WORK STEALING SCHEDULER 6/16/2010 Work Stealing Scheduler 1.

Upload

donna-lindseyCategory

view

217download

1

Pharmacy 2006

“Protecting Your Bottom Line: Strategies for Preventing Fraud and

Shop Stealing”

8 September 2006

Dean NewlanPartner

2

Overview

+ Pharmacy exposures to commercial crime

+ Shrinkage and fraud

+ Why do people steal?

+ The ECR “Shrinkage Reduction Roadmap”

+ Strategies for controlling fraud in retail

3

Commercial crime against pharmacies

+ Burglary (after hours “ram raids” increasing in frequency)

+ Armed robbery

+ Extortion (product contamination)

+ Theft of cash by staff (under-ringing of sales)

+ Internal fraud (other than cash theft)

+ Staff theft of inventory

+ External theft of inventory

+ Vendor fraud

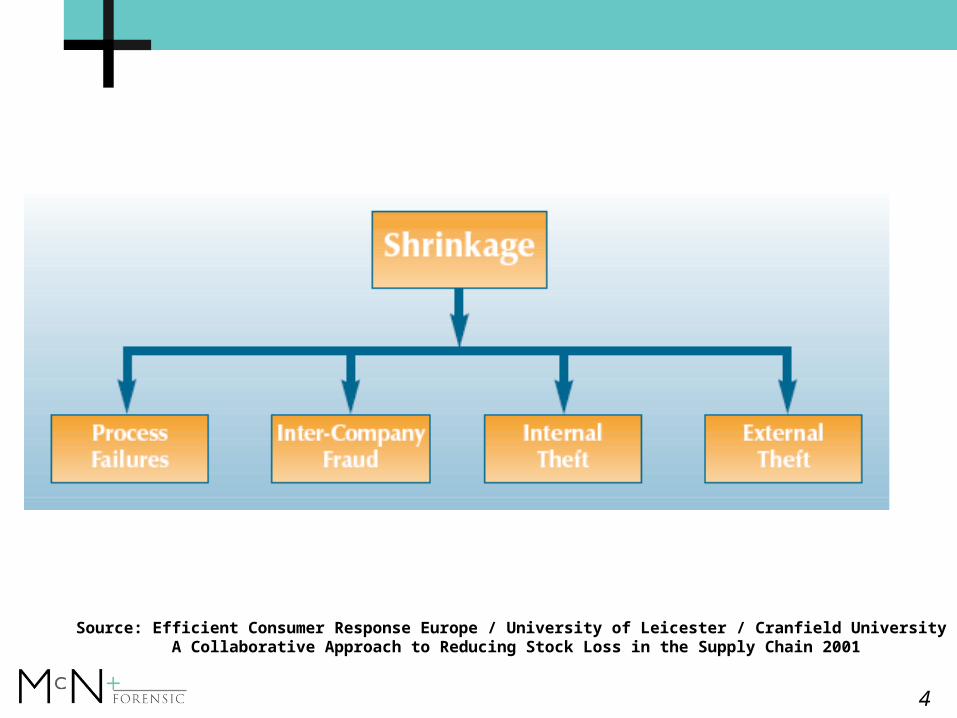

Shrinkage

4

Source: Efficient Consumer Response Europe / University of Leicester / Cranfield University A Collaborative Approach to Reducing Stock Loss in the Supply Chain 2001

