Payroll Accountingmwpayrollconf.org/.../payroll_accounting___advanced.pdf · Payroll Accounting...

57

1 Payroll Accounting (Advanced) PJ Grabowski, CPP, SPHR Consultant, HR Systems, Mercy Health [email protected] 314-628-3582 2017 Midwest Payroll Conference

Transcript of Payroll Accountingmwpayrollconf.org/.../payroll_accounting___advanced.pdf · Payroll Accounting...

1

Payroll Accounting(Advanced)

PJ Grabowski, CPP, SPHRConsultant, HR Systems, Mercy Health

314-628-3582

2017 Midwest Payroll Conference

2

Double Entry Bookkeeping

Assets – Liabilities = Equity

OR

Assets = Liabilities + Equity

2017 Midwest Payroll Conference

3

Types of Accounts

Assets – property of the company or what the

company owns

Liabilities – what the company owes to others

Equity – what the sole proprietor, partners, or

shareholders can claim as theirs; contributed capital

and retained earnings

Revenue – what the company earns from sales of

goods or services for the owner(s)

Expenses – the cost to the owner(s) to make the

goods or provide the services

2017 Midwest Payroll Conference

4

T-Accounts

Debit Credit

(left) (right)

2017 Midwest Payroll Conference

5

Assets minus Liabilities = Equity

OR

Assets = Liabilities + Equity

Debit Credit

(left) (right)

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ - + +- -

2017 Midwest Payroll Conference

6

Assets = Liabilities + Equity

Debit Credit

(left) (right)

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ - + +- -

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ +- -

Revenue Expenses

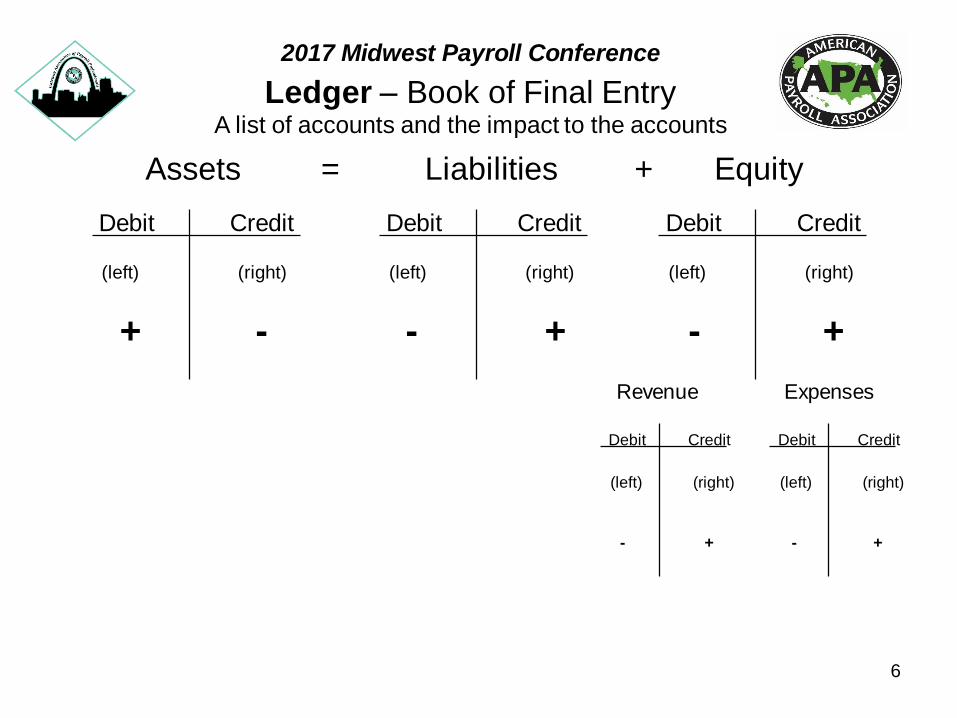

Ledger – Book of Final EntryA list of accounts and the impact to the accounts

2017 Midwest Payroll Conference

7

Journal – Book of Original EntryA daily record of transactions as they occur

Debit Credit

Payroll bank account (asset)

Corporate bank account (asset)

