Performance of the NE Multispecies Fishery (May 2013 … Final Report on the Performance of the...

111

Northeast Fisheries Science Center Reference Document 15-02 2013 Final Report on the Performance of the Northeast Multispecies (Groundfish) Fishery (May 2013 – April 2014) by Tammy Murphy, Andrew Kitts, Chad Demarest, and John Walden

-

Upload

duonghuong -

Category

Documents

-

view

215 -

download

0

Transcript of Performance of the NE Multispecies Fishery (May 2013 … Final Report on the Performance of the...

Northeast Fisheries Science Center Reference Document 15-02

2013 Final Report on thePerformance of the Northeast

Multispecies (Groundfish) Fishery(May 2013 – April 2014)

by Tammy Murphy, Andrew Kitts, Chad Demarest, and John Walden

Northeast Fisheries Science Center Reference Document 15-02

U.S. DEPARTMENT OF COMMERCENational Oceanic and Atmospheric Administration

National Marine Fisheries ServiceNortheast Fisheries Science Center

Woods Hole, MassachusettsJanuary 2015

2013 Final Report on thePerformance of the Northeast

Multispecies (Groundfish) Fishery(May 2013 – April 2014)

by Tammy Murphy, Andrew Kitts, Chad Demarest, and John Walden

NOAA Fisheries, Northeast Fisheries Science Center, 166 Water Street, Woods Hole, MA 02543

Northeast Fisheries Science Center Reference Documents

This series is a secondary scientific series designed to assure the long-term documentation and to enable the timely transmission of research results by Center and/or non-Center researchers, where such results bear upon the research mission of the Center (see the outside back cover for the mission statement). These documents receive internal scientific review, and most receive copy editing. The National Marine Fisheries Service does not endorse any proprietary material, process, or product mentioned in these documents. All documents issued in this series since April 2001, and several documents issued prior to that date, have been copublished in both paper and electronic versions. To access the electronic version of a document in this series, go to http://www.nefsc.noaa.gov/nefsc/publications/. The electronic version is available in PDF format to permit printing of a paper copy directly from the Internet. If you do not have Internet access, or if a desired document is one of the pre-April 2001 documents available only in the paper version, you can obtain a paper copy by contacting the senior Center author of the desired document. Refer to the title page of the document for the senior Center author’s name and mailing address. If there is no Center author, or if there is corporate (i.e., non-individualized) authorship, then contact the Center’s Woods Hole Labora-tory Library (166 Water St., Woods Hole, MA 02543-1026). Information Quality Act Compliance: In accordance with section 515 of Public Law 106-554, the Northeast Fisheries Science Center completed both technical and policy reviews for this report. These predissemination reviews are on file at the NEFSC Editorial Office. This document may be cited as:

Murphy T, Kitts A, Demarest C, Walden J. 2015. 2013 Final report on the performance of the northeast multispecies (groundfish) fishery (May 2013 – April 2014). US Dept Commer, Northeast Fish Sci Cent Ref Doc. 15-02; 106 p. Available from: National Marine Fisheries Service, 166 Water Street, Woods Hole, MA 02543-1026, or online at http://www.nefsc.noaa.gov/nefsc/publications/

TABLE OF CONTENTS

Table of Contents ........................................................................................................................1

List of Tables ..............................................................................................................................3

List of Figures .............................................................................................................................5

Executive Summary ....................................................................................................................6

1. Introduction ........................................................................................................................... 10

1.1. Data and Analytical Approach..................................................................................... 13

1.2. Performance of Sector and Common Pool Vessels ...................................................... 15

2. Landings and Gross Revenues ............................................................................................... 17

2.1. Landings ..................................................................................................................... 17

2.2. Gross Revenues .......................................................................................................... 18

2.2.1. Revenues by Landing Port and Home Port ........................................................... 18

2.2.2. Revenues by Species ............................................................................................ 20

2.3. Prices .......................................................................................................................... 22

3. Number of Vessels and Effort ............................................................................................... 23

3.1. Number of Vessels ...................................................................................................... 23

3.1.1. Number of Active Vessels by Home Port ............................................................. 24

3.1.2. Number of Active Vessels by Vessel Size ............................................................ 25

3.2. Number of Trips, Days Absent, and Trip Length ......................................................... 25

4. Economic Performance ......................................................................................................... 27

4.1. Revenue per Vessel ..................................................................................................... 28

4.2. Fleet Productivity ........................................................................................................ 28

5. ACE Leasing ......................................................................................................................... 29

5.1. Market Structure, Size, and Characteristics ................................................................. 30

5.2. Prices .......................................................................................................................... 31

5.3. Transfer Payments ...................................................................................................... 32

5.4. Transactions Costs ...................................................................................................... 32

6. Distributional Issues .............................................................................................................. 33

6.1. Number of Vessel Affiliations ..................................................................................... 34

6.2. Distribution of Revenue among Vessels ...................................................................... 34

1

6.3. Distribution of Revenue among Vessel Affiliations ..................................................... 35

6.4. Distribution of Revenue Using Lorenz Curves and Gini Coefficients .......................... 36

6.5. Consolidation and Concentration of Revenue among Vessel Affiliations ..................... 36

7. Employment .......................................................................................................................... 37

7.1. Number of Crew Positions .......................................................................................... 37

7.2. Number of Crew Trips ................................................................................................ 38

7.3. Number of Crew Days ................................................................................................ 38

8. Net Revenues ........................................................................................................................ 39

8.1. Average Owner and Crew Shares Per Day .................................................................. 41

8.2. Average Owner and Crew Shares per Vessel ............................................................... 42

8.3. Aggregate Owner and Crew Shares ............................................................................. 42

9. Concluding Remarks ............................................................................................................. 42

10. Acknowledgments ............................................................................................................... 43

11. References ........................................................................................................................... 44

2

LIST OF TABLES Table 1. Summary of major trends (May through April, includes all vessels with a valid limited access multispecies permit). ........................................................................................................8 Table 2. Total landings and revenue from all trips by fishing year in 2010 dollars (May through April). ....................................................................................................................................... 46 Table 3. Total landings and revenue from groundfish trips by fishing year in 2010 dollars (May through April. ........................................................................................................................... 46 Table 4. Value of landings of all species by state and port of landing in 2010 dollars (May through April, all trips). ............................................................................................................. 47 Table 5. Value of landings of all species by home port state and home port in 2010 dollars (May through April, all trips). ............................................................................................................. 48 Table 6. Value of landings of groundfish by state and port of landing in 2010 dollars (May through April, all trips). ............................................................................................................. 49 Table 7. Value of landings of groundfish by home port state and home port in 2010 dollars (May through April, all trips). ............................................................................................................. 50 Table 8. Value and landed pounds of nine allocated groundfish species* landed by limited access groundfish vessels in 2010 dollars (May through April). ........................................................... 51 Table 9. Value and landed pounds of top ten non-groundfish species* landed by limited access groundfish vessels in 2010 dollars (May through April). ........................................................... 52 Table 10. Number of vessels by fishing year (May through April). ............................................ 53 Table 11. Number of vessels with revenue from any species (all trips) by home port state. ........ 54 Table 12. Number of vessels with revenue from at least one groundfish trip by home port state.55 Table 13. Number of vessels with revenue from any species by vessel size category. ................ 56 Table 14. Number of vessels with revenue from at least one groundfish trip by vessel size category. ................................................................................................................................... 56 Table 15. Effort by active vessels (May through April). ............................................................ 57 Table 16. Average revenue per active vessel in 2010 dollars (May through April).* .................. 60 Table 17. Lowe Index (2007=1) of productivity change for the limited access groundfish fleet. 61 Table 18. Number of MRIs leasing ACE and/or PSC and amount of live pounds caught by home port state. .................................................................................................................................. 61 Table 19. Number of vessel affiliations leasing ACE and/or PSC by home port state and amount of live pounds caught. ............................................................................................................... 62 Table 20. Number of lessee MRIs by vessel size category. ........................................................ 63 Table 21. ACE and PSC lease markets by stock (live pounds). .................................................. 64 Table 22. Total allocated ACE and catch by vessel size category............................................... 65 Table 23. Volume of between-sector ACE leases by stock (live pounds). .................................. 66 Table 24. Number of between-sector ACE lease transactions, by month and fishing year. ......... 67 Table 25. ACE lease prices from hedonic model. ...................................................................... 69 Table 26. ACE lease prices from weighted mean values for single stock leases. ........................ 70

