PRM - Thailivestreamsetlive.thailivestream.com/.../events/pdf/041217074548-Oppday-PRM.pdf ·...

25

PRM 3Q2017 Financial Performance Opportunity Day 4 December 2017

Transcript of PRM - Thailivestreamsetlive.thailivestream.com/.../events/pdf/041217074548-Oppday-PRM.pdf ·...

PRM 3Q2017 Financial Performance

Opportunity Day

4 December 2017

1

The information contained in this presentation is strictly confidential and is provided by Prima Marine Public Company Limited (the "Company") to you

solely for your information. Neither this presentation nor any part hereof may be (i) used or relied upon by any other party or for any other purpose; (ii)

copied, photocopied, duplicated or otherwise reproduced in any form or by any means; or (iii) redistributed, passed on or otherwise disseminated, to

any other person either in your organization or elsewhere, without the prior written consent of the Company and its respective affiliates or advisors.

By attending this presentation, participants agree not to remove this document, or any materials provided in connection herewith, from the

conference room where such documents are provided without express consent from the Company and its respective affiliates or advisors.

Although care has been taken to ensure that the information in this presentation is accurate, and that the opinions expressed are fair and reasonable,

no representations or warranties, express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness or completeness of

the information presented or contained in this presentation. The information is subject to change without notice, its accuracy is not guaranteed, has

not been independently verified and it may not contain all material information concerning the Company and its subsidiaries. None of the Company nor

any of its respective affiliates or advisors nor any of its or their respective members, directors, officers, employees or affiliates assumes any

responsibility or liability for, the accuracy or completeness of, or any errors or omissions in, any information contained herein. Accordingly, none of

the above nor any other person accepts any liability (in negligence, or otherwise) for any loss arising from or in connection with any use of this

presentation or its contents.

This presentation is for information purposes only and does not constitute or form part of any offer or invitation by or on behalf of the Company for

sale or subscription of or solicitation or invitation of any offer to or recommendation to buy or subscribe for any securities of the Company, nor shall it

or any part of it form the basis of or be relied on in connection with any contract, commitment or investment decision in relation thereto (“Securities”)

in Thailand or any other jurisdiction. Any recipient considering a purchase of Securities is hereby reminded that any such purchase should be made

solely on the basis of the information contained in a final offering document (which may be different from the information contained in this

presentation ) and subject to the selling restrictions set out therein. No public offering of the Securities will be made in any other jurisdiction outside

of Thailand where such an offering is restricted or prohibited. This presentation should not be construed as legal, tax, investment or other advice. The

information contained herein does not take into consideration the investment objectives, financial situation or particular needs of any particular

investor, and should not be treated as giving investment advice.

In addition, this presentation contains certain financial information and results of operation, and may also contain certain projections, plans,

strategies, and objectives of the Company, that are not statements of historical fact which would be treated as forward looking statements that reflect

the Company's current views with respect to future events and financial performance. These views are based on a number of estimates and current

assumptions which are subject to business, economic and competitive uncertainties and contingencies as well as various risks which are in many cases

beyond the control of the Company, and which may change over time and may cause actual events and the Company's future results to be materially

different than expected or indicated by such statements. No assurance can be given that future events will occur, that projections will be achieved, or

that the Company's assumptions are correct. Such forward‐looking statements are not guarantees of future performance and accordingly, the actual

results, financial condition, performance or achievements of the Company may differ materially from those anticipated by the Company in the forward

looking statements. The recipient is cautioned not to place undue reliance on these forward looking statements.

In providing this presentation, the Company does not undertake to provide any recipient with access to any additional information or to update the

information contained in this presentation or to correct any inaccuracies herein which may become apparent.

Disclaimer

I. Business Overview

2

I.

II.

