Productivity and Agglomeration Benefits in … and Agglomeration Benefits in ... on the nature and...

98

20120110 Final Report June 15 2012.docx Productivity and Agglomeration Benefits in Australian Capital Cities Final report COAG Reform Council June 2012

Transcript of Productivity and Agglomeration Benefits in … and Agglomeration Benefits in ... on the nature and...

20120110 Final Report June 15 2012.docx

Productivity and Agglomeration Benefits in Australian Capital Cities Final report COAG Reform Council June 2012

20120110 Final Report June 15 2012.docx

This report has been prepared for the COAG Reform Council. SGS Economics and Planning and its associated consultants are not liable to any person or entity for any damage or loss that has occurred, or may occur, in relation to that person or entity taking or not taking action in respect of any representation, statement, opinion or advice referred to herein. SGS Economics and Planning Pty Ltd ACN 007 437 729 www.sgsep.com.au Offices in Brisbane, Canberra, Hobart, Melbourne, Sydney

Productivity and Agglomeration Benefits in Australian Capital Cities

TABLE OF CONTENTS

1 OVERVIEW 1 1.1 Introduction 1 1.2 The evolution of Australian project and policy evaluation 2 1.3 A guide to this report 5

2 URBAN AGGLOMERATION AND PRODUCTIVITY – THE THEORY 7 2.1 Purpose 7 2.2 Theoretical foundations 7

The features of agglomeration economies 8 The nature of agglomeration 9 The macroeconomic underpinnings of agglomeration 10 The sources of agglomeration economies 12 Agglomeration and human capital 13

2.3 Evidence from the literature 14 Evidence on the nature of agglomeration economies 14 Human capital and its links to agglomeration 16 Evidence of sources of agglomeration economies 18 Macroeconomic implications of agglomeration 19

2.4 Conclusions 19

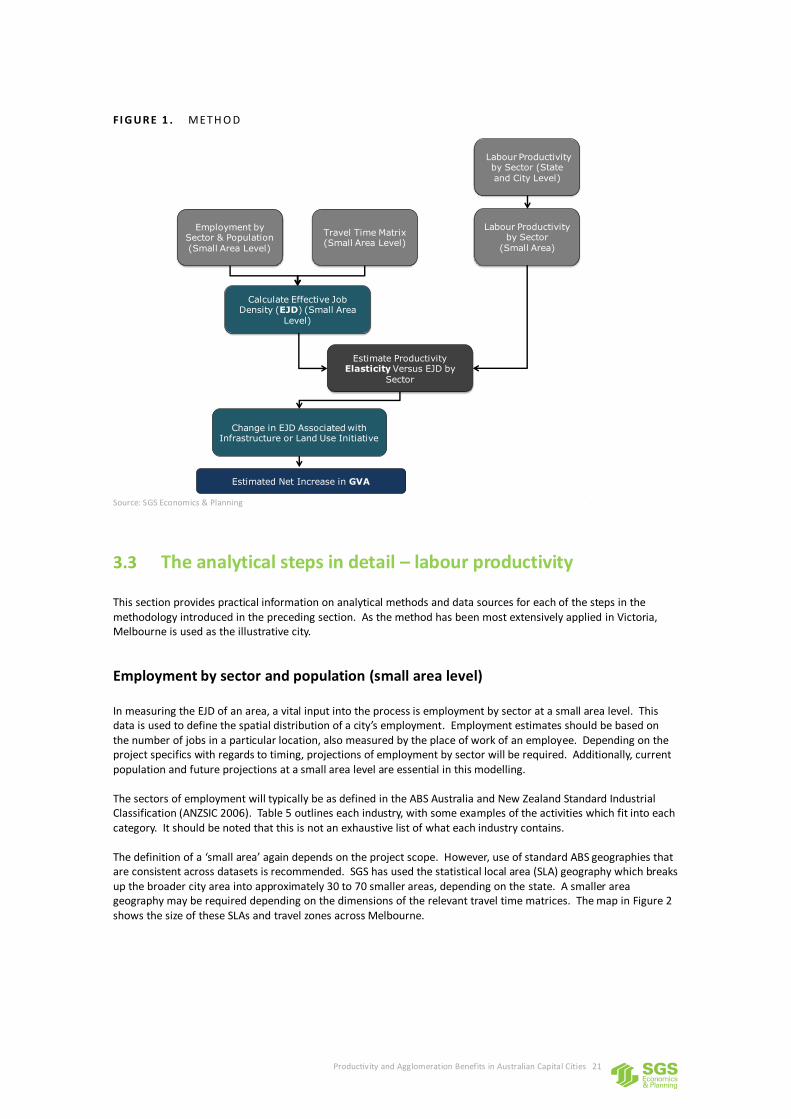

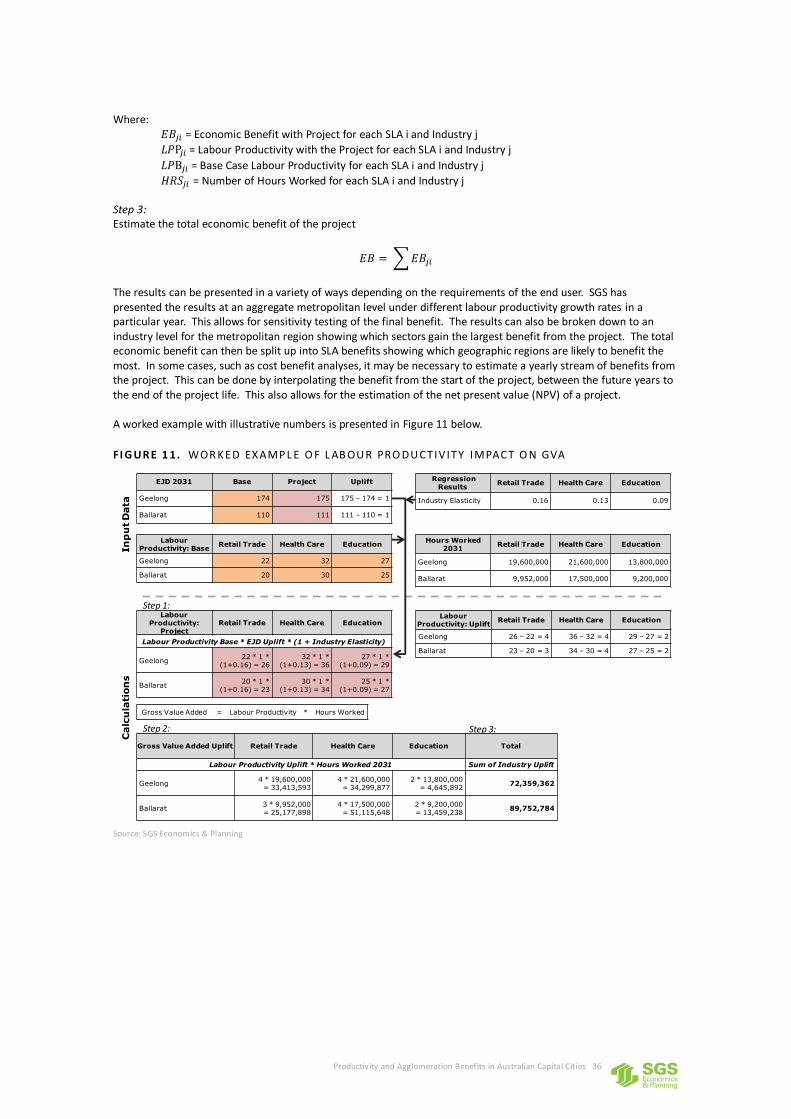

3 PRACTICAL APPLICATION IN AUSTRALIAN PROJECT AND POLICY ASSESSMENT 20 3.1 Purpose 20 3.2 Overview of method – labour productivity and agglomeration 20 3.3 The analytical steps in detail – labour productivity 21