5

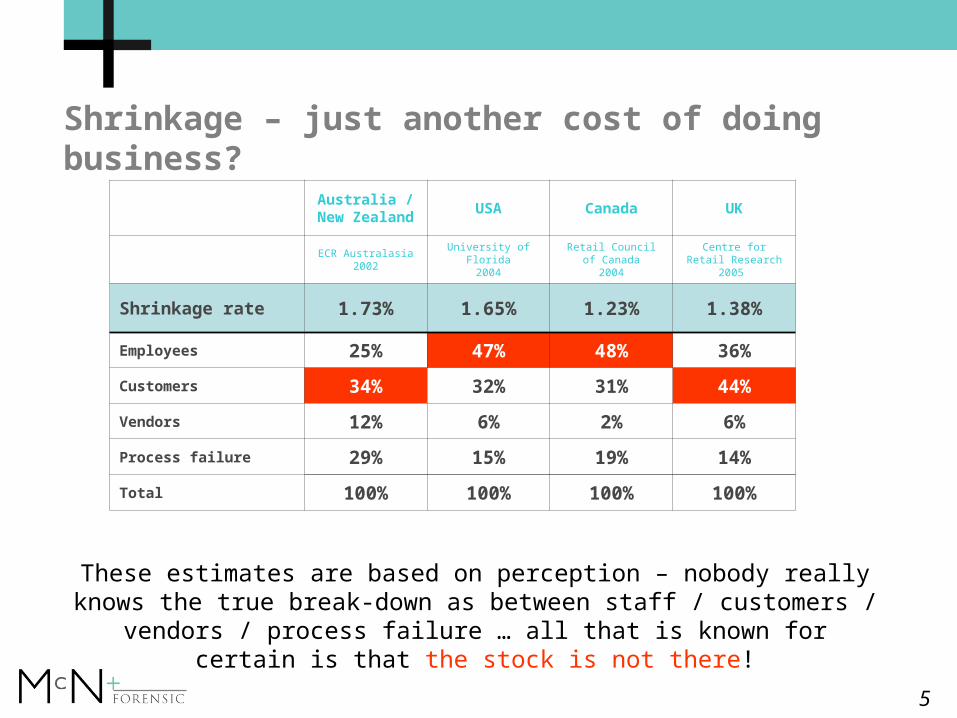

Shrinkage – just another cost of doing business?

Australia / New Zealand

USA Canada UK

ECR Australasia 2002

University of Florida2004

Retail Council of Canada

2004

Centre for Retail Research

2005

Shrinkage rate 1.73% 1.65% 1.23% 1.38%

Employees 25% 47% 48% 36%

Customers 34% 32% 31% 44%

Vendors 12% 6% 2% 6%

Process failure 29% 15% 19% 14%

Total 100% 100% 100% 100%

These estimates are based on perception – nobody really knows the true break-down as between staff / customers / vendors / process failure … all

that is known for certain is that the stock is not there!

6

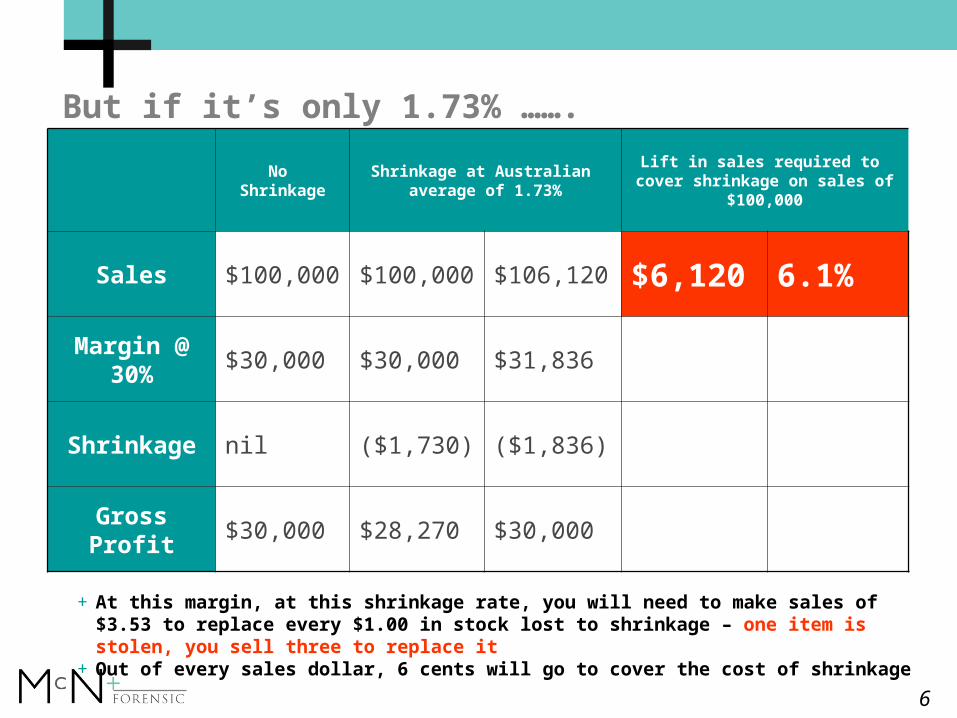

No Shrinkage

Shrinkage at Australian average of 1.73%

Lift in sales required to cover shrinkage on sales of

$100,000

Sales $100,000 $100,000 $106,120 $6,120 6.1%

Margin @ 30%

$30,000 $30,000 $31,836

Shrinkage nil ($1,730) ($1,836)

