Q1 2017 Warsaw Office Market -...

4

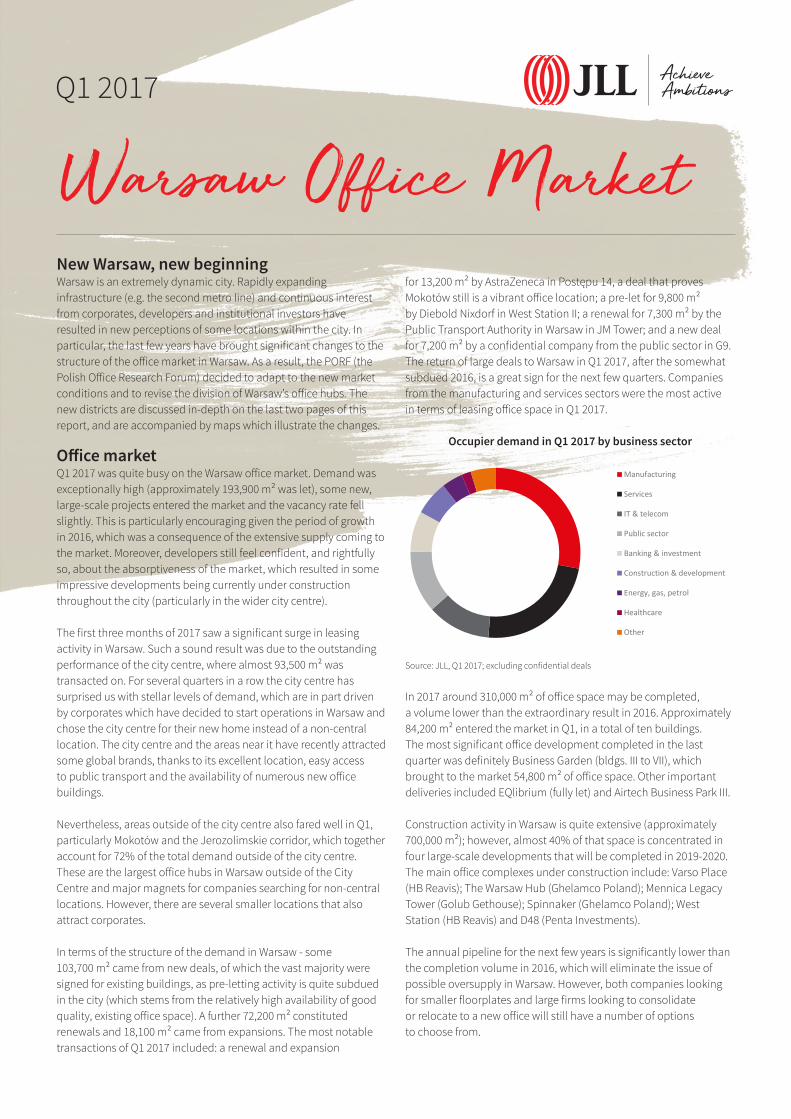

Warsaw Offi Mart Q1 2017 New Warsaw, new beginning Warsaw is an extremely dynamic city. Rapidly expanding infrastructure (e.g. the second metro line) and continuous interest from corporates, developers and institutional investors have resulted in new perceptions of some locations within the city. In particular, the last few years have brought significant changes to the structure of the office market in Warsaw. As a result, the PORF (the Polish Office Research Forum) decided to adapt to the new market conditions and to revise the division of Warsaw’s office hubs. The new districts are discussed in-depth on the last two pages of this report, and are accompanied by maps which illustrate the changes. Office market Q1 2017 was quite busy on the Warsaw office market. Demand was exceptionally high (approximately 193,900 m² was let), some new, large-scale projects entered the market and the vacancy rate fell slightly. This is particularly encouraging given the period of growth in 2016, which was a consequence of the extensive supply coming to the market. Moreover, developers still feel confident, and rightfully so, about the absorptiveness of the market, which resulted in some impressive developments being currently under construction throughout the city (particularly in the wider city centre). The first three months of 2017 saw a significant surge in leasing activity in Warsaw. Such a sound result was due to the outstanding performance of the city centre, where almost 93,500 m² was transacted on. For several quarters in a row the city centre has surprised us with stellar levels of demand, which are in part driven by corporates which have decided to start operations in Warsaw and chose the city centre for their new home instead of a non-central location. The city centre and the areas near it have recently attracted some global brands, thanks to its excellent location, easy access to public transport and the availability of numerous new office buildings. Nevertheless, areas outside of the city centre also fared well in Q1, particularly Mokotów and the Jerozolimskie corridor, which together account for 72% of the total demand outside of the city centre. These are the largest office hubs in Warsaw outside of the City Centre and major magnets for companies searching for non-central locations. However, there are several smaller locations that also attract corporates. In terms of the structure of the demand in Warsaw - some 103,700 m² came from new deals, of which the vast majority were signed for existing buildings, as pre-letting activity is quite subdued in the city (which stems from the relatively high availability of good quality, existing office space). A further 72,200 m² constituted renewals and 18,100 m² came from expansions. The most notable transactions of Q1 2017 included: a renewal and expansion for 13,200 m² by AstraZeneca in Postępu 14, a deal that proves Mokotów still is a vibrant office location; a pre-let for 9,800 m² by Diebold Nixdorf in West Station II; a renewal for 7,300 m² by the Public Transport Authority in Warsaw in JM Tower; and a new deal for 7,200 m² by a confidential company from the public sector in G9. The return of large deals to Warsaw in Q1 2017, aſter the somewhat subdued 2016, is a great sign for the next few quarters. Companies from the manufacturing and services sectors were the most active in terms of leasing office space in Q1 2017. Occupier demand in Q1 2017 by business sector Manufacturing Services IT & telecom Public sector Banking & investment Construction & development Energy, gas, petrol Healthcare Other Source: JLL, Q1 2017; excluding