3

Table 27. Ex-vessel and ACE lease prices. ................................................................................ 71 Table 28. Transfer payments from ACE and PSC leasing by stock at the MRI level. ................. 72 Table 29. Transfer payments from ACE and PSC leasing by stock at the vessel affiliation level. ................................................................................................................................................. 74 Table 30. Transfer payments from ACE and PSC leasing by lessee home port state. ................. 76 Table 31. Stock level catch, ACE, and utilization. ..................................................................... 78 Table 32. Number of vessel affiliations by fishing year. ............................................................ 80 Table 33. Number and percentage of vessel affiliations by number of active vessels owned. ..... 81 Table 34. Distribution of revenue from all species (all trips) among vessels. ............................. 82 Table 35. Distribution of revenue from groundfish (all trips) among vessels. ............................. 83 Table 36. Distribution of revenue from all species (all trips) among vessel affiliations. ............. 84 Table 37. Distribution of groundfish revenue among vessel affiliations. .................................... 85 Table 38. Number of vessel affiliations with revenue from all species by cumulative (on all trips) quartiles (ordered high revenue to low). .................................................................................... 86 Table 39. Number of vessel affiliations with revenue from groundfish by cumulative (on all trips) quartiles (ordered high revenue to low). ........................................................................... 86 Table 40. Changes in employment indicators by vessel size category (May through April, all trips). ........................................................................................................................................ 87 Table 41. Changes in employment indicators by home port state (May through April, all trips). 88 Table 42. Per day trip cost averages (in 2010 dollars). ............................................................... 90 Table 43. Per day values for groundfish trips (in 2010 dollars). ................................................. 91 Table 44. Per day values for non-groundfish trips (in 2010 dollars). .......................................... 92 Table 45. Average owner and crew share per vessel (in 2010 dollars). ....................................... 93 Table 46. Aggregate owner and crew shares by vessel size category (in 2010 dollars). .............. 93 Table 47. Aggregate owner and crew shares by homeport state (in 2010 dollars). ...................... 94

4

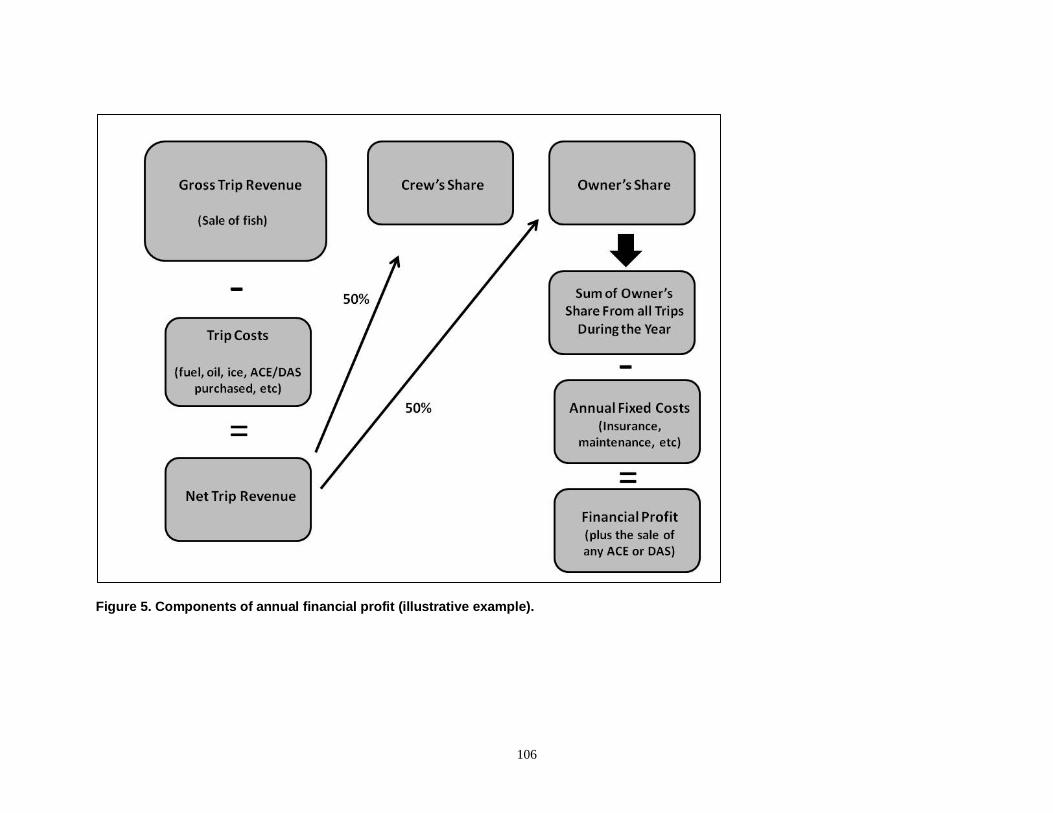

LIST OF FIGURES Figure 1. Yearly average price (in 2010 dollars) of combined groundfish vs. other species. ....... 95 Figure 2. Yearly average price (in 2010 dollars) by allocated groundfish species. ...................... 96 Figure 3. Quantity adjusted groundfish price index (base period = May through July 2007). ..... 97 Figure 4. 2013 catch and allocated ACE by vessel size category for individual stocks. ............ 102 Figure 5. Number of vessel affiliations with revenue from any species by total revenue category. ............................................................................................................................................... 103 Figure 6. Lorenz curves and Gini values at the affiliated vessel level for all species revenues (from active vessels). .............................................................................................................. 104 Figure 7. Lorenz curves and Gini values at the affiliated vessel level for groundfish revenues (from active vessels). .............................................................................................................. 105 Figure 8. Components of annual financial profit (illustrative example). ................................... 106

5

EXECUTIVE SUMMARY

This report provides an evaluation of the economic and social performance of active limited access Northeast groundfish vessels for the 2013 fishing year (May 2013 through April 2014). Table 1 contains a summary of major trends for the fishery for the period 2010-2013. The report focuses on trends from 2010 onward and on changes that occurred between 2012 and 2013. An important difference in this year’s report from previous reports is that all monetary metrics are presented in constant dollars that have been adjusted for inflation, using 2010 as the base year, rather than in nominal terms. Revenue and price metrics for the 2013 fishing year in Table 1, Table 2, and Table 3 have been presented in nominal terms (in addition to real, or constant, terms).

Fishing Year 2013 saw a continuation of the mostly negative trends seen for the limited access groundfish fleet in Fishing Year 2012 compared with the landings and revenues seen in the fishery from 2010 to 2011. The total amount of Annual Catch Entitlement (ACE) for all the allocated groundfish species declined 13% from 2012 to 2013, which is a 27.5% reduction from 2010.

Annual Catch Limits (ACLs) for 12 of the 17 allocated stocks were cut from 2012 to 2013: all three cod stocks, all three haddock stocks, all three yellowtail flounder stocks, plaice, witch flounder, and GOM winter flounder. ACLs increased from their 2012 levels for five stocks: Georges Bank and Southern New England (allocated for the first time in 2013) winter flounder, redfish, white hake, and pollock.

Groundfish fishermen could not offset a substantial loss of $28 million in groundfish revenues (in real dollars) between 2010 and 2013 with increases in non-groundfish revenues. Revenue is determined by both landings and price, and groundfish landings in 2013 continued the decline that the limited access groundfish fleet experienced in 2012. Declining groundfish landings were coupled with little growth in non-groundfish landings for the fleet in 2013. Total landings of all species on all trips were 256.4 million pounds in 2013, a 1.6% decrease from 2012 (260.5 million pounds). Total groundfish landings on all trips decreased to a four-year low of 42.2 million pounds in 2013, compared with 58.7 million pounds in 2010.

Both average groundfish price and average non-groundfish prices received by the fleet fell in 2013 to four-year lows. In 2010 dollars, average groundfish price was $1.31 per pound in 2013 (from $1.42 in 2010) and average non-groundfish price was $1.00 per pound (from $1.21 in 2010). The fall in average groundfish price is especially notable given that groundfish landings also decreased to a four-year low of 42.2 million pounds in 2013. This does not mean that there were both price and quantity declines in all groundfish species; this only occurred with cod, plaice, and redfish. There was also a change in the mix of quantities of groundfish landed with decreases in shares of cod (and a concurrent drop in price) and pollock (small increase in price) and increases in the shares of winter flounder and haddock (with decreases in prices in both of these species).

The result of these landings and price changes is that total groundfish revenue was at a four-year low of $55.2 million in 2013. Total revenue from both groundfish and non-groundfish species declined from $293.3 million in 2010 to $269.9 million (8%) in 2013.

