Potential Growth Markets for LNG LNG for Transportation · Wartsila North America ... Americas...

38

<Title of Presentation> By: <Author Name>, <Organization> <Date> <Title of Presentation> By: <Author Name>, <Organization> <Date> 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) Potential Growth Markets for LNG – LNG for Transportation John Hatley PE Americas VP Ship Power Wartsila North America 19 April 2013 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

Transcript of Potential Growth Markets for LNG LNG for Transportation · Wartsila North America ... Americas...

<Title of Presentation>

By: <Author Name>, <Organization>

<Date>

<Title of Presentation>

By: <Author Name>, <Organization>

<Date>

17th INTERNATIONAL CONFERENCE & EXHIBITION

ON LIQUEFIED NATURAL GAS (LNG 17)

Potential Growth Markets for LNG –

LNG for Transportation

John Hatley PE

Americas VP Ship Power

Wartsila North America

19 April 2013

17th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

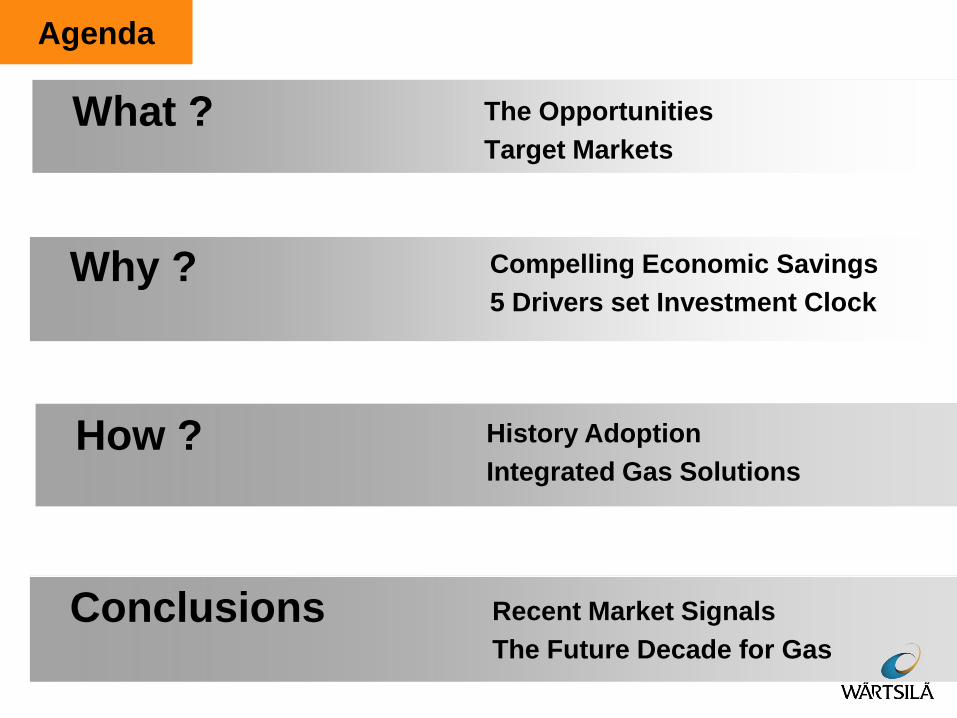

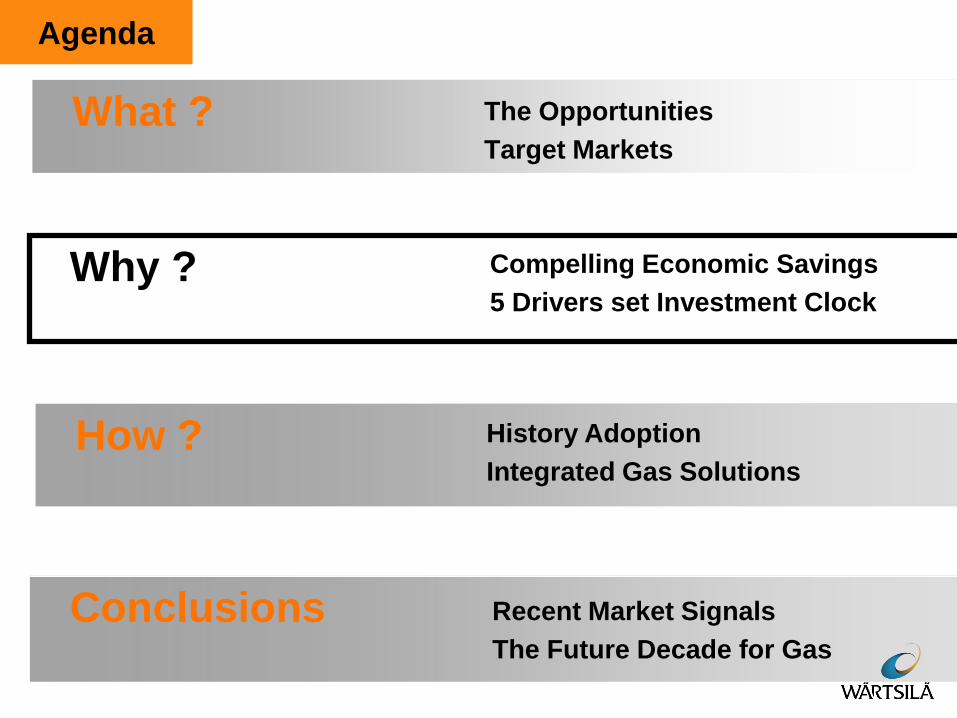

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

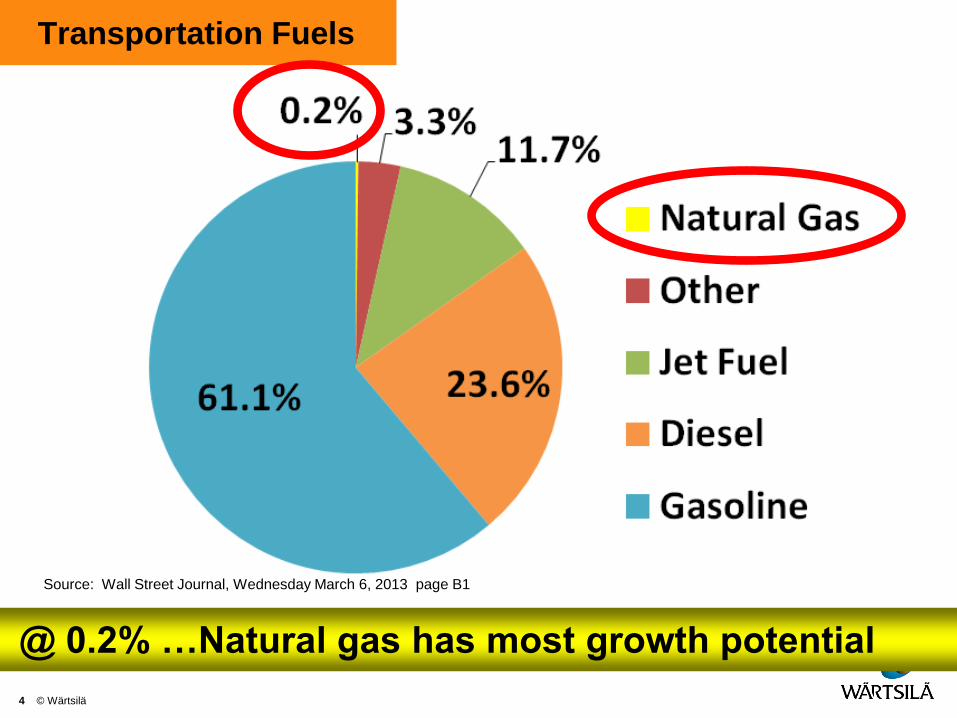

Transportation Fuels

4 © Wärtsilä

Source: Wall Street Journal, Wednesday March 6, 2013 page B1

@ 0.2% …Natural gas has most growth potential