IV. Business Outlook & Investment Plan

III. Consolidated Financial Performance

Contents

▪ Trading Business

▪ FSU

▪ Offshore Business

▪ Ship Management

Performance by Business Segment

I. Business Overview

3

Exploring & Extracting Transporting and Trading Manufacturing

44

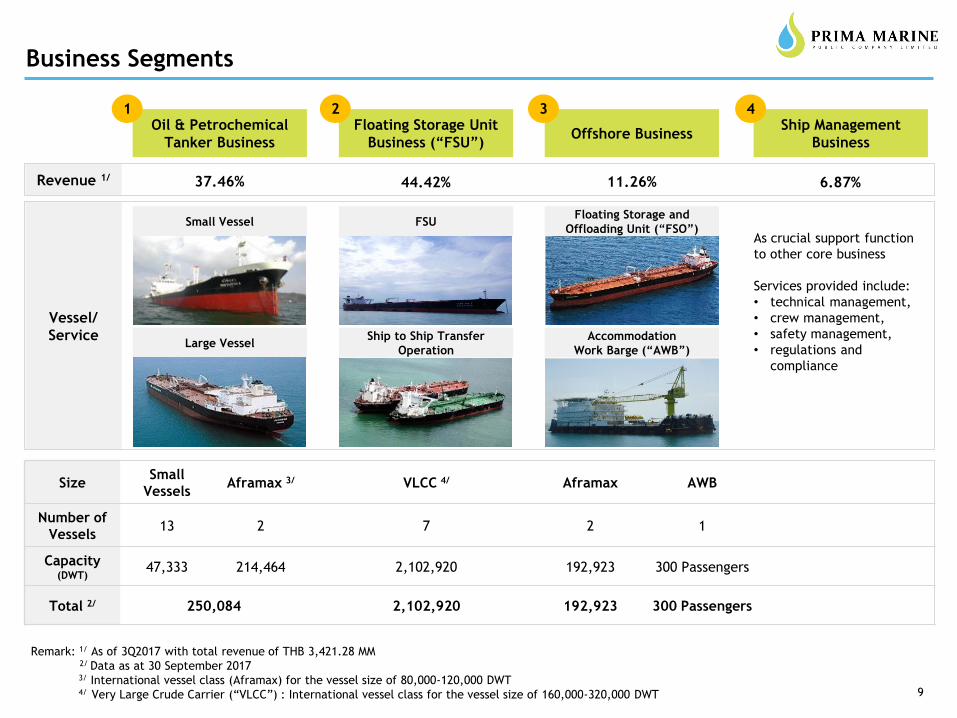

PRM’s Four Main Business Segments in Oil & Gas Supply Chain

Ship Management

Offshore Business

FSO AWB

FSU Business

FSU

Oil & Petrochemical Tanker Business

<10,000 DWT >10,000 DWT

5

Major Player in Tanker Business

Trading Area

Company NameNo. of Oil

Tankers

Vessel Sizes

DWT

Average

Age

Small Vessels

PRM Group 13 47,333 16.5

B.P.P. Supply Co., Ltd. 20 37,370 39.6

V.L Enterprise Co., Ltd. 13 33,684 18.7

Smooth Sea Co., Ltd. 6 29,344 20.7

Big Sea Co., Ltd. 12 25,630 21.1

C.& P. Co., Ltd. 4 18,012 17.8

Thai Oil Marine Co., Ltd. 3 16,917 13.0

Siam Mongkol Marine Co., Ltd. 3 13,284 22.0

P.I.N.K.Transport &Trading Co.Ltd. 3 9,057 43.0

V.C.C. Inter Marine Service 3 7,340 27.0

TMN Co., Ltd. 1 7,125 8.0

Raum-mitr Marine Oil Co., Ltd. 1 3,481 24.0

Trans Ocean Supply (1992) Co., Ltd 3 3,443 23.0

Impex Marine (Thailand) Co., Ltd. 1 2,100 30.0

Large Vessels

PRM Group 2 214,464 15

TMN Co., Ltd. 1 48,676 11.0

Thai Oil Marine Co., Ltd. 1 32,250 21.0

KEY Player of

Marine Domestic Transport

PRM Transport

• 67% of PTT marine volume

• 25% of CHEVRON marine volume

• 19% of Shell marine volume

• 25% of ESSO marine volume

Largest Oil Tanker Fleet in Thailand

Remark: Data as at 30 September 2017

No. of

Charter-in Vessels

13 vessels

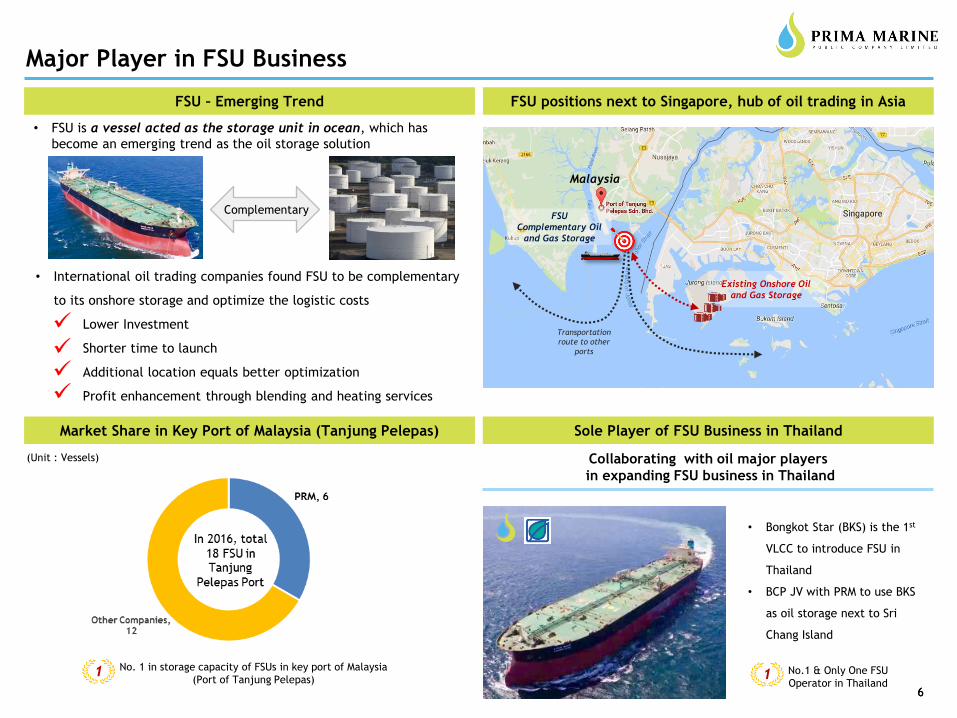

Major Player in FSU Business

6

• International oil trading companies found FSU to be complementary