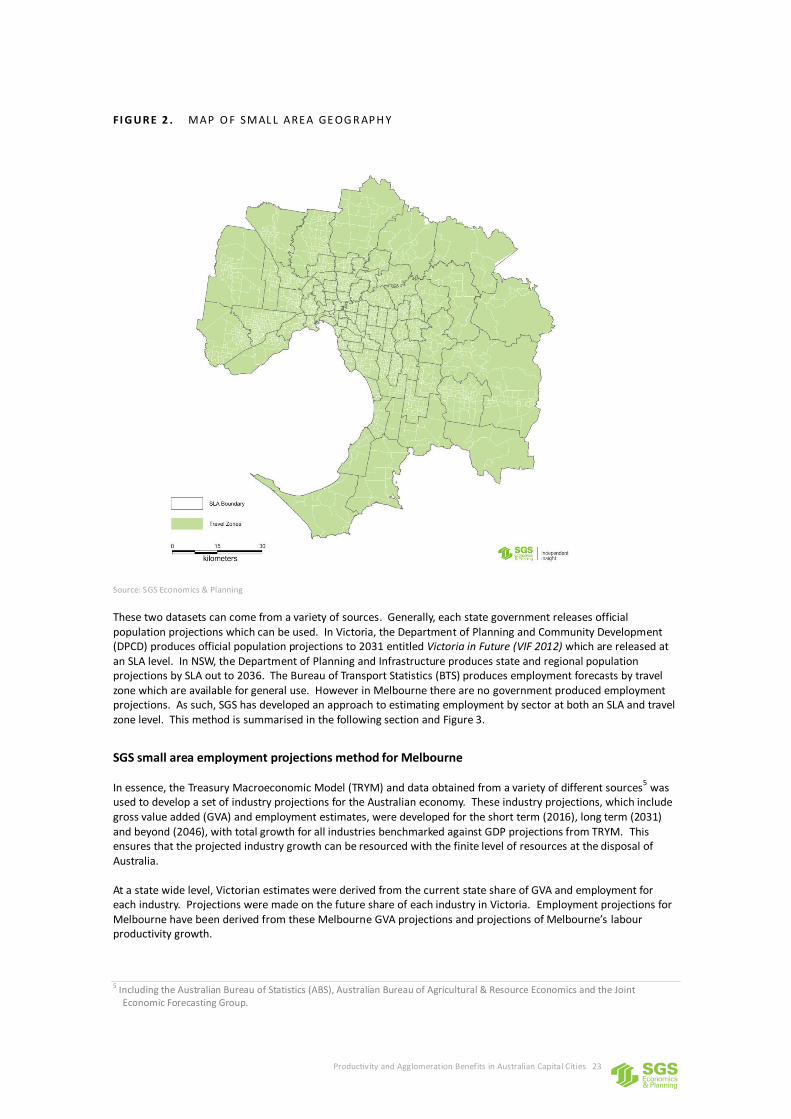

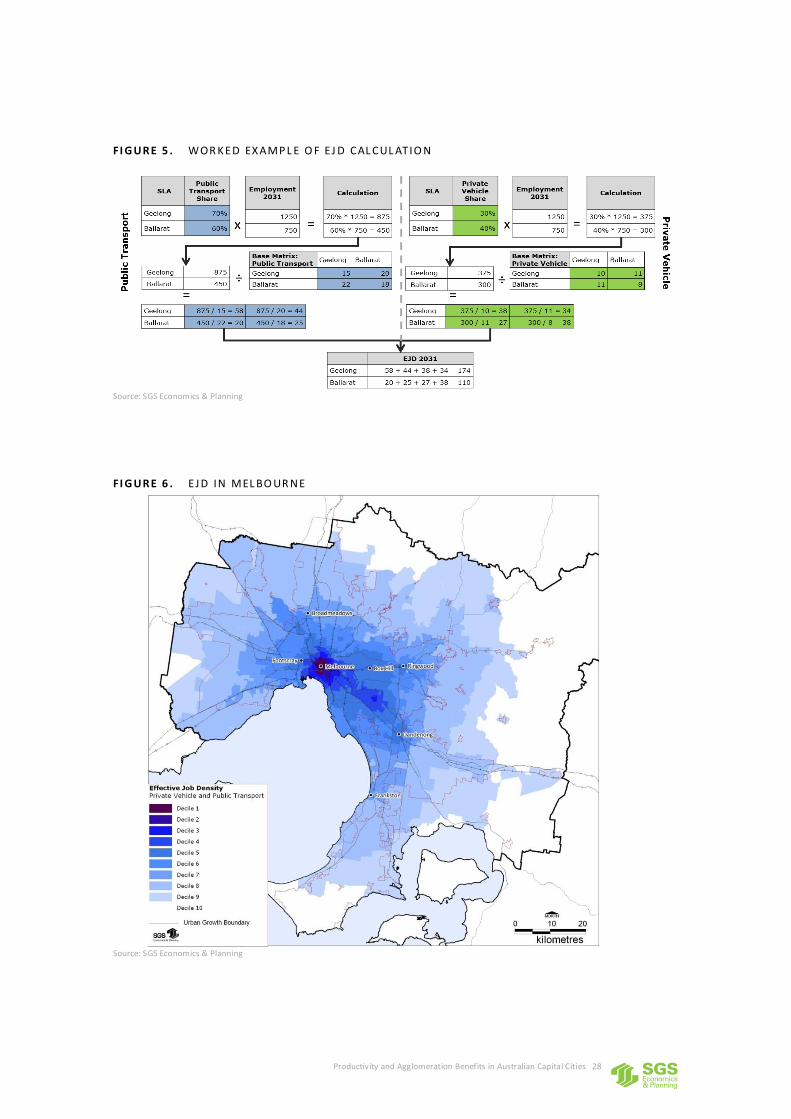

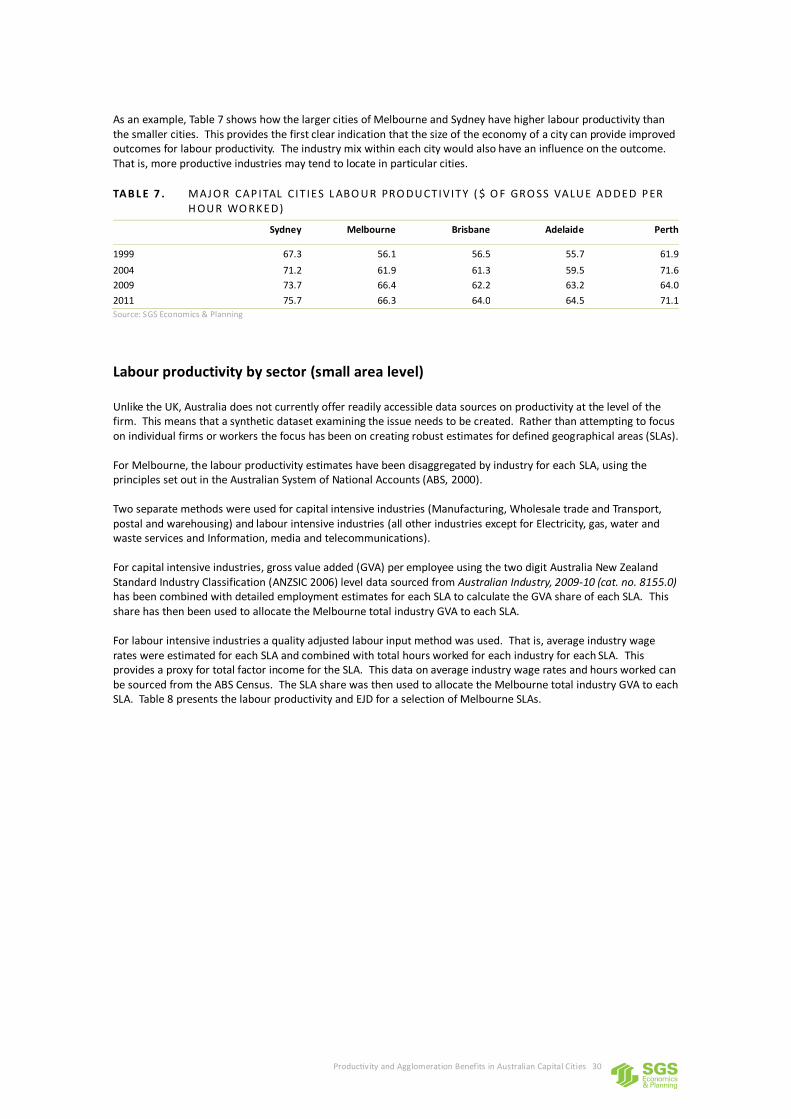

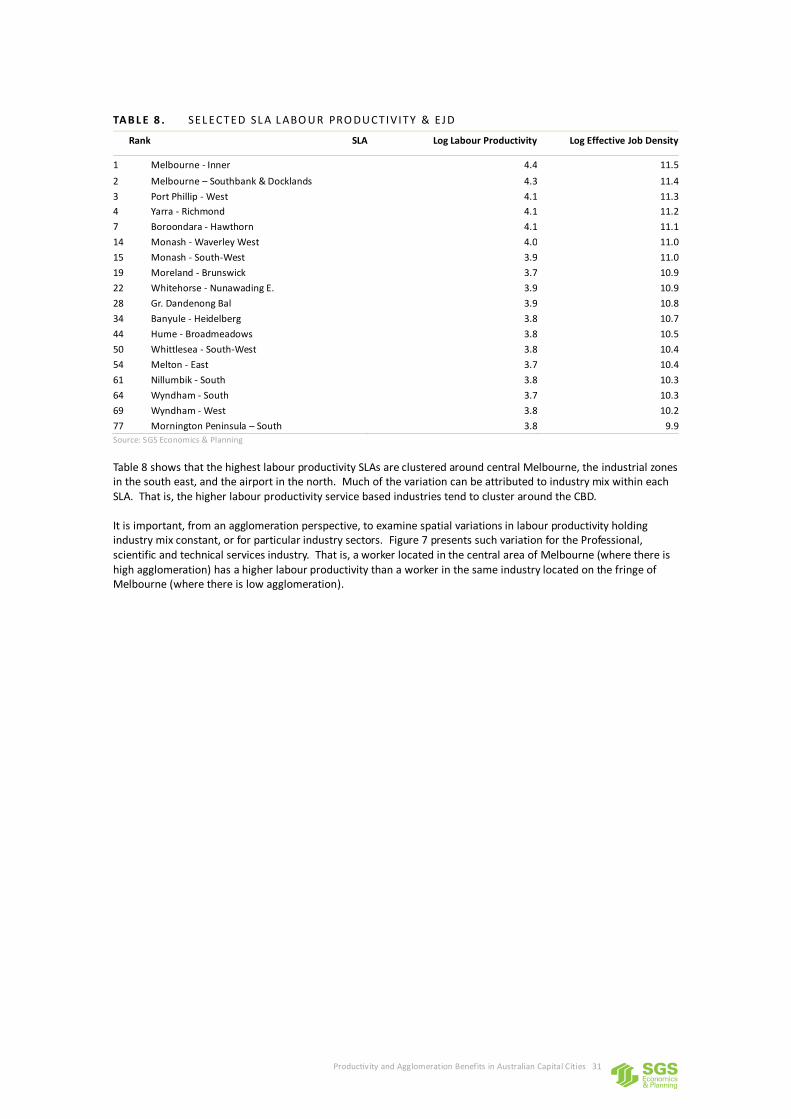

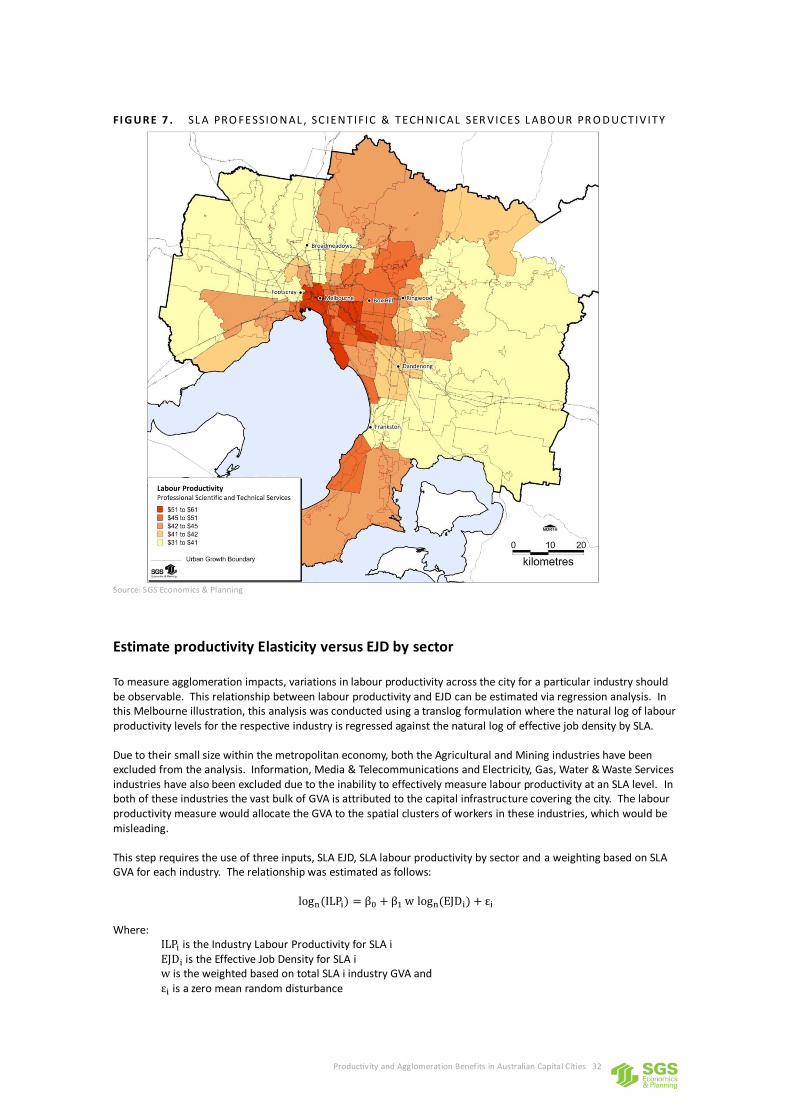

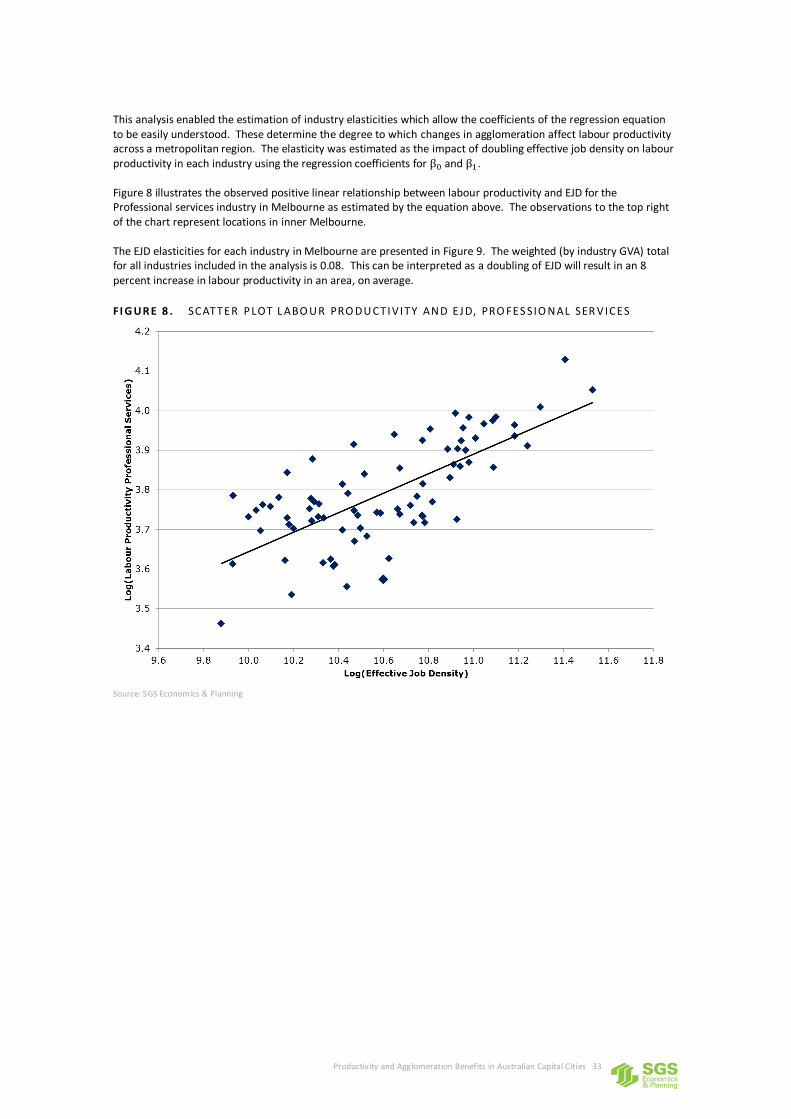

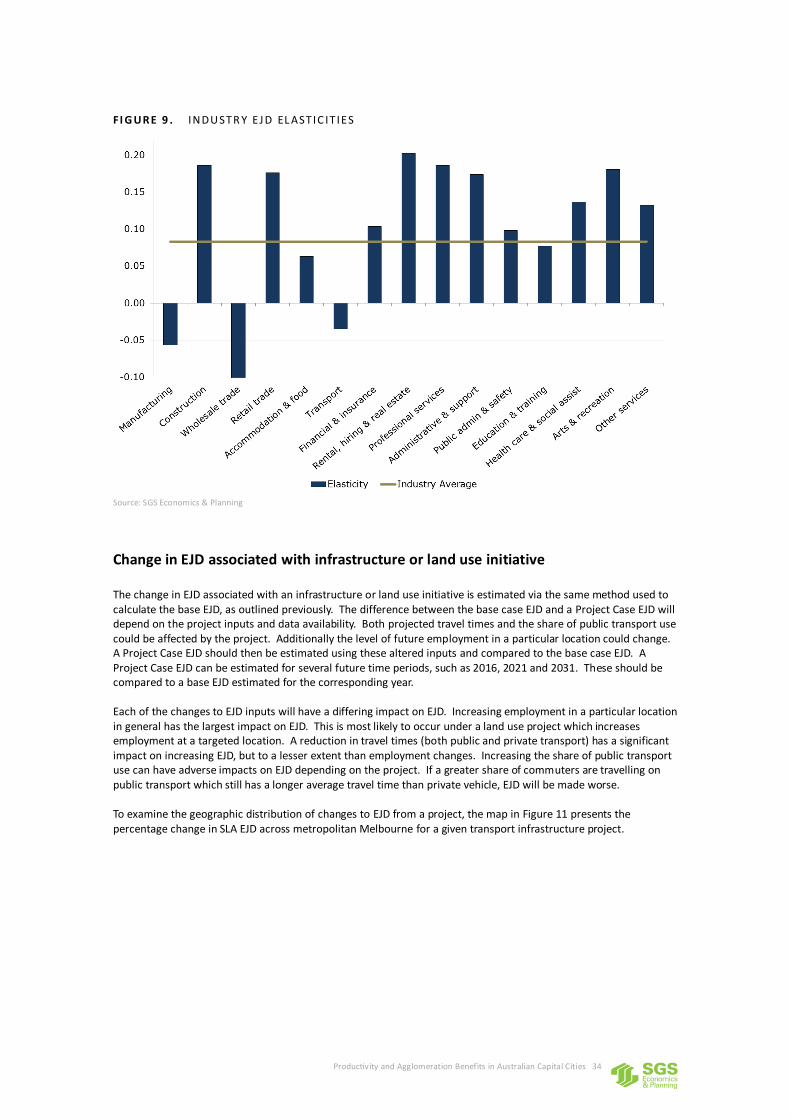

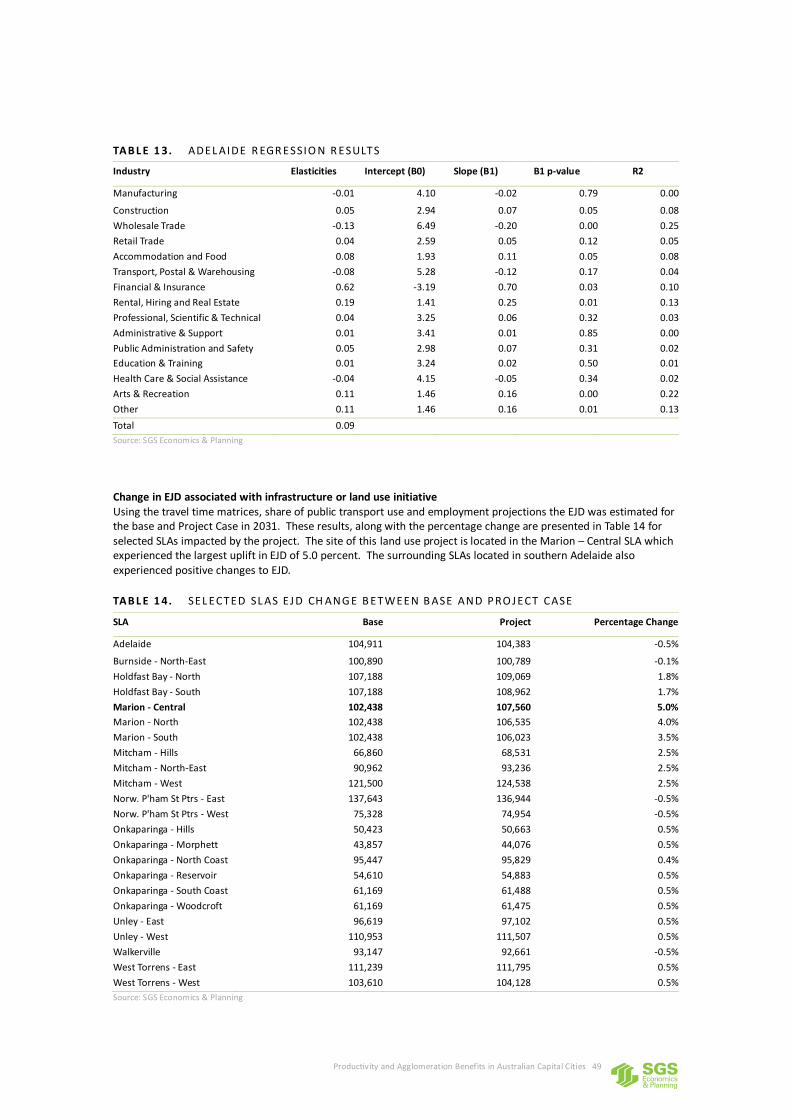

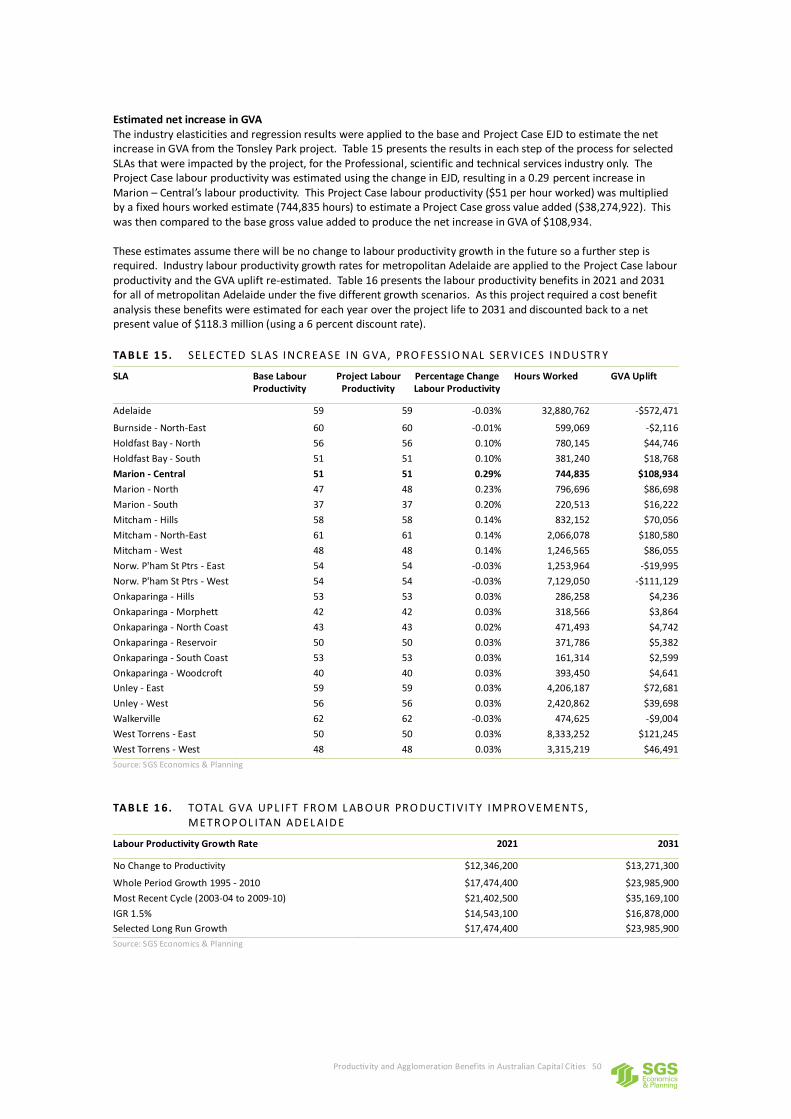

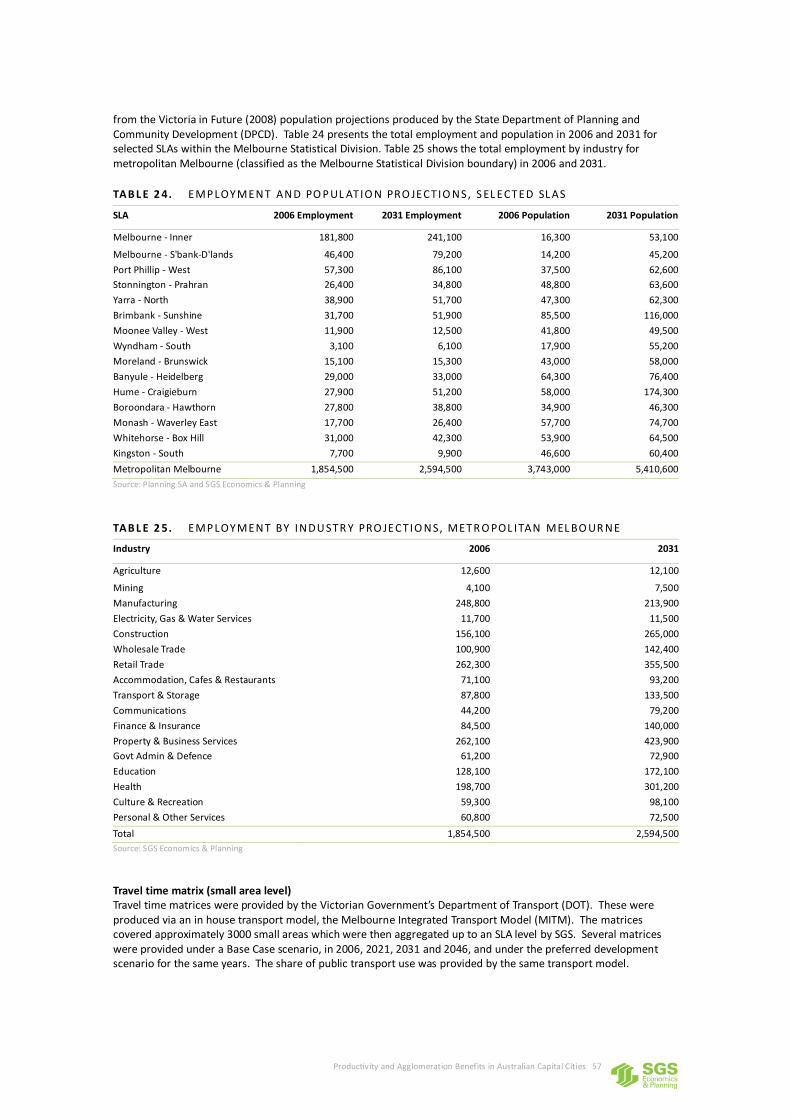

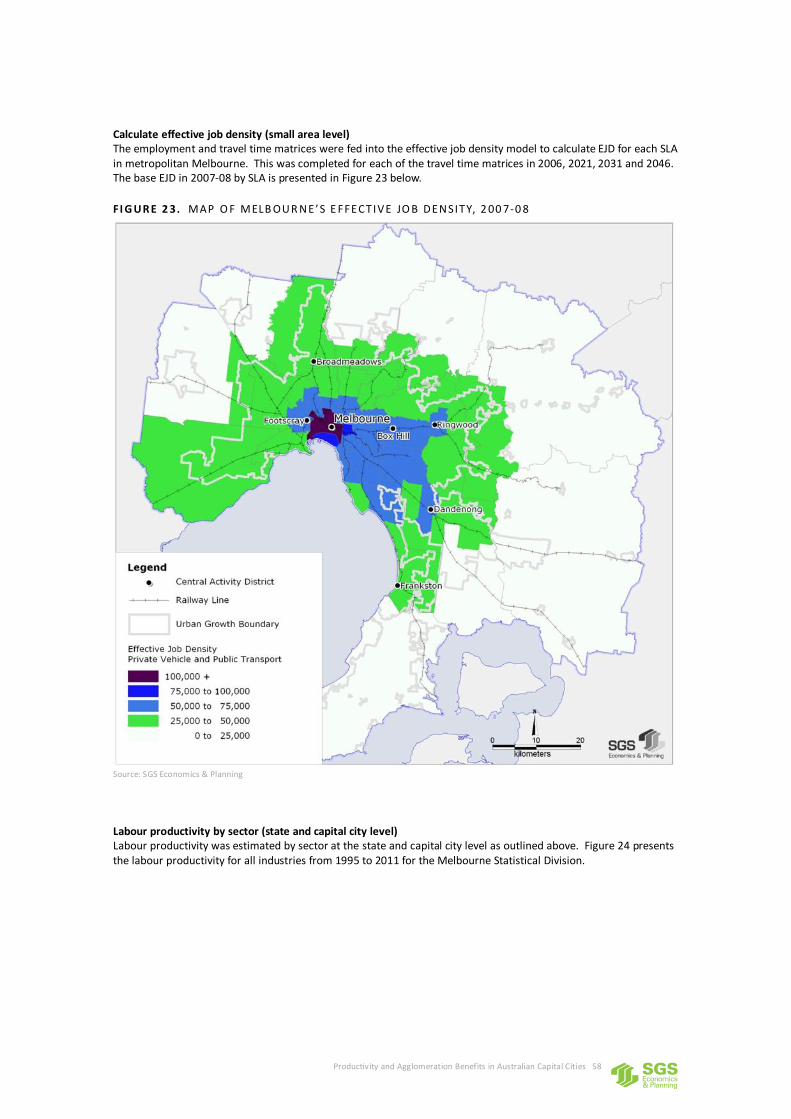

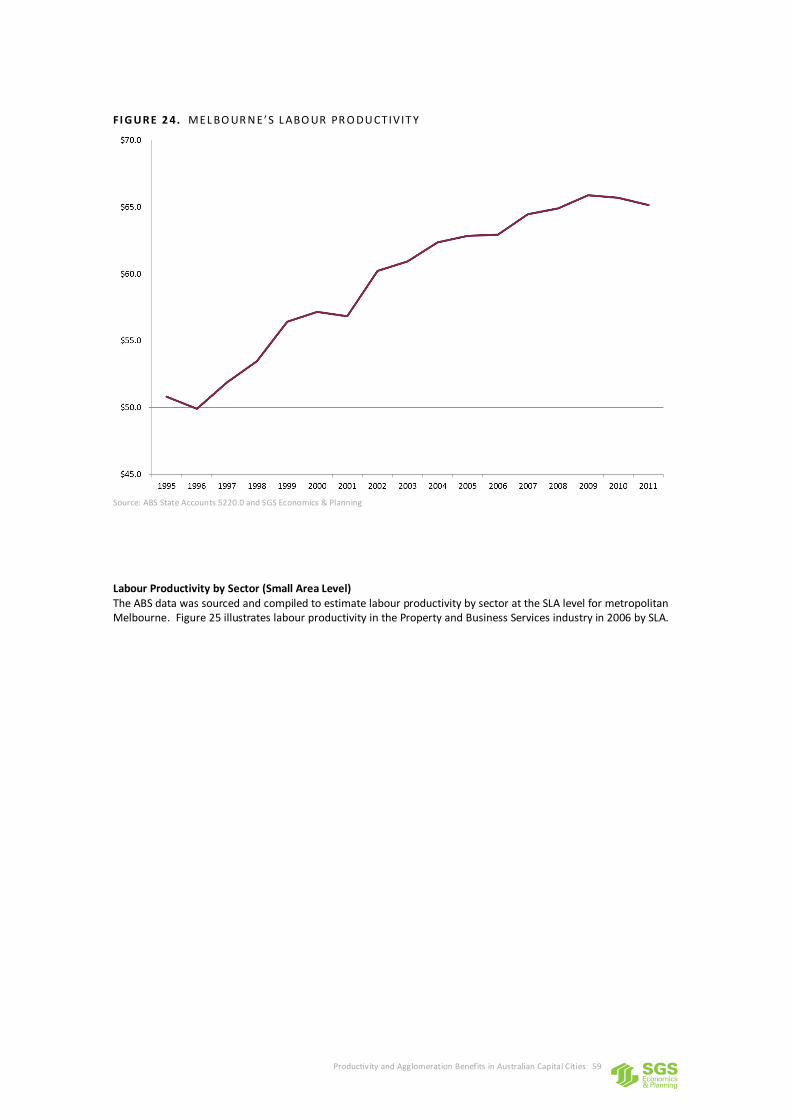

