Property Review Dubai Real Estate Report - Mashreq Review Dubai Real Estate Report Q2 2017. ... 9...

6

Property map Apartments Rent | Sales Villas Rent | Sales Offices Rent | Sales 2 3 4 5 In the Middle East for over 30 Years Property Review Dubai Real Estate Report Q2 2017

-

Upload

nguyenhuong -

Category

Documents

-

view

218 -

download

1

Transcript of Property Review Dubai Real Estate Report - Mashreq Review Dubai Real Estate Report Q2 2017. ... 9...

Property map

ApartmentsRent | Sales

VillasRent | Sales

OfficesRent | Sales2 3 4 5In the Middle East for over 30 Years

Property Review

Dubai Real Estate ReportQ2 2017

DUBAI2

54

611

611

311

11

11

11

11

44

44

44

311

311

311

611

611

2921

36

3

1433

8

56

26

16

31

46

19

2358

41

50

7

45

1

42

55

37 2

18

24

34

35

27

2238

20

28

57

40

44

52

25

53

49

32

51

15

39

10

309

1348 12

47

4

5

6

43

11

17

To SharjahTo Abu Dhabi

Arabian Gulf

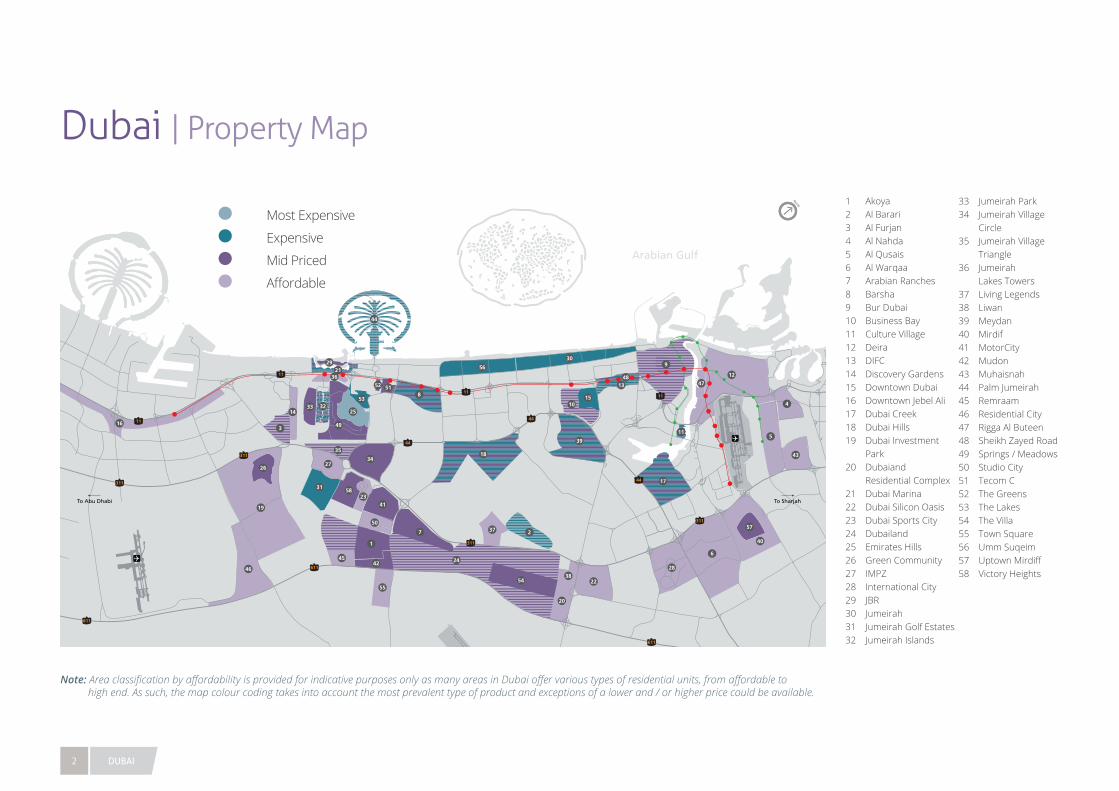

1 Akoya2 Al Barari3 Al Furjan4 Al Nahda5 Al Qusais6 Al Warqaa7 Arabian Ranches8 Barsha9 Bur Dubai10 Business Bay11 Culture Village12 Deira13 DIFC14 Discovery Gardens15 Downtown Dubai16 Downtown Jebel Ali17 Dubai Creek18 Dubai Hills19 Dubai Investment

Park20 Dubaiand

Residential Complex21 Dubai Marina22 Dubai Silicon Oasis23 Dubai Sports City24 Dubailand25 Emirates Hills26 Green Community27 IMPZ28 International City29 JBR30 Jumeirah31 Jumeirah Golf Estates32 Jumeirah Islands

33 Jumeirah Park34 Jumeirah Village

Circle35 Jumeirah Village

Triangle36 Jumeirah

Lakes Towers37 Living Legends38 Liwan39 Meydan40 Mirdif41 MotorCity42 Mudon43 Muhaisnah44 Palm Jumeirah45 Remraam46 Residential City47 Rigga Al Buteen48 Sheikh Zayed Road49 Springs / Meadows50 Studio City51 Tecom C52 The Greens53 The Lakes54 The Villa55 Town Square56 Umm Suqeim57 UptownMirdiff58 Victory Heights

