Presentation Title Here - Nationwide Financial · • Increased staffing of Case Managers dedicated...

28

Life Underwriting March 2015 AGT-0191AO-WG (03/2015)

Transcript of Presentation Title Here - Nationwide Financial · • Increased staffing of Case Managers dedicated...

Life Underwriting

March 2015

AGT-0191AO-WG (03/2015)

• iPipeline • Organizational Update • Field Underwriting Processing Tips • Underwriting Programs • Case Study • Foreign Travel & International Risk • Case Study • Reinsurance • Questions • Summary

Agenda

1 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

What is iPipeline e-Applications?

Best way to complete your fixed life apps

Forms wizard approach

Your guide to a 100% in-good-

order app

FOR INSURANCE PROFESSIONAL USE ONLY – NOT FOR DISTRIBUTION WITH THE PUBLIC

Why use iPipeline? Easier than paper

• NO questions missed • NO missing forms • NO missing signature • NO additional work

Faster than paper • Fewer touchbacks to your client • Screen guides you through what’s

important, what’s not • Cuts underwriting time down by multiple

days

More options than paper • Ability to email forms to client – sign

remotely! • Save your work and return later

Get paid

quicker

Clients covered faster

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

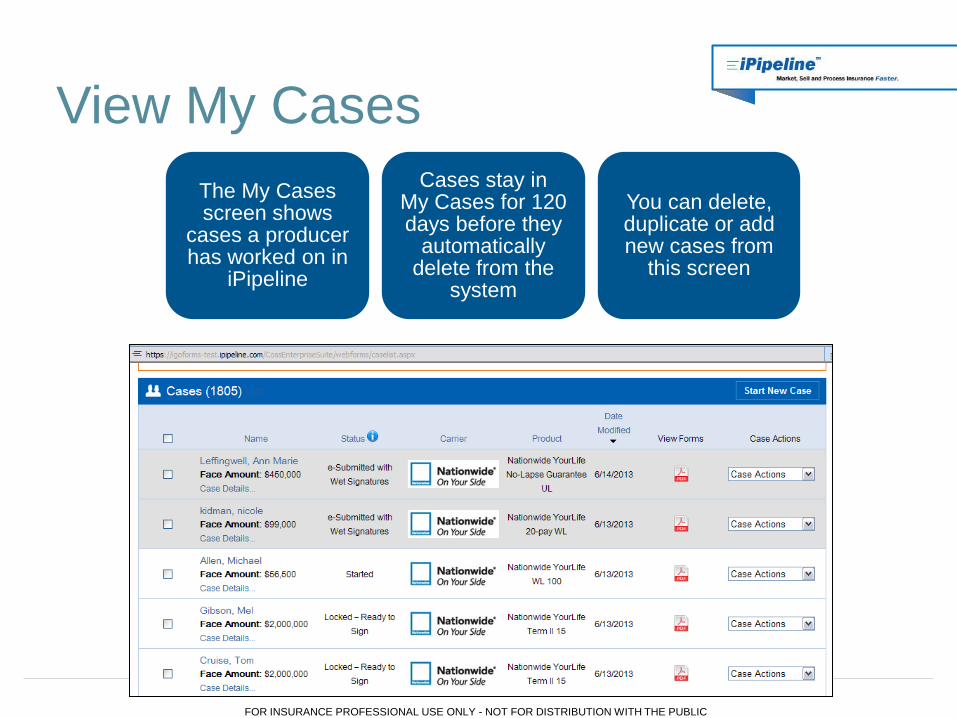

View My Cases

The My Cases screen shows

cases a producer has worked on in

iPipeline

Cases stay in My Cases for 120 days before they

automatically delete from the

system

You can delete, duplicate or add new cases from

this screen

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

e-Application information

Fields highlighted in yellow are required

for application to be in good order

Nav bar lets you know what screens

are (in)complete

Additional questions auto-

generate as necessary

FOR INSURANCE PROFESSIONAL USE ONLY – NOT FOR DISTRIBUTION WITH THE PUBLIC

Sample application pdf

Easy to read

Signatures applied across all

documents

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

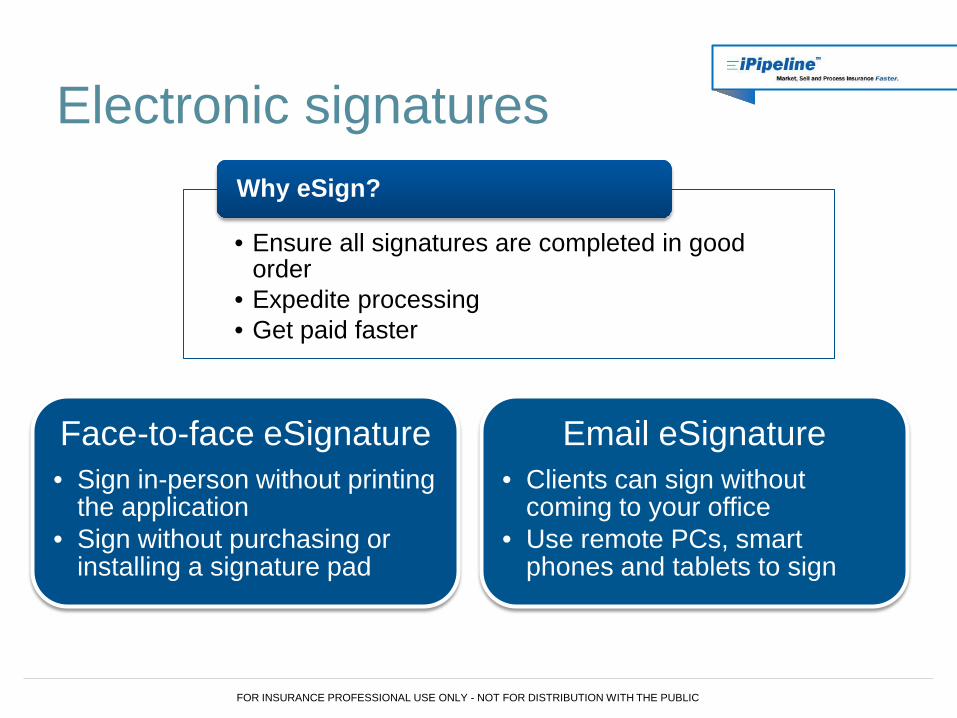

Electronic signatures

• Ensure all signatures are completed in good order

• Expedite processing • Get paid faster

Why eSign?

Face-to-face eSignature • Sign in-person without printing

the application • Sign without purchasing or

installing a signature pad

Email eSignature • Clients can sign without

coming to your office • Use remote PCs, smart

phones and tablets to sign

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Training Available Live Webexs • Schedule available at iPipeline Booth