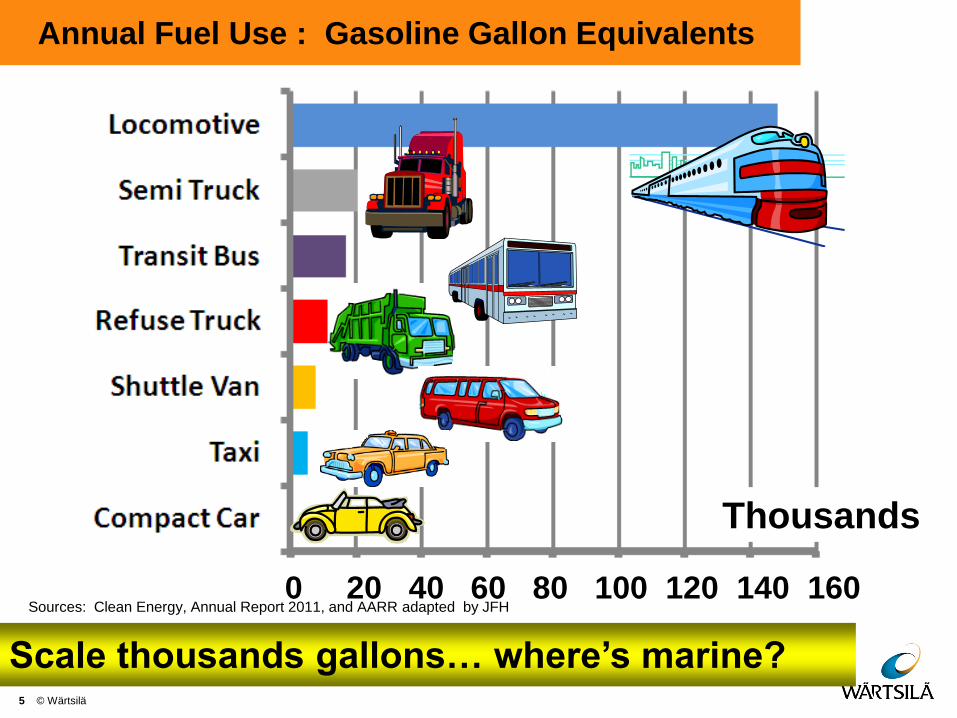

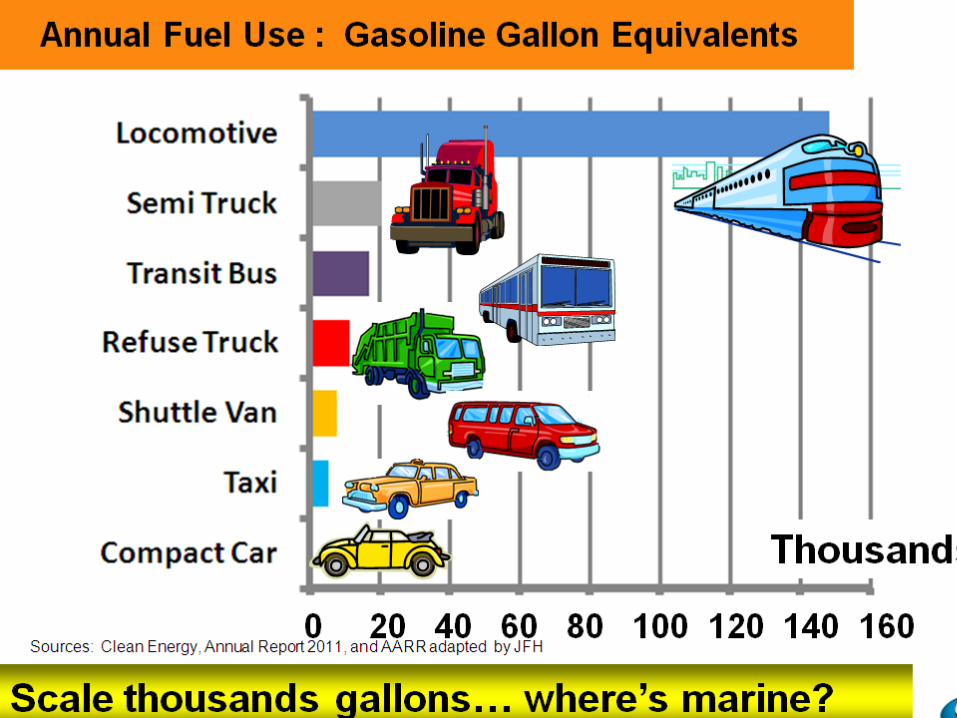

Annual Fuel Use : Gasoline Gallon Equivalents

5 © Wärtsilä

0 20 40 60 80 100 120 140 160

Thousands

Scale thousands gallons… where’s marine?

Sources: Clean Energy, Annual Report 2011, and AARR adapted by JFH

New Market Development Target

Scalability

6 © Wärtsilä LDC Gas Forum LA CA October 2010 John Hatley Americas VP Ship Power

a large number of small lot consumers ...

Prefer a small number of large lot consumers

Harbor Tug

7 © Wärtsilä

Annual 268,600

Gasoline Gallon Equivalent GGE

Ferryboat

8 © Wärtsilä

Annual 664,000

Gasoline Gallon Equivalent GGE

Offshore Supply

9 © Wärtsilä

Annual 1,072,000

Gasoline Gallon Equivalent GGE

Mississippi Towboat

10 © Wärtsilä LDC Gas Forum LA CA October 2010 John Hatley Americas VP Ship Power

Annual 2,058,000

Gasoline Gallon Equivalent GGE

Great Lakes Bulker

11 © Wärtsilä LDC Gas Forum LA CA October 2010 John Hatley Americas VP Ship Power

Annual 2,866,000

Gasoline Gallon Equivalent GGE

Coastal Cruise

12 © Wärtsilä LDC Gas Forum LA CA October 2010 John Hatley Americas VP Ship Power

Annual 6,801,000

Gasoline Gallon Equivalent GGE

Container Ship

13 © Wärtsilä LDC Gas Forum LA CA October 2010 John Hatley Americas VP Ship Power

