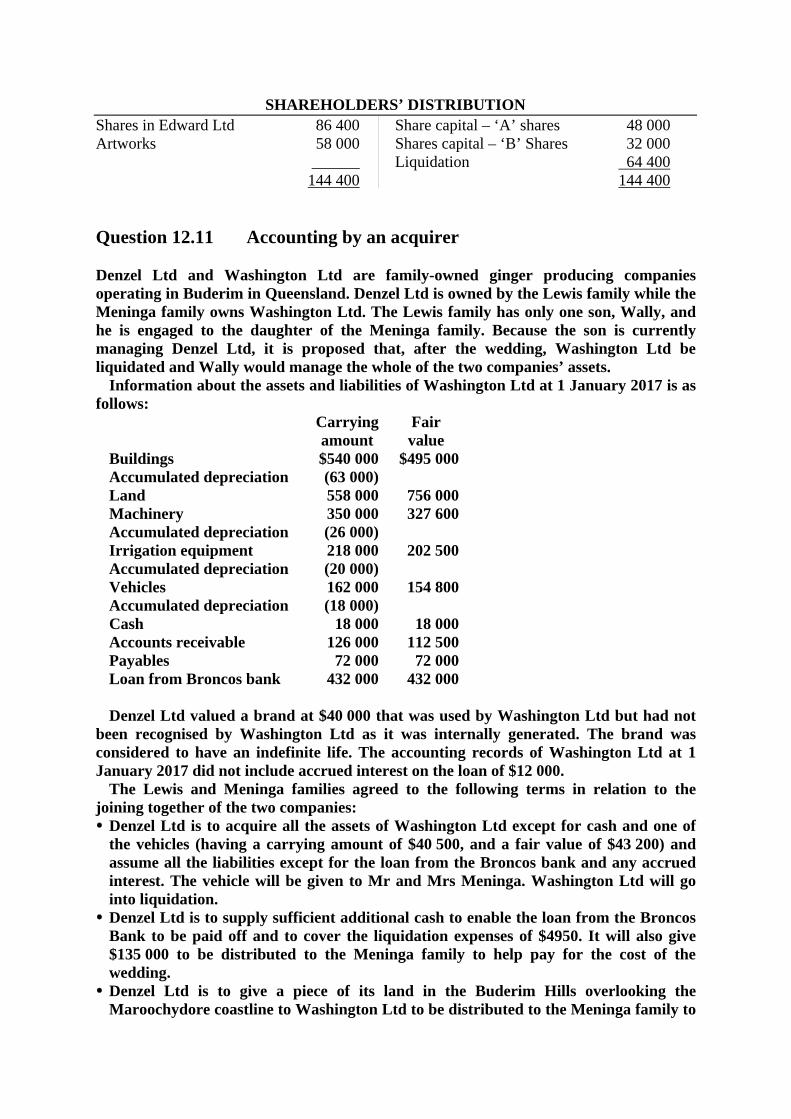

Shareholders’ Distribution. A. Acquisition Analysis – Edward Ltd – Norton Ltd Net fair value of identifiable assets and liabilities acquired Accounts receivable $44 800 Inventory 28 000 Plant 112 000 Land 35 800 Brand “Jon West” 10 000 $230 600 Consideration transferred Shareholders Shares ‘A’ shares of Norton Ltd 60 000 Shares in Edward (2/3) 40 000 x $2.16 $86 400 Artworks to B ordinary shareholders 58 000 144 400 Creditors Cash: Accounts payable 24 800 Provisions 24 000 Loans 17 200 Liquidation costs 4 000 Interest on loans 22 800 Annual leave 13 000 Total cash required 105 800 Less cash already held (16 000) 89 800 $234 200 Goodwill [$234 200 – $230 600] $3 600

EDWARD LTD General Journal

Artworks Dr 18 000 Gain Cr 18 000 (Gain on re-measurement of asset used as part of consideration in acquisition of Norton Ltd)

Accounts receivable Dr 44 800 Inventory Dr 28 000 Plant Dr 112 000 Land Dr 35 800 Brand Dr 10 000 Goodwill Dr 3 600 Payable to Norton Ltd Cr 89 800 Share capital Cr 86 400 Artworks Cr 58 000 (Acquisition of Norton Ltd) Payable to Norton Ltd Dr 89 800 Cash Cr 89 800 (Payment of consideration) Acquisition-related expenses Dr 1 300 Cash Cr 1 300 (Payment of acquisition-related costs) Share capital Dr 700 Cash Cr 700 (Payment of share issue costs) B.