Automated Demo • Available 24/7 on the Nationwide Site

PDF screen-by-screen guide

Nationwide Call Center • 1-866-678-LIFE

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Organizational Update

Large increase in WFG applications since 2011

9

Year Total WFG Life Insurance Applications Received

YOY Increase %

2011

1,301 2012

7,068 443.30% 2013

11,982 69.50% 2014

16,113 34.50% FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Organizational Update • Increased staffing of Case Managers dedicated to WFG from 0 in 2011 to 27 by 2014. • Added one Underwriting Manager, one Case Manager Supervisor, and one Team Lead • 6 leaders directly supporting WFG New Business

10

0

5

10

15

20

25

30

2011 2012 2013 2014

Case Managers

Case Managers

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Organizational Update • Consistently meet our service level agreements (since November

2014)

• Created a more manageable workload for our associates, so they can focus on the service you deserve!

• Implemented several Continuous Improvement initiatives: • More structured training approach • Improved communication – new welcome/initial

review email • Stronger resource tools for underwriters:

• Less EKGs • Consistent exception handling

11

FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

• Set appropriate expectations. All statistics are from January 2014 to present: – Base Non Tobacco Preferred Plus and Non Tobacco Preferred = 45.9%

– Long Term Care Rider Non Tobacco Preferred = 44.03%

– Base Decline = 13.0%

– LTC Decline = 31.8% – The remaining approximately 54.1% is standard or rated

– I-Pipeline applications - 62.4%

Field Underwriting

12 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

• Use iPipeline – average time service is 3 days faster

• Underwrite – gather medical, avocations, travel, and financial information to ensure underwriter has needed information to make a decision

• Fully complete the application with all medical history, physician contact information, and prescribed medications – this enables us to order medical records if required at the time of application submission

• Include cover letters – does the case make sense?

Field Underwriting

13 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

• Preferred Vendors: –APPS (American Para Professional Systems) –ExamOne –Portamedic

Field Underwriting

14 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

• Understand competition

• Nationwide’s underwriting niches: – Ages 35-65 – Standard and better risks – Build – Cardiac – Barrett’s esophagus – Aviation – Preferred Consideration for some Diabetics