Note: Area classification by affordability is provided for indicative purposes only as many areas in Dubai offer various types of residential units, from affordable to high end. As such, the map colour coding takes into account the most prevalent type of product and exceptions of a lower and / or higher price could be available.

Most Expensive

Expensive

Mid Priced

Affordable

Dubai | Property Map

© Asteco Property Management, 2017 3

Dubai | Apartments-2% -3%-3%

Rental Rates

Sales Prices

-2% -2%

Rental Rates Q-o-Q % Change

Sales Prices Q-o-Q % Change

Mid End Rental Rates

Q-o-Q % Change

High End Rental Rates

Q-o-Q % Change

Affordable Rental Rates

Q-o-Q % Change

TYPE STUDIO 1 BEDROOM 2 BEDROOMS 3 BEDROOMS % CHANGE

AED 000’S PER ANNUM FROM TO FROM TO FROM TO FROM TO Q1 2017 -Q2 2017

Q2 2016 -Q2 2017

HIGH END PROPERTIES

DIFC 65 85 80 130 110 180 150 250 0% -7%

Downtown Dubai 55 85 75 120 105 160 150 250 -6% -12%

Dubai Marina 45 90 65 110 85 150 110 220 -3% -9%

Jumeirah Beach Residence 70 90 80 120 110 140 135 200 -4% -8%

Palm Jumeirah 70 90 80 150 110 200 150 300 -1% -8%

Sheikh Zayed Road 70 80 75 125 100 160 120 200 0% -6%

MID END PROPERTIES

Business Bay 50 80 65 100 90 145 135 180 -2% -14%

Greens 55 70 70 100 100 150 115 200 -4% -9%

Jumeirah Lakes Towers 50 70 60 90 75 145 110 180 -3% -6%

AFFORDABLE PROPERTIES

Al Barsha 45 65 55 80 75 115 95 145 -1% -7%

Bur Dubai 30 60 50 80 65 120 85 170 -3% -11%

Deira 25 55 35 75 55 100 75 150 -3% -11%

Discovery Gardens 35 50 55 75 80 100 - - -2% -2%

Dubai Sports City 35 55 50 75 70 100 90 130 -2% -6%

International City 25 40 35 55 55 70 85 105 0% -9%

Jumeirah Village 35 50 50 70 65 110 90 140 -2% -8%

Supply completed in 2016

8,750Apartments

Supply completed in H1 2017

7,500Apartments

Supply expected in 2017

15,000Apartments

IncreasedproductofferingshavewidenedtheInvestorandTenant pool.

