Professional Level – Options Module Paper P6 (IRL) · Professional Level – Options Module ......

21

Professional Level – Options Module Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section A – BOTH questions are compulsory and MUST be attempted Section B – TWO questions ONLY to be attempted Tax rates and allowances are on pages 2–9 Do NOT open this question paper until instructed by the supervisor. This question paper must not be removed from the examination hall. Paper P6 (IRL) Advanced Taxation (Irish) Thursday 8 December 2016 The Association of Chartered Certified Accountants

Transcript of Professional Level – Options Module Paper P6 (IRL) · Professional Level – Options Module ......

Professional Level – Options Module

Time allowed: 3 hours and 15 minutes

This question paper is divided into two sections:

Section A – BOTH questions are compulsory and MUST be attempted

Section B – TWO questions ONLY to be attempted

Tax rates and allowances are on pages 2–9

Do NOT open this question paper until instructed by the supervisor.

This question paper must not be removed from the examination hall. Pape

r P

6 (

IRL)

Advanced Taxation(Irish)

Thursday 8 December 2016

The Association ofChartered Certified

Accountants

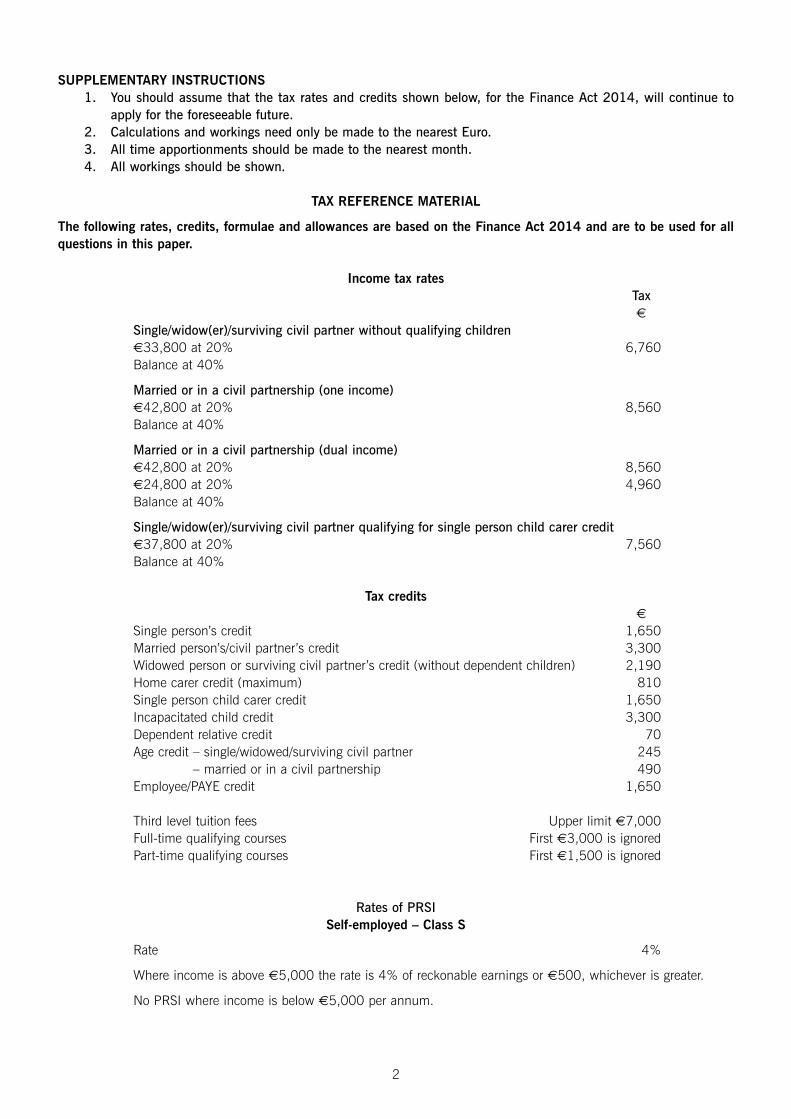

SUPPLEMENTARY INSTRUCTIONS1. You should assume that the tax rates and credits shown below, for the Finance Act 2014, will continue to

apply for the foreseeable future.2. Calculations and workings need only be made to the nearest Euro.3. All time apportionments should be made to the nearest month.4. All workings should be shown.

TAX REFERENCE MATERIAL

The following rates, credits, formulae and allowances are based on the Finance Act 2014 and are to be used for allquestions in this paper.

Income tax ratesTax€

Single/widow(er)/surviving civil partner without qualifying children€33,800 at 20% 6,760Balance at 40%

Married or in a civil partnership (one income)€42,800 at 20% 8,560Balance at 40%

Married or in a civil partnership (dual income)€42,800 at 20% 8,560€24,800 at 20% 4,960Balance at 40%

Single/widow(er)/surviving civil partner qualifying for single person child carer credit€37,800 at 20% 7,560Balance at 40%

Tax credits€

Single person’s credit 1,650Married person’s/civil partner’s credit 3,300Widowed person or surviving civil partner’s credit (without dependent children) 2,190Home carer credit (maximum) 810Single person child carer credit 1,650Incapacitated child credit 3,300Dependent relative credit 70Age credit – single/widowed/surviving civil partner 245Age credit – married or in a civil partnership 490Employee/PAYE credit 1,650

Third level tuition fees Upper limit €7,000Full-time qualifying courses First €3,000 is ignoredPart-time qualifying courses First €1,500 is ignored

Rates of PRSISelf-employed – Class S

Rate 4%

Where income is above €5,000 the rate is 4% of reckonable earnings or €500, whichever is greater.