The active limited access groundfish fleet decreased by 120 vessels over 2010-2013, to a four-year low of 735 active vessels. The number of vessels with revenue earned from taking at least one groundfish trip also decreased to a four-year low of 327 vessels in 2013, with 119 fewer vessels taking groundfish trips in 2013 than in 2010. Effort on groundfish trips generally

6

decreased in 2013. The fleet is taking fewer groundfish trips, with fewer total days absent on these trips. However, when a groundfish trip is taken, most vessels are taking lengthier trips than in prior years.

Measured from a somewhat longer time frame of 2007-2013, productivity for the Northeast Multispecies Fishery peaked in 2009 and has since slowly declined. In 2013 productivity was 4% lower than it was in 2007.

Aggregate owner shares of net revenue (gross revenue adjusted by fishing trip costs) were at a four-year low in 2013 at $122.2 million. This is an 11% decline from $136.9 million in 2010. Aggregate crew shares of net revenues also declined by 11% from $80.5 million to $71.6 million.

Opportunities to crew on groundfish vessels (measured in positions, days, or trips) declined over the period 2010-2013. For example, total crew trips declined by 15% between 2010 and 2013.

Both all species and groundfish revenues were unequally distributed in 2010, and they remained so through 2013. The distributions of both all species and groundfish revenues are more concentrated at the vessel affiliation (ownership) level than at the vessel level. The concentration of revenues among top earning vessel affiliations was marked in 2010-2013, and this level of concentration persisted and slightly increased in the top 1% in 2013. Groundfish revenue is more concentrated than all species revenue among the top earning vessel affiliations, as was the case at the vessel level.

At the vessel level, the total value of ACE/PSC lease market transfers in 2013 is estimated at 4.4 million dollars, down 46% from 2012 and 62% from 2010 (Table 28). When ownership groups are considered, the total transfer payment due to leasing is estimated at just over three million dollars, down 25% from 2012 and 53% from 2010, and implying that roughly 30% of all leasing (by value) is occurring within ownership groups.

7

Table 1. Summary of major trends (May through April, includes all vessels with a valid limited access multispecies permit).

2010 2011

Total Sector vessels

Common pool Total Sector

vessels Common

pool

Groundfish gross revenue (in 2010 dollars)

$83,212,207

$81,165,969

$2,046,238

$88,821,349

$87,982,963

$838,386

Non-groundfish gross revenue (in 2010 dollars)

$210,068,225

$115,537,375

$94,530,850

$235,565,188

$141,895,314

$93,669,874

Total gross revenue (in 2010 dollars)

$293,280,432

$196,703,344

$96,577,088

$324,386,537

$229,878,277

$94,508,260

Groundfish average price (in 2010 dollars) $1.42 $1.41 $1.58 $1.43 $1.42 $1.58

Non-groundfish average price (in 2010 dollars) $1.21 $1.18 $1.24 $1.11 $1.11 $1.11

Number of active vessels* 855 437 418 777 443 334

Number of active vessels that took a GF trip** 446 304 142 418 302 116

Number of groundfish trips 13,859 11,575 2,284 16,138 13,858 2,280

Number of non-groundfish trips 38,507 16,547 21,960 33,727 16,814 16,913

Number of days absent on groundfish trips 18,737 17,131 1,605 21,895 20,393 1,503

Number of days absent on non-groundfish trips 31,354 16,023 15,331 28,032 15,485 12,547

Total crew positions 2,268 2,166

Total crew trips 125,033 122,785

Total crew days 171,278 171,342

Throughout this report "trips" refer to commercial trips in the northeast Exclusive Economic Zone (EEZ). Past reports included party/charter trips. *Note sector plus common pool vessel counts may exceed the total vessel count because vessels may switch between sector and common pool eligibilities during the fishing year. **This refers to vessels that have revenue from at least one groundfish trip.

8

Table 1 (continued). Summary of major trends (May through April, includes all vessels with a valid limited access multispecies permit).

2012 2013

Total Sector vessels

Common pool Total Sector

vessels Common

pool

Groundfish gross revenue (in 2010 dollars) $67,815,297

$67,209,195 $606,102

$55,220,469 ($58,662,972)***

$54,211,824 ($57,592,187)***

$1,008,645 ($1,070,784)***

Non-groundfish gross revenue (in 2010 dollars) $228,136,612

$135,359,399 $92,777,213 $214,665,116 ($227,826,279)***

$129,680,139 ($137,623,316)***

$84,984,976 ($90,202,963)***

Total gross revenue (in 2010 dollars) $295,951,909

$202,568,594

$93,383,315

$269,885,585 ($286,489,251)***

$183,891,963 ($195,215,504)***

$85,993,622 ($91,273,747)***

Groundfish average price (in 2010 dollars) $1.43 $1.43 $1.71 $1.31 ($1.39)****

$1.30 ($1.38)****

$1.59 ($1.68)****

Non-groundfish average price (in 2010 dollars) $1.07 $1.03 $1.13 $1.00 ($1.06)****

$0.95 ($1.00)****

$1.10 ($1.17)****

Number of active vessels* 763 445 318 735 419 316

Number of active vessels that took a GF trip** 400 303 97 327 245 82

Number of groundfish trips 14,328 12,990 1,338 10,056 9,125 911

Number of non-groundfish trips 33,024 17,172 15,852 33,317 17,900 15,417

Number of days absent on groundfish trips 19,839 18,998 842 17,013 16,356 657

Number of days absent on non-groundfish trips 29,151 16,341 12,811 29,439 16,916 12,523

Total crew positions 2,135 2,039

Total crew trips 117,118 106,700

Total crew days 169,129 157,600

Throughout this report "trips" refer to commercial trips in the northeast Exclusive Economic Zone (EEZ). Past reports included party/charter trips. *Note sector plus common pool vessel counts may exceed the total vessel count because vessels may switch between sector and common pool eligibilities during the fishing year. **This refers to vessels that have revenue from at least one groundfish trip. ***Nominal gross revenue observed during Fishing Year 2013. ****Nominal average price during Fishing Year 2013.

9

1. INTRODUCTION

The Northeast Multispecies Fishery, referred to as the groundfish fishery, is managed by the New England Fishery Management Council (NEFMC). The groundfish fishery is carried out using both fixed and trawl gears.1 The groundfish resource is distributed throughout waters of the Gulf of Maine (GOM) and Georges Bank (GB) and, to a lesser extent, Southern New England (SNE) and the Mid-Atlantic Bight. Prior to Fishing Year 2010, the groundfish fishery was managed using effort controls, including Days at Sea (DAS). Amendment 13 to the groundfish Fishery Management Plan (FMP) was implemented in May 2004; it redefined initial allocations of DAS and allowed vessels to engage in DAS leasing and DAS transfers under certain conditions. Amendment 13 also introduced the “Sector Allocation” program, which gave fishermen the opportunity to voluntarily form sectors that would be constrained by quotas rather than DAS. Sectors could request exemption from many of the traditional input controls such as trip limits. This set the stage for Amendment 16 to the Northeast Multispecies FMP, which implemented a catch share program on 1 May 2010.

The catch share program was designed to comply with catch limit requirements and stock rebuilding deadlines required under the Magnuson-Stevens Fishery Conservation and Management Reauthorization Act of 2006 (MSA). The new groundfish management program contained two significant changes. The first consisted of “hard quota” annual catch limits (ACLs) for all 20 stocks in the groundfish complex. The second expanded the use of “sectors,” which are groups of fishing vessels allotted a share (quota) of the total groundfish ACL. Sectors are allocated subdivisions of ACLs called Annual Catch Entitlements (ACE). All permit holders with a limited access groundfish permit that was valid as of 1 May 2008, were eligible to participate in a sector, including holders of inactive permits currently held in Confirmation of Permit History (CPH).

