Penn Treaty Underwriting Guide - NJLTC

40

PTA-UND(3/04)

Transcript of Penn Treaty Underwriting Guide - NJLTC

PTA-UND(3/04)

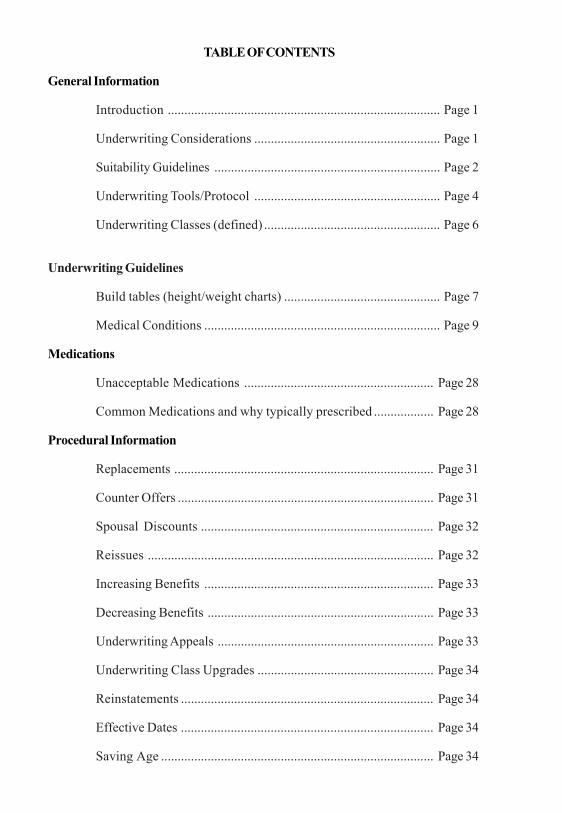

TABLE OF CONTENTS

General Information

Introduction .................................................................................. Page 1

Underwriting Considerations ........................................................ Page 1

Suitability Guidelines .................................................................... Page 2

Underwriting Tools/Protocol ........................................................ Page 4

Underwriting Classes (defined) ..................................................... Page 6

Underwriting Guidelines

Build tables (height/weight charts) ............................................... Page 7

Medical Conditions ....................................................................... Page 9

Medications

Unacceptable Medications ......................................................... Page 28

Common Medications and why typically prescribed .................. Page 28

Procedural Information

Replacements .............................................................................. Page 31

Counter Offers ............................................................................. Page 31

Spousal Discounts ...................................................................... Page 32

Reissues ...................................................................................... Page 32

Increasing Benefits ..................................................................... Page 33

Decreasing Benefits .................................................................... Page 33

Underwriting Appeals ................................................................. Page 33

Underwriting Class Upgrades ..................................................... Page 34

Reinstatements ............................................................................ Page 34

Effective Dates ............................................................................ Page 34

Saving Age .................................................................................. Page 34

IntroductionThe purpose of this guide is to assist our agency force with the Long-Term Careinsurance qualification process. Our unique Underwriting philosophy allows usto offer coverage to a very high percentage of potential applicants with the use offive different rate classes (including the Secured Risk Plan, available in mostStates). These rate classes and our diverse variety of products, including stand-alone Facility, stand-alone Home Care, comprehensive LTC, as well as both Tax-Qualified and Non-Tax qualified versions, are designed to fit the individual needsof your clients. (Please check the availability of products available within yourState on line at www.penntreaty.com or by contacting our Marketing Departmentat (800) 362-0700.)

By utilizing our risk stratification approach and charging the appropriatepremiums for a wide variety of risks, our goal is to properly classify the applicantssubmitted and issue as much of your business as possible. Those applicants whocan effectively live independently and do not exhibit signs of possible cognitiveimpairment are generally offered coverage, even if they may have had problemsobtaining ltci elsewhere.

Both you, our agents, and your clients are valued customers and we appreciateyour business. We work diligently to maintain and improve upon the best serviceavailable throughout the ltci industry. Our Underwriters are available for you tospeak with directly regarding questions of insurablility, rating, and to help you inany way. We encourage you to contact them directly at (800)222-3469 ext. #3516.

We also encourage you to use the Underwriting Wizard, available as software oron the Agent Resource Center at www.penntreaty.com. The Underwriting Wizardis the same tool utilized by our in-house Underwriting Staff and allows you toobtain a realistic quote based on your applicant’s health history. This tool can beparticularly helpful to you when attempting to correctly classify an applicant withmultiple medical conditions. The Agent Resource Center also allows you to reviewthe status of all your pending applications.

Underwriting ConsiderationsNaturally, an applicant must currently be capable of independently performing allActivities of Daily Living ( ADLs), including bathing, dressing, eating transferring,ambulating, continence and toileting. The applicant must also be capable ofperforming their Instrumental Activities of Daily Living (IADLs), including mealpreparation, light housekeeping, laundry, shopping/travel, telephoning,medication management, handling money/bill paying.

1

In addition to independence with the ADLs and IADLs, and in order to properlyevaluate the risk associated with needing Long Term Care in the future, we mustconsider several other factors which may affect the applicant’s ability to liveindependently. These factors include the following:

• Current health status, both mentally and physically, including heightand weight and all medications as well as the reasons they are beingtaken.

• Past health status including prior conditions, hospitalizations,surgeries, medications etc.

• Cognitive functioning.

• Activity Level with respect to both physical and social habits.

• Living Situation, including with whom applicant resides, wherethey reside, and the length of time they have resided in current home.

• Financial situation of applicant (see Suitability Guidelines below).

Suitability GuidelinesAlthough ltci is often an important tool that can be used to help protect individualsand their families from the potentially devastating and rising costs associated withthe risk of Long Term Care, it is important to remember that ltci is not for everyone.Prior to applying for insurance, agents must consider and discuss the client’s financialpicture and the appropriateness of purchasing ltci. Please verify requirements inyour State ( available on our website) as many States have adopted the NAIC suitabilitymodel and require the completion of Personal Worksheets designed to provide theInsurance Company insight into the applicant’s financial “picture”. (While applicantsdo have the option of not providing financial information, they must still sign theSuitability Form indicating that they do not wish to provide such information.) Whenthey choose not to provide financial information, the agent can greatly expedite theunderwriting process by having the applicant also sign and submit a Waiver Form.The following chart provides some guidelines with respect to the appropriateness ofpurchasing Long Term Care insurance.

Individual Assets(not incl. Primary residence) % of Income to be Applied to LTCi$30,000 or below Please reconsider applicants’ ltci needs$30,000 to $100,000 7 % of annual income$100,000 and above 10 % of annual income

2

The preceding figures are intended to be a practical rule of thumb, however it isimportant to remember that they are only guidelines. In certain cases, for example,those who may be eligible for Medicaid may find it appropriate for their family to payfor ltci premiums, giving the insured access to a higher quality of care in the settingof their choice.

In addition to having a reasonable expectation that premiums can be paid on aregular basis, several other factors should be taken into consideration, including thefollowing:

• The cost of care within the specific region where the applicant wouldreceive care.

• The applicant’s goals and needs with respect to the advantages and costof ltci to meet these goals and needs.

• The appropriateness of benefits in relation to the age of the applicant.

• If replacing, the appropriateness of replacement. A Comparison Formmust be competed and submitted with all replacements. All replacementsmust result in an improvement for the insured.

• The applicant should be made aware that our products are priced suchthat future rate increases are not anticipated, however, unforeseen factorsor adverse experience could affect rates and future rates may be increasedif required. The applicant should consider whether they could afford topay premiums if the rates were increased, for example, by 20%.

• The applicant should consider how their income as well as their assetsmay change in the future, including retirement, unforeseen life events, orany other factors which might affect their ability to pay premiums.

Suitability Procedures1. When required within your State (please verify if required and correct

forms needed by looking on our Website), the appropriate PersonalWorksheet must be completed and signed by your applicant and submittedwith the application for insurance. Please note that the applicant maychoose not to reveal their financial information by marking the appropriatebox, however, regardless of whether or not this information is provided,the form must be signed by the applicant and submitted to us.

2. If, upon receipt of the application and Personal Worksheet, the applicantmeets the criteria outlined in the above “Suitability Guidelines” section,we may proceed with the processing of the application.

3

3. If the Personal Worksheet indicates that the purchase of the proposedpolicy may not be suitable financially, we are required to forward theapplicant an Intent Confirmation Form, which they must complete andreturn to us in order for us to proceed.

4. If the applicant chooses not to provide their financial information bychecking the appropriate box, the agent will significantly expedite theUnderwriting process by also submitting a signed Suitability Waiver Form.Otherwise, we must again contact your applicant regarding theserequirements and receive confirmation that they wish to proceed.

Underwriting Tools and ProtocolThe application is the first and perhaps the most important tool an Underwriter utilizesduring the Underwriting process. We cannot over-emphasize the importance ofcompleting each application thoroughly and providing details regarding healthconditions, hospitalizations, accurate height and weight, as well as medications andthe reasons they are being taken. A properly completed application and good fieldUnderwriting, utilizing the proper rate classifications beginning on page 9 of thisguide and/or the Underwriting Wizard, will result in fewer declines, fewer counter-offers, and often times significantly expedites the Underwriting process. Any additionalinformation provided by the agent with respect to activity level, exercise, work orvolunteer status, living arrangements etc. can be very valuable and provide insightwhich may not be evident from the application alone. We welcome such informationand if additional space is needed, please submit an attachment, signed and dated bythe applicant which will be treated as part of the application.

All applications must be signed and dated on the actual date completed and shouldbe received in our office within 2 weeks of the date signed.