No PRSI where income is below €5,000 per annum.

2

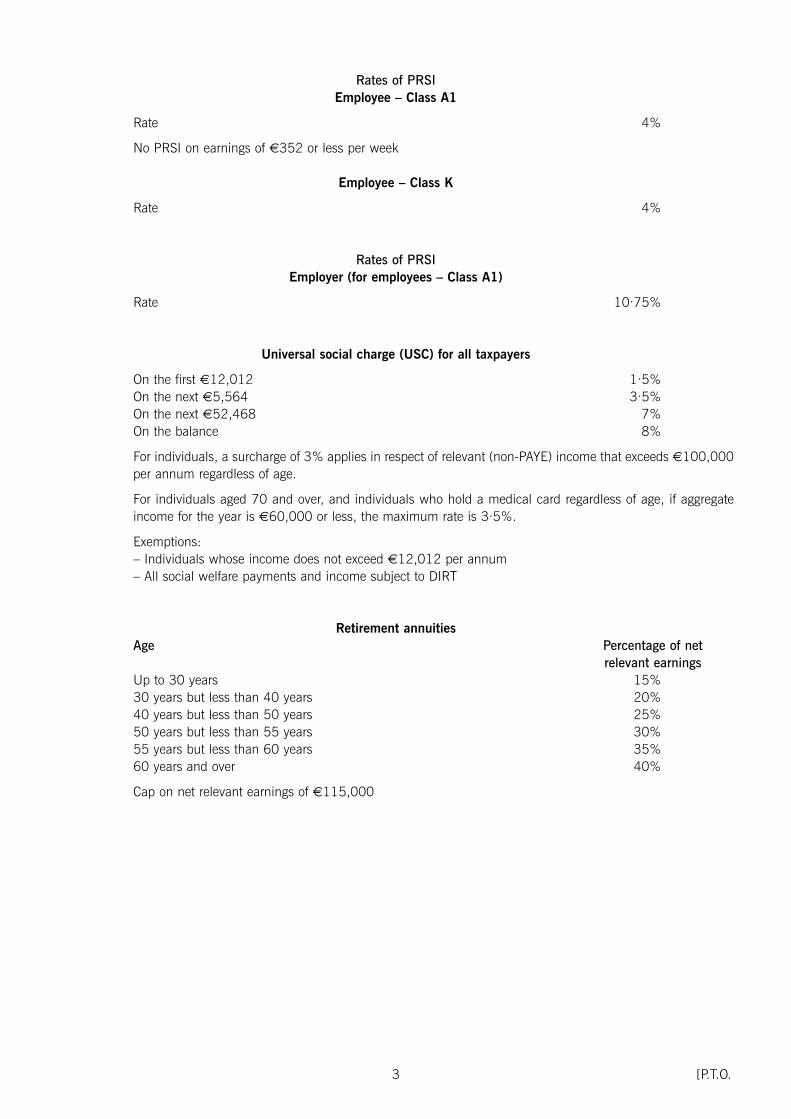

Rates of PRSIEmployee – Class A1

Rate 4%

No PRSI on earnings of €352 or less per week

Employee – Class K

Rate 4%

Rates of PRSIEmployer (for employees – Class A1)

Rate 10·75%

Universal social charge (USC) for all taxpayers

On the first €12,012 1·5%On the next €5,564 3·5%On the next €52,468 7%On the balance 8%

For individuals, a surcharge of 3% applies in respect of relevant (non-PAYE) income that exceeds €100,000per annum regardless of age.

For individuals aged 70 and over, and individuals who hold a medical card regardless of age, if aggregateincome for the year is €60,000 or less, the maximum rate is 3·5%.

Exemptions:– Individuals whose income does not exceed €12,012 per annum– All social welfare payments and income subject to DIRT

Retirement annuitiesAge Percentage of net

relevant earningsUp to 30 years 15%30 years but less than 40 years 20%40 years but less than 50 years 25%50 years but less than 55 years 30%55 years but less than 60 years 35%60 years and over 40%

Cap on net relevant earnings of €115,000

3 [P.T.O.

Corporation tax

Standard rate 12·5%Higher rate 25%

Value added tax (VAT)

Registration limitsTurnover from the supply of goods €75,000Turnover from the supply of services €37,500

Rates:Standard rate 23%Lower rate 13·5%Additional lower rate 9%

Capital gains tax (CGT)

Rates:From 6 December 2012 to date 33%From 7 December 2011 to 5 December 2012 30%From 8 April 2009 to 6 December 2011 25%From 15 October 2008 to 7 April 2009 22%From 1 December 1999 to 14 October 2008 20%

Annual exemption €1,270

Motor cars – limits on capital costs

Carbon emissions table:Category A Category B/C Category D/E Category F/G0–120g/km 121–155g/km 156–190g/km 191g/km+

Category A/B/C vehicles – capital allowances/leasing charges are based on the specified amount of €24,000regardless of the cost of the car.

Category D/E vehicles – capital allowances/leasing charges are based on 50% of either €24,000 or the costof the car, whichever is lower.

