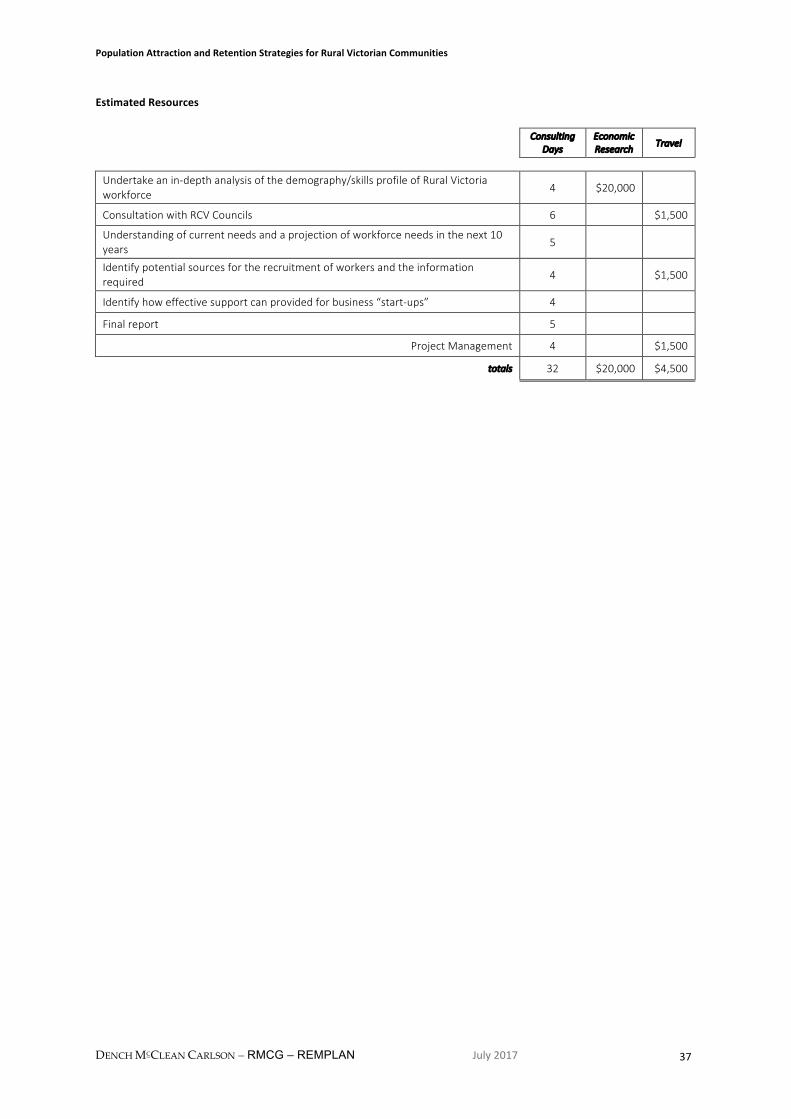

Population Attraction and Retention Strategies for …...Population Attraction and Retention...

47

Population Attraction and Retention Strategies for Rural Victorian Communities July 2017

Transcript of Population Attraction and Retention Strategies for …...Population Attraction and Retention...

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

July2017

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 2

ExecutiveSummary

RuralCouncilsVictoria(RCV)hascommissionedthePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesproject.TheprojectaimstoidentifyaprioritysetofProjectsforimplementationoverthreeyearsconsistentwithRCV’srole,mandateandcapacity,aswellasopportunitiesthatexisttoinfluenceStategovernmentpolicyandprograms.ThePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesprojecthasinvolvedthefollowingkeyactivities:

1) AreviewofpopulationandeconomictrendsinruralVictoria

2) AreviewofpopulationattractionandretentionstrategiesbeingundertakeninAustralia,theUSA,CanadaandScotland

Thereviewofpopulationandeconomictrendsnotedthat:

• RuralVictoria’spopulationisprojectedtogrowby156,470from712,376in2011to868,846in2031;muchofthisgrowthwillbeexperiencedintheperi-urbanruralLGAs

• 12of38RuralLGAsareprojectedtoexperiencenetpopulationgrowthbutwillexperienceanoveralllossofpopulationagedunder65years.17of38RuralLGAsareprojectedtoexperiencenetpopulationlossbutwillexperienceanincreaseinpeopleaged65andolder

• RuralVictoria’spopulationofpeopleagedover65istheprojectedtoincreasebysome100,000throughto2031.

• RuralVictoriageneratessome9.24%ofVictoria’sGrossStateProduct

• Between2006and2011thenumberofjobsinruralVictoriagrewbymorethan5,000however20of38ruralLGAsexperiencednetjoblossesinthisperiod

ThereviewofpopulationattractionstrategiesinAustralia,theUSA,CanadaandScotlandobservedthatarangeofprogramsareinplacetosupportruralcommunitiesandeconomiesandthatthenumberofpeopleinrurallocationsandthat:

• ScotlandandTasmaniahaddefinedpopulationgrowthtargets

• TheUSAandScotlandplacegreatemphasisonacommunityeconomicdevelopmentapproach

• TheUSAhasarangeofCommunityDevelopmentFinancialInstitutionsthatprovideaccessible/lowcostfinancetoruralcommunities,businessesandindividuals

• Canada’sAtlanticProvinceshaveinplaceanEconomicGrowthStrategythatseekstoaddressanageingworkforce

• Victoria’sBarwonSouthWestRDA’sworkonpopulationattractionidentified“marketsegments”thataremoreattractedtomovingtoarurallocation

• populationattractionisafunctionoftheavailabilityofeconomicopportunities,liveabilityincludingaccesstokeyservices,andpromotion–i.e.theprovisionofrequiredinformationtotargetmarkets

TheProjectsidentifiedaresummarizedinthetablebelow

Project Overview

RuralPopulationGrowthPolicy AdvocacyplatformtoGovernment/Opposition

RuralInvestmentAttractionProgram Identify,collateandpromotesignificantprivatesectorinvestmentopportunities

RuralWorkforceDevelopmentPlan Identifycurrent/futureworkforceneeds–bothnumbersandskills

OlderPersonsServices&AccommodationProgram

OpportunitiesforNFP/privatesectorinvestmentinservices/housingstock

AlternateServiceDelivery Identify/promoteeffectivealternateservicedeliverymodels

CommunityPlanningUpdate Collateneeds/identifycommonthemes/reflectthevoiceof“potentialentrants”

RuralPromotionProgram PromoteopportunitiesandadvantagesoflivinginruralVictoria

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 3

Contentssection page

1 Introduction 41.1 KeyProjectActivities 41.2 RuralLGAs 4

2 PopulationandEconomicTrendsinRuralVictoria 4

2.1 VictorianPopulation 52.2 RegionalCityLGAsPopulationTrends 52.3 RuralLGAsPopulationTrends 52.4 ImplicationsforPopulationAttractionProjects 62.5 RuralLGAsContributiontoGrossStateProduct 72.6 Jobs 72.7 RuralWorkforce 72.8 WorkforceAge 82.9 ImplicationsforPopulationAttractionProjects 8

3 ReviewofPopulationAttractionApproachesinOtherRuralAreas 103.1 USA 10

3.1.1 OverviewofFindings 113.1.2 PopulationAttractionStrategies 113.1.3 USDepartmentofAgriculture–RuralDevelopment 113.1.4 RuralLISC 123.1.4.1 LISCInstituteforComprehensiveCommunityDevelopment 133.1.5 NationalMainStreetCenter,Inc. 133.1.6 MarketingHometownAmerica 143.1.7 CostAdvantages 143.1.8 InvestmentReadiness 143.1.9 ImplicationsforPopulationAttractionProjects 14

3.2 Canada 153.2.1 OverviewofFindings 153.2.2 StateofRuralCanadaReport 153.2.3 AtlanticProvinces 153.2.4 BritishColumbia 163.2.5 Alberta 163.2.6 ImplicationsforPopulationAttractionProjects 17

3.3 Scotland 173.3.1 Population–PurposeTarget 173.3.2 ScottishRuralDevelopmentProgramme2014–2020 183.3.3 LEADER 193.3.4 ImplicationsforPopulationAttractionProjects 19

3.4 Australia 203.4.1 CommonwealthGovernment 203.4.2 Queensland 213.4.3 NewSouthWales 213.4.4 SouthAustralia 223.4.5 WesternAustralia 233.4.6 Tasmania 243.4.7 Victoria 25

4 RelevantStudies/Commentary 26

4.1 Peoplecount:Populationgrowthcausesbasiceconomicgrowth 264.2 Superconnectedlifestylelocations-Theriseofthe‘e-change’movement 274.3 AttractingandretainingskilledpeopleinregionalAustralia:Apractitioner’sguide 284.4 RuralMigrationTrendsandDrivers-RuralCouncilsVictoria 284.5 RegionalAustraliaInstitute 294.6 ImplicationsforPopulationAttractionProjects 30

5 RCVPopulationAttractionandRetentionProjects 305.1 KeyAssumptions 305.2 OverviewofPopulationAttractionandRetentionProjects 315.3 EstimationofRequiredResources 32

AppendixI-PopulationAttractionandRetentionProjects–DescriptionandEstimatedResourcesProject#1-RuralPopulationGrowthPolicy 34Project#2-RuralWorkforceDevelopmentPlan 36Project#3-RuralInvestmentAttractionProgram 38Project#4-OlderPersonsServicesandAccommodationProgram 40Project#5–AlternateServiceDelivery 42Project#6-CommunityPlanningUpdate 43Project#7-RuralPromotionProgram 44AppendixII-RCVAnalysis 47

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 4

1. Introduction

RuralCouncilsVictoria(RCV)hascommissionedthePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesproject.

TheprojectaimstodeterminedriversandbarrierstopopulationattractionandretentionandeconomicdevelopmentrelevanttoVictorianruralcommunitiesandidentifyaprioritysetofProjectsforimplementationoverthreeyearsconsistentwithRCV’srole,mandateandcapacity,aswellasopportunitiesthatexisttoinfluenceStategovernmentpolicyandprograms.

1.1 KeyProjectActivities

ThePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesprojecthasinvolvedthefollowingkeyactivities:

3) AreviewofpopulationandeconomictrendsinruralVictoria–i.e.the38ruralLocalGovernmentAreas(LGAs).

4) AreviewofpopulationattractionandretentionstrategiesbeingundertakeninAustralia,theUSA,CanadaandScotland(95%ofScotlandisclassifiedasrural)andtheidentificationofpracticesthatcouldbeutilisedinruralVictoria

Thefindingsof1and2werepresentedtotheRCVExecutivefordiscussionandreview

5) TheidentificationofrelevantprojectsforimplementationoverthreeyearsthatareconsistentwithRCV’srole,mandateandcapacity,aswellasopportunitiesthatexisttoinfluenceStategovernmentpolicyandprograms.

AdraftprogramofProjectswasdevelopedwithfeedbackfromaWorkingGroupoftheRCVExecutive.TheseProjectswerealsopresentedtoRCVMayorsandCEOsForum.

1.2 RuralLGAs

Thereare38ruralLGAsintheRCVnetwork(inalphabeticalorder):

AlpineShire(S) EastGippsland(S) Mitchell(S) SouthGippsland(S)

Ararat(RC) Gannawarra(S) Moira(S) SouthernGrampians(S)

BassCoast(S) Glenelg(S) Moorabool(S) Strathbogie(S)

BawBaw(S) GoldenPlains(S) MountAlexander(S) SurfCoast(S)

Benalla(RC) Hepburn(S) Moyne(S) SwanHill(S)

Buloke(S) Hindmarsh(S) Murrindindi(S) Towong(S)

Campaspe(S) Indigo(S) NorthernGrampians(S) Wellington(S)

CentralGoldfields(S) Loddon(S) Pyrenees(S) WestWimmera(S)

ColacOtway(S) MacedonRanges(S) Queenscliffe(B)

Corangamite(S) Mansfield(S) (B)=Borough/(S)=Shire/(RC)=RuralCity

Asat2016itwasestimatedthatthetotalpopulationoftheruralLGAswas731,193representing12.1%ofVictoria’spopulation.

TheruralLGAshaveatotalareaofsome17,910,437Ha–thisrepresents75%oftheVictoria’stotallandarea

2 RuralVictoriaPopulationandEconomicTrends

ThefollowingsectionsprovidesanoverviewofthepopulationandeconomictrendsintheVictorianruralLocalGovernmentAreas(LGAs).ThepopulationforecastsarethosemadeVictoriainFuture2016providedbytheDepartmentofEnvironment,Water,LandandPlanning(DWELP).

Theeconomicdataislargelybasedonthe2011ABSCensus

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 5

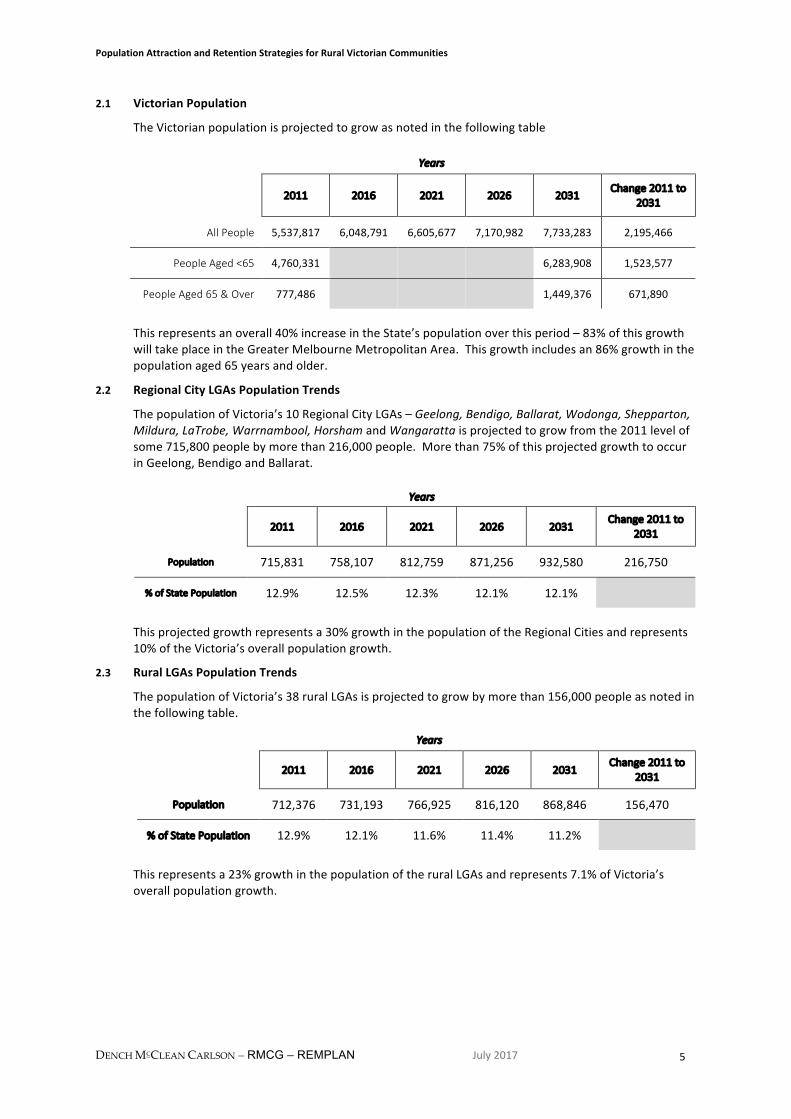

2.1 VictorianPopulation

TheVictorianpopulationisprojectedtogrowasnotedinthefollowingtable

Years

2011 2016 2021 2026 2031Change2011to

2031

AllPeople 5,537,817 6,048,791 6,605,677 7,170,982 7,733,283 2,195,466

PeopleAged<65 4,760,331 6,283,908 1,523,577

PeopleAged65&Over 777,486 1,449,376 671,890

Thisrepresentsanoverall40%increaseintheState’spopulationoverthisperiod–83%ofthisgrowthwilltakeplaceintheGreaterMelbourneMetropolitanArea.Thisgrowthincludesan86%growthinthepopulationaged65yearsandolder.

2.2 RegionalCityLGAsPopulationTrends

ThepopulationofVictoria’s10RegionalCityLGAs–Geelong,Bendigo,Ballarat,Wodonga,Shepparton,Mildura,LaTrobe,Warrnambool,HorshamandWangarattaisprojectedtogrowfromthe2011levelofsome715,800peoplebymorethan216,000people.Morethan75%ofthisprojectedgrowthtooccurinGeelong,BendigoandBallarat.

Years

2011 2016 2021 2026 2031Change2011to

2031

Population 715,831 758,107 812,759 871,256 932,580 216,750

%ofStatePopulation 12.9% 12.5% 12.3% 12.1% 12.1%

Thisprojectedgrowthrepresentsa30%growthinthepopulationoftheRegionalCitiesandrepresents10%oftheVictoria’soverallpopulationgrowth.

