Promoting food security through innovative rural finance and risk management tools

38

www.fao.org/ag/ ags Promoting food security through innovative rural finance and risk management tools Calvin Miller Senior Officer and Group Leader, AGS Emilio Hernandez Agricultural Finance Officer, AGS 15 July 2015 Rome, FAO HQ

-

Upload

food-and-agriculture-organization-of-the-united-nations -

Category

Education

-

view

255 -

download

1

Transcript of Promoting food security through innovative rural finance and risk management tools

www.fao.org/ag/ags

Promoting food securitythrough innovative rural financeand risk management tools

Calvin MillerSenior Officer and Group Leader, AGS

Emilio HernandezAgricultural Finance Officer, AGS

15 July 2015

Rome, FAO HQ

1. Results from FAO-AGS global agenda: A framework to assess trends in rural financial markets in the developing world

2. Lessons from the field: rising innovation in agricultural finance and risk management: an inclusive process?

3. Key takeaways4. Discussant views5. Questions and answers

Content

Source: Author compilation using WASDE, USDA data

World total consumption and supply of grains and oils seeds (in trillions of MT)

An analytical framework: The active search of the agricultural sector to satisfy a growing demand

0

500

1000

1500

2000

2500

3000

3500

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

Supply

Consumption

The increase in supply has been similar across the world

Total production of different commodities in Asia, LAC and Africa (in thousands of MT)

Source: FAOSTAT 1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

020000400006000080000

100000120000140000160000180000200000

Asia Latin America

Africa

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0

50000

100000

150000

200000

250000

Cereals

Fruits and vegetables

Meats

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

0

200000

400000

600000

800000

1000000

1200000

1400000

Some agricultural products are increasing in value more than others

Total export value of different commodities in Asia, LAC and Africa (in millions of USD)

Source: FAOSTAT

Asia Latin America

Africa1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

10000

20000

30000

40000

50000

60000

19931995

19971999

20012003

20052007

20092011

01000020000300004000050000600007000080000

19931995

19971999

20012003

20052007

20092011

0

2000

4000

6000

8000

10000

12000

Cereals

Fruits and vegetables

Meats

Rise in supply strongly determined by a rise in aggregate productivity levels globally

Average yields for different commodities in Asia, LAC and Africa (in thousands of Hg/Ha)

Source: FAOSTAT

Asia Latin America

Africa

Cereals

Fruits and vegetables

19931995

19971999

20012003

20052007

20092011

020406080

100120140160180

19931995

19971999

20012003

20052007

20092011

0

50

100

150

200

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0102030405060708090

100

Source: Fuglie, K.O. 2012, “Productivity Growth and Technology Capital in the Global Agricultural Economy”, in Fuglie, K.O., S.L. Wang, and V.E. Ball (eds.) (2012), Productivity Growth in Agriculture: An International Perspective, CAB International, Oxfordshire, UK.

Productivity gains have been the main source of output growth

Sources of agricultural output growth rate globally

A critical determinant of productivity has been long-term investment in agriculture

Agricultural capital stock in Asia, LAC and Africa (in million of 2005 USD)

Source: FAOSTAT

Asia Latin America and the Caribbean

Africa

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

680000

700000

720000

740000

760000

780000

800000

820000

19931994

19951996

19971998

19992000

20012002

20032004

20052006

200717000001750000180000018500001900000195000020000002050000210000021500002200000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

0

100000

200000

300000

400000

500000

600000

Dominance of domestic private investments in total agricultural capital stock

Components of agriculture investment for a sample of 31 developing countries

Source: ODI, 2012

Who has financed the rise in agricultural investments and how?

With important exceptions, the formal financial sector has played a very limited role in the provision of financial services to agriculture in developing countries.

Mounting evidence from global market analyses suggests informal sources of finance mainly from agricultural value chain (AVC) actors (i.e. wholesalers, processors, traders, warehouse operators, producer associations, etc.) have enabled a significant share of investments in agriculture.

