Piketty and the search for r Michael Roberts ASSA 2015 (URPE), Boston 4 January.

23

Piketty and the search for r Michael Roberts ASSA 2015 (URPE), Boston 4 January

-

Upload

sheena-norris -

Category

Documents

-

view

216 -

download

2

Transcript of Piketty and the search for r Michael Roberts ASSA 2015 (URPE), Boston 4 January.

Piketty and the search for r

Michael RobertsASSA 2015 (URPE), Boston 4 January

The Piketty phenomenon

• “Piketty put inequality on the map but we have got carried way by the comprehensive nature of his explanation” Paul Krugman, Columbia Law School Panel discussion, December 2014

Data matter

• “All social scientists and all citizens must take a serious interest in money, its measurement the facts surrounding it and its history. Those who have a lot of it never fail to defend their

interest. Refusing to deal with numbers rarely serves the interest of the least well-off”

Piketty p557

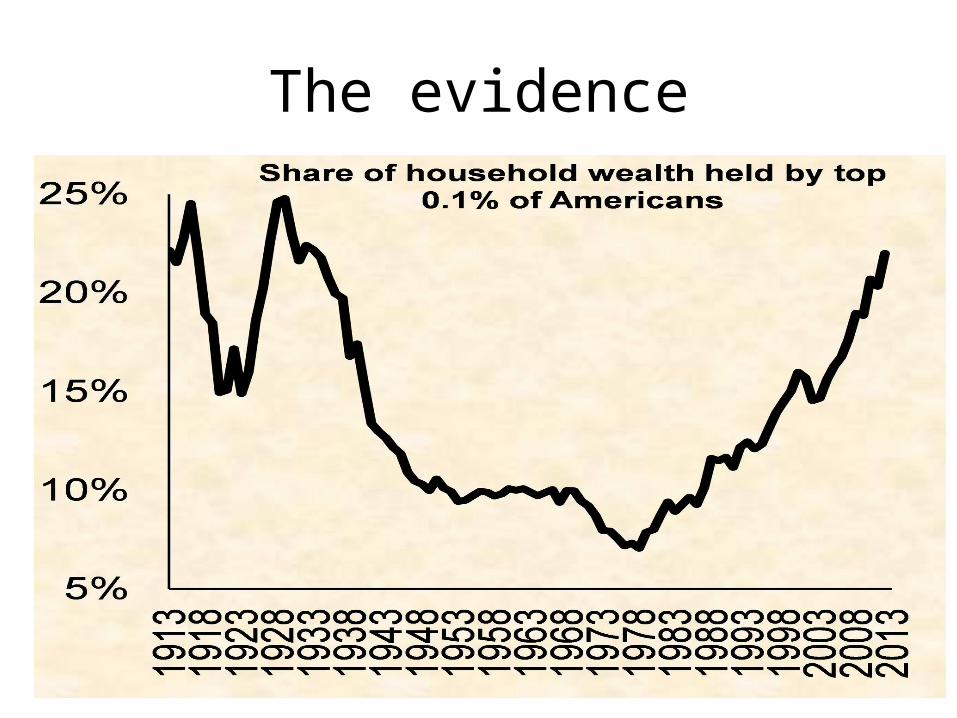

The evidence

Capital vs wealth

• “Capital is defined as the sum total of nonhuman assets that can be owned and exchanged on some market. Capital includes all forms of real property (including residential real estate) as well as financial and professional capital (plants, infrastructure, machinery, patents and so on) used by firms and government agencies.” Piketty p46

The circuit of capital

• For Marx, the circuit of capital is M-C…P…C1 to M1, namely capitalists have money capital (M) which is invested in commodities (C), means of production and raw materials, which are used by labour in production (P) to produce commodities (C1) for sale on the market for more money (M1). Capital (M) expands value to accumulate more capital (M1). But only labour created that new value.

• For Piketty, the capital process is M…M1. Money accumulates more money (or wealth). It does not matter how and so there is no need to define capital as different from wealth.