2.3 RuralLGAsPopulationTrends

ThepopulationofVictoria’s38ruralLGAsisprojectedtogrowbymorethan156,000peopleasnotedinthefollowingtable.

Years

2011 2016 2021 2026 2031Change2011to

2031

Population 712,376 731,193 766,925 816,120 868,846 156,470

%ofStatePopulation 12.9% 12.1% 11.6% 11.4% 11.2%

Thisrepresentsa23%growthinthepopulationoftheruralLGAsandrepresents7.1%ofVictoria’soverallpopulationgrowth.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 6

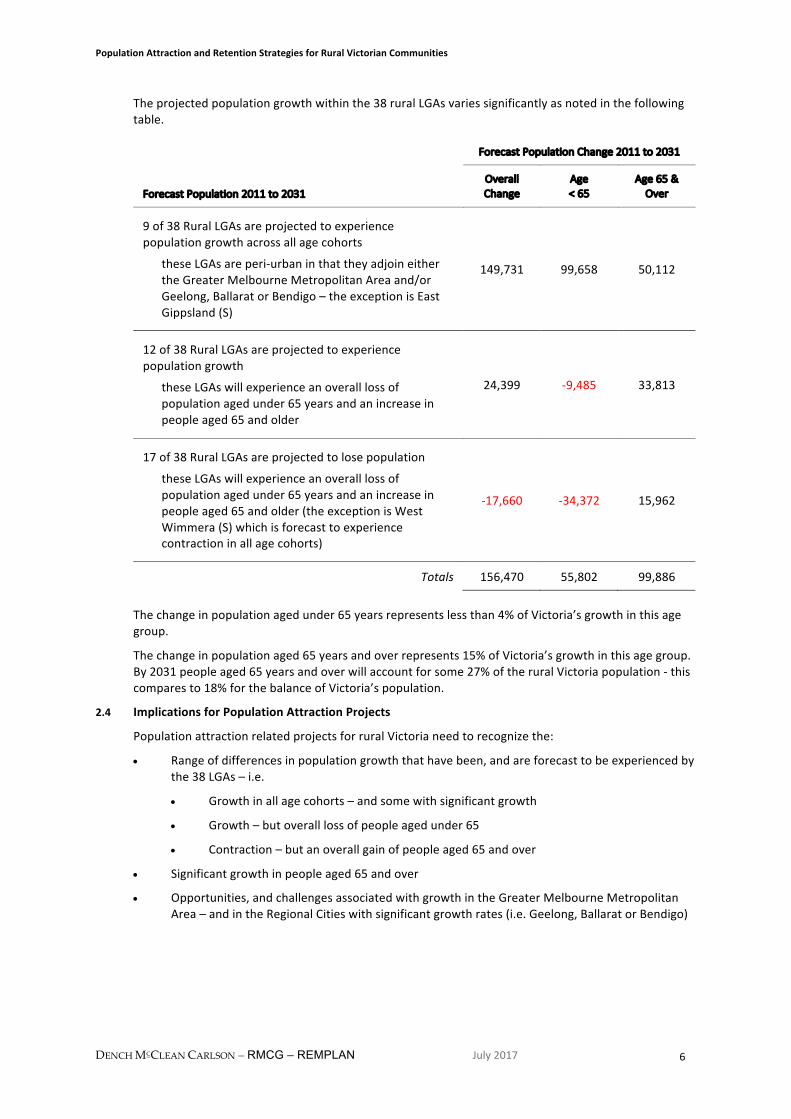

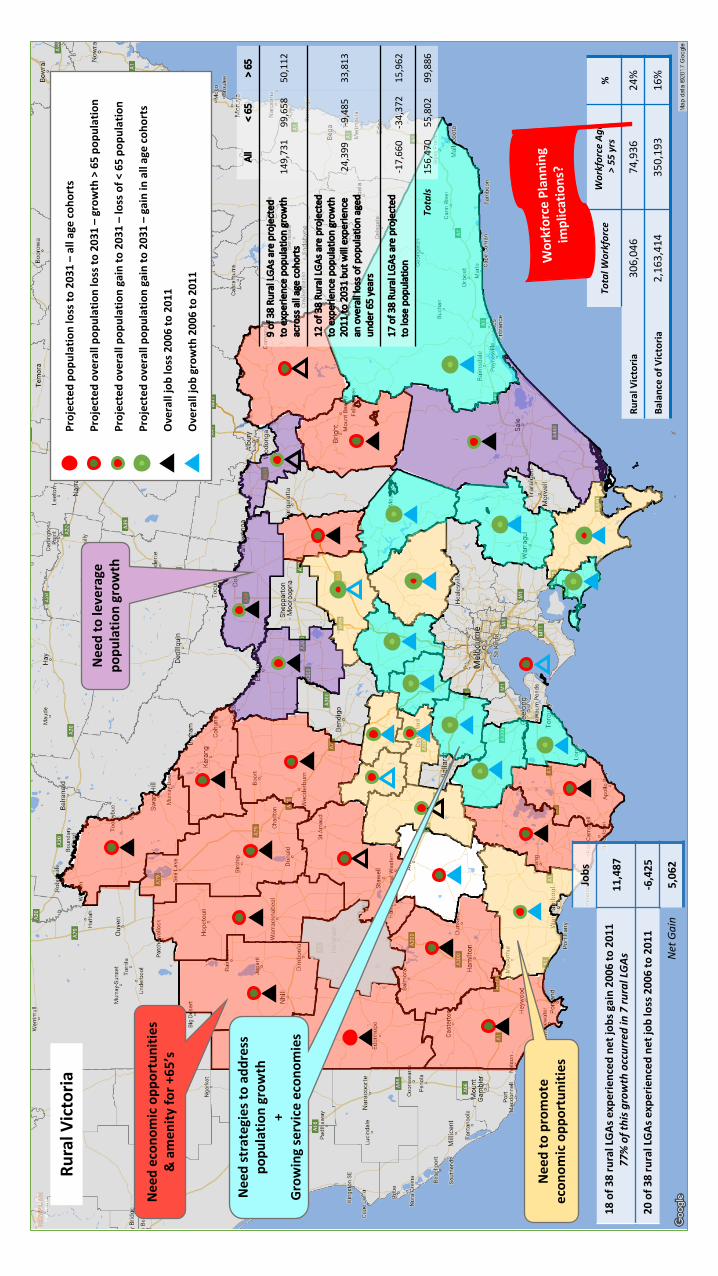

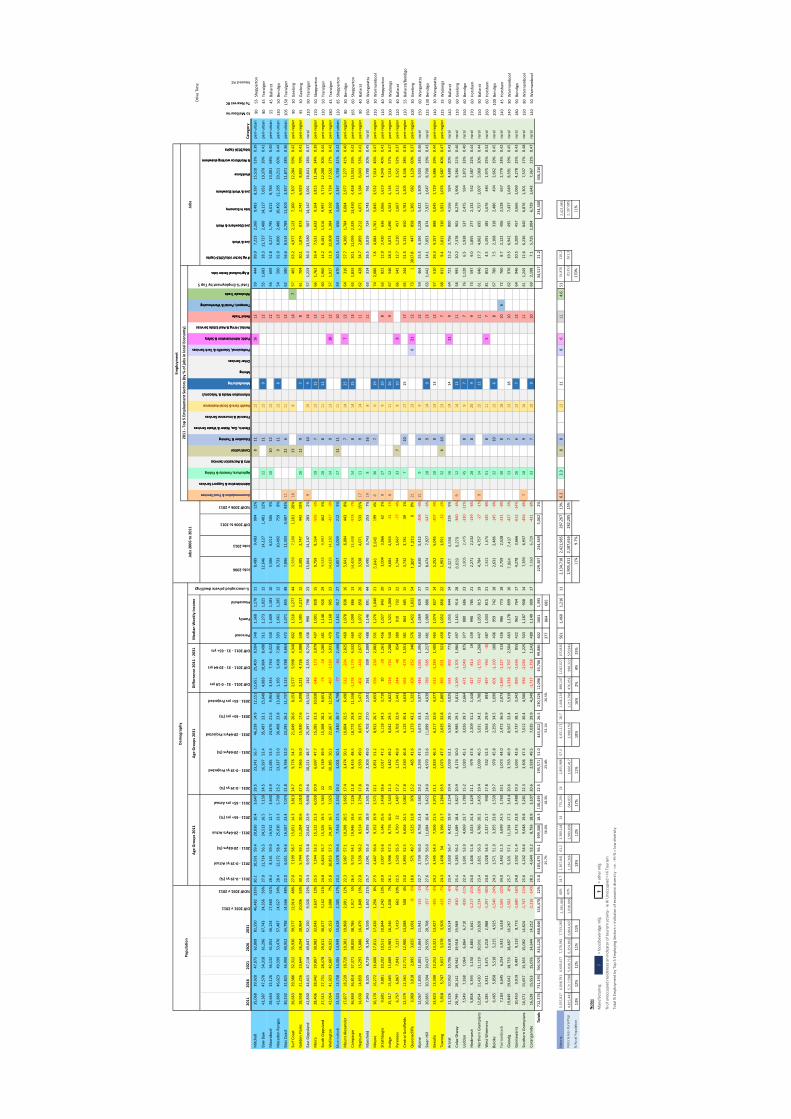

Theprojectedpopulationgrowthwithinthe38ruralLGAsvariessignificantlyasnotedinthefollowingtable.

ForecastPopulationChange2011to2031

ForecastPopulation2011to2031OverallChange

Age<65

Age65&Over

9of38RuralLGAsareprojectedtoexperiencepopulationgrowthacrossallagecohorts

theseLGAsareperi-urbaninthattheyadjoineithertheGreaterMelbourneMetropolitanAreaand/orGeelong,BallaratorBendigo–theexceptionisEastGippsland(S)

149,731 99,658 50,112

12of38RuralLGAsareprojectedtoexperiencepopulationgrowth

theseLGAswillexperienceanoveralllossofpopulationagedunder65yearsandanincreaseinpeopleaged65andolder

24,399 -9,485 33,813

17of38RuralLGAsareprojectedtolosepopulation

theseLGAswillexperienceanoveralllossofpopulationagedunder65yearsandanincreaseinpeopleaged65andolder(theexceptionisWestWimmera(S)whichisforecasttoexperiencecontractioninallagecohorts)

-17,660 -34,372 15,962

Totals 156,470 55,802 99,886

Thechangeinpopulationagedunder65yearsrepresentslessthan4%ofVictoria’sgrowthinthisagegroup.

Thechangeinpopulationaged65yearsandoverrepresents15%ofVictoria’sgrowthinthisagegroup.By2031peopleaged65yearsandoverwillaccountforsome27%oftheruralVictoriapopulation-thiscomparesto18%forthebalanceofVictoria’spopulation.

2.4 ImplicationsforPopulationAttractionProjects

PopulationattractionrelatedprojectsforruralVictorianeedtorecognizethe:

• Rangeofdifferencesinpopulationgrowththathavebeen,andareforecasttobeexperiencedbythe38LGAs–i.e.

• Growthinallagecohorts–andsomewithsignificantgrowth

• Growth–butoveralllossofpeopleagedunder65

• Contraction–butanoverallgainofpeopleaged65andover

• Significantgrowthinpeopleaged65andover

• Opportunities,andchallengesassociatedwithgrowthintheGreaterMelbourneMetropolitanArea–andintheRegionalCitieswithsignificantgrowthrates(i.e.Geelong,BallaratorBendigo)

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 7

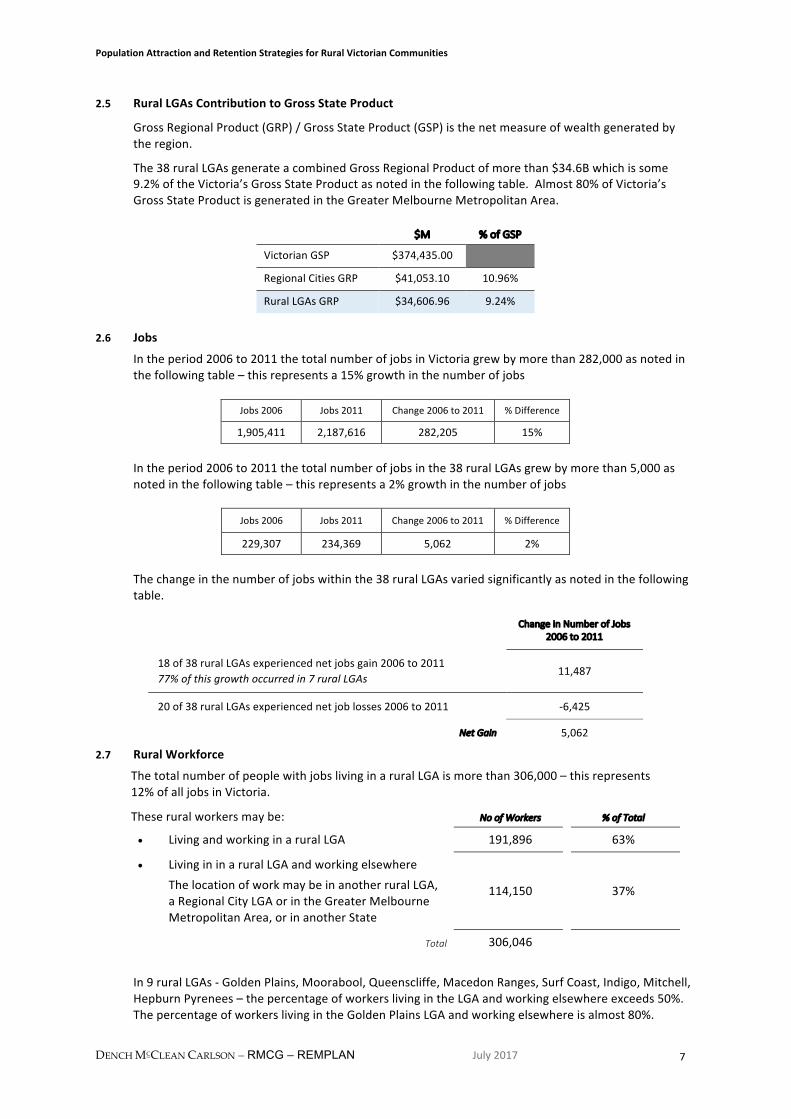

2.5 RuralLGAsContributiontoGrossStateProduct

GrossRegionalProduct(GRP)/GrossStateProduct(GSP)isthenetmeasureofwealthgeneratedbytheregion.

The38ruralLGAsgenerateacombinedGrossRegionalProductofmorethan$34.6Bwhichissome9.2%oftheVictoria’sGrossStateProductasnotedinthefollowingtable.Almost80%ofVictoria’sGrossStateProductisgeneratedintheGreaterMelbourneMetropolitanArea.

$M %ofGSP

VictorianGSP $374,435.00

RegionalCitiesGRP $41,053.10 10.96%

RuralLGAsGRP $34,606.96 9.24%

2.6 Jobs

Intheperiod2006to2011thetotalnumberofjobsinVictoriagrewbymorethan282,000asnotedinthefollowingtable–thisrepresentsa15%growthinthenumberofjobs

Jobs2006 Jobs2011 Change2006to2011 %Difference

1,905,411 2,187,616 282,205 15%

Intheperiod2006to2011thetotalnumberofjobsinthe38ruralLGAsgrewbymorethan5,000asnotedinthefollowingtable–thisrepresentsa2%growthinthenumberofjobs

Jobs2006 Jobs2011 Change2006to2011 %Difference

229,307 234,369 5,062 2%

Thechangeinthenumberofjobswithinthe38ruralLGAsvariedsignificantlyasnotedinthefollowingtable.