Following is a list of additional tools, a brief description of what these tools entail, aswell as an indication of when each of these tools are generally required:

Personal History Interview (PHI) - A telephonic interview designed to confirminformation on the application, as well as to obtain additional information regardingthe applicant’s physical health, cognitive status, and activity level.

Paramedical Interview - A face-to-face interview, conducted in the applicant’s homeby a health professional. A Paramedical interview does not include blood work,urinalysis, or other invasive testing, but is a series of questions to help us furtherevaluate the applicant’s medical history, physical condition, and cognitive status. Itis also valuable because it provides additional insight into the applicant’s activitylevel and living arrangements, which may not be as evident through the use of atelephonic interview.

4

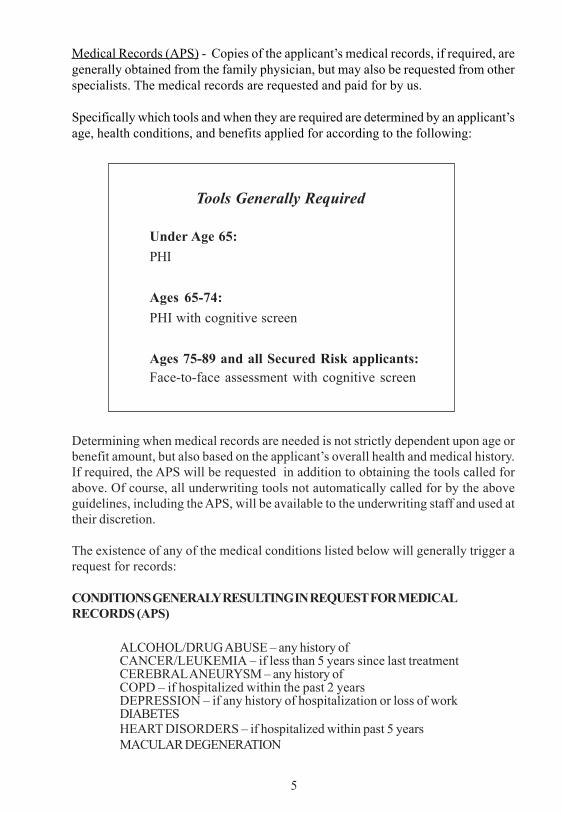

Medical Records (APS) - Copies of the applicant’s medical records, if required, aregenerally obtained from the family physician, but may also be requested from otherspecialists. The medical records are requested and paid for by us.

Specifically which tools and when they are required are determined by an applicant’sage, health conditions, and benefits applied for according to the following:

Tools Generally Required

Under Age 65:PHI

Ages 65-74:PHI with cognitive screen

Ages 75-89 and all Secured Risk applicants:Face-to-face assessment with cognitive screen

Determining when medical records are needed is not strictly dependent upon age orbenefit amount, but also based on the applicant’s overall health and medical history.If required, the APS will be requested in addition to obtaining the tools called forabove. Of course, all underwriting tools not automatically called for by the aboveguidelines, including the APS, will be available to the underwriting staff and used attheir discretion.

The existence of any of the medical conditions listed below will generally trigger arequest for records:

CONDITIONS GENERALY RESULTING IN REQUEST FOR MEDICALRECORDS (APS)

ALCOHOL/DRUG ABUSE – any history ofCANCER/LEUKEMIA – if less than 5 years since last treatmentCEREBRAL ANEURYSM – any history ofCOPD – if hospitalized within the past 2 yearsDEPRESSION – if any history of hospitalization or loss of workDIABETESHEART DISORDERS – if hospitalized within past 5 yearsMACULAR DEGENERATION

5

PERIPHERAL VASCULAR DISEASESARCOIDOSISSPINAL STENOSIS – if not surgically correctedSTROKE or TIA – any history ofSYNCOPE – if within past yearTRANSIENT GLOBAL AMNESIATREMOR

In addition to the above, an APS is likely to be requested whenever an applica-tion or applicant interview reveals any of the following:

• 3 or more conditions which are chronic (ongoing, long duration).• 4 or more current medications.• Chronic condition with lack of control, complications, or which does

not indicate regular care by a physician (indicating poorcompliance).

When the applicant is informed by the agent at time of application which tools willmost likely be required, the applicant is much more likely to understand theunderwriting process and be more willing, when necessary, to provide and/orassist us in obtaining the above information.

Underwriting ClassesThe following Underwriting Classes are currently available in most States (pleaseverify requirements within your State by checking our Website).

Preferred:Applicants who are in very good health , non smokers, and weight whichfalls within normal limits. Conditions such as well controlled hypertension,mild asthma without the use of medications, or cancer with over 5 yearssince recovery, are considered.

Premier:Applicants who are in very good health but with minor chroniccondition(s), which are well controlled and have an excellent prognosis,those who smoke, or those who have a minor problem such as mildosteoarthritis or mild, chronic depression.

Select :Applicants with more serious conditions which are adequately controlled,perhaps by the use of certain medications like steroids or in the case ofdiabetes, insulin. Also, those with significant health histories whichalthough currently well controlled are likely to increase the risk for LongTerm Care services in the future.

6

Standard (sub standard in FL):Applicants who have a very significant health condition, which althoughinsurable, greatly increases the risk for needing Long Term Care in thefuture, such as those currently being treated for cancer, severe heartconditions like cardiomyopathy, or those individuals who may have severalchronic Conditions which together, significantly increase the risk of needingLTC in the future.

Secured Risk Plan:Includes those individuals who have been diagnosed with a condition whichhistorically has been considered uninsurable. Those eligible are generallyin the beginning stages and/or exhibit little if any symptoms of the conditionand do not have an impending need for care. Examples are beginning stageParkinson’s or those who have been diagnosed with Multiple Sclerosisbut whose activities are not significantly limited. The Secured Risk Planalso allows us to offer coverage to those who, due to the significance ormultiplicity of conditions, such as diabetes with a heart condition and historyof a stroke, are not eligible for the other ltci products we offer. Those withany signs of cognitive impairment are not eligible for the Secured Risk Planor any ltci we offer.

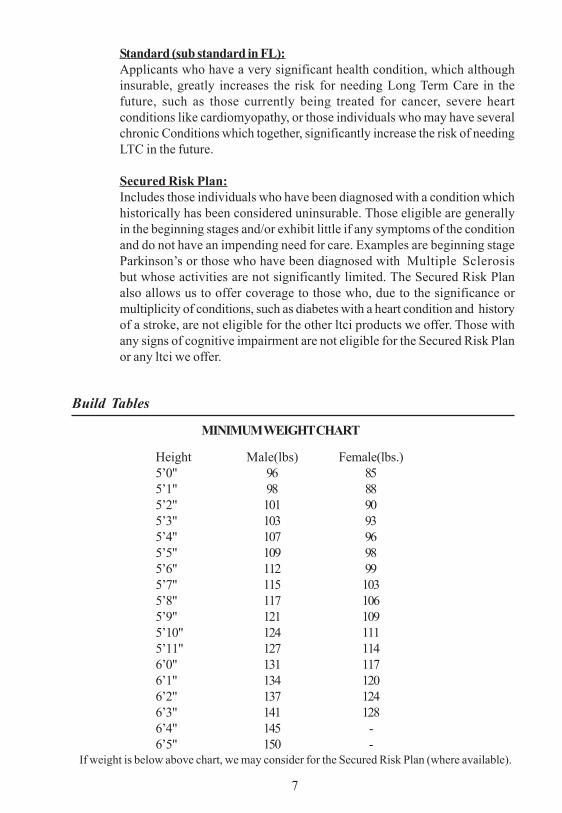

Build Tables

MINIMUM WEIGHT CHART

Height Male(lbs) Female(lbs.)5’0" 96 855’1" 98 885’2" 101 905’3" 103 935’4" 107 965’5" 109 985’6" 112 995’7" 115 1035’8" 117 1065’9" 121 1095’10" 124 1115’11" 127 1146’0" 131 1176’1" 134 1206’2" 137 1246’3" 141 1286’4" 145 -6’5" 150 -

If weight is below above chart, we may consider for the Secured Risk Plan (where available).

7

8

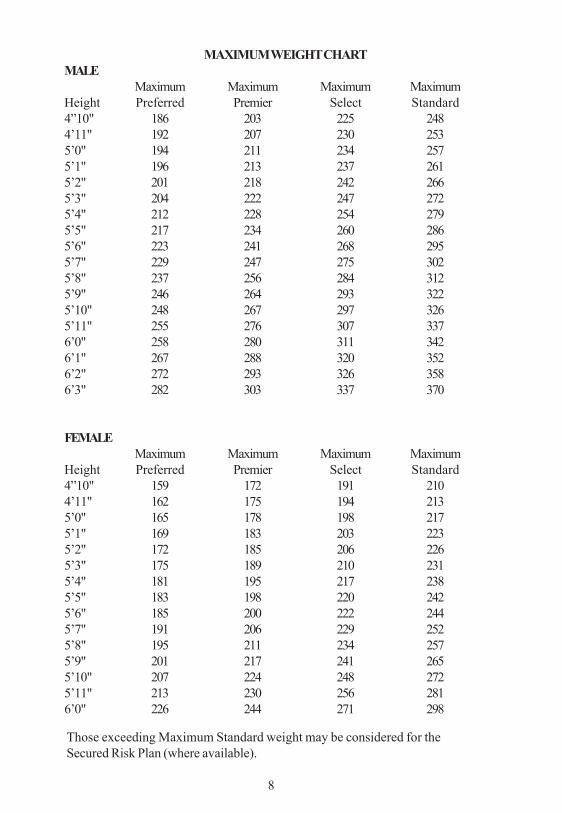

MAXIMUM WEIGHT CHARTMALE

Maximum Maximum Maximum MaximumHeight Preferred Premier Select Standard4”10" 186 203 225 2484’11" 192 207 230 2535’0" 194 211 234 2575’1" 196 213 237 2615’2" 201 218 242 2665’3" 204 222 247 2725’4" 212 228 254 2795’5" 217 234 260 2865’6" 223 241 268 2955’7" 229 247 275 3025’8" 237 256 284 3125’9" 246 264 293 3225’10" 248 267 297 3265’11" 255 276 307 3376’0" 258 280 311 3426’1" 267 288 320 3526’2" 272 293 326 3586’3" 282 303 337 370

Those exceeding Maximum Standard weight may be considered for theSecured Risk Plan (where available).