confidential deals In 2017 around 310,000 m² of office space may be completed, a volume lower than the extraordinary result in 2016. Approximately 84,200 m² entered the market in Q1, in a total of ten buildings. The most significant office development completed in the last quarter was definitely Business Garden (bldgs. III to VII), which brought to the market 54,800 m² of office space. Other important deliveries included EQlibrium (fully let) and Airtech Business Park III. Construction activity in Warsaw is quite extensive (approximately 700,000 m²); however, almost 40% of that space is concentrated in four large-scale developments that will be completed in 2019-2020. The main office complexes under construction include: Varso Place (HB Reavis); The Warsaw Hub (Ghelamco Poland); Mennica Legacy Tower (Golub Gethouse); Spinnaker (Ghelamco Poland); West Station (HB Reavis) and D48 (Penta Investments). The annual pipeline for the next few years is significantly lower than the completion volume in 2016, which will eliminate the issue of possible oversupply in Warsaw. However, both companies looking for smaller floorplates and large firms looking to consolidate or relocate to a new office will still have a number of options to choose from.

Transcript of Q1 2017 Warsaw Office Market -...

Warsaw Office MarketQ1 2017

New Warsaw, new beginningWarsaw is an extremely dynamic city. Rapidly expanding infrastructure (e.g. the second metro line) and continuous interest from corporates, developers and institutional investors have resulted in new perceptions of some locations within the city. In particular, the last few years have brought significant changes to the structure of the office market in Warsaw. As a result, the PORF (the Polish Office Research Forum) decided to adapt to the new market conditions and to revise the division of Warsaw’s office hubs. The new districts are discussed in-depth on the last two pages of this report, and are accompanied by maps which illustrate the changes.

Office marketQ1 2017 was quite busy on the Warsaw office market. Demand was exceptionally high (approximately 193,900 m² was let), some new, large-scale projects entered the market and the vacancy rate fell slightly. This is particularly encouraging given the period of growth in 2016, which was a consequence of the extensive supply coming to the market. Moreover, developers still feel confident, and rightfully so, about the absorptiveness of the market, which resulted in some impressive developments being currently under construction throughout the city (particularly in the wider city centre).

The first three months of 2017 saw a significant surge in leasing activity in Warsaw. Such a sound result was due to the outstanding performance of the city centre, where almost 93,500 m² was transacted on. For several quarters in a row the city centre has surprised us with stellar levels of demand, which are in part driven by corporates which have decided to start operations in Warsaw and chose the city centre for their new home instead of a non-central location. The city centre and the areas near it have recently attracted some global brands, thanks to its excellent location, easy access to public transport and the availability of numerous new office buildings.

Nevertheless, areas outside of the city centre also fared well in Q1, particularly Mokotów and the Jerozolimskie corridor, which together account for 72% of the total demand outside of the city centre. These are the largest office hubs in Warsaw outside of the City Centre and major magnets for companies searching for non-central locations. However, there are several smaller locations that also attract corporates.

