Premier oil results 2014

31

2014 Annual Results Presentation 26 February 2015

-

Upload

company-spotlight -

Category

Investor Relations

-

view

2.661 -

download

1

Transcript of Premier oil results 2014

2014 Annual Results

Presentation26 February 2015

Forward looking statements

This presentation may contain forward-looking statements and information that

both represents management's current expectations or beliefs concerning future

events and are subject to known and unknown risks and uncertainties.

A number of factors could cause actual results, performance or events to differ

materially from those expressed or implied by these forward-looking statements.

February 2015 | P1

Agenda

Introduction

Indonesia

Vietnam

Falkland Islands

Finance

Outlook

Tony Durrant

Roberto Lorato

Phil MacLaurin

Neil Hawkings

Richard Rose

Tony Durrant

February 2015 | P2

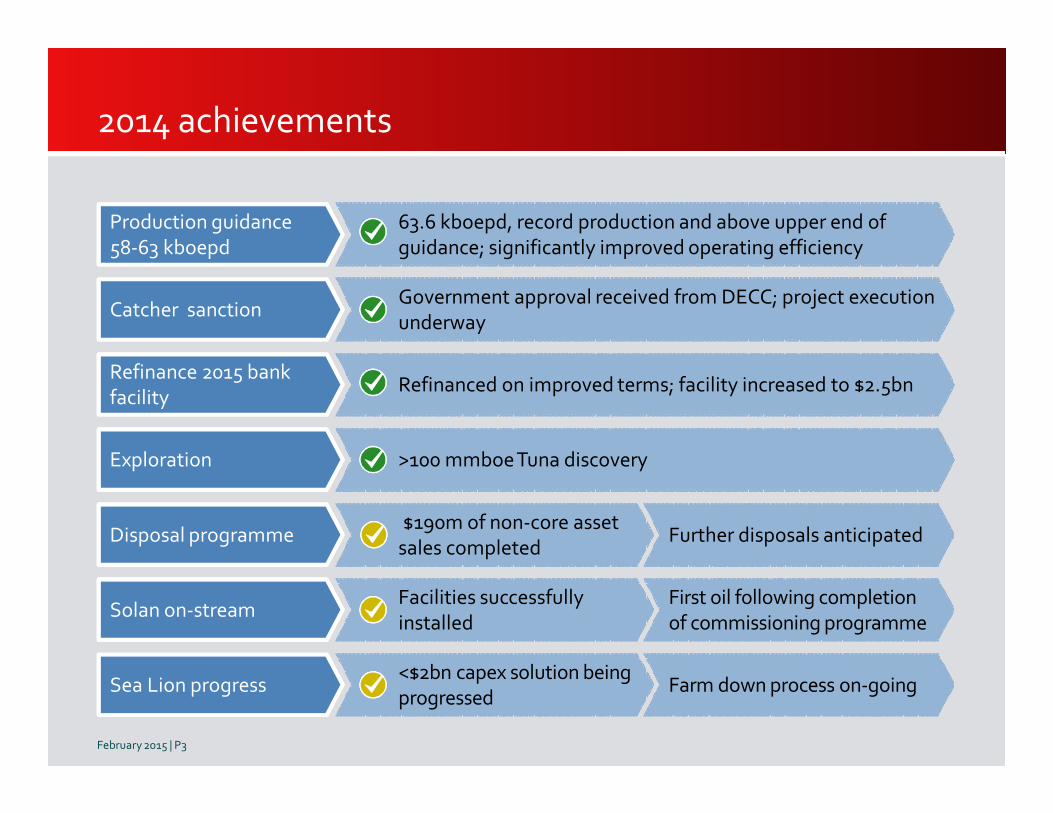

2014 achievements

Government approval received from DECC; project execution underway

Production guidance58-63 kboepd

Catcher sanction

Refinance 2015 bank facility

Exploration

Disposal programme

Solan on-stream

Sea Lion progress

63.6 kboepd, record production and above upper end of guidance; significantly improved operating efficiency

Refinanced on improved terms; facility increased to $2.5bn

>100 mmboeTuna discovery

$190m of non-core asset sales completed

Further disposals anticipated

Facilities successfully installed

First oil following completion of commissioning programme

<$2bn capex solution being progressed

Farm down process on-going

February 2015 | P3

Solan project status

• Tank, jacket and topsides installed September 2014

• Initial drilling phase and subsea work completed October 2014

• Mechanical completion and commissioning adversely affected by weather (December – February)