Annual 28,090,000

Gasoline Gallon Equivalent GGE

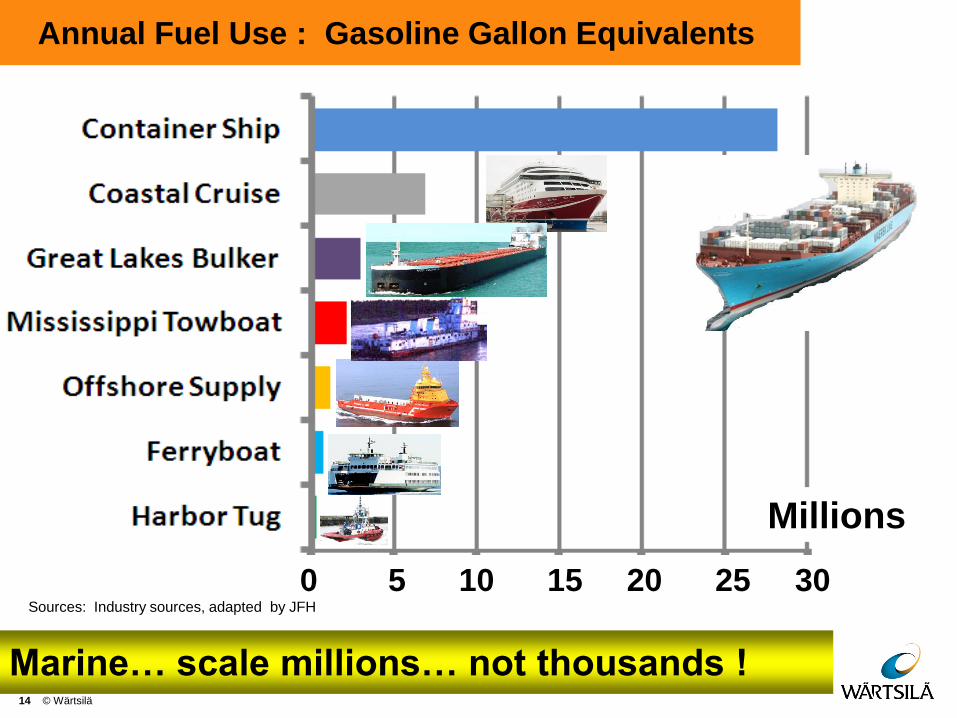

Annual Fuel Use : Gasoline Gallon Equivalents

14 © Wärtsilä

Marine… scale millions… not thousands !

0 5 10 15 20 25 30

Millions

Sources: Industry sources, adapted by JFH

Annual Fuel Use : Gasoline Gallon Equivalents

15 © Wärtsilä

Marine… scale millions… not thousands !

0 5 10 15 20 25 30

Millions

Sources: Industry sources, adapted by JFH

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

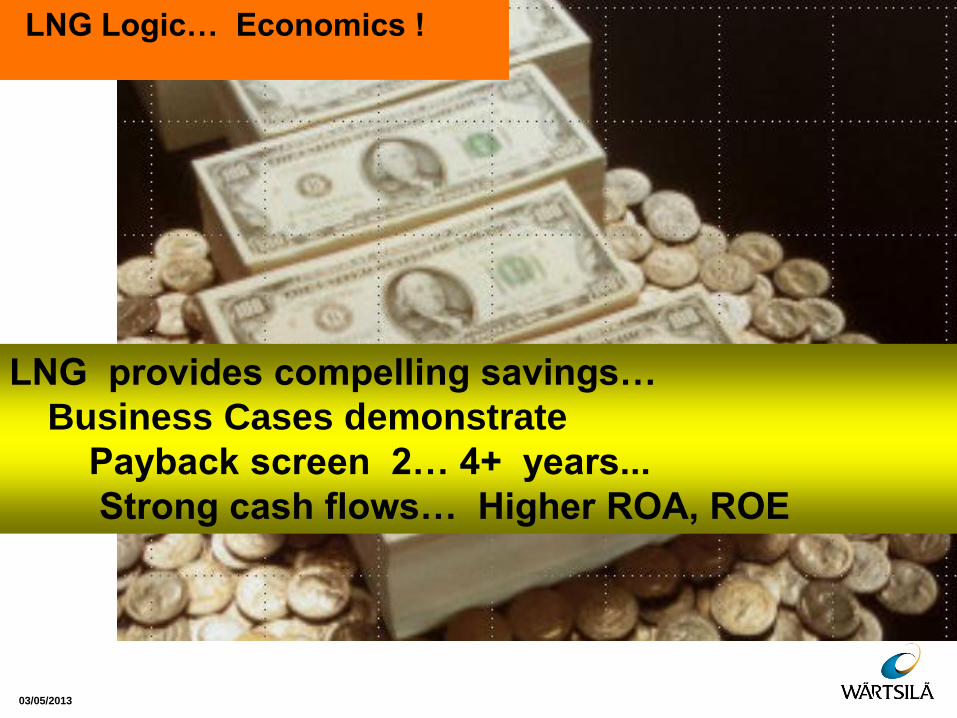

Logic… Economics !

03/05/2013

LNG Logic… Economics !

LNG provides compelling savings…

Business Cases demonstrate

Payback screen 2… 4+ years...