Gross Profit $30,000 $28,270 $30,000

But if it’s only 1.73% …….

+ At this margin, at this shrinkage rate, you will need to make sales of $3.53 to replace every $1.00 in stock lost to shrinkage – one item is stolen, you sell three to replace it

+ Out of every sales dollar, 6 cents will go to cover the cost of shrinkage

7

Sh

rin

kag

e lo

ss

Cost of Prevention

$1000 $2000 $3000 $4000 $6000$5000 $7000 $8000

$1000

$2000

$3000

$4000

$6000

$5000

$7000

$8000

Equilibrium point reached at $2900

Too much spent on shrinkage reduction

Too little spent on shrinkage reduction

In the US, security costs are estimated to be .51% of turnover

(National Retail Security Survey)

8

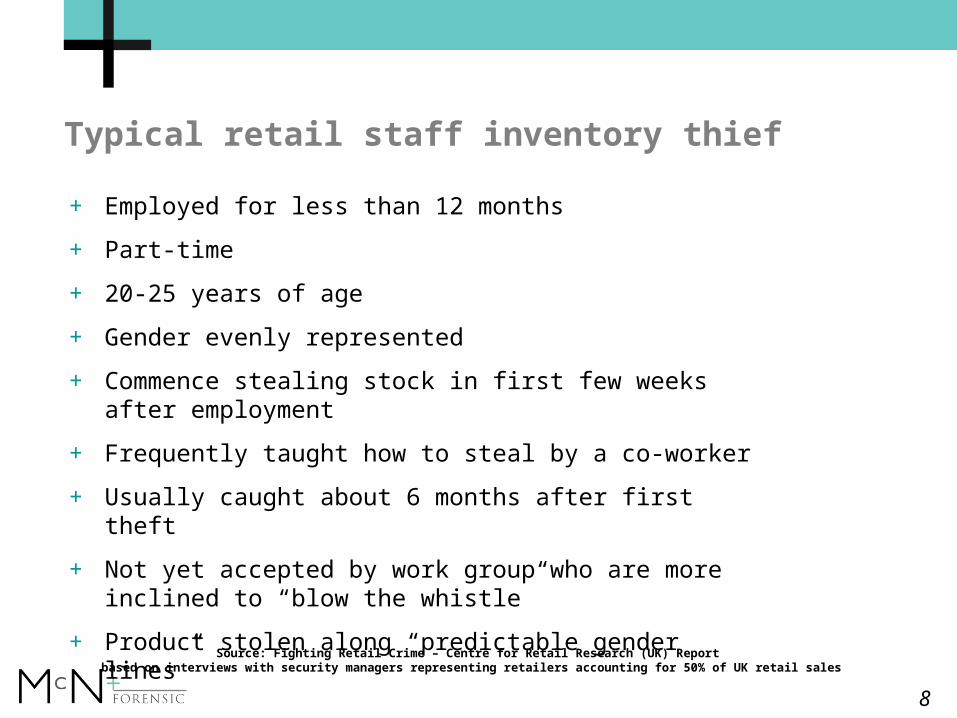

Typical retail staff inventory thief

+ Employed for less than 12 months

+ Part-time

+ 20-25 years of age

+ Gender evenly represented

+ Commence stealing stock in first few weeks after employment

+ Frequently taught how to steal by a co-worker

+ Usually caught about 6 months after first theft

+ Not yet accepted by work group who are more inclined to “blow the whistle”

+ Product stolen along “predictable gender lines”

Source: Fighting Retail Crime – Centre for Retail Research (UK) Report based on interviews with security managers representing retailers accounting for 50% of UK retail sales