These agents who are non-specialized financial service providers, are able to respond to the finance gap thanks to unique informational advantages. From their informal status, they have enabled a ‘quiet revolution’ in agribusiness operations that has effectively responded to the expansion in global demand for agricultural products.References: Reardon et al., 2012; Miller and Jones, 2010; Mildler 2008; Gonzalez-Vega, et al. 2006

Risk managementin rural and agricultural

finance

Agri-business segmentation Social and commercial insurances Traditional farming sector Emerging farming sector Commercial farming sector

Agricultural risk assessmentCapacity and competitiveness assessment Risk identification and quantificationSensitivity analysis

Agricultural risk financing Risk layering Index insurance Insurance pool Technology and

infrastructure (e.g. irrigation and warehouses)

Institutional capacity buildingData managementOrganization and governanceRegulatory/supervisory frameworkInformation and educationTechnical expertiseSavings and equity formation

Agricultural risk management

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

2

4

6

8

10

12

Africa Asia & Pacific EuropeLatin America & Caribbean Other Developed World

Av

era

ge

Ag

ric

ult

ure

Sh

are

of

To

tal C

red

it, %

Agriculture share of credit by region, 1991-2013

Other Developed refers to Australia, New Zealand, Japan and North America

Source: FAO, 2015

The investment trends contrast with a declining share of formal credit to agriculture

The lag of formal financial services to agriculture in LAC from the firm’s perspectiveAg. credit as a share of total credit vs. ag. GDP as a share of total GDP for select countries in Latin America during 2010

Source: FAO, 2011

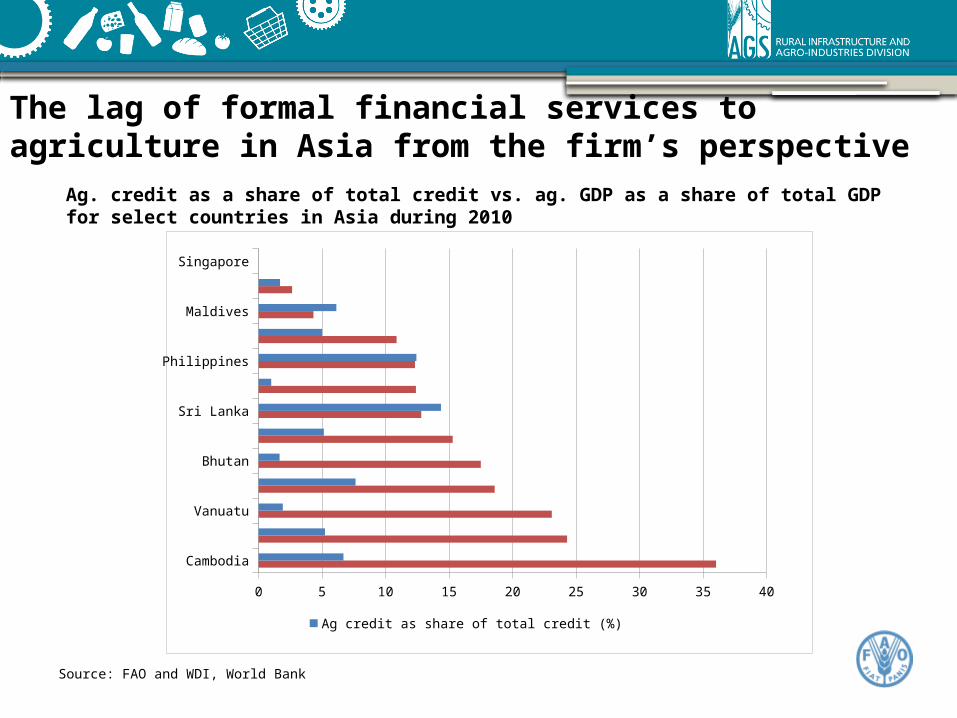

The lag of formal financial services to agriculture in Asia from the firm’s perspective

Ag. credit as a share of total credit vs. ag. GDP as a share of total GDP for select countries in Asia during 2010

Source: FAO and WDI, World Bank

Cambodia

Pakistan

Vanuatu

Bangladesh

Bhutan

Indonesia

Sri Lanka

Thailand

Philippines

Samoa

Maldives

Korea, Republic of

Singapore

0 5 10 15 20 25 30 35 40

Ag credit as share of total credit (%)Ag GDP as share of total GDP (%)

The lag of formal financial services to agriculture in Africa from the firm’s perspective

Ag. credit as a share of total credit vs. ag. GDP as a share of total GDP for select countries in Africa during 2010

Source: FAO and WDI, World Bank

Ethiopia

Liberia

Burundi

Rwanda

Malawi

Ghana

Tanzania

Uganda

Kenya

Sudan

Nigeria

Zambia

Namibia

Botswana

Seychelles

0 5 10 15 20 25 30 35 40 45 50

Ag credit as a share of total credit (%)Ag GDP as a share of total GDP (%)

The prominent role of informal financial services in rural areas of Sub-Saharan Africa

Total vs. formal use of saving and credit services in Sub-Saharan Africa region in 2011(% rural people)