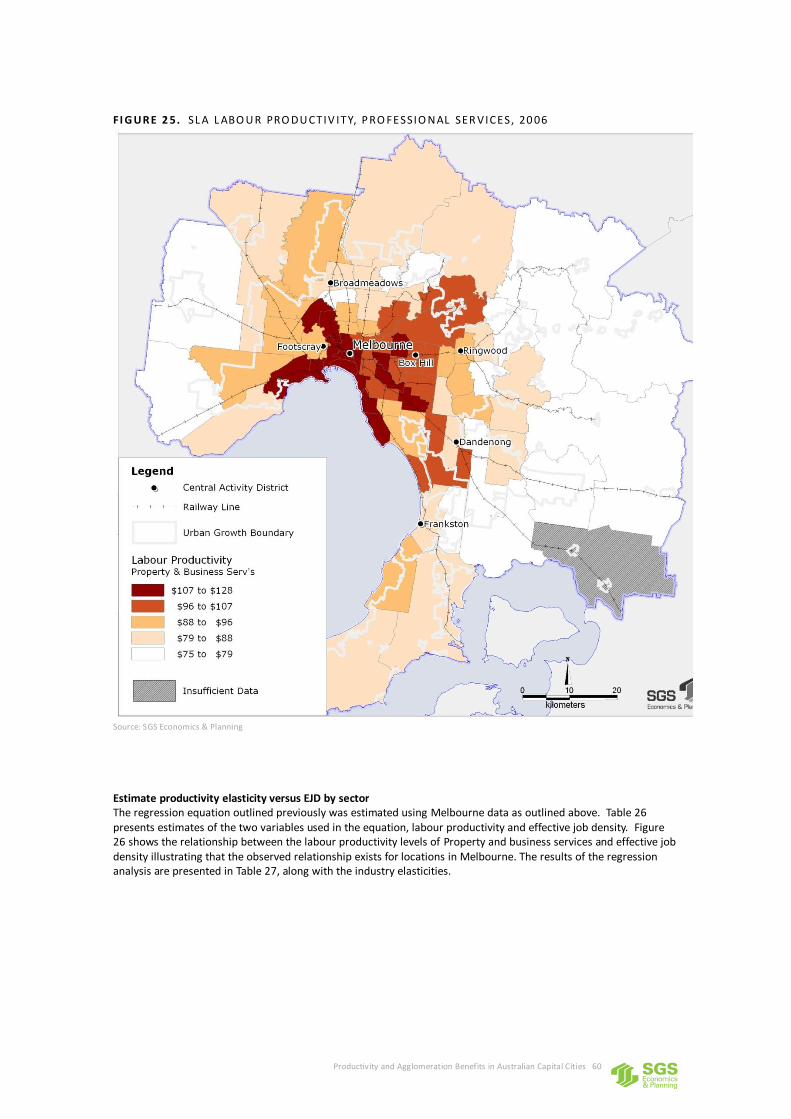

Employment by sector and population (small area level) 21 Travel time matrix (small area level) 25 Calculate effective job density (small area level) 27 Labour productivity by sector (state and capital city level) 29 Labour productivity by sector (small area level) 30 Estimate productivity Elasticity versus EJD by sector 32 Change in EJD associated with infrastructure or land use initiative 34 Estimated net increase in GVA 35