to its onshore storage and optimize the logistic costs

Lower Investment

Shorter time to launch

Additional location equals better optimization

Profit enhancement through blending and heating services

✓

✓

✓

✓

Complementary

• FSU is a vessel acted as the storage unit in ocean, which has

become an emerging trend as the oil storage solution

FSU

Complementary Oil

and Gas Storage

Existing Onshore Oil

and Gas Storage

Malaysia

Transportation

route to other

ports

FSU – Emerging Trend

Collaborating with oil major players

in expanding FSU business in Thailand

• Bongkot Star (BKS) is the 1st

VLCC to introduce FSU in

Thailand

• BCP JV with PRM to use BKS

as oil storage next to Sri

Chang Island

(Unit : Vessels)

No.1 & Only One FSU

Operator in Thailand

No. 1 in storage capacity of FSUs in key port of Malaysia

(Port of Tanjung Pelepas)1 1

Market Share in Key Port of Malaysia (Tanjung Pelepas)

FSU positions next to Singapore, hub of oil trading in Asia

Sole Player of FSU Business in Thailand

6

Myanmar

Thailand

Laos

Vietnam

Gulf of

Thailand

Malaysia

Offloading

Accommodation

• FSO vessels anchor near the rigs to support oil

and gas exploration as offshore oil offloading unit

• Provide accommodation, foods and drinks, basic

medical treatment, as well as recreation activities

for engineers and staffs working on oil rig

No. of vessels

Ow

n F

leet

Total 2 192,923 DWT

1 96,168 DWT

JV

Fle

et

196,755 DWT

Total DWT

FSO

Offshore Fleet Composition

Aframax

Aframax

No. of vessels Total capacity

Accommodation Work Barge (AWB)

Ow

n F

leet

1300 Passengers

PRM’s FSO fleet offers essential supporting services to oil exploration and

production including:

(As of 30 June 2017)

Sriracha Eagle

Southern Pearl

Navathanee

Offshore Business Fleet Location Essential services for oil exploration and production activities

No. 1 in number of FSO among Thai service provider in Gulf of Thailand1

Major Player in Offshore Business

7

Crew ManagementTechnical Management

PRM Group provides “Technical Management” and “Crew Management” service for oil & petrochemical tanker, FSU, FSO, AWB, and crew

boat. PRM’s Ship Management service ensures that every vessel under management follows rules and standards applied, and supervises

operating activities including:

• Crew recruitment

• Crew salary and other benefits

• Crew training

• Crew Performance assessment

Oil Tank

• Ship cargo operation

• Strictly carry PMS/drydock per

approved plan

• Prepare vessels for ship

inspection and survey

• Prepare documents and licenses

related to vessel operation

• Follow International Safety

Management Standard

Ship Management Service Activities

MARPOL

MLC

STCW

SOLASSIRE

Port State Control

Technical Management1 Crew Management2

Premium Ship Management Services

88

Management for Safety3

• Operating to comply with international rules and regulations

Revenue 1/

Vessel/

Service

As crucial support function

to other core business

Services provided include:

• technical management,

• crew management,

• safety management,

• regulations and

compliance

Small Vessel

Large Vessel

FSUFloating Storage and

Offloading Unit (“FSO”)

Accommodation

Work Barge (“AWB”)

Oil & Petrochemical

Tanker BusinessOffshore Business

Floating Storage Unit

Business (“FSU”)

Ship Management

Business

Remark: 1/ As of 3Q2017 with total revenue of THB 3,421.28 MM2/ Data as at 30 September 20173/ International vessel class (Aframax) for the vessel size of 80,000-120,000 DWT4/ Very Large Crude Carrier (“VLCC”) : International vessel class for the vessel size of 160,000-320,000 DWT

37.46% 44.42% 11.26% 6.87%

1 2 3 4

9

SizeSmall

VesselsAframax 3/ VLCC 4/ Aframax AWB

Number of

Vessels13 2 7 2 1

Capacity (DWT)

47,333 214,464 2,102,920 192,923 300 Passengers

Total 2/ 250,084 2,102,920 192,923 300 Passengers

Business Segments

Ship to Ship Transfer

Operation

II. Performance by Business Segment

1010

11

Performance : Trading Business

PRM Trading Trading Performance

13,500

15,500

27,750

3,039 -

10,000

20,000

30,000

40,000

50,000

2015 2016 Q1 '17 Q2 '17 Jul '17 Aug '17 Sep '17 Oct '17

USD

/Day

Time Charter Market

MR Aframax VLCC AHTS

Q2/17 Q3/17 Q3/16 YTD17 YTD16

<20,000 DWTNo of vessels 12 13 11 13 11

Capacity (DWT) 44,333 47,333 32,334 47,333 32,334

Utilization (%) 86% 85% 85% 88% 89%

>20,000 DWT No of Vessels 2 2 2 2 1

Capacity (DWT) 214,464 214,464 214,464 214,464 214,464

Utilization (%) 75% 72% 87% 79% 93%

Trading Business:

• A new small vessel (3,000 DWT) was added in Q3/2017 for hired by PTT

• All small vessels services were based on term contracts with a minimum volume of 80% of capacity commitment.

• Current PRM’s market share of each customer (<20,000 DWT):

• 67% of PTT marine vol.• 25% of Chevron marine vol.• 19% of Shell marine vol.• 25% of Esso marine vol.