Strong cash flows… Higher ROA, ROE

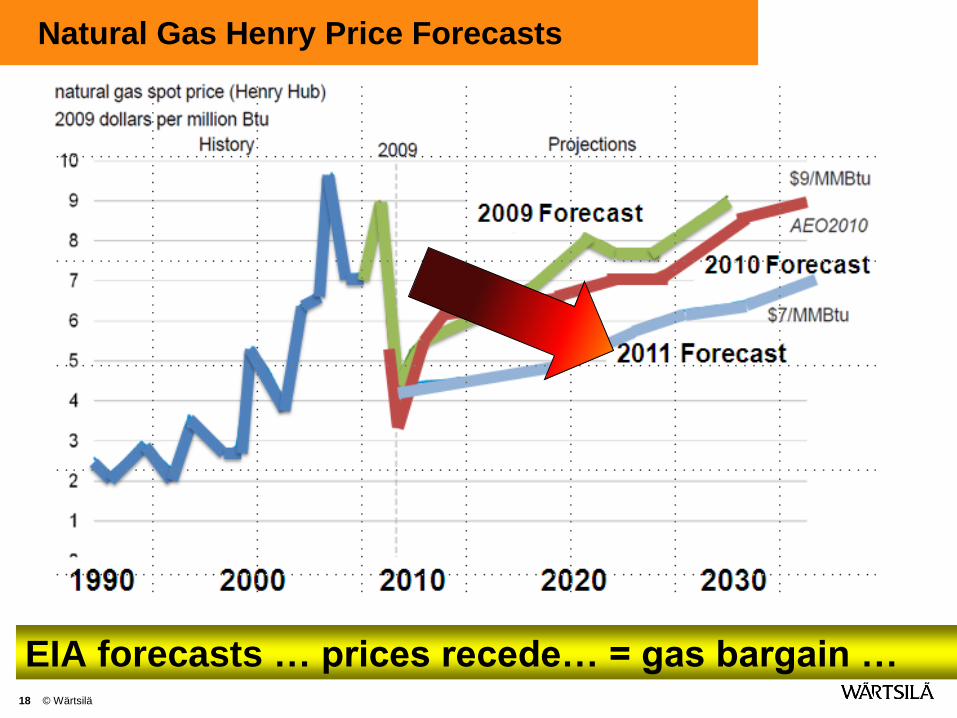

Natural Gas Henry Price Forecasts

18 © Wärtsilä

EIA forecasts … prices recede… = gas bargain …

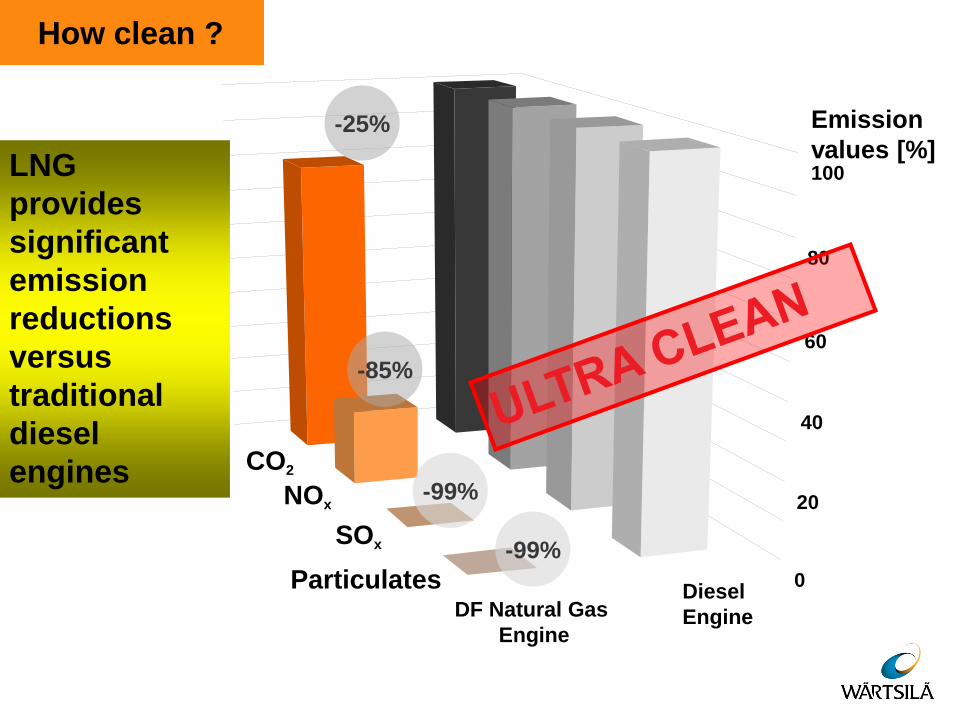

How clean ?

CO2

NOx

SOx

Particulates DF Natural Gas

Engine

Diesel

Engine

0

20

40

60

80

100

Emission

values [%] -25%

-85%

-99%

-99%

LNG

provides

significant

emission

reductions

versus

traditional

diesel

engines

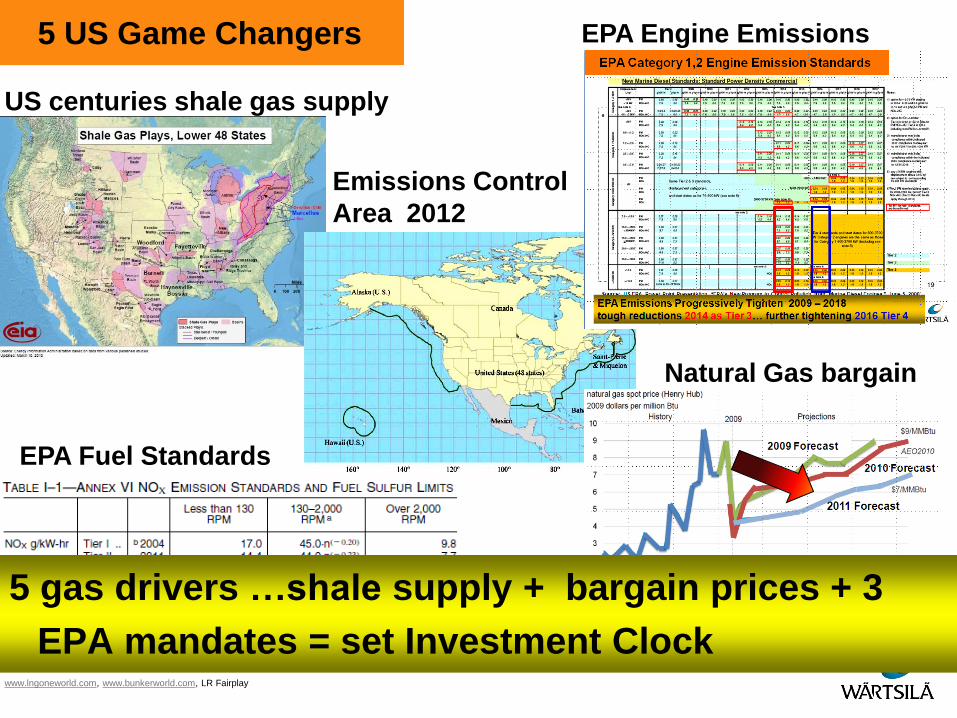

5 US Game Changers

Source:http://www.google.com/imgres?imgurl=http://www.canadiansailings.ca/canadiansailings/portals/0/April_13/emissions_area_map.jpg&imgrefurl=http://