ChangeinNumberofJobs2006to2011

18of38ruralLGAsexperiencednetjobsgain2006to201177%ofthisgrowthoccurredin7ruralLGAs

11,487

20of38ruralLGAsexperiencednetjoblosses2006to2011 -6,425

NetGain 5,062

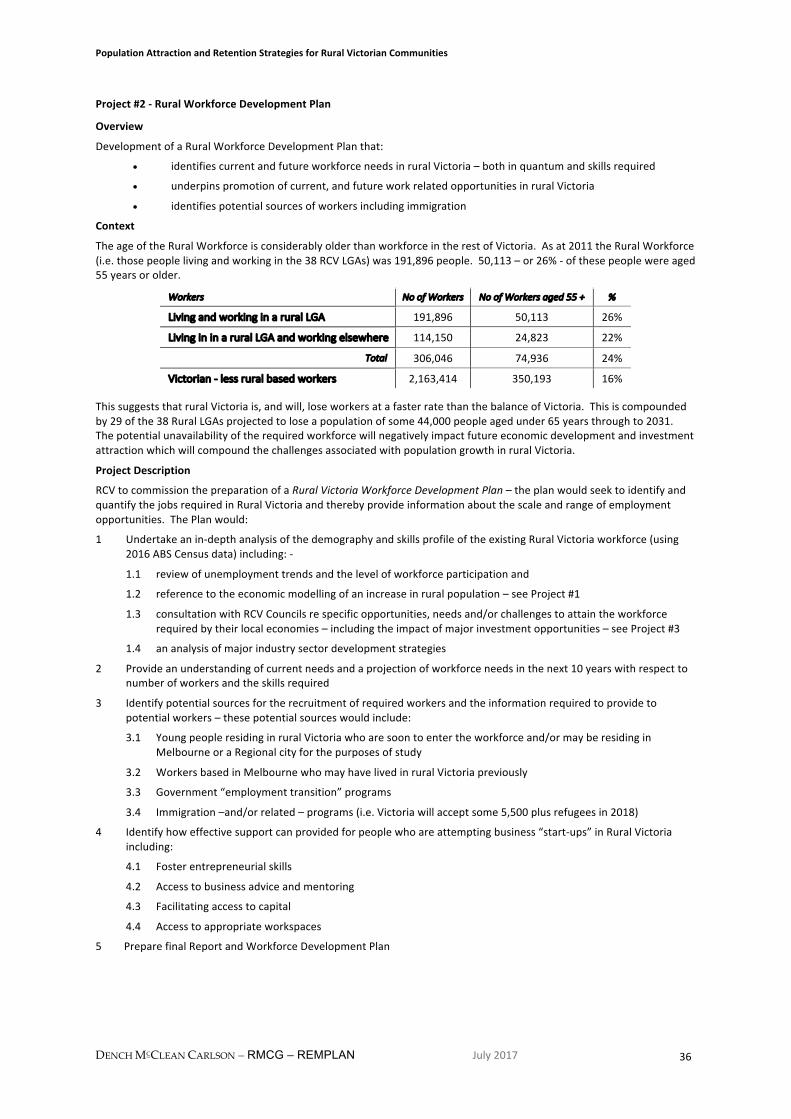

2.7 RuralWorkforce

ThetotalnumberofpeoplewithjobslivinginaruralLGAismorethan306,000–thisrepresents12%ofalljobsinVictoria.

Theseruralworkersmaybe: NoofWorkers %ofTotal

• LivingandworkinginaruralLGA 191,896 63%

• LivingininaruralLGAandworkingelsewhereThelocationofworkmaybeinanotherruralLGA,aRegionalCityLGAorintheGreaterMelbourneMetropolitanArea,orinanotherState

114,150 37%

Total 306,046

In9ruralLGAs-GoldenPlains,Moorabool,Queenscliffe,MacedonRanges,SurfCoast,Indigo,Mitchell,HepburnPyrenees–thepercentageofworkerslivingintheLGAandworkingelsewhereexceeds50%.ThepercentageofworkerslivingintheGoldenPlainsLGAandworkingelsewhereisalmost80%.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 8

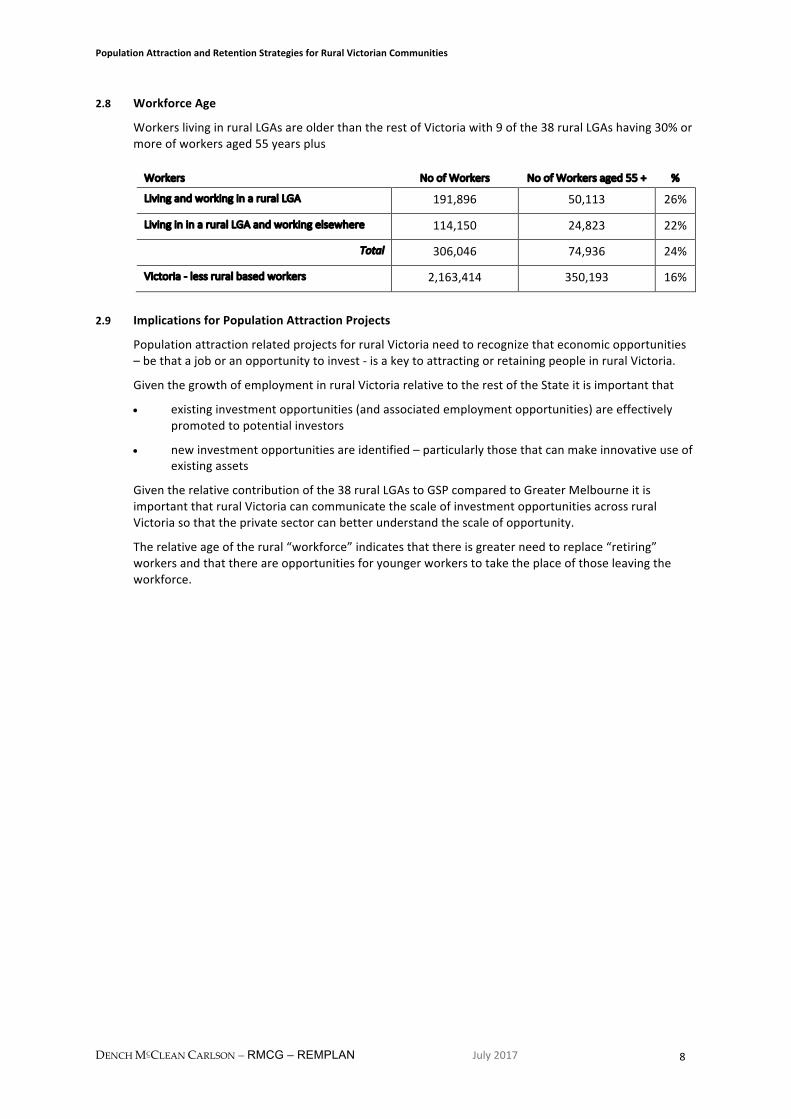

2.8 WorkforceAge

WorkerslivinginruralLGAsareolderthantherestofVictoriawith9ofthe38ruralLGAshaving30%ormoreofworkersaged55yearsplus

Workers NoofWorkers NoofWorkersaged55+ %

LivingandworkinginaruralLGA 191,896 50,113 26%

LivingininaruralLGAandworkingelsewhere 114,150 24,823 22%

Total 306,046 74,936 24%

Victoria-lessruralbasedworkers 2,163,414 350,193 16%

2.9 ImplicationsforPopulationAttractionProjects

PopulationattractionrelatedprojectsforruralVictorianeedtorecognizethateconomicopportunities–bethatajoboranopportunitytoinvest-isakeytoattractingorretainingpeopleinruralVictoria.

GiventhegrowthofemploymentinruralVictoriarelativetotherestoftheStateitisimportantthat

• existinginvestmentopportunities(andassociatedemploymentopportunities)areeffectivelypromotedtopotentialinvestors

• newinvestmentopportunitiesareidentified–particularlythosethatcanmakeinnovativeuseofexistingassets

Giventherelativecontributionofthe38ruralLGAstoGSPcomparedtoGreaterMelbourneitisimportantthatruralVictoriacancommunicatethescaleofinvestmentopportunitiesacrossruralVictoriasothattheprivatesectorcanbetterunderstandthescaleofopportunity.

Therelativeageoftherural“workforce”indicatesthatthereisgreaterneedtoreplace“retiring”workersandthatthereareopportunitiesforyoungerworkerstotaketheplaceofthoseleavingtheworkforce.

RuralV

ictoria

Projectedpo

pulatio

nlossto

2031–allageco

horts

Projectedoverallpop

ulationlossto

2031–grow

th>65po

pulatio

n

Overalljobloss2006to2011

Projectedoverallpop

ulationgainto

2031–lossof<

65po

pulatio

n

Overalljobgrow

th2006to2011

TotalW

orkforce

Workforce

Age

>55yrs

%

RuralV

ictoria

306,046

74,936

24%

BalanceofVictoria

2,163,414

350,193

16%

Projectedoverallpop

ulationgainto

2031–gainin

allagecoho

rts

Needecon

omicopp

ortunitie

s&amen

ityfo

r+65

’s

Needtoleverage

popu

latio

ngrow

th

Needtopromote

econ

omicopp

ortunitie

s

Needstrategiesto

add

ress

popu

latio

ngrow

th+

Grow

ingserviceecon

omies

Jobs

18of3

8ruralLGA

sexperienced

netjo

bsgain2006

to2011

77%ofthisg

rowthoccurredin7ru

ralLGA

s11,487

20of3

8ruralLGA

sexperienced

netjo

bloss2006to2011

-6,425

NetG

ain

5,062

All

<65

>65

9of38Ru

ralLGAsareprojected

toexperiencepo

pulatio

ngrow

th

acrossallagecoho

rts

149,731

99,658

50,112

12of3

8Ru

ralLGAsareprojected

toexperiencepo

pulatio

ngrow

th

2011to

2031bu

twillexperience

anoveralllossofp

opulationaged

un

der6

5years

24,399

-9,485

33,813

17of3

8Ru

ralLGAsareprojected

tolosepop

ulation

-17,660

-34,372

15,962

Totals

156,470

55,802

99,886

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 10

3 ReviewofPopulationAttractionApproachesinOtherRuralAreas

ThePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesprojecthasincludedareviewofpopulationattractionandretentionstrategiesandtheidentificationofpracticesthatcouldbeutilisedinruralVictoriatosupportpopulationattractionand/orretentionbeingundertakeninAustralia,theUSA,Canada,andScotland(95%ofScotlandisclassifiedasrural)

Thereviewinvolvedadesktopreviewofinformationfromrelevantwebsitesandphoneinterviewswith

• Governmentrepresentatives(bothStateandFederal)

• Universityrepresentatives

• NGOrepresentatives

3.1 USA

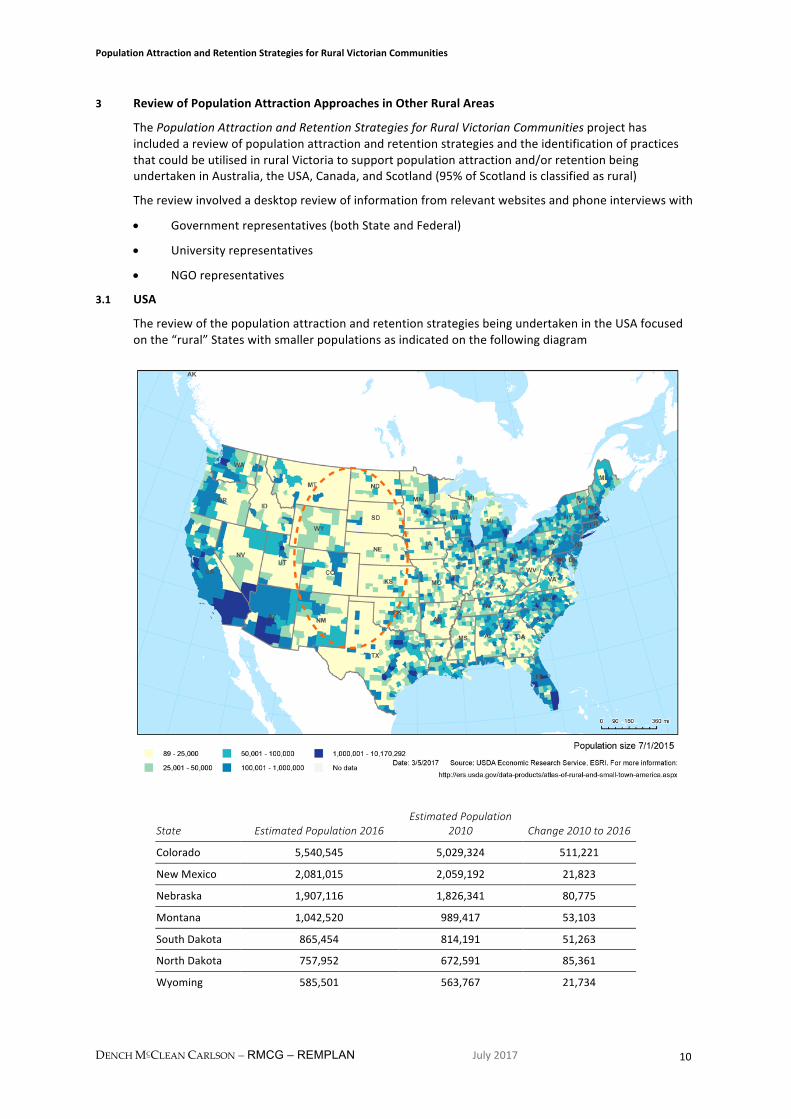

ThereviewofthepopulationattractionandretentionstrategiesbeingundertakenintheUSAfocusedonthe“rural”Stateswithsmallerpopulationsasindicatedonthefollowingdiagram

State EstimatedPopulation2016EstimatedPopulation

2010 Change2010to2016

Colorado 5,540,545 5,029,324 511,221

NewMexico 2,081,015 2,059,192 21,823

Nebraska 1,907,116 1,826,341 80,775

Montana 1,042,520 989,417 53,103

SouthDakota 865,454 814,191 51,263

NorthDakota 757,952 672,591 85,361

Wyoming 585,501 563,767 21,734

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 11

PopulationchangesinruralAmericamirrorthatoftheVictorian/Australianexperience

Thenumberofpeoplelivinginruralcountiesstoodatjustover46millionin2014—nearly15 percent of U.S. residents. However, the population of rural America has declined by116,000overthelast4years,withlossesofabout30,000peopleineachofthelast2years.Whilethesedeclinesaresmall,2010-2014isthefirstperiodofoverallpopulationdeclineonrecordforruralAmericaasawhole,andstandsinstarkcontrastwiththeurbanpopulation,which continues to grow by more than 2 million per year. Not all rural areas haveexperienced population loss in recent years. Some rural counties have seen populationgrowth, with nearly 700 growing rural counties together adding over 400,000 residentsbetween2010and2014.ThesecountiesareconcentratedinscenicareassuchastheRockyMountainsorsouthernAppalachia,orinenergyboomregionssuchasinthenorthernGreatPlains. The 1,300 rural counties losing population since 2010 are widespread in regionsdependentonfarming,manufacturing,orresourceextraction.

USDepartmentofAgriculture–RuralDevelopment

3.1.1 OverviewofFindings

Therewerenodedicatedpopulationattractionstrategies/policiesinplace.Thereiswiderecognitionthatmanyruralcommunitiesneedsupportwithrespecttoretaining/attractingpeople.

Ruralcommunities/businesseshaveaccesstoarangeofGovernmentdevelopmentprograms,fundingprogramsand/orlow/nointerestloans

ArangeofCommunityDevelopmentOrganisations(CDOs)supportruralcommunitiesparticularlywithrespecttohousing–manyCDOsare:

• providingcommunityeconomicdevelopmentprogramsaimedathelpingtoidentifyandleverageassetsthatcouldattractinvestment

• alsoCommunityDevelopmentFinancialInstitution(CDFI)whichprovidelowinterestfinancingforcommunitiesand/orbusinesses–oftenfinancingiscontingentuponacommunityhavingundertakenacommunityeconomicdevelopmentprocess

3.1.2 PopulationAttractionStrategies

Therewerenospecificpopulationattractionstrategiesbutpopulationgrowthwasadesiredoutcomeofbroaderstrategies/programsbeingundertaken.

3.1.3 USDepartmentofAgriculture–RuralDevelopment

https://www.rd.usda.gov/

Focus-helpingimprovetheeconomyandqualityoflifeinruralAmericatosupportviabilityofagriculturesector

ThekeymechanismsemployedbyUSDARDtoachievethisare:

• providingloans,grantsandloanguaranteestosupportessentialservicessuchashousing,economicdevelopment,healthcare,firstresponderservicesandequipment,andwater,electricandcommunicationsinfrastructure.

• promotingeconomicdevelopmentbysupportingloanstobusinessesthroughbanks,creditunionsandcommunity-managedlendingpools.

• providingtechnicalassistance(i.e.consulting)andinformationtohelpagriculturalproducersandcooperativesgetstartedandimprovetheeffectivenessoftheiroperations.

• providingtechnicalassistance(i.e.consulting)tohelpcommunitiesundertakecommunityempowermentprograms.helpruralresidentsbuyorrentsafe,affordablehousingandmakehealthandsafetyrepairstotheirhomes.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 12

USDAR’skeyprogramareasaresummarizedinthefollowingdiagram

loans,grantsandloanguarantees

Æ

Æ

Æ

Æ

Starting/improvedeffectivenessoftheoperationofagriculturalproducersandcooperatives

Businessstart-ups/growth–basedinruralcommunities

Communityinfrastructure/services

Housing

Communityeconomicdevelopment

and/or

technicalassistanceand/orinformation

3.1.4 RuralLISC

http://programs.lisc.org/rural_lisc/

TheLocalInitiativesSupportCorporation,knownasLISC,commencedin1980andisoneofthelargestNFPorganizationsintheUSAsupportingprojectstorevitalizecommunities.Theseincludemoreaffordablehousing,betterschools,saferstreets,growingbusinessesandprogramsimprovingfinancialstability.

