PRESENTED BY Epoch’s Quarterly Capital Markets€™s Quarterly Capital Markets Outlook January...

32

David N. Pearl Executive Vice President and Co-CIO William W. Priest Chief Executive Officer and Co-CIO PRESENTED BY The information contained in this presentation is distributed for informational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. The information contained in this presentation is accurate as of the date submitted, but is subject to change. Any performance information referenced in this presentation represents past performance and is not indicative of future returns. Any projections, targets, or estimates in this presentation are forward looking statements and are based on Epoch’s research, analysis, and assumptions made by Epoch. There can be no assurances that such projections, targets, or estimates will occur and the actual results may be materially different. Other events which were not taken into account in formulating such projections, targets, or estimates may occur and may significantly affect the returns or performance of any accounts and/or funds managed by Epoch. To the extent this presentation contains information about specific companies or securities including whether they are profitable or not, they are being provided as a means of illustrating our investment thesis. Past references to specific companies or securities are not a complete list of securities selected for clients and not all securities selected for clients in the past year were profitable. Epoch’s Quarterly Capital Markets Outlook January 14, 2015 | The webinar replay will be available on our website: www.eipny.com John Reddan Senior Research Analyst

Transcript of PRESENTED BY Epoch’s Quarterly Capital Markets€™s Quarterly Capital Markets Outlook January...

David N. Pearl

Executive Vice President and Co-CIO

William W. Priest

Chief Executive Officer and Co-CIO

PRESENTED BY

The information contained in this presentation is distributed for informational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy orinvestment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. The information contained in this presentation is accurate as of the datesubmitted, but is subject to change. Any performance information referenced in this presentation represents past performance and is not indicative of future returns. Any projections, targets, orestimates in this presentation are forward looking statements and are based on Epoch’s research, analysis, and assumptions made by Epoch. There can be no assurances that such projections,targets, or estimates will occur and the actual results may be materially different. Other events which were not taken into account in formulating such projections, targets, or estimates may occur andmay significantly affect the returns or performance of any accounts and/or funds managed by Epoch. To the extent this presentation contains information about specific companies or securitiesincluding whether they are profitable or not, they are being provided as a means of illustrating our investment thesis. Past references to specific companies or securities are not a complete list ofsecurities selected for clients and not all securities selected for clients in the past year were profitable.

Epoch’s Quarterly Capital Markets Outlook

January 14, 2015 | The webinar replay will be available on our website: www.eipny.com

JohnReddan

Senior Research Analyst

2

Global Monetary Policy Has Driven Markets

12.3% 17.4%

31.1%6.3%

56.7%

76.3%

Total Return72.6%

Total Return54.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

S&P 500 MSCI World

Cumulative Effects 2012 - 2014

P/E Expansion

EPS Growth

Dividends

Numbers may not total due to roundingSource: Standard and Poors; MSCI; Epoch Investment Partners; December 2014

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

1.0

1.5

2.0

2.5

3.0

3.5

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

%

U.S. 10-year Government Bond Yield

Source: Federal Reserve Economic Data; January 13, 2015

Yields Declined In the U.S. . . .

3

10-Year Treasury Constant Maturity Rate

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

. . . And Throughout The World

Global 10-Year Bond Yields

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15

France Switzerland Germany Japan U.S. Spain Italy

Source: Strategas; January 9, 2015

%

Japan 0.28%

Germany 0.49%

France 0.78%

Spain 1.72%

Italy 1.88%

U.S. 1.94%

Switzerland 0.22%

4

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fed ECB BoJ BOE

Central Bank Policies Are Diverging

Central bank balance sheets

Source: Pavilion Global Markets; Indexed to 100 January 1, 2007; January 2015

Index Expectation

5

If you wish to ask a question, please click on the question mark icon located on the top of the screen. 6

95

100

105

110

115

120

7/1/2014 7/31/2014 8/30/2014 9/29/2014 10/29/2014 11/28/2014 12/28/2014

Euro/USD Yen/USD GBP/USD AUD/USD CAD/USD%

Source: Federal Reserve, Epoch Investment Partners; Indexed to 100 July 1, 2014; January 2015