12

Performance : Trading Business

Revenue

Gross Profit

Unit: Million Baht

Unit: Million Baht

Trading Performance

Trading Business:

• The new vessel added in Q3 was attributable to the higher revenue for this group

• GP of two large vessels (100,000 DWT each) was suffered from very low spot rate in Q3/2017

• Financial performance of the two vessels is expected to improve significantly as they were time chartered to BCP 6 months and UNIPEC (from China) 1 year in November 2017

596.7574.3

535.3

2Q2017 3Q2017 3Q2016

34.5

7.4

71.3

2Q2017 3Q2017 3Q2016

1,724.41,381.2

YTD2017 YTD2016

88.1

228.1

YTD2017 YTD2016

13

Performance : FSU

FSU Business:

• One additional VLCC (300,000 DWT) was on hired to BCP started in Mid-June 2017 brought total FSU to 7 with total capacity of 2,102,920 DWT

• Total utilization of FSU in Q3/17 was about 89% which is the same of Q2/17

• Low GP from Q3/17 was due to lower utilization of the 2 vessels while their fixed running cost was remained

• The company is under discussion with a new customer to take this excess capacity shortly

1,032.9 1,002.3888.2

2Q2017 3Q2017 3Q2016

Unit: Million Baht

Revenue

Gross Profit

219.2 206.8288.5

2Q2017 3Q2017 3Q2016

3,140.7

2,724.2

YTD2017 YTD2016

706.5899.2

YTD2017 YTD2016

FSU Performance

Unit: Million Baht

14

Performance : Offshore Business

Unit: Million Baht

Revenue

Gross Profit

Offshore Business Performance

Unit: Million Baht

153.5107.9

150.7

2Q2017 3Q2017 3Q2016

38.1

9.7

37.1

2Q2017 3Q2017 3Q2016

385.2

424.2

YTD2017 YTD2016

65.5

85.5

YTD2017 YTD2016

Offshore Business:

• Offshore business consisted of 2 floating storage and offloading (FSO) vessels and 1 Accommodation Work Barge (AWB)

• Utilization of the two FSO vessels remains constant in Q3/17 as they were charter out to Coastal Energy Corporation (CEC) until 2020

• The contract of AWB with PTTEP was expired since mid July 2017. The customer is expected to rehire the vessel early next year.

• Currently the AWB vessel was laid-up at Sattahip which will reduce the running cost from 1.5 MTHB to 0.2 MTHB per month.

• Requirement for AWB is expected to measure significantly following the upcoming new E&P licensing and Bongkot & Erawan is effective which will increase activities for new exploration and production as well as decommissioning of the unused offshore rigs.

15

Performance : Ship Management

Ship Management Business:

• Increase in Ship management revenue derived from serviced product to new third party’s one FSU in Singapore at one container vessel in Thailand

• Total number of vessels under management included

Own vessels: • AWB 1 • FSO 2• Small Tanker 15• Large Tanker 2• FSU 7

TOTAL 26

Third Party vessels: • Container 1 • FSU 1

TOTAL 2

• Ship management contract for another third party container vessels was signed for commencement in Q4/17

Unit: Million Baht

Revenue

Gross Profit

Ship Management Performance

Unit: Million Baht

87.9130.9

85.4

2Q2017 3Q2017 3Q2016

22.4

36.9

9.8

2Q2017 3Q2017 3Q2016

299.2

277.6

YTD2017 YTD2016

71.0

36.2

YTD2017 YTD2016

III. Consolidated Financial Performance

1616

Consolidated Revenue

17

Unit: Million Baht

QOQ & YTD Revenue

YTD2017 YTD2016

7%

30%

56%

7%

10%

23%

60%

7%

439.1 438.5 393.6

528.0 485.7 473.1

153.5 107.9 150.7

27.9 117.0 61.4

2Q2017 3Q2017 3Q2016

1,149 1,079

Revenue by Price Structure

Revenue & Revenue Structure:

▪ Consolidated revenue for Q3/17 increased in all business except for offshore which was to temporary withhold of new exploration during monsoon season.

▪ Only revenue from large trading vessels (Aframax at 100,000 DWT was linked in international freight rate which is subject to high volatility.

▪ The price risk has been mitigated as the two vessels were time charter at fixed price starting November 2017.

PRM Performance

1,148

1.281.4 1,067.9

1,519.11,470.6

385.2424.2

234.9213.6

YTD2017 YTD2016

3,1773,420

20.52 3.15 (18.42)

227.89 183.43

315.19

39.05

13.04

31.08 23.80

62.14

79.02

2Q2017 3Q2017 3Q2016

Trading FSU

Offshore Ship Management

50.3 90.9

639.9

878.9

70.2

80.6

171.5

198.7

YTD2017 YTD2016

Consolidated Gross Profit

18

Unit: Million Baht

Gross Profit by Business Segment

Gross Profit:

▪ Decline in gross profit for Q3/17 as against Q3/16 and YTD/17 as against YTD/16 was due to lower utilization of vessels following to increase in number of vessels during the year which their fixed cost of services were not proportioned according to their utilization.