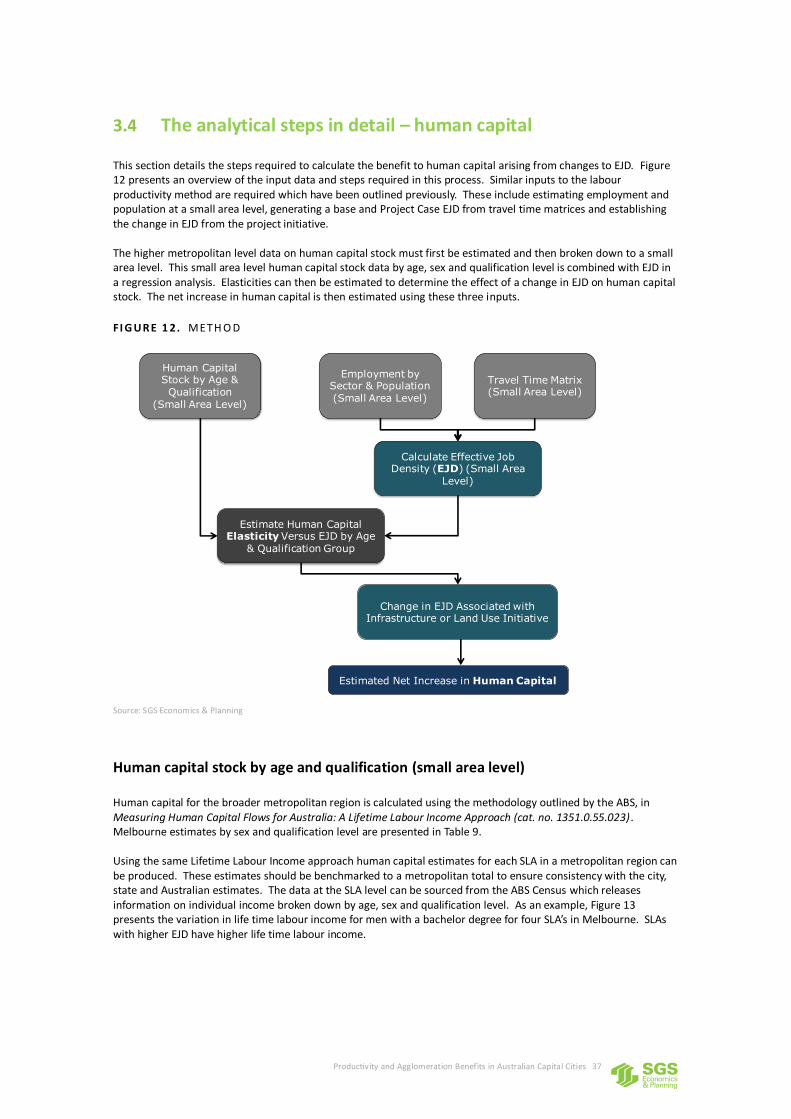

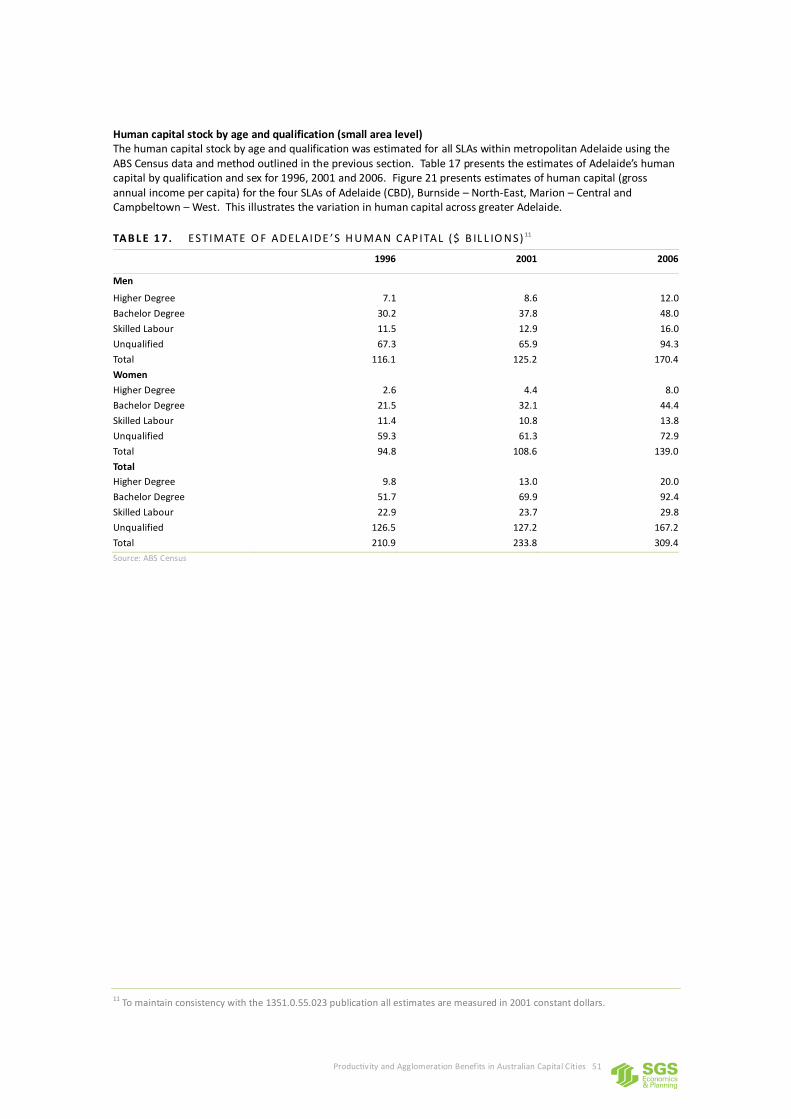

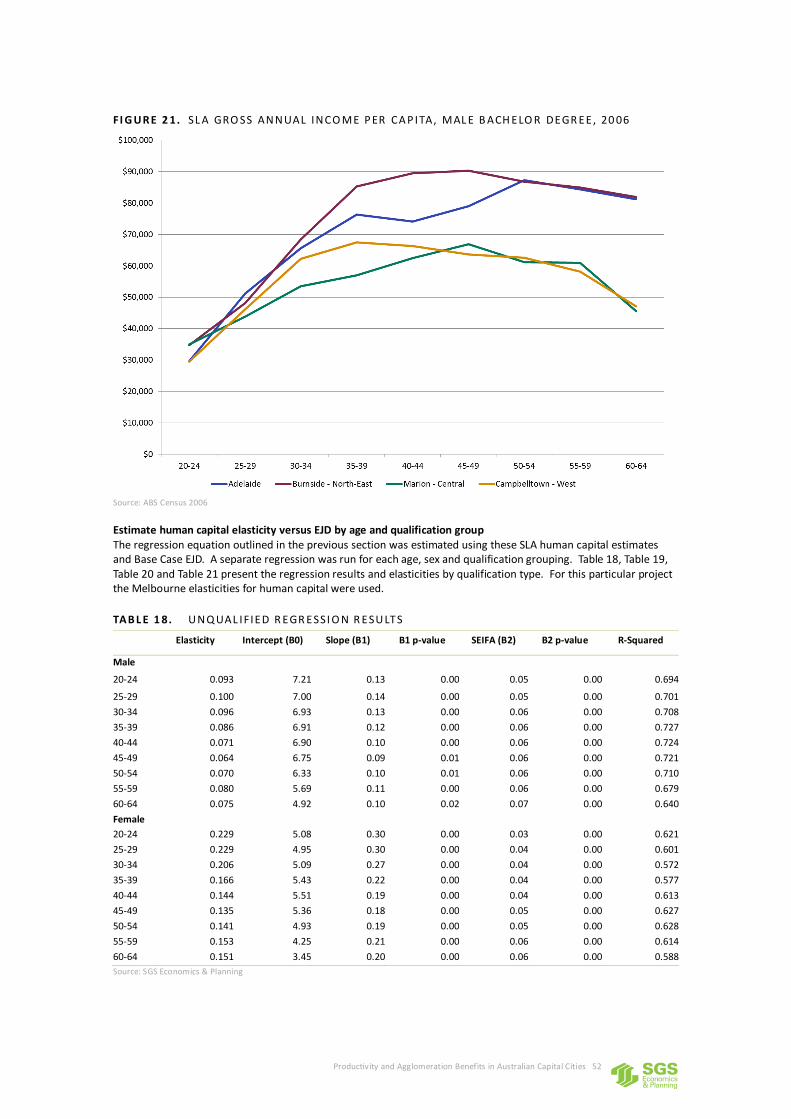

3.4 The analytical steps in detail – human capital 37 Human capital stock by age and qualification (small area level) 37 Estimate human capital elasticity versus EJD by age and qualification group 39 Estimated net increase in human capital 40

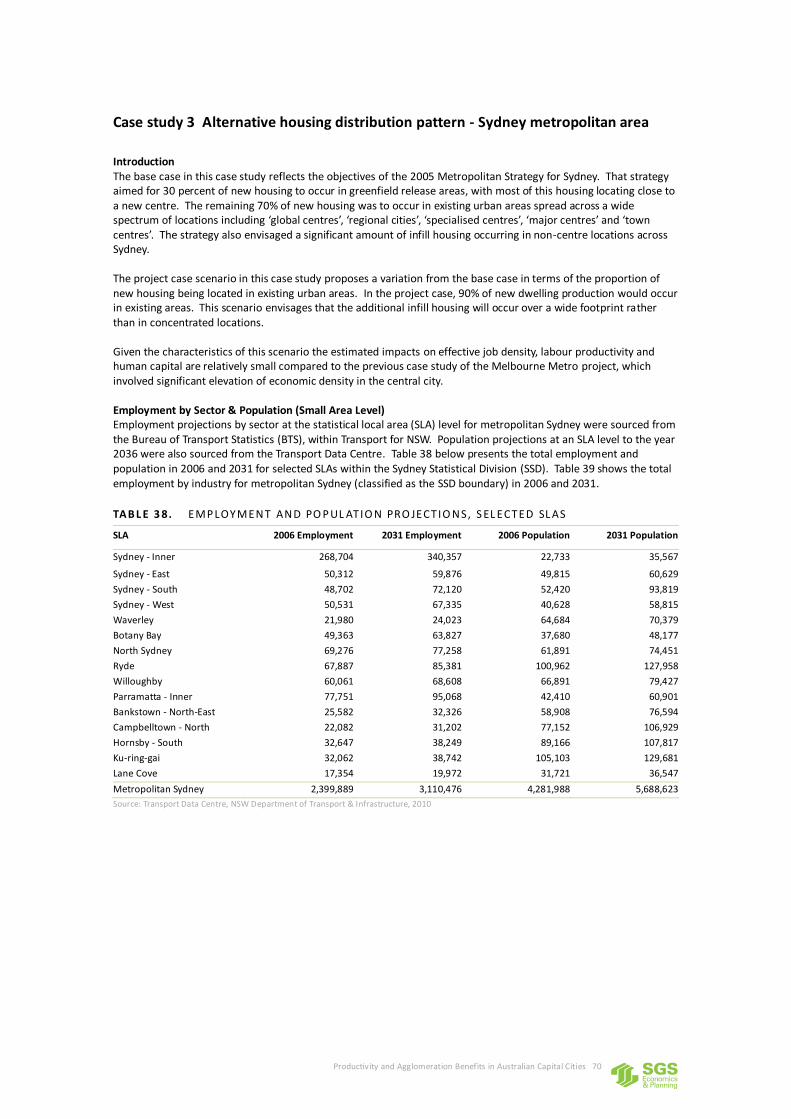

3.5 Case studies 42 Case study 1 Tonsley Park Redevelopment, Adelaide 42 Case study 2 Melbourne Metro Project – Stage One, Melbourne 56 Case study 3 Alternative housing distribution pattern - Sydney metropolitan area 70

4 A RESEARCH AGENDA FOR AUSTRALIA 84 4.1 Research issues - productivity effects of agglomeration 84

Effective density correlated with other explanatory factors 84 Use of cross sectional data to assess future productivity impacts 84

Productivity and Agglomeration Benefits in Australian Capital Cities

Data on productivity at the firm level 85 Refining the measures of effective density and productivity 85

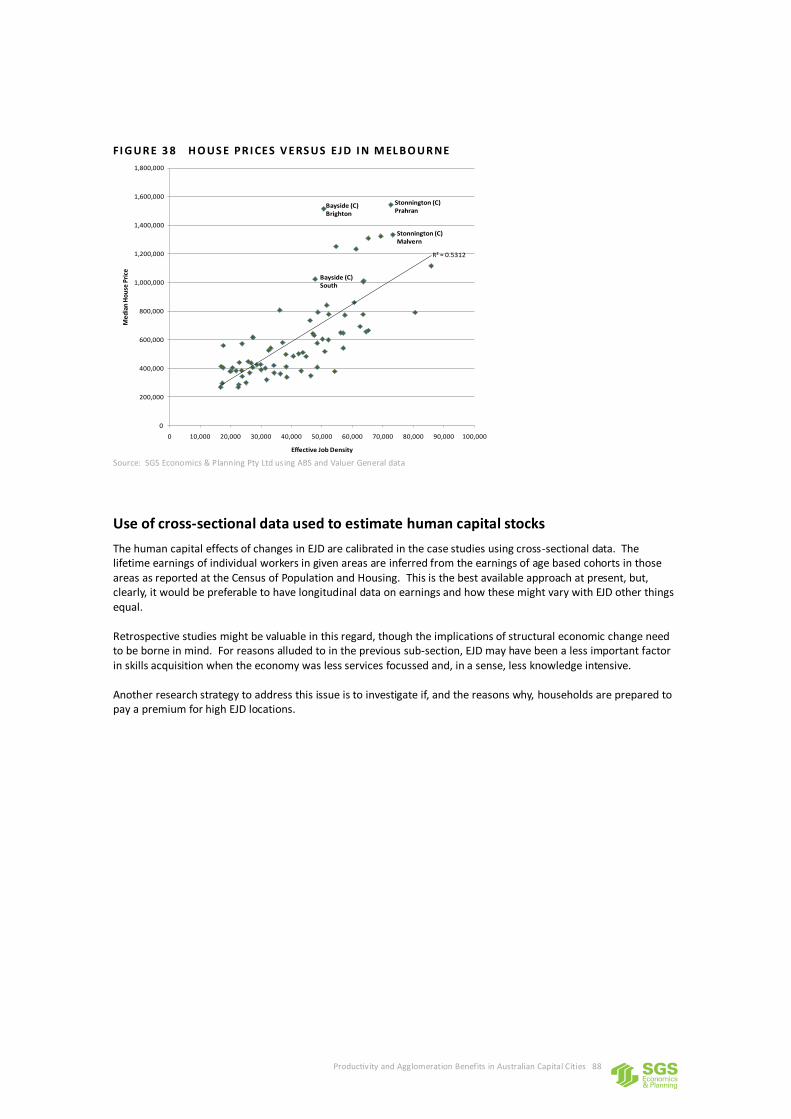

4.2 Research issues – human capital 86 Double counting with productivity effects 86 Direction of causality 86 Use of cross-sectional data used to estimate human capital stocks 88

REFERENCES 89

Productivity and Agglomeration Benefits in Australian Capital Cities 1

1 OVERVIEW

1.1 Introduction

This report responds to a research and policy development brief issued by the COAG Reform Council. The Council sought a “scoping study of empirical research on productivity and agglomeration benefits in Australian capital cities”. More specifically, the Council’s brief was aimed at:

Providing “a resource that can be used by governments as an evidence base to inform strategic planning decisions on different urban forms and settlement patterns

Assisting governments in resolving key information and data gaps on productivity and agglomeration benefits in cities.”

The genesis of the project is summarised by the COAG Reform Council as follows:

“As part of the review of capital city strategic planning systems, COAG asked the COAG Reform Council to support continuous improvement in strategic planning. To do this, the council organised a series of three workshops on common themes facing all Australian capital cities: building mandates; supporting private sector investment and innovation; and performance measurement. The council was also funded to deliver a continuous improvement project and intended to base the project on suggestions made at the workshops. Throughout the duration of these workshops, governments consistently raised the need to better understand the productivity and agglomeration benefits in our capital cities. It was highlighted that this is a major gap in our understanding of our capital cities. As a result, the COAG Reform Council agreed, with governments, to fund a scoping study of empirical research on productivity and agglomeration benefits in Australian capital cities' (CRC pers. com. June 2012)”

Thus, the brief for the project reflects an aspiration on the part of all Australian jurisdictions to lift quality and integration in city strategic planning. This includes recognition, and strategic use, of the ‘city shaping’ potential of major infrastructure investments such as inter-regional road links, metros and public transport elements which connect otherwise fragmented labour markets. Improved quality and integration in city strategic planning also encompasses an enhanced capacity to evaluate the pros and cons of different metropolitan structures, for example, poly-centric patterns of settlement and economic activity versus the mono-centric arrangement of land uses more commonly observed in Australia. A thesis underpinning the COAG ‘cities agenda’ is that urban structure can make a significant difference to the overall value delivered by major infrastructure projects, the funding of which is often a shared responsibility between the Commonwealth and other jurisdictions. This represents an important shift from previous philosophies where, in the main, the Commonwealth took a somewhat narrow portfolio perspective in appraising the merits of candidate investments. A key to this shift in philosophy is growing awareness of the productivity benefits that might accrue in cities which are structured to optimise agglomeration economies. While much of the recent policy literature emanating from the Commonwealth and other jurisdictions acknowledges the importance of urban agglomeration effects in boosting productivity, the development of practical analytical tools to isolate and measure these benefits is uneven across the country. Moreover, a lack of consensus on the nature and scope of these benefits persists. This report is a first attempt to address this information gap in COAG’s efforts to foster more productive cities. It draws together the basis, in theory, for asserting the critical importance of urban agglomeration, and then sets out a (potentially) standard method by which agglomeration economies might be measured across Australian cities using the best information which is currently available. Recognising that both the body of theory and the available relevant data are still in what might be called a ‘formative stage’, the report also proposes a research agenda to support more effective measurement of agglomeration effects for incorporation in Australian project and policy evaluation.

Productivity and Agglomeration Benefits in Australian Capital Cities 2

1.2 The evolution of Australian project and policy evaluation

As alluded to, major infrastructure projects will have impacts well beyond the interests of the sponsor agencies which, for example, may be focussed on transport issues. Their evaluation ought not be confined to a transport or any other ‘silo’, but consider impacts on a range of policy objectives relating to urban and regional settlement patterns, economy-wide productivity enhancement and human capital development. Over the past two and a half decades, all jurisdictions across Australasia have pursued a series of public sector management reforms which amount to an ‘asset management revolution’. Common initiatives have included;

Re-engineering government departments to feature sharper demarcations between service delivery agencies and central policy agencies

Mandatory corporate planning undertaken to a consistent standard across government

The requirement to conduct rigorous cost benefit analyses for all major capital projects prior to the inclusion of these proposals in the budget bidding process

The universal adoption of accrual accounting. This has made public sector managers more accountable for investment decisions and has highlighted the financial overhang from inadequate maintenance and depreciation provisioning in the past.