Dollar Strengthened Against Major Currencies

Exchange Rates In USD Terms

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

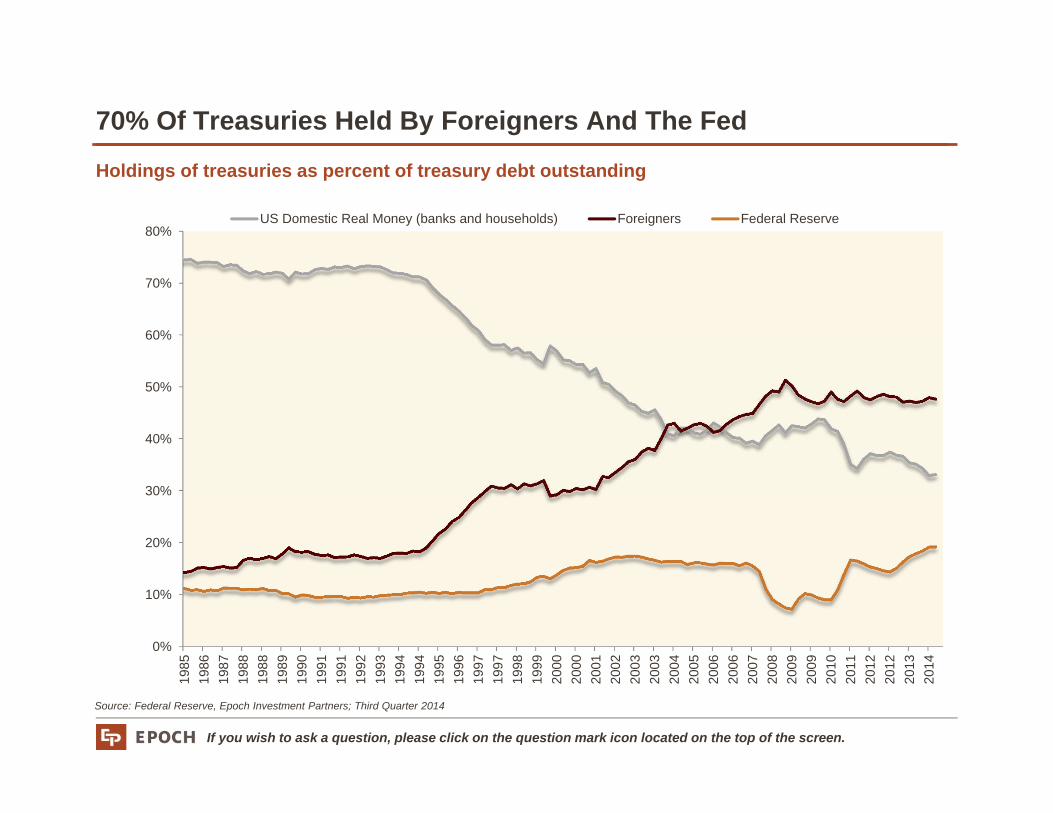

70% Of Treasuries Held By Foreigners And The Fed

0%

10%

20%

30%

40%

50%

60%

70%

80%

1985

1986

1987

1988

1988

1989

1990

1991

1991

1992

1993

1994

1994

1995

1996

1997

1997

1998

1999

2000

2000

2001

2002

2003

2003

2004

2005

2006

2006

2007

2008

2009

2009

2010

2011

2012

2012

2013

2014

US Domestic Real Money (banks and households) Foreigners Federal Reserve

Source: Federal Reserve, Epoch Investment Partners; Third Quarter 2014

Holdings of treasuries as percent of treasury debt outstanding

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

2011 Est 2012 Est 2013 Est 2014 Est GDP

The Big Problem: Secular Stagnation

World real GDP growth continues to be revised down

Source: IMF World Economic Outlook; October 2014

%

8

If you wish to ask a question, please click on the question mark icon located on the top of the screen. 9