Sectors, including state permit banks, receive ACE for nine of 13 groundfish species in the FMP and are exempt from many of the traditional effort controls.2 Each limited access groundfish permit has a potential sector contribution (PSC) that, based on that permit’s fishing history, is a percentage of the total quota allocation for each allocated groundfish stock. When a fisherman becomes a sector member, his PSC is pooled with those of the other members of that sector. The pooled PSCs of the sector become the sector’s ACE. Fishermen may hold limited access eligibilities, which are linked to a Moratorium Rights Identifier (MRI), in CPH. CPH permits are limited access groundfish eligibilities that are not attached to an actual vessel. An important consequence of Amendment 16 is that it allowed fishermen with permits in CPH to join sectors or to remain in the common pool with the option of leasing DAS, which was granted by Amendment 13. When a fisherman holding a CPH joins a sector, the PSC associated with those permits becomes part of that sector’s ACE. This is significant, because it means that a fisherman can lease the PSC associated with his CPH permits to other sector members or his

1 Fixed gear includes gillnet and hook gears including bottom longline, tub trawls, and rod and reel. 2

The nine allocated species are American plaice (Hippoglossoides platessoides), cod (Gadus morhua), haddock (Melanogrammus aeglefinus), pollock (Pollachius virens), redfish (Sebastes fasciatus), white hake (Urophycis tenuis), winter flounder (Pseudopleuronectes americanus), witch flounder (Glyptocephalus cynoglossus), and yellowtail flounder (Limanda ferruginea). The four non-allocated groundfish species are halibut (Hippoglossus hippoglossus), ocean pout (Zoarces americanus), windowpane flounder (Scophthalmus aquosus), and wolfish (Anarhichas lupus). All references to groundfish species include these 13 species unless there is specific mention of the nine allocated species. Non-groundfish species are any species other than the 13 groundfish species listed here.

10

sector can lease the PSC to other sectors through ACE trading. However, sectors are not permitted to transfer ACE to or from common pool vessels.

Fishing vessels owners may also opt to fish the quota associated with their groundfish permits, including permits they have placed in CPH, on fewer vessels (including a single vessel) to reduce the costs associated with operating multiple vessels. In 2010, approximately half (46%) of the vessels with limited access groundfish permits opted to remain in the common pool, likely because of their small individual potential contribution to a sector’s total ACE. Common pool vessels act independently of one another; each vessel is constrained by the number of DAS it can fish, by trip limits, and by time and area closures designated in the FMP. These restrictions help ensure that the groundfish catch by common pool vessels does not exceed the common pool’s allocation of the total ACL before the end of the fishing year. In 2013, nearly 43% of the active vessels with limited access groundfish permits were common pool vessels.

Nineteen sectors operated in 2013 (see 78 FR 25591, May 2, 2013).3 Four of these are “lease only” sectors,4 which hold eligible permits with accumulated ACE or DAS that they can make available to fishermen that intend to actively fish for groundfish. Each sector establishes its own rules for using its allocations, but the allocated catch restrictions are applicable to the sector as a unit (i.e., not to individual vessels in the sector). Sector enrolled permits accounted for approximately 98% of the FY 2013 commercial groundfish sub-ACL.

The trends in this report must be evaluated in the context of the quota changes that have occurred for fishing year 2013, as well as over the four years since Amendment 16 has been in place. From 2012 to 2013, several commercial sub-ACLs were cut from their 2012 levels: eastern Georges Bank cod (-43.2%), western Georges Bank cod (-61.4%), Gulf of Maine cod (-77.6%), eastern Georges Bank haddock (-45.4%), Gulf of Maine haddock (-71.4%), Georges Bank yellowtail flounder (-58.1%), SNE/MA yellowtail flounder (-22.9%), CC/GOM yellowtail flounder (-54.2%), American plaice flounder (-56.7%), witch flounder (-57.9%), Gulf of Maine winter flounder (-0.1%), northern windowpane (-24.0%), and wolfish (-15.1%). Some stocks’ sub-ACLs increased from their 2012 levels: western Georges Bank haddock (+10.5%), Georges Bank winter flounder (+4.2%), southern New England winter flounder (+299.3%), redfish (+21.7%), white hake (+17.2%), pollock (+2.2%), southern windowpane flounder (+41.7%), and halibut (+44.4%).

Sub-ACLS for several allocated stocks in 2013 were at a four-year low for the 2010-2013 time period, with substantial cuts overall since the implementation of Amendment 16 in 2010: eastern Georges Bank cod (-72.8%), western Georges Bank cod (-44.5%), Gulf of Maine cod (-81.8%), eastern Georges Bank haddock (-68.7%), Gulf of Maine haddock (-77.3%), Georges Bank yellowtail flounder (-81.2%), CC/GOM yellowtail flounder (-38.5%), American plaice flounder (-50.1%), witch flounder (-28.4%). Sub-ACLs for three allocated stocks were at a four-

3 These sectors were the Fixed Gear Sector (FGS), the Maine Coast Community Sector (MCCS), the Maine Permit Bank Sector (MEPBS), the New Hampshire Permit Bank Sector (NHPBS), the Northeast Coastal Communities Sector (NCCS), Northeast Fishery Sectors 2 through 13, and Sustainable Harvest Sectors 1 and 3 (SHS1 and SHS3). The Georges Bank Cod Hook Sector (operating since 2004) and the Georges Bank Cod Fixed Gear Sector (implemented in 2006) operated as separate sectors prior to fishing year 2010, when all members of the Georges Bank Cod Hook Sector joined FGS. In fishing year 2013, the Port Clyde Community Sector became known as the Maine Coast Community Sector. 4 The Northeast Fishery Sector IV, Sustainable Harvest 3, Maine Permit Bank, and New Hampshire Permit Bank Sectors are lease only sectors. The Sustainable Harvest 3 Sector has not explicitly prohibited fishing activity, and may transfer permits to active vessels.

11

year high in 2013, with overall increases in quota since 2010: Georges Bank winter flounder (+90.5%), redfish (+48.0%), and white hake (+50.6%).5

This report provides an evaluation of the economic and social performance of the groundfish fishery for fishing year 2013 (1 May 2013 – 30 April 2014). In this report, all references to year are for the fishing year. The report presents year-to-year comparisons for the four-year period of 2010-2013 to evaluate performance, and compares performance in 2012 and 2013. Table 1 presents data on major trends in the groundfish fishery by total fleet, sector vessels, and common pool vessels. Differences in the performance of sector and common pool vessels are discussed in Section 1.2; thereafter, the report focuses on the performance of the total groundfish fleet.

This report falls under the fisheries performance measures program developed by the NEFSC Social Sciences Branch in 2009 with extensive consultation from stakeholders in the Northeast region (see Clay et al. 2010; Plante 2010). The broad performance measure categories identified are the following: financial viability, distributional outcomes, stewardship, governance, and well-being. There are multiple indicators within each category. The Northeast indicators are part of a NMFS-wide process of developing social and economic indicators for all U.S. fisheries.6 This report includes a subset of indicators that are sufficiently developed for reporting. These cover aspects of financial viability (landings, revenue, number of vessels and effort, and average vessel performance) and distributional outcomes (employment and fleet diversity). Gross revenues are based on landings and ex-vessel (first sale) prices and―together with fishing effort, operating costs, and quantities of fishing inputs―provide an indication of vessel performance. Employment opportunity is measured by the number of crew positions, crew trips, and crew days. Fleet diversity is measured by vessel size and vessel revenue categories, and by distributions of revenues among individual vessels and vessel affiliations. Over time, additional indicators will be available for reporting as the NEFSC Social Sciences Branch’s research and the National Performance Measures Program continue to develop.

Amendment 16 contains several broad goals and objectives, carried over from Amendment 13. This report does not provide a detailed analysis of progress toward achieving these goals and objectives. However, where possible, it addresses trends related to Goal 2, Goal 4, and Objective 7, particularly for economic efficiency and diversity of the groundfish fleet.7 For example, changes in economic efficiency may be reflected by changes in revenue per unit effort and revenue per vessel and by changes in the Lowe Index, which measures productivity of the fleet. The diversity of the groundfish fleet can be explored by examining trends in (1) the number of vessels and vessel affiliations; (2) the geographic distribution of landings and revenues across ports and states; (3) employment indicators across ports and states; and (4) the distribution of revenues among vessels and vessel affiliations.

5 See NMFS Northeast Regional Office’s website: http://www.greateratlantic.fisheries.noaa.gov/aps/monitoring/nemultispecies.html . These data do not include sector carryover. 6 Contact [email protected] for more information on this national effort. The National Catch Shares Report, released in August 2013, presents performance metrics for all catch share managed fisheries in the U.S and may be found at https://www.st.nmfs.noaa.gov/economics/fisheries/commercial/catch-share-program/index. 7 Goal 2 in Amendment 16 is “create a management system so that fleet capacity will be commensurate with resources status so as to achieve goals of economic efficiency and biological conservation and that encourages diversity within the fishery.” Goal 4 is “minimize to the extent practicable, adverse impacts on fishing communities and shoreside infrastructure.” Objective 7 states: “To the extent possible, maintain a diverse groundfish fishery, including different gear types, vessel sizes, geographic locations, and levels of participation.”