Source: Compiled by author using FINDEX, 2012

0

5

10

15

20

25

30

35

40

45

50

% o

f ru

ral

po

pu

lati

on

Informal savingsmarket

Informal creditmarket

Source: Compiled by author using FINDEX, 2012

Informal credit market

Saved any money in the past year, rural

Saved at a financial institution in the past

year, rural

Loan in the past year, rural

Loan from a financial institution in the past

year, rural

0

5

10

15

20

25

30

35

% r

ural

pop

ulat

ion

Informal savings market

The prominent role of informal financial services in rural areas in East Asia and Pacific and South East Asia

Total vs. formal use of saving and credit services in the EAP and South Asia region in 2011(% rural people)

The prominent role of informal financial services in rural areas in Latin AmericaTotal vs. formal use of saving and credit services in the LAC (developing only) region in 2011 (% rural people)

Source: Compiled by author using FINDEX, 2012

Informal savings market Informal credit market

Limitations of informal finance and opportunities for the formal financial sector to serve rural areas and agriculture

The key limitation of the current scenario is that outreach is limited and the variety, adequacy and cost of financial services from these non-specialized sources are not optimal for clients. The lack of financial specialization comes at the cost of exclusion thus representing a sub-optimal equilibrium.

Motivation for field research: The macro evidence suggests an environment of constant innovation from a number of agricultural value chains actors, financial institutions and government to deliver rural and agricultural financial services by merging specialized knowledge from different actors to deal with complex climatic, production, marketing, and financial risks

References: Reardon et al., 2012; USAID, 2011; Gonzalez-Vega, et al. 2006

Producing Storing

Production

Price

Operational

Financing

Institutional

InfrastructureQuality controlTechnology

Logistics

Seasonal glut

Processing Marketing

InfrastructureStorage

Price

Product loss

Govt. policy

Technology

Product supply

Human resourceProduct qualityGovt. policy

Input Supply

Quality

Availability

InfrastructureKnowledge

Financing

These informal finance actors are able to assess risks that go beyond the individual client and include all aspects in the agricultural value chain

From supply-driven “how we lend” to client driven “how can we

structure finance to address client needs and risks”

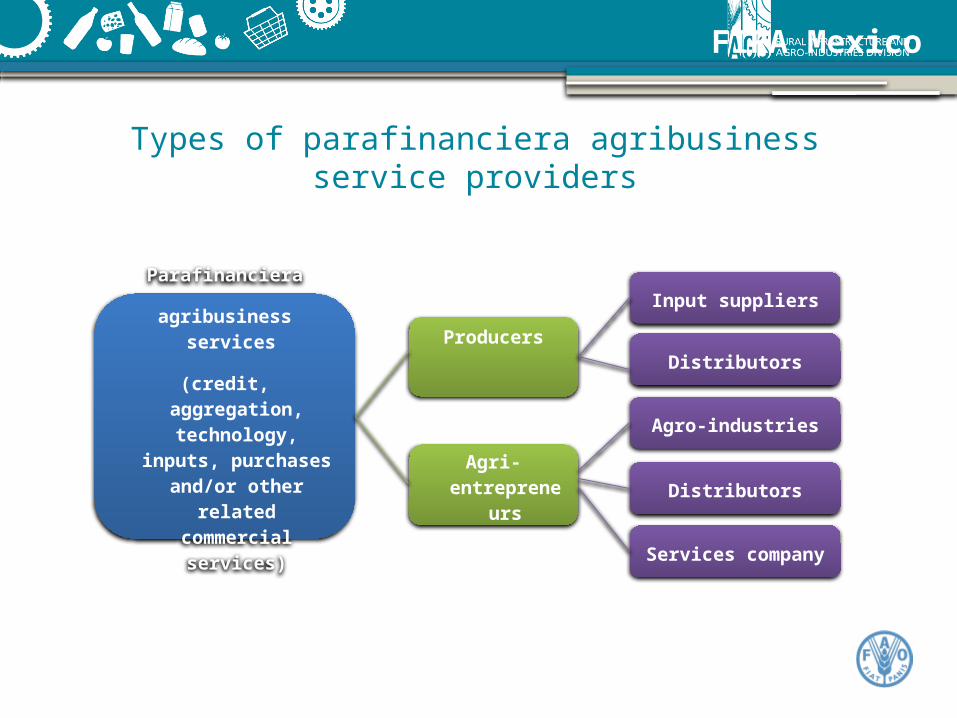

Parafinanciera

Service Provider

Bank/

Non-bank Financial Institution

Individual

Producers

Family Groups

Civil Society

90 days 8 days

Financial Institution - Parafinanciera

Line of credit

Parafinanciera - Producer

Individual credit

Producer Organizations

FIRA parafinanciera credit delivery through VC intermediaries

Mexico – Innovations in financing smallholders

FIRA Mexico

Parafinanciera

agribusiness services

(credit, aggregation, technology, inputs,

purchases and/or other related commercial

services)