NORTON LTD General Ledger

LIQUIDATION ACCOUNT

Receivables 44 800 Retained earnings 60 400 Inventory 23 200 Accumulated depreciation 32 000 Plant 133 600 Receivable from Edward Ltd 234 200 Land 20 800 Interest on loans 22 800 Annual leave payable 13 000 Liquidation costs 4 000 Shareholders’ distribution 64 400 - 326 600 326 600

LIQUIDATOR’S CASH ACCOUNT Opening balance 16 000 Accounts payable 24 800 Edward Ltd 89 800 Provisions 24 000 Loans 17 200 Liquidation costs 4 000 Interest payable 22 800 ______ Annual leave 13 000 105 800 105 800

SHAREHOLDERS’ DISTRIBUTION Shares in Edward Ltd 86 400 Share capital – ‘A’ shares 48 000 Artworks 58 000 Shares capital – ‘B’ Shares 32 000 ______ Liquidation 64 400 144 400 144 400

Question 12.11 Accounting by an acquirer

Denzel Ltd and Washington Ltd are family-owned ginger producing companies operating in Buderim in Queensland. Denzel Ltd is owned by the Lewis family while the Meninga family owns Washington Ltd. The Lewis family has only one son, Wally, and he is engaged to the daughter of the Meninga family. Because the son is currently managing Denzel Ltd, it is proposed that, after the wedding, Washington Ltd be liquidated and Wally would manage the whole of the two companies’ assets.

Information about the assets and liabilities of Washington Ltd at 1 January 2017 is as follows:

Carrying amount

Fair value

Buildings $540 000 $495 000Accumulated depreciation (63 000)Land 558 000 756 000Machinery 350 000 327 600Accumulated depreciation (26 000)Irrigation equipment 218 000 202 500Accumulated depreciation (20 000)Vehicles 162 000 154 800Accumulated depreciation (18 000)Cash 18 000 18 000Accounts receivable 126 000 112 500Payables 72 000 72 000Loan from Broncos bank 432 000 432 000 Denzel Ltd valued a brand at $40 000 that was used by Washington Ltd but had not

been recognised by Washington Ltd as it was internally generated. The brand was considered to have an indefinite life. The accounting records of Washington Ltd at 1 January 2017 did not include accrued interest on the loan of $12 000.

The Lewis and Meninga families agreed to the following terms in relation to the joining together of the two companies: Denzel Ltd is to acquire all the assets of Washington Ltd except for cash and one of

the vehicles (having a carrying amount of $40 500, and a fair value of $43 200) and assume all the liabilities except for the loan from the Broncos bank and any accrued interest. The vehicle will be given to Mr and Mrs Meninga. Washington Ltd will go into liquidation. Denzel Ltd is to supply sufficient additional cash to enable the loan from the Broncos

Bank to be paid off and to cover the liquidation expenses of $4950. It will also give $135 000 to be distributed to the Meninga family to help pay for the cost of the wedding. Denzel Ltd is to give a piece of its land in the Buderim Hills overlooking the

Maroochydore coastline to Washington Ltd to be distributed to the Meninga family to

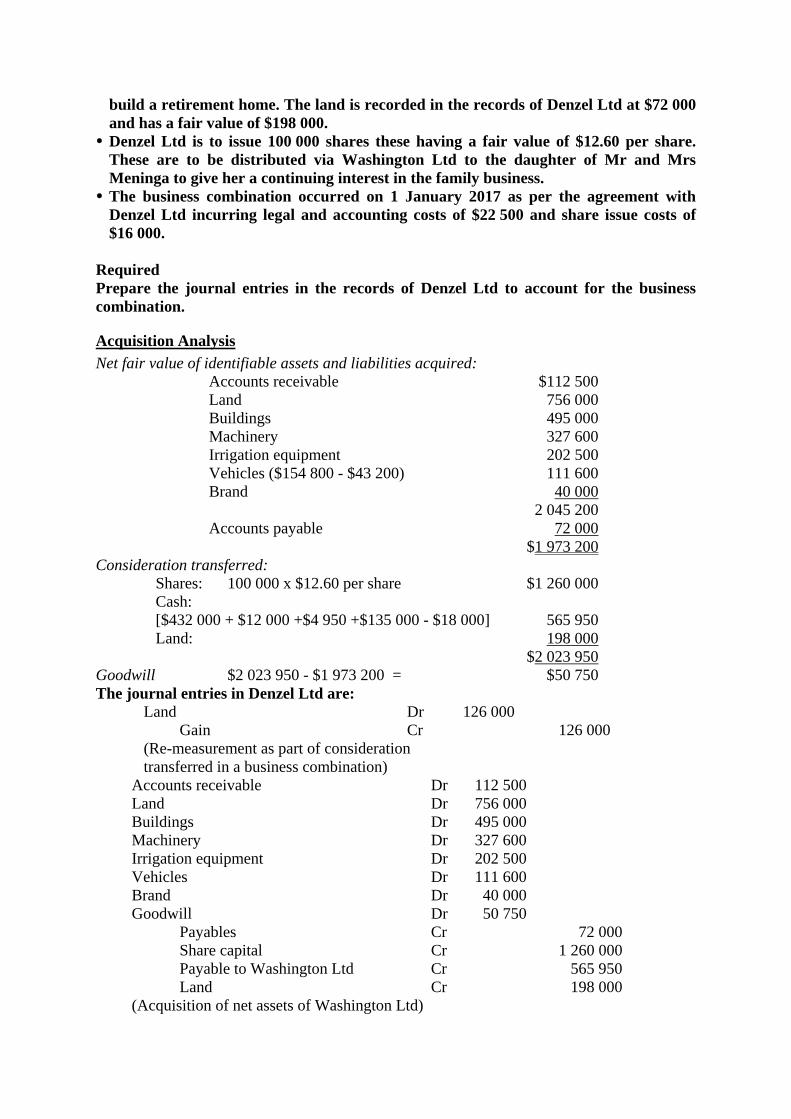

build a retirement home. The land is recorded in the records of Denzel Ltd at $72 000 and has a fair value of $198 000. Denzel Ltd is to issue 100 000 shares these having a fair value of $12.60 per share.