World More Highly Levered Than Before Financial Crisis

Source: Geneva Reports on the World Economy, Deleveraging? What Deleveraging? Authors’ calculation based on OECD, IMF and national accounts data; October 2014

%

160

165

170

175

180

185

190

195

200

205

210

215

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

World Total Debt ex-Financials

174%

World debt ex-financials percent of GDP

213%

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

0.3%

-0.3%-0.4%

-0.9%

2.0%

0.6%

0.3%

1.0%

-0.6%

2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Eurozone Germany France Italy Spain

2Q14 3Q14%

Growth Is Anemic In Most Of Europe

GDP growth quarter-over-quarter

Source: Strategas Research Partners; Third Quarter 2014

10

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

-2

-1

0

1

2

3

4

5

6

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Germany France Eurozone Spain Italy

Deflation A Real Threat

Harmonized index of consumer prices

Source: Pavilion Global Markets (Germany Federal Statistical Office and INSEE data via Bloomberg); December 2014

% Y/Y

11

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Monetary Policy

Fiscal Policy

Structural Reform

Abenomics: Shinzo Abe and the Three Arrows

Massive Quantitative Easing

Increased government spending alongside tax hike

Economic growth and inflation?

No significant actions except recent Cabinet shuffle

12

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Chinese Growth Continues To Weaken

6

7

8

9

10

11

12

5

7

9

11

13

15

17

19

Industrial Production (Left Scale) GDP (Right Scale)% Y/Y

Source: Pavilion Global Markets (NBS Data via Bloomberg); January 2015

Industrial Production and GDP Growth

% Y/Y

-4

-2

0

2

4

6

8

10

2011 2012 2013 2014 2015

Month / Month Year / Year

China Home Prices70 Medium and Large Cities

% Change

Source: Pavilion Global Markets (National Bureau of Statistics of China Data via Datastream); November 2014

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Chinese Investors Moving From Housing To Stock Market

14

1,800

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

0

100

200

300

400

500

600

700

800

900

1000New Accounts (Right Scale) Shanghai Composite (Left Scale)

Source: Pavilion Global Markets; January 2015

New Accounts, Thousands Index

Flow of funds fueling spike in Shanghai market

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

60

70

80

90

100

110

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

U.S. Eurozone Japan U.K.

