Microsoft Vision and Roadmap - The New Era of Productivity from Atidan

Upload

geoffrey-cannCategory

view

479download

3

Productivity in the New Era

We are well and truly in a new era for oil and gas

Need to make the business sweat

0

Partner with Deloitte Canada on secondment to AustraliaSeveral years working in oil sandsFind me on social mediaWeekly blog about the LNG sectorTwitter accountiTunes channel

Google me

1

• productivity is too low.• Various studies report that the productivity of Australian

workers is 65-70% that of the US Gulf Coast• stand-around time (where workers are waiting on delivery of kit,

permission to work, or completion of previous work) is morethan 40%.

• 150 separate legislative acts governed by 50 agencies providingoversight to the industry

• The unit labour costs in Australia’s gas sector are high for theglobal industry.

• Confirmed by several independent studies• Australian gas wages 35% higher than comparable roles in the

US, and on par with the Norwegians• Labour is 22-27% of the budget to build oil and gas

infrastructure• Shortages have eased considerably as the mining boom has

moderated, but unit costs have not come down.

• Supplier base has been here for decades, but not in quantity.

2

• Ramp up very quickly, and suppliers have been free to test theceiling on rates

• Operators have had to supervise suppliers more closely than typical, and now havetoo many people in the field.

2

• People – the right skills for the job• Processes – work being actually done• Organisation – the right structure• Systems – not just technology but ways of working• Performance – KPIs that actually measure and reward

productivity, not just unit cost• Supply chain – contracts with suppliers that reward productivity• Assets – only enough to do the job, productive

3

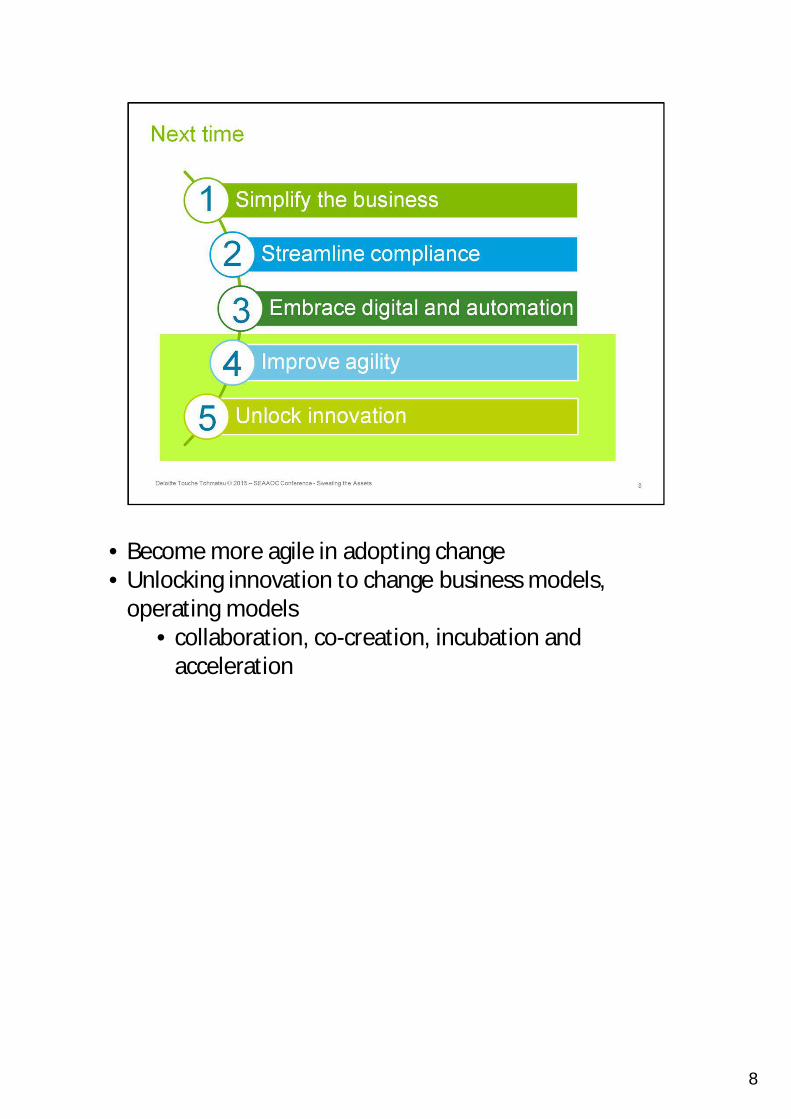

• simplification of the business• manage the asset mix

• streamlining compliance• Fraser institute survey

• embracing digital and automation• key is substituting technology for people where-

ever possible• improving agility

• McKinsey – time to 50% penetration of innovationis 35 years

• unlocking innovation (technology, business models,operating models

• collaboration, co-creation, incubation andacceleration

4

• Discover what is truly core• For upstream – geology and reservoir, initial

capital spend, production• For midstream – asset management and

optimisation• For downstream – customer requirements,

logistics• For services – cost, quality or customer

relationships• Outsource what is important but not core

• For Irving Oil, this meant shipping, oceanvessels

• KKR-Veresen deal in Alberta• Many Australian oil and gas companies trying

to do it all• Sell off remainder

• Asset sales – pipelines, gas plants, gatheringsystems, farm land, telecoms, power

5

• Stream line first? If there’s time.

5

• Pages of laws – 15,000 in the 70’s. 30,000 in the80’s. 60,000 in the 2000’s

• Compliance workers now 9% of total economy,doubled in past

• 1m employees, more than in construction andeducation

• More expensive workers• Managers spending 1 day per week in straight

compliance activities• 20% of rules deemed unnecessary by managers• $27b in annual admin costs – more than profits of

banks, all GST collections• $65b in compliance with public sector imposed

costs• $21b tax on private sector• $134b compliance cost

6

• Consequence to gas sector• $250b in red tape compliance burden• 2.6% GDP (APPEA study 2014)• $6.5b in red tape costs

6

Deloitte study on digital disruptionOil and gas not reflectedGas is combo of construction, extraction (Mining) and manufacturing (gas plant ops)

Between 6 and 15% business improvement potential

Construction – 48%, 14%Mining – 48% - 4%Manufacturing – 51% - 6%

7

• Become more agile in adopting change• Unlocking innovation to change business models,

operating models• collaboration, co-creation, incubation and

acceleration

8

9