These are to be distributed via Washington Ltd to the daughter of Mr and Mrs Meninga to give her a continuing interest in the family business. The business combination occurred on 1 January 2017 as per the agreement with

Denzel Ltd incurring legal and accounting costs of $22 500 and share issue costs of $16 000.

Required Prepare the journal entries in the records of Denzel Ltd to account for the business combination.

Acquisition Analysis

Net fair value of identifiable assets and liabilities acquired: Accounts receivable $112 500 Land 756 000 Buildings 495 000 Machinery 327 600 Irrigation equipment 202 500 Vehicles ($154 800 - $43 200) 111 600 Brand 40 000 2 045 200 Accounts payable 72 000 $1 973 200 Consideration transferred: Shares: 100 000 x $12.60 per share $1 260 000 Cash: [$432 000 + $12 000 +$4 950 +$135 000 - $18 000] 565 950 Land: 198 000 $2 023 950 Goodwill $2 023 950 - $1 973 200 = $50 750 The journal entries in Denzel Ltd are: Land Dr 126 000 Gain Cr 126 000 (Re-measurement as part of consideration transferred in a business combination) Accounts receivable Dr 112 500 Land Dr 756 000 Buildings Dr 495 000 Machinery Dr 327 600 Irrigation equipment Dr 202 500 Vehicles Dr 111 600 Brand Dr 40 000 Goodwill Dr 50 750 Payables Cr 72 000 Share capital Cr 1 260 000 Payable to Washington Ltd Cr 565 950 Land Cr 198 000 (Acquisition of net assets of Washington Ltd)

Payable to Washington Ltd Dr 565 950 Cash Cr 565 950 (Payment of purchase consideration) Acquisition-related expenses Dr 22 500 Cash Cr 22 500 (Payment of acquisition-related costs) Share capital Dr 16 000 Cash Cr 16 000 (Share issue costs)

Question 16.8 The reconstruction of accounts (formulae) approach The statements of financial position of Allthrough Ltd as at 30 June 2017 and 30 June 2016 are presented below. ALLTHROUGH LTD

Statements of Financial Position as at 30 June

2017 2016 Current assets

Cash at bank Accounts receivable Inventory Prepayments Non-current assets

$ — 127 200275 000 22 800

$ 74 600

111 300221 200 23 000

Buildings Accumulated depreciation – buildings Equipment Accumulated depreciation – equipment Land Long-term investments Total assets

639 000(111 400361 200(89 900

168 000 70 000

1 461 900

) )

$

339 000(97 600331 200(67 000

39 000 160 0001 134 700

) )

Current liabilities Bank overdraft Accounts payable Accrued expenses Current tax liability

$ 16 700215 00010 500

26 000

$ —

218 00014 000

24 000

Non-current liabilities Loan payable Debentures due 1/9/21 Total liabilities

$ 240 000 300 000 808 200

$ 150 000

200 000 606 000

Net assets Equity Share capital Retained earnings Total equity

$

$

653 700

502 100 151 600 653 700

$

$

528 700

388 100 140 600 528 700

Examination of the company’s general ledger accounts revealed the following: (a) Depreciation expense was recorded during the year as follows: buildings $13 800;

and equipment $22 900.

(b) An extension was added to the building at a cost of $300 000 cash. (c) Long-term investments with a cost of $90 000 were sold for $125 000. (d) Vacant land next to the company’s plant was purchased for $129 000 with payment

consisting of $39 000 cash and a loan payable for $90 000 due on 31 July 2018. (e) Debentures of $100 000 were issued for cash at nominal value. (f) Thirty thousand shares were issued at $3.80 per share. (g) Equipment was purchased for cash. (h) Sales for the period were $875 600; cost of sales amounted to $525 300; other

expenses (excluding depreciation, carrying amount of investments sold, interest, and bad debts) amounted to $149 400.

(i) Bad debts of $3500 were written off. (j) Income tax paid during the year amounted to $73 700. (k) Interest expense and interest paid amounted to $40 000. (l) The bank overdraft is integral part of the company’s cash management function. Required A. Prepare the statement of cash flows of Allthrough Ltd for the year ended 30 June

2017 using the direct method of presentation. B. Prepare a note disclosure to reconcile net cash flows from operating activities with

the profit for the year and also prepare any other notes required by AASB 107. A.