9

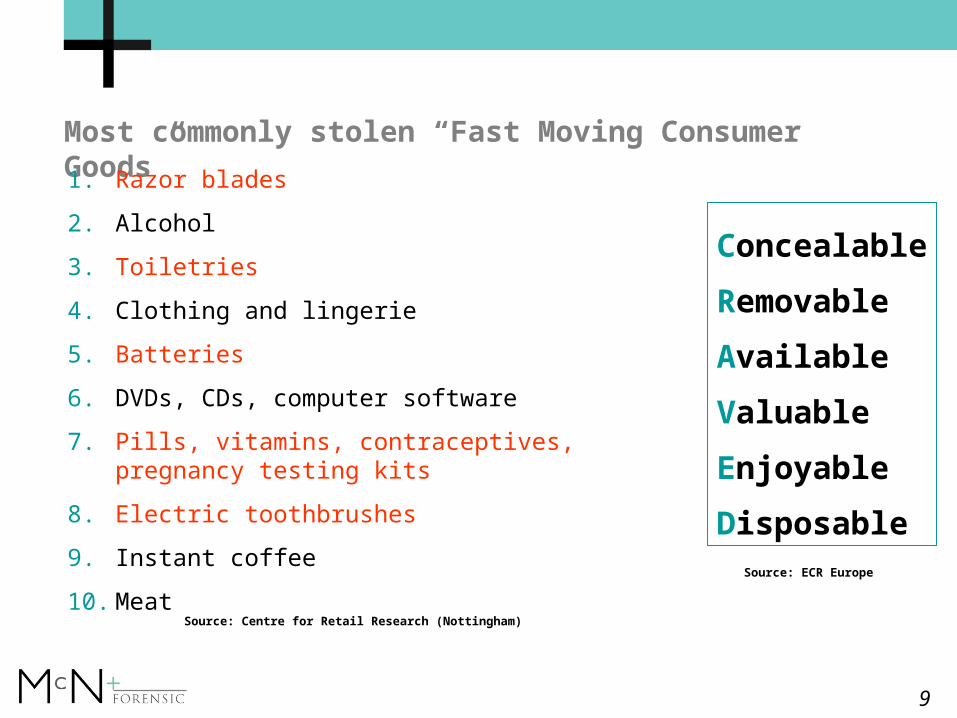

Most commonly stolen “Fast Moving Consumer Goods”

1. Razor blades

2. Alcohol

3. Toiletries

4. Clothing and lingerie

5. Batteries

6. DVDs, CDs, computer software

7. Pills, vitamins, contraceptives, pregnancy testing kits

8. Electric toothbrushes

9. Instant coffee

10. MeatSource: Centre for Retail Research (Nottingham)

Concealable

Removable

Available

Valuable

Enjoyable

DisposableSource: ECR Europe

10

A few shrinkage misconceptions

Shrinkage control is not core retail activity

Shrinkage is just a cost of doing business – we would be better off if we focused on the top line

Shrinkage is inevitable

The best way to control shrinkage is to focus resources on preventing customer theft

Line management are not responsible for controlling shrinkage – that’s the job of the loss prevention department

Floor staff have no role in preventing shrinkage – they are there to sell, not look after the stock