EIA March 2010 Shale Gas Plays Lower 48 States

www.lngoneworld.com, www.bunkerworld.com, LR Fairplay

US centuries shale gas supply

Natural Gas bargain

Emissions Control

Area 2012

EPA Engine Emissions

EPA Fuel Standards

5 gas drivers …shale supply + bargain prices + 3

EPA mandates = set Investment Clock

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

Mark Twain

History does not

repeat itself, but it

does rhyme

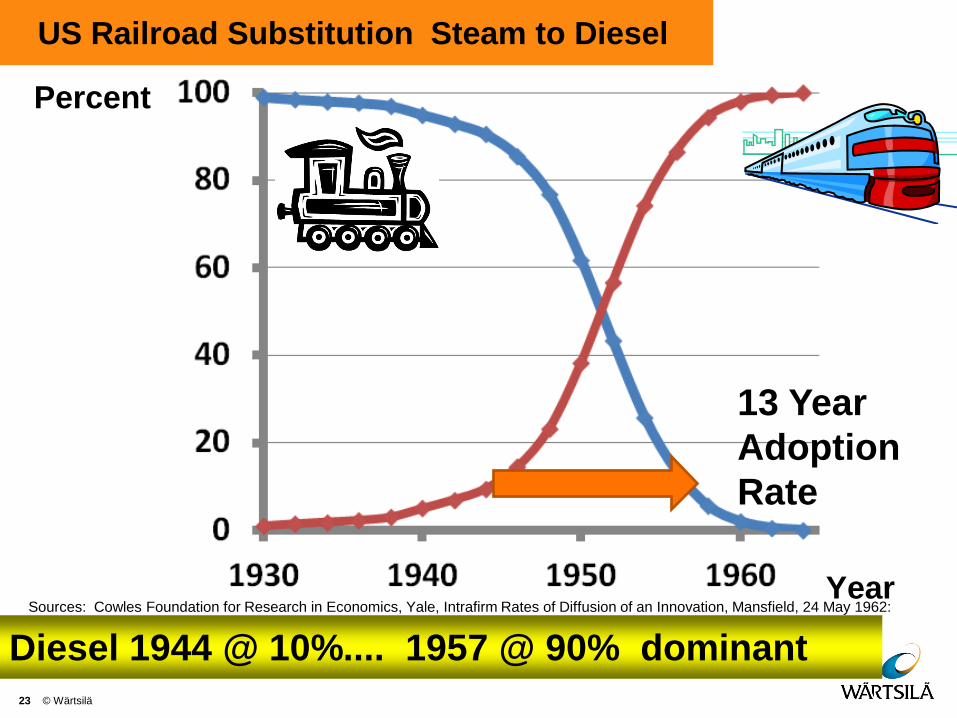

US Railroad Substitution Steam to Diesel

Percent

23 © Wärtsilä

Year

13 Year

Adoption

Rate

Sources: Cowles Foundation for Research in Economics, Yale, Intrafirm Rates of Diffusion of an Innovation, Mansfield, 24 May 1962:

adapted by JFH

Diesel 1944 @ 10%.... 1957 @ 90% dominant

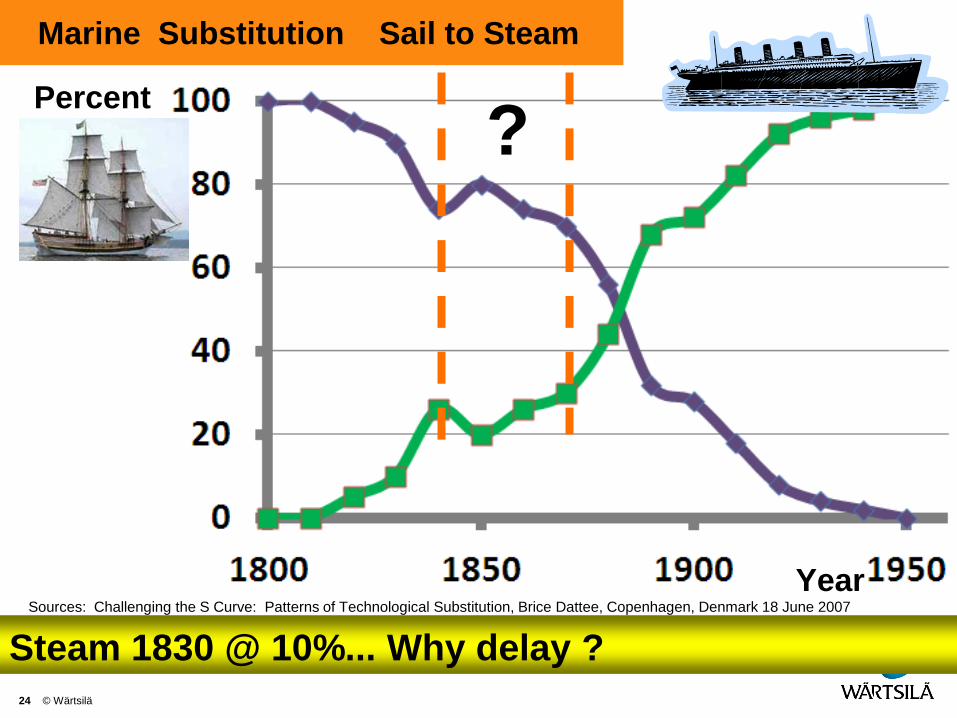

Marine Substitution Sail to Steam

Percent

24 © Wärtsilä

Year

?

Sources: Challenging the S Curve: Patterns of Technological Substitution, Brice Dattee, Copenhagen, Denmark 18 June 2007

adapted by JFH

Steam 1830 @ 10%... Why delay ?

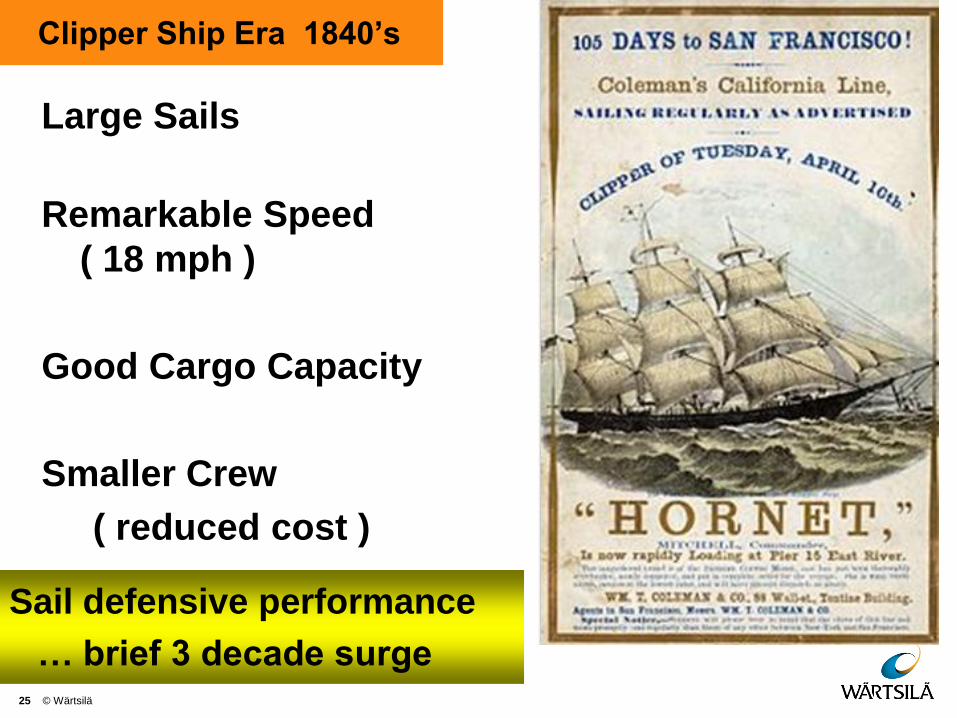

Clipper Ship Era 1840’s

Large Sails

Remarkable Speed

( 18 mph )

Good Cargo Capacity

Smaller Crew

( reduced cost )