Category F/G vehicles – do not qualify for capital allowances/leasing charges.

Benefits in kindMotor cars

Business travel Business travel Percentage of originallower limit upper limit market value of carKilometres Kilometres0 24,000 30%24,001 32,000 24%32,001 40,000 18%40,001 48,000 12%48,001 Upwards 6%

4

Preferential loan rates

Loans used to fund the cost/repair of the employee’s principal private residence 4%All other loans 13·5%

Local property tax

Tax bands for valuation purposes€

0–100,000100,001–150,000150,001–200,000200,001–250,000250,001–300,000300,001–350,000350,001–400,000400,001–450,000450,001–500,000500,001–550,000550,001–600,000600,001–650,000650,001–700,000700,001–750,000750,001–800,000800,001–850,000850,001–900,000900,001–950,000

950,001–1,000,000

Properties worth up to and including a value of €1 million will be assessed at a rate of 0·18%.

Properties worth more than €1 million will be assessed on their actual value at 0·18% on the first €1 million and at0·25% of their actual value on the portion above €1 million.

5 [P.T.O.

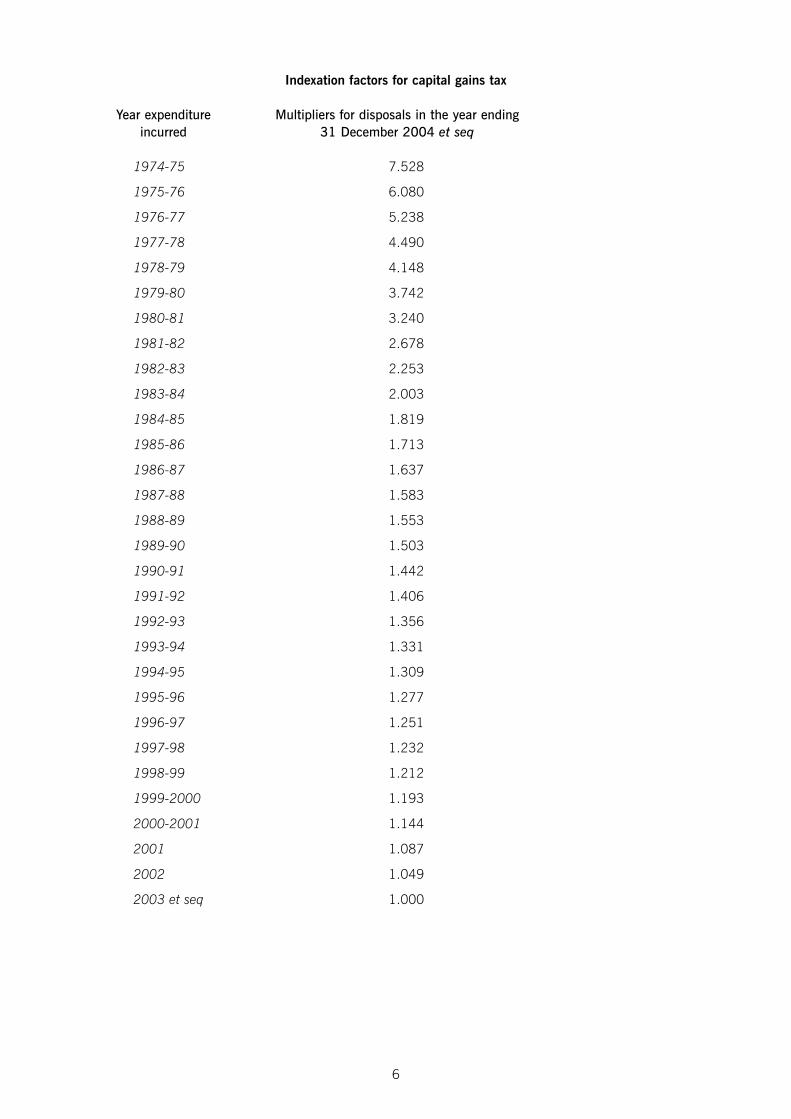

Indexation factors for capital gains tax

Year expenditure Multipliers for disposals in the year endingincurred 31 December 2004 et seq

1974-75 7.528

1975-76 6.080

1976-77 5.238

1977-78 4.490

1978-79 4.148

1979-80 3.742

1980-81 3.240

1981-82 2.678

1982-83 2.253

1983-84 2.003

1984-85 1.819

1985-86 1.713

1986-87 1.637

1987-88 1.583

1988-89 1.553

1989-90 1.503

1990-91 1.442

1991-92 1.406

1992-93 1.356

1993-94 1.331

1994-95 1.309

1995-96 1.277

1996-97 1.251

1997-98 1.232

1998-99 1.212

1999-2000 1.193

2000-2001 1.144

2001 1.087

2002 1.049

2003 et seq 1.000

6

Capital acquisitions tax

Class thresholds 2015€

Class 1: Child or minor child of deceased child(or inheritance taken by parent): 225,000

Class 2: Lineal ancestor (other than inheritance taken by parent)Lineal descendant (other than a child or a minor child of a deceased child)Brother, sister, child of brother or sister 30,150