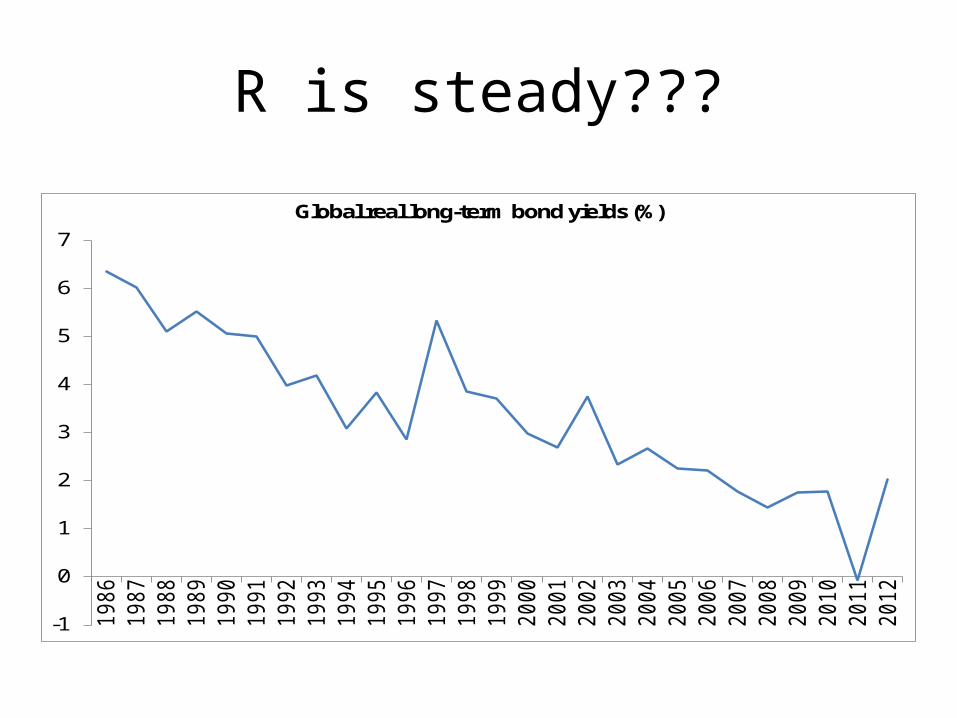

R is steady… but also variable (?)

• r “is pretty much steady around 4-5% but varies over time and between asset classes” Piketty p55

Marginal productivity or rent-seeking?

• “There is every reason to believe that r will be much greater than g in the decades ahead because of “oligarchic divergence”. This divergence is even greater because rich hide their wealth in tax havens.” Piketty, p463