11

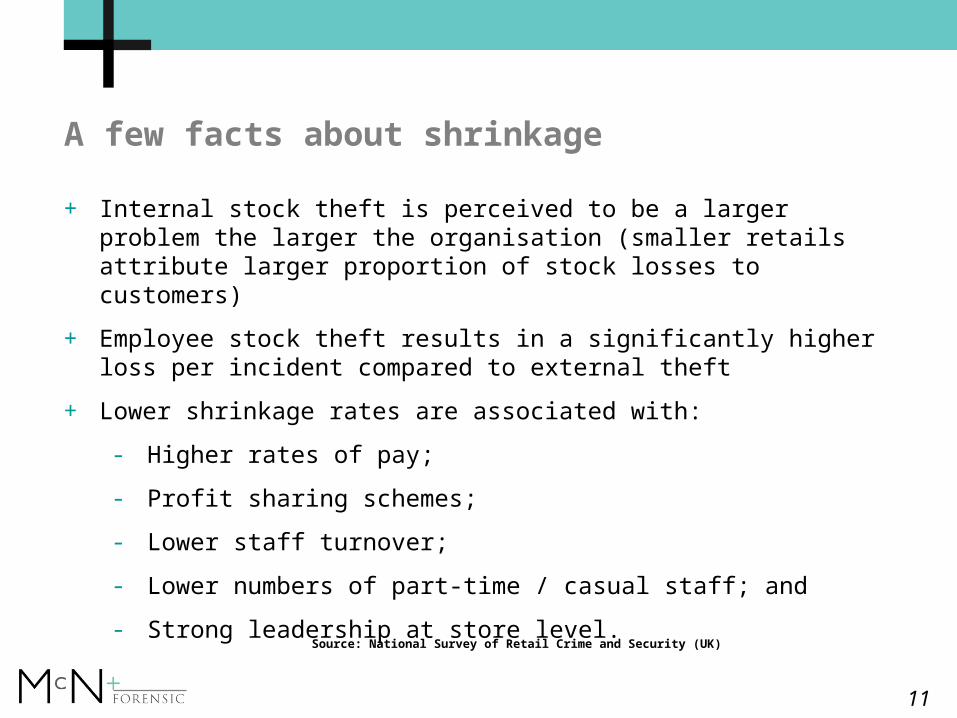

A few facts about shrinkage

+ Internal stock theft is perceived to be a larger problem the larger the organisation (smaller retails attribute larger proportion of stock losses to customers)

+ Employee stock theft results in a significantly higher loss per incident compared to external theft

+ Lower shrinkage rates are associated with:

- Higher rates of pay;

- Profit sharing schemes;

- Lower staff turnover;

- Lower numbers of part-time / casual staff; and

- Strong leadership at store level.

Source: National Survey of Retail Crime and Security (UK)

12

Staff fraud in the retail sector

+ On-line banking fraud

+ Unauthorised mark-downs (sweet-hearting for family / friends)

+ Refund fraud

+ Gift voucher theft or manipulation

+ Staff discount fraud (family / friends)

+ Loyalty card fraud (swipe own loyalty card)

+ Under-ringing sales

+ Credit card fraud

+ Lapping (substituting credit card vouchers for cash)

13

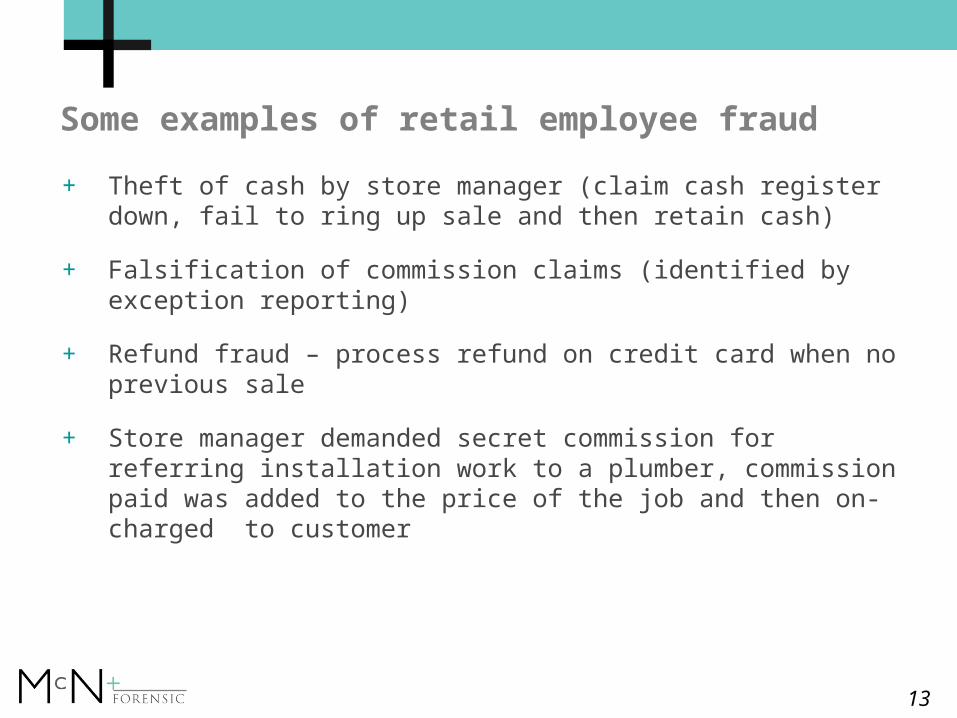

Some examples of retail employee fraud

+ Theft of cash by store manager (claim cash register down, fail to ring up sale and then retain cash)