Transfer cash for upcoming payroll from corp to division

$50,000

$50,000

8/17/17

2017 Midwest Payroll Conference

8

General Ledger – Book of Final Entry

Balance by Account

111 Division Bank Acct 112 Corporate Bank Acct

Debit + Debit +Credit - Credit -

$50,000 $50,000

Typical Balances

Assets

Liabilities

Equity

Income

Expenses

Debit

Credit

Credit

Credit

Debit

2017 Midwest Payroll Conference

Chart of Accounts

Asset Accounts 100s

Liability Accounts 200s

Equity Accounts 300s

Revenue Accounts 400s

Expense Accounts 500s

11x Current Assets

12x Long-term Investments

13x Plant, Property, and Equipment

14x Intangible Assets

111 Cash

112 Accounts Receivable

113 Inventory

Bus Unit Division FDC Dept Expense

008 011 42 0214 6010

Company Expense Account Sub Account

10 100507 7000009

2017 Midwest Payroll Conference

Account Structure

By category

$300,000 Salaries

$100,000 Fringes

$50,000 Supplies

$50,000 Fixed Costs

By activity by category—Fixed costs

$5,000 Process sales order

$2,000 Source parts

$2,000 Expedite supplier orders

$4,000 Expedite internal processing

$5,000 Receive supplier quality

$5,000 Reissue purchase orders

$9,000 Expedite customer orders

$5,000 Schedule intra-company sales

$2,000 Request engineering change

$6,000 Resolve problems

$5,000 Schedule parts

10

2017 Midwest Payroll Conference

Direct vs. Indirect Costs

The essential difference between direct costs and indirect costs is that only direct costs

can be traced to specific cost objects. A cost object is something for which a cost is

compiled, such as a product, service, customer, project, or activity. These costs are

usually only classified as direct or indirect costs if they are for production activities, not

for administrative activities (which are considered period costs).

The concept is critical when determining the cost of a specific product or activity, since

direct costs are always used to compile the cost of something, while indirect costs may

not be assigned to such a cost analysis. It can be too difficult to derive a cost-effective

methodology for the assignment of indirect costs; the result is that many of these costs

are considered part of corporate or production overhead, which will exist even if a

specific product is not created or an activity does not occur.

Examples of direct costs are direct labor, direct materials, commissions, piece rate

wages, and manufacturing supplies. Examples of indirect costs are production

supervision salaries, quality control costs, insurance, and depreciation.

Direct costs tend to be variable costs, while indirect costs are more likely to be either

fixed costs or period costs.

https://www.accountingtools.com/articles

11

2017 Midwest Payroll Conference

12

Payroll Example

Debit Credit

Salary Expense (Equity/Expense)

Salaries/wages payable (Liability)

Cost of payroll for month of July

$6,000

$6,000

8/17/17

Debit Credit

(left) (right)

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ - + +- -

Debit Credit

(left) (right)

Debit Credit

(left) (right)+ +- -

Revenue Expenses

Assets = Liabilities + Equity

211 Salaries/wages payable

511 Salary Expense

$6,000

$6,000

$50,000

2017 Midwest Payroll Conference

13

Salaries/wages payable (Liability)

Fed Inc Tax Withheld (Liability)

State Inc Tax Withheld (Liability)

Soc Security Tax Withheld (Liability)

Medicare Tax Withheld (Liability)

Health Ins Premiums (Liability)

$2,159

$1,200

$ 300

$ 372

$ 87

$ 200

8/17/17

Debit Credit

Deductions from employees checks that are owed to third parties.

Amount of EE’s Pay Owed to Others

2017 Midwest Payroll Conference

Payroll ExampleDebit Credit

Salaries/wages payable (Liability)Fed Inc Tax Withheld (Liability)

State Inc Tax Withheld (Liability)

Soc Security Tax Withheld (Liability)

Medicare Tax Withheld (Liability)

Health Ins Premiums (Liability)

$2,159$1,200

$ 300

$ 372

$ 87

$ 200

8/17/17

Debit Credit

(left) (right)

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ - + +- -

Debit Credit

(left) (right)

Debit Credit

(left) (right)+ +- -

Revenue Expenses

Assets = Liabilities + Equity

211 Salaries/wages payable

511 Salary Expense

$6,000

$6,000

$2,159

14

Deductions from employees checks that are owed to third parties.

