Prof. Ian Giddy New York University Structured Finance: Restructuring.

date post

20-Dec-2015Category

view

219download

1

Prof. Ian GiddyNew York University

Asset-BackedFinancing

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 2

Asset-Backed Securities:The Typical Structure

FORD (SPONSOR)

SPECIALPURPOSEVEHICLE

LOANS.

ISSUESASSET-BACKEDCERTIFICATES

SALE ORASSIGNMENT

LOANS.

Servicing Agreement

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 3

Example:Ford Credit Owner Trust 1999-A

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 4

The Process

Is the company

ready?

Is the company

ready?

Are the assets

suitable?

Are the assets

suitable?

What pool?What pool?

What legal

structure?

What legal

structure?

What credit

enhancement?

What credit

enhancement?

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 5

Separation of Two Businesses: Origination and Lending

SPONSORINGCOMPANY

SPECIALPURPOSEVEHICLE

ACCOUNTSRECEIVABLE

ACCOUNTSRECEIVABLE

ISSUESASSET-BACKEDCERTIFICATES

SALE ORASSIGNMENT

Asset securitization makes sense when

the assets are worth more outside the

company than within

But what makes them worth more outside?

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 6

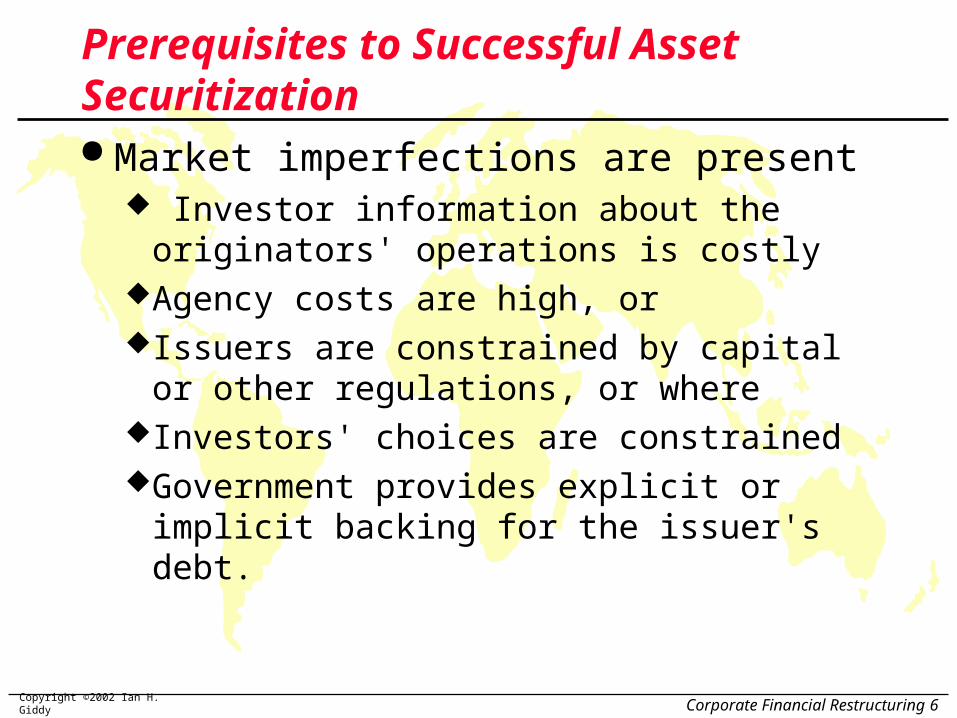

Prerequisites to Successful Asset Securitization Market imperfections are present

Investor information about the originators' operations is costly

Agency costs are high, or Issuers are constrained by capital or other

regulations, or where Investors' choices are constrainedGovernment provides explicit or implicit

backing for the issuer's debt.

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 7

For Banks: Capital Requirements

In a perfect world, adding good assets would require little additional capital, since creditors would not see any increase in the bank's risk

But if regulatory capital requirements penalize banks for holding such assets, they should: securitize the good assetsprofit from origination and servicing

In general, regulatory costs or rigidities create an incentive for banks to shrink their balance sheets by securitizing loans

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 8

A Bank’s Capital Savings

Securitization Cost-Benefit Analysis(for a regulated financial institution)

Gain/cost($ millions)

Funding cost savings Two-year bank notes vs pass-though rate

1.1

Upfront costs Underwriting SEC filing, legal fees, etc

(2.6)

Ongoing costs Letter-of-credit fee (0.5)

Capital charge Cost of capital at 25% (15%after tax)