12

The NEFSC released the first performance report for the FY2010 groundfish fishery in 2011 (see Kitts et al. 2011) and released a second performance report for FY 2011 in 2012 (see Murphy et al. 2012). In 2013, the net revenue estimation previously presented in the FY2011 report was extended to include the impact of quota leasing activities on the distribution of net revenues in the fishery for FY2011 (see Kitts and Demarest 2013).8 The FY2012 report was released in January 2014 and expanded the analyses presented in earlier reports by including a section on the impacts of quota leasing on the distribution of net revenues for different segments of the groundfish fleet (see Murphy et al. 2014).

Other efforts have been, and are being, undertaken in the Northeast to further the understanding of social and economic issues in the fisheries. A study of social capital among groundfish permit holders (Holland et al. 2010) has recently been repeated and the data collected from the second round of this study have been analyzed. Results were submitted to a scholarly journal for publication. The NEFSC implemented a revised vessel fixed costs survey in August 2012 and May 2013 that surveyed commercial fishing vessel owners in the Northeast, by vessel size and gear type. This effort resulted in cost data from 741 commercial fishing vessels, which are being analyzed with the goal of developing profitability profiles for different segments of the Northeast fleet. Socioeconomic surveys of crew and vessel owners across the Northeast fisheries have been implemented to collect basic demographic data on the fishing community and to develop additional performance indicators. An emphasis is placed on indicators that measure how well fisheries are performing in the areas of stewardship, governance, and fishing community well-being. The NEFSC concluded the first year of its socioeconomic survey of vessel crew in autumn of 2013; about 400 crew, including hired captains, were interviewed in ports in New England and the Mid-Atlantic. Results will soon be published as a NEFSC Technical Memoranda.9 The first round of data collection for NEFSC’s socioeconomic survey of vessel owners has been completed, and those data are currently being analyzed. Dr. Eric Thunberg, an economist in NMFS’ Office of Science and Technology is engaged in work to measure fleet diversity for the Northeast Multispecies Groundfish fleet, which will be available in published form shortly.10 See http://www.nefsc.noaa.gov/read/socialsci.html for more information on these and other NEFSC projects.

1.1. Data and Analytical Approach The vessels whose activities are evaluated in this report are those with valid limited

access multispecies permits during fishing years 2010-2013. An active vessel is defined as having revenue from the landing of any species on any trip while fishing under a limited access groundfish permit within the given fishing year. In this report, trips are defined as commercial trips in the Northeast Exclusive Economic Zone (EEZ). The evaluation includes only fish landed and sold. Weights are given in landed pounds (after heading/gutting) rather than in live pounds (whole fish) as prices are commonly calculated on a per landed pound basis. Gross revenues are based on what is landed and sold. Landings data in this report should not be used to conduct

8 Available at http://www.nefsc.noaa.gov/read/socialsci/pdf/QuotaTradingImpacts.pdf. 9 See the NEFSC Technical Memoranda Series at http://www.nefsc.noaa.gov/publications/tm/. The technical memo containing results from the first round of the crew survey will be published as Henry, Anna, and Julia Olson. An Overview of the Survey on the Socio-economic Aspects of Commercial Fishing Crew in the Northeast. 10 Contact Dr. Eric Thunberg at [email protected] for additional information.

13

comparisons with sector sub-ACLs or the catch monitoring reports issued for sectors, because the ACLs are calculated and monitored in live pounds and include both landings and discards.

This year’s report differs from previous ones in that all monetary metrics (revenues, prices, costs) have been adjusted for inflation by converting nominal dollars for a given year into real, constant dollars. The GDP Implicit Price Deflator was used to adjust nominal amounts for inflation, with the second quarter of calendar year 2010 as the base time period. For 2013, nominal amounts observed were indicated for selected metrics.

A groundfish trip is defined as a trip where the vessel owner or operator declared, either through the vessel monitoring system (VMS) or through the interactive voice response system, that the vessel was making a groundfish trip. This includes trips on which groundfish DAS were used, including monkfish (Lophius americanus) trips that used groundfish DAS. Other trips were also counted as groundfish trips if the dealer or vessel reported that groundfish was landed (e.g., trips with monkfish declarations that were not also using groundfish DAS).

Some statistics are reported by both home port and port of landing. “Home port” does not necessarily identify the port where fish are landed, but rather it is the information on “city and state where vessel is moored” provided by vessel owners on the vessel permit applications. Most often, the home port is the port where supplies are purchased and crew is hired, although this does not apply in all cases.11 “Landed port” is the actual port where fish are landed. We report by home port and by landed port because the implications of each are different. For example, revenue by home port gives an indication of the benefits received by vessel owners and crew (and some fishing-related businesses such as gear suppliers) based in that port. Revenue by landed port gives an indication of the benefits that other fishing-related businesses (primarily businesses that handle fish, such as dealers and processors) derive from landings in their port. We identified the top six home ports and landed ports in the Northeast and also examined changes by home port and landed port at the state level.

Some indicators in the report use a measure of time called a “day absent.” A day absent is defined as the number of days (24 hours each) a vessel is “absent” from port and is calculated by subtracting the sail date/time from the land date/time as entered on vessel logbook records, called vessel trip reports (VTRs). For comparative purposes, many measures have been calculated for both groundfish landings and all species landings. “All species” refers to the total of all species of fish or shellfish landed, including groundfish. The home port and length of a vessel are provided by the vessel owner on the vessel’s yearly permit application. Data on vessel landings, nominal prices, and nominal revenues come from seafood dealer reports. Information about the number of fishing trips and crew size is from VTRs.12 In addition to mean values, standard

11 Alternative port affiliation data are available. Principal port declaration and the vessel owner’s mailing address are also entered on the permit application. However, actual landings by port may vary widely from what a vessel owner thinks his principal port of landing will be before the fishing year begins. Also, an owner’s mailing address can be different from a vessel’s base of operation. Therefore, home port is typically used in social and economic studies to establish port affiliation (as in this report). As the home port listed for a vessel can change over the year depending on what is declared on permits, this report assigns a vessel’s home port to be the first home port that is used during FY2013. 12 All data are from GARFO’s fishing year 2010 – 2013 Data Matching Imputation System, or DMIS, database (a combination of seafood dealer reports, vessel trips reports, and quota monitoring reports) as of July 21, 2014. Differences in results reported in each year’s annual performance report are due to updates and corrections to the DMIS database. In addition, in this year’s report, all monetary amounts are reported in constant 2010 dollars (nominal monetary amounts were adjusted for inflation).

14

deviations are provided to show the degree of variability in the data. Some standard deviations are large relative to the mean, indicating that the values are widely dispersed. Therefore, care should be used when comparing mean values that have large standard deviations.

Several performance metrics in this report, including effort and revenue, are examined by vessel size category using four vessel length classes: under 30ʹ in length, 30ʹ to less than 50ʹ in length, 50ʹ to less than 75ʹ in length, and 75ʹ and longer. Many of the vessels in the under 30ʹ vessel length class are considered to be “skiffs,” a colloquial term used by fishermen and fishery managers to refer to small vessels, generally unseaworthy, used only for the attaching of a permit. Although skiffs may appear as inactive vessels in the database, the quota or DAS associated with their permits is commonly transferred to other vessels.

Some of the metrics in this report are presented at both the individual and at the affiliated vessel level. To evaluate changes at the affiliated vessel level, vessels were grouped according to ownership patterns. Permit applicants are required to list all persons and entities that have an ownership interest in the vessel for which a permit is being registered. Using this database, it is possible to find affiliations among vessels. We define “vessel affiliations” as networks of vessels connected through common owners. Vessels connected to one another through ownership, for the purpose of data analyses, are deemed a single vessel affiliation. For example, two vessels owned by one person are considered to be in one vessel affiliation. Further, a vessel owned in partnership is considered to be in the same vessel affiliation with a second vessel if that second vessel is owned by one of the partners. A vessel affiliation could have multiple vessels and/or multiple owners or it could consist of a single vessel and a single owner. A vessel affiliation can include vessels in multiple sectors and/or the common pool. It is likely that vessels in the same vessel affiliation are subject to some degree of joint decision making among common owners.