Class 3: Any other person 15,075

Rate 33%

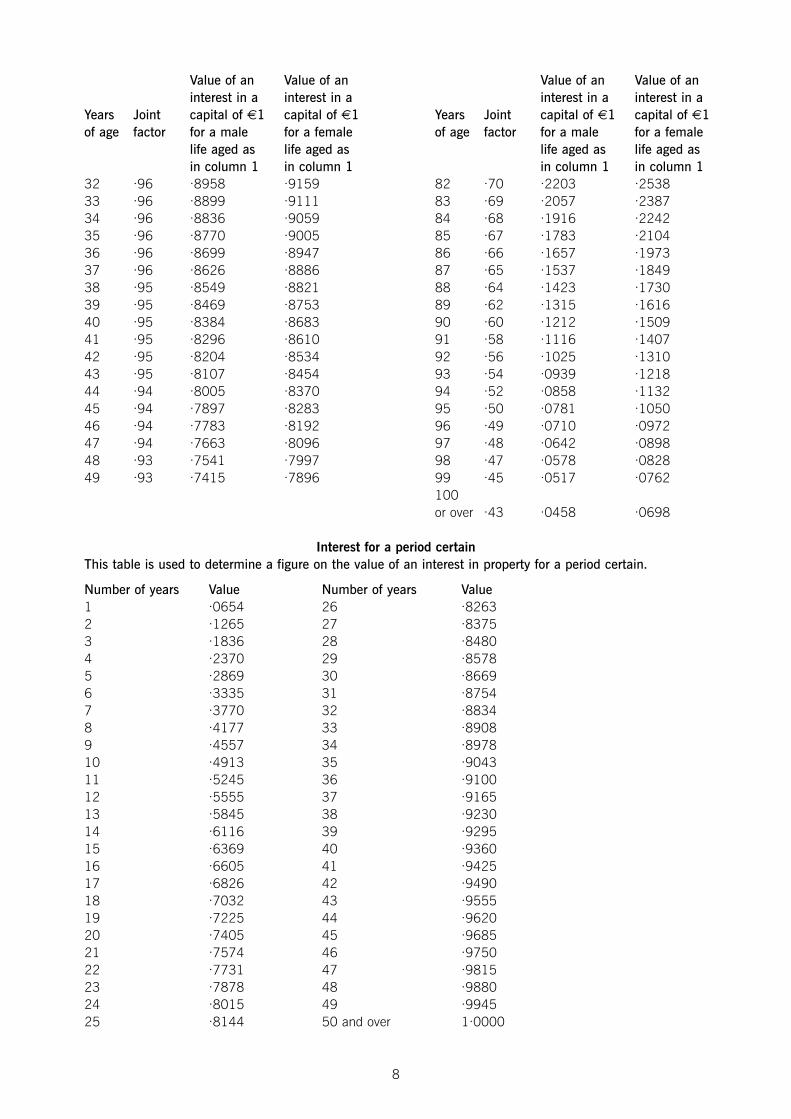

Life interest tables for capital acquisitions tax

Value of an Value of an Value of an Value of aninterest in a interest in a interest in a interest in a

Years Joint capital of €1 capital of €1 Years Joint capital of €1 capital of €1of age factor for a male for a female of age factor for a male for a female

life aged as life aged as life aged as life aged asin column 1 in column 1 in column 1 in column 1

0 ·99 ·9519 ·9624 50 ·92 ·7287 ·77911 ·99 ·9767 ·9817 51 ·91 ·7156 ·76832 ·99 ·9767 ·9819 52 ·90 ·7024 ·75723 ·99 ·9762 ·9817 53 ·89 ·6887 ·74564 ·99 ·9753 ·9811 54 ·89 ·6745 ·73355 ·99 ·9742 ·9805 55 ·88 ·6598 ·72066 ·99 ·9730 ·9797 56 ·88 ·6445 ·70697 ·99 ·9717 ·9787 57 ·88 ·6288 ·69268 ·99 ·9703 ·9777 58 ·87 ·6129 ·67789 ·99 ·9688 ·9765 59 ·86 ·5969 ·662810 ·99 ·9671 ·9753 60 ·86 ·5809 ·647511 ·98 ·9653 ·9740 61 ·86 ·5650 ·632012 ·98 ·9634 ·9726 62 ·86 ·5492 ·616213 ·98 ·9614 ·9710 63 ·85 ·5332 ·600014 ·98 ·9592 ·9693 64 ·85 ·5171 ·583015 ·98 ·9569 ·9676 65 ·85 ·5007 ·565016 ·98 ·9546 ·9657 66 ·85 ·4841 ·546217 ·98 ·9522 ·9638 67 ·84 ·4673 ·526618 ·98 ·9497 ·9617 68 ·84 ·4506 ·507019 ·98 ·9471 ·9596 69 ·84 ·4339 ·487320 ·97 ·9444 ·9572 70 ·83 ·4173 ·467921 ·97 ·9416 ·9547 71 ·83 ·4009 ·448822 ·97 ·9387 ·9521 72 ·82 ·3846 ·430123 ·97 ·9356 ·9493 73 ·82 ·3683 ·411424 ·97 ·9323 ·9464 74 ·81 ·3519 ·392825 ·97 ·9288 ·9432 75 ·80 ·3352 ·374326 ·97 ·9250 ·9399 76 ·79 ·3181 ·355927 ·97 ·9209 ·9364 77 ·78 ·3009 ·337728 ·97 ·9165 ·9328 78 ·76 ·2838 ·319829 ·97 ·9119 ·9289 79 ·74 ·2671 ·302330 ·96 ·9068 ·9248 80 ·72 ·2509 ·285531 ·96 ·9015 ·9205 81 ·71 ·2353 ·2693

7 [P.T.O.