• Subsea work to tie-in P1 and W1 scheduled for March

• Optimising use of flotel/rig capacity to complete remaining work scope

• Drilling rig contracted for P2 and W2 programme

February 2015 | P4

Targeting

plateau rate of

20-25 kbopd

by year-end

IndonesiaRoberto Lorato

Indonesia Business Unit Manager

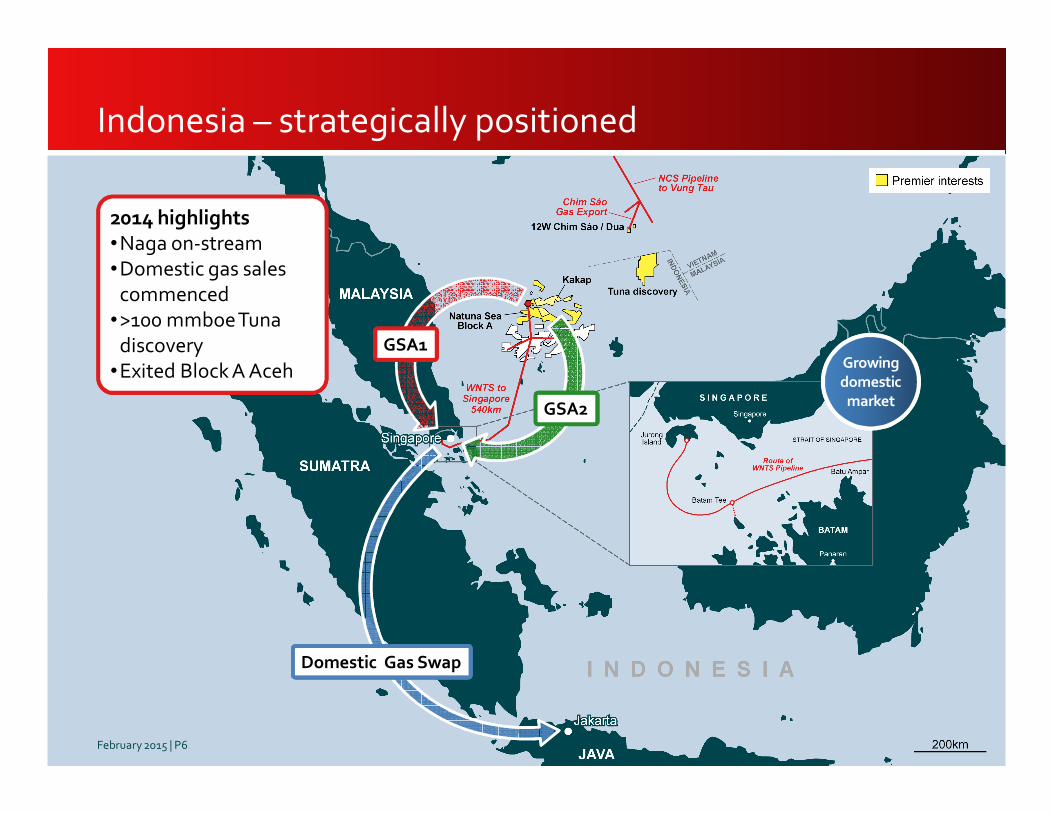

Indonesia – strategically positioned

2014 highlights•Naga on-stream•Domestic gas sales

commenced •>100 mmboeTuna

discovery•Exited Block A Aceh

GSA2

Domestic Gas Swap

GSA1Growing

domestic

market

February 2015 | P6

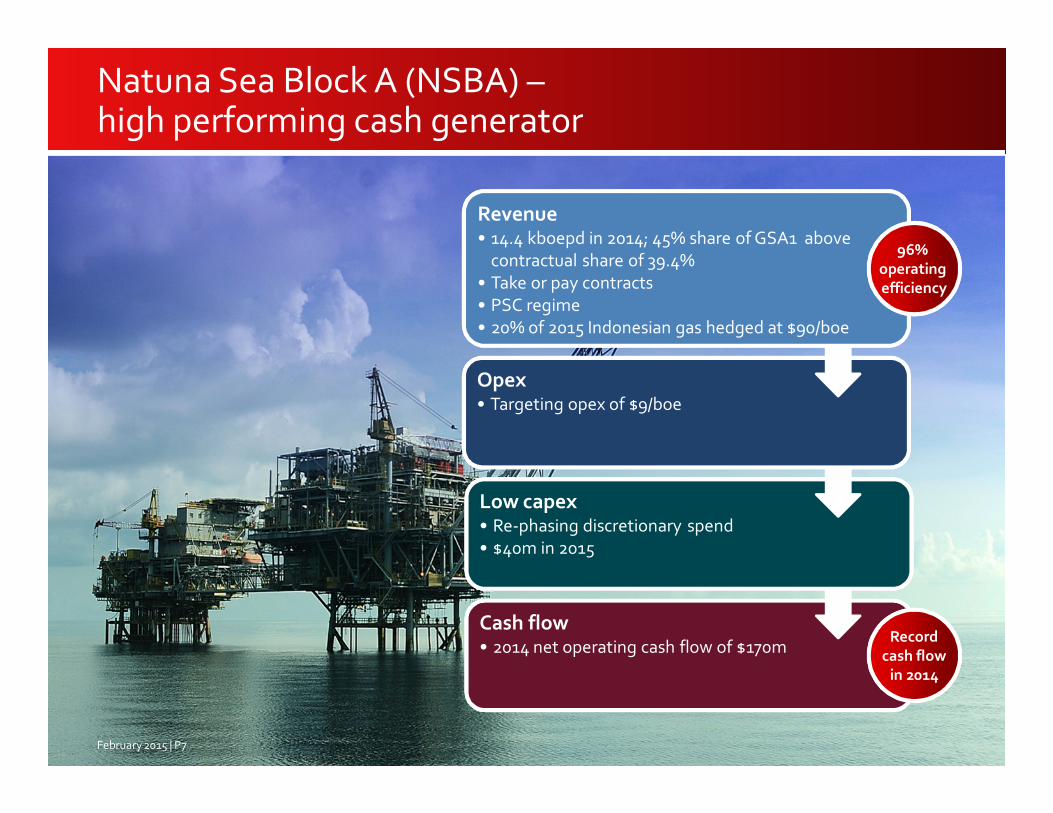

Natuna Sea Block A (NSBA) –high performing cash generator

Opex• Targeting opex of $9/boe

Revenue • 14.4 kboepd in 2014; 45% share of GSA1 above

contractual share of 39.4%

• Take or pay contracts

• PSC regime

• 20% of 2015 Indonesian gas hedged at $90/boe

Cash flow• 2014 net operating cash flow of $170m

Low capex• Re-phasing discretionary spend

• $40m in 2015

96%

operating

efficiency

Record

cash flow

in 2014

February 2015 | P7

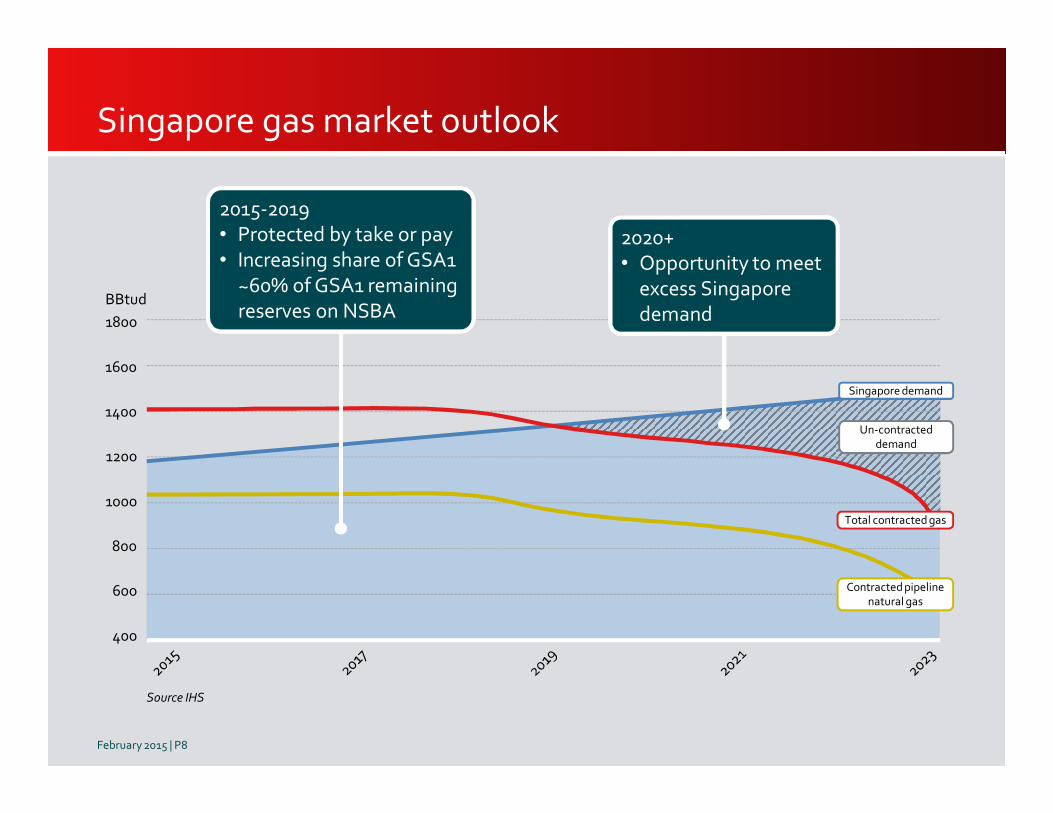

Singapore gas market outlook

1800

1600