1.2. Performance of Sector and Common Pool Vessels

There are fundamental differences in the characteristics of sector and common pool vessels and in the ACE and DAS allocations.13 A large number of common pool vessels have few or no DAS, while some common pool vessels have small vessel exemption permits (Category C) or hand gear permits (HA) excluding them from DAS constraints. Common pool vessels are regulated not only by DAS, but also by additional measures, some of which changed during the 2010 fishing year. Finally, vessels opting into the common pool landed significantly less groundfish during the landings qualification period of 1996 through 2006 than those electing to operate in sectors, which resulted in the common pool being allocated only 1-2% of the total ACL for all stocks. In 2013, sector vessels accounted for 98.2% of the total value of groundfish landed (Table 1).

This section discusses major trends in performance, broken down by sector and common pool vessels, as presented in Table 1. Differences in these performance measures should not serve alone as the basis for an evaluation of catch share versus DAS management regimes. In Sections 2 through 8 of this report, performance indicators are reported for the active groundfish fleet as a whole, with sector and common pool vessels combined.

13 These may include differences in physical characteristics of the vessel, different fishing histories, and different attitudes about sector management. Also, fishermen presumably opted to join a sector or remain in the common pool based on their analysis of the advantages and disadvantages to them of each regimen.

15

The total number of active groundfish vessels continues to decline; the fishery lost 120, or 14.0%, of its active vessels over the 2010-2013 period (Table 1). Possible reasons for the declining number of active groundfish vessels will be addressed in Section 6. In 2013, there were 735 active vessels in the limited access groundfish fleet, with 419 vessels (57%) enrolled in sectors and 316 vessels (43%) remaining in the common pool. From 2012 to 2013, the number of vessels enrolled in sectors decreased by 26 vessels and the number of vessels in the common pool decreased by two vessels (Table 1).

For both sector and common pool vessels, total gross revenues for all species (groundfish and non-groundfish) were at four-year lows in 2013. Total all species gross revenue for the entire fleet was $269.9 million, an 8.8% decrease from 2012. Total all species gross revenue fell by $18.7 million (-9.2%) from 2012 to 2013 for vessels enrolled in sectors. Common pool vessels saw total all species gross revenue fall by $7.4 million (-7.9%; Table 1).

For 2013, declines in total all species revenues for sector vessels were driven primarily by the declines in groundfish revenues, while declines in total all species revenues for common pool vessels were driven by declines in non-groundfish revenues. In 2013, sector vessels had $54.2 million dollars in gross groundfish revenues, the lowest groundfish revenues for sector vessels since the implementation of catch shares in 2010. Groundfish revenues were nearly $13.0 million (19.3%) lower in 2013 than in 2012 for sector vessels, and declining groundfish revenue accounted for 69.6% of the decline in total all species revenue for these vessels. Total non-groundfish revenues also decreased for sector vessels, but this decrease was more modest, with non-groundfish revenues declining by $5.7 million (-4.2%) from 2012 to 2013 (Table 1).

Common pool vessels also experienced a decline in non-groundfish revenue from 2012, but their groundfish revenue was higher in 2013 than it was in 2011 and 2012. Groundfish revenues for common pool vessels were just over $1.0 million in 2013, a 66.4% increase over 2012. Common pool vessels saw their non-groundfish revenue drop to a four-year low of just under $85 million in 2013, an 8.4% decline from 2012 (Table 1).

Average groundfish price decreased in 2013 for both sector and common pool vessels from 2012, by $0.13 per pound (-9.1%) for sector vessels and $0.12 per pound (-7.0%) for common pool vessels. Common pool vessels continued to receive a higher average price at the dock for groundfish than sector vessels in 2013, as they did in 2012. Sector vessels received an average groundfish price of $1.30 per pound in 2013, while common pool vessels earned an average price of $1.59 per pound for groundfish (Table 1).

Average non-groundfish price was at a four-year low, $1.00 per pound, in 2013 for the fleet as a whole. From 2012, average non-groundfish price decreased by $0.08 per pound (-7.8%) for sector vessels and by $0.03 per pound (-2.7%) for common pool vessels in 2013 (Table 1).

Effort in the groundfish fishery is represented in part by the number of active vessels, the number of trips taken, and by days absent on trips. For the fleet as a whole, 73 fewer vessels had revenue from at least one groundfish trip in 2013 than in 2012; 58 fewer sector vessels and 15 fewer common pool vessels targeted groundfish in 2013 than in 2012. The numbers of groundfish trips taken were at four-year lows in 2013 for both sector and common pool vessels. For sector vessels, the number of groundfish trips taken fell by 3,865 trips (-29.8%) from 2012 to 2013. Common pool vessels took 427 (-31.9%) fewer groundfish trips. The total numbers of days absent on groundfish trips also decreased to their lowest levels in 2013 for both sector and common pool vessels. Sector vessels had 2,642 fewer days absent (-13.9%) on groundfish trips in 2013 than in 2012, while total days absent on groundfish trips for common pool vessels fell by 185 (-22.0%; Table 1).

16

Non-groundfish effort increased for sector vessels in 2013. Sector vessels took 4.2% more non-groundfish trips (+728 trips) than in 2012, reaching a four-year high. Total days absent on non-groundfish trips also increased to a four-year high for sector vessels, with 575 more days absent in 2013 than in 2012, a 3.5% increase. In contrast, effort measures for non-groundfish decreased slightly for common pool vessels in 2013 compared with 2012; common pool vessels took 435 fewer non-groundfish trips (-2.7%), with 288 fewer days absent on non-groundfish trips (-2.2%; Table 1).

2. LANDINGS AND GROSS REVENUES

Gross revenues are one important indicator of financial performance. In commercial fishing, gross nominal revenues are a function of the amount of fish landed and the price paid at the time of sale. Prices paid by dealers vary by species and may fluctuate as a result of short- and long-term market changes. Annual changes in gross revenues can result from three different factors: changes in prices paid for fish at the dock, changes in quantity of landings, and changes in the species composition of the landings. Flexibility to target specific species and/or market categories at times when market values are high can be important in maximizing gross fishing revenues. Information is provided below on landings, overall gross revenues, and prices in 2013 compared with those in 2010 through 2012.

In this report, nominal revenues have been adjusted to account for the effects of inflation. Nominal revenues observed throughout the four-year time span were converted to real revenues using the GDP Implicit Price Deflator, with the second quarter (April-June) of calendar year 2010 as the base time period. Nearly all revenues contained in this report are in constant 2010 dollars. This approach differs from previous reports. In the 2010, 2011 and 2012 reports, nominal revenues were presented for most revenue metrics, with the exception of groundfish revenues, non-groundfish revenues, and all species revenues from all trips, which were presented in both nominal and real dollars.14 In this year’s report, we report monetary metrics in nominal amounts observed in 2013 for selected metrics only (see Tables 1-3). Unless otherwise indicated, the discussion in this report refers to monetary amounts in real or constant terms, i.e. amounts that have been adjusted for inflation. 2.1. Landings

Groundfish landings in 2013 continued the decline that the limited access groundfish fleet experienced in 2012. Declining groundfish landings were coupled with little growth in non-groundfish landings for the fleet in 2013. Total landings of all species on all trips were 256.4 million pounds in 2013, a 1.6% decrease from 2012 (260.5 million pounds). In 2013, total landings of all species were at their lowest point over the 2011-2013 time period, but higher than they were in 2010 (232.9 million pounds; Table 2). Total groundfish landings on all trips decreased to a four-year low of 42.2 million pounds in 2013, compared with 58.7 million pounds in 2010. Total groundfish landings on all trips declined 10.9% in 2013 compared with 2012 and 28.0% overall from 2010 to 2013. Total non-groundfish landings on all trips in 2013 were 214.2 million pounds, a four-year high, but less than 1% greater than in 2012. Groundfish landings

14 Table 2 (Total landings and revenue from all trips by fishing year) in the FY2010, FY2011, and FY2012 reports.

17

accounted for 16.5% of total landings in 2013, down slightly from 18.2% of total landings in 2012 (Table 2).

Total landings in 2013 of all species on groundfish trips decreased to a four-year low of 61.2 million pounds. Groundfish landings on groundfish trips also decreased to a four-year low of 42.1 million pounds.15 The overall decline in groundfish landings on groundfish trips from 2010 to 2013 is 28.1%, with an 11.1% decline occurring from 2012 to 2013. Non-groundfish landings on groundfish trips decreased to 19.1 million pounds, compared with 23.5 million pounds in 2010. Overall, non-groundfish landings on groundfish trips declined 18.6% from 2010 to 2013, with a 29.7% decrease in 2013 from 2012 (Table 3). The trends for landings data in 2013 follow the pattern seen in 2012: the groundfish fleet appears unable to adapt to the negative trends in groundfish landings by substituting non-groundfish landings.