LISC’spurposeasanon-profit*CommunityDevelopmentFinancialInstitution(CDFI)istoprovidecapitaltoprojectsinlow-income,disadvantagedandunderservedcommunitiesataffordablerates.LISCoffersthiscapitaltolocalnonprofitdevelopers,smallbusinessesandotherserviceproviderswhomaynotbeabletogetcreditintheconventionalmarketplace.LISCreceivesinvestmentcapitalfromarangeofsourcesthatincludealllevelsofgovernment,foundations,banks-todateLISChasprovidedmorethan$16.2B.

LISClaunchedRuralLISCin1995toexpanditsreachbeyondurbanareastoincluderuralcommunities.RuralLISCpartnerswith76communitydevelopmentorganizations,includingfourfinancialintermediariesworkingtotransformcommunitiesin1,973countiesacross44states.

RuralLISC'sstrategiesfollowthefivegoalsofLISC'sBuildingSustainableCommunitiesmodel:

• ExpandingInvestmentinHousingandOtherRealEstate

• IncreasingFamilyIncomeandWealth

• StimulatingEconomicDevelopment

• ImprovingAccesstoQualityEducation

• SupportingHealthyEnvironmentsandLifestyles

LISCRuralnotesthat“RuralAmerica.-is3millionsquaremilesand71millionpeople.Itiscountryside,smalltowns,mountains,farmlandandcoastalshores.RuralAmericaispartandparcelofourentirecountry,anditmatters!Ruralcommunitieslackquality,affordablehousingandhealthcare.Theyarelosingjobsandlandtosuburbansprawl.Theydonotreceivethenecessarygovernmentfundingandsupporttoprovidedecenteducationandtransportationservices.Theyareoftenunabletokeepupwithtechnologyandthemainstreameconomy.

DespitetheimageofruralAmericaasafarm-driveneconomy,lessthanninepercentofruraljobsareinthecombinedfarming,agriculturalservices,forestryandfishingindustries.

Recognizingthatruralcommunities'needsarenotfocusedonagriculturealone,RuralLISCprovidesawiderangeofservices,includingtraining,technicalassistance,informationandfinancialsupport,tohelpruralcommunitydevelopersaddresstheproblemsruralcommunitiesface.”

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 13

RuralLISCstaffcollaboratewithCDCstohelpidentifyprioritiesandchallenges,deliveringthemostappropriatesupporttomeetlocalneeds.RuralLISCforgesalliancesamongruralorganizations,funders,lendersandpolicymakers,mobilizingcorporate,governmentandphilanthropicsupporttoprovideruralcommunitydevelopmentorganizationswith:

• loans,grantsandequityinvestments

• local,statewideandnationalpolicysupport

• technicalandmanagementassistance

3.1.4.1 LISCInstituteforComprehensiveCommunityDevelopment

http://www.instituteccd.org/About-us.html

LISChasestablishedtheLISCInstituteforComprehensiveCommunityDevelopmentservesLISCstaff,organizationsandindividualswhopartnerwithLISC,andothersworkinginurbanandruralcommunitiesacrossthecountrybyprovidingtrainingandinformationaboutbestpractices,ideasandnewsfromaroundthefieldofcomprehensivecommunitydevelopment.

3.1.5 NationalMainStreetCenter,Inc.

ManyruralcentersutilisetheMainStreetapproach.

http://www.mainstreet.org/main-street/about-main-street/main-street-america/the-main-street-approach.html

Establishedin1980asaprogramoftheNationalTrustforHistoricPreservation,theNationalMainStreetCenter,Inc.workswithanationwidenetworkofcoordinatingprogramsandlocalcommunitiestoencouragepreservation-basedcommunityrevitalization,andhasequippedmorethan2,000oldercommercialdistrictswiththeskills,andorganizingframeworktheyneedforrenewalduringits35-yearhistory.

TheNationalMainStreetCenter,Inc.notesthat“since1980,over2,000communitieshavebeenpartofMainStreet,bringingrenewedenergyandactivitytoAmerica’sdowntownsandcommercialdistricts,securing$65.6billioninnewinvestment,creatingmorethan556,000netnewjobs,andrehabilitating260,000buildings.

TheMainStreetApproachbeginswithcreatingavisionforsuccessonMainStreetthatisrootedinasolidunderstandingofthemarketrealitiesofthedistrict,andisinformedbybroadcommunityengagement.MainStreetpromotesacommunity-drivenprocessthatbringsdiversestakeholdersfromallsectorstogether,invitingthemtobeproactiveparticipantsintherevitalizationprocess.Thisessentialstepprovidesafoundationforoutliningthecommunity’sownidentity,expectations,andidealswhileconfirmingrealandperceivedperceptions,needsandopportunities.Italsoensuresthatthevisionisatruereflectionofthediversityofthecommunity.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 14

Avisionofsuccessaloneisnotenough.Communitiesmustworktogethertoidentifykeystrategies,knownasCommunityTransformationStrategiesthatwillprovideaclearsenseofprioritiesanddirectionfortherevitalizationefforts.Typically,communitieswillfindtwotothreeCommunityTransformationStrategiesareneededtohelpreachacommunityvision.Thesestrategieswillfocusonbothlongandshort-termactionsthatwillmoveacommunityclosertoachievingitsgoals.

3.1.6 MarketingHometownAmerica

ThisprogramhasbeendevelopedbytheUniversityofNebraska.Theprogramprovidessupportforruralcommunitiestobeabletoundertakeaprocesstoattractpeopletoliveinruraltownsthroughtheidentificationofdesired,andshared,outcomes,thekeyassetsthatcanbeleveragedandthekeychallengestobeaddressed.

Theprojectsthatcommunitieshaveundertakenvaryaccordingtotheneedsofthecommunityinvolved.

Theprocesshasbeendevelopedusingfeedbackfrompeoplewhoareconsideringmovingtoaruralcommunity.

http://viewer.zmags.com/publication/29de58a3-/29de58a3/1

3.1.7 CostAdvantages

MostoftheStatesprovideinformationregardingtheirrelativestandingtootherStateswithrespecttothecostsassociatedwithmovingbusinessestoand/oroperatingabusiness.

3.1.8 InvestmentReadiness

ManyofthefundingprogramsthatStateGovernmentprovidetosupportlocalgovernments/townsrequirethemtobe“investmentready”.Whiletherecanabeanumberoffactorsthatrelatetobeinginvestmentreadythecommonrequirementrelatestohaving

• aneconomicdevelopmentstrategywithidentifiedpriorities

• appropriatetownplanning/landuseplanningframeworksinplace.

TheStateGovernmentswillprovidefundingfortheusetechnicalexpertise/consultingsupporttofacilitateinvestmentreadiness.

3.1.9 ImplicationsforPopulationAttractionProjects

• Strongfocusoncommunityeconomicdevelopmentrelatedprocessesincluding:-

• communityengagement

• afocusoncommunitywellbeing

• theidentificationandbroadagreementofthekeyassetsthatcanbeleveragedtoengagetheprivatesectorandgrowthelocaleconomy

• Importanceofresearchaboutunderstandingprioritiesofpeopleconsideringmovingtoruraltowns

• Availabilityofaccessible/lowcostfinance

• Accesstotechnicalsupport

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 15

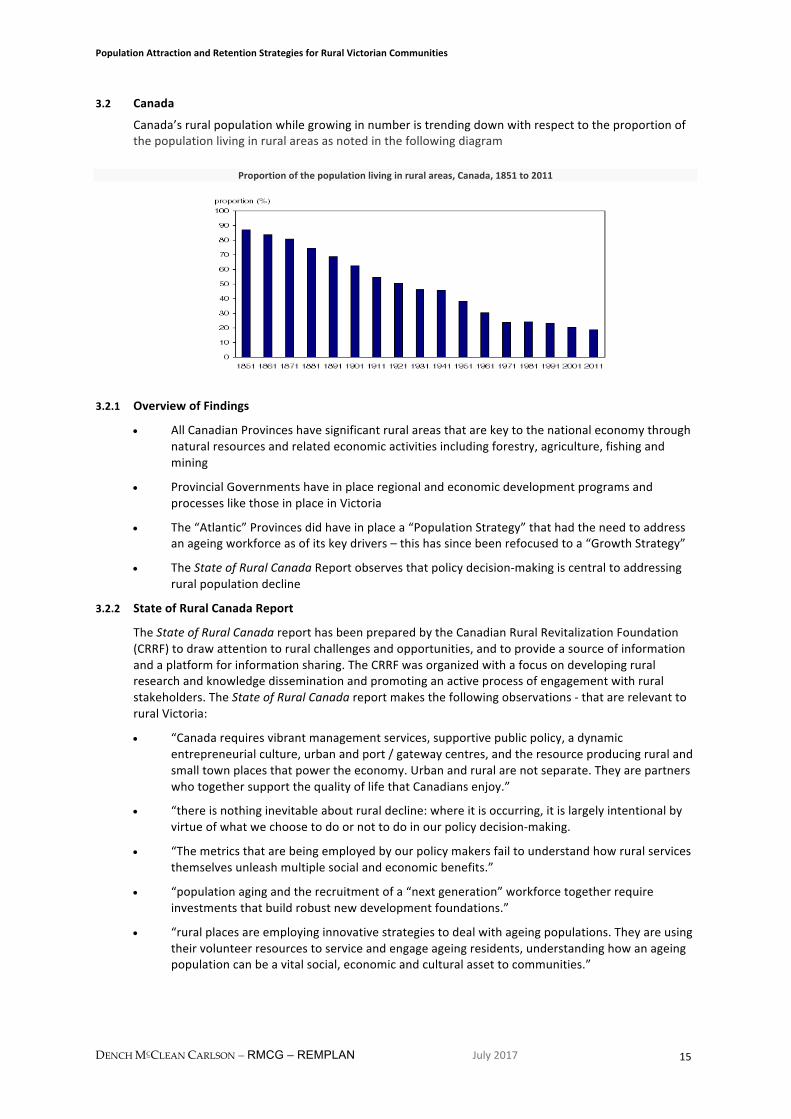

3.2 Canada

Canada’sruralpopulationwhilegrowinginnumberistrendingdownwithrespecttotheproportionofthepopulationlivinginruralareasasnotedinthefollowingdiagram

Proportionofthepopulationlivinginruralareas,Canada,1851to2011

3.2.1 OverviewofFindings

• AllCanadianProvinceshavesignificantruralareasthatarekeytothenationaleconomythroughnaturalresourcesandrelatedeconomicactivitiesincludingforestry,agriculture,fishingandmining

• ProvincialGovernmentshaveinplaceregionalandeconomicdevelopmentprogramsandprocesseslikethoseinplaceinVictoria

• The“Atlantic”Provincesdidhaveinplacea“PopulationStrategy”thathadtheneedtoaddressanageingworkforceasofitskeydrivers–thishassincebeenrefocusedtoa“GrowthStrategy”

• TheStateofRuralCanadaReportobservesthatpolicydecision-makingiscentraltoaddressingruralpopulationdecline

3.2.2 StateofRuralCanadaReport

TheStateofRuralCanadareporthasbeenpreparedbytheCanadianRuralRevitalizationFoundation(CRRF)todrawattentiontoruralchallengesandopportunities,andtoprovideasourceofinformationandaplatformforinformationsharing.TheCRRFwasorganizedwithafocusondevelopingruralresearchandknowledgedisseminationandpromotinganactiveprocessofengagementwithruralstakeholders.TheStateofRuralCanadareportmakesthefollowingobservations-thatarerelevanttoruralVictoria:

• “Canadarequiresvibrantmanagementservices,supportivepublicpolicy,adynamicentrepreneurialculture,urbanandport/gatewaycentres,andtheresourceproducingruralandsmalltownplacesthatpowertheeconomy.Urbanandruralarenotseparate.TheyarepartnerswhotogethersupportthequalityoflifethatCanadiansenjoy.”

• “thereisnothinginevitableaboutruraldecline:whereitisoccurring,itislargelyintentionalbyvirtueofwhatwechoosetodoornottodoinourpolicydecision-making.

• “Themetricsthatarebeingemployedbyourpolicymakersfailtounderstandhowruralservicesthemselvesunleashmultiplesocialandeconomicbenefits.”

• “populationagingandtherecruitmentofa“nextgeneration”workforcetogetherrequireinvestmentsthatbuildrobustnewdevelopmentfoundations.”

• “ruralplacesareemployinginnovativestrategiestodealwithageingpopulations.Theyareusingtheirvolunteerresourcestoserviceandengageageingresidents,understandinghowanageingpopulationcanbeavitalsocial,economicandculturalassettocommunities.”

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 16

• “InNewfoundland,weseethesuccessofengagingyoungentrepreneurstoaddress,inpart,localeconomicdecline.Whiletherearehurdlestoovercome,theiryouth-orientedentrepreneurshipprogramsarehelpingtorevitalizecommunityeconomiesandbuildimportantskillsforthefuture.

• “wearefacingacriticalwindowforsuccessionplanninginbusinessesacrossthecountry.

• “Ruralcommunitiesthemselvesmustbeactiveparticipantsinunderstanding,planningandinvestingintheirownfutures-AnecessaryshiftforruralCanadafromcasemaking(i.e.,repeatedlymakingthecasethatruralcommunitiesdeservemorehelpandattention),toplacemaking(i.e.,gettingonwiththetaskofplanningandbuildingcommunitieswithahighqualityoflifethatwillattractandretainbothresidentsandcapital).”

3.2.3 BritishColumbia

Nospecificpopulationattractionstrategy–focusonabroaderapproach–“onarisingtideallboatswillfloat”.TheProvincialGovernmentprovideswebsiteforeconomicdevelopmentwith“toolkits”andsuccessstoriesfromseveralsectors/locationsinBC.Manyofthesesuccessstoriesemphasizetheimportanceofcommunitiescomingtogethertoidentifyandagreekeypriorities

http://www2.gov.bc.ca/gov/content/employment-business/economic-development/success-stories

3.2.4 Alberta

Nospecificpopulationattractionstrategy.Alberta'sRegionalEconomicDevelopmentAlliances(REDAs)developedoutofaneedtostimulatelong-termeconomicdevelopmentandgrowthstrategiesinAlberta'sruralandurbancommunities.REDAsinAlbertaareautonomousgrassroots-basednon-profitorganizationscomprisedofmembercommunitiesandregionalstakeholdersthatworktogethertofosterbusinessdevelopmentandprosperityinadefinedgeographicarea.Thiscollaborationandcooperationenablesmembersandstakeholderstoundertakeprojectsthattheycouldnotnecessarilydoontheirown.

AreviewofREDAwebsitesnotesthatallhaveinformationregardingmovingtoand/orinvestingintheregion.Somesitesindicate“development”projectsbeingundertakenbytheREDA

http://communityeconomicdevelopment.alberta.ca/regional-economic-development-alliances-redas/

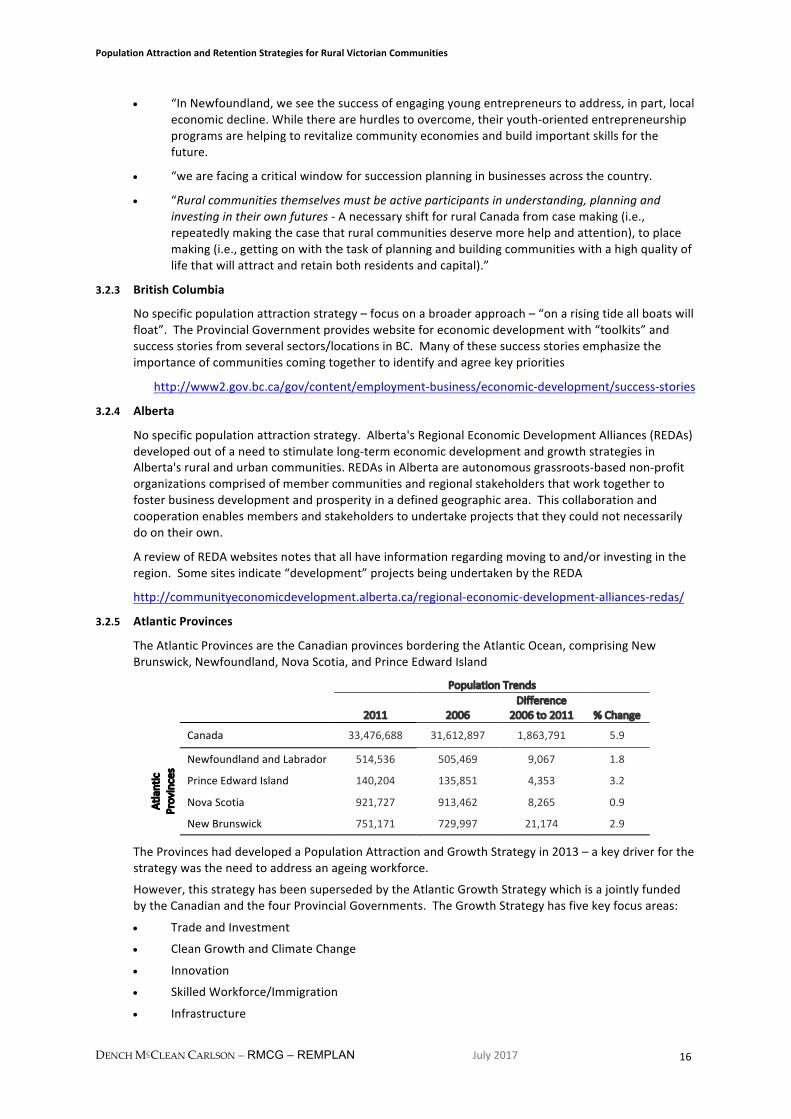

3.2.5 AtlanticProvinces

TheAtlanticProvincesaretheCanadianprovincesborderingtheAtlanticOcean,comprisingNewBrunswick,Newfoundland,NovaScotia,andPrinceEdwardIsland

PopulationTrends

2011 2006Difference

2006to2011 %Change Canada 33,476,688 31,612,897 1,863,791 5.9

Atlantic

Provinces

NewfoundlandandLabrador 514,536 505,469 9,067 1.8

PrinceEdwardIsland 140,204 135,851 4,353 3.2

NovaScotia 921,727 913,462 8,265 0.9

NewBrunswick 751,171 729,997 21,174 2.9

TheProvinceshaddevelopedaPopulationAttractionandGrowthStrategyin2013–akeydriverforthestrategywastheneedtoaddressanageingworkforce.