ALLTHROUGH LTD Statement of Cash Flows

for the year ended 30 June 2017 Cash flows from operating activities Cash receipts from customers $856 200 Cash paid to suppliers, employees and other (734 800) Cash generated from operations 121 400 Interest paid (40 000) Income taxes paid (73 700) Net cash from operating activities $7 700 Cash flows from investing activities Payment for equipment (30 000) Payments for property (339 000) Proceeds from sale of investments 125 000 Net cash used in investing activities (244 000) Cash flows from financing activities Proceeds from issue of shares 114 000 Proceeds from issue of debentures 100 000 Dividends paid (69 000) Net cash provided by financing activities 145 000 Net decrease in cash and cash equivalents (91 300) Cash and cash equivalents at beginning of period 74 600 Cash and cash equivalents at end of period $(16 700)

B. Note 1: Cash and cash equivalents Cash and cash equivalents included in the statement of cash flows are comprised of the following amounts included in the statement of financial position: 2017 2016 Cash at bank $ – $ 74 600 Bank Overdraft (16 700) – Cash and cash equivalents $(16 700) $ 74 600 The bank overdraft is integral to the company’s cash management function. Note 2: Non-cash Financing and Investing Activities During the period, property was acquired for $129 000, part of the purchase consideration amounting to $90 000 is deferred until July 2018 Note 3: Reconciliation of Net Cash from Operating Activities with Profit Profit for the year $80 000 Depreciation 36 700 Gain on sale of investments (35 000) Change in assets and liabilities Increase in accounts receivable (15 900) Increase in inventory (53 800) Decrease in prepayments 200 Decrease in accounts payable (3 000) Decrease in accrued expenses (3 500) Increase in current tax liability 2 000 Net cash from operating activities $7 700 Workings Receipts from customers

Accounts Receivable Balance b/d 111 300 Bad debts expense 3 500 Sales 875 600 Cash (from customers) 856 200 Balance c/d 127 200 986 900 986 900

Received Begin Ending From Accounts accounts Bad debts Customers = Sales + rec'able - Rec'able - $856 200 = $875 600 + $111 300 - $127 200 $3 500

Payments to suppliers, employees and other

Inventory Balance b/d 221 200 Cost of sales 525 300 A/c Payable (purchases)* 579 100 Balance c/d 275 000 800 300 800 300 *balancing item for reconstruction

Accounts Payable Cash (paid to suppliers) 582 100 Balance b/d 218 000 Balance c/d 215 000 Inventory (purchases) 579 100 797 100 797 100

Payments Begin Ending suppliers Cost of Begin Ending Accts Accts of goods = sales - invent + invent. + payable - Payable $582 100 = $525 300 - $221 200 + $275 000 + $218 000 - $215 000

Prepayments and Accrued Expenses Liability (Net) Balance b/d 9 000 Other operating expenses 149 400 Cash (paid employees/other) 152 700 Balance c/d 12 300 161 700 161 700

Payments Begin. Ending Begin Ending Employees accrued accrued prepaid prepaid Other = Expense + expenses - expenses - expenses + expenses $152 700 = $149 400 + $14 000 - $10 500 - $23 000 + $22 800

Cash payments to suppliers and employees = $582 100 + $152 700 = $734 800 Income tax paid

Current Tax Liability Cash (income tax paid) 73 700 Balance b/d 24 000 Balance c/d 26 000 Income tax expense* 75 700 99 700 99 700 *balancing item for reconstruction

Dividends paid

Profit or Loss Summary Cost of sales 525 300 Sales revenue 875 600 Other operating expenses 149 400 Proceeds from sale of invest 125 000

Depn expense - buildings 13 800 Depn expense - equipment 22 900 Cost of investments sold 90 000

Bad debts expense 3 500 Interest expense 40 000

Income tax expense 75 700 Profit for the year* 80 000

1 000 600 1 000 600 *balancing item for reconstruction

Retained Earnings Dividends paid 69 000 Balance b/d 140 600 Balance c/d 151 600 Profit 80 000 220 600 220 600 Other Explanations: Interest paid – additional info item (k) Income taxes paid – additional info item (j) Purchase of equipment – additional info item (g) ($361 200 – $331 200 = $30 000) Purchase of property – additional info items (b) and (d) ($300 000 + 39 000 = $339 000) Proceeds from sale of investments – additional info item (c ) Proceeds from issue of shares – additional info item (f) (30 000 x $3.80= $114 000) Proceeds from long term borrowings – additional info item (e)