FEMALEMaximum Maximum Maximum Maximum

Height Preferred Premier Select Standard4”10" 159 172 191 2104’11" 162 175 194 2135’0" 165 178 198 2175’1" 169 183 203 2235’2" 172 185 206 2265’3" 175 189 210 2315’4" 181 195 217 2385’5" 183 198 220 2425’6" 185 200 222 2445’7" 191 206 229 2525’8" 195 211 234 2575’9" 201 217 241 2655’10" 207 224 248 2725’11" 213 230 256 2816’0" 226 244 271 298

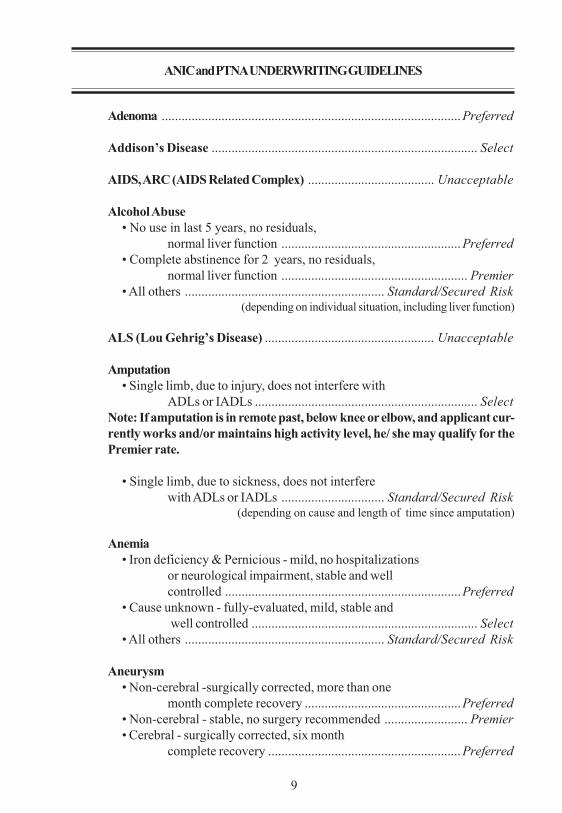

ANIC and PTNA UNDERWRITING GUIDELINES

Adenoma ..........................................................................................Preferred

Addison’s Disease ................................................................................ Select

AIDS, ARC (AIDS Related Complex) ...................................... Unacceptable

Alcohol Abuse• No use in last 5 years, no residuals,

normal liver function ......................................................Preferred• Complete abstinence for 2 years, no residuals,

normal liver function ........................................................ Premier• All others ............................................................ Standard/Secured Risk

(depending on individual situation, including liver function)

ALS (Lou Gehrig’s Disease) ................................................... Unacceptable

Amputation• Single limb, due to injury, does not interfere with

ADLs or IADLs ................................................................... SelectNote: If amputation is in remote past, below knee or elbow, and applicant cur-rently works and/or maintains high activity level, he/ she may qualify for thePremier rate.

• Single limb, due to sickness, does not interferewith ADLs or IADLs ............................... Standard/Secured Risk

(depending on cause and length of time since amputation)

Anemia• Iron deficiency & Pernicious - mild, no hospitalizations

or neurological impairment, stable and wellcontrolled .......................................................................Preferred

• Cause unknown - fully-evaluated, mild, stable andwell controlled .................................................................... Select

• All others ............................................................ Standard/Secured Risk

Aneurysm• Non-cerebral -surgically corrected, more than one

month complete recovery ...............................................Preferred• Non-cerebral - stable, no surgery recommended ......................... Premier• Cerebral - surgically corrected, six month

complete recovery ..........................................................Preferred

9

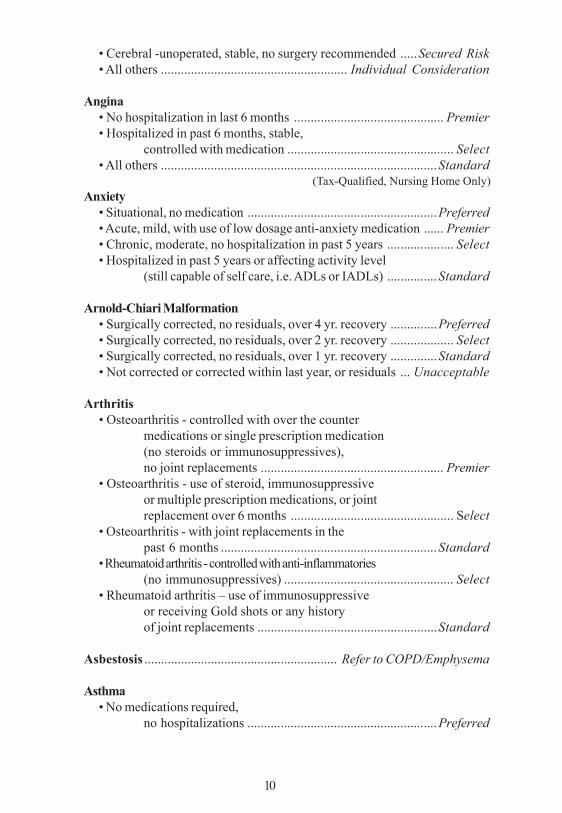

• Cerebral -unoperated, stable, no surgery recommended .....Secured Risk• All others ........................................................ Individual Consideration

Angina• No hospitalization in last 6 months ............................................. Premier• Hospitalized in past 6 months, stable,

controlled with medication .................................................. Select• All others ...................................................................................Standard

(Tax-Qualified, Nursing Home Only)Anxiety

• Situational, no medication .........................................................Preferred• Acute, mild, with use of low dosage anti-anxiety medication ...... Premier• Chronic, moderate, no hospitalization in past 5 years .................... Select• Hospitalized in past 5 years or affecting activity level

(still capable of self care, i.e. ADLs or IADLs) ...............Standard

Arnold-Chiari Malformation• Surgically corrected, no residuals, over 4 yr. recovery ..............Preferred• Surgically corrected, no residuals, over 2 yr. recovery ................... Select• Surgically corrected, no residuals, over 1 yr. recovery ..............Standard• Not corrected or corrected within last year, or residuals ... Unacceptable

Arthritis• Osteoarthritis - controlled with over the counter

medications or single prescription medication(no steroids or immunosuppressives),no joint replacements ....................................................... Premier

• Osteoarthritis - use of steroid, immunosuppressiveor multiple prescription medications, or jointreplacement over 6 months ................................................. Select

• Osteoarthritis - with joint replacements in thepast 6 months .................................................................Standard

• Rheumatoid arthritis - controlled with anti-inflammatories(no immunosuppressives) ................................................... Select

• Rheumatoid arthritis – use of immunosuppressiveor receiving Gold shots or any historyof joint replacements ......................................................Standard

Asbestosis .......................................................... Refer to COPD/Emphysema

Asthma• No medications required,

no hospitalizations .........................................................Preferred

10

• Use of single non-steroidal inhalers,no hospitalizations in past 2 years ................................... Premier

• Use of steroidal inhalers and/or oral medicationsor hospitalization in past 2 years ......................................... Select

• Frequent attacks and/or hospitalized more thanonce in the past 2 years .................................................Standard

• Requiring occasional use of oxygen ....................................Secured Risk (Tax-Qualified, Nursing Home Only)

Arteriosclerosis, ArterioscleroticHeart Disease ...................................Refer to Heart Disease and Disorders

Ataxia .........................................................................................Secured Risk

Back Disorders• Degenerative Disk Disease

Use of over the counter medications ..............................PreferredUse of prescription drugs .................................................... SelectUse of steroids or immunosuppressives or

chronic pain, no affect on activity level ..................StandardUse of steroid or immunosuppressives or

chronic pain, which affects activity level(still capable of self-carei.e. ADLs and IADLs) ........................................Secured Risk

(Tax-Qualified, Nursing Home Only)• Herniated Disk

Operated, 6 months, complete recovery .........................PreferredUnoperated, no surgery recommended,

no restrictions or affect on activity level ................PreferredUnoperated, no surgery recommended,

with restrictions or affect on activity level(still capable of self-care, i.e. ADLs and IADLs) .....Standard

(Tax-Qualified, Nursing Home Only)• Sciatica

No current treatment, no restrictions or affecton activity level, no surgery recommended ............Preferred

Current treatment, no restrictions or affecton activity level, no surgery recommended .............. Premier

With restriction or affect on activity level(still capable of self-care, i.e. ADLs and IADLs),no surgery recommended .............................................. Select