▪ Depreciation for the vessels was also increased as a result of downward adjustment of scrap value of the vessels using scrap price as at December 31, 2016 which lower than December 31, 2015.

▪ The scrap value is expected to increase in 2017 and the depreciation will be adjusted accordingly.

Gross Profit

Country Tanker Prices as of

November 2017

Tanker Prices as of

Year Ended 2016

Pakistan USD 405/LT USD 310/LT

India USD 395/LT USD 300/LT

Bangladesh USD 390/LT USD 320/LT

PRM Performance

311

262

407

932

1,249

5%

69%

8%

18%

Trading FSU Offshore Ship Management

YTD2017

1%

70%

5%

24%

3Q2017

204.8 189.6

85.4 61.9 4.7

39.5

653.7

1,003.5

YTD2017 YTD2016

931.9

1,249.0

16.7

45.4

YTD2017 YTD2016YTD2017 YTD2016

Consolidated Net Profit

19

Unit: Million Baht

QOQ Net Profit

Net Profit for Q3/17 dropped compared to Q2/17 by 25.6 MTHB or a decrease of 13%

▪ Selling and admin expense for Q3/17 increased from Q3/16 by 17 MTHB. to 82 MTHB. which corresponded to higher revenue.

▪ Financing cost for Q3/16 increased by 11 MTHB. following higher borrowing to finance new vessels.

▪ FX gain for Q3/17 was 30.4 MTHB, higher than Q3/16 by 12.5 MTHB.

▪ As the result, net profit of Q3/17 declined by 145 MTHB. or a decrease of 35% compared to 3Q/16; net profit for YTD/17 was lower than YTD/16 by 350 MTHB. or 35%

YTD Net Profit

PRM Performance

Unit: Million Baht

50.0 51.030.0 31.421.8

10.5

164.7

323.0

3Q2016

261.8

406.9

4.7

9.0

3Q2017 3Q20163Q2017

Total Assets, Liabilities, Equity and D/E ratio

20

ASSET▪ Current assets increased by 2,979 Million Baht

mainly from the increase in-cash and cash at bankgenerated from IPO

▪ Non-current assets decreased by 195 Million Bahtfrom accumulated depreciation.

LIABILITY▪ Current liabilities decreased by 402 Million Baht

from the repayment of O/D and short-term loans.▪ Non-current liabilities decreased by 336.61

Million Baht derived from repayments of long-term loans from financial institution.

SHAREHOLDER’S EQUITY▪ Shareholder’s equity increased by 3,523 Million

Baht from IPO and increased in net profit affectby dividend payouts.

D/E RATIO▪ D/E ratio decreased to 0.8x after listed in SET; and

targeted D/E ratio as of 1.5x

Statement of Financial Position Updated

Note: YTD Data as at 30 Sep 2017

Unit: Million Baht

3,795

816

7,372

7,567

30-Sep-17 YTD2016

Current Asset

Non Current Asset

1,729 2,131

3,256 3,592

6,182

2,660

30-Sep-17 YTD2016

Current Liabilities

Non Current Liabilities

Shareholders' Equity

11,167

8,383

Year Ended 2016As at 30 Sep 2017

IV. Business Outlook & Investment Plan

2121

Business Expansion Plan

Oil & Petrochemical Tanker Business1

▪ Key drivers for the oil & petrochemical tanker business are

o Domestic oil product demand which will be continuously supported by demand growth

o Penetration of EV technology which is expected to be moderate

o Transportation of oil product to Southern part of Thailand by tankers which is the most

efficient and economical

o Improvement of tanker quality and average age which will be instrumental to achieve

higher volume as customers place more emphasize on safety environmental protection