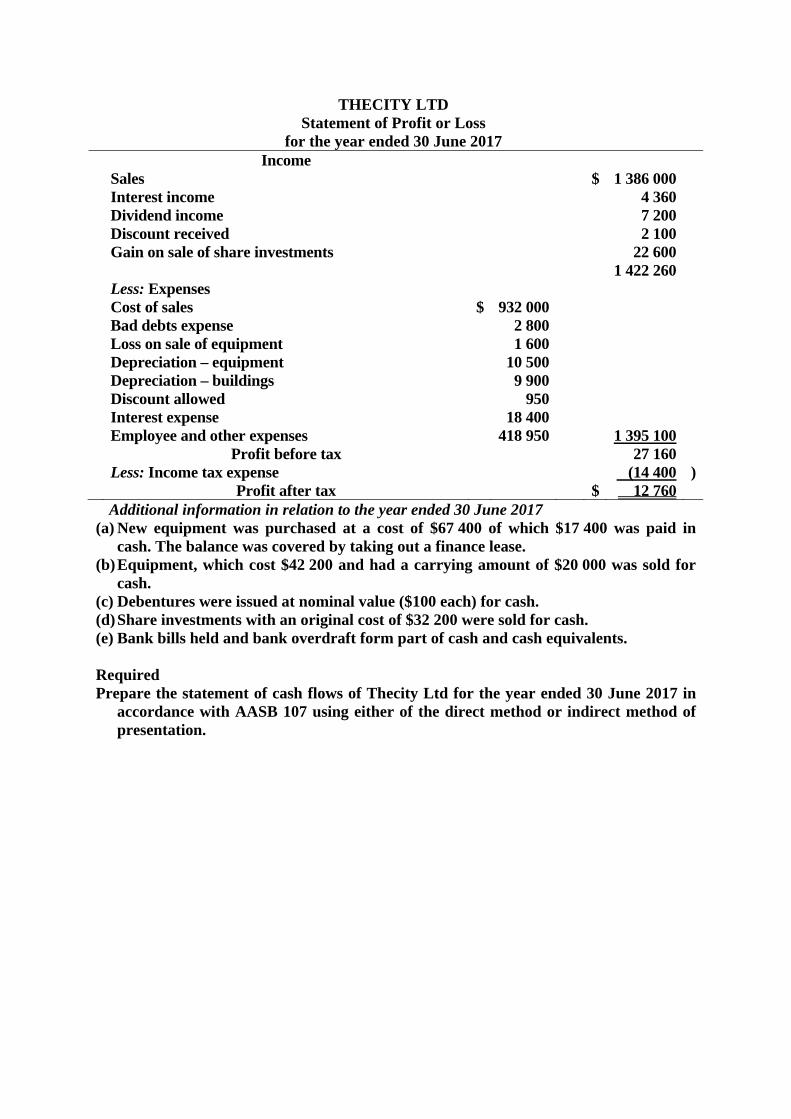

Question 16.9 The reconstruction of accounts (formulae) approach

The draft statements of financial position of Thecity Ltd as at 30 June 2017 and 30 June 2016 are presented below.

THECITY LTD Statements of Financial Position

as at 30 June 2017 2016 Assets

Cash at bank Bank bills Deposits at call Accounts receivable Allowance for doubtful debts Inventory Prepaid expenses

$ 54 80010 0006 400

49 300(2 50094 20010 800

)

$ 42 000

8 6005 000

37 800(1 90096 6004 200

)

Interest receivable Share investments Land Buildings Accumulated depreciation – buildings Equipment Accumulated depreciation – equipment Deferred tax asset

(

1 60035 60070 000

360 000104 400180 000(57 900

14 400

) )

1 80067 80070 000

240 000(94 500154 800(69 600 12 200

) )

Total assets $ 722 300 $ 574 800 Liabilities

Accounts payable Accrued expenses Interest payable Current tax liability Bank overdraft Finance lease Debentures (10%) Deferred tax liability Equity Share capital (ordinary shares, issued at $1) Retained earnings

$ 120 5209 7804 000

13 60034 80050 000

180 00023 000

206 240 80 360

$ 93 960

8 3403 000

15 00032 000

—150 00020 000

184 900 67 600

Total liabilities and equity $ 722 300 $ 574 800

THECITY LTD Statement of Profit or Loss

for the year ended 30 June 2017 Income

Sales Interest income Dividend income Discount received Gain on sale of share investments

$ 1 386 000

4 3607 2002 100

22 600

Less: Expenses Cost of sales Bad debts expense Loss on sale of equipment Depreciation – equipment Depreciation – buildings Discount allowed Interest expense Employee and other expenses

$ 932 0002 8001 600

10 5009 900

95018 400

418 950

1 422 260

1 395 100

Profit before tax Less: Income tax expense

27 160 (14 400

)

Profit after tax $ 12 760 Additional information in relation to the year ended 30 June 2017

(a) New equipment was purchased at a cost of $67 400 of which $17 400 was paid in cash. The balance was covered by taking out a finance lease.

(b) Equipment, which cost $42 200 and had a carrying amount of $20 000 was sold for cash.

(c) Debentures were issued at nominal value ($100 each) for cash. (d) Share investments with an original cost of $32 200 were sold for cash. (e) Bank bills held and bank overdraft form part of cash and cash equivalents. Required Prepare the statement of cash flows of Thecity Ltd for the year ended 30 June 2017 in

accordance with AASB 107 using either of the direct method or indirect method of presentation.