+ Falsification of commission claims (identified by exception reporting)

+ Refund fraud – process refund on credit card when no previous sale

+ Store manager demanded secret commission for referring installation work to a plumber, commission paid was added to the price of the job and then on-charged to customer

14

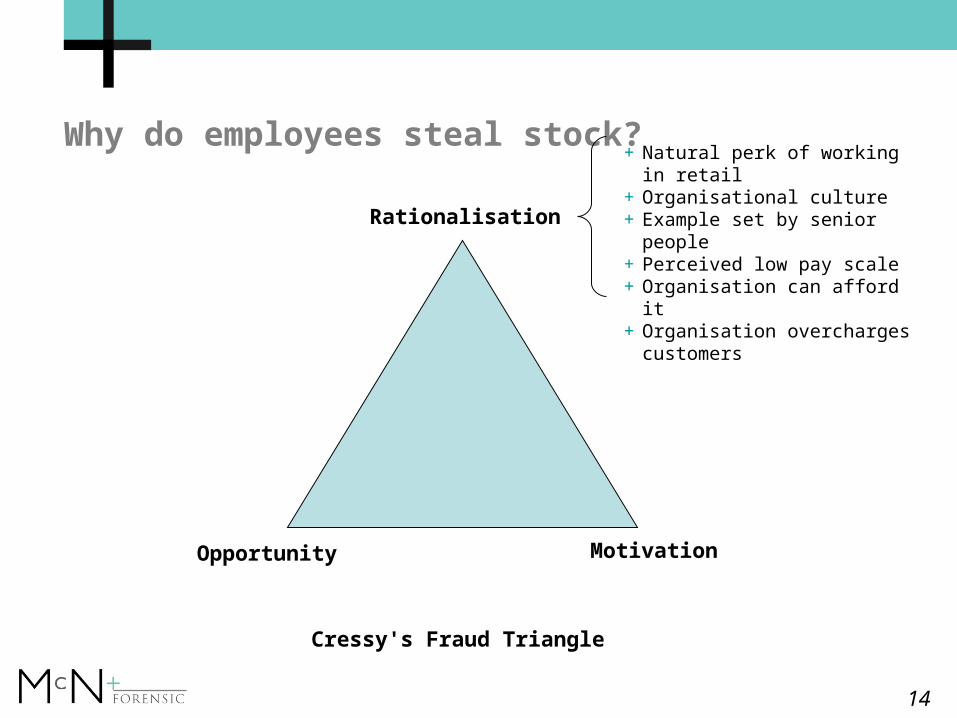

Why do employees steal stock?

Cressy's Fraud Triangle

MotivationOpportunity

Rationalisation

+ Natural perk of working in retail+ Organisational culture+ Example set by senior people+ Perceived low pay scale+ Organisation can afford it+ Organisation overcharges