1400

1200

1000

800

600

400

Source IHS

BBtud

Singapore demand

Contracted pipelinenatural gas

Total contracted gas

Un-contracteddemand

2015-2019• Protected by take or pay• Increasing share of GSA1

~60% of GSA1 remaining reserves on NSBA

2020+ • Opportunity to meet

excess Singapore demand

February 2015 | P8

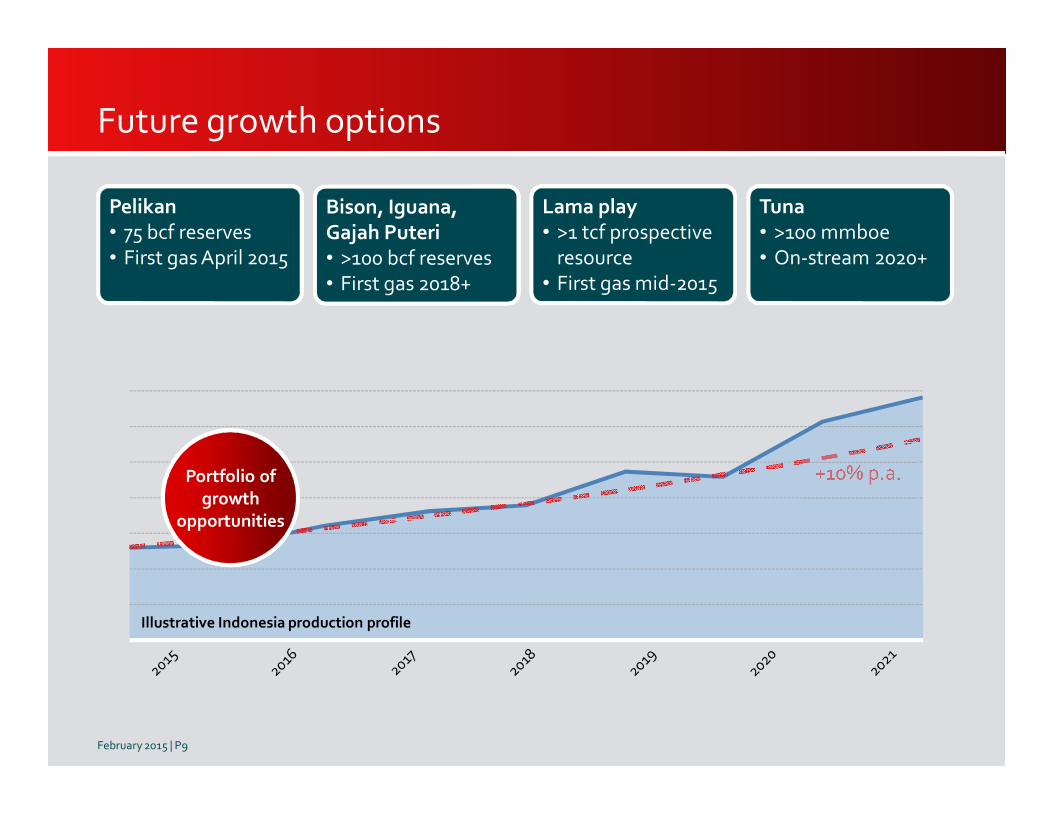

Future growth options

Pelikan• 75 bcf reserves• First gas April 2015

Lama play• >1 tcf prospective

resource• First gas mid-2015

Bison, Iguana, Gajah Puteri• >100 bcf reserves • First gas 2018+

Tuna• >100 mmboe• On-stream 2020+

Illustrative Indonesia production profile

Portfolio of

growth

opportunities

February 2015 | P9

VietnamPhil MacLaurin

Vietnam Business Unit Manager

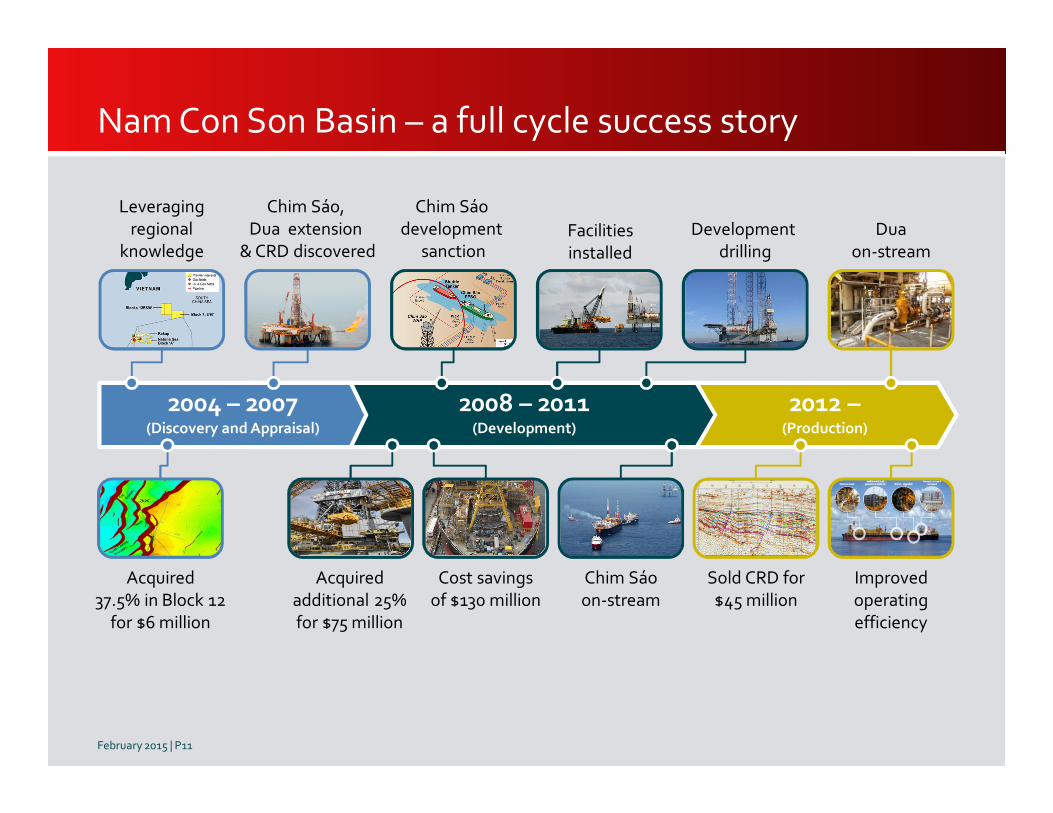

2004 – 2007(Discovery and Appraisal)

2008 – 2011(Development)

Leveraging

regional

knowledge

Chim Sáo,

Dua extension

& CRD discovered

Acquired

additional 25%

for $75 million

Facilities

installed

Cost savings

of $130 million

Chim Sáo

development

sanctionDevelopment

drilling

Improved

operating

efficiency

Dua

on-stream

2012 –(Production)