AED

per

sq

ft

2,000

1,500

1,000

500

0

-5%-10%

-7%-8%

0%0%

0%2%

0%-11%

0%0%

-4%-3%

-6%-6%

-5%-5%

-7%-7%

-6%-10%

0%3%

DIFC DowntownDubai

DubaiMarina

Jumeirah Beach

Residence

PalmJumeirah

Business Bay

Greens Jumeirah Lakes

Towers

Discovery Gardens

Dubai Sports

CityCity

Jumeirah Village

HIGH AND LUXURY END PROPERTIES MID TO HIGH END PROPERTIES AFFORDABLE PROPERTIES

From 1,300 1,100 850 1,000 1,000 1,000 1,000 800 650 700 550 700

To 2,300 2,500 2,000 1,700 2,600 1,700 1,600 1,500 900 1,000 800 1,000

Average Sales Price Q-o-Q % Change (Q1 2017 - Q2 2017) Y-o-Y % Change (Q2 2016 - Q2 2017)

International

Following a period of relative stability (Q2 2016 – Q1 2017), apartment sales prices recorded a modest quarterly declineof3%.Thisfallwasattributed,inpart,toarisingnumberofaffordableprojectlaunchesandcompletions.

With many of Dubai’s largest Developers now targeting middle-income Investors, there has been a marked shift tosmallerunitsofferinglowerpricepoints,togetherwithagreaterchoiceofpost-completionpaymentoptions.Variedandflexiblepaymentplanshavecomeasadirectresponsefromdevelopersseekingtoattract End-users struggling with the ‘high’ loan-to-value ratio stipulated by the UAE Central Bank.

Whilst rental rates have also recorded a marginal quarterly drop, the average annual decline has been more pronounced, falling by 7%.

Downward pressure on apartment rental rates is expected to continue as projects are completed and delivered to the market. As with the sales market, there has been an increase in the number and range of incentives available.Landlordsareincreasinglyofferingincentivessuchasfurnishings(withoutincrement),rentalsinclusiveof DEWA bills, or rent-free periods of up to two months.

DUBAI4

Dubai | Villas

Villa sales prices recorded a minimal change between Q1 – Q2 2017, falling 2% on average. Interestingly, although a number of established communities, such as the Meadows and Springs (with limited supply potential) followed a similar quarterly pattern, annual growth, however, was positive at 9% and 5% respectively.

Whilstrecentoff-plansaleslauncheshavebeenstrengthenedbycompetitivepricepointsandincreasinglyflexiblepaymentplans;thesecondarymarket,unsurprisingly,remainedgenerallycorrelatedtodemandandsupply fundamentals.

Villa rental rates also recorded marginal changes over the last three months. However, the average annual decline was more noteworthy at 10%.

Whilst families, who favour villas, have generally been more reluctant to move compared with couples and bachelors, there has been a rise in relocations, often within the community or to nearby developments. Tenants opted to take advantage of lower rental rates or upgrades, usually in the response to intransigent Landlords.

Pending the considerable amount of supply expected in 2017 and 2018, we do not see any drivers that would reverse this trend.