r>g

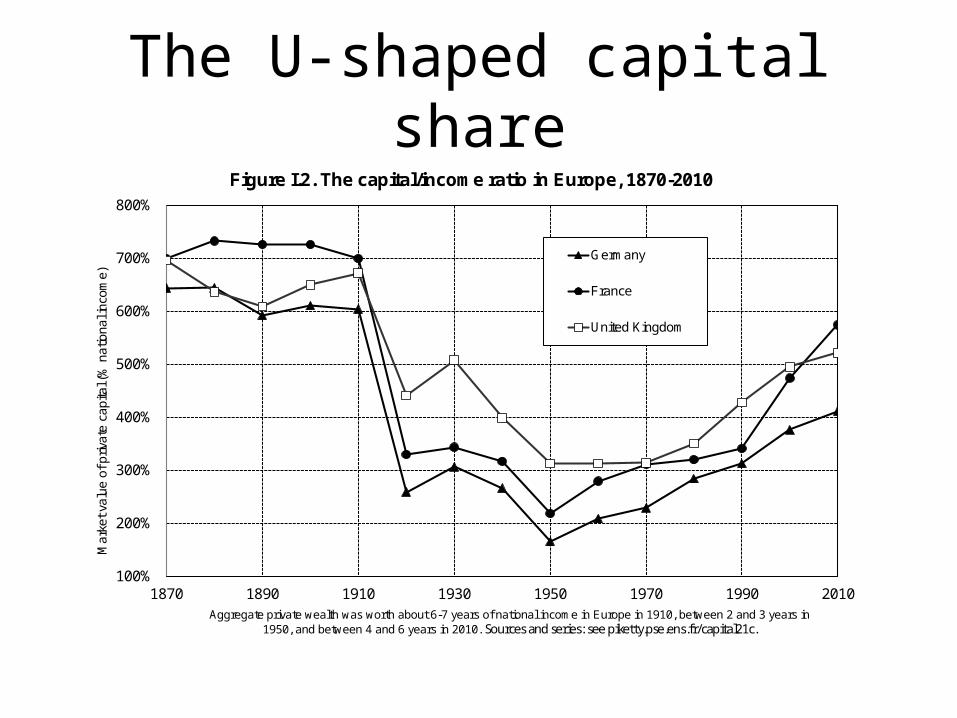

The U-shaped capital share

100%

200%

300%

400%

500%

600%

700%

800%

1870 1890 1910 1930 1950 1970 1990 2010

Ma

rke

t va

lue

of p

riva

te c

ap

ital (

% n

atio

na

l in

com

e)

Aggregate private wealth was worth about 6-7 years of national income in Europe in 1910, between 2 and 3 years in 1950, and between 4 and 6 years in 2010. Sources and series: see piketty.pse.ens.fr/capital21c.

Figure I.2. The capital/income ratio in Europe, 1870-2010

Germany

France

United Kingdom

R is steady???

-1

0

1

2

3

4

5

6

7

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Global real long-term bond yields (%)

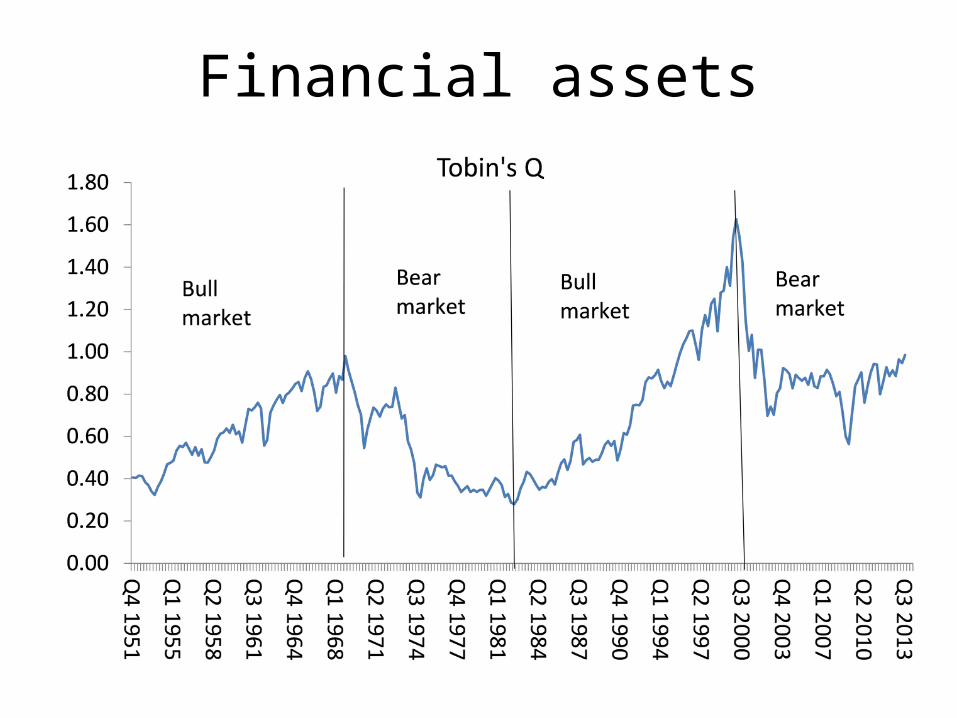

Financial assets

Real estate

• “Using Piketty and Zucman (2013)’s data, I find that a single component of the capital stock—housing—accounts for nearly 100% of the long-term increase in the capital/ income ratio, and more than 100% of the long-term increase in the net capital share of income… when housing is removed, there is a small increase in the capital/income ratio and a small decrease in the net capital share of income. The dominant role of housing in Piketty’s data reflects the influence of real price changes, particularly for land. “