In terms of the structure of the demand in Warsaw - some 103,700 m² came from new deals, of which the vast majority were signed for existing buildings, as pre-letting activity is quite subdued in the city (which stems from the relatively high availability of good quality, existing office space). A further 72,200 m² constituted renewals and 18,100 m² came from expansions. The most notable transactions of Q1 2017 included: a renewal and expansion

for 13,200 m² by AstraZeneca in Postępu 14, a deal that proves Mokotów still is a vibrant office location; a pre-let for 9,800 m² by Diebold Nixdorf in West Station II; a renewal for 7,300 m² by the Public Transport Authority in Warsaw in JM Tower; and a new deal for 7,200 m² by a confidential company from the public sector in G9. The return of large deals to Warsaw in Q1 2017, after the somewhat subdued 2016, is a great sign for the next few quarters. Companies from the manufacturing and services sectors were the most active in terms of leasing office space in Q1 2017.

Occupier demand in Q1 2017 by business sector

Manufacturing

Services

IT & telecom

Public sector

Banking & investment

Construction & development

Energy, gas, petrol

Healthcare

Other

Source: JLL, Q1 2017; excluding confidential deals

In 2017 around 310,000 m² of office space may be completed, a volume lower than the extraordinary result in 2016. Approximately 84,200 m² entered the market in Q1, in a total of ten buildings. The most significant office development completed in the last quarter was definitely Business Garden (bldgs. III to VII), which brought to the market 54,800 m² of office space. Other important deliveries included EQlibrium (fully let) and Airtech Business Park III.

Construction activity in Warsaw is quite extensive (approximately 700,000 m²); however, almost 40% of that space is concentrated in four large-scale developments that will be completed in 2019-2020. The main office complexes under construction include: Varso Place (HB Reavis); The Warsaw Hub (Ghelamco Poland); Mennica Legacy Tower (Golub Gethouse); Spinnaker (Ghelamco Poland); West Station (HB Reavis) and D48 (Penta Investments).

The annual pipeline for the next few years is significantly lower than the completion volume in 2016, which will eliminate the issue of possible oversupply in Warsaw. However, both companies looking for smaller floorplates and large firms looking to consolidate or relocate to a new office will still have a number of options to choose from.