Commercialisation, corporatisation and privatisation of infrastructure agencies have also characterised this period of reform. Most, if not all, of these asset management reforms have had a sectoral focus. That is, they are aimed at improving value for money within (rather than across) given portfolios. However, the aggregation of investment plans which seem optimal from an individual portfolio perspective will not necessarily deliver the best return for government’s total infrastructure outlay, or the best outcome for communities in terms of competitive economies and sustainable cities. Certain types of infrastructure investment can trigger a wider set of adjustments in settlement patterns which, in turn, can either support, or work against, efficient service delivery in other portfolios. They can add to, or help contain, the underlying demand for taxpayer funded facilities and services. Indeed, these infrastructure decisions are likely to be the crucial factor in bringing about patterns of settlement which are preferred on broader economic, social and environmental grounds. They can, therefore, unlock a store of social value which ranges well beyond the standard scope of an intra-portfolio analysis for government projects and certainly well beyond the narrow financial analysis undertaken by commercialised or privatised infrastructure providers. In thinking about the potential to generate cross-portfolio benefits from government investment, the nexus between regional infrastructure projects, settlement patterns and productivity is vital. In the ledger of benefits for any major infrastructure project, including highways, railways, power plants and ports, amongst others, direct user benefits will usually hold a large share. These benefits are typically well accounted for in traditional investment analyses. As outlined, the challenge in framing a superior decision making framework in respect of these projects is to properly account for their external and cross-sectoral impacts. These impacts often manifest themselves in adjustments to settlement patterns. Over time, the locational preferences of firms and households will shift to take advantage of the agglomeration economies made possible by major infrastructure projects, thereby changing the ‘shape’ of urban and regional settlement. Thus, spatiality, and the extent to which major projects help bring about a desired settlement pattern (as expressed in planning policy), are critical considerations in optimising the return from these investments. As we will discuss in the body of this paper, UK evidence shows that productivity at the firm level is positively related to effective density – the number of jobs (services) that can be accessed within a reasonable travel time from any given point in the metropolis. Analysis of synthesised data for Australian cities, in particular Melbourne, provides similar results. This type of analysis suggests that if the distribution of jobs, or the transport system, can be adjusted to build ‘effective density’, a city can gain a competitive advantage, even if other things remain constant, for example, resource endowment, aggregate labour supply and industry structure. On the face of things, what is true of productivity at the firm level is also likely to be true in human capital development. The more opportunities households can reach within a reasonable travel time, the more they learn and acquire skills and the more productive they become. If this hypothesis is borne out by the evidence, it clearly points to spatial restructuring as a strategy for building economic competitiveness through human capital enrichment.

Productivity and Agglomeration Benefits in Australian Capital Cities 3

For decades the Commonwealth has pursued what was effectively a ‘silo’ based micro-economic reform agenda. That is, it concentrated on the establishment of clear (and narrow) commercial accountabilities for single purpose infrastructure agencies. In a substantial progression from this position, various Commonwealth institutions are now canvassing the potential for further economic advantage generated from more efficient metropolitan structures, shaped by strategic infrastructure investment. For example, Treasury is now wanting to see much more careful consideration of cross-sectoral and external impacts in the evaluation of major infrastructure projects. This is no better illustrated than in a speech by Dr Ken Henry, given shortly before his retirement from the position of Secretary of the Treasury.

....... Getting it right with cities and infrastructure has significant potential, not just from a pure economic perspective, but also from a social and environmental sustainability perspective. Getting it wrong is likely to be very costly socially and environmentally. It is easy to observe some undesirable outcomes already manifest in some of Australia's cities, with inadequate infrastructure and chronic congestion. ........ ....... There remains an important role for public investment in infrastructure. There may be infrastructure projects that are of strategic importance and that may not pass a private cost-benefit analysis; perhaps because the costs and benefits need to be amortised over too many decades or for other reasons. Intelligently conducted cost benefit analysis can deal with such issues. They should be the prime guide of public infrastructure decisions. In undertaking cost-benefit analysis, consideration of the theoretical advances that shed light on the connection between infrastructure and productivity growth can be particularly helpful. I note that this conference has been considering developments in international trade theory and spatial economics. These ideas shed light on the momentum towards urbanisation. They also provide new insights into the benefits of infrastructure and, in particular, the presence of increasing returns, clusters and agglomeration economies. For example, we traditionally value the construction of a road between two cities based on the reduction in transport costs that it yields for households and businesses, and we set this against the cost of construction. However, the predominant benefits may arise from dynamic productivity gains, including the economies of scale to which transport costs are subject, and the integration of two connected markets across which goods can be traded. In this paradigm, governments can play an important role in the wealth creation process, facilitating productivity growth through creating the conditions for integration and specialisation, by getting infrastructure and planning decisions right. This suggests that there might be a positive relationship between public and private infrastructure investment, with some types of government infrastructure investment improving the marginal returns to private investment, or increasing its scope. What is clear from the accumulated evidence is that public infrastructure is not a panacea for all that ails economies, but rather a form of capital that when deployed properly, can be effective in enhancing growth and well-being. To deliver these outcomes there are two important elements for government to consider. First, the need for infrastructure investment to take place in carefully designed and planned networks. Second, the promotion, in public and private infrastructure markets, of competition. For this reason, some major international cities have a metropolitan level planning authority, which coordinates planning and development. Mega cities, such as London, Tokyo, and New York, all have metropolitan planning authorities, which underwrite their city's amenity and productivity. There have been recent calls for similarly empowered bodies in Australia. (Henry, 2010)

Henry’s sentiments are echoed in publications issued by Infrastructure Australia (IA), the Commonwealth Government’s principal adviser on infrastructure priorities. For example, in its June 2010 report to COAG, IA stated that “urban transport projects must focus integrated land use and be part of broader multi-modal transport plans”. Moreover, in the case of public transport investments, these ought to “leverage higher intensity land use outcomes in and around transit hubs” (p 17). IA goes on to explicitly require broad based evaluation of infrastructure projects, breaking from any silo perspective.

Productivity and Agglomeration Benefits in Australian Capital Cities 4

“To win Infrastructure Australia support, urban infrastructure proposals will need to be well integrated with surrounding land use, and will need to leverage high quality, higher intensity land use outcomes that maximise the benefit of the infrastructure investment and contribute to a more compact, sustainable and diverse urban form. Proponents will be encouraged to pursue opportunities that deliver on multiple national priorities for cities, such as leveraging concurrent outcomes for increased productivity; improvements to public transport operations and accessibility; provision of opportunities for affordable, diverse and age-friendly housing; showcasing water, energy and other sustainability innovations; and adapting to climate change impacts.” (IA, 2010, p20)

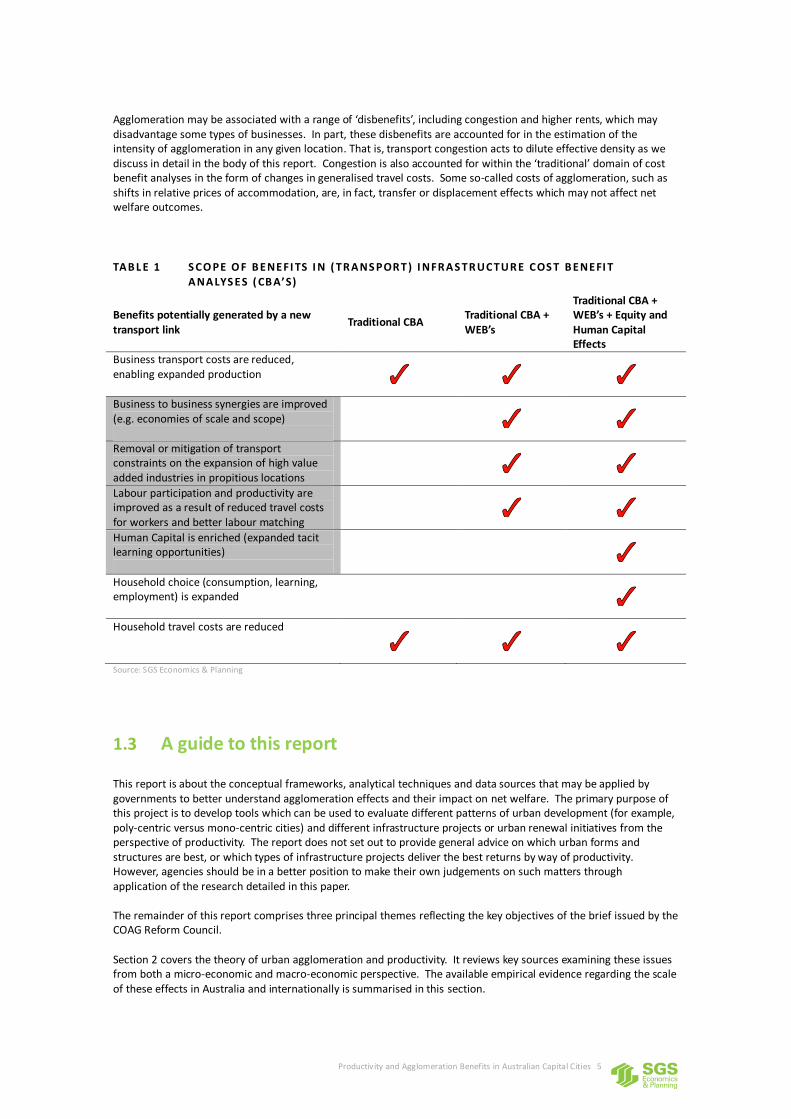

In summary, the policy agenda for more efficient and productive cities in Australia implies a significant broadening in the scope of impacts taken into account in project appraisals. We illustrate this in Table 1 with reference to a generic major transport project. ‘Traditional’ cost benefit analyses are generally confined to a relatively narrow set of user benefits and environmental externalities. Recently, these analyses have been extended to take into account ‘wider economic benefits’ (WEBs), which encompass agglomeration benefits for firms and improved labour participation and productivity through reduced travel friction. A notable published example of the difference WEBs can make to the estimated net welfare contribution of a major infrastructure project is provided by London’s CrossRail project. In this case the focus was on the fact that transport investment in question would relieve constraints on the growth potential of areas within the metropolis known to have clear competitive strengths in high value added service industries (see Text Box 1).

Text Box 1. WEBs and London’s CrossRail

“The CrossRail project in London is an underground east-west rail link connecting existing rail networks on each side of the city. An original economic appraisal had concentrated only on direct user benefits – savings in time and comfort for travellers – which were assumed to capture all of the economic benefits. The project was expected to deliver significant capacity and accessibility benefits to the city, estimated at about £12.8 billion (net present value) to transport users. But the overall project cost gave a BCR which was not sufficient to secure Government funding. Buchanan (2007) extended that analysis by developing an approach which valued the impact of CrossRail on central London growth and productivity. A key aspect of this was the quantification of potential employment growth through to 2076 and calculation of how much of this potential employment growth would be curtailed if limited transport capacity resulted in ‘crowding out’, with passengers unable or refusing to travel on heavily overcrowded lines. Buchanan estimated that wider economic benefits would add additional welfare benefits of £22 billion pounds and have a GDP impact of £44 billion pounds. These were (respectively) 1.7 and 9 times more than the conventional welfare and GDP benefits.”

Source: Quoted from Department of Transport (Victoria) 2012, p20

There is, today, a degree of consensus in the literature and amongst practitioners regarding the admissibility of these WEBs in cost benefit analyses. Somewhat more controversial is the inclusion of the human capital development impacts of major projects. This controversy is not so much related to the conceptual justification for these impacts, but rather to measurement matters, in particular the potential for double counting with firm based productivity effects. A sixth external impact of major transport projects may also be brought into consideration, that is, the capacity of these projects to offer expanded choices to households which may otherwise be locked into sub-metropolitan regions with poor educational, employment, health and service opportunities. This equity impact lies at the frontier of the current literature and is beyond the scope of the current paper. The territory of this report dealing with the identification and measurement of agglomeration effects is shown in the shaded cells of Table 1.

Productivity and Agglomeration Benefits in Australian Capital Cities 5

Agglomeration may be associated with a range of ‘disbenefits’, including congestion and higher rents, which may disadvantage some types of businesses. In part, these disbenefits are accounted for in the estimation of the intensity of agglomeration in any given location. That is, transport congestion acts to dilute effective density as we discuss in detail in the body of this report. Congestion is also accounted for within the ‘traditional’ domain of cost benefit analyses in the form of changes in generalised travel costs. Some so-called costs of agglomeration, such as shifts in relative prices of accommodation, are, in fact, transfer or displacement effects which may not affect net welfare outcomes.

TAB L E 1 S CO PE O F B ENEFI TS I N ( TR ANS POR T ) I NFR AS TR UCTUR E COS T B ENEFI T ANALYS ES ( CB A’S)

Benefits potentially generated by a new transport link

Traditional CBA Traditional CBA + WEB’s

Traditional CBA + WEB’s + Equity and Human Capital Effects

Business transport costs are reduced, enabling expanded production

Business to business synergies are improved (e.g. economies of scale and scope)

Removal or mitigation of transport constraints on the expansion of high value added industries in propitious locations

Labour participation and productivity are improved as a result of reduced travel costs for workers and better labour matching

Human Capital is enriched (expanded tacit learning opportunities)

Household choice (consumption, learning, employment) is expanded

Household travel costs are reduced

Source: SGS Economics & Planning

1.3 A guide to this report

This report is about the conceptual frameworks, analytical techniques and data sources that may be applied by governments to better understand agglomeration effects and their impact on net welfare. The primary purpose of this project is to develop tools which can be used to evaluate different patterns of urban development (for example, poly-centric versus mono-centric cities) and different infrastructure projects or urban renewal initiatives from the perspective of productivity. The report does not set out to provide general advice on which urban forms and structures are best, or which types of infrastructure projects deliver the best returns by way of productivity. However, agencies should be in a better position to make their own judgements on such matters through application of the research detailed in this paper. The remainder of this report comprises three principal themes reflecting the key objectives of the brief issued by the COAG Reform Council. Section 2 covers the theory of urban agglomeration and productivity. It reviews key sources examining these issues from both a micro-economic and macro-economic perspective. The available empirical evidence regarding the scale of these effects in Australia and internationally is summarised in this section.

Productivity and Agglomeration Benefits in Australian Capital Cities 6

Section 3 provides practical guidance on the estimation of urban agglomeration and its impact on enterprise productivity and human capital development, using the best available Australian data. This is set out in ‘user manual form’, designed to facilitate replication and testing by analysts across all Australian jurisdictions. The standard methodologies are illustrated using a variety of case studies of proposed transport and land use planning initiatives The fourth and final section of the report sets out a research agenda for improving these estimation methodologies.

Productivity and Agglomeration Benefits in Australian Capital Cities 7

2 URBAN AGGLOMERATION AND PRODUCTIVITY – THE THEORY

2.1 Purpose

This part of the report provides a review of local and international literature on the extent to which density of economic activity and urban structure might influence productivity and the accumulation of human capital. This part also identifies where Australian research and data may require strengthening to support more effective project and plan evaluation.

2.2 Theoretical foundations

Agglomeration is a term used in spatial economics to describe the benefits which flow to firms from locating in areas which have a higher density of economic activity. Locating in an area of dense economic activity (as measured by employment) allows firms to achieve economies of scale via a large customer base. Within that large customer base, the opportunity for economics of scope is also presented to firms. These concepts are defined further as follows.

Text Box 2. Key definitions

Economies of scale describe the falling per unit (marginal) cost of production as output increases. Internal economies of scale relate to a firm regardless of industry, market or environment. External economies of scale relate to a benefit to a firm from industrial organisation. Diseconomies of scale describe increasing costs (and falling profit) with increased outputs, possibly due to complex firm organisation and associated costs. Economies of scope relate to factors that make it cheaper for a range of products to be produced together rather than produced individually, via cheaper centralised functions (management, finance, IT, marketing) or from links elsewhere in the business process.

This section aims to distil the theoretical underpinnings to agglomeration by considering a number of questions. What are the nature and the sources of increasing returns (external economies of scale) that lead to agglomeration economies? Is the agglomeration economy regional or local? Is the agglomeration economy restricted to an individual industry or does it extend across multiple industries? Are the economies of scale impacts felt immediately or is there a lag between the agglomeration economy being established and productivity improving? Is the agglomeration economy driven by the volume of interactions occurring or is it driven by the nature of these interactions? In addressing these questions, this section first summarises historical advances in understanding agglomeration. Then, the nature of agglomeration and its sources are described. Much of the literature surrounding agglomeration economies is based on microeconomic theory and empirical studies. Literature related to agglomeration can be traced back to the writings of Marshall (1920). Marshall’s work,

Productivity and Agglomeration Benefits in Australian Capital Cities 8

despite the passage of a century, still provides an excellent description of the conceptual benefit which firms can gain by locating in a particular location. Since Marshall’s time, agglomeration has been measured in a number of ways including city population (Aaberg, 1973; Tabuchi, 1986), industry employment (Nakamura, 1985; Henderson, 1986), the number of industrial plants (Henderson, 2003b) and effective job density (Graham, 2006).

