Photovoltaïque: la longue marche vers la parité réseaueer.in2p3.fr/Jousse_D.pdf ·...

31

Photovoltaïque: la longue marche vers la parité réseau Didier Jousse Roscoff, 30 Mars 2010

Transcript of Photovoltaïque: la longue marche vers la parité réseaueer.in2p3.fr/Jousse_D.pdf ·...

Photovoltaïque: la longue marche vers

la parité

réseau

Didier Jousse

Roscoff, 30 Mars 2010

A key player in the solar field

PhotovoltaicElectricity production

from solar rays

CSPElectricity production from

concentrated solar heat

>

Components>

Mirrors>

Pads>

Central recevers

>

Components>

Glass>

Abrasives>

Plastics>

Crucibles

>

PV panels >

Solar

systemsComplete solutions>

AVANCIS

Contenu

Marchés: d’une dynamique portée par les tarifs subventionnés vers la viabilité

économique

Etat du marché

mondialPolitiques d’incitation au rachatTransition vers la parité

réseau

Chaîne de valeur, création d’emplois

Technologies Facteurs clé

dictés par le marché

Compétition c-Si / Couches MincesTechnologies alternatives

Market

grows

at

~30% annual

growth

rate

Courtesy

of European

Photovoltaic

Industry

Association

19%

23%

23%

34%

0% 1%Power Plant

CommercialRoofs

Farm

Roofs

ResidentialRoofs

Off-gridp

6,400

9,000

>10,000

Fortunately, module prices

are continuously

decreasing

with

quantities…

1

Module Price in 2010 ~ $2/Wp

, in 2015 will

be

~$1/Wp

System Price in 2010 ~ $5/Wp

, in 2015 will

be

~$2.5/Wp+ installation = SYSTEM

Module

Market

growth

is

completely

driven

by national Feed-In-Tariff

schemes

Exemple of Germany which

represents

55% of WW market

Germany has been veryexpert in applying

decrease

in tariff

withdecrease

in module prices(-

40% in 2009)

Exemple of Japan

who

hold

N°1 position for many

years

•First subsidized

programme in 1994

•Continuous

support during

12 years

•Stopped

the support in 2005

decrease

in number

of installations in 2006 & 2007

•New programme decided

for 2009 market

is

increasing

again

Exemple of Spain who

reached

N°1 position in 2008 and fell

right after

Too

generoustariff

+ lack

ofvisibility

leadsto bubble

•in 2005: Spain decides

an ambitious

plan for Renewables

with

an objective of 30% of electricity

production

•Purchase

price

of 45c/kWh

•in 2007, the «

cap

»

for PV was

increased

to 1200MW

•for 2009, the cap was

reduced

to 500MW

•Spanish

PV industry

is

still

struggling

to recover

Elements

for a good incentive

programme

Amount

is

adjusted

to give

an IRR between

6 and 10%

No financial

bubble

Smooth

increase

of installed

capacities

Decreases

with

size of installation

Conversion efficiency

is

the same

Distributed

energy

generation

and consumption

Reduced

cost/kWh for large plants

Premium to building vs ground

Less

environment

impact

Good public acceptance

Premium to self-consumption

Reduce

the risk

of grid

overload

Helps

promoting

energy

efficient construction

Put PV on new houses

and buildings

No retroactivity

of decisions

6 months

between

planning and connection

to grid

French FIT scheme: from

bubble

(dec

2009) to smooth

growth

?

Last change (march

2010): the 0,50€/kWh tariff

is

limited

to 250kWp

Is French tariff

a good incentive

programme ?

Amount

is

adjusted

to give

an IRR between

6 and 10%

No financial

bubble

Smooth

increase

of installed

capacities

Decreases

with

size of installation

Conversion efficiency

is

the same

Distributed

energy

generation

and consumption

Reduced

cost/kWh for large plants

Premium to building vs ground

Less

environment

impact

Good public acceptance

Premium to self-consumption

Reduce

the risk

of grid

overload

Helps

promoting

energy

efficient construction

Put PV on new houses

and buildings

No retroactivity

of decisions

6 months

between

planning and connection

N.A.