Warsaw Office Market Q1 2017

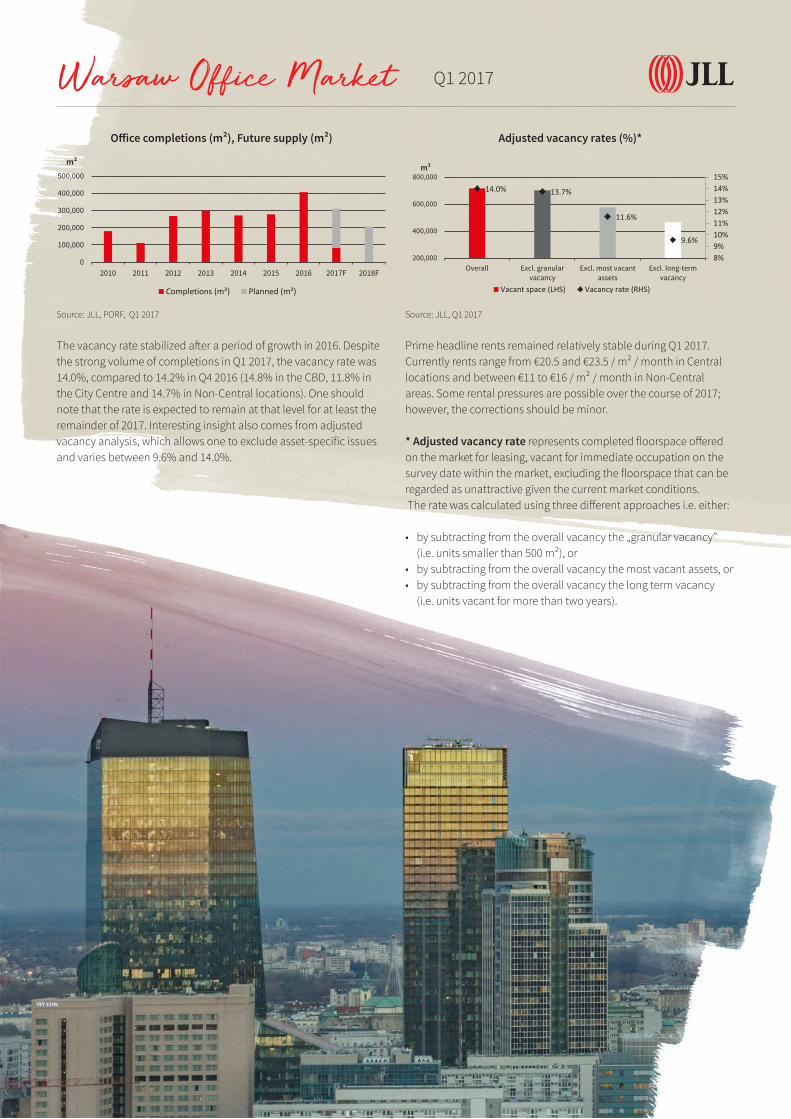

Office completions (m²), Future supply (m²)

0

100,000

200,000

300,000

400,000

500,000

2010 2011 2012 2013 2014 2015 2016 2017F 2018F

m²

Completions (m²) Planned (m²)

Source: JLL, PORF, Q1 2017

The vacancy rate stabilized after a period of growth in 2016. Despite the strong volume of completions in Q1 2017, the vacancy rate was 14.0%, compared to 14.2% in Q4 2016 (14.8% in the CBD, 11.8% in the City Centre and 14.7% in Non-Central locations). One should note that the rate is expected to remain at that level for at least the remainder of 2017. Interesting insight also comes from adjusted vacancy analysis, which allows one to exclude asset-specific issues and varies between 9.6% and 14.0%.

Adjusted vacancy rates (%)*

14.0% 13.7%

11.6%

9.6%

8%9%10%11%12%13%14%15%

200,000

400,000

600,000

800,000

Overall Excl. granularvacancy

Excl. most vacantassets

Excl. long-termvacancy

m²

Vacant space (LHS) Vacancy rate (RHS)

Source: JLL, Q1 2017

Prime headline rents remained relatively stable during Q1 2017. Currently rents range from €20.5 and €23.5 / m² / month in Central locations and between €11 to €16 / m² / month in Non-Central areas. Some rental pressures are possible over the course of 2017; however, the corrections should be minor.

* Adjusted vacancy rate represents completed floorspace offered on the market for leasing, vacant for immediate occupation on the survey date within the market, excluding the floorspace that can be regarded as unattractive given the current market conditions. The rate was calculated using three different approaches i.e. either:

• by subtracting from the overall vacancy the „granular vacancy” (i.e. units smaller than 500 m²), or

• by subtracting from the overall vacancy the most vacant assets, or • by subtracting from the overall vacancy the long term vacancy

(i.e. units vacant for more than two years).