Acquired

37.5% in Block 12

for $6 million

Chim Sáo

on-stream

Sold CRD for

$45 million

Nam Con Son Basin – a full cycle success story

February 2015 | P11

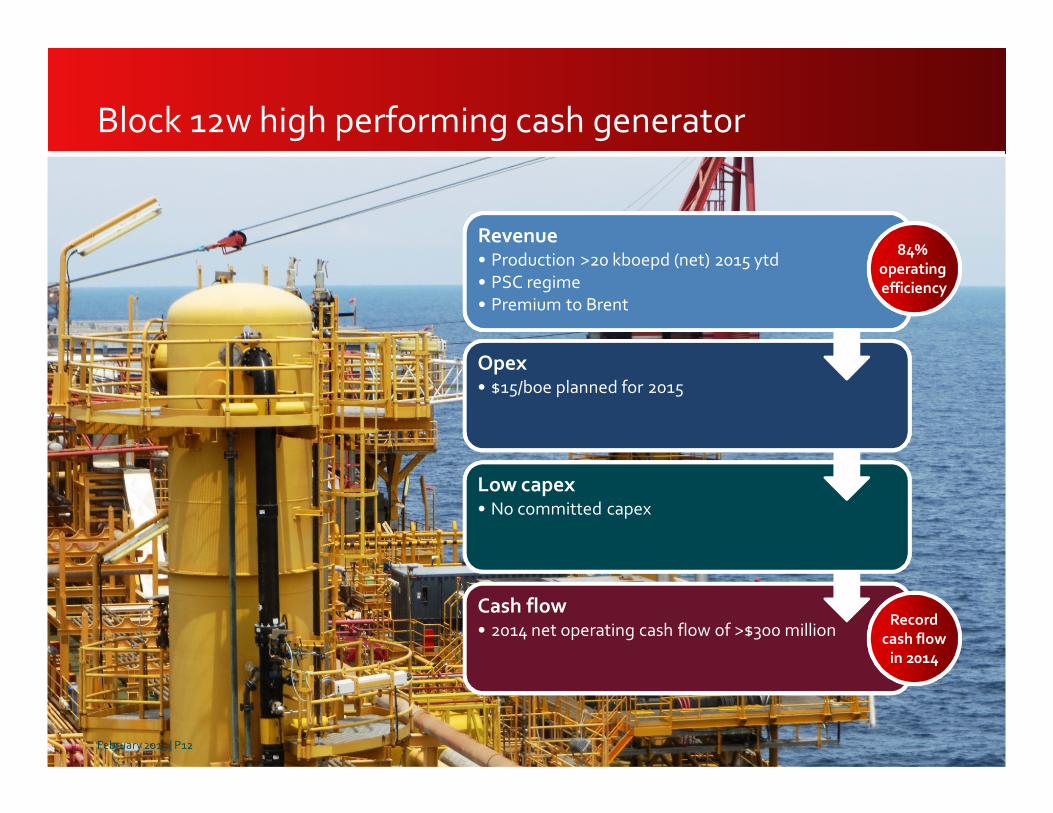

Block 12w high performing cash generator

Cash flow• 2014 net operating cash flow of >$300 million

Low capex• No committed capex

Opex• $15/boe planned for 2015

Revenue• Production >20 kboepd (net) 2015 ytd

• PSC regime

• Premium to Brent

84%

operating

efficiency

Record

cash flow

in 2014

February 2015 | P12

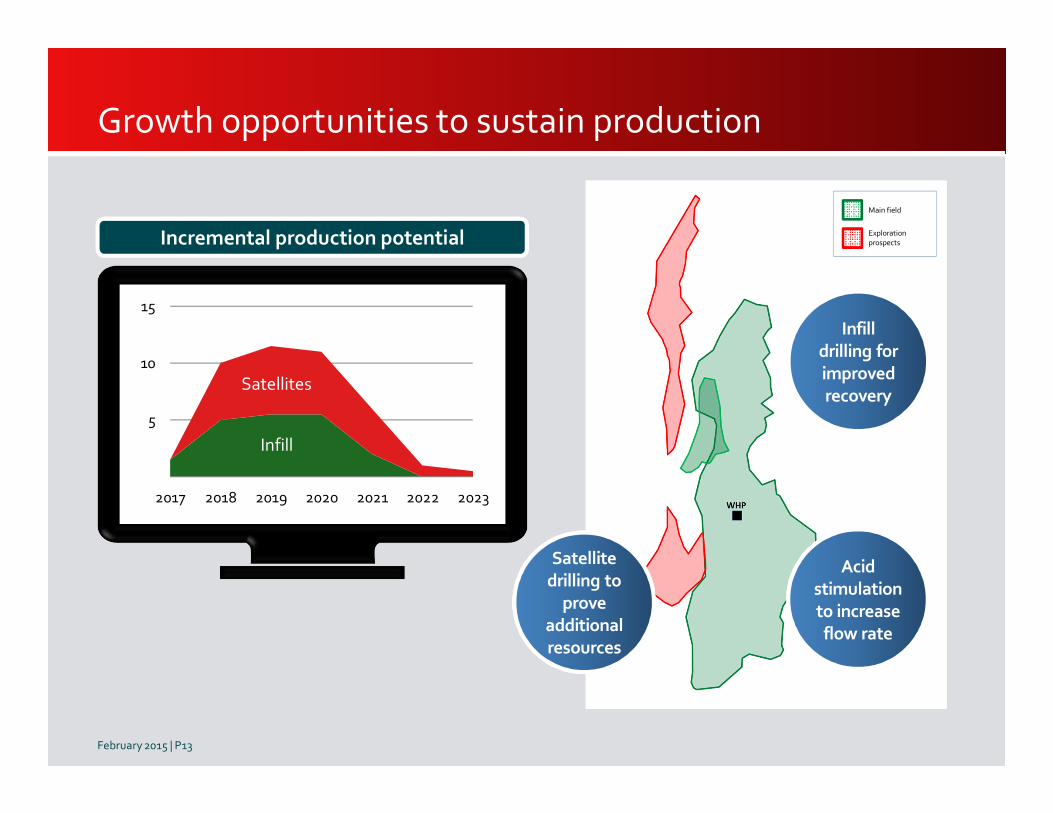

Growth opportunities to sustain production

Main field

Exploration

prospects

Satellite

drilling to

prove

additional

resources

Infill

drilling for

improved

recovery

Acid

stimulation

to increase

flow rate

Incremental production potential

February 2015 | P13

0

5

10

15

2017 2018 2019 2020 2021 2022 2023

Infill

Satellites

Falkland IslandsNeil Hawkings

Falkland Islands Business Unit Director

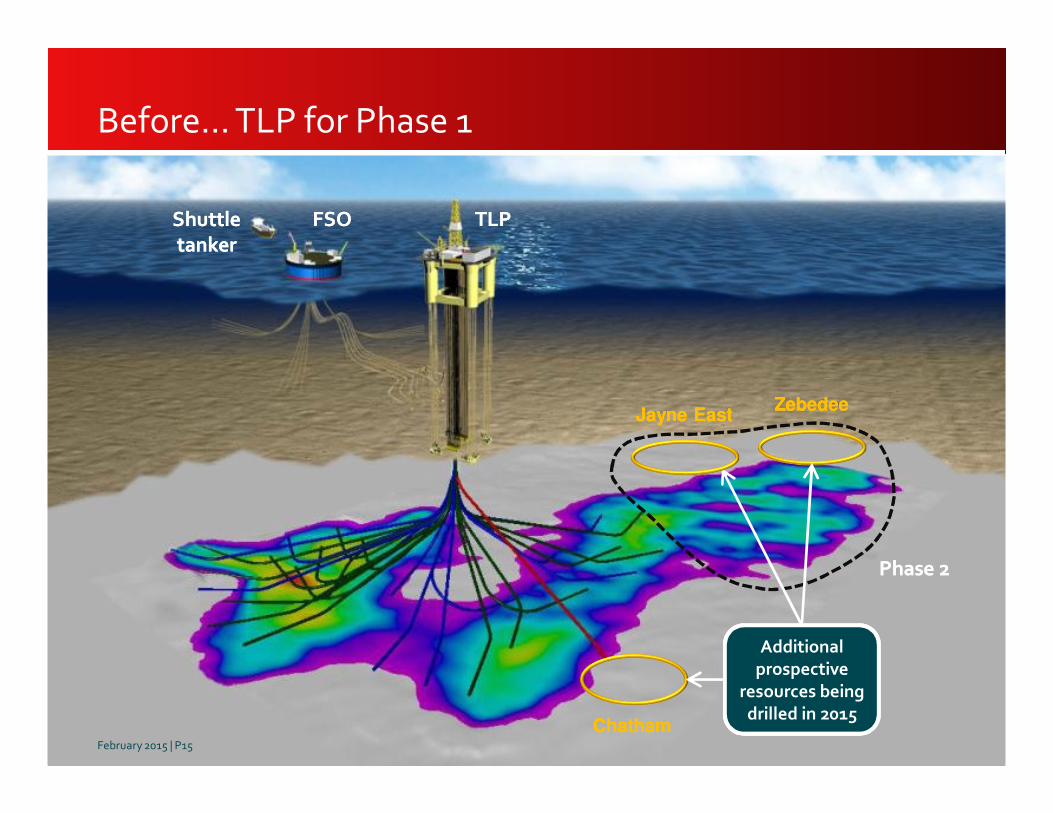

Before… TLP for Phase 1

TLPTLPFSOFSOShuttletanker

Shuttletanker

ChathamChatham

Phase 2Phase 2

ZebedeeZebedeeJayne EastJayne East

Additional

prospective

resources being

drilled in 2015

February 2015 | P15

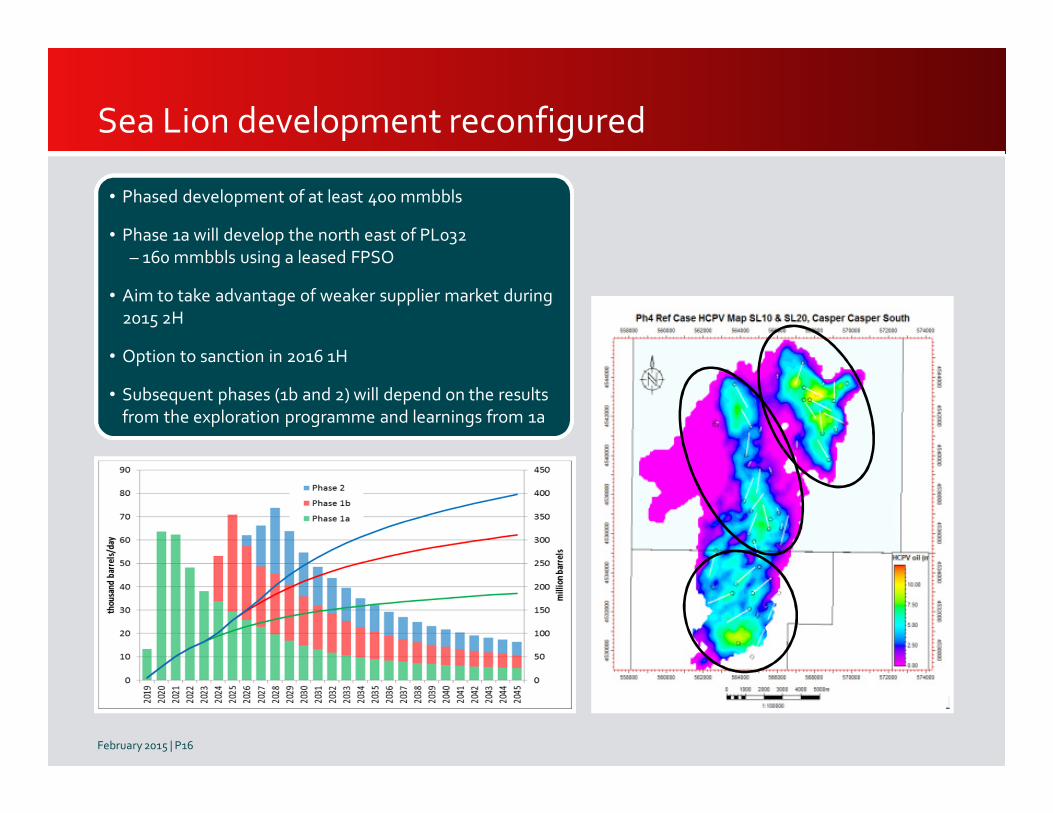

Sea Lion development reconfigured

• Phased development of at least 400 mmbbls

• Phase 1a will develop the north east of PL032

– 160 mmbbls using a leased FPSO

• Aim to take advantage of weaker supplier market during

2015 2H

• Option to sanction in 2016 1H

• Subsequent phases (1b and 2) will depend on the results

from the exploration programme and learnings from 1a

February 2015 | P16

Now… Phase 1a

Subseadrill centre