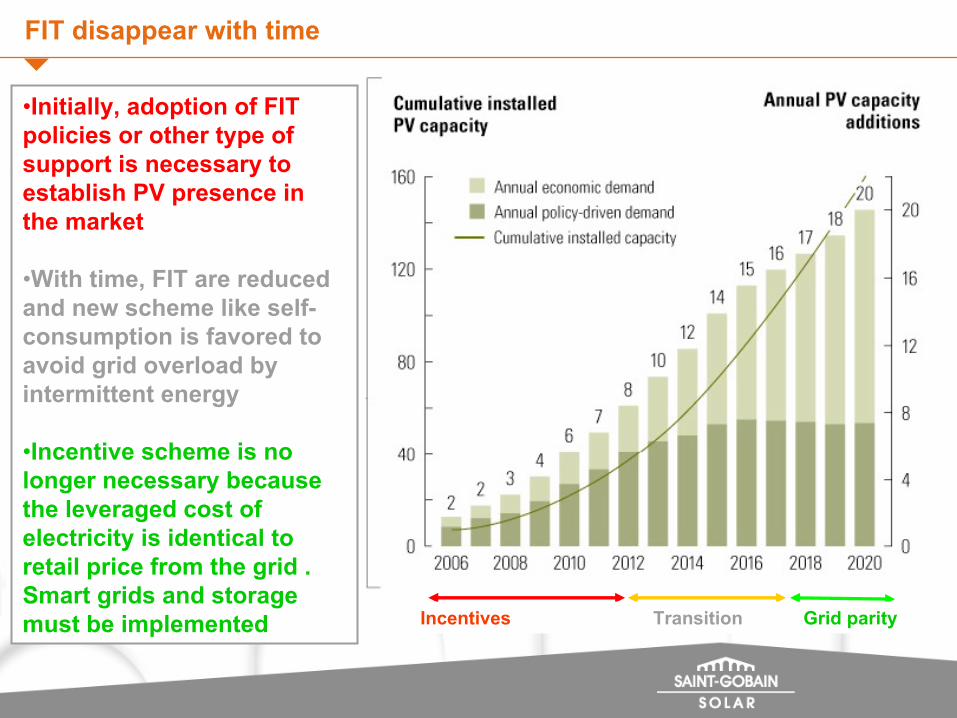

Incentives

Transition

Grid

parity

•Initially, adoption of FIT policies

or other

type of

support is

necessary

to establish

PV presence

in

the market

•With

time, FIT are reduced and new scheme

like

self-

consumption

is

favored

to avoid

grid

overload

by

intermittent energy

•Incentive

scheme

is

no longer necessary

because

the leveraged

cost

of electricity

is

identical

to

retail

price

from

the grid

. Smart grids

and storage

must be

implemented

FIT disappear with time

En Route to “Grid Parity”: Sunny regions strike gold firstDefinition

of grid

parity: Leveraged

Cost

Of Electricity

= retail

price

Source: RWE and Schott Solar

Calculation

relies on a good knowledge

of the kWh produced

over the life of the installation (25y) : illumination level, climate

effects

(T, wind), module degradation

over time, inverter

losses, amount

of financing

and interest

rate. For big

installation, the customer

will

ask

for a warranty

on the kWh output

Source: Deutsche Bank

…several

countries approach

grid

parity: Italy

first, Germany in 2013, France last

2009

2010

Main risks

for PV industry

WW market

must remain

at

more than

10 GW/year

for a few years

in order

to achieve

grid

parity

and escape from

FIT and subsidies

Public deficitsGrowing

eco-skepticism

Volatility

of public opinionOil

price

France will

not reach

grid

parity

before

2015-2020 Change in EDF policy

(multi-energy

versus nuclear)

Insufficient

link

with

the (new) construction sectorInstability

of political

positionning

A french PV company

should

rather

be

active also

in Germany or Italy (or USA) to minimize

risk

Main production areas : Japan

Germany China (Taiwan)