$50,000

111 Division Bank Acct

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

212 Fed Inc Tax Withheld payable

$1,200

Debit Credit

(left) (right)

+-

213 State Inc Tax Withheld payable

$300

15

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

214 Soc Security Tax Withheld payable

$372

Debit Credit

(left) (right)

+-

215 Medicare Tax Withheld payable

$87

16

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

216 Health Ins Premiums payable

$200

17

2017 Midwest Payroll Conference

18

Payroll cash distribution/net pay

Salaries/wages payable (Liability)

Cash from Payroll Checking Acct (Asset)

$3,841

$3, 841

8/20/17

Debit Credit

Employees are paid the cash we owe them

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Salaries/wages payable (Liability)

Division Bank Acct (Asset)

Pay employees for month of July

$3,841$3,841

8/20/17

Debit Credit

(left) (right)

Debit Credit

(left) (right)

Debit Credit

(left) (right)

+ - + +- -

Debit Credit

(left) (right)

Debit Credit

(left) (right)+ +- -

Revenue Expenses

Assets = Liabilities + Equity

211 Salaries/wages payable

511 Salary Expense

$6,000

$6,000

$2,159$3,841

$3,841

Acct Bal = $0

19

$50,000

111 Division Bank Acct

2017 Midwest Payroll Conference

20

ER Payroll tax expense

Social Sec tax payable (Liability)

Medicare tax payable (Liability

Fed Unemployment tax payable (Liability)

State Unemployment tax payable (Liability)

$831

$372

$ 87

$ 48

$324

8/17/17

Debit Credit

Expenses incurred for employer taxes

Employer’s tax liabilities; an expense of doing business

2017 Midwest Payroll Conference

Payroll ExampleDebit Credit

8/17/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

511 Salary Expense

Assets = Liabilities + Equity

211 Salaries/wages payable

$6,000$6,000

$2,159$3,841

$3,841

Acct Bal = $0

Debit Credit

(left) (right)+-

$831

512 ER Tax Expense

Payroll tax expense

Social Sec tax payable (Liability)

Medicare tax payable (Liability

Fed Unemployment tax payable (Liability)

State Unemployment tax payable (Liability)

$831

$372

$ 87

$ 48

$324

Expenses incurred for employer taxes

21

$50,000

111 Division Bank Acct

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

217 ER SS Tax payable

$372

Debit Credit

(left) (right)

+-

218 ER Medicare Tax payable

$87

22

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

219 FUTA Tax payable

$48

Debit Credit

(left) (right)

+-

220 SUI Tax payable

$324

23

2017 Midwest Payroll Conference

24

Fed Inc Tax Withheld (Liability)

State Inc Tax Withheld (Liability)

Soc Sec Tax Withheld (Liability)

Med Tax Withheld (Liability)

Health Ins Premiums (Liability)

Cash from Payroll Checking Acct (Asset)

$1,200

$ 300

$ 372

$ 87

$ 200

$2,159

8/20/17

Debit Credit

Paying taxes that were withheld from employees

Paying Employee Taxes and Health Ins

2017 Midwest Payroll Conference

Payroll Example

Debit CreditFed Inc Tax Withheld (Liability)

State Inc Tax Withheld (Liability)

Soc Sec Tax Withheld (Liability)

Med Tax Withheld (Liability)

Health Ins Premiums (Liability)

Cash from Payroll Checking Acct (Asset)Paying taxes that were withheld from employees

$1,200

$ 300

$ 372

$ 87

$ 200

8/20/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

511 Salary Expense

Assets = Liabilities + Equity

211 Salaries/wages payable

$6,000$6,000

$3,961

$2,159

Debit Credit

(left) (right)+-

$831

512 ER Tax Expense

$2,159

25

$50,000

$3, 841

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

212 Fed Inc Tax Withheld payable

$1,200

Debit Credit

(left) (right)

+-

213 State Inc Tax Withheld payable

$300

$1,200

$300

26

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

214 Soc Security Tax Withheld payable

$372

Debit Credit

(left) (right)

+-

215 Medicare Tax Withheld payable

$87

$372

$87

27

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

216 Health Ins Premiums payable

$200$200

28

2017 Midwest Payroll Conference

29

Social Sec Tax Payable (Liability)

Medicare Tax Payable (Liability)

FUTA Tax Payable (Liability)

SUTA Payable (Liability)

Cash from Payroll Checking Acct (Asset)

$372

$ 87

$ 48

$324

$831

8/20/17

Debit Credit

Paying employer taxes

Paying the Employer Taxes

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Social Sec Tax Payable (Liability)

Medicare Tax Payable (Liability)

FUTA Tax Payable (Liability)