TYPE 2 BEDROOMS 3 BEDROOMS 4 BEDROOMS 5 BEDROOMS % CHANGE

AED 000’S PER ANNUM FROM TO FROM TO FROM TO FROM TO Q1 2017 -Q2 2017

Q2 2016 -Q2 2017

Al Barsha - - 145 200 150 250 170 300 0% -12%

Arabian Ranches 110 165 130 200 140 280 210 400 -1% -13%

Dubai Sports City (Victory Heights) - - 145 175 160 200 180 320 -1% -9%

Jumeirah - - 140 230 160 250 190 350 0% -14%

Jumeirah Park - - 175 225 180 280 240 320 -1% -4%

Jumeirah Village 105 160 110 210 120 200 135 220 -3% -6%

Meadows - - 180 240 185 285 230 330 -1% -6%

Mirdif 75 125 90 140 100 180 125 200 0% -11%

Palm Jumeirah - - 250 350 300 500 350 1,000 -4% -13%

Springs 100 140 110 180 - - - - -4% -16%

The Lakes - - 170 250 210 300 300 400 -1% -6%

Umm Suqeim - - 140 240 150 300 180 320 -2% -10%

Rental Rates

-2%-1%

Sales Prices Q-o-Q % Change

Rental Rates Q-o-Q % Change

Sales Prices

AED

per

sq

ft

3,000

2,500

2,000

1,500

1,000

500

0

0%-5%

0%2%

-6%-11%

-4%9%

0%2%

-9%5%

2%2%

ArabianRanches

Dubai Sports City (Victory Heights)

JumeirahPark

JumeirahVillage

Meadows PalmJumeirah

Springs

From 900 900 800 550 900 1,500 850

To 1,400 1,200 1,300 950 1,400 4,500 1,150

Average Sales Price Q-o-Q % Change (Q1 2017 - Q2 2017) Y-o-Y % Change (Q2 2016 - Q2 2017)

Supply completed in 2016

5,000Villas

Supply completed in H1 2017

1,800Villas

Supply expected in 2017

2,900Villas

Additional supply resulted in an increased number of relocations and tenancy renegotiations, which consequently drove rental rates down.