The features of agglomeration economies

Quigley (1998) provides a useful summary of agglomeration, describing four related features which give rise to greater economic efficiency. The first feature relates to scale economies, which describes declining marginal costs as production expands. Economies of scale are linked to the theory of returns to scale, which describe the relationship between inputs and outputs. Where inputs to production are fixed, proportional outputs are defined as constant returns to scale. Where outputs are more than proportional to inputs, this is described as increasing returns to scale. Increasing returns to scale can be the result of technological innovation when inputs are fixed, however, they can also result from the productivity gains stemming from agglomeration. The second feature described by Quigley (1998) concerns shared inputs in production and consumption in producing differentiated, specialised goods. Quigley’s third and fourth features are linked to the concepts of urbanisation and localisation. The World Bank (2009) provides a succinct description of these production-related economies. Three types of production-related economies are defined by World Bank (2009): internal economies, localisation economies, and urbanisation economies. Internal economies relate to reduced marginal costs for a firm via higher production yields and fixed costs. For example, a larger firm may be able to obtain volume discounts for certain inputs. Internal economies are a form of economies of scale, as are external economies. External economies are synonymous with agglomeration economies and include urbanisation and localisation economies. Urbanisation relates to the higher levels of labour productivity evident in larger cities (in terms of population, employment, or economic production). Localisation reflects the spatial organisation of a city and the ease with which firms can interact with each other. For example, consider two cities, City A and City B, each with a population of five million people. Each city is likely to gain a labour productivity premium simply from their size. However, City A is poorly organised with economic activity spread widely and poorly linked together. City B has distinct employment centres linked tightly together via robust transport links. In this case the labour productivity in City B is likely to be higher than City A. World Bank (2009) defines these concepts further, with localisation economies described as a large number of firms in the same industry and same place, which encourages knowledge spillovers, better skills matching and sharing of inputs. Urbanisation is further described as a large number of different industries locating in the same place, and the benefits that this can generate. Reduced transport costs are the third feature defined by Quigley (1998); a feature of economies which are efficiently organised spatially. Limiting the interaction between people and business due to a lack of accessibility can impact on the economy in three key ways. These are described by the National Cooperative Highway Research Program (2001) as: 1. “By increasing business costs of current delivery operations.” 2. “By limiting or reducing business sales through a reduction in effective market size.” 3. “By increasing unit costs through loss of opportunities for scale economies in production and delivery

processes”. The fourth feature defined by Quigley is the ‘law of large numbers’ where supplies are pooled when multiple firms locate in a single area, that is, urbanisation economies. The competitive marketplace presents a firm with many potential clients, reducing risks associated with reliance on a single customer. The automotive manufacturing supply chain provides examples of the dangers of poor diversification of risk for firms, whereby the closure of the automotive assembly plant result in the closure of component manufacturers, often in the local region.

Productivity and Agglomeration Benefits in Australian Capital Cities 9

The nature of agglomeration

External economies exist where the scale of the urban environment and its component economic activities, infrastructure and resources add to the productivity of an individual firm. External economies are defined across three dimensions of scope:

Industrial Scope: The degree to which agglomeration economies extend across industries rather than being confined to firms within an industry classification or boundary.

Geographic Scope: The propensity for firms that achieve agglomeration economies to cluster in a geographically confined area to increase the potential for interactions.

Temporal Scope: The extent of continuing impact from a firm or agent’s previous interactions with another firm or agent. The concept that much business intelligence and human capital can only accrue gradually and is also subject to a degree of decay over time is central to understanding the temporal scope of agglomeration economies.

Text Box 3. Hicks-Neutral

Hicks-Neutral applies when a technology (or in this case agglomeration) change does not alter the ratio of the marginal product of capital to the marginal product of labour. That is, after the change, the ratio between the extra output gained by employing one additional unit of capital and the output gained by employing one unit of labour remains unchanged.

In other words, the relativity between the output of capital and labour remains the same.

Rosenthal and Strange (2002) seek to evaluate the scope of agglomeration economies. Firstly, they consider whether external economies enhance labour or other co-determinants of productivity. Empirical evidence from Henderson (1986) suggests that external economies affect productivity independently of land, labour, capital and materials and are thus ‘Hicks Neutral’ (see Text Box 3). Rosenthal and Strange (2002) specify that the aggregate agglomeration effect is the sum of many individual external economy effects experienced by individual firms and agents across the three dimensions of scope identified above. If the two firms ‘j’ and ‘k’ are considered, then the agglomeration impact of j on k depends on the geographic distance between the two firm’s premises defined as dGjk; the similarity of the industrial activity that occurs at each firm, referred to as industrial distance and defined as dIjk ; and on the length of time since the last interaction occurred, a temporal dimension of distance defined as dTjk. An increase in any one of these distances will diminish an agglomeration effect between j and k. The full set of benefits that accrue from an agglomeration effect is defined as K. In addition to the impact of the geographic, industrial and temporal distance between the two firms, the scale of activities at j and k also help determine the scale of agglomeration benefits experienced. The benefit accrued, depending on the scale of activities at both firms, is represented as q(xj,xk). If we hold the scale of activities constant, the benefit accruing from firm j’s interaction with firm k can be defined as (dGjk, dIjk, dTjk). The total benefit of agglomeration can be expressed as: Aj = ∑ K E K q(xj,xk) (dGjk, dIjk, dTjk), (1.0) The construction of the equation (1.0) indicates that A varies across different firms and agents because each firm or agent belongs to a particular industry at a unique location and exists for a given period of time. Rosenthal and Strange (2002) assert that most of the research on agglomeration economies to date has grouped industries and firms into politically defined regions. Activity in neighbouring regions is assumed to have little or no effect on the grouped industries and firms and productive activity in the region is assumed to be location unspecific. The measure of agglomeration benefit (above) can be further adapted to form part of an estimation of industrial output by firm j where industrial output is a function of agglomeration benefits and the size of the firm: Yj= g(Aj) f(xj) (1.1) Estimates of the above equation should provide measures of the productivity effect of the geographic, industrial and temporal dimensions of agglomeration. However, there are many challenges to estimating 1.1. Gathering the

Productivity and Agglomeration Benefits in Australian Capital Cities 10

information required to resolve all three dimensions of agglomeration benefits presents a daunting exercise and would involve measuring all forms of economic activity by industry and distance from j across a wide history of interaction. Thus, most agglomeration models only consider one or two of the three dimensions of agglomeration scope. In estimating (1.1), measures of labour, material and land inputs into a firm’s production process can be made from public data sets (especially in the case of labour but also for material). Measures of land use and other production inputs (such as capital) are generally more difficult to obtain. Where data is made available to the researcher at the level of an individual plant within a firm, more accurate estimates of external economies of scale are possible, such as those made by Henderson (2003b). Measurement error is another central challenge in estimating productivity effects. This has been surveyed considerably by Eberts and McMillen (1999). In larger cities, firms use capital and land more intensively than in smaller cities and this can create bias in the coefficient estimates when taken for firms operating in cities of different sizes (Moomaw 1981). In response to the challenges presented when trying to estimate the production function of a firm or plant, four indirect means of investigating the scope of agglomeration economies have been developed in the literature.

1. Study the growth in total employment resulting from agglomeration across a region or local area.

2. Identify new firms or plant start-ups and the number of jobs created.

3. Study the change in wages resulting from agglomeration across a region or local area.

4. Study the change in rents resulting from agglomeration across a region or local area.

There continues to be debate as to whether agglomeration economies can be ascribed to the benefits from localisation or urbanisation economies. Recent contributions to the literature (World Bank 2009, as described earlier) have suggested that these are separable and often concurrent sources of productivity advantage. Localisation economies resonate with the concept of industry clusters and are more relevant to smaller cities and towns (for example, European and Chinese cities specialising in particular manufacturing products). The concept of industry clusters relates to firms co-locating due to links within the production chain. Firms get a significant benefit from the depth of skills available for a particular sector. Urbanisation economies, on the other hand, require much larger cities and flow from the ‘cross-fertilisation’ of ideas between sectors. In this sense, agglomeration also plays out through the co-location of firms, yet these firms are not necessarily linked via a production chain. Clearly, the increased density of economic activity brought about by transport and land use projects could drive both the localisation and urbanisation components of agglomeration, but are more likely to be influential with the latter depending on the scale of the city in question.

The macroeconomic underpinnings of agglomeration

As mentioned earlier, the body of research on the macroeconomic underpinnings of agglomeration is not nearly as well developed as the microeconomic-based literature. In their working paper, Varga and Schalk (2004) attempt to converge areas of macroeconomic theory to develop a framework for empirically demonstrating how geographic structure, that is, localisation, can influence macroeconomic growth. These areas of macroeconomic theory are endogenous growth theory, the geography of knowledge spillovers, and new economic geography (Varga and Schalk 2004). This section examines literature which builds a link between agglomeration economies and endogenous growth theory, and more recently, with new economic geography theory.

Endogenous growth theory The premise of endogenous growth theory is that for productivity per capita to continue to grow over the long run, continual improvements to technology are required (Aghion and Howitt 1998). This is supported by neoclassical growth models demonstrating that without technological improvements or population growth, diminishing returns would be evident (Solow 1956, Swan 1956). In their work on endogenous growth theory, Aghion and Howitt (1998) demonstrate that population growth, in the absence of technological improvements, would also lead to a decline in aggregate output over time. Indeed, exogenous technological change is shown to be the only way long-run growth in output per capita may occur, so long as the change continually offsets the effect of diminishing returns (Aghion and Howitt 1998). Hinting at links to the notion of agglomeration economies, Aghion and Howitt (1998, p.34) note that researchers suggest factors which can be accumulated, such as ‘human capital, public infrastructure and possibly knowledge’, need to be better accounted for in endogenous growth models.

Productivity and Agglomeration Benefits in Australian Capital Cities 11

Romer (1986) shows that increased specialisation of labour across a widening pool of activities can lead to increasing returns over time. His thesis is that as an economy grows, a larger market offsets the fixed costs associated with producing a larger number of intermediate inputs. This in turn increases productivity of labour and capital, leading to growth. Endogenous growth theory helps to explain how increasing returns may be achieved via specialisation and knowledge and innovation, yet it does not account for spatial organisation and how this can contribute to productivity. New economic geography helps to bridge this gap.

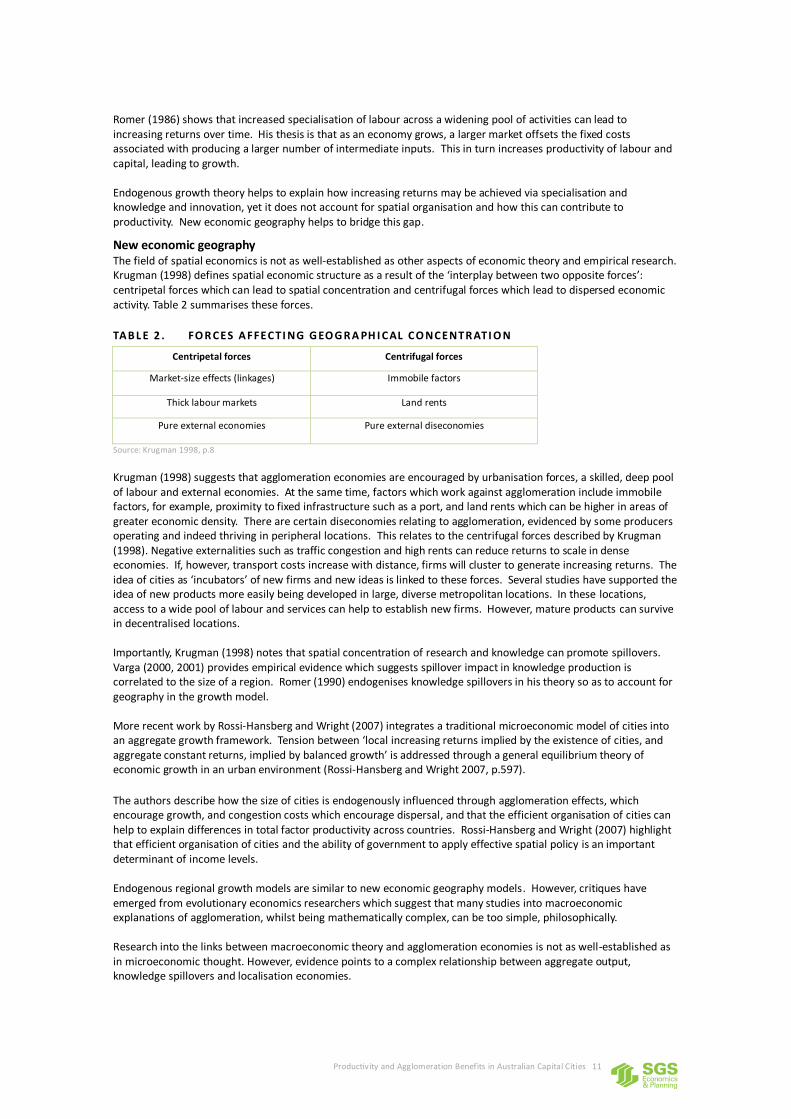

New economic geography The field of spatial economics is not as well-established as other aspects of economic theory and empirical research. Krugman (1998) defines spatial economic structure as a result of the ‘interplay between two opposite forces’: centripetal forces which can lead to spatial concentration and centrifugal forces which lead to dispersed economic activity. Table 2 summarises these forces.

TAB L E 2 . FO R CES AFFECTI NG G EO G R A PH I CAL CO NCENTR ATI O N

Centripetal forces Centrifugal forces

Market-size effects (linkages) Immobile factors

Thick labour markets Land rents

Pure external economies Pure external diseconomies

Source: Krugman 1998, p.8

Krugman (1998) suggests that agglomeration economies are encouraged by urbanisation forces, a skilled, deep pool of labour and external economies. At the same time, factors which work against agglomeration include immobile factors, for example, proximity to fixed infrastructure such as a port, and land rents which can be higher in areas of greater economic density. There are certain diseconomies relating to agglomeration, evidenced by some producers operating and indeed thriving in peripheral locations. This relates to the centrifugal forces described by Krugman (1998). Negative externalities such as traffic congestion and high rents can reduce returns to scale in dense economies. If, however, transport costs increase with distance, firms will cluster to generate increasing returns. The idea of cities as ‘incubators’ of new firms and new ideas is linked to these forces. Several studies have supported the idea of new products more easily being developed in large, diverse metropolitan locations. In these locations, access to a wide pool of labour and services can help to establish new firms. However, mature products can survive in decentralised locations. Importantly, Krugman (1998) notes that spatial concentration of research and knowledge can promote spillovers. Varga (2000, 2001) provides empirical evidence which suggests spillover impact in knowledge production is correlated to the size of a region. Romer (1990) endogenises knowledge spillovers in his theory so as to account for geography in the growth model. More recent work by Rossi-Hansberg and Wright (2007) integrates a traditional microeconomic model of cities into an aggregate growth framework. Tension between ‘local increasing returns implied by the existence of cities, and aggregate constant returns, implied by balanced growth’ is addressed through a general equilibrium theory of economic growth in an urban environment (Rossi-Hansberg and Wright 2007, p.597).

The authors describe how the size of cities is endogenously influenced through agglomeration effects, which encourage growth, and congestion costs which encourage dispersal, and that the efficient organisation of cities can help to explain differences in total factor productivity across countries. Rossi-Hansberg and Wright (2007) highlight that efficient organisation of cities and the ability of government to apply effective spatial policy is an important determinant of income levels. Endogenous regional growth models are similar to new economic geography models. However, critiques have emerged from evolutionary economics researchers which suggest that many studies into macroeconomic explanations of agglomeration, whilst being mathematically complex, can be too simple, philosophically. Research into the links between macroeconomic theory and agglomeration economies is not as well-established as in microeconomic thought. However, evidence points to a complex relationship between aggregate output, knowledge spillovers and localisation economies.