(If home health care included, Tax-Qualified homehealth care only and may require an

elimination period.)• Scoliosis

Incidental, no restrictions or affect on activity level ......Preferred

11

• Spinal StenosisSurgically corrected, complete recovery .........................PreferredUnoperated, no surgery recommended, norestrictions or affect on activity level .................................. Select

• Chronic pain or numbness, no restrictionsor affect on activity level ................................................ Standard

(Tax-Qualified, Nursing Home Only)• Chronic pain or numbness, which affects

activity level (still capable of self-carei.e. ADLs and IADLs) ............................................... Secured Risk

(Tax-Qualified, Nursing Home Only)

Bell’s Palsy ..................................................................................... Preferred

Bronchiectasis• Mild to moderate, controlled, stable

pulmonary function tests .................................................... Select• Chronic with ongoing steroid usage or

poor pulmonary function tests .......................................StandardBronchitis

• Acute, mild, well controlled .......................................................Preferred• Chronic, well controlled with use of steroid,

stable pulmonary function tests .......................................... Select• Not well controlled or poor pulmonary

function tests .......................................... Standard/Secured Risk

Bursitis ........................................................................................... Preferred

Cancer - Prostate• Over 2 years since diagnosis and treatment initiated,

PSA under 1.5, not necessarily organ-confined,but no clinical evidence of metastasis ............................ Preferred

(no involvement of bone, lymph nodes or other organs)• Over 2 years since diagnosis and treatment initiated, PSA

1.5 or over, not necessarily organ-confined, but noclinical evidence of metastasis ............................................ Select

(no involvement of bone, lymph nodes or other organs)• Under 2 years since diagnosis and treatment initiated, PSA

under 1.5, organ confined ................................................ Premier• Under 2 years since diagnosis and treatment initiated,

PSA under 1.5, not organ confined, but noclinical evidence of metastasis ............................................ Select

(No involvement of bone, lymph nodes or other organs)• Under 2 years since diagnosis and treatment initiated,

PSA1.5 or over, organ confined .......................................... Select• Less than 2 years since diagnosis and treatment initiated,

PSA 1.5 or over, not organ confined ............................... Standard

12

• Clinical evidence of metastatic cancer ....................................... Standard (Tax-Qualified, Nursing Home Only)

Medications such as lupron or radium seed implants may not be consideredcurrent treatment depending on length of time since prescribed and currentPSA levels.

Cancer - Others• Skin cancer - basal cell, squamous, removed, no metastasis ..... Preferred• Over 5 year recovery, with no recurrence .................................. Preferred• Over 2 year recovery, with no current cancer or

treatment, no metastasis ................................................... Premier• Under 2 year recovery, with no current cancer or

treatment, no metastasis ...................................................... Select• Currently under treatment or treatment in the past

2 years for metastatic cancer .......................................... Standard (Tax-Qualified, Nursing Home Only)

Note: Medications such as Tamoxifen and Ratoxifene, when used solelyfor preventative reasons, with no evidence of current cancer, will not beconsidered “treatment”.

Cane Usage (also rate for cause)Single Prong .................................................................................. PremierFour Prong ........................................................................................ Select

Cardiomegaly ................................................................................. See Heart

Carotid Artery Disease• Surgery more than 3 months ago, complete recovery………..........Premier• No surgery, with no history TIA/stroke or

syncope (blackout) ................................................... Premier• No surgery, with history of TIA/stroke,

syncope (blackout) or other symptoms .................. Standard

Carpal Tunnel Syndrome• Complete recovery or mild, non-disabling with

no surgery recommended ......................................... Preferred

Cataract• Surgically corrected ................................................................... Preferred• Surgery scheduled or recommended ......................................... Preferred

(If home health care included, Tax-Qualified only)

Cerebral Atrophy, not consistent with age ...............................Unacceptable

Cerebral Palsy ..........................................................................Unacceptable

13

Cerebral Vascular Accident ................................................... Refer to Stroke

Cerebral Vascular Disease ......................................................Unacceptable

Charcot-Marie-Tooth Disease ..................................................Unacceptable

Chronic Fatigue Syndrome• Well controlled, little effect on activities ........................................ Select• Limiting lifestyle or unable to work ..................................... Secured Risk

Chronic Obstructive Lung Disease (COPD/Emphysema)• No hospitalizations or treatment in 2 years ................................. Premier• Use of medications or treatment in the past 2 years ....................... Select• Frequent episodes of shortness of breath or

causing fatigue or hospitalized more thanonce in past 2 years ................................................ Standard

(Tax-Qualified only)• Requiring occasional use of oxygen ................................... Secured Risk

(Tax-Qualified, Nursing Home Only)

Note: Combinations of conditions are always important, particularly withCOPD. COPD in combination with conditions such as Heart Disease, Hyper-tension, Obesity or Circulatory Disorders is likely to result in a higherrating than listed above.

Cirrhosis of the Liver ................................................................ Secured Risk

Claudication ......................................................................................... Select

Colitis• No steroids or immunosuppressives, no complications ............ Preferred• Use of steroids or immunosuppressives

or colostomy required .................................................. SelectNote: Please refer to Colostomy if in place.

Colostomy ............................................................................................. Select

Note: If applicant currently works, he/she may qualify for the Premier rate.Conversely, length of time colostomy in place and overall condition of applicantalso considered. A frail applicant, for example, may qualify only for the Standardrate and not be eligible for home health care.

Congestive Heart Failure ................... Refer to Heart Disease and Disorders

CREST Syndrome• Mild symptoms, no lung involved and no signs of scleroderma ... Select

(Tax-Qualified, Nursing Home Only)

14

15

• Moderate symptoms or signs of mild lunginvolvement or limited scleroderma ................................ Standard

(Tax-Qualified, Nursing Home Only)• Others .................................................................................. Secured Risk

Crohn’s Disease (Ileitis)• Controlled with diet and/or nonsteroidals,

no complications ........................................................... Preferred• Use of steroids or immunosuppressives or

requiring colostomy ............................................................ SelectNote: Please refer to Colostomy if in place.

Cushing Disease/Syndrome• Diagnosed over 2 years ago, mild symptoms ................................. Select• Diagnosed or surgery within 2 years ................................... Secured Risk

Cystic Fibrosis• Below age 50 ......................................................................Unacceptable

• Over age 50, mild, well controlled ................................................... Select• Over age 50, all others ......................................................... Secured Risk

Cystitis ............................................................................................ Preferred

Dementia ...................................................................................Unacceptable

Depression• Acute or situational, no affect on lifestyle, complete

recovery with no current treatment ................................ Preferred• Chronic

Controlled with anti-depressants, low to mid-rangedosage levels, no affect on activity level and nohospitalization in past 5 years ..................................... Premier

Example of low to midrange dosage levels per day:Elavil – max 100 mgDesyrel – max 300 mgPamelor – max 100 mgPaxil – max 40 mgProzac – max 60 mgSinequan – max 100 mgZoloft – max 100 mg

• Controlled with anti-depressants exceedingmidrange daily dosage, no affect on activitylevel and no hospitalization in past 5 years ........................ Select

16

• Hospitalized in past 5 years or affectingactivity level (still capable of self-care,i.e. ADLs or IADLs) ................................................ Standard

• Manic-Depressive (bipolar), controlled withno affect on activity level,no hospitalizations in past 2 years .......................... Standard

• Manic-Depressive (bipolar), affecting activity level(still capable of self-care, i.e. ADLs or IADLs),no hospitalizations in past 2 years .................... Secured Risk

• Manic-Depressive, hospitalized in past 2 years ....Unacceptable• Psychosis or personality disorder. ........................Unacceptable

Diabetes Mellitus** In order to properly evaluate a diabetic risk, the A1c level, a measurement

of one’s average blood sugar level, should be known.

TYPE I (Juvenile)• A1c less than 9 ............................................................. Standard• All Others ..........................................................................SR400

TYPE II (Adult Onset) Please see table below for other risk factors and degree of control guidelines

Diagnosed within the past year• Well controlled, no other risk factors, no insulin .............. Select• Adequately controlled, or use of insulin,

no other risk factors ................................................ Standard• Poorly controlled, or other risk factor(s) ...........................SR400

Diagnosed between 1 and 10 years ago• A1c, Blood Pressure, and Lipids all well controlled,

no other risk factorsand if insulin - under 25 units .................................... Premier

• A1c, Blood Pressure, and Lipids adequately controlled,no other risk factors,and if insulin -under 75 units ....................................... Select

• A1c, Blood Pressure, or Lipids not adequatelycontrolled and/or insulin - over 75 units ................. Standard

Diagnosed between 10 and 15 years ago• A1c under 7, Blood Pressure and Lipids

adequately controlled, no other risk factors,and if insulin - under 75 units ....................................... Select

• A1c over 7, or Blood Pressure/Lipidsnot adequately controlled, or other risk factors,and if insulin -under 75 units .................................. Standard

Diagnosed over 15 years ago or any of the following:• A1c over 9, not adequately controlled,

Blood Pressure or Lipids,or any other risk factors, ...................Standard/Secured Risk

Diabetes Control/Risk Guidelines

Diabetic Control Guidelines:(A1c is the measurement of one’s average blood sugar levels)

• A1c below 7 ........................................ well controlled• A1c between 7 and 8 ............... adequately controlled• A1c between 8 and 9 ......... not adequately controlled• A1c over 9 ...................................... poorly controlled

Other Factors’ Control Guidelines with Diabetics:• Blood Pressure under 135/85 .............. well controlled• Blood Pressure under 140/90 .. adequately controlled• Blood Pressure

over 140/90 .................. not adequately controlled• LDL (lipid) under 100 .......................... well controlled• LDL (lipid) between

100 and 130 ........................ adequately controlled• LDL (lipid) over 130 .......... not adequately controlled

Other Risk Factors• Heart Conditions• Significantly Overweight• Circulatory condition or history of stroke(s), TIA(s)• End-organ disease (kidneys, eyes, etc.)• Neuropathy• History of smoking

Dialysis ...................................................................................... Secured Risk (Tax-Qualified, Nursing Home Only)

Disability:•Limitations resulting in the inability to perform duties at work cansignificantly increase the risk of being unable to perform one’s IADLsand/or ADLs. Therefore, those who are considered “disabled” and receive

17

Social Security Disability or retired due to a disability are often not eligiblefor LTC insurance. When considering a prospective applicant, the agentmust determine what condition(s) have resulted in being eligible fordisability and how this affects their future risk of needing LTC services. If,after consulting this guide, your client appears to be eligible, we suggestyou consult an Underwriter prior to submitting an application or anyonereceiving disability payments.