U.S. Growth Outlook Remains Better Than Rest Of World

Eurozone, U.S., Japan and U.K. industrial production

Source: Pavilion Global Markets, Indexed to 100 in January 2005; December 2014

Index

15

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

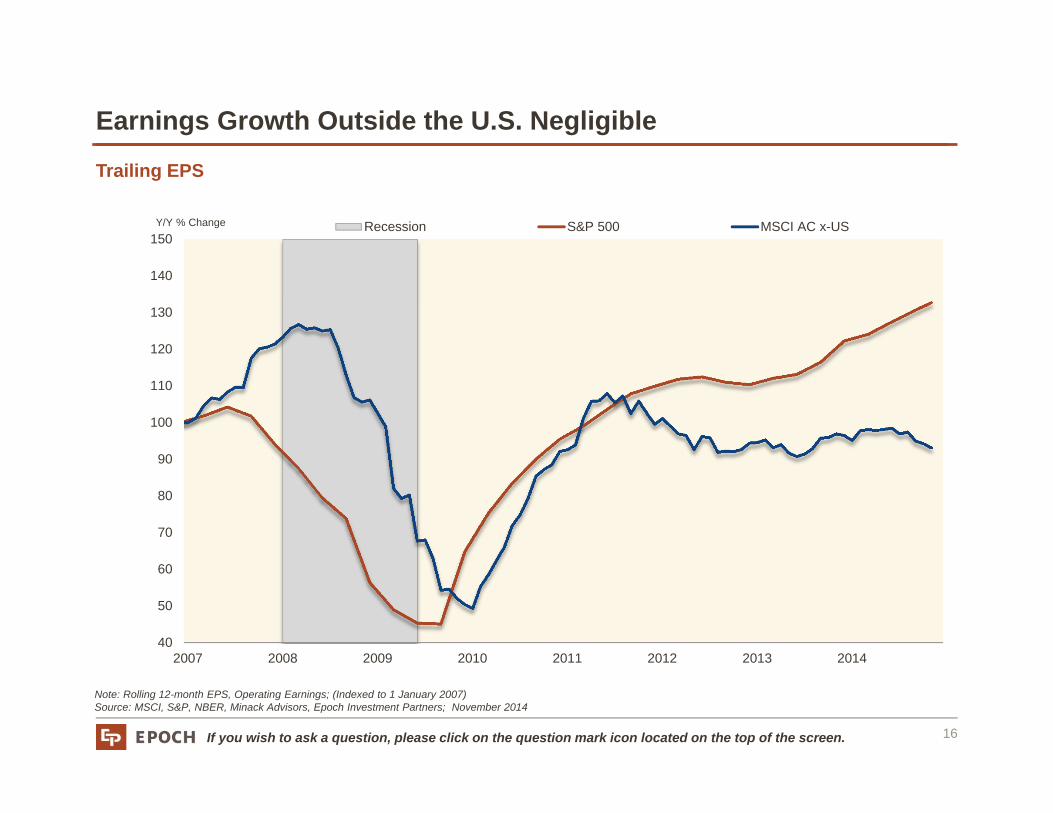

Earnings Growth Outside the U.S. Negligible

40

50

60

70

80

90

100

110

120

130

140

150

2007 2008 2009 2010 2011 2012 2013 2014

Recession S&P 500 MSCI AC x-USY/Y % Change

Trailing EPS

Note: Rolling 12-month EPS, Operating Earnings; (Indexed to 1 January 2007)Source: MSCI, S&P, NBER, Minack Advisors, Epoch Investment Partners; November 2014