Productivity and Agglomeration Benefits in Australian Capital Cities 12

The sources of agglomeration economies

Agglomeration arises both from the benefits of firms locating in an area where they can exploit a natural advantage and from firms locating together to take advantage of agglomeration economies. The relative contribution of each of these factors has been explored by Kim (1995, 1999) and Ellison and Glaeser (1999). Kim looked at agglomeration between 1860 and 1987 and regressed a location quotient – measuring the concentration of industry - against plant size, natural resource availability and dummy variables for industry sector and time. The positive coefficient returned for the natural resources variable suggested that this was highly significant. Ellison and Glaeser showed that 20 percent of agglomeration can be predicted by the presence of natural advantages. However, it is likely that, over time, the role of natural advantage in determining agglomeration has been decreasing because labour has become more mobile – enabling industries to concentrate in an area and enjoy agglomeration economies by importing labour. The research reveals little about the micro foundations of agglomeration economies. Agglomeration economies typically involve knowledge sharing, labour pooling and input sharing. Any one or multiple combinations of these micro foundations can increase productivity, which increases profitability, and leads to firm growth (Helsey and Strange, 2001). Glaeser and Mare (2001) propose that by looking at the dynamic structure of agglomeration economies, the separate contributions of different micro foundations can be identified. The lag in wage increases in response to urbanisation suggests that these shifts are the result of knowledge spillovers. Alternatively, Henderson (2003a) suggests that looking at the impact of the number of firms in a location on the productivity of their neighbours will capture the impact of knowledge spillovers. This sub-section introduces sources of agglomeration, while the following sub-section provides evidence of these sources in further detail.

Input sharing The concept of input sharing depends on the existence of scale economies in purchasing production inputs (Marshall, 1920). Without scale economies, an isolated firm could request a small batch of a production input and pay the same per unit price as for a larger order from a collective of firms. In instances where producers receive collective or multiple demands for an input, they can achieve the cost advantages from an efficient scale of production and pass some of this gain on to their customers.

Knowledge and technological spillovers With knowledge and technological spillovers, information is often exchanged between firms without being bought or sold – in contrast to input sharing (Helsey and Strange, 2002). Where exchanges do occur, these are likely to be compacted joint ventures for which data is not routinely collected. Romer (1990) defines two key sources of increasing returns: specialisation and knowledge spillovers. Economically useful knowledge is categorised into two aspects. The first is codified knowledge, which is knowledge published in books, scientific papers or patent documentation. Codified knowledge is non-rival yet partially excludable due to patenting. Nonetheless, such knowledge usually spills over into other areas. The second aspect is tacit knowledge.

Labour market pooling There are two related explanations for labour market pooling. One is that workers in large cities or industrial concentrations should be better matched to their roles. This can be examined by looking at termination rates, controlling for conditions in the local economy and industry sector. However, because employers of firms in smaller cities have fewer options with which to replace an employee should they decide to terminate the employment of that person, the actual termination rates might not indicate the full extent of matching unsuitability. Alternatively, rates of employee turnover could be studied to identify labour market pooling; high employee turnover rates indicate that workers can readily change jobs and firms can readily hire new employees. Baumgartner (1988) looks at medical practitioners and shows that in larger markets, practitioners perform a narrower range of activities, confirming that agglomeration can foster specialisation. The other explanation for labour market pooling is that it is based on risk. When a new employee commences with a firm, both the employee and the firm suffer costs if the relationship is unsuccessful and the employee is terminated. The worker will need to find another job and the employer will need to find another employee. Where the worker’s skills and the firm’s requirements are specific to an industry, both of these needs are more easily met where the industry is concentrated and there are alternative firms and alternative potential employees. Worker and firm risk are both reduced by localisation. However, industries are subject to periodic ‘shocks’ that result in workers losing their jobs. Locating in a specialised city exposes workers to a potentially greater risk of losing their job and being unable to find alternative employment locally. While this finding is intuitively sound it is difficult to test in an

Productivity and Agglomeration Benefits in Australian Capital Cities 13

Australian environment. Australia’s limited number of major cities means that there is not the level of city specialisation which is observed in the United States or Europe.

The home market effect Suppose that increasing returns result in the concentration of employment into a large factory. This, in turn, creates a large market for suppliers who seek to locate close to the large factory to reduce their transport costs. This leads to a ‘magnification’ effect where the ‘home market’ (the large factory and its suppliers) expand in a self-reinforcing process of agglomeration.

Consumption While it is broadly accepted that cities contribute to industry agglomeration and industry productivity, recent research also looks at the role of the demand side in large cities in encouraging consumption driven agglomeration of city firms. Glaeser (2001) argues that there are four processes by which this can happen. Firstly, the population of the city is large enough to create a viable local market for some goods and services that are not available in smaller centres (such as operatic performances). Secondly, a large city may create an aesthetic charm (‘pace’, ‘style’ or ‘mood’) which enhances citizen and visitor sense of wellbeing and, in doing so, encourages citizens and visitors to spend more money on leisure, food and beverage and retail goods. Thirdly, the population of the city is large enough for the provision of public goods and services that are not available in smaller centres (such as specialised medical services). Fourthly, the dense settlement pattern of cities allows goods and information to be exchanged rapidly.

Agglomeration and human capital

Agglomeration also helps to improve the quality of labour inputs available by increasing the stock of human capital. OECD describes human capital as productive wealth embodied in labour, skills and knowledge. If a large range of jobs is on offer, a worker can search through these opportunities and best match their skills to the available job, thus maximising their acquisition of skills and experience. Further to this, they have the opportunity to work in a number of different jobs and hence gain a range of experiences (which can be seen as on-the-job investment in their education) which will also translate into higher productivity. Urbanisation (the increasing relative share of cities) is also cited by Mincer (1995) as a contributing factor in the development of human capital in the United States. This helps to confirm the Matching Theory explanation for higher human capital development. Matching theory relates to the creation of relationships which are mutually beneficial over time. Glaeser and Resseger (2010) present two core knowledge-based theories on urban agglomeration. The first is based on the Marshallian concept of density and how it can facilitate learning between workers. The second theory is based on high levels of human capital and city size having a cumulative effect in further increasing productivity and knowledge. Both of these ideas suggest that age-earning profiles could be steeper in larger, more skilled cities. However, for this to be the case, productivity gains from human capital must be higher than productivity gains via technological improvements. Glaeser and Resseger (2010) provide evidence that workers learn more quickly in large metropolitan areas, particularly in areas with a higher skills profile. Whilst urbanisation and localisation boost productivity via increased economies of scale and scope, human capital improvements also lead to productivity gains via improved job-matching.

Productivity and Agglomeration Benefits in Australian Capital Cities 14

2.3 Evidence from the literature

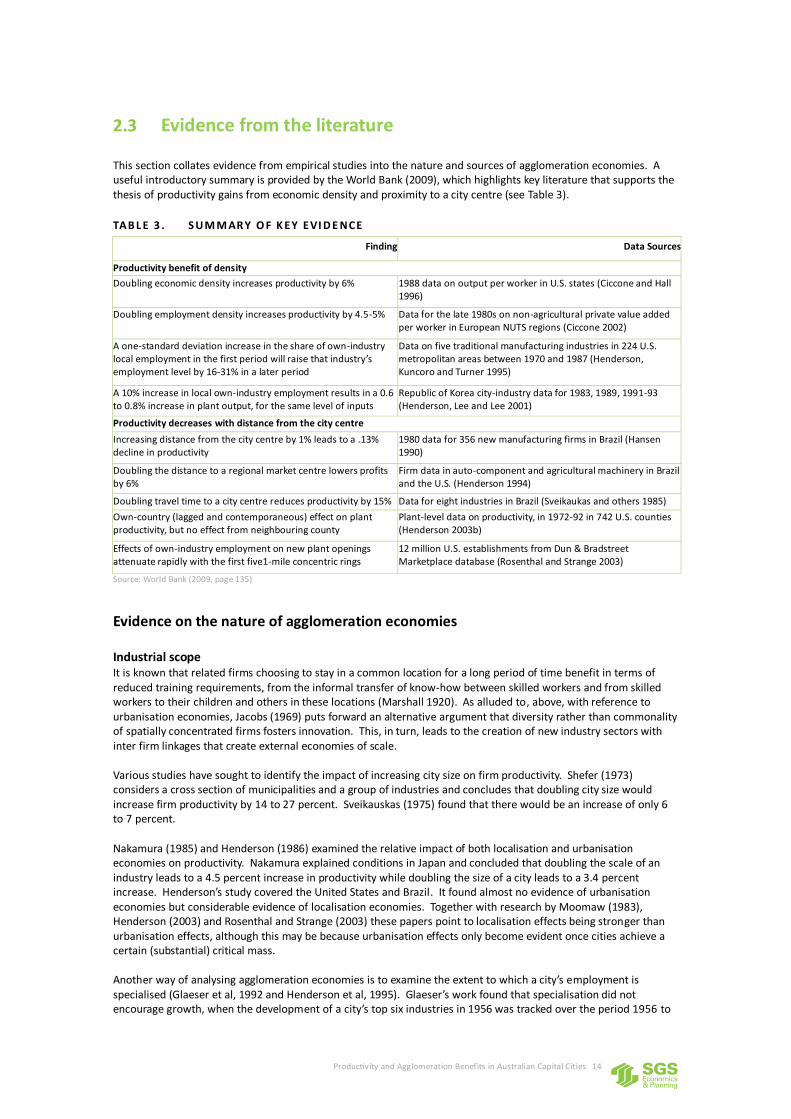

This section collates evidence from empirical studies into the nature and sources of agglomeration economies. A useful introductory summary is provided by the World Bank (2009), which highlights key literature that supports the thesis of productivity gains from economic density and proximity to a city centre (see Table 3).

TAB L E 3 . S UM M AR Y O F K EY EVI D E NCE

Finding Data Sources

Productivity benefit of density

Doubling economic density increases productivity by 6% 1988 data on output per worker in U.S. states (Ciccone and Hall 1996)

Doubling employment density increases productivity by 4.5-5% Data for the late 1980s on non-agricultural private value added per worker in European NUTS regions (Ciccone 2002)

A one-standard deviation increase in the share of own-industry local employment in the first period will raise that industry’s employment level by 16-31% in a later period

Data on five traditional manufacturing industries in 224 U.S. metropolitan areas between 1970 and 1987 (Henderson, Kuncoro and Turner 1995)

A 10% increase in local own-industry employment results in a 0.6 to 0.8% increase in plant output, for the same level of inputs

Republic of Korea city-industry data for 1983, 1989, 1991-93 (Henderson, Lee and Lee 2001)

Productivity decreases with distance from the city centre

Increasing distance from the city centre by 1% leads to a .13% decline in productivity

1980 data for 356 new manufacturing firms in Brazil (Hansen 1990)

Doubling the distance to a regional market centre lowers profits by 6%

Firm data in auto-component and agricultural machinery in Brazil and the U.S. (Henderson 1994)

Doubling travel time to a city centre reduces productivity by 15% Data for eight industries in Brazil (Sveikaukas and others 1985)

Own-country (lagged and contemporaneous) effect on plant productivity, but no effect from neighbouring county

Plant-level data on productivity, in 1972-92 in 742 U.S. counties (Henderson 2003b)

Effects of own-industry employment on new plant openings attenuate rapidly with the first five1-mile concentric rings

12 million U.S. establishments from Dun & Bradstreet Marketplace database (Rosenthal and Strange 2003)

Source: World Bank (2009, page 135)

Evidence on the nature of agglomeration economies

Industrial scope It is known that related firms choosing to stay in a common location for a long period of time benefit in terms of reduced training requirements, from the informal transfer of know-how between skilled workers and from skilled workers to their children and others in these locations (Marshall 1920). As alluded to, above, with reference to urbanisation economies, Jacobs (1969) puts forward an alternative argument that diversity rather than commonality of spatially concentrated firms fosters innovation. This, in turn, leads to the creation of new industry sectors with inter firm linkages that create external economies of scale. Various studies have sought to identify the impact of increasing city size on firm productivity. Shefer (1973) considers a cross section of municipalities and a group of industries and concludes that doubling city size would increase firm productivity by 14 to 27 percent. Sveikauskas (1975) found that there would be an increase of only 6 to 7 percent. Nakamura (1985) and Henderson (1986) examined the relative impact of both localisation and urbanisation economies on productivity. Nakamura explained conditions in Japan and concluded that doubling the scale of an industry leads to a 4.5 percent increase in productivity while doubling the size of a city leads to a 3.4 percent increase. Henderson’s study covered the United States and Brazil. It found almost no evidence of urbanisation economies but considerable evidence of localisation economies. Together with research by Moomaw (1983), Henderson (2003) and Rosenthal and Strange (2003) these papers point to localisation effects being stronger than urbanisation effects, although this may be because urbanisation effects only become evident once cities achieve a certain (substantial) critical mass. Another way of analysing agglomeration economies is to examine the extent to which a city’s employment is specialised (Glaeser et al, 1992 and Henderson et al, 1995). Glaeser’s work found that specialisation did not encourage growth, when the development of a city’s top six industries in 1956 was tracked over the period 1956 to

Productivity and Agglomeration Benefits in Australian Capital Cities 15

1987. Henderson investigated eight different industries (three evolving as high tech and five as mature industries) from 1970 to 1987 and concluded that specialisation has a positive influence on growth for mature industries but that evolving industries perform better in cities with diverse industry profiles. Duranton and Puga (2003) use French data to show that as some industries reach maturity they move from diverse cities to those with a less varied industrial profile. Theories on the origin of agglomeration economies have almost always been grounded in the concept that increasing the absolute scale of an industrial activity invariably brings benefits. For example, having more workers to choose from means workers are employed in jobs better suited to their skills (Helsey and Strange, 1990). The flip side to this argument is that diversity of industries brings cross fertilisation of technologies and leads to the birth of new industries and growth and innovation in existing ones (Chinitz, 1961). Combes (2000) finds that specialisation and diversity both have negative effects on growth for all but a few industry sectors within manufacturing. But when the same analysis is made for service industries, Combes found that while specialisation continued to have a negative effect on growth, diversity had a positive effect. The question of how agglomeration economies subside as nearby activity becomes increasingly dissimilar remains little explored in the literature. It is difficult to measure ‘industrial distance’, that is, the distance between the function of two industries. Cluster mapping based on supply relationships and the similarity of production processes such as by Ellison and Glaeser (1997) is the closest approximation available.

Geographic scope Until recently, research into agglomeration economies has defined geography on the basis of political boundaries and not assumed the gradation of effects within, and in response to firms from outside, these boundaries. Ciccone and Hall (1996) departed from this approach and measured employment density across New York State at the local (county) level. They found that doubling county population density led to an approximately 5 percent increase in productivity. Dekle and Eaton (1999) used rents to identify agglomeration economies for finance and manufacturing in Japanese prefectures. The results suggested a weak relationship to increasing urban size – a 1 percent increase in productivity for a doubling of population. Rosenthal and Strange (2003) found that industries which relied more heavily on manufactured or natural products inputs, or which produced perishable products, were more inclined to concentrate in geographic proximity. Ellison and Glaeser (1997) and Duranton and Overmans (2002) measured industry concentration and agglomeration effects at different scales and concluded that the effects are localised. Duranton and Overman (2002) found that localisation benefits dissipate beyond 50 kilometres of distance. With reference to the UK, Graham (2006) found a productivity elasticity of 0.1251 for the whole economy, 0.052 for manufacturing (with large variation within the industry) and 0.20 for services. Broadly speaking, this aligns with the theory that services prosper in very large and well-connected cities because of the rich pool of ideas on offer, whereas sectors with relatively fixed or mature business models – like manufacturing – do better in clustered locations which are relatively free of urban congestion and high land costs (World Bank, 2009). The European Conference of Transport Minister’s Round Table (2001) outlines that, by widening the area of goods markets, transport improvements may promote competition, thereby enhancing economic efficiency. The effect may be analogous to the removal of customs barriers. The removal of such barriers results in higher productivity and raises the purchasing power of populations, which benefit from the specialisation of trade. Secondly, improved transport links which increase travel speeds may have the same effect as increasing the size of the employment market, as a greater number of job-seekers will be able to travel to more distant jobs. This will allow for greater productivity as employers are better able to find employees qualified for the jobs they are seeking to fill. The Commonwealth Treasury2 outlines that “The Government also has a role in investing directly in infrastructure, innovation and Human Capital. Such direct investment may be necessary where markets for a good or service are incomplete, goods have public good characteristics, or there are positive spillovers associated with the production of a good or service”. While the Treasury recognised that there are “spillovers” which come from infrastructure and human capital investments, a methodological framework to measure the benefits from these investments is not provided.