Subseadrill centre

FPSOFPSO

Shuttletanker

Shuttletanker

ChathamChatham

ZebedeeZebedeeJayne EastJayne East

• 14 development wells

– 8 producers

– 5 water injectors

– 1 gas producer / injector

– 9 pre-drilled

• 160 mmbbls over 15 years

February 2015 | P17

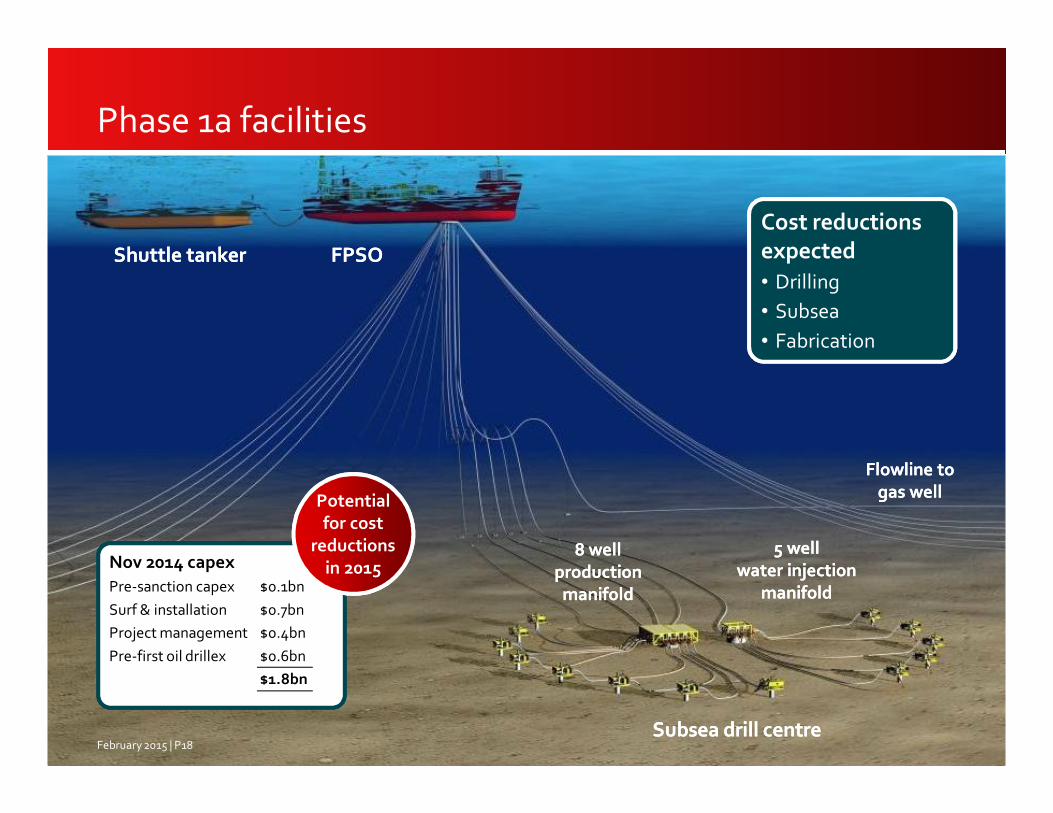

Phase 1a facilities

Subsea drill centreSubsea drill centre

FPSOFPSOShuttle tankerShuttle tanker

8 well

production

manifold

8 well

production

manifold

5 well

water injection

manifold

5 well

water injection

manifold

Flowline to

gas well

Flowline to

gas well

Nov 2014 capex

Pre-sanction capex $0.1bn

Surf & installation $0.7bn

Project management $0.4bn

Pre-first oil drillex $0.6bn

$1.8bn

Potential Potential

for cost

reductions

in 2015

Cost reductions

expected

• Drilling

• Subsea

• Fabrication

February 2015 | P18

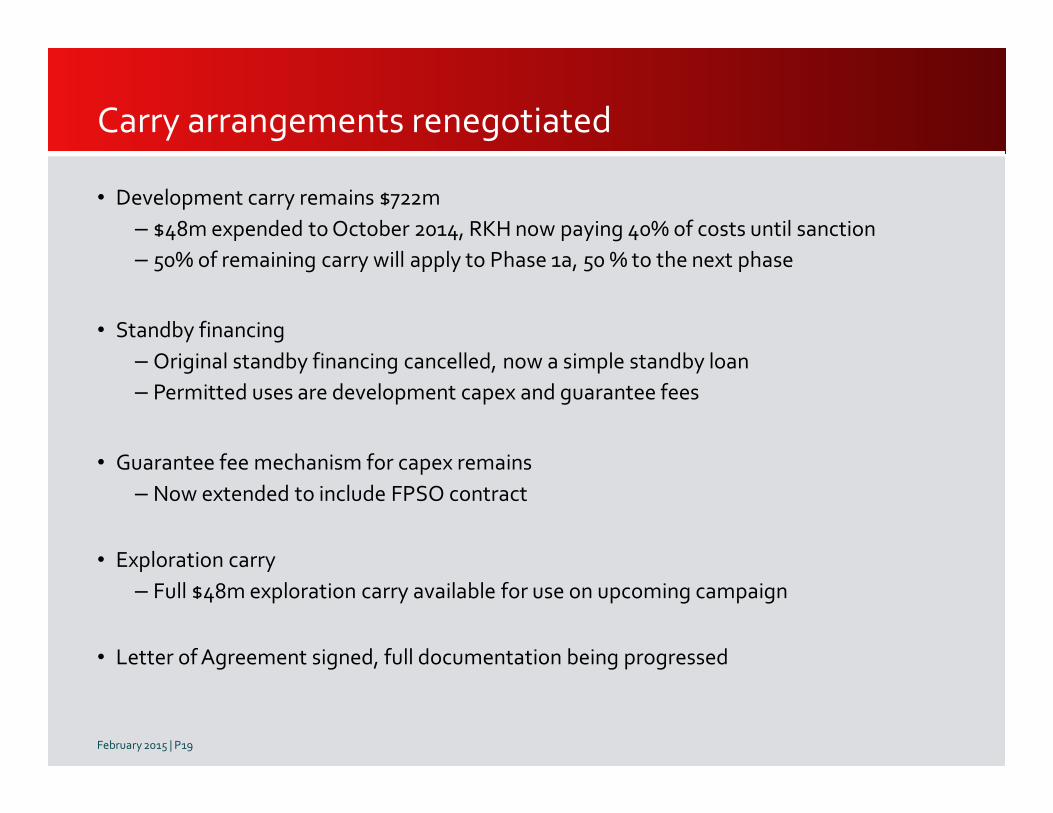

Carry arrangements renegotiated

• Development carry remains $722m

– $48m expended to October 2014, RKH now paying 40% of costs until sanction

– 50% of remaining carry will apply to Phase 1a, 50 % to the next phase

• Standby financing

– Original standby financing cancelled, now a simple standby loan

– Permitted uses are development capex and guarantee fees

• Guarantee fee mechanism for capex remains

– Now extended to include FPSO contract

• Exploration carry

– Full $48m exploration carry available for use on upcoming campaign

• Letter of Agreement signed, full documentation being progressed

February 2015 | P19

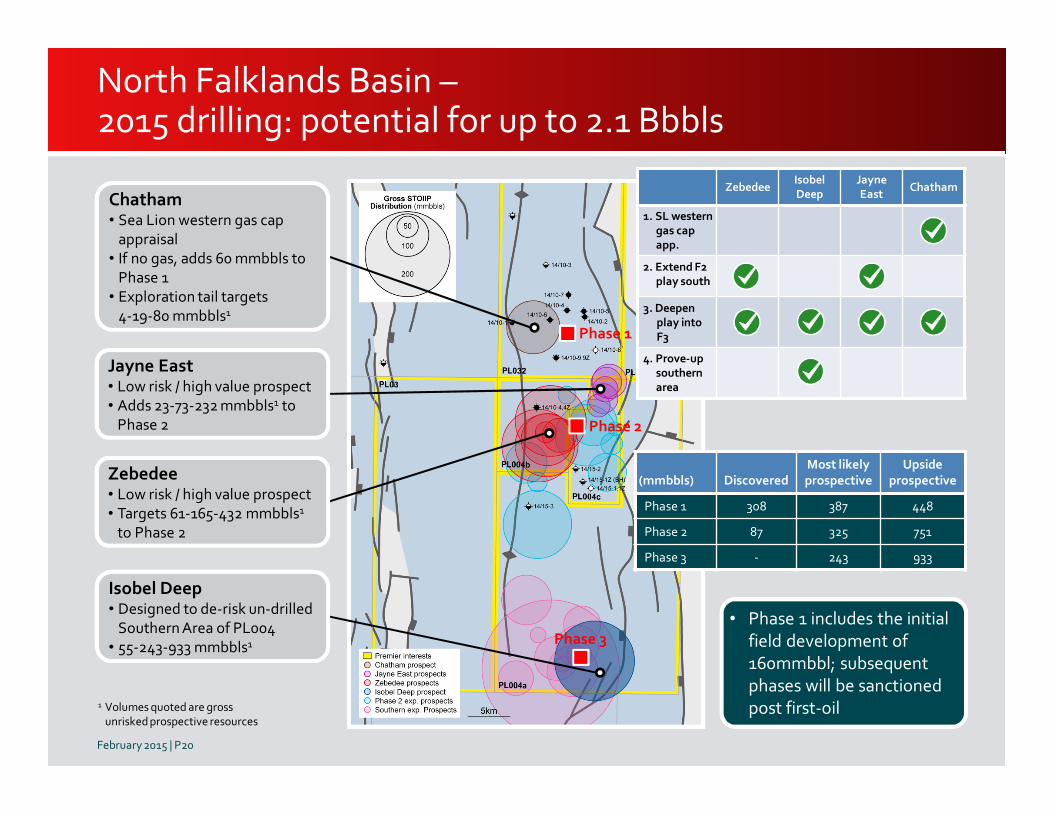

North Falklands Basin –2015 drilling: potential for up to 2.1 Bbbls

Phase 1

Phase 3

Phase 2

Chatham• Sea Lion western gas cap

appraisal