SUTA Payable (Liability)Cash from Payroll Checking Acct (Asset)

Paying employer taxes

$372

$ 87

$ 48

$324

8/20/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

511 Salary Expense

Assets = Liabilities + Equity

211 Salaries/wages payable

$6,000

$3,841 $6,000$3,841

$2,159

$ 831Debit Credit

(left) (right)+-

$831

512 ER Tax Expense

$831

30

$50,000

111 Division Bank Acct

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

217 ER SS Tax payable

$372

Debit Credit

(left) (right)

+-

218 ER Medicare Tax payable

$87

$372

$87

31

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

219 FUTA Tax payable

$48

Debit Credit

(left) (right)

+-

220 SUI Tax payable

$324

$48

$324

32

2017 Midwest Payroll Conference

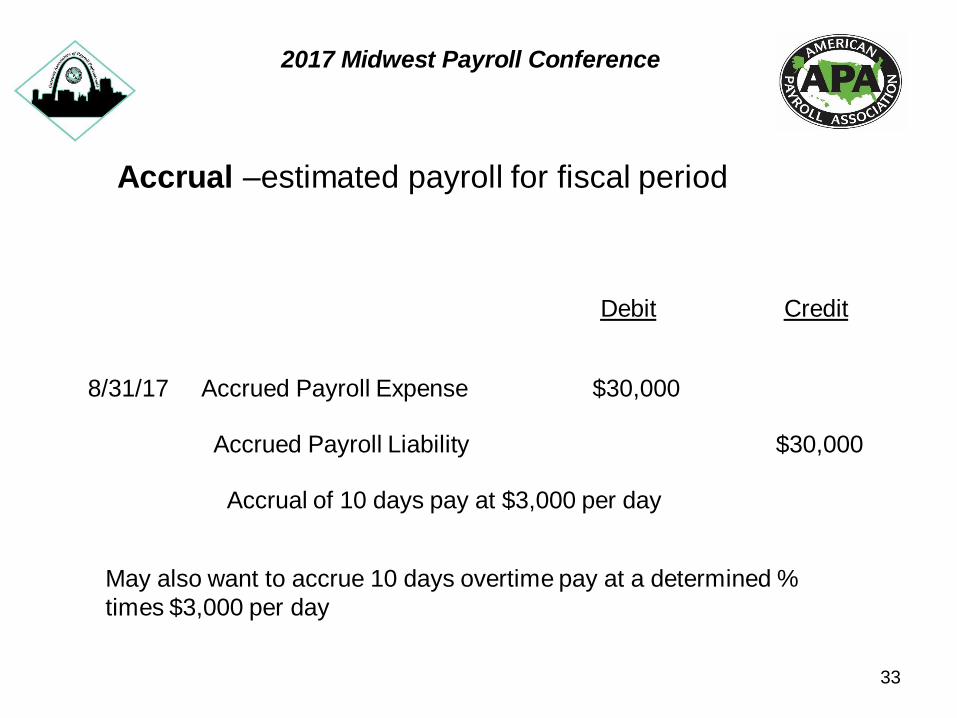

Accrual –estimated payroll for fiscal period

Debit Credit

Accrued Payroll Expense

Accrued Payroll Liability

Accrual of 10 days pay at $3,000 per day

$30,000

$30,000

8/31/17

May also want to accrue 10 days overtime pay at a determined %

times $3,000 per day

33

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Accrued Payroll Expense

Accrued Payroll Liability

Accrual of 10 days pay at $3,000 per day

$30,000$30,000

8/31/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

513 Accrued Salary Exp

Assets = Liabilities + Equity

221 Accrued Payroll Liability

$30,000$30,000

111 Cash

34

$150,000

2017 Midwest Payroll Conference

Accrued Payroll Tax Expense

Accrued SS Tax Expense

Accrued Medicare Tax Payable

Accrued FUTA Tax Payable

Accrued SUI Tax Payable

$4,155

$1,860

$ 435

$ 240

$1,620

8/31/17

Debit Credit

Expenses accrued for employer taxes

Employer’s Accrued Tax Liabilities

35

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Accr ER Tax ExpenseAccrued SS Tax Payable $1,860