16

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

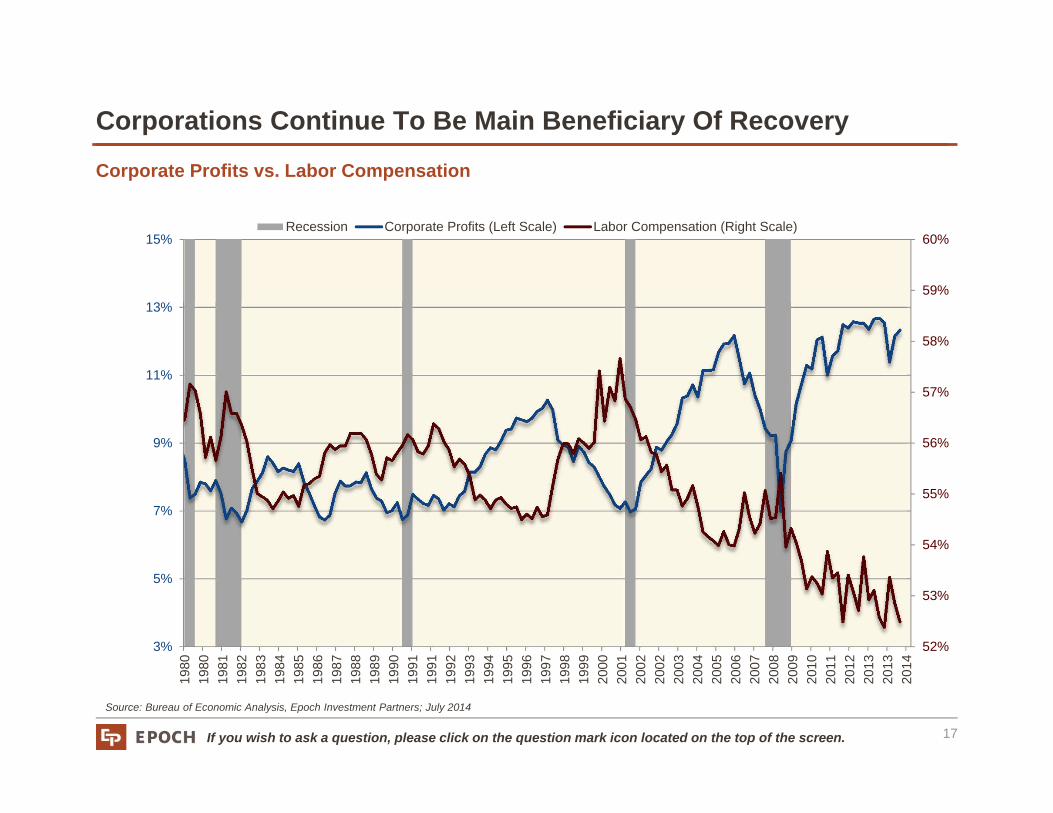

Corporations Continue To Be Main Beneficiary Of Recovery

52%

53%

54%

55%

56%

57%

58%

59%

60%

3%

5%

7%

9%

11%

13%

15%

1980

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2013

2014

Recession Corporate Profits (Left Scale) Labor Compensation (Right Scale)

Source: Bureau of Economic Analysis, Epoch Investment Partners; July 2014

Corporate Profits vs. Labor Compensation

17

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

-1000

-800

-600

-400

-200

0

200

400

105,000

107,000

109,000

111,000

113,000

115,000

117,000

119,000

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

Employment Finally Above Pre-Crisis Levels . . .

Change in employment, all private employees

Source: Bureau of Labor Statistics; December 2014

18

All Employees: Total Private Industries (Left Scale)Change In Total Private Employment (Right Scale)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