• If no gas, adds 60 mmbbls to

Phase 1

• Exploration tail targets

4-19-80 mmbbls1

Zebedee• Low risk / high value prospect

• Targets 61-165-432 mmbbls1

to Phase 2

Jayne East• Low risk / high value prospect

• Adds 23-73-232 mmbbls1 to

Phase 2

Isobel Deep• Designed to de-risk un-drilled

Southern Area of PL004

• 55-243-933 mmbbls1

1 Volumes quoted are grossunrisked prospective resources

(mmbbls) DiscoveredMost likelyprospective

Upside prospective

Phase 1 308 387 448

Phase 2 87 325 751

Phase 3 - 243 933

ZebedeeIsobelDeep

Jayne East

Chatham

1. SL western gas cap app.

2. Extend F2 play south

3. Deepen play into F3

4. Prove-up southern area

• Phase 1 includes the initial

field development of

160mmbbl; subsequent

phases will be sanctioned

post first-oil

February 2015 | P20

FinanceRichard Rose

Finance Director

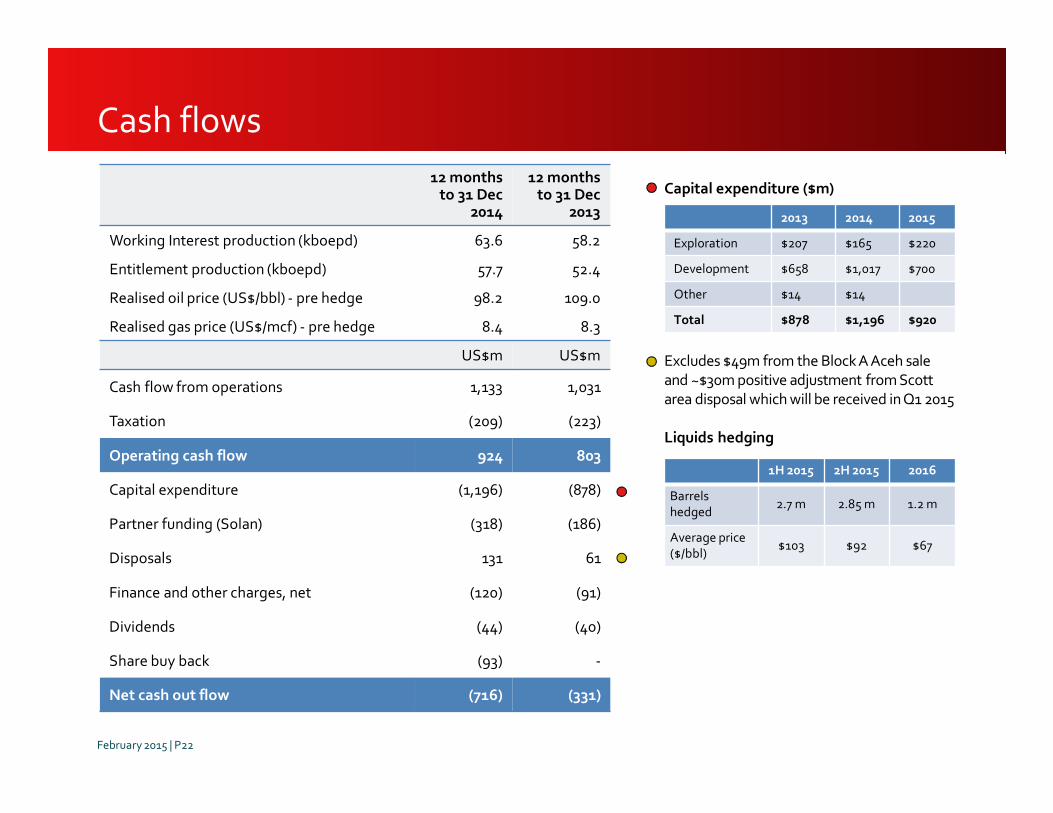

Capital expenditure ($m)

Excludes $49m from the Block A Aceh sale

and ~$30m positive adjustment from Scott

area disposal which will be received in Q1 2015

Liquids hedging

Cash flows

12 months to 31 Dec

2014

12 monthsto 31 Dec

2013

Working Interest production (kboepd) 63.6 58.2

Entitlement production (kboepd) 57.7 52.4

Realised oil price (US$/bbl) - pre hedge 98.2 109.0

Realised gas price (US$/mcf) - pre hedge 8.4 8.3

US$m US$m

Cash flow from operations 1,133 1,031

Taxation (209) (223)

Operating cash flow 924 803

Capital expenditure (1,196) (878)

Partner funding (Solan) (318) (186)

Disposals 131 61

Finance and other charges, net (120) (91)

Dividends (44) (40)

Share buy back (93) -

Net cash out flow (716) (331)

1H 2015 2H 2015 2016

Barrels hedged

2.7 m 2.85 m 1.2 m

Average price($/bbl)