Accrued Medicare Tax Payable $ 435

Accrued FUTA Tax Payable $ 240

Accrued SUI Tax Payable $1,620

Accrue for ER Taxes

$4,1558/31/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

513 Accr Salary Expense

Assets = Liabilities + Equity

221 Accrued Payroll Liability

$30,000$30,000

Debit Credit

(left) (right)+-

$4,155

514 Accr ER Tax Expense

36

$150,000

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

222 Accrued SS Tax payable

$1,860

Debit Credit

(left) (right)

+-

223 Accrued Medicare payable

$435

37

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

224 Accrued FUTA Tax payable

$240

Debit Credit

(left) (right)

+-

225 Accrued SUI Tax payable

$1,620

38

2017 Midwest Payroll Conference

Reverse Accruals in new fiscal period

Debit Credit

Accrued Payroll Liability

Accrued Payroll Expense

Reverse Salary Accrual

$30,000

$30,000

9/1/17

39

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Accrued Payroll LiabilityAccrued Payroll Expense $30,000

Reverse Salary Accrual

$30,0009/1/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

513 Accr Salary Expense

Assets = Liabilities + Equity

221 Accrued Payroll Liability

$30,000$30,000

Debit Credit

(left) (right)+-

$4155

514 Accr ER Tax Expense

$30,000$30,000

40

$150,000

111 Division Bank Acct

2017 Midwest Payroll Conference

Payroll tax expense

Accrued SS Tax Payable

Accrued Medicare Tax Payable

Accrued FUTA Tax Payable

Accrued SUI Tax Payable

$4,155

$1,860

$ 435

$ 240

$1,620

9/1/17

Debit Credit

Reverse expenses accrued for employer tax liability

Reverse employer’s accrued tax liabilities

41

2017 Midwest Payroll Conference

Payroll Example

Debit Credit

Accr ER Tax Expense

Accrued SS Tax Payable

Accrued Medicare Tax Payable

Accrued FUTA Tax Payable

Accrued SUI Tax Payable

Reverse Accrual for ER Taxes

$4,155

8/31/17

Debit Credit

(left) (right)

Debit Credit

(left)(right)

Debit Credit

(left) (right)

+ - +

+

- - Debit Credit

(left) (right)

Debit Credit

(left) (right)+

+

-

-Revenue

Assets = Liabilities + Equity

221 Accrued Payroll Liability

$30,000$30,000

Debit Credit

(left) (right)+-

$4,155

$150,000

$1,860

$ 435

$ 240

$1,620

$4,155

513 Accr Salary Expense

514 Accr ER Tax Expense

$30,000$30,000

42

111 Division Bank Acct

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

222 Accrued SS Tax payable

$1,860

Debit Credit

(left) (right)

+-

223 Accrued Medicare payable

$435

43

$1,860

$435

2017 Midwest Payroll Conference

Assets = Liabilities + Equity

Payroll Example

Debit Credit

(left) (right)

+-

224 Accrued FUTA Tax payable

$240

Debit Credit

(left) (right)

+-

225 Accrued SUI Tax payable

$1,620

44

$240

$1,620

What other expenses might need to be accrued?

2017 Midwest Payroll Conference

45

Clearing Accounts and Suspense Accounts

Both are temporary accounts used for recording income and

expense

Clearing accounts are used to hold transactions for later

posting correctly and completely• Accounts receivable check until the money is cleared

• Hold construction costs until project is complete

• Employee repays a previously received tuition reimbursement by personal

check but check has not yet cleared the bank

Suspense accounts are used when there appears to be a problem and

offsets a transaction until the problem can be resolved• Employee is owed a bonus but account to be charged has not yet been

identified

• Employee sends a personal check to payroll but reason has yet to be

determined

Both are periodically balanced to zero; if source or purpose is

unknown, balance may have to be “written off”.

2017 Midwest Payroll Conference

Financial Statements

Balance Sheet—Value of a business at a specific point in time,

generally the period end date

Assets, Liabilities, Equity (from Income Statement)