1 That is, a doubling of job density leads to a 12.5% increase in the productivity of firms. 2 www.treasury.gov.au/.../4_Productivity_Growth_Submission.rtf

Productivity and Agglomeration Benefits in Australian Capital Cities 16

Temporal scope A key issue in the literature about agglomeration economies is the question as to whether past economic environments (say, from previous decades) can continue to impact agglomeration economies many years later, albeit indirectly. Glaeser et al (1992) and Henderson et al (1995) both incorporate this consideration into their growth models. A direct dynamic effect (often referred to as ‘knowledge spill over’) involves industrial activity from many years ago positively influencing today’s productivity. A paper by Glaeser and Mare (2001) estimates the temporal scope of agglomeration economies by regressing data on wage rates against a range of worker and location attributes. This analysis shows that there is an urban wage premium of approximately 20 percent but that this premium is enjoyed more by long time city residents than by recent immigrants. Also, when long time urban workers leave their city, the wages they earn in their new location are higher the larger the city they move from. This reflects the portability of the human capital development benefits offered by urbanisation.

Human capital and its links to agglomeration

Glaeser and Resseger (2010) note that there is a strong correlation between per-worker productivity and metropolitan area population in cities with high skill levels, but that this does not hold for less skilled metropolitan areas in the United States. The authors note that area population (urbanisation) can explain 45 percent of the variation in per-worker productivity. Over the past 50 years

3 the concept of human capital has been at the forefront of economic theory and practice.

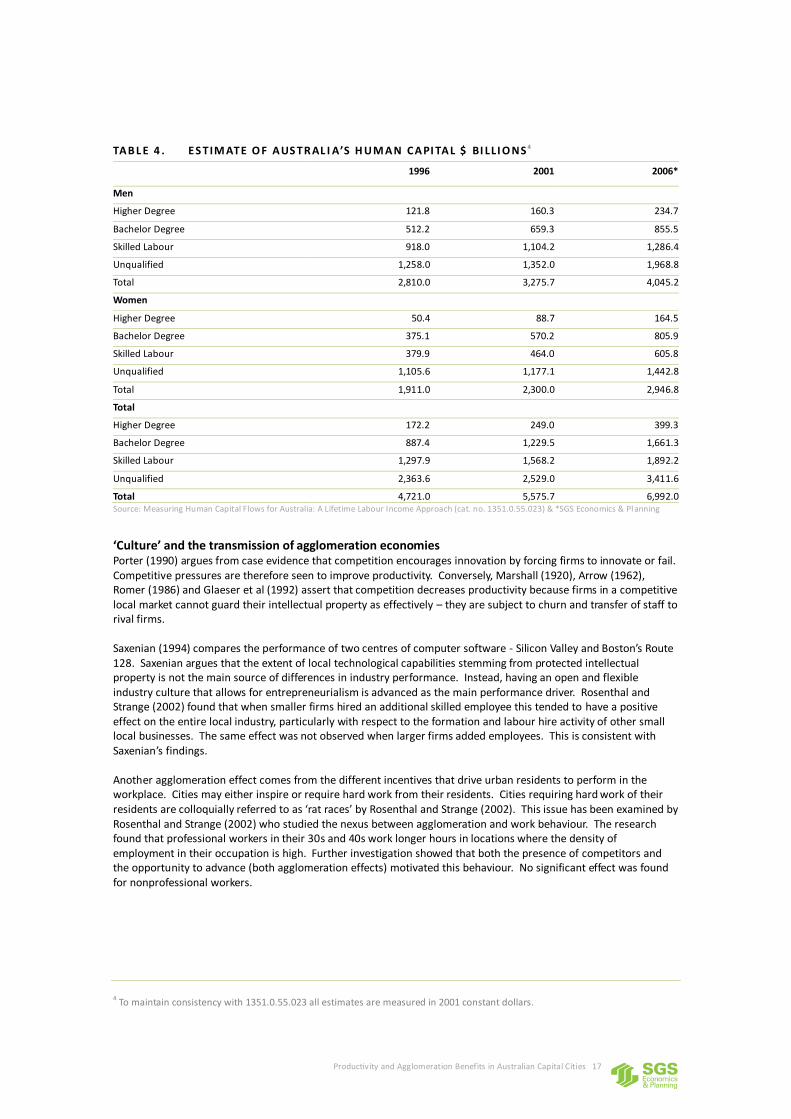

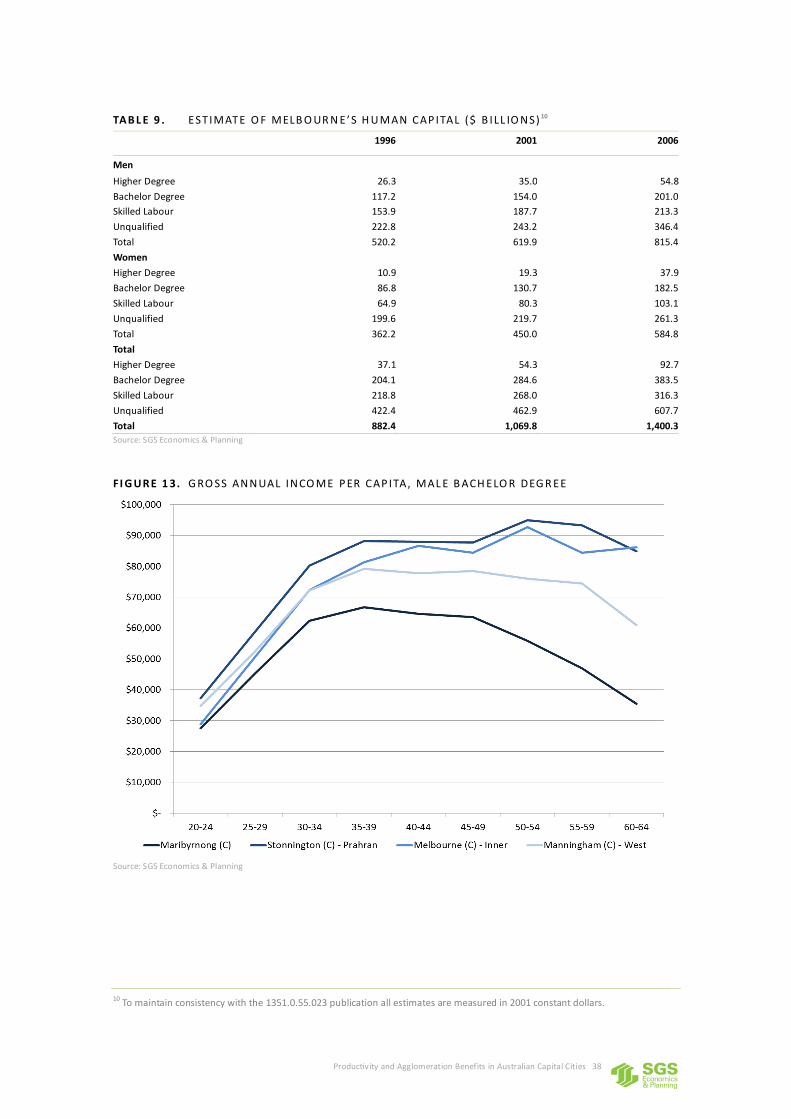

Human capital comprises the knowledge and skills which enable a worker to contribute to a firm’s production and to earn a wage. Human capital can be expanded by investment (formal education and experience gained by workers) which will increase the worker’s skill, and hence productivity. Human capital theory can be used in seeking to understand labour market outcomes and the distribution of income across society. Moreover, it also key to understanding growth in GDP. The ABS has measured Human Capital in Australia for 1981-2001 and published the estimates in Measuring Human Capital Flows for Australia: A Lifetime Labour Income Approach (cat. no. 1351.0.55.023 – see Table 4.

3 Since Becker & Schultz published their seminal work in the 1960’s.

Productivity and Agglomeration Benefits in Australian Capital Cities 17

TAB L E 4 . ES TIM ATE O F AUS TR AL I A’S H UM AN CAPI TAL $ BI LLI O NS 4

1996 2001 2006*

Men

Higher Degree 121.8 160.3 234.7

Bachelor Degree 512.2 659.3 855.5

Skilled Labour 918.0 1,104.2 1,286.4

Unqualified 1,258.0 1,352.0 1,968.8

Total 2,810.0 3,275.7 4,045.2

Women

Higher Degree 50.4 88.7 164.5

Bachelor Degree 375.1 570.2 805.9

Skilled Labour 379.9 464.0 605.8

Unqualified 1,105.6 1,177.1 1,442.8

Total 1,911.0 2,300.0 2,946.8

Total

Higher Degree 172.2 249.0 399.3

Bachelor Degree 887.4 1,229.5 1,661.3

Skilled Labour 1,297.9 1,568.2 1,892.2

Unqualified 2,363.6 2,529.0 3,411.6

Total 4,721.0 5,575.7 6,992.0 Source: Measuring Human Capital Flows for Australia: A Lifetime Labour Income Approach (cat. no. 1351.0.55.023) & *SGS Economics & Planning

‘Culture’ and the transmission of agglomeration economies Porter (1990) argues from case evidence that competition encourages innovation by forcing firms to innovate or fail. Competitive pressures are therefore seen to improve productivity. Conversely, Marshall (1920), Arrow (1962), Romer (1986) and Glaeser et al (1992) assert that competition decreases productivity because firms in a competitive local market cannot guard their intellectual property as effectively – they are subject to churn and transfer of staff to rival firms. Saxenian (1994) compares the performance of two centres of computer software - Silicon Valley and Boston’s Route 128. Saxenian argues that the extent of local technological capabilities stemming from protected intellectual property is not the main source of differences in industry performance. Instead, having an open and flexible industry culture that allows for entrepreneurialism is advanced as the main performance driver. Rosenthal and Strange (2002) found that when smaller firms hired an additional skilled employee this tended to have a positive effect on the entire local industry, particularly with respect to the formation and labour hire activity of other small local businesses. The same effect was not observed when larger firms added employees. This is consistent with Saxenian’s findings. Another agglomeration effect comes from the different incentives that drive urban residents to perform in the workplace. Cities may either inspire or require hard work from their residents. Cities requiring hard work of their residents are colloquially referred to as ‘rat races’ by Rosenthal and Strange (2002). This issue has been examined by Rosenthal and Strange (2002) who studied the nexus between agglomeration and work behaviour. The research found that professional workers in their 30s and 40s work longer hours in locations where the density of employment in their occupation is high. Further investigation showed that both the presence of competitors and the opportunity to advance (both agglomeration effects) motivated this behaviour. No significant effect was found for nonprofessional workers.

4 To maintain consistency with 1351.0.55.023 all estimates are measured in 2001 constant dollars.

Productivity and Agglomeration Benefits in Australian Capital Cities 18

Evidence of sources of agglomeration economies

Evidence of input sharing Holmes (1999) investigates the connection between a firm’s location in close concentration with similar firms and its engagement in input sharing with other firms. Holmes uses Census data on manufacturing sales at the establishment (firm) level and Census data on purchased inputs. Purchased inputs are divided by sales to give purchased input intensity which is also a measure of vertical dis-integration or input sharing. The differences in purchased input intensity between locations of concentrated similar firms and other locations across the USA were then examined. It was found that across all industries, moving from an un-concentrated location (fewer than 500 employees in the same industry) to a concentrated location (10,000 to 24,999 neighbouring employees in the same industry) resulted in a 3 percent increase in purchased input intensity. It can also be expected that in the presence of input sharing by purchasers, input suppliers would carry out more specialised functions. Because industry classification protocols typically place vertically integrated stages of production in the same category, it is difficult to test this theory. Holmes looks at the textile industry for which specialised textile finishing plants are afforded a separate industry classification from the rest of the industry, finding that where the industry was more concentrated, the ratio of specialised finishing plants to total plants tended to be higher. World Bank (2009) suggests input-sharing is an important channel for agglomeration economies, as density of activity allows more refined specialisation and wider variety of intermediate inputs.

Evidence of knowledge and technological spillovers To address the challenges of a lack of official data about knowledge spillovers, Jaffee et al (1993) use the location of firm patent citations to create a ‘paper trail’ of knowledge and technological spillovers. They found that spillovers from research to firms are greater when research and firms are co-located, with citations five to 10 times more likely to come from the same municipal area than control patents. This effect is expected to vary with industry scope – being most pronounced in those industries that are highly innovative or knowledge intensive (Audretsch and Feldman, 1996). Workers are the primary carriers of knowledge and technological spillovers. Rauch (1993) looks at the impact of education levels on wages and rents. Where average education levels were high in a district based sector this sharing of information as a public good was shown to increase wages across the sector. Rents were also shown to be higher, because the productivity reflected in higher wages was capitalised by the housing market. Charlot and Duranton (2002) find that workplace communication is more extensive in urban areas but that this accounts for only 10 percent of the urban education effect. This suggests that other knowledge and technological spillovers are taking place or that improved education levels impact other micro foundations of agglomeration economies. In summary, the exact channel of interaction whereby increased levels of education flows through to increase productivity across an industry sector is poorly understood.

Evidence of labour market pooling Simon (1988) considers the relationship between the unemployment rate and a city’s level of specialisation. Unemployment rates are shown to be greater in cities with higher degrees of specialisation - consistent with the idea of industry shocks being an important issue. It could therefore be expected that workers in specialised cities demand higher wages to compensate them for this risk. Diamond and Simon (1990) show that workers do, indeed, demand higher wages in more specialised cities and that these higher wages are also related to the cyclical variability of employment by industry. Costa and Kahn (2001) advance the argument that risk is lower and matches of employee to role are better in larger cities. In looking at ’power couples‘ – married couples where both partners have at least a bachelor degree qualification - Costa and Kahn documented a substantial increase over time in the proportional representation of this group in large cities – from 32 percent in 1940 to 50 percent in 1990. This may result from these couples having met, partnered and stayed in large cities, or it may be explained by large cities being better able to offer career opportunities that closely match the abilities of both partners than smaller cities. To test for each of these explanations, Costa and Kahn look at the differences between the location patterns of ’power couples‘ other types of couples, single persons and unmarried couples and concluded that 36 percent of the increase in concentration of ‘power couples‘ in large cities can be ascribed to the dual career hypothesis. Therefore, if the productivity of the highly educated is important for economic performance, large cities have a productivity advantage in so far as they have the ability to better match employees to roles that meet their abilities and achievable aspirations.

Productivity and Agglomeration Benefits in Australian Capital Cities 19

Evidence of the home market effect Krugman (1980) and Davis & Weinstein (1996) formally investigated this phenomenon, examining regional agglomeration across Japanese prefectures. They identified substantial increasing return effects on industrial concentration in eight of 19 prefectures. They concluded that the home market effect is an important determinant of regional concentration in both large cities and smaller localities. Hanson (1998a) looked at the shift in Mexican industrial production from Mexico City to cities along the US border in response to the NAFTA trade liberalisation agreement. In this instance, the opportunities from trade with international markets began to outweigh home market advantages from locating in the Mexico City megalopolis.

Consumption Taking Glaeser’s (2001) work as a base, Waldfogel (2003) investigates the concept that the larger markets in cities enable goods to be more closely tailored to individual consumer tastes. Waldfogel looked at radio listening patterns and identified that as a city’s population increased by one million residents, the proportion of the population who listened to radio increased by 2percent. Waldfogel identified that the number of radio stations targeting particular ethno linguistic subcultures (African and Hispanic) also increased with city population size. This suggested that radio stations were able to diversify their offer in larger cities and thus increase their total listening audience (market size). Tabuchi and Yoshida (2000) found that the real wages (spending power) of city residents was elastic (by between -7 and 12 percent) depending on city size. This is evidence that some city residents are willing to forego wages to enjoy the consumption benefits of living in a large city.

Macroeconomic implications of agglomeration

Davis, Fisher and Whited (2011) explore how important agglomeration is for aggregate growth via a dynamic stochastic general equilibrium model of cities, using aggregate data and city-level panel data. They find that local agglomeration has an impact on the growth rate of per capita consumption, raising it by about 10 percent. At the same time, this approach finds the net impact of density to be relatively small. Notably, the authors estimate that without agglomeration benefits, per capita consumption and housing would need to be ‘three percent large in each period in perpetuity’.

2.4 Conclusions