$103 $92 $67

February 2015 | P22

2013 2014 2015

Exploration $207 $165 $220

Development $658 $1,017 $700

Other $14 $14

Total $878 $1,196 $920

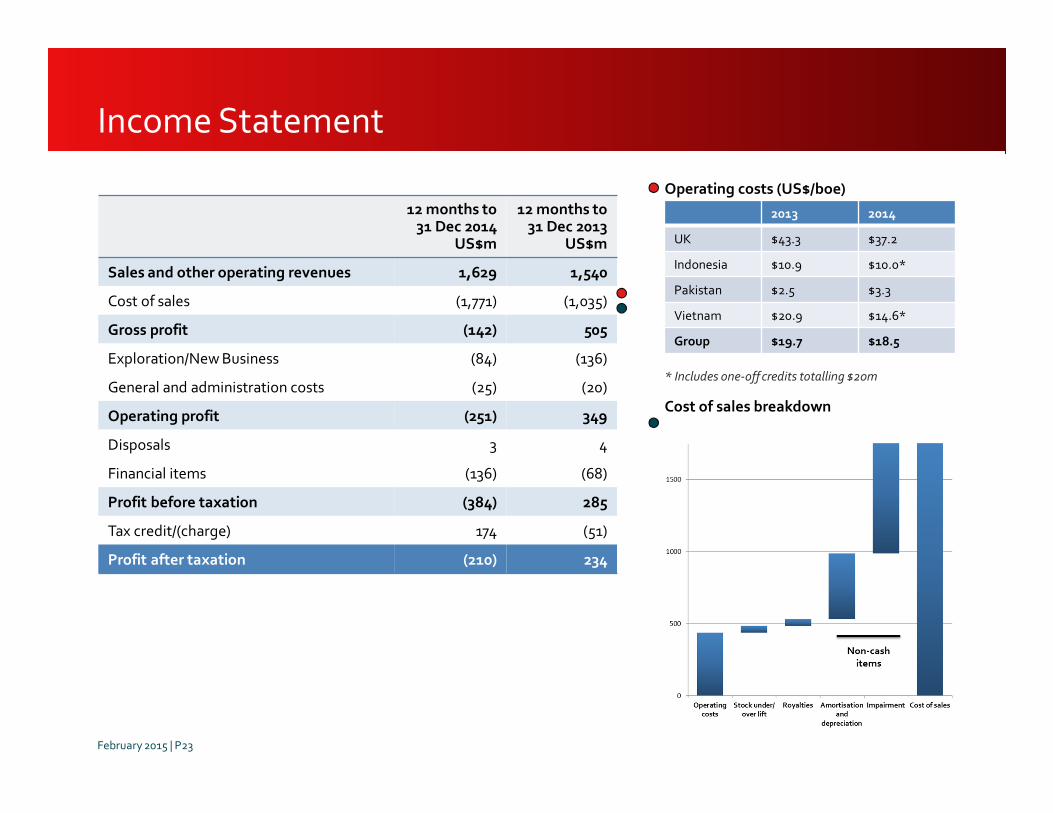

12 months to31 Dec 2014

US$m

12 months to 31 Dec 2013

US$m

Sales and other operating revenues 1,629 1,540

Cost of sales (1,771) (1,035)

Gross profit (142) 505

Exploration/New Business (84) (136)

General and administration costs (25) (20)

Operating profit (251) 349

Disposals 3 4

Financial items (136) (68)

Profit before taxation (384) 285

Tax credit/(charge) 174 (51)

Profit after taxation (210) 234

Income Statement

Operating costs (US$/boe)

* Includes one-off credits totalling $20m

Cost of sales breakdown

2013 2014

UK $43.3 $37.2

Indonesia $10.9 $10.0*

Pakistan $2.5 $3.3

Vietnam $20.9 $14.6*

Group $19.7 $18.5

February 2015 | P23

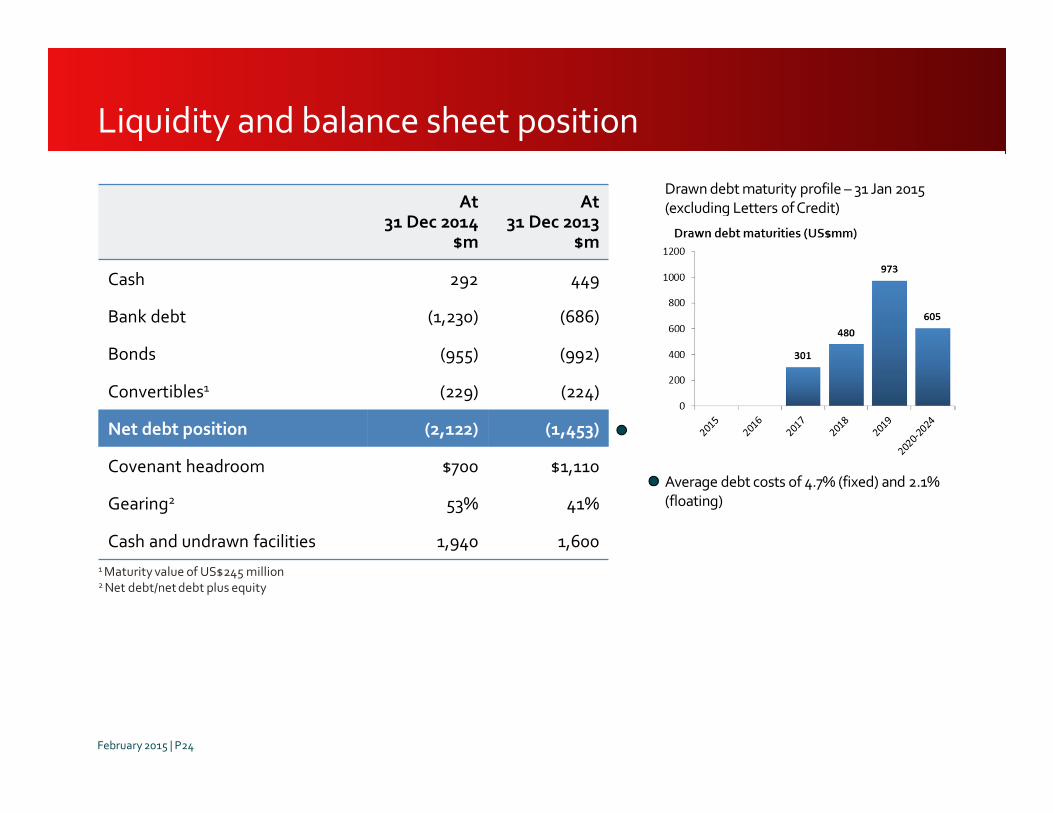

Liquidity and balance sheet position

At31 Dec 2014

$m

At31 Dec 2013

$m

Cash 292 449

Bank debt (1,230) (686)

Bonds (955) (992)

Convertibles1 (229) (224)

Net debt position (2,122) (1,453)

Covenant headroom $700 $1,110

Gearing2 53% 41%

Cash and undrawn facilities 1,940 1,600

1 Maturity value of US$245 million2 Net debt/net debt plus equity

Drawn debt maturity profile – 31 Jan 2015

(excluding Letters of Credit)

Average debt costs of 4.7% (fixed) and 2.1%

(floating)

February 2015 | P24

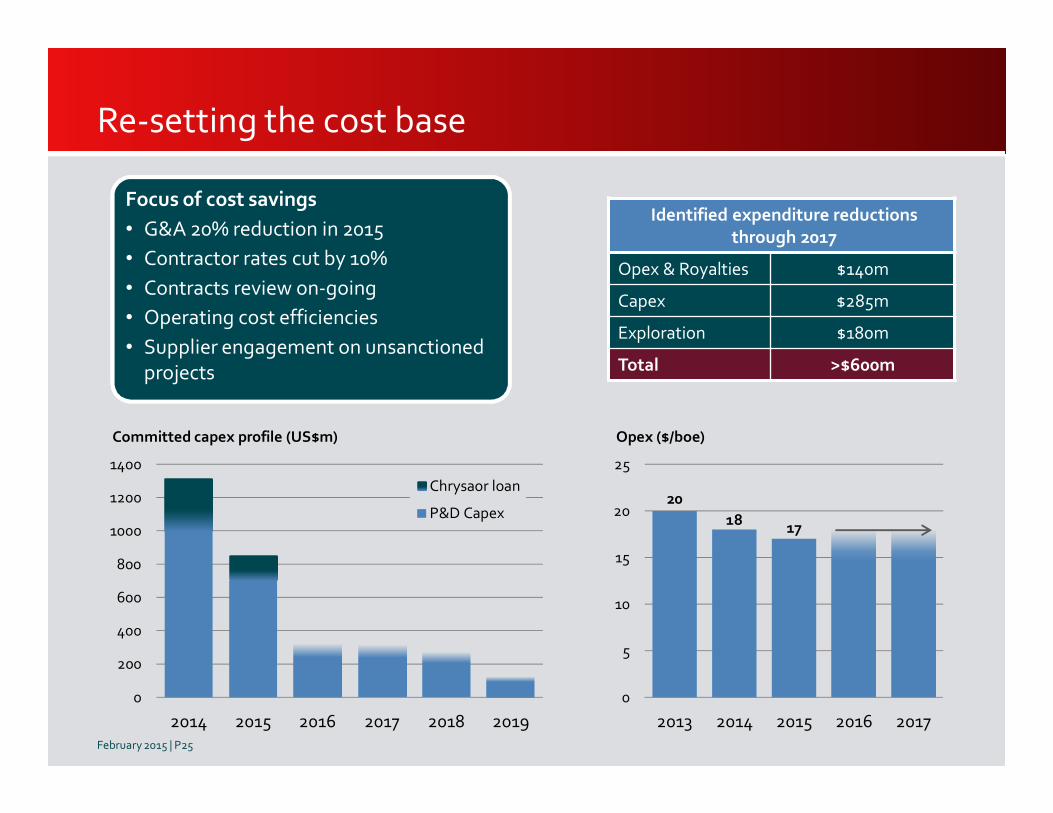

Re-setting the cost base

20

1817

0

5

10

15

20

25

2013 2014 2015 2016 2017

Opex ($/boe)