Value of an Value of an Value of an Value of aninterest in a interest in a interest in a interest in a

Years Joint capital of €1 capital of €1 Years Joint capital of €1 capital of €1of age factor for a male for a female of age factor for a male for a female

life aged as life aged as life aged as life aged asin column 1 in column 1 in column 1 in column 1

32 ·96 ·8958 ·9159 82 ·70 ·2203 ·253833 ·96 ·8899 ·9111 83 ·69 ·2057 ·238734 ·96 ·8836 ·9059 84 ·68 ·1916 ·224235 ·96 ·8770 ·9005 85 ·67 ·1783 ·210436 ·96 ·8699 ·8947 86 ·66 ·1657 ·197337 ·96 ·8626 ·8886 87 ·65 ·1537 ·184938 ·95 ·8549 ·8821 88 ·64 ·1423 ·173039 ·95 ·8469 ·8753 89 ·62 ·1315 ·161640 ·95 ·8384 ·8683 90 ·60 ·1212 ·150941 ·95 ·8296 ·8610 91 ·58 ·1116 ·140742 ·95 ·8204 ·8534 92 ·56 ·1025 ·131043 ·95 ·8107 ·8454 93 ·54 ·0939 ·121844 ·94 ·8005 ·8370 94 ·52 ·0858 ·113245 ·94 ·7897 ·8283 95 ·50 ·0781 ·105046 ·94 ·7783 ·8192 96 ·49 ·0710 ·097247 ·94 ·7663 ·8096 97 ·48 ·0642 ·089848 ·93 ·7541 ·7997 98 ·47 ·0578 ·082849 ·93 ·7415 ·7896 99 ·45 ·0517 ·0762

100or over ·43 ·0458 ·0698

Interest for a period certainThis table is used to determine a figure on the value of an interest in property for a period certain.

Number of years Value Number of years Value 1 ·0654 26 ·82632 ·1265 27 ·83753 ·1836 28 ·84804 ·2370 29 ·85785 ·2869 30 ·86696 ·3335 31 ·87547 ·3770 32 ·88348 ·4177 33 ·89089 ·4557 34 ·897810 ·4913 35 ·904311 ·5245 36 ·910012 ·5555 37 ·916513 ·5845 38 ·923014 ·6116 39 ·929515 ·6369 40 ·936016 ·6605 41 ·942517 ·6826 42 ·949018 ·7032 43 ·955519 ·7225 44 ·962020 ·7405 45 ·968521 ·7574 46 ·975022 ·7731 47 ·981523 ·7878 48 ·988024 ·8015 49 ·994525 ·8144 50 and over 1·0000

8

Stamp duty

Non-residential property (regardless of value) 2%

Residential property: Owner occupiers and investorsFirst €1,000,000 1%Excess over €1,000,000 2%

NB: Where applicable value added tax (VAT) should be excluded from the chargeable consideration.

Stocks and marketable securities

Where the aggregate consideration is less than €1,000 0%Where the aggregate consideration exceeds €1,000 1%

Revenue audits

Schedule of tax geared penalties

Net penalty after reduction where there is:Category of Penalty as a % Cooperation Cooperation AND Cooperation ANDtax default of tax underpaid only a prompted an unprompted

qualifying qualifying disclosure disclosure

Deliberate behaviour 100% 75% 50% 10%Careless behaviour with 40% 30% 20% 5%significant consequencesOther careless behaviour 20% 15% 10% 3%

Note: The mitigation (reduction) of penalties in the above table is available to taxpayers on their first default. In thecase of a second or third default, if a taxpayer deliberately or carelessly makes incorrect returns within a five-yearperiod of the first default they may not avail of full mitigation.

9 [P.T.O.

This is a blank page.Question 1 begins on page 11.

10

Section A – BOTH questions are compulsory and MUST be attempted

1 You should assume that today’s date is 1 November 2015

You have recently taken the following notes from a client meeting:

Your client Walter Osborne (aged 67) holds shares in a number of companies which operate retail paint shops in boththe UK and Ireland. Walter is, and always has been, UK resident and domiciled. He is a director of all the companieswhich he owns and spends 90% of his working week managing his UK businesses.

He has sought your taxation advice in relation to the proposed disposal of his three Irish paint businesses toImpression plc, a large Irish retail chain. All three Irish businesses are operated by companies, are profitable andprepare accounts up to 31 December each year. The disposals are due to take place on 10 December 2015.Impression plc and the three Irish companies are all value added tax (VAT) registered.

Walter is aware that UK tax liabilities will probably arise on the disposals, but he will receive separate advice from hisUK accountant in this regard. Walter wishes to minimise any exposure to Irish taxes, and his UK accountant hasadvised him that, because of his age, he may be able to get an exemption from Irish capital gains tax (CGT) on someor all of the sales proceeds.

Details of the three Irish businesses are as follows:

The Blue Shop

The trade is carried on by Blue Shop Ltd (BSL), which was incorporated in Ireland on 1 April 2009. BSL has anissued share capital of 100 ordinary shares of €1 each, which is all owned by Walter.