Diverticulosis – Diverticulitis ........................................................ Preferred

Down’s Syndrome .....................................................................Unacceptable

Drug Abuse• Complete abstinence for 5 years, no residuals ........................... Preferred• Complete abstinence for 2 years, no residuals ............................. Premier• All others or any history IV drug use ..................................Unacceptable

Emphysema ............................................................................. Refer to COPD

Epilepsy• Well-controlled with no seizures in past 2 years ........................ Preferred• Currently controlled with no more than

one seizure in past 6 months ............................................... Select• More than one seizure in past 6 months .................................... Standard

Esophagitis ...................................................................................... Preferred

Fibromyalgia• Mild pain with no symptoms of fatigue or mild fatigue ................ Premier• Mild to moderate pain and/or moderate Fatigue ............................. Select

(Tax-Qualified policies are more likely to be offered.)• Severe pain and/or severe fatigue………..............................……Standard

(Tax-Qualified policies are more likely to be offered.)

Fractures• Due to injury/trauma with complete recovery ...............................Preferred• Compression fractures due to Osteoporosis Single

occurrence more than 2 years ago withcomplete recovery .......................................................... Standard

(Tax-Qualified, Nursing Home Only)• All others ............................................................................. Secured Risk

Gallbladder Disorders ..................................................................... Preferred

18

Gastritis ........................................................................................... Preferred

Gaucher’s Disease .................................................................... Secured Risk

Glaucoma• Well controlled, stable with minimal vision loss ....................... Preferred• Poorly controlled or unstable with minimal vision loss .................. Select• Vision loss causing functional impairment .........................Unacceptable

Gout ................................................................................................. Preferred

Graves Disease ................................................................................ Preferred

Guillain-Barre Syndrome• Full recovery, no residual weakness .......................................... Preferred• Post syndrome, with residual weakness ........ Select/Standard (TQ only)• Currently afflicted ...............................................................Unacceptable

Heart Disease and Disorders• No hospitalization or Single hospitalization

over 1 year ago, stable ..................................................... Premier• Single hospitalization in last 1 year, stable ..................................... Select• More than one hospitalization in past 1 year ............................ Standard

(Tax-Qualified, Nursing Home Only)Unless:• Cardiomyopathy

Without CHF (Congestive Heart Failure) or singleepisode of CHF in the past 2 years ......................... Standard

(Tax-Qualified, Nursing Home Only)All others ................................................................. Secured Risk

(Tax-Qualified, Nursing Home Only)• Congestive Heart Failure

Single episode, surgically corrected, no treatmentin past 1 year (no Cardiomyopathy) .......................... Premier

Single episode, hospitalized within past 1 year,currently stable, controlled with medications(no Cardiomyopathy) ................................................... Select

Single episode with Cardiomyopathy ............................ StandardAll others ................................................................. Secured Risk

• Atrial FibrillationSingle episode, more than 1 year ago ............................... PremierMore than one episode or episode in past 1 year ago ........ Select

Note: Combinations of conditions are always important, particularly with HeartConditions. Heart Conditions in combination with conditions such as diabetes,Hypertension, Obesity or Circulatory Disorders is likely to result in a higherrating than listed above.

19

20

Hemochromatosis• Mild, no organ or joint involument, normal stable

blood studies, early diagnosis and treatment ..................Premier• Others ............................................................................................Select

Hemophilia ................................................................................. Secured Risk

Hemorrhoids .................................................................................... Preferred

Hepatitis• Acute, complete recovery, normal liver function

(unless Hepatitis C) ........................................................Preferred• Chronic, active, elevated enzymes (abnormal liver function)

or history of Hepatitis C ...........................................Secured Risk

Hernia .............................................................................................Preferred

Hip Replacement ....................................................... See Joint Replacement

HIV positive .............................................................................Unacceptable

Hodgkin’s Disease ...................................................................... See Cancer

Huntington’s Chorea ............................................................... Unacceptable

Hydrocephalus ......................................................................... Secured Risk

Hyperlipidemia ............................................................................... Preferred

Hypertension• Adequately controlled, readings under 140/90 ......................... Preferred• Not adequately controlled, readings under 170/100 ....................Premier• Poorly controlled, readings of 170/100 or over ...............................Select

Note: Combinations of conditions are always important, particularly withHypertension. Hypertension in combination with conditions such as Diabetes,Heart Disease, Obesity or Circulatory Disorders is likely to result in a higherrating than listed above.

Hyperthyroidism ............................................................................. Preferred

Hypothyroidism .............................................................................. Preferred

Idiopathic Thrombocytopenic Purpura• Asymptomatic ........................................................................... Standard• Recurrent Bleeding or platelet transfusions ....................... Secured Risk

Incontinence• Urinary

Surgically corrected, complete recovery .......................... PreferredStress incontinence, mild, infrequent ............................ PreferredStress incontinence, wearing protection..........................PremierNeurogenic Bladder ................................................ Secured Risk

• Fecal ......................................................................................Unacceptable

Irritable Bowel Syndrome .............................................................. Preferred

Joint Replacement• Due to trauma, over 6 months, complete recovery ................... Preferred• Due to Arthritis .................................................................... See Arthritis

Kidney Failure ......................................................................... Secured Risk (Tax-Qualified, Nursing Home Only)

Kidney Stones ................................................................................. Preferred

Kidney Removal (donor) .................................................................. Preferred

Kidney Removal (due to disease) ..........................................................Select

Kidney Transplant (recipient) .................................................. Secured Risk

Knee Replacement .....................................................See Joint Replacement

Laminectomy & Spinal Fusion• Over 1 year, full recovery, no restrictions

or affect onactivity level ............................................... Preferred• Over 1 year, recovered, but has impacted

activity level (still capable of self-care,i.e. with ADLs and IADLs) ...............................................Premier

• Under 1 year, full recovery, no restrictionsor affect on activity level ....................................................Select

• Under 1 year, with restrictions or affect onactivity level .......................................................... Unacceptable

Leukemia• No symptoms or treatment in the past 5 years,

single occurrence .............................................................Premier• No symptoms or treatment in the past 2 years,

or history of recurrence ......................................................Select• Currently under treatment ......................................................... Standard

(Tax-Qualified, Nursing Home Only)

21

Lung Surgery (Pneumonectomy, Lobectomy, Pneumothorax)• Over 3 months, 80% of lung capacity remaining ...........................Select• Over 3 months, less than 80% of lung capacity remaining ....... Standard• Over 3 months, requiring occasional use of oxygen .......... .Secured Risk

(Tax-Qualified, Nursing Home Only)• Less than 3 months or continuous use of oxygen .............Unacceptable

Lupus• External, discoid, inactive ............................................................Premier• Internal, systemic

No use of steroids ......................................................... StandardCurrent use or history of use of steroids ................ Secured Risk

Lyme Disease• Complete recovery, no residuals ............................................... Preferred• Under treatment, no neurological involvement ..............................Select• With neurological symptoms .............................................. Secured Risk

Lymphoma ................................................................................... See Cancer

Macular Degeneration• Minimal visual impairment, slowly progressive

(sometimes referred to as dry Macular Degeneration) ........Select(Tax-Qualified only, no home health care

and max lifetime benefits may be limited)• Moderate visual impairment, slowly progressive, no affect

on activity level (can still be referred to asdry Macular Degeneration) .................................... Standard

(Tax-Qualified only, no home health careand max lifetime benefits may be limited)

• Significant visual impairment, resulting in reduction of activitylevel, such as discontinuation of driving, (sometimesreferred to as Wet Macular Degeneration) .............Unacceptable

Manic Depression ..................................................................See Depression

Memory Loss ........................................................................... Unacceptable

Meniere’s Syndrome ...................................................................... Preferred

Meningitis• One year complete recovery, no residuals ................................ Preferred• One year complete recovery with minor residuals

(such as seizures) ............................ refer to the specific residual• Less than one year recovery or more significant residuals

(such as permanent paralysisor mental impairment) ............................................. Unacceptable

22

Multiple Sclerosis ..................................................................... Secured Risk

Muscular Dystrophy ................................................................ Unacceptable

Myasthenia Gravis ..................................................................... Secured Risk

Nephrectomy ......................................... See Kidney Removal/Kidney Donor

Nephritis• Acute, no renal failure ................................................................ Preferred• Chronic .......................................... rate according to cause of condition

Neuralgia• Acute, mild ................................................................................ Preferred• Chronic (such as Diabetic, Peripheral, Alcoholic), but mild ............ Select• Chronic and severe or affecting activity level ........................... Standard

Neurofibromatosis ........................................................................... Standard (Tax-Qualified, Nursing Home Only)

Neurogenic Bladder ........................................................... See Incontinence

Obsessive Compulsive Disorder• No medications, does not affect activity level ........................... Preferred• Controlled with medications, does not affect

with activity level ......................................................... Select• All others ........................................................................... Unacceptable

Obesity ................................................................................ See Weight Chart

Organ Transplants• One year, complete recovery, no complications,

condition stable ....................................................... Secured Risk

Organic Brain Syndrome ........................................................ Unacceptable

Osteomyelitis• One year, complete recovery ..................................................... Preferred• Within last year, no longer being treated and no residuals ......... Premier• Currently being treated ........................................................ Secured Risk

Osteoporosis• Minor loss of bone density, has not contributed to

any fractures,may be being treated withmedications such as Fosamax or Didronelor with Calcium supplements ........................................... Premier

23

• With history of compression fractures ............................... Secured Risk

Note: If Osteoporosis is an incidental finding, (such as it was noted in an X-raytaken for another condition), and there are no symptoms, no history of fracturesand no treatment recommended and applicant is otherwise healthy and active,Preferred rating will be offered.