customers

15

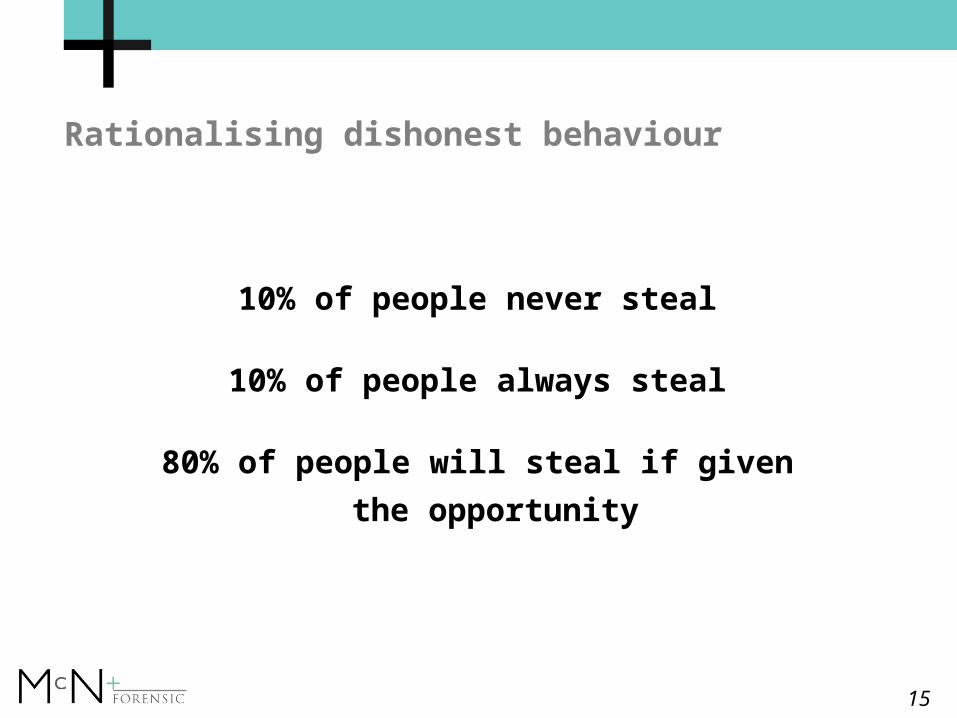

10% of people never steal

10% of people always steal

80% of people will steal if given the

opportunity

Rationalising dishonest behaviour

16

ECR Shrinkage Reduction Roadmap

Source: Efficient Consumer Response Europe / University of Leicester / Cranfield University A Collaborative Approach to Reducing Stock Loss in the Supply Chain 2001

17

Steps to reducing shrinkage

Written company shrinkage policy

Adopt a “whole of business” approach to shrinkage reduction

High levels of intra-company co-operation – accurate measurement

Watch margin closely and investigate variances

Staff incentives program / profit share

Avoid blind spots in display areas / convex mirrors

Regular stock takes

CCTV (no dummy camera domes longer storage cycle)

Warning at entry to store

Staff training

Conduct regular shrinkage reduction projects

Electronic Data Tagging (EAS / RFID / Smart Cards / Source Tagging)

Realign sales staff responsibilities

Data mining to look for indicative pattern (location, employee, time of day)

18

Fraud and corruption control – AS 8001 Fraud and Corruption

Standard

Section 2 Planning and Resourcing

Section 3 Prevention

Section 4 Detection

2.1 Fraud and corruption control planning

2.2 Review of the fraud and corruption control plan

2.3 Fraud and corruption control resources

2.4 Internal audit activity in fraud and corruption control

Section 5 Response

3.1 Implementing and maintaining an integrity framework

3.2 Senior Management commitment to controlling the risks of fraud and corruption

3.3 Line management accountability

3.4 Internal control

3.5 Assessing fraud and corruption risk

3.6 Communication and awareness

3.7 Employment screening

3.8 Supplier and customer vetting

4.1 Implementing a fraud and corruption detection program

4.2 Role of the external auditor in detection of fraud

4.3 Mechanisms for reporting suspected incidents

4.4 Whistleblower protection program

5.1 Investigation

5.2 Internal reporting and escalation

5.3 Disciplinary procedures

5.4 External reporting

5.5 Civil action for recovery of losses

5.6 Review of internal controls

5.7 Insurance

19

Steps to reducing fraud (other than staff theft) Apply relevant parts of Fraud and Corruption Control as 8001-2003

Scrupulous control over on-line banking

Tighten internal controls

Fraud risk assessment

Data mining – look for indicators of fraudulent activity

Increase awareness of relevant managers and staff

Set the example as owners / managers

Job rotation / annual leave policy

Alternative reporting avenues (whistleblower line)

20

Dean NewlanMcGrathNicol+Forensic

Telephone 61 3 9038 3151Mobile 0412 731 040Email [email protected]