Walter bought the shop premises personally for €300,000 (excluding VAT) on 1 April 2009. Walter was the firstowner of the premises, which were newly constructed. Walter has rented the premises to BSL (which has 100% VATdeductibility) since then. The single option to tax the letting for VAT purposes was availed of. Walter spent €100,000(excluding VAT) on an extension to the premises in June 2011. In May 2013, that extension was demolished and anew extension was constructed at a cost of €200,000 (excluding VAT).

The offer from Impression plc is as follows:

– €700,000 for the premises, excluding any applicable VAT; and– €1,000,000 for the share capital of BSL. This valuation is based on the following company assets:

€

Goodwill 800,000Equipment 120,000Inventory 80,000

All of the above figures exclude VAT.

The goodwill was internally generated by BSL and has no base cost. The payables and cash at bank figures arenot significant.

The Red Shop

Red Shop Ltd (RSL) was incorporated in Ireland in June 2004. RSL has an issued share capital of 10,000 shares of€1 each. The market values of RSL’s assets are as follows:

€

Goodwill 240,000Shop premises 350,000Equipment 100,000Inventory 60,000Apartment in Dublin 150,000

The shop premises cost €250,000 (excluding VAT) in July 2004. The apartment in Dublin cost €200,000(excluding VAT) in 2007 and was bought as an investment. The payables and cash at bank figures are not significant.

RSL is a 100% subsidiary of Brush Ltd, a company incorporated in Ireland, which acquired the share capital of RSLin June 2004. Apart from the shareholding in RSL, Brush Ltd has no other assets or liabilities. The share capital of

11 [P.T.O.

Brush Ltd comprises 30,000 ordinary shares of €1 each and is all owned directly by Walter who acquired the sharesfor their par value in 2003.

Impression plc has offered €900,000 to buy the shares in Brush Ltd from Walter.

The Green Shop

Green Shop Ltd (GSL) was incorporated in Ireland in September 1987. It has an issued share capital of 80,000shares of €1 each, which is owned equally by Walter (40,000 shares) and his wife, Mary, (40,000 shares) who bothacquired the shares on incorporation for their par value.

Mary (aged 49) is also UK resident and domiciled and has never worked in or been a director of GSL.

Impression plc will only buy selected assets from GSL. They are not interested in buying the shares.

GSL purchased its shop premises for €100,000 in October 1987. The premises were exempt from VAT and nosignificant development has taken place since then. During the negotiation stage, Impression plc stated it was notinterested in buying the shop premises. GSL sold the premises to Mary in October 2015 for €150,000. The marketvalue of the premises on the date of sale was €200,000.

The remaining assets and liabilities of GSL at market value (after the sale of the premises) are as follows:

€

Goodwill 450,000Equipment 60,000Inventory 50,000Cash at bank (including the sale proceeds of the premises) 190,000Trade payables (70,000)Bank loan (100,000)

The goodwill was internally generated by GSL and has no base cost. The original cost of the equipment was €80,000on 1 March 2011. The market value of the inventory is the same as its cost.

Impression plc will buy the goodwill, equipment and inventory at the valuations shown, and GSL will then pay itsliabilities. The remaining cash in the company will be distributed to the shareholders of GSL following a liquidation ofthe company. The liquidator’s fees will be €6,000.

Both Walter and Mary have a marginal income tax rate of 51%.

12

Required:

Write a letter to Walter which provides:

(i) Advice on Walter’s exposure to Irish capital gains tax (CGT). (4 marks)

(ii) An explanation (with supporting calculations) of the various Irish taxation issues for Walter, Mary and theirthree companies associated with the disposal of:

– The Blue Shop premises and Walter’s shareholding in Blue Shop Ltd (BSL) to Impression plc.– Walter’s shareholding in Brush Ltd to Impression plc.– The Green Shop premises to Mary and the remaining assets of Green Shop Ltd (GSL) to Impression plc,

followed by the liquidation of GSL.

Note: The following mark allocation is provided as guidance for this requirement:

The Blue Shop 5·5 marksThe Red Shop 2·5 marksThe Green Shop 14 marks

(22 marks)

(iii) A summary of the total after-tax proceeds available to Walter and Mary, following the disposal of the threebusinesses. (2 marks)

(iv) Your recommendation on how Walter’s tax position in relation to the disposal of the Red Shop business maybe improved. (3 marks)

Notes:1. The annual exemption for capital gains tax (CGT) may be ignored.2. The payment dates for the various taxes are NOT required.3. You are NOT required to advise on the UK tax implications of the disposals.

Professional marks will be awarded in question 1 for the appropriateness of the format and presentation of theletter and the effectiveness with which the information is communicated. (4 marks)

(35 marks)

13 [P.T.O.

2 Sam Baldwyn, a widower, resident and domiciled in Ireland, died on 19 October 2015, leaving an estate comprising60 ordinary shares in Gaucho Ltd and various other assets.

Sam was survived by his two adult children, Donald and Katy, both of whom are Irish resident and domiciled. Since2012, Donald and Katy have lived together in an apartment in central Dublin, which they jointly own.

Specific bequests

Sam’s will provided for the following specific bequests (all valuations are as at Sam’s date of death):

(1) Donald and Katy each received 30 shares in Gaucho Ltd.

Gaucho Ltd is a manufacturing company with an issued ordinary share capital of 100 shares of €1 each. Samacquired his shares in Gaucho Ltd at par on the company’s incorporation in April 2003.