• A note on Piketty and diminishing returns to capital, Matthew Rognlie, June 15, 2014

Never read Capital

• “I never managed really to read it. I mean I don’t know if you’ve tried to read it. Have you tried?... The Communist Manifesto of 1848 is a short and strong piece. Das Kapital, I think, is very difficult to read and for me it was not very influential…. The big difference is that my book is a book about the history of capital. In the books of Marx there’s no data.”

Interview in New Republic

r does not fall

• “the rate of return on capital is a central concept in many economic theories. In particular, Marxist analysis emphasises the falling rate of profit – a historical prediction that has turned out to be quite wrong, although it does contain an interesting intuition.” Piketty p52

More pessimistic than Marx

• “Karl Marx thought that the falling rate of profit would inevitably bring about the fall of the capitalist system. In a sense, I am more pessimistic than Marx, because even given a stable rate of return on capital, say around 5 percent on average, and steady growth, wealth would continue to concentrate, and the rate of accumulation of inherited wealth would go on increasing.” Piketty interview in The Baffler

Zero productivity

• “like his predecessors Marx totally neglected the possibility of durable technological progress and steadily increasing productivity, which is a force that can to some extent serve as a counterweight to the process of accumulation and concentration of capital” Piketty p10

• “Marx’s theory implicitly relies on a strict assumption of zero productivity growth over the long run”. Piketty p27

Infinite accumulation

• Piketty argues that Marx’s r falls because in his model of capitalism, there is “an infinite accumulation of capital” and “as ever more increasing quantities of capital lead inexorably to a falling rate of profit (i.e. return on capital) and eventually to their own downfall, while growth in net income (g) falls to zero.”

Piketty p228

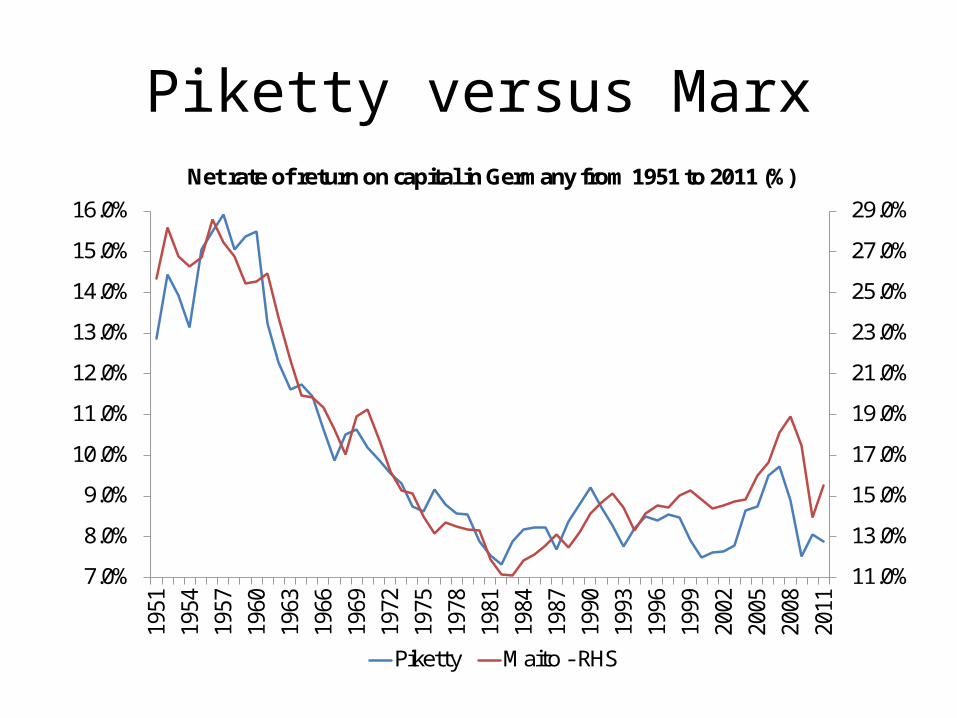

Marx’s r: the evidence

Piketty versus Marx

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

23.0%

25.0%

27.0%

29.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

Net rate of return on capital in Germany from 1951 to 2011 (%)