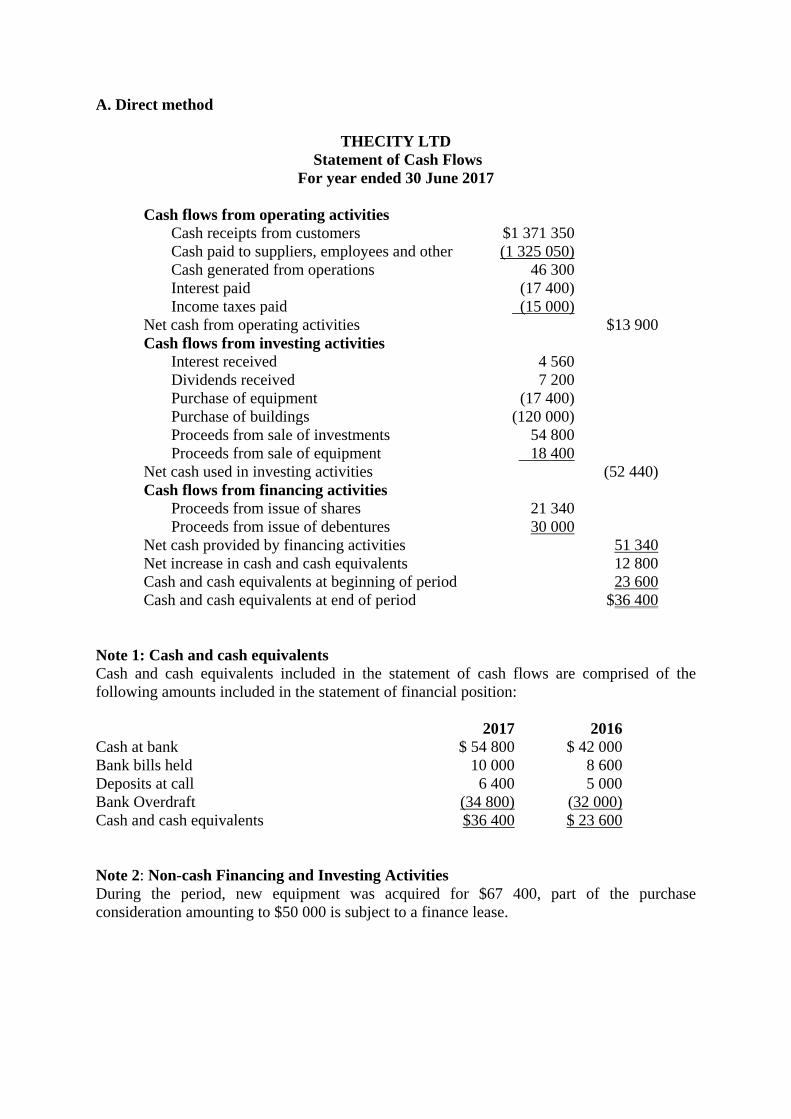

A. Direct method

THECITY LTD Statement of Cash Flows

For year ended 30 June 2017 Cash flows from operating activities Cash receipts from customers $1 371 350 Cash paid to suppliers, employees and other (1 325 050) Cash generated from operations 46 300 Interest paid (17 400) Income taxes paid (15 000) Net cash from operating activities $13 900 Cash flows from investing activities Interest received 4 560 Dividends received 7 200 Purchase of equipment (17 400) Purchase of buildings (120 000) Proceeds from sale of investments 54 800 Proceeds from sale of equipment 18 400 Net cash used in investing activities (52 440) Cash flows from financing activities Proceeds from issue of shares 21 340 Proceeds from issue of debentures 30 000 Net cash provided by financing activities 51 340 Net increase in cash and cash equivalents 12 800 Cash and cash equivalents at beginning of period 23 600 Cash and cash equivalents at end of period $36 400 Note 1: Cash and cash equivalents Cash and cash equivalents included in the statement of cash flows are comprised of the following amounts included in the statement of financial position: 2017 2016 Cash at bank $ 54 800 $ 42 000 Bank bills held 10 000 8 600 Deposits at call 6 400 5 000 Bank Overdraft (34 800) (32 000) Cash and cash equivalents $36 400 $ 23 600 Note 2: Non-cash Financing and Investing Activities During the period, new equipment was acquired for $67 400, part of the purchase consideration amounting to $50 000 is subject to a finance lease.

Workings Receipts from customers

Allowance for Doubtful Debts Accounts receivable* (bad debts written off)

2 200 Balance b/d 1 900

Balance c/d 2 500 Bad debts expense 2 800 4 700 4 700 *balancing item for reconstruction

Accounts Receivable Balance b/d 37 800 Allowance for doubt debts 2 200 Sales revenue 1 386 000 (bad debts written off) Discount allowed 950 Cash (from customers) 1 371 350 Balance c/d 49 300 1 423 800 1 423 800

Cash receipts = Sales – Increase in Accounts Receivable – Bad debts written off – Discount allowed

= 1 386 000 – 11 500 – 2 200 – 950 = 1 371 350

Payments to suppliers, employees and other

Inventory Balance b/d 96 600 Cost of sales 932 000 A/c Payable (purchases)* 929 600 Balance c/d 94 200 1 026 200 1 026 200 *balancing item for reconstruction

Accounts Payable Discount received 2 100 Balance b/d 93 960 Cash (paid to suppliers) 900 940 Inventory (purchases) 929 600

Balance c/d 120 520 1 023 560 1 023 560

Prepaid Expenses / Accrued Expenses Liability (Net) Balance b/d (Prepaid exp) 4 200 Balance b/d (Accrued exp) 8 340 Cash (paid employees/other) 424 110 Employee other expenses 418 950