Donald has worked for Gaucho Ltd since 1 February 2009. Katy is a graphic designer. She has never worked forGaucho Ltd and does not intend to. Each share in Gaucho Ltd was valued at €15,000 as part of a majorityholding and at €10,000 as part of a minority holding.

The remaining 40 shares in Gaucho Ltd have been held by Jim Steele since incorporation. Jim is a close familyfriend but is not related to the Baldwyn family.

(2) Donald and Katy each received an equal (50%) share in the business premises, from which Gaucho Ltdoperates.

The premises had been owned personally by Sam and had been used for the purposes of Gaucho Ltd’s tradesince January 2012. The premises were valued at €300,000.

(3) Donald received Sam’s principal private residence in Dublin, valued at €400,000.

(4) Katy received a commercial property in London, UK, valued at €500,000.

(5) Sam’s brother, Charlie, received Irish government securities valued at €100,000. Sam had bought thesesecurities in April 2009. Charlie is resident in the USA and is Irish domiciled.

Residue

The will provided that the residue of Sam’s estate be divided equally between Donald and Katy.

Sam was also a partner in a local firm of consulting architects. No mention of the goodwill attaching to Sam’spartnership share was made in his will. The other partners recently offered the executors of Sam’s estate €200,000for his share of the goodwill. Katy has confirmed independently that this is an accurate valuation.

The balance at bank, after payment of all estate liabilities, was €76,000.

Prior gifts or inheritances

Donald and Charlie have never previously received any gifts or inheritances. Katy received a gift with a taxable valueof €10,000 from Charlie in 2005.

Proposals

– Donald is considering disclaiming his interest in the principal private residence in favour of Katy.

– Katy is considering giving both her shareholding in Gaucho Ltd and her interest in the business premises toDonald.

– Donald and Jim Steele have been discussing the possibility of Jim selling to Donald his 40 shares in Gaucho Ltd.

14

Required:

(a) Explain the capital acquisitions tax (CAT) implications of the bequests received by each of the beneficiaries(Donald, Katy and Charlie) based on the above scenario. Support your explanations with calculations of theCAT payable and a summary of the total CAT payable by each of the beneficiaries. (13 marks)

(b) Explain the CAT implications of the following proposals, supporting your explanations with relevantcalculations:

(1) If Donald disclaims his interest in the principal private residence in favour of Katy.(2) If Katy gives her shareholding in Gaucho Ltd and her interest in the business premises to Donald as soon

as she receives these assets. (7 marks)

(c) Set out the various tax implications for Donald, if Jim sells his 40 shares in Gaucho Ltd to him at asubstantial discount below their market value, because of his close friendship with the Baldwyn family.

Note: Calculations are NOT required for this part. (5 marks)

(25 marks)

15 [P.T.O.

Section B – TWO questions ONLY to be attempted.

3 Sounds Ltd is an Irish incorporated and resident company, which operates a restaurant. The company also has anumber of other sources of income.

The share capital of Sounds Ltd comprises 400 ordinary shares of €1 each, owned as follows:

Number of sharesBen Wilson 55Caroline Wilson (Ben’s wife) 35Rhonda Wilson (Ben’s sister) 40Conor Wilson (Ben’s brother) 40John Fogerty 25Susan Morris 40Mary Smith 40Pat O Neill 35Paul Hamilton 40Juliette Watters 50

––––400––––

There is no share premium account as the ordinary shares were issued at par.

Ben Wilson, Caroline Wilson and Rhonda Wilson are directors of Sounds Ltd. Conor Wilson (a full-time musician) isnot a director and does not work for the company.

The other six shareholders are not directors of Sounds Ltd and are not related to the Wilson family. All of these othershareholders work full-time in the company.

The following information has been extracted from the financial statements of Sounds Ltd for the year ended 31 December 2015.

€

Trading income 500,000Capital allowances (20,000)Deposit interest received gross (DIRT not withheld) 2,000Rental income 40,000Rental loss brought forward from 2014 (10,000)Trading loss brought forward from 2014 (20,000)Chargeable gain (as adjusted for corporation tax purposes) 2,000Dividends received from Irish companies (gross) 700

The following additional information is available:

(1) On 1 January 2015, Ben and Rhonda made loans to Sounds Ltd of €10,000 each, to finance the purchase ofnew equipment. These loans have no specific repayment date and Sounds Ltd paid €1,000 interest to each ofthem in the year ended 31 December 2015. This interest cost has been deducted in arriving at the tradingincome of Sounds Ltd.

(2) On 1 June 2015, Sounds Ltd made an interest-free car loan of €20,000 to Conor. The entire loan wasoutstanding at 31 December 2015.

(3) On 1 November 2015, Sounds Ltd paid €5,000 in relation to travel and accommodation for Conor while he wastouring with his band. This expense was deducted in arriving at the trading income of Sounds Ltd.

16

Required:

(a) State, giving reasons, why Sounds Ltd is a close company. (2 marks)

(b) Explain the various tax consequences of items (1) to (3) above for both the individuals involved and SoundsLtd. Support your explanations with calculations, where relevant.

Note: The following mark allocation is provided as guidance for this requirement:

Item 1 5·5 marksItem 2 3 marksItem 3 1·5 marks

(10 marks)

(c) Calculate the corporation tax liability (excluding surcharges) of Sounds Ltd for the year ended 31 December2015. (4 marks)

(d) Compute the close company surcharge arising on Sounds Ltd for the year ended 31 December 2015.(4 marks)

(20 marks)

17 [P.T.O.