25 © Wärtsilä

Sail defensive performance

… brief 3 decade surge

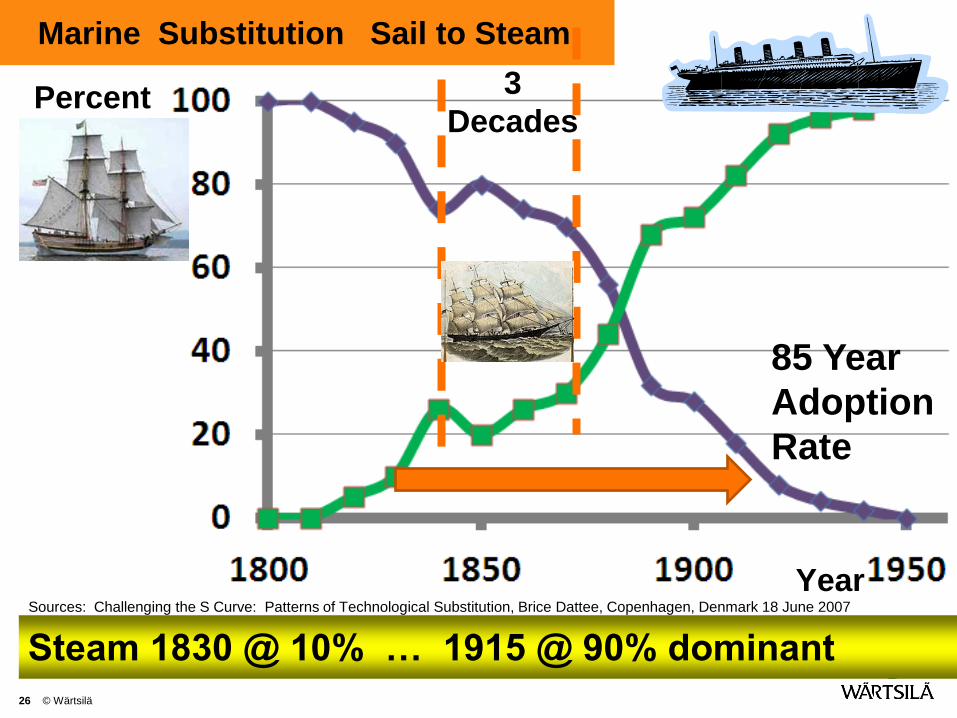

Marine Substitution Sail to Steam

Percent

26 © Wärtsilä

Year

3

Decades

85 Year

Adoption

Rate

Sources: Challenging the S Curve: Patterns of Technological Substitution, Brice Dattee, Copenhagen, Denmark 18 June 2007