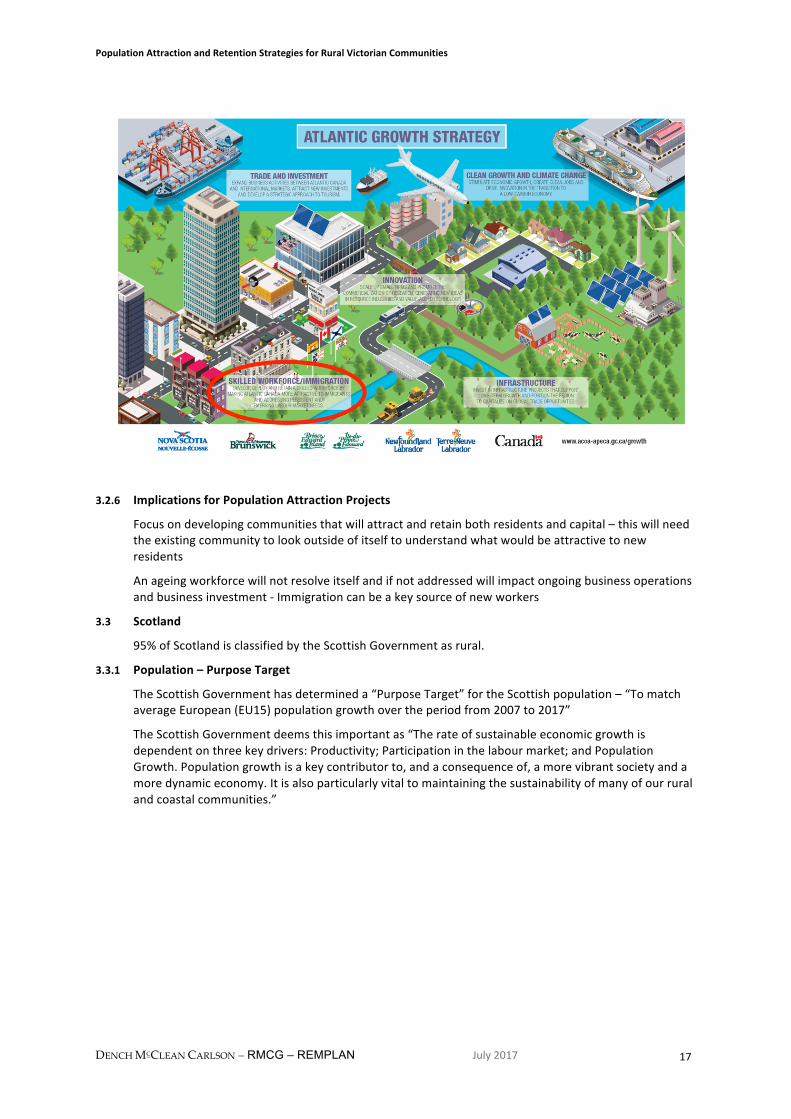

However,thisstrategyhasbeensupersededbytheAtlanticGrowthStrategywhichisajointlyfundedbytheCanadianandthefourProvincialGovernments.TheGrowthStrategyhasfivekeyfocusareas:

• TradeandInvestment

• CleanGrowthandClimateChange

• Innovation

• SkilledWorkforce/Immigration

• Infrastructure

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 17

3.2.6 ImplicationsforPopulationAttractionProjects

Focusondevelopingcommunitiesthatwillattractandretainbothresidentsandcapital–thiswillneedtheexistingcommunitytolookoutsideofitselftounderstandwhatwouldbeattractivetonewresidents

Anageingworkforcewillnotresolveitselfandifnotaddressedwillimpactongoingbusinessoperationsandbusinessinvestment-Immigrationcanbeakeysourceofnewworkers

3.3 Scotland

95%ofScotlandisclassifiedbytheScottishGovernmentasrural.

3.3.1 Population–PurposeTarget

TheScottishGovernmenthasdetermineda“PurposeTarget”fortheScottishpopulation–“TomatchaverageEuropean(EU15)populationgrowthovertheperiodfrom2007to2017”

TheScottishGovernmentdeemsthisimportantas“Therateofsustainableeconomicgrowthisdependentonthreekeydrivers:Productivity;Participationinthelabourmarket;andPopulationGrowth.Populationgrowthisakeycontributorto,andaconsequenceof,amorevibrantsocietyandamoredynamiceconomy.Itisalsoparticularlyvitaltomaintainingthesustainabilityofmanyofourruralandcoastalcommunities.”

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 18

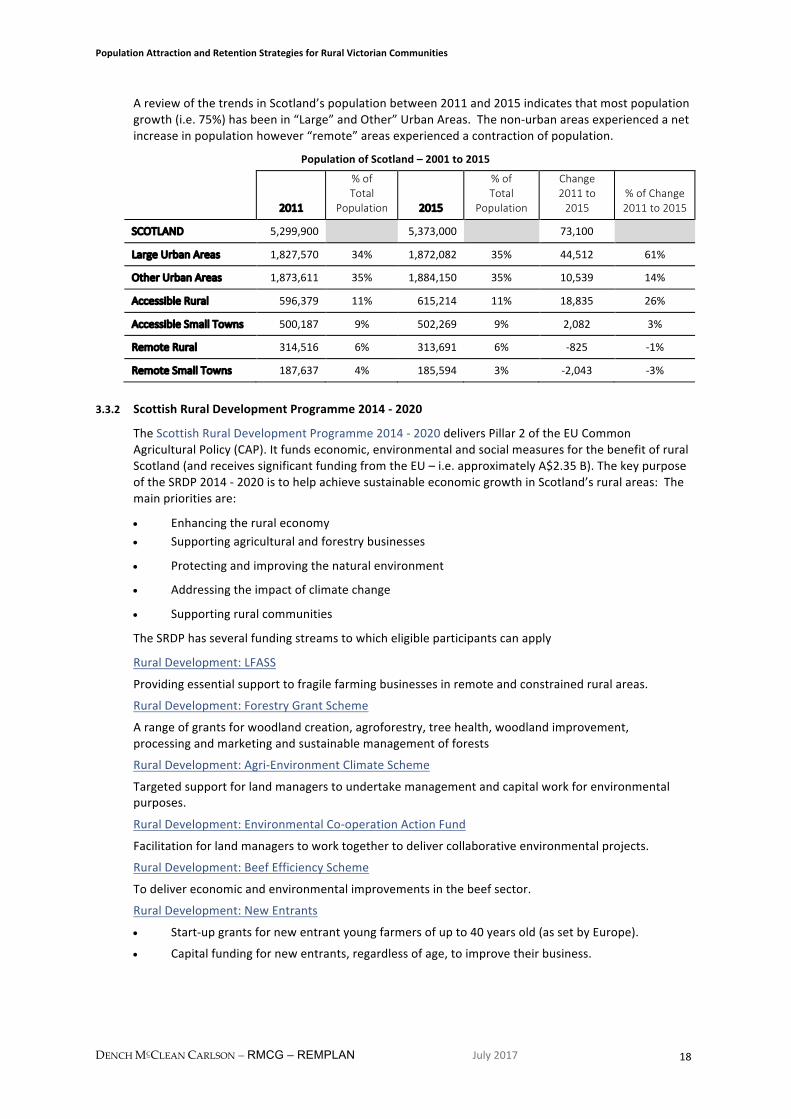

AreviewofthetrendsinScotland’spopulationbetween2011and2015indicatesthatmostpopulationgrowth(i.e.75%)hasbeenin“Large”andOther”UrbanAreas.Thenon-urbanareasexperiencedanetincreaseinpopulationhowever“remote”areasexperiencedacontractionofpopulation.

PopulationofScotland–2001to2015

2011

%ofTotal

Population 2015

%ofTotal

Population

Change2011to2015

%ofChange2011to2015

SCOTLAND 5,299,900 5,373,000 73,100

LargeUrbanAreas 1,827,570 34% 1,872,082 35% 44,512 61%

OtherUrbanAreas 1,873,611 35% 1,884,150 35% 10,539 14%

AccessibleRural 596,379 11% 615,214 11% 18,835 26%

AccessibleSmallTowns 500,187 9% 502,269 9% 2,082 3%

RemoteRural 314,516 6% 313,691 6% -825 -1%

RemoteSmallTowns 187,637 4% 185,594 3% -2,043 -3%

3.3.2 ScottishRuralDevelopmentProgramme2014-2020

TheScottishRuralDevelopmentProgramme2014-2020deliversPillar2oftheEUCommonAgriculturalPolicy(CAP).Itfundseconomic,environmentalandsocialmeasuresforthebenefitofruralScotland(andreceivessignificantfundingfromtheEU–i.e.approximatelyA$2.35B).ThekeypurposeoftheSRDP2014-2020istohelpachievesustainableeconomicgrowthinScotland’sruralareas:Themainprioritiesare:

• Enhancingtheruraleconomy• Supportingagriculturalandforestrybusinesses

• Protectingandimprovingthenaturalenvironment

• Addressingtheimpactofclimatechange

• Supportingruralcommunities

TheSRDPhasseveralfundingstreamstowhicheligibleparticipantscanapply

RuralDevelopment:LFASS

Providingessentialsupporttofragilefarmingbusinessesinremoteandconstrainedruralareas.

RuralDevelopment:ForestryGrantScheme

Arangeofgrantsforwoodlandcreation,agroforestry,treehealth,woodlandimprovement,processingandmarketingandsustainablemanagementofforests

RuralDevelopment:Agri-EnvironmentClimateScheme

Targetedsupportforlandmanagerstoundertakemanagementandcapitalworkforenvironmentalpurposes.

RuralDevelopment:EnvironmentalCo-operationActionFund

Facilitationforlandmanagerstoworktogethertodelivercollaborativeenvironmentalprojects.

RuralDevelopment:BeefEfficiencyScheme

Todelivereconomicandenvironmentalimprovementsinthebeefsector.

RuralDevelopment:NewEntrants

• Start-upgrantsfornewentrantyoungfarmersofupto40yearsold(assetbyEurope).

• Capitalfundingfornewentrants,regardlessofage,toimprovetheirbusiness.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 19

RuralDevelopment:CroftingAgriculturalGrantScheme

Grantsto*crofterstotakeforwardimprovementsontheircroftswhichwillhelptosustaintheirbusiness.

*Note-Acrofterisonewhohastenureanduseoftheland,typicallyasatenantfarmer,especiallyinruralareas

RuralDevelopment:FoodProcessing,MarketingandCo-operation

SupportforSMEsinthefoodanddrinksectorwithstart-upgrantsfornewenterprises,andbusinessdevelopmentgrants.

RuralDevelopment:SmallFarmsGrantScheme

Targetedsupportforsmallfarmsthatfacesimilarissuesascroftersregardingsustainability.

RuralDevelopment:KnowledgeTransferandInnovationFund(KITF)

Takingadvantageofstrongperformanceinresearchanddevelopmentandensuringthatthelearningfromhereandelsewherecanbetransferredtoonthegroundimprovement.KTIFwillassistinthesharingandimplementationofinnovativewaysofimprovingworkingpracticesalongwithcontinuingsupportforMonitorFarms.

RuralDevelopment:AdvisoryService

ExpandedAdvisoryServicewhichwillprovideadviceandassistancetofarmers,croftersandotherlandmanagers.Weareaimingforthistobeavailablefrom2016.

RuralDevelopment:Broadband

Supportforbroadbandprovisioninruralareas.

ScottishRuralNetwork

Supportingandpromotingruraldevelopmentthroughthesharingofideasandbestpractice.

3.3.3 LEADER

LEADERisabottom-upmethodofdeliveringsupporttocommunitiesforruraldevelopment–thisprogramrunsthroughouttheEU.TheaimofLEADERistoincreasesupporttolocalruralcommunityandbusinessnetworkstobuildknowledgeandskills,andencourageinnovationandcooperationtotacklelocaldevelopmentobjectives.GrantsareawardedbyLocalActionGroupstoprojectsthatsupportdeliveryofaLocalDevelopmentStrategy.LocalDevelopmentStrategiesincludeactionsthatwillallowindividuals,communitiesandbusinessesto:

• drivecommunityactiononclimatechange

• enhanceruralservicesandfacilities,includingtransportinitiatives

• enhancenatural/culturalheritage,tourismandleisure

• supportfoodanddrinkinitiatives(forexampleshortsupplychains,communityfood)

• buildco-operationwithotherLAGsinScotland,UKandEurope

• exchangelearningandknowledgewitheachother,realisetheirpotential,buildopportunitiesforall

3.3.4 ImplicationsforPopulationAttractionProjects

Recognitionoftheimportanceofpopulationgrowthtooveralleconomicgrowth

Involvementofcommunitiesinidentifying/developingrelevantsolutions

Accesstosignificantlevelsoffunding-programstargetedatspecificruralneeds/relatedsectors–includingsupportfornewentrants

Sharing/exchangeofknowledgeandlearnings

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 20

3.4 Australia

AreviewofprogramsandprocessinAustraliaidentifiesthattheCommonwealth,andallStateGovernmentsareattemptinginvariouswaystoaddressgrowthinregionalandruralareas.Thecommonthemeistheidentificationandprioritizationofprojectsthatareseentosupportimprovedeconomicand/orcommunityoutcomeswithinvariousregionsineachState.

TheonlyStatethathasaformal“populationattraction”strategyinplaceisTasmaniaincludingatargetforthelevelofpopulationtobeachieved.

3.4.1 CommonwealthGovernment

TheCommonwealthGovernmentsupportsregionalandruraldevelopmentthroughawiderangeofinitiativesacrossarangeofgovernmentdepartments.

RegionalAustraliaMinisterialTaskforce

TheRegionalAustraliaMinisterialTaskforcechairedbythePrimeMinisterwillaimtoimprovethelivesofrural,regionalandremoteAustralians.Itwillcomeupwithideasacrossportfoliosincludinghealth,education,transportandinfrastructure,employment,industryandcommunications.

Regions2030

TheCommonwealthGovernmenthasrecentlyreleaseditsRegions2030policywhichbringtogetherexistingandnewfundingprogramsaimedatsupportgrowthinregionalandruralAustraliawithafocusonthefollowingareas:

• Jobsandeconomicdevelopment

• Infrastructure

• Health

• Education

• Communications

DepartmentofInfrastructureandRegionalDevelopment

TheDepartmentprovides:

• arangeofprograms“whicharefundedundertheInfrastructureInvestmentProgrammeaswellastheRegionalandCommunityProgrammes.Additionalfundingassistanceisalsoofferedforlocalroads.”–notalloftheseprogramsareavailabletoruralVictoria

• adviceandassistancetodepartmentsandagenciescompletingRegionalAustraliaImpactStatements(RAIS)aspartofthepolicydevelopmentandCabinetsubmissionprocess

DecentralisationofGovernmentDepartments

MorerecentlytheMinisterforInfrastructureandRegionalDevelopmenthasrequiredallMinsterstoprovideinformationregardingthepotentialtomovemajorcity-baseddepartmentsandagenciesintoregionalAustralia.Thisinformationwillbeusedtodevelopbusinesscasesforsuchmovementbylate2017

CommunityDevelopmentFinancialInstitutions(CDFI)PilotProject

TheAustraliaGovernmentnotedtheworkofCommunityDevelopmentFinancialInstitutions(CDFI)intheUSAandUK–seeSection3.1.4.

In2014,theAustralianGovernment–throughtheDepartmentofSocialServices-undertookaCommunityDevelopmentFinancialInstitutions(CDFI)PilotProject–TheCDFIpilotprojectsoughtto“buildthecapacityandresilienceofdisadvantagedandfinanciallyexcludedindividualsbyattractinginvestmentandinjectingfundsintocommunityfinanceorganisationsthatofferthemfinancialservicesandproductsthattheywouldotherwisenotbeabletoaccessfrommainstreamsources.”