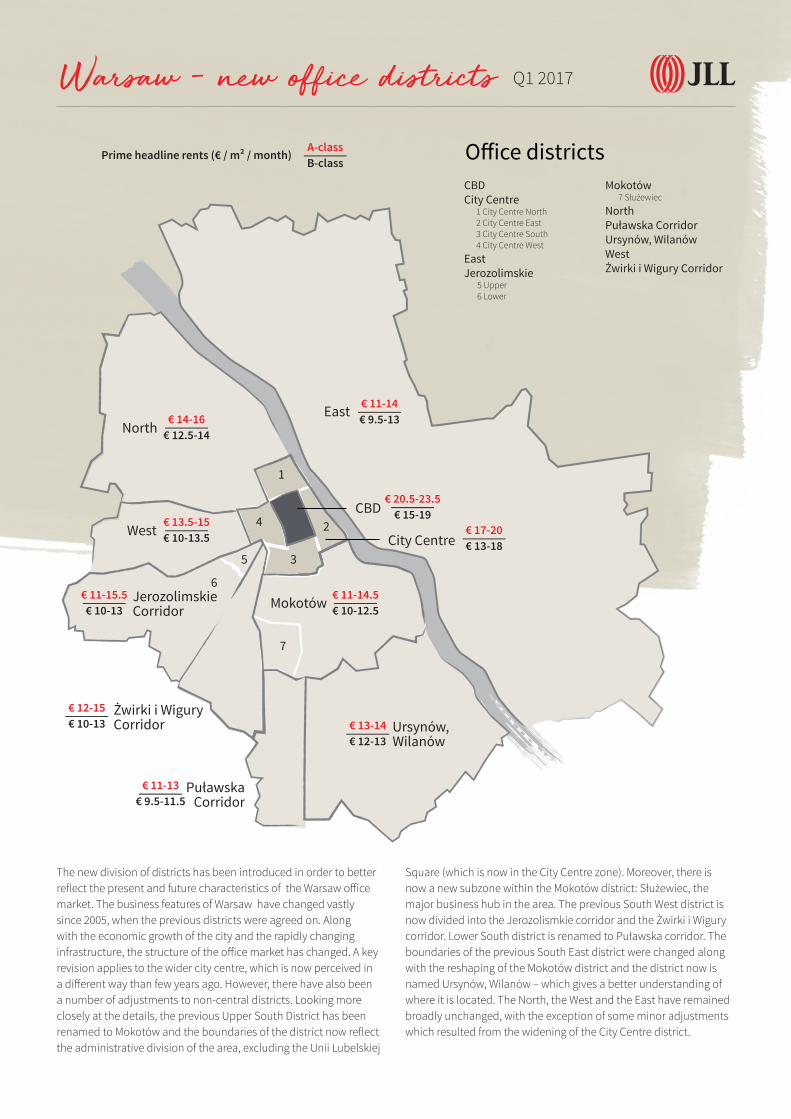

Warsaw – new office districts Q1 2017

The new division of districts has been introduced in order to better reflect the present and future characteristics of the Warsaw office market. The business features of Warsaw have changed vastly since 2005, when the previous districts were agreed on. Along with the economic growth of the city and the rapidly changing infrastructure, the structure of the office market has changed. A key revision applies to the wider city centre, which is now perceived in a different way than few years ago. However, there have also been a number of adjustments to non-central districts. Looking more closely at the details, the previous Upper South District has been renamed to Mokotów and the boundaries of the district now reflect the administrative division of the area, excluding the Unii Lubelskiej

Square (which is now in the City Centre zone). Moreover, there is now a new subzone within the Mokotów district: Służewiec, the major business hub in the area. The previous South West district is now divided into the Jerozolismkie corridor and the Żwirki i Wigury corridor. Lower South district is renamed to Puławska corridor. The boundaries of the previous South East district were changed along with the reshaping of the Mokotów district and the district now is named Ursynów, Wilanów – which gives a better understanding of where it is located. The North, the West and the East have remained broadly unchanged, with the exception of some minor adjustments which resulted from the widening of the City Centre district.

East

Ursynów, Wilanów

Mokotów

1

4

5

6

7

2

3City Centre

CBD

North

Office districtsCBDCity Centre

1 City Centre North2 City Centre East3 City Centre South4 City Centre West

EastJerozolimskie

5 Upper6 Lower

Mokotów7 Służewiec

NorthPuławska CorridorUrsynów, WilanówWestŻwirki i Wigury Corridor

Prime headline rents (€ / m² / month)

West

JerozolimskieCorridor

Żwirki i WiguryCorridor

PuławskaCorridor

A-class—

B-class

€ 14-16—€ 12.5-14

€ 13.5-15—€ 10-13.5

€ 11-15.5—

€ 10-13

€ 12-15—

€ 10-13

€ 11-13 —€ 9.5-11.5

€ 13-14 —

€ 12-13

€ 11-14.5 —€ 10-12.5

€ 17-20 —

€ 13-18

€ 20.5-23.5 —

€ 15-19

€ 11-14 —€ 9.5-13

jll.plCOPYRIGHT © JONES LANG LASALLE IP, INC. 2017. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.

Warsaw – new office districts Q1 2017

The changes in the City Centre are quite significant. The CBD has been extended as far to the east as Nowy Świat Street. The City Centre is now significantly larger. In the north it extends as far as the Dworzec Gdański railway station. To the west it now ends at Karolkowa Street, instead of Towarowa, as it did before. In the south the City Centre extends to Unii Lubelskiej Square. The eastern border remains unchanged and is still marked by Vistula river. The City Centre district is also now divided into four subzones: City Centre East, West, North and South. If you have any questions regarding the new division of the city, please do not hesitate to contact us.

Research Analyst

Research & Consultancy [email protected]

+48 22 167 0433

Head of Research & Consultancy

[email protected] +48 22 167 0000