Agri-entrepreneurs

Services company

Distributors

Agro-industries

Distributors

Input suppliers

Producers

Types of parafinanciera agribusiness service providers

FIRA Mexico

Summary of the parafinanciera system

BRAC, Bangladesh -

BRAC Bank

BRAC Cold Storage

Potato farmers

Potato seed dealers

Wholesaler

Buyers/Farmers

Home Consumption &

Seeds

Potato production

Sales by Farmers

Seeds &

inputsFinancing

Financing

Financing

Financing LoanRepayments

Payment

Payment (Service Charge)

Seed Payment

Potato production, cold storage, finance and marketing

The ECX WHR Financing -lending

Ethiopian Commodity Exchange – managing market risks

T+1

60 (30) days

A blended approach to AgVCF inclusion

Companies

Farmers / groups

BDS providers

MFIs

Commercial Banks

Terrafina Local NGO

Rabo AdvisoryServices

FAO & Int NGOs

Rabobank (guarantee) Rabobank (loans)

Adapted from Harms

Ethiopian ComEx and WHR

Field level

monitoring

Assistance to farmers

Loan/lease

disbursement

Selection of farmersValue additions:

GuidanceMarket linkages

Problem identificationIntervention

Association

Farmer

Bank/ Mobile

Banking

United Finance Limited – lending, leasing, factoring

UFL, Bangladesh

Bolivia –Innovations led by specialized financial institutions: the case of CIDRE

Long term investment credit

Loan for irrigation

Payment for produce

Irrigation services

Credit payment

Sale of production

TA in irrigation management and governance

Source: Derived from CIDRE information

Irrigation management association

CIDRE

Traders of agricultural produce

for local markets

Member producers in communities

Suppliers of irrigation equipment

Key enablers of financial products offered

CIDRE: Focus on long-term credit products for agricultural irrigation Savvy search for long term funding for the FI Investment in R&D for product design based on modern

irrigation techniques and agricultural value chain dynamics Critical reliance on a regulatory framework allowing for

experimentation in rural finance services Ability to identify alternative collateral requirements:

irrigation shares

Key limitations of models used

CIDRE: Large investment in R&D of the product to assess the

client and all commercial actors involved, which needed support from international development agencies with shared vision

A policy reform being put in place creates uncertainty as interest rates, lending methodology and portfolio structure will be centrally set

CIDRE results

Fiscal year 2008 2009 2010 2011 2012 2013

Assets (millions of USD) 13.4 15.9 21.1 31.2 38.0 51.9

Number of active borrowers 4,198.0 2,836.0 4,194.0 5,156.0 7,180.0 9,344.0

% of rural borrowers 93.1 76.9 64.0 59.6 58.4 58.3Gross Loan Portfolio (millions of USD) 10.2 11.5 17.0 25.7 34.1 47.5