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 21

Theevaluationofthepilotrecommendedthatoneoftherecommendationsarisingfromanevaluationofthepilotwasto“Extendthepilotforafurtherthreeyears.ThiswouldallowtimetoconductamorethoroughanalysisofthelongitudinalimpactsofCDFIsonfinancialexclusion.ItwouldalsofacilitatethedevelopmentofaCDFIsectorinAustralia”thefullevaluationcanbefoundathttps://www.dss.gov.au/sites/default/files/documents/02_2013/cdfi_evaluation_report_0.pdf

3.4.2 Queensland

EconomicDevelopmentQueensland(EDQ)hasestablishedtheAdvancingOurCitiesandRegionsStrategy.EDQnotesthatthe“Advancingourcitiesandregionsstrategyisaninnovativeapproachtorenewingandrepurposingsurplusandunderutilisedstatepropertytodeliverbettercommunityoutcomes,createjobsanddriveeconomicgrowth.

http://www.edq.qld.gov.au/infrastructure/advancing-our-cities-and-regions-strategy.html

PropertyQueenslandwithintheDepartmentofStateDevelopmentisworkingwithgovernmentland-owningagenciestoidentifysitesthatrepresentpropertyopportunitiesthatwilldeliverongovernmentpriorities, andgenerateeconomicdevelopmentandcommunityoutcomes.

Tohelpachievethisstrategy,eighteconomicandcommunityzoneshavebeenidentifiedwhereEconomicDevelopmentQueensland(EDQ)willleadthedeliveryofarangeofprojects,manyofwhichwillbeiconicdevelopmentstotransformprecinctsandcatalyseeconomicgrowthanddiversificationinourcitiesandregions.”

Developmentswillneedtodeliverstrongcommunitybenefits,meetbroadergovernmentprioritiessuchasinnovation,affordablehousingandexpandedtourism,andwillinvolveengagementwithlocalgovernments,thecommunity,stakeholdersandindustry.

NewprojectswillalsobuildonEDQ'sexistingdevelopmentportfolioofcommunity,residential,urbanrenewalandindustrialdevelopmentsandprovideadditionalincomeforreinvestmentinfutureinfrastructureprojects.

ProjectsofNote

AgeinginPlacepilotprojecthttp://www.edq.qld.gov.au/infrastructure/ageing-in-place-pilot-project.html

TheAgeinginPlacepilotprojectisaboutcaringforpeopleastheyentertheirsenioryearsbyprovidingsuitablehousingoptionstoenablepeopletostayintheirtowns,closetofriendsandfamily.Theprojectwillenhanceregionalliveabilityandsupportsustainabilityinlocalcommunitieswherethereisashortfallindwellingssuitableforolderpeople.OftenresidentsinmoreremoteorregionaltownsthroughoutQueenslandareconfrontedwiththedifficultdecisiontomovetoabiggercentrebecauseofalackofappropriateaccommodationintheirowncommunities.

IndustrialIncubator

Conceptistoprovidefacilitiestosupportstart-up“industrial”businesses–i.e.tradeservices,constructionetc.inruralcentres

3.4.3 NewSouthWales

TheNSWGovernmenthasestablishedtheRegionalDevelopmentFramework:whichhasthefollowingkeyareasoffocus:-

Program1:providingqualityservicesandinfrastructureinregionalNSW

Program2:aligningefforttosupportgrowingregionalcentres

Program3:identifyingandactivatingeconomicpotential

http://www.industry.nsw.gov.au/invest-in-nsw/regional-opportunities/regional-development-framework

TheprocessforidentifyingregionalprioritiesinNSWisyettobeimplemented.TheRegionalLeadershipGroupwillbecomethecoredecisionmakinggroupforeachregion.Itwillconsistofwillincludethe“rightpeoplefromeachagencyinvolvedinon-the-groundregionaldeliveryaswellasrepresentatives

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 22

fromJointOrganisationsand/orRegionalOrganisationsofCouncils,andtherelevantRegionalParliamentarySecretary.TheRegionalLeadershipGroupwillagreeontheprioritiesforeachregion

TheimplementationoftheRegionalDevelopmentFrameworkwillbesupportedby

TheRegionalEnablersProject

TheRegionalEnablersProjectseekstoidentifythekeyeconomicdriversforregionssothatinvestmentscanbetargetedtothosesectors.ThisprojecthasalreadybeenpilotedinthreeregionsandisbeingrolledoutacrosstheState.

TheRegionalEconomicOpportunitiesandInfrastructurePrioritiesProject

TheRegionalEconomicOpportunitiesandInfrastructurePrioritisationProjectwillinvolveacomprehensiveliteraturereviewofproposalsfromalllevelsofgovernmentandnon-governmentorganisations,andtargetedstakeholderengagementtoidentifythekeyeconomicopportunitiesandbarriersinregionalNSW.TheprojectwillapplymodellingtoprioritiseprojectssothatinformationcaninformtheworkofInfrastructureNSW.

EnhancingCostBenefitAnalysis

TheDepartmentofIndustryislookingatwaysofenhancingitscostbenefitanalysistoensurethatestimatesareaccurate,reliableandbasedoncomprehensiveinformation.Thiswillinvolvetakingintoconsiderationnon-marketbenefitsandcommercialassessmentsofflowonprospects.Inusingthismethodology,itisexpectedthatresourceswillbemoreefficientlyallocatedtoactivitieswiththebestlongtermbenefitsforregionalcommunitiesandtheState.

3.4.3.1 Evocities

Thisisacollaborationofsevenregionalcitiestopromotetheadvantagesofliving/investinginaregionalcity.TheEvoCitieswebsitesnotesthatthe“campaignaimstochangeperceptionsoflifeinaregionalcityandencouragepeopletolive,workandinvestinanEvoCity.ItshowcasestheabundanceofopportunitiesintheEvocitiesduetotheirlowercostofliving,strongcareerandbusinessopportunitiesandenhancedlifestyle.

3.4.3.2 BalranaldShireCouncil

BalranaldShireCouncilhasproducedaresourceforPopulationAttractionandRetention–theresourceincludes:

StrategicLeverstoBuildingCapacityforPopulationAttractionandRetention–including:• EconomicDevelopmentLevers• SocialCapitalDevelopment

Levers• LiveabilityDevelopmentLevers

PopulationAttractionandRetentionStrategies–includingstrategiesfor:• AttractionandRetentionofImmigrationandMigrants• AttractionandRetentionofYouth• AttractionandRetentionofRetirees• AttractionandRetentionofHealthProfessionals• EmploymentGeneration

3.4.4 SouthAustralia

SAdoesnothaveapopulationattractionstrategy/goalforruralcommunities.Thefollowingfundingprogramswereofferedasinitiativestosupportruralcommunities

RegionalDevelopmentFund

ThereareseveralprogramsthathavebeensupportedundertheRegionalDevelopmentFund

FundmyIdea

TheCountryCabinet‘FundMyIdea’Programprovides$150,000perannumtosupportcommunitiesthathostCountryCabinetmeetings,forprojectproposalsthatwillassistthecommunitymeetitseconomicandsocialneeds.

Projectsarenominatedbyandvotedonbythegeneralpublic.

http://www.pir.sa.gov.au/regions/grants/regional_development_fund/country_cabinet_fund_my_idea_program

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 23

RegionalFoodInitiatives

TheRegionalFoodInitiativesProgramhascommitted$600,000overatwo-yearperiodbetween2014-16tosupportregionally-basedfoodorganisationstobuildastrongerregionalfoodpresenceinSouthAustralia

http://www.pir.sa.gov.au/regions/grants/regional_development_fund/regional_food_initiatives_program

MajorProjects

TheMajorProjectsProgramsupportsmajoreconomicprojectsdesignedtostrengthenregionalindustries,supportlocaleconomiesandopportunitiesthroughinvestmentinstrategicprojects.

http://www.pir.sa.gov.au/regions/grants/regional_development_fund/major_projects_program

CommunityInfrastructure

TheCommunityInfrastructureProgramsupportsinvestmentinregionalcommunitiestodeveloptheireconomicinfrastructureandgrowtheircapabilitiesasafoundationforfuturejobsandeconomicgrowth.

http://www.pir.sa.gov.au/regions/grants/regional_development_fund/community_infrastructure_program

SmallGrants

In2014-15theSmallGrantsProgramawardedover$1.29milliontosupportnewregionalemploymentandinvestmentopportunitieslinkedwithStateGovernmentpriorities.

http://www.pir.sa.gov.au/regions/grants/regional_development_fund/small_grants_program

SouthAustralianRiverMurraySustainabilityProgram

TheRiverMurrayiscentraltothesocialandeconomicstructureoftheSouthAustralianMurray-DarlingBasinregion.

Therivercorridorishometomorethan90,000peoplewhorelyontheprosperityoftheirlocalindustriestosustaintheircommunities.

Byworkingtodevelopmoreindustriesintheregionthatarelessdependentonwater,ourrivercommunitiesarebetterplacedtorespondandbemoreresilienttotheeffectsoffluctuatingwateravailabilityandfutureclimatechangechallenges.

SARMSishelpingto:

• buildstrongandsustainableirrigationcommunities

• securewaterresourcesneededforahealthyenvironmentandaprosperousstate

• boostregionalproductivityandhelprivercommunitiesadapttoafutureofreducedwateravailability.

http://pir.sa.gov.au/regions/sarms

IndustryParticipationpolicy

TheSouthAustralianIndustryParticipationPolicy(IPP)specifiesthatforallexpenditureabove$33,000,thegovernmentmustdetermineifthereisabusinessinthestateortheregionthatcandelivertheproductorservice.

www.industryadvocate.sa.gov.au/industry-participation-policy

3.4.5 WesternAustralia

WA’sDepartmentofRegionalDevelopmentadvisesthatthereisnoruralpopulationattractionstrategy.Thedepartmentpromotesandfacilitatestheeconomic,businessandsocialdevelopmentofnineregionsinWesternAustralia:

Kimberley

Pilbara

Gascoyne

MidWest

Wheatbelt

Peel

SouthWest

GreatSouthern

Goldfields-Esperance

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 24

MajorProjects

Theregionaldevelopmentorganizationforeachoftheabovehaveidentifiedarangeofmajorprojects–thesehavebeenclassifiedintothefollowingareasofstrategicfocus

• AboriginalInitiatives

• Agriculture

• Community&Culture

• EconomicDevelopment

• Education

• Health

• Housing

• Justice

• Parks,Wildlife&Environment

• Recreation&Sport

• Roads&Transport

• Tourism

• Water

Note-TheRegionsandMajorProjectslistedabovearelinkedtotherespectivewebpages

3.4.6 Tasmania

TheTasmanianGovernmenthasestablishedthePopulationGrowthStrategywhichaimstogrowthestate’spopulation,fromthecurrent515,000people,to650,000peopleby2050andhasasitsvisionforTasmaniatothebestplaceinthecountrytolive,work,investandraiseafamily.

TheTasmanianGovernmenthasobservedthat“Tasmaniahastheoldestandslowestgrowingpopulationinthecountry.Unlesswetakeactionnow,Tasmania’spopulationislikelytogointodeclineinthenextfourdecades.Adecliningpopulationwillresultinaslowingeconomy,fewerpeopleinourworkforcetosupportthoseunabletoworkandareducedcapacitytofundessentialservicessuchaseducationandhealth.”

TheStrategyhasthreekeyareasoffocus:

Objectives

Jobcreationandworkforcedevelopment

tofacilitatejobcreationandidentifycurrentandfutureemploymentopportunitiestoinforminvestmentineducationandtrainingandmigrationstrategies

KeyStrategies

Activelypursueinvestment,businessrelocationandjobcreation

Identifyandprojectcurrentandfutureemploymentopportunities

Investinrealskillsforrealjobs

Liveability tobuildandpromoteTasmania’sliveabilityandfosteraculturewhichisvibrant,inclusive,respectfulandsupportive

KeyStrategies

Retainourbestandbrightest

IncreaseengagementwiththeTasmaniandiasporaandencouragethemtoreturnhome

Activelypursueoverseasmigration

Increaseourshareofhumanitarianentrants

Increasenumbersofinternationalstudents

Migration toactivelypursueandfacilitateoverseasandinterstatemigrationaswellasencouragereturnoftheTasmaniandiaspora

KeyStrategies

Nurtureourvibrantcommunities

Supportfamiliestoachieveawork-lifebalance

AssistmigrantstosettleandfeelwelcomeinTasmania

Createinclusiveandsupportivecommunities

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 25

3.4.7 Victoria

Thereisnopolicywithrespecttopopulationattractiontoregional/ruralVictoria.AllregionshavecompletedaRegionalGrowthPlanthatidentifiedwherefuturepopulationgrowthcanbeaccommodatedandthedevelopmentrequiredtosupportpopulationgrowth.

RegionalPlans

RegionsinVictoriahavedevelopedregionalplansthathaveidentifieddevelopmentprioritiesfortheregion.Thevariousregionsallaspireregardinggrowth–therearenospecificpopulationtargetsespousedbysuchplans.

RegionalPartnerships

MorerecentlytheStateGovernmenthasintroducednineRegionalPartnershipsacrossregionalandruralVictoria.Thepartnershipsaimtoengagewithcommunitiesonprioritiesfortheirregion,buildingonexistingstrategiesandplans-harnessingthegoodideas,theenergyandthepassionoflocals.PrioritieswillbepresenteddirectlytotheVictorianGovernment’sRuralandRegionalMinisterialCommittee.

BarwonSouthWestRegion

TheBarwonSouthWest(BSW)RDACommitteehasundertakenthedevelopmentofastudythatseekstoidentifyhowtheregioncanattractmorepeopletoresideand/orinvestintheBSWregion–thestudyidentified:

• asummaryofpopulationinfluences,drivers,attractorsandbarriersinthecontextofregionalVictoriaandtheBarwonSouthWest.ThesefallwithinfourkeyareasofLifestyle,Economic,Environment,andConnections

LIFESTYLE ECONOMICINFLUENCE/TRENDS Ageing agricultural workforce Ageing population - need for health services

DRIVERS Regional centre services Diverse range of services

INFLUENCE/TRENDS Reducing agricultural labour intensity Strong population growth in metropolitan Melbourne, decreasing affordability.

DRIVERS Regional centre employment Diverse range of jobs

ATTRACTORS Education Pace of life Health services Shopping

BARRIERS Lack of health and other services

ATTRACTORS Lower cost of living/housing Jobs

BARRIERS Lack of relevant employment Lower pay Cost of relocation Internet speed and availability

ENVIRONMENT CONNECTIONS

INFLUENCE/TRENDS Tree change, sea change movement (s)

DRIVERS Coastal amenity

INFLUENCE/TRENDS Social and professional/business networks

DRIVERS Inclusive communities

ATTRACTORS Natural beauty

BARRIERS Distance - many towns and areas are too far to commute to a regional centre

ATTRACTORS Family and friends Return migration

BARRIERS No social networks Loss of professional networks Responsibility to care for elderly relatives in current location

• targetmarketsmostlikelytobeattractedtotheregionandbestalignedwithexistingeconomicandlifestyleopportunitiesintheBSW:

• Overseasmigrants,includingskilledmigrantsandrecentmigrantgroupsalreadyinMelbourne;

• Students,includingbothregionalandmetropolitanstudents;

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 26

• Regionalreturners,especiallyyoungfamilies;

• Businessowners,bothexistingwithintheregionandthosewithinmetropolitanMelbournewithpotentialtomovetoregionalareasorsetuparegionaloffice;and

• “Planttheseed”:touristsandstudentswhomayvisittheregionshortterm,andthenreturntoresideatalatertime.

• Objectiveswithrespecttoattractingpopulation:

Objective1: establishincentivesforbusinessesandgovernmentagenciestorelocatetotheregion

Objective2: attractskilled,youngAustralianstoliveintheBSW,especiallydiaspora

Objective3: addresslabourshortagesandincreaselocalpopulationthroughtargetedmigration

Objective4: retainandimprovehighereducationopportunitiesintheregion

Objective5: promoteliveabilitygains,especiallyinruralcentres

Objective6: improveresourcesforstrategicplanninginruralandregionalareas

4 RelevantStudies/Commentary

Areviewofrelevantstudiesand/orcommentarynotesthatthepopulationattractionandthereasonsforpeoplewantingtomovetorurallocationsaremultifactorial.

4.1 Peoplecount:Populationgrowthcausesbasiceconomicgrowth

Overview Populationgrowthiseconomicgrowth.Takingstepstoattractpeopletomovetoacommunityisanimportantstrategy.

PostedonJanuary19,2017byKurtSchindler,MichiganStateUniversityExtension

“Oneofthecharacteristicsoftheneweconomyisthatjobsfollowpeople.Peoplemovetoqualityplaces.Currentlymillennialstendtoseekurban,largecitydowntownstolive.Thattrendwillcontinueforsomeyearsyet.Itisageneralization.Noteveryonefitsthatmold.Thetaskforruralcommunitiesorsmalltownsistodefinetheirnicheandtargetthosepeoplewhoseektheassetsandattributestheyhavetooffer.