7.7

Net benefit 5.7

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 9

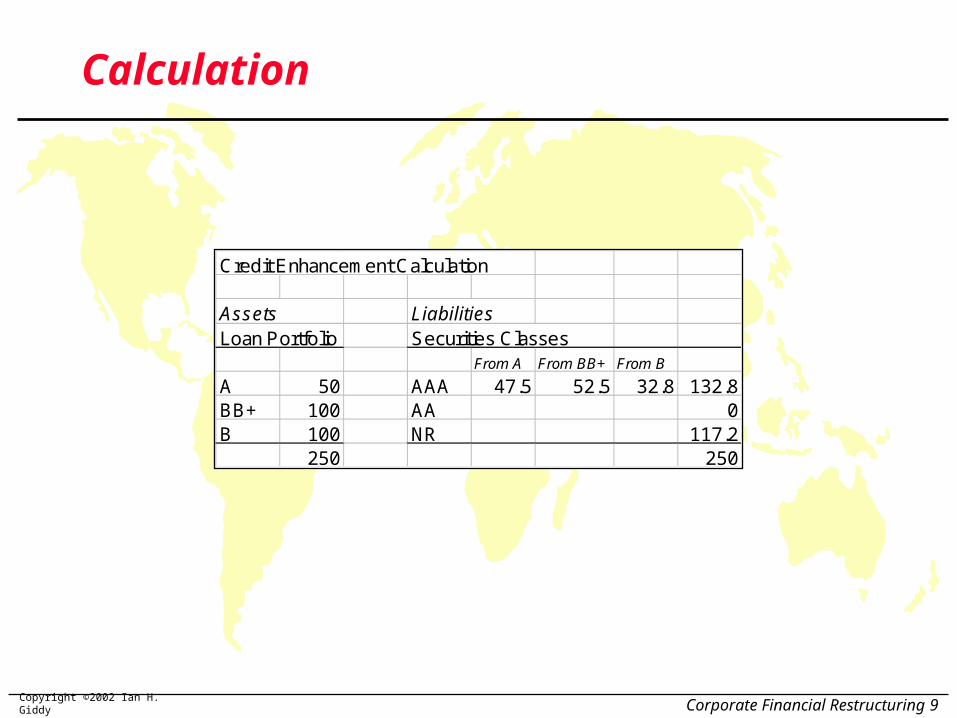

Calculation

Credit Enhancement Calculation

Assets LiabilitiesLoan Portfolio Securities Classes

From A From BB+ From B

A 50 AAA 47.5 52.5 32.8 132.8BB+ 100 AA 0B 100 NR 117.2

250 250

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 10

For Corporations: “Pure Play” Argument

Separate the credit of the assets from the credit of the originator:

Identify and isolate good assets from a company or financial institution

Use those assets as backing for high-quality securities to appeal to investors.

Such separation makes the quality of the asset-backed security independent of the creditworthiness of the originator.

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 11

Sears: Asset-Backed Financing?

SEARS

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 12

Legal Aspects

Goal: Credit quality must be solely based on the quality of the assets and the credit enhancement backing the obligation, without any regard to the originator's own creditworthiness

Otherwise, quality of the ABS issue would be dependent on the originator's credit, and the whole rationale of the asset-backed security would be undermined.

LEGAL

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 13

Three conditions enable the separation of the assets and the originator The transfer must be a true sale, or its legal

equivalent. If originator is only pledging the assets to secure a debt, this would be regarded as collaterized financing in which the originator would stay directly indebted to the investor.

The assets must be owned by a special-purpose corporation, whose ownership of the sold assets is likely to survive bankruptcy of the seller.

The special-purpose vehicle that owns the assets must be independent

LEGAL

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 14

The Alternative: Synthetic ABS

DB (Originator)

SPECIALPURPOSEVEHICLE

REFERENCE

POOL OF LOANS

(Stay on

balance sheet)

ISSUESASSET-BACKEDCERTIFICATES

CREDIT SWAPAGREEMENT

TOP QUALITYINVESTMENTS

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 15

Finance Co. Ltd(Seller)

FCL 1997-A(Special Purpose Co.)

Investors

Financial GuaranteeProvider

(if required)

Servicing Agreement

Proceeds

Sale of Assets

Proceeds

Asset-BackedSecurities

GuaranteeAgreement

Rating Agency

Top Rating

TrusteeTrust

Agreement

Finance Co.’sCustomers

Hire-PurchaseAgreement

Credit Enhancement: Guarantee Method

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 16

Finance Co. Ltd(Seller)

FCL 1997-A(Special Purpose Co.)

Senior

Proceeds

Sale of Assets

Rating Agency

Top Rating

Credit Enhancement:An Alternative Approach

Subordinated

More Subordinated

Lower Rating

No Rating

Financial GuaranteeProvider

(if required)GuaranteeAgreement

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 17

Atherton Capital(Seller)

Atherton FLF 1998-A(Special Purpose Co.)