. . . But Wage Inflation Has Yet To Materialize

0

1

2

3

4

5

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

1. Production and & Non-Supervisory: Total Private IndustrySource: Federal Reserve Economic Data; December 2014

Average Hourly Earnings1% Change Y/Y

19

Earnings growth elusive

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

50

70

90

110

130

150

170

190

210

230

250S&P/Case-Shiller 20-City Composite Home Price Index

20

Source: Federal Reserve Economic Data; October 2014

Housing Prices Recovering Slowly

Wealth effect slow to rebound

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

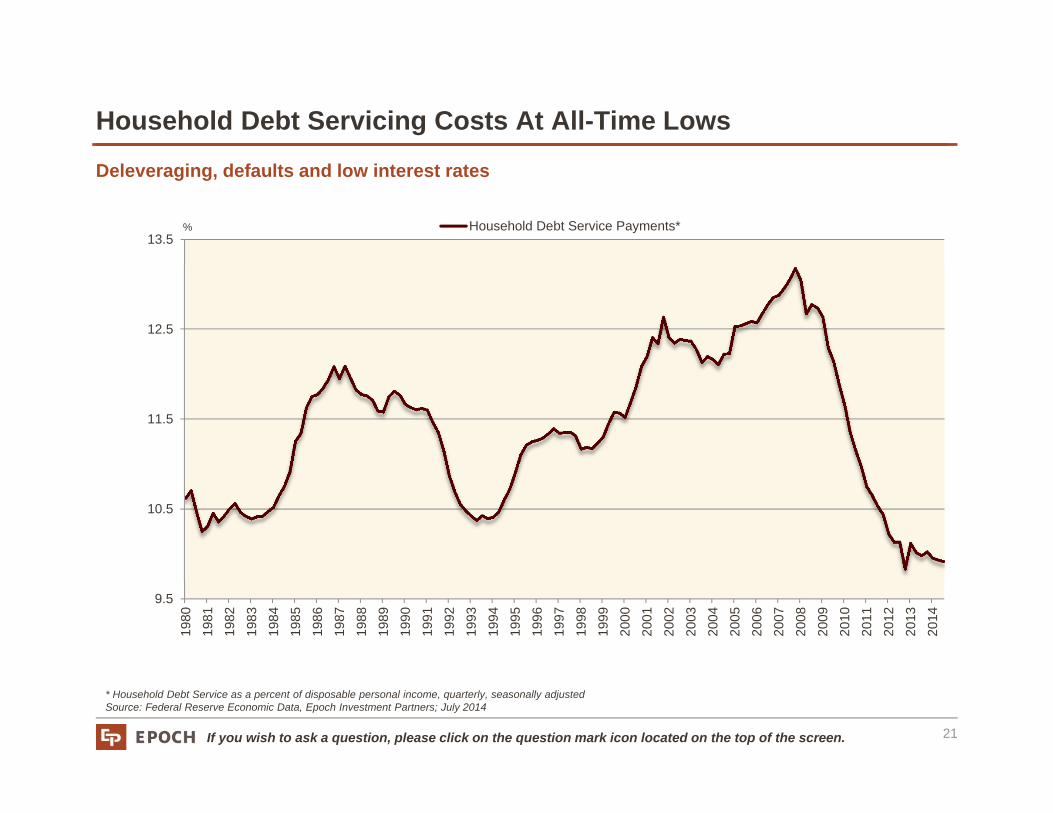

Household Debt Servicing Costs At All-Time Lows

9.5

10.5

11.5

12.5

13.5

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Household Debt Service Payments*

* Household Debt Service as a percent of disposable personal income, quarterly, seasonally adjustedSource: Federal Reserve Economic Data, Epoch Investment Partners; July 2014

%

21

Deleveraging, defaults and low interest rates

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Gasoline Prices Decline With Oil . . .

40

60

80

100

120

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Dec

-09

Feb-

10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb-

11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Gasoline (Right Scale) Oil (Left Scale)

1. US Regular All Formulations Gas Price, Dollars per Gallon, Weekly, Not Seasonally Adjusted2. West Texas IntermediateSource: Federal Reserve Economic Data, Epoch Investment Partners; January 2015