Theultimatelocalgoalfortheneweconomyistoattractandretainthesepeople-assets:well-educatedyouth,seniors,immigrantsandentrepreneurs.Forgrowthintheneweconomy,acommunityandregionshouldhaveadeliberate,purposeful,formally-adoptedpopulationattractionstrategy.Suchastrategymayinvolvemanyofthesamethingsthecommunitydoestoattracttourists,attractmedicalstafftoalocalhospital,andmore.

Whatattractspeopletoatown,countyandregion?Thesamethingsthathavealreadybeenpointedoutinthisseries:greenandblueinfrastructure,vibrantdowntowns,arts,culture,activityandthingstodo.Butmorespecifically,itcomesdownto“placematters”.Peopleareattractedtoaplace.Thetypesofplaceswhicharepopularandsuccessfulingettingnewpopulationhavethefollowing:• Entrepreneurialinfrastructure–acommunitythatissupportiveofnewbusinessesstartupsand

hasprogramssuchaseconomicgardeninginplace• Diversity–communitiesthataretolerantofandsociallywelcomediversityofrace,religions,

beliefsandlife-styles.• Greenandblueinfrastructure–naturalareas,parks,trails,waterresourcesandsoon• Socialinfrastructure–acommunitywithsocialactivities,eventsandthingstodo• Publictransportationinfrastructure–achoiceastohowonegetsaroundthecommunity,not

justautomobile,butalsobike,walking,andpublictransportationtoandbetweenamenities• Varietyofhousing–achoiceofdifferenttypesofhousing,notjustsinglefamilyhomesonlots,

butalsohousingdowntown,apartmentbuildings,andsoon(whatisimportantistoprovidechoice)

• Informationtechnologyinfrastructure–high-speedinternet• Collaborativecapacity–acommunitythatworkstogetherandhasmanycollaborativeand

cooperativeseffortsforaccomplishingcommunity-wideprojects

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 27

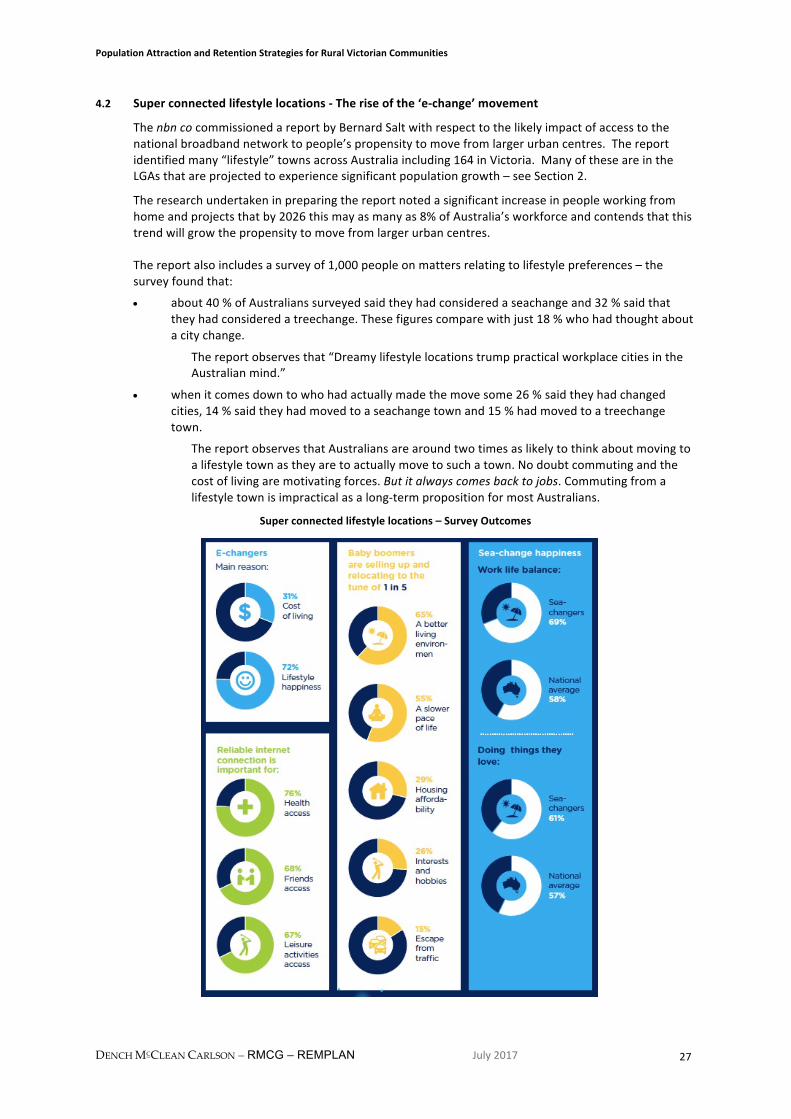

4.2 Superconnectedlifestylelocations-Theriseofthe‘e-change’movement

ThenbncocommissionedareportbyBernardSaltwithrespecttothelikelyimpactofaccesstothenationalbroadbandnetworktopeople’spropensitytomovefromlargerurbancentres.Thereportidentifiedmany“lifestyle”townsacrossAustraliaincluding164inVictoria.ManyoftheseareintheLGAsthatareprojectedtoexperiencesignificantpopulationgrowth–seeSection2.

Theresearchundertakeninpreparingthereportnotedasignificantincreaseinpeopleworkingfromhomeandprojectsthatby2026thismayasmanyas8%ofAustralia’sworkforceandcontendsthatthistrendwillgrowthepropensitytomovefromlargerurbancentres.

Thereportalsoincludesasurveyof1,000peopleonmattersrelatingtolifestylepreferences–thesurveyfoundthat:

• about40%ofAustralianssurveyedsaidtheyhadconsideredaseachangeand32%saidthattheyhadconsideredatreechange.Thesefigurescomparewithjust18%whohadthoughtaboutacitychange.

Thereportobservesthat“DreamylifestylelocationstrumppracticalworkplacecitiesintheAustralianmind.”

• whenitcomesdowntowhohadactuallymadethemovesome26%saidtheyhadchangedcities,14%saidtheyhadmovedtoaseachangetownand15%hadmovedtoatreechangetown.

ThereportobservesthatAustraliansarearoundtwotimesaslikelytothinkaboutmovingtoalifestyletownastheyaretoactuallymovetosuchatown.Nodoubtcommutingandthecostoflivingaremotivatingforces.Butitalwayscomesbacktojobs.Commutingfromalifestyletownisimpracticalasalong-termpropositionformostAustralians.

Superconnectedlifestylelocations–SurveyOutcomes

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 28

Thereportpostulatesthat“superconnectivitymadeavailablebyaccesstothenbn™networkinthe2020sandAustralianswilllookatwaysoftelecommutingfromanyofthebythen650townswithinstrikingdistanceofcapitalcities.Whoknows,by2030perhapstheproportionofAustralianslivinginthise-changezone(between30kmand150kmfromacapitalcityCBD)mightrisefrom15percenttodaytocloserto20percent?”

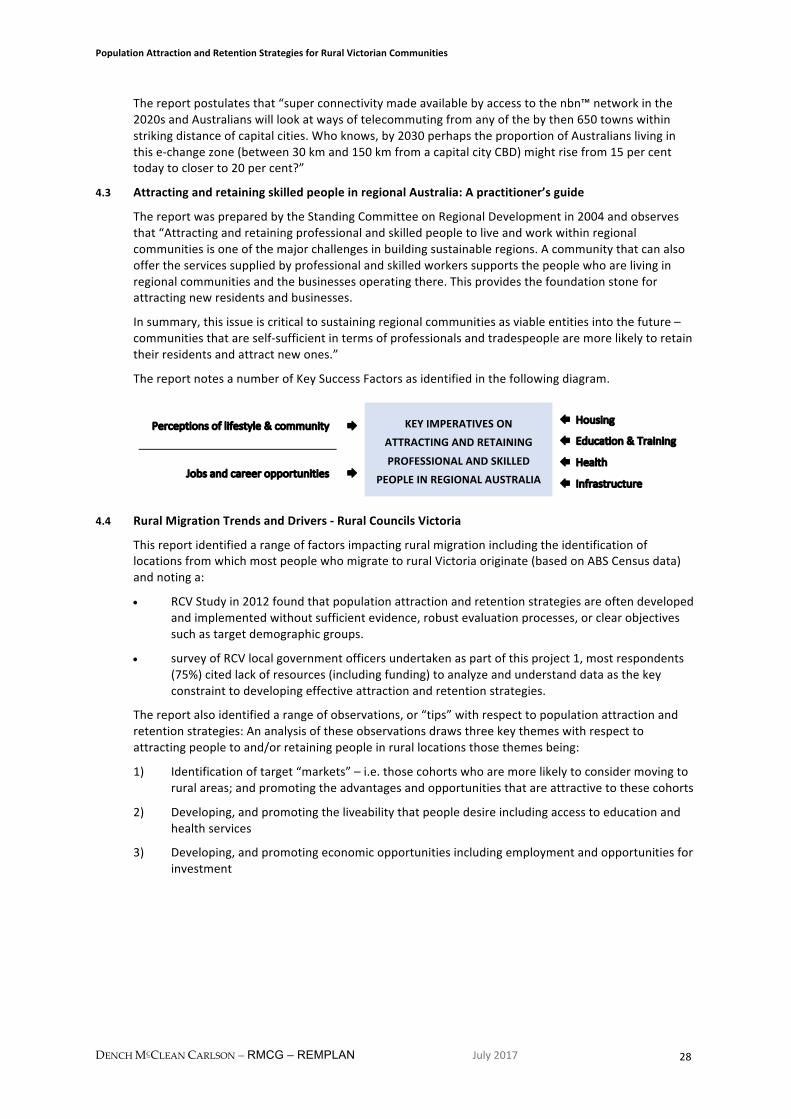

4.3 AttractingandretainingskilledpeopleinregionalAustralia:Apractitioner’sguide

ThereportwaspreparedbytheStandingCommitteeonRegionalDevelopmentin2004andobservesthat“Attractingandretainingprofessionalandskilledpeopletoliveandworkwithinregionalcommunitiesisoneofthemajorchallengesinbuildingsustainableregions.Acommunitythatcanalsooffertheservicessuppliedbyprofessionalandskilledworkerssupportsthepeoplewhoarelivinginregionalcommunitiesandthebusinessesoperatingthere.Thisprovidesthefoundationstoneforattractingnewresidentsandbusinesses.

Insummary,thisissueiscriticaltosustainingregionalcommunitiesasviableentitiesintothefuture–communitiesthatareself-sufficientintermsofprofessionalsandtradespeoplearemorelikelytoretaintheirresidentsandattractnewones.”

ThereportnotesanumberofKeySuccessFactorsasidentifiedinthefollowingdiagram.

Perceptionsoflifestyle&community Æ KEYIMPERATIVESONATTRACTINGANDRETAININGPROFESSIONALANDSKILLED

PEOPLEINREGIONALAUSTRALIA

ÅHousing

ÅEducation&Training

ÅHealth

ÅInfrastructureJobsandcareeropportunities Æ

4.4 RuralMigrationTrendsandDrivers-RuralCouncilsVictoria

ThisreportidentifiedarangeoffactorsimpactingruralmigrationincludingtheidentificationoflocationsfromwhichmostpeoplewhomigratetoruralVictoriaoriginate(basedonABSCensusdata)andnotinga:

• RCVStudyin2012foundthatpopulationattractionandretentionstrategiesareoftendevelopedandimplementedwithoutsufficientevidence,robustevaluationprocesses,orclearobjectivessuchastargetdemographicgroups.

• surveyofRCVlocalgovernmentofficersundertakenaspartofthisproject1,mostrespondents(75%)citedlackofresources(includingfunding)toanalyzeandunderstanddataasthekeyconstrainttodevelopingeffectiveattractionandretentionstrategies.

Thereportalsoidentifiedarangeofobservations,or“tips”withrespecttopopulationattractionandretentionstrategies:Ananalysisoftheseobservationsdrawsthreekeythemeswithrespecttoattractingpeopletoand/orretainingpeopleinrurallocationsthosethemesbeing:

1) Identificationoftarget“markets”–i.e.thosecohortswhoaremorelikelytoconsidermovingtoruralareas;andpromotingtheadvantagesandopportunitiesthatareattractivetothesecohorts

2) Developing,andpromotingtheliveabilitythatpeopledesireincludingaccesstoeducationandhealthservices

3) Developing,andpromotingeconomicopportunitiesincludingemploymentandopportunitiesforinvestment

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 29

AnAnalysisRuralMigrationTrendsandDrivers

Themes Needto:

Targetedmarketing&promotion

addresskeydecisiondriversformovingtoruralVictoria

identifytargetcohortsthataremorelikelytoconsidermigratingtorurallocations

promotekeyadvantagesoflivinginruralareas/communities

ensurethatnewcomers,potentialnewcomersandvisitorshavereadyaccesstoinformation

Liveabilitydevelop,andpromote,theaccesstoeducationandhealthservices

haveprocessestoengageyoungpeople

Economicopportunities

fosteremploymentandworkforcedevelopmentopportunities

fosterthedevelopmentofexistingandorthe“start-up”oflocalbusinesses

haveidentifiedandexpediteprivatesectorinvestmentopportunities

haveeffectivecommunityeconomicdevelopmentprocesses

4.5 RegionalAustraliaInstitute

TheRegionalAustraliaInstitute(RAI)hasreleasedthereport“LightingUpourGreatSmallCities:ChallengingMisconceptions”whichananalysisoftheeconomicopportunitiesin31regionalcitiesthroughoutAustralia–seehttp://www.regionalaustralia.org.au/home/wp-content/uploads/2017/06/Lighting-Up-our-Great-Small-Cities_Report_EMBARGOED.pdf

TheRAI’sprojectionsoffutureregionalcitycontendsthat“regionalcitieshavethepotentialtoproduce$375billioninoutputin2031,representinga65percentincreasefrom2013levelsandacontributionof15percenttothenationaleconomy’

Thereportcontendsthefollowing“myths”regardingthecapacityandcapabilityofregionalcitieswithrespecttoattractinginvestmentanddeliveringpositivereturnsforinvestors:

Myth1:SloworDecliningGrowth

Australiaengagesinamostlynegativepublicdiscussionaboutregionaleconomies.Asideeffectofthislong-termdebateisthatmanybelievethatregionalcityeconomicperformanceinevitablylagsmetropolitanoutcomesandthat‘manyregionalcitiesaresufferinglowandnegativegrowth’.

Myth2:RegionalCitieswillbeLeftBehindintheNewEconomyWorld

Australia’seconomyisbecomingservicesfocusedwiththegrowthofjobsconcentratinginneweconomyindustries.Itisassumedthatregionalcitiesareinevitablybeingleftbehindinthistrend.However,Regionalcitiesarealreadyproducingmoreoutputinneweconomyindustries(finance,education, health and professional services) than old industries (agriculture, mining andmanufacturing).

Myth3:PopulationSizeistheMostImportantFactorinPredictingEconomicPerformance

Regional cities are often characterised as interesting, only when they are big. This drives amisconceptionthatallthebenefitsofcitiesgrowwithpopulationsize.Infact,whenitcomestoparticipation, historical growth or projected growth in output there is no statistical differencebetweenbigorsmallregionalcities.Thechallengeforpolicymakersatthenational,stateandlocallevelsistocultivatecityperformance,notsize.

Myth4:PastPerformanceistheBestPredictorofFutureGrowth

Whiletrendsareimportant,historydoesnotpredeterminethedestinyofacity.Changingmacro-economicconditionsarehavingasignificantimpactonregionalcitygrowthtrajectoriesandathirdof all regional cities have already or are predicted to change their output growth trajectories.Developingsmartstrategiesthatrespondtochangingtrajectoriesisimportanttosuccessfulsmallcitiespolicy.

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 30

Akeytenantofthereportistheneedtodemonstratetotheprivatesectorthatthereareattractiveinvestmentopportunitiesoutsideofthecapitalcities.

Whilethisreportisonregionalcitiesitstandstoreasonthatthesimilarmisconceptionsimpactinvestmentopportunitiesinruralareas.

4.6 ImplicationsforPopulationAttractionProjects

Populationattractionisdependentonacombinationoffactorsmostnotably:-

• Economicopportunities–i.e.accesstoemploymentand/orinvestmentopportunities

• Liveability–i.e.accesstorelevantservicesand/oradesiredlifestyle

• Promotion–i.e.providingrelevantinformationtotargetmarkets

5 RCVPopulationAttractionandRetentionProjects

ThePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesprojecthassoughttoconsolidatethelessonsofRCV’spriorprojectsalongwithevidencefromthebroaderknowledgebasetodetermineapractical,actionablesetofProjectsfortheStrongerRuralCouncilsInitiative(SRCI)tosupportoverthenextthreeyearsforthebenefitofitsmembersandthatareconsistentwithRCV’srole,mandateandcapacity,aswellasopportunitiesthatexisttoinfluenceStategovernmentpolicyandprograms.