% PAR (30+ days) - - 2.13 1.91 1.68 0.0149

% gross loan portfolio, rural 81.6 71.9 5.0 52.6 55.0 54.6

Average outstanding balance 2,425.3 4,051.4 4,046.7 4,454.6 4,745.9 5,079.0

Operational self sufficiency 1.1 1.4 1.1 1.2 1.1 1.1

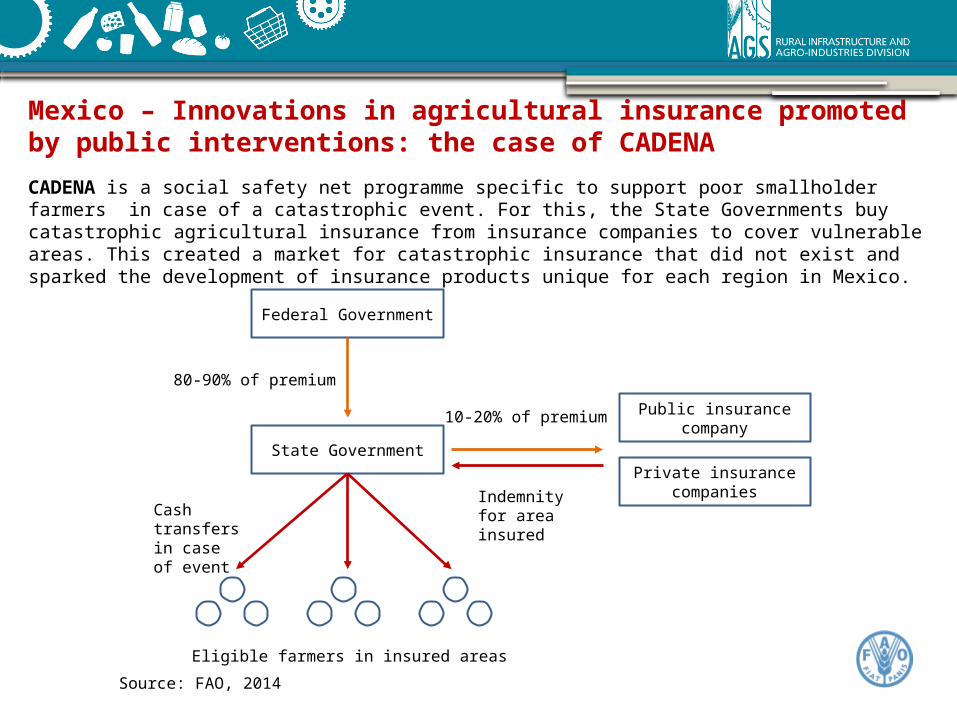

CADENA is a social safety net programme specific to support poor smallholder farmers in case of a catastrophic event. For this, the State Governments buy catastrophic agricultural insurance from insurance companies to cover vulnerable areas. This created a market for catastrophic insurance that did not exist and sparked the development of insurance products unique for each region in Mexico.

Mexico – Innovations in agricultural insurance promoted by public interventions: the case of CADENA

Federal Government

State GovernmentPrivate insurance

companies

Public insurance company

Eligible farmers in insured areas

80-90% of premium

10-20% of premium

Indemnity for area insured

Cash transfers in case of event

Source: FAO, 2014

Key enablers for the agricultural insurance product offered The budget for the program became predictable and fiscally manageable as

premiums are fixed ex-ante.

A national market was created for catastrophic agricultural insurance products (index and multi-peril), inclusive of high-risk and marginalized States, that did not exist before and that is uncommon globally given the challenge of insuring systemic risks.

Public and private insurance companies compete for that market and have the incentive to invest in the development of insurance products tailored to the risk-vulnerability ratio of each Mexican State. This enabled the expansion of the area covered per Peso spent, relative to an ex-post approach

The delivery of index insurance products are meant to insure a portfolio, not an individual farmer. The prevalence of basis risk in index insurance products is spread in a wide area and it is borne by the State so it is easier to tolerate

CADENA results

CADENA has facilitated a wide expansion of agricultural insurance covering 12 mo Ha in 2013 representing 65% of total area under production and covers 98% of the country’s municipalities. This represents a safety net for 3.7 mo smallholders, equivalent to 82% of the estimated smallholder population.

2003 2004 2005 2006 2007 2008 2009 2010 20110%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1000

1500

2000

2500

CADENA: Number and Percentage of Municipalities Insured

NUMBER OF MUNICIPALITIES INSURED % municipalities insured

Source: FAO, 2014 Source: Data from SAGARPA

Private and public share of the catastrophic insurance market

Coverage of CADENA at the municipality level

Key limitations of model used

Cost-efficiency depends greatly on State Governments building specialized units to determine most appropriate coverage needs, but large federal subsidies are a disincentive to do this. Relying only on coverage advice from insurance companies has not resulted in appropriate coverage for some States, resulting in additional public expenditures

Availability and sustainability of public resources to fund the programme (currently a premium market of over USD 190 m a year)

Pre-existing capacity of public agencies to collect and analyze relevant climatic and production time series data needs to exist in order to facilitate the development of new insurance products in the short term

Key takeaways

There is a favorable global agribusiness environment that motivates innovation mainly among private domestic agricultural actors that are heterogeneous and less organized, who are not well known

Agricultural financing innovations in business models, financial instruments and use of technology are able to include poorer smallholder families

The level of inclusion that is achievable will depend strongly on pre-existing conditions related to the enabling environment and level of local capacities

Depending on this context, different private or public leaders in the design of finance arrangements emerge, all of them forming partnerships between them to merge their unique knowledge on the various types of risks to manage

Barriers to making these partnerships systematic are the key constraint for mainstreaming innovations. These barriers relate to the difficulty of establishing coordination between actors that operate in very different professional networks

Thank you for your attention!

www.fao.org/ag/ags

www.ruralfinanceandinvestment.org