Piketty Maito - RHS

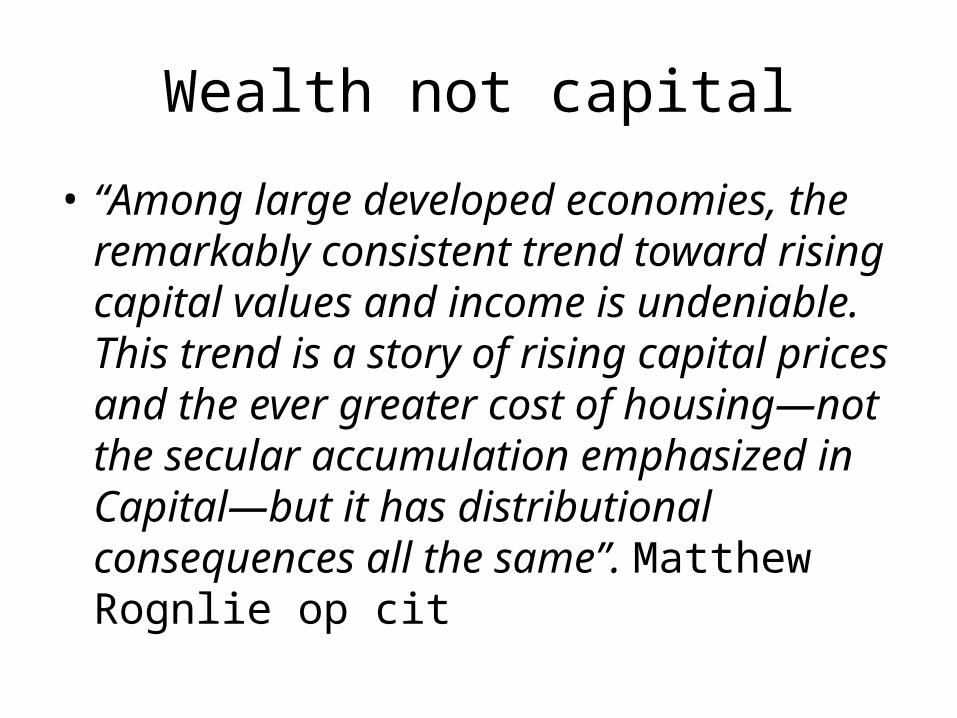

Wealth not capital

• “Among large developed economies, the remarkably consistent trend toward rising capital values and income is undeniable. This trend is a story of rising capital prices and the ever greater cost of housing—not the secular accumulation emphasized in Capital—but it has distributional consequences all the same”. Matthew Rognlie op cit

Capital is good

• “The fact remains that capital is useful in itself. The inequalities associated with it are problematic, but not capital per se. And there is much more capital today than formerly.”

• “when the growth rate is 1 percent, or even negative, as in some European countries today, … this is not a problem from a strictly economic point of view, but it certainly is in social terms, because it brings about great concentrations of wealth. In response to which, progressive wealth and inheritance taxes are of great utility.” Piketty interview, op cit

Which is the right r?

• The central unanswered question for Piketty’s thesis is this. Is rising inequality the central contradiction of capitalism and thus its grave digger?

• Is it a tendency for a rising net return on capital (Piketty) or is it the tendency for a falling rate of profit (Marx) that is the key contradiction of capitalism in the 21st century?

• If it is the former, then all we need to do is to introduce a progressive tax system. We don’t need to bury capitalism, as we can save it.

• But if it is the latter, then the main contradiction in the capitalist mode of production would not be resolved. The solution then is one of replacing the capitalist mode of production.