adapted by JFH

Steam 1830 @ 10% … 1915 @ 90% dominant

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

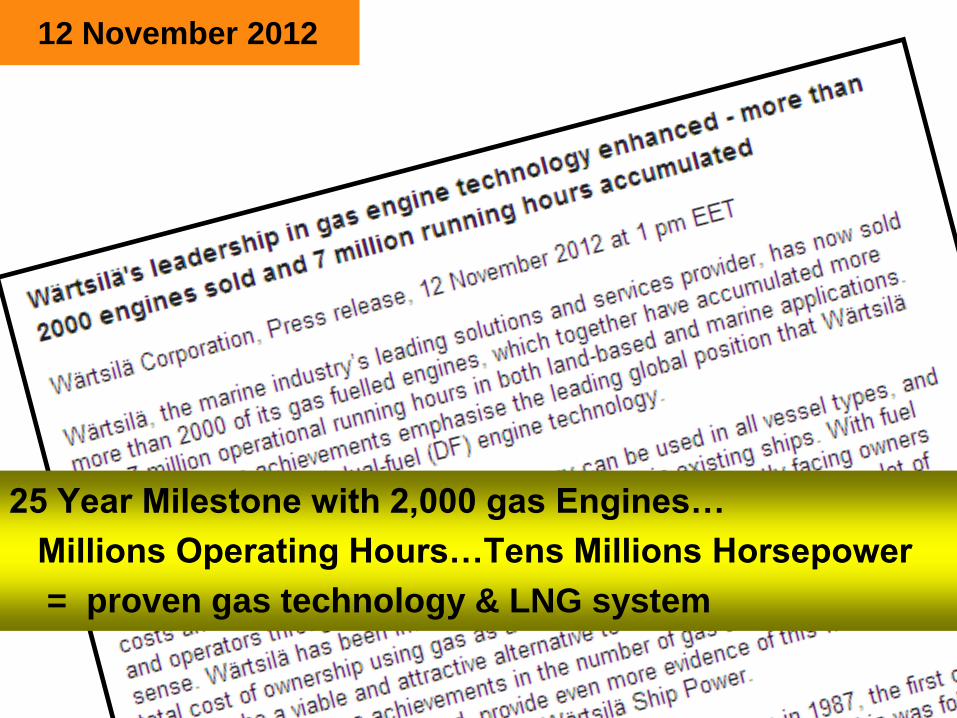

12 November 2012

25 Year Milestone with 2,000 gas Engines…

Millions Operating Hours…Tens Millions Horsepower

= proven gas technology & LNG system

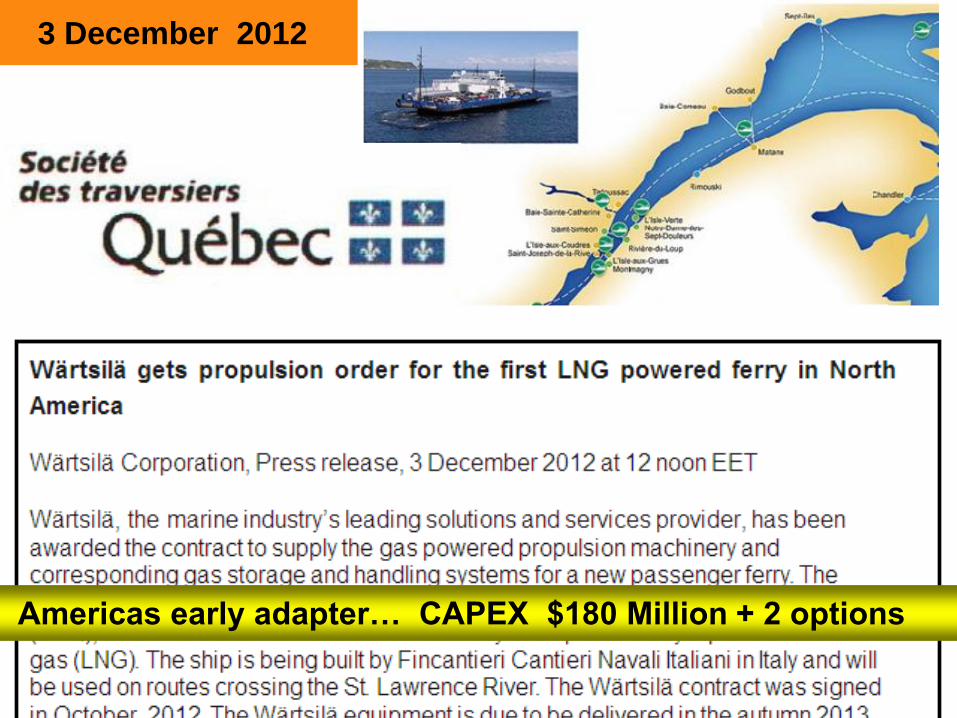

3 December 2012

03/05/2013

29

Americas early adapter… CAPEX $180 Million + 2 options

4 December 2012

03/05/2013

30

Americas early adopter … CAPEX $380 Million + 3 Options

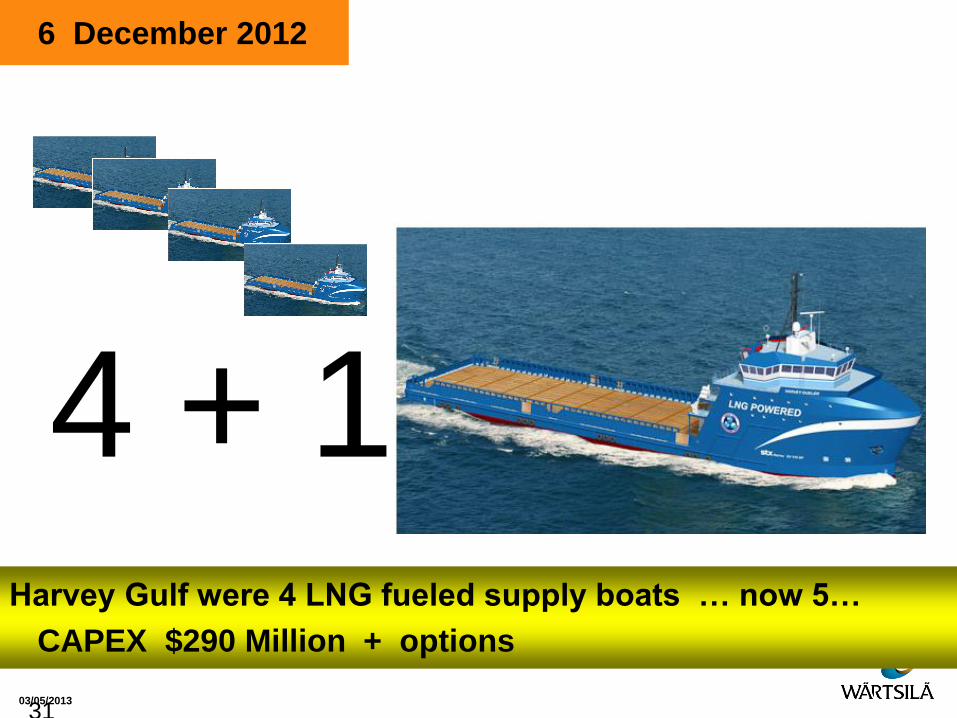

6 December 2012

03/05/2013

31

Harvey Gulf were 4 LNG fueled supply boats … now 5…

CAPEX $290 Million + options

4 + 1

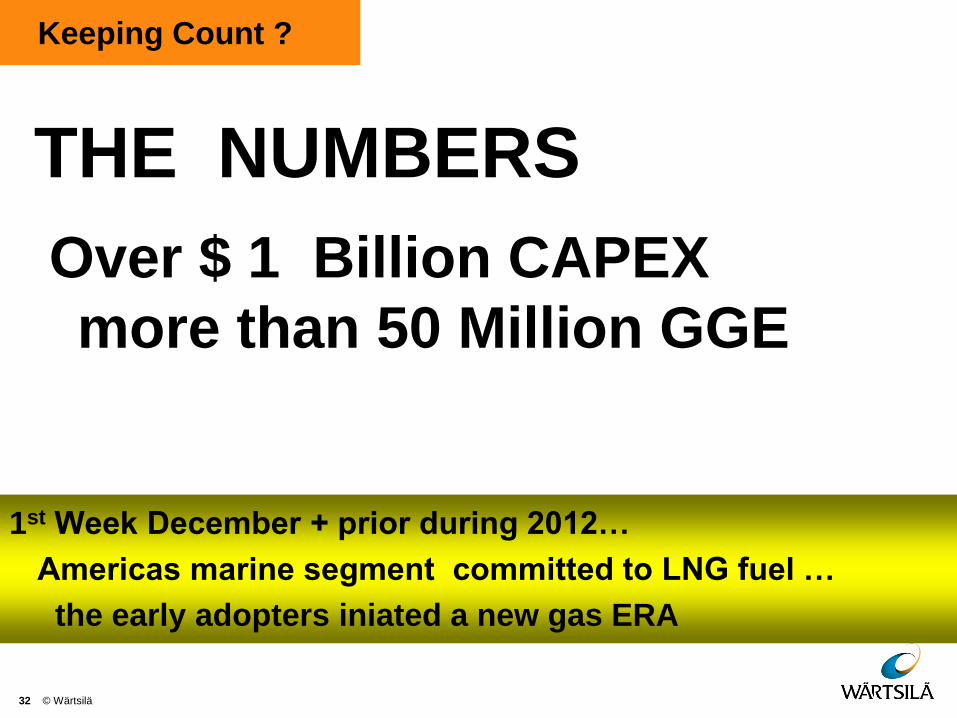

Keeping Count ?

THE NUMBERS

32 © Wärtsilä

1st Week December + prior during 2012…

Americas marine segment committed to LNG fuel …

the early adopters iniated a new gas ERA

Over $ 1 Billion CAPEX

more than 50 Million GGE

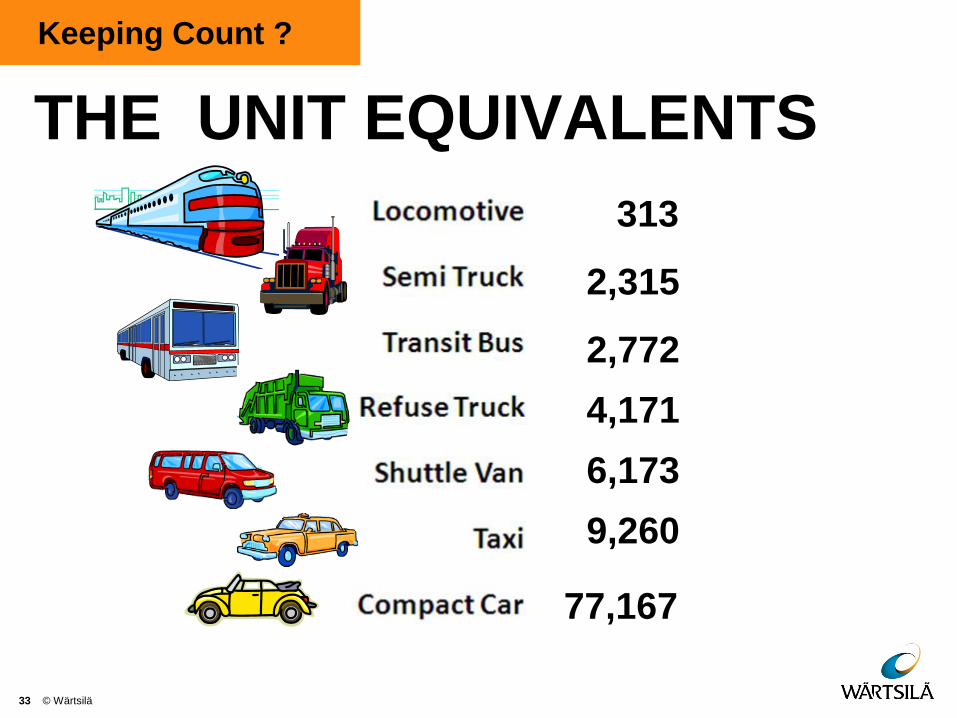

Keeping Count ?