Investors

Servicing Agreement

Proceeds

Sale of Assets

Proceeds

Asset-BackedSecurities

Mellon Mortgage(Servicer)

Franchisees(Borrowers)

LoanAgreement

Example:Franchise Loan Securitization

Servicing Advisor

LoanPayments

Class Rating Subordination

A1,A2,A-x AAA 28%B AA 22%C A 16.5%D BBB 12%E BB 8.5%F B 5.5%Issuer balance NR 0%

Class Rating Subordination

A1,A2,A-x AAA 28%B AA 22%C A 16.5%D BBB 12%E BB 8.5%F B 5.5%Issuer balance NR 0%

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 18

Deal documentation

List information requirementsDue diligence &

Meeting with management

Issuer/BankerRequests rating

Pool credit analysisLegal analysisStress testing

Credit enhancementnegotiation

Rating committeePresale reportFinal report

Rating Process

Surveillance

“Rating CLOs” (Fitch)

on Workshop Website

giddy.org/abs-hypo.htm

“Rating CLOs” (Fitch)

on Workshop Website

giddy.org/abs-hypo.htm

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 19

Trade Receivable Backed CP

Over $500 billion outstanding in US alone

Key feature is pooling of different companies’ trade receivables, allowing smaller companies to take advantage of ABS market

Need two-tier legal structure – SPV at level of each company’s receivables pool, and at multi-company program (the “conduit”)

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 20

Corporation ACorporation B

Corporation C

SPECIAL PURPOSE VEHICLE“CONDUIT”

Creditenhancement

facilityprovider

Liquidityfacility

provider

Sponsor/administrator

Legal ownerINVESTORS

Trade receivables Trade

receivables Trade receivables

Payments on maturing ABCP

Fees Fees

FeesNominaldividends

Trade Receivable-BackedCommercial Paper (ABCP)

Pool APool B

Pool C

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 21

Example:Ford Credit Owner Trust 1999-A

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 22

Ford

What is the nature and value of the assets?

How strong is the legal structure? Is the collateral sufficient? Would you

recommend purchasing the subordinated tranche?

What could go wrong with this deal? What could go right?

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 23

Ford Structure

Ford Ford Motor Credit

Ford Credit Auto

Rec. Two LP

Ford Credit Auto

Owner Trust

Receivables

Class A-1 to A6

Class B

Class C

Class D

Class A-5 and A-6

Class D

Sale

Sale

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 24

Ford Credit Auto Owner Trust

What are the economic benefits and costs to Ford in this ABS deal?

What do the underlying assets earn? What rates do the securities pay? Other costs? Who gets the excess spread?

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 25

Ford Credit Auto Owner Trust

Interest cost Underwriting fees Rating agency and other securitization costs Servicing fees Other costs Default losses

….compare with Ford Credit’s alternative

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 26

Corporation or Financial Institution requires additional funds to givecustomers financing or to finance a future revenue stream.

Are funds freely available from banks ?

Does the firm/FI have good, self-liquidatingassets ?

Do the assets have a sufficiently high yieldto cover servicing and other costs ?

Would the assets be worth more (have a cheaper all-in funding cost) if they were

isolated from the company/FI ?

Securitize the assets

Borrow frombanks

Issue equity ormezzanine capital

Get out of thefinancingbusiness

Use assets as collateral for on-balance

sheet debt

No

Yes

Yes

Yes

Yes

No

No

No

The Decision Process

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 27

Ford Structure: Default or Loss?

ReceivablesClass A-1 to A6

Class B

Class C

Class D

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 28

Can an ABS SPV Declare Bankruptcy?

Only assets in SPV available to protect investors

No need for protection from creditors Obligations are defined as limited to those

available from the assets No recourse to originator So default and bankruptcy have different

meaning than for normal corporation.

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 29

Ford Structure: Waterfall

Receivables Class A-1 to A6

Class B

Class C

Class D

Ford Structure: Waterfall

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 32

Other Deals – Check the Paydown Structure

DVI Receivables Stratford

ABSresearch.com

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 33

Paydown: Waterfall vs Soft Bullet Structure

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 34

Implications of Waterfall Upgrades

The capital allocated to a well-balanced ABS portfolio should slowly decrease over time, whereas the same cannot be said of a similar corporate loan portfolio.

Rating upgrades should be the norm in the ABS world, and downgrades the exception (currently, the situation is exactly the opposite). In the corporate world, we should rather expect downgrades to equal upgrades over long time intervals.

An ABS portfolio should be traded much more actively than a corporate loan portfolio to take advantage of its inherent rating volatility.

Copyright ©2002 Ian H. Giddy Corporate Financial Restructuring 38

Contact Info

Ian H. Giddy

NYU Stern School of Business

Tel 212-998-0426; Fax 212-995-4233

http://giddy.org