Balance c/d (Accrued exp) 9 780 Balance c/d (Prepaid exp) 10 800 438 090 438 090 Cash paid to suppliers & employees = $900 940 + $424 110 = $1 325 050

Cash paid = Cost of sales + Employee/Other expenses – Discount received – Decrease in Inventory – Increase in Accounts Payable + Increase in Prepaid expenses – Increase in Accrued Expenses

= 932 000 + 418 950 – 2 100 – 2 400 – 26 560 + 6 600 – 1 440 = 1 325 050

Interest paid

Interest Payable Cash (interest paid) 17 400 Balance b/d 3 000 Balance c/d 4 000 Interest expense 18 400 21 400 21 400

Interest paid = Interest Expense – Increase in Interest Payable = 18 400 – 1 000 = 17 400

Income taxes paid Journal entry: Income Tax Expense Dr 14 400 Deferred Tax Asset Dr 2 200 Current Tax Liability Cr 13 600 Deferred Tax Liability Cr 3 000

Current Tax Liability Cash (income tax paid) 15 000 Balance b/d 15 000 Balance c/d 13 600 ITE/DTA/DTL 13 600 28 600 28 600

Income tax paid = Income tax expense + Decrease in Current tax liability + Increase in Deferred tax asset – Increase in Deferred tax liability

= 14 400 + 2 200 + 1 400 – 3 000 = 15 000

Interest received

Interest Receivable Balance b/d 1 800 Cash (interest received) 4 560 Interest income 4 360 Balance c/d 1 600 6 160 6 160 Interest received = Interest Income + Decrease in Interest Receivable

= 4 360 + 200 = 4 560

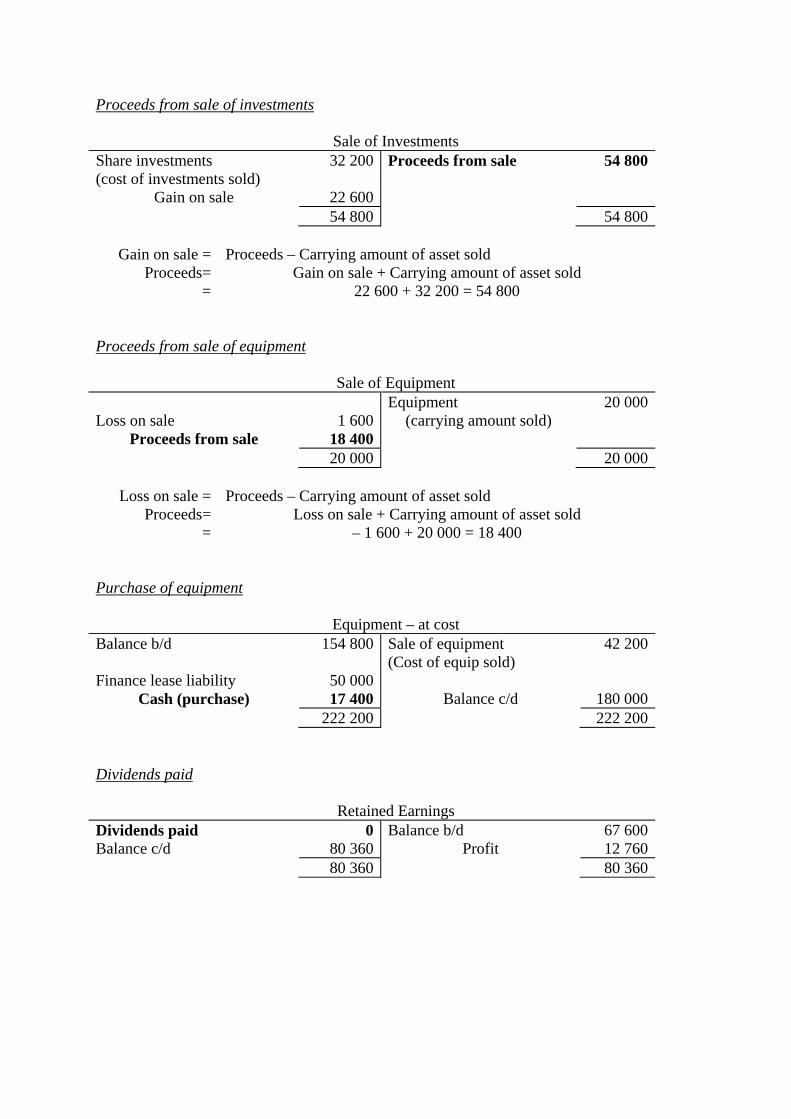

Proceeds from sale of investments

Sale of Investments Share investments 32 200 Proceeds from sale 54 800 (cost of investments sold)

Gain on sale 22 600 54 800 54 800

Gain on sale = Proceeds – Carrying amount of asset sold Proceeds= Gain on sale + Carrying amount of asset sold

= 22 600 + 32 200 = 54 800 Proceeds from sale of equipment

Sale of Equipment Equipment 20 000 Loss on sale 1 600 (carrying amount sold)