Till 2006: Japanese

and German companies

acquire

leadership thanks to their

internal

marketsSince

2006: China and Taiwan invest massively

in c-Si sector

for exportPrice gap between

German

and Chinese

module (1.7 vs 1.3 €/Wp)c-Si Cells, Modules are commoditiesLarge integrated

manufacturersThin

Film likely

to secure

more value in Europe

Value analysis

and job creation

Rapport PoignantAssemblée NationaleJuillet 2009

Tax

credit

and high

tariff

in France maintains

high

system price

for residential

systems

Installation costs

are higher than

in Germany due to building integration

(in part)

Module cost

goes

down faster than

installation cost

More jobs are expected

in installation and maintenance than

in cell/module manufacturing

Competition

between

asian

actors will

maintain

overcapacities

and low

margins

in c-Si cell/module

Value decomposition (€/Wp)

0

2

4

6

8

10

2009 Res.France

2010 Res.France

2010 Res.Germany

2010 Ground

PV System, installed

Vente/InstallAdm/ConnexBOSModulingCell

Contenu

Marchés: d’une dynamique portée par les tarifs subventionnés vers la viabilité

économique

Etat du marché

mondialPolitiques d’incitation au rachatTransition vers la parité

réseau

Chaîne de valeur, création d’emplois

Technologies Facteurs clé

dictés par le marché

Compétition c-Si / Couches MincesTechnologies alternatives

PV installed

market

in MW in 2007

0

200

400

600

800

1000

1200

Germany Spain USA Japan Italy France Ro

Asia RoW

MW

con

nect

ed

off gridfaçadesresidential

rooffarm

roofcommercial roofpower plant

Key drivers for the technology

Small Residential Large Commercial Ground

Plant€/Wp*€/kWhWp/m2

Aesthetic

(in part)

€/Wp*€/kWh

Warranty

on kWhBuilding compatible

€/Wp*€/kWh

Warranty

on kWhEnvironment

compatible

The market

is largely

technology- agnostic

Who

cares today

if its

TV is

Plasma or LCD ?

Regulations

have an impact on technological

choices

* installed

19%

23%

23%

34%

0% 1%

2009

2010

Exemple: la gamme de toits Saint-Gobain Solar

a

Thin

Film has fewer

process

steps

all in one place, more efficient cost

down with quantities

but…proven

Cryst-Silicon

technology

has a better

image of durability

+ -+ -+ -

On-glass monolithicIntegration

Scribe 1 Scribe 2 Scribe 3

Veeco

All the physics

of PV in one page !

Absorptioncoefficient

determinescell

thickness

c-Si = 80µmThinFilm=1µm

No (efficient) transparent

PV !!!

Main Thin

Film technologies in one page !!

1 µm

Silicium

Ag

TCO

Glass Substrate

IntercalaireGlass

SiOSn

a-Si:H

/ µc-Si:H

SnO2:F

Ag1 µmMetallic reflecting layer

Absorber

Transparent layer TCO

nip

PE-CVD

PE-CVD, HW-CVD

Sputtering, evaporation

a-Si:H, µc-Si:HPLX or Diamant

Solar + TCO

PLX

SnO2

: FCdS

CdTe

ZnTe:CuAl, Ti

TCOCouche

tampon

Absorber

Metallic reflecting layer

n

p

Couche

adhésion

Glass Substrate

IntercalaireGlass

PE-CVDChemical bath deposition

Closed Spaced

SublimationSCS

sputtering evaporation

CdTePLX or Diamant

Solar + TCO

PLX

TCO = Transparent Conducting Oxide = SnO2:F or ZnO:Al

Mo

CuInSe

CdSZnO

IntercalaireGlass

Glass Substrate

TCOCouche

tampon

Absorber

Metallic reflectinglayer sputtering

Chemical bath deposition

CVD, sputtering

Souttering/sélénisationOU Co-evaporation

CIGS

2 µm

Float Diamant

Solar

PLX + Mo

Some

materials

can

be

coated

on flexible substrates

with

Roll-to-Roll manufacturing

:

Foil a-Si CIGS

Metal Unisolar, Fuji ,

Xunlight

Global Solar, Miasolé, Nanosolar, Odersun, Solopower, Nexcis

Polymer Flexcell Ascent

Solar, Solarion

The graph that

keeps

all of us alive

NB : best cell

lab

module -2% , lab

module industrial

-2%

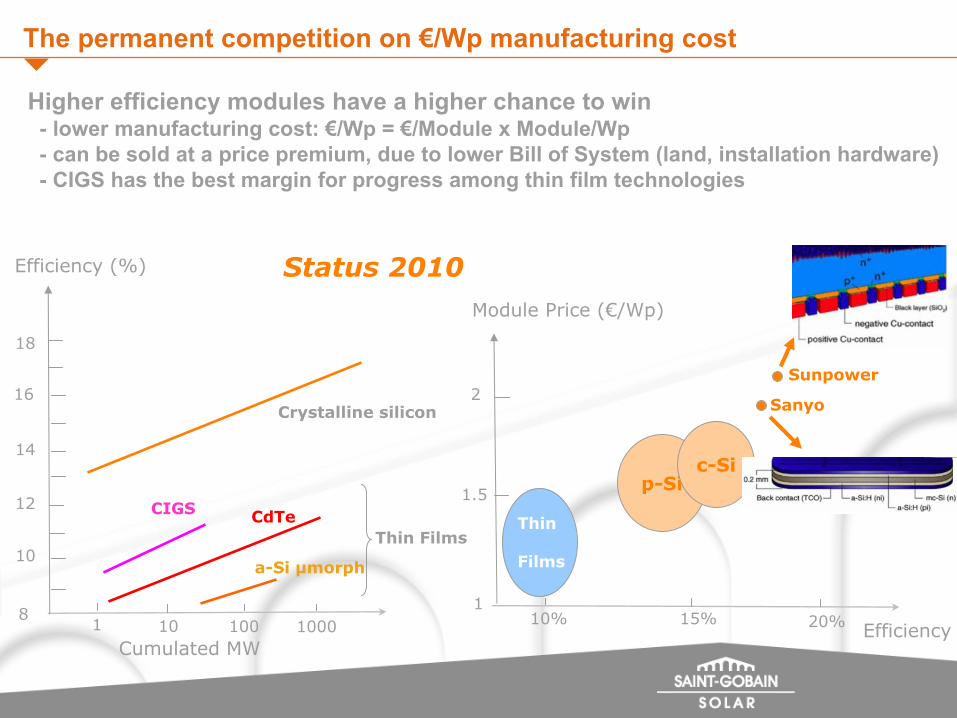

Higher

efficiency

modules have a higher

chance to win -

lower

manufacturing

cost: €/Wp

= €/Module x Module/Wp -

can

be

sold

at

a price

premium, due to lower

Bill of System (land, installation hardware) -

CIGS has the best margin

for progress

among

thin

film technologies

The permanent competition

on €/Wp

manufacturing

cost

16

Efficiency

(%)

12

14

18

20%

10

Efficiency

Module Price (€/Wp)

15%

p-Sic-Si

Sanyo

Sunpower

Cumulated

MW

a-Si µmorph

CdTe

8

CIGS

1 10 100 10%

Thin

Films

1

1.5

2

1000

Thin

Films

Crystalline

silicon

Status

2010

Importance of good timing: the success

story of First Solar

Shortage

of c-Si in the 2005-2008 period

maintains

high

module price

First Solar

was

able to sell

its

first modules above

$2/Wp

operating margin

of 40% in spite of huge

ramp-up costs

Installed

capacity

in 2010= 1200 MW

AVANCIS -

a large-scale technological and industrial challenge

> AVANCIS : 29 years in photovoltaic1981 ARCO Solar starts initial R&D on CIGS1990

Siemens Solar acquires ARCO Solar1998 Start of commercial CIGS production in Camarillo, CA2002

Shell Solar acquires Siemens Solar2004

Development of RTP process in Munich2006

Shell and Saint-Gobain form AVANCIS2009 AVANCIS becomes 100% Saint-Gobain

> An R&D centre in MunichAn experimental production line for 60 Wp

modules15.1% module efficiency demonstratedA test site for modules

> An ambitious program of production linesSince October 2008

the first 20 MW

plant in Torgau

(Germany) on a Saint-Gobain Glass siteProgram of fast industrial development on modular units

of 100 to 300 MW

Solar wall of the OpTIC

centre in North Wales

R&D centre in Munich

Plant in Torgau

Arguments in favor

of Thin

Films : kWh/kWp

efficiency

•Better

response

at

small

illumination levels(few %)