• Communication is critical – before, during, and after

Field Underwriting

15 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

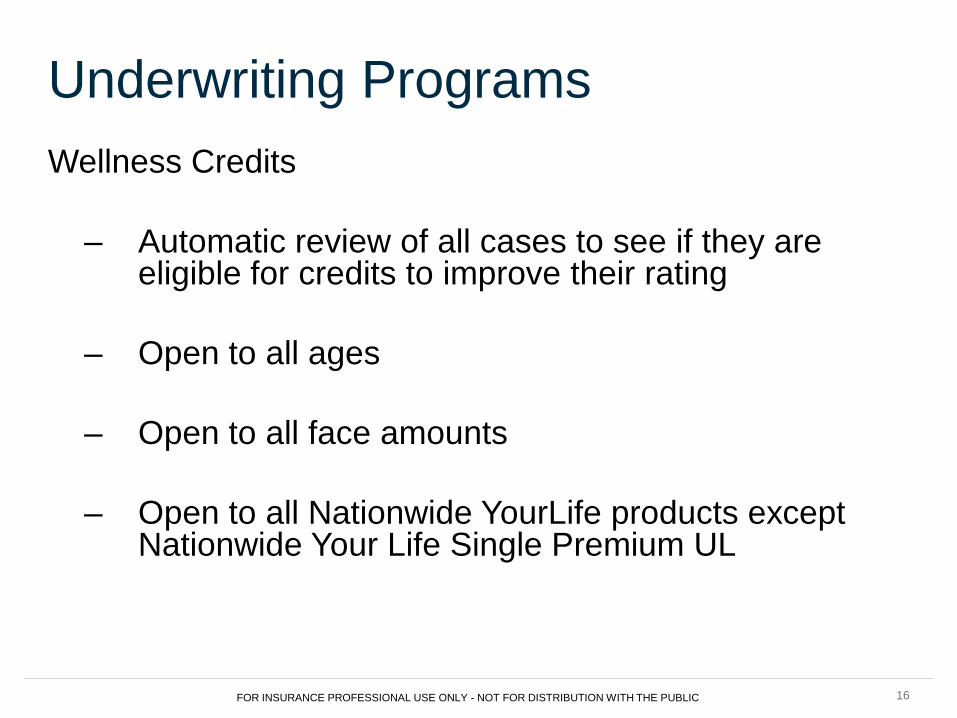

Underwriting Programs Wellness Credits

– Automatic review of all cases to see if they are

eligible for credits to improve their rating

– Open to all ages

– Open to all face amounts

– Open to all Nationwide YourLife products except Nationwide Your Life Single Premium UL

16 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Underwriting Programs Placement Improvement Program (PIP) – Table C to Standard

– Insured’s 15 to 70 – Policies with specified amounts totaling $100,000 and $10 Million – Policy increases where the original policy was issued at Table C or

better – Available on Whole Life series, Accumulation VUL, Protection VUL

and Survivorship VUL Other Opportunities to offer better rating using:

– Preferred Stretch Guidelines – Business Decisions

17 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Case Study • 65 Male applying for $100,000 Indexed UL, $100,000 LTC • Diagnosed w/ Diabetes and Hypertension 2 years ago • Medications: Lisinopril, Metformin • Insurance exam – 5.9.170, BP 115/80, Both parents lived to age 80+ • Insurance Labs – Glucose 95, A1c 6.1, Chol 205, Chol/HDL 3.0 • Medical records – Well controlled Diabetes since diagnosis in March 2013, A1c results

between 6.1-6.5, with last 3 readings below 6.3 • Medical records cont. Hypertension well controlled, 12 month average – 115/78

– What factors make this a favorable case?

• Family history, Consistent A1c control, recent Diabetes diagnosis, and age

– What would be the best case rating? • We would consider preferred on this case due to the favorable factors. Would also

be considered “best case” for Diabetic applying for LTC: Approve LTC Table B.

18 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Include a fully completed Foreign Questionnaire and copy of visa or green card, if not a US citizen and for all foreign national cases and if travel within the next 12 months or previous travel history.

General guidelines for Foreign National’s in A/B countries: • Permanent coverage only • No LTC or supplemental benefits • Ages 18 – 70 • Classification of Table D or less • Applications & exam taken on US soil

Foreign Travel & International Risk

19 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

General guidelines for Foreign National’s in A/B countries:

• Occupation should be technical or professional in nature

• Applicant should have connection to US (property, visiting,

business, etc.)

• A country (autobind up to $10,000,000)

• A country (can consider NTPP)

Foreign Travel & International Risk

20 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Changes effective early September:

– Allow NTPP rates on travel to A and B countries (B countries used to be at best preferred)

– Foreign nationals in B countries can autobind reinsurers up to $5,000,000 ($1,000,000 retention only – no autobind)

– Some B country residents can consider NTP – Brazil, China, Israel, Mexico (previously best case standard).

Foreign Travel & International Risk

21 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Case Study • 29 Female, Applying for $200,000 Indexed UL, $200,000 LTC rider • Application indicates clear history, Mexican citizen, Housekeeping • Income - $25,000, in US x 10 years • Received copy of consular ID – expires 5/17 • No driver’s license, takes public transport • Received foreign questionnaire – no travel plans, Mexican citizen, not fluent in English • Medically qualifies for Non-tobacco preferred plus

o What factors make this a favorable case?