Otitis Media .................................................................................... Preferred

Oxygen Usage• Intermittent or Occasional Use ........................................... Secured Risk

(Nursing Home Only)• Continuous Use ................................................................. Unacceptable

Paget’s Disease• Of the breast .......................................................................... See Cancer• Diagnosed more than 2 years ago, no history

of fractures or other symptoms .................................... Select• History of fractures, change in bone structure or

diagnosed in past 2 years ...................................... Standard

Pancreatitis ..................................................................................... Preferred

Parkinson’s Disease ................................................................. Secured Risk(No affect on activity level, still capableof self-care, i.e. ADLs and IADLs)

Peptic Ulcer ..................................................................................... Preferred

Peripheral Neuropathy ......................................................................... Select

Peripheral Vascular Disease ................................................................ Select

Note: Combinations of conditions are always important, particularly withCirculatory Disorders. Circulatory Disorders in combination with conditionssuch as Diabetes, Heart Disease, Hypertension or Obesity is likely to resultin a higher rating than listed above.

Peritonitis ...................................................................................... Preferred

Phlebitis• Acute ........................................................................................ Preferred• Chronic ........................................................................................... Select

Pick’s Disease ......................................................................... Unacceptable

Polio• Complete recovery, no residuals ............................................... Preferred

24

• Post-Polio Syndrome .......................................................... Secured Risk

Polycythemia Vera• In remission for over 2 years .................................................... Standard• Currently active or treatment within the past 2 years ......... Secured Risk

Polymyalgia Rheumatica• No medications needed .............................................................. Premier• Well-controlled with non-steroidals ............................................... Select• Use of steroids .......................................................................... Standard

Prostatectomy• Benign, complete recovery ....................................................... Preferred• Malignant ..............................................................................See Cancer

Prostatitis ....................................................................................... Preferred

Renal Failure .................................................................. See Kidney Failure

Restless Leg Syndrome .................................................................. Preferred

Retinal Detachment ........................................................................ Preferred

Sarcoidosis• Over 3 year recovery, no history of lung or liver

involvement and no complications .................................... Select• No symptoms or treatment in the past 2 yrs,

no complications ........................................................... Standard• Active or symptoms or treatment in the past 2 years .......... Secured Risk

Schizophrenia ......................................................................... Unacceptable

Sciatica .......................................................................... See Back Disorders

Scleroderma• Localized or limited without internal organ involvement .......... Standard

(Tax-Qualified, Nursing Home Only)• Others ................................................................................. Secured Risk

Seizures .................................................................................... .See Epilepsy

Senility ................................................................................... Unacceptable

Sleep Apnea• Stable, no C-PAP Machine ........................................................ Preferred• Use of C-PAP machine ................................................................... Select

25

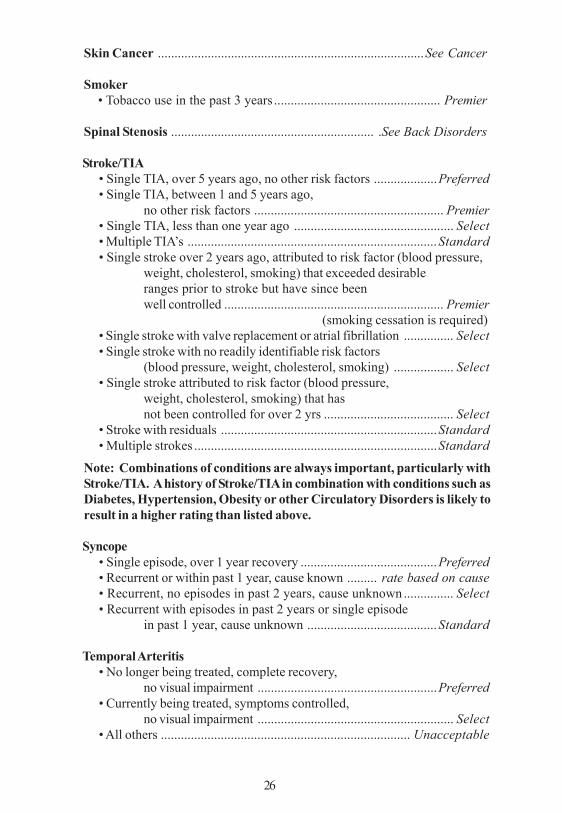

Skin Cancer ................................................................................See Cancer

Smoker• Tobacco use in the past 3 years .................................................. Premier

Spinal Stenosis ............................................................. .See Back Disorders

Stroke/TIA• Single TIA, over 5 years ago, no other risk factors ...................Preferred• Single TIA, between 1 and 5 years ago,

no other risk factors ......................................................... Premier• Single TIA, less than one year ago ................................................ Select• Multiple TIA’s ...........................................................................Standard• Single stroke over 2 years ago, attributed to risk factor (blood pressure,

weight, cholesterol, smoking) that exceeded desirableranges prior to stroke but have since beenwell controlled .................................................................. Premier

(smoking cessation is required)• Single stroke with valve replacement or atrial fibrillation ............... Select• Single stroke with no readily identifiable risk factors

(blood pressure, weight, cholesterol, smoking) .................. Select• Single stroke attributed to risk factor (blood pressure,

weight, cholesterol, smoking) that hasnot been controlled for over 2 yrs ....................................... Select

• Stroke with residuals .................................................................Standard• Multiple strokes .........................................................................Standard

Note: Combinations of conditions are always important, particularly withStroke/TIA. A history of Stroke/TIA in combination with conditions such asDiabetes, Hypertension, Obesity or other Circulatory Disorders is likely toresult in a higher rating than listed above.

Syncope• Single episode, over 1 year recovery .........................................Preferred• Recurrent or within past 1 year, cause known ......... rate based on cause• Recurrent, no episodes in past 2 years, cause unknown............... Select• Recurrent with episodes in past 2 years or single episode

in past 1 year, cause unknown .......................................Standard

Temporal Arteritis• No longer being treated, complete recovery,

no visual impairment ......................................................Preferred• Currently being treated, symptoms controlled,

no visual impairment ........................................................... Select• All others ........................................................................... Unacceptable

26

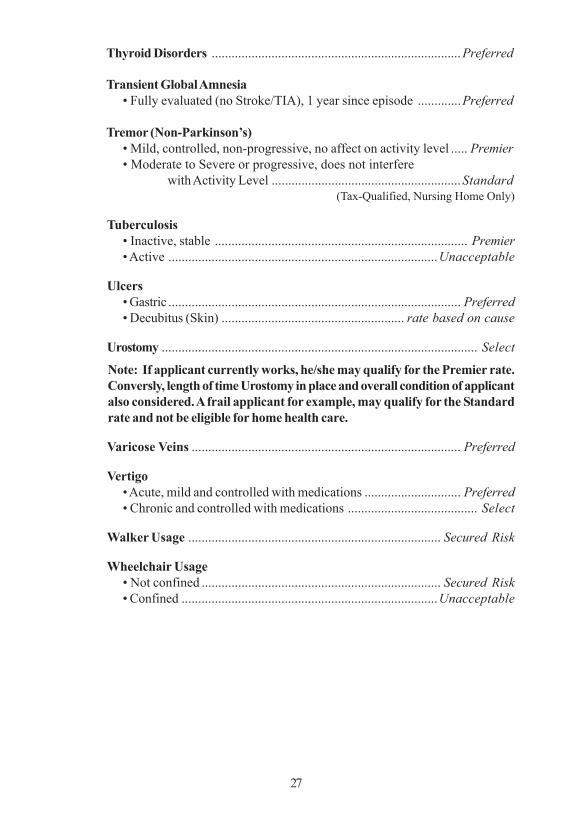

Thyroid Disorders ...........................................................................Preferred

Transient Global Amnesia• Fully evaluated (no Stroke/TIA), 1 year since episode .............Preferred

Tremor (Non-Parkinson’s)• Mild, controlled, non-progressive, no affect on activity level ..... Premier• Moderate to Severe or progressive, does not interfere

with Activity Level .........................................................Standard (Tax-Qualified, Nursing Home Only)

Tuberculosis• Inactive, stable ............................................................................ Premier• Active .................................................................................Unacceptable

Ulcers• Gastric ........................................................................................ Preferred• Decubitus (Skin) ....................................................... rate based on cause

Urostomy ............................................................................................... Select

Note: If applicant currently works, he/she may qualify for the Premier rate.Conversly, length of time Urostomy in place and overall condition of applicantalso considered. A frail applicant for example, may qualify for the Standardrate and not be eligible for home health care.