2.2. Gross Revenues

Gross revenues for the groundfish fleet began declining in 2012 and continued to decline in 2013. Non-groundfish revenues earned by the fleet have fallen in the past two years and therefore cannot offset losses in groundfish revenues. Total gross revenue in 2013 from all species landed on all trips was $269.9 million, an 8.8% decrease from 2012 ($296.0 million). Gross revenue for all species landed on all trips taken by the limited access groundfish fleet was at a four-year low in 2013, declining 8.0% overall from 2010-2013 (Table 2).

Groundfish revenue in 2013 on all trips decreased to a four-year low of $55.2 million (18.6% lower than in 2012), with a 33.6% decline from 2010 to 2013. Non-groundfish revenue on all trips decreased to $214.7 million (-5.9%) compared with 2012 and was at a three-year low for the 2011-2013 period, but the revenue was still higher than it was in 2010 (Table 2).

Total gross revenue from all species landed on groundfish trips in 2013 was $75.5 million, a four-year low, with a 18.6% decline from 2012 and a 29.2% decline from 2010 (Table 3). Groundfish revenue on groundfish trips in 2013 was $55.0 million, a four-year low for the 2010-2013 time period, with an 18.7% decrease from 2012 and a 33.7% decrease from 2010. Non-groundfish revenues on groundfish trips decreased in 2013 to a four-year low of $20.5 million, from $25.1 million in 2012 (Table 3). 2.2.1. Revenues by Landing Port and Home Port

Trends for all species revenues in 2013 by landing state and home port state (Table 4 and

Table 5) were mixed. New England states that are home port states for vessels that have traditionally targeted groundfish experienced mostly negative trends. All species revenues for Massachusetts, New Hampshire, and New York were at four-year lows in 2013, from both a landed port and home port perspective. Massachusetts experienced the biggest declines in absolute terms and New Hampshire experienced the biggest declines in percentage terms. Massachusetts has seen all species revenues decline by $25.5 million (-14.6%) as a landed port state and $21.4 million (-14.3%) over 2010-2013. In New Hampshire, all species revenues have fallen over 2010-2013 by $2.2 million (-31.9%) for the state as a landed port state and $2.1 million (-27.0%) for the state as a home port state (Table 4 and Table 5).

15 Note that almost 100% of groundfish landings occurred on groundfish trips. For that reason, groundfish landing values for all trips and groundfish trips are nearly identical.

18

Rhode Island was the only state to see gains in all species revenue in 2013 from both a landed port and home port perspective. Overall, from 2010 to 2013, all species revenue has increased $6.7 million (+22.0%) for Rhode Island as a landed port and $2.1 million (+5.9%) for the state as a home port state (Table 4 and Table 5).

Maine has experienced more mixed trends for all species revenue, depending on whether all species revenues are viewed from a landed or home port state perspective. Overall, since 2010, all species revenues for Maine as a landed port state have increased 7.6%, while all species revenues earned by active limited access groundfish vessels that are homeported in Maine have fallen 13.1% over the same period. In the remaining Northeast states, trends for all species revenues varied (Table 4 and Table 5).

The value of groundfish landed on all trips was at a four-year low for Massachusetts and New Hampshire in 2013 from both a landed and home port state perspective. Massachusetts experienced the greatest losses in absolute terms; over the past four years, Massachusetts has lost $29.0 million (-39.4%) in groundfish revenues as a landed port state and $22.2 million (-37.4%) as a home port state. In percentage terms, New Hampshire has lost $1.3 million (-40.3%) as a landed port state and $1.3 million (-36.4%) as a homeport state in groundfish revenues over the same period. Groundfish revenues earned by vessels homeported in Maine were at a four-year low in 2013, declining 18.4% over 2010-2013. As a landed port state, groundfish revenues for Maine were lower in 2013 than in 2011 and 2012 but higher than they were in 2010.

Connecticut was the only state to see a four-year high for groundfish revenues as both a landed and home port state in 2013. Over 2010-2013, groundfish revenues have grown by $117,103 (1302.5%) for Connecticut as a landed port state and by $34,420 (62.6%) as a home port state. As landing port states, New Jersey, New York, and Rhode Island all saw four-year highs in 2013 for groundfish revenues. From a home port state perspective, these three states experienced increases in groundfish revenues from 2012, ranging from 2.0% (Rhode Island) to 186.4% (New Jersey).16 However, groundfish revenues from groundfish vessels homeported in New Jersey, New York, and Rhode Island have fallen overall since 2010, by 51.2%, 24.6%, and 23.8%, respectively (Table 6 and Table 7).

All species and groundfish revenues are also presented for the six major groundfish ports in the Northeast. Massachusetts ports Boston, Gloucester, and New Bedford have been especially hard hit in 2013; both all species and groundfish revenues were at a four-year low in 2013 for the three ports, both from the landed and home port perspective.

Gloucester has seen all species revenues decline 37.2% (-$14.8 million) as a landed port and 31.8% (-$8.0 million) as a home port over the past four years (Table 4 and Table 5). Declining all species revenues in Gloucester are being driven by the port’s losses in groundfish revenues. Groundfish revenues for Gloucester have fallen 47.4% as a landed port and 43.9% as a home port over the 2010-2013 time period (Table 6 and Table 7).

The value of all species landed in Boston has decreased 11.6% (-$1.7 million) from 2010 to 2013 (Table 4). All species revenues earned by groundfish boats homeported in Boston fell 9.8% (-$2.7 million) over the past four years (Table 5). Groundfish revenues also fell to four-year lows in 2013 for Boston as both a landed port and a home port. Over the past four years, groundfish revenues have declined 16.4% for Boston as a landed port and 25.9% as a home port (Table 6 and Table 7).

16 The growth seen in groundfish revenues from 2012 to 2013 for New Jersey, New York, and Rhode Island as home port states may be due to the influence of Superstorm Sandy, which occurred in late October 2012. For all three states as home port states, groundfish revenues were at a four-year low in 2012.

19

The limited access groundfish fleet in the port of New Bedford has also experienced declines, despite being less dependent on groundfish revenues than the groundfish fleet in Gloucester and Boston. New Bedford has lost 9.0% (-$8.7 million) in the value of all species landed in the port from 2010 to 2013 (Table 4). As a home port, all species revenues declined 11.2% (-$7.3 million) in the past four years (Table 5). Groundfish revenues for New Bedford are at a four-year low from both the landed port and home port perspective. As a landed port, New Bedford experienced a 37.3% (-$11.0 million) loss over 2010-2013 (Table 6). Groundfish revenues earned by groundfish vessels homeported in New Bedford have fallen 31.4% (-$5.8 million) from 2010 to 2013 (Table 7).

Massachusetts’ southernmost major port, Chatham, has seen more positive trends in all species revenues, for the portion of limited access groundfish fleet active there, than northern ports in the state. This is partially because, by 2013, many of the limited access groundfish vessels active in Chatham were targeting non-groundfish species rather than groundfish. Over the four-year time series, all species revenues peaked in 2011 for Chatham as a landed port and grew 9.0% overall (Table 4). Chatham saw a similar trend in all species revenues earned by groundfish vessels homeported there; all species revenues for Chatham as a home port peaked in 2011 and grew 23.6% over 2010-2013. However, groundfish revenues for Chatham as both a landed port and a home port were at a four-year low in 2013. As a landed port, groundfish revenues declined 66.6% (-$1.5 million) over 2010-2013 (Table 6). Groundfish revenues for Chatham as a home port declined 68% (-$1.6 million) over the same time period (Table 7).

Portland, Maine, experienced small increases in all species revenues in 2013, both as a landed port and a home port. All species revenues as a landed port increased 2.8% (+$0.2 million) from 2012 to 2013 to achieve a four-year high and grew 39.1% (+$2.5 million) over the four-year time span (Table 4). All species revenues from groundfish vessels homeported in Portland have stayed in the 12- to 13-million-dollar range over 2010-2013, growing 5.7% from 2012 to 2013 and declining very slightly by 0.1% over the four years (Table 5). While groundfish revenues fell in 2013 by 10.7% (-$0.6 million) compared with 2012 for Portland as a landed port, they have grown 54.1% (+$1.9 million) over 2010-2013 (Table 6). As a home port, Portland experienced a slight increase of 4.7% (+$0.4 million) in groundfish revenues in 2013 compared with 2012, but groundfish revenues have declined by 7.5% (-$0.8 million) over the four-year time span (Table 7).