Proceeds from sale 18 400 20 000 20 000

Loss on sale = Proceeds – Carrying amount of asset sold Proceeds= Loss on sale + Carrying amount of asset sold

= – 1 600 + 20 000 = 18 400 Purchase of equipment

Equipment – at cost Balance b/d 154 800 Sale of equipment

(Cost of equip sold) 42 200

Finance lease liability 50 000 Cash (purchase) 17 400 Balance c/d 180 000

222 200 222 200 Dividends paid

Retained Earnings Dividends paid 0 Balance b/d 67 600 Balance c/d 80 360 Profit 12 760 80 360 80 360

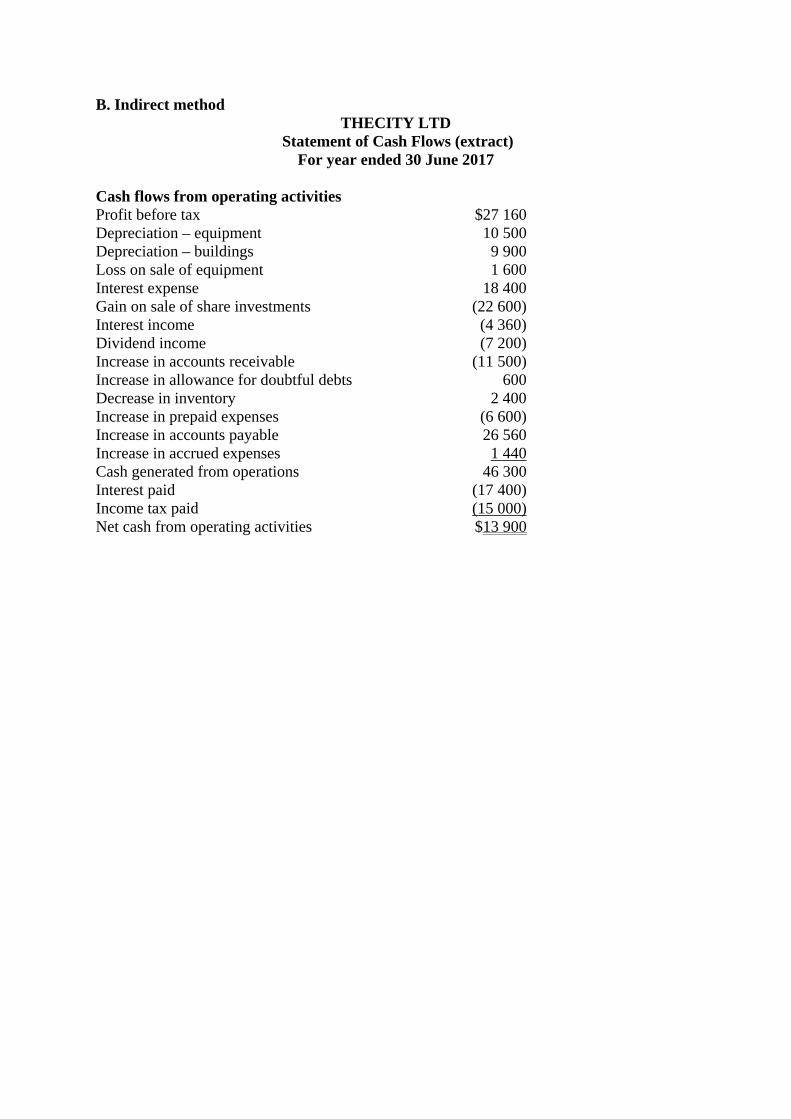

B. Indirect method THECITY LTD

Statement of Cash Flows (extract) For year ended 30 June 2017

Cash flows from operating activities Profit before tax $27 160 Depreciation – equipment 10 500 Depreciation – buildings 9 900 Loss on sale of equipment 1 600 Interest expense 18 400 Gain on sale of share investments (22 600) Interest income (4 360) Dividend income (7 200) Increase in accounts receivable (11 500) Increase in allowance for doubtful debts 600 Decrease in inventory 2 400 Increase in prepaid expenses (6 600) Increase in accounts payable 26 560 Increase in accrued expenses 1 440 Cash generated from operations 46 300 Interest paid (17 400) Income tax paid (15 000) Net cash from operating activities $13 900

![TIN & Surface Interpolationweb.pdx.edu/~jduh/courses/geog493f12/Week06.pdfMicrosoft PowerPoint - Week06.ppt [Compatibility Mode] Author jduh Created Date 10/29/2012 6:25:57 PM ...](https://static.fdocuments.us/doc/165x107/5f832bbbe5e1454be4340ebc/tin-surface-jduhcoursesgeog493f12week06pdf-microsoft-powerpoint-week06ppt.jpg)

![PRBL004 - Lecture 6 - External Administration.ppt [Read-Only]learnline.cdu.edu.au/units/lbaresources/bus/prbl... · 3 Sophisticated investor exemption s 708(8) – (11) Do not need](https://static.fdocuments.us/doc/165x107/5e3bf9c6c91f0f46fb5c4bb5/prbl004-lecture-6-external-read-onlylearnlinecdueduauunitslbaresourcesbusprbl.jpg)