4 You should assume that today’s date is 14 August 2015

Alison Quinn and Eva McGrath are directors and shareholders of Genoa Ltd, which trades as a clothing wholesaler.Alison (aged 38) and Eva (aged 51) each own 50% of the share capital of Genoa Ltd and work full-time in thebusiness of the company. They are both single and have no other sources of income.

Prior to setting up Genoa Ltd, both Alison and Eva had worked as employees of a local company and they havecalculated that when they retire each will be entitled to a guaranteed pension of €10,000 per annum from thatcompany’s pension scheme and approximately €9,000 per annum from the State old age pension.

Neither Alison nor Eva has been part of a pension scheme since setting up Genoa Ltd, and they have sought youradvice in relation to paying into a new pension scheme. However, before they agree to contribute to a new pensionscheme, they require information regarding how their existing pension funds and any new funds established in theinterim will be dealt with on maturity.

The following additional information is available:

(i) The tax adjusted profit of Genoa Ltd for the year ended 31 December 2015 is expected to be €220,000, beforemaking any provision for director’s pension arrangements. This profit will be comprised solely of Case I incomeand has been computed after deducting the normal directors’ remuneration paid to Alison and Eva of €72,000each.

(ii) Genoa Ltd has surplus cash of €200,000 in the company bank account available for investment in a suitablepension scheme.

Two alternatives are currently being considered for the funding of the new pension scheme:

(1) Genoa Ltd would pay additional directors’ remuneration of €100,000 (gross) to each director and they wouldeach use their additional remuneration to pay a premium on their own personal retirement annuity scheme.

(2) Genoa Ltd would pay dividends of €100,000 to each director and they would each use their dividends to paya premium on their own personal retirement annuity scheme.

Required:

(a) Explain the options available to Alison and Eva when their pension fund matures, together with the taxtreatment. (6 marks)

(b) Explain the tax implications of each of the two alternatives for the new pension scheme from the perspectiveof both Genoa Ltd and the two directors (Alison and Eva) and advise on which of the two alternatives is themore tax efficient overall. (10 marks)

(c) Recommend another more tax efficient alternative and assess this from the perspective of both Genoa Ltdand the two directors. (4 marks)

(20 marks)

18

This is a blank page.Question 5 begins on page 20.

19 [P.T.O.

5 You should assume that today’s date is 1 March 2016

Your client, Christine Wood, owns 100% of the share capital of two companies as follows:

Albatross Ltd

Albatross Ltd is based in Cork, Ireland and is involved in the manufacture and sale of electronic equipment towholesalers in Ireland.

Songbird Ltd

Songbird Ltd operates a coffee shop in Dublin. The shop premises, which were built in 2014, were bought by thecompany for €300,000 (excluding value added tax (VAT)) on 1 February 2015. VAT was reclaimed on thistransaction on the basis that the company had 100% deductibility.

Both Albatross Ltd and Songbird Ltd are VAT registered and submit bi-monthly VAT returns and prepare accounts to31 December each year.

Christine has sought your advice in relation to the following issues:

VAT – Songbird Ltd

On 1 July 2015, Songbird Ltd set up a ‘Barista training school’ which delivers courses on ‘how to make excellentcoffee’ in part of its shop premises. The training has been determined to be a VAT exempt activity. At the end of theinitial interval, Songbird Ltd calculated that 80% of its supplies were taxable activities and the remaining 20% wereexempt. The training courses have become popular and Christine expects that their proportion of total sales willincrease steadily.

Christine is unsure about whether she can reclaim input VAT on overheads such as electricity and telephone, wherea single bill covers the entire premises.

New equipment costing €15,000 (excluding VAT) has been ordered from a supplier in Italy and will be installed inthe training room in April 2016 for use in the training activity only.

Corporation tax (CT) – Albatross Ltd and Songbird Ltd

The financial projections indicate that:

– Albatross Ltd will incur an average net loss of €100,000 per annum for the next three years and will achieve aprofit of approximately €20,000 per annum thereafter.

– Songbird Ltd will make average net profits of €150,000 per annum for the next three years and thereafter.

Christine is keen to optimise the overall CT position of the two companies. She is willing to undertake any restructuringwhich will help achieve this objective but is concerned about any potentially adverse tax consequences of such arestructuring.

Capital gains tax – Christine

Christine sold a residential investment property in Galway, Ireland in July 2015 for net proceeds (after costs ofdisposal) of €300,000. She had bought the property for €410,000 (including incidental costs of acquisition) in June2007. The acquisition of the property was financed through a bank loan. Christine negotiated to have €50,000 ofthe bank loan written off in June 2015. Christine disposed of no other assets during 2015.

20

Required:

(a) Advise Christine on the value added tax (VAT) implications for Songbird Ltd of the new training activity.(8 marks)

(b) Advise Christine on the potential utilisation of the expected losses in Albatross Ltd against the expectedprofits in Songbird Ltd. Your advice should include an analysis of the current position and a recommendationas to any action which should be taken to optimise the overall corporation tax (CT) position of the twocompanies including the resulting tax consequences of your proposal. (10 marks)

(c) Advise Christine on her capital gains tax (CGT) position in respect of her disposal of the residential investmentproperty in Galway. (2 marks)

(20 marks)

End of Question Paper

21