The port of Point Judith, Rhode Island, saw mostly gains in 2013. All species revenues for the port as landed port were are four-year high in 2013, growing 30% (+$6.6 million) from 2010-2013 (Table 4). From a home port perspective, all species revenues grew 13.9% (+3.2 million) for the four-year time span (Table 5). In 2013, revenues for groundfish landed in the port achieved a four-year high, growing 39.9% (+$0.6 million) over the four-year period (Table 6). For vessels homeported in Point Judith, groundfish revenue increased 7.8% from 2012 but declined 19.5% (-$0.5 million) over the four-year time series (Table 7).

2.2.2. Revenues by Species

Most allocated groundfish species saw declines in revenues from 2012 to 2013. Groundfish revenues from cod, yellowtail flounder, American plaice flounder, witch flounder, redfish, white hake and pollock all decreased compared with 2012. These revenue decreases ranged from 9.5% for American plaice flounder to 45.2% for yellowtail flounder. The only two

20

allocated groundfish species to see increases in revenue in 2013 were haddock (+46.3%) and winter flounder (+0.9%; Table 8).

Revenue from cod declined to a four-year low of just under $9.0 million in 2013, declining $17.6 million and 66.2% over the four-year time span. In 2013, both decreased landings of cod and a decreased price for cod contributed to the drop in revenue. The price of cod in real terms decreased from $2.41/lb in 2012 to $2.11 in 2013. Revenues for American plaice flounder, yellowtail flounder, and witch flounder also fell to four-year lows in 2013. American plaice flounder revenues decreased 9.5% from 2012; this decline can be attributed to both lower landings and a lower price in 2013 compared with 2012. The decrease in yellowtail flounder revenues (-$2.1 million) is due to lower landings of the species in 2013; the price of yellowtail flounder increased from $1.43/lb in 2012 to $1.48/lb in 2013. Similarly, the declines in witch flounder in 2013 were due to decreased landings, with landings falling from 2.0 million pounds to 1.3 million pounds. The price of witch flounder increased from $1.88 in 2012 to $2.28 in 2013 (Table 8).

Haddock and winter flounder revenues both increased in 2013 compared with 2012. From 2012, haddock revenue increased 46.3% (+$2.3 million) in 2013. This increase occurred due to higher landings of haddock, which rose from 2.2 million pounds in 2012 to 5.5 million pounds in 2013. The price of haddock fell from $2.29 in 2012 to $1.34 in 2013. Over the four-year time span, haddock revenues have decreased 64.3% from 2010 to 2013 (Table 8). Winter flounder revenues slightly increased (+0.9%) in 2013 compared with 2012. This is due to an increase in landings from 4.8 million pounds to 5.9 million pounds; the price of winter flounder decreased to $1.56/lb (Table 8).

The top ten non-groundfish species landed by limited access groundfish vessels by value are presented in Table 9. Sea scallops were the mostly highly valued non-groundfish species landed by limited access groundfish vessel, bringing in $72.6 million in revenue in 2013. Revenue from sea scallops landed while fishing under a limited access groundfish permit accounted for 26.9% of total all species revenue and 33.8% of total non-groundfish revenue. While sea scallop revenue has grown 1.3% over the four-year time span, it decreased 15.5% (-$13.3 million) from 2012 to 2013. This was due to a 26.5% fall in sea scallop landings; the price of scallops rose from $9.63/lb in 2012 to $11.07 in 2013 (Table 9).

Lobster, loligo squid, herring, skate and Jonah crab all saw increases in revenue from 2012 to 2013. These increases ranged from 6.0% for loligo squid to 21.6% for herring. For lobster, loligo squid, herring and Jonah Crab, increases in revenues are due to increased landings; prices fell in 2013 for each of these species. In 2013, skates were the only non-groundfish species that had an increase in revenue, but a decrease in landings (-6%) from 2012. The increase in revenue from skates is due to a price increase from $0.28/lb in 2012 to $0.32/lb in 2013 (Table 9).

Revenues decreased in 2013 for monkfish, summer flounder (fluke), silver hake (whiting), and scup landed by the limited access groundfish fleet, with revenues for all but scup at four-year lows. From 2012 to 2013, monkfish revenues decreased by 14.6% to $13.0 million. This decline is due to both lower landings (-6.9%) and a decrease in the price of monkfish; the price of monkfish fell from $2.15/lb in 2012 to $1.97 in 2013. Summer flounder (fluke) revenues fell by 7.7% in 2013 from 2012 to a four-year low of $15.6 million. The decline was due to decreased landings, which more than offset the price increase of $0.16/lb from 2012 to 2013. Silver hake (whiting) revenues were at a four-year low of $8.4 million in 2013, a 9.5% decrease from 2012 and a 23.9% decrease since 2010. Both landings and the price of silver hake (whiting)

21

were at a four-year lows in 2013. Revenues for scup landed by the fleet were down 3.9% in 2013 but were higher than they were in 2010 or 2011; scup revenues have grown 26.5% from 2010-2013. The decline in scup revenues for 2013 is due to decreased landings; the real price of scup increased by $0.01/lb (Table 9).

Revenues from non-groundfish species landed by the limited access groundfish fleet fell 5.9% in 2013 from 2012. While non-groundfish revenues have grown slightly (+2.0%) from 2010-2013 (+$4.6 million), the 2013 decline in total non-groundfish revenues is especially notable because this means groundfish fishermen who tended to land non-groundfish species that experienced declining revenues in 2013 were unable to offset the significant drop in groundfish revenues with revenues from non-groundfish landings (Table 2).

2.3. Prices

Data on average groundfish and non-groundfish price trends are presented in Table 1 and Figure 1, and data for price trends for the nine allocated groundfish species are presented in Figure 2. Price data presented in Table 1, Figure 1 and Figure 2 reflect prices after adjusting for inflation; prices are in real terms (in constant 2010 dollars). Nominal average prices for groundfish and non-groundfish in 2013 are also presented in Table 1, along with real average prices for 2013.

In 2013, the average price of the nine allocated groundfish species (as a group) fell to four-year low, as did the average price of all non-groundfish species (as a group; Figure 1). From 2012 to 2013, average groundfish price fell from $1.43/lb to $1.31/lb, while average non-groundfish price declined from $1.07 to $1.00 (Table 1). The prices of yellowtail flounder, witch flounder, and pollock all increased in 2013 from 2012. These increases ranged from $0.05/lb for yellowtail flounder to $0.40/lb for witch flounder. The price of yellowtail flounder reached a four-year high in 2013 at $1.48/lb, as did the price of pollock, at $1.08/lb. All of the remaining allocated groundfish species experienced price decreases from 2012 to 2013. The largest price decreases occurred for haddock (-$0.95/lb), winter flounder (-$0.33/lb) and cod (-$0.30/lb), with winter flounder and cod at four-year lows of $1.56/lb and $2.11/lb, respectively. American plaice flounder, redfish, and white hake also saw price decreases ranging from $0.02/lb for white hake to $0.08/lb for redfish. The price of redfish was at a four-year low of $0.50/lb in 2013 (Figure 2).

Using the simple average real prices of all groundfish species combined that are presented in Table 1 to compare changes in prices over time may be misleading, because, although this average has been adjusted for inflation, it does not account for annual changes in the quantity and mix of groundfish species landed. A price index was therefore constructed to more accurately reflect price trends of groundfish species. The approach used the “Fisher Ideal” index (Balk 2008), which was constructed from price and quantity data recorded in dealer purchases of all groundfish species. Quarterly data were used in all fishing years from 2007 through 2013. May-July (quarter 1) of 2007 was set as the base period, with a value of 1. The Fisher Price Index is constructed using nominal prices.

The index values (Figure 3) show how combined nominal prices have changed in relation to quarter 1 2007 nominal prices. A value less than 1 means that prices are lower compared with the base time period, while a value greater than 1 indicates that prices have increased relative to quarter 1 in 2007. In 2013, the quarterly adjusted groundfish price index declined in quarters 1 and 2, from 2012 quarter 4 levels. The index then rose in quarter 3, before falling again in quarter 4. Compared with 2007, all values were greater than 1, indicating higher prices.

22

Generally, the price index was lower in 2013 than in 2012. However, the decline in 2013 is in relation to prices that reached a six-year high in the fourth quarter of 2012.

3. NUMBER OF VESSELS AND EFFORT

Effort indicators provide information about the amount of fishing that occurred to produce the landings. In this report, three indicators were used to measure fishing activity and effort: the number of active fishing vessels, the number of fishing trips, and the number of days absent from port.

3.1. Number of Vessels