• Employed, US x 10 years, no travel planned, valid consular ID with expiration > 1 year from application date

o How would we handle?

• We would be willing to offer preferred, since the proposed insured is from one of our designated “B” countries (Mexico, China, Brazil) and qualifies for Non-tobacco preferred plus. LTC rider would be declined due to non-green card resident.

22 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Case Study

• 42 Female, applying for $1,500,000 IUL with $500,000 Long term care rider • Application – clear history, last Dr. visit 1/13 – normal checkup, build 5.0.100 • Occupation – Attorney, income $200,000, Net Worth $2,500,000 • Insurance exam – 5.1.97, BP 132/75, history of abdominal pain in 2009 with antibiotic

treatment and normal abdominal and pelvic ultrasounds • Insurance Labs – Cholesterol 156, Chol/HDL ratio 2.32 remaining labs within normal

limits • Medical records – Medical history on exam confirmed by medical records. Last Dr. visit

we have is from January 2013 Weight on that visit was 5.1.98 and was between 94-99 lbs in all visits from 2010 – 2013.

o What are your concerns, if any with this information? o How would you quote this applicant? o Could Long Term Care present a challenge on this case?

23 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Two types of reinsurance: • Automatic – happens behind the scenes • Facultative – we initiate

–Determine we are not interested in the risk –Believe a reinsurer is able to provide a better

decision –We pass the entire premium and risk

Understanding Reinsurance

24 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Reinsurance is not a “bad” word:

• When do we use reinsurance? –Certain impairments – Positive CDT, Hep C

• Why do we use reinsurance? –Mitigate our individual corporate risk –They are “noted” industry experts –Helps with our product pricing, drives down cost of

insurance

Understanding Reinsurance

25 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Questions

26 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

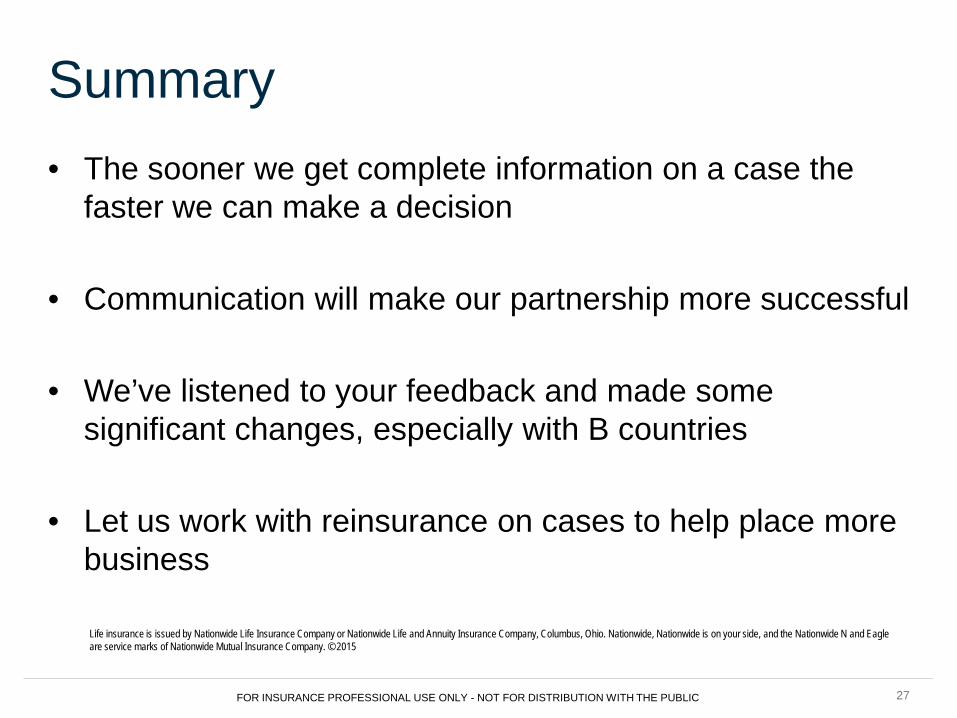

• The sooner we get complete information on a case the faster we can make a decision

• Communication will make our partnership more successful

• We’ve listened to your feedback and made some significant changes, especially with B countries

• Let us work with reinsurance on cases to help place more business

Summary

27 FOR INSURANCE PROFESSIONAL USE ONLY - NOT FOR DISTRIBUTION WITH THE PUBLIC

Life insurance is issued by Nationwide Life Insurance Company or Nationwide Life and Annuity Insurance Company, Columbus, Ohio. Nationwide, Nationwide is on your side, and the Nationwide N and Eagle are service marks of Nationwide Mutual Insurance Company. © 2015