Producing a tailwind for consumers

1 2$/Gallon $/Barrel

22

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

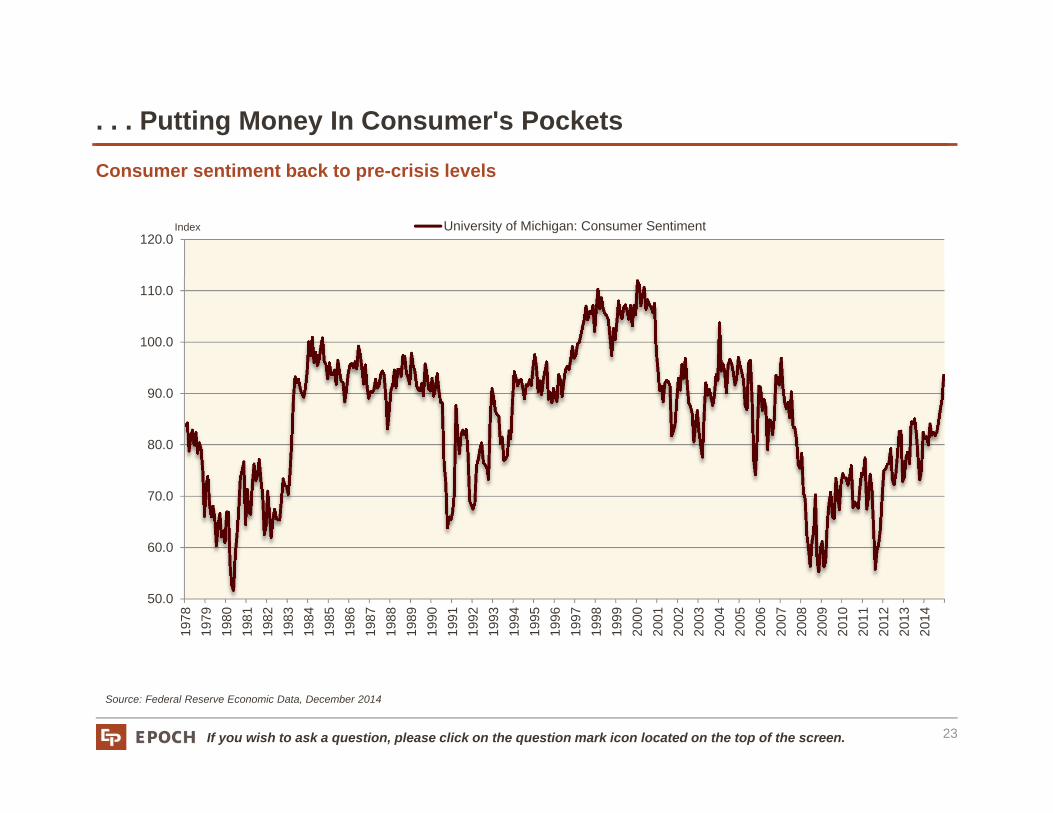

. . . Putting Money In Consumer's Pockets

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

University of Michigan: Consumer Sentiment

Consumer sentiment back to pre-crisis levels

Source: Federal Reserve Economic Data, December 2014

Index

23

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Non-OPEC Supply Growth Is Expected To Outpace Demand Growth

The IEA's forecast for 2014 growth

Source: IEA, Bemstein analysis, 2014

24

1.43

0.170.04 0.02

0.15

-0.08-0.03

1.65

0.07

-0.19-0.26

-0.38

0.220.29

0.15 0.190.1 0.07 0.02

1.04

0.66

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

U.S

.

Can

ada

Rus

sia

Afric

a

Lat.

Am

Asia

OE

CD

ex-

U.S

.

Tota

l Non

-OP

EC

Iraq

Oth

er O

PE

C

Sau

di

Nig

eria

Iran

Liby

a

Tota

l OP

EC

Tota

l Sup

ply

U.S

.

Sur

ope

Oth

er O

EC

D

OEC

D D

eman

d

Chi

na

Asia

Lat.

Am

Mid

dle

Eas

t

Afric

a

FSU

Oth

er O

EC

D

Non

-OEC

D

Tota

l Dem

and

Supply Demand

No IEA Forecasts forOPEC Production

IEA

201

4 O

il Su

pply

& D

eman

d G

row

th (M

bpd)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

0

2

4

6

8

10

12

14

16

20

30

40

50

60

70

80

90

100

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

World Oil Demand (Left Scale) OPEC Excess Production Capacity (Right Scale)

OPEC Spare Capacity Not What It Used To Be

Source: Simmons & Company, 'Oil Macro: Oil Supply & Demand Balances', December 2014

OPEC spare capacity vs. global demand

Dem

and

(mb/

d)

25

Excess Capacity (m

b/d)

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Bond Proxies Trading At Premium To Market

0.0

5.0

10.0

15.0

20.0

25.0

S&P 500 Real Estate Investment Trusts Information Technology Utilities

Source: Standard & Poors, Epoch Investment Partners, January 2015

26

S&P 500 sector forward P/E

Multiple

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

Jump In M&A Activity In Europe And North America

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

North America Western Europe Asia Pacific (Developed)

Volume of announced M&A deals by region

$ Billions

Source: Pavilion Global Markets (Data via Bloomberg), 2Q 2014 at Pro-rata; December 2014