ThePopulationAttractionandRetentionStrategiesforRuralVictorianCommunitiesprojecthasconsideredtheimplicationsforpopulationattractionandretentionandeconomicdevelopmentrelevanttoVictorianruralcommunitiesarisingfromtheimplicationsarisingfromthereviewof:

• population,demographicandeconomicdataforeachofthe38RCVLGAs

• populationattractionandretentioneffortsinAustralia,USA,CanadaandScotland

• previousRCV,andotherrelevantstudies

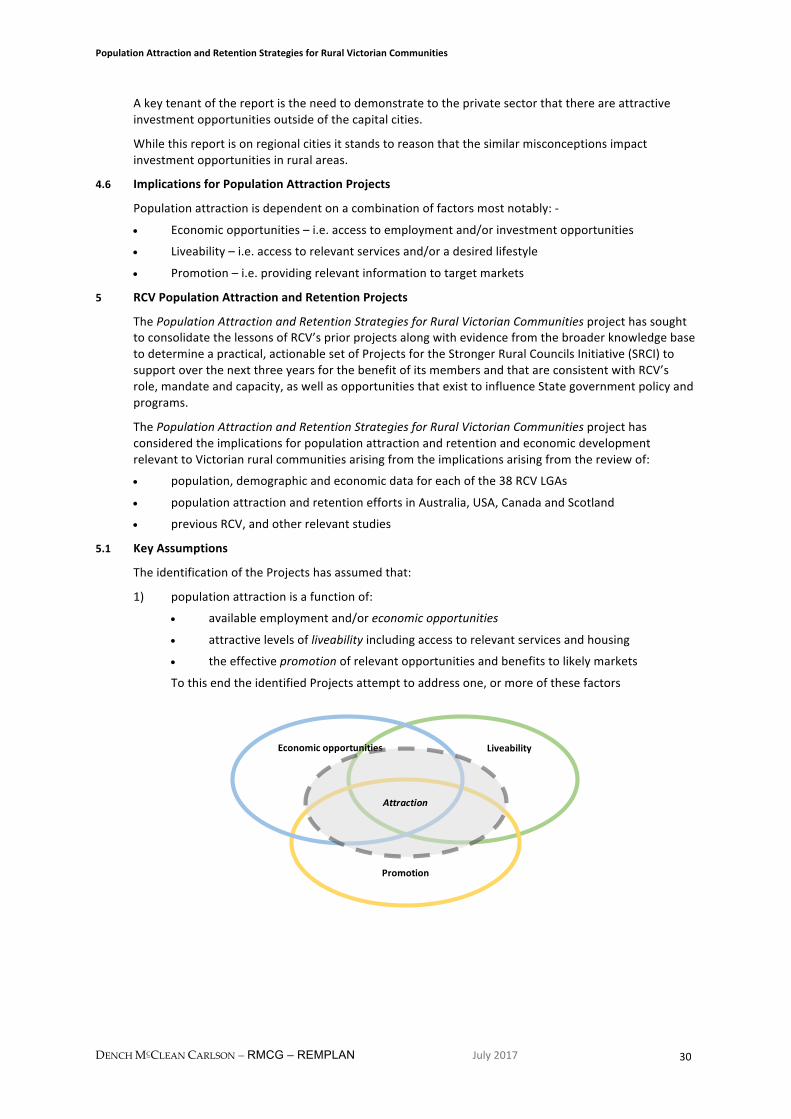

5.1 KeyAssumptions

TheidentificationoftheProjectshasassumedthat:

1) populationattractionisafunctionof:

• availableemploymentand/oreconomicopportunities

• attractivelevelsofliveabilityincludingaccesstorelevantservicesandhousing

• theeffectivepromotionofrelevantopportunitiesandbenefitstolikelymarkets

TothisendtheidentifiedProjectsattempttoaddressone,ormoreofthesefactors

Liveability

Promotion

Economicopportunities

Attraction

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 31

2) collectively,theProjectsneedtoaddvaluetoruralLGAsinvarioussituationsi.e.thosethatareprojectedto:

• losepopulation–butexperiencearelativegrowthofpopulationaged65yearsplus–andhaveexperiencedanetlossofjobs

• gainpopulation–butwillexperienceanetlossofpopulationagedunder65years–buthaveexperiencedanetlossofjobs

• gainpopulation–butwillexperienceanetlossofpopulationagedunder65yearsandhaveexperiencedanetincreaseinjobs

• gainpopulationacrossageagesandhaveexperiencedanetincreaseinjobs

3) RCVCouncilsareresourceconstrainedand/orhavelimitedskills/experiencewithrespecttoundertakingactivitiessuchamarketresearch,Investmentattraction–particularlywiththeprivatesector,andpromotion

4) Thereisnocommonmechanism/portalforpromotingruralVictoriatokeymarkets

5) RCVhaslimitedresourceswithrespecttothedeliveryofsignificantprojects

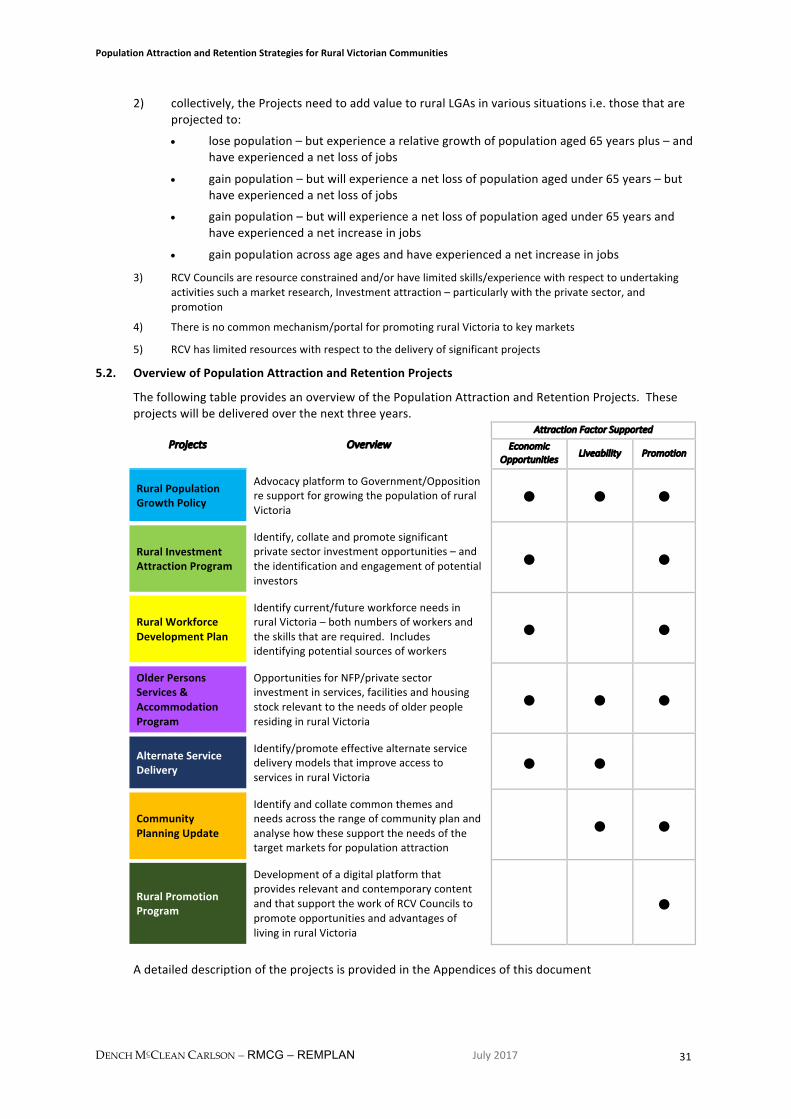

5.2. OverviewofPopulationAttractionandRetentionProjects

ThefollowingtableprovidesanoverviewofthePopulationAttractionandRetentionProjects.Theseprojectswillbedeliveredoverthenextthreeyears.

Projects OverviewAttractionFactorSupported

EconomicOpportunities

Liveability Promotion

RuralPopulationGrowthPolicy

AdvocacyplatformtoGovernment/OppositionresupportforgrowingthepopulationofruralVictoria

n n n

RuralInvestmentAttractionProgram

Identify,collateandpromotesignificantprivatesectorinvestmentopportunities–andtheidentificationandengagementofpotentialinvestors

n n

RuralWorkforceDevelopmentPlan

Identifycurrent/futureworkforceneedsinruralVictoria–bothnumbersofworkersandtheskillsthatarerequired.Includesidentifyingpotentialsourcesofworkers

n n

OlderPersonsServices&AccommodationProgram

OpportunitiesforNFP/privatesectorinvestmentinservices,facilitiesandhousingstockrelevanttotheneedsofolderpeopleresidinginruralVictoria

n n n

AlternateServiceDelivery

Identify/promoteeffectivealternateservicedeliverymodelsthatimproveaccesstoservicesinruralVictoria

n n

CommunityPlanningUpdate

Identifyandcollatecommonthemesandneedsacrosstherangeofcommunityplanandanalysehowthesesupporttheneedsofthetargetmarketsforpopulationattraction

n n

RuralPromotionProgram

DevelopmentofadigitalplatformthatprovidesrelevantandcontemporarycontentandthatsupporttheworkofRCVCouncilstopromoteopportunitiesandadvantagesoflivinginruralVictoria

n

AdetaileddescriptionoftheprojectsisprovidedintheAppendicesofthisdocument

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 32

5.3. EstimationofRequiredResources

Anestimationoftheresourcesthatwillberequiredtodelivertheprojectshasbeenundertaken.Thisincludesanestimationofthe

• Consultingdaysrequiredtoundertaketheproject

• ProjectManagementhours–thisassumesthatRCVhaslimitedresourceswithrespecttoprojectmanagementandthateachprojectwillrequireresourcestoorganizerequirementswithrespectto:

• relevantmeetings

• engagementandconsultationwithRCVCouncilsandotherstakeholders

• otherexpertise

• Additionalexpertisethatmayberequired–thisexpertisefallintooneormoreofthefollowingcategories:

• EconomicResearchandImpactModelling

• EconomicDevelopmentandInvestmentAttraction

• LandUseAnalysis

• GraphicDesign–includingdigitalplatformdevelopmentandoperation

• EventManagement

• Relatedtravelcosts

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 33

Appendix1-PopulationAttractionandRetentionProjects–DescriptionandEstimatedResources

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities

DENCH MCCLEAN CARLSON – RMCG – REMPLAN July2017 34

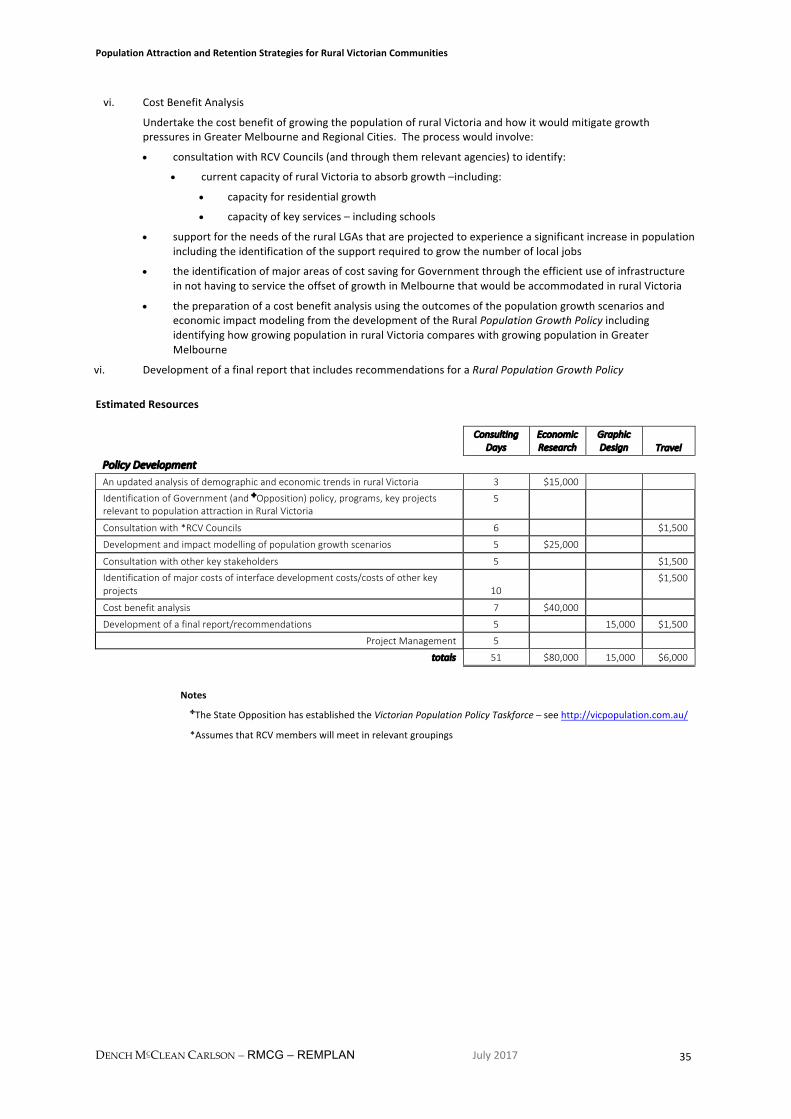

Project#1-RuralPopulationGrowthPolicy

Overview

RCVtocommissionthedevelopmentofaRuralPopulationGrowthPolicytoadvocatetoGovernment,andtheOpposition,themeritsofsupportingpopulationgrowthinRuralVictoria.

Context

Theforecastforthecollectivepopulationgrowthofthe38RCVLGAsto2031represents7%ofVictoriapopulationgrowthinthisperiod–thisgrowth:

• ishighlyconcentratedwith9of38RuralLGAsareprojectedtoexperiencepopulationgrowthacrossallagecohorts–7oftheseLGAsadjoinGreaterMelbourneand/orGeelong

ÆNeedsupportforaddressingfast

growingpopulations

• includesalossofpeopleagedunder65.12of38RuralLGAsareprojectedtoexperiencepopulationgrowth2011to2031butwillexperienceanoveralllossofpopulationagedunder65years

• willnotbeexperiencedin17of38RuralLGAsthatareprojectedtolosepopulation

ÆNeedsupportfor

growingpopulationandjobs

Between2006and2011thenumberofjobsinRuralVictoriagrewby5,062representing1.8%ofthegrowthinjobsinVictoria.Jobsin18ofthe38RCVlocaleconomiesgrewbyalmost11,500from2006to2011with5LGAsaccountingforalmost70%ofthisgrowth.20RCVlocaleconomiesexperiencedalossofatotalof6,425jobsinthesameperiod.

ÆNeedsupportfor

growinginvestmentandjobs

ProjectDescription

RCVtocommissionthedevelopmentofaRuralPopulationGrowthPolicytoadvocatetoGovernment,andtheOpposition,themeritsofsupportingpopulationgrowthinRuralVictoria.ThePolicywouldfosterawiderunderstandingoftheneedfor,benefitofandcommunityandpoliticalsupportforpopulationgrowthinruralVictoriaandwouldadvocateforpopulationgrowthinruralVictoriaandthatwould:

• supportimprovedaccesstoservices(includingthoseinhealth,educationandrecreation)tomaintainpositivelevelsofliveabilityforruralLGAsthathaveexperienced:

• acontractionofpopulation

• significantpopulationgrowth(i.e.peri-urbanLGAs)

• supportgreaterlevelsofprivatesectorinvestmentinruralVictoria

• supportworkforcerequirements(seealsoProject#2)

• growthepopulationofpeopleagedunder65

ThedevelopmentoftheRuralPopulationGrowthPolicywouldinvolve:

i. AnupdatedanalysisofdemographicandeconomictrendsinruralVictoriabasedon2016ABSCensusdata–andotherrelevantsources

ii. identificationofrelevant:

• Governmentpolicyandprograms(e.g.ReductionofPayrollTax,removalofStampDuty,increaseofFirstHomeBuyersBonus)

• Priorityprojects–asespousedbyRDACommitteesandRegionalPartnerships–andthelevelofinvestmentrequiredtodeliversuchprojects

• Oppositionpolicy

iii. ConsultationwithRCVCouncilsregarding:

• keystrengths,

• thecurrentcapacitytosupportpopulationgrowth,

• barrierstopopulationgrowthandkeyneeds;and

• policygaps

iv. DevelopmentandimpactmodellingofpopulationgrowthscenariosforruralVictoriaincludingtheimpactonemploymentandeconomicgrowth

v. Consultationwithotherkeystakeholdersincluding:

• DTFrecurrentlevelsofGovernmentexpenditureinruralVictoria

• RDVrefuturepolicydirection

• Oppositionrerelevantpolicyplatforms

PopulationAttractionandRetentionStrategiesforRuralVictorianCommunities