THE UNIT EQUIVALENTS

33 © Wärtsilä

313

2,315

2,772

4,171

6,173

9,260

77,167

15 January 2013 Viking Grace …

3 May 2013 34 © Wärtsilä

Length: 214.0 m

Breadth: 31.8 m

Speed 22 knots

Passengers: 2800

Cabins: 880

In service: 2013

Shipyard: STX Finland Oy

Ship Owner: Viking Line

LNGpac Tanks

2 @ 200m3 each

Safe, Clean, LNG Cruise Ship … CAPEX $320 Million

5 March 2013

03/05/2013

3 LNG plants each at 250K tons/yr

Geismar, Jumping Pond, & Sarnia…Online 2015

Source: http://www.bizjournals.com/houston/news/2013/03/05/shell-planning-lng-units-in-us-canada.html

Supply security and price stability = certainty

…certainty breeds investment

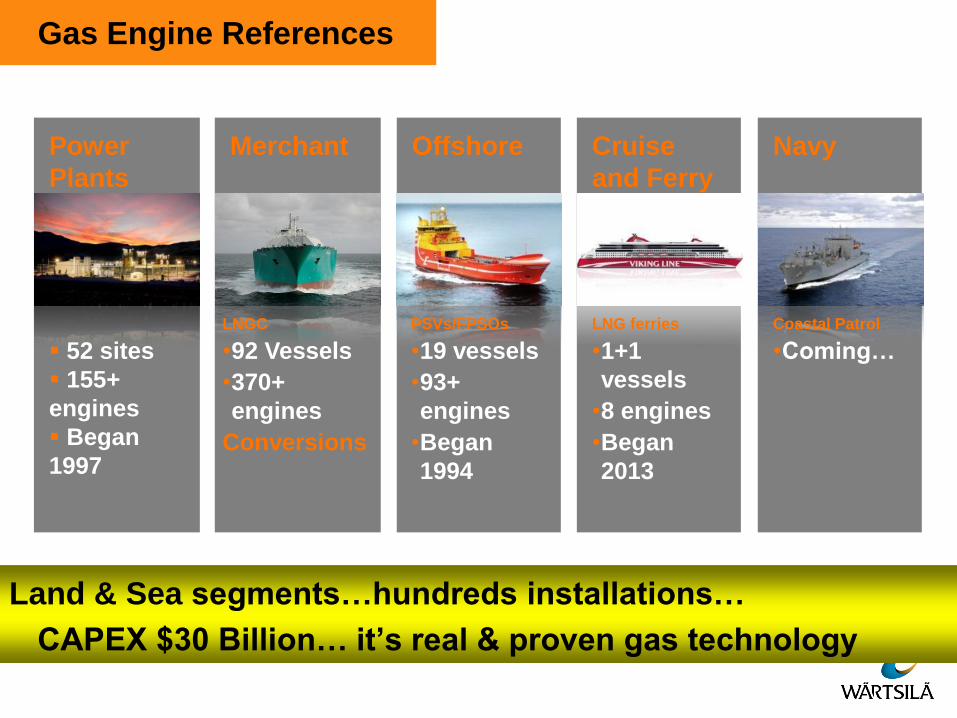

Gas Engine References

Land & Sea segments…hundreds installations…

CAPEX $30 Billion… it’s real & proven gas technology

Power

Plants

52 sites

155+

engines

Began

1997

Merchant

LNGC

•92 Vessels

•370+

engines

Conversions

Offshore

PSVs/FPSOs

•19 vessels

•93+

engines

•Began

1994

Cruise

and Ferry

LNG ferries

•1+1

vessels

•8 engines

•Began

2013

Navy

Coastal Patrol

•Coming…

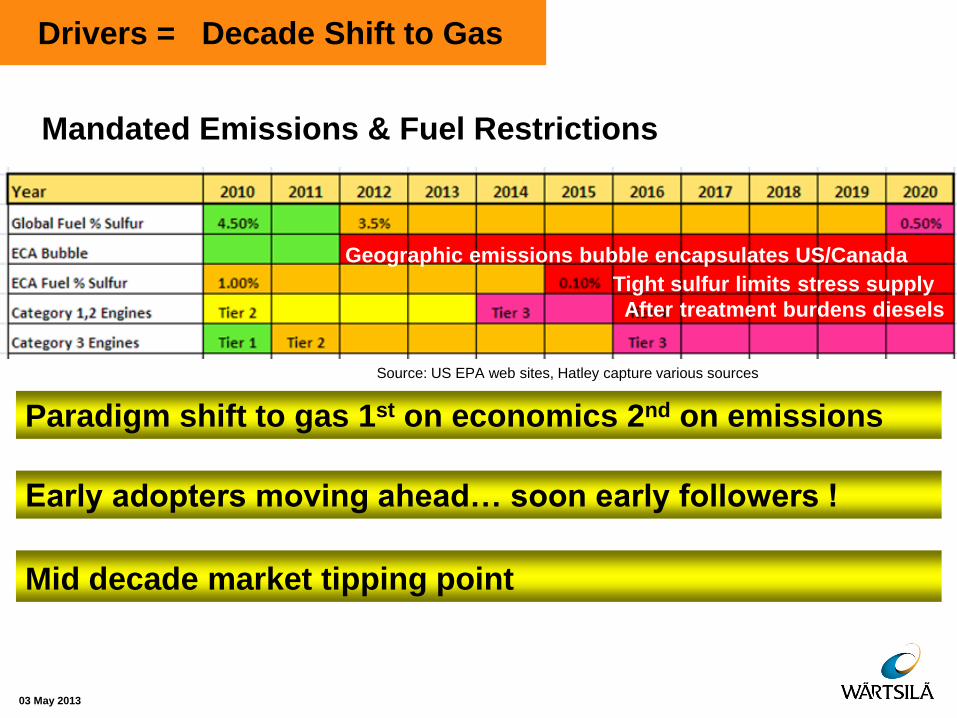

Drivers = Decade Shift to Gas

03 May 2013

Mid decade market tipping point

Source: US EPA web sites, Hatley capture various sources

Geographic emissions bubble encapsulates US/Canada

Tight sulfur limits stress supply

After treatment burdens diesels

Paradigm shift to gas 1st on economics 2nd on emissions

Early adopters moving ahead… soon early followers !

Mandated Emissions & Fuel Restrictions

Agenda

What ?

Why ?

Compelling Economic Savings

5 Drivers set Investment Clock

How ?

History Adoption

Integrated Gas Solutions

Conclusions

Recent Market Signals

The Future Decade for Gas

The Opportunities

Target Markets

![WARTSILA AUTONOMOUS VESSEL ADVANCES - NAMEPAWARTSILA AUTONOMOUS VESSEL ADVANCES 1 15.3.2018 [Presentation name / Author] Kevin Humphreys Business Development Manager - Americas Wartsila](https://static.fdocuments.us/doc/165x107/5e6a9f937b476068ef466113/wartsila-autonomous-vessel-advances-namepa-wartsila-autonomous-vessel-advances.jpg)