27

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

0

50

100

150

200

250

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Dividends Buybacks

Buybacks And Dividends Continue To Be A Favored Use Of Cash

28

$ Billions

Source: Standard and Poors, Epoch Investment Partners; September 2014

S&P 500 quarterly buybacks and dividends

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

-500

0

500

1,000

1,500

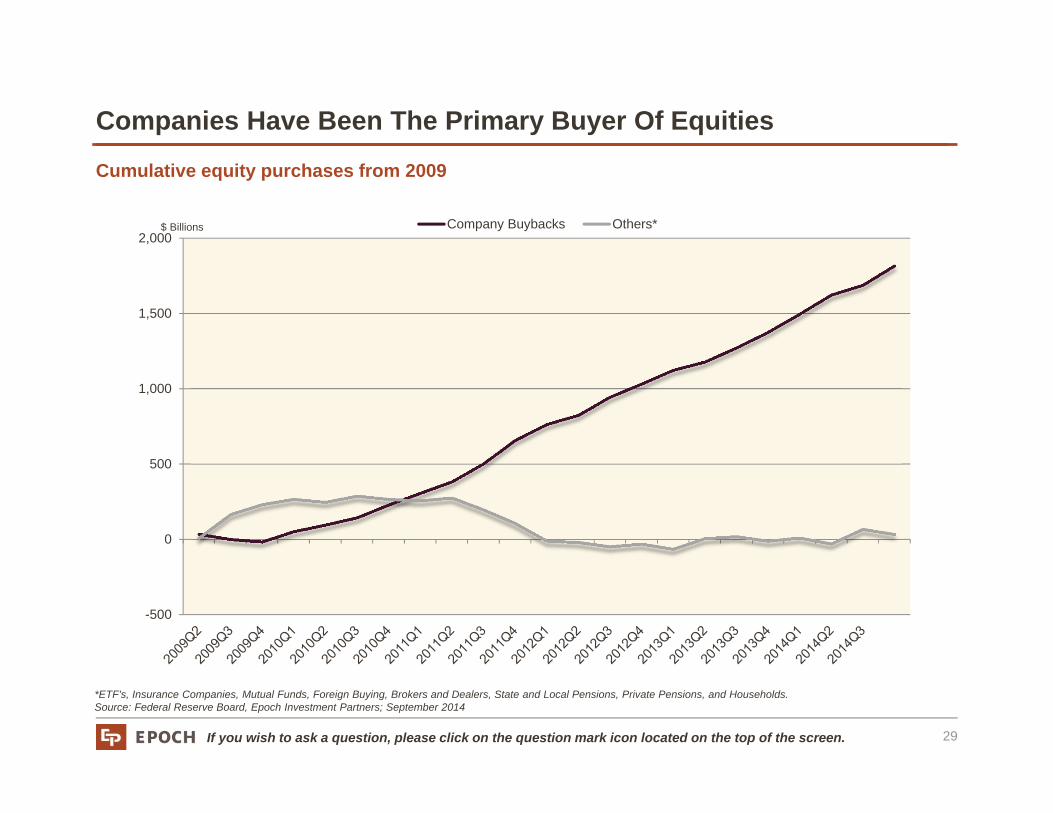

2,000Company Buybacks Others*

*ETF's, Insurance Companies, Mutual Funds, Foreign Buying, Brokers and Dealers, State and Local Pensions, Private Pensions, and Households.Source: Federal Reserve Board, Epoch Investment Partners; September 2014

$ Billions

Companies Have Been The Primary Buyer Of Equities

Cumulative equity purchases from 2009

29

White Paper

30

At Epoch, we invest in companies that are disciplined capital allocators.

We identify companies with track records of investing free cash flow for profitablegrowth AND returning excess free cash flow to investors. If management cannot earn above its cost of capital by investing in internal

projects or acquisitions, it should return the cash to shareholders. If the company decides to return excess free cash flow to investors, we see

dividends, share repurchases and debt paydowns as equivalent ways to achieve that objective.

31

The effects of QE are fading • The end of abnormally low volatility • Valuation expansion phase is over• Future returns will rely on company fundamentals

The world is growing . . . slowly, and unevenly • "Global Champions" will have the flexibility to adapt (specifically in Europe)• Companies will have fewer opportunities for organic growth• Companies generating cash will distribute more to shareholders

Cash dividends Share buybacks Debt reduction

• Above-average growth within select areas, including: The "Internet of things" Aerospace Health care

Implications

If you wish to ask a question, please click on the question mark icon located on the top of the screen.

A replay of this presentation will be available shortly on our website www.eipny.com

Please feel free to contact us at 212-303-7200

Question & Answer Section

32