Varicose Veins ................................................................................. Preferred

Vertigo• Acute, mild and controlled with medications ............................. Preferred• Chronic and controlled with medications ....................................... Select

Walker Usage ............................................................................ Secured Risk

Wheelchair Usage• Not confined ........................................................................ Secured Risk• Confined .............................................................................Unacceptable

27

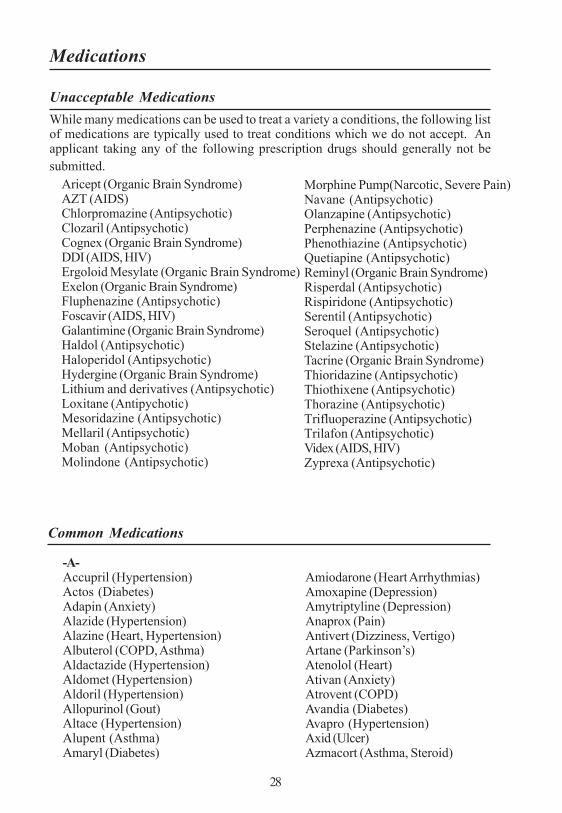

Medications

Unacceptable MedicationsWhile many medications can be used to treat a variety a conditions, the following listof medications are typically used to treat conditions which we do not accept. Anapplicant taking any of the following prescription drugs should generally not besubmitted.

-A-Accupril (Hypertension)Actos (Diabetes)Adapin (Anxiety)Alazide (Hypertension)Alazine (Heart, Hypertension)Albuterol (COPD, Asthma)Aldactazide (Hypertension)Aldomet (Hypertension)Aldoril (Hypertension)Allopurinol (Gout)Altace (Hypertension)Alupent (Asthma)Amaryl (Diabetes)

Common Medications

Amiodarone (Heart Arrhythmias)Amoxapine (Depression)Amytriptyline (Depression)Anaprox (Pain)Antivert (Dizziness, Vertigo)Artane (Parkinson’s)Atenolol (Heart)Ativan (Anxiety)Atrovent (COPD)Avandia (Diabetes)Avapro (Hypertension)Axid (Ulcer)Azmacort (Asthma, Steroid)

28

Morphine Pump(Narcotic, Severe Pain)Navane (Antipsychotic)Olanzapine (Antipsychotic)Perphenazine (Antipsychotic)Phenothiazine (Antipsychotic)Quetiapine (Antipsychotic)Reminyl (Organic Brain Syndrome)Risperdal (Antipsychotic)Rispiridone (Antipsychotic)Serentil (Antipsychotic)Seroquel (Antipsychotic)Stelazine (Antipsychotic)Tacrine (Organic Brain Syndrome)Thioridazine (Antipsychotic)Thiothixene (Antipsychotic)Thorazine (Antipsychotic)Trifluoperazine (Antipsychotic)Trilafon (Antipsychotic)Videx (AIDS, HIV)Zyprexa (Antipsychotic)

Aricept (Organic Brain Syndrome)AZT (AIDS)Chlorpromazine (Antipsychotic)Clozaril (Antipsychotic)Cognex (Organic Brain Syndrome)DDI (AIDS, HIV)Ergoloid Mesylate (Organic Brain Syndrome)Exelon (Organic Brain Syndrome)Fluphenazine (Antipsychotic)Foscavir (AIDS, HIV)Galantimine (Organic Brain Syndrome)Haldol (Antipsychotic)Haloperidol (Antipsychotic)Hydergine (Organic Brain Syndrome)Lithium and derivatives (Antipsychotic)Loxitane (Antipychotic)Mesoridazine (Antipsychotic)Mellaril (Antipsychotic)Moban (Antipsychotic)Molindone (Antipsychotic)

-B-Baclofen (Spasm, Multiple Sclerosis)Beclovent (Asthma, Steroid)Beconase (Asthma, Steroid)Brethine (Asthma, COPD)Bumex (Hypertension, Edema)Buspar (Anxiety)

C-Calan (Heart)Calcimar (Osteoporosis)Capoten (Hypertension)Capozide (Hypertension)Captopril (Hypertension)Carbidopa (Parkinson’s)Cardizem (Heart, Hypertension)Cardura (Hypertension)Casodex (Cancer/Prostate)Catapres (Hypertension)Celebrex (Arthritis)Centrax (Anxiety)Clinoril (Arthritis)Clonazepam (Seizures)Corgord (Heart, Hypertension)Coumadin (Blood Thinner)Cozaar (Hypertension)

-D-Darvocet (Pain)DepoProvera (Cancer)Desyrel (Depression)Diabenese (Diabetes)Diabeta (Diabetes)Didronel (Osteoporosis, Pagets

Disease)Digoxin (Heart Rhythym)Dilantin (Epilepsy)Diltiazem (Heart, Hypertension)Ditropan (Incontinence)Dypyridamole (Circulation, Stroke)Diuril (Hypertension)Dyazide (Hypertension, Edema)

-E-Effexor (Depression)Elavil (Depression)

29

Eldepryl (Parkinson’s)Eulexin (Cancer/Prostate)

-F-Feldene (Arthritis)Flomax (Prostate)Flonase (Asthma, Steroid)Flovent (Asthma, Steroid)Fosomax (Osteoporosis)

-G-Glipizide (Diabetes)Glucophage (Diabetes)Glyburide (Diabetes)Gold (Rheumatoid Arthritis)

-H-HCTZ (Hypertension)Heparin (Blood Thinner)Hytrin (Hypertension)

-I-Imuran (Cancer)Imipramine (Anxiety)Inderal (Heart, Hypertension)Indocin (Arthritis)Insulin (Diabetes)Isoptin (Heart)Isordil (Angina, Heart)

-K-K-lor (Hypertension)Kaochlor (Hypertension)Kaon (Hypertension)Klonopin (Seizures)

-L-Lanoxin (Heart)Lasix (Edema, Hypertension)Laquenil (Arthritis)Levodopa (Parkinson’s)Librax (Anxiety)Librium (Anxiety)Lipitor (Cholesterol)Lopressor (Hypertension)Lorazepam (Anxiety)

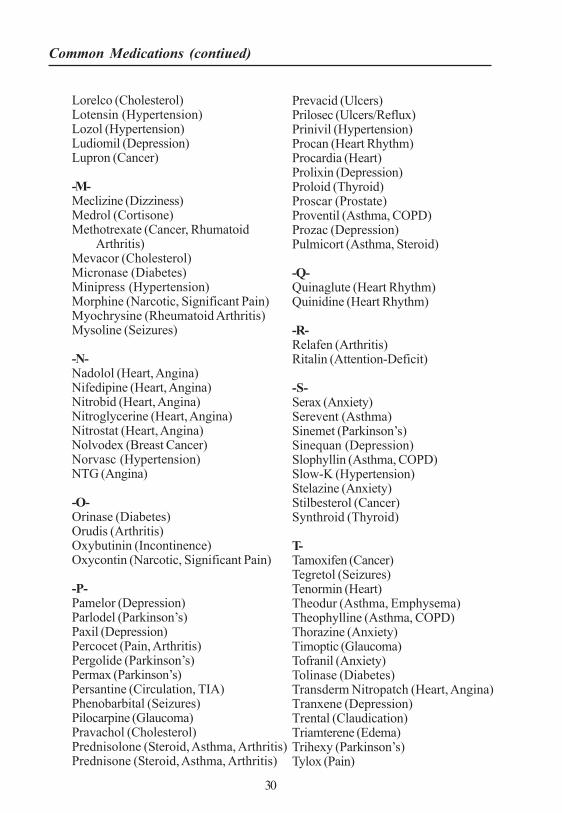

Common Medications (contiued)

Lorelco (Cholesterol)Lotensin (Hypertension)Lozol (Hypertension)Ludiomil (Depression)Lupron (Cancer)

-M-Meclizine (Dizziness)Medrol (Cortisone)Methotrexate (Cancer, Rhumatoid

Arthritis)Mevacor (Cholesterol)Micronase (Diabetes)Minipress (Hypertension)Morphine (Narcotic, Significant Pain)Myochrysine (Rheumatoid Arthritis)Mysoline (Seizures)

-N-Nadolol (Heart, Angina)Nifedipine (Heart, Angina)Nitrobid (Heart, Angina)Nitroglycerine (Heart, Angina)Nitrostat (Heart, Angina)Nolvodex (Breast Cancer)Norvasc (Hypertension)NTG (Angina)

-O-Orinase (Diabetes)Orudis (Arthritis)Oxybutinin (Incontinence)Oxycontin (Narcotic, Significant Pain)