Income Statement—Summarizes revenue and expenses for a

period of time

Income, Expenses, Retained Earnings, Contributed Capital

46

2017 Midwest Payroll Conference

Subsystems

Cash Receipts Journal—All receipts of cash

Cash Payment Journal—All payments of cash

Purchases Journal—All purchases of merchandise or services

on credit

Sales Journal—All sales of merchandise or services on credit

Payroll Journal—All payroll and personnel expenses/liabilities

General Journal—All remaining transactions

Separate Ledgers may also be maintained

Payroll Ledger

2017 Midwest Payroll Conference

48

Financial Ratios

2017 Midwest Payroll Conference

Number ratios, percent ratios, fraction ratios

Sales / Net Income = Number ratio

$400,000 / $40,000 = 10

Expressed as 10:1 ratio

New Income / Sales = Percent ratio

$40,000 / $400,000 = .10

Expressed as 10%

Net Income / Sales = Fraction ratio

$40,000 / $400,000 = 1/10

Expressed as 1/10th

49

Financial Ratios

2017 Midwest Payroll Conference

Liquidity ratio—Ability to pay short-term debts

Current ratio = Current assets / current liabilities

$20,000 / $10,000 = 2:1

Business owns $2.00 of current assets for each $1 of

current liabilities owed

Leverage ratios—Relative amount of funds in the business supplied

by creditors and shareholders; ability to meet long-term financial

obligations

Debt-equity ratio = Long term liabilities / equity

$150,000 / $500,000 = .3

Ratio of less than 1.5 is generally acceptable

$750,000 / $500,000 = 1.5

50

Financial Ratios

2017 Midwest Payroll Conference

Profitability ratios—Management’s ability to generate a financial

return on sales or investments; also called ROI (Return on

Investment). Ratio of profit to capital, or rate of return from capital

(equity plus long-term debt)

Net Income / (Equity + Long Term Debt) = ROI

$200,000 / ($750,000 + $250,000) = .20 or 20%

51

2017 Midwest Payroll Conference

Sarbanes-Oxley Compliance

Publicly traded companies

CEO and CFO certifications

Complaint procedures established

No loans to officers or directors

Payroll’s roll in SOX

Develop process and workflow maps

Create written documentation

Audit recordkeeping and retention

Identify and communicate gaps and risks

Prepare action plans, when needed

Monitor progress of action plans

Monitor outsourcing companies

SAS 70 Type I and II

52

2017 Midwest Payroll Conference

Internal Controls

Segregation of duties

Rotation of job duties

Check distribution

Negative deductions

Secure blank check stock

Time and salary change approvals

Internal auditors

GAAP

Generally Accepted Accounting Principles

Business Entity Concept—Personal transactions kept separate from business

transactions

Continuing Concern Concept—On-going business with assets valued at cost, not a

business for sale with assets valued at FMV

Time Period Concept—Fiscal Year may, or may not, coincide with Calendar Year

Cost Principle—Assets valued at cost minus depreciation since this is an on-going

business concern

Objectivity Principle—Assets are valued without respect to personal opinions or emotions

Matching Principle—Expenses and revenue are recorded in the period in which they are

spent or earned

Realization Principle—Revenue is recognized (or realized) when earned

Consistency Principle—Transactions must be recorded in a consistent manner

53

2017 Midwest Payroll Conference

54

2017 Midwest Payroll Conference

International Financial Reporting Standards

IFRS

Approximately 120 nations and reporting jurisdictions permit or

require IFRS. Approximately 90 countries have fully confirmed with

IFRS.

The IFRS Foundation is the legal entity under which the International

Accounting Standards Board (IASB) operates. The Foundation is

governed by a board of 22 trustees.

IFRS Foundation is the new name, approved in January 2010, of the

IASC Foundation. The name change formally took effect on 1 July

2010. From that date, the Foundation's website (including IASB

materials) also changed to www.ifrs.org

55

2017 Midwest Payroll Conference

International Financial Reporting Standards

IFRS

The objectives of the IFRS Foundation are:

• to develop, in the public interest, a single set of high quality, understandable,

enforceable and globally accepted financial reporting standards based upon clearly

articulated principles. These standards should require high quality, transparent and

comparable information in financial statements and other financial reporting to help

investors, other participants in the world’s capital markets and other users of financial

information make economic decisions

• to promote the use and rigorous application of those standards

• in fulfilling the above objectives, to take account of, as appropriate, the needs of a

range of sizes and types of entities in diverse economic settings

• to promote and facilitate adoption of International Financial Reporting Standards

(IFRSs), being the standards and interpretations issued by the IASB, through the

convergence of national accounting standards and IFRSs.

56

2017 Midwest Payroll Conference

What is the difference between the

IFRS and GAAP?

PwC has a free, 256 page download

IFRS and US GAAP: similarities and differences

https://www.pwc.com/us/en/cfodirect/publications/accounting-guides/ifrs-and-us-gaap-

similarities-and-differences.html

Questions?

57

2017 Midwest Payroll Conference