0

200

400

600

800

1000

1200

1400

2014 2015 2016 2017 2018 2019

Committed capex profile (US$m)

Chrysaor loan

P&D Capex

Focus of cost savings

• G&A 20% reduction in 2015

• Contractor rates cut by 10%

• Contracts review on-going

• Operating cost efficiencies

• Supplier engagement on unsanctioned projects

Identified expenditure reductions

through 2017

Opex & Royalties $140m

Capex $285m

Exploration $180m

Total >$600m

February 2015 | P25

OutlookTony Durrant

CEO

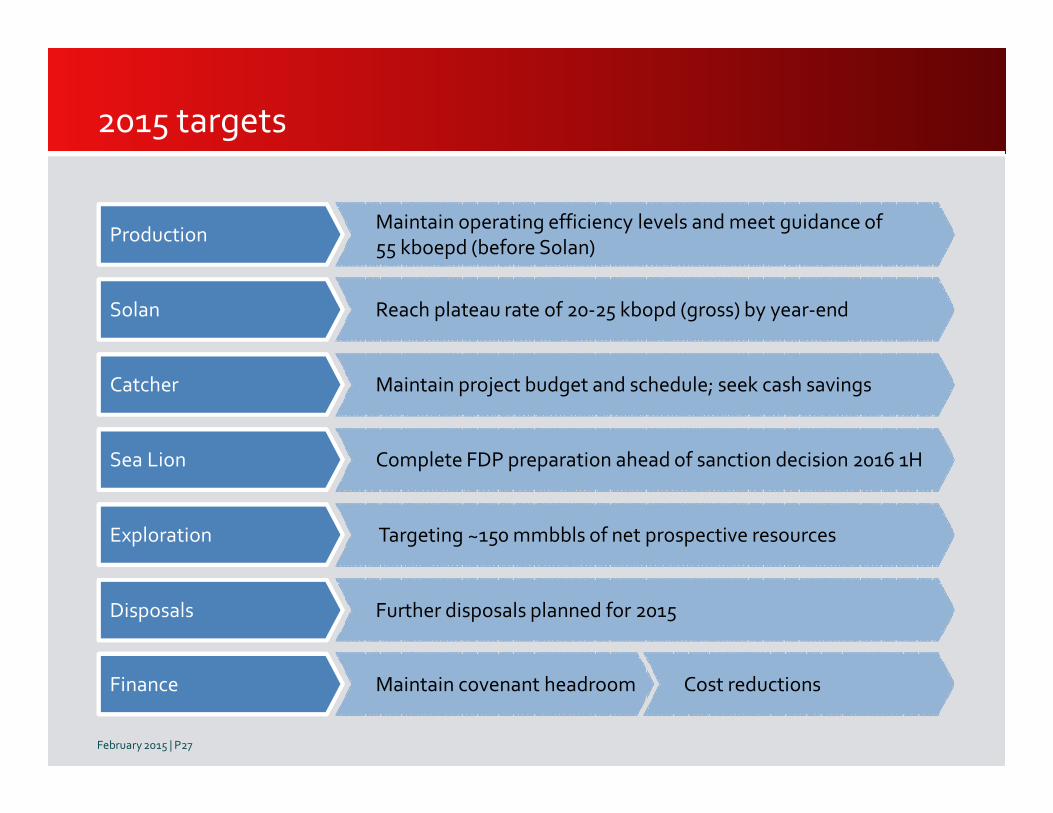

2015 targets

Reach plateau rate of 20-25 kbopd (gross) by year-end

Production

Solan

Catcher

Sea Lion

Exploration

Finance

Disposals

Maintain operating efficiency levels and meet guidance of55 kboepd (before Solan)

Maintain project budget and schedule; seek cash savings

Complete FDP preparation ahead of sanction decision 2016 1H

Targeting ~150 mmbbls of net prospective resources

Maintain covenant headroom Cost reductions

Further disposals planned for 2015

February 2015 | P27

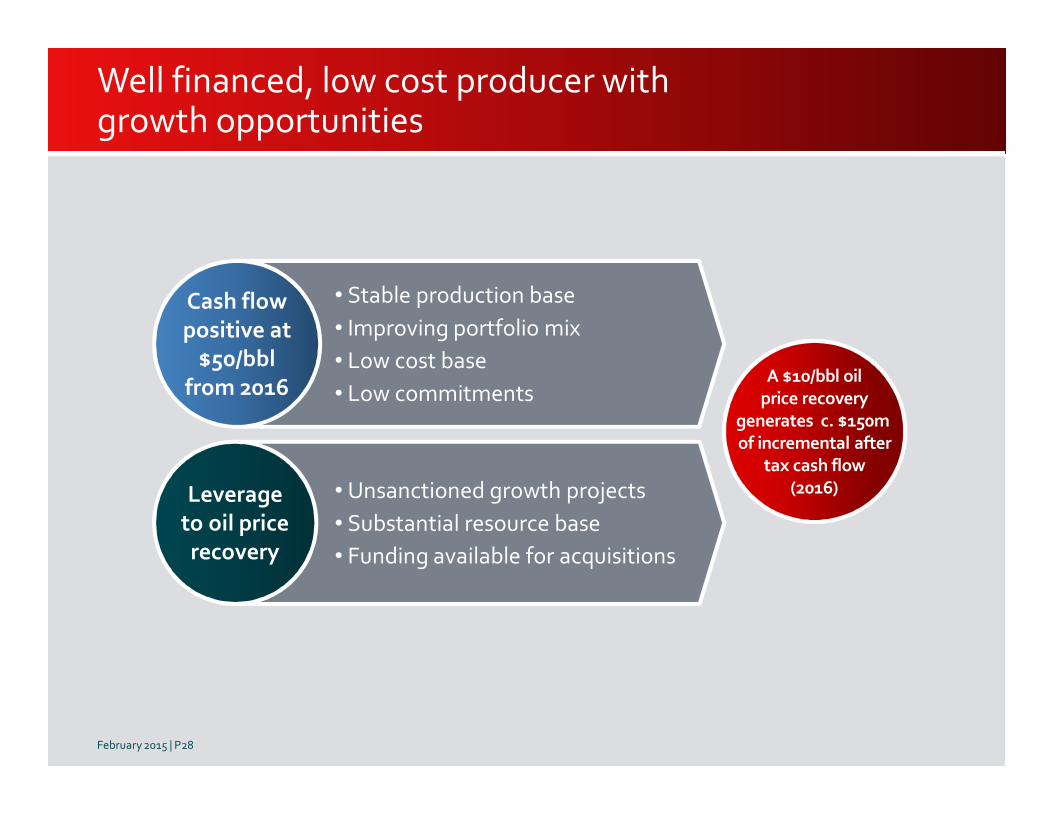

Well financed, low cost producer withgrowth opportunities

February 2015 | P28

A $10/bbl oil

price recovery

generates c. $150m

of incremental after

tax cash flow

(2016)• Unsanctioned growth projects

• Substantial resource base

• Funding available for acquisitions

Leverage

to oil price

recovery

• Stable production base

• Improving portfolio mix

• Low cost base

• Low commitments

Cash flow

positive at

$50/bbl

from 2016

Q&A

Premier Oil Plc

23 Lower Belgrave Street

London

SW1W 0NR

Tel: +44 (0)20 7730 1111

Fax: +44 (0)20 7730 4696

Email: [email protected]

www.premier-oil.com

February 2015