FSU Business2

▪ The FSU business will continuously be supported by

o Limited onshore land available to build tank farm for physical trading in Singapore

o Fuel’s specification change

o Increase in global oil demand and supply

Offshore Business3

▪ The offshore business will be supported by

o Stable crude oil price

o Thai government regulation on Thai flag vessel (Cabotage Law) will enhance PRM’s

opportunity in offshore business

o Petroleum Concession Act expected to become effective

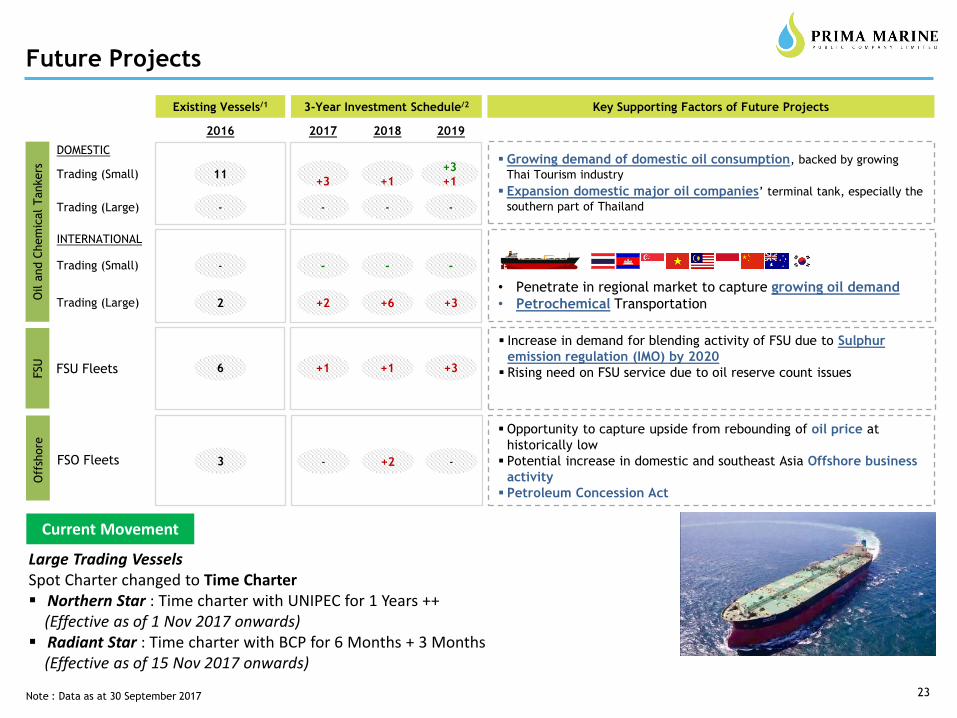

22

23

Existing Vessels/1 3-Year Investment Schedule/2 Key Supporting Factors of Future Projects

▪ Growing demand of domestic oil consumption, backed by growing

Thai Tourism industry

▪ Expansion domestic major oil companies’ terminal tank, especially the

southern part of Thailand

FSO Fleets

• Penetrate in regional market to capture growing oil demand

• Petrochemical Transportation

11

2016

-

-

2

2017 2018 2019

+3 +1

+3

+1

- - -

- - -

+2 +6 +3

- +2 -

▪ Increase in demand for blending activity of FSU due to Sulphur

emission regulation (IMO) by 2020

▪ Rising need on FSU service due to oil reserve count issues

▪ Opportunity to capture upside from rebounding of oil price at

historically low

▪ Potential increase in domestic and southeast Asia Offshore business

activity

▪ Petroleum Concession Act

Note : Data as at 30 September 2017

Trading (Small)

Trading (Large)

Oil a

nd C

hem

ical

Tankers

Trading (Small)

Trading (Large)

DOMESTIC

INTERNATIONAL

FSU FleetsFSU

Off

shore

6 +1 +1 +3

3

Future Projects

Large Trading VesselsSpot Charter changed to Time Charter▪ Northern Star : Time charter with UNIPEC for 1 Years ++(Effective as of 1 Nov 2017 onwards)

▪ Radiant Star : Time charter with BCP for 6 Months + 3 Months(Effective as of 15 Nov 2017 onwards)

Current Movement

24

Q&A

THANK YOU