•STC measured

at

1000 W/m2, real life at

~300•This is

valid

for all thin

film technologies

•Better

behavior

at

elevated

temperatures(few %)

•Temperature

coefficient is

semiconductor related

•Valid

for CdTe

and a-Si only

•A-Si gives

higher

kWh/kWp

than

others(+ few %)

•due to above

factors

+ module makers

rating their

nominal power as «

stabilized

efficiency

»

Arguments in favor

of Thin

Films : Energy

Pay-Back

Time & CO2 content

•Recycling

policies

in place : PV Cycle, First Solar

•Chemical

availability

of some

elements

will

become

a concern

(after

10GW)•Issues for Te, In new phases like

new alloy

of Cu-Sn-Zn-S or-Se by IBM (2010)

V. Fthenakis

et al., PV-SEC Hamburg, 2009

c-Si case studyREC

Thin

Film case study: First Solar

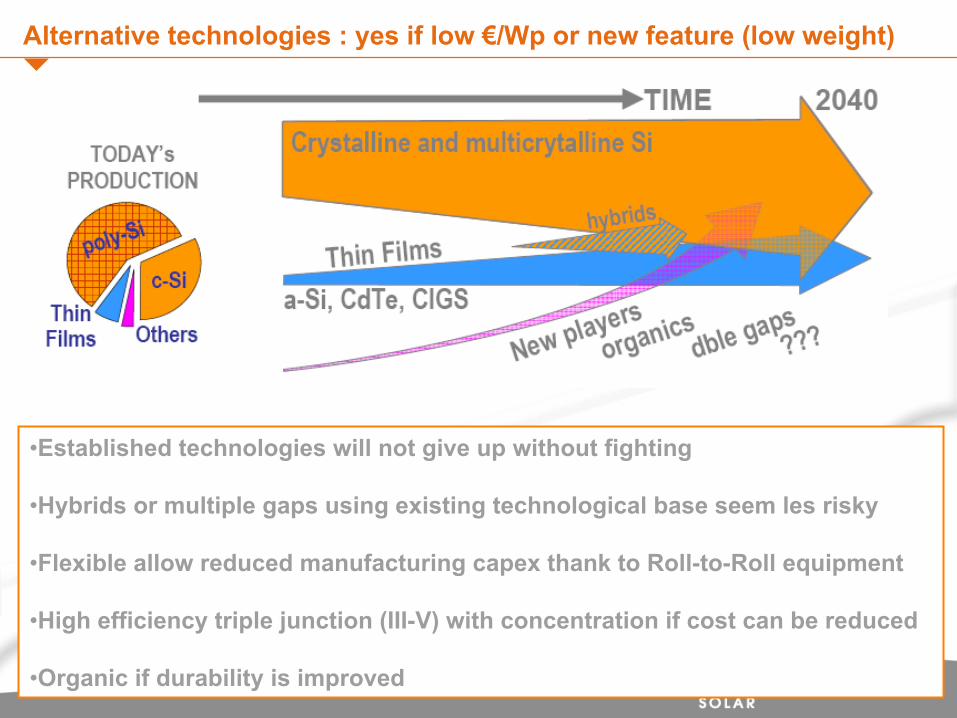

Alternative technologies : yes

if low

€/Wp

or new feature

(low

weight)

•Established

technologies will

not give

up without

fighting

•Hybrids

or multiple gaps using

existing

technological

base seem

les risky

•Flexible allow

reduced

manufacturing

capex

thank

to Roll-to-Roll equipment

•High efficiency

triple junction

(III-V) with

concentration if cost

can

be

reduced

•Organic

if durability

is

improved

Contact:

Thank youSG Solar

Sunstyle®

: 9MW being installed in Perpignan

Sources: H2G (Jacques Schmitt), EPIA, DB, Rapport PoignantSaint-Gobain RechercheSaint-Gobain SolarSaint-Gobain Solar

SystemsAVANCIS