-P-Pamelor (Depression)Parlodel (Parkinson’s)Paxil (Depression)Percocet (Pain, Arthritis)Pergolide (Parkinson’s)Permax (Parkinson’s)Persantine (Circulation, TIA)Phenobarbital (Seizures)Pilocarpine (Glaucoma)Pravachol (Cholesterol)Prednisolone (Steroid, Asthma, Arthritis)Prednisone (Steroid, Asthma, Arthritis)

Prevacid (Ulcers)Prilosec (Ulcers/Reflux)Prinivil (Hypertension)Procan (Heart Rhythm)Procardia (Heart)Prolixin (Depression)Proloid (Thyroid)Proscar (Prostate)Proventil (Asthma, COPD)Prozac (Depression)Pulmicort (Asthma, Steroid)

-Q-Quinaglute (Heart Rhythm)Quinidine (Heart Rhythm)

-R-Relafen (Arthritis)Ritalin (Attention-Deficit)

-S-Serax (Anxiety)Serevent (Asthma)Sinemet (Parkinson’s)Sinequan (Depression)Slophyllin (Asthma, COPD)Slow-K (Hypertension)Stelazine (Anxiety)Stilbesterol (Cancer)Synthroid (Thyroid)

T-Tamoxifen (Cancer)Tegretol (Seizures)Tenormin (Heart)Theodur (Asthma, Emphysema)Theophylline (Asthma, COPD)Thorazine (Anxiety)Timoptic (Glaucoma)Tofranil (Anxiety)Tolinase (Diabetes)Transderm Nitropatch (Heart, Angina)Tranxene (Depression)Trental (Claudication)Triamterene (Edema)Trihexy (Parkinson’s)Tylox (Pain)

30

Common Medications (contiued)

31

ReplacementsWhen applying for coverage intended to replace existing coverage, a ReplacementForm must be signed by the applicant and agent and submitted along with theapplication. If the existing coverage is with another company (external replacement),a Comparison Form must also be submitted. A Comparison Form is not required if theapplicant wishes to replace a policy which they currently have with our company(internal replacement).

Upon receipt of an application indicating an external replacement, most states requireus to notify, in writing, the company providing the existing coverage that the applicantintends to replace their policy.

The agent should take into consideration that all benefits under the new plan will bebased on the applicant’s attained age and their rate class will be based on theircurrent health. Regardless if internal or external, the replacement must be in the bestinterest of the policyholder/applicant. If the proposed policy does not improve thecoverage currently held by the applicant, (improved coverage, reduced premium,etc.), the request for new coverage will be denied.

Counter OffersWhen an applicant does not qualify for the coverage applied, we will make everyattempt to offer alternative coverage. Depending on the circumstances, this “counteroffer” may be the same product at a different rate class or, when waranted, we mayoffer a different product. Counter offers may also be in the form of reduced benefits,higher elimination period, or offering a Tax Qualified policy in lieu of a Non-Taxqualified policy.

-V-Valium (Anxiety)Vancenase (Asthma, Steroid)Vanceril (Emphysema, Asthma, Steroid)Ventolin (COPD)Verapamil (Heart, Hypertension)Vioxx (Arthritis)Vivactil (Depression)Voltaren (Rheumatoid Arthritis)

-W-Warfarin (Blood Thinner)

-X-Xanax (Anxiety)

-Z-Zestril (Hypertension)Zoloft (Anxiety)Zyloprim (Gout)

Common Medications (contiued)

Once we determine that a counter offer is necessary, the agent is informed of theoffer. Often times there are several options in terms of which benefits best fit theclients needs and we therefore await the agent’s reply and instructions on specificallyhow the policy should be issued.

Although our ability to counter offer utilizing our variety of products and rate classesallows many policies to be placed which would otherwise be rejected, we realize thatplacing a count-offer is often times difficult. Many counter offers may be avoided bygood field underwriting and utilizing the Underwriting Guidelines in this book at timeof application. We also welcome pre-qualification calls, where the agent can speakdirectly to an Underwriter who will offer suggestions on how the application shouldbe submitted based on the information provided. As mentioned in the Introduction,the Underwriting Wizard can also assist you in rating an applicant appropriately.

Spousal DiscountThe States of Michigan, New Jersey, and South Dakota require the spousal discountto be applied to any policy where the applicant has a spouse, regardless of whetherthe spouse applies for or is issued coverage. In all other States, the spousal discountis applied to each policy when, together, both spouses apply for and are issuedcoverage.We also will apply the spousal discount to a policy if the applicant’s spouse is anexisting policyholder of ours. If the second spouse’s policy is issued within one yearof the first spouse’s policy, we will also apply the spousal discount to the firstspouse’s policy upon the next renewal date.

Please note that if one spouse cancels their coverage within the 30 day free examinationperiod, the spousal discount will be removed from the remaining spouse’s policy. Inthe event of death, however, the spousal discount will remain in effect on the survivingspouse’s policy.

Those eligible for the spousal discount include all legally married couples, includingsame sex marriages or common law marriages, according to the laws within the Stateof issuance. Those legal spouses who do not have the same last name should submitevidence, such as a notarized document or copy of a jointly filed tax return, provingtheir marital status.

ReissuesAll requests to change coverage received in our office within 30 days of policydelivery to the applicant, will be considered for Reissue. The request must clearlyindicate what changes are desired and must be signed by the policyholder. Thesechanges may be additional benefits, reduction of benefits, or change in policy form.Aside from reductions, none of these changes are guaranteed and therefore must bereviewed and approved by an Underwriter. Any such change, if approved, will be

32

made effective as of the effective date of the policy, and a new schedule page reflectingthe changes will be forwarded to the agent or policyholder.

Requests for changes to an existing policy which the policyholder has had more than30 days will not be processed as a reissue, but instead will be processed as an“Increase in Coverage” or “Decrease in Coverage” (please see below).

Increasing BenefitsThere are three ways a policyholder can add coverage to an existing policy with ourcompany:

1. Replace the existing policy with a new policy. The agent should take intoconsideration that all benefits under the new plan will be based on theapplicant’s attained age and must ensure that replacement is in thepolicyholder’s best interest. (Please see “Replacements” on page 31.)

2. Purchase a second policy to supplement the existing plan. Please notethat the total daily benefit allowed under all policies cumulatively maynot exceed the maximum daily benefit allowed under the policy beingpurchased.

3. Add benefits to the existing policy. “Add-ons” to daily benefit or maximumbenefit periods or amounts can only be made to those plans which arecurrently being marketed. These add-ons, if approved, will be based onthe policyholder’s attained age.

Regardless of which method is used to add coverage, the additional benefits will beUnderwritten and, in order to be considered, a completed application must besubmitted.

Decreasing BenefitsUnless required otherwise by your state, requests to reduce benefits will be honoredas of the policy’s next renewal date and must be submitted, in writing, and signed bythe policyholder. We cannot reduce benefits below our normal policy minimums. Norcan a policyholder delete the benefits provided by the base policy while maintainingbenefits provided by attached riders.

Underwriting AppealsAlthough it is in our interest to offer the best rate class available for each applicantbased on their individual circumstances, we understand that you, as the agent, andyour clients may not always agree with the Underwriting decision. We encourageyou to contact us and we will be happy to review such cases and wherever possible,

33

while maintaining the applicant’s privacy, discuss the reason(s) for our decision. Weare also happy to review any additional medical information including letters fromphysicians which may give us additional insight into an applicant’s health statusand/or risk factors.

Underwriting Class UpgradesWith certain acute conditions, the “time since recovery”, as indicated in the enclosedguidelines, is an important factor in determining the correct rate class. If, accordingto the Underwriting guidelines, an existing policyholder appears to qualify for abetter rating than originally issued, we will be happy to review a new application anddetermine if we can upgrade the policyholder to a better rating. If approved, anupgrade is generally not made prior to the policy being in force for one year and ismade effective on the policy’s next renewal date. Upgrades on existing benefits willbe based on the policyholder’s original issue age, while any increases in benefits(add-ons) are based on the policyholder’s attained age. We encourage agents tocontact the Underwriting Department prior to completing an application for Upgradein order to determine whether the policyholder may be eligible.

ReinstatementsReinstatements are processed in accordance with the Reinstatement provisionsdescribed within each policy. In general, we will consider reinstatement for a periodof six months following the policy’s renewal date. Upon receipt of a completedapplication (please use current new business application) and at least a quarterlypremium, we will review to determine if reinstatement is possible and notify theclient. If eligible, the premium will be applied and billing will resume accordingly. Ifnot eligible, the premium check will be returned directly to the client.

Effective DatesIn all States but New York, where the effective date of the policy is the date written (ifissued), the effective date of policies is the date issued, unless requested otherwiseby the agent/applicant. If requested, we will generally make the policy effective up tothirty days subsequent to issuance. If a later effective date is desired, we will considermaking effective up to sixty days after issuance if requested during Underwritingand upon receipt of a valid reason, such as replacement of an existing policy.

Saving AgeIn all states but New York, where the effective date of the policy is the date ofapplication, the issue age will generally correspond to the applicant’s age at time ofapplication, regardless of whether or not the applicant has a birthday following date

34

of application. If specifically requested by the applicant, we can “save age” of anapplicant who has had a birthday within 30 days prior to signing the application. Ifthe application is approved and when specifically requested, the effective date willprecede the applicant’s birthday by one day and the rates will be based on thisyounger age. We cannot save age of any applicant if their birthday preceded thesigning of the application by more than 30 days. All applications must be signed anddated on the actual date completed and should be received in our office within 2weeks of the date signed.

35

_____________________________________________________

_____________________________________________________

_____________________________________________________

_____________________________________________________

_____________________________________________________

_____________________________________________________

_____________________________________________________

_____________________________________________________