© Asteco Property Management, 2017 5

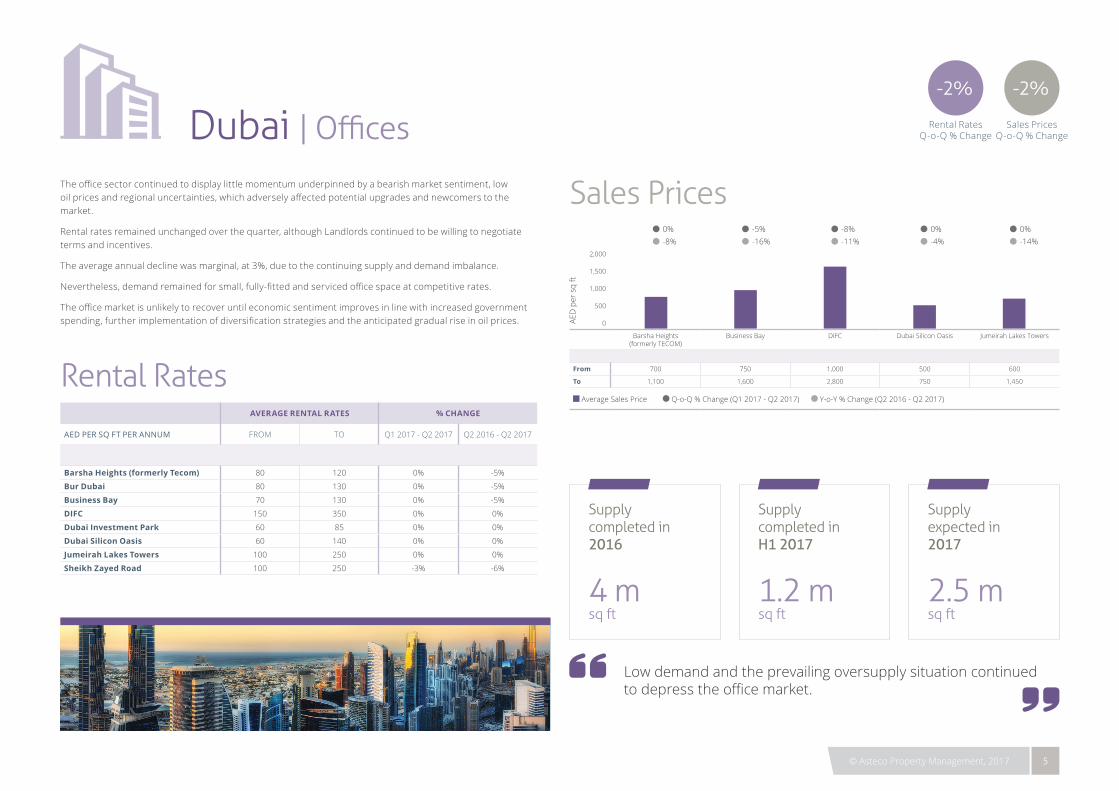

Theofficesectorcontinuedtodisplaylittlemomentumunderpinnedbyabearishmarketsentiment,lowoilpricesandregionaluncertainties,whichadverselyaffectedpotentialupgradesandnewcomerstothemarket.

Rental rates remained unchanged over the quarter, although Landlords continued to be willing to negotiate terms and incentives.

The average annual decline was marginal, at 3%, due to the continuing supply and demand imbalance.

Nevertheless,demandremainedforsmall,fully-fittedandservicedofficespaceatcompetitiverates.

Theofficemarketisunlikelytorecoveruntileconomicsentimentimprovesinlinewithincreasedgovernmentspending,furtherimplementationofdiversificationstrategiesandtheanticipatedgradualriseinoilprices.

Rental RatesAVERAGE RENTAL RATES % CHANGE

AED PER SQ FT PER ANNUM FROM TO Q1 2017 - Q2 2017 Q2 2016 - Q2 2017

Barsha Heights (formerly Tecom) 80 120 0% -5%

Bur Dubai 80 130 0% -5%

Business Bay 70 130 0% -5%

DIFC 150 350 0% 0%

Dubai Investment Park 60 85 0% 0%

Dubai Silicon Oasis 60 140 0% 0%

Jumeirah Lakes Towers 100 250 0% 0%

Sheikh Zayed Road 100 250 -3% -6%

-2%-2%

Sales Prices Q-o-Q % Change

Rental Rates Q-o-Q % ChangeDubai | Offices

Sales Prices

AED

per

sq

ft

2,000

1,500

1,000

500

0

-5%-16%

-8%-11%

0%-4%

0%-14%

0%-8%

Barsha Heights (formerly TECOM)

Business Bay DIFC Dubai Silicon Oasis Jumeirah Lakes Towers

From 700 750 1,000 500 600

To 1,100 1,600 2,800 750 1,450

Average Sales Price Q-o-Q % Change (Q1 2017 - Q2 2017) Y-o-Y % Change (Q2 2016 - Q2 2017)

Supply completed in 2016

4 msq ft

Supply completed in H1 2017

1.2 msq ft

Supply expected in 2017

2.5 msq ft

Low demand and the prevailing oversupply situation continued todepresstheofficemarket.

DISCLAIMER:TheinformationcontainedinthisreporthasbeenobtainedfromandisbaseduponsourcesthatAstecoPropertyManagementbelievestobereliable;however,nowarrantyorrepresentation,expressedorimplied,ismadetothe accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any special listing conditions imposed by our principals. Asteco Property Management will not be held responsible for any third-party contributions. All opinions and estimates included in this report constitute Asteco Property Management’s judgment, as of the date of this report and are subject to change without notice. Figures contained in this report are derived from a basket of locations highlighted in this report and therefore represent a snapshot of the UAE market. Averages, however, represent a wider range of areas. Particularly exclusive or unique projects have been excluded from the data to avoid distorting averages. Due care and attention has been used in the preparation of forecast information. However, actual results may vary from forecasts and any variation may be materially positive or negative. Forecasts, by their very nature, involve risk and uncertainty because they relate to future events and circumstances which are beyond Asteco Property Management’s control. For a full in-depth study of the market, please contact Asteco Property Management’s Research team. Asteco Property Management LLC. Commercial License No. 218551. Paid-up Capital AED 4,000,000. | ORN 180

Dubai Real Estate ReportQ2 2017